UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2019

or

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________

Commission File Number: 333-226885

BIOPLUS LIFE CORP

(Exact name of registrant as specified in its charter)

| Nevada | 30-0987011 | |

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

No 9 & 10 Jalan P4/8B Bandar Teknologi Kajang Semenyih Selangor, Malaysia |

43500 | |

| (Address of Principal Executive Offices) | (Zip Code) |

+60 3 8703 2020

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| Non-accelerated filer [X] | Smaller reporting company [X] | |

| Emerging growth company [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $0 due to lack of trading market.

As of May 26, 2020, there were 362,905,561 shares of common stock, no par value, outstanding.

| 2 |

FORWARD-LOOKING STATEMENTS

Certain statements made in this Annual Report on Form 10-K are “forward-looking statements” (within the meaning of the Private Securities Litigation Reform Act of 1995) regarding the plans and objectives of management for future operations. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements of the Registrant to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The forward-looking statements included herein are based on current expectations that involve numerous risks and uncertainties. The Registrant’s plans and objectives are based, in part, on assumptions involving the continued expansion of business. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of the Registrant. Although the Registrant believes its assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate and, therefore, there can be no assurance the forward-looking statements included in this Report will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by the Registrant or any other person that the objectives and plans of the Registrant will be achieved.

Unless stated otherwise, the words “we,” “us,” “our,” “Company” or “BioPlus” in this Annual Report collectively refers to BioPlus Life Corp., a Nevada corporation and its wholly owned subsidiaries and variable interest entities described herein.

BUSINESS DESCRIPTION

Industry Overview

This section includes market and industry data that we have developed from publicly available information; various industry publications and other published industry sources and our internal data and estimates. Although we believe the publications and reports are reliable, we have not independently verified the data. Our internal data, estimates and forecasts are based upon information obtained from trade and business organizations and other contacts in the market in which we operate and our management’s understanding of industry conditions.

At this time, Bioplus Life Corp. mainly serves consumers in Malaysia, although the Company may evaluate and change this focus in the future and expand into other countries. Given most of the demand for our products currently originates from Malaysia, we will focus solely upon the Healthcare Industry within Malaysia.

Malaysia saw real GDP growth of 5% in 2017, which led to an improvement in consumer sentiment. As Malaysians were more confident in making purchases, various health care and beauty care categories including skin care and health supplement showed signs of recovery. At the same time, the growing importance of halal-certified products amongst the Muslim population in Malaysia also led to rising demand for halal products in beauty and personal care during 2017. Halal-certified beauty and personal care products are manufactured in compliance with good manufacturing practice (GMP) provided by the Department of Islamic Advancement of Malaysia (JAKIM). This information can be found at http://www.euromonitor.com/beauty-and-personal-care-in-malaysia/report.

In line with the national economic blueprint, healthcare sector is one of the National Key Economic Areas (NKEA) set to drive the country towards a high-income nation by 2020. From 2011 to 2015, the healthcare industry recorded an average growth rate of 15%. In 2016 alone, the industry grew by 23% from 2015—with an estimated actual contribution of approximately RM4-5 billion to Malaysia’s economy. In the latest budget 2018, government has allocated RM26.58 billion to the MOH (Ministry of Health), indicating a 9.5% or 1.7 billion increase compared to the 2017 budget. This information can be found at https://today.mims.com/an-extensive-overview-on-the-possibility-of-improving-malaysia- healthcare-system.

| 3 |

Going forward, it is estimated that Malaysia has successfully attracted 19,488 retirees from 120 countries to settle in the country since 2002. About 10 percent of the total population will be over the age of 60 in 2020, making Malaysia an aging nation. It is estimated that the market worth of the Aged Care industry in Malaysia by 2020 will be $1.4 billion, which induced a growing demand for healthcare industry in the country. This information can be found at http://infomed.com.my/malaysia-health-expenditure-20-billion-2025.

Corporate History

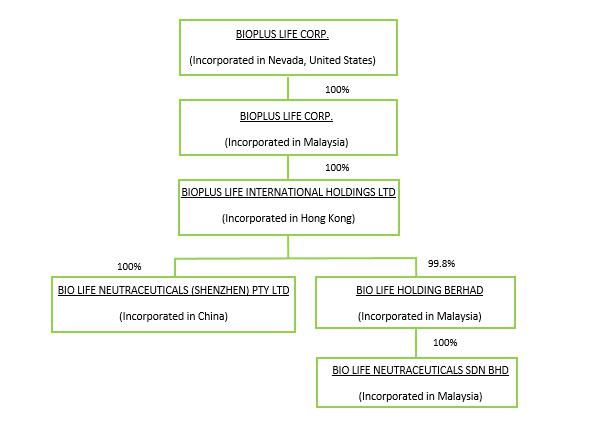

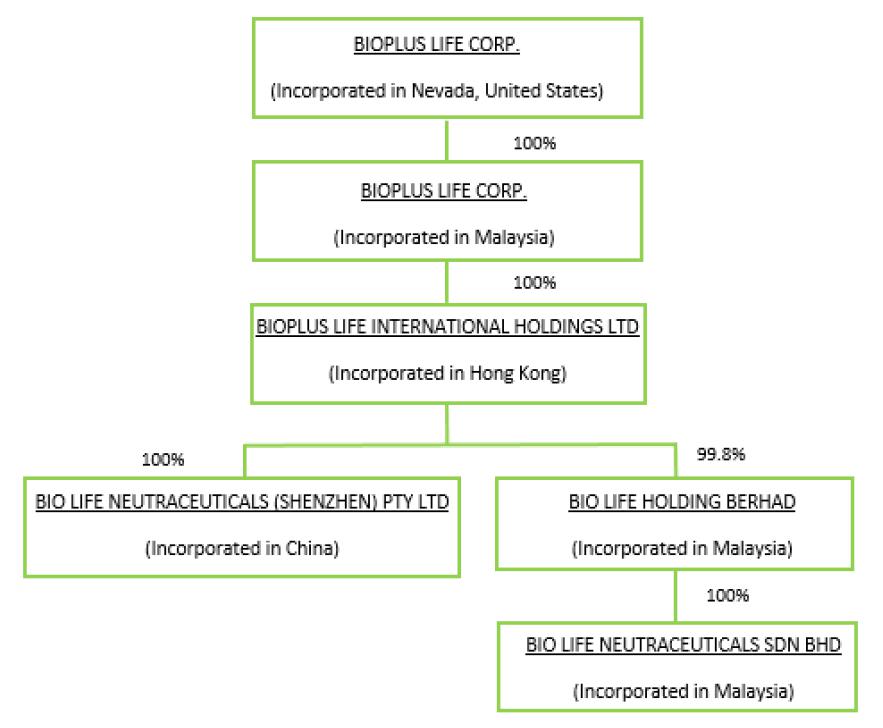

Bioplus Life Corp., a Nevada corporation (“Company”), was incorporated under the laws of the State of Nevada on April 13, 2017. On July 10, 2017, the Company acquired 100% of the equity interests of Bioplus Life Corp., a Malaysian company. On July 19, 2017, the Company, through its Malaysian subsidiary, Bioplus Life Corp., acquired 100% of the equity interests of Bioplus Life International Holdings Ltd, a Hong Kong company. On October 27, 2017, the Company through its Hong Kong subsidiary, Bioplus Life International Holdings Ltd, acquired 100% equity interest of Bioplus Life Corp. (ShenZhen), a company incorporated in China.

On June 11, 2018, the Company through its subsidiary in Hong Kong, Bioplus Life International Holdings Ltd, acquired 99.8% equity interest of Bio Life Holdings Berhad, a company incorporated in Malaysia. Bio Life Holdings Berhad owns 100% of the equity interests of Bio Life Neutraceuticals Sdn. Bhd., a company incorporated in Malaysia.

Our corporate structure is depicted below:

| 4 |

Our corporate complex is located at No. 9 and No. 10, Jalan P4/8B, Bandar Teknologi Kajang, 43500 Semenyih, Selangor Darul Ehsan, Malaysia, which are two adjoining commercial structures. Our corporate offices are located in the No. 9 building. Our manufacturing facilities comprise the remainder of the space in both buildings.

Our website is http://www.bionutry.com and our phone number is +60 3 8703 2020.

Business Information

Bioplus Life Corp., through its wholly owned subsidiaries, specializing in manufacturing and selling health and beauty care products. Our mission is to create awareness for good health and personal care to improve our customers’ quality of life. We seek to achieve this by offering an affordable solution to existing health food businesses through the production, information, advisory and services pertaining to our product line. Our website, http://www.bionutry.com, can be utilized to inquire about our product offerings, but we do not directly sell any products through our website. At this time, we primarily sell our products to third party companies.

Our product series, or line, includes, but is not strictly limited to, products that fall into the following categories: bone, fiber, bee-propolis, cardiovascular health, herbal, health beverages, apple stem cell, beauty care, feminine health, UT care, anti-oxidant and eye health series. These health and beauty supplies are designed to help improve the consumers’ metabolism rate, burn excessive fats, provide anti-aging effects and improve the overall health and physical appearance of our customers.

The majority of our products have been halal certified and, at the same time, awarded with a health manufacturing license by the Ministry of Health Malaysia (MOH) to accommodate the high demand for Muslims’ HALAL food while also meeting the expectations of the public on a safe and hygienic food supply. It is the belief, and hope, of the Company that this assurance from an esteemed regulatory body will also serve to prove our continuing commitment in supplying quality goods to our customers.

Through our two factories located in Semenyih, Malaysia, we are able to deliver a one stop service. This begins with the initiation of product concept, to sourcing new and potential ingredients or raw materials, we then begin development of new product formulations, and we continue to customize production until products are ready to be shipped to our customers. This ‘one-stop-shop’ method of operating allows us to reduce the resources and cost needed to create our products, while also decreasing the amount of time needed from inception to shipping.

Since 2019, our health and beauty products have been sold through independent wholesalers who are supported with our sales and marketing team, and we have achieved the following:

| - | Worldwide halal certification; | |

| - | Available to consumers besides Muslim community; | |

| - | Professional certification ensuring safe and high-quality health products; | |

| - | Maintaining low cost, low capital, zero inventory, low threshold to help more people start a business easily with our platform; | |

| - | Current products are listed at http://www.bionutry.com | |

| - | Wechat mode: Take your goods directly from the platform and sell them through your own network; | |

| - | Internet model: Register for an online store, take the goods directly, change the price and sell with a profit; | |

| - | WeChat + Internet are operated concurrently 24/7. |

| 5 |

Research and Development activities have also been carried out continuously to ensure innovation and quality of the product is maintained and improved. Conforer Global Sdn Bhd, Mon Space (M) Sdn Bhd, Oriental Inchaway Sdn Bhd, Nina G Holdings Sdn Bhd, and Go3u Trading Sdn Bhd are our most substantial customers over our past three fiscal years, who comprised between 10% to 16% of our total sales. Remaining sales for the past three fiscal years have been broken up into roughly fifty customers in varying quantities.

The heightened awareness of the public towards the importance of healthcare has helped to create vast market potential for future development. In the future, our company will be expanding its business to Thailand, India and China to improve our ability to meet the demand the Company perceives from consumers in these countries.

Key Products

The following is a brief description of our key products. A full list of our products, as well as additional product details, can be found at http://www.bionutry.com.

| 2019 | 2018 | |||||||||||||||

| Top 5 Products | Sales | % | Sales | % | ||||||||||||

| Fiber | 729,509 | 42 | % | 1,023,746 | 41 | % | ||||||||||

| Lady Health | 286,334 | 17 | % | 313,655 | 13 | % | ||||||||||

| Telospan | 88,311 | 5 | % | 362,684 | 14 | % | ||||||||||

| Skin Care & Cosmetic | 8,626 | 1 | % | 5,778 | 1 | % | ||||||||||

| Green Propolis | 48,964 | 3 | % | 72,432 | 3 | % | ||||||||||

| Others | 560,465 | 32 | % | 692,197 | 28 | % | ||||||||||

| Total | 1,722,209 | 100 | % | 2,470,492 | 100 | % | ||||||||||

Fiber

|

|

Many of us associate fiber with digestive health and bodily functions that we’d rather not think about. However, eating foods high in dietary fiber can do so much more than keep you regular. It can lower your risk for heart disease, stroke, and diabetes, improve the health of your skin, and help you lose weight. It may even help prevent colon cancer. Fiber, also known as roughage, is the part of plant-based foods (grains, fruits, vegetables, nuts, and beans) that the body can’t break down. It passes through the body undigested, keeping your digestive system clean and healthy, easing bowel movements, and flushing cholesterol and harmful carcinogens out of the body. |

Lady Health

|

Lady Health, clinically proven synergistic blend of Traditionally Malaysia and Korea herbal extracts that together offer relief for uncomfortable feelings associated with menopause. Research has shown this combination to promote healthy management of hot flashes, night sweats, nervous irritability, dizzy spells, vaginal dryness, numbness and tingling, occasional emotional discontent, and occasional fatigue and sleeplessness. Unlike some common menopause formulations with ingredients that bring safety concerns, Our Lady Health formulation has a record of safety, is non-estrogenic and has a long history of use in Asia. |

| 6 |

Telospan

|

|

Telospan works at cell level in the body, After taking Telospan, it can be easily absorbed by the body, enters the bloodstream, then passes to every single cell. Telospan activates telomeric gene when reaching the cells, produce telomerase and thus extend telomere. Telospan promote cell function and cell life. Scientific research has proved that human cells will divide up 50 times throughout the cell life. Cells divide once every two and half year. Telomere will be shortened in every cell division process until the end of cell life with no telomere. However, Resveratrol can activate the production of telomere in human body which lengthen the telomere by 30%. As a result, cell division can occur more than 50 times which is approximately 65 times. With the increase of 30% in telomere length, human lifespan also increases by 30% which is 25 to 30 years longer. |

Skin Care and Cosmetics

|

Skin care and cosmetics are products used to enhance or change the appearance of the face or the texture of the external body. Most of our cosmetics are designed for use of applying to the face and body. They are generally mixtures of chemical compounds derived from natural sources (such as coconut oil, jojoba oil, plant extract), or may be synthetic or artificial. The products such as breast firming cream, feminine cleanser, lip balm, moisturizer, face firming spray, cleanser, mask and several other products. |

| 7 |

Green Propolis

|

Did you know that honey isn’t the only thing that bees make? Bees also produce a compound called propolis from the sap on needle-leaved trees or evergreens. When they combine the sap with their own discharges and beeswax, they create a sticky, greenish-brown product used as a coating to build their hives. This is propolis.

Thousands of years ago, ancient civilizations used propolis for its medicinal properties. Greeks used it to treat abscesses. Assyrians put it on wounds and tumors to fight infection and help the healing process. Egyptians used it to embalm mummies. |

Others

|

|

We also have generated different categories of products to fulfill the different targeted needs of consumer. These products generally are antioxidant food and supplements that and relate to diabetes treatment, bone health, immune system, cardiovascular health, and collagen repair. |

Marketing

As mention we sell primarily through wholesalers whom we attract through word of mouth. Our current marketing strategy is to systematically promote our capabilities and our past performance to our customers. We periodically make visits to potential clients within a reasonable distance from our offices to introduce ourselves and explain why our clients prefer our services to those offered by competitors. We also will fine-tune and revamp our corporate website to better promote the list of our products offered. In addition, we also plan to pursue marketing campaigns by utilizing the internet, social media, and perhaps print media. These plans have not yet been determined in sufficient detail to outline herein and our marketing plan is currently a work in progress.

Key Supplier

The raw materials contained in our products are highly dependent on our major supplier, Bio Life Solutions Sdn Bhd., an unrelated Malaysian company. Bio Life Solutions Sdn Bhd has supplied more than 80% of the raw materials that make up our products over the past 3 fiscal years. At our current and our anticipated future operating levels, our supplier has indicated that they will have ample supply to fulfill our orders for raw materials while also fulfilling any and all orders they may receive from other customers.

Government Regulations

All of the principal products we offer for sale are registered under Malaysia’s Food Act 1983 (Act 281) & Regulations. At this time, we only offer our products in Malaysia so presently this is the only pertinent government regulation, as all products require authorization from the Food and Quality Division of Ministry of Health according to the Food Act of 1983 and Food Regulations 1985 in order to be sold in Malaysia.

| 8 |

Competition

The industry in which we compete is highly competitive. Competition in the health and beauty care industry, with a focus on health supplements in particular, is very intense particularly in Malaysia. We face competition from various retail health supplement providers, pharmacies, and multi-level marketing companies which supply health supplement products. These competitors generate significant traffic and have established brand recognition and financial resources.

We believe that the principal competitive factors in our market includes the quality of health supplements, the efficiency and effectiveness of the health supplements, strength and depth of relationships with clients, the ability to identify the changing needs and requirements of prospective clients, and the scope of service. Through utilizing our competitive strengths, we believe that we have a competitive edge over other competitors due to the breadth of our product offerings, one stop convenience, pricing, our service, our reputation and product safety. We are confident we can develop and enlarge our market share in Malaysia and potentially further into the overseas market.

Future Plans

In the future, subject to available funds, we intend to increase our current production capacity with the enhancement of our factory with modernized and fully automated equipment. In addition, we plan to invest heavily in research and development activities to innovate and develop new products to address the future market needs.

We also anticipate expanding into new geographical areas, with a particular focus, at least initially, on expanding into Thailand, India and China. At present, we do not have any distinct timeline in place for expansion into these countries. We also plan to expand our market coverage to include the halal market, the aging population market and the pet market as we see the underlying potential in these three market sectors. When we begin these efforts, we plan to hire more employees to support our operations in different countries. We believe that hiring fifteen to twenty employees will be sufficient in order to support our operations. We may also evaluate potential acquisitions in the future which we feel may have some synergy with our current operations.

Employees

As of December 31, 2019, we have 19 full-time employees. Currently, our full-time employees currently devote approximately 50 hours per week to the operations of our Company. We do not presently have pension, health, annuity, insurance, stock options, profit sharing, or similar benefit plans; however, we may adopt plans in the future. There are presently no personal benefits available to our Officers and/or Directors and our employees. We intend to hire more staff to assist in the development and execution of our business operations.

Product Liability.

Due to nature of the Company’s business, the Company may face claims for product liability resulting from any illnesses, adverse conditions or reactions related to use of its products. Presently, the Company does not maintain any product liability insurance to cover any such claims.

RISK FACTORS

An investment in our common stock involves a number of very significant risks. You should carefully consider the following known material risks and uncertainties in addition to other information in this Form 10-K in evaluating our company and its business before purchasing shares of our company’s common stock. You could lose all or part of your investment due to any of these risks.

| 9 |

Risk Factors Relating to Our Business

WE HAVE LIMITED OPERATING HISTORY AND LIMITED BUSINESS GROWTH. We have been operational since April 2017; therefore, we have had limited operations which makes it difficult to evaluate our business and our prospects. In addition, to date, we have not experienced substantial growth in our business. The likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered by a small operating company trying to expand its business enterprise and the highly competitive environment in which we will operate. In addition, we are confronting the negative impact of COVID-19 on our business, which has been substantial. Consequently, there can be no assurance that the business of the Company will grow in the future. Moreover, because of our limited operating history, it is difficult to extrapolate any meaningful projections about the Company’s future.

THE CURRENT PANDEMIC OF THE NOVEL CORONAVIRUS, OR COVID-19, AND THE FUTURE OUTBREAK OF OTHER HIGHLY INFECTIOUS OR CONTAGIOUS DISEASES, COULD MATERIALLY AND ADVERSELY IMPACT OR DISRUPT OUR FINANCIAL CONDITION, RESULTS OF OPERATIONS, CASH FLOWS AND PERFORMANCE. An outbreak of respiratory illness caused by COVID-19 emerged in late 2019 and has spread globally, including Malaysia. The coronavirus is considered to be highly contagious and poses a serious public health threat. The World Health Organization labeled the coronavirus a pandemic on March 11, 2020, given its threat beyond a public health emergency of international concern the organization had declared on January 30, 2020.

Our revenues, workforce and our wholesalers are concentrated in Malaysia. The epidemic has resulted in lockdown of cities, travel restrictions, and the temporary closure of stores and facilities in Malaysia for the past few months. The negative impacts of the COVID-19 outbreak on our business have included:

| ● | quarantines impeded our ability to sell our products and recruit new wholesalers, which has result in a dramatic reduction in sales. Travel restrictions limited other parties’ ability to visit and meet us in person. Although most communication could be achieved via video calls, this form of remote communication may be less effective in building trust and engaging new agents and traders. | |

| ● | the operations of our wholesalers have been and could continue to be negatively impacted by the epidemic, which may in turn adversely impact future sales. |

Additionally, the pandemic has affected our overall ability to react timely to mitigate the impact of this event and has substantially hampered our efforts to provide our investors with timely information and comply with our filing obligations with the Securities and Exchange Commission.

WE HAVE A HISTORY OF LOSSES. Since the inception, we have had a history of losses. Our accumulated deficit as of December 31, 2019 is $216,550. We cannot provide assurances that we will achieve profitable operations in the future.

WE FACE MARKET COMPETITION AND OUR OPERATING RESULTS WILL SUFFER IF WE FAIL TO COMPETE EFFECTIVELY. We face competition from other companies in the supplement and nutraceutical business in Malaysia and elsewhere in the Pacific Rim. Many of our competitors have stronger financial and other capacities, including research and development, than us.

If our competitors market products that are more effective, safer or less expensive or that reach the market sooner than our future products, if any, we may not achieve commercial success. In addition, because of our limited resources, it may be difficult for us to stay abreast of any changes in the market. If we fail to stay at the forefront of innovative products, we may be unable to compete effectively. Advances or products developed by our competitors may render our products obsolete, less competitive or not economical.

| 10 |

WE MAY FACE PRODUCT LIABILITY CLAIMS. Due to the nature of our business, we may face claims for product liability. These claims may arise from the adverse conditions or reactions to the use of our products. While we feel confident in health benefits of our products, we cannot provide assurances that product liability claims will arise in the future.

Moreover, litigation or adverse publicity resulting from these allegations could materially and adversely affect our business, regardless of whether the allegations are valid or whether we are liable. Currently we have no product liability insurance coverage, and even if there was such coverage, there would be no assurance that such coverage would be sufficient to properly protect us. Further, claims of this type, whether substantiated or not, may divert our financial and management resources from revenue generating activities and the business operation.

Presently, we do not have insurance to cover any product liability claims. This lack of insurance may cause a material adverse impact on the Company if product liability claims arise.

INEFFECTIVE RISK MANAGEMENT POLICIES AND PROCEDURES. The Company relies on a combination of technical and human factors to protect the Company against risks. Its policies, procedures and practices are used to identify, monitor and control a variety of risks, including risks related to human error and hardware and software errors. The Company’s standard of operations has been developed internally. These risk-management methods may not adequately prevent losses and may not protect us against all risks, in which case our business, economic conditions, operations and cash flows may be materially adversely affected.

WE WILL NEED ADDITIONAL FINANCING IN ORDER TO GROW OUR BUSINESS. We do not have significant assets with which to expand our business. We intend to expand our business through increased marketing efforts in Malaysia and elsewhere of our blood based genomic screening process. These additional expenditures are intended to be funded from cash on hand and, if necessary, third party sources, including the incurring of debt and/or the sale of additional equity securities. In addition to requiring additional financing to fund expansion, the Company may require additional financing to fund working capital and operating losses in the future should the need arise. The incurrence of debt creates additional financial leverage and therefore an increase in the financial risk of the Company’s operations. The sale of additional equity securities will be dilutive to the interests of current equity holders. In addition, there can be no assurance that such additional financing, whether debt or equity, will be available to the Company or that it will be available on acceptable commercial terms. Any inability to secure such additional financing on appropriate terms could have a materially adverse impact on the business, financial condition and operating results of the Company.

| 11 |

WE AND OUR VENDORS ARE SUBJECT TO LAWS AND REGULATIONS THAT COULD REQUIRE US TO MODIFY OUR CURRENT BUSINESS PRACTICES AND INCUR INCREASED COSTS, WHICH COULD HAVE A MATERIAL ADVERSE EFFECT ON OUR BUSINESS, FINANCIAL CONDITION AND RESULTS OF OPERATIONS. In our industry, we are subject to numerous laws and regulations, including labor, employment and taxation laws to which most retailers are typically subject to. The formulation, manufacturing, packaging, labelling, distribution, sale and storage of our products are subject to extensive regulation by various federal agencies and regulatory bodies. If we fail to comply with those regulations, we would subject to significant penalties or claims, which would harm our business operations. In addition, the adoption of new regulations or changes in the interpretations of existing regulations may result in significant compliance costs or discontinuation of product sales and may impair the marketability of our products, resulting in significant loss of net sales. Our failure to comply with regulations may result in enforcement actions and imposition of penalties or otherwise harm the distribution and sale of our products.

WE EXPECT OUR NET SALES AND OPERATING RESULTS TO VARY SIGNIFICANTLY FROM QUARTER TO QUARTER. A number of factors will influence our sales and results, including changes in:

| ● | General economic conditions; | |

| ● | The demand for our products; | |

| ● | Our ability to retain, grow our business and attract new clients; | |

| ● | Administrative costs; | |

| ● | Advertising and other marketing costs; |

AS A RESULT OF THE VARIABILITY OF THESE AND OTHER FACTORS, OUR OPERATING RESULTS IN FUTURE QUARTERS MAY BE BELOW THE EXPECTATIONS OF PUBLIC MARKET ANALYSTS AND INVESTORS. If we fail to maintain a quality service and value, our sales are likely to be negatively affected. Our success depends on the safety and hygiene product that we produce through our in house manufacturing company. Our future customers will identify our product with a certain level of quality and value. If we could not meet this perceived value or level of quality, we may be negatively affected and our operating results may suffer.

THE SUCCESS OF OUR BUSINESS DEPENDS ON OUR ABILITY TO MAINTAIN AND ENHANCE OUR REPUTATION AND BRAND. We believe that our reputation in the healthcare industry is of significant importance to the success of our business. A well-recognized brand is critical to increasing our customer base and, in turn, increasing our revenue. Since the healthcare industry is highly competitive, our ability to remain competitive depends to a large extent on our ability to maintain and enhance our reputation and brand, which could be difficult and expensive. To maintain and enhance our reputation and brand, we need to successfully manage many aspects of our business, such as cost- effective marketing campaigns to increase brand recognition and awareness in a highly competitive market.

We will continue to conduct various marketing and brand promotion activities. We cannot assure you, however, that these activities will be successful and achieve the brand promotion goals we expect. If we fail to maintain and enhance our reputation and brand, or if we incur excessive expenses in our efforts to do so, our business, financial conditions and results of operations could be adversely affected.

BUSINESS DISRUPTIONS COULD SERIOUSLY HARM OUR FUTURE REVENUE AND FINANCIAL CONDITION AND INCREASE OUR COSTS AND EXPENSES. Our operations could be subject to power shortages, telecommunications failures, wildfires, water shortages, floods, earthquakes, hurricanes, typhoons, fires, extreme weather conditions, medical epidemics, including the current COVID-19 virus, and other natural or man-made disasters or business interruptions. The occurrence of any of these business disruptions could seriously harm our operations and financial condition and increase our costs and expenses. Unfavorable global economic conditions could adversely affect our business, financial condition, or results of operations.

| 12 |

We do not carry insurance for all categories of risk that our business may encounter. Although we intend to obtain some form of business interruption insurance in the future, there can be no assurance that we will secure adequate insurance coverage or that any such insurance coverage will be sufficient to protect our operations to significant potential liability in the future. Any significant uninsured liability may require us to pay substantial amounts, which would adversely affect our financial position and results of operations.

WE MAY INCUR SIGNIFICANT COSTS TO BE A PUBLIC COMPANY TO ENSURE COMPLIANCE WITH U.S. CORPORATE GOVERNANCE AND ACCOUNTING REQUIREMENTS AND WE MAY NOT BE ABLE TO ABSORB SUCH COSTS. We may incur significant costs associated with our public company reporting requirements, costs associated with newly applicable corporate governance requirements, including requirements under the Sarbanes-Oxley Act of 2002 and other rules implemented by the Securities and Exchange Commission. We expect these costs to approximate $50,000 per year, consisting of $25,000 in legal, $20,000 in audit and $5,000 for EDGAR filing and transfer agent fees. We expect all of these applicable rules and regulations to significantly increase our legal and financial compliance costs and to make some activities more time consuming and costly. We may not be able to cover these costs from our operations and may need to raise or borrow additional funds. We also expect that these applicable rules and regulations may make it more difficult and more expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified individuals to serve on our board of directors or as executive officers. We are currently evaluating and monitoring developments with respect to these newly applicable rules, and we cannot predict or estimate the amount of additional costs we may incur or the timing of such costs. In addition, we may not be able to absorb these costs of being a public company which will negatively affect our business operations.

OUR SOLE OFFICER AND DIRECTOR MAY HAVE A CONFLICT OF INTEREST WITH THE MINORITY SHAREHOLDERS AT SOME TIME IN THE FUTURE. SINCE THE MAJORITY OF OUR SHARES OF COMMON STOCK ARE OWNED BY OUR SOLE OFFICER AND DIRECTOR, OUR OTHER STOCKHOLDERS MAY NOT BE ABLE TO INFLUENCE CONTROL OF THE COMPANY OR DECISION MAKING BY MANAGEMENT OF THE COMPANY. Our sole officer and director beneficially owns approximately 77.18% of our outstanding common stock. The interests of our sole officer and director may not be, at all times, the same as that of our other shareholders. He is not a passive investor but also is an executive of the Company, his interests as an executive may, at times, be adverse to those of passive investors. Where those conflicts exist, our shareholders will be dependent upon our sole director exercising, in a manner fair to all of our shareholders, their fiduciary duties as officers or as member of the Company’s Board of Directors. Also, our director will have the ability to control the outcome of most corporate actions requiring shareholder approval, including the sale of all or substantially all of our assets and amendments to our articles of incorporation. This concentration of ownership may also have the effect of delaying, deferring or preventing a change of control of us, which may be disadvantageous to minority shareholders.

BECAUSE OUR OFFICERS AND DIRECTORS MAY IN FUTURE HAVE OUTSIDE BUSINESS ACTIVITIES, THERE IS A POTENTIAL CONFLICT OF INTEREST, INCLUDING THE AMOUNT OF TIME THEY WILL BE ABLE TO DEDICATE TO THE COMPANY. Currently our sole officer, who is also a director, have been working on promoting business for the Company. A potential conflict of interest may arise in the future that may cause our business to fail, including conflicts of interest in allocating their time to our company and their other business interests. While our officers have verbally agreed to devote sufficient time and attention to the affairs of the Company, we have no written arrangement with our officers regarding this matter. As a result, we may face conflicts between business decisions that they may have to make regarding our operations and that of their other business interests.

| 13 |

BECAUSE OUR MANAGEMENT DOES NOT HAVE PRIOR EXPERIENCE RUNNING A PUBLIC COMPANY, WE MAY HAVE TO HIRE INDIVIDUALS OR SUSPEND OR CEASE OPERATIONS. Because our management has limited prior experience in running a public company, including the preparation of reports under the Securities Act of 1934, we may have to hire additional experienced personnel to assist us with the preparation thereof. If we need the additional experienced personnel and we do not hire them, we could fail in our plan of operations and have to suspend operations or cease operations entirely.

INDEPENDENT AUDIT COMMITTEE. Although the common stock is not listed on any national securities exchange, for purposes of independence we use the definition of independence applied by NASDAQ. Currently, the Company has no independent audit committee. The full board of directors’ functions as audit committee and is comprised of three directors, one of whom is considered to be “independent” in accordance with the requirements set forth in NASDAQ Listing Rule 5605(a)(2). An independent audit committee plays a crucial role in the corporate governance process, assessing our Company’s processes relating to our risks and control environment, overseeing financial reporting, and evaluating internal and independent audit processes. The lack of an independent audit committee may prevent the board of directors from being independent from management in its judgments and decisions and its ability to pursue the responsibilities of an audit committee without undue influence. We may have difficulty attracting and retaining directors with the requisite qualifications. If we are unable to attract and retain qualified, independent directors, the management of the business could be compromised. An independent audit committee is required for listing on any national securities exchange; therefore, until such time as we meet the audit committee independence requirements of a national securities exchange, we will be ineligible for listing on any national securities exchange.

POTENTIAL DATA BREACHES. If we are successful, our services will generate and process a large quantity of personal health condition data. We face risks inherent in handling large volumes of data and in protecting the security of such data. In particular, we face a number of challenges relating to data inter-connected with regional labs, including:

| ● | protecting the data in and hosted on our system, including against hacking on our system by outside parties or our employees; |

| ● | addressing concerns related to privacy and sharing, safety, security and others; |

| ● | complying with applicable laws, rules and regulations relating to the collection, use, disclosure of personal information, including any requests from regulatory and government authorities relating to such data; |

| ● | Any systems failure or security breach or lapse that results in the release of user data could harm our reputation and brand and, consequently, our business, in addition to exposing us to potential legal liability. |

As we expand our operations, we may be subject to these laws in other jurisdictions where our customers and other participants are located. The laws, rules and regulations of other jurisdictions may impose more stringent or conflicting requirements and penalties than those in Malaysia, compliance with which could require significant resources and costs. Our privacy policies and practices concerning the collection, use and disclosure of user data are posted on our websites. Any failure, or perceived failure, by us to comply with our posted privacy policies or with any regulatory requirements or privacy protection-related laws, rules and regulations could result in proceedings or actions against us by authorities or others. These proceedings or actions may subject us to significant penalties and negative publicity, require us to change our business practices, increase our costs and severely disrupt our business.

| 14 |

CROSS-BORDER OPERATIONS. As we plan to continue expanding our existing cross-border operations into existing and other markets, we will face risks associated with expanding into markets in which we have limited or no experience and in which our company may be less well-known. We may be unable to attract a sufficient number of customers and other participants, fail to anticipate competitive conditions or face difficulties in operating effectively in these new markets. The expansion of our cross-border business will also expose us to risks relating to staffing and managing cross-border operations, increased costs to protect intellectual property, tariffs and other trade barriers, differing and potentially adverse tax consequences, increased and conflicting regulatory compliance requirements, lack of acceptance of our service offerings, challenges caused by distance, language and cultural differences, exchange rate risk and political instability. Accordingly, any efforts we make to expand our cross-border operations may not be successful, which could limit our ability to grow our revenue, net income and profitability.

RISKS RELATED TO DOING BUSINESS IN ASIA PACIFIC REGION. Changes in the political and economic policies of the local government may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies. Accordingly, our financial condition and results of operations are affected to a significant extent by economic, political and legal developments in Asia Pacific region.

The Asia Pacific economy differs from the economies of most developed countries in many respects, including the extent of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. In addition, the government continues to play a significant role in regulating industry development by imposing industrial policies. The government also exercises significant control over economic growth by allocating resources, controlling payment of foreign currency-denominated obligations, setting monetary policy, regulating financial services and institutions and providing preferential treatment to particular industries or companies.

The local government has implemented various measures to encourage economic growth and guide the allocation of resources. Some of these measures may benefit the overall economy, but may also have a negative effect on us. Our financial condition and results of operation could be materially and adversely affected by government control over capital investments or changes in tax regulations that are applicable to us. In addition, the government has implemented in the past certain measures, including interest rate increases, to control the pace of economic growth. These measures may cause decreased economic activity, which in turn could lead to a reduction in demand for our services and consequently have a material adverse effect on our businesses, financial condition and results of operations.

YOU MAY EXPERIENCE DIFFICULTIES IN EFFECTING SERVICE OF LEGAL PROCESS, ENFORCING FOREIGN JUDGMENTS OR BRINGING ORIGINAL ACTIONS IN MALAYSIA BASED ON UNITED STATES OR OTHER FOREIGN LAWS AGAINST US OR OUR MANAGEMENT. Our operating subsidiary is incorporated in Malaysia and conducts substantially all of our operations in Asia Pacific. All of our executive officers and directors reside outside the United States and all of their assets are located outside of the United States. As a result, it may be difficult or impossible for shareholders to bring an action against us or against these individuals in Malaysia in the event that you believe that your rights have been infringed under the securities laws of the United States or otherwise. Even if you are successful in bringing an action of this kind, the laws of Malaysia may render you unable to enforce a judgment against our assets or the assets of our directors and officers. There is no statutory recognition in Malaysia of judgments obtained in the United States, although the courts of Malaysia will generally recognize and enforce a non-penal judgment of a foreign court of competent jurisdiction without retrial on the merits. The rights of shareholders to take legal action against us and our directors, actions by minority shareholders and the fiduciary responsibilities of our directors are to a large extent governed by the common law of Malaysia. The common law of Malaysia is derived in part from comparatively limited judicial precedent in Malaysia as well as from English common law, which provides persuasive, but not binding, authority in a court in Malaysia. The rights of our shareholders and the fiduciary responsibilities of our directors under Malaysian law are not as clearly established as they would be under statutes or judicial precedents in the United States. In particular, Malaysia has a less developed body of securities laws than the United States and provides significantly less protection to investors. As a result, our public shareholders may have more difficulty in protecting their interests through actions against us, our management, our directors or our major shareholders than would shareholders of a corporation incorporated in a jurisdiction in the United States.

| 15 |

Risks Related to Our Common Stock

SALES OF OUR COMMON STOCK IN RELIANCE ON RULE 144 MAY REDUCE PRICES IN THAT MARKET BY A MATERIAL AMOUNT. A significant number of the outstanding shares of our common stock are “restricted securities” within the meaning of Rule 144 under the Securities Act. As restricted securities, those shares may be resold only pursuant to an effective registration statement or pursuant to the requirements of Rule 144 or other applicable exemptions from registration under the Securities Act and as required under applicable state securities laws. Rule 144 provides in essence that an affiliate (i.e., an officer, director or control person) who has held restricted securities for a prescribed period may, under certain conditions, sell every three months, in brokerage transactions, a number of shares that does not exceed 1.0% of the issuer’s outstanding common stock. The alternative limitation on the number of shares that may be sold by an affiliate, which is related to the average weekly trading volume during the four calendar weeks prior to the sale is not available to stockholders of companies whose securities are not traded on an “automated quotation system”; because the OTC-QB Market is not such a system, market-based volume limitations are not available for holders of our securities selling under Rule 144.

Pursuant to the provisions of Rule 144, there is no limit on the number of restricted securities that may be sold by a non-affiliate (i.e., a stockholder who has not been an officer, director or control person for at least 90 consecutive days before the date of the proposed sale) after the restricted securities have been held by the owner for a prescribed period, although there may be other limitations and/or criteria to satisfy. A sale pursuant to Rule 144 or pursuant to any other exemption from the Securities Act, if available, or pursuant to registration of shares of our common stock held by our stockholders, may reduce the price of our common stock in any market that may develop.

YOU MAY NOT BE ABLE TO LIQUIDATE YOUR INVESTMENT SINCE THERE IS NO ASSURANCE THAT A PUBLIC MARKET WILL DEVELOP FOR OUR COMMON STOCK OR THAT OUR COMMON STOCK WILL EVER BE APPROVED FOR TRADING ON A RECOGNIZED EXCHANGE. There is no established public trading market for our securities. Although we intend to be quoted on the OTC-QB Market in the United States, our shares are not and have not been quoted on any exchange or quotation system. We cannot assure you that a market maker will agree to file the necessary documents with the FINRA, nor can there be any assurance that such an application for quotation will be approved or that a regular trading market will develop or that if developed, will be sustained. In the absence of a trading market, an investor may be unable to liquidate its investment, which will result in the loss of your investment.

OUR COMMON STOCK IS SUBJECT TO THE “PENNY STOCK” RULES OF THE SEC AND THE TRADING MARKET IN OUR SECURITIES IS LIMITED, WHICH MAKES TRANSACTIONS IN OUR STOCK CUMBERSOME AND MAY REDUCE THE VALUE OF AN INVESTMENT IN OUR STOCK. Under U.S. federal securities legislation, our common stock will constitute “penny stock”. Penny stock is any equity security that has a market price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require that a broker or dealer approve a potential investor’s account for transactions in penny stocks, and the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve an investor’s account for transactions in penny stocks, the broker or dealer must obtain financial information and investment experience objectives of the person, and make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prepared by the Commission relating to the penny stock market, which, in highlight form sets forth the basis on which the broker or dealer made the suitability determination. Brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock. Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

| 16 |

IN THE FUTURE, WE MAY ISSUE ADDITIONAL COMMON AND PREFERRED SHARES, WHICH WOULD REDUCE INVESTORS’ PERCENT OF OWNERSHIP AND MAY DILUTE OUR SHARE VALUE. Our Articles of Incorporation authorize the issuance of 600,000,000 shares of common stock. As of the date of this filing, the Company had 362,905,561 shares of common stock outstanding. Accordingly. In addition, we have the right to issue 20,000,000 shares of preferred stock. The preferred stock is known as “blank check” as the Board of Directors is authorized to set the rights, privileges and preference of the preferred stock. The future issuance of common stock and preferred may result in substantial dilution in the percentage of our common stock held by our then existing shareholders. We may value any common stock issued in the future on an arbitrary basis. The issuance of common stock or preferred stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common stock.

WE ARE NOT A FULLY REPORTING COMPANY UNDER SECTION 12(G) OF THE SECURITIES EXCHANGE ACT OF 1934, RATHER WE WILL BE SUBJECT TO THE REPORTING REQUIREMENTS OF SECTION 15(D) OF THE EXCHANGE ACT WHICH IS LESS RESTRICTIVE ON US AND OUR INSIDERS. In order for us to become a fully reporting company under Section 12(g) of the Exchange Act, we will have to file a Registration Statement on Form 8-A. If we do not become subject to Section 12 of the Exchange Act, we will be subject to Section 15(d) of the Exchange Act, and as such we will not be required to comply with (i) the proxy statement requirements which means shareholders may have less notice of pending matters, and (ii) the Williams Act which requires disclosure of persons or groups that acquire 5% of a company’s publicly traded stock and also regulates tender offers. In addition, our officer, director and 10% stockholder will not be required to submit reports to the SEC on their stock ownership and stock trading activity. These reports include Form 3, 4 and 5. Therefore, as a shareholder, less information and disclosure concerning these matters will be available to you.

WE DO NOT INTEND TO PAY ANY CASH DIVIDENDS ON OUR COMMON STOCK, OUR STOCKHOLDERS WILL NOT BE ABLE TO RECEIVE A RETURN ON THEIR SHARES UNLESS THEY SELL THEM. We intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares unless they sell them. There is no assurance that stockholders will be able to sell shares when desired.

OUR COMMON STOCK PRICE IS LIKELY TO BE HIGHLY VOLATILE WHICH MAY SUBJECT US TO SECURITIES LITIGATION THEREBY DIVERTING OUR RESOURCES WHICH MAY AFFECT OUR PROFITABILITY AND RESULTS OF OPERATION. The market price for our common stock is likely to be highly volatile as the stock market in general and the market for Internet-related stocks.

| 17 |

The following factors will add to our common stock price’s volatility:

| - | fluctuations in our quarterly financial results or the quarterly financial results of companies perceived to be similar to us; | |

- |

changes in estimates of our financial results or recommendations by securities analysts; | |

| - | changes in market valuations of similar companies; | |

| - | changes in our capital structure, such as future issuances of securities or the incurrence of additional debt; | |

| - | regulatory developments in Malaysia or other countries wherein we expect to conduct business; | |

- |

litigation involving our company, our general industry or both; | |

| - | investors’ general perception of us; and | |

| - | changes in general economic, industry and market conditions. |

Many of these factors are beyond our control. These factors may decrease the market price of our common stock, regardless of our operating performance. In the past, plaintiffs have initiated securities class action litigation against a company following periods of volatility in the market price of its securities. In the future, we may be the target of similar litigation. Securities litigation could result in substantial costs and liabilities and could divert management’s attention and resources.

REDUCED DISCLOSURE REQUIREMENTS APPLICABLE TO EMERGING GROWTH COMPANIES MAY MAKE OUR COMMON STOCK LESS ATTRACTIVE TO INVESTORS. We qualify as an “emerging growth company” under the JOBS Act. As a result, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements. For so long as we are an emerging growth company, we will not be required to:

| ● | have an auditor report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; |

| ● | comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

| ● | submit certain executive compensation matters to shareholder advisory votes, such as “say-on-pay” and “say-on-frequency;” and |

| ● | disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the CEO’s compensation to median employee compensation. |

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We will remain an emerging growth company for up to five full fiscal years, although if the market value of our common stock that is held by non-affiliates exceeds $700 million as of any January 31 before that time, we would cease to be an emerging growth company as of the following December 31, or if our annual revenues exceed $1 billion, we would cease to be an emerging growth company the following fiscal year, or if we issue more than $1 billion in non-convertible debt in a three-year period, we would cease to be an emerging growth company immediately.

| 18 |

Notwithstanding the above, we are also currently a “smaller reporting company,” meaning that we are not an investment company, an asset-backed issuer, nor a majority-owned subsidiary of a parent company that is not a smaller reporting company, and has a public float of less than $75 million and annual revenues of less than $50 million during the most recently completed fiscal year. If we are still considered a “smaller reporting company” at such time as we cease to be an “emerging growth company,” we will be subject to increased disclosure requirements. However, the disclosure requirements will still be less than they would be if we were not considered either an “emerging growth company” or a “smaller reporting company.” Specifically, similar to “emerging growth companies”, “smaller reporting companies” are able to provide simplified executive compensation disclosures in their filings; are exempt from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that independent registered public accounting firms provide an attestation report on the effectiveness of internal control over financial reporting; are not required to conduct say-on-pay and frequency votes until annual meetings occurring on or after January 21, 2015; and have certain other decreased disclosure obligations in their SEC filings, including, among other things, only being required to provide two years of audited financial statements in annual reports. Decreased disclosures in its SEC filings due to its status as an “emerging growth company” or “smaller reporting company” may make us less attractive to investors given that it will be harder for investors to analyze the Company’s results of operations and financial prospects and, as a result, it may be difficult for us to raise additional capital as and when we need it.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

Our properties are located at No. 9 & 10, Jalan P4/8B, Bandar Teknologi Kajang, 43500 Semenyih, Selangor Darul Ehsan, Malaysia. The real estate is owned by Bio Life Neutraceuticals Sdn Bhd., one of our tiered subsidiaries. We acquired the property in June 2016. The property was pledged to Maybank Islamic Berhad under a bank loan in the principal amount of $935,500USD at 4% interest. The facility requires equal monthly instalment payments of $4,492USD for a term of 20 years. The property is two, three story buildings, each consisting of roughly 1,714 square meters.

There are presently no pending legal proceedings to which the Company or any of its property is subject, or any material proceedings to which any director, officer or affiliate of the Company, any owner of record or beneficially of more than five percent of any class of voting securities is a party or has a material interest adverse to the Company, and no such proceedings are known to the Company to be threatened or contemplated against it.

ITEM 4. MINE SAFETY DISCLOSURES.

None.

| 19 |

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Market Information

As of the date of this filing, we have not applied to FINRA for the symbol, at the moment there is no established public market for our common stock, and a public market may never develop. In addition, there may never be substantial activity in such market. If there is substantial activity, such activity may not be maintained, and no prediction can be made as to what prices may prevail in such market.

If we become able to have our shares of common stock quoted on the OTC-QB tier of OTC Markets, we will then try, through a broker-dealer and its’ clearing firm, to become eligible with the DTC to permit our shares to be traded electronically. If an issuer is not “DTC-eligible,” its shares cannot be electronically transferred between brokerage accounts, which, based on the realities of the marketplace as it exists today (especially OTC Markets), means that shares of an issuer will not be able to be traded (technically the shares can be traded manually between accounts, but this may take days and is not a realistic option for issuers relying on broker-dealers for stock transactions - like all the companies on the OTC Markets). What this means is that while DTC-eligibility is not a requirement to trade on the OTC Markets, it is however a necessity to efficiently process trades on the OTC Markets if a company’s stock is going to trade with any volume. There are no assurances that our shares will ever become DTC-eligible or, if they do, how long it may take.

Capital Stock

Our authorized capital stock consists of 600,000,000 shares of common stock, no par value per share, and 20,000,000 shares of preferred stock, no par value per share. As of the date of this filing, there are 362,905,561 shares of our common stock issued and outstanding that was held by 163 stockholders of record and no shares of preferred stock issued and outstanding. The shares of preferred stock are “blank check’ meaning the Company’s Board of Directors can issue shares of preferred stock in such series with such rights, privileges and preferences as determined from time to time by the Board of Directors without shareholder approval.

Dividend Policy

The Company has not declared or paid any cash dividends on its Common Stock and does not intend to declare or pay any cash dividend in the foreseeable future. The payment of dividends, if any, is within the discretion of the Board of Directors and will depend on the Company’s earnings, if any, its capital requirements and financial condition and such other factors as the Board of Directors may consider.

Securities Authorized for Issuance under Equity Compensation Plans

The Company does not have any equity compensation plans or any individual compensation arrangements with respect to its Common Stock or Preferred Stock. The issuance of any of our Common Stock or Preferred Stock is within the discretion of our Board of Directors, which has the power to issue any or all of our authorized but unissued shares without stockholder approval.

Recent Sales of Unregistered Securities

None

ITEM 6. SELECTED FINANCIAL DATA.

As a “smaller reporting company” as defined by Rule 12b-2 of the Exchange Act, the Company is not required to provide this information.

| 20 |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

GENERAL

Our Company was incorporated in April 2017. Consequently, the following discussion and analysis of the results of operations and financial condition of the Company is for fiscal years ended December 31, 2019 and December 31, 2018, respectively. This information should be read in conjunction with the notes to the financial statements that are included elsewhere herein. The consolidated financial statements presented herein (and to which this discussion relates) reflect the results of operations of the Company and its Malaysian subsidiary. Our discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors. We use words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions to identify forward-looking statements. We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, except as required by law. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this quarterly report, which are designed to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

Company Overview

Our financial statements are prepared in US Dollars and in accordance with accounting principles generally accepted in the United States. See information immediately below for information concerning the exchange rates at the Malaysian translated into US Dollars (“USD”) at various pertinent dates and for pertinent periods.

Translation of amounts from the local currency of the Company into US$1 has been made at the following exchange rates for the respective years:

| As of and for the year ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| Year-end MYR : US$1 exchange rate | 4.0925 | 4.1385 | ||||||

| Yearly average MYR : US$1 exchange rate | 4.1427 | 4.0352 | ||||||

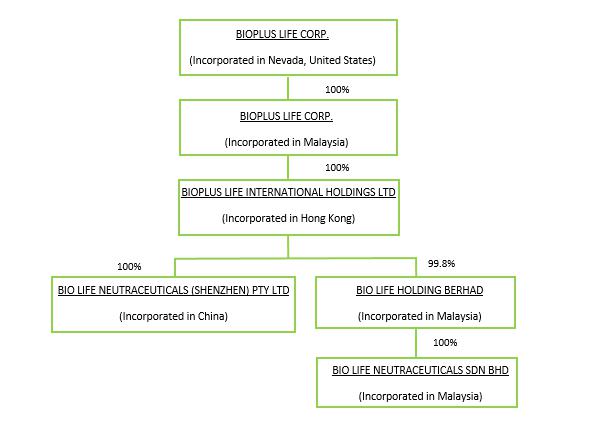

Bioplus Life Corp., a Nevada corporation (“Company”), was incorporated under the laws of the State of Nevada on April 13, 2017. On July 10, 2017, the Company acquired 100% of the equity interests of Bioplus Life Corp., a Malaysian company. On July 19, 2017, the Company, through its Malaysian subsidiary, Bioplus Life Corp., acquired 100% of the equity interests of Bioplus Life International Holdings Ltd, a Hong Kong company. On October 27, 2017, the Company through its Hong Kong subsidiary, Bioplus Life International Holdings Ltd, acquired 100% equity interest of Bioplus Life Corp. (ShenZhen), a company incorporated in China.

On June 11, 2018, the Company through its subsidiary in Hong Kong, Bioplus Life International Holdings Ltd, acquired 99.8% equity interest of Bio Life Holdings Berhad, a company incorporated in Malaysia. Bio Life Holdings Berhad owns 100% of the equity interests of Bio Life Neutraceuticals Sdn. Bhd., a company incorporated in Malaysia.

| 21 |

Summary of Business

Bioplus Life Corp., through its wholly owned subsidiaries, specializing in manufacturing and selling health and beauty care products. Our corporate complex is located at No. 9 and No. 10, Jalan P4/8B, Bandar Teknologi Kajang, 43500 Semenyih, Selangor Darul Ehsan, Malaysia, which are two adjoining commercial structures. Our corporate offices are located in the No. 9 building. Our manufacturing facilities comprise the remainder of the space in both buildings.

Our website is http://www.bionutry.com and our phone number is +60 3 8703 2020.

| 22 |

RESULTS OF OPERATIONS

Results of Operations for the Year Ended December 31, 2019 Compared to the Year Ended December 31, 2018 (Audited).

The following table sets forth key components of the results of operations for fiscal year ended December 31, 2019 and 2018, respectively. The discussion following the table addresses these results.

| Year

ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| REVENUE | $ | 1,722,209 | $ | 2,470,492 | ||||

| COST OF REVENUE | (914,739 | ) | (1,311,646 | ) | ||||

| GROSS PROFIT | 807,470 | 1,158,846 | ||||||

| OTHER INCOME | 21,143 | 3,540 | ||||||

| OPERATING EXPENSES | ||||||||

| General and operating expenses | (855,274 | ) | (1,154,532 | ) | ||||

| Finance cost | (33,242 | ) | (35,879 | ) | ||||

| TOTAL EXPENSES | (888,516 | ) | (1,190,411 | ) | ||||

| LOSS FROM OPERATIONS | (59,903 | ) | (28,025 | ) | ||||

| Income tax expense | (33,289 | ) | (82,319 | ) | ||||

| NET LOSS | $ | (93,192 | ) | $ | (110,344 | ) | ||

| Other comprehensive income: | ||||||||

| Foreign currency translation gain/(loss) | 32,702 | (95,519 | ) | |||||

| COMPREHENSIVE LOSS | $ | (60,490 | ) | $ | (205,863 | ) | ||

Revenues. For the annual period ended December 31, 2019, we had revenues of $1,722,209 as compared to revenues of $2,470,492 for the annual period ended December 31, 2018, a decrease of approximately 30.2% from the prior annual period. The decrease in revenues for the current annual period is due to economic slowdown has caused the reduced in demand from wholesalers and retailers.

Cost of revenues. For the annual period ended December 31, 2019, we had cost of revenues of $914,739, as compared to cost of revenues of $1,311,646 for the annual period ended December 31, 2018, a decrease of approximately 30% from the prior annual period. The decrease in cost of revenues for the current year end period reflects the reduction in product sales for the same year end period.

Other Income. For the annual period ended December 31, 2019, we had other income of $21,143, as compared $3,540 for the annual period ended December 31, 2018. The increase in other income for the current annual period is due to gain arising from disposal of motor vehicle. We did not have a similar transaction in the prior year end period.

| 23 |

Operating Expenses. For the annual period ended December 31, 2019, we had total operating expenses of $888,516, as compared to total operating expenses of $1,190,411 for the annual period ended December 31, 2018, a decrease of approximately 24.5%. Operating expenses consists of general and operating expenses which includes depreciation of fixed assets, stock grants to officers/directors, shares issuances to service providers, employee compensation and benefits, professional fees and marketing and travel expenses. The decrease in general and operating expenses for the current year period reflects decrease in bad debt written off, and a reduction in commission paid due to reduced sales and bonus payments to staff and officers.

Loss from operations. We had a loss from operations of $59,903 for the annual period ended December 31, 2019 compared with a loss from operations of $28,025 for the annual period ended December 31, 2018 for the reasons discussed above.

Tax expense. For the year ended December 31, 2019, we had income tax expense of $33,289 compared with income tax expense of $82,319 for the prior annual period. The decrease in this expense for the current year end period is due to decrease in deferred tax.

Foreign currency translation gain/loss. For the annual period ended December 31, 2019, we had foreign currency translation gain of $32,702 compared with foreign currency translation loss $95,519 for the prior annual period. Foreign currency translation gain/loss represents the movement of the US Dollar against the Malaysian Ringgit.

LIQUIDITY AND CAPITAL RESOURCES

As of December 31, 2019, we had working capital of $206,903 compared with working capital of $307,651 as of December 31, 2018.

Our primary uses of cash have been for operations. The main sources of cash have been from operational revenues and the private placement of our common stock. The following trends are reasonably likely to result in a material decrease in our liquidity over the near to long term:

| ● | Addition of administrative and marketing personnel as the business grows, |

| ● | Development of a Company website, |

| ● | Increases in advertising and marketing in order to attempt to generate more revenues, and |

| ● | The cost of being a public company. |

Chong Khooi You, President/CEO, a major shareholder of the Company, has undertaken to financially support the company so that the Company will be sufficient to sustain its current level of operation for at least the next 12 months of operations. In this respect, Company has the ability to continue as a going concern, if the Company is unable to obtain adequate capital. The accompanying financial statements do not include any adjustments to reflect the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

| 24 |

Summary of Cash Flows

The following is a summary of the Company’s cash flows from operating and financing activities for the years ended December 31, 2019 and 2018:

| For the year ended December 31, | ||||||||

| (in Thousands) | 2019 | 2018 | ||||||

| Cash and cash equivalents beginning of year | $ | 255,554 | $ | 175,073 | ||||

| Net cash flow provided by/(used in): | ||||||||

| Operating activities | (146,845 | ) | (146,453 | ) | ||||

| Investing activities | (58,557 | ) | (205,276 | ) | ||||

| Financing activities | 20,822 | 523,842 | ||||||

| Foreign currency translation adjustment | (1,754 | ) | (91,632 | ) | ||||

| Net cash increase (decrease) for the year | (186,334 | ) | 80,481 | |||||

| Cash, end of the year | $ | 69,220 | $ | 255,554 | ||||

Operating Activities

During the year ended December 31, 2019, the Company incurred a loss from operations of $59,903 which, after adjusting for depreciation and interest expense, and changes in operating assets and liabilities, resulted in net cash of $146,845 being used in operating activities during the year. By comparison, during the year ended December 31, 2018, the Company incurred a loss from operations of $28,025 which, after adjusting for depreciation and interest expense, and changes in operating assets and liabilities, resulted in net cash of $146,453 in operating activities during the period. Although there amount for both annual period was relatively flat, there was movement in amounts due from directors, amounts due from related parties and other receivables, deposits and prepayments, among others.

Investing Activities

During the year ended December 31, 2019, cash flow from investing activities consisted of purchase of the property, plant and equipment of $(58,557) compared with similar purchases of $(205,276) for the prior year end period. The difference is due to a reduction in corporate asset investments.

Financing Activities

For the year ended December 31, 2019, the cash provided by financing activities primarily consisted of the receipt of application funds $104,000, offset by $(33,242) in interest expense, $(21,743) in repayment of loans and $(28,193) in repayment of purchase borrowing. For the year ended December 31, 2018, the cash provided by financing activities primarily consisted of proceeds from stock issuances of $585,000 offset by offset by $(35,879) in interest expense, $(39,445) in repayment of loans and $(26,519) in repayment of purchase borrowing.

Our financial statements reflect the fact that we have sufficient revenue to cover our operating expenses for the next 12 months, although at present time, we are under-capitalized. The Company intends to continue with capital investment or other financing to fund its marketing/ promotional campaigns and the expansion of production capacity for 2020 and beyond to achieve a 20% to 30% increase in revenues in Malaysia, China, India and African markets. If continued funding and capital resources are unavailable at reasonable terms, the Company may not be able to implement its expansion plan.

| 25 |

Summary of Significant Accounting Policies

| ● | Basis of presentation |

These accompanying financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”).

| ● | Use of estimates |