UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

(Mark One)

or

Commission File Number:

(Exact name of registrant as specified in its charter) |

| ||

(State or Other Jurisdiction of Incorporation or Organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

|

| |

|

| |

|

| |

| ||

(Address of Principal Executive Offices) |

| (Zip Code) |

+1

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class |

| Trading Symbol(s) |

| Name of each exchange where registered |

|

|

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As of June 30, 2023, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $

As of December 31, 2023, there were

CONTENTS

| 2 |

| Table of Contents |

FORWARD-LOOKING STATEMENTS

Certain statements made in this Annual Report on Form 10-K are “forward-looking statements” (within the meaning of the Private Securities Litigation Reform Act of 1995) regarding the plans and objectives of management for future operations. Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements of the Registrant to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The forward-looking statements included herein are based on current expectations that involve numerous risks and uncertainties. The Company’s plans and objectives are based, in part, on assumptions involving the continued expansion of business. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of the Company. Although the Company believes its assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate and, therefore, there can be no assurance the forward-looking statements included in this Report will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by the Company or any other person that the objectives and plans of the Company will be achieved.

Unless stated otherwise, the words “we,” “us,” “our,” or “the Company” in this Annual Report collectively refers to BioNexus Gene Lab Corp., a Wyoming corporation and our wholly owned subsidiaries, MRNA Scientific Sdn. Bhd. (formerly BioNexus Gene Lab Sdn. Bhd.) (“MRNA Scientific”), and Chemrex Corporation Sdn. Bhd. (“Chemrex”), both Malaysian companies (“Subsidiaries”). “BGLC” or “BioNexus” refers to BioNexus Gene Lab Corp. “RM” refers to Malaysian Ringgit, the legal currency of Malaysia. “USD,” “US$,” or “$” refer to US dollars, the legal currency of the United States.

We acquired Chemrex on December 31, 2020, pursuant to a Share Exchange Agreement with Chemrex its shareholders. We acquired all of the issued and outstanding shares of capital stock of Chemrex from the Chemrex shareholders in exchange for 68,487,261 shares of common stock of BioNexus issued to the Chemrex shareholders.

Our principal corporate office is Unit 02, Level 10, Tower B, Avenue 3, The Vertical Business Suite II, Bangsar South, 8 Jalan Kerinchi, Kuala Lumpur, Malaysia. The MRNA Scientific Malaysia lab is located at Lab 353, Chemical Science Centre, University Science Malaysia, George Town, Penang, Malaysia and it also has a blood collection center located at 1st floor, Lifecare Medical Centre, Kuala Lumpur, Malaysia. Chemrex offices and supply hub is located at 4 Jalan CJ 1/6 Kawasan Perusahaan Cheras Jaya, Selangor, Malaysia.

Our corporate telephone number is +1 307 241 6898 and its website is www.bionexusgenelab.com. Chemrex’s telephone number is (+60) 1922-23815 and its website is www.chemrex.com.my. These websites do not form part of this Form 10-K.

| 3 |

| Table of Contents |

Item 1. Business.

Overview

The Company, through its wholly owned subsidiary Chemrex, focuses on the sale of chemical raw materials for the manufacture of industrial, medical, appliance, aero, automotive, mechanical, and electronic industries in the Southeast Asia region. These countries include Malaysia, Indonesia, Vietnam, and other countries in Southeast Asia.

In addition, the Company, through its wholly owned subsidiary, MRNA Scientific, is in the business of developing and providing safe, effective, and non-invasive liquid biopsy tests for the early detection of biomarkers that we believe are linked to diseases to minimize treatment costs and improve patient management. Our non-invasive blood tests provide analysis of changes in RNA to detect the potential risk of 11 different diseases.

Corporate History

BioNexus was incorporated in the State of Wyoming on May 12, 2017. On August 23, 2017, the Company acquired all of the outstanding capital stock of MRNA Scientific Sdn. Bhd. (formerly BioNexus Gene Lab Sdn. Bhd), a Malaysian corporation incorporated in Malaysia on April 7, 2015, which it then subsequently changed its name to MRNA Scientific Sdn. Bhd. (“MRNA Scientific”) on September 19, 2023.

On December 31, 2020, BioNexus consummated a Share Exchange Agreement with Chemrex and the Chemrex shareholders, pursuant to which we acquired all of the issued and outstanding shares of capital stock of Chemrex, which was incorporated in Malaysia on September 29, 2004, from the Chemrex shareholders in exchange for 68,487,261 shares of common stock of BioNexus issued to the Chemrex shareholders.

Initial Public Offering

On July 20, 2023, the Company entered into an underwriting agreement (the "Underwriting Agreement") with Network 1 Financial Securities, Inc., as underwriter (the "Underwriter") pursuant to which the Company agreed to issue and sell, in a firm commitment underwritten public offering by the Company (the "Offering") of 1,250,000 shares of common stock, no par value, priced at a public offering price of $4.00 per share.

In addition, pursuant to the Underwriting Agreement, the Underwriter was granted a 45-day option (the "Over-Allotment Option") to purchase up to an additional 187,500 shares of common stock at the public offering price of $4.00 per share. The Underwriter fully exercised the Over-Allotment Option on July 24, 2023.

The securities were offered by the Company pursuant to the registration statement on Form S-1 (File No. 333-269753), which was originally filed with the U.S. Securities and Exchange Commission (the "Commission") under the Securities Act of 1933, as amended, on February 14, 2023, and declared effective by the Commission on July 19, 2023.

On July 24, 2023, the Offering closed, and the Company issued and sold 1,437,500 shares of common stock, including 187,500 shares sold pursuant to the exercise of the Over-Allotment Option. The Offering was priced at $4.00 per share for total gross proceeds of $5.75 million before deducting underwriting discounts, commissions, and offering expenses. Pursuant to the Underwriting Agreement, the Underwriter received an 8% underwriting discount on the public offering price for the shares common stock. The Company therefore received net proceeds, before expenses, of $5,290,000 from the sale of the common stock. In addition, the Company issued to the Underwriter warrants to purchase up to an aggregate of 115,000 shares of the Company's common stock (the "Underwriter's Warrants") at an exercise price of $4.40 per share. The Underwriter's Warrants are exercisable from July 24, 2023 until July 24, 2028.

Reverse stock split

On June 5, 2023, the Company filed an Article of Amendment to the Articles of Incorporation with the Wyoming Secretary of State to modify the ratio of the Reverse Stock Split from one-for-ten (10) to one-for-twelve (12) (the “Revised Reverse Stock Split”). Upon effectiveness of the Revised Reverse Stock Split, every twelve (12) outstanding shares of common stock were combined into and automatically became one share of common stock. No fractional shares were issued in connection with the Revised Reverse Stock Split and all such fractional shares or odd lots (less than 100 shares to any record or beneficial holder) that were issuable in the Revised Reverse Stock Split were rounded up to the nearest whole share, or rounded up to 100 shares, respectively.

The Revised Reverse Stock Split was approved and authorized by a majority of the Company’s stockholder on May 8, 2023 and by the Board of Directors of the Company on May 8, 2023.

On July 19, 2023, the Financial Industry Regulatory Authority announced the Revised Reverse Stock Split.

| 4 |

| Table of Contents |

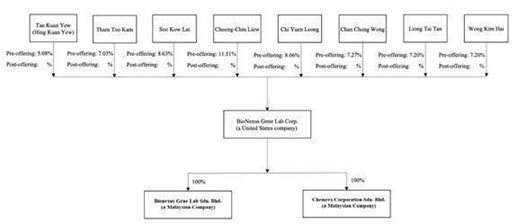

Corporate Structure

The corporate structure as of the date of this filing depicted below:

Chemical Raw Material Business

Our Products

Chemrex, our wholly owned subsidiary, is involved in the wholesale of chemical raw material products. We purchase raw chemical materials, mostly fibre re-enforced polymers (“FRP”), from domestic and international manufacturers and sell them to manufacturers in Southeast Asia. The FRP and other raw materials we offer are used to produce a wide variety of goods, including handrails, bench tops, automotive and aero parts, cleanroom panels, and covers for various instruments used in manufacturing.

A substantial portion of the Company's revenue comes from the sale of FRP products. FRP products are highly sought after by our customers due to:

| · | The material's lightweight coupled with high strength. The material's ability to be a good electrical insulator with no electro-magnetic behavior and no electric spark. |

|

|

|

| · | The material's rust-free nature and resistance to acid, alkali, organic dissolvents, and other gas and liquid mixtures. |

|

|

|

| · | The material's resistance to aging with more than 20 years of useful life under normal working conditions. |

|

|

|

| · | The material's ease of maintenance. |

| 5 |

| Table of Contents |

Chemical Raw Material Product Examples

Listed below are some examples of FRP chemical raw material products the company sells. In addition, there are both general purpose and more specific use case materials.

|

| Polyester Resin SHCP 268

SHCP 268 is a thixotropic, quick-curing unsaturated polyester resin suitable as a general-purpose resin. It can be used in generally all FRP products. However, it does not have significant structural integrity, chemical resistance, or UV resistance properties and as a result its application is limited. For example, one of the ways this material has been used is in the construction of train seats. |

|

|

|

|

| Polyester Resin 9509

This is a premium raw material compared to Polyester Resin SHCP 268 and is priced higher. Like Polyester Resin SHCP 268, it is a general-purpose material but provides more structural integrity and is longer lasting. Customers have used this material to produce marine boats and water slides. |

|

|

|

|

| Polyester Resin 2802

This is also a more premium grade of resin. It has a niche use case and is generally used as a key component in the pultrusion process by certain manufacturers. |

Chemical Raw Material Product Applications

Our chemicals are used to produce a wide variety of finished goods. Common products utilizing our FRP materials include handrails, bench tops, automotive and aero parts, panelling for hospital/laboratory/industrial clean rooms, and covers for various instruments used in manufacturing. Some examples of FRP end-user products manufactured by our customers are displayed below:

Medical and Industrial Equipment

Platform, Handrail and Decking

| 6 |

| Table of Contents |

Medical appliances

Research and Development

As part of our current research and development efforts, we are working closely with external R&D companies, such as Sift Center Sdn.Bhd. (www.siftcenter.com) and PCA Group Sdn.Bhd. (www.pcagroup.com), to produce and supply FRP products to Shell petrol stations in Malaysia. Sift Center Sdn. Bhd. and PCA Group Sdn. Bhd. are attempting to use the infusion vacuum process to produce Electrical Vehicle (EV) charging and hydrogen fueling stations. As part of our collaboration, we will provide the resin and fiberglass required to produce the infusion vacuum chamber and our technical expertise regarding the viability of the design.

Sales and Marketing

| · | Online Promotion. We market our product offerings through our website, www.chemrex.com.my. We utilize Google’s search engine optimization to drive traffic to our website. We also engaged Pan Pages, an internet marketing company, to further market our products to new consumers over the internet. New prospective customers can forward their inquiries via phone or our website. Our marketing and technical representatives will then contact the prospective customer and discuss how we can fulfill their order and accommodate any specific requests. Our marketing team also conducts online searches and attempts to identify new customers from time to time. |

|

|

|

| · | Product Display. We invite current and potential customers to examine our product range at our warehouse in order that customers can get a more comprehensive assessment of our product’s quality. |

|

|

|

| · | Marketing Personnel. Our product sales and marketing are performed internally by our Managing Director, Mr. Tham Too Kam, our Executive Director, Mr. Tan Liong Tai, and our Marketing Manager, Mr. Chan Kwan Wah, together with three marketing and technical representatives. In addition, our marketing team visits our existing customers monthly, and we have several discussions with them to obtain information of new potential competitors in the market. |

|

|

|

| · | Business Introduction from Suppliers. We meet our suppliers regularly. From time to time, our suppliers also will provide us with the contact details of new potential customers to whom we can provide our products, and our marketing personnel will follow up on these new sales leads. |

Our Chemical Raw Material Customers

Most of our existing customers are well-established manufacturers and contractors with long-term relationships with Chemrex who regularly place orders. Typically, they would give us a forecast of the products they need and place their orders monthly. Our top five customers, based on revenue, accounted for approximately 25.99% of our revenue for the fiscal year ended December 31, 2023.

Chemrex Top 5 Customers |

|

|

|

|

|

| ||

A |

| $ | 601,433 |

|

|

| 6.15 | % |

B |

| $ | 569,441 |

|

|

| 5.82 | % |

C |

| $ | 496,591 |

|

|

| 5.08 | % |

D |

| $ | 490,731 |

|

|

| 5.02 | % |

E |

| $ | 384,449 |

|

|

| 3.93 | % |

Total |

|

| 2,542,645 |

|

|

| 25.99 | % |

From time to time, we assist customers with their new product development or projects with suitable and compatible raw materials. In addition, leveraging on our prior successful dealings with local and international raw materials manufacturers, we often collaborate with our customer's research teams to meet their new product needs, such as the various technical and aesthetic requirements of their new products or projects.

Our Chemical Raw Material Suppliers

We consider our major vendors in each period to be those vendors that accounted for more than 10% of overall purchases in such period. We had four suppliers accounted for 17.38%, 17.05%, 14.50% and 9.57% of the Company’s total chemical raw material purchase, respectively. We had four major vendors during the fiscal year ended December 31, 2023, who collectively accounted for 58.50% of total purchases. We had four major vendors during the fiscal year ended December 31, 2022, who collectively accounted for 57.08% of total purchases. We purchase from a variety of suppliers and believe these raw materials are widely available. If we were unable to purchase from our primary suppliers, we do not expect we would face difficulties in locating another supplier at substantially the same price. We have secure and efficient access to all the raw materials necessary to produce customers’ products saving them the trouble of sourcing from several distributors. We believe our relationships with the suppliers of these raw materials are strong. While the prices of such raw materials may vary greatly from time to time, we believe we could hedge such risk by adjusting our price or absorb the higher cost at times if necessary.

| 7 |

| Table of Contents |

Fiscal Year |

| 2023 |

| |||||

|

| Cost of |

|

| % of Cost |

| ||

Vendor Name |

| Revenue (USD) |

|

| of Revenue |

| ||

A |

|

| 1,467,381 |

|

|

| 17.38 | % |

B |

|

| 1,439,569 |

|

|

| 17.05 | % |

C |

|

| 1,224,113 |

|

|

| 14.50 | % |

D |

|

| 808,113 |

|

|

| 9.57 | % |

Total |

|

| 4,939,176 |

|

|

| 58.50 | % |

|

|

|

|

|

|

|

|

|

Fiscal Year |

| 2022 |

| |||||

|

| Cost of |

|

| % of Cost |

| ||

Vendor Name |

| Revenue (USD) |

|

| of Revenue |

| ||

A |

|

| 1,425,867 |

|

|

| 14.75 | % |

B |

|

| 1,424,476 |

|

|

| 14.73 | % |

C |

|

| 1,171,511 |

|

|

| 12.12 | % |

D |

|

| 1,497,142 |

|

|

| 15.48 | % |

Total |

|

| 5,518,996 |

|

|

| 57.08 | % |

Quality Control Policies

We have a strict quality control process centered around the handling, storage, and expiry dates of our chemical raw materials before they are delivered to our customers. All products supplied by us are attached with a Certificate of Analysis ("COA") issued by manufacturers. COA contains the batch numbers, test result data, and manufacturing date. There are also labels on the packaging of our products stating the production date and batch number.

Competition

Based on the information provided by our customers and suppliers, Malaysia's industrial chemical market size is approximately USD 50 million per annum, and our current market share is around 20% of the domestic market. In the wider Southeast Asian region, including Indonesia, Thailand, Vietnam, Philippines, Myanmar, and Cambodia, we rely on close relationships with our distributors to distribute our product to customers. As a result, the market size of the Southeast Asian market is USD 500 million per annum, and our current market share is around 2.0% of the Southeast Asian market.

As Chemrex's clients are primarily in Malaysia, we consider Chemrex's principal competitors to be in the Malaysian domestic market for selling chemical raw materials. Chemex's competitors include Kaliba Sdn.Bhd. ("Kaliba"), Myeast Sdn.Bhd. and RP Product Sdn.Bhd. Some of these competitors, such as Kaliba, may have greater resources than us. They are leading providers of Fibreglass reinforced materials such as Polyester Resin, Chopped Strand Mat, and Woven Roving, many of which overlap with our product offerings.

Additionally, most of the chemical raw materials we distribute are made to industry standard specifications and either produced by or available from multiple sources. Our suppliers may also distribute directly or through multiple chemical distributors. Even for products that are unique in formulation or other characteristics, there are typically other products available that are functional substitutes, such as natural plant fiber products, such that we face significant competition even where we are the exclusive distributors of a specialty product. Hence, our suppliers may also choose to limit their distribution outsourcing, particularly with respect to higher margin products, or to partner with other wholesalers or resellers for distribution, which could increase competition.

Competitive Advantages

Notwithstanding the competition, we are a well-established and are a reliable quality composite material distributor with professional services. In addition, we offer the following benefits to our existing and potential customers:

| · | Technical Expertise: Our technical staff, comprising two chemists and one engineer, are highly competent and familiar with the technical advancements in the FRP industry. They provide technical know-how on mixing various products and offer product suggestions or modifications to our customers, which may involve strengthening or enhancing existing products sold by our customers. |

|

|

|

| · | Pricing Advantage: As a prominent reseller of FRP products in the domestic market with significant market share, we distribute our products at a relatively higher volume than our competitors. Hence, we enjoy volume discounts from our suppliers, which we are able to pass on to our customers. As a result, prospective customers could incur higher prices if they purchase from some of our competitors. |

|

|

|

| · | Convenience: We provide a wide variety of over 100 FRP products. In contrast, some of our competitors might have a smaller product range. In addition, prospective customers could incur higher logistical costs if they purchase from many different sellers instead of relying on us as a one stop shop for all their business needs. |

|

|

|

| · | Sourcing New Raw Materials for product development: We source a broad range of raw materials worldwide. This global reach greatly expands our potential customer base and provides more opportunities for our existing customers to develop new products from a wider variety of raw materials. |

| 8 |

| Table of Contents |

Growth strategy

The composite raw materials market is expected to reach an estimated $40.2 billion by 2024 globally and is forecasted to grow at a CAGR of 3.3% from 2019 to 2024. Furthermore, the composites end-user market is expected to reach an estimated $114.7 billion by 2024 globally. The major drivers for growth in this market are the increasing demand for lightweight materials in the aerospace, defense, and automotive industries. Also, corrosion and chemical resistance materials are in demand in the construction and pipe and water tank industries. With our wide variety of product offerings, we are well-positioned to take advantage of this increase in chemical composite market demand. Source: Composites Market: Trends, Opportunities and Competitive Analysis (https://www.researchandmarkets.com/categories/chemicals-materials)

In the future, we intend to develop automated warehousing and logistics powered by artificial intelligence to guide our inventory control/movement and business decisions in a more streamlined and efficient manner. We also intend to deepen our ties with our major business partners, who have cooperated with us successfully for many years. We further intend to hire more young and talented professionals to open more domestic and foreign markets in an effort to implement and sustain business growth. We are constantly seek new products through various channels, such as trade shows, to add to our product line in an effort to expand our customer base. From 2023 to 2024, we are projecting 8% revenue growth, mainly driven by more orders for our raw materials from electric vehicle charging station manufacturers. From 2025 onwards, we are projecting that the growth rate will stabilize at 7%.

Regulatory Matters

We are unaware of and do not anticipate spending significant resources to comply with governmental regulations. We are subject to the laws and regulations of various jurisdictions in Malaysia.

Listed below are the licenses Chemrex currently holds to conduct its business in Malaysia.

License/Permit/Approval | Holding entity | Issuing authority | Date of grant | Date of expiry |

Warehouse License | Chemrex | District Town Council of Selangor | September 22, 2022 | September 21, 2023 |

Importer Certificate | Chemrex | Department of Custom | October 14, 2020 | Expired once the goods cleared from the Custom |

Product Liability

Due to the nature of Chemrex's business, we may face claims for product liability resulting from any environmental or personal injury because of the chemical raw materials sold by Chemrex. We currently do not hold any insurance should a claim arise.

MRNA Diagnostics Business

Through our subsidiary MRNA Scientific, we also engaged in applying genomic testing to enable early disease diagnosis and health management.

MRNA Scientific's principal office address is Unit 02, Level 10, Tower B, Avenue 3, The Vertical Business Suite II, Bangsar South, 8 Jalan Kerinchi, Kuala Lumpur, Malaysia. Our molecular genomic lab is located at Lab 353, Chemical Science Centre, University Science Malaysia, George Town, Penang,

Malaysia, and we have a colon cancer and infectious diseases screening lab located at 4th floor, Lifecare Medical Centre, Kuala Lumpur, Malaysia. MRNA Scientific's telephone number is (+6018-2218762) and website is www.bionexusgenelab.com.

Our Non-invasive Blood Tests

At MRNA Scientific, we focus on developing and marketing safe, effective, and non-invasive blood tests to detect diseases in their early stages to minimize treatment costs and improve patient outcomes. Our non-invasive blood tests analyze changes in ribonucleic acid ("RNA") to detect specific risks and intricate of individuals' health conditions for eight cancers (nasopharyngeal, lung, liver, stomach, breast, cervical, prostate, and colon), two inflammatory bowel diseases (ulcerative colitis and crohn's) and osteoarthritis. In addition, heart attack, stroke, and mental disorders risk screening have also been included as of 2023/2024. To increase accuracy, we believe that genomic screening can be utilized in conjunction with conventional procedures for disease detection, such as imaging and biopsies.

We derive our revenue through screening patient blood samples utilizing the certain biomarkers we developed. We do not collect samples ourselves but rather market our screening service to healthcare providers, such as doctors, laboratories, and hospitals that collect the samples. MRNA Scientific is the only commercial molecular lab in Malaysia that detects cancer, inflammatory bowel diseases, and osteoarthritis risk via RNA with a certified GeneChip from the Food and Drug Administration ("FDA"). Our screening process can also help guide personalized medicines and therapies for individual patients according to their needs and risks.

Development of Screening Process

MRNA Scientific's co-founder, late Dr. Choong-Chin Liew, developed and tested a novel approach in blood-based genomic analysis and screening by identifying biomarkers in Ribonucleic acid (RNA). Dr. Liew's research has determined that communication occurs between cells in blood and tissue as blood circulates throughout the body and subtle changes occur in cell communication when a person suffers from an injury or disease. These cell-to-cell interactions induce changes in blood gene expression. Clinical studies performed by Dr. Liew and others have demonstrated that blood gene expression profiles can be used to develop personalized signatures capable of differentiating diseased patients from healthy ones.

| 9 |

| Table of Contents |

We take advantage of profiling these changes, which enables us to identify unique molecular signatures (biomarkers) reflecting disease activity which can then be used to develop disease-specific molecular diagnostic assays. We use these biomarkers as the basis for screening tests for early disease detection and generate revenue from providing screening services.

The Screening Process

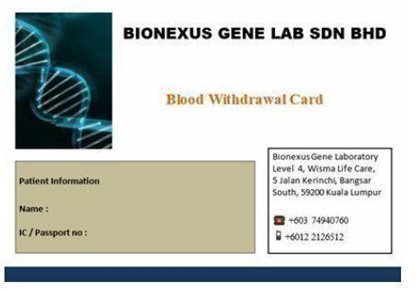

Our screening services begin with a blood sample from the patient. We do not conduct sample collection ourselves. Rather, a nurse or health care provider phlebotomist will draw 2.5 ml of blood from patients using an Paxgene tube. The blood and a completed company Blood Withdrawal Card are then sent to our lab via a third-party courier service.

A copy of the company form is shown below.

All blood samples delivered to us are labeled with the patient's name, personal identity number, and laboratory reference number on the tube where the blood sample is maintained for safekeeping.

At our lab, the patient's RNA is extracted from the sample in a biosafety cabinet, followed by microcentrifuge and spectrophotometer to check the spectrophotometric concentration and quality of the extracted RNA. The RNA is purified, and biotinylated RNA will be mixed with purification beads and transferred to a U-bottom 96-well plate. Then, the plate will be placed onto a magnetic ring stand where labeled cRNA will be captured. The remaining solution will be removed, and the captured pellet will be cleaned-up to obtain cRNA with high purity. Then, purified cRNA will be fragmented for hybridization) and hybridized onto a genechip (we utilize the GeneChip 3' IVT PLUS Reagent Kit to prepare the biotinylated target from purified total RNA samples suitable for hybridization to GeneChip arrays). Double-stranded cDNA will be synthesized from the total RNA using reverse transcriptase and oligo-dT primers. An in-vitro transcription (IVT) reaction is then done to produce biotin-labeled cRNA from the cDNA (16 hours incubation) and scanned through the Affymetrix station. Once the overnight hybridization is completed, the Genechips will be washed with dedicated buffers and solutions to remove excess cRNAs and hybridization solutions. Washed chips will be stained with staining buffers to illuminate attached cRNAs. Specific experimental information is defined using AMDS software on a PC-compatible workstation. Stained chips are ready for scanning. The chips will be transferred into the scanner, and the image will be processed into data files. The data collected from microarray analysis are analyzed using our propriety software and algorithm to generate the disease risk score report for the individual patient.

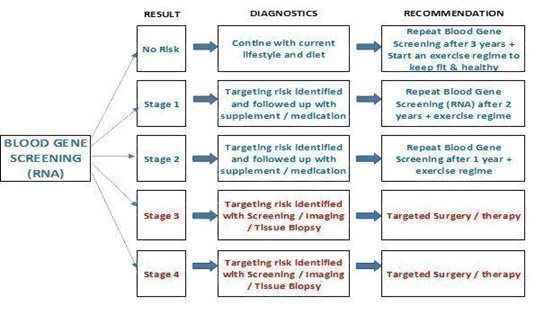

Our software generates a report, which we forward to the healthcare provider for further consultation with the patient. This report can be used by the patient and the patient's physician to plan future tests and therapies and contains. The diagram below details the diagnostics and recommendations the report provided based on the screening results.

| 10 |

| Table of Contents |

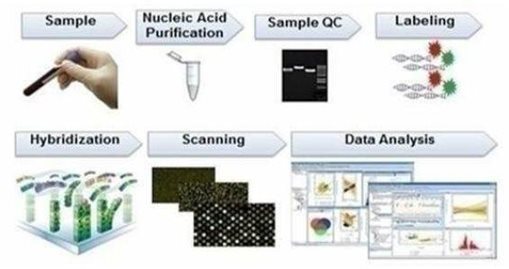

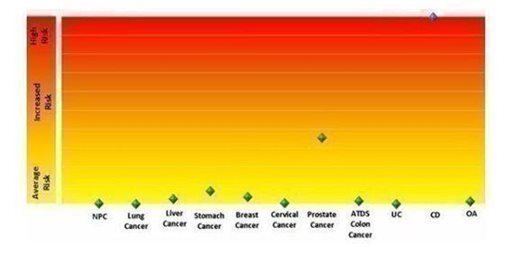

The process for effectuating RNA analysis depicted in the picture below.

The raw data obtained will be analyzed and quality control processed by our lab in Malaysia using proprietary software to calculate the risk analysis of 11 different diseases. We simplify the result into a graph which is contained in the patient booklet provided to the health care professional. A sample graph is depicted below.

In the above chart, NPC is Nasopharyngeal Cancer, ATDS is Ascending, Transverse, Descending, and Sigmoid Colon Cancer, and OA is Osteoarthritis.

The following cautionary text is contained in the results booklet we provide to the healthcare provider and each patient. The results booklet contains recommendations to assist with a physician's final diagnosis and treatment plan and is not meant to be medical advice. Below is the disclaimer that is included in each result booklet.

| 11 |

| Table of Contents |

This report/screening is not intended or implied as a substitute for professional medical advice, diagnostics, or treatment. The content, including text, graphics, and information in the report, illustrates the risk score only. MRNA Scientific Sdn. Bhd. makes no representation and assumes no responsibility for the accuracy of the information, as such information and contents are subject to change without notice. You are encouraged to review any medical condition or treatment with your doctor.

The key proprietary aspect of our process is our algorithm software, biomarkers, and the RNA extraction, preservation, quality control, hybridization, and data analysis processes developed by Dr. Liew. First, the gene expression from a reference population representing a specific disease condition is filtered using a quality assurance process based on repeatability data. Our proprietary algorithm software then analyzes this collected data and processes checked by the laboratory manager to ensure all the steps are followed in the deriving predictive model for each disease condition. Once these models have been established, they can be applied to the data from a new sample to make risk predictions for this individual. Each disease/disorder has a similar group of diseased/disordered genes identified through years of our research and clinical trials in Malaysia.

Customer Service and Quality Control Policies

We envision this division of our business to provide high-quality screening tests. Our competitive advantage lies in our turnaround time, expert interpretation, and easy-to-understand reports with timely clinical decision-making. In addition, we are dedicated to continuous quality improvement in our services and is committed to sensitivity and specificity priorities on each test.

We are committed to maintaining the confidentiality of patient information and to compliance with all privacy, security, and electronic transaction requirements of the Health Medical Act and Regulations and Code of Professional Conduct of the Malaysian Medical Council. Third parties requesting results, including any requests directly from the patient, are directed to the ordering facility. A copy of our screening test report includes reference ranges, interpretive comments, and footnotes. We submit test results electronically to healthcare providers, individual clients, and/or the Malaysian Health Ministry (HHS) regarding reportable diseases. Clients are responsible for compliance with CDC-specific statutes concerning reportable conditions. Patient test results are retained indefinitely.

All samples handled by our laboratory are treated as though they are infectious. The greatest dangers to healthcare workers exposed to blood and body fluids are hepatitis B, hepatitis C, and HIV viruses. Our laboratory turnaround time is monitored closely and compared to standardized laboratory metrics for continuous quality improvement. Laboratory scientists and technologists are all highly experienced in handling complex tests. Our scientists, and our supervisors monitor performance indicators for all laboratory services. Performance improvement initiatives are regularly instituted and reviewed as part of an ongoing quality improvement program.

Business Development and Growth Strategy

In April 2017, we began marketing our screening services to healthcare providers, laboratories, and hospitals, all of which have licensed doctors or staff. As mentioned above, our screening service provides a risk analysis report of 11 diseases, of which eight are different forms of cancer. In Malaysia, the cost of the analysis is not covered by health insurance. Thus, patients are required to pay out of pocket for our services, which currently range from $200 for a single colon cancer screening to $975 for all 11 diseases under our screening protocol.

In November 2017, we expanded our marketing efforts to companies, business organizations, and insurance agents. As a result of these efforts, during November and December 2017, we entered arrangements with two companies in Kuala Lumpur to screen their employees for 11 diseases/disorders (lung cancer, colon cancer, nasopharyngeal cancer, liver cancer, stomach cancer, breast cancer, cervical cancer, prostate cancer, inflammatory bowel diseases (ulcerative colitis & Crohn’s disease), and osteoarthritis pursuant to which each company paid us $50,000. We completed the screening process of these two companies in the first quarter of 2019 and continue to market our services to other local companies in the Kuala Lumpur metropolitan area. In 2022, we had entered an arrangement with a clinical lab to conduct screening for the 11 diseases.

Our pricing strategy is consistent with our objectives, costs, competition, and demand for the product. Our management administers the policies to match the market needs. We charge the following prices to individuals for our tests:

| · | $200 for Colon Cancer Screening (Single Colon Cancer screening per blood sample) |

|

|

|

| · | $975 for Blood-based Genomic Signature (BGS) Screening for 11 diseases/disorders (Molecular RNA Cancer Screening per blood sample) |

The price for each test charged to hospitals, clinics, and other healthcare operators is subject to an incentive-based rebate that ranges from 20% to 25% based on the monthly volume of tests conducted.

As of December 31st, 2023, we work with 27 liquid biopsy sample collection centers, 12 in Klang Valley (comprised of our capital city Kuala Lumpur) and towns on the northern and southern fringes of the capital city), and 15 public hospitals and labs nationwide. These 27 locations account for approximately 90% of our patient population in 2022 and 2021.

We aim to have more healthcare providers in the Klang Valley referring patients to us for screening protocol. Once we have established our brand and reputation in Klang Valley, we will expand to other large cities in Malaysia. On August 25, 2022, we presented our MRNA screening service to the Health Ministry of Malaysia for nationwide implementation. Deputy Director Generals from Public Health and Cancer Divisions had scheduled another meeting on January 17, 2023. In the January’ meeting, the information we shared on the cost saving of $1.15 billion (RM 5.1 billion) in treatment expenses and $30.88m (RM135,861,660) in screening expenses for 68,617 persons (0.2% of the population) annually. Even though there have been changes in personnel in the normal course of operations with the Ministry of Health, including the previous changes of Government, we maintain our contacts and continue to advocate the merit of early disease detection as a Public Health opportunity, whereby not only can costs be saved but quality of life and mortality can be improved. While we continue to build opportunities to work with the Government and are exploring multiple channels including electronic marketing, marketing services and collaboration with specialist centres for advocacy. In 2023 we signed several deals with specialist centres to advocate the benefits of early detection & screening and provide opportunities for their patients to benefit from our testing.

| 12 |

| Table of Contents |

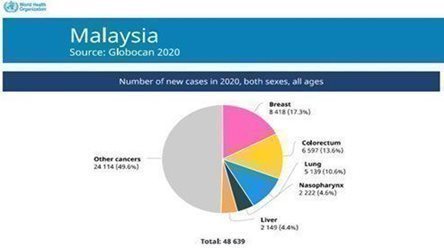

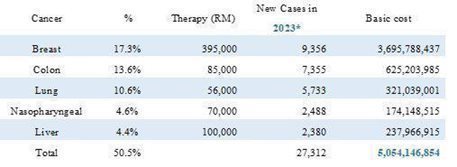

Some prevalent cancer cases in Malaysia from Globocan 2020 endorsed by WHO

Cancer screening costs from a diagnostic center is priced at $882 (RM3,880) as compared to MRNA screening at $432 (RM1,900), quantity genechip purchase would drastically reduce the screening cost.

We believe that an increase in our marketing and promotional efforts will correlate to increased revenues and the expansion of our business. Our growth and expansion strategies are as follows:

| · | Continue to leverage our relationships with healthcare providers. To date, we have relied upon the efforts of management and their relationships with healthcare providers to create continued interest in our blood-based genomic screening. These relationships have been located primarily in the Klang Valley market. In 2024, it will be our priority to not only increase the number of healthcare providers that are able to offer our services through partnership, but we are in the process of developing a referral system to allow an expanded network of healthcare providers to promote our “ BGS “ testing via referring them to an existing sample collection site. |

|

|

|

| · | Allocate more capital resources to our marketing efforts. Apart from sales through existing relationships with healthcare providers, we intend to allocate more capital to marketing and promotion. Our current strategy proposes to increase the awareness of our “ BGS “ testing to the public, via direct marketing through wellness and healthcare key opinion leaders (“KOL”). We are currently in talks with various successful parties and wellness providers in the Klang Valley area to form partnerships on public awareness. |

|

|

|

| · | Increase focus on corporate clients. To date, we have entered arrangements with six corporate clients to provide our 11 diseases/disorders screening services to their employees. In addition, we intend to solicit more corporate clients in the Klang Valley and major cities in Malaysia. We commenced these efforts last year and will continue in 2024. Our officers and the Marketing Companies will undertake these efforts. |

|

|

|

| · | Expand to other regions in Malaysia. We intend to expand to other large cities in Malaysia, such as Penang, Ipoh, Seremban, Melaka, Johor Bahru, and Kuantan. |

|

|

|

| · | Expand to other International Regions. We have been in discussions with key market access experts and professionals in Europe to explore the possibility of offering our screening products in Europe. Additionally, we are in the midst of discussing the terms of a partnership with one of the largest testing, screening, and genetic sequencing providers in Hong Kong for the purposes of expanding our services to Hong Kong. |

Competition

We believe that we have the only commercial molecular lab in Malaysia that provides liquid biopsy screenings that detect the risk of cancer, inflammatory diseases, and osteoarthritis risk via RNA biomarkers and provides a report which patients and physicians can use to plan for future tests and personalized therapies. Based on prior private conversations with the USA Thermo Fisher representative in Malaysia, there is a medical lab using similar equipment on DNA screening.

| 13 |

| Table of Contents |

Competitive Strengths

We believe that we have several competitive strengths compared to these other health diagnostic tools. They are as follows:

| · | Our screening (a simple blood draw) is less invasive, unlike tissue biopsies. A tissue biopsy is a procedure in which a physician removes a piece of tissue or a sample of cells from a patient's body to be analyzed in a laboratory. If a patient experiences certain signs and symptoms or the physician has identified an area of concern, he may undergo a biopsy to determine whether the patient has cancer or another ailment. While biopsies can have higher accuracy, it is a more invasive procedure that is difficult to repeat and thus impractical for periodic monitoring. Our screening tests are a form of liquid biopsy which utilizes RNA biomarkers. Broadly speaking, a liquid biopsy is the collection of a body fluid sample to test for relevant biomarkers to inform patient management, most applied to the collection of peripheral blood for analysis of cell-freecirculating tumor ribonucleic acids (RNA). Since liquid biopsies are performed on peripheral blood, which is easy to access, it allows for more widespread use, particularly in patients who cannot have surgery. As a result, liquid biopsies can reduce the time to treatment, improve the efficiency of medical staff and resources, and be used to screen more diseases. |

|

|

|

| · | Non-DNA blood tests for diseases like cancer are not dispositive. There currently exist various examinations to detect diseases in patients. For example, abnormally high or low levels of certain substances in your body can be a sign of disease. Testing of blood, urine or other body fluids that measure these substances can help doctors make a diagnosis. However, abnormal lab results are not a sure sign of disease. Conventional blood tests are an important tool but are not always reliable because of low sensitivity, specificity, and predictive value. |

|

|

|

| · | Other Conventional tests could require a longer turnaround time. Imaging is a procedure in which physicians utilize pictures of areas inside the body that help the doctor see whether a disease is present. These images can be taken in several ways, including a CT scan, Nuclear Scan, MRI, PET Scan, and Ultrasound. Imaging is useful in providing physicians with real-time images to assist with diagnosis. However, imaging techniques can have longer turnaround times, the information provided can be limited, and the patient may be exposed to radiation. |

|

|

|

| · | Our screening provides a predictive risk assessment for developing the 11 diseases. Most other screening procedures detect diseases only when they are already present in the body and most cases, in the final stages of the disease, making it difficult to treat or reverse. Our screening can detect the 11 diseases at an earlier stage before any symptoms even appear. Early detection and targeted medical intervention could be crucial in saving patients' lives and financial resources. |

|

|

|

| · | Our screening measures the current risk of a specific individual rather than their lifetime risk. DNA tests measure a specific individual's lifetime risk based on their DNA. However, since DNA does not change with external factors, it cannot quantify an individual's specific risk of the disease materializing. However, our RNA-based test is highly specific since RNA expression changes with lifestyle and other external factors. Hence, at-risk patients can make timely adjustments to their lifestyles to reduce the potentiality of these diseases. Lifestyle adjustments may include reduction or changes to food, tobacco, and alcohol intake, change of working environment, and the implementation of exercise programs, among other changes. |

Seasonality

The nature of our business does not appear to be affected by seasonal variations.

Regulatory Matters

We are unaware of and do not anticipate spending significant resources to comply with governmental regulations. We are and will be subject to the laws and regulations of those jurisdictions in which we operate. Generally, business licensing requirements, income taxes, and payroll taxes apply to all business operations. The development and operation of our business are not subject to special regulatory and/or supervisory requirements. We only require an operating permit from the City Hall of Kuala Lumpur, Malaysia, which we have received. However, we cannot predict whether we would be able to comply with other regulations if implemented.

Product Liability

Due to the nature of our business, we may face claims for product liability resulting from the inaccurate or erroneous diagnosis using our screening process. MRNA Scientific does not currently have insurance against any such claims.

Research and Development

There are three persons in the R&D team consists of 1 scientist, and 2 laboratory managers.

Our research and development budget over the years is listed in the following table:

|

| Research & |

| |

|

| Development |

| |

Year |

| (self-funded) |

| |

2017 |

| $ | 0 |

|

2018 |

| $ | 0 |

|

2019 |

| $ | 25,000 |

|

2020 |

| $ | 45,000 |

|

2021 |

| $ | 45,000 |

|

2022 |

| $ | 173,300 |

|

2023 |

| $ | 48,537 |

|

| 14 |

| Table of Contents |

Our Properties

The corporate office for MRNA Scientific is located at Unit 2, Level 10, Tower B, Avenue 3, The Vertical Business Suite II, Bangsar South, 8 Jalan Kerinchi, Bangsar South, 59200 Kuala Lumpur, Malaysia. The lease commenced on December 16, 2018 and terminates on December 15, 2024. The space consists of 1,300 square feet with an annual rent of approximately $13,500.

We also have two laboratories. One of our laboratories is located at 4th Floor, Wisma Life Care, No. 5, Jalan Kerinchi, Bangsar South, 59200 Kuala Lumpur, Malaysia. The lease commenced on November 1, 2016 and terminates on October 31, 2023 but continues on a month to month basis. The annual rent is approximately $6,800. The other laboratory is located at Lab 353, University Science Malaysia, George Town, Penang, Malaysia. The lease commenced on December 1, 2017 and terminates on November 30, 2024. The space consists of 1,500 square feet with an annual rent of approximately $7,300.

On July 2, 2012, we purchased a 25,000 sq. ft wholesale distribution center at 4, Jalan CJ 1/6, Kawasan Perusahaan Cheras Jaya, 43200 Cheras, Selangor, Malaysia, and two investment properties for $1,395,210. The two investment properties are listed below.

| · | A 1,100 sq ft condominium located at No. B-17-03, Duet Residence, Jalan Kinrara 6, Bandar Kinrara, 47180 Puchong, Selangor, purchased on August 26, 2020; |

|

|

|

| · | A 2,000 sq ft commercial building located at First floor, No. 2B Pelangi Avenue, Jalan Kelicap 42A/KU1, Klang Bandar, Diraja, 41050 Klang, Selangor purchased on September 21, 2020. |

On January 18, 2024, we entered into a lease for the first-floor unit at No. 5-1, Jalan CJ3/13-2, Pusat Bandar Cheras Jaya, 43200 Cheras, Selangor. The lease terminates on January 17, 2025. The purpose of this lease is to provide housing accommodation for our warehouse staff.

Intellectual Property

As of date of this filing, we have 1 trademark registered with the Intellectual Property Corporation of Malaysia. We do not have any patents, copyright, or licensing rights. Additionally, for MRNA Scientific, we rely on trade secrets and know-how using the process developed by and assigned to the Company by Dr. Liew, one of Our Founders. However, there is no assurance that others will not independently develop the same or similar technology or obtain unauthorized access to such trade secrets, know-how, and other unpatented technology. To protect our rights in these areas, we require all laboratory managers that work in our lab to enter into strict confidentiality agreements.

As part of our on-going software development process that has been supplemented by our Initial Public Offering, we are in the process of developing from the original source code, a Cloud Based (SaaS) implementation and evolutionary development of our Machine Learning sample analysis software. We are working with additional experts in the field, via contract and with the view to expand our internal team, and this work is being overseen by our CEO, Mr. Su-Leng Tan Lee, who has a background in Computer Science, Machine Learning, and Artificial Intelligence.

While we have attempted to protect the unpatented proprietary technology that we develop or acquire and will continue to attempt to protect future proprietary technology through patents, copyrights, and trade secrets, we believe that our success will depend, to a large extent, upon continued innovation and technological expertise.

Employees

As of date of this filing, Chemrex has 18 full-time employees, and MRNA Scientific has 12 full time employees. We believe we have good relations with our employees. The company presently is covered by social security insurance and contributes to the Employee Provident Fund of its employees, a compulsory pension scheme for all Malaysian citizens and permanent residents who are working in Malaysia.

The following table sets out the number of Chemrex's employees, excluding external experts, categorized by functions as of the date of this filing:

|

| Number of |

| |

Function |

| Employees |

| |

Director |

|

| 5 |

|

Sales & Marketing |

|

| 4 |

|

Warehouse |

|

| 6 |

|

Administration & Purchaser |

|

| 2 |

|

Finance |

|

| 2 |

|

Total |

|

| 18 |

|

The following table sets out the number of MRNA Scientific's employees, excluding external experts, categorized by functions as of the date of this filing:

|

| Number of |

| |

Function |

| Employees |

| |

Director |

|

| 2 |

|

Finance |

|

| 1 |

|

Lab Operation |

|

| 2 |

|

Research & Development |

|

| 1 |

|

Marketing & Business Development |

|

| 3 |

|

General & Administration |

|

| 2 |

|

Total |

|

| 12 |

|

| 15 |

| Table of Contents |

The following table sets out the number of BGLC's employees, excluding external experts, categorized by functions as of the date of this filing:

|

| Number of |

| |

Function |

| Employees |

| |

Chief Executive Officer |

|

| 1 |

|

Total |

|

| 1 |

|

Currently, we have entered into employment agreements with our officers. We do not have stock options, profit sharing, or similar benefit plans. However, as appropriate after our Initial Public Offering, the Company plans to table at the next Annual Meeting of Shareholders an Equity Compensation Plan that will assist the Company to align the interests of its Key Personnel with the success of the Company, improving employee retention and paving the way for growth in Shareholder value. The Company is currently exploring multiple methods to expand its Executive Team, including advertising and engaging with specialist recruitment agencies to bolster our human capital and business development resources.

Insurance

For our Chemrex operations, we maintain third-party liability insurance to cover claims in respect of personal injury or property or environmental damage arising from accidents on our chemical warehouse and office or relating to our operations. Our employees presently are covered by Social Security insurance (SOCSO) and retirement fund (EPF). We do not maintain business interruption insurance or key person insurance. Our insurance coverage is consistent with the industry and sufficient to cover our key assets, facilities, and liabilities. Also, as part of our Chemrex business, we maintain burglary and fire insurance for our property at 4, Jalan CJ 1/6, Kawasan Perusahaan Cheras Jaya, 43200 Cheras, Selangor, Malaysia, and fidelity guarantee insurance against our employees.

Legal Proceedings

We are not subjected to nor engaged in any litigation, arbitration, or claim of material importance, and no litigation, arbitration, or claim of material importance is known to us to be pending or threatened by or against our Company that would have a material adverse effect on our Company's results of operations or financial condition.

| 16 |

| Table of Contents |

Item 1A. Risk Factors

RISK FACTORS

An investment in our common stock involves a number of very significant risks. You should carefully consider the following known material risks and uncertainties in addition to other information in this Form 10-K in evaluating our company and its business before purchasing shares of our company’s common stock. You could lose all or part of your investment due to any of these risks.

Risk Factors Related to Our Financial Prospects and Capitalization

We are an early commercial-stage company and have a limited operating history, which may make it difficult to evaluate our current business and predict our future performance.

We are an early commercial-stage company and has a limited operating history. Our limited operating history may make it difficult to evaluate our current business and this makes predictions about our future success or viability subject to significant uncertainty. In combination with other anticipated increased operating expenses in connection with becoming a public company, these anticipated changes in our operating expenses may make it difficult to evaluate our current business, assess our future performance relative to prior performance and accurately predict our future performance.

We will continue to encounter risks and difficulties frequently experienced by early commercial-stage companies, including those associated with increasing the size of our organization and the prioritization of our commercial, research, and business development activities. If we do not address these risks successfully, our business could suffer.

Our growth (organic and inorganic) may require substantial capital and long-term investments.

Our competitiveness and growth depend on our ability to fund our capital expenditures. We cannot assure you that it will be able to fund our capital expenditures at reasonable costs due to adverse macroeconomic conditions, our performance or other external factors.

In the future, we expect to incur significant costs in connection with its operations. We intend to expand our business through increased marketing efforts of MRNA Scientific and Chemrex. These development activities generally require a substantial investment before we can determine commercial viability, and the proceeds of this offering will not be sufficient to fully fund these activities. We expect to need to raise additional funds through public or private equity or debt financings, collaborations or licensing arrangements to continue to fund or expand our operations.

Our actual liquidity and capital funding requirements will depend on numerous factors, including:

| · | the scope and duration of and expenditures associated with our discovery efforts and research and development programs; |

|

|

|

| · | the costs to fund our commercialization strategies for any product candidates for which we receive marketing authorization or otherwise launch and to prepare for potential product marketing authorizations, as required; |

|

|

|

| · | the costs of any acquisitions of complementary businesses or technologies that we may pursue; |

|

|

|

| · | potential licensing or partnering transactions, if any; |

|

|

|

| · | Our facilities expenses, which will vary depending on the time and terms of any facility lease or sublease we may enter into, and other operating expenses; |

|

|

|

| · | the scope and extent of the expansion of our sales and marketing efforts; |

|

|

|

| · | the settlement of the government investigation described below, potential and pending litigation, potential payor recoupments of reimbursement amounts, and other contingencies; |

| · | the commercial success of our products; |

|

|

|

| · | Our ability to obtain more extensive coverage and reimbursement for our tests and therapeutic products, if any, including in the general, average-risk patient population; and |

|

|

|

| · | Our ability to collect its accounts receivable. |

The availability of additional capital, whether from private capital sources (including banks) or the public capital markets, fluctuates as our financial condition and market conditions in general change. There may be times when the private capital sources and the public capital markets lack sufficient liquidity or when our securities cannot be sold at attractive prices or at all, in which case we would not be able to access capital from these sources. In addition, a weakening of our financial condition or deterioration in its credit ratings could adversely affect our ability to obtain necessary funds. Even if available, additional financing could be costly or have adverse consequences.

| 17 |

| Table of Contents |

We may incur net losses in the near future.

We have devoted substantial resources to the development and commercialization of the products of MRNA Scientific and Chemrex. We might not remain profitable for any period. Our failure to achieve profitability would negatively affect our business, financial condition, results of operations, and cash flows. If we are unable to execute our sales and marketing strategy and our products are unable to gain sufficient acceptance in the market, we may be unable to generate sufficient revenues to sustain our business.

Any additional capital we raise may not be available on satisfactory terms and may adversely affect stockholders’ holdings or rights.

Additional capital, if needed, may not be available on satisfactory terms or at all. In addition, the terms of any financing may adversely affect stockholders’ holdings or rights. Debt financing, if available, may include restrictive covenants. To the extent that we raise additional funds through collaborations and licensing arrangements, it may be necessary to relinquish some rights to our technologies or grant licenses on terms that may not be favorable to us.

If we are not able to obtain adequate funding when needed, we may be required to delay development programs or sales and marketing initiatives. If we are unable to raise additional capital in sufficient amounts or on satisfactory terms, we may have to make reductions in our workforce and may be prevented from continuing our discovery, development, and commercialization efforts and exploiting other corporate opportunities. In addition, it may be necessary to work with a partner on one or more of our tests or products under development, which could lower the economic value of those products to us. Each of the foregoing may harm our business, operating results, and financial condition and may impact our ability to continue as a going concern.

Raising additional capital may lead to dilution of shareholdings by our existing shareholders, restrict our operations, and may further result in fair value loss, adversely affecting our financial results.

We may seek additional funding through a combination of equity and debt financings and collaborations. To the extent that we raise additional capital through the sale of equity or convertible debt securities, the ownership interest of existing holders of our shares will be diluted, and the terms may include liquidation or other preferences that adversely affect the rights of our existing shareholders.

The incurrence of additional indebtedness or the issuance of certain equity securities could result in increased fixed payment obligations and could also result in certain additional restrictive covenants, such as limitations on our ability to incur additional debt or issue additional equity, limitations on our ability to acquire or license IP rights and other operating restrictions that could adversely impact our ability to conduct its business.

Risk Factors Related to Our Business and Industry

General Business and Industry Risks

We are unable to predict the duration of future economic conditions.

Future economic downturns, prolonged slow growth or stagnation in the economy could materially adversely affect our business, results of operations, financial condition and cash flows.

Global economic conditions could materially adversely impact demand for our products and services.

Our operations and performance depend significantly on economic conditions. Global financial conditions continue to be subject to volatility arising from international geopolitical developments and global economic phenomenon, as well as general financial market turbulence and natural phenomena such as the COVID-19 pandemic. Uncertainty about global economic conditions could result in

| · | customers postponing purchases of its products and services in response to tighter credit, unemployment, negative financial news and/or declines in income or asset values and other macroeconomic factors, which could have a material negative effect on demand for its products and services; and |

|

|

|

| · | third-party suppliers being unable to produce devices for its products or raw materials in the same quantity or on the same timeline or being unable to deliver such parts and components as quickly as before or subject to price fluctuations, which could have a material adverse effect on the services and products provided by MRNA Scientific; and accordingly, on its business, results of operations or financial condition. |

Access to public financing and credit can be negatively affected by the effect of these events on Malaysian, U.S. and global credit markets. The health of the global financing and credit markets may affect its ability to obtain equity or debt financing in the future and the terms at which financing or credit is available to us. These instances of volatility and market turmoil could adversely affect its operations and the trading price of its common stock.

| 18 |

| Table of Contents |

Our risk management programs, processes, or procedures for identifying and addressing risks in MRNA Scientific’s business may not be adequate or effectively applied, and this may adversely impact its businesses.

MRNA Scientific relies on a combination of technical and human factors to protect us against risks. MRNA Scientific policies, procedures and practices are used to identify, monitor and control a variety of risks, including risks related to human error and hardware and software errors. The administration and results of each test are reviewed by a physician and a scientist in Malaysia before the results are released to the patient. The Company’s standard of operations was primarily developed by Dr. Liew. These risk-management methods may not adequately prevent losses and may not protect us against all risks, in which case our business, economic conditions, operations and cash flows may be materially adversely affected.

We have risk-management policies, control systems and compliance manuals in place; however, there is no guarantee that such policies, systems, and manuals will be effectively applied in every circumstance by our staff. For example, employees could override the system technology and theoretically waive requirements, thereby exposing the company accurately conduct its quality control.

We may be adversely impacted by changes in laws and regulations, or in their application.

Currently, there are no governmental regulations that materially restrict our screening business in Malaysia. MRNA Scientific’s laboratory in Malaysia was established through an invitation by the Malaysian Health Minister alongside a government grant of $1,250,000. MRNA Scientific’s screening tests have gone through preclinical and clinical trials involving private hospitals and government agencies including the Institute of Medical Research (IMR), Malaysian Biotechnology Corporation (BiotechCorp) and the Clinical Research Centre (CRC). The findings of the preclinical and clinical trials are published in peer reviewed journals such as the Journal of Molecular and Cellular Cardiology, and Physiological Genomics. Once published, MRNA Scientific would do confirmational tests before applying for commercialization. MRNA Scientific’s Malaysian lab is currently national operating under an operating license granted by the city of Kuala Lumpur.

The Malaysian government passed the Pathology Laboratory Bill of 2007 (“Pathology Act”). However, since 2007, the government has not implemented the regulations underlying the legislation nor has the government enforced the Pathology Act. Any such regulations could establish criteria for the various classes and specialties of laboratories, the organization and management system of the laboratory, the qualification and experience of the person-in-charge, the qualification and competence of pathologists, scientific and technical staff engaged to conduct tests, and the standards of laboratory practice. MRNA Scientific cannot predict whether it would be able to comply with the Pathology Act and its regulations, if implemented. In addition, there also is a risk that the regulations arising from the Pathology Act or new legislation or regulations could increase MRNA Scientific’ costs of doing business or otherwise prevent us from carrying out the expansion of its business. Accordingly, our business may be harmed if we are not able to comply with any future governmental legislation or regulations, including the Pathology Act.

MRNA Scientific is currently operating under a license granted by the City Hall of Kuala Lumpur, Malaysia. Under Malaysian and local laws, we may continue to operate under its current operating license which MRNA Scientific Malaysia currently has. We cannot predict whether there will be future regulations which may impact its ability to conduct its business.

Currently, there are no governmental regulations that affect Chemrex’s business in Malaysia and it may continue to operate under an operating license granted by the Kajang Town Hall of Selangor, Malaysia. Future legislation or regulations could increase Chemrex’s costs of doing business or otherwise prevent us from carrying out the expansion of its business.

Business disruptions could seriously harm our future revenue and financial condition and increase its costs and expenses.

Our operations could be subject to power shortages, telecommunications failures, wildfires, water shortages, floods, earthquakes, hurricanes, typhoons, fires, extreme weather conditions, medical epidemics and other natural or man-made disasters or business interruptions. The occurrence of any of these business disruptions could seriously harm MRNA Scientific’ operations and financial condition and increase MRNA Scientific’ costs and expenses. Unfavorable global economic conditions could adversely affect our business, financial condition, or results of operations.

We do not carry insurance for all categories of risk that our business may encounter. Although MRNA Scientific intend to obtain some form of business interruption insurance in the future, there can be no assurance that we will secure adequate insurance coverage or that any such insurance coverage will be sufficient to protect our operations to significant potential liability in the future. Any significant uninsured liability may require us to pay substantial amounts, which would adversely affect our financial position and results of operations.

Our lack of insurance could expose us to significant costs and business disruption.

We currently do not have any product liability or disruption insurance to cover our operations in Malaysia or overseas. We have determined that the costs of insuring for these risks and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. If we suffer any losses, damages or liabilities in the course of our business operations, we may not have adequate insurance coverage to provide sufficient funds to cover any such losses, damages or product claim liabilities. Therefore, there may be instances when we will sustain losses, damages and liabilities because of our lack of insurance coverage, which may in turn materially and adversely affect our financial condition and results of operations.

As a public company, we may become subject to the Section 404 of the Sarbanes-Oxley Act, or SOX 404, which requires that we include a report from management on the effectiveness of our internal control over financial reporting in our annual report on Form 10-K and in our quarterly report on Form 10-Q if we are qualified as an accelerated filer.

| 19 |

| Table of Contents |

We are currently a “smaller reporting company”, meaning that we are not an investment company, an asset- backed issuer, or a majority-owned subsidiary of a parent company that is not a smaller reporting company and annual revenues of less than $50.0 million during the most recently completed fiscal year. In the event that we are still considered a “smaller reporting company,” at such time as we cease being an “emerging growth company,” we will be required to provide additional disclosure in our SEC filings. However, similar to an “emerging growth companies”, “smaller reporting companies” are able to provide simplified executive compensation disclosures in their filings; are exempt from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that independent registered public accounting firms provide an attestation report on the effectiveness of internal control over financial reporting; and have certain other decreased disclosure obligations in their SEC filings, including, among other things, only being required to provide two years of audited financial statements in annual reports. Decreased disclosures in our SEC filings due to our status as a “smaller reporting company” may make it harder for investors to analyze our results of operations and financial prospects.

Our independent registered public accounting firm may be required to attest to and report on the effectiveness of our internal control over financial reporting. Our management may conclude that our internal control over financial reporting is not effective. Moreover, even if our management concludes that our internal control over financial reporting is effective, our independent registered public accounting firm, after conducting its own independent testing, may issue a report that is qualified if it is not satisfied with our internal controls or the level at which our controls are documented, designed, operated or reviewed, or if it interprets the relevant requirements differently from us. In addition, after we become a public company, our reporting obligations may place a significant strain on our management, operational and financial resources and systems for the foreseeable future. We may be unable to timely complete our evaluation testing and any required remediation.

During the course of documenting and testing our internal control procedures, in order to satisfy the requirements of SOX 404, we may identify other weaknesses and deficiencies in our internal control over financial reporting. In addition, if we fail to maintain the adequacy of our internal control over financial reporting, as these standards are modified, supplemented or amended from time to time, we may not be able to conclude on an ongoing basis that we have effective internal control over financial reporting in accordance with SOX 404. If we fail to achieve and maintain an effective internal control environment, we could suffer material misstatements in our financial statements and fail to meet our reporting obligations, which would likely cause investors to lose confidence in our reported financial information. This could in turn limit our access to capital markets, harm our results of operations, and lead to a decline in the trading price of our shares. Additionally, ineffective internal control over financial reporting could expose us to increased risk of fraud or misuse of corporate assets and subject us to potential delisting from the stock exchange on which we list, regulatory investigations and civil or criminal sanctions. We may also be required to restate our financial statements from prior periods.

Fluctuations in foreign currency exchange rates could have a material adverse effect on our financial results.