UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2020

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM ______ TO ______

COMMISSION FILE NUMBER 000-26731

GREENLAND TECHNOLOGIES HOLDING CORPORATION

(Exact name of Registrant as specified in its charter)

| British Virgin Islands | 001-38605 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

11-F, Building #12, Sunking Plaza, Gaojiao Road Hangzhou, Zhejiang People’s Republic of China |

311122 | |

| (Address of principal executive offices) | (Zip Code) |

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (86) 010-53607082

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Ordinary shares, no par value | GTEC | The Nasdaq Stock Market LLC |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

NONE

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed be Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting Company, or an emerging growth Company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting Company,” and “emerging growth Company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| Non-accelerated filer | ☒ | Smaller reporting Company | ☒ | |

| Emerging growth Company | ☒ | |||

If an emerging growth Company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell Company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the ordinary shares outstanding held by non-affiliates of the registrant, computed by reference to the closing sales price for the ordinary shares of $3.9, as reported on the Nasdaq Capital Market, was approximately $39.08 million.

As of March 31, 2021, there were 10,498,127 shares of the registrant’s ordinary shares outstanding.

TABLE OF CONTENTS

i

Cautionary Note Regarding Forward Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. These statements, which express management’s current views concerning future business, events, trends, contingencies, financial performance, or financial condition, appear at various places in this report and use words like “aim,” “anticipate,” “assume,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “future,” “goal,” “intend,” “likely,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “see,” “seek,” “should,” “strategy,” “strive,” “target,” “will,” and “would” and similar expressions, and variations or negatives of these words. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, some of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted. These risks and uncertainties include the following:

| ● | The availability and adequacy of our cash flow to meet our requirements; | |

| ● | Economic, competitive, demographic, business, and other conditions in our local and regional markets; | |

| ● | Changes or developments in laws, regulations, or taxes in our industry; | |

| ● | Actions taken or omitted to be taken by third parties including our suppliers and competitors, as well as legislative, regulatory, judicial, and other governmental authorities; | |

| ● | Competition in our industry; | |

| ● | The loss of or failure to obtain any license or permit necessary or desirable in the operation of our business; | |

| ● | Changes in our business strategy, capital improvements, or development plans; | |

| ● | The Company’s ability to devise and implement effective internal controls and procedures; | |

| ● | The availability of additional capital to support capital improvements and development; and | |

| ● | Global or national health concerns, including the outbreak of epidemic or contagious diseases such as the COVID-19 epidemic; and | |

| ● | Other risks identified in this Report and in our other filings with the Securities and Exchange Commission or the SEC. |

This Report should be read completely and with the understanding that actual future results may be materially different from what we expect. The forward-looking statements included in this Report are made as of the date of this Report and should be evaluated with consideration of any changes occurring after the date of this Report. We will not update forward-looking statements even though our situation may change in the future and we assume no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Financial Presentation

We operate on a December 31 fiscal year end. Unless otherwise indicated, references in this Annual Report on Form 10-K to an individual year means the fiscal year ended December 31. For example, “2020” refers to the fiscal year ended December 31, 2020.

ii

| ITEM 1. | BUSINESS |

General

The registrant was incorporated on December 28, 2017 as a British Virgin Islands Company with limited liability. The registrant was incorporated as a blank check company for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, recapitalization, reorganization or similar business combination with one or more target businesses. Following the Business Combination (as described and defined below) in October 2019, the registrant changed its name from Greenland Acquisition Corporation to Greenland Technologies Holding Corporation (“Greenland”).

Greenland serves as the parent Company for the primary operating Company, Zhongchai Holding (Hong Kong) Limited, a holding Company formed under the laws of Hong Kong on April 23, 2009 (“Zhongchai Holding”). Through Zhongchai Holding and other subsidiaries, Greenland develops and manufactures traditional transmission products for material handling machineries in the People’s Republic of China (PRC), as well as develops electric industrial vehicles, which are expected to be produced in the near future.

Greenland, through its subsidiaries, is:

| ● | a leading developer and manufacturer of transmission products for material handling machineries in China; and | |

| ● | since December 2020, a developer of electric industrial vehicles, with our first model of electric industrial vehicle expected to be available in the third or fourth quarter of 2021. |

Greenland’s transmission products are key components for forklift trucks, used in manufacturing and logistic applications such as factories, workshops, warehouses, fulfilment centers, shipyards, and seaports. Forklifts play an important role in logistics for many enterprises across different industries in the PRC and around the globe. Generally, industries with the largest demand for forklifts are transportation, warehousing logistics, electrical machinery, and automobile.

Greenland has experienced an increase in demand for forklifts in the manufacturing industry in the PRC, as its revenue increased from approximately $52.40 million in the fiscal year of 2019 to $66.86 million in the fiscal year of 2020. The increased revenue of approximately $14.46 million was primarily due to the fact that demand for our products has returned to normal and continued to grow. Based on the revenues in the fiscal year ended December 31, 2020 and 2019, Greenland believes that it is one of the major developers and manufacturers of transmission products for small and medium-sized forklift trucks in China.

Greenland’s transmission products are used in 1-ton to 15-tons forklift trucks, some with mechanical shift and some with automatic shift. Greenland sells these transmission products directly to forklift-truck manufacturers. In the fiscal year ended December 31, 2020 and 2019, Greenland sold an aggregate of more than 108,913 and 83,567 sets of transmission products, respectively, to more than 100 forklift manufacturers in the PRC.

In December 2020, Greenland launched a new division to focus on the electric industrial vehicle market, a market that Greenland intends to develop to diversify its product offerings. With this new division, Greenland plans to develop and deploy the next generation of industrial vehicles. Greenland plans to establish a new facility on the east coast of the U.S. and start producing electric industrial vehicles between the third and fourth quarter of 2021.

1

Significant Activities since Inception

Initial Public Offering

On July 27, 2018, we consummated our initial public offering of 4,400,000 units, including a partial exercise by the underwriters of their over-allotment option in the amount of 400,000 units. Each unit consists of one ordinary share, no par value, one warrant to purchase one-half of one ordinary share and one right to receive one-tenth of one ordinary share upon the consummation of our initial business combination, pursuant to a registration statement on Form S-1. Warrants must be exercised in multiples of two warrants, and each two warrants are exercisable for one ordinary share at an exercise price of $11.50 per share. The units were sold in our initial public offering at an offering price of $10.00 per unit, generated $44,000,000 (before underwriting discounts and offering expenses) in gross proceeds.

Simultaneously with the consummation of our initial public offering, we completed a private placement of 282,000 units, issued to Greenland Asset Management Corporation (the “Sponsor”) and Chardan Capital Markets, LLC, which generated $2,820,000 in gross proceeds.

Business Combination

On October 24, 2019, we consummated our business combination with Zhongchai Holding (the “Business Combination”) after a special meeting, where the shareholders of Greenland considered and approved, among other matters, a proposal to adopt a share exchange agreement (the “Share Exchange Agreement”), dated as of July 12, 2019, among (i) Greenland, (ii) Zhongchai Holding, (iii) the Sponsor in the capacity as the purchaser representative (the “Purchaser Representative”), and (iv) Cenntro Holding Limited, the sole member of Zhongchai Holding (the “Zhongchai Equity Holder” or the “Seller”).

Pursuant to the Share Exchange Agreement, Greenland acquired from the Seller all of the issued and outstanding equity interests of Zhongchai Holding in exchange for 7,500,000 newly issued ordinary shares, no par value of Greenland, to the Seller (the “Exchange Shares”). As a result, the Seller became the controlling shareholder of Greenland, and Zhongchai Holding became a directly and wholly owned subsidiary of Greenland. The Business Combination was accounted for as a reverse merger effected by the Share Exchange Agreement, where Zhongchai Holding is considered the acquirer for accounting and financial reporting purposes.

The Business Combination was accounted for as a reverse recapitalization (the “Recapitalization Transaction”) in accordance with Accounting Standard Codification (“ASC”) 805, Business Combinations. For accounting and financial reporting purposes, Zhongchai Holding is considered the acquirer based on the following facts and circumstances:

| ● | Zhongchai Holding’s operations comprise the ongoing operations of the combined entity; | |

| ● | The officers of the newly combined company consist of Zhongchai Holding’s executives, including the Chief Executive Officer, Chief Financial Officer, and General Counsel; and | |

| ● | The former shareholders of Zhongchai Holding own a majority voting interests in the combined entity. |

As a result of Zhongchai Holding being the accounting acquirer, the financial reports filed with the SEC by the Company subsequent to the Business Combination are prepared “as if” Zhongchai Holding is the predecessor and legal successor to the Company. The historical operations of Zhongchai Holding are deemed to be those of the Company. Thus, the financial statements included in this report reflect (i) the historical operating results of Zhongchai Holding prior to the Business Combination; (ii) the combined results of Zhongchai Holding and Greenland following the Business Combination in October 2019; (iii) the assets and liabilities of Zhongchai Holding at their historical cost, and (iv) Greenland’s equity structure for all periods presented. Zhongchai Holding received 7,500,000 shares of Greenland in exchange for all the share capital, which is reflected retroactively to December 31, 2017 and will be utilized for calculating earnings per share in all prior periods. No step-up basis of intangible assets or goodwill was recorded in the Business Combination transaction, which is consistent with the treatment of the transaction as a reverse recapitalization of Zhongchai Holding.

Incorporation of Greenland Technologies Corp.

On January 14, 2020, Greenland Technologies Corp. was incorporated under the laws of the state of Delaware (“Greenland Tech”). Greenland Tech is a wholly-owned subsidiary of the registrant. We aim to use Green Tech as the US operation site for the Company in order to promote sales of our robotic products for the North American market in the near future.

2

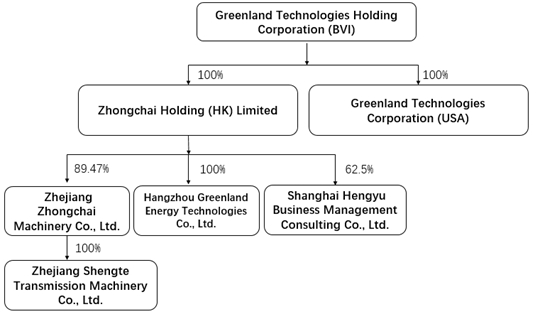

Corporate Structure

The following diagram illustrates the current corporate structure of Greenland, including the jurisdiction of formation and ownership interest of each of its subsidiaries.

Greenland was incorporated on December 28, 2017 as a British Virgin Islands Company with limited liability. As a result of the consummation of the Business Combination, Greenland serves as the parent Company for Zhongchai Holding.

Zhongchai Holding was incorporated in Hong Kong on April 23, 2009. From April 23, 2009 to November 1, 2011, Zhongchai Holding was a subsidiary of Equicap, Inc., a Nevada corporation with its stock quoted on the OTC Markets until July 29, 2011.

Greenland Technologies Corporation was incorporated in the state of Delaware on January 14, 2020 as a wholly owned subsidiary of Greenland (“Greenland Tech”). The Company aims to use it as its U.S. operation site to promote sales of electric engineering vehicles, including electric forklifts, electric loading vehicles, electric digging vehicles, and other products for the North American market in the near future. Greenland Tech currently does not conduct any business activities.

Zhejiang Zhongchai Machinery Co., Ltd. (“Zhejiang Zhongchai”), an 89.47% owned subsidiary of Zhongchai Holding, was incorporated in the PRC on November 21, 2005 and engages in the business of designing, manufacturing, and selling transmission products mainly for forklift trucks. The remaining 10.53% of Zhejiang Zhongchai’s capital stock is owned by Xinchang County Jiuxin Investment Management Partnership (LP) (“Jiuxin”), an entity owned by Mengxing He, director and general manager of Zhejiang Zhongchai and legal representative, executive director, and general manager of Shengte (as defined below).

Hangzhou Greenland Energy Technologies Co., Ltd., formerly known as Hangzhou Greenland Robotic Co., Ltd. prior to November 6, 2020 (“Hangzhou Greenland”), a wholly-owned subsidiary of Zhongchai Holding, was incorporated in the PRC on August 9, 2019 and engages in the business of research and development of electric engineering vehicles, including electric forklifts, electric loading vehicles, electric digging vehicles, and other products. Hangzhou Greenland is also committed to product supply chain integration and overseas sales.

Zhejiang Shengte Transmission Machinery Co., Ltd. (“Shengte”), a PRC Company incorporated on February 24, 2006, has been a wholly-owned subsidiary of Zhejiang Zhongchai since May 21, 2007. Shengte was engaged in the business of manufacturing and selling of gears used in Zhejiang Zhongchai’s transmission products. In 2019, Shengte ceased its business operations with most of its assets transferred to Zhejiang Zhongchai; only the employee’s social benefit function, in the local region, remains effective.

Shanghai Hengyu Business Management Consulting Co., Ltd. (“Hengyu”), a 62.5% owned subsidiary of Zhongchai Holding, was incorporated in PRC on September 10, 2005 and holds no assets other than an account receivable owed by Cenntro Holding Limited (“Cenntro Holding”), the sole member of Zhongchai Holding prior to the closing of the Business Combination. The remaining 37.5% of Hengyu’s capital stock is beneficially owned by Peter Zuguang Wang.

3

Products

Greenland provides transmission systems and integrated powertrains for material handling machineries, particularly for electric forklift trucks. In order to expand and diversify existing product offerings, Greenland recently has entered into the electric industry vehicles market, by designing and developing.

Transmission products for material handling machineries

Transmission Systems. For 14 years, Greenland, along with its subsidiaries, specialized in designing, developing, and manufacturing a wide range of transmission systems for material handling machineries, in particular forklift trucks. The range of the transmission systems covers from one ton to fifteen tons machineries. Most transmission systems contain auto transmission features. This feature allows for easy machine operations. In addition, Greenland provides transmission system for internal combustion powered machineries as well as for electrical powered machineries. Greenland has experienced an increasing demand for electric powered transmission systems. These transmission systems are key components for material handling machinery assembly. To meet this increasing demand, Greenland is able to providing these transmission systems to major forklift truck original equipment manufacturers (“OEMs”) as well as certain global branded manufacturers.

Integrated Powertrain. Greenland has newly designed and developed unique powertrains, which integrates electric motor, speed reduction gearbox, and driving axles into a combined integral module, in order to meet a growing demand for advanced electric forklift trucks. This integrated powertrain will enable the OEMs to significantly shorten design cycle, improve machinery efficiency, and simplify manufacturing process. There is a new trend that OEMs would rather use an integrated powertrain than separate electric motor, speed reduction gearbox, and driving axles, particularly in electric forklift trucks. Currently, Greenland makes two tons to three and a half-tons integrated powertrains for few electric forklift truck OEMs. Greenland is in the process to add more integrated powertrain products for electric forklift truck OEMs with different sizes.

Electric Industrial Vehicles (to be launched in third or fourth quarter 2021)

There is an increasing demand for electric industrial vehicles where sustainable energies are used in order to reduce air pollutions and lower carbon monoxide emissions. For Greenland, it plans to enter into the electric industrial vehicles market by utilizing its existing technologies, know-hows, supply chains, and market access. Greenland’s teams have been developing 1.8 tons electric loader vehicle (GEL1800) and plans to setup an assembly facility on the east coast of the United States for final assembly. GEL1800 will be our first electric industry vehicle product and will be available in the third or fourth quarter of 2021. Other models, such as models with loading capacity of one and a half tons or five tons are currently under development. Greenland will co-operate with global parts suppliers to utilize their matured supply chain, which will enable it to shorten its development cycle and make quicker market entrance.

4

Competitive Strengths

Greenland believes that it is in the right position and the right time to supply a new generation of industrial vehicles that is green, safe, and cost-effective. The following is a summary of Greenland’s competitive strengths.

Favorable Market Trends

Greenland believes that a number of key industry trends in the PRC will continue to benefit Greenland and its subsidiaries and continue to drive its growth, including:

| ● |

Increasingly stringent regulations over carbon emission, which urge market participants to adopt low or zero-emission material handling and construction equipment; | |

| ● |

Increasing demand for a safer work environment and better healthy worker’s condition will drive growth of electric material handling equipment or industry vehicle, which generates no exhausts and a low level of noise in operation; | |

| ● | Increasing labor cost, which accelerates labor substitution with machinery in material handling and logistic activities; | |

| ● |

Strong competitiveness of USA branded products in the USA, in which the next generation of electric industrial vehicle will be assembled and sold; | |

| ● |

Increasing government support for improving efficiency in the PRC’s logistics industry, which is a key market for material handling machinery such as forklifts and loaders; and | |

| ● | Increasing government support for logistic mechanization, including in the form of subsidies. |

As a result of these favorable industry trends, Greenland believes that it is well-positioned to capitalize on the increasing market demand for transmission products in the PRC as well as on the growing demand for emission-free and labor substitution by electric vehicles in the United States.

Well-Developed Manufacturing Capabilities Leading to Higher Efficiency

Greenland’s well-developed manufacturing process contributes to manufacturing efficiency and cost-effectiveness. Specifically, a combination of modern operational and management systems, advanced manufacturing equipment, experienced manufacturing know-hows, skilled workforce, and flexible manufacturing system allows Greenland to shorten the “time to market” for its new products. Moreover, the combination allows Greenland to timely adjust its lines of products in anticipation of changes in market demands.

Robust Research and Product Development Capabilities

Research and product development capabilities have been critical to Greenland’s historical growth and current market position. Such capabilities include the following:

| ● | Strong R&D team. Greenland’s research and development team is comprised of more than 69 professionals, or over 10% of Greenland’s employees. It is led by Dr. Lei Chen, former professor at The University of Texas – Austin, who has many years of experience in research and development in introducing and adopting new technologies. | |

| ● | Facilities. Greenland’s research and development facilities consist of a transmission technology center and a electric industry vehicle center. The transmission technology center is accredited by the Zhejiang provincial government. The technology center is made up of a product development and design department, a research center, three research departments that focuses on design, application, and manufacturing of internal combustion engines, and a post-doctoral workstation (certified by the PRC Ministry of Human Resource and Social Security). |

5

Strategic Service Network

The ability to provide timely after-sales services is critical in building and maintaining a loyal and solid customer base. We have strategically established an after-sales service network in locations with developed economies. For example, the eastern provinces of the PRC generally have significant demand for logistics services. Accordingly, Greenland, through its subsidiaries, has operated an in-house service center and retained service providers that conduct businesses predominantly in these regions. Users of Greenland’s products are able to reach the Company through a service line, through which Greenland is able to provide prompt on-site technical services.

Experienced Management Team with Successful Track Records

Greenland’s senior management team is comprised of individuals who have operational experience, market knowledge, international management skill, and technical expertise. In addition, each member of the senior management team has a proven track record in building and turning companies into successful enterprises.

| ● | Peter Zuguang Wang has served as the sole director of Zhongchai Holding since April 2009 and the chairman of Zhejiang Zhongchai since September 2017. He has over 20 years of experience in technology and management, along with a unique background in research and development, operation, finance and management. Mr. Wang was the co-founder of Unitech Telecom (now a part of UTStarcom, Nasdaq: UTSI). | |

| ● | Raymond Z. Wang has served as the Chief Executive Officer of Zhongchai Holding since April 2019. He has more than ten years of management and corporate governance experience, and has served as president and vice president for two international companies and vice chairman of the board for a non-profit organization. Mr. Wang’s experience includes warehouse management, logistics modernization, financial management, organizational management, business process optimization, and customer channel acquisition. | |

| ● | Jing Jin, Chief Financial Officer, a Certified Public Account, has over 10 years of experience in accounting, budgeting, and financial planning across operations in the PRC and overseas. Prior to August 2019, Mr. Jin has also served as the chief financial officer of Tantech Holdings Ltd. (Nasdaq: TANH). | |

| ● | Lei Chen, Chief Scientist, has over 25 years of experience as a scientist in both U.S. and PRC. He is skillful in unconventional solutions by crossing different science and technology disciplines. Dr. Chen has expertise in laser spectroscopy, high-speed data acquisition, atomic and molecular physics, Nanomaterial, software and hardware architecture and design, combustion engine and electrical motor, and livestock husbandry. Dr. Chen’s experience and scientific knowledge is valuable to Zhongchai Holding’s research and development efforts with respect to transmission products and future robotic products. |

Customers

Greenland, through its subsidiaries, sells most of its products domestically in the PRC. Its customer bases are primarily in the businesses of material handling equipment and forklift trucks. Greenland believes that its customers include some of the leading manufacturers in their respective market segments. Greenland also supplies to the PRC subsidiaries of a number of blue-chip international brands based in Europe and Asia.

During the years ended December 31, 2020 and 2019, Greenland’s five largest customers contributed 48.85% and 43.62%, respectively, of its total revenues. In the same periods, Greenland’s single largest customer, Hangcha Group, accounted for 21.25% and 14.03%, respectively, of Greenland’s total revenue. Greenland sells products to Hangcha Group based on purchase orders submitted to its subsidiary, Zhongchai Holding.

6

Suppliers

Greenland purchases its raw materials from various suppliers for use in the manufacture of its products.

The key raw materials used to manufacture its products are processed metal-based parts and components, including iron castings and gears, which are purchased from our domestic suppliers in the PRC. Most of our suppliers are located within close proximity to our manufacturing facilities, which reduces our transportation and inventory costs.

The prices for iron and steel and other raw materials have historically fluctuated significantly in the PRC, which in turn has affected the Company’s business and operation results. Greenland closely monitors changes in raw material prices and seeks to adjust its inventory of raw materials during inflation periods. In addition, Greenland seeks to minimize the impact of fluctuations in raw material prices by adopting bidding processes in its raw material procurement process Greenland also seeks to price its products to reflect the expected fluctuations in raw material prices to the extent possible. However, there can be no assurance that Greenland could precisely estimate any increase in raw material price or pass on such increase to its customer.

Production

Greenland’s products are comprised of a number of major parts and components, including gearbox housing, gears, bearings, oil pumps, gear shafts, hydraulics, and electrical components. The gearbox housing and gears parts are processed in-house at its manufacturing facility in Xinchang County, Zhejiang Province, PRC. Components of such products, in general, are sourced, from third parties, assembled, and integrated to form finished products. The finished products then undergo further adjustments, fine tunings, testing, and quality inspections. At the end of the inspection process and prior to shipment to our warehouses for storage and distribution, the finished products are coated and painted.

For the manufacturing of its electric industrial vehicles, Greenland plans to establish a new facility on the east coast of the U.S. and start producing electric industrial vehicles between the third and fourth quarter of 2021.

Inventory and Warehousing

Greenland undertakes inventory control in order to reduce the risks of under and over-stocking. On average, Greenland typically maintains a 30 days stock piles for production needs. It generally increases its inventories toward the end of the year in order to meet any production demand, in anticipation of any demands increase, from the second quarter of the following year. Furthermore, Greenland maintains higher inventories at year-end because Chinese New Year typically falls in January or February, which affects production and transportation of raw materials. Greenland has installed an enterprise resource planning (“ERP”) system, which provides real-time information about purchases, production schedules, and supplies of the raw materials. The ERP system has substantially improved Greenland’s inventory controls, providing the Company with quick access to various data and easy formulation of operating models, and allowing the Company to keep its inventory at an appropriable level to facilitate the manufacturing process. Due to the COVID-19 outbreak, the Company’s production significantly decreased during the first quarter of the fiscal year 2020. However, since March 2020, the Company’s production has returned to normal, and the Company experienced a substantial increase in production demand in November and December 2020.

Research and Development

Greenland’s research and development team selects research or development projects or both and draws up preliminary project proposals based on various factors, such as industry and market trends, customer feedback, and input from other departments (i.e. finance and manufacturing departments).

Greenland’s management, including the heads and lead managers of various internal departments, such as sales and marketing and finance departments, as well as the Chief Executive Officer and Chief Technology Officer, reviews the preliminary project proposals and its research and development team formulates a final plan for each approved project after considering suggestions and comments by its management. The final plans will include detailed schedules and budgets for the projects. Greenland’s finance department monitors budget overruns. Any increase in the original budget must be reviewed and approved by management before the relevant project can continue.

Greenland has also focused on research and development with respect to a new electric industrial vehicle.

7

Strategic Growth Opportunity in the Electric Industrial Vehicle Industry

Greenland will expand its market presence by entering the electric industrial vehicle industry. With our strategic supply chain partners, we have leveraged our robust research and development capabilities, as well as our industry and market experience to develop a new product line of electric industrial vehicles. By July 2021, Greenland expects to complete its first production-ready model of electric industrial vehicle product. A compact electric loader vehicle with a payload capacity of approximately 1,800 kilograms (or 3,968 lbs.). This new product line of electric industrial vehicles will offer a better return on investment when compared to existing Internal Combustion (“IC”) industrial vehicles by leveraging Greenland’s established global supply chain and expertise in the electrification of material handling vehicles. Following the first electric loader product, Greenland intends to expand its product line to other industrial vehicles and sizes.

We believe that electric industrial vehicles, which include electric loaders, excavators and forklift trucks, have the following advantages over traditional IC vehicles:

| ● | Zero carbon emission. Fully electric industrial vehicles are completely emission free leading to less pollution from local usage. In addition, electrical power generation produces less carbon emissions when compared to fossil fuel. This results in a more environmentally friendly and sustainable power source. | |

| ● |

Lower energy usage and maintenance costs. Electric industrial vehicles offer a significant saving in energy consumption when compared to diesel equipment. Conventional internal combustion power systems require costly routine maintenance that increases with age. Without the need to maintain these internal combustion engines, electric industrial vehicles provide significantly less maintenance costs and less operational downtime resulting in a greater return on investment. | |

| ● |

Lower level of noise and vibration. Electric vehicles are proven to produce less sound and vibration when compared to internal combustion vehicles due to the lack of complicated transmission components and coolant pumps. The low noise levels of electric industrial vehicles offer new opportunities to businesses such as working at night in urban areas or during the day close to noise-sensitive locations like parks and hospitals. | |

| ● | Demand for Better Workplace Safety and New Applications. Conventional excavators and loaders that use internal combustion engines create significant fumes, emissions, noises and vibrations which can harm the health of staff and surrounding residents. These problems can be addressed by the adoption of electric powered equipment which produce zero emissions, low levels of noise and minor vibrations. This creates a safer work environment and new business opportunities for indoor applications. |

We believe that the electric industrial vehicle market presents a substantial opportunity for Greenland’s future business growth:

Fast Growing Market. The global construction equipment market is anticipated to grow at a compound annual growth rate (“CAGR”) of 3.9% from 2020 to 2025, reaching US$205 billion1. The North American market is projected to exhibit one of the fastest growth rates during the forecast period. Consequently, we believe this growth will increase with the introduction of the United State infrastructure overhaul program. Should the program be implemented, then it will be a powerful driver of growth in the engineering and construction industry that will proliferate the demand for industrial vehicles and equipment.

Call for Carbon Emission Reduction. Global efforts to reduce greenhouse gas and carbon emissions continue to grow with proposals such as the current US administration seeking a target of net zero emission by 2050. These strategies will result in government and public support for the adoption of emission zero technologies and equipment across industries thus boosting the demand for eco-friendly electric powered industrial vehicles. As such, we expect that the demand for electric industrial vehicles will increase rapidly.

Highly Fragmented and Emerging Market. The electric industrial vehicle market is highly fragmented with few, if any, dominant local market participants. Although a few conventional industrial vehicles and construction equipment makers are in the process of electric products development a majority are years away from product deployment. This is to avoid cannibalization with the mature fossil fuel-powered equipment product lines which results in the lack of incentive to launch the full-electric industrial vehicles at the near term. As a result, with the early mover advantage together with Greenland’s strong research and development capability, we believe that Greenland is well positioned to secure a meaningful role in the electric industrial vehicle market.

| 1 | - Marketsandmarkets Nov 2020 Report: Construction Equipment Market by Type (Excavator-Crawler & Mini, Loader-Backhoe, Skid-steer, Wheel, Dozer, Dump Truck, Others), Electric Equipment, Propulsion, Power Output, Application, Rental, Aftertreatment Device and Region - Global Forecast to 2025 |

8

High Technology Barriers for New Entrants. To compete in the electric industrial vehicle market, enterprises need a high-level of core technologies and capabilities in order to successfully develop a commercial product. The investment and expertise required create a high barrier of entry for new market players. Greenland’s success in the material handling industry and its achievements in research and development milestones gives Greenland the opportunity and the competitive edge to successfully compete in the industrial vehicle market.

Trademarks and Other Intellectual Property

Greenland relies on a combination of trademark, copyright, patent, software registration, and trade secret laws to protect its intellectual property rights. Despite these precautions, it may be possible for third parties to infringe our Company’s intellectual property rights.

Patents

As of December 31, 2020, Greenland held 108 registered patents, with the PRC National Intellectual Property Administration (“CNIPA”), 98 of which are utility patents and 10 of which are invention patents. These patents relate to the manufacturing of products.

As of December 31, 2020, Greenland had been granted 2 trademarks registered with the CNIPA.

Greenland’s intellectual property also includes technical data such as test results and operating data from projects, drawings, designs, and machinery and manufacturing techniques it developed in-house.

Sales and Marketing

Greenland sells its products in PRC through its sales and marketing teams. To promote Greenland’s brand, sales employees also attend trade shows and exhibitions to showcase our products.

As of December 31, 2020, Greenland’s sales and marketing team consisted of 14 employees. Members of its sales and marketing teams have extensive experience and knowledge in the material handling equipment sector of the manufacturing industry. They are primarily responsible for identifying business opportunities, promoting products, collecting customer feedbacks and market information, bidding for or negotiating orders, and collecting payments.

Competition

The transmission industry is fragmented and highly competitive in the PRC. Under the current market trend, domestically produced transmissions account for the largest share of the PRC market. International brand manufacturers equipped with better technology and capital resources are also aiming to expand into the PRC. As a result, it is expected that the PRC transmission market will become more competitive.

The typical competitive criteria are quality, price, technology, after-sales service, product offering, and performance record. The transmissions market is capital intensive; in capital and operating cost. In addition, the manufacturing process requires technical expertise and significant research and development budgets. As a result, companies entering the market must have significant financial and technical resources. Moreover, the time and cost required to establish a proven track record, necessary for general market acceptance, are substantial. An extensive after-sales service network is essential for a Company to gain general market acceptance.

Greenland believes that it is able to compete based on its market position, strong research and development capabilities, high quality products, integrated service systems, and strong relationships with its customers.

Our key competitors are Shaoxing Advance Gearbox Co., Ltd., Changsha Zhongchuan Transmission Machinery Co. Ltd., and Ganzhou Wuhuan Machine Co., Ltd.

9

Employees

As of December 31, 2020, the total number of full-time employees employed at Greenland and its subsidiaries was 328. The following table sets forth the number of its full-time employees by the function as of December 31, 2020:

| Function | Number | |||

| Management | 8 | |||

| Administration | 33 | |||

| Production | 186 | |||

| Research and development | 69 | |||

| Sales and marketing | 14 | |||

| Other | 18 | |||

| Total | 328 | |||

Greenland maintains mandatory social security insurance for its our employees pursuant to Chinese laws. Furthermore, it contributes mandatory social security funds for employees with respect to retirement, medical, work-related injury, maternity, and unemployment benefits.

Greenland has not had any labor strikes or other labor disturbances that have materially interfaced with its operations, and it believes that it has maintained a good work relationship with its employees.

Regulations

PRC Law and Regulation

Policy Relating to the Foreign Invested General Equipment Manufacturing Industry

PRC implements its guidance on foreign investment in different industries through the Catalogue for the Guidance of Foreign Investment Industries jointly amended and promulgated by the National Development and Reform Commission and the Ministry of Commerce from time to time. According to the new catalogue which became effective on July 28, 2017, the business activities that we engage in are classified as “permitted” or “encouraged” foreign invested industries.

Law and Regulation Relating to Product Quality

Pursuant to the Product Quality Law of the PRC which was promulgated on February 22, 1993 and amended on December 29, 2018, it is prohibited to produce or sell products that do not meet the standards or requirement for safeguarding human health and ensuring human and property safety.

Where a defective product causes physical injury to a person or damage to property, the aggrieved party may claim compensation against the producer or the seller of such product. Where the responsibility for product defects lies with the producer, the seller shall, after settling compensation, have the right to recover such compensation from the producer, and vice versa. Violations of the Product Quality Law may result in the imposition of fines. In addition, the seller or the producer may be ordered to suspend operation and its business license may be revoked. Criminal liability may be incurred in serious cases.

Law and Regulation Relating to Production Safety

Pursuant to the Production Safety Law of the PRC (the “Production Safety Law”) promulgated by the Standing Committee of the National People’s Congress on June 29, 2002, amended on August 27, 2009 and August 31, 2014 and effective on December 1, 2014, enterprises and institutions shall be equipped with the conditions for safe production as provided in the Production Safety Law and other relevant laws, administrative regulations, national standards and industrial standards. Any entity that is not equipped with such conditions is not allowed to engage in production and business operation activities.

10

The law also requires manufacturers to offer education and training programs to their employees regarding production safety and to hire qualified employees who have completed special trainings to engage in specialized operations. Manufacturers are required to provide protection equipment that meets the national or industry standards to employees and to supervise and educate them regarding the use of such equipment. In addition, the design, manufacture, installation, use, inspection and maintenance of safety equipment are required to conform to applicable national or industry standards. Furthermore, emergency measures shall be established by an enterprise to prepare for the occurrence of any accidents threatening safe production.

Law and Regulation Relating to Environmental Protection

The laws and regulations governing the environmental requirements for all units that cause environmental pollution and other public hazards in the PRC include but not limited to the Environmental Protection Law of the People’s Republic of China, the Prevention, the Environmental Impact Assessment Law of the People’s Republic of China and the Administrative Regulations on Environmental Protection for Acceptance Examination Upon Completion of Buildings. Pursuant to these laws and regulations, depending on the impacts on the environment caused by the project, an environmental impact study report and impact analysis table or environmental impact registration form shall be submitted by a developer for approval before commencement of construction or property development.

In addition, upon completion of the property development, relevant environmental authorities and the construction units will perform inspections to ensure compliance, with the applicable environmental standards and regulations, prior to the delivery of property to the purchasers.

Law and Regulation Relating to Labor Protection

Pursuant to the Labor Law of the PRC and the Labor Contract Law of the PRC which were promulgated on January 1, 1995 (amended on December 29, 2018) and January 1, 2008 (amended on December 28, 2012), respectively, labor contracts shall be concluded if labor relationships are to be established between the employer and the employees.

Pursuant to the Social Insurance Law of the PRC which was promulgated on October 28, 2010 and last amended on December 29, 2018, employees shall participate in basic pension insurance, basic medical insurance and unemployment insurance. Basic pension, medical and unemployment insurance contributions shall be paid by both employers and employees. Employees shall also participate in work-related injury insurance and maternity insurance. Work-related injury insurance and maternity insurance contributions shall be paid by employers rather than employees. An employer shall make registration with the local social insurance agency in accordance with the provisions of the Social Insurance Law of PRC. Moreover, an employer shall declare and make social insurance contributions in full and on time. Pursuant to the Regulations on Management of Housing Provident Fund which was promulgated on April 3, 1999 and amended on March 24, 2019, employers shall undertake registration at the competent administrative center of housing provident fund and then, upon the examination by such administrative center of housing provident fund, undergo the procedures of opening the account of housing provident fund for their employees at the relevant bank. Enterprises are also obliged to timely pay and deposit housing provident fund for their employees in full amount.

Law and Regulation Relating to Tax

Enterprise Income Tax

On March 16, 2007 and December 6, 2007 respectively, the National People’s Congress of China and the State Council of the PRC enacted the Enterprise Income Tax Law of the PRC and the Implementation Regulations of Enterprise Income Tax Law of the PRC (collectively the “PRC EIT Law”), both of which became effective on January 1, 2008. The PRC EIT Law imposes a uniform enterprise income tax rate of 25% on all residence enterprises, including foreign-invested enterprises, and terminates most of the tax exemptions, reductions and preferential treatments available under previous tax laws and regulations.

However, the PRC EIT Law and its implementation rules permit certain “high-technology enterprises strongly supported by the state” which hold independent ownership of core intellectual property and simultaneously meet a list of other criteria, financial or non-financial, as stipulated in the Implementation Rules, to enjoy a 15% enterprise income tax rate subject to certain new qualification criteria. The SAT, the PRC Ministry of Science and Technology and the MOF jointly issued the Administrative Rules for the Certification of High and New Technology Enterprise delineating the specific criteria and procedures for “high and new technology enterprises” certification.

11

Under the PRC EIT Law, enterprises are classified as either “resident enterprises” or “non-resident enterprises.” Pursuant to PRC EIT Law and its implementation rules, besides enterprises established within the PRC, enterprises established outside PRC whose “de facto management bodies” are located in PRC are considered “resident enterprises” for PRC enterprise income tax purposes and subject to the uniform 25% enterprise income tax rate for their global income. According to the implementation rules of the PRC EIT Law, “de facto management body” refers to a managing body that exercises, in substance, overall management and control over the manufacture and business, personnel, accounting and assets of an enterprise.

Withholding Tax

The PRC EIT Law removes the prior tax exemption and imposes a 10% withholding tax on dividends paid by foreign-invested enterprises to foreign investors. However, for foreign investors whose home countries or regions have signed bilateral tax agreements with PRC, the withholding tax rate may be reduced to as low as 5% depending on the terms of the applicable tax treaty. In accordance with the Arrangement between Mainland PRC and Hong Kong for the Avoidance of Double Taxation and Prevention of Fiscal Evasion with respect to Taxes on Income signed on August 21, 2006, the 5% withholding tax rate applies to dividends paid by a PRC Company to a Hong Kong tax resident, provided that the recipient is a Company that holds directly at least 25% of the interest of the PRC Company, otherwise, the applicable withholding tax rate should be 10%. Further, pursuant to the Notice on the Issues concerning the Application of the Dividend Clauses of Tax Agreements issued by the SAT on February 20, 2009, the preferential tax rate under the relevant tax treaties shall only apply to a tax resident from the other side that directly holds at least 25% of the interest of a PRC Company for a period of consecutive 12 months prior to receiving the dividends.

Value Added Tax

The Provisional Regulations of the PRC Concerning Value Added Tax (the “VAT Regulations”), was promulgated on December 13, 1993 and amended by the State Council and became effect on November 19, 2017. Under the VAT Regulations and its implementation regulations, value added tax, or the VAT, is imposed on the sales of goods and provision of processing, repair and replacement services within the PRC and the importation of goods into PRC. The VAT standard rate had been 17% of the gross sale price until April 30, 2018, after which date the rate was reduced to 16%. VAT rate was further reduced to 13% starting from April 1, 2019.

On April 4, 2018, the Ministry of Finance and the State Administration of Taxation issued the Circular on Adjustment of VAT Rates, which became effective as of May 1, 2018. According to the Circular on the Adjustment of VAT Rates, relevant VAT rates have been reduced from May 1, 2018, such that VAT rates of 17% and 11% applicable to the taxpayers who have VAT taxable sales activities or imported goods are adjusted to 13% and 9%, respectively.

Law and Regulation Relating to Intellectual Property Rights

Copyright Law

According to the Copyright Law of the PRC, which was amended on February 26, 2010 and became effective on April 1, 2010, Chinese citizens, legal entities or other organizations shall enjoy the copyright in their works, whether published or not, which include works of literature, art, natural sciences, social sciences, engineering and technology, etc. Copyright owners shall enjoy various kinds of rights, including the right of publication, right of authorship and right of reproduction.

Patent Law

Pursuant to the Patent Law of the PRC which was amended on December 27, 2008 and became effective on October 1, 2009, the patent administration departments of the State Council are responsible for the administration of patents across the nation. The patent administration departments of provincial, autonomous region or municipal governments are responsible for administering patents within their respective jurisdictions. The PRC patent system adopts a “first come, first file” principle, which means where more than one person files a patent application for the same invention, a patent will be granted to the person who files the application first. To be patentable, invention or utility models must meet three criteria: novelty, inventiveness and practicability. Invention patents are valid for 20 years, while utility model patents and design patents are valid for 10 years, commencing from the date of application. The patentee shall pay annual fees commencing from the year when the parent right is granted. If the patentee does not pay annual fees according to the requirements, the patent will be terminated prior to its expiry. Other person must obtain consent or a proper license from the patent owner to use the patent. Otherwise, the use constitutes an infringement of the patent rights. The infringer must, in accordance with the applicable regulations, undertake to cease the infringement, take remedial action and/or pay damages.

12

Trademark Law

Pursuant to the Trademark Law of the PRC which was amended on August 30, 2013 and became effective on May 1, 2014, the right to exclusive use of a registered trademark shall be limited to trademarks which have been approved for registration and to commodities for which the use of trademark has been approved. The period of validity of a registered trademark shall be 10 years, counted from the day the registration is approved. If a trademark registrant wishes to use a trademark after the expiration of the duration of the trademark registration, according to the requirements, a registration renewal application should be filed within 12 months prior to the expiration. Each registration renewal is valid for 10 years. Using a trademark that is identical with a registered trademark on the same commodities without the licensing of the registrant of the registered trademark; or using a trademark that is similar to a registered trademark on the same commodities, or using a trademark that is identical with or similar to the registered trademark on similar commodities without the licensing of the registrant of the registered trademark, which is likely to cause confusion; selling commodities that infringe upon the exclusive right to use a registered trademark; forging, manufacturing a registered trademark which was registered by others without authorization, or selling a registered trademark forged or manufactured without authorization; changing a registered trademark and putting the commodities with the changed trademark into the market without the consent of the registrant of the registered trademark; providing, intentionally, convenience for activities infringing upon others’ exclusive right to use a registered trademark, and facilitating others to commit infringement on the exclusive right to use a registered trademark, constitutes an infringement of the exclusive right to use a registered trademark. The infringer must undertake to cease the infringement, take remedial action and pay damages. The infringer also may be subject to fines or even criminal punishment.

Domain Names

The domain names are protected under the Administrative Measures for Internet Domain Names promulgated by Ministry of Industry and Information Technology, or the MIIT, on August 24, 2017, the effective date of which was November 1, 2017. MIIT is the major regulatory body responsible for the administration of the PRC Internet domain names, under supervision of which PRC Internet Network Information Center, or CNNIC, is responsible for the daily administration of CN domain names and Chinese domain names. On September 25, 2002, CNNIC promulgated the Implementation Rules of Registration of Domain Name, or the CNNIC Rules, which was renewed on June 5, 2009 and May 29, 2012, respectively. Pursuant to the Administrative Measures on the Internet Domain Names and the CNNIC Rules, the registration of domain names adopts the “first to file” principle and the registrant shall complete the registration via the domain name registration service institutions. In the event of a domain name dispute, the disputed parties may lodge a complaint to the designated domain name dispute resolution institution to trigger the domain name dispute resolution procedure in accordance with the CNNIC Measures on Resolution of the Top-Level Domains Disputes, file a suit to the People’s Court or initiate an arbitration procedure.

Law and Regulation Relating to Foreign Currency Exchange

The principal regulations governing foreign currency exchange in the PRC are the Foreign Exchange Administrative Regulations (the “SAFE Regulations”) which was promulgated by the State Council and last amended on August 5, 2008. Under the SAFE Regulations, the RMB is generally freely convertible for current account items, including the distribution of dividends, trade and service related foreign exchange transactions, but not for capital account items, such as direct investment, loan, repatriation of investment and investment in securities outside the PRC, unless the prior approval of the State Administration of Foreign Exchange is obtained.

U.S. Laws and Regulations

Vehicle Safety and Testing

We expect to be required to comply with federal laws administered by National Highway Traffic Safety Administration (“NHTSA”), including the CAFE standards, Theft Prevention Act requirements, consumer information labeling requirements, Early Warning Reporting requirements regarding warranty claims, field reports, death and injury reports and foreign recalls, owner’s manual requirements and additional requirements for cooperating with safety investigations and defect and recall reporting. The U.S. Automobile Information and Disclosure Act also requires manufacturers of motor vehicles to disclose certain information regarding the manufacturer’s suggested retail price, optional equipment and pricing. In addition, federal law requires inclusion of fuel economy ratings, as determined by the U.S. Department of Transportation and the Environmental Protection Agency (the “EPA”), and 5-star safety ratings as determined by NHTSA, if available.

Battery Safety and Testing

Our battery packs of electric industrial vehicles will be subject to various U.S. regulations that govern transport of “dangerous goods,” defined to include lithium batteries, which may present a risk in transportation. We expect to use lithium battery packs in our electric industrial vehicles. The use, storage and disposal of our battery packs are regulated under existing laws and are the subject of ongoing regulatory changes that may add additional requirements in the future.

13

| ITEM 1A. | RISK FACTORS |

Smaller reporting companies are not required to provide the information required by this item.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

The address of our principal executive offices and corporate offices is 11-F, Building #12, Sunking Plaza, Gaojiao Road, Hangzhou, Zhejiang Province, People’s Republic of China, 311122.

Greenland’s headquarters, manufacturing and R&D facilities are all located in Xinchang County, Zhejiang Province, PRC.

Properties Owned by us

As of December 31, 2020, Greenland held land use rights of four parcels of land with an aggregate site area of approximately 81,171 square meters, located in Xinchang County, Zhejiang Province, PRC. The terms of these land use rights are due to expire on November 14, 2062.

As of December 31, 2020, Greenland held three building ownership certificates for three buildings with an aggregate gross floor area of approximately 44,751 square meters. These properties are primarily used for production and office purposes.

Properties Leased by us

As of December 31, 2020, Greenland leased one property for its operations with an aggregate gross floor area of approximately 200 square meters. The rent per month is RMB10,950 (approximately $1,580) and the duration of the lease is from June 01, 2019 to May 31, 2020.

We consider our current office space adequate for our current operations.

| ITEM 3. | LEGAL PROCEEDINGS |

From time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. Litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise from time to time that may harm our business. There are currently no legal proceedings or claims that we believe will have a material adverse effect on our business, financial condition or operating results, except the following matter.

| ITEM 4. | MINE SAFETY DISCLOSURES |

None.

14

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our ordinary shares are traded on the Nasdaq Capital Market under the symbol “GTEC.” Our ordinary shares commenced public trading on August 8, 2018.

The market price of our ordinary shares is subject to significant fluctuations in response to variations in our quarterly operating results, general trends in the market, and other factors, over many of which we have little or no control. In addition, broad market fluctuations, as well as general economic, business, and political conditions, may adversely affect the market for our ordinary shares, regardless of our actual or projected performance. We cannot assure you that there will be a market for our ordinary shares in the future.

As of March 26, 2021, the last sale price reported on the Nasdaq Capital Market for our ordinary shares was approximately $15.50 per share.

Dividend Policy

Prior to the business combination on October 24, 2019, Zhejiang Zhongchai has paid approximately $0.16 million in dividends to its shareholders.

Shareholders of Record

As of March 19, 2021, we have 9 recorded holders of our ordinary shares. This number excludes any estimate by us of the number of beneficial owners of shares held in street name, the accuracy of which cannot be guaranteed.

Effective August 11, 1993, the SEC adopted Rule 15g-9, which established the definition of a “penny stock,” for purposes relevant to the Company, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require: (i) that a broker or dealer approve a person’s account for transactions in penny stocks; and (ii) that the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve a person’s account for transactions in penny stocks, the broker or dealer must (i) obtain financial information and investment experience and objectives of the person; and (ii) make a reasonable determination that the transactions in penny stocks are suitable for that person and that person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prepared by the Commission relating to the penny stock market, which, in highlight form, (i) sets forth the basis on which the broker or dealer made the suitability determination; and (ii) states that the broker or dealer received a signed, written agreement from the investor prior to the transaction. Disclosure also has to be made about the risks of investing in penny stock in both public offerings and in secondary trading, and about commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

15

Transfer Agent

The transfer agent for our capital stock is Continental Stock Transfer & Trust Company, located at 1 State Street 30th Floor, New York, NY 10004-1561. Their telephone number is (212) 509-4000.

Equity Compensation Plan Information

For information on the securities authorized for issuance under our equity compensation plan, please see “Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters.”

Recent Sales of Unregistered Securities

Since our inception on December 28, 2017, we did not have sales of unregistered securities other than those already disclosed in the quarterly reports on Form 10-Q in the fiscal years 2019 and 2018 and the current affair reports on Form 8-K and the following transactions.

Pursuant to the Service Agreement entered into and by The Company and Chineseinvestors.com, Inc., an Indiana corporation (“CIIX”) on August 21, 2019 (the “Service Agreement”), CIIX were to provide certain investor relations services to the Company for a period of three months beginning on August 21, 2019. Pursuant to the Service Agreement, the Company were to pay CIIX fees consisting of three equal monthly instalments of $12,000 and 5,000 restricted ordinary shares, no par value, of the Company on a quarterly basis during the term of the Consulting Agreement. On February 24, 2020, Greenland and CIIX entered into a termination agreement (the “CIIX Termination Agreement”) to terminate their respective obligations under the Service Agreement. Pursuant to the CIIX Termination Agreement, the Company agreed to issue 5,000 ordinary shares, no par value (the “CIIX Termination Shares”) to CIIX. Upon CIIX’s receipt of the CIIX Termination Shares, the Company will have fully satisfied its payment obligations under the Service Agreement.

Pursuant to the Investor Relations Consulting Agreement entered into and by The Company and Skyline Corporate Communication Group, LLC, a Massachusetts limited liability Company (“SCCG”) on August 15, 2019 (the “Consulting Agreement”), SCCG were to provide certain investor relations services to the Company for a period of twelve months beginning on August 15, 2019. Pursuant to the Consulting Agreement, the Company were to pay SCCG fees consisting of $5,000 per month and 1,250 restricted ordinary shares, no par value, of the Company on a quarterly basis during the term of the Consulting Agreement. On February 25, 2020, Greenland and SCCG entered into a termination agreement (the “SCCG Termination Agreement”) to terminate their respective obligations under the Consulting Agreement. Pursuant to the SCCG Termination Agreement, the Company agreed to issue 10,000 ordinary shares, no par value (the “SCCG Termination Shares”) to SCCG. Upon SCCG’s receipt of the SCCG Termination Shares, the Company will have fully satisfied its payment obligations under the Consulting Agreement.

On October 24, 2020, the board of directors held a meeting and executed resolutions to approve the issuance of 120,000 ordinary shares to Raymond Wang, our chief executive officer, to offset unpaid salary to him in the amount of $120,833.33 and the issuance of 135,000 ordinary shares to Jing Jin, our chief financial officer, to offset unpaid salary to him in the amount of $60,000 and his personal loan to us in the amount of $75,000. On November 10, 2020, we issued 135,000 ordinary shares to Jing Jin. On December 30, 2020 and February 8, 2021, we issued 69,000 and 51,000 ordinary shares to Raymond Wang, respectively.

| ITEM 6. | SELECTED FINANCIAL DATA |

As a smaller reporting Company, as defined by Item 10(f)(1) of Regulation S-K, we are not required to provide the information requested by this Item.

16

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF GREENLAND TECHNOLOGIES HOLDING CORPORATION |

The following discussion and analysis of financial condition and results of operations relates to the operations and financial condition reported in the consolidated financial statements of the Company thereto, which appear elsewhere in this Report, and should be read in conjunction with such financial statements and related notes included in this Report. Except for the historical information contained herein, the following discussion, as well as other information in this Report, contain “forward-looking statements,” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the “safe harbor” created by those sections. Actual results and the timing of the events may differ materially from those contained in these forward-looking statements due to many factors, including those discussed in the “Forward-Looking Statements” set forth elsewhere in this Report.

Overview

The registrant was incorporated on December 28, 2017 as a British Virgin Islands Company with limited liability. The registrant was incorporated as a blank check Company for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, recapitalization, reorganization or similar business combination with one or more target businesses. Following the Business Combination (as described and defined below) in October 2019, the registrant changed its name from Greenland Acquisition Corporation to Greenland Technologies Holding Corporation (“Greenland”).

On July 27, 2018, we consummated our initial public offering of 4,400,000 units, including a partial exercise by the underwriters of their over-allotment option in the amount of 400,000 units. Each unit consists of one ordinary share, no par value, one warrant to purchase one-half of one ordinary share, and one right to receive one-tenth of one ordinary share upon the consummation of our initial business combination, pursuant to a registration statement on Form S-1. Warrants must be exercised in multiples of two warrants, and each two warrants are exercisable for one ordinary share at an exercise price of $11.50 per share. The units were sold in our initial public offering at an offering price of $10.00 per unit, generated $44,000,000 (before underwriting discounts and offering expenses) in gross proceeds.

Simultaneously with the consummation of our initial public offering, we completed a private placement of 282,000 units, issued to Greenland Asset Management Corporation (the “Sponsor”) and Chardan Capital Markets, LLC, generated $2,820,000 in gross proceeds.

On October 24, 2019, we consummated our business combination with Zhongchai Holding (the “Business Combination”) following a special meeting, where the shareholders of Greenland considered and approved, among other matters, a proposal to adopt and entered into the Share Exchange Agreement that allowed Greenland to acquire from the Seller all of the issued and outstanding equity interests of Zhongchai Holding in exchange for 7,500,000 newly issued ordinary shares, no par value of Greenland, issued to the Seller. As a result, the Seller became the controlling shareholder of Greenland, and Zhongchai Holding became a directly and wholly owned subsidiary of Greenland. The Business Combination was accounted for as a reverse merger effected by a share exchange, wherein Zhongchai Holding is considered the acquirer for accounting and financial reporting purposes.

In connection with the Business Combination, all the outstanding rights of the Company were converted into 468,200 ordinary shares on a one-tenth (1/10) ordinary share per right basis if holders of the rights elected to convert their rights into the underlying ordinary shares.

17

On December 17, 2019, the Company’s warrants, which were trading under the ticker symbol “GTECW,” were delisted from the Nasdaq Capital Market by the Nasdaq Listing Qualifications Staff.

On January 14, 2020, Greenland Technologies Corp. was incorporated under the laws of the State of Delaware (“Greenland Tech”). Greenland Tech is the 100% owned subsidiary of the registrant. We aim to use it as the US operation site of the Company and promote sales of our robotic products for the North American market in the near future.

Greenland serves as the parent Company for the primary operating Company, Zhongchai Holding (Hong Kong) Limited, a holding Company formed under the laws of Hong Kong on April 23, 2009 (“Zhongchai Holding”). Through Zhongchai Holding and other subsidiaries, Greenland develops and manufactures traditional transmission products for material handling machineries in the People’s Republic of China (PRC), as well as develops electric industrial vehicles, which are expected to be produced in the near future.

Greenland, through its subsidiaries, is:

| ● | a leading developer and manufacturer of transmission products for material handling machineries in China; and | |

| ● | a developer of electric industrial vehicles, which is expected to be available in the third or fourth quarter of 2021. |

Greenland’s transmission products are key components for forklift trucks, used in manufacturing and logistic applications such as factories, workshops, warehouses, fulfilment centers, shipyards, and seaports. Forklifts play an important role in logistics for many enterprises across different industries in the PRC and around the globe. Generally, industries with the largest demand for forklifts are transportation, warehousing logistics, electrical machinery, and automobile.

Greenland has experienced increased demand for forklifts in the manufacturing industry in the PRC, as its revenue increased from approximately $52.40 million in the fiscal year 2019 to approximately $66.86 million in the fiscal year 2020. Based on revenues in the fiscal year ended December 31, 2020 and 2019, Greenland believes that it is one of the major developers and manufacturers of transmission products for small and medium-sized forklift trucks in PRC.

Greenland’s transmission products are used in 1-ton to 15-tons forklift trucks, some with mechanical shift and some with automatic shift. Greenland sells these transmission products directly to forklift truck manufacturers. In the fiscal year ended December 31, 2020 and 2019, Greenland sold an aggregate of more than 108,913 and 83,567 sets of transmission products, respectively, to more than 100 forklift manufacturers in the PRC.

In December 2020, Greenland launched a new division to focus on the electric industrial vehicle market, a market that Greenland intends to develop to diversify its product offerings. With this new division, Greenland plans to develop and deploy the next generation of industrial vehicles. Greenland plans to establish a new facility on the east coast of the U.S. and start producing electric industrial vehicles between the third and fourth quarter of 2021.

18

Impact of COVID-19 Pandemic on Our Operations and Financial Performance

The COVID-19 pandemic has severely affected China and the rest of the world. In an effort to contain the spread of the COVID-19 pandemic, China and many other countries have taken precautionary measures, such as imposing travel restrictions, quarantining individuals infected with or suspected of being infected with COVID-19, encouraging or requiring people to work remotely, and canceling public activities, among others. These ongoing measures adversely affected our operations and financial performance in 2020.

Specifically, the COVID-19 pandemic adversely affected our revenue in the first half of 2020. For example, from February 3, 2020 to the end of February 2020, the Company closed all of its operating offices in Zhejiang Province, including manufactory, in response to the emergency measures imposed by local government. The pandemic also significantly limited suppliers’ ability to provide low-cost, high-quality merchandise to the Company on a timely basis.

Since late March 2020, the Company’s business operations have gradually recovered from the negative impacts due to lockdown, and the Company’s backlogged orders were mostly processed during the rest of fiscal year 2020, which contributed to an increase in its revenues for the year ended December 31, 2020.