UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the fiscal year ended

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report .. . . . . . . . . . . . . . .

For the transition period from to

Commission file number:

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of Incorporation or Organization)

(Address of Principal Executive Offices)

Telephone:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The |

Securities registered or to be registered pursuant to Section 12(g) of the Act

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to section 15(d) of the Act

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 9,560,222.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐Yes ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files)

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Emerging growth company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange

Act.

†The term “new or revised financial accounting standard” refers to any updated issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b) . ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP | ☐ | ☒ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court

☐ Yes ☐No

Table of Contents

i

ii

General Matters

Unless otherwise noted or the context indicates otherwise “we”, “us”, “our”, the “Company”, the “Corporation” or “IMV” refer to IMV Inc. and its subsidiaries.

Unless otherwise indicated, financial information in this Annual Report on Form 20-F (this “Annual Report”) has been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. Unless otherwise noted herein, all references to “$,” “US$,” “United States dollars,” or “dollars” are to the currency of the United States and “C$,” “Canadian dollars,” are to the currency of Canada.

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and as such, we have elected to comply with certain reduced U.S. public company reporting requirements.

Unless otherwise indicated, the Company has obtained the market and industry data contained in this Annual Report from its internal research, management’s estimates and third-party public information and other industry publications. While the Company believes such internal research, management’s estimates and third-party public information is reliable, such internal research and management’s estimates have not been verified by any independent sources, excluding the Company’s annual audit of the financial statements, and the Company has not verified any third-party public information. While the Company is not aware of any misstatements regarding the market and industry data contained in this Annual Report, such data involves risks and uncertainties and are subject to change based on various factors, including those described under “Cautionary Statement Regarding Forward-Looking Information and Statements” and “Item 3.D. Risk Factors”.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that are subject to risks and uncertainties. These forward-looking statements include information about possible or assumed future results of our business, financial condition, results of operations, liquidity, plans and objectives. In some cases, you can identify forward-looking statements by terminology such as “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “expect,” “predict,” “potential,” or the negative of these terms or other similar expressions. The statements we make regarding the following matters are forward-looking by their nature and are based on certain of the assumptions noted below:

| ● | the Corporation’s ability to raise sufficient capital and obtain additional funding on reasonable terms when necessary; |

| ● | positive results of preclinical assays, studies and clinical trials; |

| ● | the Corporation’s ability to successfully develop existing and new product candidates; |

| ● | the Corporation’s ability to hire and retain skilled staff; |

| ● | the products and technology offered by the Corporation’s competitors; |

| ● | general business and economic conditions, including as a result of the ongoing COVID-19 pandemic, as well as political crisis, such as terrorism, war, political instability or other conflict; |

| ● | adverse macroeconomic conditions including inflation, disruptions in global market conditions and the increase in labour costs; |

| ● | the Corporation’s ability to accurately assess and anticipate the impact of COVID-19 on the Corporation’s clinical studies and trials and operations generally; |

| ● | the Corporation’s ability to protect its intellectual property; |

| ● | the coverage and applicability of the Corporation’s intellectual property rights to any of its product candidates; |

| ● | the expectation that the Common Shares will continue to be listed on the Toronto Stock Exchange (“TSX”) and the Nasdaq Stock Market LLC (“Nasdaq”), including as it relates to the Corporation regaining compliance with the Nasdaq listing requirements, such as the Minimum Market Value of Listed Securities Requirement (“MVLS”); |

| ● | the Corporation’s ability to manufacture its product candidates, if approved, and to meet demand; |

| ● | the general regulatory environment in which the Corporation operates; |

iii

| ● | the Corporation’s ability to collaborate with governmental authorities with respect to the clinical development of its product candidates; and |

| ● | obtaining necessary regulatory approvals for its product candidates and the timing in respect thereof. |

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. The forward-looking statements are based on our beliefs, assumptions and expectations of future performance, taking into account the information currently available to us. These statements are only predictions based upon our current expectations and projections about future events. There are important factors that could cause our actual results, levels of activity, performance or achievements to differ materially from the results, levels of activity, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to, those factors identified under the Risk Factors listed below in Item 3.D. of this Annual Report. Furthermore, unless otherwise stated, the forward-looking statements contained in this Annual Report are made as of the date hereof, and we have no intention and undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, changes or otherwise, except as required by law.

RISK FACTORS SUMMARY

The following is a summary of the principal risk factors and uncertainties described in more detail in this report that make an investment in the Corporation speculative or risky:

Risks Related to the Financial Position and Need for Additional Capital

| ● | The Corporation has incurred significant losses since its inception and expects to incur losses for the foreseeable future and may never achieve or maintain profitability. Our management has concluded that these factors raise substantial doubt about our ability to continue as a going concern. |

| ● | The Corporation will need substantial additional funding. If the Corporation is unable to raise capital when needed, the Corporation would be forced to delay, reduce, terminate or eliminate product development programs, potentially including the ongoing and planned clinical trials of maveropepimut-S (“MVP-S” previously known as DPX-Survivac) or commercialization efforts. |

| ● | Raising additional capital may cause dilution to existing shareholders, restrict operations or require the Corporation to relinquish rights to its technologies or product candidates. |

Risks Related to the Development and Commercialization of the Corporation’s Product Candidates

| ● | The Corporation depends heavily on the success of MVP-S and other product candidates. All of the product candidates are still in preclinical or clinical development. Clinical trials of the product candidates may not be successful. If the Corporation is unable to commercialize the product candidates, for which it receives regulatory approval, or experiences significant delays in doing so, the business may be materially harmed. |

| ● | If clinical trials of the product candidates, such as the ongoing and planned clinical trials of MVP-S or of DPX-SurMAGE fail to demonstrate safety and efficacy to the satisfaction of the U.S. Food and Drug Administration (“FDA”), Health Canada or similar regulatory authorities outside the United States and Canada or do not otherwise produce positive results, the Corporation may incur additional costs or experience delays in completing, or ultimately be unable to complete, the development and commercialization of the product candidates. |

| ● | The design or the Corporation’s execution of clinical trials may not support regulatory approval. |

| ● | If the Corporation is unable to establish sales and marketing capabilities or enter into agreements with third parties to sell and market its product candidates, the Corporation may not be successful in commercializing its product candidates if and when they are approved. |

iv

Risks Related to the Corporation’s Dependence on Third Parties

| ● | If the Corporation is not able to establish collaborations for the development and commercialization of its product candidates, the Corporation’s commercialization program could be delayed, diminished, or terminated. |

| ● | The Corporation relies on third parties to conduct its clinical trials, and those third parties may not perform satisfactorily, including failing to meet deadlines for the completion of such trials. |

| ● | The Corporation relies on third parties to conduct its clinical trials, and those third parties may not perform satisfactorily, including failing to meet deadlines for the completion of such trials. |

Risks Related to the Manufacturing of the Corporation’s Product Candidates

| ● | The Corporation depends on third-party contract manufacturers and suppliers to obtain the Corporation’s raw ingredients and intermediate drug substances, which are necessary for the production of the Corporation’s product candidates. |

| ● | The Corporation does not have its own manufacturing facilities or personnel and expects to rely on third parties, such as Contract Development and Manufacturers (“CDMOs”), for the manufacture of future product candidates. |

| ● | The Corporation has no experience manufacturing commercial quantities of products and does not currently have the resources to commercially manufacture any products that the Corporation may develop, and for which it receives regulatory approval. |

Risks Related to the Corporation’s Intellectual Property

| ● | If the Corporation is unable to obtain and maintain patent protection for its technology and products, or if the Corporation’s licensors are unable to obtain and maintain patent protection for the technology or products that the Corporation licenses from them, or if the scope of the patent protection obtained is not sufficiently broad, the Corporation’s competitors could develop and commercialize technology and products similar or identical to that of the Corporation’s, and its ability to successfully commercialize its technology and products may be adversely affected. |

Risks Related to Regulatory Approval of the Corporation’s Product Candidates and Other Legal Compliance Matters

| ● | If the Corporation is not able to obtain, or if there are delays in obtaining, required regulatory approvals, the Corporation may not be able to commercialize, in a timely manner or at all, its product candidates, and its ability to generate revenue may be materially impaired. |

GLOSSARY

“AACR” is the American Association for Cancer Research;

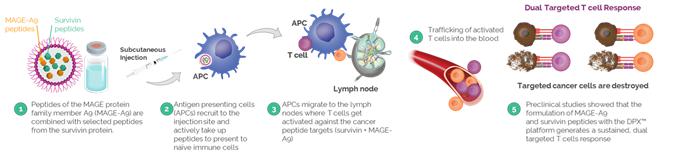

“APC” means antigen presenting cells;

“Applicable Withholding Taxes” means the aggregate amount of any federal, provincial, local or foreign taxes and other amounts required by law to be withheld;

“Armistice” means Armistice Capital, LLC;

v

“ASCT” means autologous stem cell transplant;

“ATM” means at-the-market;

“BLA” means biologics license application;

“BPCIA” means the Biologics Price Competition and Innovation Act of 2009;

“CAO” means Chief Accounting Officer;

“CBCA” means Canadian Business Corporations Act

“CDMOs” means Contract Development and Manufacturers;

“CEO” means Chief Executive Officer;

“cGMP” means Good Manufacturing Practices;

“Complete Response Letter” is a document indicating that the review cycle of an FDA application is complete and the application is not ready for approval;

“CPA” means cyclophosphamide;

“CPI” means Immune Checkpoint Inhibitor immunotherapy type;

“CR” means complete response per RECIST criteria v1.1;

“CTA” means clinical trial application;

“DPX” or “DPX Platform” means IMV Inc.’s DPX® immune-educating delivery technology;

“DSUs” means deferred share units;

“DSU Plan” refers to the Company’s deferred share unit compensation plan for its Non-Executive Directors;

“ECOG” refers to is a measure of patient functionality and is measured according to a standardized measure ranging from 0-5. Oken et al., Toxicity and response criteria of the Eastern Cooperative Oncology Group. Am J Clin Oncol. 1982 Dec;5(6):649-655. PMID: 7165009

“EMA” means the European Medicines Agency;

“Fair Market Value” In the context of the Company’s stock option plan or deferred share unit plan, means the volume weighted average per share for the five trading days immediately preceding the award date;

“FCHUQc” means La Fondation du CHU de Quebec;

“FDA” means United States Food and Drug Administration;

“FDCA” means the Federal Food, Drug, and Cosmetic Act;

“GCP” means Good Clinical Practices;

vi

“GLP” means Good Laboratory Practice;

“Horizon” means the Horizon Technology Finance Corporation;

“IRB” means independent institutional review board;

“IRAP IAP” means the National Research Council of Canada Industrial Research Assistance Program, Innovation Assistance Program;

“IRS” means the Internal Revenue Service of the Company;

“IT” means the Information Technology function of the Company;

“Master Fund” means the Armistice Capital Master Fund Ltd.;

“MOA” means mechanism of action;

“MVLS” means the Market Value of Listed Securities;

“MVP-S” means IMV Inc.’s maveropepimut-S product candidate (previously known as “DPX-Survivac”);

“Nasdaq” means the Nasdaq Stock Market LLC;

“NDA” means new drug application;

“NHL” means Non-Hodgkin Lymphoma;

“NMIBC” means non-muscle invasive bladder cancer;

“Non-Executive Director” means any director of the Corporation who is not an employee or officer of the Corporation or of its subsidiaries;

“NRC IRAP” means the National Research Council of Canada Industrial Research Assistance Program;

“ODD” means Orphan Drug Designation from the FDA;

“ORR” means Objective Response Rate;

“PFIC” means passive foreign investment company;

“PBMC” means peripheral blood mononuclear cells;

“PD-L1” means Program Death Ligand 1;

“PFS” means progression free survival;

“PHSA” means the Public Health Service Act;

“Piper Sandler” means Piper Sandler & Co.;

“PR” means partial response;

“QEF Election” means a qualified electing fund election;

vii

“r/r DLBCL” means relapsed/refractory Diffuse Large B Cell Lymphoma;

“SABCS” means the San Antonio Breast Cancer Symposium;

“SD” means stable disease;

“SITC” means the Society for Immunotherapy of Cancer;

“Termination” in the context of the Company’s deferred share unit plan means cessation of a Non-Executive Director’s directorship for any reason, including such person’s death

“TSX” means the Toronto Stock Exchange;

“UHN” means the University Health Network;

“U.S. Treasury” means the United States Treasury Department;

“VLP” means virus-like particles;

“VWAP” means volume weighted average price;

viii

Part I

| ITEM 1. | Identity of Directors, Senior Management and Advisors |

Not required.

| Item 2. | Offer Statistics and Expected TimeTable |

Not required.

| Item 3. | Key Information |

| ITEM 3.A. | Reserved |

[Reserved]

| ITEM 3.B. | Capitalization and Indebtedness |

Not required.

| ITEM 3.C. | Reasons for the Offer and Use of Proceeds |

Not required.

| ITEM 3.D. | Risk Factors |

The following is a list of risks that the Company faces in its normal course of business. The risks and uncertainties set out below are not the only ones the Company is facing. There are additional risks and uncertainties that the Company does not currently know about or that the Company currently considers immaterial which may also impair the Company’s business operations and cause the price of the Common Shares of the Company to decline. If any of the following risks actually occur, the Company’s business may be harmed and the Company’s financial condition and results of operations may suffer significantly. Investors should carefully consider the risk factors set out below and consider all other information contained herein and in the Company's other public filings before making an investment decision. The risks set out below are not an exhaustive list and should not be taken as a complete summary or description of all the risks associated with the Company's business and the biotechnology business generally.

Risks Related to the Financial Position and Need for Additional Capital

The Corporation has incurred significant losses since its inception and expects to incur losses for the foreseeable future and may never achieve or maintain profitability. Our management has concluded that these factors raise substantial doubt about our ability to continue as a going concern.

Since its inception, the Corporation has incurred significant operating losses. The net loss was $38.0 million for the year ended December 31, 2022, $36.6 million for the year ended December 31, 2021 and $23.4 million for the year ended December 31, 2020. As of December 31, 2022, the Corporation had an accumulated deficit of $192.9 million. To date, the Corporation has financed operations primarily through public offerings in Canada, private placements of securities, grants and license and collaboration agreements. The Corporation has devoted substantially all efforts to research and development, including clinical trials. IMV expects to continue to incur significant expenses and increasing operating losses for at least the next several years. The Corporation anticipates that the expenses will increase substantially if and as the Corporation:

| ● | initiates or continues the clinical trials of MVP-S and other product candidates, such as DPX-SurMAGE; |

| ● | seeks regulatory approvals for the product candidates that successfully complete clinical trials; |

1

| ● | establishes a sales, marketing and distribution infrastructure to commercialize product candidates for which the Corporation may obtain regulatory approval; |

| ● | maintains, expands and protects the Corporation’s intellectual property portfolio; |

| ● | continues other research and development efforts; |

| ● | hires additional clinical, quality control, scientific and management personnel; and |

| ● | adds operational, financial and management information systems and personnel, including personnel to support product candidate development and planned commercialization efforts. |

To become and remain profitable, the Corporation must develop and eventually commercialize a product or products with significant market potential. This development and commercialization will require the Corporation to be successful in a range of challenging activities, including successfully completing preclinical testing and clinical trials of the product candidates, obtaining regulatory approval for these product candidates and marketing and selling those products that obtain regulatory approval. The Corporation is only in the preliminary stages of some of these activities. The Corporation may never succeed in these activities and may never generate revenues that are significant or large enough to achieve profitability. Even if profitability is achieved, the Corporation may not be able to sustain or increase profitability on a quarterly or annual basis. Failure to become and remain profitable would decrease the value of the Corporation and could impair the Corporation’s ability to raise capital, expand the business, maintain research and development efforts, obtain regulatory approvals, commercialize products or continue operations. A decline in the value of the Corporation could also cause shareholders to lose all or part of their investment.

We have concluded that our historical recurring losses from operations and negative cash flows from operations as well as our dependence on equity and other financings raise substantial doubt about our ability to continue as a going concern and management has included an explanatory paragraph relating to our ability to continue as a going concern in our financial statements for the years ended December 31, 2022, and 2021. However, the consolidated financial statements of the Corporations do not include any adjustments that might result from the outcome of this uncertainty.

The Corporation will need substantial additional funding. If the Corporation is unable to raise capital when needed, the Corporation would be forced to delay, reduce, terminate or eliminate product development programs, potentially including the ongoing and planned clinical trials of MVP-S or commercialization efforts.

The Corporation expects expenses to increase in connection with the ongoing activities, particularly as the Corporation continues the research, development and clinical trials of, and seeks regulatory approval for, the product candidates. In addition, if the Corporation obtains regulatory approval of any of the product candidates, the Corporation expects to incur significant commercialization expenses for product sales, marketing, manufacturing and distribution. Furthermore, the Corporation will need to obtain additional funding in connection with continuing operations. If the Corporation is unable to raise capital when needed or on attractive terms, the Corporation would be forced to delay, reduce, terminate or eliminate the product development programs, potentially including the ongoing and planned clinical trials of MVP-S.

As of December 31, 2022, the Corporation had cash and cash equivalents of $21.2 million and working capital of $18.2 million.

The Corporation will need to obtain significant funding prior to the commercialization of any of its product candidates, if approved, including funding to complete all of the required clinical trials related to such product candidates. The Corporation does not currently have funds available to enable the Corporation to complete all of the required clinical trials for the commercialization of MVP-S, if approved, and to fund operating expenses through the completion of these trials. The Corporation expects that it will require $100 million or more to conduct the clinical trials and fund operating expenses through the completion of these ongoing trials.

The Corporation’s future capital requirements will depend on many factors, including:

| ● | the progress and results of the clinical trials of MVP-S and other product candidates; |

2

| ● | the scope, progress, results and costs of preclinical development, laboratory testing and clinical trials for other product candidates; |

| ● | the costs, timing and outcome of regulatory review of any product candidate; |

| ● | the costs of commercialization activities, including product sales, marketing, manufacturing and distribution, for any of the product candidates for which regulatory approval is received; |

| ● | revenue, if any, received from commercial sales of the Corporation’s product candidates, should any of the product candidates be approved by the FDA, Health Canada or a similar regulatory authority outside the United States and Canada; the costs of preparing, filing and prosecuting patent applications, maintaining and enforcing the Corporation’s intellectual property rights and defending intellectual property related claims; |

| ● | the extent to which the Corporation acquires or invests in other businesses, products and technologies; |

| ● | the emergence of competing therapies to the Corporation’s products for which is receives regulatory approval; |

| ● | the Corporation’s ability to obtain government or other third-party funding; and |

| ● | the Corporation’s ability to establish collaborations on favorable terms, if at all, particularly arrangements to market and distribute product candidates on a worldwide basis. |

Conducting preclinical testing and clinical trials is a time consuming, expensive and uncertain process that takes years to complete, and the Corporation may never generate the necessary data or results required to obtain regulatory approval and achieve product sales. In addition, the Corporation’s product candidates, if approved, may not achieve commercial success. The Corporation’s commercial revenues, if any, will be derived from sales of products that the Corporation does not expect to be commercially available for several years, if at all. Accordingly, the Corporation will need to continue to rely on additional funding to achieve the Corporation’s business objectives. Additional funding may not be available on acceptable terms to the Corporation, or at all.

Raising additional capital may cause dilution to existing shareholders, restrict operations or require the Corporation to relinquish rights to its technologies or product candidates.

Until such time, if ever, as the Corporation can generate substantial product revenues, the Corporation expects to finance its cash needs through a combination of equity offerings, debt financings, government or other third-party funding, marketing and distribution arrangements and other collaborations, strategic alliances and licensing arrangements. Currently, the Corporation does not have any committed external source of funds. The Corporation will require substantial funding to complete the ongoing and planned clinical trials of MVP-S and other product candidates and to fund operating expenses and other activities. To the extent that the Corporation raises additional capital through the sale of equity or convertible debt securities, the shareholders ownership interest will be diluted, and the terms of these securities may include liquidation or other preferences that adversely affect the shareholders. Debt financing involves agreements that include covenants limiting or restricting the Corporation’s ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends. If the Corporation raises additional funds through government or other third-party funding, marketing and distribution arrangements or other collaborations, strategic alliances or licensing arrangements with third parties, the Corporation may have to relinquish valuable rights to its technologies, future revenue streams, research programs or product candidates or to grant licenses on terms that may not be favorable.

Risks Related to the Development and Commercialization of the Corporation’s Product Candidates

The Corporation depends heavily on the success of MVP-S and other product candidates. All of the product candidates are still in preclinical or clinical development. Clinical trials of the product candidates may not be successful. If the Corporation is unable to commercialize the product candidates, for which it receives regulatory approval, or experiences significant delays in doing so, the business may be materially harmed.

3

All of the product candidates of the Corporation are still in preclinical or clinical development. The Corporation may never be able to obtain regulatory approval for any of its product candidates. The Corporation has committed significant human and financial resources to the development of MVP-S, and the DPX Platform. The ability to generate product revenues, which is not expected to occur for at least the next several years, if ever, will depend heavily on the successful development and eventual commercialization of these product candidates, especially MVP-S, the most advanced product candidate. The success of these product candidates will depend on several factors, including the following:

| ● | successful completion of preclinical studies and clinical trials; |

| ● | receipt of marketing approvals from the FDA, Health Canada and similar regulatory authorities outside the United States and Canada; |

| ● | establishing commercial manufacturing capabilities by identifying and securing arrangements with third party manufacturers for the product candidates; |

| ● | maintaining patent and trade secret protection and regulatory exclusivity for the product candidates; |

| ● | launching commercial sales of the product candidates, if and when approved, whether alone or in collaboration with others; |

| ● | acceptance of the products, if and when approved, by patients, the medical community and third party payors; |

| ● | effectively competing with other therapies; and |

| ● | a continued acceptable safety profile of the products following approval. |

If the Corporation does not achieve one or more of these factors in a timely manner or at all, the Corporation could experience significant delays or an inability to successfully commercialize its product candidates, if approved, which would materially harm its business.

If clinical trials of the product candidates, such as the ongoing and planned clinical trials of MVP-S or of DPX-SurMAGE fail to demonstrate safety and efficacy to the satisfaction of the FDA, Health Canada or similar regulatory authorities outside the United States and Canada or do not otherwise produce positive results, the Corporation may incur additional costs or experience delays in completing, or ultimately be unable to complete, the development and commercialization of the product candidates.

Before obtaining regulatory approval for the sale of any product candidate, the Corporation must conduct extensive clinical trials to demonstrate the safety, purity and potency, or efficacy, of the product candidates in humans. Clinical testing is expensive, difficult to design and implement, can take many years to complete and is uncertain as to outcome. A failure of one or more of the Corporation’s clinical trials can occur at any stage of testing. The outcome of preclinical testing and early clinical trials may not be predictive of the success of later clinical trials, and interim results of a clinical trial do not necessarily predict final results. Moreover, preclinical and clinical data are often susceptible to varying interpretations and analyses, and many companies that have believed their product candidates performed satisfactorily in preclinical studies and clinical trials have nonetheless failed to obtain marketing approval of their products.

The Corporation may experience numerous unforeseen events during, or as a result of, clinical trials that could delay or prevent the Corporation’s ability to receive regulatory approval or commercialize its product candidates, if approved. Unforeseen events that could delay or prevent the Corporation’s ability to receive regulatory approval or commercialize its product candidates include:

| ● | regulators or institutional review boards may not authorize the Corporation or its investigators to commence a clinical trial or conduct a clinical trial at a prospective trial site; |

| ● | the Corporation may have delays in reaching or fail to reach agreement on acceptable clinical trial contracts or clinical trial protocols with prospective trial sites; |

| ● | clinical trials of the product candidates may produce negative or inconclusive results, and the Corporation may decide, or regulators may require, additional clinical trials be conducted or product development programs be abandoned; |

4

| ● | the number of patients required for clinical trials of the product candidates may be larger than anticipated, enrollment in these clinical trials may be slower than anticipated or participants may drop out of these clinical trials at a higher rate than anticipated; |

| ● | the Corporation’s third party contractors may fail to comply with regulatory requirements or meet their contractual obligations in a timely manner, or at all; |

| ● | the Corporation might have to suspend or terminate clinical trials of its product candidates for various reasons, including a finding that the participants are being exposed to unacceptable health risks; |

| ● | regulators or institutional review boards may require that the Corporation or its investigators suspend or terminate clinical research for various reasons, including noncompliance with regulatory requirements or a finding that the participants are being exposed to unacceptable health risks; |

| ● | the cost of clinical trials of the product candidates may be greater than anticipated; |

| ● | the supply or quality of the product candidates or other materials necessary to conduct clinical trials of the product candidates may be insufficient or inadequate; and |

| ● | the Corporation’s product candidates may have undesirable side effects or other unexpected characteristics, causing the Corporation or its investigators, regulators or institutional review boards to suspend or terminate the trials. |

In addition, the patients recruited for clinical trials of the product candidates may have a disease profile or other characteristics that are different than expected and different than what the clinical trials were designed for, which could adversely impact the results of the clinical trials.

If the Corporation is required to conduct additional clinical trials or other testing of its product candidates beyond those that are currently contemplated, if the Corporation is unable to successfully complete clinical trials of its product candidates or other testing, if the results of these trials or tests are not positive or are only modestly positive or if there are safety concerns, the Corporation may:

| ● | be delayed in obtaining marketing approval for its product candidates; |

| ● | not obtain marketing approval at all; |

| ● | obtain approval for indications or patient populations that are not as broad as intended or desired; |

| ● | obtain approval with labeling that includes significant use restrictions or safety warnings, including boxed warnings; |

| ● | have the product removed from the market after obtaining marketing approval; |

| ● | be subject to additional post marketing testing requirements; or |

| ● | be subject to restrictions on how the product is distributed or used. |

The Corporation’s product development costs will also increase if delays in testing or approvals are experienced. The Corporation does not know whether any clinical trials will begin as planned, will need to be restructured or will be completed on schedule, or at all. Significant clinical trial delays could also shorten any periods during which the Corporation may have the exclusive right to commercialize its product candidates, if approved, or allow the Corporation’s competitors to bring products to market before the Corporation does and impair the Corporation’s ability to commercialize its product candidates, if approved, and may harm the business and results of operations.

Interim, “topline” and preliminary data from our clinical trials that we announce or publish from time to time may change as more patient data become available and are subject to audit and verification procedures that could result in material changes in the final data.

From time to time, we may publish interim, “topline” or preliminary data from our clinical trials. Interim, “topline” or preliminary data from clinical trials that we may complete are subject to the risk that one or more of the clinical outcomes may materially change as patient enrollment continues and more patient data become available. Interim, “topline” and preliminary data also remain subject to audit and verification procedures that may result in the final data being materially different from the preliminary data we previously published. As a

5

result, interim, “topline,” and preliminary data should be viewed with caution until the final data are available. Differences between interim, “topline” and preliminary data and final data could significantly harm our business prospects and may cause the trading price of our common stock to fluctuate significantly.

Further, others, including regulatory agencies, may not accept or agree with our assumptions, estimates, calculations, conclusions or analyses or may interpret or weigh the importance of data differently, which could impact the value of the particular program, the approvability or commercialization of the particular product candidate or product and our business in general. In addition, the information we choose to publicly disclose regarding a particular study or clinical trial is based on what is typically extensive information, and you or others may not agree with what we determine is the material or otherwise appropriate information to include in our disclosure, and any information we determine not to disclose may ultimately be deemed significant with respect to future decisions, conclusions, views, activities or otherwise regarding a particular product candidate or our business. If the interim, “topline,” or preliminary data that we report differ from actual results, or if others, including regulatory authorities, disagree with the conclusions reached, our ability to obtain approval for and commercialize our product candidates, our business, operating results, prospects or financial condition may be harmed.

We are developing MVP-S for multiple indications in combination with Keytruda®, which exposes us to additional risks.

We currently have multiple ongoing clinical studies evaluating MVP-S with Merck’s checkpoint inhibitor, pembrolizumab (KEYTRUDA®). Even if the MVP-S and Keytruda® combination were to receive marketing approval or be commercialized, we would continue to be subject to the risks that the FDA, European Medicines Agency (“EMA”) or other comparable foreign regulatory authorities could revoke approval of Keytruda®, or safety, efficacy, manufacturing or supply issues could arise with Keytruda®. If the FDA, EMA or other comparable foreign regulatory authorities revoke their approval of Keytruda®, or if safety, efficacy, commercial adoption, manufacturing or supply issues arise with Keytruda®, we may be unable to obtain approval of or successfully market MVP-S.

Additionally, if the third-party provider of Keytruda® is unable to produce sufficient quantities for clinical trials, if the cost becomes prohibitive, or if our third-party provider is unable to meet applicable regulatory requirements, our development efforts would be impaired, which would have an adverse effect on our business, financial condition, results of operations and growth prospects.

If the Corporation experiences delays or difficulties in the enrollment of patients in clinical trials, receipt of necessary regulatory approvals could be delayed or prevented.

The Corporation may not be able to initiate or continue clinical trials for its product candidates, if the Corporation is unable to locate and enroll a sufficient number of eligible patients to participate in these trials as required by the FDA, Health Canada or similar regulatory authorities outside the United States and Canada. In addition, many of the Corporation’s competitors have ongoing clinical trials for product candidates that could be competitive with the Corporation’s product candidates, and patients who would otherwise be eligible for the Corporation’s clinical trials may instead enroll in clinical trials of the Corporation’s competitors’ product candidates.

Patient enrollment is affected by other factors including:

| ● | severity of the disease under investigation; |

| ● | eligibility criteria for the study in question; |

| ● | perceived risks and benefits of the product candidate under study; |

| ● | efforts to facilitate timely enrollment in clinical trials; |

| ● | patient referral practices of physicians; |

| ● | the ongoing COVID-19 pandemic and the efforts to mitigate it; |

| ● | the ability to monitor patients adequately during and after treatment; and |

| ● | proximity and availability of clinical trial sites for prospective patients. |

6

The actual amount of time for full enrollment could be longer than planned. Enrollment delays in these ongoing and planned trials or any of the Corporation’s other clinical trials may result in increased development costs for its product candidates, which would cause the value of the Corporation to decline and limit the Corporation’s ability to obtain additional financing, including financing needed to complete the ongoing and planned trials of MVP-S. The Corporation’s inability to enroll a sufficient number of patients for these clinical trials or any of the other clinical trials would result in significant delays or may require the Corporation to abandon one or more clinical trials altogether.

Risks Related to the Development and Commercialization of the Corporation’s Product Candidates

If serious adverse or undesirable side effects are identified during the development of any product candidate, the Corporation may need to abandon or limit the development of some of its product candidates.

All of the Corporation’s product candidates are still in preclinical or clinical development and their risk of failure is high. It is impossible to predict when or if any of the Corporation’s product candidates will receive regulatory approval. If the Corporation’s product candidates are associated with undesirable side effects or have characteristics that are unexpected, the Corporation may need to abandon their development or limit development to certain uses or subpopulations in which the undesirable side effects or other characteristics are less prevalent, less severe or more acceptable from a risk benefit perspective.

If the Corporation does not achieve projected development goals in the time frames the Corporation announced and expected, the commercialization of future product candidates, if approved, may be delayed and, as a result, its share price may decline.

From time to time, the Corporation estimates the timing of the anticipated accomplishment of various scientific, clinical, regulatory and other product development goals, which are sometimes refer to as milestones. These milestones may include the commencement or completion of preclinical studies and clinical trials and the submission of regulatory filings. From time to time, the Corporation may publicly announce the expected timing of some of these milestones. All of these milestones are and will be based on numerous assumptions. The actual timing of these milestones can vary dramatically compared to its estimates, in some cases for reasons beyond its control. If the Corporation does not meet these milestones as publicly announced, or at all, revenue may be lower than expected, the development and commercialization, if approved, of future product candidates may be delayed or never achieved and, as a result, the Corporation share price may significantly decline.

The design or the Corporation’s execution of clinical trials may not support regulatory approval.

The design or execution of a clinical trial can determine whether its results will support regulatory approval and flaws in the design or execution of a clinical trial may not become apparent until the clinical trial is well advanced. In some instances, there can be significant variability in safety or efficacy results between different trials of the same product candidate due to numerous factors, including changes in trial protocols, differences in size and type of the patient populations, adherence to the dosing regimen and other trial protocols and the rate of dropout among clinical trial participants. The Corporation does not know whether any Phase 2, Phase 3 or other clinical trials the Corporation may conduct will demonstrate consistent or adequate efficacy and safety outcomes to obtain regulatory approval to market the Corporation’s product candidates.

Further, the FDA, Health Canada and comparable foreign regulatory authorities have substantial discretion in the approval process and in determining when or whether regulatory approval will be obtained for any of the Corporation’s product candidates. The Corporation’s product candidates may not be approved even if they achieve their primary endpoints in future Phase 3 clinical trials or registration trials. The FDA, Health Canada or other regulatory authorities may disagree with the Corporation’s trial design and the Corporation’s interpretation of data from preclinical studies and clinical trials. In addition, any of these regulatory authorities may change requirements for the approval of a product candidate even after reviewing and providing comments or advice on a protocol for a pivotal Phase 3 clinical trial that has the potential to result in FDA, Health Canada or other agencies’ approval. In addition, any of these regulatory authorities may also approve a product candidate for fewer or more limited indications than the Corporation requests or may grant approval contingent on the performance of costly post-marketing clinical trials. The FDA, Health Canada or other regulatory authorities may not approve the labeling claims that the Corporation believes would be necessary or desirable for the successful commercialization of its product candidates.

7

Even if any of the Corporation’s product candidates, including MVP-S, receive regulatory approval, they may fail to achieve the degree of market acceptance by physicians, patients, healthcare payors and others in the medical community necessary for commercial success.

If MVP-S or any other product candidates receive marketing approval, they may nonetheless fail to gain sufficient market acceptance by physicians, patients, healthcare payors and others in the medical community. Gaining market acceptance for the DPX' based products may be particularly difficult as, to date, the FDA has only approved a limited number of cancer immunotherapies and the DPX' based products are based on a novel technology. If these products do not achieve an adequate level of acceptance, the Corporation may not generate significant product revenues and may not become profitable. The degree of market acceptance of the Corporation’s product candidates, if approved for commercial sale, will depend on a number of factors, including:

| ● | efficacy and potential advantages compared to alternative treatments; |

| ● | the ability to offer its product candidates for sale at competitive prices; |

| ● | convenience and ease of administration compared to alternative treatments; |

| ● | the willingness of the target patient population to try new therapies and of physicians to prescribe these therapies; |

| ● | the strength of marketing and distribution support; |

| ● | sufficient third party coverage or reimbursement; and |

| ● | the prevalence and severity of any side effects. |

If the Corporation is unable to establish sales and marketing capabilities or enter into agreements with third parties to sell and market its product candidates, the Corporation may not be successful in commercializing its product candidates if and when they are approved.

The Corporation does not have a sales or marketing infrastructure and has no experience in the sale, marketing or distribution of pharmaceutical products. To achieve commercial success for any of its product that would be approved in the future, the Corporation must either develop a sales and marketing organization or outsource these functions to third parties. The Corporation currently intends to establish commercialization arrangements with third parties.

There are risks involved with entering into arrangements with third parties to perform these services. If the Corporation enters into arrangements with third parties to perform sales, marketing and distribution services, its product revenues or the profitability of these product revenues are likely to be lower than if the Corporation were to market and sell any products that it develops. In addition, the Corporation may not be successful in entering into arrangements with third parties to sell and market its product candidates or doing so on terms that are favorable to the Corporation. The Corporation likely will have little control over such third parties, and any of them may fail to devote the necessary resources and attention to sell and market its products effectively. If the Corporation does not establish sales and marketing capabilities successfully, either on its own or in collaboration with third parties, it will not be successful in commercializing its product candidates.

The Corporation faces substantial competition, which may result in others discovering, developing or commercializing products before or more successfully than it may.

The development and commercialization of new drug products is highly competitive. The Corporation faces competition with respect to its current or contemplated product candidates, and will face competition with respect to any products that it may seek to develop or commercialize in the future, from major pharmaceutical companies, specialty pharmaceutical companies and biotechnology companies worldwide. There are a number of large pharmaceutical and biotechnology companies that currently market and sell products or are pursuing the development of products for the treatment of the disease indications for which the Corporation is developing its current or contemplated product candidates. Potential competitors also include academic institutions, government agencies and other public and private research organizations that conduct research, seek patent protection and establish collaborative arrangements for research, development, manufacturing and commercialization.

8

Some of these competitive products and therapies are based on scientific approaches that are the same as or similar to the Corporation’s approaches, and others are based on entirely different approaches. Many marketed therapies for the indications that the Corporation is currently pursuing, or indications that it may in the future seek to address using the DPX platform, are widely accepted by physicians, patients and payors, which may make it difficult for the Corporation to replace with any products that the Corporation successfully develops and are permitted to market.

There are many FDA approved cancer therapies that may provide equivalent or better efficacy compared to the therapeutic potential of MVP-S.

In addition, the Corporation estimates that there are numerous cancer immunotherapy products in clinical development by many public and private biotechnology and pharmaceutical companies targeting numerous different cancer types. A number of these are in late-stage development.

The Corporation’s competitors may develop products that are more effective, safer, more convenient or less costly than any that the Corporation is developing or that would render its product candidates obsolete or non-competitive. The Corporation’s competitors may also obtain FDA, Health Canada or other regulatory approval for their products more rapidly than the Corporation.

Many of the Corporation’s competitors have significantly greater financial resources and expertise in research and development, manufacturing, preclinical testing, conducting clinical trials, obtaining regulatory approvals and marketing approved products than the Corporation. Mergers and acquisitions in the pharmaceutical, biotechnology and device industries may result in even more resources being concentrated among a smaller number of the Corporation’s competitors. Smaller and other early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large and established companies. These third parties compete with the Corporation in recruiting and retaining qualified scientific and management personnel, establishing clinical trial sites and patient registration for clinical trials, as well as in acquiring technologies complementary to, or necessary for, the Corporation’s programs.

Even if the Corporation is able to commercialize any product candidates, if approved, the products may become subject to unfavorable pricing regulations, third-party reimbursement practices or healthcare reform initiatives, which would harm the business.

The regulations that govern marketing approvals, pricing and reimbursement for new drug products vary widely from country to country. In the United States, healthcare reform legislation may significantly change the approval requirements in ways that could involve additional costs and cause delays in obtaining approvals. Some countries require approval of the sale price of a drug before it can be marketed. In many countries, the pricing review period begins after marketing or product licensing approval is granted. In some foreign markets, prescription pharmaceutical pricing remains subject to continuing governmental control even after initial approval is granted. As a result, the Corporation might obtain regulatory approval for a product in a particular country, but then be subject to price regulations that delay the commercial launch of the product, possibly for lengthy time periods, and negatively impact the revenues the Corporation is able to generate from the sale of the product in that country. Adverse pricing limitations may hinder the Corporation’s ability to recoup its investment in one or more product candidates, even if its product candidates obtain regulatory approval.

The Corporation’s ability to commercialize any products successfully also will depend in part on the extent to which reimbursement for these products and related treatments will be available from government health administration authorities, private health insurers and other organizations. Government authorities and third-party payors, such as private health insurers and health maintenance organizations, decide which medications they will pay for and establish reimbursement levels. A primary trend in the United States healthcare industry and elsewhere is cost containment. Government authorities and third-party payors have attempted to control costs by limiting coverage and the amount of reimbursement for particular medications. Increasingly, third party payors are requiring that drug companies provide them with predetermined discounts from list prices and are challenging the prices charged for medical products. The Corporation cannot be sure that reimbursement will be available for any product that it commercializes and, if reimbursement is available, the level of reimbursement. Reimbursement may impact the demand for, or the price of, any product candidate for which the Corporation obtains marketing approval. Obtaining reimbursement for the Corporation’s product candidates, if approved, may be particularly difficult because of the higher prices often associated with drugs or biologics administered under the supervision of a physician. If reimbursement is not available

9

or is available only to limited levels, the Corporation may not be able to successfully commercialize any product candidate for which the Corporation obtained marketing approval.

There may be significant delays in obtaining reimbursement for newly approved drugs and biologics, and coverage may be more limited than the purposes for which the drug or biologic is approved by the FDA, Health Canada or similar regulatory authorities outside the United States or Canada. Moreover, eligibility for reimbursement does not imply that any drug or biologic will be paid for in all cases or at a rate that covers the Corporation’s costs, including research, development, manufacture, sale and distribution. Interim reimbursement levels for new drugs or biologics, if applicable, may also not be sufficient to cover the Corporation’s costs and may not be made permanent. Reimbursement rates may vary according to the use of the drug or biologic and the clinical setting in which it is used, may be based on reimbursement levels already set for lower cost drugs or biologics, and may be incorporated into existing payments for other services. Net prices for drugs or biologics may be reduced by mandatory discounts or rebates required by government healthcare programs or private payors and by any future relaxation of laws that presently restrict imports of drugs or biologics from countries where they may be sold at lower prices than in Canada or the United States. Third party payors often rely upon Medicare coverage policy and payment limitations in setting their own reimbursement policies. The Corporation’s inability to promptly obtain coverage and profitable payment rates from both government funded and private payors for any approved products that the Corporation develops could have a material adverse effect on the Corporation’s operating results, the Corporation’s ability to raise capital needed to commercialize products and the Corporation’s overall financial condition.

The Corporation’s reliance on government funding adds uncertainty to the Corporation’s research and commercialization efforts of its government-funded product candidates.

The Corporation has received significant funding from government organizations since its inception totaling over US$17 million. There is no assurance the Corporation will continue to apply for and/or be awarded government funding in the future. If the Corporation is unable to obtain additional government funding, it will have to either obtain funds through raising additional capital or arrangements with strategic partners or others, if available, that may require the Corporation to relinquish material rights to certain technologies or potential markets. There is no certainty that financing from governments will be available in amounts the Corporation requires, in addition to other funding sources, to pursue the planned activities or on acceptable terms, if at all.

Product liability lawsuits against the Corporation could cause the Corporation to incur substantial liabilities and to limit commercialization of any products that the Corporation may develop.

The Corporation faces an inherent risk of product liability exposure related to the testing of its product candidates in human clinical trials and will face an even greater risk if the Corporation commercially sells any products that it maydevelop and for which it receives regulatory approval. None of the Corporation’s product candidates have been widely used over an extended period of time, and therefore, safety data is limited. If the Corporation cannot successfully defend itself against claims that its product candidates or products for which it receives regulatory approval caused injuries, it will incur substantial liabilities. Regardless of merit or eventual outcome, liability claims may result in:

| ● | decreased demand for any product candidates or products that it may develop and for which it receives regulatory approval; |

| ● | injury to the Corporation’s reputation and significant negative media attention; |

| ● | withdrawal of clinical trial participants; |

| ● | significant costs to defend the related litigation; |

| ● | substantial monetary awards to trial participants or patients; |

| ● | loss of revenue; and |

| ● | the inability to commercialize any products that the Corporation may develop and for which it receives regulatory approval. |

The Corporation currently maintains a clinical trial liability insurance coverage in the amount of $10 million, which may not be adequate to cover all liabilities that it may incur. The Corporation will need to increase its insurance

10

coverage when it begins commercializing its product candidates, if approved. Insurance coverage is increasingly expensive. The Corporation may not be able to maintain insurance coverage at a reasonable cost or in an amount adequate to satisfy any liability that may arise.

The Corporation may expend its limited resources to pursue a particular product candidate or indication and fail to capitalize on product candidates or indications that may be more profitable or for which there is a greater likelihood of success.

Because the Corporation has limited financial and managerial resources, the Corporation focuses on research programs and product candidates for specific indications. As a result, the Corporation may forego or delay pursuit of opportunities with other product candidates or for other indications that later prove to have greater commercial potential. The Corporation’s resource allocation decisions may cause the Corporation to fail to capitalize on viable commercial products or profitable market opportunities. The Corporation’s spending on current and future research and development programs and product candidates for specific indications may not yield any commercially viable products.

The Corporation has based its research and development efforts on its DPX platform. Notwithstanding the large investment to date and anticipated future expenditures in its DPX platform, the Corporation has not yet developed, and may never successfully develop, any marketed drugs using this approach. As a result of pursuing the development of product candidates using the DPX platform, the Corporation may fail to develop product candidates or address indications based on other scientific approaches that may offer greater commercial potential or for which there is a greater likelihood of success.

The Corporation’s long term business plan is to develop DPXTM based products for the treatment of various cancers and infectious diseases. The Corporation may not be successful in its efforts to identify or discover additional product candidates that may be manufactured using its DPX platform. Research programs to identify new product candidates require substantial technical, financial and human resources. These research programs may initially show promise in identifying potential product candidates, yet fail to yield product candidates for clinical development.

If the Corporation does not accurately evaluate the commercial potential or target market for a particular product candidate, the Corporation may relinquish valuable rights to that product candidate through collaboration, licensing or other royalty arrangements in cases in which it would have been more advantageous for the Corporation to retain sole development and commercialization rights to such product candidate.

Risks Related to the Corporation’s Dependence on Third Parties

If the Corporation is not able to establish collaborations, the Corporation may have to alter its development and commercialization plans.

The Corporation’s drug development programs and the potential commercialization of its product candidates will require substantial additional cash to fund expenses. For some of the Corporation’s product candidates, the Corporation plans to collaborate with pharmaceutical and biotechnology companies for the development and potential commercialization of those product candidates.

The Corporation faces significant competition in seeking appropriate collaborators. Whether the Corporation reaches a definitive agreement for a collaboration will depend, among other things, upon its assessment of the collaborator’s resources and expertise, the terms and conditions of the proposed collaboration, and the proposed collaborator’s evaluation of a number of factors. Those factors may include the design or results of clinical trials, the likelihood of approval by the FDA, Health Canada or similar regulatory authorities outside the United States and Canada, the potential market for the subject product candidate, the costs and complexities of manufacturing and delivering such product candidate to patients, the potential of competing products, the existence of uncertainty with respect to the Corporation’s ownership of technology, which can exist if there is a challenge to such ownership without regard to the merits of the challenge and industry and market conditions generally. The collaborator may also consider alternative product candidates or technologies for similar indications that may be available to collaborate on and whether such a collaboration could be more attractive than the one with the Corporation for its product candidate. The Corporation may also be restricted under existing license agreements from entering into agreements on certain terms with potential collaborators. Collaborations are complex and time consuming to negotiate and document. The Corporation may not be able to negotiate collaborations on a timely basis, on acceptable terms, or at all.

11

The Corporation will need to raise capital or develop collaborations with third parties to commercialize its products. If the Corporation is not able to obtain such funding or enter into collaborations for any such product candidate, the Corporation may have to curtail the development of such product candidate, reduce or delay its development program or one or more of its other development programs, delay its potential commercialization or reduce the scope of any sales or marketing activities, or increase its expenditures and undertake development or commercialization activities at the Corporation’s own expense. If the Corporation elects to increase its expenditures to fund development or commercialization activities on its own, the Corporation may need to obtain additional capital, which may not be available to the Corporation on acceptable terms or at all. If the Corporation does not have sufficient funds, the Corporation may not be able to further develop these product candidates or bring these product candidates to market and generate product revenue.

The Corporation expects to depend on collaborations with third parties for the development and commercialization of its product candidates. If those collaborations are not successful, the Corporation may not be able to capitalize on the market potential of these product candidates.

The Corporation intends to establish commercialization arrangements with third parties. The Corporation’s likely collaborators for any development, distribution, marketing, licensing or broader collaboration arrangements include large and mid-size pharmaceutical companies, regional and national pharmaceutical companies and biotechnology companies.

Potential delays include delays in manufacture or clinical trials, failure to produce sufficient quantities of product to conduct trials, or failure to complete trials. The Corporation’s collaborators may fail to meet contractual obligations. They could also pursue other technologies or develop alternative products that could compete with the products the Corporation is developing. If the Corporation does enter into any such arrangements with any third parties, the Corporation will likely have limited control over the amount and timing of resources that its collaborators dedicate to the development or commercialization of its product candidates. The Corporation’s ability to generate revenues from these arrangements will depend on its collaborators’ abilities to successfully perform the functions assigned to them in these arrangements.

Collaborations involving the Corporation’s product candidates would pose the following risks to the Corporation:

| ● | collaborators have significant discretion in determining the efforts and resources that they will apply to these collaborations; |

| ● | collaborators may not pursue development and commercialization of the Corporation’s product candidates or may elect not to continue or renew development or commercialization programs based on clinical trial results, changes in the collaborator’s strategic focus or available funding, or external factors such as an acquisition that diverts resources or creates competing priorities; |

| ● | collaborators may delay clinical trials, provide insufficient funding for a clinical trial program, stop a clinical trial or abandon a product candidate, repeat or conduct new clinical trials or require a new formulation of a product candidate for clinical testing; |

| ● | collaborators could independently develop, or develop with third parties, products that compete directly or indirectly with the Corporation’s products or product candidates if the collaborators believe that competitive products are more likely to be successfully developed or can be commercialized under terms that are more economically attractive than the Corporation’s; |

| ● | a collaborator with marketing and distribution rights to one or more products may not commit sufficient resources to the marketing and distribution of such product or products; |

| ● | collaborators may not properly maintain or defend the Corporation’s intellectual property rights or may use the Corporation’s proprietary information in such a way as to invite litigation that could jeopardize or invalidate the Corporation’s proprietary information or expose the Corporation to potential litigation; |

12

| ● | disputes may arise between the collaborators and the Corporation that result in the delay or termination of the research, development or commercialization of the Corporation’s products or product candidates or that result in costly litigation or arbitration that diverts management attention and resources; and |

| ● | collaborations may be terminated and, if terminated, may result in a need for additional capital to pursue further development or commercialization of the applicable product candidates. For example, the Corporation could have to build a sales force. |

Collaboration agreements may not lead to development or commercialization of product candidates in the most efficient manner, or at all. In addition, there have been a significant number of recent business combinations among large pharmaceutical companies that have resulted in a reduced number of potential future collaborators. If a present or future collaborator of the Corporation were to be involved in a business combination, the continued pursuit and emphasis on the Corporation’s product development or commercialization program could be delayed, diminished or terminated.

The Corporation relies on third parties to conduct its clinical trials, and those third parties may not perform satisfactorily, including failing to meet deadlines for the completion of such trials.

The Corporation does not independently conduct clinical trials of its product candidates. The Corporation relies on third parties, such as contract research organizations, clinical data management organizations, medical institutions and clinical investigators, to perform this function. The Corporation’s reliance on these third parties for clinical development activities reduces its control over these activities but does not relieve the Corporation of its responsibilities. The Corporation remains responsible for ensuring that each of its clinical trials is conducted in accordance with the general investigational plan and protocols for the trial. Moreover, the FDA requires the Corporation to comply with standards, commonly referred to as Good Clinical Practices, for conducting, recording and reporting the results of clinical trials to assure that data and reported results are credible and accurate and that the rights, integrity and confidentiality of trial participants are protected. The Corporation is also required to register ongoing clinical trials and post the results of completed clinical trials on a government sponsored database, ClinicalTrials.gov, within certain timeframes. Failure to do so can result in fines, adverse publicity and civil and criminal sanctions. Furthermore, these third parties may also have relationships with other entities, some of which may be the Corporation’s competitors. If these third parties do not successfully carry out their contractual duties, meet expected deadlines or conduct the Corporation’s clinical trials in accordance with regulatory requirements or the Corporation’s stated protocols, the Corporation will not be able to obtain, or may be delayed in obtaining, regulatory approvals for its product candidates and will not be able to, or may be delayed in its efforts to, successfully commercialize its product candidates.

The Corporation also relies on other third parties to store and distribute drug supplies for its clinical trials. Any performance failure on the part of the Corporation’s existing or future distributors could delay clinical development or regulatory approval of its product candidates or commercialization of its products, if approved, producing additional losses and depriving the Corporation of potential product revenue.

Risks Related to the Manufacturing of the Corporation’s Product Candidates

The Corporation depends on third-party contract manufacturers and suppliers to obtain the Corporation’s raw ingredients and intermediate drug substances, which are necessary for the production of the Corporation’s product candidates.