UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

ANNUAL REPORT PURSUANT TO SECTIONS 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FORM 10-K

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended March 31, 2012

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to

Commission File Number: 814-61

CAPITAL SOUTHWEST CORPORATION

(Exact name of registrant as specified in its charter)

|

Texas

|

75-1072796

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

|

12900 Preston Road, Suite 700, Dallas, Texas

|

75230

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant's telephone number, including area code: (972) 233-8242

Securities registered pursuant to section 12(b) of the Act: None

Securities registered pursuant to section 12(g) of the Act: Common Stock, $1.00 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO x.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES o NO x.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO o.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check One):

Large accelerated filer o Accelerated filer x Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

YES o NO x.

The aggregate market value of the voting stock held by non-affiliates of the registrant as of September 30, 2011 was $193,363,554, based on the last sale price of such stock as quoted by The Nasdaq Stock Market on such date.

The number of shares of common stock outstanding as of May 1, 2012 was 3,754,538.

Documents Incorporated by Reference

Proxy Statement for Annual Meeting of Shareholders to be held July 18, 2012 is incorporated by reference in this Annual Report on Form 10-K in response to Part III.

TABLE OF CONTENTS

|

PART I

|

Page

|

|

|

Item 1.

|

1

|

|

|

Item 1A.

|

11

|

|

|

Item 1B.

|

19

|

|

|

Item 2.

|

19

|

|

|

Item 3.

|

19

|

|

|

Item 4.

|

19

|

|

|

PART II

|

||

|

Item 5.

|

19

|

|

|

Item 6.

|

21

|

|

|

Item 7.

|

22

|

|

|

Item 7A.

|

28

|

|

|

Item 8.

|

29

|

|

|

Item 9.

|

71

|

|

|

Item 9A.

|

71

|

|

|

Item 9B.

|

72

|

|

|

PART III

|

||

|

Item 10.

|

72

|

|

|

Item 11.

|

72

|

|

|

Item 12.

|

72

|

|

|

Item 13.

|

73

|

|

|

Item 14.

|

73

|

|

|

PART IV

|

||

|

Item 15.

|

74

|

|

|

76

|

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements regarding the plans and objectives of management for future operations. Any such forward-looking statements may involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by any forward looking statements. Forward-looking statements which involve assumptions and describe our future plans, strategies and expectations are generally identifiable by use of the words “may,” “will,” “should,” “expect,” “anticipate,” “estimate,” “believe,” “intend” or “project” or the negative of these words or other variations on these words or comparable terminology. These forward-looking statements are based on assumptions that may be incorrect, and we cannot assure you that the projections included in these forward-looking statements will come to pass. Our actual results could differ materially from those expressed or implied by the forward-looking statements as a result of various factors, including the factors discussed in Item 1A entitled “Risk Factors” in Part I of this Annual Report on Form 10-K and elsewhere in this Annual Report on Form 10-K. Other factors that could cause actual results to differ materially include changes in the economy and future changes in laws or regulations and conditions in our operating areas.

We have based the forward-looking statements included in this Annual Report on Form 10-K on information available to us on the date of this Annual Report on Form 10-K, and we assume no obligation to update any such forward-looking statements, unless we are required to do so by applicable law. However, you are advised to consult any additional disclosures that we may make directly to you or through reports that we in the future may file with the SEC, including subsequent annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K.

PART I

Item 1. Business

Overview

Capital Southwest Corporation ("CSC") was organized as a Texas corporation on April 19, 1961. Until September 1969, we operated as a licensee under the Small Business Investment Act of 1958. At that time, CSC transferred to our wholly-owned subsidiary, Capital Southwest Venture Corporation ("CSVC"), certain assets and our license as a small business investment company ("SBIC"). CSVC is a closed-end, non-diversified investment company registered under the Investment Company Act of 1940 (the "1940 Act"). Prior to March 30, 1988, CSC was registered as a closed-end, non-diversified investment company under the 1940 Act. On that date, we elected to become a business development company ("BDC") subject to the provisions of the 1940 Act, as amended by the Small Business Incentive Act of 1980. Because CSC wholly owns CSVC, the portfolios of CSC and CVSC are referred to collectively as "our," "we" and "us." Capital Southwest Management Company ("CSMC"), a wholly-owned subsidiary of CSC, is the management company for CSC and CSVC. CSMC generally incurs all normal operating and administrative expenses, including, but not limited to, salaries and related benefits, rent, equipment and other administrative costs required for its day-to-day operations.

Our portfolio is a composite of companies, consisting of companies in which we have controlling interests, developing companies and marketable securities of established publicly traded companies. We make available significant managerial assistance to the companies in which we invest and believe that providing material assistance to such investee companies is critical to their business development activities.

The 12 largest investments we own had a combined cost of $49,252,842 and a value of $529,313,328, representing 94.7% of the value of our consolidated investment portfolio at March 31, 2012. The following table illustrates our 12 largest investments at March 31, 2012. A full description of these investments is set forth under the heading “Consolidated Schedule of Investments” in Item 8.

|

CSC

|

||||||||

|

Cost

|

Value

|

|||||||

|

The RectorSeal Corporation

|

$ | 52,600 | $ | 166,300,000 | ||||

|

Encore Wire Corporation

|

5,800,000 | 121,458,210 | ||||||

|

Alamo Group Inc.

|

2,190,937 | 85,138,938 | ||||||

|

The Whitmore Manufacturing Company

|

1,600,000 | 67,200,000 | ||||||

|

Heelys, Inc.

|

102,490 | 20,498,082 | ||||||

|

Media Recovery, Inc.

|

5,415,000 | 18,700,000 | ||||||

|

Hologic, Inc.

|

220,000 | 13,637,271 | ||||||

|

Extreme International, Inc.

|

3,325,875 | 10,162,000 | ||||||

|

Trax Holdings, Inc.

|

8,200,000 | 9,800,000 | ||||||

|

Cinatra Clean Technologies, Inc.

|

13,563,842 | 6,002,348 | ||||||

|

CapStar Holdings Corporation

|

3,703,619 | 5,338,000 | ||||||

|

iMemories, Inc.

|

5,078,479 | 5,078,479 | ||||||

|

|

$ | 49,252,842 | $ | 529,313,328 | ||||

Investment Criteria and Objectives

We are a venture capital investment company whose objective is to achieve capital appreciation through long-term investments in businesses believed to have favorable growth potential. Our investment interests are focused on growth capital, management-led buyouts and acquisition in a broad range of industry segments.

Our investment team has identified the following investment criteria that we believe are important in evaluating prospective portfolio companies:

|

|

·

|

Excellent Management: Management teams with a proven record of achievement, exceptional ability, unyielding determination and unquestionable integrity. We believe management teams with these attributes are more likely to manage the companies in a manner that protects our debt investment and enhances the value of our equity investment.

|

|

|

·

|

Investment Size: $5 million to $15 million of equity capital. We occasionally partner with other investors to engage in larger transactions.

|

|

|

·

|

Established Companies with Positive Cash Flow: We generally seek to invest in established companies with sound historical financial performance. We typically focus on companies that have historically generated near positive EBITDA (earnings before interest, taxes, depreciation and amortization) to $10 million of EBITDA.

|

|

|

·

|

Industry: We primarily focus on companies having competitive advantages in their respective markets and/or operating in industries with barriers to entry, which may help protect their market position. Overall, our portfolio is spread over many diverse industries.

|

|

|

·

|

Location: We focus on companies located in the United States, and we are most focused on the Southwest, Southeast, Midwest and Mountain Regions.

|

|

|

·

|

Quality referral from a reputable source: Excellent management is the cornerstone of our investment philosophy; therefore, it is helpful if mutually-known parties reach out to us on behalf of prospective investments. Accomplished managers generally have prior investors or directors willing to speak on their behalf.

|

We provide a platform that enables successful operators to build businesses at their desired pace and on their terms. Our investment approach is distinctive because we:

|

|

·

|

Provide long-term, patient capital for sustained growth. Our public ownership structure eliminates the pressure to exit our investments in the five to seven year timeframe typical of most venture capital and private equity partnerships. A third of our active investments have been held continuously for over 20 years.

|

|

|

·

|

Leave control with current owners. We find that the best recipe for success is a committed management team with significant ownership. Over half of our active portfolio companies are minority holdings. When operating control and ownership control remain with the management team, they have the flexibility to execute plans that serve customers, employees and shareholders well for the long term.

|

|

|

·

|

Have a time-tested business model. Many investment firms are first or second time funds – in other words, relatively unproven managers with unproven models. In contrast, we have partnered with over 160 companies to achieve superior returns for owners, management teams and investors for half a century.

|

|

|

·

|

Always have funds to invest. Our significant capital base enables us to fund businesses today and in the future, should the need arise. Since we take our responsibility as partners seriously, we have provided follow-on financing for a number of our portfolio companies, often years after our initial investment.

|

Investment Process

Our investment strategy involves a "team" approach, whereby potential transactions are screened by our investment team before they are presented to the Board of Directors for approval. Our investment team generally categorizes the investment process into seven distinctive stages:

|

|

·

|

Deal Generation/Origination: Deal generation and origination is maximized through long-standing and extensive relationships with industry contacts, brokers, commercial and investment bankers, entrepreneurs, service providers, such as lawyers and accountants, as well as current and former portfolio companies and investors.

|

|

|

·

|

Screening: Once it is determined that a potential investment has met our investment criteria, we will perform preliminary due diligence or screening. It is during this stage that we will take into consideration potential investment structures and price terms, as well as regulatory compliance. Upon successful screening of the proposed investment, the investment team makes a recommendation to move forward. We then issue a non-binding term sheet.

|

|

|

·

|

Term Sheet: The non-binding term sheet will include the key economic terms based upon our analysis performed during the screening process as well as a proposed timeline and our qualitative expectation for the transaction. Upon execution of the term sheet, we begin our formal due diligence process.

|

|

|

·

|

Due Diligence: Due diligence is performed by the leader of the designated investment team and certain external resources who together perform due diligence to understand the relationships among the prospective portfolio company’s business plan, operations and financial performance. Additionally, we may include site visits with management and key personnel; detailed review of historical and projected financial statements; interviews with key customers and suppliers; detailed evaluation of company management, including background checks; review of material contracts; in-depth industry, market and strategy analysis; and review by legal, environmental or other consultants, if needed. In certain cases, we may decide not to make an investment based on the results of due diligence.

|

|

|

·

|

Document and Close: Upon completion of a satisfactory due diligence review, our investment team presents its findings, in writing, to our Board of Directors for approval. If any adjustments to the investment terms or structures are proposed by our Board of Directors, such changes are made and applicable analysis is updated. Upon Board approval for the investment, we will re-confirm our regulatory company compliance, process and finalize all required legal documents and fund the investment.

|

|

|

·

|

Post-Investment: We continuously monitor the status and progress of our portfolio companies. We offer managerial assistance to our portfolio companies, giving them access to our investment experience, direct industry expertise and contacts. The same investment team lead that was involved in the investment process will continue involvement in the portfolio company post-investment. This provides for continuity of knowledge and allows the investment team to maintain a strong business relationship with key management of our portfolio companies for post-investment assistance and monitoring purposes. As part of the monitoring process, our investment team leader will analyze monthly/quarterly/annual financial statements versus the previous periods, review financial projections, meet with management, attend board meetings and review all compliance certificates and covenants. While we maintain limited involvement in the ordinary course of operations of our portfolio companies, we maintain a higher level of involvement in non-ordinary course financings, potential acquisitions and other strategic activities.

|

|

|

·

|

Exit Strategies: While our approach is primarily focused on providing long-term patient capital for sustained growth, we assist our portfolio companies in developing and planning exit opportunities, including any sale or merger of our portfolio companies, at the appropriate time. We assist in the structure, timing, execution and transition of the exit strategy.

|

Determination of Net Asset Value and Portfolio Valuation Process

We determine our net asset value per share on a quarterly basis. The net asset value per share is equal to our total assets minus liabilities divided by the total number of shares of common stock outstanding.

We determine in good faith the fair value of our portfolio investments pursuant to a valuation policy in accordance with Accounting Standards Codification ("ASC") Topic 820, Fair Value Measurements and Disclosures (“ASC 820”) and a valuation process approved by our Board of Directors and in accordance with the 1940 Act. Our valuation policy is intended to provide a consistent basis for determining the fair value of the portfolio.

As described below, we undertake a multi-step valuation process each quarter in connection with determining the fair value of our investments, with our Board of Directors ultimately and solely responsible for overseeing, reviewing and approving, in good faith, our estimate of the fair value of each individual investment.

|

|

·

|

Our quarterly valuation process begins with each portfolio company or investment being initially valued by the investment team leader responsible for the portfolio investment; and

|

|

|

·

|

Preliminary valuation conclusions will then be reviewed and discussed with our investment team; and

|

|

|

·

|

Our Board of Directors will assess the valuations and will ultimately approve the fair value of each investment in our portfolio, in good faith.

|

Our Board of Directors is ultimately and solely responsible for determining the fair value of portfolio investments on an annual basis. Annually, Duff & Phelps, LLC ("Duff & Phelps") provides third party valuation consulting services to our Board of Directors, which consists of certain limited procedures that our Board of Directors identifies and requests them to perform. For the year ended March 31, 2012, the Board of Directors asked Duff & Phelps to perform the limited procedures on six investments comprising approximately 85.8% of the total investments at fair value as of March 31, 2012. Upon completion of the limited procedures, Duff & Phelps concluded that the fair value of those investments, subject to the limited procedures, did not appear unreasonable.

Competition

We compete for attractive investment opportunities with private equity funds, venture capital partnerships and corporations, venture capital affiliates of industrial and financial companies, SBICs and wealthy individuals. We believe we are able to be competitive with these entities primarily on the basis of the experience and contacts of our management team and our responsive and efficient investment analysis and decision-making processes; however, this competitive environment could have a material adverse effect on our ability to acquire attractive investments.

Regulation

Regulation as a Business Development Company

We have elected to be regulated as a BDC under the 1940 Act. The 1940 Act contains prohibitions and restrictions relating to transactions between BDCs and their affiliates, principal underwriters and affiliates of those affiliates or underwriters. The 1940 Act requires that a majority of the members of the board of directors of a BDC be persons other than “interested persons,” as defined in the 1940 Act. In addition, the 1940 Act provides that we may not change the nature of our business so as to cease to be, or to withdraw our election as, a BDC unless approved by a majority of our outstanding voting securities.

The 1940 Act defines “a majority of the outstanding voting securities” as the lesser of (i) 67% or more of the voting securities present at a meeting if the holders of more than 50% of our outstanding voting securities are present or represented by proxy or (ii) more than 50% of our voting securities.

The following is a brief description of the 1940 Act provisions applicable to BDCs, which is qualified in its entirety by reference to the full text of the 1940 Act and rules issued thereunder by the SEC.

|

|

·

|

Generally, to be eligible to elect BDC status, a company must primarily engage in the business of furnishing capital and making significant managerial assistance available to companies that do not have ready access to compare through conventional financial channels. Such companies that satisfy certain additional criteria are defined as "eligible portfolio companies." In general, in order to qualify as a BDC, a company must: (i) be a domestic company; (ii) have registered a class of its securities pursuant to Section 12 of the Securities Exchange Act of 1934; (iii) operate for the purpose of investing in the securities of certain types of portfolio companies, including early stage or emerging companies and businesses suffering or just recovering from financial distress (see following paragraph); (iv) make available significant managerial assistance to such portfolio companies; and (v) file a proper notice of election with the SEC.

|

|

|

·

|

An eligible portfolio company generally is a domestic company that is not an investment company or a company excluded from investment company status pursuant to exclusions for certain types of financial companies (such as brokerage firms, banks, insurance companies and investment banking firms) and that: (i) does not have a class of securities listed on a national securities exchange; (ii) does have a class of equity securities listed on a national securities exchange with a market capitalization of less than $250 million; or (iii) is controlled by the BDC itself or together with others (control under the 1940 Act is presumed to exist where a person owns at least 25% of the outstanding voting securities of the portfolio company) and has a representative on the Board of Directors of such company.

|

|

|

·

|

We are required to provide and maintain a bond issued by a reputable fidelity insurance company to protect the BDC. Furthermore, as a BDC, we are prohibited from protecting any director or officer against any liability to us or our shareholders arising from willful malfeasance, bad faith, gross negligence or reckless disregard of the duties involved in the conduct of such person’s office.

|

|

|

·

|

We are required to adopt and implement written policies and procedures reasonably designed to prevent violation of the federal securities laws, review these policies and procedures annually for their adequacy and the effectiveness of their implementation and designate a chief compliance officer to be responsible for administering these policies and procedures.

|

Qualifying Assets

The 1940 Act provides that we may not make an investment in non-qualifying assets unless at the time at least 70% of the value of our total assets (measured as of the date of our most recently filed financial statements) consists of qualifying assets. Qualifying assets include: (i) securities of eligible portfolio companies; (ii) securities of certain companies that were eligible companies at the time we initially acquired their securities and in which we retain a substantial interest; (iii) securities of certain controlled companies; (iv) securities of certain bankrupt, insolvent or distressed companies; (v) securities received in exchange for or distributed in or with respect to any of the foregoing; and (vi) cash items, U.S. government securities and high-quality short-term debt. The SEC has adopted a rule permitting a BDC to invest its funds in certain money market funds. The 1940 Act also places restrictions on the nature of the transactions in which, and the persons for whom, securities can be purchased in some instances in order for the securities to be considered qualifying assets.

Managerial Assistance to Portfolio Companies

In order to count portfolio securities as qualifying assets for the purpose of the 70% test, we must either control the issuer of the securities or must offer to make available to the issuer of the securities (other than small and solvent companies described above) significant managerial assistance; except that, where we purchase such securities in conjunction with one or more other persons acting together, one of the other persons in the group may make available such managerial assistance. Making available managerial assistance means, among other things, any arrangement whereby the BDC, through its directors, officers or employees, offers to provide, and, if accepted, does so provide, significant guidance and counsel concerning the management, operations or business objectives and policies of a portfolio company.

Marketable Securities and Idle Funds Investments

Pending investments in “qualifying assets,” as described above, our investments may consist of cash, cash equivalents, U.S. government securities, short-term investments in secured debt investments, independently rated debt investments and diversified bond funds, which we refer to, collectively, as marketable securities and idle funds investments, so that 70% of our assets are qualifying assets.

Senior Securities

We are permitted by the 1940 Act, under specific conditions, to issue multiple classes of debt and a single class of preferred stock if our asset coverage, as defined by the 1940 Act, is at least 200% after the issuance of the debt or the preferred stock (i.e. such senior securities may not be in excess of our net assets). Under specific conditions, we are also permitted by the 1940 Act to issue warrants.

Common Stock

Except under certain conditions, we may sell our securities at a price that is below the prevailing net asset value per share only during the 12-month period after (i) a majority of our directors and our disinterested investors have determined that such sale would be in the best interests of us and our stockholders and (ii) the holders of a majority of our outstanding voting securities and the holders of a majority of our voting securities held by persons who are not affiliated person of ours approve such issuances. A majority of the disinterested directors must determine in good faith that the price of the securities being sold is not less than a price which closely approximates market value of the securities, less any distribution discount or commission.

Code of Ethics

We adopted a code of ethics pursuant to Rule 17j-1 under the 1940 Act that establishes procedures for personal investments and restricts certain personal securities transactions. Personnel subject to the code may invest in securities for their personal investment accounts including securities that may be purchased or held by us, so long as such investments are made in accordance with the code’s requirements. Certain transactions involving certain persons closely related to us including our directors, officers and employees, may require approval of the SEC. However, the 1940 Act ordinarily does not restrict transactions between us and our portfolio companies.

We may be periodically examined by the SEC for compliance with the 1940 Act.

Small Business Investment Company Regulations

CSVC is licensed by the Small Business Administration ("SBA") to operate as a SBIC under Section 301(c) of the Small Business Investment Act of 1958.

SBICs are designed to stimulate the flow of private equity capital to eligible small businesses. Under SBIC regulations, an SBIC may make loans to eligible small businesses, invest in equity securities of such businesses and provide them with consulting and advisory services.

Under current SBIC regulations, eligible small businesses generally include businesses that (together with their affiliates) have a tangible net worth not exceeding $18 million and have average annual net income after federal income taxes not exceeding $6 million (average net income to be computed without benefit of any carryover loss) for the two most recent fiscal years. In addition, an SBIC must devote 20% of its investment activity to "smaller" concerns as defined by the SBA. A smaller concern generally includes businesses that have a tangible net worth not exceeding $6 million and have average annual net income after federal income taxes not exceeding $2 million (average net income to be computed without benefit of any net carryover loss) for the two most recent fiscal years. SBIC regulations also provide alternative size standard criteria to determine eligibility for designation as an eligible small business or smaller concern, which criteria depend on the primary industry in which the business is engaged and are based on such factors as the number of employees and gross revenue. However, once an SBIC has invested in a company, it may continue to make follow on investments in the company, regardless of the size of the portfolio company at the time of the follow on investment, up to the time of the portfolio company’s initial public offering.

The SBA prohibits an SBIC from providing funds to small businesses for certain purposes, such as relending and investment outside the United States, to businesses engaged in a few prohibited industries and to certain "passive" (non-operating) companies. In addition, without prior SBA approval, an SBIC may not invest an amount equal to more than approximately 30% of the SBIC’s regulatory capital in any one portfolio company and its affiliates.

The SBA places certain limitations on the financing terms of investments by SBICs in portfolio companies (such as limiting the permissible interest rate on debt securities held by an SBIC in a portfolio company). Although prior regulations prohibited an SBIC from controlling a small business concern except in limited circumstances, regulations adopted by the SBA in 2002 now allow an SBIC to exercise control over a small business for a period of seven years from the date on which the SBIC initially acquires its control position. This control period may be extended for an additional period of time with the SBA’s prior written approval.

The SBA restricts the ability of a SBIC to lend money to any of its officers, directors and employees or to invest in affiliates thereof. The SBA also prohibits, without prior SBA approval, a "change of control" of a SBIC or transfers that would result in any person (or a group of persons acting in concert) owning 10% or more of a class of capital stock of a licensed SBIC. A "change of control" is any event which would result in the transfer of the power, direct or indirect, to direct the management and policies of a SBIC, whether through ownership, contractual arrangements or otherwise.

An SBIC (or group of SBICs under common control) may generally have outstanding debentures guaranteed by the SBA in amounts up to twice the amount of the privately-raised funds of the SBIC(s). Debentures guaranteed by the SBA have a maturity of 10 years, require semi-annual payments of interest, do not require any principal payments prior to maturity and, historically, were subject to certain prepayment penalties. Those prepayment penalties no longer apply as of September 2006. As of March 31, 2012 and 2011, we had no SBA-guaranteed debentures.

SBICs must invest idle funds that are not being used to make loans in investments permitted under SBIC regulations in the following limited types of securities: (i) direct obligations of, or obligations guaranteed as to principal and interest by, the United States government, which mature within 15 months from the date of the investment; (ii) repurchase agreements with federally insured institutions with a maturity of seven days or less (and the securities underlying the repurchase obligations must be direct obligations of or guaranteed by the federal government); (iii) certificates of deposit with a maturity of one year or less, issued by a federally insured institution; (iv) a deposit account in a federally insured institution that is subject to a withdrawal restriction of one year or less; (v) a checking account in a federally insured institution; or (vi) a reasonable petty cash fund.

SBICs are periodically examined and audited by the SBA’s staff to determine their compliance with SBIC regulations and are periodically required to file forms with the SBA.

Taxation as a Regulated Investment Company

We elected to be treated as a regulated investment company (a "RIC"), taxable under Subchapter M of the Internal Revenue Code of 1986, as amended (the "Code"), for federal income tax purposes. In general, a RIC is not taxed on its income or gains to the extent it distributes such income or gains to its shareholders. In order to qualify as a RIC, we must, in general, (1) annually derive at least 90% of our gross income from dividends, interest and gains from the sale of securities and similar sources (the "Income Source Rule"); (2) quarterly meet certain investment asset diversification requirements; and (3) annually distribute at least 90% of our investment company taxable income as a dividend (the "Income Distribution Rule"). Any taxable investment company income not distributed is subject to corporate level tax. Any taxable investment company income distributed generally is taxable to shareholders as dividend income.

In addition to the requirement that we must annually distribute at least 90% of our investment company taxable income, we may either distribute or retain our realized net capital gains from investments, but any net capital gains not distributed may be subject to corporate level tax. It is our current intention not to distribute net capital gains. Any net capital gains distributed generally will be taxable to shareholders as long-term capital gains.

In lieu of actually distributing our realized net capital gains, we as a RIC may retain all or part of our net capital gains and elect to be deemed to have made a distribution of the retained portion to our shareholders under the "designated undistributed capital gain" rules of the Code. We currently intend to retain and so designate all of our net capital gains. In this case, the "deemed distribution" generally is taxable to our shareholders as long-term capital gains. Although we pay tax at the corporate rate on the amount deemed to have been distributed, our shareholders receive a tax credit equal to their proportionate share of the tax paid and an increase in the tax basis of their shares by the amount per share retained by us.

To the extent that we retain capital gains and have a "deemed distribution," each shareholder will receive an IRS Form 2439 that will reflect each shareholder's receipt of the deemed distribution income and a tax credit equal to each shareholder's proportionate share of the tax paid by us. This tax credit, which is paid at the corporate rate, is often credited at a higher rate than the actual tax due by a shareholder on the deemed distribution income. The "residual" credit can be used by the shareholder to offset other taxes due in that year or to generate a tax refund to the shareholder. Tax exempt investors may file for a refund.

Although we may retain income and gains subject to the limitations described above (including paying corporate level tax on such amounts), we could be subject to an additional 4% excise tax if we fail to distribute 98% of our aggregate annual taxable income.

The NASDAQ Global Select Market Corporate Governance Regulations

The Nasdaq Global Select Market has adopted corporate governance regulations with which listed companies must comply in order to remain listed. We believe we are in compliance with such corporate governance listing standards. We intend to monitor our compliance with all future listing standards and to take all necessary actions to ensure that we stay in compliance.

Securities Act of 1934 and Sarbanes-Oxley Act Compliance

We are subject to the reporting and disclosure requirements of the Securities Exchange Act of 1934 (the “Exchange Act”), including the filing of quarterly, annual and current reports, proxy statements and other required items. In addition, we are subject to the Sarbanes-Oxley Act of 2002, which imposes a wide variety of regulatory requirements on publicly-held companies and their insiders. For example:

|

|

·

|

pursuant to Rule 13a-14 of the Exchange Act, our Chief Executive Officer and Chief Financial Officer are required to certify the accuracy of the financial statements contained in our periodic reports;

|

|

|

·

|

pursuant to Item 307 of Regulation S-K, our periodic reports are required to disclose our conclusions about the effectiveness of our disclosure controls and procedures;

|

|

|

·

|

pursuant to Rule 13a-15 of the Exchange Act, our management is required to prepare a report regarding its assessment of our internal control over financial reporting, and our independent registered public accounting firm separately audits our internal control over financial reporting; and

|

|

|

·

|

pursuant to Item 308 of Regulation S-K and Rule 13a-15 of the Exchange Act, our periodic reports must disclose whether there were significant changes in our internal control over financial reporting or in other factors that could significantly affect these controls subsequent to the date of their evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses.

|

Corporate information

Our principal executive offices are located at 12900 Preston Road, Suite 700, Dallas, Texas 75230. We maintain a Website on the Internet at www.capitalsouthwest.com. You can review the filings we have made with the SEC, free of charge by linking directly from our website to NASDAQ, a database that links to EDGAR, the Electronic Data Gathering, Analysis, and Retrieval System of the SEC. You may also use the site to access our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. The public may read and copy materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website that contains the reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. The charters adopted by the committees of our Board of Directors are also available on our website. Information contained on our website is not incorporated by reference into this Annual Report on Form 10-K, and you should not consider that information to be part of this Annual Report on Form 10-K.

Employees

As of March 31, 2012, we had fifteen employees, each of whom was employed by our management company, CSMC. These employees include our corporate officers, investment and portfolio management professionals and administrative staff. We will hire additional investment professionals and additional administrative personnel, as necessary. All of our employees are located in our Dallas office.

Item 1A. Risk Factors

Investing in our common stock involves a number of significant risks. In addition to other information contained in this Annual Report on Form 10-K, investors should consider the following information before making an investment in our common stock. The risks and uncertainties described below decrease the material risks we face; However, risks and uncertainties not presently known to us, or not presently deemed material by us, may also impair our operations and performance. If any of the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected. If that happens, the trading price of our common stock could decline, and you may lose all or part of your investment.

RISKS RELATED TO ECONOMIC CONDITIONS

The current state of the economy and financial markets increases the likelihood of adverse effects on our financial position and results of operations. Continued economic adversity could impair our portfolio companies’ financial position and operating results and affect the industries in which we invest, which could, in turn, harm our operating results.

The broader economic fundamentals of the U.S. economy remain uncertain. Unemployment levels remain elevated and consumer fundamentals remain depressed, which has led to significant reductions in spending by both consumers and businesses. In the event that the U.S. economy remains depressed, it is likely that the financial results of small to mid-size companies, like those in which we invest, could experience deterioration or limited growth from current levels, which could ultimately lead to difficulty in meeting their debt service requirements and increase defaults. In addition, the end markets for certain of our portfolio companies’ products and services have experienced negative economic trends. Consequently, we can provide no assurance that the performance of certain of our portfolio companies will not be negatively impacted by these economic and other conditions, which could also have a negative impact on our future results.

RISKS RELATED TO OUR BUSINESS AND STRUCTURE

Our investment portfolio is and will continue to be recorded at fair value, with our Board of Directors having final responsibility for overseeing, reviewing and approving, in good faith, our estimate of fair value. As a result, there is and will continue to be uncertainty as to the value of our portfolio investments.

Under the 1940 Act, we are required to carry our portfolio investments at market value or, if there is no readily available market value, at fair value as determined by us, with our Board of Directors having final responsibility for overseeing, reviewing and approving, in good faith, our estimate of fair value. Typically, there is not a public market for the securities of the privately held companies in which we have invested and generally will continue to invest. As a result, we value these securities quarterly at fair value based on inputs from management and our investment team, along with the oversight, review and approval of our Board of Directors.

The determination of fair value and consequently, the amount of unrealized gains and losses in our portfolio, are to a certain degree, subjective and dependent on a valuation process approved by our Board of Directors. Certain factors that may be considered in determining the fair value of our investments include external events, such as private mergers, sales and acquisitions involving comparable companies. Because of the inherent uncertainty of the valuation of portfolio securities which do not have readily ascertainable market values, our fair value determinations may differ materially from the values a third party would be willing to pay for such securities or the values which would be applicable to unrestricted securities having a public market. Due to this uncertainty, our fair value determinations may cause our net asset value on a given date to be materially understated or overstate the value that we may ultimately realize on one or more of our investments. As a result, investors purchasing our common stock based on an overstated net asset value may pay a higher price than the value of our investments might warrant. Conversely, investors selling shares during a period in which the net asset value understates the value of our investments may receive a lower price for their shares than the value of our investments might warrant.

Our financial condition and results of operations will depend on our ability to effectively manage any future growth and deploy capital.

Our ability to achieve our investment objective of maximizing our portfolio’s total return by generating income from our debt investments and capital appreciation from our equity and equity-related investments depends on our ability to effectively manage and deploy capital, which depends, in turn, on our investment team’s ability to identify, evaluate and monitor, and our ability to finance and invest in, companies that meet our investment criteria.

Accomplishing our investment objective on a cost-effective basis is largely a function of our investment team’s handling of the investment process, its ability to provide competent, attentive and effective services and our access to investments offering acceptable terms. In addition to monitoring the performance of our existing investments, members of our investment team are called upon, from time to time, to provide managerial assistance to some of our portfolio companies. These demands on their time may distract them and slow the rate of investment.

Even if we are able to grow and build upon our investment operations, any failure to manage or sustain our growth effectively could have a material adverse effect on our business, financial condition, results of operations and prospects. The results of our operations will depend on many factors, including the availability of opportunities for investment, readily accessible short and long-term funding alternatives in the financial markets and economic conditions. Furthermore, if we cannot successfully operate our business or implement our investment policies and strategies as described herein, it could negatively impact our ability to pay dividends.

Sustaining growth depends on our ability to identify, evaluate, finance, and invest in companies that meet our investment criteria. Accomplishing such results on a cost-effective basis is a function of our marketing capabilities and skillful management of the investment process. Failure to achieve future growth could have a material adverse effect on our business, financial condition, and results of operations. The results of our operations will depend on many factors, including the availability of opportunities for investment, readily accessible short and long-term funding alternatives in the financial markets and economic conditions. Furthermore, if we cannot successfully operate our business or implement our investment policies and strategies as described herein, it could negatively impact our ability to pay dividends.

If we fail to invest our capital effectively, our return on equity may be decreased, which could reduce the price of the shares of our common stock.

We operate in a highly competitive market for investment opportunities.

We compete for attractive investment opportunities with private equity funds, venture capital partnerships and corporations, venture capital affiliates of industrial and financial companies, SBICs and wealthy individuals. Some of these competitors are substantially larger and have greater financial, technical and marketing resources, and some are subject to different and frequently less stringent regulations. As a result of this competition, we may not be able to take advantage of attractive investment opportunities from time to time and there can be no assurance that we will be able to identify and make investments that satisfy our objectives. A significant increase in the number and/or size of our competitors in our target market could force us to accept less attractive investment terms. Furthermore, many of our competitors are not subject to the regulatory restrictions that the 1940 Act imposes on us as a BDC.

We are dependent upon management for our future success.

Selection, structuring and closing our investments depends upon the diligence and skill of our management, which is responsible for identifying, evaluating, negotiating, monitoring and disposing of our investments. Our management’s capabilities may significantly impact our results of operations. If we lose any member of our management team and he/she cannot be promptly replaced with an equally capable team member, we may not be able to operate our business as we expect and our ability to compete could be harmed, which could cause our operating results to suffer.

Our success depends on attracting and retaining qualified personnel in a competitive environment.

Our growth will require that we retain new investment and administrative personnel in a competitive environment. Our ability to attract and retain personnel with the requisite credentials, experience and skills depends on several factors, including but not limited to, our ability to offer competitive wages, benefits and professional growth opportunities.

The competitive environment for qualified personnel may require us to take certain measures to ensure that we are able to attract and retain experienced personnel. Such measures may include increasing the attractiveness of our overall compensation packages, altering the structure of our compensation packages through the use of additional forms of compensation or other steps. The inability to attract and retain experienced personnel would have a material adverse effect on our business.

Our business model depends to a significant extent upon strong referral relationships, and our inability to maintain or develop these relationships, as well as the failure of these relationships to generate investment opportunities, could adversely affect our business.

We expect that members of our management team will maintain their relationships with intermediaries, financial institutions, investment bankers, commercial bankers, financial advisors, attorneys, accountants, consultants and other individuals within our network, and we will rely to a significant extent upon these relationships to provide us with potential investment opportunities. If our management team fails to maintain its existing relationships or develop new relationships with sources of investment opportunities, we will not be able to grow our investment portfolio. In addition, individuals with whom members of our management team have relationships are not obligated to provide us with investment opportunities, and therefore, there is no assurance that such relationships will generate investment opportunities for us.

We will be subject to corporate-level income tax if we are unable to qualify as a RIC under Subchapter M of the Code.

To maintain RIC tax treatment under the Code, we must meet the following annual distribution, income source and asset diversification requirements:

|

|

·

|

The annual distribution requirement for a RIC will be satisfied if we distribute to our stockholders on an annual basis at least 90% of our net ordinary income and realized short-term capital gains in excess of realized net long-term capital losses, if any. Depending on the level of taxable income earned in a tax year, we may choose to carry forward taxable income in excess of current year distributions into the next year and pay a 4% excise tax on such income. Any such carryover taxable income must be distributed through a dividend declared prior to filing the final tax return related to the year which generated such taxable income.

|

|

|

·

|

The source of income requirement will be satisfied if we obtain 90% of our income for each year from distributions, interest, gains from the sale of stock or securities or similar sources.

|

|

|

·

|

The asset diversification requirement will be satisfied if we meet certain asset diversification requirements at the end of each quarter of our taxable year. To satisfy this requirement, at least 50% of the value of our assets must consist of cash, cash equivalents, U.S Government securities, securities of other RICs, and other acceptable securities; no more that 25% of the value of our assets can be invested in the securities, other than U.S Government securities or securities of other RICs, of two or more issuers that are controlled, as determined under applicable Code rules, by us and that are engaged in the same or similar or related trades or businesses or of certain “qualified publicly traded partnerships.”

|

Failure to meet these requirements may result in us having to dispose of certain unqualified investments quickly in order to prevent the loss of RIC status. If we fail to maintain RIC tax treatment for any reason and are subject to corporate income tax, the resulting corporate taxes could substantially reduce our net assets, the amount of income available for distribution and the amount of our distributions. In addition, to the extent we had unrealized gains, we would have to establish deferred tax liabilities for taxes, which would reduce our net asset value accordingly. In addition, our shareholders would lose the tax credit realized when we, as a RIC, decide to retain the net realized capital gain and make deemed distributions of net realized capital gains, and pay taxes on behalf of our shareholders at the end of the tax year. The loss of this pass-through tax treatment could have a material adverse effect on the total return, if any, obtainable from an investment in our common stock.

We may not be able to pay you dividends, our dividends may not grow over time and a portion of our dividends paid to you may be a return of capital.

We intend to pay semi-annual dividends to our shareholders out of assets legally available for distribution. We cannot assure you that we will achieve investment results that will allow us to pay a specified level of cash dividends, previously projected dividends for future periods or year-to-year increases in cash dividends. Our ability to pay dividends might be adversely affected by, among other things, the impact of one or more of the risk factors described herein. In addition, the inability to satisfy the asset coverage test applicable to us as a BDC could limit our ability to pay dividends. All dividends will be paid at the discretion of our Board of Directors and will depend upon our earnings, our financial condition, maintenance of our RIC status, compliance with applicable BDC regulations, CSVC’s compliance with applicable SBIC regulations and such other factors as our Board of Directors may deem relevant from time to time. We cannot assure you that we will pay dividends to our shareholders in the future.

Historically, we have retained net realized capital gains, paid the resulting tax at the corporate level and retained the after-tax gains to supplement our equity capital and support continuing additions to our portfolio. Our shareholders then report such capital gains on their tax returns, receive credit for the tax we paid and are deemed to have reinvested the amount of the retained after-tax gain. We cannot assure you that we will achieve investment results or maintain a RIC tax status that will allow any specified level of cash distributions or our shareholders’ current tax treatment of realized and retained capital gains.

We may in the future choose to pay dividends in our own stock, in which case you may be required to pay tax in excess of the cash receive.

We may distribute taxable dividends that are payable in part in our stock as well as stock in any of our other public holdings. Under an IRS revenue procedure, up to 90% of any such taxable dividend declared on or before December 31, 2013 with respect to taxable years ended on or before December 31, 2012 could be payable in our stock. Where the IRS revenue procedure is not currently applicable, the IRS has also issued private letter rulings on cash and stock dividends paid by RICs and real estate investment trusts using a 20% cash standard (and, more recently, the 10% cash standard of the above-referenced IRS revenue procedure) if certain requirements are satisfied. Taxable shareholders receiving such dividends will be required to include the full amount of the dividend as ordinary income (or as long-term capital gain to the extent such distributions is properly designated as a capital gain dividend) to the extent of our current and accumulated earnings and profits for United States federal income tax purposes. As a result, a U.S. shareholder may be required to pay tax with respect to such dividends in excess of any cash received. If a U.S. shareholder sells the stock it receives as a dividend in order to pay this tax, the sales proceeds may be less than the amount included in income with respect to the dividend, depending on the market price of our stock at the time of the sale. Furthermore, with respect to non-U.S. shareholders, we may be required to withhold U.S. tax with respect to such dividends, including in respect of all or a portion of such dividend that is payable in stock. In addition, if a significant number of our shareholders determine to sell shares of our stock in order to pay taxes owed on dividends, it may put downward pressure on the trading price of our stock.

Because we intend to distribute substantially all of our net ordinary income to our shareholders to maintain our status as a RIC, we may need additional capital to finance our growth.

In order to satisfy the requirements applicable to a RIC and to minimize corporate-level taxes, we intend to distribute to our shareholders substantially all of our net ordinary income. We may carry forward excess undistributed taxable income into the next year, net of the 4% excise tax. Any such carryover taxable income must be distributed through a dividend declared prior to filing the final tax return related to the year which generated such taxable income.

Accordingly, in the event that we develop a need for additional capital in the future to sustain or grow our operations or for any other reason, we cannot assure you that any sources for such funding will be available to us for potential capital needs in the future. If additional funds are not available to us, we could be forced to curtail or cease new investment activities, and our net asset value could decline.

Changes in laws or regulations governing our operations or our failure to comply with those laws or regulations may adversely affect our business.

We and our portfolio companies are subject to regulation by laws at the local, state and federal level. These laws and regulations, as well as their interpretation, may be changed from time to time. Accordingly, any changes in these laws and regulations or failure to comply with them could have a material adverse effect on our business. Certain of these laws and regulations pertain specifically to BDCs such as us.

Terrorist attacks, act of war or natural disasters may affect any market for our common stock, impact the businesses in which we invest and harm our business, operating results and financial condition.

Terrorist attacks, acts of war or natural disasters may disrupt our operations, as well as the operations of the businesses in which we invest. Such acts have created, and continue to create, economic and political uncertainties and have contributed to global economic instability. Future terrorist activities, military or security operations, or natural disasters could further weaken the domestic/global economies and create additional uncertainties, which may negatively impact the businesses in which we invest directly or indirectly and, in turn, could have a material adverse impact on our business, operating results and financial condition. Losses from terrorist attacks and natural disasters are generally uninsurable.

RISKS RELATED TO OUR INVESTMENTS

Our investments in portfolio companies involve higher levels of risk, and we could lose all or part of our investment.

Investing in our portfolio companies involves a number of significant risks. Among other things, these companies:

|

|

·

|

may have limited financial resources and may be unable to meet their obligations under their debt instruments that we hold, which may be accompanied by a deterioration in the value of any collateral and a reduction in the likelihood of us realizing any guarantees from subsidiaries or affiliates of our portfolio companies that we may have obtained in connection with our investment, as well as a corresponding decrease in the value of the equity components of our investments;

|

|

|

·

|

may have shorter operating histories, narrower product lines, smaller market shares and/or significant customer concentrations than larger businesses, which tend to render them more vulnerable to competitors’ actions and market conditions, as well as general economic downturns;

|

|

|

·

|

are more likely to depend on the management talents and efforts of a small group of persons; therefore, the death, disability, resignation, termination, or significant under-performance of one or more of these persons could have a material adverse impact on our portfolio company and, in turn, on us;

|

|

|

·

|

may have less predictable operating results, may from time to time be parties to litigation, may be engaged in rapidly changing businesses with products subject to a substantial risk of obsolescence and may require substantial additional capital to support their operations, finance expansion or maintain their competitive position; and

|

|

|

·

|

may have less publicly available information about their businesses, operations and financial condition. We are required to rely on the ability of our management team and investment professionals to obtain adequate information to evaluate the potential returns from investing in these companies. If we are unable to uncover all material information about these companies, we may not make a fully informed investment decision and may lose all or part of our investment.

|

In addition, in the course of providing significant managerial assistance to certain of our portfolio companies, certain of our officers and directors may serve as directors on the boards of such companies. To the extent that litigation arises out of our investments in these companies, our officers and directors may be named as defendants in such litigation, which could result in an expenditure of funds (through our indemnification of such officers and directors) and the diversion of management’s time and resources.

We may not have the funds or ability to make additional investments in our portfolio companies.

We may not have the funds or ability to make additional investments in our portfolio companies. After our initial investment in a portfolio company, we may be called upon from time to time to provide additional funds to such company or have the opportunity to increase our investment through the exercise of a warrant to purchase common stock. There is no assurance that we will make, or will have sufficient funds to make, follow-on investments. Any decisions not to make a follow-on investment or any inability on our part to make such an investment may have a negative impact on a portfolio company in need of such an investment, may result in a missed opportunity for us to increase our participation in a successful operation or may reduce the expected yield on the investment.

Certain of our portfolio companies are highly leveraged.

Some of our portfolio companies have incurred substantial indebtedness in relation to their overall capital base. Such indebtedness often has terms that will require the balance of the loan to be refinanced when it matures. If portfolio companies cannot generate adequate cash flow to meet the principal and interest payments on their indebtedness, the value of our investments could be reduced or eliminated through foreclosure on the portfolio company’s assets or by the portfolio company’s reorganization or bankruptcy.

Defaults by our portfolio companies may harm our operating results.

A portfolio company’s failure to satisfy financial or operating covenants imposed by us or other lenders could lead to non-payment of interest and other defaults and, potentially, termination of its loans and foreclosure on its secured assets, which could trigger cross-defaults under other agreements and jeopardize a portfolio company’s ability to meet its obligations under the debt or equity securities that we hold. We may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms, which may include the waiver of certain financial covenants, with a defaulting portfolio company.

There is limited publicly available information regarding the companies in which we invest.

Many of the securities in our portfolio are issued by privately held companies. There is generally little or no publicly available information about such companies, and we must rely on the diligence of our management to obtain the information necessary for our decision to invest. There can be no assurance that such diligence efforts will uncover all material information necessary to make fully informed investment decisions.

Potential sales of large volume of publicly traded companies’ stocks could have an adverse effect on our ultimate gain.

In March 2012, Form S-3 registration statements of Alamo Group, Inc. (NYSE: ALG), Encore Wire Corporation (NASDAQ: WIRE) and Heelys Inc. (NASDAQ: HLYS) were filed with the Securities and Exchange Commission (“SEC”). As a result of these registrations becoming effective with the SEC, restrictions in the sale of the common stock of these companies imposed by Rule 144 of the Securities Exchange Act of 1933 were lifted, and valuation discounts previously applied to these holdings were removed. Due to our ownership of a large number of shares of the stocks and fluctuation in the trading prices, sales of these stocks may be traded at a discount to fair market value. Sales may also be limited by unfavorable market conditions. The size of our investments may preclude or delay the disposition of such securities, Our potential sales of these stocks could have an adverse impact on the price of these stocks and subsequently affect the potential gain we could receive from the sales.

RISKS RELATING TO OUR COMMON STOCK

Investment in shares of our common stock should not be considered a complete investment program.

Our stock is intended for investors seeking long-term capital appreciation. Our investments in portfolio securities generally require many years to reach maturity, and such investments generally are illiquid. An investment in our shares should not be considered a complete investment program. Each prospective purchaser should take into account his or her investment objectives as well as his or her other investments when considering the purchase of our shares.

Our common stock often trades at a discount from net asset value.

Our common stock is listed on The NASDAQ Global Market ("NASDAQ"). Shareholders desiring liquidity may sell their shares on NASDAQ at current market value, which has often been below net asset value. Shares of closed-end investment companies frequently trade at discounts from net asset value, which is a risk separate and distinct from the risk that a fund’s performance will cause its net asset value to decrease.

The market price of our common stock may fluctuate significantly.

The market price and marketability of shares of our common stock may from time to time be significantly affected by numerous factors, including:

|

|

·

|

our investment results;

|

|

|

·

|

market conditions;

|

|

|

·

|

departure of our key personnel;

|

|

|

·

|

changes in regulatory policies, accounting pronouncements or tax guidelines, particularly with respect to RICs, BDCs or SBICs; and

|

|

|

·

|

other influences and events over which we have no control and that may not be directly related to us.

|

Item 1B. Unresolved Staff Comments

We have no unresolved comments from the staff of the SEC.

Item 2. Properties

We maintain our offices at 12900 Preston Road, Suite 700, Dallas, Texas 75230, where we rent approximately 7,250 square feet of office space pursuant to a lease agreement expiring in September 2014. We believe that our offices are adequate to meet our current and expected future needs.

Item 3. Legal Proceedings

We may, from time to time, be involved in litigation arising out of our operations in the normal course of business or otherwise. Furthermore, third parties may try to seek to impose liability on us in connection with the activities of our portfolio companies. We have no current pending legal proceedings to which we are a party or to which any of our assets is subject.

Item 4. Mine Safety Disclosures

Not Applicable.

PART II

|

Item 5.

|

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

PRICE RANGE OF COMMMON STOCK AND HOLDERS

Our common stock is traded on the NASDAQ Global Select Market under the symbol “CSWC.” The following high and low selling prices for shares during each quarter of the last two fiscal years were taken from quotations provided to the Company by NASDAQ:

|

Quarter Ended

|

High

|

Low

|

||||||

|

March 31, 2012

|

$ | 96.46 | $ | 81.42 | ||||

|

December 31, 2011

|

92.10 | 70.07 | ||||||

|

September 30, 2011

|

101.67 | 71.79 | ||||||

|

June 30, 2011

|

98.26 | 89.90 | ||||||

|

March 31, 2011

|

$ | 104.81 | $ | 89.14 | ||||

|

December 31, 2010

|

111.01 | 90.47 | ||||||

|

September 30, 2010

|

93.50 | 86.25 | ||||||

|

June 30, 2010

|

96.61 | 84.26 | ||||||

DIVIDENDS

The payment dates and amounts of cash dividends per share since April 1, 2009 are as follows:

|

Payment Date

|

Cash Dividend

|

|||

|

May 29, 2009

|

$ | 0.40 | ||

|

November 30, 2009

|

0.40 | |||

|

May 28, 2010

|

0.40 | |||

|

November 30, 2010

|

0.40 | |||

|

May 31, 2011

|

0.40 | |||

| November 30, 2011 | 0.40 | |||

The amounts and timing of cash dividend payments have generally been dictated by requirements of the Internal Revenue Code (“IRC”) regarding the distribution of taxable net investment income (ordinary income) of regulated investment companies. Instead of distributing realized long-term capital gains to shareholders, the Company has ordinarily elected to retain such gains to fund future investments.

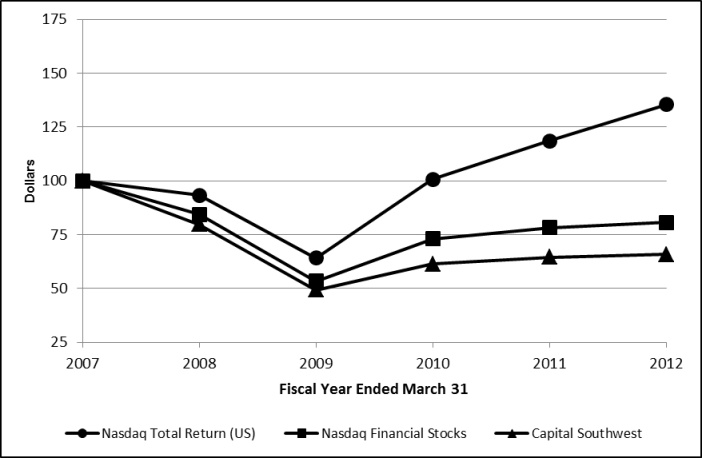

Performance Graph

The following graph compares our cumulative total shareholder return during the last five years (based on the market price of our common stock and assuming reinvestment of all dividends and tax credits on retained long-term capital gains) with the Total Return Index for NASDAQ (U.S. companies) and with the Total Return Index for Nasdaq Financial Stocks. Both indices were provided by NASDAQ.

Comparison of Five Year Cumulative Total Returns

Item 6. Selected Financial Data

The following table provides selected financial data relating to our historical financial condition and results of operations as of and for each of the years ended March 31, 2008 through 2012. This data should be read in conjunction with Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes.

Selected Consolidated Financial Data

(In thousands except per share data)

|

Financial Position

(as of March 31)

|

2012

|

2011

|

2010

|

2009

|

2008

|

|||||||||||||||

|

Investments at cost

|

$ | 88,993 | $ | 98,355 | $ | 100,023 | $ | 89,339 | $ | 81,027 | ||||||||||

|

Unrealized appreciation

|

469,553 | 390,918 | 377,920 | 307,296 | 466,544 | |||||||||||||||

|

Investments at market or fair value

|

558,546 | 489,273 | 477,943 | 396,635 | 547,571 | |||||||||||||||

|

Total assets

|

632,989 | 543,214 | 491,175 | 417,543 | 586,685 | |||||||||||||||

|

Net assets

|

628,706 | 539,233 | 486,926 | 415,263 | 583,700 | |||||||||||||||

|

Shares outstanding

|

3,755 | 3,753 | 3,741 | 3,741 | 3,889 | |||||||||||||||

|

Changes in Net Assets

(years ended March 31)

|

||||||||||||||||||||

|

Net investment income

|

$ | 2,544 | $ | 1,804 | $ | 2,091 | $ | 10,183 | $ | 3,715 | ||||||||||

|

Net realized gain on investments

|

10,578 | 38,885 | 826 | 10,756 | 240 | |||||||||||||||

|

Net increase (decrease) in unrealized appreciation before distributions*

|

78,635 | 12,999 | 70,624 | (159,246 | ) | (142,969 | ) | |||||||||||||

|

Increase (decrease) in net assets from operations before distributions

|

91,757 | 53,688 | 73,541 | (138,307 | ) | (139,014 | ) | |||||||||||||

|

Cash dividends paid

|

(3,003 | ) | (2,994 | ) | (2,993 | ) | (12,257 | ) | (2,333 | ) | ||||||||||

|

Employee stock options exercised

|

99 | 745 | – | – | 231 | |||||||||||||||

|

Stock option expense

|

1050 | 957 | 675 | 503 | 263 | |||||||||||||||

|

Change in pension plan funded status

|

(430 | ) | (88 | ) | 440 | (1,473 | ) | (1,178 | ) | |||||||||||

|

Treasury stock

|

– | – | – | (16,903 | ) | – | ||||||||||||||

|

Increase (decrease) in net assets

|

$ | 89,473 | $ | 52,308 | $ | 71,663 | $ | (168,437 | ) | $ | (142,031 | ) | ||||||||

|

Per share data

(as of March 31)

|

||||||||||||||||||||

|

Net assets

|

$ | 167.45 | $ | 143.68 | $ | 130.14 | $ | 110.98 | $ | 150.09 | ||||||||||

|

Closing market price

|

94.55 | 91.53 | 90.88 | 76.39 | 123.72 | |||||||||||||||

|

Cash dividends paid

|

.80 | .80 | .80 | 3.26 | .60 | |||||||||||||||

*See Note 3 Investments.

|

Item 7.

|

Management's Discussion and Analysis of Financial Condition and Results of Operations

|

The following discussion should be read in conjunction with our financial statements and the notes thereto included elsewhere in this Annual Report on Form 10-K.

Statements we make in the following discussion which express a belief, expectation or intention, as well as those that are not historical fact, are forward-looking statements that are subject to risks, uncertainties and assumptions. Our actual results, performance or achievements, or industry results, could differ materially from those we express in the following discussion as a result of a variety of factors, including the risks and uncertainties we have referred to under the headings “Cautionary Statement Concerning Forward-Looking Statements” and “Risks Factors” in Part I of this report.

Results of Operations