UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-04321

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to section 12(g) of the Act:

None | ||

| (Title of class) | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

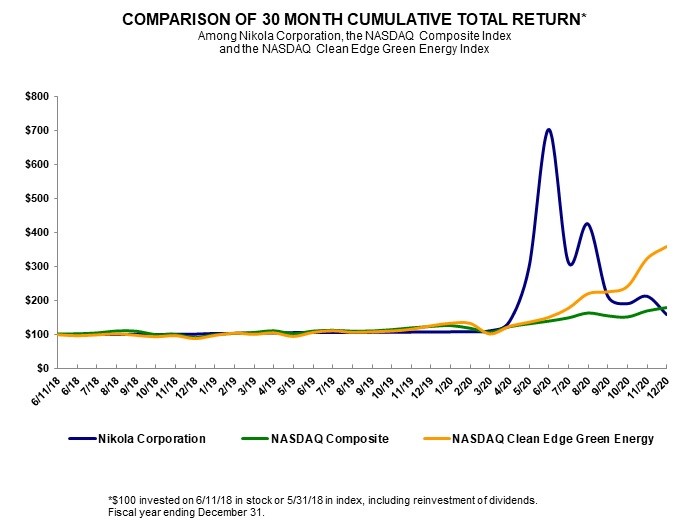

The aggregate market value of voting stock held by non-affiliates of the Registrant on June 30, 2020, based on the closing price of $67.53 for shares of the Registrant’s common stock as reported by The Nasdaq Stock Market LLC, was approximately $12.5 billion. Shares of common stock beneficially owned by each executive officer, director, and holder of more than 10% of our common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The registrant had outstanding 391,945,919 shares of common stock as of February 19, 2021.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10 (as to directors and Section 16(a) Beneficial Ownership Reporting Compliance), 11, 12, 13 and 14 of Part III incorporate by reference information from the registrant’s proxy statement to be filed with the Securities and Exchange Commission in connection with the solicitation of proxies for the registrant’s 2021 Annual Meeting of Stockholders to be held on June 8, 2021.

TABLE OF CONTENTS

| Page | |||||

Forward-Looking Statements

This report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. When used in this report, the words “anticipate,” “believe,” “expect,” “estimate,” “intend,” “plan,” "will," and similar expressions are intended to identify forward looking statements. These are statements that relate to future periods and include our financial and business performance; expected timing with respect to the build out of our manufacturing facilities, joint venture with Iveco and production and attributes of our BEV and FCEV trucks; expectations regarding our hydrogen fuel station rollout plan; timing of completion of prototypes, validation testing, volume production and other milestones; changes in our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects and plans; planned collaboration with our business partners; our future capital requirements and sources and uses of cash; the potential outcome of investigations, litigation, complaints, product liability claims and/or adverse publicity; the implementation, market acceptance and success of our business model; developments relating to our competitors and industry; the impact of health epidemics, including the COVID-19 pandemic, on our business and the actions we may take in response thereto; our expectations regarding our ability to obtain and maintain intellectual property protection and not infringe on the rights of others; our ability to obtain funding for our operations; the outcome of any known and unknown regulatory proceedings; our business, expansion plans and opportunities; changes in applicable laws or regulations; and anticipated trends and challenges in our business and the markets in which we operate.

i

Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those expected. These risks and uncertainties include, but are not limited to, those risks discussed in Item 1A of this report, as well as our ability to execute our business model, including market acceptance of our planned products and services; changes in applicable laws or regulations; risks associated with the outcome of any legal, regulatory or judicial proceeding; the effect of the COVID-19 pandemic on our business; our ability to raise capital; our ability to compete; the success of our business collaborations; regulatory developments in the United States and foreign countries; the possibility that we may be adversely affected by other economic, business, and/or competitive factors; and our history of operating losses. These forward-looking statements speak only as of the date hereof. We expressly disclaim any obligation or undertaking to update any forward-looking statements contained herein to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

In this report, all references to “Nikola,” “we,” “us,” or “our” mean Nikola Corporation.

Nikola™ is a trademark of Nikola Corporation. We also refer to trademarks of other corporations and organizations in this report.

Summary of Risk Factors

Our business is subject to numerous risks and uncertainties that could affect our ability to successfully implement our business strategy and affect our financial results. You should carefully consider all of the information in this report and, in particular, the following principal risks and all of the other specific factors described in Item 1A. of this report, “Risk Factors,” before deciding whether to invest in our company.

•We are an early stage company with a history of losses, and expect to incur significant expenses and continuing losses for the foreseeable future.

•We may be unable to adequately control the costs associated with our operations.

•Our business model has yet to be tested and any failure to commercialize our strategic plans would have an adverse effect on our operating results and business, harm our reputation and could result in substantial liabilities that exceed our resources.

•Our limited operating history makes evaluating our business and future prospects difficult and may increase the risk of your investment.

•We expect to need to raise additional funds and these funds may not be available to us when we need them. If we cannot raise additional funds when we need them, our operations and prospects could be negatively affected.

•If we fail to manage our future growth effectively, we may not be able to market and sell our vehicles successfully.

•Our bundled lease model may present unique problems that may have an adverse effect on our operating results and business and harm our reputation.

•We may face legal challenges in one or more states attempting to sell directly to customers which could materially adversely affect our costs.

•We face risks and uncertainties related to litigation, regulatory actions and government investigations and inquiries.

•Our success will depend on our ability to economically manufacture our trucks at scale and build our hydrogen fueling stations to meet our customers’ business needs, and our ability to develop and manufacture trucks of sufficient quality and appeal to customers on schedule and at scale is unproven.

•We may experience significant delays in the design, manufacture, launch and financing of our trucks, including in the build out of our manufacturing plant, which could harm our business and prospects.

ii

PART I

Item 1. Business

Company Overview

Who We Are

Our vision is to be the zero-emissions transportation industry leader. We plan to realize this vision through world-class partnerships, groundbreaking research and development, and a revolutionary business model.

According to the Environmental Protection Agency, or EPA, and the European Environment Agency, or EEA, the transportation industry causes an estimated 25% to 30% of U.S. and EU greenhouse gas, or GHG, emissions. While heavy-duty trucking represents less than 10% of the transportation industry, it is responsible for approximately 40% of transportation industry GHG according to the International Council on Clean Transportation, or ICCT. With ever-expanding e-commerce freight demands, zero-emission vehicles are believed to be one of the only viable options for a sustainable future.

We are a technology innovator and integrator, working to develop innovative energy and transportation solutions. We are pioneering a business model that will enable corporate customers to integrate next-generation truck technology, hydrogen fueling infrastructure, and related maintenance. By creating this ecosystem, we and our strategic business partners and suppliers hope to build a long-term competitive advantage for clean technology vehicles and next generation fueling solutions.

Our expertise lies in design, innovation, and software and engineering. We assemble, integrate, and commission our vehicles in collaboration with our business partners and suppliers. Our approach has always been to leverage strategic partnerships to help lower cost, increase capital efficiency and increase speed to market. To date, we have assembled world-class partners and we will continue to use this approach.

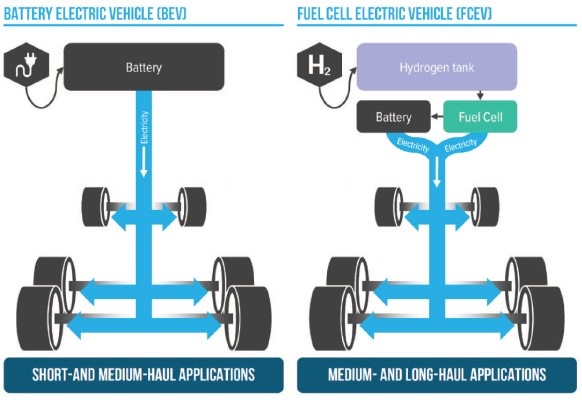

We operate in two business units: Truck and Energy. The Truck business unit is developing and commercializing battery electric vehicles, or BEV, and hydrogen fuel cell electric vehicles, or FCEV, Class 8 trucks that provide environmentally friendly, cost-effective solutions to the short-haul, medium-haul and long-haul trucking sector. The Energy business unit is focused on developing and constructing a network of hydrogen fueling stations to meet hydrogen fuel demand for our FCEV and other customers, as well as potential solutions for BEV customers.

The key differentiator of our business model is our planned network of hydrogen fueling stations. Historically, investing in alternative fuel vehicles represented a high risk for both original equipment manufacturers, or OEMs, and customers due to the uncertainty of the fueling infrastructure. Existing fuel providers have limited incentive to deploy required resources and capital to develop an alternative fuel infrastructure due to a lack of known demand. The inability to tackle both sides of this equation has prohibited hydrogen from reaching its full potential to date. Our approach aims to solve this ‘‘chicken or the egg’’ problem.

For FCEV customers, we are offering a unique bundled lease model, which provides truck, hydrogen fuel, and maintenance. Our go-to-market strategy will be offering a fixed price per mile through a 7 year or 700,000 mile lease to our customers, although alternative structures may be available especially in the early stages of the FCEV roll-out. Our bundled lease model will significantly de-risk infrastructure development by locking in fuel demand from our dedicated route customers. This locked in demand will ensure high station utilization.

We believe our station network will provide a competitive advantage and help accelerate the adoption of our FCEV. We believe our product portfolio and hydrogen fueling network provide a key strategic advantage that differentiates us from competitors and will allow us to provide significant and valuable innovation to the estimated $600 billion global heavy-duty commercial vehicle and the related fueling and maintenance ecosystems.

1

Market

Total Addressable Market

We believe our unique bundled lease, which includes the FCEV truck, fuel, and maintenance, will allow us to expand our total addressable market significantly when compared to traditional OEMs.

Globally, the total addressable market, or TAM, is estimated to be a $600 billion per year with steady growth expected to continue as e-commerce and global economic growth fuel the need for more heavy-duty trucks.

Based on data provided by ACT Research, the estimated $600 billion TAM is as follows:

•Global Class 8 Truck Sales Market: Approximately $118 billion ($36 billion U.S. market, $32 billion EU market, $50 billion rest of world or ROW)

•Global Fueling Market: Approximately $367 billion ($63 billion U.S. market, $93 billion EU market, $211 billion ROW)

•Global Service and Maintenance Market: Approximately $112 billion ($29 billion U.S. market, $26 billion EU market, $57 billion ROW)

According to ACT Research, the active Class 8 truck population is expected to grow by approximately 5.0% annually from 2019 to 2023.

Class 8 Market Segmentation

Private Fleet vs. For-Hire Fleet Segmentation

ACT Research segments the on-highway Class 8 freight market between private and for-hire fleets, representing 53% and 47% of the Class 8 market, respectively. Private fleets, such as PepsiCo or Sysco, are almost all regular route operations or ‘‘dedicated’’ routes running point-to-point. The for-hire market, such as JB Hunt, XPO Logistics, can be further broken down into: contract 32%, spot 12%, and dedicated 3%. Dedicated for-hire fleets are mostly outsourced by shippers to run point-to-point.

Length of Haul Segmentation

ACT Research breaks down the Class 8 truck market by the length-of-haul. The length-of-haul refers to the distance of an outbound load, and does not account for a return trip.

•Short-haul less than 100 miles: applications include agricultural and drayage operations.

•Medium-haul 100-250 miles: applications include private fleet distribution, less than truckload operations, and regional for-hire fleets.

•Long-haul over 250 miles: applications include regular and irregular for-hire fleets, and private fleet regular route operations.

E-commerce Driving Expansion of Freight Moved by Trucks

According to the Freight Analysis Framework and the U.S. Department of Transportation Statistics, in 2017, approximately 40% of all freight was moved by trucks in the U.S. and that amount is expected to continue to grow. According to Eurostat, in Europe, approximately 52% of all freight in 2017 was moved by trucks. That number is expected to grow approximately 30% through 2030. According to ACT Research, globally, the active Class 8 truck population is expected to increase from 7.3 million in 2018, to 9.2 million in 2023, as emerging markets drive volume growth.

2

Shift to Zero-Emission Vehicles

According to EPA and the EEA reports as of 2017, the transportation industry causes an estimated 25% to 30% of U.S. and European GHG emissions. While heavy-duty trucking represents less than 10% of the vehicle population, the ICCT estimates it is responsible for approximately 40% of emissions from the transportation industry, making them disproportionate contributors to pollution. Diesel vehicles are a major source of harmful air pollutants and GHG emissions. The associated local air pollution, particulates of oxides of nitrogen and particulate matter emissions, negatively impacts health and quality of life. Additionally, diesel exhaust has been classified as a potential human carcinogen by the EPA and the International Agency for Research on Cancer. Studies done on exposure to high levels of diesel exhaust indicate a greater risk of lung cancer.

A significant share of global GHG emissions stem from heavy-duty vehicle transportation. We believe zero-emission vehicles are one of the viable options to reduce emissions in the transportation sector to meet climate, ozone, and regulatory targets. According to the U.S. Emissions Center for Climate and Energy Solutions, in 2017, U.S. GHG emissions totaled 6,457 million metric tons, or MMT, of CO2 equivalents. Medium and heavy-duty vehicles accounted for 7% of total emissions, equal to 431 MMT of CO2 equivalents. The EEA’s report on GHG in Europe found that in 2017, EU GHG emissions totaled 4,481 MMT of CO2 equivalents. Heavy-duty vehicles accounted for 5% of total emissions, equal to 224 MMT of CO2 equivalents.

A strong consensus among the largest governments calls for a global push to shift to zero-emission vehicles and the eventual elimination of internal combustion engine, or ICE vehicles. According to the Center for Climate Protections ‘‘Survey on Global Activities to Phase Out ICE Vehicles’’ report, actions being taken by national and local governments include:

•The following cities signed the C40 Fossil-Fuel-Free Streets Declaration: Electric buses by 2025, ICE vehicles banned by 2030: Athens, Auckland, Barcelona, Cape Town, Copenhagen, Heidelberg, London, Los Angeles, Madrid, Milan, Mexico City, Paris, Quito and Rome.

•Additionally, Delhi, Hamburg, Oslo, Oxford, and Tokyo, have all began to implement and propose plans to move towards all zero-emissions vehicles.

Countries Phasing Out ICE Vehicles (specific actions vary by country):

•Austria: No new ICE vehicles sold after 2020;

•China: End production and sales of ICE vehicles by 2040;

•Denmark: 5,000 electric vehicles, or EVs, on the road by 2019, tax incentive in place;

•France: Ban the sale of petrol and diesel cars by 2040;

•Germany: No registration of ICE vehicles by 2030 (passed by legislature); cities can ban diesel cars;

•India: Target of no new ICE vehicles sold after 2030;

•Ireland: No new ICE vehicles sold after 2030; Incentive program in place for EV sales;

•Israel: No new ICE vehicle imports after 2030;

•Japan: Incentive program in place for EV sales;

•Netherlands: No new ICE vehicles sold after 2030; Phase out begins 2025;

•Norway: Sell only electric and hybrid vehicles starting in 2025;

•Portugal: Official target and incentive in place for EV Sales;

•Scotland: No new ICE vehicles sold after 2032;

3

•South Korea: EVs account for 30% of auto sales by 2020;

•Spain: Incentive package to promote sales of alternative energy vehicles;

•Sweden: Ban of new ICE vehicle sales in 2030;

•Taiwan: Phase out fossil fuel-powered motorcycles by 2035 and fossil fuel-powered vehicles by 2040. Additionally, the replacement of all government vehicles and public buses with electric versions by 2030;

•United Kingdom: Ban the sale of petrol and diesel cars starting in 2030

With such strong sentiment to reduce global GHG emissions from leading governments, OEMs will have to spend significant additional research and development on existing models to remain compliant in the near term, or they will face heavy fines. In Europe, there will be a mandatory 15% reduction in CO2 emissions by 2025, and a 30% reduction target by 2030. There will be a financial penalty for failure to achieve these targets. The level of the penalties is 4,250 Euros and 6,800 Euros per gCO2 / tonne-kilometre, or tkm, in 2025 and 2030, respectively. Conventional diesel technology will most likely not be able to meet the European targets set for 2025 and 2030. These ambitious CO2 targets are likely ‘‘technology-forcing’’ towards alternative powertrains such as battery-electric and hydrogen fuel cell.

In early 2021, the Biden administration has established measurable steps and metrics with the purpose of limiting global climate change. Changes already enacted to accomplish this goal include re-joining the Paris Climate Agreement, an international treaty designed to reduce climate change, and promising to replace the U.S. government’s existing vehicle fleet with “net zero emission” electric vehicles.

In addition to the steps already taken, we expect that the U.S. government will enact stricter vehicle emissions standards while offering incentives that drive vehicle owners and manufacturers to zero emission solutions. This market shift to clean energy transportation, backed by the Biden administration, offers a background in which we believe we are well-positioned to succeed.

In addition, consumers are increasingly demanding that corporations take action to reduce their carbon footprint. An article by Nielsen from 2018 cited that nearly half (48%) of U.S. consumers said they would ‘‘definitely’’ or ‘‘probably’’ change their consumption habits to reduce their impact on the environment, placing reducing emissions high on the agenda for large corporations. For example:

•Amazon has pledged to become carbon neutral by 2040;

•BP has pledged to become carbon neutral by 2050;

•DB Schenker plans to make its transport activities in European cities emission-free by 2030;

•DHL set a goal to reduce all logistics-related emissions to zero by 2050;

•UPS has committed to sourcing 40% of its ground fuel from low carbon or alternative fuels by 2025;

•Walmart set a goal of an 18% emissions reduction in their own operations by 2025 and to work with suppliers to reduce emissions by 1 gigaton by 2030; and

•Microsoft has committed to be carbon negative by 2030, and that by 2050 it hopes will have sequestrated enough carbon to account for all direct emissions it has ever made.

U.S. Market Policy Trends

•Major shift and greater alignment on climate change policy – Federal government and increasing numbers of states moving in similar policy directions (i.e., electric vehicles, infrastructure, roadmaps).

4

•Federal government advancing aggressive executive actions to move the U.S. to transportation electrification and decarbonization; California is advancing comprehensive zero-emissions market development strategy.

•More state legislatures and regulatory agencies moving to consider transportation electrification planning and funding programs – key regions are emerging.

•Hydrogen and fuel cell technology receiving increased attention as a zero-emission and low carbon fuel type, spurring hydrogen production and hydrogen marketplace discussions are emerging at national level and in multiple states.

•National hydrogen coalition development - 11 companies have partnered to form Hydrogen Forward - initiative focused on advancing hydrogen development in the U.S. Founding members include – Air Liquide, Anglo American, Bloom Energy, CF Industries, Chart Industries, Cummins Inc., Hyundai, Linde, McDermott, Shell and Toyota.

•Increasing numbers of states focusing on grid modernization efforts, including energy storage targets, innovative pilot programs, advanced rate design pilots, electric grid resilience, and battery storage deployments.

Federal Policy Update - Biden Administration Executive Orders

Protecting Public Health and the Environment and Restoring Science to Tackle the Climate Crisis

•Directs federal agencies to consider revising vehicle fuel economy and emissions standards to ensure that such standards cut pollution.

•Establishes an Interagency Working Group on the Social Cost of GHG to account for the benefits of reducing climate pollution to address GHG.

Tackling the Climate Crisis at Home and Abroad, Create Jobs, and Restore Scientific Integrity Across Federal Government

•Center the Climate Crisis in U.S. Foreign Policy and National Security Considerations

•Take a Whole-of-Government Approach to the Climate Crisis

•Leverage the Federal Government’s Footprint and Buying Power to Lead by Example

▪Directs the federal agencies to procure carbon pollution-free electricity and clean, zero-emission vehicles to create good-paying, union jobs and stimulate clean energy industries.

▪Directs federal agencies to eliminate fossil fuel subsidies as consistent with applicable law and identify new opportunities to spur innovation, commercialization, and deployment of clean energy technologies and infrastructure.

•Rebuild Our Infrastructure for a Sustainable Economy

▪The order catalyzes the creation of jobs in construction, manufacturing, engineering and the skilled-trades by directing steps to ensure that every federal infrastructure investment reduces climate pollution and that steps are taken to accelerate clean energy and transmission projects under federal siting and permitting processes in an environmentally sustainable manner.

•Advance Conservation, Agriculture, and Reforestation

•Revitalize Energy Communities

5

•Secure Environmental Justice and Spur Economic Opportunity

Hydrogen Fuel Cell and Battery Technology Momentum

With the global push to eliminate ICE vehicles, battery-electric and fuel cell technologies currently stand out as the best alternatives to diesel. Both battery costs, a key cost competent of a BEV, and electricity prices, a key cost component in hydrogen fuel production, have decreased significantly over the past decade, and prices continue to decrease. These cost reductions significantly improve the economics of BEV and FCEV trucks.

A January 2020 report published by the Hydrogen Council highlighted how policy and economic forces are converging, creating unprecedented momentum in the hydrogen sector. This momentum is buoyed by:

•66 countries having announced net zero-emissions as a target by 2050;

•Approximately 80% decrease in global average renewable energy prices since 2010; and

•Expected 55 times growth in electrolysis capacity by 2025 compared to 2015.

Zero-Emission Vehicles Enabled by Significant Reduction in Battery Cost and Renewable Electricity Prices

The majority of the cost of production of a BEV truck, and a major cost component of a FCEV truck, lie in the cost of the battery. As illustrated in a 2019 report by Bloomberg NEF, from 2010 to 2018, lithium-ion battery prices have fallen from $1,160 per kilowatt-hour, or kWh, to $176 per kWh, representing an 85% cost reduction. As investment in battery technology continues to increase as a result of OEMs allocating more capital to next-generation powertrain technology, this trend in battery cost reduction is expected to continue. Conversely, vehicles that run on lithium-ion battery-electric power can experience battery capacity and performance loss over time, depending on the use and age of the battery.

For hydrogen production, we expect electricity costs to account for approximately 75% to 85% of the total cost. Per Lazard’s November 2019 Levelized Cost of Energy Analysis, the cost of producing renewable energy has dropped significantly since 2009. In 2009, the global average solar and wind levelized cost of energy was $359 per megawatt-hour, or MWh, and $135 per MWh, respectively. In 2019, these costs were $40 per MWh for solar and $41 per MWh for wind, representing a cost reduction of 89% and 70%, respectively.

Renewable energy prices are expected to continue to fall as production capacity is set to expand by 50% between 2019 to 2024. This trend will further reduce renewable energy prices, which will drive the cost of hydrogen production even lower.

According to Wood Mackenzie, in the U.S., the world’s second-largest solar market, power purchase agreements, or PPAs, are now trending between $20 to $30 per MWh, and on a global scale, prices have been observed as low as $17 per MWh. Lower solar energy production cost is expected to allow us to produce renewable hydrogen at a cost that is competitive with existing diesel solutions.

Industry Focused on TCO

In the highly competitive trucking industry, when choosing between truck models that meet their technical and safety requirements, customers mainly base their purchasing decision on total cost of ownership, or TCO. TCO is the total cost of owning the truck through its lifecycle, including lease cost or purchase payment, fuel cost, service, and maintenance. According to ACT Research, traditionally, TCO for diesel trucks (excluding driver wages, benefits, and insurance), is typically broken down into cost of fuel (approximately 50%), purchase or lease payments on truck (approximately 22%), and repairs and maintenance (approximately 28%).

According to ACT Research, historically, diesel fuel comprises 40% to 60% of TCO, depending on prevailing diesel fuel prices. With the incumbent ICE technology, fleet operators are also forced to accept volatility in their largest cost component, creating risk and uncertainty. Our bundled lease will provide customers TCO clarity for the first time in the industry’s history.

6

Industry and Competition

Competition in the Class 8 heavy-duty truck industry is intense and new regulatory requirements for vehicle emissions, technological advances, and shifting customer demands are causing the industry to evolve towards zero-emission solutions. We believe the primary competitive factors in the Class 8 market include, but are not limited to:

•vehicle safety;

•total cost of ownership (TCO);

•product performance and uptime;

•availability of charging or re-fueling network;

•emissions profile;

•vehicle quality and reliability;

•technological innovation;

•improved vehicle operational visibility;

•ease of autonomous capability development; and

•service options.

Similar to traditional OEMs in the passenger vehicle market, incumbent commercial transportation OEMs are burdened with legacy systems and the need to generate sufficient return on existing infrastructure, which historically created a reluctance to embrace new zero-emission drivetrain technology. This reluctance created an opportunity for us.

However, we believe the global push for lower emissions combined with vast technological improvements in fuel cell and battery-electric powertrain technologies has awakened well-established OEMs to begin investing in zero-emission vehicle platforms.

BEV Competition

Tesla, Daimler, Volvo, as well as other automotive manufactures, have announced their plans to bring Class 8 BEV trucks to the market over the coming years. Tesla announced its concept vehicle, the Tesla Semi, in November 2017. Daimler announced its plans for the eCascadia, which is the electric version of their flagship Freightliner Cascadia, in June 2018. Volvo announced plans to commercialize its BEV heavy-duty truck, the VNR Electric, in December 2018. Other competitors include BYD, who we believe is currently selling Class 8 BEV trucks, Peterbilt, XOS, Lion, Volvo, Hyliion, and potentially Cummins. We believe all of these competitors are in various stages of rolling out their vehicles, including pilot programs and providing test vehicles to customers.

FCEV Competition

Due to higher barriers to entry, there are fewer competitors in the FCEV Class 8 market. However, Hyundai and Toyota have chosen to focus their efforts on FCEV as the powertrain of the future. Hyundai intends to enter the European market for heavy-duty vehicles with their FCEV truck, the Hyundai Xcient. In addition, others such as Hyundai have announced they plan to offer FCEV trucks and invest in hydrogen stations for refueling. Toyota is collaborating with Kenworth, an American manufacturer for medium and heavy-duty trucks, to jointly develop an FCEV heavy-duty truck, and Daimler and Volvo recently announced a proposed joint venture to develop fuel cell systems for heavy-duty trucks. Other potential competitors include Navistar, Hino and Hyzon.

7

Competitors in Context

Most of our current and potential competitors have greater financial, technical, manufacturing, marketing, and other resources than we do. They may be able to deploy greater resources to the design, development, manufacturing, distribution, promotion, sales, marketing and support of their BEV and FCEV truck programs. Additionally, many of our competitors also have greater name recognition, longer operating histories, larger sales forces, broader customer and industry relationships, and greater resources than we do.

Although our competitors may have certain advantages we do not possess, we believe we are positioned to compete favorably. Although we do not have the same name recognition, or operating history as most of our competition, we are free from the burden of legacy infrastructure and design. We believe we have the benefit of a head start and the advantage of beginning from a blank slate, which is critical when introducing new technology.

Products

As the commercial transportation sector transitions towards zero-emission solutions, we believe there will be a need to offer tailored solutions that meet the needs of each customer. Unlike the passenger vehicle market, where users typically return home each day, the commercial vehicle market contains multiple use cases often requiring vehicles to be out on the road for days, or weeks at a time. By offering both BEV (for short and medium-haul, city, regional, and drayage deliveries) and FCEV (for medium and long-haul) solutions, we believe we are uniquely positioned to disrupt the commercial transportation sector by providing solutions that address the full range of customer needs.

The electrical propulsion of our BEV and FCEV trucks has a modular design which allows the batteries and associated controls to be configured to either a BEV or FCEV propulsion. Our architecture inside the centralized e-axle is configured for the appropriate power needs for the BEV and FCEV for a wide range of applications. Our cab-over design allows us to address both the European and North American markets which provide engineering and manufacturing synergies.

8

We have developed a portfolio of proprietary electrified architectures and associated technologies that are embedded and integrated into our BEV and FCEV vehicles. Our principal vehicle offerings include:

Nikola's Class 8 BEV - Nikola Tre

The Nikola Tre Class 8 truck is based on the S-WAY platform from Iveco and integrates our electrified propulsion, technology, controls and infotainment. In addition, we redesigned the majority of the high-visibility components and body panels of the S-WAY truck, and added several new interior features including a digital cockpit with an infotainment screen, instrument screen and panel, redesigned steering wheel, and new seats. The cab-over design is desirable for city center applications due to shorter vehicle length, improved maneuverability, and better visibility. The Nikola Tre BEV will be marketed for short and medium-haul applications in North America and Europe.

The BEV version of Nikola Tre will be the first to market, addressing the near-term market opportunity as this version does not require a roll-out of charging infrastructure. BEVs run on a fully electric drivetrain powered by rechargeable batteries. Our BEV has an estimated range of 250 to 350 miles and is designed to address the short and medium-haul market. During the initial roll-out, customers will be responsible for their own charging needs.

Sales of the Nikola Tre BEV are expected to begin in late 2021 in North America. We expect that BEV sales will principally be made direct to customers.

Nikola's Class 8 FCEV's - Nikola Tre and Nikola Two

FCEVs use fuel cells on-board to convert hydrogen into electricity to power the electric motors which transmit power to the wheels. The fuel cell generates electricity through a chemical reaction, supplied from on-board tanks, and oxygen from the atmosphere. A much smaller battery (compared to our BEV) provides supplemental power to the drivetrain, and stores energy recovered during regenerative braking. The voltage and charge of the battery are maintained through a combination of power supplied from the fuel cell and energy captured through regenerative braking.

9

In North America, we plan to develop and launch two FCEV truck platforms.

The Nikola Tre FCEV is targeted for medium and long-haul missions ranging from 300 – 500 miles per day. Its scalable architecture is expected to handle the majority of the North American day-cab market. The Tre FCEV leverages the Tre BEV platform with modifications for hydrogen fuel cell operation, improved aerodynamics, and lightweighting. The Nikola Tre FCEV is expected to launch in 2023.

The Nikola Two Sleeper Cab is targeted for long-haul missions with an operational range up to approximately 900 miles. This configuration allows for longer operation between fueling and is specifically designed for long-haul applications and extended highway operation. The Nikola Two FCEV is expected to launch in the second half of 2024.

We expect that in the longer term as autonomous technologies relieve hours of service restrictions, FCEVs will be an ideal option for longer continuous hauls.

Our FCEVs are designed to allow us to address the longer-term opportunity by combining our fuel cell technology and a network of hydrogen stations across North America.

Hydrogen Fueling Stations

We are developing fueling and charging stations in North America and Europe to support our BEV and FCEV customers and to help capture first mover advantage with respect to next generation fueling infrastructure.

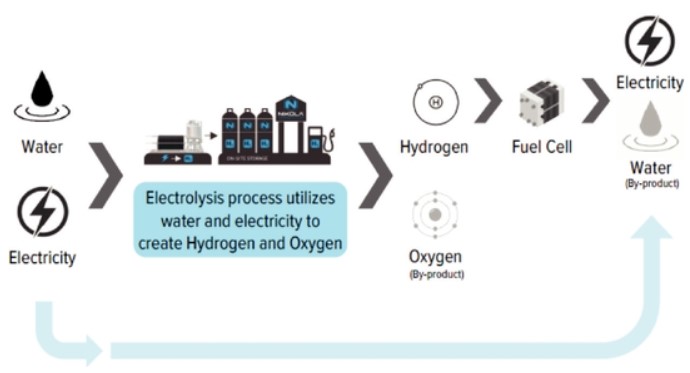

We intend to collaborate with strategic partners to deploy multiple stations based on a variety of factors including cost, reliability, and carbon intensity of energy sources. In certain cases where electricity can be procured in a cost-effective manner, hydrogen fuel will be produced on-site, via electrolysis. In other cases, hydrogen fuel will be produced off-site and delivered to fueling stations under a supply "hub and spoke" structure.

Electricity input for on-site hydrogen fuel production will be purchased via long-term supply agreements where feasible. Hydrogen production sites are expected to have daily production capacity of 8,000 kg and could support approximately 200 FCEV trucks per day. These sites are designed to be scalable to up to 40,000 kg per day of production, if needed. Our stations are expected to contain at least eight heavy-duty (for commercial trucks) and up to four light-duty (for vehicles) hydrogen fueling dispensers. We also plan to install electric fast charging to support BEV trucks.

Each fueling and charging station will be designed to maximize the utilization from the start and is anticipated to generate substantial revenue and cash flow, which can be used to fund the development of future stations.

First Test Station Installed at Nikola's Phoenix HQ

Through our partnership with Nel ASA, a Norwegian hydrogen company, or Nel, we have initiated the development of the hydrogen station infrastructure by completing our first 1,000 kg demo station in the first quarter of 2019 at our corporate headquarters in Phoenix, Arizona. The demo hydrogen station offers hydrogen storage and dispensing and serves as a model for future hydrogen stations.

10

Overall Fueling Station Rollout Strategy

Given the anticipated minimum range of 300 miles for our FCEV trucks and our desire to rapidly expand hydrogen fueling infrastructure across North America to promote the decarbonization of the freight industry, we are conceptually planning on deploying fueling stations at intervals of no more than 250 miles apart, to accommodate less efficient driving styles, heavy payloads, climbing steep grades, and local travel within a metropolitan area.

The station locations will be planned to coincide with the greatest volumes of existing truck traffic, existing population centers and freight hubs, major freeway intersections, and available incentives. We envision our early station rollout seeking to cover as broad of a geographic range as possible across the freight routes that are likely to see the greatest volumes of FCEV adoption.

Following deployment of a broad fueling station network, we envision increasing the density of the fueling station locations based upon customer demand for fuel and satisfying the needs of secondary routes within the network.

First Stations to Support Customers with Dedicated Routes

Initially, our fueling and charging stations will be built to support carefully selected fleet customers who have dedicated routes along major interstate corridors. For example, we have partnered with Anheuser-Busch, or AB, as a launch customer because they have dedicated freight routes between their twelve breweries and six distribution centers. Stations will be built in Southern California and in Phoenix, Arizona to support AB's freight movements along Interstate 10 from their brewery in Van Nuys, California to their distribution center in Chandler, Arizona.

California Hydrogen Station Strategy

Our initial plan is to build up to approximately ten stations in California. These stations will supply fuel for our launch customers in those geographies that have dedicated routes in California. California is offering incentives to build out our hydrogen fueling infrastructure, including opportunities for funding along major freeway corridors. We expect to begin securing sites in 2021 and then proceeding to build in phases to support customer demand.

After the California station build-out, we plan to strategically target other states offering incentives.

Single-Station Dedicated Route Strategy

After maximizing incentives offered by states, our strategy is to build hydrogen fueling stations along dedicated routes according to the needs of strategically selected customers. We anticipate the need for up to 700 stations in North America. This overall strategy is designed to enable a capital-efficient roll-out of hydrogen stations, ensuring high utilization and predictability of demand, while allowing us to also sell hydrogen to third-party purchasers.

The layout and freight movement along our interstate system provides ample opportunities to expand our hydrogen station network in the U.S., as road freight is concentrated along the relatively few and significant corridors that form the National Highway Freight Network.

European Station Network Strategy

The European hydrogen station network will be built following a similar strategy. Several highly trafficked freight corridors exist in Europe, with logistics hubs in proximity to consumption centers, freight ports, and corridor crossroads. We plan to strategically deploy hydrogen stations along the key corridors and logistical hubs to maximize the efficiency of station deployment. Ultimate station roll-out strategy and timing will also consider potential local incentives offered in Europe to ensure the most economically favorable station roll-out. We believe that a network of 70 to 90 hydrogen stations will provide approximately 85% coverage of Western European freight corridors.

11

Power Sourcing Strategy, and Over Time, 100% Zero-Emission Goal

During our initial hydrogen station roll-out, we intend to source power based on the most economical power mix available at each hydrogen production site. Over time, our goal is to support each fueling station with 100% zero-emission power, whenever feasible.

Our energy business unit has established a strong team with deep energy industry experience, to provide focus and expertise in the key areas required to establish a comprehensive, low cost, safe, reliable and efficient hydrogen delivery system to our customers.

In January 2021, we secured approval of an innovative electricity rate schedule with Arizona Public Service Company (APS), which accelerates our goal to develop and provide hydrogen fuel at price parity with diesel to the commercial transportation industry. By facilitating low-cost production of hydrogen, the Arizona Corporation Commission’s approval of this rate schedule paves the way for the curtailment of GHG in the transportation sector, while also providing benefits to key constituents via novel grid-balancing solutions.

We believe APS’s competitive electric rate will help lead the creation of the hydrogen economy in Arizona. We estimate that under the rate structure, we will be able to deliver hydrogen at market leading prices and within the ranges required for us to offer competitive lease rates for our trucks customers.

Playing a Key Role in The Future of Energy Generation and Storage

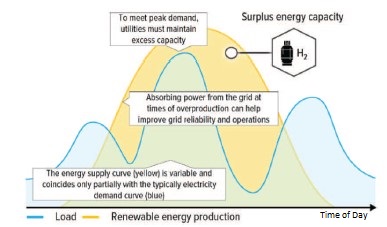

The steady off-peak demand load of our hydrogen stations, and our ability to have our power supply temporarily interrupted during peak power demand, makes us a highly attractive customer for utilities, grid operators and other power providers. Our station model also provides the critical advantage of being able to take excess power generated during periods of low power demand. Given this power demand profile, and our ability to help optimize the energy grid, we believe we will have the opportunity to source power at prices below prevailing market rates.

Given our ability to level out demand and store night-time and other off-peak energy that might otherwise go unused, we believe our hydrogen strategy will provide critical solutions to the future of electric energy generation, transmission, and storage and help usher in the next generation of power supply.

Service, Maintenance, and Parts

Our proposed bundled lease includes the required maintenance and parts for our Class 8 vehicles. Service and maintenance of an electric vehicle is expected to be lower than the traditional ICE vehicle which has been proven thus far in the electric passenger vehicle market as well as in early development of Class 7 and 8 trucks. Fewer moving parts, no emissions compliance requirements and considerably reduced complexity of certain key drivetrain components in our trucks should result in fewer breakdowns and less preventative maintenance. These factors should lead to better uptime, lower costs for operators, and positive feedback from drivers. The asset utilization, productivity, and reduced downtime should favorably impact fleet operating margins.

A key requirement for our fleet customers is knowing there is an available service infrastructure for the maintenance, repair, and availability of parts for our vehicles. We are building a strong network of maintenance providers, a robust preventative maintenance program, as well as several levels of service to support fleet complexity, application, and duty cycles.

We have assembled a nimble and adaptable service, maintenance, and parts solutions for our vehicles, which is expected to include the following options:

•Electric vehicles have a system of sensors and controls that allow for precise monitoring of the vehicle and component operation performance. We will use this data to provide smart predictive maintenance, which will decrease downtime and costs by identifying a potential problem before it results in a breakdown. Preventative maintenance will be customized to match duty cycle and fleet applications.

12

•We will have the ability to provide over the air updates and software fixes when the vehicles are stopped. This can significantly reduce the time for repair, improve uptime, and continually monitor performance, efficiency, and overall utilization.

•In cases where a customer has their own maintenance expertise and infrastructure, we will identify and provide certification of technicians and procedures for items that can be maintained at their shops. This could include procedures such as tire changes, wearable parts, chassis, and brake services.

•In cases where the customer does not have a maintenance infrastructure or for more complex items, we plan to utilize a dealer network for maintenance and warranty work. The network will monitor day to day trip activity and incorporate support at the origin and destination for our truck routes. We also intend to support our partners with the latest diagnostic technologies like augmented reality and web-enabled video to support technicians for complex tasks or newly identified issues.

•If a vehicle requires maintenance of a complex system or component such as the fuel cell, e-axle, or battery-pack, some of those items can be removed and replaced with limited downtime. This will allow us to repair the downed component in the background and minimize vehicle downtime. We are also planning to develop a network of trained technicians that can travel to a customer or service partner as necessary. We also expect to have dedicated vendor agreements to service and maintain a specific fleet on premises or very close in proximity to the truck's domicile location.

•Additionally, we will procure replacement parts, components, and all aftermarket support supplies. These components and materials will be inventoried, warehoused and distributed by third party logistic providers currently engaged in supplying the Class 8 truck industry.

Customers and Reservations

Target Customers

We target large Class 8 fleet customers with established sustainability goals, as well as fleets operating along dedicated routes that are located in regions offering strong incentives for developing hydrogen infrastructure and/or delivering zero-emission vehicles.

BEV Customer Strategy

The BEV truck is designed for short and medium-haul applications, making it ideal for urban metro, inner-city, local delivery, port operations, and drayage applications. Our goal is to first target large corporate customers to establish early market share and strengthen brand identity.

For BEVs, we expect that some early U.S. sales will be in states such as California or New York where incentive programs already exist.

FCEV Customer Strategy

For the FCEV truck, we are planning to develop and construct initial hydrogen stations in Arizona and California. Therefore, early customers will likely be located in these states, or have extensive transportation routes within or between them.

We will also target dedicated fleets with either nationwide or significant regional distribution networks and dedicated route networks (i.e., where trucks operate between two fixed points, e.g., production plant and distribution hub) along highly trafficked freight corridors. This strategy allows for gradual, strategic, and capital-efficient development of the hydrogen infrastructure required to support FCEV trucks in operation. We will expand the FCEV offering to the entire Class 8 truck market once the fueling infrastructure is sufficiently developed.

13

Customer Reservations

Our list of FCEV non-binding reservations potentially represents more than two years of production. The FCEV reservation book was frozen in the fall of 2019 in order for us to focus on negotiating with strategic fleet partners to convert pre-orders to binding contracts with deposits for initial FCEV roll out. We do not hold deposits related to the FCEV orderbook. We intend to convert a significant portion of the existing reservations into binding orders, once we have fixed production dates for FCEV trucks. We will likely require a significant deposit to secure binding orders at least six months prior to delivery.

We are working to select our initial BEV customers strategically and are in dialogue with several customers. We expect to select one or two launch customers to participate in fleet testing and the initial production of the BEV truck.

First Ever Zero-Emission Beer Run

In November 2019, we completed AB's first ever zero-emissions beer-run. The Nikola Two prototype FCEV delivered six pallets of Bud Light weighing approximately 15,000 pounds. The total load hauled, including the trailer, was approximately 27,000 pounds. The delivery was made on city streets where the beer was delivered to one of AB's distributors. The distributor then delivered the beer to the St. Louis Blues arena for consumption at that night's game.

Partnerships and Suppliers

Our business model is validated and supported by world-class strategic partnerships that significantly reduce execution risk, improve commercialization timeline, and provide a long-term competitive advantage. These world-class partners have accelerated our internal development, growth, and learning and have positioned us to revolutionize the transportation sector. We believe our partnerships help increase the depth and breadth of our competitive advantage as well.

Our partnership philosophy is a recognition that the world's toughest challenges require bold solutions and a collaborative effort from multiple parties. Our goal is to provide zero-emission solutions to the transportation sector and to usher in next-generation grid solutions. With the help of our partners, we believe our chances of success are greatly improved. We are inspired by the knowledge that if we are successful, the whole world wins.

The following is a list of the partners who have chosen to embark upon this journey with us. With their help, we plan to drive out emissions from the transportation sector.

Co-Development Partners

Iveco

Iveco is a subsidiary of CNH Industrial, which designs, manufactures and distributes under the Iveco brand a wide range of light, medium and heavy commercial vehicles and off-road trucks with over 163,000 units sold in 2019. Iveco with its affiliates and joint ventures has significant manufacturing presence in Europe, as well as production facilities in Asia, Africa and Latin America, where it produces vehicles equipped with the latest technologies. Iveco can provide technical support in close proximity to their customers, the world over. Iveco is the European market leader in CNG/LNG alternative propulsion technologies for trucks.

During fiscal year 2019, we entered into an agreement with Iveco under which it will provide advisory services, including project coordination, drawings and documentation support, engineering support, vehicle integration, product validation support, purchasing, and the implementation of the Iveco World Class Manufacturing Methodology.

Iveco and its affiliate, FPT Industrial, S.p.A., will provide engineering and manufacturing expertise to industrialize our BEV and FCEV trucks. In Europe, we established a joint venture with Iveco, and together, we are jointly developing cab-over BEV and FCEV trucks for sale in the European market. In North America, we will be responsible for manufacturing and production at our greenfield facility in Coolidge, Arizona.

14

•North America Engineering and Production Alliance: Iveco agreed to provide $100.0 million of engineering and production support and access to intellectual property valued at $50.0 million to help bring our trucks to the North American market. This alliance significantly de-risks our operational execution by leveraging the expertise and capabilities of one of the world's leading commercial vehicle manufacturers, and we retain 100% of the North American business as a result.

•Europe Joint Venture: Our 50/50 joint venture with Iveco will leverage Iveco's engineering expertise and existing production and sales/service footprint. This joint venture allows us to accelerate penetration into the attractive European market while minimizing execution risk and optimizing capital allocation and our management bandwidth.

In addition to the manufacturing and production expertise, one of the key benefits of this partnership is our ability to leverage Iveco's existing assortment of parts, thereby decreasing our purchasing expenses, and accelerate the vehicle validation process.

Bosch

Bosch is a leading global supplier of technology and services to automotive, industrial, energy, building technology, and consumer end-markets with approximately 394,500 employees and sales of approximately 71.6 billion euros in 2020.

Working with Bosch, we have re-imagined the commercial vehicle powertrain from the ground up. Bosch will supply their latest design rotors and stators for our electric truck e-axles as well as state-of-the-art inverters. We are also working with Bosch on the fuel cell assembly utilizing Bosch components.

Other Key Industry Partners and Suppliers

Hanwha

Hanwha is a world leader in renewable energy and solar panel manufacturing and is partnering with us to assist in obtaining clean energy for our hydrogen fueling network. Hanwha Q Cells is our exclusive solar panel provider (to third-party solar farm developers), which will help generate the clean electricity that is critical to the production of renewable hydrogen.

Nel

We have partnered with Nel for the build out of our on-site gaseous hydrogen production and fuel dispensing stations. Nel is an industry leader in the manufacturing of electrolyzers.

Romeo Power

Romeo is an energy storage technology company focused on designing and manufacturing lithium-ion battery modules and packs for commercial electric vehicles. Romeo provides us with battery modules for the battery pack designed by Nikola and integrated into our trucks.

EDAG

EDAG is a global engineering service provider to the commercial vehicle industry. EDAG provides support for our cab and chassis engineering services.

WABCO

WABCO is a leading global supplier of braking control components and air management systems to medium- and heavy-duty trucks. WABCO provides us with industry-leading safety technologies including electronic braking systems, as well as traction and stability control technologies.

15

MAHLE

Mahle is a leading global supplier of thermal management systems for heavy-duty trucks. Mahle provides us with industry leading thermal management system technologies.

Manufacturing and Production

Leveraging Iveco's Capacity for Initial Units

We plan to produce and sell BEV and FCEV trucks in North America and Europe. Our joint venture with Iveco provides us with manufacturing capacity to build trucks for the North American market before the completion of our planned manufacturing plant in Coolidge, Arizona. During the fourth quarter of 2020, we made significant progress at our joint venture manufacturing facility on Iveco’s campus in Ulm, Germany. The building dismantling and building refurbishment, including the civil works (floor, heating, system, and walls), have been completed. The assembly of the customized Automatic Guided Vehicle Systems (AGVs) has begun and is on pace to begin onsite installation in March 2021. The crane and subgroup infrastructure has also been installed and is on track for completion by the end of February 2021. The logistics warehouse, internal logistics, end of line, finishing, enterprise resource planning system implementation, and the ordering and installation of tools and equipment are all on pace for completion by the end of May 2021, with trial production set to begin in June 2021.

We have also completed assembling the first five BEV prototype trucks at the Ulm, Germany facility and will assemble the next nine in the first half of 2021. In the second half of 2021, we expect to begin production of the BEV truck for North America delivery at the joint venture manufacturing facility. These first trucks will be imported into North America to fulfill launch customer orders. We also plan to build both the BEV and FCEV trucks for the European market in Iveco's Ulm, Germany facility.

U.S. Production Facility

In 2019, we acquired an approximately 400-acre parcel of real property in Coolidge, Arizona, which is located about 50 miles south of Phoenix, Arizona. We believe the parcel is well suited for our planned greenfield manufacturing facility due to its proximity to the Interstate 10 highway, the Interstate 8 highway, and a railway spur that abuts the parcel.

In July 2020, we broke ground on phase one of the U.S. manufacturing facility in Coolidge, Arizona. In a benchmark example of cooperation and collaboration between us, the City of Coolidge, Pinal County, and our general contractor, Walbridge, the facility’s master site plan has been completed, submitted, and approved by the City of Coolidge. Currently, the construction of the assembly shop is on track to be completed towards the end of 2021.

Based on our current rate of construction, we have decided to advance our truck build plan and have scheduled production trials starting second half of 2021. The full completion of the assembly shop will continue through 2021, followed by a ramp up to a full production volume.

At the end of December 2020, we celebrated our first steel column erection, and will continue to build out the steel structure through the end of February 2021. The underground utility work is ongoing, as is the roof installation. The civil work to support our manufacturing equipment has started and is expected to continue until May 2021. All work is proceeding as planned and scheduled.

Manufacturing equipment is ordered and either in fabrication or en route for installation.

In January 2021, we entered into a master utility agreement with Global Water Resources, Inc., a pure-play water resource management company, to provide water and wastewater services to our manufacturing plant in Coolidge, Arizona. This agreement helps with our goal of creating the smallest environmental footprint possible in the design and construction of our manufacturing site. The engagement of Global Water reflects a shared commitment to a sustainable future for Arizona and beyond.

Our production targets include:

16

Phase 1—Low Volume Production—up to 5,000 units per year:

•Warehouse space (approximately 100,000 - 150,000 square feet)

•Low-volume production capacity (approximately 5,000 units per year)

•Trial production to begin in the second half of 2021

•Expect to complete construction by the end of 2021

•Expect commissioning and start-up with the BEV truck in production in the first quarter of 2022

Phase 2—High Volume Production—up to 30,000 units per year:

•Expect to begin construction early-2021

•Expect to complete manufacturing facility (approximately 1,000,000 square feet)

•High-volume production capacity (approximately 30,000 units per year)

•Expect to complete construction by the end of 2022

•Expect commissioning and start-up with Nikola Two FCEV in production in the second half of 2023

European Production

We expect to utilize Iveco's excess capacity for the foreseeable future, giving us the ability to produce 10,000 units per year. The joint venture may seek to build a greenfield manufacturing facility, once we have sufficient hydrogen station network density in Europe to facilitate sales over 10,000 units per year. We anticipate national and local grants and loan support may be available to help fund a greenfield development in Europe.

Development Timeline

The development timeline for our trucks has accelerated upon entering a production alliance with Iveco. This partnership provides us the benefit of leveraging Iveco's expertise, and the Class 8 S-WAY truck platform in the design, development, testing and validation of the BEV truck. By focusing initial development efforts on the BEV truck, we were able to accelerate our go-to-market strategy by approximately 1-2 years.

BEV Development

During the fourth quarter of 2020, we completed the assembly of the first five prototype Nikola Tre BEVs. All trucks are in the commissioning process and are ramping up to full speed, torque, and payload hauling capacity as part of our level two software release and vehicle validation process. Four trucks are in North America undergoing powertrain, durability, and extreme weather testing. One truck remains in Europe for ABS braking, traction control, and electronic stability control testing. We have started assembling the next nine prototype trucks at the Ulm, Germany facility.

Upcoming key milestones in the commercialization of the Nikola Tre BEV truck are as follows:

•Start of trial production at Iveco's facility in Ulm, Germany in the second quarter of 2021

•Start of trial production at our facility in Coolidge, Arizona in the second half of 2021

FCEV Development

Key milestones in the commercialization of the Nikola Tre FCEV (North America) trucks are as follows:

•Nikola Tre FCEV start of alpha builds in Coolidge, Arizona and Ulm, Germany in the second quarter of 2021

17

•Testing of Nikola Tre alpha trucks in the U.S. in the fourth quarter of 2021

•Alpha customer fleet and on-road validation in the second quarter of 2022

•Testing of beta trucks in U.S. in the third quarter of 2022

•Beta customer fleet and on-road validation and mile accumulation in the fourth quarter of 2022

•Start of production in Coolidge, Arizona for sale into North American market in the second half of 2023

Key milestones in the commercialization of the Nikola Two FCEV (North America) is as follows:

•Alpha customer fleet and on-road validation and mile accumulation in the fourth quarter of 2022

•Beta customer fleet and on-road validation and mile accumulation in the fourth quarter of 2023

•Start of production in Coolidge, Arizona for sale into the North American market in the second half of 2024

Key milestones in the commercialization of the Nikola Tre FCEV (Europe) is as follows:

•Nikola Tre FCEV start of production at Iveco's facility in Ulm, Germany for sale into the European market in 2024

Strategy

Management Team Focused on Execution and Efficient Capital Allocation

Given the capital-intensive nature of our business model, we recognize efficient capital allocation will be an important determinant of our long-term success. We believe our disciplined and creative approach to optimize capital allocation will allow us to execute on our ambitious business plan.

Capital optimization measures include:

•Our strategic partnerships with world-class automotive suppliers to develop leading next-generation powertrain technology. Our ability to leverage expertise from OEM and top-tier supplier brands has allowed us to accelerate the production of our product portfolio while minimizing development cost. Our joint venture with Iveco allows us to manufacture trucks, gain market share, and start generating revenue prior to building a greenfield manufacturing facility by utilizing Iveco's excess capacity.

•Our strategy to build our manufacturing facility in two phases. Our multi-phased approach to building our greenfield production plant in the U.S. allows us to produce up to approximately 5,000 units a year and allows us to generate revenue one full year before the completion of our fully scaled manufacturing facility.

•Our hydrogen station roll-out plan. Our unique hydrogen station roll-out plan allows us to build stations in coordination with FCEV truck deliveries, providing us with revenue and cash flow, which can be used to minimize the amount of outside capital needed during the buildout of our hydrogen station network.

Capture Early Mover Advantage

Given the speed at which the BEV and FCEV truck market is transforming, we have accelerated the production of our BEV truck to be early to market and we expect to generate revenue by late 2021. By being one of the first movers in the North American market, we expect to capture customers and any applicable zero-emission vehicle related incentives, including incentives available to those that are early adopters of BEV technology.

18

Maintain Strategic Partnership Focus to Drive Execution

Our position as a pioneer in the market has attracted global leaders across our supply chain, creating an extensive network for us to leverage. Our key partners include Iveco, Bosch, Romeo, WABCO, EDAG, Mahle, Nel, Hanwha, and others. We believe the expertise and know-how of these partners broaden our executional capability, reduce time to market, and solidify our technological leadership. In addition, these leading suppliers and partners will also allow us to manufacture and deliver our products with high quality standards. For example, our partnership with Iveco provides us with flexibility, scalability, and speed to market, while product design, supply chain management, and quality control are managed by our engineering team. Additionally, this partnership has allowed us to enter the European market in a capital efficient manner, and years earlier than we originally anticipated. By entering into strategic partnerships, we can reduce execution risk and increase speed to market, which provides a critical advantage as we look to execute upon our vision.

Leverage Hydrogen Station Dynamics to Transition Energy Future

We believe that the hydrogen station network, and the production and distribution of hydrogen, will provide a competitive advantage that drives sustained profitability and stockholder value over the long term. We believe that hydrogen-powered Class 8 trucks will be the product of choice in the medium- and long-haul markets. As OEMs begin to widely adopt hydrogen fuel cell technology, and there will be a greater need for hydrogen distribution along key transportation routes, we expect to be in a strong position to be the leading provider of hydrogen to commercial transportation companies. By enabling the world's leading heavy-duty hydrogen station network, we anticipate playing a major role in the energy transformation of the future.

Continued Focus on Technological Innovations

We intend to continue to attract top talent to further enhance our talent pool and drive technological innovations. Additionally, we plan to further enhance our battery and fuel cell related technology to achieve better performance and shorten charging and fueling time, while increasing the range of our product portfolio.

Future Market Opportunities

Autonomous Driving

Our trucks can be designed with autonomous driving in mind, which may provide revenue to us in the future as well as potential cost savings to customers. Given the nature of our dedicated route customers, operating point-to-point interstate routes between our hydrogen stations, we believe our trucks provide the perfect testing environment for further development and advancement of autonomous technology. When the various regulatory agencies have approved some level of autonomy, we will consider a partnership with one of the autonomous software leaders to deploy its technology on our vehicles.

Autonomous driving represents significant incremental revenue opportunities for us as we could charge customers an additional fee for each mile driven autonomously. According to the U.S. Federal Motor Carrier Safety Association, in the U.S., truck drivers face total hours restrictions that do not allow them to operate their vehicles more than 11 hours a day. In Europe, drivers are generally restricted to 9 hours a day, according to the European Parliament. Autonomous driving will help achieve higher utilization by removing the limitations on how long a truck driver can operate.

In addition to the incremental revenue opportunity for us and the potential cost savings available to fleet operators as a result of autonomous technology, we believe autonomy will significantly improve safety and asset utilization which would increase the revenue generating potential for both us and our customers.

Energy Optimization

The global energy mix is in transition with more than 60% of new capacity coming from renewable energy sources, based on the Global Market Outlook for Solar Power provided by SolarPower Europe. The transition away from fossil fuel-based energy generation, such as coal, natural gas, etc., is beneficial to the environment, but is not without its challenges. As renewable energy makes up a greater share of the energy mix, daily energy production becomes more volatile, and the energy production curve becomes less predictable.

19

With fossil-fuel based energy, demand peaks are typically addressed by burning natural gas in turbine-based power plants. With certain types of renewable energy, one does not have similar control over energy production, and instead the production curve is determined based on the daily solar cycle and weather patterns, which means daily energy production becomes more volatile. This increased volatility creates a distorted energy production curve, resulting in both predictable (e.g., the sun comes out every day) and unpredictable (e.g., the wind blows stronger on some days compared to others) surplus energy production capacity. This surplus energy typically goes unused, and in extreme cases must be traded away at zero or even negative revenue to the utility provider.

Hydrogen production can be used to balance the grid by taking excess energy production and storing it for future use. We can also help balance the grid by allowing utilities and power providers to interrupt hydrogen station electricity consumption during peak demand. Our ability to turn excess energy into hydrogen may offer operators and energy providers the ability to increase revenue by selling us otherwise wasted off-peak generating capacity. Additionally, the ability to store unused energy in the form of hydrogen reduces the need for peak power generating plants that are typically costly to build and operate, and that historically are heavily underutilized. Instead, we could potentially build excess hydrogen storage on-site, then sell excess hydrogen back to the grid during periods of peak demand.

20

Sales and Marketing

We take an insight-driven, strategic approach to our go-to-market strategy. Across the product portfolio, we are commissioning studies, conducting focus groups and gaining insight intended to focus sales and marketing efforts in a customer and partner-centric way and grounded on a foundation of zero-emissions. Our primary brand awareness is generated through traditional and social media.

Research and Development

Our research and development activities take place out of our headquarters facility in Phoenix, Arizona and at our development partners' facilities located around the world.

The primary areas of focus for research and development by us and our partners include, but are not limited to:

•fuel cell;

•battery pack and battery management systems, or BMS;

•vehicle controls;

•infotainment;

•e-axle and inverter;

•functional safety;

•energy storage; and

•hydrogen production, storage, and dispensing.

Most of our current activities are focused on the research and development of our BEV and FCEV trucks. We work closely with our partners, including without limitation, Iveco and Bosch to develop truck platforms and bring them to market.

We have purchased equipment that will aid in the development, validation and testing of our powertrain, battery and fuel cell related technology. We expect our research and development expenses to increase for the foreseeable future as we continue to invest in research and development activities to expand our product offering for both the North American and the European markets.

Intellectual Property

Our success depends in part upon our ability to protect our core technology and intellectual property. We protect our intellectual property rights, both in the U.S. and abroad, through a combination of patent, trademark, copyright and trade secret protection, as well as confidentiality and invention assignment agreements with our employees and consultants. We seek to control access to, and distribution of, our proprietary information through non-disclosure agreements with our vendors and business partners. Unpatented research, development, know-how, and engineering skills make a vital contribution to our business, and we pursue patent protection when we believe it is possible and consistent with our overall strategy for safeguarding intellectual property.

As of December 31, 2020, we own or co-own approximately 20 issued U.S. utility patents, 9 issued U.S. design patents, 16 issued foreign patents and 52 pending or allowed foreign and U.S. patent applications. In addition, we have approximately 2 registered U.S. trademarks, 18 registered foreign trademarks, 35 pending U.S. trademark applications, and 12 pending foreign trademark applications. Our patents and patent applications are directed to, among other things, vehicle and vehicle powertrain (including battery and fuel cell technology), hydrogen fueling, off-road vehicle, and personal watercraft technologies.

21

Headquarters and R&D Facility

In June 2019, we moved into our headquarters and R&D facility in Phoenix, Arizona, which consists of more than 150,000 square feet and where we are capable of designing, building, and testing prototype vehicles in-house.

Our People

Overview