UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____ to ____

Commission file number 001-38477

BIGLARI HOLDINGS INC.

(Exact name of registrant as specified in its charter)

| INDIANA | 82-3784946 | |

| (State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) |

|

17802 IH 10 West, Suite 400 San Antonio, Texas |

78257 | |

| (Address of principal executive offices) | (Zip Code) |

(210) 344-3400

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbols | Name of each exchange on which registered |

|

Class A Common Stock, no par value Class B Common Stock, no par value |

BH.A BH |

New York Stock Exchange New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer x | Non-accelerated filer o | Smaller reporting company o | Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of June 30, 2019 was approximately $137,552,014.

Number of shares of common stock outstanding as of February 17, 2020:

| Class A common stock – | 206,864 | |

| Class B common stock – | 2,068,640 |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement to be filed for its 2020 Annual Meeting of Shareholders are incorporated by reference into Part III of this Form 10-K.

|

Business |

Biglari Holdings Inc. is a holding company owning subsidiaries engaged in a number of diverse business activities, including property and casualty insurance, media and licensing, restaurants, and oil and gas. The Company’s largest operating subsidiaries are involved in the franchising and operating of restaurants. Biglari Holdings is founded and led by Sardar Biglari, Chairman and Chief Executive Officer of the Company. The Company’s long-term objective is to maximize per-share intrinsic value. All major investment and capital allocation decisions are made for the Company and its subsidiaries by Mr. Biglari.

As of December 31, 2019, Mr. Biglari’s beneficial ownership was approximately 64.4% of the Company’s outstanding Class A common stock and 55.4% of the Company’s outstanding Class B common stock.

Restaurant Operations

The Company’s restaurant operations are conducted through two subsidiaries: Steak n Shake Inc. (“Steak n Shake”) and Western Sizzlin Corporation (“Western Sizzlin”). As of December 31, 2019, Steak n Shake had 368 company-operated restaurants, 29 franchise partner units, and 213 traditional franchise units. As of December 31, 2019, 107 of the company-operated restaurants were temporarily closed. We anticipate re-opening the temporarily closed stores as counter service units. Western Sizzlin had 4 company-operated restaurants and 48 franchise units.

Steak n Shake is engaged in the ownership, operation, and franchising of Steak n Shake restaurants. Founded in 1934 in Normal, Illinois, Steak n Shake is a classic American brand serving premium burgers and milkshakes. Steak n Shake is headquartered in Indianapolis, Indiana.

Western Sizzlin is engaged primarily in the franchising of restaurants. Founded in 1962 in Augusta, Georgia, Western Sizzlin offers signature steak dishes as well as other classic American menu items. Western Sizzlin also operates two other concepts: Great American Steak & Buffet, and Wood Grill Buffet. Western Sizzlin is headquartered in Roanoke, Virginia.

Operations

A typical company-operated restaurant management team consists of a general manager, a restaurant manager and other managers depending on the operating complexity and sales volume of the restaurant. Each restaurant’s general manager has primary responsibility for the day-to-day operations of his or her unit. Restaurant operations obtain food products and supplies from independent national distributors. Purchases are centrally negotiated to ensure uniformity in product quality.

Franchising

Restaurant operations’ traditional franchising program extends the brands to areas in which there are no current development plans for company stores. The expansion plans include seeking qualified new franchisees and expanding relationships with current franchisees. Restaurant operations typically seek franchisees with both the financial resources necessary to fund successful development and significant experience in the restaurant/retail business. Both restaurant chains assist franchisees with the development and ongoing operation of their restaurants. In addition, personnel assist franchisees with site selection, approve restaurant sites, and provide prototype plans, construction support, and specifications. Restaurant operations’ staff provides both on-site and off-site instruction to franchise restaurant management and associates.

In addition to the traditional franchise arrangements described above, Steak n Shake initiated a franchise partner program during 2018 to transition company-operated restaurants to franchise partnerships. The franchise agreement stipulates that the franchisee make an upfront investment totaling $10,000. Steak n Shake, as the franchisor, assesses a fee of up to 15% of sales as well as 50% of profits. Potential franchise partners are screened based on entrepreneurial attitude and ability, but they become franchise partners based on achievement. Each must meet the gold standard in service. Franchise partners are required to be hands-on operators, limited to a single location.

International

We have a corporate office in Monaco and an international organization with personnel in various functions to support our international business. As of December 31, 2019, we operated three company locations in Europe to promote the Steak n Shake brand to prospective franchisees. Similar to our traditional domestic franchise agreements, a typical international franchise development agreement includes development and franchise fees in addition to subsequent royalty fees based on the gross sales of each restaurant. As of December 31, 2019, there were a total of 31 franchise units in Europe and the Middle East.

1

Competition

The restaurant business is one of the most intensely competitive industries. As there are virtually no barriers to entry into the restaurant business, competitors may include national, regional and local establishments. There may be established competitors with financial and other resources that are greater than the Company’s restaurant operations capabilities. Restaurant businesses compete on the basis of price, menu, food quality, location, and customer service. The restaurant business is often affected by changes in consumer tastes and by national, regional, and local economic conditions. The performance of individual restaurants may be impacted by factors such as traffic patterns, demographic trends, weather conditions, and competing restaurants.

Government regulations

The Company is subject to various global, federal, state and local laws affecting its restaurant operations. Each of the restaurants must comply with licensing and regulation by a number of governmental authorities, i.e., health, sanitation, safety and fire agencies in the jurisdiction in which the restaurant is located. Various federal and state labor laws govern our relationship with our employees, e.g., minimum wage, overtime pay, unemployment tax, health insurance, and workers’ compensation. Federal state and local government agencies have established regulations requiring that we disclose nutritional information. To date, none of the Company’s restaurant operations have been materially adversely affected by such laws or been affected by any difficulty, delay or failure to obtain required licenses or approvals.

Trademark and licenses

The name and reputation of Steak n Shake is a material asset and management protects it and other service marks through appropriate registrations.

Insurance Business

Our insurance business is composed of First Guard Insurance Company and its agency, 1st Guard Corporation (collectively “First Guard”). First Guard is a direct underwriter of commercial truck insurance, selling physical damage and nontrucking liability insurance to truckers. First Guard is headquartered in Venice, Florida.

First Guard competes for truck insurance with other companies. The commercial truck insurance business is highly competitive in the areas of price and service. Vigorous competition is provided by large, well-capitalized companies and by small regional insurers. First Guard’s insurance products are marketed primarily through direct response methods via the Internet or by telephone. First Guard’s cost-efficient direct response marketing methods enable it to be a low-cost truck insurer. First Guard uses its own claim staff to manage claims. Seasonal variations in First Guard’s insurance business are not significant. However, extraordinary weather conditions or other factors may have a significant effect upon the frequency or severity of claims.

The insurance business is stringently regulated by state insurance departments. First Guard operates under licenses issued by various insurance authorities. Such supervision and regulation include matters relating to authorized lines of business, capital and surplus requirements, licensing of insurers, investments, the filing of annual and other financial reports prepared on the basis of Statutory Accounting Principles, the filing and form of actuarial reports, dividends, and a variety of other financial and non-financial matters.

Oil and Gas Business

On September 9, 2019, a wholly-owned subsidiary of the Company, Southern Oil Company, acquired the stock of Southern Oil of Louisiana Inc. (collectively “Southern Oil”). Southern Oil primarily operates oil and natural gas properties offshore in the shallow waters of the Gulf of Mexico. Southern Oil is headquartered in Metairie, Louisiana.

The oil and gas industry is fundamentally a commodity business. Southern Oil’s operations and earnings, therefore, may be significantly affected by changes in oil and natural gas prices. Southern Oil competes with fully integrated, major global petroleum companies, as well as independent and national petroleum companies. In addition, the company is subject to a variety of risks inherent in the oil and gas businesses, including a wide range of local, state, and federal regulations.

Media and Licensing Business

Maxim’s business lies principally in media and licensing. Maxim is headquartered in New York City, New York.

Maxim competes for licensing business with other companies. The nature of the licensing business is predicated on projects that materialize with irregularity. In addition, publishing is a highly competitive business. The Company's magazines and related publishing products and services compete with other mass media, including the Internet.

Maxim products are marketed under various registered brand names, including, but not limited to, “MAXIM®” and “Maxim®”.

2

Investments

The Company and its subsidiaries have invested in The Lion Fund, L.P. and The Lion Fund II, L.P. (collectively, “the investment partnerships”). The investment partnerships operate as private investment funds. As of December 31, 2019, the fair value of the investments was $666.1 million. These investments are subject to a rolling five-year lock-up period under the terms of the respective partnership agreements.

Employees

The Company employs 10,906 persons.

Additional information with respect to Biglari Holdings’ businesses

Information related to our reportable segments may be found in Part II, Item 8 of this Form 10-K.

Biglari Holdings maintains a website (www.biglariholdings.com) where its annual reports, press releases, interim shareholder reports and links to its subsidiaries’ websites can be found. Biglari Holdings’ periodic reports filed with the Securities and Exchange Commission (the “SEC”), which include Form 10-K, Form 10-Q, Form 8-K and amendments thereto, may be accessed by the public free of charge from the SEC and through Biglari Holdings’ website. In addition, corporate governance documents such as Corporate Governance Guidelines, Code of Conduct, Compensation Committee Charter and Audit Committee Charter are posted on the Company’s website and are available without charge upon written request. The Company’s website and the information contained therein or connected thereto are not intended to be incorporated into this report on Form 10-K.

|

Risk Factors |

Biglari Holdings and its subsidiaries (referred to herein as “we,” “us,” “our,” or similar expressions) are subject to certain risks and uncertainties in its business operations which are described below. The risks and uncertainties described below are not the only risks we face. Additional risks and uncertainties not presently known or that are currently deemed immaterial may also impair our business operations.

Risks relating to Biglari Holdings

We are dependent on our Chairman and CEO.

Our success depends on the services of Sardar Biglari, Chairman and Chief Executive Officer. All major investment and capital allocation decisions are made for the Company and its subsidiaries by Mr. Biglari. If for any reason the services of Mr. Biglari were to become unavailable, a material adverse effect on our business could occur.

Sardar Biglari, Chairman and CEO, beneficially owns over 50% of our outstanding shares of common stock, enabling Mr. Biglari to exert control over matters requiring shareholder approval.

Mr. Biglari has the ability to control the outcome of matters submitted to our shareholders for approval, including the election or removal of directors, the amendment of our certificate of incorporation or bylaws, along with other significant transactions. In addition, Mr. Biglari has the ability to control the management and affairs of the Company. This control position may conflict with the interests of some or all of the Company’s passive shareholders, and reduce the possibility of a merger proposal, tender offer or proxy contest for the removal of directors.

We are a “controlled company” within the meaning of the New York Stock Exchange rules and thus can rely on exemptions from certain corporate governance requirements.

Because Mr. Biglari beneficially owns more than 50% of the Company’s outstanding voting stock, we are considered a “controlled company” pursuant to New York Stock Exchange rules. As a result, we are not required to comply with certain director independence and board committee requirements. The Company does not have a governance and nominating committee.

Our historical growth rate is not indicative of our future growth.

When evaluating our historical growth and prospects for future growth, it is important to consider that while our business philosophy has remained constant our mix of business has changed and will continue to change. Our business model makes it difficult to assess our prospects for future growth.

3

Biglari Holdings’ access to capital is subject to restrictions that may adversely affect its ability to satisfy its cash requirements or implement its growth strategy.

We are a holding company and are largely dependent upon dividends and other sources of funds from our subsidiaries in order to meet our needs. Steak n Shake’s credit facility contains restrictions on its ability to pay dividends to Biglari Holdings. In addition, the ability of our insurance subsidiaries to pay dividends to Biglari Holdings is regulated by state insurance laws, which limit the amount of, and in certain circumstances may prohibit the payment of, cash dividends. Furthermore, as a result of our substantial investments in The Lion Fund, L.P. and The Lion Fund II, L.P., investment partnerships controlled by Mr. Biglari, our access to capital is restricted by the terms of their respective partnership agreements, as described more fully below. There is also a high likelihood that we will make additional investments in these investment partnerships. Taken together, these restrictions may result in our having insufficient funds to satisfy our cash requirements. As a result, we may need to look to other sources of capital which may be more expensive or may not be available.

Competition.

Each of our operating businesses faces intense competitive pressure within the markets in which they operate. Competition may arise domestically as well as internationally. Accordingly, future operating results will depend to some degree on whether our operating units are successful in protecting or enhancing their competitive advantages. If our operating businesses are unsuccessful in these efforts, our periodic operating results may decline from current levels in the future. We also highlight certain competitive risks in the sections below.

Unfavorable domestic and international economic, societal and political conditions could hurt our operating businesses.

To the extent that the economy worsens for a prolonged period of time, one or more of our significant operations could be materially harmed. In addition, our restaurant operations depend on having access to borrowed funds through the capital markets at reasonable rates. To the extent that access to credit is restricted or the cost of funding increases, our business could be adversely affected.

Our operating businesses face a variety of risks associated with doing business in foreign markets.

There is no assurance that our international operations will remain profitable. Our international operations are subject to all of the risks associated with our domestic operations, as well as a number of additional risks, varying substantially country by country. These include, inter alia, international economic and political conditions, corruption, terrorism, social and ethnic unrest, foreign currency fluctuations, differing cultures and consumer preferences.

In addition, we may become subject to foreign governmental regulations that impact the way we do business with our international franchisees and vendors. These include antitrust and tax requirements, anti-boycott regulations, international trade regulations, the USA Patriot Act, the Foreign Corrupt Practices Act, and applicable local law. Failure to comply with any such legal requirements could subject us to monetary liabilities and other sanctions, which could harm our business and our financial condition.

Potential changes in law or regulations may have a negative impact on our Class A common stock and Class B common stock.

In prior years, bills have been introduced in Congress that, if enacted, would have prohibited the listing of common stock on a national securities exchange if such common stock was part of a class of securities that has no voting rights or carries disproportionate voting rights. Although these bills have not been acted upon by Congress, there can be no assurance that such a bill (or a modified version thereof) will not be introduced in Congress in the future. Legislation or other regulatory developments could make the shares of Class A common stock and Class B common stock ineligible for trading on the NYSE or other national securities exchanges.

We may not be able to adequately protect our intellectual property, which could decrease the value of our brand and products.

The success of our business depends on the continued ability to use the existing trademarks, service marks, and other components of our brand to increase brand awareness and further develop branded products. While we take steps to protect our intellectual property, our rights to our trademarks could be challenged by third parties or our use of these trademarks may result in a liability for trademark infringement, trademark dilution, or unfair competition, adversely affecting our profitability. We may also become subject to these risks in the international markets in which we operate and in which we plan to expand. Any impairment of our intellectual property or brands, including due to changes in U.S. or foreign intellectual property laws or the absence of effective legal protections or enforcement measures, could adversely impact our business, financial condition and results of operations.

Litigation could have a material adverse effect on our financial position, cash flows and results of operations.

We are or may be from time to time a party to various legal actions, investigations and other proceedings brought by employees, consumers, policyholders, suppliers, shareholders, government agencies or other third parties in connection with matters pertaining to our business, including related to our investment activities. The outcome of such matters is often difficult to assess or quantify and the cost to defend future proceedings may be significant. Even if a claim is unsuccessful or is not fully pursued, the negative publicity surrounding any negative allegation regarding our Company, our business or our products could adversely affect our reputation. While we believe that the ultimate outcome of routine legal proceedings individually and in the aggregate will not have a material impact on our financial position, we cannot assure that an adverse outcome on, or reputational damage from, any of these matters would not, in fact, materially impact our business and results of operations for the period when these matters are completed or otherwise resolved.

4

Risks Relating to Our Restaurant Operations

Our restaurant operations face intense competition from a wide range of industry participants.

The restaurant business is one of the most competitive industries. As there are virtually no barriers to entry into the restaurant business, competitors may include national, regional and local establishments. There may be established competitors with financial and other resources that are greater than the Company’s restaurant operations capabilities. Restaurant businesses compete on the basis of price, menu, food quality, location, and customer service. The restaurant business is often affected by changes in consumer tastes and by national, regional, and local economic conditions. The performance of individual restaurants may be impacted by factors such as traffic patterns, demographic trends, weather conditions, and competing restaurants. Additional factors that may adversely affect the restaurant industry include, but are not limited to, food and wage inflation, safety, and food-borne illness.

Changes in economic conditions may have an adverse impact on our restaurant operations.

Our restaurant operations are subject to normal economic cycles affecting the economy in general or the restaurant industry in particular. The restaurant industry has been affected by economic factors, including the deterioration of global, national, regional and local economic conditions, declines in employment levels, and shifts in consumer spending patterns. Declines in consumer restaurant spending could be harmful to our financial position and results of operations. As a result, decreased cash flow generated from our business may adversely affect our financial position and our ability to fund our operations. In addition, macroeconomic disruptions could adversely impact the availability of financing for our franchisees’ expansions and operations.

Steak n Shake’s credit facility matures on March 19, 2021.

The term loan under Steak n Shake’s credit facility matures on March 19, 2021. As of December 31, 2019, $181,498 was outstanding. Biglari Holdings and other affiliates (other than Steak n Shake’s subsidiaries) do not guarantee any of the debt. Steak n Shake may need to seek additional financing, which may not be available on terms commensurate with its current financing arrangement. The inability to refinance the debt would negatively impact our operations and financial condition.

Our cash flows and financial position could be negatively impacted if we are unable to comply with the restrictions and covenants in Steak n Shake’s debt agreements.

Covenants in Steak n Shake’s credit facility include restrictions on, among other things, its ability to incur additional indebtedness and to make distributions to the Company. Steak n Shake’s ability to make payments on its credit facility and to fund operations depends on its ability to generate cash, which is subject to general economic, financial, competitive, regulatory and other factors that are beyond our control. Steak n Shake may not generate sufficient cash flow from operations to service this debt or to fund its other liquidity needs. Steak n Shake’s failure to service its debt could constitute an event of default that, if not cured or waived, could result, among other things, in the acceleration of their indebtedness, which would negatively impact our operations. However, neither the Company nor any of our affiliates (other than Steak n Shake’s subsidiaries) provide any guarantees of Steak n Shake’s indebtedness.

Steak n Shake’s re-opening of temporarily closed stores may not be successful in reversing its declining sales or profitability.

Since 2017, Steak n Shake has experienced declining sales and profitability. As of December 31, 2019, a total of 107 Steak n Shake restaurants were temporarily closed. Steak n Shake is actively working to re-open these stores as counter service units. There are no assurances that Steak n Shake will be able to restore profitability after re-opening closed stores.

Fluctuations in commodity and energy prices and the availability of commodities, including beef and dairy, could affect our restaurant business.

The cost, availability and quality of ingredients restaurant operations use to prepare their food is subject to a range of factors, many of which are beyond their control. A significant component of our restaurant business’ costs is related to food commodities, including beef and dairy products, which can be subject to significant price fluctuations due to seasonal shifts, climate conditions, industry demand, changes in commodity markets, and other factors. If there is a substantial increase in prices for these food commodities, our results of operations may be negatively affected. In addition, our restaurants are dependent upon frequent deliveries of perishable food products that meet certain specifications. Shortages or interruptions in the supply of perishable food products caused by unanticipated demand, problems in production or distribution, disease or food-borne illnesses, inclement weather, or other conditions could adversely affect the availability, quality, and cost of ingredients, which would likely lower revenues, damage our reputation, or otherwise harm our business.

5

Adverse weather conditions or losses due to casualties could negatively impact our operating performance.

Property damage caused by casualties and natural disasters, instances of inclement weather, flooding, hurricanes, fire, and other acts of nature can adversely impact sales in several ways. Many of Steak n Shake’s and Western Sizzlin’s restaurants are located in the Midwest and Southeast portions of the United States. During the first and fourth quarters, restaurants in the Midwest may face harsh winter weather conditions. During the third and fourth quarters, restaurants in the Southeast may experience hurricanes or tropical storms. Our sales and operating results may be negatively affected by these harsh weather conditions, which could make it more difficult for guests to visit our restaurants, necessitate the closure of restaurants, cause physical damage, or lead to a shortage of employees.

We are subject to health, employment, environmental, and other government regulations, and failure to comply with existing or future government regulations could expose us to litigation or penalties, damage our reputation, and lower profits.

We are subject to various global, federal, state, and local laws and regulations affecting our restaurant operations. Changes in existing laws, rules and regulations applicable to us, or increased enforcement by governmental authorities, may require us to incur additional costs and expenses necessary for compliance. If we fail to comply with any of these laws, we may be subject to governmental action or litigation, and our reputation could be accordingly harmed. Injury to our reputation would, in turn, likely reduce revenues and profits.

The development and construction of restaurants is subject to compliance with applicable zoning, land use, and environmental regulations. Difficulties in obtaining, or failure to obtain, the required licenses or approvals could delay or prevent the development of a new restaurant in a particular area.

In recent years, there has been increased legislative, regulatory, and consumer focus on nutrition and advertising practices in the food industry. As a result, restaurant operations have become subject to regulatory initiatives in the area of nutrition disclosure or advertising, such as requirements to provide information about the nutritional content of our food products. The operation of the Steak n Shake and Western Sizzlin franchise system is also subject to franchise laws and regulations enacted by a number of states, and to rules promulgated by the U.S. Federal Trade Commission. Any future legislation regulating franchise relationships may negatively affect our operations, particularly our relationship with franchisees. Failure to comply with new or existing franchise laws and regulations in any jurisdiction or to obtain required government approvals could result in a ban or temporary suspension on future franchise sales. Further national, state and local government initiatives, such as mandatory health insurance coverage, or proposed increases in minimum wage rates could adversely affect our business.

Risks Relating to Our Investment Activities

Our investment activities are conducted primarily through outside investment partnerships, The Lion Fund, L.P. and The Lion Fund II, L.P., which are controlled by Mr. Biglari.

Our investment activities are conducted mainly through these outside investment partnerships. Under the terms of their partnership agreements, each contribution made by the Company to the investment partnerships is subject to a five-year lock-up period, and any distribution upon our withdrawal of funds will be paid out over a two-year period (and may be paid in-kind rather than in cash, thus increasing the difficulty of liquidating these investments). As a result of these provisions and our consequent inability to access this capital for a defined period, our capital invested in the investment partnerships may be subject to an increased risk of loss of all or a significant portion of value, and we may become unable to meet our capital requirements. There is a high likelihood that we will make additional investments in these investment partnerships in the future.

We also have a services agreement with Biglari Capital Corp., the general partner of the investment partnerships (“Biglari Capital”), and Biglari Enterprises LLC (collectively, the “Biglari Entities”), in which the Company pays a fixed fee to the Biglari Entities for business and administrative-related services. The Biglari Entities are owned by Mr. Biglari. There can be no assurance that the fees paid will be commensurate with the benefits received.

The incentive allocation to which Mr. Biglari, as Chairman and Chief Executive Officer of Biglari Capital, is entitled under the terms of the respective partnership agreements is equal to 25% of the net profits allocated to the limited partners in excess of a 6% hurdle rate over the previous high-water mark.

Our investments are unusually concentrated and fair values are subject to a loss in value.

Our investments are predominantly held through the investment partnerships, which generally invest in common stocks. These investments are largely concentrated in the common stock of one investee, Cracker Barrel Old Country Store, Inc. A significant decline in the major values of these investments may produce a large decrease in our consolidated shareholders’ equity and can have a material adverse effect on our consolidated book value per share and earnings.

6

We are subject to the risk of possibly becoming an investment company under the Investment Company Act of 1940.

We run the risk of inadvertently becoming an investment company, which would require us to register under the Investment Company Act of 1940, as amended (the “Investment Company Act”). Registered investment companies are subject to extensive, restrictive and potentially adverse regulations relating to, among other things, operating methods, management, capital structure, dividends and transactions with affiliates. Registered investment companies are not permitted to operate their business in the manner in which we operate our business, nor are registered investment companies permitted to have many of the relationships that we have with our affiliated companies.

To avoid becoming and registering as an investment company under the Investment Company Act, we operate as an ongoing enterprise, with approximately 11,000 employees, along with an asset base from which to pursue acquisitions. Furthermore, Section 3(c)(3) of the Investment Company Act excludes insurance companies from the definition of “investment company”. Because we monitor the value of our investments and structure transactions accordingly, we may structure transactions in a less advantageous manner than if we did not have Investment Company Act concerns, or we may avoid otherwise economically desirable transactions due to those concerns. In addition, adverse developments with respect to our ownership of certain of our operating subsidiaries, including significant appreciation or depreciation in the market value of certain of our publicly traded holdings, could result in our inadvertently becoming an investment company. If it were established that we were an investment company, there would be a risk, among other material adverse consequences, that we could become subject to monetary penalties or injunctive relief, or both, in an action brought by the SEC, that we would be unable to enforce contracts with third parties or that third parties could seek to obtain rescission of transactions with us undertaken during the period it was established that we were an unregistered investment company.

Risks Relating to Our Insurance Business

Our success depends on our ability to underwrite risks accurately and to charge adequate rates to policyholders.

Our results of operations depend on our ability to underwrite and set rates accurately for risks assumed. A primary role of the pricing function is to ensure that rates are adequate to generate sufficient premiums to pay losses, loss adjustment expenses, and underwriting expenses.

Our insurance business is vulnerable to significant catastrophic property loss, which could have an adverse effect on its financial condition and results of operations.

Our insurance business faces a significant risk of loss in the ordinary course of its business for property damage resulting from natural disasters, man-made catastrophes and other catastrophic events. These events typically increase the frequency and severity of commercial property claims. Because catastrophic loss events are by their nature unpredictable, historical results of operations may not be indicative of future results of operations, and the occurrence of claims from catastrophic events may result in significant volatility in our insurance business’ financial condition and results of operations from period to period. We attempt to manage our exposure to these events through reinsurance programs, although there is no assurance we will be successful in doing so.

Our insurance business is subject to extensive existing state, local and foreign governmental regulations that restrict its ability to do business and generate revenues.

Our insurance business is subject to regulation in the jurisdictions in which it operates. These regulations may relate to, among other things, the types of business that can be written, the rates that can be charged for coverage, the level of capital and reserves that must be maintained, and restrictions on the types and size of investments that can be placed. Regulations may also restrict the timing and amount of dividend payments. Accordingly, existing or new regulations related to these or other matters or regulatory actions imposing restrictions on our insurance business may adversely impact its results of operations.

Risks Relating to Our Media and Licensing Business

Our media business faces significant competition from other magazine publishers and other forms of media, including digital media, and as a result our media business may not be able to improve its operating results.

Our media business competes principally with other magazine publishers. The proliferation of choices available to consumers for information and entertainment has resulted in audience fragmentation and has negatively impacted overall consumer demand for print magazines and intensified competition with other magazine publishers for share of print magazine readership. Our media business also competes with digital publishers and other forms of media. This competition has intensified as a result of the proliferation of mobile devices and the shift in consumer preference from print media to digital media for the delivery and consumption of content.

Competition among print magazine and digital publishers for advertising is primarily based on the circulation and readership of magazines and the number of visitors to websites, respectively, and the demographics of customers, advertising rates, plus the effectiveness of advertising sales teams. The proliferation of new platforms available to advertisers, combined with continuing competition from print platforms, has impacted both the amount of advertising our media business is able to sell and the rates it can command.

7

Our pursuit of licensing opportunities for the Maxim brand may prove to be unsuccessful.

Maxim’s success depends to a significant degree upon its ability to develop new licensing agreements to expand its brand. However, these licensing efforts may be unsuccessful. We may be unable to secure favorable terms for future licensing arrangements, which could lead to, among other things, disputes with licensing partners that hinder our ability to grow the Maxim brand. Future licensing partners may also fail to honor their contractual obligations or take other actions that can diminish the value of the Maxim brand. Disputes could also arise that prevent or delay our ability to collect licensing revenues under these arrangements. If any of these developments occur or our licensing efforts are otherwise not successful, the value and recognition of the Maxim brand, as well as the prospects of our media business, could be materially, adversely affected.

Our media business is exposed to risks associated with weak economic conditions.

Because magazines are generally discretionary purchases for consumers, circulation revenues are sensitive to general economic conditions and economic cycles. Certain economic conditions such as general economic downturns, including periods of increased inflation, unemployment levels, interest rates, gasoline and other energy prices, or declining consumer confidence, may negatively impact consumer spending. Reduced consumer spending or a shift in consumer spending patterns away from discretionary items will likely result in reduced demand for our media business’ magazines and may result in decreased revenues.

Risks Relating to Our Oil and Gas Business

Our oil and gas business is exposed to the effects of volatile commodity prices.

The single largest variable that affects Southern Oil’s results of operations is the price of crude oil and natural gas. The price we receive for our oil and natural gas production heavily influences Southern Oil’s revenue and profitability. Extended periods of low prices for crude oil or natural gas can have a material adverse impact on our results of operations.

Our scope of business is concentrated in the shallow waters of the Gulf of Mexico.

Any disruption of its extractive business would adversely affect Southern Oil’s revenues and profitability. Southern Oil’s operations are therefore subject to disruption from natural or human causes beyond its control, including physical risks from hurricanes, severe storms, and other forms of system failures, any of which could result in suspension of operations or harm to people or the natural environment.

Our oil and gas business can be adversely affected by political or regulatory developments affecting our operations.

Southern Oil’s operations can be affected by changing economic, regulatory and political environments. Litigation or changes in national, state, or local environmental regulations or laws, including those designed to stop or impede the development or production of oil and natural gas, could adversely affect Southern Oil’s operations and profitability.

| Item 1B. | Unresolved Staff Comments |

None.

8

| Item 2. | Properties |

Restaurant Properties

As of December 31, 2019, restaurant operations included 662 company-operated and franchise locations. Restaurant operations own the land and building for 152 restaurants. The following table lists the locations of the restaurants, as of December 31, 2019.

| Steak n Shake | Western Sizzlin | |||||||||||||||||||||||

Company Operated | Franchise Partner | Traditional Franchise | Company Operated | Franchise | Total | |||||||||||||||||||

| Domestic: | ||||||||||||||||||||||||

| Alabama | 2 | — | 7 | — | 6 | 15 | ||||||||||||||||||

| Arizona | 1 | — | 1 | — | — | 2 | ||||||||||||||||||

| Arkansas | — | — | 7 | — | 13 | 20 | ||||||||||||||||||

| California | 1 | — | 7 | — | 1 | 9 | ||||||||||||||||||

| Colorado | 1 | — | 2 | — | — | 3 | ||||||||||||||||||

| Delaware | — | — | 1 | — | — | 1 | ||||||||||||||||||

| Florida | 71 | 9 | 7 | — | — | 87 | ||||||||||||||||||

| Georgia | 20 | 1 | 15 | — | 5 | 41 | ||||||||||||||||||

| Illinois | 57 | 2 | 10 | — | — | 69 | ||||||||||||||||||

| Indiana | 61 | 5 | 5 | — | — | 71 | ||||||||||||||||||

| Iowa | 3 | — | — | — | — | 3 | ||||||||||||||||||

| Kansas | — | — | 4 | — | — | 4 | ||||||||||||||||||

| Kentucky | 12 | 2 | 12 | — | — | 26 | ||||||||||||||||||

| Louisiana | — | — | 2 | — | — | 2 | ||||||||||||||||||

| Maryland | — | — | 1 | — | 1 | 2 | ||||||||||||||||||

| Michigan | 19 | — | — | — | — | 19 | ||||||||||||||||||

| Mississippi | — | — | 6 | — | 1 | 7 | ||||||||||||||||||

| Missouri | 31 | 2 | 23 | — | — | 56 | ||||||||||||||||||

| Nebraska | — | — | 1 | — | — | 1 | ||||||||||||||||||

| Nevada | — | — | 6 | — | — | 6 | ||||||||||||||||||

| North Carolina | 5 | 1 | 9 | — | 6 | 21 | ||||||||||||||||||

| Ohio | 55 | 2 | 3 | — | 1 | 61 | ||||||||||||||||||

| Oklahoma | — | — | 3 | — | 5 | 8 | ||||||||||||||||||

| Pennsylvania | 7 | — | 4 | — | — | 11 | ||||||||||||||||||

| South Carolina | 1 | — | 3 | — | 2 | 6 | ||||||||||||||||||

| Tennessee | 7 | 2 | 17 | — | 3 | 29 | ||||||||||||||||||

| Texas | 11 | 3 | 19 | — | 1 | 34 | ||||||||||||||||||

| Virginia | — | — | 2 | 3 | 3 | 8 | ||||||||||||||||||

| Washington | — | — | 1 | — | — | 1 | ||||||||||||||||||

| Washington DC | — | — | 1 | — | — | 1 | ||||||||||||||||||

| West Virginia | — | — | 3 | 1 | — | 4 | ||||||||||||||||||

| International: | ||||||||||||||||||||||||

| France | 2 | — | 23 | — | — | 25 | ||||||||||||||||||

| Italy | — | — | 1 | — | — | 1 | ||||||||||||||||||

| Portugal | — | — | 4 | — | — | 4 | ||||||||||||||||||

| Qatar | — | — | 1 | — | — | 1 | ||||||||||||||||||

| Saudi Arabia | — | — | 1 | — | — | 1 | ||||||||||||||||||

| Spain | 1 | — | 1 | — | — | 2 | ||||||||||||||||||

| Total | 368 | 29 | 213 | 4 | 48 | 662 | ||||||||||||||||||

As of December 31, 2019, 107 of the 368 Steak n Shake company-operated stores were temporarily closed. We anticipate re-opening the temporarily closed stores as counter service units.

Oil and Gas Properties

Southern Oil operates oil and natural gas wells in Texas and Louisiana. It’s operations are primarily offshore in the shallow waters of the Gulf of Mexico.

9

|

Legal Proceedings |

We are involved in various legal proceedings and have certain unresolved claims pending. We believe, based on examination of these matters and experiences to date, that the ultimate liability, if any, in excess of amounts already provided in our consolidated financial statements is not likely to have a material effect on our results of operations, financial position or cash flow.

On January 29, 2018, a shareholder of the Company filed a purported class action complaint against the Company and the members of our Board of Directors in the Superior Court of Hamilton County, Indiana. The shareholder generally alleges claims of breach of fiduciary duty by the members of our Board of Directors and unjust enrichment to Mr. Biglari as a result of the dual class structure.

On March 26, 2018, a shareholder of the Company filed a purported class action complaint against the Company and the members of our Board of Directors in the Superior Court of Hamilton County, Indiana. This shareholder generally alleges claims of breach of fiduciary duty by the members of our Board of Directors. This shareholder sought to enjoin the shareholder vote on April 26, 2018 to approve the dual class structure. On April 16, 2018, the shareholder withdrew their motion to enjoin the shareholder vote on April 26, 2018.

On May 17, 2018, the shareholders who filed the January 29, 2018 complaint and the March 26, 2018 complaint filed a new, consolidated complaint against the Company and the members of our Board of Directors in the Superior Court of Hamilton County, Indiana. The shareholders generally allege claims of breach of fiduciary duty by the members of our Board of Directors and unjust enrichment to Mr. Biglari arising out of the dual class structure. The shareholders seek, for themselves and on behalf of all other shareholders as a class, a declaration that the defendants breached their duty to the shareholders and the class, and to recover unspecified damages, pre-judgment and post-judgment interest, and an award of their attorneys’ fees and other costs.

On December 14, 2018, the judge of the Superior Court of Hamilton County, Indiana issued an order granting the Company’s motion to dismiss the shareholders’ lawsuits. On January 11, 2019, the shareholders filed an appeal of the judge’s order dismissing the lawsuits. On December 4, 2019, the Indiana Court of Appeals issued a unanimous decision affirming the trial court’s decision to dismiss the shareholder litigation. On January 20, 2020, the shareholders filed a petition to transfer with the Indiana Supreme Court seeking review of the decision of the Court of Appeals. The Company opposed the petition. The Indiana Supreme Court has not ruled upon the petition to transfer.

On September 8, 2014, two former restaurant manager employees filed a purported class action lawsuit against Steak n Shake (Drake v. Steak n Shake). On January 30, 2017, a former restaurant manager employee filed a purported class action lawsuit against Steak n Shake (Clendenen v. Steak n Shake). The plaintiffs generally allege claims that Steak n Shake improperly classified its managerial employees as exempt. On July 26, 2019, the Company agreed to settle both cases for $8,350 and the Court approved the terms of the settlement. The settlement is reflected in selling, general and administrative expenses in the consolidated statement of earnings.

|

Mine Safety Disclosures |

Not applicable.

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Biglari Holdings’ Class A common stock and Class B common stock are listed for trading on the NYSE, trading symbol: BH.A and BH, respectively.

Shareholders

Biglari Holdings had 2,630 beneficial shareholders of its Class A common stock and 5,314 beneficial shareholders of its Class B common stock as of February 10, 2020.

Dividends

Biglari Holdings has never declared a dividend.

10

Issuer Purchases of Equity Securities

From November 5, 2019 through November 26, 2019, Sardar Biglari purchased 7,699 shares of Class A common stock at an average price paid per share of $557.33. Mr. Biglari may be deemed to be an “affiliated purchaser” as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934, as amended. The purchases were made through open market transactions.

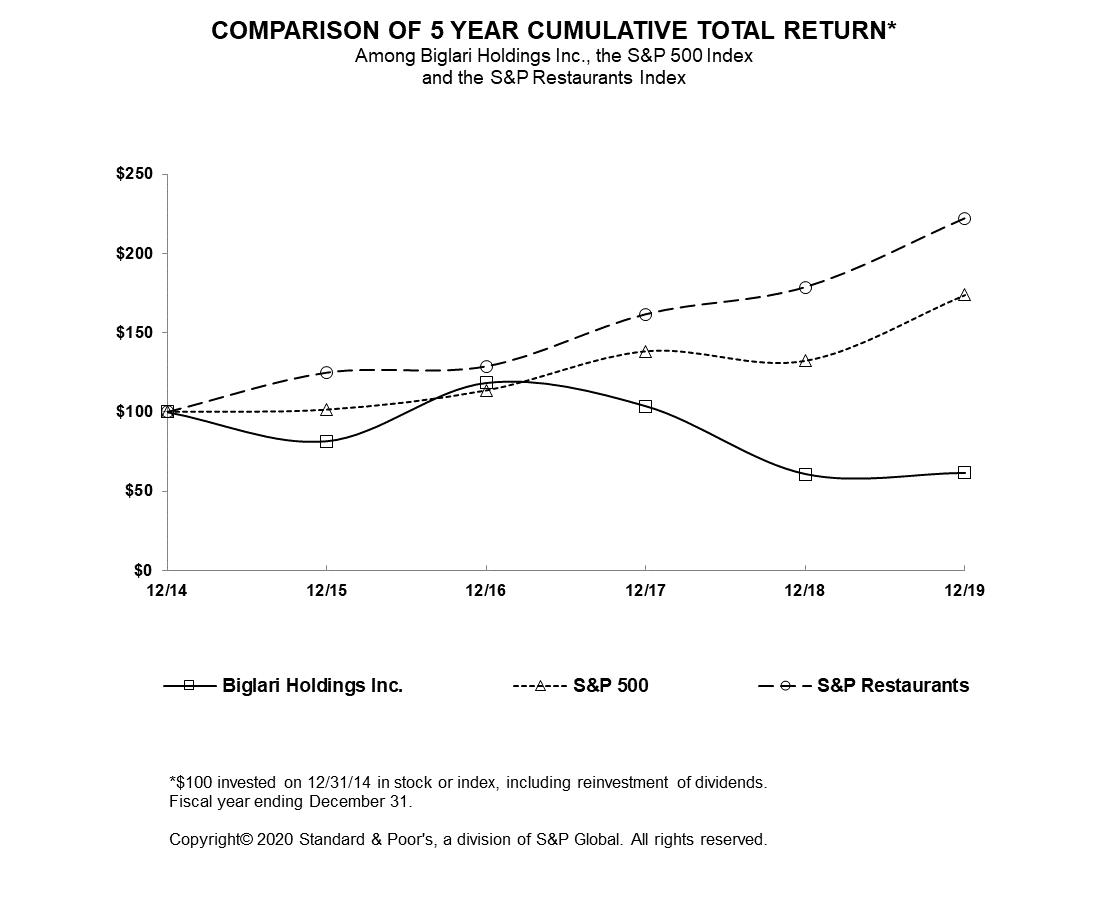

Performance Graph

The graph below matches Biglari Holdings Inc.'s cumulative 5-year total shareholder return on its Class A common stock and Class B common stock with the cumulative total returns of the S&P 500 Index and the S&P Restaurants Index. The graph tracks the performance of a $100 investment in our common stock and in each index (with the reinvestment of all dividends) from December 31, 2014 to December 31, 2019.

The preceding stock price performance graph and related information shall not be deemed “soliciting material” or to be “filed” with the SEC, nor shall such information be incorporated by reference into any future filings under the Securities Exchange Act of 1934, as amended, or the Securities Act of 1933, as amended, except to the extent that we specifically incorporate it by reference into such filings.

Securities Authorized for Issuance Under Equity Compensation Plans

Biglari Holdings does not have any equity compensation plans.

11

| Item 6. | Selected Financial Data |

(dollars in thousands except per share data)

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| Revenue: | ||||||||||||||||||||

| Total revenues | $ | 668,838 | $ | 809,894 | $ | 839,804 | $ | 850,076 | $ | 861,452 | ||||||||||

| Earnings: | ||||||||||||||||||||

| Net earnings (loss) | $ | 45,380 | $ | 19,392 | $ | 50,071 | $ | 99,451 | $ | (15,843 | ) | |||||||||

| Net earnings (loss) per equivalent Class A share | $ | 131.64 | $ | 55.71 | $ | 136.01 | $ | 271.22 | $ | (33.94 | ) | |||||||||

| Year-end data: | ||||||||||||||||||||

| Total assets | $ | 1,139,309 | $ | 1,029,493 | $ | 1,063,584 | $ | 1,096,967 | $ | 987,079 | ||||||||||

| Long-term notes payable and other borrowings | $ | 263,182 | $ | 240,001 | $ | 256,994 | $ | 281,555 | $ | 296,062 | ||||||||||

| Biglari Holdings Inc. shareholders’ equity | $ | 616,298 | $ | 570,455 | $ | 571,328 | $ | 531,940 | $ | 451,372 | ||||||||||

Earnings per share of common stock is based on the weighted average number of shares outstanding during the period. The issuance of dual class common stock on April 30, 2018 is applied to years 2015 through 2017 on a retrospective basis for the calculation of earnings per share. The Company has applied the “two-class method” of computing earnings per share as prescribed in Accounting Standards Codification 260, “Earnings Per Share.”

For total assets, periods prior to 2016 were adjusted for the reclassifications of debt issuance costs and deferred taxes. For long-term notes payable and other borrowings, periods prior to 2016 were adjusted for the reclassification of debt issuance.

As of January 1, 2018, franchise royalties and fees are composed of royalties and fees from Steak n Shake and Western Sizzlin franchisees. Royalties are based upon a percentage of sales of the franchise restaurant and are recognized as earned. Franchise royalties are billed on a monthly basis. Initial franchise fees when a new restaurant opens or at the start of a new franchise term are recorded as deferred revenue when received and recognized as revenue over the term of the franchise agreement. This represents a change in methodology under the January 1, 2018 adoption of Accounting Standards Codification 606 for we have historically recognized initial franchise fees upon the opening of a franchise restaurant. Comparative prior periods have not been adjusted.

12

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

(dollars in thousands except per share data)

Biglari Holdings Inc. is a holding company owning subsidiaries engaged in a number of diverse business activities, including property and casualty insurance, media and licensing, restaurants, and oil and gas. The Company’s largest operating subsidiaries are involved in the franchising and operating of restaurants. Biglari Holdings is founded and led by Sardar Biglari, Chairman and Chief Executive Officer of Biglari Holdings. The Company’s long-term objective is to maximize per-share intrinsic value. All major investment and capital allocation decisions are made for the Company and its subsidiaries by Mr. Biglari.

As of December 31, 2019, Mr. Biglari’s beneficial ownership was approximately 64.4% of the Company’s outstanding Class A common stock and 55.4% of the Company’s outstanding Class B common stock.

Business Acquisition

On September 9, 2019, a wholly-owned subsidiary of the Company, Southern Oil Company, acquired the stock of Southern Oil of Louisiana Inc. (collectively “Southern Oil”) for $51,505 in cash. Southern Oil primarily operates oil and natural gas properties offshore in the shallow waters of the Gulf of Mexico. The Company’s financial results include the results of Southern Oil from the acquisition date to the end of the year.

Net earnings attributable to Biglari Holdings shareholders are disaggregated in the table that follows. Amounts are recorded after deducting income taxes.

| 2019 | 2018 | 2017 | ||||||||||

| Operating businesses: | ||||||||||||

| Restaurant | $ | (10,734 | ) | $ | (2,613 | ) | $ | 9,725 | ||||

| Insurance | 5,584 | 4,915 | 3,097 | |||||||||

| Oil and gas | 5,921 | — | — | |||||||||

| Media | 572 | 796 | 435 | |||||||||

| Other | 742 | 472 | 506 | |||||||||

| Total operating businesses | 2,085 | 3,570 | 13,763 | |||||||||

| Corporate | (8,661 | ) | (8,661 | ) | 32,072 | |||||||

| Investment partnership gains | 60,773 | 33,240 | 11,080 | |||||||||

| Interest expense on notes payable | (8,817 | ) | (8,757 | ) | (6,844 | ) | ||||||

| $ | 45,380 | $ | 19,392 | $ | 50,071 | |||||||

The following discussion should be read in conjunction with Item 1, Business and our Consolidated Financial Statements and the notes thereto included in this Form 10-K. The following discussion should also be read in conjunction with the “Cautionary Note Regarding Forward-Looking Statements” and the risks and uncertainties described in Item 1A, Risk Factors set forth above.

Our Management Discussion and Analysis generally discusses 2019 and 2018 items and year-to-year comparisons between 2019 and 2018. Discussions of 2017 items and year-to-year comparisons between 2018 and 2017 can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of our Annual Report on Form 10-K for the year ended December 31, 2018 filed with the SEC on February 25, 2019.

13

Management’s Discussion and Analysis (continued)

Restaurants

Our restaurant businesses, which include Steak n Shake and Western Sizzlin, comprise 662 company-operated and franchise restaurants as of December 31, 2019.

| Steak n Shake | Western Sizzlin | |||||||||||||||||||||||

Company- operated | Franchise | Traditional | Company- operated | Franchise | Total | |||||||||||||||||||

| Total stores as of December 31, 2016 | 417 | — | 173 | 3 | 64 | 657 | ||||||||||||||||||

| Net restaurants opened (closed) | (2 | ) | — | 27 | 1 | (6 | ) | 20 | ||||||||||||||||

| Total stores as of December 31, 2017 | 415 | — | 200 | 4 | 58 | 677 | ||||||||||||||||||

| Net restaurants opened (closed) | (2 | ) | — | 13 | — | (3 | ) | 8 | ||||||||||||||||

| Total stores as of December 31, 2018 | 413 | — | 213 | 4 | 55 | 685 | ||||||||||||||||||

| Corporate stores transitioned | (29 | ) | 29 | — | ||||||||||||||||||||

| Net restaurants opened (closed) | (16 | ) | — | — | — | (7 | ) | (23 | ) | |||||||||||||||

| Total stores as of December 31, 2019 | 368 | 29 | 213 | 4 | 48 | 662 | ||||||||||||||||||

As of December 31, 2019, 107 of the 368 Steak n Shake company-operated stores were temporarily closed. We anticipate re-opening the temporarily closed stores as franchise partner or company-operated counter service units. The term “same-store sales” refers to the sales of company-operated units that have been open at least 18 months at the beginning of the current period and have remained open through the end of the period. Same-store traffic measures the number of patrons who walk through the same units.

Restaurant operations for 2019, 2018 and 2017 are summarized below.

| 2019 | 2018 | 2017 | |||||||||||||||||

| Revenue | |||||||||||||||||||

| Net sales | $ | 578,164 | $ | 740,922 | $ | 781,856 | |||||||||||||

| Franchise royalties and fees | 27,189 | 30,998 | 20,773 | ||||||||||||||||

| Other revenue | 4,867 | 3,770 | 4,524 | ||||||||||||||||

| Total revenue | 610,220 | 775,690 | 807,153 | ||||||||||||||||

| Restaurant cost of sales | |||||||||||||||||||

| Cost of food | 176,346 | 30.5 | % | 223,273 | 30.1 | % | 238,143 | 30.5 | % | ||||||||||

| Restaurant operating costs | 307,337 | 53.2 | % | 393,348 | 53.1 | % | 404,373 | 51.7 | % | ||||||||||

| Rent | 17,266 | 3.0 | % | 19,835 | 2.7 | % | 18,514 | 2.4 | % | ||||||||||

| Total cost of sales | 500,949 | 636,456 | 661,030 | ||||||||||||||||

| Selling, general and administrative | |||||||||||||||||||

| General and administrative | 47,685 | 7.8 | % | 57,684 | 7.4 | % | 60,527 | 7.5 | % | ||||||||||

| Marketing | 39,476 | 6.5 | % | 55,063 | 7.1 | % | 49,589 | 6.1 | % | ||||||||||

| Other expenses | 1,753 | 0.3 | % | 2,383 | 0.3 | % | 2,222 | 0.3 | % | ||||||||||

| Total selling, general and administrative | 88,914 | 14.6 | % | 115,130 | 14.8 | % | 112,338 | 13.9 | % | ||||||||||

| Impairments | 8,186 | 1.3 | % | 5,677 | 0.7 | % | 1,789 | 0.2 | % | ||||||||||

| Depreciation and amortization | 21,174 | 3.5 | % | 18,831 | 2.4 | % | 20,623 | 2.6 | % | ||||||||||

| Interest on finance leases and obligations | 7,816 | 8,207 | 9,082 | ||||||||||||||||

| Earnings (loss) before income taxes | (16,819 | ) | (8,611 | ) | 2,291 | ||||||||||||||

| Income tax expense (benefit) | (6,085 | ) | (5,998 | ) | (7,434 | ) | |||||||||||||

| Contributions to net earnings | $ | (10,734 | ) | $ | (2,613 | ) | $ | 9,725 | |||||||||||

Cost of food, restaurant operating costs and rent expense are expressed as a percentage of net sales.

General and administrative, marketing, other expenses, impairments and depreciation and amortization are expressed as a percentage of total revenue.

14

Management’s Discussion and Analysis (continued)

Net sales during 2019 were $578,164 representing a decrease of $162,758 when compared to 2018. The decreased performance of our restaurant operations in 2019 was driven by a decline in Steak n Shake’s same-store sales of $35,250 and the balance of the decrease was attributable to the closure of stores. Same-store sales decreased 6.9% whereas customer traffic decreased by 11.2%.

Franchise royalties and fees in 2019 were $27,189 compared to $30,998 in 2018. The decrease in franchise royalties and fees during 2019 compared to 2018 was attributable to decreases in marketing fees of $1,858 and forfeited development fees of $1,698. During 2019, Steak n Shake opened 29 franchise units and closed 29. Western Sizzlin did not open any new franchise units and closed seven.

The cost of food in 2019 was $176,346 or 30.5% of net sales, compared with $223,273 or 30.1% of net sales in 2018. Restaurant operating costs during 2019 were $307,337 or 53.2% of net sales, compared to $393,348 or 53.1% of net sales in 2018. The decrease in cost of food and restaurant operating costs during 2019 compared to 2018 was attributable to lower net sales resulting from store closures and decreased same-store sales.

Selling, general and administrative expenses during 2019 were $88,914 or 14.6% of total revenues compared to $115,130 or 14.8% of total revenues during 2018. General and administrative expenses decreased by $9,999 during 2019 compared to 2018, primarily because of decreased personnel costs of $17,918, offset by settlements of class action complaints of $8,350. Marketing expense decreased by $15,587 in 2019 compared to 2018 primarily driven by a reduction in television and print advertising.

Asset impairments increased $2,509 during 2019 compared to 2018 primarily due to store closures. Depreciation and amortization expense increased $2,343 during 2019 compared to 2018 primarily as a result of the depreciation of finance lease assets.

Interest on obligations under leases was $7,816 during 2019, versus $8,207 during 2018. The year-over-year decrease in interest expense is primarily attributable to the maturity and retirement of lease obligations. The total obligations under leases outstanding on December 31, 2019 were $78,749 compared to $64,200 on December 31, 2018.

Insurance

First Guard is a direct underwriter of commercial truck insurance, selling physical damage and nontrucking liability insurance to truckers. Earnings of our insurance business are summarized below.

| 2019 | 2018 | 2017 | ||||||||||

| Premiums written | $ | 28,746 | $ | 26,465 | $ | 24,242 | ||||||

| Insurance losses | 16,924 | 15,457 | 14,959 | |||||||||

| Underwriting expenses | 5,345 | 5,374 | 4,765 | |||||||||

| Pre-tax underwriting gain | 6,477 | 5,634 | 4,518 | |||||||||

| Other income and expenses | ||||||||||||

| Investment income and commissions | 1,337 | 1,163 | 701 | |||||||||

| Other income (expense) | (711 | ) | (582 | ) | (449 | ) | ||||||

| Total other income | 626 | 581 | 252 | |||||||||

| Earnings before income taxes | 7,103 | 6,215 | 4,770 | |||||||||

| Income tax expense | 1,519 | 1,300 | 1,673 | |||||||||

| Contribution to net earnings | $ | 5,584 | $ | 4,915 | $ | 3,097 | ||||||

First Guard’s insurance products are marketed primarily through direct response methods via the Internet or by telephone. First Guard’s cost-efficient direct response marketing methods enable it to be a low-cost trucking insurer.

15

Management’s Discussion and Analysis (continued)

In 2019, premiums earned increased $2,281 or 8.6% compared to 2018. Pre-tax underwriting gain during 2019 was $6,477, an increase of $843 or 15.0% compared to 2018.

Insurance premiums and other on the consolidated statement of earnings includes premiums written, investment income and commissions. In the preceding table, investment income and commissions are included in other income.

Oil and Gas

Southern Oil primarily operates oil and natural gas properties offshore in the shallow waters of the Gulf of Mexico. Southern Oil was acquired on September 9, 2019. The financial results for Southern Oil from the acquisition date to the end of the year are summarized below.

| 2019 | ||||

| Oil and gas revenue | $ | 24,436 | ||

| Oil and gas production costs | 7,259 | |||

| Depreciation, depletion and accretion | 8,218 | |||

| General and administrative expenses | 927 | |||

| Earnings before income taxes | 8,032 | |||

| Income tax expense | 2,111 | |||

| Contribution to net earnings | $ | 5,921 | ||

Media and Licensing

Maxim’s business lies principally in media and licensing. Earnings of our media and licensing operations are summarized below.

| 2019 | 2018 | 2017 | ||||||||||

| Media and licensing revenue | $ | 4,099 | $ | 6,576 | $ | 7,708 | ||||||

| Media and licensing cost | 3,181 | 4,152 | 6,527 | |||||||||

| General and administrative expenses | 176 | 1,329 | 1,570 | |||||||||

| Depreciation and amortization | — | 27 | 50 | |||||||||

| Earnings (loss) before income taxes | 742 | 1,068 | (439 | ) | ||||||||

| Income tax expense (benefit) | 170 | 272 | (874 | ) | ||||||||

| Contribution to net earnings | $ | 572 | $ | 796 | $ | 435 | ||||||

We acquired Maxim with the idea of transforming its business model. The magazine developed the Maxim brand, a franchise we are utilizing to generate nonmagazine revenue, notably through licensing, a cash-generating business related to consumer products, services, and events.

Investment Partnership Gains

Earnings from our investments in partnerships are summarized below.

| 2019 | 2018 | 2017 | ||||||||||

| Investment partnership gains | $ | 78,133 | $ | 40,411 | $ | 6,965 | ||||||

| Tax expense (benefit) | 17,360 | 7,171 | (4,115 | ) | ||||||||

| Contribution to net earnings | $ | 60,773 | $ | 33,240 | $ | 11,080 | ||||||

Investment partnership gains include gains and losses from changes in the market values of underlying investments and dividends earned by the partnerships. Dividend income has a lower effective tax rate than income from changes in market values. Changes in the market values of investments can be highly volatile. The investments held by the investment partnerships are largely concentrated in the common stock of one investee, Cracker Barrel Old Country Store, Inc.

16

Management’s Discussion and Analysis (continued)

The investment partnerships hold the Company’s common stock as investments. The Company’s pro-rata share of its common stock held by the investment partnerships is recorded as treasury stock even though these shares are legally outstanding. Gains and losses on Company common stock included in the earnings of the partnerships are eliminated.

Interest Expense

The Company’s interest expense is summarized below.

| 2019 | 2018 | 2017 | ||||||||||

| Interest expense on notes payable and other borrowings | $ | (12,442 | ) | $ | (11,677 | ) | $ | (11,040 | ) | |||

| Tax benefit | (3,625 | ) | (2,920 | ) | (4,196 | ) | ||||||

| Interest expense net of tax | $ | (8,817 | ) | $ | (8,757 | ) | $ | (6,844 | ) | |||

Interest expense during 2019 increased by $765 compared to 2018 primarily due to higher average interest rates during 2019.

Income Taxes

Consolidated income tax expense was $9,761 in 2019 versus a benefit of $2,637 in 2018. Income tax expense increased by $12,398 during 2019 compared to 2018, primarily due to an increase in tax expense for investment partnership gains of $10,189.

Corporate

Corporate expenses exclude the activities in the restaurant, insurance, media and licensing, oil and gas, and other companies. Corporate net losses of $8,661 during 2019 remained flat compared to 2018.

Financial Condition

Our consolidated shareholders’ equity on December 31, 2019 was $616,298, an increase of $45,843 compared to the December 31, 2018 balance. The increase was primarily due to net income of $45,380.

Consolidated cash and investments are summarized below.

| December 31, | ||||||||

| 2019 | 2018 | |||||||

| Cash and cash equivalents | $ | 67,772 | $ | 48,557 | ||||

| Investments | 44,856 | 33,860 | ||||||

| Investments reported in other current assets | — | 4,463 | ||||||

| Fair value of interest in investment partnerships | 666,123 | 715,102 | ||||||

| Total cash and investments | 778,751 | 801,982 | ||||||

| Less: portion of Company stock held by investment partnerships | (160,581 | ) | (157,622 | ) | ||||

| Carrying value of cash and investments on balance sheet | $ | 618,170 | $ | 644,360 | ||||

Unrealized gains/losses of Biglari Holdings’ stock held by the investment partnerships are eliminated in the Company’s consolidated financial results.

Liquidity

Our balance sheet continues to maintain significant liquidity. Consolidated cash flow activities are summarized below.

| 2019 | 2018 | 2017 | ||||||||||

| Net cash provided by operating activities | $ | 93,683 | $ | 20,678 | $ | 25,780 | ||||||

| Net cash used in investing activities | (69,982 | ) | (25,290 | ) | (11,548 | ) | ||||||

| Net cash used in financing activities | (8,010 | ) | (7,530 | ) | (23,000 | ) | ||||||

| Effect of exchange rate changes on cash | (5 | ) | (78 | ) | 165 | |||||||

| Increase (decrease) in cash, cash equivalents and restricted cash | $ | 15,686 | $ | (12,220 | ) | $ | (8,603 | ) | ||||

In 2019, cash from operating activities increased by $73,005 compared to 2018, primarily because of increased distributions from investment partnerships. Distributions from investment partnerships were $129,329 and $29,660 during 2019 and 2018, respectively. Distributions to partners were higher during 2019 primarily because of tax liabilities from capital gains in the partnerships. Changes in working capital accounts decreased by $2,131 and $12,043 during 2019 and 2018, respectively. The decrease of working capital accounts during 2018 was primarily tied to the payment of the 2017 CEO incentive fee of $7,353. No incentive fees were accrued during 2019 and 2018.

17

Management’s Discussion and Analysis (continued)

Net cash used in investing activities increased during 2019 by $44,692 compared to 2018. The purchase price of Southern Oil during 2019, net of cash acquired was $51,062. Capital expenditures during 2019 were $2,386 higher than capital expenditures during 2018. The increase during 2019 compared to 2018 was primarily because of $7,594 in capitalized development costs by Southern Oil, which was offset by decreased capital expenditures by our restaurant businesses of $5,020. Purchases of investments, net of redemptions of fixed maturity securities were $5,818 during 2019 compared to $10,084 during 2018. Distributions from investment partnerships of $40,000 during 2019 and $39,040 during 2018 were reinvested into the investment partnerships in each year.

During 2019 and 2018 we incurred debt payments of $8,010 and $7,579, respectively.

We intend to meet the working capital needs of our operating subsidiaries principally through anticipated cash flows generated from operations, cash on hand, existing credit facilities, and the sale of excess properties. We continually review available financing alternatives.

Steak n Shake Credit Facility

On March 19, 2014, Steak n Shake and its subsidiaries entered into a credit agreement which provided for a senior secured term loan facility in an aggregate principal amount of $220,000. The term loan is scheduled to mature on March 19, 2021. As of December 31, 2019, $181,498 was outstanding. The Company is evaluating refinancing options although alternatives may not be available on terms commensurate with its current financing arrangement. Biglari Holdings is not a guarantor under the credit facility.

The term loan amortizes in equal quarterly installments at an annual rate of 1.0% of the original principal amount of the term loan, subject to mandatory prepayments from excess cash flow, asset sales and other events described in the credit agreement. The balance will be due at maturity.

Borrowings bear interest at a rate per annum equal to a base rate or a Eurodollar rate (minimum of 1%) plus an applicable margin. Interest on the term loan is based on a Eurodollar rate plus an applicable margin of 3.75% or on the prime rate plus an applicable margin of 2.75%. The interest rate on the term loan was 5.55% and 6.28% as of December 31, 2019 and 2018, respectively.

The credit agreement includes customary affirmative and negative covenants and events of default. As of December 31, 2019, we were in compliance with all covenants. Steak n Shake’s credit facility contains restrictions on its ability to pay dividends to Biglari Holdings.

The term loan is secured by first priority security interests in substantially all the assets of Steak n Shake. Disruptions in debt capital markets that restrict access to funding when needed could adversely affect the results of operations, liquidity and capital resources of Steak n Shake.

Western Sizzlin Revolver

As of December 31, 2019 and 2018, Western Sizzlin had no debt outstanding under its revolver.

Critical Accounting Policies

Certain accounting policies require us to make estimates and judgments in determining the amounts reflected in the consolidated financial statements. Such estimates and judgments necessarily involve varying, and possibly significant, degrees of uncertainty. Accordingly, certain amounts currently recorded in the financial statements will likely be adjusted in the future based on new available information and changes in other facts and circumstances. A discussion of our principal accounting policies that required the application of significant judgments as of December 31, 2019 follows.

Consolidation

The consolidated financial statements include the accounts of Biglari Holdings Inc. and the wholly owned subsidiaries of Biglari Holdings Inc. We consolidate limited partnership entities if we are the general partner of such entities and for which no substantive removal rights exist. The analysis as to whether to consolidate an entity is subject to a significant amount of judgment. All intercompany accounts and transactions are eliminated in consolidation.

18

Management’s Discussion and Analysis (continued)

Our interests in the investment partnerships are accounted for as equity method investments because of our retained limited partner interest in the investment partnerships. The Company records gains from investment partnerships (inclusive of the investment partnerships’ unrealized gains and losses on their securities) in the consolidated statement of earnings based on our proportional ownership interest in the investment partnerships.

Impairment of Restaurant Long-lived Assets

We review company-operated restaurants for impairment on a restaurant-by-restaurant basis when events or circumstances indicate a possible impairment. Assets included in the impairment assessment generally consist of property, equipment and leasehold improvements directly associated with an individual restaurant as well as any related finance or operating lease assets. We test for impairment by comparing the carrying value of the asset to the undiscounted future cash flows expected to be generated by the asset. If the total estimated future cash flows are less than the carrying amount of the asset, the carrying value is written down to the estimated fair value, and a loss is recognized in earnings. The future cash flows expected to be generated by an asset requires significant judgment regarding future performance of the asset, fair market value if the asset were to be sold, and other financial and economic assumptions.

Oil and Natural Gas Reserves

The estimation of proved reserves, which is based on the requirement of reasonable certainty, is an ongoing process based on rigorous technical evaluations, commercial and market assessments and detailed analysis of well and reservoir information such as flow rates and reservoir pressures. Although we are reasonably confident that proved reserves will be produced, the timing and amount recovered can be affected by a number of factors including, reservoir performance, government policies, and significant changes in long-term oil and natural gas price levels. In addition, proved reserves could be affected by an extended period of low prices which could reduce the level of our partners’ capacity to fund their share of joint projects. Accordingly, reserve estimates are generally different from the quantities of natural gas and oil that are ultimately recovered. We cannot predict the amounts or timing of future reserve revisions.

Income Taxes