Table of Contents

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

(State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

Title of each class: |

Trading Symbol(s) |

Name of each exchange on which registered: | ||

N/A |

| ☒ | Accelerated filer | ☐ | ||||

Non-accelerated filer |

☐ | Smaller reporting company | ||||

| Emerging growth company | ||||||

Table of Contents

GRAYSCALE® ETHEREUM TRUST (ETH)

TABLE OF CONTENTS

Table of Contents

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains “forward-looking statements” with respect to the financial conditions, results of operations, plans, objectives, future performance and business of Grayscale Ethereum Trust (ETH) (the “Trust”). Statements preceded by, followed by or that include words such as “may,” “might,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or “continue,” the negative of these terms and other similar expressions are intended to identify some of the forward-looking statements. All statements (other than statements of historical fact) included in this Quarterly Report that address activities, events or developments that will or may occur in the future, including such matters as changes in market prices and conditions, the Trust’s operations, the plans of Grayscale Investments, LLC (the “Sponsor”) and references to the Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially from such statements. These statements are based upon certain assumptions and analyses the Sponsor made based on its perception of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including, but not limited to, those described in “Part I, Item 1A. Risk Factors” of our Annual Report on Form 10-K and in “Part II, Item 1A. Risk Factors” herein. Forward-looking statements are made based on the Sponsor’s beliefs, estimates and opinions on the date the statements are made and neither the Trust nor the Sponsor is under a duty or undertakes an obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, other than as required by applicable laws. Investors are therefore cautioned against relying on forward-looking statements.

Unless otherwise stated or the context otherwise requires, the terms “we,” “our” and “us” in this Quarterly Report refer to the Sponsor acting on behalf of the Trust.

A glossary of industry and other defined terms is included in this Quarterly Report, beginning on page 25.

This Quarterly Report supplements and where applicable amends the Memorandum, as defined in the Trust’s Amended and Restated Declaration of Trust and Trust Agreement, for general purposes.

INDUSTRY AND MARKET DATA

Although we are responsible for all disclosure contained in this Quarterly Report on Form 10-Q, in some cases we have relied on certain market and industry data obtained from third-party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications in conjunction with our assumptions regarding the Ethereum industry and market. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings “Forward-Looking Statements,” “Part I, Item 1A. Risk Factors” in the Annual Report on Form 10-K for the year ended December 31, 2023, filed with the Securities and Exchange Commission (the “SEC”) on February 23, 2024 (the “Annual Report”), and “Part II, Item 1A. Risk Factors” in this Quarterly Report on Form 10-Q.

1

Table of Contents

March 31, 2024 |

December 31, 2023 |

|||||||

| Assets: |

||||||||

| Investment in Ether, at fair value (cost $ |

$ | $ | ||||||

| |

|

|

|

|||||

| Total assets |

$ | $ | ||||||

| |

|

|

|

|||||

| Liabilities: |

||||||||

| Sponsor’s Fee payable, related party |

$ | $ | ||||||

| |

|

|

|

|||||

| Total liabilities |

||||||||

| |

|

|

|

|||||

| Net assets |

$ | $ | ||||||

| |

|

|

|

|||||

| Net Assets consists of: |

||||||||

| Paid-in-capital |

||||||||

| Accumulated net investment loss |

( |

) | ( |

) | ||||

| Accumulated net realized gain on investment in Ether |

||||||||

| Accumulated net change in unrealized appreciation on investment in Ether |

||||||||

| |

|

|

|

|||||

| $ | $ | |||||||

| |

|

|

|

|||||

| Shares issued and outstanding, no par value (unlimited Shares authorized) |

||||||||

| |

|

|

|

|||||

| Principal market net asset value per Share |

$ | $ | ||||||

| |

|

|

|

|||||

March 31, 2024 |

Quantity of Ether |

Cost |

Fair Value |

% of Net Assets |

||||||||||||

Investment in Ether |

$ | $ | % | |||||||||||||

Net assets |

$ | $ | % | |||||||||||||

December 31, 2023 |

Quantity of Ether |

Cost |

Fair Value |

% of Net Assets |

||||||||||||

Investment in Ether |

$ | $ | % | |||||||||||||

Net assets |

$ | $ | % | |||||||||||||

Three Months Ended March 31, |

||||||||

2024 |

2023 |

|||||||

Investment income: |

||||||||

Investment income |

$ | $ | ||||||

Expenses: |

||||||||

Sponsor’s Fee, related party |

||||||||

Net investment loss |

( |

) | ( |

) | ||||

Net realized and unrealized gain from: |

||||||||

Net realized gain on investment in Ether |

||||||||

Net change in unrealized appreciation on investment in Ether |

||||||||

Net realized and unrealized gain on investment |

||||||||

Net increase in net assets resulting from operations |

$ | $ | ||||||

Three Months Ended March 31, |

||||||||

2024 |

2023 |

|||||||

Increase in net assets from operations: |

||||||||

Net investment loss |

$ | ( |

) | $ | ( |

) | ||

Net realized gain on investment in Ether |

||||||||

Net change in unrealized appreciation on investment in Ether |

||||||||

Net increase in net assets resulting from operations |

||||||||

Increase in net assets from capital share transactions: |

||||||||

Shares issued |

||||||||

Net increase in net assets resulting from capital share transactions |

||||||||

Total increase in net assets from operations and capital share transactions |

||||||||

Net assets: |

||||||||

Beginning of period |

||||||||

End of period |

$ | $ | ||||||

Change in Shares outstanding |

||||||||

Shares outstanding at beginning of period |

||||||||

Shares issued |

||||||||

Net increase in Shares |

||||||||

Shares outstanding at end of period |

||||||||

| • | Level 1 – Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities that the Trust has the ability to access. Since valuations are based on quoted prices that are readily and regularly available in an active market, these valuations do not entail a significant degree of judgment. |

| • | Level 2 – Valuations based on quoted prices in markets that are not active or for which significant inputs are observable, either directly or indirectly. |

| • | Level 3 – Valuations based on inputs that are unobservable and significant to the overall fair value measurement. |

Fair Value Measurement Using |

||||||||||||||||

| (Amounts in thousands) | Amount at Fair Value |

Level 1 |

Level 2 |

Level 3 |

||||||||||||

| March 31, 2024 |

||||||||||||||||

| Assets |

||||||||||||||||

| Investment in Ether |

$ | $ | $ | $ | ||||||||||||

| |

|

|

|

|

|

|

|

|||||||||

Fair Value Measurement Using |

||||||||||||||||

| (Amounts in thousands) | Amount at Fair Value |

Level 1 |

Level 2 |

Level 3 |

||||||||||||

| December 31, 2023 |

||||||||||||||||

| Assets |

||||||||||||||||

| Investment in Ether |

$ | $ | $ | $ | ||||||||||||

| |

|

|

|

|

|

|

|

|||||||||

| (Amounts in thousands, except Ether amounts) | Quantity |

Fair Value |

||||||

| Beginning balance as of January 1, 2023 |

$ | |||||||

| |

|

|

|

|||||

| Ether contributed |

||||||||

| Ether distributed for Sponsor’s Fee, related party |

( |

) | ( |

) | ||||

| Net change in unrealized appreciation on investment in Ether |

||||||||

| Net realized gain on investment in Ether |

||||||||

| |

|

|

|

|

|

|

|

|

| Ending balance as of December 31, 2023 |

$ | |||||||

| |

|

|

|

|||||

| (Amounts in thousands, except Ether amounts) | Quantity |

Fair Value |

||||||

| Beginning balance as of January 1, 2024 |

$ | |||||||

| |

|

|

|

|||||

| Ether contributed |

||||||||

| Ether distributed for Sponsor’s Fee, related party |

( |

) | ( |

) | ||||

| Net change in unrealized appreciation on investment in Ether |

||||||||

| Net realized gain on investment in Ether |

||||||||

| |

|

|

|

|||||

| Ending balance as of March 31, 2024 |

$ | |||||||

| |

|

|

|

|||||

Three Months Ended March 31, |

||||||||

2024 |

2023 |

|||||||

Per Share Data |

||||||||

Principal market net asset value, beginning of period |

$ | $ | ||||||

Net increase in net assets from investment operations: |

||||||||

Net investment loss |

( |

) | ( |

) | ||||

Net realized and unrealized gain |

||||||||

Net increase in net assets resulting from operations |

||||||||

Principal market net asset value, end of period |

$ | $ | ||||||

Total return |

% | % | ||||||

Ratios to average net assets: |

||||||||

Net investment loss |

- |

% | - |

% | ||||

Expenses |

- |

% | - |

% | ||||

Table of Contents

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read together with, and is qualified in its entirety by reference to, our unaudited financial statements and related notes included elsewhere in this Quarterly Report, which have been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). The following discussion may contain forward-looking statements based on assumptions we believe to be reasonable. Our actual results could differ materially from those discussed in these forward-looking statements. Factors that could cause or contribute to these differences include, but are not limited to, those set forth under “Part II, Item 1A. Risk Factors” in this Quarterly Report, or in “Part I, Item 1A. Risk Factors” and “Forward-Looking Statements” or other sections of our Annual Report on Form 10-K for the year ended December 31, 2023.

Trust Overview

The Trust is a passive entity that is managed and administered by the Sponsor and does not have any officers, directors or employees. The Trust holds Ether and, from time to time on a periodic basis, issues Creation Baskets in exchange for deposits of Ether. As a passive investment vehicle, the Trust’s investment objective is for the value of the Shares (based on Ether per Share) to reflect the value of Ether held by the Trust, determined by reference to the Index Price, less the Trust’s expenses and other liabilities. While an investment in the Shares is not a direct investment in Ether, the Shares are designed to provide investors with a cost-effective and convenient way to gain investment exposure to Ether. To date, the Trust has not met its investment objective and the Shares quoted on OTCQX have not reflected the value of Ether held by the Trust, less the Trust’s expenses and other liabilities, but instead have traded at both premiums and discounts to such value, which at times have been substantial. The Trust is not managed like a business corporation or an active investment vehicle.

Forks

The Ethereum Network operates using open-source protocols, meaning that any user can download the software, modify it and then propose that the users and validators, as applicable, of Ethereum adopt the modification. When a modification is introduced and a substantial majority of users and validators consent to the modification, the change is implemented and the network remains uninterrupted. However, if less than a substantial majority of users and validators consent to the proposed modification, and the modification is not compatible with the software prior to its modification, the consequence would be what is known as a “hard fork” of the Ethereum Network, with one group running the pre-modified software and the other running the modified software. The effect of such a fork would be the existence of two versions of Ethereum running in parallel, yet lacking interchangeability. Holders of Ether on the original Ethereum Network, at the time the block is validated and the fork occurs, can then also receive an identical amount of new tokens on the new network.

Recent Developments

The ETH Trust Distribution

On April 23, 2024 the Sponsor announced the formation of Grayscale Ethereum Mini Trust (the “ETH Trust”) and its intention to effectuate the initial creation of shares of the ETH Trust through the contribution by the Trust of a certain amount of Ether to the ETH Trust as consideration and in exchange for newly created shares of the ETH Trust (“ETH Shares”).

The ETH Trust has filed a registration statement on Form S-1 (Registration No. 333-278878) (as amended, the “ETH Trust Form S-1”) relating to the proposed issuance of baskets of ETH Shares to certain authorized participants on an ongoing basis, commencing following consummation of the ETH Trust Distribution (as defined below). Prior to effectiveness of the ETH Trust Form S-1, the ETH Trust will file a registration statement on Form 8-A (the “ETH Trust Form 8-A”) to register the ETH Shares under the Exchange Act, which is expected to become effective concurrently with the effectiveness of the ETH Trust Form S-1. Following the effectiveness of the ETH Trust Form S-1 and the ETH Trust Form 8-A, and approval of the ETH Trust 19b-4 Application (as defined below), the newly created ETH Shares will then be distributed to shareholders of the Trust as of a date to be determined by the Sponsor (the “Record Date”), pro rata based on a 1:1 ratio, such that for each one Share held by each shareholder on the Record Date, such shareholder will be entitled to receive one ETH Share on a subsequent date to be determined by the Sponsor (the “Distribution Date”) (such transactions collectively, the “ETH Trust Distribution”).

In connection with the ETH Trust Distribution, the Sponsor anticipates that NYSE Arca will file an application with the SEC pursuant to Rule 19b-4 under the Exchange Act, to list the Shares of the ETH Trust on NYSE Arca (the “ETH Trust 19b-4 Application”). In addition, the ETH Trust intends to rely on an exemption or other relief from the SEC under 17 CFR §§ 242.101 and 102 (“Regulation M”) to operate its redemption program.

As of the date of this filing, the ETH Trust 19b-4 Application has not been approved by the SEC and an exemption or other relief from Regulation M is not available for the ETH Trust. The Sponsor makes no representation as to when or if such approval will be obtained and when such an exemption or relief will be available. The ETH Trust will not seek effectiveness of its registration statement and no offering of ETH Shares will take place unless and until such approval is obtained and such an exemption or relief is available.

As a result of the contemplated ETH Trust Distribution, following the Distribution Date, the Trust will hold a portion of the Ether that was held by the Trust as of the Record Date and the ETH Trust would hold the remaining portion of the Ether that was held by the Trust as of the Record Date, in each case, reduced by the portion of the sponsor’s fee attributable to such Ether accrued and paid between the Record Date and the Distribution Date. Neither the number of outstanding Shares nor the exposure of shareholders of the Trust to Ether underlying their aggregate shareholdings (including Shares and ETH Shares) are expected to change as a result of the contemplated ETH Trust Distribution. No consent, authorization, approval or proxy is being sought from shareholders in connection with the ETH Trust Distribution, and shareholders will not need to pay any consideration, exchange or surrender existing Shares or take any other action to receive ETH Shares on the Distribution Date. Following the ETH Trust Distribution, the Trust and the ETH Trust will operate as independent NYSE Arca listed exchanged-traded commodity products, and neither will have any share ownership, beneficial or otherwise, in the other.

The Sponsor does not expect the ETH Trust Distribution to be a taxable event for the Trust or its shareholders.

The Trust has filed a preliminary information statement on Schedule 14C (Registration No. 000-56193), describing the terms and conditions of the ETH Trust Distribution. For the avoidance of doubt, the Trust will not execute the ETH Trust Distribution as described herein or therein unless and until (i) NYSE Arca’s application with the SEC pursuant to Rule 19b-4 under the Exchange Act to list the Shares of the Trust on NYSE Arca has been approved, (ii) the ETH Trust 19b-4 Application has been approved and (iii) the ETH Trust Form S-1 and ETH Trust Form 8-A have become effective. There can be no assurance as to whether or when such approvals will be obtained or whether or when the ETH Trust Distribution will be effected.

14

Table of Contents

Critical Accounting Policies and Estimates

Investment Transactions and Revenue Recognition

The Trust considers investment transactions to be the receipt of Ether for Share creations and the delivery of Ether for Share redemptions or for payment of expenses in Ether. At this time, the Trust is not accepting redemption requests from shareholders. The Trust records its investment transactions on a trade date basis and changes in fair value are reflected as net change in unrealized appreciation or depreciation on investments. Realized gains and losses are calculated using the specific identification method. Realized gains and losses are recognized in connection with transactions including settling obligations for the Sponsor’s Fee in Ether.

Principal Market and Fair Value Determination

To determine which market is the Trust’s principal market (or in the absence of a principal market, the most advantageous market) for purposes of calculating the Trust’s net asset value in accordance with U.S. GAAP (“Principal Market NAV”), the Trust follows Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 820-10, which outlines the application of fair value accounting. ASC 820-10 determines fair value to be the price that would be received for Ether in a current sale, which assumes an orderly transaction between market participants on the measurement date. ASC 820-10 requires the Trust to assume that Ether is sold in its principal market to market participants or, in the absence of a principal market, the most advantageous market. Market participants are defined as buyers and sellers in the principal or most advantageous market that are independent, knowledgeable, and willing and able to transact.

The Trust only receives Ether in connection with a creation order from the Authorized Participant (or a Liquidity Provider) and does not itself transact on any Digital Asset Markets. Therefore, the Trust looks to market-based volume and level of activity for Digital Asset Markets. The Authorized Participant(s), or a Liquidity Provider, may transact in a Brokered Market, a Dealer Market, Principal-to-Principal Markets and Exchange Markets (referred to as “Trading Platform Markets” in this Quarterly Report), each as defined in the FASB ASC Master Glossary (collectively, “Digital Asset Markets”).

In determining which of the eligible Digital Asset Markets is the Trust’s principal market, the Trust reviews these criteria in the following order:

| • | First, the Trust reviews a list of Digital Asset Markets that maintain practices and policies designed to comply with anti-money laundering (“AML”) and know-your-customer (“KYC”) regulations, and non-Digital Asset Trading Platform Markets that the Trust reasonably believes are operating in compliance with applicable law, including federal and state licensing requirements, based upon information and assurances provided to it by each market. |

| • | Second, the Trust sorts these Digital Asset Markets from high to low by market-based volume and level of activity of Ether traded on each Digital Asset Market in the trailing twelve months. |

| • | Third, the Trust then reviews pricing fluctuations and the degree of variances in price on Digital Asset Markets to identify any material notable variances that may impact the volume or price information of a particular Digital Asset Market. |

| • | Fourth, the Trust then selects a Digital Asset Market as its principal market based on the highest market-based volume, level of activity and price stability in comparison to the other Digital Asset Markets on the list. Based on information reasonably available to the Trust, Trading Platform Markets have the greatest volume and level of activity for the asset. The Trust therefore looks to accessible Trading Platform Markets as opposed to the Brokered Market, Dealer Market and Principal-to-Principal Markets to determine its principal market. As a result of the aforementioned analysis, a Trading Platform Market has been selected as the Trust’s principal market. |

The Trust determines its principal market (or in the absence of a principal market the most advantageous market) annually and conducts a quarterly analysis to determine (i) if there have been recent changes to each Digital Asset Market’s trading volume and level of activity in the trailing twelve months, (ii) if any Digital Asset Markets have developed that the Trust has access to, or (iii) if recent changes to each Digital Asset Market’s price stability have occurred that would materially impact the selection of the principal market and necessitate a change in the Trust’s determination of its principal market.

15

Table of Contents

The cost basis of Ether received in connection with a creation order is recorded by the Trust at the fair value of Ether at 4:00 p.m., New York time, on the creation date for financial reporting purposes. The cost basis recorded by the Trust may differ from proceeds collected by the Authorized Participant from the sale of the corresponding Shares to investors.

Investment Company Considerations

The Trust is an investment company for GAAP purposes and follows accounting and reporting guidance in accordance with the FASB ASC Topic 946, Financial Services – Investment Companies. The Trust uses fair value as its method of accounting for Ether in accordance with its classification as an investment company for accounting purposes. The Trust is not a registered investment company under the Investment Company Act of 1940. GAAP requires management to make estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. Actual results could differ from those estimates and these differences could be material.

Review of Financial Results (unaudited)

Financial Highlights for the Three Months Ended March 31, 2024 and 2023

(All amounts in the following table and the subsequent paragraphs, except Share, per Share, Ether and price of Ether amounts, are in thousands)

| Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| Net realized and unrealized gain on investment in Ether |

$ | 4,006,549 | $ | 1,902,063 | ||||

|

|

|

|

|

|||||

| Net increase in net assets resulting from operations |

$ | 3,953,056 | $ | 1,872,425 | ||||

|

|

|

|

|

|||||

| Net assets (1) |

$ | 10,711,110 | $ | 5,521,623 | ||||

|

|

|

|

|

|||||

| (1) | Net assets in the above table and subsequent paragraphs are calculated in accordance with U.S. GAAP based on the Digital Asset Market price of Ether on the Digital Asset Trading Platform that the Trust considered its principal market, as of 4:00 p.m., New York time, on the valuation date. |

Net realized and unrealized gain on investment in Ether for the three months ended March 31, 2024 was $4,006,549, which includes a realized gain of $45,780 on the transfer of Ether to pay the Sponsor’s Fee and net change in unrealized appreciation on investment in Ether of $3,960,769. Net realized and unrealized gain on investment in Ether for the period was driven by Ether price appreciation from $2,281.10 per Ether as of December 31, 2023, to $3,637.95 per Ether as of March 31, 2024. Net increase in net assets resulting from operations was $3,953,056 for the three months ended March 31, 2024, which consisted of the net realized and unrealized gain on investment in Ether, less the Sponsor’s Fee of $53,493. Net assets increased to $10,711,110 at March 31, 2024, a 58% increase for the three-month period. The increase in net assets resulted from the aforementioned Ether price appreciation, partially offset by the withdrawal of approximately 18,359 Ether to pay the foregoing Sponsor’s Fee.

Net realized and unrealized gain on investment in Ether for the three months ended March 31, 2023 was $1,902,063, which includes a realized gain of $21,794 on the transfer of Ether to pay the Sponsor’s Fee and net change in unrealized appreciation on investment in Ether of $1,880,269. Net realized and unrealized gain on investment in Ether for the period was driven by Ether price appreciation from $1,201.33 per Ether as of December 31, 2022, to $1,828.98 per Ether as of March 31, 2023. Net increase in net assets resulting from operations was $1,872,425 for the three months ended March 31, 2023, which consisted of the net realized and unrealized gain on investment in Ether, less the Sponsor’s Fee of $29,638. Net assets increased to $5,521,623 at March 31, 2023, a 51% increase for the three-month period. The increase in net assets resulted from the aforementioned Ether price appreciation, partially offset by the withdrawal of approximately 18,668 Ether to pay the foregoing Sponsor’s Fee.

Cash Resources and Liquidity

The Trust has not had a cash balance at any time since inception. When selling Ether, Incidental Rights and/or IR Virtual Currency in the Digital Asset Market to pay Additional Trust Expenses on behalf of the Trust, the Sponsor endeavors to sell the exact amount of Ether, Incidental Rights and/or IR Virtual Currency needed to pay expenses in order to minimize the Trust’s holdings of assets other than Ether. As a consequence, the Sponsor expects that the Trust will not record any cash flow from its operations and that its cash balance will be zero at the end of each reporting period. Furthermore, the Trust is not a party to any off-balance sheet arrangements.

In exchange for the Sponsor’s Fee, the Sponsor has agreed to assume most of the expenses incurred by the Trust. As a result, the only ordinary expense of the Trust during the periods covered by this Quarterly Report was the Sponsor’s Fee. The Trust is not aware of any trends, demands, conditions or events that are reasonably likely to result in material changes to its liquidity needs.

16

Table of Contents

Selected Operating Data

| Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| (All Ether balances are rounded to the nearest whole Ether) |

||||||||

| Ether: |

||||||||

| Opening balance |

2,962,630 | 3,037,631 | ||||||

| Creations |

— | — | ||||||

| Sponsor’s Fee, related party |

(18,359 | ) | (18,668 | ) | ||||

|

|

|

|

|

|||||

| Closing balance |

2,944,271 | 3,018,963 | ||||||

| Accrued but unpaid Sponsor’s Fee, related party |

— | — | ||||||

|

|

|

|

|

|||||

| Net closing balance |

2,944,271 | 3,018,963 | ||||||

|

|

|

|

|

|||||

| Number of Shares: |

||||||||

| Opening balance |

310,158,500 | 310,158,500 | ||||||

| Creations |

— | — | ||||||

|

|

|

|

|

|||||

| Closing balance |

310,158,500 | 310,158,500 | ||||||

|

|

|

|

|

|||||

| As of March 31, | ||||||||

| 2024 | 2023 | |||||||

| Price of Ether on principal market (1) |

$ | 3,637.95 | $ | 1,828.98 | ||||

|

|

|

|

|

|||||

| Principal Market NAV per Share (2) |

$ | 34.53 | $ | 17.80 | ||||

|

|

|

|

|

|||||

| Index Price (3) |

$ | 3,637.90 | $ | 1,829.14 | ||||

|

|

|

|

|

|||||

| NAV per Share (3) |

$ | 34.53 | $ | 17.80 | ||||

|

|

|

|

|

|||||

| (1) | The Trust performed an assessment of the principal market at March 31, 2024 and 2023, and identified the principal market as Coinbase. |

| (2) | As of March 31, 2024 and 2023, the Principal Market NAV per Share was calculated using the fair value of Ether based on the price provided by Coinbase, the Digital Asset Trading Platform that the Trust considered its principal market, as of 4:00 p.m., New York time, on the valuation date. Prior to February 23, 2024, Principal Market NAV was referred to as NAV and Principal Market NAV per Share was referred to as NAV per Share. |

| (3) | The Trust’s NAV per Share is derived from the Index Price as represented by the Index as of 4:00 p.m., New York time, on the valuation date. The Trust’s NAV per Share is calculated using a non-GAAP methodology where the price is derived from multiple Digital Asset Trading Platforms. Prior to February 23, 2024, NAV was referred to as Digital Asset Holdings and NAV per Share was referred to as Digital Asset Holdings per Share. See “Item 1. Business – Overview of the ETH Industry and Market – ETH Value – The Index and the Index Price” in the Trust’s Annual Report on Form 10-K for a description of the Index and the Index Price. The Digital Asset Trading Platforms included in the Index as of March 31, 2024 were Coinbase, Kraken, LMAX Digital and Crypto.com. The Digital Asset Trading Platforms included in the Index as of March 31, 2023 were Coinbase, Kraken, LMAX Digital and Binance.US. See “Item 1. Business – Valuation of ETH and Determination of NAV” in the Trust’s Annual Report on Form 10-K for a description of the Trust’s NAV per Share. |

For accounting purposes, the Trust reflects creations and the Ether receivable with respect to such creations on the date of receipt of a notification of a creation but does not issue Shares until the requisite amount of Ether is received. At this time, the Trust is not accepting redemption requests from shareholders. Subject to receipt of regulatory approval from the SEC and approval by the Sponsor in its sole discretion, the Trust may in the future operate a redemption program. The Trust has not sought such relief as of the date of this Quarterly Report, and even if such relief is sought in the future, no assurance can be given as to the timing of such relief or that such relief will be granted.

As of March 31, 2024, the Trust had a net closing balance with a value of $10,710,962,523, based on the Index Price (non-GAAP methodology). As of March 31, 2024, the Trust had a total market value of $10,711,109,737, based on the Digital Asset Market price of Ether on the Trust’s principal market (Coinbase).

As of March 31, 2023, the Trust had a net closing balance with a value of $5,522,106,455, based on the Index Price (non-GAAP methodology). As of March 31, 2023, the Trust had a total market value of $5,521,623,421, based on the Digital Asset Market price of Ether on the Trust’s principal market (Coinbase).

Historical NAV and Ether Prices

As movements in the price of Ether will directly affect the price of the Shares, investors should understand recent movements in the price of Ether. Investors, however, should also be aware that past movements in the Ether price are not indicators of future movements. Movements may be influenced by various factors, including, but not limited to, government regulation, security breaches experienced by service providers, as well as political and economic uncertainties around the world.

17

Table of Contents

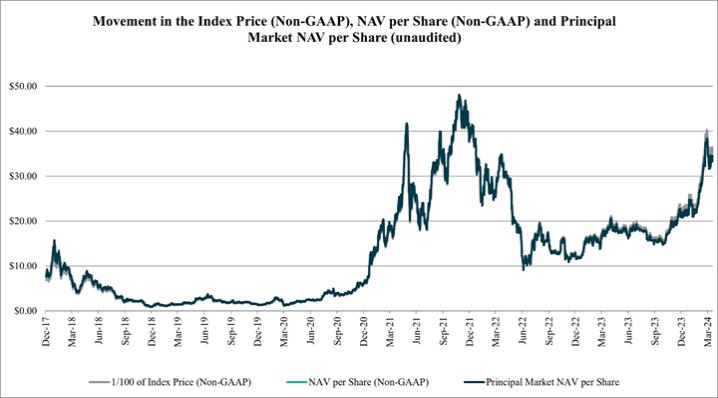

The following chart illustrates the movement in the Trust’s NAV per Share (as adjusted for the Share Split for periods prior to December 17, 2020) versus the Index Price and the Trust’s Principal Market NAV per Share (as adjusted for the Share Split for periods prior to December 17, 2020) from December 14, 2017 to March 31, 2024. For more information on the determination of the Trust’s NAV, see “Item 1. Business – Overview of the ETH Industry and Market – ETH Value – The Index and the Index Price” in the Trust’s Annual Report on Form 10-K.

18

Table of Contents

The following table illustrates the movements in the Index Price from April 1, 2019 to March 31, 2024. During such period, the Index Price has ranged from $109.83 to $4,776.32, with the straight average being $1,546.49 through March 31, 2024. The Sponsor has not observed a material difference between the Index Price and average prices from the constituent Digital Asset Trading Platforms individually or as a group.

| High | Low | |||||||||||||||||||||||||||

| Period |

Average | Index Price | Date | Index Price | Date | End of period |

Last business day |

|||||||||||||||||||||

| Twelve months ended March 31, 2020 |

$ | 194.09 | $ | 350.60 | 6/26/2019 | $ | 109.83 | 3/16/2020 | $ | 133.55 | $ | 133.55 | ||||||||||||||||

| Twelve months ended March 31, 2021 |

$ | 641.22 | $ | 1,987.17 | 2/20/2021 | $ | 130.15 | 4/1/2020 | $ | 1,900.34 | $ | 1,900.34 | ||||||||||||||||

| Twelve months ended March 31, 2022 |

$ | 3,120.63 | $ | 4,776.32 | 11/9/2021 | $ | 1,784.40 | 6/26/2021 | $ | 3,287.56 | $ | 3,287.56 | ||||||||||||||||

| Twelve months ended March 31, 2023 |

$ | 1,655.28 | $ | 3,492.35 | 4/4/2022 | $ | 913.51 | 6/18/2022 | $ | 1,829.14 | $ | 1,829.14 | ||||||||||||||||

| Twelve months ended March 31, 2024 |

$ | 2,123.36 | $ | 4,033.10 | 3/11/2024 | $ | 1,531.25 | 10/12/2023 | $ | 3,637.90 | $ | 3,566.13 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| April 1, 2019 to March 31, 2024 |

$ | 1,546.49 | $ | 4,776.32 | 11/9/2021 | $ | 109.83 | 3/16/2020 | $ | 3,637.90 | $ | 3,566.13 | ||||||||||||||||

The following table illustrates the movements in the Digital Asset Market price of Ether, as reported on the Trust’s principal market, from April 1, 2019 to March 31, 2024. During such period, the price of Ether has ranged from $110.29 to $4,776.95, with the straight average being $1,546.52 through March 31, 2024.

| High | Low | |||||||||||||||||||||||||||

| Period |

Average | Digital Asset Market Price |

Date | Digital Asset Market Price |

Date | End of period |

Last business day |

|||||||||||||||||||||

| Twelve months ended March 31, 2020 |

$ | 194.10 | $ | 350.76 | 6/26/2019 | $ | 110.29 | 3/16/2020 | $ | 133.58 | $ | 133.58 | ||||||||||||||||

| Twelve months ended March 31, 2021 |

$ | 641.25 | $ | 1,987.10 | 2/20/2021 | $ | 130.22 | 4/1/2020 | $ | 1,899.98 | $ | 1,899.98 | ||||||||||||||||

| Twelve months ended March 31, 2022 |

$ | 3,120.74 | $ | 4,776.95 | 11/9/2021 | $ | 1,785.68 | 6/26/2021 | $ | 3,284.17 | $ | 3,284.17 | ||||||||||||||||

| Twelve months ended March 31, 2023 |

$ | 1,655.32 | $ | 3,493.00 | 4/4/2022 | $ | 913.24 | 6/18/2022 | $ | 1,828.98 | $ | 1,828.98 | ||||||||||||||||

| Twelve months ended March 31, 2024 |

$ | 2,123.33 | $ | 4,033.86 | 3/11/2024 | $ | 1,530.88 | 10/12/2023 | $ | 3,637.95 | $ | 3,564.53 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| April 1, 2019 to March 31, 2024 |

$ | 1,546.52 | $ | 4,776.95 | 11/9/2021 | $ | 110.29 | 3/16/2020 | $ | 3,637.95 | $ | 3,564.53 | ||||||||||||||||

The following chart sets out the historical closing prices for the Shares as reported by OTCQX and the Trust’s NAV per Share from June 20, 2019 to March 31, 2024.

19

Table of Contents

ETHE Premium/(Discount): ETHE Share Price vs. NAV per Share (Non-GAAP) ($)

The following chart sets out the historical premium and discount for the Shares as reported by OTCQX and the Trust’s NAV per Share from June 20, 2019 to March 31, 2024.

ETHE Premium/(Discount): ETHE Share Price vs. NAV per Share (Non-GAAP) (%)

Item 3. Quantitative and Qualitative Disclosures about Market Risk

The Trust Agreement does not authorize the Trust to borrow for payment of the Trust’s ordinary expenses. The Trust does not engage in transactions in foreign currencies which could expose the Trust or holders of Shares to any foreign currency related market risk. The Trust does not invest in derivative financial instruments and has no foreign operations or long-term debt instruments.

Item 4. Controls and Procedures

The Trust maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in its Exchange Act reports is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms, and that such information is accumulated and communicated to the Principal Executive Officer and Principal Financial and Accounting Officer of the Sponsor, and to the audit committee of the board of directors of the Sponsor, as appropriate, to allow timely decisions regarding required disclosure.

20

Table of Contents

Under the supervision and with the participation of the Principal Executive Officer and the Principal Financial and Accounting Officer of the Sponsor, the Sponsor conducted an evaluation of the Trust’s disclosure controls and procedures, as defined under Exchange Act Rule 13a-15(e). Based on this evaluation, the Principal Executive Officer and the Principal Financial and Accounting Officer of the Sponsor concluded that the Trust’s disclosure controls and procedures were effective as of the end of the period covered by this report.

Changes in Internal Control Over Financial Reporting

There was no change in the Trust’s internal controls over financial reporting that occurred during the Trust’s most recently completed fiscal quarter that has materially affected, or is reasonably likely to materially affect, these internal controls.

21

Table of Contents

PART II – OTHER INFORMATION:

Item 1. Legal Proceedings

The Sponsor and an affiliate of the Trust, Grayscale Bitcoin Trust (BTC) (“Grayscale Bitcoin Trust”), are currently parties to certain legal proceedings. Although the Trust is not a party to these proceedings, the Trust may in the future be subject to legal proceedings or disputes.

On January 30, 2023, Osprey Funds, LLC (“Osprey”) filed a suit in Connecticut Superior Court against the Sponsor alleging that statements the Sponsor made in its advertising and promotion of Grayscale Bitcoin Trust violated the Connecticut Unfair Trade Practices Act, and seeking statutory damages and injunctive relief. On April 17, 2023, the Sponsor filed a motion to dismiss the complaint and, following briefing, a hearing on the motion to dismiss was held on June 26, 2023. On October 23, 2023, the Court denied the Sponsor’s motion to dismiss. On November 6, 2023, the Sponsor filed a motion for reargument of the Court’s order denying the Sponsor’s motion to dismiss. On November 16, 2023, Osprey filed an opposition to the Sponsor’s motion for reargument, and on November 30, 2023, the Sponsor filed a reply in further support of its motion for reargument. On March 11, 2024, the Court denied the Sponsor’s motion for reargument. On March 25, 2024, the Sponsor filed an application for interlocutory appeal. On March 28, 2024, Osprey filed an opposition to the Sponsor’s application for interlocutory appeal. On April 1, 2024, the Court denied the Sponsor’s application for interlocutory appeal. On April 10, 2024, Osprey filed a motion to amend the complaint. The Sponsor and Grayscale Bitcoin Trust believe this lawsuit is without merit and intend to vigorously defend against it.

In October 2021, NYSE Arca filed a proposal with the SEC pursuant to Rule 19b-4 under the Exchange Act for a rule change to list the shares of Grayscale Bitcoin Trust on NYSE Arca as an exchange-traded product, and in June 2022, the SEC issued a final order disapproving NYSE Arca’s proposed rule change. In June 2022, the Sponsor filed a petition for review of the SEC’s final order in the United States Court of Appeals for the District of Columbia Circuit. In August 2023, the D.C. Circuit Court of Appeals granted the Sponsor’s petition and vacated the SEC’s order as arbitrary and capricious. The SEC did not seek panel rehearing or rehearing en banc. In October 2023, the D.C. Circuit Court of Appeals remanded the matter to the SEC. Ultimately, on January 10, 2024, the SEC approved NYSE Arca’s 19b-4 application to list the shares of the Grayscale Bitcoin Trust on NYSE Arca as an exchange-traded product. However, even though NYSE Arca’s request with respect to Grayscale Bitcoin Trust was approved, there is no guarantee that a similar application to list Shares of the Trust on NYSE Arca, or another national securities exchange, if any, would also be approved.

On March 6, 2023, Alameda Research, Ltd. (“Alameda”) filed a suit against the Sponsor, DCG, Michael Sonnenshein and Barry Silbert, the Chief Executive Officer of DCG, in the Court of Chancery of the State of Delaware alleging various breach of contract and fiduciary duty claims, including that the defendants had breached the terms of the trust agreements of Grayscale Bitcoin Trust and the Trust for failing to reduce the Sponsor’s fees and operate a redemption program (the “Initial Complaint”). On April 4, 2023, the Sponsor, DCG, Michael Sonnenshein and Barry Silbert moved to dismiss the Initial Complaint. On May 19, 2023, the Sponsor filed a brief in support of its motion to dismiss. On September 15, 2023, Alameda filed an amended complaint (the “Amended Complaint”) alleging breach of contract and fiduciary duty claims concerning the Sponsor’s purported failure to operate a redemption program that are substantially similar to those alleged in the Initial Complaint. The Amended Complaint eliminated certain causes of action asserted in the Initial Complaint concerning the defendants’ purported breaches of the terms of the trust agreements and breaches of fiduciary duty based on the Sponsor’s fees for the Grayscale Bitcoin Trust and the Trust. On December 8, 2023, the Sponsor filed a motion to dismiss the Amended Complaint and its supporting brief. On January 19, 2024, Alameda voluntarily dismissed the action without prejudice, thereby terminating the action. No consideration of any kind was offered or exchanged in connection with Alameda’s voluntary dismissal.

As of the date of this Quarterly Report, the Sponsor does not expect the foregoing proceedings, either individually or in the aggregate, to have a material adverse effect on the Trust’s business, financial condition or results of operations.

The Sponsor and/or the Trust may be subject to additional legal proceedings and disputes in the future.

Item 1A. Risk Factors

There have been no material changes to the Risk Factors last reported under “Part I, Item 1A. Risk Factors” of the registrant’s Annual Report on Form 10-K.

22

Table of Contents

Period |

(a) Total Number of Shares of ETHE Purchased |

(b) Average Price Paid per Share of ETHE |

(c) Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (1) |

(d) Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs (1) |

||||||||||||

(in millions) |

||||||||||||||||

January 1, 2024 – January 31, 2024 |

— | $ | — | — | $ | 200.0 | ||||||||||

February 1, 2024 – February 29, 2024 |

— | — | — | 200.0 | ||||||||||||

March 1, 2024 – March 31, 2024 |

— | — | — | 200.0 | ||||||||||||

Total |

— | $ | — | — | $ | 200.0 | ||||||||||

| (1) | On March 2, 2022, the Board approved the purchase by DCG, the parent company of the Sponsor, of up to an aggregate total of $200 million worth of Shares of the Trust and shares of any of the following five investment products the Sponsor also acts as the sponsor and manager of, including Grayscale Bitcoin Trust (BTC) (NYSE Arca: GBTC), Grayscale Bitcoin Cash Trust (BCH) (OTCQX: BCHG), Grayscale Digital Large Cap Fund LLC (OTCQX: GDLC), Grayscale Ethereum Classic Trust (ETC) (OTCQX: ETCG), and Grayscale Stellar Lumens Trust (XLM) (OTCQX: GXLM). Subsequently, DCG authorized such purchase. The Share purchase authorization does not obligate DCG to acquire any specific number of Shares in any period, and may be expanded, extended, modified, or discontinued at any time. From March 2, 2022 through April 30, 2024, DCG had not purchased any Shares of the Trust under this authorization. |

Table of Contents

Item 6. Exhibits

| Exhibit |

Exhibit Description | |

| 4.1 | ||

| 10.1 | ||

| 31.1 | ||

| 31.2 | ||

| 32.1 | ||

| 32.2 | ||

| 101.INS* | Inline XBRL Instance Document – the instance document does not appear in the Interactive Data File because its XBRL tags are embedded within the Inline XBRL document. | |

| 101.SCH* | Inline XBRL Taxonomy Extension Schema Document | |

| 101.CAL* | Inline XBRL Taxonomy Extension Calculation Linkbase Document | |

| 101.LAB* | Inline XBRL Taxonomy Extension Label Linkbase Document | |

| 101.PRE* | Inline XBRL Taxonomy Extension Presentation Linkbase Document | |

| 101.DEF* | Inline XBRL Taxonomy Extension Definition Linkbase Document | |

| 104 | Cover Page Interactive Data File—The cover page interactive data file does not appear in the interactive data file because its XBRL tags are embedded within the inline XBRL document. | |

| * | Pursuant to Rule 406T of Regulation S-T, these interactive data files are deemed not filed or part of a registration statement or prospectus for purposes of Sections 11 or 12 of the Securities Act of 1933, as amended, are deemed not filed for the purposes of Section 18 of the Securities and Exchange Act of 1934, as amended, and otherwise are not subject to liability under those sections. |

24

Table of Contents

GLOSSARY OF DEFINED TERMS

“Actual Exchange Rate”— With respect to any particular asset, at any time, the price per single unit of such asset (determined net of any associated fees) at which the Trust is able to sell such asset for U.S. dollars (or other applicable fiat currency) at such time to enable the Trust to timely pay any Additional Trust Expenses, through use of the Sponsor’s commercially reasonable efforts to obtain the highest such price.

“Additional Trust Expenses”— Together, any expenses incurred by the Trust in addition to the Sponsor’s Fee that are not Sponsor-paid Expenses, including, but not limited to, (i) taxes and governmental charges, (ii) expenses and costs of any extraordinary services performed by the Sponsor (or any other service provider) on behalf of the Trust to protect the Trust or the interests of shareholders (including in connection with any Incidental Rights and any IR Virtual Currency), (iii) any indemnification of the Custodian or other agents, service providers or counterparties of the Trust, (iv) the fees and expenses related to the listing, quotation or trading of the Shares on any Secondary Market (including legal, marketing and audit fees and expenses) to the extent exceeding $600,000 in any given fiscal year and (v) extraordinary legal fees and expenses, including any legal fees and expenses incurred in connection with litigation, regulatory enforcement or investigation matters.

“Administrator”— The Bank of New York Mellon, a New York corporation authorized to do a banking business.

“Administrator Fee”— The fee payable to any administrator of the Trust for services it provides to the Trust, which the Sponsor will pay such administrator as a Sponsor-paid Expense.

“Agent”— A Person appointed by the Trust to act on behalf of the shareholders in connection with any distribution of Incidental Rights and/or IR Virtual Currency.

“Authorized Participant”— Certain eligible financial institutions that have entered into an agreement with the Trust and the Sponsor concerning the creation of Shares. Each Authorized Participant (i) is a registered broker-dealer, (ii) has entered into a Participant Agreement with the Sponsor and (iii) owns a digital wallet address that is known to the Custodian as belonging to the Authorized Participant or a Liquidity Provider.

“Basket”— A block of 100 Shares.

“Basket Amount”— On any trade date, the amount of Ether required as of such trade date for each Creation Basket, as determined by dividing (x) the amount of Ether owned by the Trust at 4:00 p.m., New York time, on such trade date, after deducting the amount of Ether representing the U.S. dollar value of accrued but unpaid fees and expenses of the Trust (converted using the Index Price at such time, and carried to the eighth decimal place), by (y) the number of Shares outstanding at such time (with the quotient so obtained calculated to one one-hundred-millionth of one Ether (i.e., carried to the eighth decimal place)), and multiplying such quotient by 100.

“Blockchain” or “Ethereum Blockchain”— The public transaction ledger of the Ethereum Network on which transactions in Ether are recorded.

“Creation Basket”— Basket of Shares issued by the Trust in exchange for deposits of the Basket Amount required for each such Creation Basket.

“Custodial Services”— The Custodian’s services that (i) allow Ether to be deposited from a public blockchain address to the Trust’s Digital Asset Account and (ii) allow the Trust and the Sponsor to withdraw Ether from the Trust’s Digital Asset Account to a public blockchain address the Trust or the Sponsor controls pursuant to instructions the Trust or the Sponsor provides to the Custodian.

“Custodian”— Coinbase Custody Trust Company, LLC.

“Custodian Agreement”— The Amended and Restated Custodial Services Agreement, dated as of June 29, 2022, by and between the Trust and the Sponsor and Custodian that governs the Trust’s and the Sponsor’s use of the Custodial Services provided by the Custodian as a fiduciary with respect to the Trust’s assets.

“Custodian Fee”— Fee payable to the Custodian for services it provides to the Trust, which the Sponsor shall pay to the Custodian as a Sponsor-paid Expense.

“DCG”— Digital Currency Group, Inc.

25

Table of Contents

“Digital Asset Account”— A segregated custody account controlled and secured by the Custodian to store private keys, which allow for the transfer of ownership or control of the Trust’s Ether on the Trust’s behalf.

“Digital Asset Market”— A “Brokered Market,” “Dealer Market,” “Principal-to-Principal Market” or “Exchange Market” (referred to as “Trading Platform Market” in this Quarterly Report), as each such term is defined in the Financial Accounting Standards Board Accounting Standards Codification Master Glossary.

“Digital Asset Trading Platform”— An electronic marketplace where trading platform participants may trade, buy and sell Ether based on bid-ask trading. The largest Digital Asset Trading Platforms are online and typically trade on a 24-hour basis, publishing transaction price and volume data.

“Digital Asset Trading Platform Market”— The global trading platform market for the trading of Ether, which consists of transactions on electronic Digital Asset Trading Platforms.

“DSTA”— The Delaware Statutory Trust Act, as amended.

“DTC”— The Depository Trust Company. DTC is a limited purpose trust company organized under New York law, a member of the U.S. Federal Reserve System and a clearing agency registered with the SEC. DTC will act as the securities depository for the Shares.

“Ether”— Ethereum tokens, which are a type of digital asset based on an open source cryptographic protocol existing on the Ethereum Network, comprising units that constitute the assets underlying the Trust’s Shares.

“Ethereum Network”— The online, end-user-to-end-user network hosting the public transaction ledger, known as the Ethereum Blockchain, and the source code comprising the basis for the cryptographic and algorithmic protocols governing the Ethereum Network. See “Item 1. Business—Overview of the ETH Industry and Market” in our Annual Report.

“Ethereum Proof-of-Work” or “ETHPoW”— A type of digital currency based on an open source cryptographic protocol existing on the Ethereum Proof-of-Work network, which came into existence following the Ethereum hard fork on September 15, 2022.

“Exchange Act”— The Securities Exchange Act of 1934, as amended.

“FINRA”— The Financial Industry Regulatory Authority, Inc., which is the primary regulator in the United States for broker-dealers, including Authorized Participants.

“GAAP”— United States generally accepted accounting principles.

“Genesis”— Genesis Global Trading, Inc., a wholly owned subsidiary of Digital Currency Group, Inc., which served as a Liquidity Provider from October 3, 2022 to September 12, 2023.

“Grayscale Securities”— Grayscale Securities, LLC, a wholly owned subsidiary of the Sponsor, which as of the date of this Quarterly Report, is the only acting Authorized Participant.

“Incidental Rights”— Rights to acquire, or otherwise establish dominion and control over, any virtual currency or other asset or right, which rights are incident to the Trust’s ownership of Ether and arise without any action of the Trust, or of the Sponsor or Trustee on behalf of the Trust.

“Index”— The CoinDesk Ether Price Index (ETX).

“Index License Agreement”— The license agreement, dated as of February 1, 2022, between the Index Provider and the Sponsor governing the Sponsor’s use of the Index for calculation of the Index Price, as amended by Amendment No. 1 thereto and as the same may be amended from time to time.

“Index Price”— The U.S. dollar value of an Ether derived from the Digital Asset Trading Platforms that are reflected in the Index, calculated at 4:00 p.m., New York time, on each business day. See “Item 1. Business—Overview of the ETH Industry and Market—ETH Value—The Index and the Index Price” in our Annual Report for a description of how the Index Price is calculated. For purposes of the Trust Agreement, the term Ether Index Price shall mean the Index Price as defined herein.

“Index Provider”— CoinDesk Indices, Inc., a Delaware corporation that publishes the Index. Prior to its sale to an unaffiliated third party on November 20, 2023, DCG was the indirect parent company of CoinDesk Indices, Inc. As a result, CoinDesk Indices, Inc. was an affiliate of the Sponsor and the Trust and was considered a related party of the Trust.

26

Table of Contents

“Investment Advisers Act”— Investment Advisers Act of 1940, as amended.

“Investment Company Act”— Investment Company Act of 1940, as amended.

“Investor”— Any investor that has entered into a subscription agreement with an Authorized Participant, pursuant to which such Authorized Participant will act as agent for the investor.

“IR Virtual Currency”— Any virtual currency tokens, or other asset or right, acquired by the Trust through the exercise (subject to the applicable provisions of the Trust Agreement) of any Incidental Right.

“Liquidity Provider”— A service provider that facilitates the purchase of Ether in connection with the creation of Baskets.

“Marketing Fee”— Fee payable to the marketer for services it provides to the Trust, which the Sponsor will pay to the marketer as a Sponsor-paid Expense.

“NAV”— The aggregate value, expressed in U.S. dollars, of the Trust’s assets (other than U.S. dollars or other fiat currency), less its liabilities (which include estimated accrued but unpaid fees and expenses), a Non-GAAP metric, calculated in the manner set forth under “Item 1. Business—Valuation of ETH and Determination of NAV” in our Annual Report. See also “Item 1. Business—Investment Objective” in our Annual Report for a description of the Trust’s Principal Market NAV, as calculated in accordance with GAAP. Prior to February 23, 2024, NAV was referred to as Digital Asset Holdings.

“NAV Fee Basis Amount”— The amount on which the Sponsor’s Fee for the Trust is based, as calculated in the manner set forth under “Item 1. Business—Valuation of ETH and Determination of NAV” in our Annual Report.

“OTCQX”— The OTCQX tier of OTC Markets Group Inc.

“Participant Agreement”— An agreement entered into by an Authorized Participant with the Sponsor that provides the procedures for the creation of Baskets and for the delivery of Ether required for Creation Baskets.

“Principal Market NAV”— The net asset value of the Trust determined on a GAAP basis. Prior to February 23, 2024, Principal Market NAV was referred to as NAV.

“SEC”— The U.S. Securities and Exchange Commission.

“Secondary Market”— Any marketplace or other alternative trading system, as determined by the Sponsor, on which the Shares may then be listed, quoted or traded, including but not limited to, the OTCQX tier of the OTC Markets Group Inc.

“Securities Act”— The Securities Act of 1933, as amended.

“Shares”— Common units of fractional undivided beneficial interest in, and ownership of, the Trust.

“Share Split”— A 9-for-1 Share split of the Trust’s issued and outstanding Shares, which was effective on December 17, 2020 to shareholders of record as of the close of business on December 14, 2020.

“Sponsor”— Grayscale Investments, LLC.

“Sponsor-paid Expenses”— The fees and expenses incurred by the Trust in the ordinary course of its affairs that the Sponsor is obligated to assume and pay, excluding taxes, but including: (i) the Marketing Fee, (ii) the Administrator Fee, (iii) the Custodian Fee and fees for any other security vendor engaged by the Trust, (iv) the Transfer Agent fee, (v) the Trustee fee, (vi) the fees and expenses related to the listing, quotation or trading of the Shares on any Secondary Market (including customary legal, marketing and audit fees and expenses) in an amount up to $600,000 in any given fiscal year, (vii) ordinary course, legal fees and expenses, (viii) audit fees, (ix) regulatory fees, including, if applicable, any fees relating to the registration of the Shares under the Securities Act or the Exchange Act, (x) printing and mailing costs, (xi) costs of maintaining the Trust’s website and (xii) applicable license fees, provided that any expense that qualifies as an Additional Trust Expense will be deemed to be an Additional Trust Expense and not a Sponsor-paid Expense.

“Sponsor’s Fee”— A fee, payable in Ether, which accrues daily in U.S. dollars at an annual rate of 2.5% of the NAV Fee Basis Amount of the Trust as of 4:00 p.m., New York time, on each day; provided that for a day that is not a business day, the

27

Table of Contents

calculation of the Sponsor’s Fee will be based on the NAV Fee Basis Amount from the most recent business day, reduced by the accrued and unpaid Sponsor’s Fee for such most recent business day and for each day after such most recent business day and prior to the relevant calculation date.

“Transfer Agent”— Continental Stock Transfer & Trust Company, a Delaware corporation.

“Transfer Agent Fee”— Fee payable to the Transfer Agent for services it provides to the Trust, which the Sponsor will pay to the Transfer Agent as a Sponsor-paid Expense.

“Trust”— Grayscale Ethereum Trust (ETH), a Delaware statutory trust, formed on December 13, 2017 under the DSTA and pursuant to the Trust Agreement.

“Trust Agreement”— The Amended and Restated Declaration of Trust and Trust Agreement between the Trustee and the Sponsor establishing and governing the operations of the Trust, as amended by Amendments No. 1, No. 2, and No. 3 thereto and as the same may be amended from time to time.

“Trustee”— Delaware Trust Company (formerly known as CSC Trust Company of Delaware), a Delaware trust company, is the Delaware trustee of the Trust.

“U.S.”— United States.

“U.S. dollar” or “$”— United States dollar or dollars.

28

Table of Contents

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned in the capacities* indicated, thereunto duly authorized.

| Grayscale Investments, LLC | ||||

| as Sponsor of Grayscale Ethereum Trust (ETH)

| ||||

| By: | /s/ Michael Sonnenshein | |||

| Name: | Michael Sonnenshein | |||

| Member of the Board of Directors | ||||

| and Chief Executive Officer | ||||

| Title: | (Principal Executive Officer)*

| |||

| By: | /s/ Edward McGee | |||

| Name: | Edward McGee | |||

| Member of the Board of Directors and Chief Financial Officer | ||||

| Title: | (Principal Financial Officer and Principal Accounting Officer)* | |||

Date: May 3, 2024

| * | The Registrant is a trust and the persons are signing in their capacities as officers or directors of Grayscale Investments, LLC, the Sponsor of the Registrant. |

29