UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

OR

Commission File Number

(Exact name of Registrant as specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer |

(

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

☒ |

|

Accelerated filer |

|

☐ |

|

Non-accelerated filer |

|

☐ |

|

Small reporting company |

|

|

|

|

|

|

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the $66.97 closing price of the shares of common stock on the New York Stock Exchange on June 30, 2023, was $

The number of shares of Registrant’s Common Stock outstanding as of February 23, 2024 was

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement relating to the 2024 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the Registrant’s fiscal year ended December 31, 2023.

1 |  2023 Form 10-K

2023 Form 10-K

Table of Contents

|

|

Page |

PART I |

|

|

Item 1. |

4 |

|

Item 1A. |

11 |

|

Item 1B. |

26 |

|

Item 1C. |

26 |

|

Item 2. |

27 |

|

Item 3. |

27 |

|

Item 4. |

27 |

|

|

|

|

PART II |

|

|

Item 5. |

28 |

|

Item 6. |

29 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

30 |

Item 7A. |

45 |

|

Item 8. |

47 |

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

95 |

Item 9A. |

95 |

|

Item 9B. |

96 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

96 |

|

|

|

PART III |

|

|

Item 10. |

97 |

|

Item 11. |

97 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

97 |

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

98 |

Item 14. |

98 |

|

|

|

|

PART IV |

|

|

Item 15. |

99 |

2 | 2023 Form 10-K

Unless the context requires otherwise, references in this Annual Report on Form 10-K (“Form 10-K”) to “our company,” the “Company,” “we,” “us,” and “our” refer to Dayforce, Inc. and its direct and indirect subsidiaries on a consolidated basis. References to Dayforce reflect the Dayforce people platform. Effective January 31, 2024, Ceridian HCM Holding Inc. changed its corporate name to Dayforce, Inc. We ceased trading under the ticker symbol "CDAY" and began trading under our new ticker symbol, "DAY," on the New York Stock Exchange ("NYSE"), and Toronto Stock Exchange ("TSX") effective on February 1, 2024.

We and our subsidiaries own or have the rights to various trademarks, trade names and service marks, including the following: Dayforce®, Ceridian®, Powerpay® and various logos used in association with these terms. Solely for convenience, the trademarks, trade names and service marks and copyrights referred to herein are listed without the ©, ®, and ™, symbols, but such references are not intended to indicate, in any way, that Dayforce, Inc., or the applicable owner, will not assert, to the fullest extent under applicable law, our or their, as applicable, rights to these trademarks, trade names, and service marks. Other trademarks, service marks, or trade names appearing in this Form 10-K are the property of their respective owners.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K contains, or incorporates by reference, not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (“Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”) and that are subject to the safe harbor created by those sections. All statements other than statements of historical fact or relating to present facts or current conditions included in this Form 10-K are forward-looking statements. Forward-looking statements give our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance and business. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “anticipate,” “estimate,” “expect,” "assume", “project,” “seek,” “plan,” “intend,” “believe,” “will,” “may,” “could,” “continue,” “likely,” “should,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events but not all forward-looking statements contain these identifying words.

Forward-looking statements are based on our current expectations and assumptions regarding our business, the economy, and other future conditions. Because forward-looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by the forward-looking statements. Important factors that could cause actual results to differ materially from those in the forward-looking statements include regional, national, or global political, economic, business, competitive, market, and regulatory conditions and those risks described in Part I, Item IA, “Risk Factors” of this Form 10-K. Although we have attempted to identify important risk factors, there may be other risk factors not presently known to us or that we presently believe are not material that could cause actual results and developments to differ materially from those made in or suggested by the forward-looking statements contained in this Form 10-K. If any of these risks materialize, or if any of the above assumptions underlying forward-looking statements prove incorrect, actual results and developments may differ materially from those made in or suggested by the forward-looking statements contained in this Form 10-K. For the reasons described above, we caution against relying on any forward-looking statements. Any forward-looking statement made by us in this Form 10-K speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update or to revise any forward-looking statement, whether as a result of new information, future developments, or otherwise, except as may be required by law. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should be viewed as historical data.

3 | 2023 Form 10-K

PART I

Item 1. Business.

Overview

Dayforce, Inc., formerly known as Ceridian HCM Holding Inc., is a global human capital management (“HCM”) software company. Dayforce, our flagship Cloud HCM platform, provides a full suite of HCM functionality, including global human resources (“HR”), payroll and tax, workforce management, benefits, and talent intelligence functionality. In addition to Dayforce, we sell Powerpay, a Cloud HR and payroll solution for the Canadian small business market, through both direct sales and established partner channels. We also continue to support customers using our legacy North America solutions and customers using our acquired solutions in the Asia Pacific Japan ("APJ") region. We invest in maintenance and necessary updates with the legacy technology to support our customers and continue to migrate them to Dayforce. Revenue from our recurring solutions includes investment income generated from holding customer funds, also referred to as float revenue or float.

The following five strategic growth levers drive our long-term perspectives, near-term decision making, and stockholder alignment:

Products and Solutions

Dayforce

Dayforce is a single application that provides continuous real-time calculations across all modules to enable, for example, payroll administrators access to data through the entire pay period, and managers access to real-time data to optimize work schedules. Our Dayforce platform is used by organizations, regardless of industry or size, to optimize management of the entire employee lifecycle, including attracting, hiring, engaging, paying, and developing their people. In 2023, we received several accolades for our Dayforce solution, including being named as a Leader in the 2023 Gartner® Magic Quadrant™ for Cloud HCM Suites for 1,000+ Employee Enterprises for the fourth consecutive year; Leader in compliance, payroll administration, and overall product satisfaction in the Gartner Critical Capabilities for Cloud HCM suites for 1000+ Employee Enterprises; Top 5 solution in the 2023 Constellation Shortlist™ for both Global HCM Suites and Workforce Management Suites; Leader in the Sapient Insights Group HR Systems Survey for Time Management Systems and in the Sapient Insights HR Survey - HRMS Voice of the Customer User Experience and Vendor Satisfaction.

Human Resources

Dayforce Human Resources provides HR professionals, managers, and employees a single, complete record for all of their HR information. Our HR functionality is centered on a comprehensive, flexible workflow engine that streamlines and automates administrative tasks. The component maintains a record of critical forms for the employee, such as signed workplace policy agreements, Occupational Safety and Health Administration regulations, and direct deposit information.

In addition to its primary record-keeping functionality, Dayforce HR comes with an organizational management system that allows managers to view the profiles of their team members, which includes contact and time off details, as well as pay, benefits, and performance data. It is also accessible to employees, who can view the organizational chart, appropriate information about other employees in the organization, and their own pay and time details. There are several self-service options available in the product as well, such as change of address or adding a dependent, making it easy for employees to keep their profiles up to date.

4 | 2023 Form 10-K

Payroll and Tax

Dayforce empowers employers to manage their global payroll needs within a single system. Through our Dayforce platform, payroll administrators with localized payroll functionality are able to make updates to time and pay in real-time. Dayforce supports payroll in over 200 countries and territories around the world, whilst providing employers with a centralized global view of their payroll data. This global payroll model is powered by a combination of company-owned and partner unified payroll engines with an automated data exchange that affords employees and administrators to have a consistent, intuitive single user experience. Native payroll is available in certain countries across North America, APJ, and Europe, the Middle East, and Africa ("EMEA"), where Dayforce’s continuous calculation engine offers flexibility, accuracy, and efficiency in the payroll process. In these native markets, we also manage the movement and remittance of taxes to tax authorities on behalf of our customers. With a flexible rules-based configuration and regional partnerships, Dayforce helps organizations with regulation and compliance concerns regardless of where employees work or live. We are continuing to innovate and expand payroll functionality into new markets to enhance the customer experience for large enterprises operating globally.

In addition to customers who use our payroll services, certain customers use our tax filing services on a stand-alone basis. We recently modernized the technology platforms used to provide stand-alone tax services. Beginning in 2023, with the technology migration complete, we classified recurring revenues from stand-alone tax customers as Dayforce recurring revenue.

Workforce Management

Dayforce Workforce Management helps organizations equitably manage their workforces, improve operational efficiency, and enhance compliance by configuring the system to meet complex employment and working time rules and policies. Through Dayforce Workforce Management, customers are offered time and attendance, absence management, scheduling, task management, and labor planning. A variety of options are available for organizations to capture time and attendance data such as physical clocks and the mobile application.

Dayforce Wallet

Dayforce Wallet is a digital payment solution that gives employees instant access to their net earnings through on-demand pay requests. With Dayforce Wallet, employees’ funds are loaded onto a paycard, which generates interchange fee revenue when used. As of December 31, 2023, we had more than 1,860 customers signed onto Dayforce Wallet with over 1,150 customers live on the product and the average registration rate was above 60% of all eligible employees.

Benefits

Dayforce Benefits assists benefits administrators from enrollment to ongoing benefits administration, including eligibility, open enrollment and Affordable Care Act ("ACA") management. Our proprietary Benefits Decision Support scoring system guides employees through a self-service experience, giving information about each of the available benefit plans and the impact of plan options, to help them choose the best option for their specific needs.

The system integrates with hundreds of benefits carriers, contains a library of qualifiers to help define eligibility rules, and leverages real-time connections to payroll and HR to inform eligibility and calculate employee deductions. In addition, we offer Benefits Intelligence, which leverages enrollment data to get visibility into elections at the plan and option levels to help administrators analyze their program.

Talent Intelligence

Dayforce Talent Intelligence, a suite of next generation talent acquisition and talent management solutions powered by Artificial Intelligence (“AI”) and driven by data, helps organizations recruit, hire, retain, and develop their workforce. Dayforce Talent Intelligence transforms talent management and recruitment strategies by using AI in conjunction with talent data from across the employee lifecycle to provide organizations insights that enable them to make more efficient, accurate, and fair talent decisions. Talent Intelligence can also objectively measure workforce demographics while identifying inequity in everything from payroll to promotion opportunities to help employers create actionable policy changes. Customers can leverage Talent Intelligence tools for recruiting, onboarding, engagement, performance management, succession planning, compensation management, and employee career planning and skills development.

5 | 2023 Form 10-K

Powerpay

Powerpay is a Cloud platform that provides scalable and straightforward payroll and HR solutions. We offer Powerpay for Canadian organizations with fewer than 100 employees.

Other

We also offer payroll and payroll-related services using legacy technology and on-premise technology from our acquired businesses in APJ, which we formerly referred to as Bureau. We invest in maintenance and necessary updates to support our customers. However, we generally stopped selling our legacy North America payroll solutions to new customers in the United States ("U.S.") and Canada, and we intend to stop actively selling our acquired on-premise payroll solutions to new customers on a stand-alone basis. In addition to customers who use our legacy payroll services, prior to modernizing the technology platforms utilized for stand-alone tax services, certain customers used our legacy tax filing services on a stand-alone basis through 2022.

Services and Support

We offer a broad portfolio of services to enable customer success. We believe it is important to work closely with our customers to understand their needs and deliver technology solutions and support that address them. We continue to increase our global reach in supporting and serving our customers. As part of our international strategy, we work with partners to perform services in certain geographies where we do not currently have international operations or the particular service required by our customers.

Implementation and Professional Services

Our internal implementation team leverages proprietary onboarding technology for new customer activation and professional services work. Our internal team is supplemented by third party services partners and system integration partners (“SI”). Our implementation services include solution configuration and activation for new customers. Professional services include add-on implementation services for existing customers, ongoing product configuration changes when the customer does not have the resources to do it themselves, product usage consulting and a variety of additional services, such as report writing, usage audits, and process improvement.

Customer Support

Our global customer support organization provides 24/7 application support from locations across North America, APJ, and EMEA. Our support function is organized into teams of representatives with deep product and domain expertise across our platform. These teams are aligned to groups of customers based on geography and product type to provide a combination of deep product and industry knowledge, consistent relationships, and high availability.

Customers

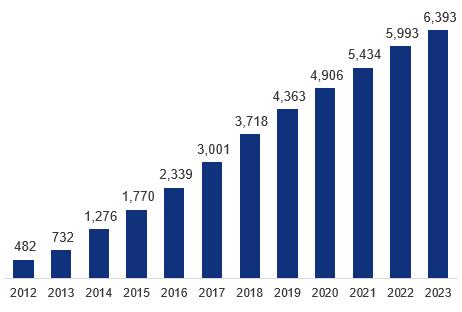

Dayforce is designed to serve organizations with 100 to over 100,000 employees. The Dayforce customer base has increased from 482 as of December 31, 2012 to 6,393 customers* on the platform as of December 31, 2023 representing approximately 6.84 million global employees*. We define a customer as a single organization, such as a company, a non-profit association, an educational institution, or government entity. We also have approximately 38,000 Powerpay customer accounts. No single customer accounted for more than 2% of our revenues during the year ended December 31, 2023.

Selling and Marketing

We sell our Cloud solutions through a direct sales force and a variety of third-party channels, organized by customer size and geography. We market Dayforce to organizations with more than 100 employees. We market Powerpay to organizations with fewer than 100 employees in Canada. The majority of our revenue growth comes from new Cloud customers.

* Excluding the 2021 acquisitions of Ascender HCM Pty Limited ("Ascender") and ATI ROW, LLC and Dayforce Mexico S. de R.L. de C.V. (formerly known as ADAM HCM MEXICO, S. de R.L. de C.V.) (collectively, "ADAM HCM")

6 | 2023 Form 10-K

Technology, Hosting, and Research and Development (“R&D”)

Technology and innovation are at the core of Dayforce, Inc. Our innovation and development process is customer-driven. We work directly with customers to understand their needs and to deliver solutions that address their challenges, taking into consideration the entire user experience, without being constrained by individual modules or applications. We are committed to protecting the information of our customers, our employees, and our contractors, along with other business data.

Our R&D team is responsible for the design, development, and testing of our applications. We believe that our modern Cloud technology stack, agile design and development methodology, and efficient software deployment process enable us to innovate quickly in response to industry trends. We host Cloud-based applications and serve the majority of our customers from data centers operated by third party providers, primarily Microsoft Azure, AWS, VMWare Cloud on AWS, and Navisite. While we control and have access to our servers and all of the components of our network that are located in our external data centers, we do not control the operation of these facilities. Additionally, we host our internal systems through data centers that we operate and lease in the U.S. and APJ.

Dayforce National Trust Bank

The Office of Comptroller of the Currency (the "OCC") authorized the Ceridian National Trust Bank (the "CNTB") to open on January 3, 2023. Effective on this date, the CNTB commenced banking operations, acting as trustee for our U.S. payroll trust. Historically, certain aspects of our U.S. client money movement activity were subject to regulation at both the federal and individual state levels with resulting inherent complexity across multiple jurisdictions. With the establishment of the CNTB, U.S. regulatory oversight will now be under the OCC, a single federal government agency. Our payroll trust structure will continue to benefit our customers by providing bankruptcy-remoteness protection for client funds pending remittance to employees of our clients, tax authorities, and other payees. On January 31, 2024, the CNTB became the Dayforce National Trust Bank (the "DNTB").

Intellectual Property

Our success depends, in part, on our ability to protect our proprietary technology and intellectual property. We rely on a combination of patents, copyrights, trade secrets, trade names, and trademarks, as well as confidentiality and nondisclosure agreements and other contractual protections, to establish and to safeguard our intellectual property rights.

Competition

The market for HCM technology solutions is highly competitive and subject to changing technology and shifting client needs. We compete with firms that provide both integrated and point solutions for HCM, as well as with local providers in each jurisdiction that we operate. Globally, we compete with legacy payroll service providers, as well as Cloud-enabled client-server HCM providers. We also face competition from modern HCM providers, whose solutions have been specifically built as single application platforms in the Cloud. In addition, we face competition from large, long-established enterprise application software vendors.

Competition in the global HCM market is primarily based on product and service quality, including ease of use and accessibility of technology, breadth of offerings, reputation, and price. We believe that we are competitive in each of these areas and that our single application always-on technology and product innovations, combined with our commitment to service and our geographic reach, distinguishes us from our competitors.

Seasonality

We have in the past and expect in the future to experience seasonal fluctuations in our revenues and new customer contracts with the fourth quarter historically being our strongest quarter for new customer contracts, renewals, and customer go-lives. Although the growth of our Cloud solutions and the ratable nature of our fees makes this seasonality less apparent in our overall results of operations, we expect our revenue to fluctuate quarterly and to be higher in the fourth and first quarters of each year. Fourth quarter revenue is driven by year-end processing fees and Dayforce customer go-lives; and first quarter revenue is driven by revenue earned for printing of year-end tax packages.

Environmental, Social, and Governance ("ESG") and Human Capital

We believe that transparency and accountability are essential to any company’s success. Our approach to ESG and Human Capital is guided by five pillars: Governance and Trust; Our People; Tech for Good; Our Communities; and the Environment.

7 | 2023 Form 10-K

Governance and Trust

We safeguard the trust given to us by our partners, our customers, and their employees. This means upholding high standards of corporate governance and ethics, ensuring customer data is protected, and developing products that are reliable and effective.

Our People

As of December 31, 2023, we had 9,084 employees, including 4,563 employees in North America, 2,906 in APJ, and 1,615 in EMEA. We provide a wide range of compensation and benefits to our employees that enhance the workplace experience. In addition to salaries, these benefits (which vary by country and region) include annual bonuses, equity awards, a global employee stock purchase program, retirement savings plans, healthcare and insurance benefits, fertility and family building benefits, health savings and flexible savings spending accounts, unlimited time away from work, parental leave, flexible and remote work options, employee assistance programs, and tuition reimbursement.

Promoting diversity, equity, and inclusion within our workforce is also a priority for us. We have a company-wide employee Global Diversity Advisory Council, and our nine employee resource groups foster inclusion, connection, and career development opportunities for their members. Our Achieving Corporate Equity program helps to empower high-potential diverse talent and improve the internal mobility of employees from underrepresented and underserved communities.

As of December 31, 2023, women represented approximately 50% of our global workforce, including approximately 44% of employees in manager-level roles and above, and approximately 36% in vice president-level roles and above. In the U.S., approximately 12% of our workforce was Asian, 11% was Black or African American, 6% was Hispanic or Latino, 3% was multiracial, less than 1% was Native Hawaiian or Pacific Islander, American Indian or Alaska Native, and approximately 65% was White. In the U.S., people of color represented approximately 24% of employees in manager-level roles and above, and approximately 27% of employees in vice president-level roles and above.

The health, safety, and wellbeing of our employees is of high importance to us. We host an annual global Mental Health Summit, and we offer two paid wellness days to all employees. In addition, our global emergency threat monitoring and mass communications system helps to ensure connectivity and support for our employees both during and after natural disasters and other dangerous events.

We are committed to providing meaningful professional development opportunities to our workforce. We maintain a culture of continuous learning and empowerment through programs that include professional skills training, leadership development, and job shadowing and job rotation opportunities.

Our ability to attract and retain top talent remains critical to our continued success as a business, and our employee Net Promoter Score in 2023 was 50.

Tech for Good

We believe that Tech for Good and responsible innovation can have a positive impact on all stakeholders. Our Dayforce Wallet product provides individuals with on-demand access to their earned pay, which enables them to better cover both everyday expenses as well as any urgent or unplanned costs. Our AI Governance Framework closely evaluates the potential use of AI from idea through all key stages of the product development lifecycle. Our Dayforce Engagement product helps our customers build a culture of inclusion and respect within their workforce, and it gives them the ability to measure employee sentiment on equity and belonging. Our Career Explorer product provides our customers’ employees access to data-driven career pathing, gives them information about open internal roles that match their interests and abilities, and provides actionable steps to help them reach their career goals.

Our Communities

We are committed to giving back to the communities in which we live and work. Through our employee-led charity Dayforce Cares, formerly Ceridian Cares, we provide financial support to individuals and families struggling with basic needs and quality of life across the U.S. and Canada. Since its inception, the foundation has given over $6.5 million in grants to over 4,500 people in need. In addition, 50% of our employees globally participated in our giving and volunteering program in 2023.

8 | 2023 Form 10-K

Environment

We are committed to doing our part to help address the climate crisis. This includes actively working to decrease our carbon footprint by pursuing two near-term reduction targets that cover Scope 1, 2, and 3 emissions. Our decarbonization strategy includes consolidating our physical footprint globally, expanding our cloud strategy to sustainably deliver our data and technology solutions, and significantly reducing our in-house print operations. Each year, we source 100% renewable electricity across our global operations through the purchase of high-quality Energy Attribute Certificates. In 2023, we launched a new Responsible Sourcing Initiative to enhance the sustainability of our supply chain. We also developed a company-wide Environmental Sustainability Policy and added new provisions to our Vendor Code of Conduct to further embed sustainable practices into our direct operations and procurement processes.

We encourage you to review our ESG Report for more detailed information which can be found on our website at https://www.dayforce.com/who-we-are/corporate-responsibility. In addition, past ESG reports, our Task Force on Climate-related Financial Disclosures Index, SASB Index, consolidated EEO-1 report, and ESG-related policies and principles can be found here. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference into, and is not considered part of, this Form 10-K.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements, Section 16 reports, and amendments to reports and any registration statements filed or furnished pursuant to Sections 13(a), 14 and 15(d) of the Exchange Act are available, free of charge at http://investors.dayforce.com as soon as reasonably practicable after we file such material with, or furnish it to, the Securities and Exchange Commission (“SEC”), and are also available on the SEC’s website at http://www.sec.gov.

Our restated certificate of incorporation, our fourth amended and restated bylaws, charters of our Acquisition and Finance, Audit, Compensation, and Corporate Governance and Nominating Committees of our Board of Directors (the “Board”), our Corporate Governance Guidelines, and our Code of Conduct, as well as any waivers from and amendments to our Code of Conduct are available on our website at https://investors.dayforce.com/corporate-governance/governance-documents. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference into, and is not considered part of, this Form 10-K.

Information about Our Executive Officers

Our executive officers as of February 28, 2024 are as follows:

Name |

|

Age |

|

Position |

David D. Ossip |

|

57 |

|

Chair and Chief Executive Officer |

Samer Alkharrat |

|

55 |

|

Executive Vice President and Chief Revenue Officer |

Christopher R. Armstrong |

|

55 |

|

Executive Vice President and Chief Operating Officer |

Stephen H. Holdridge |

|

63 |

|

President, Customer and Revenue Operations |

Jeffrey S. Jacobs |

|

48 |

|

Head of Accounting and Financial Reporting |

Jeremy R. Johnson |

|

40 |

|

Executive Vice President and Chief Financial Officer |

Joseph B. Korngiebel |

|

53 |

|

Executive Vice President, Chief Product and Technology Officer |

William E. McDonald |

|

59 |

|

Executive Vice President, General Counsel and Corporate Secretary |

David D. Ossip

Mr. Ossip is our Chair of the Board and Chief Executive Officer. Mr. Ossip has held the position of Chair since August 2015 and sole Chief Executive Officer since November 2023. Previously, Mr. Ossip served as our Co-Chief Executive Officer from February 2022 until November 2023, and our Chief Executive Officer from July 2013 until February 2022. Mr. Ossip joined the Company following the Company’s acquisition of Dayforce Corporation in 2012, where he held the position of Chief Executive Officer. Mr. Ossip previously served as a director for Dragoneer Growth Opportunities Corp., a NYSE listed company, Dragoneer Growth Opportunities Corp. II, a Nasdaq listed company, and Dragoneer Growth Opportunities Corp. III, a Nasdaq listed company.

9 | 2023 Form 10-K

Samer Alkharrat

Mr. Alkharrat is our Executive Vice President and Chief Revenue Officer, positions he has held since June 2023. Prior to joining the Company, Mr. Alkharrat served as Chief Partner Officer at Workday, Inc., a provider of enterprise cloud applications, from March 2022 to February 2023. Previously, he held the position of President and Chief Revenue Officer at C3 AI, an artificial intelligence software provider, from June 2021 to February 2022. Prior to that, he served as the Senior Vice President of Worldwide Sales at VMware LLC, a cloud service provider, from November 2019 to 2021. From August 2010 to November 2019, Mr. Alkharrat held the position of Chief Operating Officer at SAP SE, an enterprise application software provider.

Christopher R. Armstrong

Mr. Armstrong is our Executive Vice President, Chief Operating Officer, a position he has held since February 2022. Mr. Armstrong joined the Company in 2004, and since then has held several commercial and operational leadership roles, including Executive Vice President, Chief Customer Officer from February 2020 until February 2022, Executive Vice President, Chief Operating Officer from May 2019 until February 2020, Executive Vice President, Operations from March 2018 until May 2019, and Executive Vice President, Customer Support from April 2016 until March 2018.

Stephen H. Holdridge

Mr. Holdridge is our President, Customer and Revenue Operations, a position he has held since February 2023. Mr. Holdridge joined the Company in January 2020, serving as Global Head of Services until February 2022 and Executive Vice President, Chief Customer Officer from February 2022 until February 2023. Prior to joining the Company, Mr. Holdridge held the position of Senior Executive Vice President, Worldwide Services at MicroStrategy, Inc., an analytics and business intelligence company, from November 2017 until July 2019.

Jeffrey S. Jacobs

Mr. Jacobs is our Head of Accounting and Financial Reporting and serves as the principal accounting officer, positions he has held since May 2020. Mr. Jacobs served as our Vice President, Finance from December 2016 until May 2020. Mr. Jacobs is a certified public accountant (inactive).

Jeremy R. Johnson

Mr. Johnson is our Executive Vice President, Chief Financial Officer, a position he has held since January 2024. Prior to joining the Company, Mr. Johnson held the position of Chief Financial Officer at SmartRecruiters, Inc., a talent acquisition software platform, from September 2021 until December 2023. In addition to his role as Chief Financial Officer, for the period August 2022 to April 2023, Mr. Johnson also served as interim Chief Executive Officer for SmartRecruiters, Inc. Prior to that, Mr. Johnson held the position of Senior Vice President, Financial Planning and Analysis and Investor Relations at the Company from December 2020 to August 2021, and a variety of other roles within Finance at the Company from January 2012 to December 2020. Mr. Johnson is a certified public accountant.

Joseph B. Korngiebel

Mr. Korngiebel is our Executive Vice President, Chief Product and Technology Officer, positions he has held since July 2020. Prior to joining the Company, Mr. Korngiebel held various positions at Workday, Inc., a provider of enterprise cloud applications, since March 2006, including Chief Technology Officer from May 2017 until July 2020.

William E. McDonald

Mr. McDonald is our Executive Vice President and General Counsel, positions he has held since July 2021, and Corporate Secretary, a position he has held since February 2016. Mr. McDonald served as Senior Vice President, Deputy General Counsel of the Company from February 2016 until July 2021.

10 | 2023 Form 10-K

Item 1A. Risk Factors.

Our business ordinarily encounters and addresses risks, some of which can cause our future results to be different than we currently anticipate. The risk factors described below represent our current view of some of the most important risks facing our business and are important to its understanding. The following information includes a number of forward-looking statements and should be read in conjunction with information contained in this Annual Report on Form 10-K, including the Management’s Discussion and Analysis of Financial Condition and Results of Operations, the Quantitative and Qualitative Disclosures About Market Risk and the consolidated financial statements and related notes.

Risks Related to Our Business and Industry

Revenues from our Cloud solutions have grown substantially over the last few years, and we believe a significant portion of our market capitalization is based upon maintaining our high Cloud solutions growth rate. Our efforts to continue increasing use of our Cloud solutions may not succeed and may reduce our revenue growth rate.

Our ability to continue to grow the revenues from our Cloud solutions through execution against our growth levers depends on the quality of our platform and solutions, and our ability to design our Cloud solutions to meet consumer demand; and our ability to increase sales from existing customers depends on our customers’ satisfaction with our product and need for additional solutions. Our participation in new markets for native payroll, sales to our existing base of customers, and application expansion in various modules and features, including the Dayforce Wallet, is relatively new, and it is uncertain whether these areas will ever result in significant revenues for us. Further, the entry into new markets, sales to our existing base of customers, or the introduction of new features, functionality, or applications beyond our current markets and functionality may not be successful.

The success of our growth strategies will depend upon our ability to anticipate and to adapt to changes in technology and industry standards, and to effectively develop, introduce, market, and gain broad acceptance of new product and service offerings and enhancements incorporating the latest technological advancements. Our success is also subject to the risk of future disruptive technologies, such as large language models, AI, and machine learning. The failure to develop enhancements to our applications for, or that incorporate, technologies such as AI, machine learning, and large language models may impact our ability to increase the efficiency of and reduce costs associated with our customers’ operations. We may not be able to successfully provide new or enhanced functionality and features for our existing solutions, including those that may involve AI or machine learning or be created using AI or machine learning, that achieve market acceptance or that keep pace with rapid technological developments.

We believe a significant portion of our market capitalization is based upon our high Cloud revenue growth rate, and if we are unable to sell our Cloud solutions, including the Dayforce Wallet, into new markets or to further penetrate existing markets, or to increase sales from existing customers, or we have failures in new product functionalities, our revenue may not grow as expected, which could have a material adverse effect on our market capitalization, and our business, financial condition, and results of operations.

If the movement of funds to initiate payroll-related transactions on behalf of our customers is disrupted, we may suffer significant losses which could have a material adverse effect on our business, financial condition, and results of operations.

Our payroll and tax processing services involve the movement of significant funds from the account of a customer to its employees and to relevant taxing authorities. Typically, we rely upon third party vendors to initiate payments on behalf of our customers. These payments are made in a large number of jurisdictions, in great volume and in short time windows, all of which raise the possibility of an error that disrupts the movement of funds. Further, these types of transactions are subject to an increasingly complex series of regulations and laws that we, and/or our third-party vendors must comply with. Failure to comply with these regulations and laws could result in consequences up to and including a regulator enjoining us and/or our third-party vendors from engaging in the movement of funds. In addition, as described elsewhere, the systems on which these payroll-related transactions are based are in some cases antiquated or manual or may be subject to processing and/or technological errors in communicating with third-party technology systems. Any disruption or delay to data flow in these critical time periods could lead to the disruption of fund movement. Any disruption of fund movement could have significant consequences, including defaults under our customer agreements and exposure to monetary damages, in addition to reputational harm, that could have a material adverse effect on our business, financial condition and results of operations.

Our aging software infrastructure, technology, and sophistication of these systems, and our migration to new platforms, has and will continue to lead to increased costs, vulnerability to cyber-attack, or disruptions in operations that could have a material adverse effect on our business, market brand, financial condition, and results of operations.

11 | 2023 Form 10-K

Our business continues to demand the use of sophisticated systems and technology, including technology infrastructure assets. These systems and technologies must be refined, updated and/or replaced with more advanced systems on a regular basis in order for us to meet both our customers’ and employees’ demands and expectations. Some of the crucial platforms on which we host our back office and legacy systems are aged and need to be replaced or are in the process of being replaced. Some of our customer instances have, and in the future will be, migrated to public Cloud environments. These technological changes are expensive and have and will continue to impact our profitability and demand attention from our senior leadership. If we are unable to replace our aged, crucial platforms, if some or all these platforms fail to operate due to a software error or infrastructure failure, if we fail to continue to refine and update our systems and technologies on a timely basis or within reasonable cost parameters, if we do not appropriately and timely train our employees to operate any of these new systems, if we fail to migrate to new systems in a manner free from disruption, if the new systems fail to perform as desired, or if we are unable to appropriately protect any of these systems, we could suffer the loss of data, vulnerabilities to cyber-attack, system outages or other performance problems, which could have a material adverse effect on our business, financial condition, and results of operations.

An information security breach of our systems or the loss of, or unauthorized access to, customer information or sensitive company information; the failure to comply with the U.S. Federal Trade Commission’s (“FTC”) ongoing consent order regarding data protection; or a system disruption could have a material adverse effect on our business, market brand, financial condition, and results of operations.

Our business is dependent on our payroll, transaction, financial, accounting, and other data processing systems. We rely on these systems, which are maintained both internally and externally at third parties, to process, on a daily and time sensitive basis, a large number of complicated transactions. We, both through our internal systems and systems maintained by third parties, electronically receive, process, store, and transmit data and personal information about our customers and their employees, as well as our vendors and other business partners. We keep this information confidential. However, both our internal and third-party partners’ websites, networks, applications and technologies, and other information systems have been, and may in the future be targeted by malevolent parties for sabotage, disruption, ransom, or data misappropriation. Further, as we grow by acquisition, these risks become acute in the period following the acquisition, as we set about integrating the acquisition target’s systems into ours. Additionally, as we retire our legacy products like our bureau payroll services or sunset certain acquired products, we are decreasing investments in maintaining those systems which creates the potential for a security breach of one of those systems. The uninterrupted operation of our information systems and our ability to maintain the confidentiality and integrity of personal information and other customer and individual and company information that resides on our systems are critical to the successful operation of our business. We, and our third party providers, maintain systems and processes designed to protect this data and maintain business continuity, but notwithstanding such protective measures, there is a risk of intrusion, cyber-attacks or tampering that could compromise the integrity and privacy of this data. Any information security breach in our business processes or of our processing systems (whether they are maintained internally or externally at third parties) has the potential to impact our customer information and sensitive company information, including our financial reporting capabilities, which could result in the potential loss of business and our ability to accurately report financial results. If any of these systems fail to operate properly or become disabled even for a brief period of time, we could potentially miss a critical filing period, resulting in potential fees and penalties, or lose control of customer data, all of which could result in financial loss, a disruption of our business, liability to customers, regulatory intervention, or damage to our reputation. Further, our employees, service providers, and third parties frequently work on a remote or hybrid model, which may involve relying on less secure systems and may increase the risk of cybersecurity-related incidents. We cannot guarantee these private work environments and electronic connections to our work environment have the same security measures deployed in our physical offices.

Additionally, security breaches of customer and user information which occur outside of our systems may nevertheless result in increased business costs, lost revenues, damage to reputation, and exposure to litigation. In most instances, our customers administer access to the data of their employees and service providers. While we encourage customers to implement certain security controls, they may not implement appropriate controls to protect the identities used to access our products. As a result, customers may suffer a cybersecurity attack on their own systems, unrelated to our own, and allow a malicious actor access to the customer’s information held on our platform. Even if such a breach is unrelated to our security programs or practices, such breach could cause us reputational harm and require us to incur significant economic and operational consequences in order to adequately assess and respond to the breach, including further protecting our customers from their own vulnerabilities, and to implement appropriate safeguards to protect against future breaches.

We are subject to a twenty-year consent order with the FTC that became final in June 2011 stemming from a December 2009 criminal hack into our discontinued U.S. payroll application. We conceded no wrongdoing in the order and we were not subject to any monetary fines or penalties. However, in connection with the order, we are required to, among other things, maintain a comprehensive information security program that is reasonable and appropriate for our size and complexity, and for the type of personal information we collect. We are also required to have portions of our security

12 | 2023 Form 10-K

program, which apply to certain segments of our U.S. business, reviewed by an independent third party on a biennial basis. Maintaining, updating, monitoring, and revising an information security program in an effort to ensure that it remains reasonable and appropriate in light of changes in security threats, changes in technology, and security vulnerabilities that arise from legacy systems is time-consuming and complex, and is an ongoing effort.

While we have taken and continue to take steps to ensure compliance with the consent order, if we are determined not to be in compliance with the consent order, or if any new breaches of security occur, the FTC may take enforcement actions or other parties may initiate a lawsuit. Any such resulting fines and penalties could have a material adverse effect on our liquidity and financial results, and any reputational damage therefrom could adversely affect our relationships with our existing customers and our ability to attain new customers. Insurance may be inadequate or may not be available in the future on acceptable terms, or at all. In addition, our insurance policies may not cover all claims made against us, and defending a lawsuit, regardless of its merit, could be costly, divert management’s attention, or damage our reputation.

Our solutions and our business are subject to a variety of laws and regulations, including those regarding privacy, data protection, and information security. Any failure by us or our third party service providers, as well as the failure of our services, to comply with these laws could have a material adverse effect on our business, financial condition, and results of operations.

Failure to comply with privacy, data protection, and information security laws and regulations could have a material adverse effect on our business, results of operations or financial condition, or have other adverse consequences. These laws, which are not uniform, govern the collection, storage, hosting, transfer (including in some cases, the transfer outside the country of collection), use, disclosure, security, retention, and destruction of personal information; they require us to give notice to individuals of privacy practices; give individuals certain access and correction rights with respect to their personal information; and regulate the use or disclosure of personal information for secondary purposes such as marketing. Under certain circumstances, some of these laws require us to provide notification to affected individuals, clients, data protection authorities and/or other regulators in the event of a data breach. In many cases, these laws apply not only to third-party transactions, but also to transfers of information among the Company and its subsidiaries. The European Union (the “EU”) General Data Protection Regulation (the “GDPR”), the California Consumer Protection Act (the “CCPA”) and its successor, the California Privacy Rights Act (“CPRA”), are among the most comprehensive of these laws. The number of related laws and regulations we are subject to continue to increase as we enter new markets in Europe, Asia Pacific, and Latin America, and as we continue our entry into the consumer space through our Dayforce Wallet product. Restrictions on transfers of personal information from one geography to another continue to evolve. Complying with these laws and requirements, has resulted in significant costs to our business and may continue to require us to amend certain of our business practices. Further, enforcement actions and investigations by regulatory authorities related to data security incidents and privacy violations continue to increase. The future enactment of more restrictive laws, rules, or regulations and/or future enforcement actions or investigations could have a material adverse impact on us through increased costs or restrictions on our businesses and noncompliance could result in significant regulatory penalties and legal liability and damage our reputation. Restrictions on cross border data flows and data residency requirements may negatively impact our clients’ and our own ability to transfer personal information to the U.S. and other countries as part of our provision of services, and in support of our own operations, potentially impacting revenues. In addition, data security events and concerns about privacy abuses by other companies are changing consumer and social expectations for enhanced privacy and data protection. As a result, even the perception of noncompliance, whether or not valid, may damage our reputation. Finally, our ability to produce data-driven insights for our customers as we continue to leverage AI in our HCM technology may be constrained by current and future privacy, social and ethics regulatory requirements and considerations, thereby restricting our ability to use data in innovative ways. These regulatory requirements and considerations may also impose burdensome and costly requirements on our ability to leverage data, and potentially result in brand or reputational harm.

Our business plan is focused on an aggressive growth strategy. If we fail to manage our growth effectively or if our strategy is not successful, we may be unable to execute our business plan, to maintain high levels of service, or to adequately address competitive challenges.

We have experienced, and we believe we will continue to experience, a period of rapid growth in our operations and Cloud solutions. The growth of our operations and Cloud solutions has and may continue to place a strain on our management, administrative, operational, technological, and financial infrastructure. In order to manage our growth effectively, we will need to continuously improve our management, administrative, operational, technological, and financial systems, and our internal controls, reporting systems, and procedures to scaled global capabilities which may require investment as we grow and could result in disruption as we transform. Our attempts to develop new or enhanced functionality to our services, whether as part of our anticipated development road map or in response to enhancement requests we have committed to our customers, has been, and will continue to be expensive and impact our profitability. Failure to effectively manage growth or to achieve a profitable growth strategy could result in problems or delays in implementing customers, declines in quality or customer satisfaction, decreased profitability on new customer deals, increases in costs, complications or delays in

13 | 2023 Form 10-K

introducing new features or fixing or updating our existing technology and infrastructure, or other operational challenges; and any of these difficulties could have a material adverse effect on our business, financial condition, and results of operations.

The markets in which we participate are highly competitive, and if we do not compete effectively, it could have a material adverse effect on our business, financial condition, and results of operations.

The markets in which we participate are highly competitive, and competition could intensify in the future. We believe the principal competitive factors in our market include: breadth and depth of product functionality, scalability and reliability of applications, robust workforce management, comprehensive tax services, modern and innovative Cloud technology platforms combined with an intuitive user experience, rapid technological change such as the rise of large language models, multi-country and jurisdiction domain expertise in payroll and HCM, quality of implementation and customer service, integration with a wide variety of third party applications and systems, total cost of ownership and return on investment, brand awareness, and reputation, pricing and distribution.

We face a variety of competitors, some of which are long-established providers of HCM solutions. Many of our current and potential competitors are larger, have greater name recognition, longer operating histories, larger marketing budgets, and significantly greater resources than we do, and are able to devote greater resources to the development, promotion, and sale of their products and services. Some of our competitors do or could offer HCM solutions bundled as part of a larger product offering. Furthermore, our current or potential competitors may be acquired by third parties with greater available resources and the ability to initiate or to withstand substantial price competition. In addition, many of our competitors have established marketing relationships, access to larger customer bases, and major distribution agreements with consultants, system integrators, and resellers. Our competitors have and may continue to establish cooperative relationships among themselves or with third parties that may further enhance their product offerings or resources. Although we have a global partnership strategy, additional investment and efforts will be necessary to fully implement and scale such a strategy.

If our competitors’ products, services, or technologies become more accepted than our applications are today, if they are successful in bringing their products or services to market earlier than ours, or if their products or services are more technologically capable than ours, it could have a material adverse effect on our business, financial condition, and results of operations. In addition, some of our competitors may offer their products and services at a lower price compared to our products or their current pricing impacting our ability to achieve our target pricing. If we are unable to achieve our target pricing levels or if we experience significant pricing pressures, it could have a material adverse effect on our business, financial condition, and results of operations.

Our international growth strategy has and will continue to expose us to risks inherent in international sales and operations.

We have and will continue to expand our operations and sales into new international markets. Our expanding international operations are subject to risks that could adversely affect those operations or our business as a whole, including but not limited to the costs of establishing a market presence, localizing product and service offerings for foreign customers, difficulties in managing and staffing international operations, and increased expenses related to introducing corporate policies and controls in our international operations and increased reliance on partners to provide services in additional geographies. Further, the expansion of our product offering into new international markets has and will continue to result in an expansion of our monitoring of local laws and regulations, which increases our costs as well as the risk of the product not incorporating in a timely fashion or at all the necessary changes to enable a customer to be compliant with such laws, or in manual workarounds that are prone to errors.

Moreover, as part of our international strategy, we work with partners to perform services in certain geographies where we do not currently have international operations or the particular service required by our customers. As a result, we may experience business impact if our partners do not carry out the services as committed, or at a quality level that our customers demand, including potential for reduced margin from additional expense or impact to customer relationships.

Our international growth strategy has and may continue to include growth via acquisition. Our growth following an acquisition may also be dependent on our ability to transition acquired customers from current and legacy products to Dayforce, migrate and integrate acquired technologies or to increase sales by addressing broader HCM needs with additional modules of Dayforce.

If we are unable to provide the required services on a multinational basis, or if we are unable to effectively manage our international expansion, we could be subject to negative customer experiences, harm to our reputation or loss of customers, claims for any fines, penalties or other damages suffered by our customer, and other financial harm, including fines, penalties, or other damages suffered by us directly, which would negatively impact revenue and earnings. Although we have a multinational strategy, additional investment and efforts may be necessary to implement such strategy. Some of our business partners also have international operations and are subject to the risks described above.

14 | 2023 Form 10-K

Customers depend on our solutions to assist them to comply with applicable laws, which requires us and our third party providers to constantly monitor applicable laws and to make applicable changes to our solutions. If our solutions have not been updated to enable the customer to comply with applicable laws or we fail to update our solutions on a timely basis, it could have a material adverse effect on our business, financial condition, and results of operations.

Customers use our solutions to assist them to comply with payroll, HR, and other applicable laws for which the solutions are intended for use. We and our third party providers must monitor all applicable laws and as such laws expand, evolve, or are amended in any way, and when new regulations or laws are implemented, we may be required to modify our solutions to assist our customers to comply with such new regulations or laws, which requires an investment of our time and resources. We are also reliant on our third party providers to modify the solutions that they provide to our customers as part of our solutions to comply with changes to such laws and regulations. The number of laws and regulations that we are required to monitor has and will continue to increase as we expand both the geographic regions in which the solutions are offered and the types of products we offer to customers. These risks have become exacerbated as we expand by acquisition and are most acute in the period following the acquisition as we integrate the acquired business and its systems. In the event our solutions fail to assist a customer to comply with applicable laws, we are subject to negative customer experiences, harm to our reputation or loss of customers, claims for any fines, penalties or other damages suffered by our customer, and other financial harm, including fines, penalties, or other damages suffered by us directly.

If our current or future applications fail to perform properly, our reputation could be adversely affected, our market share could decline, and we could be subject to liability claims, which could have a material adverse effect on our business, financial condition, and results of operations.

Our applications are inherently complex and may contain material defects or errors that we are not yet aware of. Because of the large amount of data that we collect and manage, it is possible that failures or errors in our systems could result in data loss or corruption or cause the information that we collect to be incomplete or to contain inaccuracies that our customers regard as significant. Any defects in functionality or that cause interruptions in the availability of our applications could result in reputational, competitive, operational, or other business harm as well as financial costs and regulatory action, any of which could have a material adverse effect on our business, financial condition, and results of operations. In addition, the costs incurred in correcting any material defects or errors might be substantial. While we conduct standard due diligence during our acquisition process, these risks are heightened as we grow by acquisition and dedicate resources to integrating the acquisition target’s systems into ours and take on the vulnerabilities that may exist at the acquisition target.

If we fail to manage our technical operations infrastructure, our existing customers may experience service outages, and our new customers may experience delays in the implementation of our applications, which could have a material adverse effect on our business, financial condition, and results of operations.

We have experienced and will continue to experience significant growth in the number of users, transactions, and data that our operations infrastructure supports, including the acquisition of new systems via strategic transactions. We seek to maintain sufficient capacity in our operations infrastructure to meet the needs of our customers and to facilitate the rapid provision of new customer activations and the expansion of existing customer activations. In addition, we need to continue to properly manage our technological operations infrastructure to support version control, changes in hardware and software parameters, and the evolution of our applications. We have experienced, and may in the future experience, website disruptions, outages, and other performance problems. These problems may be caused by a variety of factors, including infrastructure changes, human or software errors, viruses, security attacks, fraud, increased resource consumption from expansion or modification to our Dayforce code, spikes in customer usage, denial of service issues and Cloud interruptions run by third party service providers and our ability to react. The risks of these problems occurring may be exacerbated by our strategic acquisitions, especially in the period following the acquisition as we integrate the acquisition target’s systems into ours, as well as our aging technology infrastructure which in some cases is supported by older platforms. In some instances, we may not be able to identify the cause or causes of these performance problems within an acceptable period of time. If we do not accurately predict our infrastructure requirements, our existing customers may experience service outages that may subject them to financial penalties, causing us to incur financial liabilities and customer losses.

Our growth depends in part on the success of our strategic relationships with third parties who provide us with services and license us software for use in or with both our applications and our internal operations.

In order to maintain and grow our business, we do, and we anticipate that we will continue to, depend on the continuation and expansion of relationships with third parties who provide us with services. These service provider partners include connected payroll partners, implementation partners, systems integrators, third party sales channel partners, the operators of data centers, and banks and other providers who execute wire transfers and other money movement services to support our customer payroll and tax services. Our agreements with these third party service providers are typically non-exclusive and do not prohibit them from working with our competitors. If any third-party service providers on which we rely to provide

15 | 2023 Form 10-K

us with services experience a disruption, go out of business, are acquired by our competitors, experience a decline in quality, or terminate their relationship with us, we could experience a material adverse effect on our business, financial condition, and results of operation.

In addition, we license software from third parties for use in or with both our applications and our internal operations, and the inability to maintain these licenses could result in increased costs, or reduced service levels, which could have a material adverse effect on our business, financial condition, and results of operations. To the extent that our applications depend upon the successful operation of third party software in conjunction with our software, any undetected errors or defects in this third party software could prevent the deployment or impair the functionality of our applications, delay new application introductions, and result in a failure of our applications, which could have a material adverse effect on our business, financial condition, and results of operations.

Any failure to offer high-quality technical support services may adversely affect our relationships with our customers and could have a material adverse effect on our business, financial condition, and results of operations.

Once our applications are deployed, our customers depend on our support organization and the support capabilities of our partners to resolve technical issues relating to our applications, as well as our partner’s applications. We have recently engaged in a rebalancing of our global workforce that particularly impacted our support organization, which may result in disruption as we fill existing positions in our APJ geographies. We or our partners may be unable to respond quickly enough to accommodate short-term increases in customer demand for support services, and we may be limited in our ability to resolve the technical issues our customers have with our technology, or our partner’s technology. We or our partners also may be unable to modify the format of our or our partners’ support services to compete with changes in support services provided by our competitors. Increased customer demand for these services, without corresponding revenues, could increase costs and have an adverse effect on our results of operations. Ultimately, a client could elect to terminate their agreement due to dissatisfaction with support, resulting in lost recurring revenue. In addition, our sales process is highly dependent on our applications and business reputation and on positive recommendations from our existing customers. Any failure to maintain high-quality technical support, or a market perception that we do not maintain high-quality support, could adversely affect our reputation and our ability to sell our applications to existing and prospective customers, which could have a material adverse effect on our business, financial condition, and results of operations.

If our customers are not satisfied with the implementation and professional services provided by us or our partners, it could have a material adverse effect on our business, financial condition, and results of operations.

Our business depends on the ability to implement our solutions on a timely, accurate, and cost-efficient basis and to provide professional services at the high level demanded by our customers. Implementation and other professional services may be performed by our own staff, by a third party, or by a combination of the two. If a customer is not satisfied with the timely access or the quality of work performed, then we could incur loss of revenue or additional costs to address the situation, the customer’s dissatisfaction with such services could damage our ability to expand the number of applications subscribed to by that customer or we could be liable for loss or damage suffered as a result, any of which could have a material adverse effect on our business, financial condition, and results of operations. If a new customer is dissatisfied with implementation, the customer could refuse to go-live, which could result in a delay in our collection of fees or could result in a customer seeking repayment of its implementation fees or suing us for damages or could force us to enforce the termination provisions in our customer contracts in order to collect revenue. In addition, negative publicity related to our customer relationships, regardless of its accuracy, may affect our ability to compete for new business with current and prospective customers, which could also have a material adverse effect on our business, financial condition, and results of operations.

We depend on our senior management team, and the loss of one or more key employees or an inability to attract and to retain highly skilled employees could have a material adverse effect on our business, financial condition, and results of operations.

Our success depends largely upon the continued services of our senior management team. Our executive officers, senior management or other key personnel have limited or no notice period applicable to their employment. Therefore, they could terminate their employment with us at any time. Additionally, we do not maintain key employee insurance on any of our executive officers, senior management, or key employees. The loss of one or more of our executive officers, senior management, or key employees could have a material adverse effect on our business, financial condition, and results of operations.

To execute our growth plan, we must attract and retain highly qualified personnel. Competition for talent is intense and has become more intense in recent years, including without limitation for individuals with high levels of experience in designing and developing software and Internet-related services and senior sales executives. We have, from time to time, experienced the need to increase compensation for current and prospective employees to retain and recruit employees of the desired qualifications which impacts our ability to profitably operate our business. In addition, we have and we expect to continue

16 | 2023 Form 10-K

to experience, difficulty in hiring and retaining employees with appropriate qualifications, the cumulative loss of which could raise the risk of failures to operate our business to the quality needed and could have a material adverse effect on our business, financial condition, and results of operations.

If our vendors or affiliates initiate payroll-related transactions on behalf of our customers and do not receive funds from the customer sufficient to cover the amounts paid on their behalf, we may suffer significant losses which could have a material adverse effect on our business, financial condition, and results of operations.