UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2020

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _____________.

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report:

Commission file number: 001-38773

China SXT Pharmaceuticals, Inc.

(Exact name of Registrant as Specified in its Charter)

British Virgin Islands

(Jurisdiction of Incorporation or Organization)

178 Taidong Rd North, Taizhou

Jiangsu, China

(Address of Principal Executive Offices)

Feng Zhou

178 Taidong Rd North, Taizhou

Jiangsu, China

+86- 523-86298290

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange On Which Registered | |

| Ordinary shares, par value US$0.001 per share | NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of March 31, 2020 was: 34,667,707 ordinary shares, par value $0.001 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☐ | Non-accelerated filer ☒ | Emerging growth company ☒ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | U.S. GAAP | ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board |

☐ | Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

CHINA SXT PHARMACEUTICALS, INC.

FORM 20-F ANNUAL REPORT

TABLE OF CONTENTS

i

CERTAIN INFORMATION

In this annual report on Form 20-F, unless otherwise indicated, “we,” “us,” “our,” the “Company” and “China SXT” refer to China SXT Pharmaceuticals, Inc., a company organized in the British Virgin Islands, its predecessor entities and its subsidiaries.

Unless the context indicates otherwise, all references to “China” and the “PRC” refer to the People’s Republic of China, all references to “Renminbi” or “RMB” are to the legal currency of the People’s Republic of China, all references to “U.S. dollars,” “dollars” and “$” are to the legal currency of the United States. This annual report contains translations of Renminbi amounts into U.S. dollars at specified rates solely for the convenience of the reader. We make no representation that the Renminbi or U.S. dollar amounts referred to in this report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all. On March 31, 2020, the cash buying rate announced by the People’s Bank of China was RMB7.0808 to $1.00.

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements” for purposes of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 that represent our beliefs, projections and predictions about future events. All statements other than statements of historical fact are “forward-looking statements,” including any projections of earnings, revenue or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new projects or other developments, any statements regarding future economic conditions or performance, any statements of management’s beliefs, goals, strategies, intentions and objectives, and any statements of assumptions underlying any of the foregoing. Words such as “may”, “will”, “should”, “could”, “would”, “predicts”, “potential”, “continue”, “expects”, “anticipates”, “future”, “intends”, “plans”, “believes”, “estimates” and similar expressions, as well as statements in the future tense, identify forward-looking statements.

These statements are necessarily subjective and involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any future results, performance or achievements described in or implied by such statements. Actual results may differ materially from expected results described in our forward-looking statements, including with respect to correct measurement and identification of factors affecting our business or the extent of their likely impact, and the accuracy and completeness of the publicly available information with respect to the factors upon which our business strategy is based or the success of our business.

Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of whether, or the times by which, our performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and management’s belief as of that time with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to, those factors discussed under the headings “Risk Factors”, “Operating and Financial Review and Prospects,” and elsewhere in this report.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

1

3.A. Selected Financial Data

The following table presents the selected consolidated financial information of our company. The selected consolidated statements of operations data for the years ended March 31, 2020, 2019 and 2018 and the selected consolidated balance sheets data as of March 31, 2020 and 2019 have been derived from our audited consolidated financial statements, which are included in this annual report beginning on page F-1. Our audited consolidated financial statements are prepared and presented in accordance with accounting principles generally accepted in the United States, or U.S. GAAP. Our historical results do not necessarily indicate results expected for any future period. You should read the following selected financial data in conjunction with the consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this report.

| For the years ended March 31, | ||||||||||||

| 2020 | 2019 | 2018 | ||||||||||

| Summary Consolidated Statements of Operations: | ||||||||||||

| Operating revenue | $ | 5,162,268 | $ | 7,012,026 | $ | 7,019,243 | ||||||

| Cost of revenue | (2,458,566 | ) | (2,400,491 | ) | (3,617,748 | ) | ||||||

| Gross Profit | 2,703,702 | 4,611,535 | 3,401,495 | |||||||||

| Operating expense | ||||||||||||

| Selling | 1,583,284 | 1,605,497 | 512,482 | |||||||||

| General and administrative | 2,461,535 | 1,236,546 | 1,256,747 | |||||||||

| Total operating expenses | 4,044,819 | 2,842,043 | 1,769,229 | |||||||||

| Other income (expense) | ||||||||||||

| Other income (expense), net | (9,048,477 | ) | 21,967 | (4,582 | ) | |||||||

| (Loss) income before income taxes (benefits) | (10,389,594 | ) | 1,791,459 | 1,627,684 | ||||||||

| Provision (benefit) for income taxes | (101,722 | ) | 252,232 | 440,103 | ||||||||

| Net income (loss) | (10,287,872 | ) | 1,539,227 | 1,187,581 | ||||||||

| Net income (loss) attributable to China SXT Pharmaceuticals, Inc. | $ | (10,287,872 | ) | $ | 1,539,227 | $ | 1,187,581 | |||||

The following table presents our summary consolidated balance sheet data as of March 31, 2020 and 2019.

| March 31, | March 31, | |||||||

| 2020 | 2019 | |||||||

| Summary Consolidated Balance Sheet Data: | ||||||||

| Cash and cash equivalents | $ | 7,287,032 | $ | 9,130,849 | ||||

| Other assets | 14,415,146 | 8,339,984 | ||||||

| Total assets | $ | 21,702,178 | $ | 17,470,833 | ||||

| Total liabilities | 12,300,825 | 6,363,078 | ||||||

| Total shareholders’ equity | $ | 9,401,353 | $ | 11,107,755 | ||||

3.B. Capitalization and Indebtedness

Not Applicable.

3.C. Reasons For The Offer And Use Of Proceeds

Not Applicable.

2

3.D. Risk Factors

An investment in our ordinary shares involves a high degree of risk. You should carefully consider the risks and uncertainties described below together with all other information contained in this annual report, including the matters discussed under the headings “Forward-Looking Statements” and “Operating and Financial Review and Prospects” before you decide to invest in our ordinary shares. We are a holding company with substantial operations in China and are subject to a legal and regulatory environment that in many respects differs from the United States. If any of the following risks, or any other risks and uncertainties that are not presently foreseeable to us, actually occur, our business, financial condition, results of operations, liquidity and our future growth prospects could be materially and adversely affected.

Risks Related to the COVID-19 Pandemic

In December 2019, a novel strain of coronavirus was reported to have surfaced in Wuhan, China, which has and is continuing to spread throughout China and other parts of the world, including the United States. On January 30, 2020, the World Health Organization declared the outbreak of the coronavirus disease (COVID-19) a “Public Health Emergency of International Concern,” and on March 11, 2020, the World Health Organization characterized the outbreak as a “pandemic.” Governments in affected countries are imposing travel bans, quarantines and other emergency public health measures, which have caused material disruption to businesses globally resulting in an economic slowdown. These measures, though temporary in nature, may continue and increase depending on developments in the COVID-19’s outbreak.

Jiangsu Province, where we conduct a substantial part of our business, was materially impacted by the COVID-19. We have been following the recommendations of local health authorities to minimize exposure risk for our employees, including the temporary closures of our offices and production, and having employees work remotely. Our on-site work was not resumed until mid-March, 2020 upon the approval from the local government. Due to the extended lock-down and self-quarantine policies in China, we have experienced significant business disruption for the past two and a half months. Some of our employees in other provinces are still subject to the lock-down policy implemented by the local governments and could not return to work. Our production was resumed in mid-March, 2020. Due to the material impacts of COVID-19 on our logistics, our production was picking up slowly and returned to the normal level in May, 2020.

The extent to which the COVID-19 continues to impact the Company’s business, sales, and results of operations will depend on future developments, which are highly uncertain and will include emerging information concerning the severity of the coronavirus and the actions taken by governments and private businesses to attempt to contain the coronavirus, but is likely to result in a material impact on our business operations at least for the near term.

Risks Related to the May 2019 Private Placement and the Forbearance Agreement

The Company completed a private placement on May 2, 2019 (the “May 2019 Private Placement”) with two unaffiliated institutional investors (each, a “Investor” or “Holder”, collectively, “Investors” or “Holders”) pursuant to certain Securities Purchase Agreement dated April 16, 2019, as amended on May 2, 2019 (the “Purchase Agreement”). The securities sold by the Company in the May 2019 Private Placement consisted of (1) Senior Convertible Notes in the aggregate principal amount of $15 million (each, a “Note” and collectively, the “Notes”), consisting of (i) Series A Senior Convertible Notes (“Series A Notes”) and (ii) Series B Senior Secured Convertible Notes (“Series B Notes”) and (2) Warrants (“Series A Warrants”) to purchase 596,658 of the Company’s ordinary shares, and (3) Warrants (“Series B Warrants”, collectively with Series A Warrants, “Warrants”) to purchase 298,330 of the Company’s ordinary shares. The Purchase Agreement, the Notes, Series A Warrants and Series B Warrants and other transaction documents in connection with the May 2019 Private Placement are referred to as “Transaction Documents”.

On July 23, and July 29, 2019 the Company received event of default redemption notices from two Holders claiming that the Company failed to timely make the payment for the Installment Amount (as defined in the Notes) due under the terms of Series A Note, therefore, the Holders elected to effect the redemption of Series A Notes.

If the Company fails to fulfill its obligation under the forbearance agreements with its investors in May 2019 private placement, it will cause significant dilution of to existing shareholders when the Holders elect to convert shares under the Notes or exercise the Warrants, and cause material adverse effect on the Company’s cash flow, financial conditions and operation results if the Holders require us to repay in cash.

The Company completed a private placement on May 2, 2019 (the “May 2019 Private Placement”) with two unaffiliated institutional investors (each, a “Investor” or “Holder”, collectively, “Investors” or “Holders”) pursuant to certain Securities Purchase Agreement dated April 16, 2019, as amended on May 2, 2019 (the “Purchase Agreement”). The securities sold by the Company in the May 2019 Private Placement consisted of (1) Senior Convertible Notes in the aggregate principal amount of $15 million (each, a “Note” and collectively, the “Notes”), consisting of (i) Series A Senior Convertible Notes (“Series A Notes”) and (ii) Series B Senior Secured Convertible Notes (“Series B Notes”) and (2) Warrants (“Series A Warrants”) to purchase 596,658 of the Company’s ordinary shares, and (3) Warrants (“Series B Warrants”, collectively with Series A Warrants, “Warrants”) to purchase 298,330 of the Company’s ordinary shares. The Purchase Agreement, the Notes, Series A Warrants and Series B Warrants and other transaction documents in connection with the May 2019 Private Placement are referred to as “Transaction Documents”.

3

On July 23, and July 29, 2019the Company received event of default redemption notices from two Holders claiming that the Company failed to timely make the payment for the Installment Amount (as defined in the Notes) due under the terms of Series A Note, therefore, the Holders elected to effect the redemption of Series A Notes.

Upon negotiation with the Investors, on December 13, 2019, the Company entered into certain Forbearance and Amendment Agreements (each a “Forbearance Agreement”, collectively with other ancillary agreements, as amended from time to time, the “Forbearance Agreements”) with each Investor. Concurrently with the execution of the Forbearance Agreement, the Investors and the Company have entered into the Lock-Up Agreements, Leak-Out Agreements and Mutual Releases.

Due to the Company’s failure to obtain timely approval from State Administration of Foreign Exchange in People’s Republic of China to redeem Series A Notes in cash as previously contemplated, we separately amended and restated the Leak-Out Agreements (each an “Amended Leak-Out Agreement”) with each Investor on March 3, 2020.

Any failure by us to meet our payment and other obligations under the Forbearance Agreements, including failure to timely convert the shares under Series A Note per Holders’ conversion notices, could lead to defaults under our Forbearance Agreement. In the event of a default that we cannot remedy, the Holders may require us to redeem all or portion of the outstanding principal of the Notes with unpaid and accrued interests, make-whole amount, liquidated damages and late charges, if any. Payment of redemption price may negatively impact our liquidity, financial condition and results of operations of the Company.

The conversion of the Series A Notes will dilute the ownership interest of existing shareholders or may otherwise depress the price of our ordinary shares.

The conversion of some or all of the Series A Notes will dilute the ownership interests of existing shareholders to the extent we deliver shares of our ordinary shares upon conversion of the Notes. The Notes are convertible at the option of the holders of the Series A Notes prior to October 15, 2020 under certain circumstances as provided in the indenture governing the Notes. Any sales in the public market of the ordinary shares issuable upon such conversion could adversely affect prevailing market prices of our ordinary shares. In addition, the existence of the Notes may encourage short selling by market participants because the conversion of the Notes could be used to satisfy short positions, or anticipated conversion of the Notes into shares of our ordinary shares could depress the price of our ordinary shares.

The terms of Transaction Documents and Forbearance Agreements could impede our ability to enter into certain transactions or obtain additional financing and could result in our paying premiums or penalties to the holders of the Notes and Warrants.

The terms of the Notes and other Transaction Documents, prohibit us from entering into a “fundamental transaction” (as defined in the Notes and such Transaction Documents) (including generally, a merger, sale of all or substantially all of our assets, or permitting a purchase tender or exchange offering resulting in a person or group of persons owning at least 50% of the outstanding shares of our Ordinary Shares) unless, among other things, the successor resulting from the fundamental transaction assumes all of our obligations under the Notes, the applicable warrants and the associated transaction documents.

The Notes and Warrants require us to deliver the number of Ordinary Shares issuable upon conversion or exercise within a specified time period. If we are unable to deliver such shares within the timeframe required, we may be obligated to reimburse the Holder for the cost of purchasing the Ordinary Shares in the open market or pay them the profit they would have realized upon the conversion or exercise and sale of such shares.

We may also be obligated to redeem the Notes at a premium upon the occurrence of an event of default (as defined in the Notes) or a change of control (as defined in the Notes). The Warrants also contain features that may require us to repurchase such warrants upon the occurrence of a change of control or other event of default.

The payments we may be obligated to make as described above may adversely affect our results of operations and cash flows.

4

Failure to maintain effectiveness of the registration statement could materially adversely affect our company.

We have agreed, at our expense, to prepare a registration statement covering the Conversion Shares and Warrant Shares in connection with the Offering pursuant to our recent Private Placement with certain buyers (“the May 2019 Private Placement”). The May 2019 Private Placement was closed on May 2, 2019 (“Closing Date”). We are obligated to file the registration statement with the SEC within certain period after the Closing Date and maintain such registration statement effective until the Investors have sold all Registrable Securities as defined in the Registration Right Agreement, including but not limited to, all the Ordinary Shares issuable upon conversion of the Notes and exercise of the Warrants. The registration statement was declared effective on June 27, 2019. However, if we fail to maintain its effectiveness, such failure will be deemed as an event of default under the Transaction Documents and resulting in Holders’ right to convert at the alternative conversion price. Such failure could materially adversely affect us.

The exercise prices of the warrants and conversion prices of the convertible notes are not indications of our value.

The exercise prices of the warrants and the conversion prices of the convertible notes may not necessarily bear any relationship to the book value of our assets, past operations, cash flows, losses, financial condition or any other established criteria for value. You should not consider the exercise price or the conversion price as an indication of the value of the Ordinary Shares underlying the warrants. After May 30, 2019, the Ordinary Shares may trade at prices above or below such exercise prices.

Risks Related to Our Business

We have limited sources of working capital and will need substantial additional financing

The working capital required to implement our business plan will most likely be provided by funds obtained through offerings of our equity, debt, debt-linked securities, and/or equity-linked securities, and revenues generated by us. No assurance can be given that we will have revenues sufficient to sustain our operations or that we would be able to obtain equity/debt financing in the current economic environment. If we do not have sufficient working capital and are unable to generate sufficient revenues or raise additional funds, we may delay the completion of or significantly reduce the scope of our current business plan; delay some of our development and clinical or marketing efforts; postpone the hiring of new personnel; or, under certain dire financial circumstances, substantially curtail or cease our operations.

To date, we have relied almost exclusively on organically generated revenues and financing transactions to fund our operations. Our inability to obtain sufficient additional financing would have a material adverse effect on our ability to implement our business plan and, as a result, could require us to significantly curtail or potentially cease our operations. At March 31, 2020, we had cash and cash equivalents of $7,287,032, total current assets of $19,636,313 and total current liabilities of $12,264,314. At March 31, 2019, we had cash and cash equivalents of $9,130,849, total current assets of $15,588,100 and total current liabilities of $6,321,372. We will need to engage in capital-raising transactions in the near future. Such financing transactions may well cause substantial dilution to our shareholders and could involve the issuance of securities with rights senior to the outstanding shares. Our ability to complete additional financings is dependent on, among other things, the state of the capital markets at the time of any proposed offering, market reception of the Company and the likelihood of the success of its business model and offering terms. There is no assurance that we will be able to obtain any such additional capital through asset sales, equity or debt financing, or any combination thereof, on satisfactory terms or at all. Additionally, no assurance can be given that any such financing, if obtained, will be adequate to meet our capital needs and to support our operations. If we do not obtain adequate capital on a timely basis and on satisfactory terms, our revenues and operations and the value of our Ordinary Shares and Ordinary Share equivalents would be materially negatively impacted and we may cease our operations.

5

Although we were incorporated 15 years ago, our significant business lines have a limited operating history, which makes it difficult to evaluate our future prospects and results of operations.

We only started to produce Directly-Oral TCMP and After-Soaking-TCMP as our principal products three years ago. As a result, our past operating results are not an accurate indication of the lines of business we are principally engaged in currently. Thus, you should consider our future prospects in light of the risks and uncertainties experienced by early stage companies in evolving markets rather than typical companies of our age. Some of these risks and uncertainties relate to our ability to:

| ● | attract additional customers and increased spending per customer; |

| ● | increase awareness of our brand and develop customer loyalty; |

| ● | respond to competitive market conditions; |

| ● | respond to changes in our regulatory environment; |

| ● | manage risks associated with intellectual property rights; |

| ● | maintain effective control of our costs and expenses; |

| ● | raise sufficient capital to sustain and expand our business; |

| ● | attract, retain and motivate qualified personnel; and |

| ● | upgrade our technology to support additional research and development of new products. |

If we are unsuccessful in addressing any of these risks and uncertainties, our business may be materially and adversely affected.

Our investment in Huangshan Panjie Investment LLP Fund may not be successful.

In June 2019 the Company entered into a limited partnership agreement with Huangshan Panjie Investment Management Co., Ltd. (the “GP”), one of the general partner of Huangshan Panjie Investment LLP Fund (“the Fund”), to join the Fund as a limited partner. Pursuant to the limited partnership agreement and its supplements and the Company is committed to contribute $7 million (RMB50 million) into the Fund in two installments, with one installment of $3.5 million (RMB 25 million) made on June 14, 2019, and the second installment of $3.5 million (RMB 25 million) to be made no later than October 31, 2019. The GP will take 20% carried interest.

The Company’s investment in the Fund is to leverage the Fund’s capacity to incubate TCM, pharmaceutical or bio-tech start-ups so as to give the Company a steady line of acquisition candidates complementary to its core business. However, there is no guarantee that the start-ups incubated by the Fund will be suitable acquisition target or, if the Company was able to identify suitable target, it will be able to execute the acquisition or consolidate the acquisition target into the Company’s business.

In June 2020, the Company agreed with the Fund, the GP and other limited partners to withdraw the installment of $3.5 million (RMB 25 million) made on June 14, 2019. The Company received payment of $2.8 million (RMB 20 million) on June 30, 2020 and expects to receive the rest within 3 months after the issuance date of these financial statements. If we are unsuccessful in collecting the rest of the investment, our business may be materially and adversely affected.

Our failure to compete effectively may adversely affect our ability to generate revenue.

We compete with other companies, many of whom are developing or can be expected to develop products similar to ours. Many of our competitors are also more established than we are, and have significantly greater financial, technical, marketing and other resources than we presently possess. Some of our competitors, such as “Huichuntang” and “Tongrentang”, have greater name recognition and a larger customer base. These competitors may be able to respond more quickly to new or changing opportunities and customer requirements and may be able to undertake more extensive promotional activities, offer more attractive terms to customers, and adopt more aggressive pricing policies. We cannot assure you that we will be able to compete effectively with current or future competitors or that the competitive pressures we face will not harm our business.

6

Our dependence on a small number of customers could adversely affect our business or results of operations.

We derive a substantial portion of our revenue from a relatively small number of customers. For additional information regarding Suxuantang’s customer concentrations, see “Consolidated Financial Statements - Note 2 (v) 4). Concentration Risks.” We expect that Suxuantang’s largest customers will continue to account for a substantial portion of its total net revenue for the foreseeable future. Suxuantang has long-standing relationships with many of its significant customers. However, because Suxuantang’s customers generally contract with a finite duration, Suxuantang may lose these customers if the contracts are not renewed or replaced. The loss or reduction of, or failure to renew or replace, any significant contracts with any of these customers could materially reduce Suxuantang’s revenue and cash flows. If Suxuantang does not replace them with other customers, the loss of business from any one of such customers could have a material adverse effect on our business or results of operations.

We are dependent on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations.

Our success is, to a certain extent, attributable to the management, sales and marketing, and research and development expertise of key personnel. We are dependent upon the services of Mr. Zhou, our President, Chief Executive Officer and Chairman of the Board, for the continued growth and operation of our Company, due to his industry experience, as well as his personal and business contacts in the PRC. We may not be able to retain Mr. Zhou for any given period of time. Although we have no reason to believe that Mr. Zhou will discontinue his services with us or Taizhou Suxuantang, the interruption or loss of his services would adversely affect our ability to effectively run our business and pursue our business strategy as well as our results of operations. Additionally, Jingzhen Deng, our Chief Scientific Officer (R&D team leader) and Chief Operation Officer, performs key functions in the operation of our business. There can be no assurance that we will be able to retain these officers after the terms of their employment expire. The loss of these officers could have a material adverse effect upon our business, financial condition, and results of operations. We do not carry key man life insurance for any of our key personnel, nor do we foresee purchasing such insurance to protect against the loss of key personnel.

We may not be able to hire and retain qualified personnel to support our growth and if we are unable to retain or hire these personnel in the future, our ability to improve our products and implement our business objectives could be adversely affected.

We must attract, recruit and retain a sizeable workforce of technically competent employees. Competition for senior management and personnel in the PRC is intense and the pool of qualified candidates in the PRC is very limited. We may not be able to retain the services of our senior executives or personnel, or attract and retain high-quality senior executives or personnel in the future. This failure could materially and adversely affect our future growth and financial condition.

If we fail to increase our brand recognition, we may face difficulty in obtaining new customers.

Although our brand is well-respected in TCMP industry, we still believe that maintaining and enhancing our brand recognition in a cost-effective manner outside of that market is critical to achieving widespread acceptance of our current and future products and services and is an important element in our effort to increase our customer base. Successful promotion of our other brands, or Suxuantang outside the TCMP industry, will depend largely on our ability to maintain a sizeable and active customer base, our marketing efforts and ability to provide reliable and useful products and services at competitive prices. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses we will incur in building our brand. If we fail to successfully promote and maintain our brand, or if we incur substantial expenses in an unsuccessful attempt to promote and maintain our brand, we may fail to attract enough new customers or retain our existing customers to the extent necessary to realize a sufficient return on our brand-building efforts, in which case our business, operating results and financial condition, would be materially adversely affected.

Any disruption in the supply chain of raw materials and our products could adversely impact our ability to produce and deliver products.

As to the products we manufacture, we must manage our supply chain for raw materials and delivery of our products. Supply chain fragmentation and local protectionism within China further complicates supply chain disruption risks. Local administrative bodies and physical infrastructure built to protect local interests pose transportation challenges for raw material transportation as well as product delivery throughout China. In addition, profitability and volume could be negatively impacted by limitations inherent within the supply chain, including competitive, governmental, legal, natural disasters, and other events that could impact both supply and price. Any of these occurrences could cause significant disruptions to our supply chain, manufacturing capability and distribution system that could adversely impact our ability to produce and deliver some of our products.

7

Additionally, some of the raw materials we use are procured from farmers, who can be faced with environmental risks outside of their control. If these farmers are unable to control any environmental issues, they may not have the ability to supply continuously and stably.

Our success depends on our ability to protect our intellectual property.

Our success depends on our ability to obtain and maintain patent protection for products developed utilizing our technologies, in the PRC and in other countries, and to enforce these patents. There is no assurance that any of our existing and future patents will be held valid and enforceable against third-party infringement or that our products will not infringe any third-party patent or intellectual property. Although we have filed additional patent applications with the Patent Administration Department of the PRC, there is no assurance that they will be granted.

Any patents relating to our technologies may not be sufficiently broad to protect our products. In addition, our patents may be challenged, potentially invalidated or potentially circumvented. Our patents may not afford us protection against competitors with similar technology or permit the commercialization of our products without infringing third-party patents or other intellectual property rights.

We also rely on or intend to rely on our trademarks, trade names and brand names to distinguish our products from the products of our competitors, and have registered or will apply to register a number of these trademarks. However, third parties may oppose our trademark applications or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products, which could result in loss of brand recognition and could require us to devote resources to advertising and marketing these new brands. Further, our competitors may infringe our trademarks, or we may not have adequate resources to enforce our trademarks.

In addition, we also have trade secrets, non-patented proprietary expertise and continuing technological innovation that we shall seek to protect, in part, by entering into confidentiality agreements with licensees, suppliers, employees and consultants. These agreements may be breached and there may not be adequate remedies in the event of a breach. Disputes may arise concerning the ownership of intellectual property or the applicability of confidentiality agreements. Moreover, our trade secrets and proprietary technology may otherwise become known or be independently developed by our competitors. If patents are not issued with respect to products arising from research, we may not be able to maintain the confidentiality of information relating to these products.

Our TCMP business is subject to inherent risks relating to product liability and personal injury claims.

TCMP companies, similar to pharmaceutical companies, are exposed to risks inherent in the manufacturing and distribution of TCMP products, such as with respect to improper filling of prescriptions, labeling of prescriptions, adequacy of warnings, and unintentional distribution of counterfeit drugs. In addition, product liability claims may be asserted against us with respect to any of the products we sell and as a distributor, we are required to pay for damages for any successful product liability claim against us, although we may have the right under applicable PRC laws, rules and regulations to recover from the relevant manufacturer for compensation we paid to our customers in connection with a product liability claim. We may also be obligated to recall affected products. If we are found liable for product liability claims, we could be required to pay substantial monetary damages. Furthermore, even if we successfully defend ourselves against this type of claim, we could be required to spend significant management, financial and other resources, which could disrupt our business, and our reputation as well as our brand name may also suffer. We, like many other similar companies in China, do not carry product liability insurance. As a result, any imposition of product liability could materially harm our business, financial condition and results of operations. In addition, we do not have any business interruption insurance due to the limited coverage of any available business interruption insurance in China, and as a result, any business disruption or natural disaster could severely disrupt our business and operations and significantly decrease our revenue and profitability.

8

We face risks related to research and the ability to develop new TCMP products.

Our growth and survival depends on our ability to consistently discover, develop and commercialize new products and find new and improved technology and platforms. As such, if we fail to make sufficient investments in research, be attentive to consumer needs or focus on the most advanced technology, our current and future products could be surpassed by more effective or advanced products of other companies.

Our business requires a number of permits and licenses in order to carry on their business.

Pharmaceutical companies in China are required to obtain certain permits and licenses from various PRC governmental authorities, including Good Manufacturing Practice (“GMP”) certification. We are also required to obtain a Pharmaceutical Product Permit.

Also, we participate in the manufacture of Chinese medicine, which is subject to various PRC laws and regulations pertaining to the pharmaceutical industry. We have obtained certificates, permits, and licenses required for the operation of a pharmaceutical enterprise and the manufacturing of pharmaceutical products in the PRC. We are required to meet GMP standards in order to continue manufacturing pharmaceutical products. We are required to renew the GMP every five years and our current GMP expires in 2019. There is no guarantee we will be able to renew the GMP when it next expires.

We cannot assure you that we can maintain all required licenses, permits and certifications to carry on our business at all times, and in the past from time to time we may have not been in compliance with all such required licenses, permits and certifications. Moreover, these licenses, permits and certifications are subject to periodic renewal and/or reassessment by the relevant PRC governmental authorities and the standards of such renewal or reassessment may change from time to time. We intend to apply for the renewal of these licenses, permits and certifications when required by then applicable laws and regulations. Any failure by us to obtain and maintain all licenses, permits and certifications necessary to carry on our business at any time could have a material adverse effect on our business, financial condition and results of operations. In addition, any inability to renew these licenses, permits and certifications could severely disrupt our business and prevent us from continuing to carry on our business. Any changes in the standards used by governmental authorities in considering whether to renew or reassess our business licenses, permits and certifications, as well as any enactment of new regulations that may restrict the conduct of our business, may also decrease our revenue and/or increase our costs and materially reduce our profitability and prospects. Furthermore, if the interpretation or implementation of existing laws and regulations changes or if new regulations come into effect requiring us to obtain any additional licenses, permits or certifications that were previously not required to operate our existing businesses, we cannot assure you that we will successfully obtain such licenses, permits or certifications.

Our innovative Directly-Oral-TCMP and After-Soaking-Oral-TCMP in China are subject to continuing regulation by the CFDA. If the labeling or manufacturing process of an approved medicine is significantly modified, the CFDA requires that we obtain a new pre-market approval or pre-market approval supplement. Furthermore, there is no specific law or details of regulations that apply to our innovative Directly-Oral-TCMP and After-Soaking-Oral-TCMP, but we will be required to comply with all existing and new rules related to them.

Price control regulations may decrease our profitability.

The laws of the PRC provide for the government to fix and adjust prices. The prices of certain TCMP products we distribute, including those listed in the Chinese government’s catalogue of medications that are reimbursable under the PRC’s social insurance program, or the Insurance Catalogue, are subject to control by the relevant state or provincial price administration authorities. The PRC establishes price levels for products based on market conditions, average industry cost, supply and demand and social responsibility. In practice, price control with respect to these medicines sets a ceiling on their retail price. The actual price of such medicines set by manufacturers, wholesalers and retailers cannot historically exceed the price ceiling imposed by applicable government price control regulations. Although, as a general matter, government price control regulations have resulted in lower drug prices over time, there has been no predictable pattern for such decreases. It is possible that additional products may be subject to price control, or that price controls may be increased in the future. To the extent that our products are subject to price control, our revenue, gross profit, gross margin and net income will be affected since the revenue we derive from our sales will be limited and we may face no limitation on our costs. Further, if price controls affect both our revenue and costs, our ability to be profitable and the extent of our profitability will be effectively subject to determination by the applicable regulatory authorities in the PRC. Since May 1998, the relevant PRC governmental authorities have ordered price reductions on thousands of pharmaceutical products. Such reductions, along with any future price controls or government mandated price reductions may have a material adverse effect on our financial condition and results of operations, including significantly reducing our revenue and profitability.

9

If the TCMP products we produce are replaced by other medicines or are removed from the PRC’s insurance catalogue in the future, our revenue may suffer.

Under Chinese regulations, patients purchasing medicine listed by the central and/or provincial governments in the insurance catalogue may be reimbursed, in part or in whole, by a social medicine fund. Accordingly, pharmaceutical distributors prefer to engage in the distribution of medicine listed in the insurance catalogue. Currently, 95% of our TCMP products, including 11 Advanced TCMP products are listed in the insurance catalogue. The content of the insurance catalogue is subject to change by the PRC Ministry of Labor and Social Security, and new medicine may be added to the insurance catalogue by provincial level authorities as part of their limited ability to change certain medicines listed in the insurance catalogue. If the TCMP products we produce are replaced by other medicines or removed from the insurance catalogue in the future, our revenue may suffer.

Adverse publicity associated with our products, ingredients or network marketing program, or those of similar companies, could harm our financial condition and operating results.

The results of our operations may be significantly affected by the public’s perception of our product and similar companies. This perception is dependent upon opinions concerning:

| ● | the safety and quality of our products and ingredients; |

| ● | the safety and quality of similar products and ingredients distributed by other companies; and |

| ● | our sales force. |

Adverse publicity concerning any actual or purported failure to comply with applicable laws and regulations regarding product claims and advertising, good manufacturing practices, or other aspects of our business, whether or not resulting in enforcement actions or the imposition of penalties, could have an adverse effect on our goodwill and could negatively affect our sales and ability to generate revenue. In addition, our consumers’ perception of the safety and quality of products and ingredients as well as similar products and ingredients distributed by other companies can be significantly influenced by media attention, publicized scientific research or findings, widespread product liability claims and other publicity concerning our products or ingredients or similar products and ingredients distributed by other companies. Adverse publicity, whether or not accurate or resulting from consumers’ use or misuse of our products, that associates consumption of our products or ingredients or any similar products or ingredients with illness or other adverse effects, questions the benefits of our or similar products or claims that any such products are ineffective, inappropriately labeled or have inaccurate instructions as to their use, could negatively impact our reputation or the market demand for our products.

Risks Related to Our Corporate Structure

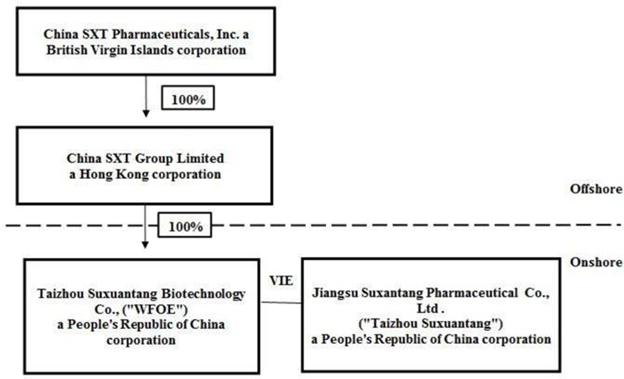

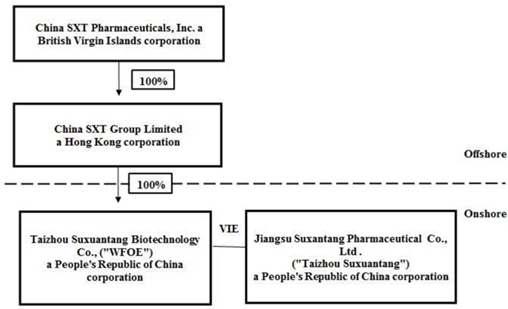

We rely on contractual arrangements with our variable interest entities in China for our business operations, which may not be as effective in providing operational control or enabling us to derive economic benefits as through ownership of controlling equity interests.

We rely on and expect to continue to rely on our wholly owned PRC subsidiary’s contractual arrangements with Taizhou Suxuantang and its respective shareholders to operate business. These contractual arrangements may not be as effective in providing us with control over Taizhou Suxuantang as ownership of controlling equity interests would be in providing us with control over, or enabling us to derive economic benefits from the operations of Taizhou Suxuantang. Under the current contractual arrangements, as a legal matter, if Taizhou Suxuantang or any of their shareholders fails to perform its, his or her respective obligations under these contractual arrangements, we may have to incur substantial costs and resources to enforce such arrangements, and rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which we cannot assure you will be effective. For example, if shareholders of a variable interest entity were to refuse to transfer their equity interests in such variable interest entity to us or our designated persons when we exercise the purchase option pursuant to these contractual arrangements, we may have to take a legal action to compel them to fulfill their contractual obligations.

If (i) the applicable PRC authorities invalidate these contractual arrangements for violation of PRC laws, rules and regulations, (ii) any variable interest entity or its shareholders terminate the contractual arrangements or (iii) any variable interest entity or its shareholders fail to perform their obligations under these contractual arrangements, our business operations in China would be materially and adversely affected, and the value of your stock would substantially decrease. Further, if we fail to renew these contractual arrangements upon their expiration, we would not be able to continue our business operations unless the then current PRC law allows us to directly operate businesses in China.

In addition, if any variable interest entity or all or part of its assets become subject to liens or rights of third-party creditors, we may be unable to continue some or all of our business activities, which could materially and adversely affect our business, financial condition and results of operations. If any of the variable interest entities undergoes a voluntary or involuntary liquidation proceeding, its shareholders or unrelated third-party creditors may claim rights to some or all of these assets, thereby hindering our ability to operate our business, which could materially and adversely affect our business and our ability to generate revenues.

10

All of these contractual arrangements are governed by PRC law and provide for the resolution of disputes through arbitration in the PRC. The legal environment in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. In the event we are unable to enforce these contractual arrangements, we may not be able to exert effective control over our operating entities and we may be precluded from operating our business, which would have a material adverse effect on our financial condition and results of operations.

Taizhou Suxuantang’s shareholders may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.

The equity interests of Taizhou Suxuantang are held by Mr. Feng Zhou, who is our founder, director. His interests may differ from the interests of our Company as a whole. He may breach, or cause Taizhou Suxuantang to breach, or refuse to renew the existing contractual arrangements we have with Taizhou Suxuantang, which would have a material adverse effect on our ability to effectively control Taizhou Suxuantang and receive economic benefits from them. For example, the shareholders may be able to cause our agreements with Taizhou Suxuantang to be performed in a manner adverse to us by, among other things, failing to remit payments due under the contractual arrangements to us on a timely basis. We cannot assure you that when conflicts of interest arise, any or all of these shareholders will act in the best interests of our Company or such conflicts will be resolved in our favor.

Currently, we do not have any arrangements to address potential conflicts of interest between these shareholders and our Company, except that we could exercise our purchase option under the exclusive option agreement with these shareholders to request them to transfer all of their equity interests in Taizhou Suxuantang to a PRC entity or individual designated by us, to the extent permitted by PRC laws. If we cannot resolve any conflict of interest or dispute between us and the shareholders of Taizhou Suxuantang, we would have to rely on legal proceedings, which could result in the disruption of our business and subject us to substantial uncertainty as to the outcome of any such legal proceedings.

Contractual arrangements in relation to our variable interest entity may be subject to scrutiny by the PRC tax authorities and they may determine that we or our PRC variable interest entity owe additional taxes, which could negatively affect our results of operations and the value of your investment.

Under applicable PRC laws and regulations, arrangements and transactions among related parties may be subject to audit or challenge by the PRC tax authorities within ten years after the taxable year when the transactions are conducted. The PRC enterprise income tax law requires every enterprise in China to submit its annual enterprise income tax return together with a report on transactions with its related parties to the relevant tax authorities. The tax authorities may impose reasonable adjustments on taxation if they have identified any related party transactions that are inconsistent with arm’s length principles. We may face material and adverse tax consequences if the PRC tax authorities determine that the contractual arrangements between our WFOE, our variable interest entity Taizhou Suxuantang and the shareholders of Taizhou Suxuantang were not entered into on an arm’s length basis in such a way as to result in an impermissible reduction in taxes under applicable PRC laws, rules and regulations, and adjust Taizhou Suxuantang’s income in the form of a transfer pricing adjustment. A transfer pricing adjustment could, among other things, result in a reduction of expense deductions recorded by Taizhou Suxuantang for PRC tax purposes, which could in turn increase their tax liabilities without reducing WFOE’s tax expenses. In addition, if WFOE requests the shareholders of Taizhou Suxuantang to transfer their equity interests in Taizhou Suxuantang at nominal or no value pursuant to these contractual arrangements, such transfer could be viewed as a gift and subject WFOE to PRC income tax. Furthermore, the PRC tax authorities may impose late payment fees and other penalties on Taizhou Suxuantang for the adjusted but unpaid taxes according to the applicable regulations. Our results of operations could be materially and adversely affected if Taizhou Suxuantang’s tax liabilities increase or if they are required to pay late payment fees and other penalties.

If we exercise the option to acquire equity ownership of Taizhou Suxuantang, the ownership transfer may subject us to certain limitation and substantial costs.

Pursuant to the contractual arrangements, WFOE has the exclusive right to purchase all or any part of the equity interests in Taizhou Suxuantang from Taizhou Suxuantang’s shareholders for a nominal price, unless the relevant government authorities or then applicable PRC laws request that a minimum price amount be used as the purchase price, in such case the purchase price shall be the lowest amount under such request. The shareholders of Taizhou Suxuantang will be subject to PRC individual income tax on the difference between the equity transfer price and the then current registered capital of Taizhou Suxuantang. Additionally, if such a transfer takes place, the competent tax authority may require WFOE to pay enterprise income tax for ownership transfer income with reference to the market value, in which case the amount of tax could be substantial.

11

Risks Related to Our Ordinary Shares

Our ordinary shares may be thinly traded and you may be unable to sell at or near ask prices or at all if you need to sell your shares to raise money or otherwise desire to liquidate your shares.

Our ordinary shares may be “thinly-traded”, meaning that the number of persons interested in purchasing our ordinary shares at or near bid prices at any given time may be relatively small or non-existent. This situation may be attributable to a number of factors, including the fact that we are relatively unknown to stock analysts, stock brokers, institutional investors and others in the investment community that generate or influence sales volume, and that even if we came to the attention of such persons, they tend to be risk-averse and might be reluctant to follow an unproven company such as ours or purchase or recommend the purchase of our shares until such time as we became more seasoned. As a consequence, there may be periods of several days or more when trading activity in our shares is minimal or non-existent, as compared to a seasoned issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. Broad or active public trading market for our ordinary shares may not develop or be sustained.

The market price for our ordinary shares may be volatile.

The market price for our ordinary shares may be volatile and subject to wide fluctuations due to factors such as:

| ● | the perception of U.S. investors and regulators of U.S. listed Chinese companies; |

| ● | our operating and financial performance; |

| ● | quarterly variations in the rate of growth of our financial indicators, such as net income per share, net income and revenues; |

| ● | the public reaction to our press releases, our other public announcements and our filings with the SEC; |

| ● | strategic actions by our competitors; |

| ● | changes in revenue or earnings estimates, or changes in recommendations or withdrawal of research coverage, by equity research analysts; |

| ● | speculation in the press or investment community; |

| ● | the failure of research analysts to cover our Ordinary Shares; |

| ● | sales of our Ordinary Shares by us or other shareholders, or the perception that such sales may occur; |

| ● | changes in accounting principles, policies, guidance, interpretations or standards; |

| ● | additions or departures of key management personnel; |

| ● | actions by our shareholders; |

| ● | domestic and international economic, legal and regulatory factors unrelated to our performance; and |

| ● | the realization of any risks described under this “Risk Factors” section. |

The stock markets in general have experienced extreme volatility that has often been unrelated to the operating performance of particular companies. These broad market fluctuations may adversely affect the trading price of our Ordinary Shares. Securities class action litigation has often been instituted against companies following periods of volatility in the overall market and in the market price of a company’s securities. Such litigation, if instituted against us, could result in very substantial costs, divert our management’s attention and resources and harm our business, operating results and financial condition.

12

For as long as we are an emerging growth company, we will not be required to comply with certain reporting requirements, including those relating to accounting standards and disclosure about our executive compensation, that apply to other public companies.

In April 2012, President Obama signed into law the JOBS Act. We are classified as an “emerging growth company” under the JOBS Act. For as long as we are an emerging growth company, which may be up to five full fiscal years, unlike other public companies, we will not be required to, among other things, (i) provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act, (ii) comply with any new requirements adopted by the PCAOB requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer, (iii) provide certain disclosure regarding executive compensation required of larger public companies or (iv) hold nonbinding advisory votes on executive compensation. We will remain an emerging growth company for up to five years, although we will lose that status sooner if we have more than $1.07 billion of revenues in a fiscal year, have more than $700 million in market value of our Ordinary Shares held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period.

To the extent that we rely on any of the exemptions available to emerging growth companies, you will receive less information about our executive compensation and internal control over financial reporting than issuers that are not emerging growth companies. If some investors find our Ordinary Shares to be less attractive as a result, there may be a less active trading market for our Ordinary Shares and our stock price may be more volatile.

If we fail to establish and maintain proper internal financial reporting controls, our ability to produce accurate financial statements or comply with applicable regulations could be impaired.

Pursuant to Section 404 of the Sarbanes-Oxley Act, we will be required to file a report by our management on our internal control over financial reporting, including an attestation report on internal control over financial reporting issued by our independent registered public accounting firm. However, while we remain an emerging growth company, we will not be required to include an attestation report on internal control over financial reporting issued by our independent registered public accounting firm. The presence of material weaknesses in internal control over financial reporting could result in financial statement errors which, in turn, could lead to errors in our financial reports and/or delays in our financial reporting, which could require us to restate our operating results. We might not identify one or more material weaknesses in our internal controls in connection with evaluating our compliance with Section 404 of the Sarbanes-Oxley Act. In order to maintain and improve the effectiveness of our disclosure controls and procedures and internal controls over financial reporting, we will need to expend significant resources and provide significant management oversight. Implementing any appropriate changes to our internal controls may require specific compliance training of our directors and employees, entail substantial costs in order to modify our existing accounting systems, take a significant period of time to complete and divert management’s attention from other business concerns. These changes may not, however, be effective in maintaining the adequacy of our internal control.

If we are unable to conclude that we have effective internal controls over financial reporting, investors may lose confidence in our operating results, the price of the Ordinary Shares could decline and we may be subject to litigation or regulatory enforcement actions. In addition, if we are unable to meet the requirements of Section 404 of the Sarbanes-Oxley Act, the Ordinary Shares may not be able to remain listed on the NASDAQ Capital Market.

As a foreign private issuer, we are not subject to certain U.S. securities law disclosure requirements that apply to a domestic U.S. issuer, which may limit the information publicly available to our shareholders.

As a foreign private issuer we are not required to comply with all of the periodic disclosure and current reporting requirements of the Exchange Act and therefore there may be less publicly available information about us than if we were a U.S. domestic issuer. For example, we are not subject to the proxy rules in the United States and disclosure with respect to our annual general meetings will be governed by British Virgin Islands requirements. In addition, our officers, directors and principal shareholders are exempt from the reporting and “short-swing” profit recovery provisions of Section 16 of the Exchange Act and the rules thereunder. Therefore, our shareholders may not know on a timely basis when our officers, directors and principal shareholders purchase or sell our Ordinary Shares.

13

As a foreign private issuer, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from the NASDAQ Stock Market corporate governance listing standards. These practices may afford less protection to shareholders than they would enjoy if we complied fully with corporate governance listing standards.

As a foreign private issuer, we are permitted to take advantage of certain provisions in the NASDAQ Stock Market listing rules that allow us to follow British Virgin Islands law for certain governance matters. Certain corporate governance practices in the British Virgin Islands may differ significantly from corporate governance listing standards as, except for general fiduciary duties and duties of care, British Virgin Islands law has no corporate governance regime which prescribes specific corporate governance standards. When our Ordinary Shares are listed on the Nasdaq Capital Market, we intend to continue to follow British Virgin Islands corporate governance practices in lieu of the corporate governance requirements of the Nasdaq Stock Market in respect of the following: (i) the majority independent director requirement under Section 5605(b)(1) of the NASDAQ Stock Market listing rules, (ii) the requirement under Section 5605(d) of the NASDAQ Stock Market listing rules that a compensation committee comprised solely of independent directors governed by a compensation committee charter oversee executive compensation, (iii) the requirement under Section 5605(e) of the NASDAQ Stock Market listing rules that director nominees be selected or recommended for selection by either a majority of the independent directors or a nominations committee comprised solely of independent directors and (iv) the requirement under Section 5605(b)(2) of the NASDAQ Stock Market listing rules that our independent directors hold regularly scheduled executive sessions. British Virgin Islands law does not impose a requirement that our board of directors consist of a majority of independent directors. Nor does British Virgin Islands law impose specific requirements on the establishment of a compensation committee or nominating committee or nominating process. Therefore, our shareholders may be afforded less protection than they otherwise would have under corporate governance listing standards applicable to U.S. domestic issuers.

We may lose our foreign private issuer status in the future, which could result in significant additional costs and expenses.

As discussed above, we are a foreign private issuer, and therefore, we are not required to comply with all of the periodic disclosure and current reporting requirements of the Exchange Act. The determination of foreign private issuer status is made annually on the last business day of an issuer’s most recently completed second fiscal quarter, and, accordingly, the next determination will be made with respect to us on September 30, 2020. We would lose our foreign private issuer status if, for example, more than 50% of our Ordinary Shares are directly or indirectly held by residents of the U.S. and we fail to meet additional requirements necessary to maintain our foreign private issuer status. If we lose our foreign private issuer status on this date, we will be required to file with the SEC periodic reports and registration statements on U.S. domestic issuer forms beginning on January 1, 2021, which are more detailed and extensive than the forms available to a foreign private issuer. We will also have to mandatorily comply with U.S. federal proxy requirements, and our officers, directors and principal shareholders will become subject to the short-swing profit disclosure and recovery provisions of Section 16 of the Exchange Act. In addition, we will lose our ability to rely upon exemptions from certain corporate governance requirements under the NASDAQ Stock Market listing rules. As a U.S. listed public company that is not a foreign private issuer, we will incur significant additional legal, accounting and other expenses that we will not incur as a foreign private issuer, and accounting, reporting and other expenses in order to maintain a listing on a U.S. securities exchange.

The requirements of being a public company may strain our resources and divert management’s attention.

As a public company, we are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, the Sarbanes-Oxley Act, the Dodd-Frank Act, the listing requirements of the securities exchange on which we list, and other applicable securities rules and regulations. Despite recent reforms made possible by the JOBS Act, compliance with these rules and regulations will nonetheless increase our legal, accounting, and financial compliance costs and investor relations and public relations costs, make some activities more difficult, time-consuming or costly and increase demand on our systems and resources, particularly after we are no longer an “emerging growth company.” The Exchange Act requires, among other things, that we file annual, quarterly, and current reports with respect to our business and operating results as well as proxy statements.

14

As a result of disclosure of information in this annual report and in filings required of a public company, our business and financial condition will become more visible, which we believe may result in threatened or actual litigation, including by competitors and other third parties. If such claims are successful, our business and operating results could be harmed, and even if the claims do not result in litigation or are resolved in our favor, these claims, and the time and resources necessary to resolve them, could divert the resources of our management and adversely affect our business, brand and reputation and results of operations.

We also expect that being a public company and these new rules and regulations will make it more expensive for us to obtain director and officer liability insurance, and we may be required to accept reduced coverage or incur substantially higher costs to obtain coverage. These factors could also make it more difficult for us to attract and retain qualified members of our board of directors, particularly to serve on our audit committee and compensation committee, and qualified executive officers.

We do not intend to pay dividends for the foreseeable future.

We currently intend to retain any future earnings to finance the operation and expansion of our business, and we do not expect to declare or pay any dividends in the foreseeable future. As a result, you may only receive a return on your investment in our Ordinary Shares if we are successfully listed and the market price of our Ordinary Shares increases.

The obligation to disclose information publicly may put us at a disadvantage to competitors that are private companies.

As a public company, we are required to file periodic reports with the Securities and Exchange Commission upon the occurrence of matters that are material to our Company and shareholders. Although we may be able to attain confidential treatment of some of our developments, in some cases, we will need to disclose material agreements or results of financial operations that we would not be required to disclose if we were a private company. Our competitors may have access to this information, which would otherwise be confidential. This may give them advantages in competing with our Company. Similarly, as a U.S. public company, we will be governed by U.S. laws that our competitors, which are mostly private Chinese companies, are not required to follow. To the extent compliance with U.S. laws increases our expenses or decreases our competitiveness against such companies, our public Company status could affect our results of operations.

A sale or perceived sale of a substantial number of shares of our Ordinary Shares may cause the price of our Ordinary Shares to decline.

All of our executive officers and directors and all of our shareholders have agreed not to sell shares of our Ordinary Shares for a period of six months following our initial public offering, subject to extension under specified circumstances. See “Lock-Up Agreements.” Ordinary shares subject to these lock-up agreements will become eligible for sale in the public market upon expiration of these lock-up agreements, subject to limitations imposed by Rule 144 under the Securities Act of 1933, as amended. If our shareholders sell substantial amounts of our Ordinary Shares in the public market, the market price of our Ordinary Shares could fall. Moreover, the perceived risk of this potential dilution could cause shareholders to attempt to sell their shares and investors to short our ordinary shares. These sales also may make it more difficult for us to sell equity or equity-related securities in the future at a time and price that we deem reasonable or appropriate.

15

Risks Related to Doing Business in China

Recent scrutiny and potential tightened regulation of public companies with majority of its operation in China may have adverse impact on our share performance and even our listing on the Nasdaq Capital Market.

At various times in recent years, the United States and China have had significant disagreements over political and economic issues. Controversies may arise in the future between the two countries. Any political or trade controversies between the United States and China, whether or not directly related to our business, could reduce the price of our ordinary shares.

In June 2019, a bipartisan group of lawmakers introduced bills in both houses of the U.S. Congress, and passed requiring the SEC to maintain a list of issuers for which the Public Company Accounting Oversight Board, or the PCAOB is not able to inspect or investigate an auditor report issued by a foreign public accounting firm. The proposed Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges (EQUITABLE) Act prescribes increased disclosure requirements for these issuers and, beginning in 2025, the delisting from U.S. national securities exchanges of issuers included on the SEC’s list for three consecutive years. On May 20, 2020, the U.S. Senate passed the Holding Foreign Companies Accountable Act, or HFCA Act, which in effect would prohibit securities of any registrant from being listed on any of the U.S. securities exchanges or traded “over-the-counter” if registrant’s financial statements have, for a period of three years, been audited by an accounting firm branch or office that is not subject to PCAOB inspection. Although our independent registered public accounting firm is located in the United States and subject to the regular inspection of PCAOB to assess its compliance with the applicable professional standards, enactment of any of such legislations or other efforts to increase U.S. regulatory access to audit information could cause investor uncertainty for affected Chin-based issuers, and our share price could be adversely affected. There is uncertainty as to whether and when these bills or legislations will be enacted in the proposed form, or at all.