January 12, 2023

Division of Corporation Finance

U.S. Securities & Exchange Commission

100 F Street, NE

Washington, D.C. 20549

| Re: | Sunlands Technology Group |

Form 20-F for the Year Ended December 31, 2021

Filed April 27, 2022

File No. 001-38423

| Attn: | Division of Corporation Finance Office of Trade & Services |

VIA EDGAR

Dear Nasreen Mohammed, Joel Parker, Alyssa Wall and Taylor Beech:

This letter sets forth the responses of Sunlands Technology Group (the “Company”) to the comments (the “Comments”) the Company received from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) in a letter dated December 23, 2022.

For the Staff’s convenience, we have included herein the Comments in bold, and the Company’s responses are set forth immediately below the Comments.

General Note to the Staff:

The Company respectfully submits in this letter its proposed amendments to the disclosures contained in the Company’s annual report on Form 20-F for the fiscal year ended December 31, 2021 filed with the Commission on April 27, 2022 (the “2021 Annual Report”) (with new language indicated by underlines and deleted language indicated by strike-through marks). The Company undertakes to include the proposed disclosures substantially as set forth below in its annual report on Form 20-F for the fiscal year ended December 31, 2022 (the “2022 Annual Report”), subject to the Staff’s further review and comment with appropriate revisions and updates to reflect the Company’s circumstances at the time when it files the 2022 Annual Report.

Form 20-F for the Year Ended December 31, 2021

Item 3. Key Information, page 1

1. Please explain whether the VIE structure is used to provide investors with exposure to foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the operating companies.

Response

In response to the Staff’s Comments, the Company intends to revise the first paragraph under “Contractual Arrangements and Corporate Structure” on page 46 of the 2021 Annual Report to clarify that the VIE structure is used to provide investors with exposure to foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the operating companies. Please

1

see the Company’s responses to comment 4 below for the revised disclosure. The Company will include comparable disclosure in the 2022 Annual Report.

2. Please remove your disclosure that uses terms such as “we” or “our” (i.e. “our consolidated VIEs”) when describing activities or functions of the VIEs, as you do not have ownership or control of the VIEs.

Response

In response to the Staff’s Comments, the Company intends to revise the definition of “we,” “us,” “our company,” “our Company,” “our Group” and “our” on pages i and 1 of the 2021 Annual Report as follows:

“we,” “us,”

“our company,” “our Company,” “our Group” and “our,” refer to Sunlands Technology Group,

previously known as Sunlands Online Education Group, a Cayman Islands company and its subsidiaries and, in the context of describing

our operations and consolidated financial information, its consolidated variable interest entities, or VIEs, and VIEs’ subsidiaries.

The Company also undertakes to include such revised definition in the 2022 Annual Report and ensure the disclosures throughout the 2022 Annual Report will clearly differentiate the holding company and its subsidiaries on the one hand from the VIEs on the other hand.

3. We note you carve Hong Kong out from your definition of “China” or “PRC.” Please expand your disclosure to clarify that the legal and operational risks associated with operating in China also apply to operations in Hong Kong. Additionally, please discuss the applicable laws and regulations in Hong Kong, as well as the related risks and consequences. For example, address how regulatory actions related to data security or anti-monopoly concerns in Hong Kong have or may impact the company’s ability to conduct its business, accept foreign investment or list on a U.S. or foreign exchange. Move your various discussions of China’s Enterprise Tax Law to a more prominent place in this Item 3.

Response

In response to the Staff’s Comments, the Company respectfully advises the Staff that it intends to revise the definition of “China” or “PRC” on page i of the 2021 Annual Report as follows. The Company will include comparable disclosure in the 2022 Annual Report.

“China”

or “PRC” refers to the People’s Republic of China; excluding, for the purposes of this annual report only,

and only in the context of describing PRC laws, regulations and other legal or tax matters in this annual report, excludes Hong

Kong, Macau and Taiwan;

The Company also intends to clarify, as applicable, that the legal and operational risks associated with operating in China also apply to operations in Hong Kong throughout the annual report. Please see the Company’s responses to comment 11 below for the revised disclosure. The Company will include comparable disclosure throughout the 2022 Annual Report.

The Company respectfully advises the Staff that it does not have material operations in Hong Kong. The Company did not have any revenue generated in Hong Kong for the years ended December 31, 2019, 2020 and 2021 and currently does not have any employees or material assets or licenses in Hong Kong. Furthermore, the Company currently does not consider Hong Kong to be a main target market or expect to have material operations in Hong Kong in the foreseeable future.

In light of the foregoing, the Company respectfully submits that the regulatory actions related to data security or anti-monopoly concerns in Hong Kong do not have a material impact on its ability to conduct its business, accept foreign investment or list on a U.S. or foreign exchange.

2

In response to the Staff’s Comments, the Company intends to move up the risk factors “—If we are classified as a PRC resident enterprise for PRC enterprise income tax purposes, such classification could result in unfavorable tax consequences to us and our non-PRC shareholders and ADS holders” and “—We face uncertainty with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies” to a more prominent place in this Item 3, right before the risk factor “—We cannot assure you that we will not be subject to liability claims or legal or regulatory liability for any inappropriate or illegal content, which could subject us to liabilities and cause damages to our reputation” on page 17, in the 2021 Annual Report. The Company will also include comparable disclosure in the 2022 Annual Report.

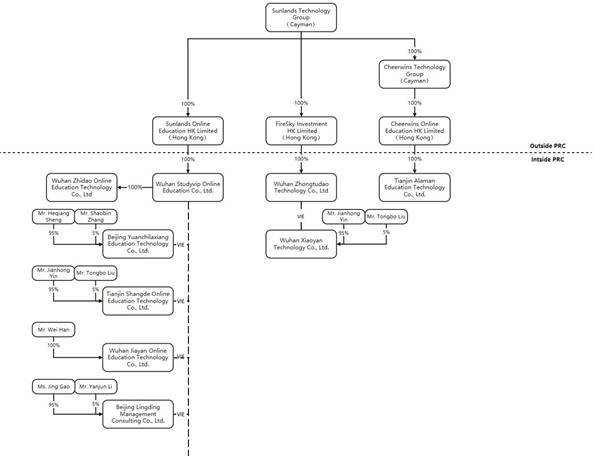

4. We note your disclosure of the organizational structure of your company and contractual arrangements with the consolidated VIEs beginning on page 81. Please provide the diagram of the company’s corporate structure early in Item 3. Please also revise your diagram to remove arrows on the dashed lines representing relationships with the VIEs. Also in Item 3, please describe all contracts and arrangements through which you claim to have economic rights and exercise control that results in consolidation of the VIEs’ operations and financial results into your financial statements. Describe the relevant contractual agreements between the entities and how this type of corporate structure may affect investors and the value of their investment, including how and why the contractual arrangements may be less effective than direct ownership and that the company may incur substantial costs to enforce the terms of the arrangements. Disclose the uncertainties regarding the status of the rights of the Cayman Islands holding company with respect to its contractual arrangements with the VIEs, the VIEs’ founders and owners, and the challenges the company may face enforcing these contractual agreements due to legal uncertainties and jurisdictional limits.

Response

In response to the Staff’s Comments, the Company respectfully advises the Staff that it intends to update the diagram illustrating its organizational structure on page 81 of the 2021 Annual Report to address the Staff’s Comments and disclose the revised diagram prominently on page 1 of the 2021 Annual Report under “Item 3. Key Information—Our Holding Company Structure.” The Company will include the revised diagram in the 2022 Annual Report.

3

In responses to the Staff’s Comments, the Company respectfully advises the Staff that it intends to revise the paragraphs on page 46 as follows and will include the same revised disclosure prominently on page 2 of the 2021 Annual Report under “Item 3. Key Information.” The Company will also include comparable disclosure in the 2022 Annual Report.

Contractual Arrangements and Corporate Structure

We are

a Cayman Islands company and currently conduct substantially all of our business operations in the PRC through our subsidiaries

incorporated in the PRC, and the contractual arrangements among our PRC subsidiaries and the VIEs. Our

subsidiaries control the VIEs in the PRC, through a series of contractual arrangements. We conduct a significant portion of our businesses

in China through the VIEs. It is the VIEs that hold our key operating licenses, provide services to our

customers, and enter into contracts with our suppliers. We operate our businesses this way

because PRC laws and regulations restrict foreign investment in companies that engage in value-added telecommunication services. These

contractual arrangements entered into with the VIEs allow us to (i) exercise effective control over the VIEs (i) direct

the activities of the VIEs that most significantly impact the VIEs’ economic performance, (ii) receive substantially all of

the economic benefits of the VIEs, and (iii) have an exclusive option to purchase all or part of the equity interests in the VIEs when

and to the extent permitted by PRC law. The VIE structure is used to provide investors with exposure to foreign investment in China-based

companies where PRC law restricts direct foreign investment in such operating companies in the PRC. These contractual arrangements

include the operating agreements, equity pledge agreements, exclusive purchase option agreements, shareholder voting right trust agreements,

loan agreements, and cooperation agreements, as the case may be. As a result of these contractual arrangements, we exert effective

control over, and are considered the

4

primary beneficiary of the VIEs for accounting purposes and are able to consolidate their operating results in our financial statements under U.S. GAAP.

It is important to note

that investors in the ADSs are purchasing equity securities of a Cayman Islands holding company rather than equity securities issued by

our subsidiaries and the VIEs. More specifically, investors in the ADSs or our ordinary shares would not be holding any ownership interest,

directly or indirectly, in the VIEs under current PRC laws and regulations as investors would only have the contractual relationship with

the operating entities in the PRC. Neither such investors nor the holding company itself have an equity ownership in, direct investment

in, or control of, through such ownership or investment, the VIEs. Investors who are non-PRC residents may never directly hold equity

interests in the VIEs under current PRC laws and regulations.

We do not have any equity interests in the VIEs who are owned by certain nominee shareholders. Any of such nominee shareholders could

breach their contractual arrangements with us by, among other things, failing to conduct their operations in an acceptable manner or taking

other actions that are detrimental to our interests. In the event that the shareholders of the VIEs breach the terms of these contractual

arrangements and voluntarily liquidate the VIEs, or the VIEs declare bankruptcy and all or part of their assets become subject to liens

or rights of third-party creditors, or are otherwise disposed of without our consent, we may be unable to conduct some or all business

operations or otherwise benefit from the assets held by the VIEs and their shareholders, which could have a material adverse effect on

our and the VIEs’ business, financial condition and results of operations. As a result, control through these

contractual arrangements may be less effective than direct ownership, and we could face heightened challenges, risks and costs

in enforcing these contractual arrangements due to legal uncertainties and jurisdictional limits, because there are substantial

uncertainties regarding the interpretation and application of current and future PRC laws, regulations, and rules relating to the legality

and enforceability of these contractual arrangements. If the PRC government finds such agreements to be illegal, we could be subject to

severe penalties or be forced to relinquish our interests in the VIEs.

The Company further respectfully directs the Staff to pages 81 to 84 of the 2021 Annual Report for a detailed discussion of the company’s corporate structure, including who hold equity ownership interests of each entity, and all contracts and arrangements through which the Company claims to have economic rights and exercises control that results in consolidation of the VIEs’ operations and financial results into the Company’s financial statements. The Company intends to include the same disclosure on page 2 of the 2021 Annual Report under “Item 3. Key Information” as well and will also include comparable disclosure in the 2022 Annual Report.

5. We note your disclosure that the Cayman Islands holding company controls and receives the economic benefits of the VIEs’ business operations through contractual agreements between the VIEs and your Wholly Foreign-Owned Enterprises (WFOEs). We also note your disclosure that the Cayman Islands holding company is the primary beneficiary of the VIEs. However, neither the investors in the holding company nor the holding company itself have an equity ownership in, direct foreign investment in, or control of, through such ownership or investment, the VIEs. Accordingly, please revise your disclosure to refrain from implying that the contractual agreements are equivalent to equity ownership in the business of the VIEs. Any references to control or benefits that accrue to you because of the VIEs should be limited to a clear description of the conditions you have satisfied for consolidation of the VIEs under U.S. GAAP. Additionally, your disclosure should clarify that you are the primary beneficiary of the VIEs for accounting purposes. Please also disclose, if true, that the VIE agreements have not been tested in a court of law. This comment applies to disclosure about the VIEs throughout the filing.

Response

In responses to the Staff’s Comments, the Company intends to revise the disclosure on page 1 of the 2021 Annual Report as follows and as set forth in its responses to comment 4 above, as well as to revise

5

the other disclosures about the VIEs throughout the filing accordingly. The Company will include such revised disclosures in the 2022 Annual Report.

Our Holding Company Structure

Sunlands

Technology Group is a Cayman Islands holding company. It conducts its operations in China through its PRC subsidiaries and consolidated

variable interest entities, or the VIEs. However, we and our direct and indirect subsidiaries do not, and it is virtually impossible

for them to, have any equity interests in the VIEs in practice as current PRC laws and regulations restrict foreign investment in companies

that engage in value-added telecommunication services. As a result, we depend on certain contractual arrangements with the VIEs to operate

a significant portion of our business. This structure allows us to exercise effective control over the VIEs,

and is designed to replicate substantially the same economic benefits as would be provided by direct ownership be considered

the primary beneficiary of the VIEs for accounting purposes, which serves the purpose of consolidating the VIEs’ operating results

in our financial statements under U.S. GAAP. The VIEs are owned by certain nominee shareholders, not us. Most of the nominee shareholders

of the VIEs are also beneficial owners of our company. Investors in our ADSs are purchasing equity securities of a Cayman Islands holding

company rather than equity securities issued by our subsidiaries and the VIEs. Investors who are non-PRC residents may never directly

hold equity interests in the VIEs under current PRC laws and regulations. As used in this annual report, “we,” “us,”

“our company,” “our,” or “Sunlands” refers to Sunlands Technology Group and its subsidiaries. and,

in the context of describing our consolidated financial information, business operations and operating data, our consolidated VIEs.

“Variable interest entities” or “VIEs” refers

to Beijing Yuanchilaxiang Education Technology Co., Ltd. (formerly known as “Beijing Shangde Online Education Technology

Co., Ltd”), or Beijing Sunlands, Wuhan Xiaoyan Technology Co., Ltd., or Wuhan Xiaoyan, Wuhan Jiayan Online Education Technology

Co., Ltd., or Wuhan Jiayan, Beijing Odysseus Education Technology Co., Ltd., or Beijing Odysseus, Wuhan Hadeliang Online Education

Technology Co., Ltd., or Wuhan Hadeliang, Tianjin Shangde Online Education Technology Co., Ltd., or Tianjin Shangde, Wuhan

Fangtang Education Technology Co., Ltd., or Wuhan Fangtang, Beijing Zhiziyuanshui Education Technology Co., Ltd., or Beijing Zhiziyuanshui,

Beijing Feibian Education Technology Co., Ltd., or Beijing Feibian, and Beijing Lingding Management Consulting Co., Ltd., or

Beijing Lingding. The VIEs primarily conduct operations in China. The VIEs are consolidated for accounting purposes but are not entities

in which we own equity. Our Company does not conduct operations by ourselves.

Our

corporate structure involves unique risks to investors in the ADSs. In 2019, 2020 and 2021, the amount of revenues generated by the VIEs

accounted for 93.4%, 47.3% and 21.4%, respectively, of our total net revenues. As of December 31, 2020 and 2021, total assets of the

VIEs, excluding amounts due from other consolidated entities in the our company, equaled to 32.7% and 33.6% of our consolidated total

assets as of the same dates, respectively. As of the date of this annual report, to the best knowledge of our directors and

management, the VIE agreements Our contractual arrangements with the VIEs have not been tested in a court

of law in the PRC. If the PRC government deems that our contractual arrangements with the VIEs do not comply with PRC regulatory

restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations

change in the future, we could be subject to material penalties or be forced to relinquish our contractual interests in those

operations or otherwise significantly change our corporate structure. We and our investors face significant uncertainty about potential

future actions by the PRC government that could affect the legality and enforceability of the contractual arrangements with the VIEs

and, consequently, significantly affect our ability to consolidate the financial results of the VIEs and the financial performance of

our company as a whole. Our ADSs may decline in value or become worthless if we are unable to effectively enforce our contractual control

rights over the assets and operations of the VIEs that conduct a significant portion of our and the VIEs’ business in China.

See “Item 3. Key Information-3.D. Risk Factor-Risks Related to Our Corporate Structure” for detailed discussion.

6

6. Disclose each permission or approval that you, your subsidiaries, or the VIEs are required to obtain from Chinese authorities to operate your business and to offer securities to foreign investors. In addition to your disclosure regarding the CSRC and CAC, state whether you, your subsidiaries, or VIEs are covered by permissions requirements from any other governmental agency that is required to approve the VIE’s operations, and state affirmatively whether you have received all requisite permissions or approvals and whether any permissions or approvals have been denied. Please also describe the consequences to you and your investors if you, your subsidiaries, or the VIEs: (i) do not receive or maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, or (iii) applicable laws, regulations, or interpretations change and you are required to obtain such permissions or approvals in the future.

Response

In responses to the Staff’s Comments, the Company intends to revise the disclosure under “Licenses and Approvals” on page 63 as follows and include such revised disclosure prominently on page 2 of the 2021 Annual Report under “Item 3. Key Information.” The Company will also include comparable disclosure in the 2022 Annual Report.

Licenses and Approvals

Our PRC subsidiaries and

the VIEs have obtained all material licenses and approvals required for our and the VIEs’ operations in China, except as

disclosed in “Item 3. Key Information-3.D. Risk Factors-Risk Related to Our Business-We face risks associated with our

lack of a private school operating permit for our online education services as well as uncertainties surrounding PRC

laws and regulations governing the education industry in general, including the Law for Promoting Private Education and its Implementation

Rules”, “Item 3. Key Information-3.D. Risk Factors-Risks Related to Our Business-We face regulatory risks and uncertainties

with respect to the licensing requirement for the online transmission of internet audio-visual programs”, and “Item 3. Key

Information-3.D. Risk Factors-Risk Related to Our Business-OurThe failure to obtain and maintain other approvals,

licenses, permits or filings applicable to our or the VIEs’ business could have a material adverse impact on our and the

VIEs’ business, financial conditions and results of operations.”

The following table sets

forth a list of material licenses and approvals, subject to further renewal, that our PRC subsidiaries and the VIEs are required

to obtain and have obtained to carry out our and the VIEs’ operations in China and none of such material

licenses and approvals obtained had been denied or rescinded.

| License | Entity Holding the License | Status |

| Value-added telecommunications business license (ICP certificate) | Beijing Sunlands (VIE) | Obtained |

Publication business operating license |

Wuhan Shangde (PRC subsidiary) | Obtained |

| Beijing Sunlands (VIE) | Obtained | |

| License for the Production and Operation of Radio and Television Program | Beijing Sunlands (VIE) | Obtained |

| Food Business License | Beijing Feibian Education Technology Co., Ltd. (Subsidiary of a VIE) | Obtained |

7

| Beijing Baobian Consumer Technology Co., Ltd. (Subsidiary of a VIE) | Obtained |

Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we or any of the VIEs may be required to obtain additional licenses, permits, filings, registrations or approvals for business operations in the future. If we are or any of the VIEs is found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required licenses, permits, filings, registrations or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures. In addition, if we or any of the VIEs had inadvertently concluded that such licenses, approvals, permits, registrations or filings were not required, or if applicable laws, regulations or interpretations change in a way that requires us or any of the VIEs to obtain such licenses, approval, permits, registrations or filings in the future, we or the relevant VIEs may be unable to obtain such necessary licenses, approvals, permits, registrations or filings in a timely manner, or at all, and such licenses, approvals, permits, registrations or filings may be rescinded even if obtained. Any such circumstance may subject us or the relevant VIEs to fines and other regulatory, civil or criminal liabilities, and we or the relevant VIEs may be ordered by the competent government authorities to suspend relevant operations, which will materially and adversely affect our or the VIEs’ business operation. For risks relating to licenses and approvals required for business operations in China, see “Item 3. Key Information-3.D. Risk Factors-Risk Related to Our Business.”

In addition, the PRC government has recently indicated an intent to exert more oversight over overseas securities offerings and published a series of laws and regulations to regulate such transactions. In connection with our prior overseas offerings and NYSE listing status, as of the date of this annual report, we (i) have not been required to obtain any permission from or complete any filing with the CSRC, and (ii) have not been required to go through a cybersecurity review by the CAC. As advised by our PRC legal counsel, under the currently effective PRC laws and regulations, we, as a company that has been listed on a foreign stock exchange before the promulgation of the Revised Cybersecurity Review Measures, are not required to go through a cybersecurity review by the CAC to conduct a security offering or maintain our listing status on the NYSE, based on their consultation with competent government authorities. As the Draft Overseas Listing Regulations have not come into effect, under the currently effective PRC laws and regulations, we are currently not required to obtain any permission from or complete any filing with the CSRC to conduct a securities offering or maintain our listing status on the NYSE. However, there are substantial uncertainties as to how PRC governmental authorities will regulate overseas listings and offerings in general and whether we are required to complete any filing or obtain any specific regulatory approval from the CSRC, the CAC or any other PRC governmental authorities for our future overseas securities offerings. If we had inadvertently concluded that such approvals or filings were not required, or if applicable laws, regulations or interpretations change in a way that requires us to complete such filings or obtain such approvals in the future, we may be unable to fulfill such requirements in a timely manner, or at all, and such approvals or filings may be rescinded even if obtained or completed. Any such circumstance could subject us to penalties, including fines, suspension of business and revocation of required licenses, significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. For more detailed information, see “Item 3. Key Information-D. Risk Factors-Risks Related to Doing Business in China-The approval, filing or other requirements of the China Securities Regulatory Commission or other PRC government authorities may be required under PRC law in connection with our issuance of securities overseas.”

8

The Company also intends to revise the disclosure under “Item 3. Key Information-D. Risk Factors” on page 8 to page 11 as follows. The Company will also include comparable disclosure in the 2022 Annual Report.

We face risks associated

with our lack of a private school operating permit for our online education services as well as uncertainties

surrounding PRC laws and regulations governing the education industry in general, including the Law for Promoting Private Education and

its Implementation Rules.

……

Moreover, the MOE, jointly

with certain other PRC government authorities, promulgated the Opinions on Guiding and Regulating the Orderly and Healthy Development

of Educational Mobile Apps on August 10, 2019, or the Opinions on Educational Apps, which requires, among others, mobile apps that offer

services for school teaching and management, student learning and student life, or home-school interactions, with school faculty, students

or parents as the main users, and with education or learning as the main application scenarios, be filed with the competent provincial

regulatory authorities for education before the end of 2019. In addition, on November 11, 2019, MOE issued the Administrative Measures

on Filing of Educational Mobile Apps, which requires, among others, that educational mobile app providers shall file their educational

mobile apps and that filings of existing educational mobile apps shall be completed before January 31, 2020. See “Item 4. Information

on the Company—4.B. Business Overview—Regulations—Regulations on Online and Distance Education.” Our

The educational mobile apps Shangde Jigou and Shangde Zikao have been filed with competent regulatory authority as required under

the Opinions on Educational Apps. However, in order to implement the requirements under the Opinions on Further Alleviating the

Burden of Homework and After-School Tutoring for Students in Compulsory Education, the education authorities require the re-filing of

educational mobile Apps. As of the date of this annual report, we have completed the re-filing procedure of Shangde Zikao and Shangde

Jigou. as the Opinions on Educational Apps are relatively new and evolving, and our and the VIEs’ business model and

practices are continuing to evolve and change, we cannot assure you that we are in full compliance with all relevant rules and will

be able to complete or maintain such filing in relation with any of our or the VIEs’ new apps and comply with other regulatory requirements

under the Opinions on Educational Apps in a timely manner, or at all. For example, the filings of certain of our or the VIEs’

educational mobile apps, such as Meiri Lexue, Feibian Jiaoyu, Jixiang Jiaoyu, Zhizi Ketang, Zhizi Yunketang,

Zhizi Kaoyan, Zhizi Renli, Jiayan Ketang, Gaozhi Kuaiji Fangtang Youke and Banmo Ketang Sanjing

Shuhua, have not been completed. If we fail to promptly complete such filing and comply with other applicable regulatory

requirements, we may be blacklisted by the MOE or its local counterparts and prohibited from submitting any filings for six months, or

may be subject to fines, regulatory orders to suspend our or the VIEs’ operations or other regulatory and disciplinary sanctions.

……

Our

The failure to obtain and maintain other approvals, licenses, permits or filings applicable to our or the VIEs’ business

could have a material adverse impact on our and the VIEs’ business, financial conditions and results of operations.

……

One of our subsidiaries, Wuhan Shangde, has registered “online educational training” in its authorized scope of business. However, the VIEs, and certain of their operating subsidiaries currently do not include “occupational training” and “educational facilitation services” in their authorized scope of business. Based on our consultation with the competent government authorities in Beijing, such government authorities currently may not accept applications for inclusion of “occupational training,” “educational facilitation services” or similar items in the scope of business of companies that do not hold a private school operating permit. For additional information about the private school operating

9

permit, see “—We

face risks associated with our lack of a private school operating permit for our online education services

as well as uncertainties surrounding PRC laws and regulations governing the education industry in general, including the Law for Promoting

Private Education and its Implementation Rules.” Even if our the application were to be accepted, there

is no assurance that it will be approved by the government authorities in a timely fashion, or at all. Furthermore, certain of the

VIEs and their operating subsidiaries that engage in online educational services may be required by relevant government authorities to

obtain the Value-Added Telecommunications Business Operating License and the License for the Production and Operation of Radio and Television

Program. If it comes to the attention of the government authorities that the VIEs and their operating subsidiaries are operating beyond

their respective authorized scope of business, we may be subject to fines, confiscation of the gains derived from the noncompliant operations,

or may be required to cease the VIEs’ noncompliant operations. In addition, we and the VIEs deliver courses in live streaming

format on our proprietary live streaming platform which the relevant authorities may regard as a live-streaming platform and may thus

require us and the VIEs to make necessary filings as a live-streaming platform. See “Item 4. Information on the Company—4.B.

Business Overview—Regulations—Regulations Relating to Internet Live Streaming Services.”

……

3.D. Risk Factors, page 2

7. Include risk factor disclosure explaining whether there are laws/regulations in Hong Kong that result in oversight over data security, how this oversight impacts the company’s business and the offering, and to what extent the company believes that it is compliant with the regulations or policies that have been issued.

Response

The Company respectfully advises the Staff that as mentioned in its responses to comment 3 above, it currently does not, and does not expect to in the foreseeable future, have material operations in Hong Kong. Therefore, the Company does not believe that the application of Hong Kong laws, including those that may result in oversight over data security, will have a material impact on the Company’s business or offering by the Company of its securities.

Summary of Risk Factors, page 2

8. In your summary of risk factors, disclose the risks that your corporate structure and being based in or having the majority of the company’s operations in China poses to investors. For example, specifically discuss risks arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and that rules and regulations in China can change quickly with little advance notice; and the risk that the Chinese government may intervene or influence your operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in your operations and/or the value of your securities. Your disclosure should address how recent statements and regulatory actions by China’s government, such as those related to the use of variable interest entities, have or may impact the company’s ability to conduct its business, accept foreign investments, or list on a U.S. or other foreign exchange. Acknowledge any risks that any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Please provide cross-references to the relevant individual detailed risk factors in the annual report.

10

Response

In response to the Staff’s Comments, the Company intends to revise the Summary of Risk Factors on pages 2 to 4 of the 2021 Annual Report as follows and include comparable disclosure in the 2022 Annual Report.

We face various legal and

operational risks and uncertainties as a company based in and primarily operating in China. The PRC government has significant authority

to exert influence on the ability of a China-based company, like us, to conduct its business, accept foreign investments or be listed

on a U.S. stock exchange. For example, we face risks associated with regulatory approvals of offshore offerings, anti-monopoly regulatory

actions, cybersecurity and data privacy, as well as the uncertainty on whether lack of inspection from the U.S.

Public Company Accounting Oversight Board, or PCAOB, will continue to be able to satisfactorily inspect or investigate completely registered

public accounting firms headquartered in mainland China and Hong Kong on our auditors. The PRC government may also

intervene with or influence our and the VIEs’ operations as the government deems appropriate to further regulatory, political

and societal goals. The PRC government has recently published new policies that significantly affected educational industry and we cannot

rule out the possibility that it will in the future further release regulations or policies regarding educational industry that could

adversely affect our and the VIEs’ business, financial condition and results of operations. Any such action, once taken by

the PRC government, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors

and cause the value of such securities to significantly decline or in extreme cases, become worthless. Furthermore, as a Cayman

Islands holding company with no business operations, the Company conducts its operations in China through its PRC subsidiaries and the

VIEs and the VIEs’ subsidiaries. Thus, our corporate structure involves unique risks to investors in the ADSs.

You should carefully consider all of the information in this annual report before making an investment in the ADSs. Below please find a summary of the principal risks and uncertainties we face, organized under relevant headings. In particular, as we are a China-based company incorporated in the Cayman Islands, you should pay special attention to subsections headed “Item 3. Key Information 3.D. Risk Factors-Risks Related to Doing Business in China” and “Item 3. Key Information-3.D. Risk Factors-Risks Related to Our Corporate Structure.”

……

| · | Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in policies, laws and regulations in China, could adversely affect us. The enforcement of laws and rules and regulations in China may change quickly with little advance notice, which could result in a material adverse change in our and the VIEs’ operations and the value of our ADSs. For details, please see pages 28 to 29. |

| · | The PRC government’s significant oversight over our and the VIEs’ business operation in China could result in a material adverse change in our and the VIEs’ operations in China and the value of our ADSs. The Chinese government may intervene or influence our and the VIEs’ operations in China at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or become worthless. For details, please see page 29. |

Risks Related to Doing Business in China, page 27

11

9. Given the Chinese government’s significant oversight and discretion over the conduct of your business, please revise to highlight separately the risk that the Chinese government may intervene or influence your operations at any time, which could result in a material change in your operations and/or the value of your securities. Also, given recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, acknowledge the risk that any such action could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Response

In response to the Staff’s Comments, the Company intends to revise the risk factors on pages 28 to 29 of the 2021 Annual Report as follows and include comparable disclosure in the 2022 Annual Report.

Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in policies, laws and regulations in China, could adversely affect us. The enforcement of laws and rules and regulations in China may change quickly with little advance notice, which could result in a material adverse change in our and the VIEs’ operations and the value of our ADSs.

The PRC legal system is a civil law system based on written statutes. Unlike the common law system, prior court decisions under the civil law system may be cited for reference but have limited precedential value.

In 1979, the PRC government began to promulgate a comprehensive system of laws and regulations governing economic matters in general. The overall effect of legislation over the past three decades has significantly enhanced the protections afforded to various forms of foreign investments in China. However, China has not developed a fully integrated legal system, and recently enacted laws and regulations may not sufficiently cover all aspects of economic activities in China. In particular, the interpretation and enforcement of these laws and regulations involve uncertainties and may change quickly with little advance notice, which could result in a material adverse change in our and the VIEs’ operations and the value of our ADSs. Since PRC administrative and court authorities have significant discretion in interpreting and implementing statutory provisions and contractual terms, it may be difficult to evaluate the outcome of administrative and court proceedings and the level of legal protection we enjoy. These uncertainties may affect our judgment on the relevance of legal requirements and our ability to enforce our contractual rights or tort claims. In addition, the regulatory uncertainties may be exploited through unmerited or frivolous legal actions or threats in attempts to extract payments or benefits from us.

The

PRC government has significant oversight and discretion over the conduct of our business and may intervene with or influence our operations

as the government deems appropriate to further regulatory, political and societal goals. The PRC government has recently published new

policies that adversely affected educational industry, especially the educational services related to K-12 students, and we cannot rule

out the possibility that it will in the future further release regulations or policies regarding educational industry that could further

adversely affect our business, financial condition and results of operations. Furthermore, the PRC government has also recently indicated

an intent to exert more oversight and control over securities offerings and other capital markets activities that are conducted overseas

and foreign investment in China-based companies like us. Any such action, once taken by the PRC government, could significantly limit

or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly

decline or in extreme cases, become worthless.

However, as there are still regulatory uncertainties in this regard, we cannot assure you that we will be able to comply with new laws and regulations in all respects in a timely manner, and we may be ordered to rectify, suspend or terminate any actions or services that are deemed illegal by the regulatory

12

authorities and become subject to material penalties, which may materially harm our and the VIEs’ business, financial condition, results of operations and prospects.

Furthermore, the PRC legal system is based in part on government policies and internal rules, some of which are not published on a timely basis or at all and may have a retroactive effect. As a result, we may not be aware of our or the VIEs’ violation of any of these policies and rules until sometime after the violation. In addition, any administrative and court proceedings in China may be protracted, resulting in substantial costs and diversion of resources and management attention.

The PRC government’s significant oversight over our and the VIEs’ business operation in China could result in a material adverse change in our and the VIEs’ operations in China and the value of our ADSs. The Chinese government may intervene or influence our and the VIEs’ operations in China at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers. Any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or become worthless.

The PRC government has significant oversight and discretion over the conduct of our and the VIEs’ business and may intervene with or influence our and the VIEs’ operations as the government deems appropriate to further regulatory, political and societal goals. The PRC government has recently published new policies that adversely affected educational industry, especially the educational services related to K-12 students, and we cannot rule out the possibility that it will in the future further release regulations or policies regarding educational industry that could further adversely affect our and the VIEs’ business, financial condition and results of operations. Furthermore, the PRC government has also recently indicated an intent to exert more oversight and control over securities offerings and other capital markets activities that are conducted overseas and foreign investment in China-based companies like us. See “Item 3. Key Information-D. Risk Factors-Risks Related to Doing Business in China-Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in policies, laws and regulations in China, could adversely affect us. The enforcement of laws and rules and regulations in China may change quickly with little advance notice, which could result in a material adverse change in our and the VIEs’ operations and the value of our ADSs.” for details. Any such action, once taken by the PRC government, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or in extreme cases, become worthless.

10. In light of recent events indicating greater oversight by the Cyberspace Administration of China (CAC) over data security, particularly for companies seeking to list on a foreign exchange, please revise your risk factor on page 15 to explain how this oversight impacts your business and to what extent you believe that you are compliant with the regulations or policies that have been issued by the CAC to date.

Response

In response to the Staff’s Comments, the Company intends to revise the risk factor on pages 15 to 16 of the 2021 Annual Report as follows. The Company will also include comparable disclosure in the 2022 Annual Report.

We are subject to a variety of laws and other obligations regarding data protection, any failure to comply with applicable laws and obligations could have a material adverse effect on our and the VIEs’ business, financial condition and results of operations.

We are subject to various regulatory requirements relating to the security and privacy of data, including restrictions on the collection, storage and use of personal information and requirements to take steps to prevent personal data from being divulged, stolen, or tampered with. See “Item 4.

13

Information on the Company-4.B.

Business Overview-Regulation-Regulations Relating to Internet Information Security and Privacy Protection.” Regulatory requirements

regarding the protection of data are constantly evolving and can be subject to differing interpretations or significant change, making

the extent of our and the VIEs’ responsibilities in that regard uncertain. For example, the Cybersecurity Cyber

Security Law of the PRC became effective in June 2017, but there are great uncertainties as to the interpretation and application

of the law. It is possible that those regulatory requirements may be interpreted and applied in a manner that is inconsistent with our

and the VIEs’ practices. In addition, the Office of the Central Cyberspace Affairs Commission, the MIIT, the Ministry of

Public Security, and the SAMR jointly issued an announcement on January 23, 2019 regarding carrying out special campaigns against mobile

internet application programs collecting and using personal information in violation of applicable laws and regulations, which prohibits

business operators from collecting personal information irrelevant to their services, or forcing users to give authorization in disguised

manner. In addition, the PRC regulatory authorities have recently taken steps to strengthen the regulation on data protection and conducted

several rounds of relevant inspections recently. We have been taking and will continue to take reasonable measures to comply with such

announcement, provisions and inspection requirements.

On June 10, 2021, the Standing

Committee of the National People’s Congress promulgated the PRC Data Security Law, effective on September 1, 2021. On August

17 July 30, 2021, the State Council promulgated the Regulations on Critical Information Infrastructure Security Protection,

which became effective on September 1, 2021. On August 20, 2021, the Standing Committee of the National People’s Congress promulgated

the PRC Personal Information Protection Law, which came into effect on November 1, 2021. On November 11, 2021, the CAC published

for public comment the Regulations on Cyber Data Security Management (Draft for Comments), or the Draft Cyber Data Security Regulations.

The Draft Cyber Data Security Regulations stipulates that the data processing operators listed overseas shall conduct an annual data security

assessment by themselves or a data security service institution, and submit the annual data security assessment report of the previous

year to the competent cybersecurity authority before January 31 of each year. As of the date of this annual report, the Draft Cyber Data

Security Regulations was not formally adopted and the final version and effective date of such regulations are subject to change with

substantial uncertainty. In addition, on January 4, 2022, the CAC announced the adoption of the Revised Cybersecurity

Review Measures, which became effective on February 15, 2022 and repealed the Cybersecurity Review Measures promulgated on April 13,

2020. Such Measures further restate and expand the applicable scope of the cybersecurity review. Pursuant to the Revised Cybersecurity

Review Measures, critical information infrastructure operators that procure internet products and services, and network platform operators

engaging in data processing activities, must be subject to the cybersecurity review if their activities affect or may affect national

security. In addition, network platform operators holding over one million users’ personal information shall apply with the Cybersecurity

Review Office for a cybersecurity review before listing abroad. On January 4, 2022, On the same date, the CAC published

the Administrative Provisions on Internet Information Service Algorithm Recommendation on its website, which became effective on March

1, 2022.

These newly promulgated

laws and regulations reflect PRC government further attempts to strengthen the legal protection for the national network security, data

security, the security of critical information infrastructure and the security of personal information protection. For details on regulations

over cybersecurity, data protection and privacy in the PRC, see See “Item 4. Information on the Company-4.B.

Business Overview-Regulation-Regulations Relating to Internet Information Security and Privacy Protection”.

We believe, to the best

of our knowledge, our and the VIEs’ business operations do not violate any of the above PRC laws and regulations currently in force

in all material aspects except for the uncertainties as disclosed in this annual report. We have been taking and will continue to take

reasonable measures to comply with such laws, regulations, announcement, provisions and inspection requirements; However,

however, as these laws, regulations, announcements and provisions are relatively new, and the related implementation rules

have yet been promulgated, it remains uncertain how these laws, regulations, announcements and provisions will be implemented.

14

We cannot assure you we can adapt our and the VIEs’ operations to it in a timely manner. Evolving interpretations of such laws, regulations, announcements and provisions or any future regulatory changes might impose additional restrictions on or obligations of us and the VIEs generating and processing personal information and other data. We and the VIEs may be subject to additional regulations, laws and policies adopted by the PRC government to apply more stringent social and ethical standards in cybersecurity and data privacy resulting from the increased global focus on this area. To the extent that we need to alter our and the VIEs’ business model or practices to adapt to these announcement and provisions and future regulations, laws and policies, we could incur additional expenses.

Any failure, or perceived

failure by us or the VIEs, or by third-party partners, to maintain the security of our students’ data and

other confidential information or to comply with applicable privacy, cybersecurity, data security and personal information protection

laws, regulations, policies, contractual provisions, industry standards, and other requirements, may result in civil or regulatory liability,

including governmental or data protection authority enforcement actions and investigations, fines, penalties, enforcement orders requiring

us or the VIEs to cease operating in a certain way, litigation, or adverse publicity, and may require us or the VIEs

to expend significant resources in responding to and defending allegations and claims. Moreover, claims or allegations that we and

the VIEs have failed to adequately protect users’ data, or otherwise violated applicable privacy, cybersecurity, data security and

personal information protection laws, regulations, policies, contractual provisions, industry standards, or other requirements, may result

in damage to our reputation and a loss of confidence in us by users or partners, potentially causing us to lose users, business partners

and revenues, which could have a material adverse effect on our and the VIEs’ business, financial condition and results of operations.

Furthermore, the PRC regulatory and enforcement regime with regard to privacy, cybersecurity, data security and personal information

protection is still evolving. PRC regulators have been increasingly focused on regulation in the areas of cybersecurity, data security

and data protection. We cannot assure you that relevant regulators will not interpret or implement these laws or regulations in ways that

negatively affect us or the VIEs. It is possible that we and the VIEs may become subject to additional or new laws, regulations,

policies and interpretations, which may result in additional expenses to us and the VIEs and subject us and the VIEs

to potential liability and negative publicity. We expect that these areas will receive greater attention and focus from regulators, and

attract continued or greater public scrutiny and attention going forward, which could increase our compliance costs and

subject us and the VIEs to heightened risks and challenges associated with data security and protection. If we and the VIEs

are unable to manage these risks, we and the VIEs could become subject to penalties, fines, suspension of business and revocation

of required licenses, and our reputation and results of operations could be materially and adversely affected.

You may experience difficulties in effecting service of legal process..., page 29

11. Please revise your risk factor to disclose how many of your directors are located in China and Hong Kong. In this regard, it appears your disclosure only references your senior executive officers. Please also address the risks associated with the difficulty of effecting service of process and collecting judgments in Hong Kong. In this regard, we note your disclosure only speaks to China, yet it appears you have operations and assets in Hong Kong, and it is unclear whether any of your directors reside in Hong Kong.

Response

In response to the Staff’s Comments, the Company intends to revise the risk factor on page 29 of the 2021 Annual Report as follows and include comparable disclosure in the 2022 Annual Report.

You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in China, including Hong Kong, against us or our management named in the annual report based on foreign laws.

15

We are an exempted

company incorporated under the laws of the Cayman Islands, we conduct substantially all of our operations in China, and We

are a Cayman Islands company and currently conduct substantially all business operations in the PRC through our subsidiaries incorporated

in the PRC and the contractual arrangements among our PRC subsidiaries and the VIEs. Substantially all of our and the VIEs’

assets are located in China. In addition, all our directors and senior executive officers reside within China for a significant

portion of the time and most are PRC nationals, while two of our directors are Hong Kong residents. We do not have any material operations

or assets in Hong Kong. As a result, It may be difficult for our shareholders to effect service of process upon us

or those persons inside China, including Hong Kong. In addition, neither China nor Hong Kong has does not

have treaties providing for the reciprocal recognition and enforcement of judgments of courts with the Cayman Islands and many

other countries and regions. Therefore, recognition and enforcement in China or Hong Kong of judgments of a court in any of these

non-PRC jurisdictions in relation to any matter not subject to a binding arbitration provision may be difficult or impossible.

Item 4. Information on the Company, page 43

12. To ensure such disclosure is included prominently in the filing, please move the discussions under the headings Recent Regulatory Development Draft Cybersecurity Measures, Potential CSRC Approval Required for the Listing of our ADSs, Contractual Arrangements and Corporate Structure, Transfer of Funds and Other Assets, Condensed Consolidating Schedule, and Restrictions on Foreign Exchange and the Ability to Transfer Cash between Entities, Across Borders and to U.S. Investors, and any subsequent revisions to such disclosure that you make in response to our comments below, to Item 3.

Response

In response to the Staff’s Comments, the Company intends to move the disclosure under the headings “Recent Regulatory Development Draft Cybersecurity Measures,” “Potential CSRC Approval Required for the Listing of our ADSs,” “Contractual Arrangements and Corporate Structure,” “Transfer of Funds and Other Assets,” “Condensed Consolidating Schedule” and “Restrictions on Foreign Exchange and the Ability to Transfer Cash between Entities, Across Borders and to U.S. Investors” on pages 45 to 52 of the 2021 Annual Report and any subsequent revisions to the above disclosure to Item 3 of the 2021 Annual Report. The Company will include comparable disclosure prominently in Item 3 in the 2022 Annual Report.

13. Where you discuss the Holding Foreign Companies Accountable Act, please expand your disclosure to also discuss the Accelerating Holding Foreign Companies Accountable Act and discuss the inspection time frames under both Acts.

Response

In response to the Staff’s Comments and to reflect the statement dated December 15, 2022 by the Public Company Accounting Oversight Board (PCAOB) that it was able, in 2022, to inspect and investigate completely issuer audit engagements of registered public accounting firms headquartered in China and Hong Kong, the Company intends to revise the risk factors on pages 35 and 36 of the 2021 Annual Report as follows and include such revised risk factor in the 2022 Annual Report.

Our ADSs will be delisted and our ADSs and shares will be prohibited from trading in the over-the-counter market under the Holding Foreign Companies Accountable Act, or the HFCAA, if the PCAOB is unable to inspect or fully investigate auditors located in China.

As part of a continued regulatory focus in the United States on access to audit and other information currently protected by national law, in particular China’s, the Holding Foreign Companies Accountable Act, or the HFCAA has been signed into law on December 18, 2020. The HFCAA states if the SEC determines that we have filed audit reports issued by a registered public accounting firm

16

that has not been subject

to inspection for the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit our ADS from being traded on a national

securities exchange or in the over-the-counter trading market in the U.S. Accordingly, under the current law this could happen in 2024.

On December 29, 2022, the Accelerating Holding Foreign Companies Accountable Act became the law, which reduced the time period before

our ADSs could be delisted from the exchange and prohibited from over-the-counter trading in the U.S. from 2024 to 2023. If

this happens, There is no certainty that we will be able to list our ADSs on a non-U.S. exchange or that a market for our shares

will develop outside of the U.S. The delisting of our ADSs, or the threat of their being delisted, may materially and adversely affect

the value of your investment.

On December 2, 2021, the SEC adopted final amendments to its rules implementing the HFCAA (the “Final Amendments”). The Final Amendments include requirements to disclose information, including the auditor name and location, the percentage of shares of the issuer owned by governmental entities, whether governmental entities in the applicable foreign jurisdiction with respect to the auditor has a controlling financial interest with respect to the issuer, the name of each official of the Chinese Communist Party who is a member of the board of the issuer, and whether the articles of incorporation of the issuer contains any charter of the Chinese Communist Party. The Final Amendments also establish procedures the SEC will follow in identifying issuers and prohibiting trading by certain issuers under the HFCAA.

On December 16, 2021, PCAOB

issued the HFCAA Determination Report, according to which our auditor is subject to the determinations that the PCAOB is unable to inspect

or investigate completely. In March 2022, the SEC issued its first “conclusive list of issuers identified under the HFCAA”

indicating that those companies are now formally subject to the delisting provisions if they remain on the list for three

two consecutive years. We anticipate being were added to the list on May 4, 2022 shortly after the

filing of this the annual report for the fiscal year ended on December 31, 2021 on Form 20-F.

On December 15, 2022, the PCAOB determined that it was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong in 2022 and vacated its previous determinations to the contrary. As a result, we do not expect to be identified as a Commission-Identified Issuer under the HFCAA for the fiscal year ended December 31, 2022 after we file our annual report on Form 20-F for such fiscal year. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control. Should the PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination. The lack of the PCAOB inspections in China will prevent the PCAOB from fully evaluating audits and quality control procedures of our auditor, as a result of which we and investors will be deprived of the benefits of such PCAOB inspections, which could cause investors to lose confidence in our audit procedures and the quality of our financial statements.

The HFCAA or other efforts

to increase U.S. regulatory access to audit information could cause investor uncertainty for affected issuers, including us, and the market

price of the ADSs could be adversely affected. Additionally, whether the PCAOB will be able to conduct inspections of our auditor

before the issuance of our financial statements on Form 20-F for the year ended December 31, 2023, which is due by April 30, 2024, or

at all, is subject to substantial uncertainty and depends on factors out of our and our auditor’s control. If our auditor

is unable to be inspected in time, we could be delisted from the New York Stock Exchange and our ADSs will not be permitted for trading

“over-the-counter” either. Such a delisting would substantially impair your ability to sell or purchase our ADSs when you

wish to do so, and the risk and uncertainty associated with delisting would have a negative impact on the price of our ADSs. Also, such

a delisting would significantly affect our ability to raise capital on terms acceptable to us, or at all, which would have a material

adverse impact on our business, financial condition and prospects.

17

Recent Regulatory Development Draft Cybersecurity Measures, page 45

14. State whether you, your subsidiaries, or the VIEs are covered by permissions requirements from the CAC. To the extent you have determined that permission is not required or applicable, discuss how you came to that conclusion, why that is the case, and the basis on which you made that determination. Tell us whether you consulted counsel in this determination, and if not, state as much and explain why such an opinion was not obtained.

Response

In response to the Staff’s Comments, the Company intends to add the following paragraph to the disclosure under “Recent Regulatory Development Draft Cybersecurity Measures” on page 46 and include such revised disclosure prominently under “Item 3. Key Information.” The Company will also include such disclosure prominently in the 2022 Annual Report.

As advised by our PRC legal counsel, Tian Yuan Law Firm, under the currently effective PRC laws and regulations, the Company, its subsidiaries and the VIEs are not covered by permissions requirements from the CAC to conduct a security offering or maintain our listing status on the NYSE, on the following grounds: (i) our PRC legal counsel has consulted the competent government authorities which acknowledged that, under the currently effective PRC laws and regulations, a company that has been listed on a foreign stock exchange before the promulgation of the Revised Cybersecurity Review Measures is not required to go through a cybersecurity review by the CAC to conduct a securities offering or to maintain its listing status on the foreign stock exchange on which its securities have been listed; (ii) as of the date hereof, none of the Company, its subsidiaries and the VIEs has been identified by any PRC governmental authority as an “ critical information infrastructure operator” that will be subject to the CAC’s cybersecurity review requirements. However, there remain uncertainties on the interpretation and implementations of the Cybersecurity Review Measures. If the CAC or other regulatory agencies later require that we obtain their approvals for our future offshore offerings, we may be unable to obtain such approvals in a timely manner, or at all, and such approvals may be rescinded even if obtained. Any such circumstance could significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Potential CSRC Approval Required for the Listing of our ADSs, page 46

15. State whether you, your subsidiaries, or the VIEs are covered by permissions requirements from the CSRC. To the extent you have determined that permission is not required or applicable, discuss how you came to that conclusion, why that is the case, and the basis on which you made that determination. Tell us whether you consulted counsel in this determination, and if not, state as much and explain why such an opinion was not obtained.

Response

In response to the Staff’s Comments, the Company intends to revise the disclosure under “Potential CSRC Approval Required for the Listing of our ADSs” on page 46 and include such revised disclosure prominently under “Item 3. Key Information.” The Company will also include such disclosure prominently in the 2022 Annual Report.

Moreover, on December 24, 2021, the CSRC issued the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) and the Administrative Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments), collectively the Draft Overseas Listing Regulations, for public comments, which require, among others, that PRC domestic companies that seek to offer and list securities in overseas markets, either in direct or indirect means, are required to file the required documents with the CSRC within three working days after its application for overseas listing is submitted. As of the date of this annual report, the Draft Overseas Listing Regulations were released for public

18

comments only and the final version and effective date of such regulations are subject to change with substantial uncertainty. As advised by our PRC legal counsel, Tian Yuan Law Firm, since the Draft Overseas Listing Regulations have not come into effect, under the currently effective PRC laws and regulations, we or the VIEs are currently not required to obtain any permission from or complete any filing with the CSRC in order for us to conduct a securities offering or maintain our listing status on the NYSE. However, our PRC legal counsel also advises that, if and when the Draft Overseas Listing Regulations become effective in the current form, we may be required to go through the filing procedures with the CSRC to conduct an overseas securities offering. Moreover, there are substantial uncertainties as to how PRC governmental authorities will regulate overseas offerings and listings in general and we cannot assure you that we will not be required to obtain the approval of the CSRC or of potentially other regulatory authorities to maintain the listing.

Transfer of Funds and Other Assets, page 46

16. Please quantify any dividends or distributions that a subsidiary or the VIEs have made to the holding company and which entity made such transfer, and their tax consequences. In addition, clarify whether your statement that “[y]our PRC subsidiaries had made cumulative capital contributions of US$200.0 million to [y]our PRC subsidiaries,” should refer to the holding company or the VIEs instead. Your disclosure should also make clear if no transfers, dividends, or distributions between the holding company, your subsidiaries, and the VIEs, other than those currently described, have been made to date. Provide cross-references to the condensed consolidating schedule and the consolidated financial statements.

Response

In response to the Staff’s Comments, the Company intends to revise the paragraphs on pages 46 to 48 of the 2021 Annual Report as follows. The Company will include such revised disclosure in the 2022 Annual Report.

Transfer of Funds and Other Assets

Under relevant PRC laws and regulations, we are permitted to remit funds to the VIEs through loans rather than capital contributions. The VIEs funded their operations primarily using cash generated from operating and financing activities. In addition, Sunlands Technology Group and the VIEs may, from time to time, lend cash to each other to settle the payment obligations on each other’s behalf to provide temporary working capital support. In 2019, 2020 and 2021, the net amounts of working capital support provided by our PRC subsidiaries to the VIEs were RMB1,110.4 million, RMB1,475.3 million and RMB12.5 million (US$2.0 million), respectively. For more information, see “Item 4. Information on the Company-4.A. History and Development of the Company-Condensed Consolidating Schedule,” and our consolidated financial statements included elsewhere in this annual report.

As of December 31, 2021,

our PRC subsidiaries Sunlands Technology Group had made cumulative capital contributions of US$200.0 million to

our PRC subsidiaries through an intermediate holding company. These funds have been used by our PRC subsidiaries for their operations.

Our PRC subsidiaries maintained certain personnel for sales and marketing, research and development, and general and administrative functions

to support the operations of the VIEs.

In 2019, 2020 and 2021, the VIEs transferred RMB1,230.2 million, RMB17.1 million and RMB62.6 million (US$9.8 million) of service fees to our PRC subsidiaries pursuant to the contractual arrangements, respectively. The outstanding balance of service fees owed by the VIEs to our PRC subsidiaries was nil as of each of December 31, 2019, 2020 and 2021. There were no other assets transferred between VIEs and non-VIEs in 2019, 2020 and 2021.

19

As advised by our PRC

legal advisor counsel, for any amounts owed by the VIEs to our PRC subsidiaries under the VIE agreements, unless

otherwise required by PRC tax authorities, we are able to settle such amounts without limitations under the current effective PRC laws

and regulations, provided that the VIEs have sufficient funds to do so and that the VIEs, in case in the form of non-enterprise institution,

follow the principles of openness, fairness and impartiality, fix the price reasonably and regulate the decision-making, and do not damage

the state interests, the interests of the non-enterprise institution or the rights and interests of the teachers and students when conducting

such related party transaction. Our subsidiaries are permitted to pay dividends to their shareholders, and eventually to Sunlands Technology

Group, only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Such payment

of dividends by entities registered in China is subject to limitations, which could result in limitations on the availability of cash

to fund dividends or make distributions to shareholders of our securities. For example, our PRC subsidiaries and the VIEs are required

to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable

as cash dividends except in the event of a solvent liquidation of the companies. For more details, see “Item 3. Key Information-D.

Risk Factors-Risks Related to Doing Business in China-We may rely on dividends and other distributions on equity paid by our PRC subsidiaries

to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiaries to make payments to

us could have a material and adverse effect on our ability to conduct our business.” Sunlands Technology Group has not

previously declared or paid any a special cash dividend of US$1.36 per ordinary share (or US$0.68 per ADS)

to holders of its ordinary shares and ADSs on June 14, 2022, and is in the process of the distribution of such dividend. or

dividend in kind, and has Except for that, we have no plan to declare or pay any dividends in the near future on our shares

or the ADSs representing our ordinary shares. As of the date of this annual report, no transfers, dividends, or distributions between

Sunlands Technology Group, our PRC subsidiaries, and the VIEs, other than those currently described, have been made. We currently

intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business. As of the date

of this annual report, we do not have cash management policies in place that dictate how funds are transferred between Sunlands Technology

Group, our subsidiaries, the VIEs and the investors. Rather, the funds can be transferred in accordance with the applicable laws and regulations

discussed in this section. See “Item 8.-Financial Information-8.A. Consolidated Statements and Other Financial Information-Dividend

Policy.”