UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31 , 2021

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number: 001-38429

(Exact Name of Registrant as Specified in Its Charter)

N/A

(Translation of Registrant’s Name Into English)

(Jurisdiction of Incorporation or Organization)

(Address of Principal Executive Offices)

Phone: +86 21 25099255

Email: sam@bilibili.com

(Name, Telephone,

E-mail

and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class |

Trading Symbol(s) |

Name of Each Exchange On Which Registered | ||

9626 |

The Stock Exchange of Hong Kong Limited |

Securities registered or to be registered pursuant to Section 12(g) of the act: None

Securities for which there is a reporting obligation pursuant to section 15(d) of the act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2021, there were 390,604,587 ordinary shares outstanding, par value $0.0001 per share, being the sum of 83,715,114 Class Y ordinary shares and 306,889,473 Class Z ordinary shares (excluding 2,767,265 Class Z ordinary shares issued and reserved for future issuance upon the exercising or vesting of awards granted under our share incentive plans).

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation Yes ☐ No

S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2

of the Exchange Act. Accelerated filer ☐ |

Non-accelerated filer ☐ |

Emerging growth company |

If an emerging growth company that prepare its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† |

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued |

Other ☐ | |||||||

by the International Accounting Standards Board ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule ☒ No

12b-2

of the Exchange Act). ☐ Yes (APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

i

INTRODUCTION

Unless otherwise indicated and except where the context otherwise requires, all discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed herein are due to rounding, and references in this annual report on Form

20-F

to: | • | “ADRs” are to the American depositary receipts that evidence the ADSs; |

| • | “ADSs” are to the American depositary shares, each of which represents one Class Z ordinary share; |

| • | “average monthly interactions” for a period is calculated by dividing the total number of interactions based on our interactions features such as bullet chats, commentaries, following, favorites, sharing, bilibili moment posts, likes, messaging, coin casting and virtual gifting etc., among other things, during the specified period by the number of months in such period; |

| • | “average monthly revenue per paying user” for a period is calculated by dividing the sum of revenues from mobile games and VAS during the specified period by the total number of monthly paying users during such period; |

| • | “average monthly revenue per MAU” for a period is calculated dividing the sum of revenues during the specified period by the total number of MAU during that period then further by the number of months in the specified period; |

| • | “average daily time spent per active user on our mobile apps” for a period is calculated by dividing the total time spent on our mobile apps (including smart TV and other smart devices) during the specified period (excluding time spent on Bilibili operating games, Bilibili Comic and Maoer) by the average number of active users per day during such period, further divided by the number of days during the specified period; |

| • | “Bilibili” are to Bilibili Inc., and “we,” “us,” “our company” and “our” are to Bilibili Inc. and its subsidiaries, and, in the context of describing our operations and consolidated financial information, its variable interest entities, or VIEs, in China and their subsidiaries (which are collectively referred to as consolidated affiliated entities in China), including but not limited to Shanghai Hode Information Technology Co., Ltd., or Hode Information Technology, and Shanghai Kuanyu Digital Technology Co., Ltd., or Shanghai Kuanyu, and their subsidiaries; |

| • | “bullet chat” or “bullet chatting” are to a commenting function that enables content viewers to send comments that fly across the screen like bullets, which we refer to as bullet chats herein. Bullet chats are context-based and can be viewed by the audiences who watch the same content, and therefore can intrigue interactive commenting among content viewers. Only official member can send bullet chats on our platform; |

| • | “China” or the “PRC” are to the People’s Republic of China, excluding, for the purposes of this annual report only, Hong Kong, Macau and Taiwan; |

| • | “Class Y ordinary shares” are to our Class Y ordinary shares, par value US$0.0001 per share; |

| • | “Class Z ordinary shares” are to our Class Z ordinary shares, par value US$0.0001 per share; |

| • | “CSRC” are to the China Securities Regulatory Commission; |

| • | “Generation Z+”, “Gen Z+” or “younger generations” are to, for the purposes of this annual report only, the demographic cohort of individuals in China born from 1985 to 2009; |

| • | “HK$” or “Hong Kong dollars” or “HK dollars” are to Hong Kong dollars, the lawful currency of Hong Kong; |

1

| • | “Hong Kong” or “HK” or “Hong Kong S.A.R.” are to the Hong Kong Special Administrative Region of the PRC; |

| • | “Hong Kong Listing Rules” are to the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited, as amended or supplemented from time to time; |

| • | “Hong Kong Stock Exchange” are to The Stock Exchange of Hong Kong Limited; |

| • | “Main Board” are to the stock market (excluding the option market) operated by the Hong Kong Stock Exchange which is independent from and operated in parallel with the Growth Enterprise Market of the Hong Kong Stock Exchange; |

| • | “monthly active users” or “MAU” are to the sum of our mobile apps MAU and PC MAU after eliminating duplicates so that each active registered user that logged on both our Bilibili mobile app and our Bilibili PC website would only be counted towards mobile apps MAU and not PC MAU during a given month. We calculate mobile apps MAU based on the number of mobile devices (including smart TV and other smart devices) that launched our mobile apps during a given month. We count mobile MAU of Bilibili Comic, a mobile app offering anime and comic content, and Maoer, an audio platform offering audio drama, towards our MAU. We calculate PC MAU by dividing the total number of IP addresses used by users to visit our PC website during a given month by an estimate of the average number of IP addresses used by each user. “Average MAU” for a period is calculated by dividing the sum of MAU during the specified period by the number of months in such period; |

| • | “official members” are to users who pass our multiple-choice membership exam consisting of 100 questions, after which additional interactive and community features, such as bullet chatting and commenting, will become available to them; |

| • | “our platform” are to “Bilibili” mobile apps, PC websites, Smart TV, Bilibili Comic, Maoer and a variety of related features, functionalities, tools and services that we provide to users and content creators; |

| • | “occupationally generated videos” or “OGV” are to Bilibili-produced or jointly produced content and licensed content procured from third-party production companies; |

| • | “paying users” on our platform are to users who make payments for various products and services on our platform, including purchases in mobile games offered on our platform and payments for VAS (excluding purchases on our e-commerce platform). A user who makes payments across different products and services offered on our platform using the same registered account is counted as one paying user and we add the number of paying users of Maoer towards our total paying users without eliminating duplicates. “Average monthly paying user” for a period is calculated by dividing the sum of monthly paying users during the specified period by the number of months in such period; |

| • | “professional user generated videos” or “PUGV” are to videos generated by users that exhibits creativity as well as a certain level of professional production and editing capabilities; |

| • | “retention rate”, as applied to any cohort of users who visit our platform in a given period, are to the percentage of these users who make at least one repeat visit after a certain duration; the “12th-month retention rate” for any cohort of users in a given month is the retention rate in the twelfth month after the applicable month; |

| • | “premium members” are to members who have subscribed to our premium membership, which allows these members to enjoy exclusive or advance access to our premium content. We calculate premium members based on the number of members whose premium package is still valid by the last day of a given month; |

| • | “RMB” and “Renminbi” are to the legal currency of China; |

2

| • | “shares” or “ordinary shares” are to our Class Y and Class Z ordinary shares, par value US$0.0001 per share; |

| • | “US$,” “U.S. dollars,” “$,” and “dollars” are to the legal currency of the United States; |

| • | “VAS” are to value-added services, including premium membership, live broadcasting, Bilibili Comic, Maoer and other value-added services; |

| • | “video-based content” are to, for the purposes of this annual report only, video content on video-centric platforms and non-video-centric platforms as well as mobile games. Non-video-centric platforms include social media, instant messaging, e-commerce, browser, and other kind of platforms; and |

| • | “videolization” are to the trend of video integrating into the scenarios of everyday life, |

Our reporting currency is the Renminbi because our business is mainly conducted in China and a substantial majority of our revenues is denominated in Renminbi. This annual report contains translations of Renminbi amounts into U.S. dollars at specific rates solely for the convenience of the reader. The conversion of Renminbi into U.S. dollars in this annual report is based on the exchange rate set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report were made at a rate of RMB6.3726 to US$1.00, the exchange rate on December 30, 2021 set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade.

3

FORWARD-LOOKING STATEMENTS

This annual report on Form

20-F

contains forward-looking statements that reflect our current expectations and views of future events. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigations Reform Act of 1995. You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to,” “potential,” “continue” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include statements relating to:

| • | our goals and strategies; |

| • | our future business development, financial conditions and results of operations; |

| • | the expected growth of the online entertainment and mobile games industries in China; |

| • | our expectations regarding demand for and market acceptance of our products and services; |

| • | our expectations regarding our relationships with users, content providers, game developers and publishers, advertisers and other partners; |

| • | competition in our industry; |

| • | relevant government policies and regulations relating to our industry; |

| • | the outcome of any current and future litigation or legal or administrative proceedings; and |

| • | other factors described under “Item 3. Key Information—D. Risk Factors.” |

You should read this annual report and the documents that we refer to in this annual report and have filed as exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect. Other sections of this annual report discuss factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements.

You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

4

PART I.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

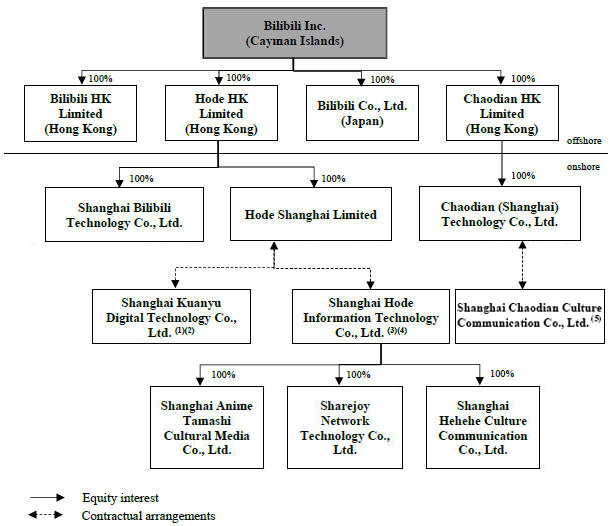

Our Holding Company Structure and Contractual Arrangements with the VIEs

Bilibili Inc. is not a Chinese operating company but a Cayman Islands holding company with no equity ownership in its VIEs. We conduct our operations primarily through our PRC subsidiaries, the VIEs and their subsidiaries in China. PRC laws and regulations prohibit foreign investment in internet cultural business (except for music), the internet audio-visual program business, the radio and television program production and operation business, and the production of audio-visual products and/or electronic publications. Accordingly, we operate these businesses in China through the VIEs, and rely on contractual arrangements among our PRC subsidiaries, the VIEs and their shareholders, as applicable, to control the business operations of the VIEs. Revenues contributed by the VIEs accounted for 97.2%, 86.0% and 74.5% of our total revenues for the years of 2019, 2020 and 2021, respectively. As used in this annual report, “we,” “us,” “our company” and “our” refers to Bilibili Inc., its subsidiaries, and, in the context of describing our operations and consolidated financial information, the VIEs and their subsidiaries in China (collectively referred to as consolidated affiliated entities), including but not limited to, Hode Information Technology, which was established in May 2013 to expand our operations; and Shanghai Kuanyu, whose control was obtained by us in July 2014 to further expand our operations, and their subsidiaries.

The following chart illustrates our company’s organizational structure, including our principal subsidiaries and consolidated affiliated entities as of the date of this annual report:

5

Notes:

| (1) | Mr. Rui Chen holds 100% equity interests in Shanghai Kuanyu. He is also the chairman of our board of directors and our chief executive officer. |

| (2) | Shanghai Kuanyu has four subsidiaries. |

| (3) | Mr. Rui Chen, Mr. Yi Xu and Ms. Ni Li hold 52.3%, 44.3%, and 3.4% equity interests in Hode Information Technology, respectively, as of the date of this annual report. Mr. Chen is our controlling shareholder, the chairman of our board of directors and our chief executive officer. Mr. Xu is our founder, director and president. Ms. Li is the vice chairwoman of our board of directors and chief operating officer. |

| (4) | Hode Information Technology has 35 subsidiaries. |

| (5) | Chaodian (Shanghai) Technology Co., Ltd., or “Chaodian Technology”, has entered into a series of contractual arrangements with Shanghai Chaodian Culture Communication Co., Ltd., or “Chaodian Culture”, and its individual shareholders, through which we obtained control over the operations of, and enjoyed all economic benefits of Chaodian Culture. Mr. Rui Chen, Mr. Yi Xu, Ms. Ni Li, Mr. Xujun Chai, Shanghai Kuanyu and Hode Information Technology hold 31.2%, 9.5%, 6.8%, 5.1%, 44.6% and 2.8% equity interests in Chaodian Culture, respectively, as of the date of this annual report. Mr. Xujun Chai is an employee of our company. |

Holders of our Class Z ordinary shares or the ADSs hold equity interest in Bilibili Inc., our Cayman Islands holding company, and do not have direct or indirect equity interests in the VIEs and their subsidiaries.A series of contractual agreements, including powers of attorney, equity pledge agreements, letter of undertakings, exclusive business cooperation agreements, and exclusive option agreements, have been entered into by and among our subsidiaries, the VIEs and their respective shareholders, as applicable. Terms contained in each set of contractual arrangements with the VIEs and their respective shareholders are substantially similar. As a result of the contractual arrangements, we have effective control over and are considered the primary beneficiary of these companies, and we have consolidated the financial results of these companies in our consolidated financial statements. For more details of these contractual arrangements, see “Item 4. Information on the Company—C. Organizational Structure—Agreements that provide us effective control over the relevant VIEs.”

6

However, the contractual arrangements may not be as effective as direct ownership in providing us with control over the VIEs and we may incur substantial costs to enforce the terms of the arrangements. In addition, these agreements have not been tested in PRC courts. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We rely on contractual arrangements with the VIEs and their shareholders for our operations in China, which may not be as effective in providing operational control as direct ownership” and “—The shareholders of the VIEs may have potential conflicts of interest with us, which may materially and adversely affect our business.”

There are also substantial uncertainties regarding the interpretation and application of current and future PRC laws, regulations and rules regarding the status of the rights of Bilibili, a Cayman Islands holding company, with respect to its contractual arrangements with the VIEs and their individual shareholders. It is uncertain whether any new PRC laws or regulations relating to VIE structures will be adopted or if adopted, what they would provide. If we or any of the existing or past VIEs is found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the PRC government finds that the agreements that establish the structure for operating our businesses in China do not comply with PRC regulations on foreign investment in internet and other related businesses, or if these regulations or their interpretation change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations” and “—Substantial uncertainties exist with respect to how the Foreign Investment Law may impact the viability of our current corporate structure and operations.”

Our corporate structure is subject to risks associated with our contractual arrangements with the VIEs. If the PRC government deems that our contractual arrangements with the VIEs do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change or are interpreted differently in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. Bilibili, its PRC subsidiaries and VIEs, and investors of Bilibili face uncertainty about potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIEs and, consequently, significantly affect the financial performance of the VIEs and our company as a whole. For a detailed description of the risks associated with our corporate structure, please refer to risks disclosed under “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.”

PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations, including data security or anti-monopoly related regulations, in this nature may cause the value of such securities to significantly decline or be of little or no value. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PRC government’s significant oversight over our business operation could result in a material adverse change in our operations and the value of our Class Z ordinary shares and the ADSs.”

Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our securities. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us.”

Permissions Required from the PRC Authorities for Our Operations

We conduct our business primarily through our subsidiaries and VIEs in China. Our operations in China are governed by PRC laws and regulations. As of the date of this annual report, our PRC subsidiaries and VIEs have obtained the requisite licenses and permits from the PRC government authorities that are material for the business operations of Bilibili, its PRC subsidiaries and VIEs in China, including, among others, Value-added Telecommunication Business Licenses, License for Online Transmission of Audio-Visual Programs, Online Culture Operating Permits and License for Production and Operation of Radio and Television Program. Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we may be required to obtain additional licenses, permits, filings or approvals for the functions and services of our platform in the future. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Business and Industry—We face uncertainties with respect to the enactment, interpretation and implementation of Notice 78 and Notice 3.” and “—If we fail to obtain and maintain the licenses and approvals required within the complex regulatory environment applicable to our businesses in China, or if we are required to take compliance actions that are time-consuming or costly, our business, financial condition and results of operations may be materially and adversely affected.”

7

Furthermore, the PRC government has recently indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. On December 24, 2021, the CSRC issued a draft of the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies, and a draft of Administration Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies, for public comments, according to which, the issuer or its affiliated major domestic operating company, as the case may be, shall file with the CSRC and report the relevant information for its

follow-on

offshore offering and other equivalent offshore offering activities. As of the date of this annual report, the aforementioned draft provisions have not been adopted and there still exists substantial uncertainties surrounding the CSRC requirements at this stage. The approval of, or report and filing with the CSRC, or other governmental authorities may be required in connection with our future offshore offerings, and, if required, we cannot predict if we will be able to obtain such approval or complete such report and filing process.For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The approval of, or report and fillings with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under PRC law, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing and report process.”

The Holding Foreign Companies Accountable Act

The Holding Foreign Companies Accountable Act, or the HFCAA, was enacted on December 18, 2020. The HFCAA states if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the Public Company Accounting Oversight Board (United States), or the PCAOB, for three consecutive years beginning in 2021, the SEC shall prohibit our shares or ADSs from being traded on a national securities exchange. Since our auditor is located in China, a jurisdiction where the PCAOB has been unable to conduct inspections without the approval of the Chinese authorities, our auditor is not currently inspected by the PCAOB, which may impact our ability to remain listed on a United States exchange. The related risks and uncertainties could cause the value of the ADSs to significantly decline. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PCAOB is currently unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections over our auditor deprives our investors with the benefits of such inspections” and “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The ADSs will be prohibited from trading in the United States under the Holding Foreign Companies Accountable Act, or the HFCAA, in 2024 if the PCAOB is unable to inspect or fully investigate auditors located in China, or in 2023 if proposed changes to the law are enacted. The delisting of the ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment.”

Cash and Asset Flows through Our Organization

Bilibili Inc. transfers cash to its wholly-owned Hong Kong subsidiaries, by making capital contributions or providing loans, and the Hong Kong subsidiaries transfer cash to the subsidiaries in China by making capital contributions or providing loans to them. Because Bilibili Inc. and its subsidiaries control the VIEs through contractual arrangements, they are not able to make direct capital contribution to the VIEs and their subsidiaries. However, they may transfer cash to the VIEs by loans or by making payments to the VIEs for inter-group transactions.

Prior to December 31, 2019, Bilibili Inc., through its intermediate holding companies, had provided capital contribution and loans of aggregately RMB4.1billion to its subsidiaries in China. For the years ended December 31, 2020 and 2021, Bilibili Inc., through its intermediate holding companies, had provided capital contribution and loans of aggregately RMB5.3 billion and RMB7.6 billion (US$1,201.5 million) to its subsidiaries in China. For the years ended December 31, 2019, 2020 and 2021, the VIEs received financings of RMB1.3 billion, RMB990.3 million and RMB3.3 billion (US$519.0 million) from WFOEs, respectively.

8

The VIEs may transfer cash to our WFOEs by paying consulting and services charges according to the exclusive business cooperation agreement, and the VIEs may receive cash from our WFOEs under business agreements. For the years ended December 31, 2019 and 2020, the VIEs paid of aggregately RMB 551.8 million and 488.9 million to WFOEs. For the years ended December 31, 2021, the VIEs received of aggregately RMB 1.0 billion from WFOEs.

For the years ended December 31, 2019, 2020 and 2021, no dividends or distributions were made to Bilibili Inc. by our subsidiaries. Under PRC laws and regulations, our PRC subsidiaries and VIEs are subject to certain restrictions with respect to paying dividends or otherwise transferring any of their net assets to us. Remittance of dividends by a wholly foreign-owned enterprise out of China is also subject to examination by the banks designated by SAFE. The amounts restricted include the

paid-up

capital and the statutory reserve funds of our PRC subsidiaries and VIEs, in a total of RMB1.8 billion, RMB1.2 billion and RMB3.8 billion (US$598.2 million) as of December 31, 2019, 2020 and 2021, respectively. Furthermore, cash transfers from our PRC subsidiaries to entities outside of China are subject to PRC government control of currency conversion. Shortages in the availability of foreign currency may temporarily delay the ability of our PRC subsidiaries and VIEs to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. For risks relating to the fund flows of our operations in China, see “Item 3. Key Information—Risk Factors—Risks Relating to Doing Business in China—We may rely on dividends paid by our PRC subsidiaries to fund cash and financing requirements. Any limitation on the ability of our PRC subsidiaries to pay dividends to us could have a material adverse effect on our ability to conduct our business and to pay dividends to our shareholders and ADS holders.” In the years ended December 31, 2019, 2020 and 2021, no assets other than cash were transferred through our organization.

Bilibili Inc. has not declared or paid any cash dividends, nor does it have any present plan to pay any cash dividends on its ordinary shares in the foreseeable future. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business. See “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information—Dividend Policy.” For the Cayman Islands, PRC and U.S. federal income tax considerations applicable to an investment in our Class Z ordinary shares or the ADSs, see “Item 10. Additional Information—E. Taxation.” For purposes of illustration, the following discussion reflects the hypothetical taxes that might be required to be paid within China and Hong Kong, assuming that: (i) we have taxable earnings, and (ii) we determine to pay a dividend in the future:

Taxation Calculation (1) |

||||

| Hypothetical pre-tax earnings(2) |

100.0 | % | ||

| Tax on earnings at statutory rate of 25% (3) |

(25.0 | )% | ||

| Net earnings available for distribution |

75.0 | % | ||

| Withholding tax at standard rate of 10% (4) |

(7.5 | )% | ||

| Net distribution to Parent/Shareholders |

67.5 | % | ||

Notes:

| (1) | For purposes of this example, the tax calculation has been simplified. The hypothetical book pre-tax earnings amount, not considering timing differences, is assumed to equal Chinese taxable income. |

| (2) | Under the terms of VIE agreements, our PRC subsidiaries may charge the VIEs for services provided to VIEs. These fees shall be recognized as expenses of the VIEs, with a corresponding amount as service income by our PRC subsidiaries and eliminate in consolidation. For income tax purposes, our PRC subsidiaries and VIEs file income tax returns on a separate company basis. The fees paid are recognized as a tax deduction by the VIEs and as income by our PRC subsidiaries and are tax neutral. |

| (3) | Certain of our subsidiaries and VIEs qualifies for a 15% preferential income tax rate in China. However, such rate is subject to qualification, temporary in nature, and may not be available in a future period when distributions are paid. For purposes of this hypothetical example, the table above reflects a maximum tax scenario under which the full statutory rate would be effective. |

| (4) | PRC Enterprise Income Tax Law imposes a withholding income tax of 10% on dividends distributed by a Foreign Invested Enterprises (“FIE”) to its immediate holding company outside of China. A lower withholding income tax rate of 5% is applied if the FIE’s immediate holding company is registered in Hong Kong or other jurisdictions that have a tax treaty arrangement with China, subject to specific qualification requirements at the time of the distribution. For purposes of this hypothetical example, the table above assumes a maximum tax scenario under which the full withholding tax would be applied even though we have Hong Kong subsidiaries and would likely make any dividends through them. |

9

The table above has been prepared under the assumption that all profits of the VIEs will be distributed as fees to our PRC subsidiaries under tax neutral contractual arrangements. If in the future, the accumulated earnings of the VIEs exceed the fees paid to our PRC subsidiaries (or if the current and contemplated fee structure between the intercompany entities is determined to be

non-substantive

and disallowed by Chinese tax authorities), the VIEs could, as a matter of last resort, make a non-deductible

transfer to our PRC subsidiaries for the amounts of the stranded cash in the VIEs. This would result in such transfer being non-deductible

expenses for the VIEs but still taxable income for the PRC subsidiaries. Such a transfer and the related tax burdens would reduce our after-tax

income to approximately 50.6% of the pre-tax

income. Our management believes that there is only a remote possibility that this scenario would happen. Financial Information Related to Our Consolidated Affiliated Entities

The following table presents the condensed consolidating schedule of financial information of Bilibili Inc., its wholly owned subsidiaries that are the primary beneficiaries of the VIEs, and our other subsidiaries, the VIEs and the VIEs’ subsidiaries as of the dates presented.

Selected Condensed Consolidated Statements of Operations and Comprehensive Loss Data

For the Year Ended December 31, 2021 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Third-party revenues |

— | 258,686 | 6,257,462 | 12,867,536 | — | 19,383,684 | ||||||||||||||||||

| Inter-company consulting and services revenues (1) |

— | 590,905 | 2,367 | — | (593,272 | ) | — | |||||||||||||||||

| Other inter-company revenues (2) |

— | 2,054,227 | 403,379 | 1,574,896 | (4,032,502 | ) | — | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenues |

— |

2,903,818 |

6,663,208 |

14,442,432 |

(4,625,774 |

) |

19,383,684 |

|||||||||||||||||

| Third-party costs and expenses |

(12,405 | ) | (5,448,830 | ) | (4,068,228 | ) | (16,283,295 | ) | — | (25,812,758 | ) | |||||||||||||

| Inter-company consulting and services costs and expenses (1) |

— | — | — | (593,272 | ) | 593,272 | — | |||||||||||||||||

| Other inter-company costs and expenses (2) |

— | (515,329 | ) | (3,246,077 | ) | (271,096 | ) | 4,032,502 | — | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total costs and expenses |

(12,405 |

) |

(5,964,159 |

) |

(7,314,305 |

) |

(17,147,663 |

) |

4,625,774 |

(25,812,758 |

) | |||||||||||||

| Loss from subsidiaries and VIEs (3) |

(6,713,764 | ) | (3,518,404 | ) | (2,897,007 | ) | — | 13,129,175 | — | |||||||||||||||

| (Loss)/Gain from non-operations |

(63,059 | ) | (110,321 | ) | 52,150 | (163,146 | ) | — | (284,376 | ) | ||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Loss before income tax expenses |

(6,789,228 |

) |

(6,689,066 |

) |

(3,495,954 |

) |

(2,868,377 |

) |

13,129,175 |

(6,713,450 |

) | |||||||||||||

| Income tax expenses |

— | (33,842 | ) | (22,450 | ) | (38,997 | ) | — | (95,289 | ) | ||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net loss |

(6,789,228 |

) |

(6,722,908 |

) |

(3,518,404 |

) |

(2,907,374 |

) |

13,129,175 |

(6,808,739 |

) | |||||||||||||

| Net loss attributable to noncontrolling interests |

— | 9,144 | — | 10,367 | — | 19,511 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net loss attributable to Bilibili Inc.’s shareholders |

(6,789,228 |

) |

(6,713,764 |

) |

(3,518,404 |

) |

(2,897,007 |

) |

13,129,175 |

(6,789,228 |

) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

For the Year Ended December 31, 2020 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Third-party revenues |

— | 92,898 | 2,254,871 | 9,651,207 | — | 11,998,976 | ||||||||||||||||||

| Inter-company consulting and services revenues (1) |

— | 1,007,741 | 13,855 | — | (1,021,596 | ) | — | |||||||||||||||||

| Other inter-company revenues (2) |

— | 1,059,370 | 166,860 | 667,765 | (1,893,995 | ) | — | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenues |

— | 2,160,009 |

2,435,586 |

10,318,972 |

(2,915,591 |

) |

11,998,976 |

|||||||||||||||||

| Third-party costs and expenses |

(44,090 | ) | (3,318,462 | ) | (1,846,340 | ) | (9,931,047 | ) | — | (15,139,939 | ) | |||||||||||||

| Inter-company consulting and services costs and expenses (1) |

— | — | — | (1,021,596 | ) | 1,021,596 | — | |||||||||||||||||

| Other inter-company costs and expenses (2) |

— | (256,902 | ) | (1,435,506 | ) | (201,587 | ) | 1,893,995 | — | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total costs and expenses |

(44,090 |

) |

(3,575,364 |

) |

(3,281,846 |

) |

(11,154,230 |

) |

2,915,591 |

(15,139,939 |

) | |||||||||||||

| Loss from subsidiaries and VIEs (3) |

(2,940,906 | ) | (1,632,936 | ) | (845,469 | ) | — | 5,419,311 | — | |||||||||||||||

| (Loss)/Gain from non-operations |

(26,708 | ) | 79,138 | 79,517 | 8,368 | — | 140,315 | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Loss before income tax expenses |

(3,011,704 |

) |

(2,969,153 |

) |

(1,612,212 |

) |

(826,890 |

) |

5,419,311 |

(3,000,648 |

) | |||||||||||||

| Income tax expenses |

— | (5,565 | ) | (20,724 | ) | (27,080 | ) | — | (53,369 | ) | ||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net loss |

(3,011,704 |

) |

(2,974,718 |

) |

(1,632,936 |

) |

(853,970 |

) |

5,419,311 |

(3,054,017 |

) | |||||||||||||

| Net loss attributable to noncontrolling interests |

— | 38,104 | — | 8,501 | — | 46,605 | ||||||||||||||||||

| Accretion to redeemable noncontrolling Interests |

— | (4,292 | ) | — | — | — | (4,292 | ) | ||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net loss attributable to Bilibili Inc.’s shareholders |

(3,011,704 |

) |

(2,940,906 |

) |

(1,632,936 |

) |

(845,469 |

) |

5,419,311 |

(3,011,704 |

) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

10

For the Year Ended December 31, 2019 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Third-party revenues |

— | 5,010 | 716,580 | 6,056,332 | — | 6,777,922 | ||||||||||||||||||

| Inter-company consulting and services revenues (1) |

— | 1,266,411 | — | — | (1,266,411 | ) | — | |||||||||||||||||

| Other inter-company revenues (2) |

— | 301,674 | 88,174 | 531,830 | (921,678 | ) | — | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenues |

— |

1,573,095 |

804,754 |

6,588,162 |

(2,188,089 |

) |

6,777,922 |

|||||||||||||||||

| Third-party costs and expenses |

(14,762 | ) | (1,774,197 | ) | (688,312 | ) | (5,795,826 | ) | — | (8,273,097 | ) | |||||||||||||

| Inter-company consulting and services costs and expenses (1) |

— | — | — | (1,266,411 | ) | 1,266,411 | — | |||||||||||||||||

| Other inter-company costs and expenses (2) |

— | (320,724 | ) | (525,402 | ) | (75,552 | ) | 921,678 | — | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total costs and expenses |

(14,762 |

) |

(2,094,921 |

) |

(1,213,714 |

) |

(7,137,789 |

) |

2,188,089 |

(8,273,097 |

) | |||||||||||||

| Loss from subsidiaries and VIEs (3) |

(1,311,565 | ) | (859,014 | ) | (446,178 | ) | — | 2,616,757 | — | |||||||||||||||

| Gain/(Loss) from non-operations |

37,354 | 71,878 | (3,876 | ) | 122,116 | — | 227,472 | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Loss before income tax expenses |

(1,288,973 |

) |

(1,308,962 |

) |

(859,014 |

) |

(427,511 |

) |

2,616,757 |

(1,267,703 |

) | |||||||||||||

| Income tax expenses |

— | (15,264 | ) | — | (20,603 | ) | — | (35,867 | ) | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net loss |

(1,288,973 |

) |

(1,324,226 |

) |

(859,014 |

) |

(448,114 |

) |

2,616,757 |

(1,303,570 |

) | |||||||||||||

| Net loss attributable to noncontrolling interests |

— | 12,661 | — | 1,936 | — | 14,597 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net loss attributable to Bilibili Inc.’s shareholders |

(1,288,973 |

) |

(1,311,565 |

) |

(859,014 |

) |

(446,178 |

) |

2,616,757 |

(1,288,973 |

) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Selected Condensed Consolidated Balance Sheets Data

As of December 31, 2021 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Cash and cash equivalents |

1,748,896 | 4,956,403 | 440,695 | 377,114 | — | 7,523,108 | ||||||||||||||||||

| Time deposits |

7,625,337 | — | — | 6,997 | — | 7,632,334 | ||||||||||||||||||

| Accounts receivable, net |

— | 79,350 | 778,667 | 524,311 | — | 1,382,328 | ||||||||||||||||||

| Amounts due from Group companies (4) |

23,306,176 | 9,329,586 | 8,680,893 | 391,951 | (41,708,606 | ) | — | |||||||||||||||||

| Amount due from related parties |

— | 1,937,592 | 1,741 | 101,983 | — | 2,041,316 | ||||||||||||||||||

| Prepayments and other current assets |

11,773 | 280,689 | 708,401 | 1,806,185 | — | 2,807,048 | ||||||||||||||||||

| Short-term investments |

13,107,720 | 767,935 | 257,943 | 927,124 | — | 15,060,722 | ||||||||||||||||||

| Long-term investments, net |

1,448,100 | 2,038,157 | 270,801 | 1,745,466 | — | 5,502,524 | ||||||||||||||||||

| Other non-current assets |

— | 3,711,745 | 1,465,037 | 4,926,989 | — | 10,103,771 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total assets |

47,248,002 |

23,101,457 |

12,604,178 |

10,808,120 |

(41,708,606 |

) |

52,053,151 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Accounts payable |

— | 244,808 | 951,797 | 3,164,301 | — | 4,360,906 | ||||||||||||||||||

| Salary and welfare payables |

— | 641,560 | 10,883 | 343,008 | — | 995,451 | ||||||||||||||||||

| Taxes payable |

— | 55,575 | 19,378 | 128,817 | — | 203,770 | ||||||||||||||||||

| Short-term loans |

— | 688,448 | 143,658 | 400,000 | — | 1,232,106 | ||||||||||||||||||

| Deferred revenue |

40,167 | 962 | 411,800 | 2,192,460 | — | 2,645,389 | ||||||||||||||||||

| Accrued liabilities and other payables |

126,512 | 807,547 | 298,373 | 1,184,523 | — | 2,416,955 | ||||||||||||||||||

| Amounts due to Group companies (4) |

— | 24,009,991 | 10,484,469 | 7,214,146 | (41,708,606 | ) | — | |||||||||||||||||

| Amounts due to related parties |

— | 98,207 | 326 | 117,901 | — | 216,434 | ||||||||||||||||||

| Other long-term payable |

17,784,092 | 259,161 | 102 | 222,719 | — | 18,266,074 | ||||||||||||||||||

| Deficit in subsidiaries and VIEs (3) |

7,593,564 | 3,887,067 | 4,170,459 | — | (15,651,090 | ) | — | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total liabilities |

25,544,335 |

30,693,326 |

16,491,245 |

14,967,875 |

(57,359,696 |

) |

30,337,085 |

|||||||||||||||||

| Total Bilibili Inc’s Shareholders’ equity/(deficit) (3) |

21,703,667 | (7,593,564 | ) | (3,887,067 | ) | (4,170,459 | ) | 15,651,090 | 21,703,667 | |||||||||||||||

| Noncontrolling interests |

— | 1,695 | — | 10,704 | — | 12,399 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total shareholders’ equity/(deficit) |

21,703,667 |

(7,591,869 |

) |

(3,887,067 |

) |

(4,159,755 |

) |

15,651,090 |

21,716,066 |

|||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total liabilities and shareholders’ equity/(deficit) |

47,248,002 |

23,101,457 |

12,604,178 |

10,808,120 |

(41,708,606 |

) |

52,053,151 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

11

As of December 31, 2020 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Cash and cash equivalents |

159,040 | 3,574,397 | 595,482 | 349,190 | — | 4,678,109 | ||||||||||||||||||

| Time deposits |

4,697,928 | — | — | 22,161 | — | 4,720,089 | ||||||||||||||||||

| Accounts receivable, net |

— | 28,123 | 682,419 | 343,099 | — | 1,053,641 | ||||||||||||||||||

| Amounts due from Group companies (4) |

12,559,285 | 5,889,341 | 3,640,606 | 173,596 | (22,262,828 | ) | — | |||||||||||||||||

| Amount due from related parties |

— | 105,602 | 13 | 59,117 | — | 164,732 | ||||||||||||||||||

| Prepayments and other current assets |

80,246 | 70,025 | 231,868 | 1,383,648 | — | 1,765,787 | ||||||||||||||||||

| Short-term investments |

716,658 | 318,273 | 1,146,949 | 1,175,309 | — | 3,357,189 | ||||||||||||||||||

| Long-term investments, net |

935,594 | 61,076 | 12,325 | 1,223,943 | — | 2,232,938 | ||||||||||||||||||

| Other non-current assets |

— | 2,736,729 | 972,983 | 2,183,411 | — | 5,893,123 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total assets |

19,148,751 |

12,783,566 |

7,282,645 |

6,913,474 |

(22,262,828 |

) |

23,865,608 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Accounts payable |

— | 114,301 | 627,625 | 2,332,372 | — | 3,074,298 | ||||||||||||||||||

| Salary and welfare payables |

— | 430,030 | 15,660 | 288,686 | — | 734,376 | ||||||||||||||||||

| Taxes payable |

— | 9,015 | 11,685 | 106,492 | — | 127,192 | ||||||||||||||||||

| Short-term loans |

— | — | — | 100,000 | — | 100,000 | ||||||||||||||||||

| Deferred revenue |

30,646 | 12,412 | 304,956 | 1,769,992 | — | 2,118,006 | ||||||||||||||||||

| Accrued liabilities and other payables |

84,539 | 656,345 | 47,422 | 449,370 | — | 1,237,676 | ||||||||||||||||||

| Amounts due to Group companies (4) |

— | 12,357,299 | 6,152,556 | 3,752,973 | (22,262,828 | ) | — | |||||||||||||||||

| Other long-term payable |

8,340,922 | 331,294 | — | 19,640 | — | 8,691,856 | ||||||||||||||||||

| Deficit in subsidiaries and VIEs (3) |

3,092,444 | 1,818,983 | 1,941,724 | — | (6,853,151 | ) | — | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total liabilities |

11,548,551 |

15,729,679 |

9,101,628 |

8,819,525 |

(29,115,979 |

) |

16,083,404 |

|||||||||||||||||

| Total Bilibili Inc’s Shareholders’ equity/(deficit) (3) |

7,600,200 | (3,092,444 | ) | (1,818,983 | ) | (1,941,724 | ) | 6,853,151 | 7,600,200 | |||||||||||||||

| Noncontrolling interests |

— | 146,331 | — | 35,673 | — | 182,004 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total shareholders’ equity/(deficit) |

7,600,200 |

(2,946,113 |

) |

(1,818,983 |

) |

(1,906,051 |

) |

6,853,151 |

7,782,204 |

|||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total liabilities and shareholders’ equity/(deficit) |

19,148,751 |

12,783,566 |

7,282,645 |

6,913,474 |

(22,262,828 |

) |

23,865,608 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Selected Condensed Consolidated Cash Flows Data

For the Year Ended December 31, 2021 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Consulting and services charges from/(to) Group companies |

— | 637,787 | — | (637,787 | ) | — | — | |||||||||||||||||

| Other operating cashflow from/(to) Group companies |

— | 854,325 | (2,538,232 | ) | 1,683,907 | — | — | |||||||||||||||||

| Operating cashflow (to)/from third-parties |

(104,672 | ) | (3,382,667 | ) | 2,569,410 | (1,729,079 | ) | — | (2,647,008 | ) | ||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash (used in)/provided by operating activities |

(104,672 |

) |

(1,890,555 |

) |

31,178 |

(682,959 |

) |

— |

(2,647,008 |

) | ||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Investments in and loans to subsidiaries, VIEs and VIEs’ subsidiaries (3)(4) |

(11,168,671 | ) | (2,409,051 | ) | (3,012,727 | ) | — | 16,590,449 | — | |||||||||||||||

| Purchase of short-term investments |

(48,781,106 | ) | (3,643,036 | ) | (6,714,400 | ) | (12,610,305 | ) | — | (71,748,847 | ) | |||||||||||||

| Maturities of short-term investments |

36,744,305 | 3,224,958 | 7,601,200 | 12,954,425 | — | 60,524,888 | ||||||||||||||||||

| Placements of time deposits |

(10,658,126 | ) | — | — | (39,318 | ) | — | (10,697,444 | ) | |||||||||||||||

| Maturities of time deposits |

7,600,828 | — | — | 54,319 | — | 7,655,147 | ||||||||||||||||||

| Other investing activities |

(1,153,850 | ) | (4,811,039 | ) | (1,081,210 | ) | (3,265,756 | ) | — | (10,311,855 | ) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash used in investing activities |

(27,416,620 |

) |

(7,638,168 |

) |

(3,207,137 |

) |

(2,906,635 |

) |

16,590,449 |

(24,578,111 |

) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Investments and loans from subsidiaries, VIEs and VIEs’ subsidiaries (3)(4) |

— | 10,407,294 | 2,875,929 | 3,307,226 | (16,590,449 | ) | — | |||||||||||||||||

| Proceeds from issuance of ordinary shares, net of issuance costs of HKD337,143 |

19,288,423 | — | — | — | — | 19,288,423 | ||||||||||||||||||

| Proceeds from issuance of convertible senior notes, net of issuance costs of US$13,857 |

10,085,520 | — | — | — | — | 10,085,520 | ||||||||||||||||||

| Other financing activities |

3 | 571,548 | 143,658 | 300,000 | — | 1,015,209 | ||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash provided by financing activities |

29,373,946 |

10,978,842 |

3,019,587 |

3,607,226 |

(16,590,449 |

) |

30,389,152 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

12

For the Year Ended December 31, 2020 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) | ||||||||||||||||||||||||

| Consulting and services charges from/(to) Group companies |

— | 1,074,899 | — | (1,074,899 | ) | — | — | |||||||||||||||||

| Other operating cashflow from/(to) Group companies |

— | 503,109 | (1,089,126 | ) | 586,017 | — | — | |||||||||||||||||

| Operating cashflow (to)/from third-parties |

(113,574 | ) | (1,950,786 | ) | 852,087 | 1,965,376 | — | 753,103 | ||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash (used in)/provided by operating activities |

(113,574 |

) |

(372,778 |

) |

(237,039 |

) |

1,476,494 |

— |

753,103 |

|||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Investments in and loans to subsidiaries, VIEs and VIEs’ subsidiaries (3)(4) |

(5,102,250 | ) | (2,728,972 | ) | (1,257,779 | ) | — | 9,089,001 | — | |||||||||||||||

| Purchase of short-term investments |

(455,347 | ) | (6,342,424 | ) | (5,959,501 | ) | (13,973,904 | ) | — | (26,731,176 | ) | |||||||||||||

| Maturities of short-term investments |

465,726 | 6,083,275 | 4,874,052 | 13,498,485 | — | 24,921,538 | ||||||||||||||||||

| Placements of time deposits |

(9,604,228 | ) | (1,277,553 | ) | — | (25,515 | ) | — | (10,907,296 | ) | ||||||||||||||

| Maturities of time deposits |

4,925,241 | 2,737,236 | — | 7,896 | — | 7,670,373 | ||||||||||||||||||

| Other investing activities |

(600,067 | ) | (973,590 | ) | (358,478 | ) | (1,928,125 | ) | — | (3,860,260 | ) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash used in investing activities |

(10,370,925 |

) |

(2,502,028 |

) |

(2,701,706 |

) |

(2,421,163 |

) |

9,089,001 |

(8,906,821 |

) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Investments and loans from subsidiaries, VIEs and VIEs’ subsidiaries (3)(4) |

— | 4,922,860 | 3,175,854 | 990,287 | (9,089,001 | ) | — | |||||||||||||||||

| Proceeds from issuance of ordinary shares, net of issuance costs of US$563 |

2,817,458 | — | — | — | — | 2,817,458 | ||||||||||||||||||

| Proceeds from issuance of convertible senior notes, net of issuance costs of US$13,857 |

5,594,779 | — | — | — | — | 5,594,779 | ||||||||||||||||||

| Other financing activities |

3 | (176,821 | ) | — | 100,000 | — | (76,818 | ) | ||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash provided by financing activities |

8,412,240 |

4,746,039 |

3,175,854 |

1,090,287 |

(9,089,001 |

) |

8,335,419 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| For the Year Ended December 31, 2019 |

||||||||||||||||||||||||

Bilibili Inc. |

Other Subsidiaries |

Primary Beneficiaries of VIEs |

VIEs and VIEs’ Subsidiaries |

Eliminating adjustments |

Consolidated Totals |

|||||||||||||||||||

(RMB, in thousands) |

||||||||||||||||||||||||

| Consulting and services charges from/(to) Group companies |

— | 1,510,512 | 68,700 | (1,579,212 | ) | — | — | |||||||||||||||||

| Other operating cashflow (to)/from Group companies |

— | (542,315 | ) | (485,077 | ) | 1,027,392 | — | — | ||||||||||||||||

| Operating cashflow (to)/from third-parties |

(17,418 | ) | (1,516,853 | ) | 905,703 | 823,119 | — | 194,551 | ||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash (used in)/provided by operating activities |

(17,418 |

) |

(548,656 |

) |

489,326 |

271,299 |

— |

194,551 |

||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Investments in and loans to subsidiaries, VIEs and VIEs’ subsidiaries (3)(4) |

(4,731,748 | ) | (1,518,767 | ) | (551,137 | ) | — | 6,801,652 | — | |||||||||||||||

| Purchase of short-term investments |

(101,003 | ) | (2,399,107 | ) | (938,100 | ) | (6,535,669 | ) | — | (9,973,879 | ) | |||||||||||||

| Maturities of short-term investments |

69,762 | 2,895,102 | 914,800 | 6,113,861 | — | 9,993,525 | ||||||||||||||||||

| Placements of time deposits |

(2,552,392 | ) | (2,360,123 | ) | — | (7,584 | ) | — | (4,920,099 | ) | ||||||||||||||

| Maturities of time deposits |

2,267,265 | 1,602,309 | — | 7,584 | — | 3,877,158 | ||||||||||||||||||

| Other investing activities |

(440,026 | ) | (826,161 | ) | (571,672 | ) | (1,097,123 | ) | — | (2,934,982 | ) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash used in investing activities |

(5,488,142 |

) |

(2,606,747 |

) |

(1,146,109 |

) |

(1,518,931 |

) |

6,801,652 |

(3,958,277 |

) | |||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Investments and loans from subsidiaries, VIEs and VIEs’ subsidiaries (3)(4) |

— | 4,493,163 | 1,007,749 | 1,300,740 | (6,801,652 | ) | — | |||||||||||||||||

| Proceeds from issuance of ordinary shares, net of issuance costs of US$9,376 |

1,647,711 | — | — | — | — | 1,647,711 | ||||||||||||||||||

| Proceeds from issuance of convertible senior notes, net of issuance costs of US$11,805 |

3,356,106 | — | — | — | — | 3,356,106 | ||||||||||||||||||

| Other financing activities |

531,237 | (456,212 | ) | — | — | — | 75,025 | |||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net cash provided by financing activities |

5,535,054 |

4,036,951 |

1,007,749 |

1,300,740 |

(6,801,652 |

) |

5,078,842 |

|||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1) | It represents the elimination of the intercompany consulting and services charges at the consolidation level. |

| (2) | It mainly includes technical support services provided by other subsidiaries and VIEs to the primary beneficiaries of VIEs. |

| (3) | It represents the elimination of the investment among Bilibili Inc., other subsidiaries, primary beneficiaries of VIEs, and VIEs and VIEs’ subsidiaries. |

| (4) | It represents the elimination of intercompany balances among Bilibili Inc., other subsidiaries, primary beneficiaries of VIEs, and VIEs and VIEs’ subsidiaries. |

13

A. |

[Reserved] |

B. |

Capitalization and Indebtedness |

Not applicable.

C. |

Reasons for the Offer and Use of Proceeds |

Not applicable.

D. |

Risk Factors |

Summary Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows, and prospects. These risks are discussed more fully below and include, but are not limited to, risks related to:

Risks Related to Our Business and Industry

| • | We operate in a fast-evolving industry. We cannot guarantee that we will successfully implement our commercialization strategies or develop new ones, or generate sustainable revenues and profit. |

| • | We have incurred significant losses and we may continue to experience losses in the future. |

| • | If we fail to anticipate user preferences and provide products and services to attract and retain users, or if we fail to keep up with rapid changes in technologies and their impact on user behavior, we may not be able to attract sufficient user traffic to remain competitive, and our business and prospects may be materially and adversely affected. |

| • | Our business depends on our ability to provide users with interesting and useful content, which in turn depends on the content contributed by the content creators on our platform. |

| • | Our business generates and processes a large amount of data, and we are required to comply with PRC and other applicable laws relating to privacy and cybersecurity. The improper use or disclosure of data could have a material and adverse effect on our business and prospects. |

| • | Any compromise of cybersecurity of our platform could materially and adversely affect our business, operations and reputation. |

| • | Increases in the costs of content on our platform may have an adverse effect on our business, financial condition and results of operations. |

| • | If the content contained within videos, live broadcasting, games, audios and other content formats on our platform is deemed to violate any PRC laws or regulations, our business, financial condition and results of operations may be materially and adversely affected. |

| • | If the content contained within videos, live broadcasting, games, audios and other content formats on our platform is considered inappropriate or offensive, our business, financial condition and results of operations may be materially and adversely affected. |

| • | We face uncertainties with respect to the enactment, interpretation and implementation of Notice 78 and Notice 3. |

Risks Related to Our Corporate Structure

| • | We are a Cayman Islands holding company conducting our operations primarily through our PRC subsidiaries, the VIEs and their subsidiaries in China; we have no equity ownership in the VIEs and their subsidiaries. Holders of our Class Z ordinary shares or the ADSs hold equity interest in Bilibili Inc., our Cayman Islands holding company, and do not have direct or indirect equity interests in the VIEs and their subsidiaries. If the PRC government finds that the agreements that establish the structure for operating our business do not comply with PRC laws and regulations, or if these regulations or their interpretations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. Bilibili, its PRC subsidiaries and VIEs, and investors of Bilibili face uncertainty about potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIEs and, consequently, significantly affect the financial performance of the VIEs and our company as a whole. |

14

| • | If the PRC government finds that the agreements that establish the structure for operating our businesses in China do not comply with PRC regulations on foreign investment in internet and other related businesses, or if these regulations or their interpretation change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. |

Risks Related to Doing Business in China

| • | The PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations in this nature may cause the value of such securities to significantly decline. Uncertainties in the interpretation and enforcement of PRC laws and regulations could limit the legal protections available to you and us. |

| • | We face uncertainties with respect to the interpretation and implementation of the Anti-Monopoly Guidelines for the Internet Platform Economy Sector and other anti-monopoly and competition laws and how it may impact our business operations. |

| • | The PCAOB is currently unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections over our auditor deprives our investors with the benefits of such inspections. |

| • | The ADSs will be prohibited from trading in the United States under the Holding Foreign Companies Accountable Act, or the HFCAA, in 2024 if the PCAOB is unable to inspect or fully investigate auditors located in China, or in 2023 if proposed changes to the law are enacted. The delisting of the ADSs, or the threat of their being delisted, may materially and adversely affect the value of your investment. |

| • | The approval of, or report and fillings with the CSRC or other PRC government authorities may be required in connection with our offshore offerings under PRC law, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing and report process. |

| • | Regulation and censorship of information disseminated over the mobile and internet in China may adversely affect our business and subject us to liability for content posted on our platform. |

Risks Related to Our Listed Securities

| • | The trading price of our listed securities have been and are likely to continue to be volatile, regardless of our operating performance, which could result in substantial losses to our investors. |

| • | We adopt different practices as to certain matters as compared with many other companies listed on the Hong Kong Stock Exchange. |

Risks Related to Our Business and Industry

We operate in a fast-evolving industry. We cannot guarantee that we will successfully implement our commercialization strategies or develop new ones, or generate sustainable revenues and profit.

We operate in a fast-evolving industry, and our commercialization model is evolving. We generate revenues primarily by providing our users with valuable content, such as videos, mobile games and live broadcasting. We also generate revenues from advertising,

e-commerce

and other services. We cannot assure you that we can successfully implement the existing commercialization strategies to sustainably generate growing revenues, or that we will be able to develop new commercialization strategies to grow our revenues. If our strategic initiatives do not enhance our ability to commercialize or enable us to develop new commercialization approaches, we may not be able to maintain or increase our revenues or recover any associated costs. In addition, we may introduce new products and services to expand our revenue streams, including products and services with which we have little or no prior development or operating experience. If these new or enhanced products or services fail to engage users, content creators or business partners, we may fail to diversify our revenue streams or generate sufficient revenues to justify our investments and costs, and our business and operating results may suffer as a result. 15

We have incurred significant losses and we may continue to experience losses in the future.