PART II – INFORMATION REQUIRED IN OFFERING CIRCULAR

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted before the offering statement filed with the Commission is qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor may there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful before registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

PRELIMINARY OFFERING CIRCULAR

SUBJECT TO COMPLETION DATED _________, 2025

Minimum Offering: N/A

Maximum Offering: 10,000,000 Series C Preferred Units

UC ASSET LP

Series C Preferred Units

$1.00 per unit

This is our secondary public offering (“SPO”). We are offering a maximum of 10,000,000 series C preferred units representing limited partner interests at a price of $1.00 per unit. The minimum investment is 500 preferred units, or $500 based on the per unit price.

We estimate that we will receive a net proceeds of $9.65 million if we sell the maximum amount of securities offered, after fees, commissions and other costs.

Our preferred units may be converted into common units, both of which represent limited partner interests. See Item 14 “Securities Being Offered” contained in this Offering Circular. Potential investors are urged to consult their tax advisor regarding the tax consequences to them of acquiring, holding and disposing of our preferred units, in light of their particular circumstances.

Prior to this offering, our common units have been traded and quoted on platforms operated by the OTC Market Group, first on OTCQX from January 01, 2019, and then on OTCQB from January 01, 2024. Our trading was temporarily moved to the expert market between June 2024 till August 2024, due to the absence of qualified auditor report, which we provided later on August 09, 2024. Our stocks restarted trading under Pink Current status, and was moved back to OTCQB on November 05, 2024.

There is no public market for our preferred units. However, our preferred units will be eligible for conversion into common units, at the discretion of unit holders, after 12 months of holding period.

We intend to offer and sell the Series C preferred units through Reg A+ selling platforms such as “rialtomarkets.com”. We also will offer and sell through the efforts of the members of our general partner, UCF Asset LLC, acting on our behalf. We may use other supplementary underwriters or broker-dealers to offer or sell preferred units in this offering.

The offering will terminate upon the earlier of: (i) a date determined by our general partner after the minimum number of preferred units is sold, or (ii) __________, which is one calendar year after the qualification of the offering statement of which this Offering Statement forms a part. The proceeds of this offering from sales by the respective selling platforms or other supplementary brokers will be placed into escrow account designated by them, if any. However, there will be no escrow account for proceeds from direct sale by the members of our general partner, nor if the respective selling platforms or supplementary brokers do not designate escrow accounts.

Some of our Risk Factors include:

| ● | General risk related to our Partnership: We have a limited operating history. We are significantly dependent on our general partner and its members. Our investors will have limited ability to exercise control over the operation of our partnership due to their status as limited partners. |

| ● | Risks Related to our Operations in General: Real estate investments are illiquid. Our portfolio may not appreciate in value. Our properties may not generate any income to include rent income. Our portfolio may not be diversified due to limited size. We may not have control over costs arising from maintenance of properties, including tax and insurance. We may not have control over costs arising from redevelopment or renovation of properties. We may not be able to find sufficient properties available to achieve our investment goals. We may overpay for our properties at the point of acquisition, and may be forced to sell properties under their fair market value. We may suffer losses that are not covered by insurance. We may have limited control over the performance of our investments in other real estate companies. And our debt investment may become uncollectible. |

| ● | Risks Related to Cannabis Property Investment: Business activities of our cannabis tenant may remain illegal under U.S. federal law, while federal government’s approach towards cannabis laws and regulations may change to become more adversary. Security Exchange Commission (SEC) may change policies and act against public companies for investing in properties used for cannabis cultivation. Business institutions, such as banks and insurance companies, may refrain from providing services to cannabis-related properties. State and local governments may change laws and regulations on cannabis activities. And our cannabis tenants may become non-compliant with state and local laws and regulations. |

| ● | Risks Related to This Offering, our Preferred Units and Common Units: Investors will not have access to funds subscribed to our offering, during a portion of the offering period. Investors may experience dilution of their investment when converting their holdings into common units. Investment in our preferred shares will only be redeemable or eligible for company repurchases under specific conditions. Our preferred units are not publicly traded. Our common units have limited trading activities, so investors may not be able to resell their units at satisfactory prices, even after converted into common units. Value of investment will be subject to market fluctuations. |

Further, there are risks associated with federal laws regarding investment companies and federal taxes, as well as other domestic and international eco-political factors.

See “Risk Factors” section in Item 3: Summary and Risk Factors, for a more comprehensive discussion of risks to consider before purchasing the securities offered in this Offering Circular.

This offering is being conducted pursuant to an exemption from registration under Regulation A of the Securities Act of 1933, as amended. The disclosure we are providing to you herein contains the information required by the Offering Circular format described in Part II of an offering statement on Form 1-A under Regulation A.

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Our partnership is managed by our general partner under the terms of our partnership’s Limited Partnership Agreement. Our and our general partner’s principal office is located at 537 Peachtree Street NE, Atlanta, Georgia 30308. Our phone number is (470) 475-1035. Our website is www.ucasset.com.

The United States Securities and Exchange Commission does not pass upon the merits of or give its approval to any securities offered or the terms of the offering, nor does it pass upon the accuracy or completeness of any offering circular or other solicitation materials. These securities are offered pursuant to an exemption from registration with the Commission; however, the Commission has not made an independent determination that the securities offered are exempt from registration.

The date of this Offering Circular is , 2025.

ITEM 2: TABLE OF CONTENTS

Until , 2025 (90 days after qualification of the offering statement of which this Offering Circular forms a part), all dealers that buy, sell or trade our common units, whether or not participating in this offering, may be required to deliver a copy Offering Circular subject to the provisions of Rule 251(d)(2)(ii) under Regulation A.

- i -

IMPORTANT INFORMATION ABOUT THIS OFFERING CIRCULAR

Please carefully read the information in this document and any accompanying supplement, which we refer to collectively as the Offering Circular. You should rely only on the information contained in this Offering Circular prepared by or on behalf of us and delivered or made available to you. Neither we nor any person acting on our behalf have authorized anyone to provide you with additional or different information. We are offering to sell, and seeking offers to buy, any securities offered herein only in jurisdictions where offers and sales are permitted. The information contained in this Offering Circular is accurate only as of its date, regardless of its time of delivery or of any sale of our securities offered herein. Our business, financial condition, operating results, and prospects may have changed since that date.

As used in this Offering Circular, references to “we,” “us,” “our,” or the “partnership” refer to UC Asset LP and references to “general partner” refer to UCF Asset LLC, the general partner of UC Asset LP.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Offering Circular contains forward-looking statements. All statements other than statements of historical facts contained in this Offering Circular, including statements regarding our future results of operations and financial position, business strategy, and likelihood of success and other plans and objectives of management for future operations, and future results of current and anticipated products are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “aim,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Offering Circular are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Offering Circular and are subject to a number of risks, uncertainties and assumptions described under the sections in this Offering Circular titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Offering Circular. Forward-looking statements are subject to inherent risks and uncertainties, some of which cannot be predicted or quantified and some of which are beyond our control. The events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. Moreover, new risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties that we may face. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

- ii -

ITEM 3: SUMMARY and RISK FACTORS

This summary highlights information contained elsewhere in this Offering Circular. This summary does not contain all of the information you should consider before investing in the securities offered in this Offering Circular. You should read this entire Offering Circular carefully, especially the section in this Offering Circular titled “Risk Factors,” before making an investment decision.

Overview

Our Company

UC Asset LP (“UC Asset,” the “Company,” the “Partnership”, “we,” or “us”) is a limited partnership formed on February 01, 2016, under the laws of the State of Delaware. We have executive offices in both the State of Georgia, and the State of Oklahoma.

The business purpose of our Partnership is to invest in real estate for capital appreciation.

Our business model is to invest “innovatively” in real estate, by investing in properties before the market situation may experience substantial change due to the emergence of new technologies, new economic factors, and/or new regulations. In addition, we may implement innovative financial engineering strategies to enhance our returns.

Since 2021, we have been exploring opportunities to acquire and renovate historic landmark buildings, with the potential to convert them into short-term rental (via platforms such as Airbnb) properties.

Beginning in 2023, our major business focus has shifted to investing in real estate dedicated to cannabis cultivation.

Risks Related to Our Business

Our business and our ability to execute our business strategy are subject to a number of risks as more fully described in the section titled “Risk Factors.” These risks include, among others:

| ● | Real estate investments are illiquid, and it is difficult for managers to adjust their portfolio in response to changing circumstances. Our portfolio, due to its limited size, is not diversified, and thereby more vulnerable to negative impacts from changing circumstances. Our performance may be negatively impacted by factors beyond our control, including regional factors in metro Atlanta, Georgia, and Oklahoma City, Oklahoma, where all our portfolio properties are concentrated. |

| ● | Cannabis Property Investments are exposed to high risks from legal and regulatory perspective. Business activities of our cannabis tenant may remain illegal under U.S. federal law, while federal government’s approach towards cannabis laws and regulations may change to become more adversary. Security Exchange Commission (SEC) may change policies and act against public companies for investing in properties used for cannabis cultivation. Business institutions, such as banks and insurance companies, may refrain from providing services to cannabis-related properties. And our cannabis tenants may become non-compliance with state and local laws and regulations, particularly if those laws and regulations will change. |

| ● | Our management team are lean, in the sense that our general partner has only two members, and the loss of either of them could adversely affect our ability to continue operations. |

| ● | No active market exists for our preferred units offered herein, and the trading activity of our common units is limited. Investors may not be able to resell their shares at satisfactory prices, even after converted into common units. |

Regulation A+

We are offering our Series C preferred units pursuant to rules by the Securities and Exchange Commission mandated under the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. These offering rules are often referred to as “Regulation A+”, or “Reg A+” for short, among which we are relying upon “Tier 2” of Regulation A +.

We completed our Initial Public Offering(“IPO”) under Reg A+ in the year 2018 and, in compliance with the requirements of Tier 2 of Reg A+, have been publicly filing annual, semiannual, and current event reports with the Securities and Exchange Commission (“SEC”) since the qualification of our IPO’s offering statement. We will continue to meet these filing requirements, regardless of whether this offering statement, of which this Offering Circular constitutes a part, will be qualified by the SEC.

Generally, no sale may be made to you in this offering if you do not satisfy the investor suitability standards described in this Offering Circular under Plan of Distribution. We encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

- 1 -

The Offering

We are offering a maximum number of 10,000,000 shares of Series C Preferred Units (“Series C”, “Preferred Units”, or “the offered Units”) at an offering price of $1.00 per unit. For the terms and conditions of Series C, please refer to a generic copy of the certificate of Series C, which is contained herein as an Exhibit.

This is our secondary public offering (“SPO”). The Company is authorized to issue and deliver the offered Units under Section 4.01(a) of our current by-law, which is the 7th amended and restated version of our Limited Partnership Agreement (“By-law”, or “LPA”), dated May 31, 2023. A link to our current By-law can be found at the EDGAR system: https://www.sec.gov/Archives/edgar/data/1723517/000121390023040858/ea178827ex3-2_ucassetlimit.htm

Our initial public offering (“IPO”) was a Reg A+ tier 2 offering qualified by SEC on June 14, 2018, subsequently amended and qualified by SEC on Sept 12, 2018. Our IPO was closed on October 12, 2018. We raised $1.45 million through IPO. Since January 2, 2019, our shares have been quoted and traded on the OTC Markets, initially on the OTCQX segment, and then, starting from January 2, 2023, on the OTCQB segment.

The following table lists key elements of our SPO:

| Series C preferred units offered by us | Maximum: 10,000,000 units | |

| Series C preferred units to be outstanding after this offering | Maximum: 10,000,000 units | |

| Use of proceeds | We intend to use the proceeds of this offering to acquire certain cannabis properties in Edmond, Oklahoma, and to invest in acquisition and renovation of additional properties, cannabis or non-cannabis, in other metro areas to include Atlanta, Georgia, and other uses. See “Use of Proceeds” for a more detailed description. | |

| Offering price | $1.00 per unit | |

| Gross Proceeds | Maximum: $10,000,000 | |

| Duration | The offering will terminate upon the earlier of: (i) a date determined by our general partner, or (ii) 12 months after the date of qualification of our offering statements by SEC. | |

| Risk factors | See “Risk Factors” and other information included in this Offering Circular for a discussion of factors that you should consider carefully before deciding to invest in our common units. | |

| Preferred Dividend | Subject to the larger of i)net operating proceeds generated from portfolio investments which will be formed using net proceeds raised through this Offering; or ii) net income of the Company, holders of Series C preferred units shall receive a preferred dividend at 8% per annum, equivalent to $0.08 per unit annually, to be distributed on an annual basis. Terms and conditions applicable. Please refer to Exhibit: Certificate of Series C Preferred Units for more information. | |

| Secondary trading | Twelve months following the closing date of our SPO, all Series C units will become eligible for conversion into common units. Our common units are currently traded on OTCQB. | |

| Conversion Ratio | The number of common units that will be issued to a shareholder for converting any number of Series C preferred units shall be equal to the sum amount of the total face value of the converted preferred units and the total unpaid dividend due on those converted preferred units, divided by Conversion Price, and then rounded to the nearest integer. | |

| Conversion Price | Conversion Price shall be set at the highest of 1) $1.00 per unit; or 2) audited book value per common unit of the most recent audited financial statement preceding the conversion date. |

- 2 -

Investing in the securities offered in this Offering Circular involves a high degree of risk, to the extent that you may lose all of your investment. You should carefully consider the risks described below, as well as the other information in this Offering Circular before deciding whether to invest in our preferred units. The occurrence of any of the events or developments described below could harm our financial condition, results of operations, business, and prospects. Additional risks and uncertainties that are not presently known to us or that we currently deem immaterial also may harm our business, financial conditions, result of operations, and prospects.

General Risks Related to our Partnership

We have a limited operating history.

We were formed in February 2016 and have a limited operating history. As a result, there is only a limited period on which to base an assumption that our business operations will prove to be successful. Our future operating results will depend on many factors, including our ability to raise adequate working capital, availability of properties for investment, and our ability to manage portfolio of properties.

We are significantly dependent on our general partner and its members.

Our business plan is significantly dependent upon the abilities and continued participation of our current members, especially the managing members, of our general partner. The loss or unavailability of their services would have an adverse effect on our business, operations, and prospects. There can be no assurance that we would be able to locate or employ personnel to replace any one of the current members of our general partner, should any of them have their services discontinued. In the event that all of their services become unavailable, we may be required to cease pursuing our business, which could result in a loss to your investment.

Our general partner has broad discretion to manage our partnership, and you will have limited ability to exercise control over the operation of our partnership.

UCF Asset LLC, our general partner, has the power to make operational decisions without input from the limited partners. Our general partner determines our major policies, including our policies regarding financing, growth and debt capitalization. Our general partner may amend or revise these and other policies without a vote of the limited partners. Our general partner’s broad discretion increases the uncertainty and risks you face as a limited partner.

Our ability to make distributions to our limited partners is subject to fluctuations in our operating results and financial performance.

We do not currently have an established policy on paying distributions to our common unit holders. Since our IPO, we have made only one dividend distribution of $0.10 per common unit in the year 2021. There is no guarantee or assurance that we may pay any distributions to common unit holders in the future. Meanwhile, preferred shareholders will be entitled to receive preferred dividends whether or not any dividends are distributed to common unit holders. The Company’s ability to pay preferred dividends is subject to fluctuations in our operating results and financial performance.

Risks Related to our Operations in General

Real estate investments are illiquid.

Because real estate investments are relatively illiquid, our ability to promptly sell one or more properties or investments in our portfolio in response to changing economic, financial and investment conditions may be limited. We may be unable to realize our investment objectives by sale, other disposition or refinance at attractive prices within any given period of time or may otherwise be unable to complete any exit strategy.

- 3 -

Our portfolio may not appreciate in value.

We intend to invest in undervalued properties for capital appreciation. There is no assurance that our real estate investments will appreciate in value or will ever be sold at a profit. The marketability and value of the properties will depend upon many factors beyond the control of our management, such as general economic conditions, availability of financing, interest rates and other factors, including supply and demand, that are beyond our control.

Our properties may not generate any income during the time of holding.

We also intend to manage our invested properties to generate income such as rental income, during the time we hold these portfolio properties. There is no assurance that our portfolio properties will generate any income during our holding period. Our ability to generate income from any properties will depend upon many factors beyond the control of our management, such as general economic conditions, availability of financing, interest rates and other factors, including supply and demand, that are beyond our control.

Our portfolio may not be diversified due to limited size.

Our capital is limited and so is the size of our portfolio, and hence we will focus on limited sections of markets, both geographically and industrially, when selecting our investment properties. The lack of diversification may result in our performance being volatile, as it may be disproportionally affected by adverse changes in regional and industrial and other segmental conditions.

We may not have control over costs arising from maintenance of properties, including taxes and insurance.

Most of our portfolio properties will likely require regular maintenance to preserve their value, this will include paying property taxes and insurance and utility bills. These maintenance costs may rise due to factors beyond our control, including the decisions by local governments and utility companies, and local economic conditions which may cause the maintenance costs to rise.

We may not have control over costs arising from redevelopment or renovation of properties.

Subject to the condition of invested properties, we may retain contractors to redevelop and/or renovate them to increase our profit, or, our third-party business partners who have managing power over our portfolio properties may choose to redevelop and/or renovate them. As a result, we will be subject to risks in connection with the ability of our contractors and/or business partners to control costs, which will be subject to their ability to build in conformity with plans and specification, to complete projects in time, and to other economic factors which may be beyond their and our control.

Inventory or available properties might not be sufficient to achieve our investment goals.

We may not be successful in identifying suitable properties that meet our acquisition criteria, or in consummating acquisitions or investments on satisfactory terms. Failures in identifying or consummating acquisitions would impair the pursuit of our business plan.

The consideration paid for our target acquisition may exceed fair market value.

The consideration that we pay for a property will be based upon numerous factors, and the acquisition may be purchased in a negotiated transaction rather than through a competitive bidding process. We cannot assure anyone that the purchase price that we pay for an acquisition of a property will be a fair price, or that the location or other relevant economic and financial data of any properties that we acquire will meet acceptable risk profiles.

We may be forced to sell properties under fair market value and thereby may suffer a loss.

Like any real estate business, we may face shortage of cash flow and other distressful situations under which we may have to sell properties to obtain cash. In addition, we may obtain lines of credit or other financing that may be secured by our properties, which may result in a forced sale or even foreclosure of the pledged properties, if we do not have adequate cash to pay back our financing obligations. In any of these events, some or all of our portfolio properties will likely be sold under their fair market value, which will increase the risk of losing our investment in these properties.

- 4 -

We may suffer losses that are not covered by insurance.

The geographic areas in which we hold properties may be at risk for damage to property due to certain weather-related and environmental events, including such things as severe thunderstorms, hurricanes, flooding, and tornadoes, as well as other damages due to unexpected events such as theft and fire. To the extent possible, the general partner may but is not required to attempt to acquire insurance against those hazards. However, such insurance may not be available in all areas, nor are all hazards insurable. In addition, an insurance company may deny coverage for certain claims or determine that the value of the claim is less than the cost to restore the property, resulting in further losses to our partnership.

We may have limited control over the performance of our investments in other real estate companies.

We may invest in other real estate companies in forms of equity or debt or a combination of both. We may have limited control and even no control over the management and performance of these companies. There is no assurance or guarantee that our equity investment in other real estate companies will generate return, or that our debt investment in them will be paid back. Further, if the company we invested in is a public company, our investment in it may be subject to risks of volatility of the trading price and volume of its stocks, which is beyond our control.

Our debt investment may become uncollectible.

We may invest part of our cash reserve into debt instruments, including but not limited to government, municipal and/or corporate bonds, with the intention of improving our profitability. Any of these debt investments may become uncollectible due to economic and other factors that are beyond our control.

Risks Related to Cannabis Property Investment

Business activities of our cannabis tenant may remain illegal under U.S. federal law.

We have invested and intend to continue investing in properties which, through direct and indirect business relationships, are leased to state-licensed cannabis growers. The business activities of our cannabis tenants, while believed to be compliant with applicable U.S. state and local laws, are currently illegal under U.S. federal law. There have been campaigns to federally legalize those regulated cannabis business, but there is no guarantee or assurance that federal legalization of cannabis business will happen in the foreseeable future. Our revenue generated from those properties may still be interpreted by federal authorities as from sources involved with illegal activities, and adverse actions may be taken by federal authorities against us, including but not limited to forfeit related revenue and impose fines.

The U.S. federal government’s approach towards cannabis laws and regulations may change to become more adversary.

For the past two decades, the U.S. federal government, including its legislative and executive branches, have been advocating measures to legalize certain activities pursuant to the cultivation, transportation, transaction and consumption of cannabis products. In addition to other moves, the Department of Justice published a notice of proposed rulemaking (NPRM) on May 21, 2024, to transfer marijuana from schedule I of the Controlled Substances Act (CSA) to schedule III of the CSA, consistent with the view of the Department of Health and Human Services (HHS) that marijuana has a currently accepted medical use, has a potential for abuse less than the drugs or other substances in schedules I and II, and that its abuse may lead to moderate or low physical dependence or high psychological dependence. However, this rule change has not been finalized. In general, the U.S. federal government’s approach towards cannabis and cannabis-related activities remains uncertain, and the uncertainty may increase. If the U.S. federal government’s approach toward cannabis laws and regulations will change to restrict activities pursuant to cultivation, transportation, transaction and consumption of cannabis products, it will have a material adverse effect on our current and future cannabis tenants, and may in turn have a material adverse effect on our cannabis property investments.

- 5 -

Security Exchange Commission (SEC) may change policies and take action against public companies for investing in properties used for cannabis cultivation

There are a few other U.S. public companies besides us, which invest in properties directly or indirectly leased to cannabis growers. Among those two of them are listed on major national exchanges: Innovative Industrial Properties Inc (NYSE: IIPR) and Power REIT (NYSE American: PW). As far as we are aware of, there is no current action taken by SEC against those company solely on the basis that they have portfolio properties which are leased to cannabis growers, and we don’t expect SEC to take any actions of this kind in the foreseeable future. However, there is no assurance that SEC will not change its policies and start to take actions against public companies solely for investing in properties used for cannabis cultivation. If so, we may be assessed financial punishment, ordered to exit our investment in cannabis properties, or disqualified to continue operating as a public company.

Business institutions may refrain from providing services to cannabis-related properties

Many business institutions which provide services critical to our continuous operation, including but not limited to commercial banks, insurance companies, licensed broker dealers, auditors, and realtors, are subject to federal regulations or are beneficiaries of federal grants and services. Therefore, these institutions may take precautious measures to not provide certain services to us, in regard of our investments in cannabis properties. This may limit the scope and quality of services we can receive, and therefore have material adverse effects on our performance.

State and local governments may change laws and regulations on cannabis activities

We believe that our cannabis tenants are currently in compliance with applicable state and local laws and regulations, and expect them to continue being so. However, some states and local governments have changed, and may continue to change, laws and/or regulations to apply more restrictions on cultivation, transportation, transaction and consumption of cannabis products. Any such change will have material adverse effect on our current and future cannabis tenants, and may in turn have a material adverse effect on our cannabis property investments.

Our cannabis tenants may become non-compliance with state and local laws and regulations

Cannabis cultivation is highly regulated business at state and local level. Cannabis growers are subject to a significant amount of reporting requirements, examinations, and other burdensome regulatory obligations. Tenants to our cannabis properties may not always be capable of maintaining their status as in compliance with state and local laws and regulations. If any of these tenants become non-compliant, they will have to decrease and even cease their cultivation operations, and may have to terminate their leases. This may result in material loss of value of our cannabis properties.

Investment Company Risks

Investors will not receive the benefit of the regulations provided to real estate investment trusts or investment companies.

We are not a real estate investment trust and enjoy a broader range of permissible activities. Neither are we an investment company under the Investment Company Act of 1940 (referred to as the “1940 Act”). We intend to continue operating in such manner. As a result, investors will be exposed to certain risks that would not be present if we were subjected to a more restrictive regulatory situation.

The exemption from the Investment Company Act of 1940 may restrict our operating flexibility.

We do not believe that at any time we will be deemed an “investment company” under the 1940 Act as we do not intend on trading or selling securities. However, if at any time we may be deemed an “investment company,” we believe we will be afforded an exemption under Section 3(c)(5)(C) of the 1940 Act, as Section 3(c)(5)(C) of the 1940 Act excludes from regulation as an “investment company” any entity that is primarily engaged in the business of purchasing or otherwise acquiring “mortgages and other liens on and interests in real estate”. Maintaining this exemption may adversely affect our ability to acquire or retain investments, engage in future business activities that we consider potentially profitable, or may compel us to dispose of investments we would otherwise prefer to keep.

- 6 -

If we are deemed to be an investment company, we may be required to institute burdensome compliance requirements, and our activities may be restricted.

If we are ever deemed to be an investment company under the 1940 Act, we may be subject to certain restrictions, including restrictions on the nature of our investments and restrictions on the issuance of securities. In addition, we may have imposed upon us certain burdensome requirements, including registration as an investment company; adoption of a specific form of corporate structure; and reporting, record keeping, voting, proxy, compliance policies and procedures and disclosure requirements and other rules and regulations.

Federal Income Tax Risks

The Internal Revenue Service may challenge our characterization of material tax aspects of your investment in our common units.

You are urged to consult with your own tax advisor with respect to the federal, state, local, and foreign tax considerations of an investment in our partnership. We do not intend to seek any rulings from the Internal Revenue Service regarding any of the tax issues impacting our partnership. Accordingly, we cannot assure you that the tax conclusions discussed in this offering, if contested, would be sustained by the Internal Revenue Service or any court.

You may realize taxable income without cash distributions, and you may have to use funds from other sources to fund tax liabilities.

As a limited partner, you will be required to report your allocable share of our taxable income on your personal income tax return regardless of whether you have received any cash distribution from us. It is possible that your shares will be allocated taxable income in excess of your cash distributions. As a result, you may have to use funds from other sources to pay your tax liability.

You may not be able to benefit from any tax losses that are allocated to your investments.

Units in our partnership, whether common or preferred, may be allocated their share of tax losses if any arise. Section 469 of the Internal Revenue Code limits the allowance of deductions for losses attributable to passive activities, which are defined generally as activities in which the taxpayer does not materially participate. Any tax losses allocated to investors will be characterized as passive losses, and, accordingly, the deductibility of such losses will be subject to these limitations. Losses from passive activities are generally deductible only to the extent of a taxpayer’s income or gains from passive activities and will not be allowed as an offset against other income, including salary or other compensation for personal services, active business income or “portfolio income”, which includes non-business income derived from dividends, interest, royalties, annuities and gains from the sale of property held for investment. Accordingly, you may receive no benefit from your share of tax losses unless you are concurrently being allocated passive income from other sources.

We may be audited which could subject you to additional tax, interest, and penalties.

Our federal income tax returns may be audited by the Internal Revenue Service. Any audit of our partnership could result in an audit of your tax return. The results of any such audit may require adjustments of items unrelated to your investment, in addition to adjustments to items related to our partnership. In the event of any such audit or adjustments, you might incur attorneys’ fees, court costs, and other expenses in contesting deficiencies asserted by the Internal Revenue Service. You may also be liable for interest on any underpayment and penalties from the date your tax was originally due. The tax treatment of all partnership items will generally be determined at the partnership level in a single proceeding rather than in separate proceedings with each partner, and our general partner is primarily responsible for contesting federal income tax adjustments proposed by the Internal Revenue Service. In such a contest, our general partner may choose to extend the statute of limitations to all partners and, in certain circumstances, may bind the partners to a settlement with the Internal Revenue Service. Further, our general partner may cause us to take advantage of simplified flow-through reporting of partnership items. If so, adjustments to partnership items would continue to be determined at the partnership level however, and any such adjustments would be accounted for in the year they take effect, rather than in the year to which such adjustments relate. Our general partner will have the discretion in such circumstances either to pass along any such adjustments to the partners or to bear such adjustments at the partnership level.

- 7 -

Risks Related to This Offering, our Preferred Units and Common Units

Investors will not have use of funds subscribed during a portion of the offering period.

We cannot assure you that all or any offered securities will be sold, or that they will be sold in a timely manner. We have no firm commitment from anyone to purchase all or any of our securities offered. During a portion of the offering period, until a closing or a cancellation occurs, investors will not have use of the funds they have provided to subscribe to the offering.

You may experience dilution of your investment in the future.

You may experience dilution by purchasing preferred C units if and when they are converted into common units. See the “Dilution” section of this Offering Circular for a more detailed discussion. Also, in the future if we issue additional common units, or securities convertible into or exchangeable or exercisable for common units, our limited partners, including investors who purchase preferred C units in this offering, could experience dilution at that time also.

Our common units have limited trading activity, and you may not be able to resell your units at satisfactory price.

Our common units have been quoted and traded on the OTC markets since January 2019 (OTCQX from 2019 to 2023, and OTCQB starting from January 2024 till now). However, the trading volume of our common units is limited, and there is no assurance that our common units will continue to be quoted and traded on OTCQB or any other trading platforms. In addition, there are no public trading markets for our preferred units offered in this Offering Circular, and we have no intention of applying for our preferred units to be traded on any public platforms. Because of the lack of any active market for our preferred units, and because of the limited trading activity of our common units, you may be unable to exit your investments, either by selling your preferred units, or by converting your preferred units into common units and then selling those common units, at a price that you consider attractive or satisfactory.

Your investment may not be redeemable or eligible for company repurchases

Our partnership does not currently have a redemption or repurchase program for common units, and there is only limited conditions under which our partnership will redeem or repurchase (“buy back”) your preferred units. We have repurchased limited amounts of our common units, through private transactions. However, the repurchase prices were significantly lower than both the trading price of our common units and the book value per common unit, at the time of repurchase.

Value of your investment will be subject to market fluctuations.

Like any publicly traded securities, the market price (public trading price) of our common units are subject to substantial fluctuations. The value of your investment measured by its market price, therefore, will be subject to substantial fluctuations and may result in substantial loss of value of your investment.

If relations between the United States and China worsen, our Chinese investors may take actions that may have adverse impact on market price of our common units.

A significant number of our common units are and will be owned by Chinese individuals. At various times during recent years, the U.S. and China have had significant disagreements over political and economic issues. Controversies may arise in the future between these two countries. Any political or trade controversies between the U.S. and China, whether or not directly related to our business, could prompt our Chinese investors to take certain actions that may reduce the market price of our common units.

- 8 -

The price per unit of our Series C preferred units being offered is slightly higher than the most recent audited amount of net book value per unit of our common units. As of December 31, 2024, we had a net tangible book value of $0.93 per common unit, on the basis of historical cost. Meanwhile, our offered price for Series C is $1.00 per unit. Besides, the net tangible book value is subject to fluctuations and is expected to change from time to time,

When preferred units are eligible to be converted into common units, the conversion price will be set at the higher of 1) the most recent audited amount of net book value per unit of our common units; or 2) $1.00 per unit. At this moment, our audited book value per common unit is $0.93 per unit. If the Company will suffer a loss in the future and result in its net book value per common unit becoming significantly lower than $1.00, the conversion price will still be set at $1.00, and therefore become significantly higher than the net book value per common unit. In that case, you may experience significant dilution of your investment upon conversion.

Our Limited Partnership Agreement (“LPA”) includes terms which intend to protect investors from dilution arisen out of future issuance of shares. The LPA prohibits our Partnership from issuing common units at a price lower than the most recent net book value per common unit, or issuing any securities that can be converted into common units at a conversion price less than the most recent net book value per common unit. However, these protections may be changed if our partners, including both General Partner and Limited Partners, amend our partnership agreement and remove these protections. If such amendment occurs, the Partnership may be able to issue additional common units, or securities convertible into or exchangeable or exercisable for common units, at a unit price significantly lower than the unit price of previous investors; and our limited partners, including investors who purchase preferred units in this offering, could experience additional dilution, and any such issuances may result in downward pressure on the value of our common units.

- 9 -

This is our secondary public offering. We are offering a maximum amount of 10,000,000 Series C preferred units representing limited partner interests in our partnership.

Our common units are quoted and traded on the OTCQB® Venture Market (“OTCQB”), an electronic quoting platform managed by the OTC Markets Group Inc. Our Series C preferred units will be new issues of securities with no established trading market, and we have no intention of having them listed on a national securities exchange, quotation system or over-the-counter market. Series C preferred units will be eligible to convert into our common units, and will immediately become eligible to be traded on OTCQB as any shares of our common units.

We may offer and sell these Series C preferred units:

| ● | through one or more underwriters or other dealers or agents licensed to sell or resell securities pursuant to Regulation A; AND/OR |

| ● | through the efforts of the members of our general partner acting on our behalf; AND/OR |

| ● | in any other manner permitted by applicable law and rules. |

We believe, in the event our securities are offered through the efforts of the members of our general partner, that the members of our general partner are exempt from registration as a broker-dealer under the provisions of Rule 3a4-1 promulgated under the Securities Exchange Act of 1934 (the “Exchange Act”). In particular, the members (a) are not subject to a statutory disqualification, (b) will not be compensated in connection with their participation by payment of commissions or other remuneration based either directly or indirectly on transactions in securities, (c) are not an associated persons of a broker or dealer, (d) intend to primarily perform substantial duties for or on behalf of our partnership otherwise than in connection with this offering, (e) were not a broker or dealer, or an associated person of a broker or dealer, within the preceding 12 months, and (f) do not participate in selling and offering of securities for any issuer more than once every 12 months other than for our partnership.

Underwriters or agents could make sales in privately negotiated transactions and any other method permitted by law. Securities may be sold in one or more of the following transactions: (a) block transactions (which may involve crosses) in which a broker-dealer may sell all or a portion of the securities as agent but may position and resell all or a portion of the block as principal to facilitate the transaction; (b) purchases by a broker-dealer as principal and resale by the broker-dealer for its own account pursuant to a prospectus supplement; (c) a special offering, an exchange distribution or a secondary distribution in accordance with the applicable rules of the platforms where our securities are or will be quoted and traded; (d) ordinary brokerage transactions and transactions in which a broker-dealer solicits purchasers, including to publicly solicit via electronic communications such as internet; or (e) through a combination of any of these methods. Broker-dealers may also receive compensation from purchasers of these securities which is not expected to exceed those customary in the types of transactions involved.

Supplements to this Offering Circular will be filed and distributed to identify any underwriters, dealers or agents involved in the offering, and will set forth any applicable purchase price, fee, commission or discount arrangement with such underwriters, dealers or agents, and among such underwriters, dealers or agents, or the basis upon which such amounts may be calculated.

If underwriters are used in the sale, they will acquire the securities for their own account and may resell the securities from time to time in one or more transactions at a fixed public offering price or at varying prices determined at the time of sale. The obligations of the underwriters to purchase the securities will be subject to the conditions set forth in the applicable underwriting agreement. We may offer the securities to the public through underwriting syndicates represented by managing underwriters or by underwriters without a syndicate. Subject to certain conditions, the underwriters may be obligated to purchase all of the securities offered by this offering circular.

Any underwriters, dealers or agents that may be engaged in any of the transactions described above may perform separate services for us in the ordinary course of business. We may have agreements with the underwriters, dealers or agents, to indemnify them against specified civil liabilities, including liabilities under the Securities Act or to contribute with respect to payments that the underwriters, dealers or agents may be required to make.

Unless sooner withdrawn or canceled by us, this offering will continue until the earlier of (i) a date determined by the general partner at its sole discretion; or (ii) ______________ (the “Offering Termination Date”), which is one calendar year after the qualification of the offering statement of which this Offering Circular forms a part.

- 10 -

Investors seeking to purchase our Preferred C Units and who satisfy the “qualified purchaser” standards as described below should:

| ● | read the entire Offering Statement (of which this Offering Circular forms a part) and any of its supplements; |

| ● | complete and execute a copy of the subscription agreement (a copy of which is included as an exhibit to the Offering Statement); and |

| ● | provide a check, bank draft or money order, or ACH instructions payable in U.S. dollars to us for the full purchase price of the offered securities being purchased. |

By executing the subscription agreement and paying the full purchase price for the subscribed preferred units, each investor agrees to accept the terms of the subscription agreement and attests that the investor meets the minimum standards of a “qualified purchaser,” and that such subscription does not exceed 10% of the greater of such (natural person) investor’s annual income or net worth.

Upon executing the subscription agreement, subscriptions will be binding upon investors, and will be accepted or rejected within 30 days after receiving the subscription. The fund sent for the subscription is irrevocable and nonrefundable, unless the subscription is rejected, or the offering is withdrawn or canceled.

If the offering is withdrawn or canceled prior to the Offering Termination Date, all proceeds will be promptly returned without interest or deduction to the investors.

We reserve the right to reject any investor’s subscription in whole or in part for any reason, including if we determine in our sole and absolute discretion that such investor is not a “qualified purchaser.” If any prospective investor’s subscription is rejected, all funds received from such investors will be promptly returned without interest or deduction.

Our officers and executives, including members of our general partners, will not purchase preferred C units offered in this offering circular.

Minimum Purchase Requirements

The minimum investment in our preferred C units is 500 units, or $500 based on the per unit price.

Qualified Purchaser

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Pricing Considerations

We determined the offering price of our preferred units in this offering based upon the assessment of our general partner as well as other considerations, including:

| ● | historical and present trading price of our common units; |

| ● | our last audited net equity per common units; and |

| ● | our past and present operation. |

Expenses

Investors will not pay our offering expenses, which are expected to be approximately $225,000. These expenses include legal, accounting, printer, contract employees, promotion, and other offering costs. In addition to offering expenses, we may pay a fee or commission to underwriters as a percentage of the proceeds from selling our offered securities by the underwriters.

- 11 -

ITEM 6: USE OF PROCEEDS TO ISSUERS

Our goal is to raise $9.65 million in net proceeds from this round of offering, assuming an offering price of $1.00 per unit, after deducting estimated offering expenses.

We anticipate that we will use the net proceeds of this offering as follows:

|

25% of Goal Reached

|

●

|

$2.0 million of the net proceeds will be used to acquire and improve a cannabis property (the “Green Oak property”), which is right across the street from our Apple Valley property we currently own in Edmond, Oklahoma. More information about the Green Oak property can be found below within this Item 6. | |

| ● | The remaining net proceeds will be used for working capital and general investment purposes. | ||

| 50% of Goal Reached ($4.75 million) |

● | $2.0 million of the net proceeds will be used to acquire and improve the Green Oak property. More details of this property can be found below within this Item. | |

| ● | $1.6 million of the net proceeds will be used to acquire and improve a cannabis property located in Edmond, Oklahoma (the “Waterloo property”), which shares investors and management with the Green Oak property. More details of Waterloo Property can be found below within this Item 6. | ||

| ● | $800,000 will be used on following possible initiatives, at the sole discretion of our management, subject to business and economic factors: 1) paying down any debt that bears a interests rate of 12% per annum or higher; 2) purchasing short-rental properties in the metro Atlanta area for instant cash income and long term property value appreciation; or 3) providing supplemental capital for the Rufus Rose House project (See Item 7: “other investments//other real estate investments//Rufus Rose House project” for more information.) | ||

| ● | The remaining net proceeds will be used for working capital and general purposes. | ||

| 75% of Goal Reached ($7.20 million) |

● | $3.6 million of the net proceeds will be used to acquire and improve the Green Oak property and the Waterloo property. More details of these properties can be found below within this Item. | |

| ● | $2.0 million will be used to either build a new cannabis property or to acquire an existing one that meets the same standards as our current Apple Valley property. | ||

| ● | $1.2 will be used on following possible initiatives, at the sole discretion of our management, subject to business and economic factors: 1) paying down any debt that bears a interests rate of 12% per annum or higher; 2) purchasing short-rental properties in the metro Atlanta area for instant cash income and long term property value appreciation; or 3) providing supplemental capital for the Rufus Rose House project (See Item 7 for more information about Rufus Rose House project.) | ||

| ● | The remaining net proceeds will be used for working capital and general purposes. | ||

| 100% of Goal Reached ($9.65 million) |

● | $3.6 million of the net proceeds will be used to acquire and improve the Green Oak property and the Waterloo property. See below for more details of these properties. | |

| ● | $4.0 million will be used to build or acquire two cannabis properties which meet the same standards as our current Apple Valley property. | ||

| ● | $1.6 million will be used on following possible initiatives, at the sole discretion of our management, subject to business and economic factors: 1) paying down any debt that bears a interests rate of 12% per annum or higher; 2) purchasing short-rental properties in the metro Atlanta area for instant cash income and long term property value appreciation; or 3) providing supplemental capital for the Rufus Rose House project (See Item 7 for more information about Rufus Rose House project.) | ||

| ● | The remaining net proceeds will be used for working capital and general purposes. |

- 12 -

The table below provides estimates of the number of preferred units we’ll need to sell, in order to reach our net proceeds goals.

| 25% | 50% | 75% | 100% | |||||||||||||

| Series C Preferred units sold | 2,500,000 | 5,000,000 | 7,500,000 | 10,000,000 | ||||||||||||

| Gross Proceeds | $ | 2,500,000 | $ | 5,000,000 | $ | 7,500,000 | $ | 10,000,000 | ||||||||

| Offering Expenses1 | $ | 150,000 | $ | 175,000 | $ | 200,000 | $ | 225,000 | ||||||||

| Selling Commissions & Fees2 | $ | 50,000 | $ | 75,000 | $ | 100,000 | $ | 125,000 | ||||||||

| Net Proceeds | $ | 2,300,000 | $ | 4,750,000 | $ | 7,200,000 | $ | 9,650,000 | ||||||||

| Acquiring and Improving Green Oak Property | $ | 2,000,000 | $ | 2,000,000 | $ | 2,000,000 | $ | 2,000,000 | ||||||||

| Acquiring and Improving Waterloo Property | $ | 0 | $ | 1,600,000 | $ | 1,600,000 | $ | 1,600,000 | ||||||||

| Building or Acquiring Other Cannabis Properties | $ | 0 | $ | 0 | $ | 2,000,000 | $ | 4,000,000 | ||||||||

| Paying Debt, Acquiring & Renovating Properties 3 | $ | 0 | $ | 800,000 | $ | 1,200,000 | $ | 1,600,000 | ||||||||

| Working Capital & General Purpose | $ | 300,000 | $ | 350,000 | $ | 400,000 | $ | 450,000 | ||||||||

| Total Use of Net Proceeds | $ | 2,300,000 | $ | 4,750,000 | $ | 7,200,000 | $ | 9,650,000 | ||||||||

| (1) | These expenses include $50,000 in legal costs, $20,000 accounting costs, $5,000 in blue-sky compliance, and the rest are promotion and other miscellaneous costs. |

| (2) | We have not reached agreements with any brokers. We estimate commission to be at 1% of gross proceeds plus a fixed fee of $25,000, however, actual fees and commission could be more. |

| (3) | This may include: i) paying down any debt that bears 12% or higher annual interest; ii) purchasing short-rental properties in the metro Atlanta area; or iii) providing supplemental capital for the Rufus Rose House project. |

The expected use of the net proceeding from this offering reflects our intentions based on our current business plans and financial conditions. As of the date of this Offering Circular, we cannot predict with certainty the specific uses for the net proceeds to be received upon the completion of this offering, nor can we predict with certainty the amount that we will actually spend on the uses set forth above. Notably, we have not reached any legally binding agreements with the current owners of either the Green Oak property or the Waterloo property. There is no guarantee that we will be able to acquire these two properties at the prices listed above, or at any prices desirable for us.

The amounts and timing of our actual expenditure of the net proceeds from this offering may vary significantly depending on numerous factors. Consequently, our general partner will retain broad discretion over the allocation of the net proceeding from this offering, including the option to invest the net proceeds in a variety of assets, ventures, and capital preservation investments, which may be substantially different from the uses of proceeds set forth hereinabove.

- 13 -

The Green Oak property

The Green Oak property is a 1.19-acre lot, hosting 13 detached buildings (units), each of which provides 1,800 square feet of growing and office spaces:

Pic 6.1: The Green Oak property

The table below is projected profit and loss (P&L) based on numbers provided by the LLC which currently owns this property. We used reasonable efforts to verify these numbers but cannot guarantee their accuracy.

Tab 6.1: Projected Annual Operating Income/Expense of Green Oak Property *

| Operating Income | $ | 399,000 | ||

| Rent Income | $ | 399,000 | ||

| Operating Expense | $ | 52,000 | ||

| Insurance | $ | 13,000 | ||

| Professional Fees | $ | 9,000 | ||

| Water | $ | 25,000 | ||

| Miscellaneous | $ | 5,000 | ||

| Operating Profit (Before Depreciation and Property Tax) | $ | 347,000 |

| * | Based on info provided by the current owner and rounded to thousands. |

The Waterloo property

The Waterloo property is a 0.83-acre lot, hosting 12 detached buildings (units), each of which provides 1,200 square feet of growing and office spaces:

Pic 6.2: The Waterloo property

- 14 -

The table below is projected profit and loss (P&L) based on numbers provided by the LLC which currently owns this property. We used reasonable efforts to verify these numbers but cannot guarantee their accuracy.

Tab 6.2: Projected Annual Operating Income/Expense of Waterloo Property *

| Operating Income | $ | 239,000 | ||

| Rent Income | $ | 239,000 | ||

| Operating Expense | $ | 39,000 | ||

| Insurance | $ | 9,000 | ||

| Professional Fees | $ | 9,000 | ||

| Water | $ | 16,000 | ||

| Miscellaneous | $ | 5,000 | ||

| Operating Profit (Before Depreciation and Property Tax) | $ | 200,000 |

| * | Based on data provided by the current owner and rounded to thousands. |

Important Notice:

Based on our research, the revenue from both Green Oak and Waterloo Property declined significantly for the year 2024 compared to 2023. According to our research, this decline is primarily due to the inability of most units to pass the state fire marshal’s inspection and secure their Certificates of Occupancy (CO) in a timely manner, resulting in the suspension of operations. We believe this setback is temporary and presents an opportunity to acquire the property at a discounted price. We plan to invest in improving all units in the event we acquire them in order to expedite the application process for CO. As of the date of this Offering Circular, a substantial portion of units have successfully obtained their CO.

- 15 -

ITEM 7: DESCRIPTION OF BUSINESS

Overview

UC Asset LP is a limited partnership formed on February 10, 2016, under the laws of the State of Delaware. Our principal office address is 537 Peachtree Street, NE, Atlanta, GA, 30308. We have an executive office at the address of 7408 Apply Valley Rd, Edmond, OK, 73034.

The business purpose of our Partnership is to invest in real estate for capital appreciation, primarily from the appreciation of property value, with cash rental income as supplementary revenue to increase our capital return.

Our business strategy is to invest in properties that are considerably undervalued or have considerable potential to appreciate in the near future. This often involves innovative investment models, under which we will invest in niche markets where the property value is expected to experience dramatic increases, due to the emergence of new technologies, new economic factors, and/or new regulations.

Prior to the year 2023, the Company had invested in residential properties, a piece of farmland, and a historic landmark building. As of and by date of this Offering Circular, the majority of the Company’s portfolio consists of these investments.

Starting from the year 2023, the Company has shifted its primary business focus to investing in “cannabis properties” or “cannabis real estate”, which, by our definition, refers to real estate properties used to cultivate cannabis plants with intention of producing legalized medical or recreational cannabis flower products. Generally, the term “cannabis real estate” also includes other real estate properties such as retail spaces for cannabis dispensaries, industrial facilities for processing and purifying cannabinoids, and manufacturing spaces for producing cannabinoids-containing products. However, we do not, and have no intention to, invest in any other kinds of cannabis real estate besides properties for cultivation.

In this Offering Circular, the term “cannabis properties” or “cannabis real estate” will specifically refer to cannabis cultivation facilities, unless otherwise stated.

Our partnership is managed by our general partner, UCF Asset LLC, under the terms of our Partnership Agreement. Except for limited conditions defined in our limited partnership agreement, UCF Asset LLC as general partner has authority to exercise full management of our partnership. Limited partners are passive investors and have limited power over our partnership and our general partner.

General Partner

UCF Asset LLC is a limited liability company formed on January 26, 2016, under the law of the State of Georgia. The principal office of our general partner is the same as that of our partnership.

The individuals who, directly or indirectly, own and control our general partner are “Larry” Xianghong Wu with a 90% interest and Jason Cunningham with a 10% interest. Larry Wu is the managing member of our general partner.

UCF Asset LLC does not engage in any business activities other than managing our partnership.

The general partner may be removed, upon consent of the limited partners representing at least sixty-six and two-thirds percent (66 2/3%) of the outstanding common units voting as a single class, where (i) the general partner has been convicted of fraud, embezzlement, or a similar felony by a court of competent jurisdiction in a final judgement, or (ii) the general partner materially and willfully breaches our limited partnership agreement.

- 16 -

The general partner may, at any time, assign all or a portion of its partnership interest to any persons and, in the general partner’s sole discretion, admit the persons as an additional or substitute general partner.

The primary purpose of this SPO is to raise capital to expand our portfolio of cannabis cultivation properties, and to do the other things discussed under the heading “Use of Proceeds”.

In this section, we will discuss:

| ● | Description of our first cannabis property: Apple Valley; |

| ● | ROI of Our Cannabis Portfolio, in Comparison to Our Peers; |

| ● | Our Cannabis Investment Strategy |

Description of our First Cannabis Property: Apple Valley

In May 2023, we made our first cannabis property investment by acquiring 50% ownership of Apple Valley Property. Subsequently, we acquired 100% ownership of this property in March 2025. Located in Edmond, a suburban town in the metro Oklahoma City area, this property is 20 miles from downtown Oklahoma City and 30 miles from its primary airport.

This property is a 100% indoor growing facility, equipped with fully computerized control of critical environment factors, including light exposure, temperature, humidity, carbon dioxide level, irrigation and fertilization.

It has approximately 16,550 square feet of growing space, plus a detached office building of 1,550 square feet.

Pic 7.1: Interior of one of the growing rooms, Apple Vally Property

- 17 -

Pic 7.2: Interior of one of the growing rooms, Apple Vally Property

Pic 7.3: Computerized control systems, Apple Vally Property.

- 18 -

Pict 7.4: Overview of Growing Facility. Apple Valley Property.

Pict 7.5: Detached office building, Apple Valley Property. Overview.

Pic 7.6: Detached office building, Apple Valley Property. Interior.

- 19 -

ROI of Our Cannabis Portfolio, in Comparison to Our Peers

By the end of year 2024, we had invested $1.0 million into our cannabis portfolio. Since April 2024 and for the rest of the year, we received $12,000 in net cash income from this portfolio each month, realizing an annualized cash-by-cash ROI is 14.4%.

At this moment, our non-cash investments in cannabis properties, in the form of Series B preferred shares issued for acquisition, have no impact on the ROI allocated to our common shareholders, because holders of the Series B preferred shares will not be allocated any profit or loss. In the future, these preferred shares may be eligible for conversion into common shares. The terms of conversion are designed to ensure that our expected net cash income from related cannabis properties will increase proportionally, so that ROI allocated to our common shareholders, after the conversion, will remain the same (For detailed information about the terms and conditions of Series B preferred shares, please refer to Exhibit 3.4 of this Offering Circular).

For the reason above, we believe cash-by-cash ROI can be used as an effective measurement of our total ROI allocated to common shareholders, as far as our cannabis portfolio is concerned.

Based on publicly available information, we believe that our cannabis portfolio ROI was significantly higher than industry average. For example, Players Club Capital stated in January 2025 that “Cap rates for (cannabis cultivation) properties typically range from 7-10%” (https://www.playersclub.capital/blog/cannabis-properties-offer-investors-higher-cap-rates).

We also believe that our ROI is higher than the ROI of similar portfolios held by any other public companies during the year 2024, based on our interpretation of their SEC filings. However, we may have misinterpreted their filings, and we strongly recommend investors to conduct their own research on this matter. Further, even if our portfolio did outperform our peers, there is no assurance that we will continue doing so.

Our Cannabis Investment Strategy

We believe we have developed an investment strategy which is distinguishable from those of most cannabis property investors, public or private. We believe our strategy has proven to be successful, and will continue to produce satisfying results, although there is no assurance of this.

| 1. | We invest when the cannabis industry is likely to be at a periodic low point |

Members of our management team has been following the development of legal cannabis industry from as early as 2013. Yet when our Company was founded in 2016, we decided that cannabis industry was in a “wild west” phase, and, despite the potential for higher gains, investors would be exposed to higher risk of uncertainty, which outweighed the benefits for smaller investors like us. In 2020, we observed that the industry was maturing. However, after further research, we determined that cannabis properties were overpriced in most regions and held back our investments. This action helped us dodge the sharp drop in cannabis property prices during 2021-22.

- 20 -

In the year 2023, we concluded that cannabis property prices had possibly reached their periodical low. Meanwhile, the industry reached a stage of maturity where the risk of uncertainty was more acceptable. We made our first investment in May 2023 and increased our investment in March 2025.

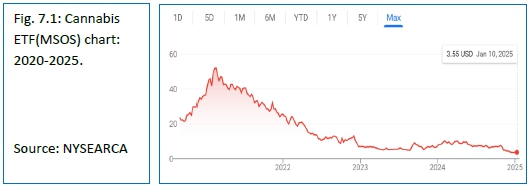

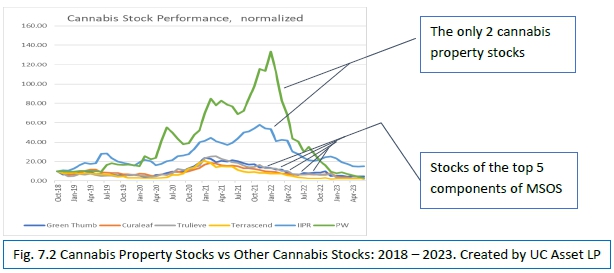

We believe our decision is in line with the real movements of the market, shown in the following charts. The first is Cannabis ETF(NYSE/ARCA: MSOS) chart since its formation until January 2025. After a fast climb to its peak at $51.94 in February 2021, MSOS has lost 93% of its value and is possibly at a periodic low point. The second chart shows that the stock of companies investing in cannabis properties have experienced a similar pattern, only with much larger volatility (than MSOS companies).

- 21 -

Assuming that stock performance correlates with valuation used in private deals, the above charts suggest that investing after 2023, whether on the stock market or on private transactions, presents lower entry points for investors, than investing at any time between 2020-2022.

We believe the next 12-18 months may present periodic low entry points to cannabis property investors.

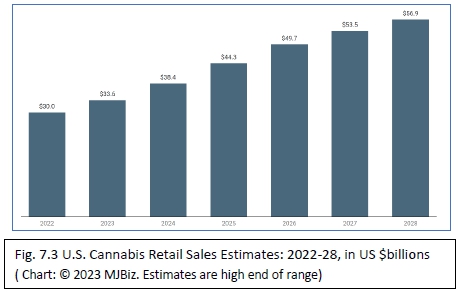

Cannabis is still a young industry with huge potential of growth. Combined U.S. medical and recreational cannabis sales could reach $33.6 billion by the end of 2023. Retail cannabis sales are projected to be upwards of $53.5 billion by 2027, according to an analysis conducted by MJBiz Factbook. (https://insights.mjbizdaily.com/factbook-2023/)

Meanwhile, cultivators are exiting the market at a rapid pace, significantly reducing market supply. Taking the State of Oklahoma (where our cannabis portfolio is based) as an example, the number of licenses for cannabis growers was about 10,000 by the end of 2021, and had dropped to around 3,000 by December 2024 (Source: Oklahoma Medical Marijuana Authority).

The combination of increasing market demand and decreasing market supply, in our opinion, may lead to an increase in cannabis product prices in the next 12-24 months, which may also result in an increase in the value of cannabis properties, however, there is no assurance of this.

Further, there are potential policy developments that may increase the value of cannabis properties. Among these the access to bank service for the cannabis industry may be the most promising. Please see the section “Trend Information” of Item 9 of this Offering Circular for more discussion on this matter.

| 2. | We invest in “premium” properties featuring advanced technologies |

We have observed that, in the earlier stage of US cannabis industry, when the profit margin of cannabis products was much higher, investors intended to build “low-tech” growing facilities, which required less capital and less time to complete, enabling investors to get their products to the market faster and cheaper. For investors who wanted to maximize their short-term returns, this appeared to be a reasonable strategy.

Typical “low-tech” cannabis cultivation facilities include: i) massive growing spaces converted from vacant factories or warehouses; ii) growing spaces converted from smaller spare spaces, such as used containers, used mobile houses, or basements in residential houses; iii) green-houses converted from conventional agricultural green-houses or built to the standard of conventional agricultural green-houses; iv) outdoor growing facilities with mobile tents, which are usually plastic; and iv) outdoor growing farmlands with almost no improvements.

- 22 -

The following collage shows some examples of these “low-tech” cannabis properties:

In contrast, we chose to invest in “premium” properties, i.e., cultivation facilities designed to achieve comprehensive control of environment, including light exposure, temperature, humidity, carbon dioxide level, irrigation, and fertilization. The environmental control is computerized and can be programmed to accommodate different cannabis strains for higher yields and better quality. “Premium” properties usually require higher initial investments per square foot to construct.