As filed with the Securities and Exchange Commission on December 29, 2017

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VICTORY COMMERCIAL MANAGEMENT INC.

(Exact name of registrant as specified in its charter)

| Nevada | 6510 | 37-1865646 | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

3rd Floor, 369 Lexington Ave,

New York, NY 10017

212-922-2199

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Registered Agent Inc.

769 Basque Way

Carson City, Nevada 89706

(775) 885-7800

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Arila Zhou, Esq.

Hunter Taubman Fischer & Li LLC

1450 Broadway 26th Floor

New York, New York 10018

(212) 530-2210

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer [ ] | Accelerated Filer [ ] |

Non-Accelerated Filer [ ] (Do not check if a smaller reporting company) |

Smaller reporting company [X] |

Emerging growth company [X]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided in Section 7(a)(2)(B) of the Securities Act. [ ]

CALCULATION OF REGISTRATION FEE

| Title

of Each Class of Securities to be Registered | Amount to be registered (1) | Proposed

maximum offering price per share (2) | Proposed

Maximum Aggregate Offering Price | Amount

of Registration Fee | ||||||||||||

| Common Stock, par value $0.0001 per share | 5,000,000 | $ | 1.00 | $ | 5,000,000 | $ | 622.50 | |||||||||

| Total | 5,000,000 | $ | 1.00 | $ | 5,000,000 | $ | 622.50 | |||||||||

| (1) | In addition, pursuant to Rule 416 under the Securities Act of 1933, this Registration Statement includes an indeterminate number of additional shares as may be issuable as a result of stock splits or stock dividends which occur during this continuous offering. |

| (2) | There is no current market for the securities. Although the registrant's common stock has a par value of $0.0001 per share, the registrant believes that the calculations offered pursuant to Rule 457(f)(2) are not applicable and, as such, the registrant has valued the common stock in good faith and for the purposes of the registration fee, based on $1.00 per share. In the event of a stock split, stock dividend or similar transaction involving our common stock, the number of shares registered shall automatically be increased to cover the additional shares of common stock issuable pursuant to Rule 416 under the Securities Act of 1933, as amended. |

| 2 |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION,

DATED December 29, 2017

Registration Statement No. 333-

VICTORY COMMERCIAL MANAGEMENT INC.

5,000,000 shares of Common Stock

This is the self-underwritten public offering of shares of common stock of Victory Commercial Management Inc., a Nevada corporation (the “Company” or “VCM”, “we”, “us”), par value $0.0001 per share (“Common Stock”). We may offer and sell (the “Offering”) from time to time up to 5,000,000 shares of our Common Stock (the “Shares”) at a fixed price of $1.00 per share (the “Offering Price”). There is no minimum number of Shares that must be sold by us for the offering to proceed, and we will retain the proceeds from the sale of any of the offered Shares.

There is presently no public market for our shares of Common Stock. We intend to apply to have our shares quoted on the OTC Bulletin Board, or OTCBB, promptly after the date of this prospectus. We cannot guarantee that our securities will be approved for quoting on OTCBB. We cannot assure you that our securities will continue to be quoted on OTCBB after this offering. We also intend to apply to have our shares listed on OTCQB market. However, we cannot guarantee that our shares will be approved for listing on OTCQB.

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012, and, as such, we have elected to take advantage of certain reduced reporting requirements for this prospectus and may elect to comply with certain reduced public company reporting requirements for future filings, as applicable.

The offering is being conducted on a self-underwritten, best efforts basis, which means our management and/or controlling shareholder will attempt to sell the Shares pursuant to this prospectus directly to the public, with no commission or other remuneration payable to them for any Shares they may sell. In offering the Shares on our behalf, management and/or controlling shareholder will rely on the safe harbor from broker-dealer registration set forth in Rule 3a4-1 under the Securities and Exchange Act of 1934, as amended (the “Exchange Act”). The Shares will be offered at a fixed price of $1.00 per share for a period of 180 days from the effective date of this prospectus. The Offering shall terminate on the earlier of (i) the date when we decide to do so until 180 days from the effective date of this prospectus, or (ii) when the Offering is fully subscribed for

| Offering Price Per Share | Underwriting Discounts and Commissions | Proceeds to Company Before Expenses | ||||||||

| Common Stock | $ | 1.00 | Not Applicable | $ | 5,000,000 | |||||

| Total | $ | 1.00 | Not Applicable | $ | 5,000,000 | |||||

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read this entire prospectus and any amendments or supplements carefully before you make your investment decision.

Investing in these shares of Common Stock involves significant risks. See “Risk Factors” beginning on page 11 of this prospectus.

These securities have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission nor has the Securities and Exchange Commission or any state securities commission passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this Prospectus is December 29, 2017

| 3 |

TABLE OF CONTENTS

We have not authorized any person to give you any supplemental information or to make any representations for us. You should not rely upon any information about us that is not contained in this prospectus or in one of our public reports filed with the Securities and Exchange Commission (“SEC”) and incorporated into this prospectus. Information contained in this prospectus or in our public reports may become stale. You should not assume that the information contained in this prospectus, any prospectus supplement or the documents incorporated by reference are accurate as of any date other than their respective dates, regardless of the time of delivery of this prospectus or of any sale of the shares. Our business, financial condition, results of operations and prospects may have changed since those dates. The selling stockholders are offering to sell, and seeking offers to buy, shares of our Common Stock only in jurisdictions where offers and sales are permitted.

The information in this preliminary prospectus is not complete and is subject to change. No person should rely on the information contained in this document for any purpose other than participating in our proposed offering, and only the preliminary prospectus issued on December 29, 2017, is authorized by us to be used in connection with our proposed offering. The preliminary prospectus will only be distributed by us and no other person has been authorized by us to use this document to offer or sell any of our securities.

| 4 |

This summary highlights selected information appearing elsewhere in this prospectus. While this summary highlights what we consider to be the most important information about us, you should carefully read this prospectus and the registration statement of which this prospectus is a part in its entirety before investing in our Common Stock, especially the risks of investing in our Common Stock, which we discuss later in “Risk Factors,” and our consolidated financial statements and related notes beginning on page 11 and F-1, respectively.

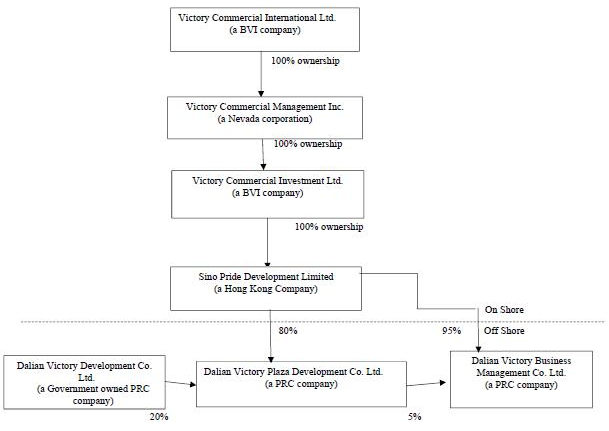

Unless the context requires otherwise, the words the “Company,” “VCM” “we,” “us” or “our” are references to the combined business of Victory Commercial Management Inc., a Nevada corporation. References to “China” or “PRC” are references to the People’s Republic of China, excluding Hong Kong Special Administrative Region of China, Macau Special Administrative Region of China and the Taiwan Region. References to “RMB” are to Renminbi, the legal currency of China, and all references to “$”, “USD” and dollar are to the U.S. dollar, the legal currency of the United States. References to “VCI” are to Victory Commercial Investment Ltd., our wholly-owned subsidiary formed under the laws of the British Virgin Islands. Reference to “Sino Pride” are to Sino Pride Development Limited., a company formed under the laws of Hong Kong and a wholly-owned subsidiary of VCI. References to “DVPD” are Dalian Victory Plaza Development Co., Ltd., an entity formed under the PRC laws and an 80%-owned subsidiary of Sino Pride. References to “DVBM” are Dalian Victory Business Management Co. Ltd., a corporation formed under the laws of the People’s Republic of China and 5% owned by DVPD and 95% owned by Sino Pride.

All market and industry data provided in this prospectus represents information that is generally available to the public and was not prepared for us for a fee. We did not fund nor were we otherwise affiliated with these sources and we are not attempting to incorporate the information on external web sites into this prospectus. We are only providing textual reference of the information of market and industry data and the web addresses provided in this prospectus are not intended to be hyperlinks and we do not assure that those external web sites will remain active and current.

This prospectus contains translations of RMB amounts and Hong Kong Dollar (“HK$”) amount into USD at specified rates solely for the convenience of the reader. The relevant exchange rates are listed below:

| For the years ended | ||||||||||||

| December 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

| Year Ended RMB: USD exchange rate | 6.9430 | 6.4920 | 6.2046 | |||||||||

| Year Average RMB: USD exchange rate | 6.9100 | 6.4890 | 6.3940 | |||||||||

| Year Ended HK$: USD exchange rate | 7.7534 | 7.7500 | 7.7531 | |||||||||

| Year Average HK$: USD exchange rate | 8.0730 | 8.0620 | 8.0650 | |||||||||

Special Note Regarding Forward-Looking Statements

This report contains forward-looking statements and information that are based on the beliefs of our management as well as assumptions made by and information currently available to us. Such statements should not be unduly relied upon. When used in this report, forward-looking statements include, but are not limited to, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan” and similar expressions, as well as statements regarding new and existing products, technologies and opportunities, statements regarding market and industry segment growth and demand and acceptance of new and existing products, any projections of sales, earnings, revenue, margins or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements regarding future economic conditions or performance, uncertainties related to conducting business in China, any statements of belief or intention, and any statements or assumptions underlying any of the foregoing. These statements reflect our current view concerning future events and are subject to risks, uncertainties and assumptions. There are important factors that could cause actual results to vary materially from those described in this report as anticipated, estimated or expected, including, but not limited to: competition in the industry in which we operate and the impact of such competition on pricing, revenues and margins, volatility in the securities market due to the general economic downturn; SEC regulations which affect trading in the securities of “penny stocks,” and other risks and uncertainties. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward- looking statements, even if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe harbor under the Private Securities Litigation Reform Act of 1995 may be available. Notwithstanding the above, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Exchange Act expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. Because we may from time to time be considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to us at certain times.

| 5 |

ITEM 3. SUMMARY INFORMATION, RISK FACTORS AND RATIO OF EARNINGS TO FIXED CHANGES.

Overview

We are a Nevada corporation that operates through our indirectly owned subsidiaries Dalian Victory Plaza Development Co., Ltd. (“DVPD”) and Dalian Victory Business Management Co., Ltd. (“DVBM”) and primarily engage in the business of commercial real estate lease and operation with a multi-functional underground shopping center (the “Victory Plaza”), currently scheduled to be renovated in Dalian, Liaoning Province of China.

We provide lease and day-to-day management operations of the Victory Plaza and aim at establishing a multi-functional shopping center, which differs from traditional retail shopping centers. Traditional retail centers typically have a few anchor tenants and rely on foot traffic. However, in recently years, due to the fast development of e-commerce and online shopping in China, particularly the fast expansion of Alibaba and Taobao, traditional retail centers become less attractive to customers. Thus, many traditional shopping centers encounter decreased revenue and financial difficulty due to this shift in consumer behavior and the financial distress of certain retailers. In order to stay competitive and adapt to the change of the market, we plan to renovate our underground Victory Plaza to attract tenants that we expect are more resilient to e-commerce alternatives by providing essential services in our premises, including but not limited to:

| ● | Health &wellness services, | |

| ● | Specialty retail, | |

| ● | Entertainment, beauty & other services, | |

| ● | Dining, and | |

| ● | Internet cafes. |

Our target tenants will engage in the local community and tend to have local residents and tourists that drive to the retail center and have an in-person individualized shopping and entertaining experience that is less likely to be replaced by e-commerce alternatives.

The Victory Plaza

DVPD was established in 1993 located at the core area of Qingniwa CBD in Dalian as a sino-foreign cooperative joint venture under the laws of PRC. The registered capital and additional paid in capital totaled $34,000,000 (RMB 249 million). Sino Pride holds 80% of its equity interest along with Dalian Victory Development Co., Ltd (20%). At the time of establishment, DVPD was one of the most leading underground shopping mall development operators in China and had won a lot of award and titles in the past.

DVPD developed and opened Victory Plaza in 1998. Victory Plaza is a multi-functional underground shopping center located in Dalian, a major city and seaport of Liaoning province of China. Dalian is a financial, shipping and logistics center for Northeast Asia with a population close to 6.7 million. Gifted with mild climate and multiple beaches, Dalian is a popular destination among domestic tourists and foreign visitors, especially from Japan, South Korea and Russia.

Total rental space is approximately 137,500 square meters (1,480,038 square feet). As of December 31, 2016, approximately 69%, or 94,502 square meters (1,017,211 square feet), of total rental space were sold to retailer; approximately 14%, or 18,828 square meters (202,663 square feet), of total rental space were sold to retailer with the option of purchase-back by the Company; approximately 17%, or 24,246 square meters (260,982 square feet), of total rental space are owned by the Company. As the date hereof, we have apparel retail shops (approximately 51%), 3C appliance shops (approximately 26%), catering shops (approximately 11%), entertainment (9%) and service related (3%) in Victory Plaza.

| 6 |

During the fiscal year 2016, we generated revenue of USD $3.9 million from rent income compared to revenue of USD$6.6 million form rent income during the fiscal year 2015. The decrease in rent income was primarily due to the negative impact of booming E-commerce online stores from 2012 to 2016 in China. Entrepreneurs and investors have less interest in retail store business in recent years. The direct impact to us was store vacancy rate increased. Our rented stores space was approximately 14,400 square meters (155,000 square feet) in December 2016, a decrease of 4,470 square meters (48,115 square feet), or 24%, compared to 18,870 square meters (203,115 square feet) in December 2015. Decreased occupancy rate driven down the unit rental price consequently. Average rental per square meter was $247 (RMB1,717) in December 2016, a decrease of $70 (RMB482), or 22%, compared to $317 (RMB2,199) in December 2015.

Management fee income for the year ended December 31, 2016 was $4.8 million, a decrease of $1.1 million, or 19%, compared to $5.9 million in the corresponding period in 2015. The decrease in management fee was primarily due to the decreased occupancy rate in Victory Plaza.

Renovation Plan

In order to attract customers and tenants that are more resilient to e-commerce alternatives, we have been working on the plan to renovate the Victory Plaza. Before we can commence the renovation, we have to apply for permits or approvals from local governments, such as construction works planning permits, approvals for fire protection design and construction works commencement permits. The rental space at Victory Plaza to be renovated will be approximately 113,800 square meters (1,224,933 square feet). According to our current renovation plan, we expect to complete the renovation by the second half of 2020 and reach the maximum profitability of the Victory Plaza by the end of 2021. As of the date hereof, we have finalized the plan of the renovation and are in the process of obtaining necessary permit and license to commence our first stage of the renovation, which we expect to occur in the next three months. The total anticipated cost of the renovation is RMB77,870,000 (approximately $11,215,600). We plan to fund the renovation through outside financing. However, there is no guarantee that we will not change our renovation plan or fulfill our plan if not changed, or obtain sufficient fund to carry out our renovation plan.

Implications of Our Being an “Emerging Growth Company”

Because we had less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An “emerging growth company” may take advantage of reduced reporting requirements that are otherwise generally applicable to public companies. In particular, as an emerging growth company, we:

| ● | may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations, or MD&A; | |

| ● | are not required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives, which is commonly referred to as “compensation discussion and analysis”; | |

| ● | are not required to obtain an attestation and report from our auditors on our management’s assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; | |

| ● | are not required to obtain a non-binding advisory vote from our shareholders on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay,” “say-on frequency” and “say-on-golden-parachute” votes); | |

| ● | are exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and CEO pay ratio disclosure; | |

| ● | are eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act; and | |

| ● | will not be required to conduct an evaluation of our internal control over financial reporting for two years. |

| 7 |

We intend to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under §107 of the JOBS Act.

Certain of these reduced reporting requirements and exemptions were already available to us due to the fact that we also qualify as a “smaller reporting company” under SEC rules. For instance, smaller reporting companies are not required to obtain an auditor attestation and report regarding management’s assessment of internal control over financial reporting, are not required to provide a compensation discussion and analysis, are not required to provide a pay-for-performance graph or CEO pay ratio disclosure, and may present only two years of audited financial statements and related MD&A disclosure.

EMPLOYEES

We currently have 331 employees including our executive officers. Among them, there are 5 senior managers holding collegial degrees or above with the average of more than 15 years’ experiences in different aspects of operation and management of large shopping centers. In addition, we have 44 department managers holding collegial degree or above with the average of more than 10 years’ experience in investment attraction, property management, project finance, HR and other areas.

CORPORATE INFORMATION

Our principal executive office is located at 3rd Floor, 369 Lexington Ave., New York, New York, 10017 and our telephone number is 212-922-2199. The information contained therein or connected thereto shall not be deemed to be incorporated into this prospectus or the registration statement of which it forms a part.

OFFERING SUMMARY

| Issuer: | Victory Commercial Management Inc. | |

| Securities being Offered: | up to 5,000,000 shares of Common Stock | |

| Price per Share: | ||

| Duration of the Offering: | Up to 180 days | |

| Shares Outstanding as of December 29, 2017 | 20,700,000 shares of Common Stock | |

| Shares Outstanding following the consummation of the Offering: | Up to 25,700,000 shares of Common Stock | |

| Amount of the Offering: | up to $5,000,000 | |

| Minimum purchase | Not applicable | |

| Symbol: | Not applicable | |

| Transfer Agent: | VStock Transfer, LLC 18 Lafayette Place Woodmere, New York 11598

|

| 8 |

| Use of Proceeds | We plan to devote the net proceeds of the offering for i) renovation of the Victory Plaza, ii) general working capital to meet the needs of the continued development and operation of the Victory Plaza; and (iii) other general working capital and corporate matters. See the “Use of Proceeds” section beginning on page 24. | |

| Risk Factors | The Common Stock offered hereby involves a high degree of risk and should not be purchased by investors who cannot afford the loss of their entire investment. See “Risk Factors” beginning on Page 11. | |

| Plan of Distribution | The shares of Common Stock covered by this prospectus may be sold by the selling stockholder in the manner described under “Plan of Distribution.” | |

| Dividend Policy: | We have no present plan to declare dividends and plan to retain our earnings to continue to grow our business. |

Summary Financial Information

The following summary financial data for the fiscal years ended December 31, 2016 and 2015. This information is only a summary and does not provide all of the information contained in our financial statements and related notes. You should read the “Management’s Discussion and Analysis of Financial Condition and Results of Operation” beginning on page 46 of this prospectus and our consolidated financial statements and related notes included elsewhere in this prospectus.

STATEMENT OF OPERATIONS DATA:

| For

the Years Ended December 31, | ||||||||

| 2016 | 2015 | |||||||

| Revenues | $ | 9,482,875 | $ | 13,378,699 | ||||

| Operating expenses | 16,000,768 | 18,951,506 | ||||||

| Loss from operations | (6,517,893 | ) | (5,572,807 | ) | ||||

| Other expenses | (4,638,309 | ) | (6,246,593 | ) | ||||

| Net loss | (11,156,202 | ) | (11,819,400 | ) | ||||

| Net loss attributable to noncontrolling interest | (2,338,888 | ) | (2,405,625 | ) | ||||

| Net loss attributable to the Company’s common shareholder | $ | (8,817,314 | ) | $ | (9,413,775 | ) | ||

| Loss per common share attributable to the Company’s common shareholder - basic and diluted: | $ | (0.43 | ) | $ | (0.45 | ) | ||

| Weighted-average shares outstanding, basic and diluted | 20,700,000 | 20,700,000 | ||||||

| 9 |

BALANCE SHEETS DATA:

| As of December 31, | ||||||||

| 2016 | 2015 | |||||||

| ASSETS | ||||||||

| Rental properties, net | $ | 24,459,300 | $ | 27,163,918 | ||||

| Cash and cash equivalents | 32,762 | 206,351 | ||||||

| Tenant and other receivables, net of allowance for doubtful accounts | 447,061 | 219,289 | ||||||

| Prepaid expenses and other assets | 1,125,734 | 312,427 | ||||||

| Property and equipment, net | 903,118 | 1,297,308 | ||||||

| Garage-sold in 2016, net | - | 10,315,868 | ||||||

| Intangible assets, net | 1,160 | 3,101 | ||||||

| ROU assets, net | 1,026,589 | 3,917,462 | ||||||

| TOTAL ASSETS | $ | 27,995,724 | $ | 43,435,724 | ||||

| LIABILITIES AND DEFICIT | ||||||||

| Liabilities | ||||||||

| Bank loans payable | $ | 61,513,950 | $ | 67,618,712 | ||||

| Property financing agreements payable | 68,592,614 | 77,856,030 | ||||||

| Accounts payable and accrued liabilities | 3,486,848 | 3,266,956 | ||||||

| Deferred rental income | 4,782,483 | 7,311,843 | ||||||

| Leases liability payable | 8,753,702 | 11,932,207 | ||||||

| Other payables | 16,987,414 | 10,890,719 | ||||||

| Loans payable to related party | 10,623,074 | 11,361,060 | ||||||

| Due to shareholder | 63,227,013 | 63,481,482 | ||||||

| Interest payable to related parties | 10,006,239 | 10,118,840 | ||||||

| Total Liabilities | 247,973,337 | 263,837,849 | ||||||

| Commitments and Contingencies | ||||||||

| Deficit | ||||||||

| Victory Commercial Management Inc. Shareholder’s Deficit | ||||||||

| Common stock, $0.0001 par value, 600,000,000 shares authorized; | - | - | ||||||

| 20,700,000 shares issued and outstanding* | 2,070 | 2,070 | ||||||

| Paid-in capital | 10,814,219 | 10,814,219 | ||||||

| Accumulated deficit | (188,034,199 | ) | (179,216,885 | ) | ||||

| Accumulated other comprehensive loss | (2,678,023 | ) | (11,826,787 | ) | ||||

| Total stockholder’s deficit attributable to the Company’s common shareholder | (179,895,933 | ) | (180,227,383 | ) | ||||

| Noncontrolling interest | (40,081,680 | ) | (40,174,742 | ) | ||||

| Total Deficit | (219,977,613 | ) | (220,402,125 | ) | ||||

| TOTAL LIABILITIES AND DEFICIT | $ | 27,995,724 | $ | 43,435,724 | ||||

| 10 |

An investment in our Common Stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this prospectus, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, the trading price of our shares of Common Stock, once we successfully list our Common Stock on OTCBB, could decline, and you may lose all or part of your investment. You should read the section entitled “Cautionary Note Regarding Forward Looking Statements” below for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this prospectus.

Risks Relating to Our Business

Our independent registered public accounting firm added an emphasis paragraph to its audit report describing an uncertainty related to our ability to continue as a going concern.

Due to our limited capital resources, our independent registered public accounting firm has issued a report that describes an uncertainty related to our ability to continue as a going concern. The auditors’ report discloses that we had net loss of $11,156,202 and $11,819,400 for the years ended December 31, 2016 and 2015, respectively; an accumulated deficit of $188,034,199 at December 31, 2016. As of November 30, 2017, to our knowledge, there were total of 453 litigations against us for unpaid rent from leaseback owners and for the past due of purchase-back property from current owners of properties. Total claims amounted $22,295,450 (RMB147,350,632). These conditions raise substantial doubt about our ability to continue as a going concern and may make it difficult for us to raise capital and make our securities an unattractive investment for potential investors. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty. We may be unable to continue operations if we cannot generate revenues in excess of our expenses.

Majority of our business, assets and operations are located in the People’s Republic of China.

The majority of our business, assets and operations are located in the People’s Republic of China. The economy of the PRC differs from the economies of most developed countries in many aspects. The economy of the PRC has been transitioning from a planned economy to a market-oriented economy. Although in recent years the PRC’s government has implemented measures emphasizing the utilization of market forces for economic reform, the reduction of state ownership of productive assets and the establishment of sound corporate governance in business enterprises, a substantial portion of productive assets in the PRC is still owned by the PRC’s government. In addition, the PRC’s government continues to play a significant role in regulating industry by imposing industrial policies. The PRC’s government exercises significant control over the PRC’s economic growth through the allocation of resources, controlling payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies. Some of these measures benefit the overall economy of the PRC, but may have a negative effect on us.

Actions of government or change of policies may adversely affect our business, financial condition and results of operations.

We are at risk from significant and rapid change in the legal systems, regulatory controls, and practices in areas in which we operate. These affect a wide range of areas including the real estate development approval system, employment practices, financing and sale of the buildings; our property rights; data protection; environment, health and safety issues; macro-economic policies and accounting, taxation and stock exchange regulation. Accordingly, changes to, or violation of, these systems, controls or practices could increase costs and have material and adverse impacts on the reputation, performance and financial condition of our development and operation.

We may not be able to obtain sufficient capital and may be forced to limit the scope of our operations.

We have sustained recurring losses and experienced negative cash flow from operations in recent years. As of December31, 2016 and 2015, we had generated cumulative losses of approximately $188,034,199 and $179,216,885, respectively; and we expect to continue to incur losses until completion of our renovation plan. We believe that our existing cash resources will not be sufficient to sustain operations during the next twelve months. We need to generate revenue and raise funding in order to sustain our operations and continue to implement our business plan. If adequate additional financing is not available on reasonable terms, we may not be able to undertake the renovation of our Victory Plaza or continue to develop and expand the services of our Victory Plaza, which may as a result impact our cash flow and we would have to modify our renovation plan accordingly. There is no assurance that additional financing will be available to us.

| 11 |

In connection with our growth strategies, we may experience increased capital needs and accordingly, we may not have sufficient capital to fund our future operations without additional capital investments. Our capital needs will depend on numerous factors, including (i) our profitability; (ii) the development of competitive projects undertaken by our competitors; and (iii) the level of our investment in operation and renovation. We cannot assure you that we will be able to obtain capital in the future to meet our needs.

If we cannot obtain additional funding, we may be required to: (i) modify our renovation plan, to the worst case, abandon the renovation plan; (ii) limit our operations and expansion; (iii) limit our marketing efforts; and (iv) decrease or eliminate capital expenditures. Such reductions could have a materially adverse effect on our business and our ability to compete the renovation.

Even if we do find a source of additional capital, we may not be able to negotiate terms and conditions for receiving such additional capital that are favorable to us. Any future capital investments could dilute or otherwise materially and adversely affect the holdings or rights of our existing shareholders. In addition, new equity or convertible debt securities issued by us to obtain financing could have rights, preferences and privileges senior to the Common Stock offered hereof. We cannot give you any assurances that any additional financing will be available to us, or if available, will be on terms favorable to us.

We derive the majority of our revenues from rental business in the PRC and any downturn in the Chinese economy could have a material adverse effect on our business and financial condition.

The majority of our revenues are expected to be generated from rentals and management fee of our Victory Plaza in the PRC and we anticipate that revenues from such rentals and management fee will continue to represent the substantial portion of our total revenues in the near future. Our revenues can also be affected by changes in the general economy. Our success is influenced by a number of economic factors which affect retail business and commercial real estate, such as employment levels, business conditions, interest rates and taxation rates. Adverse changes in these economic factors, among others, may restrict consumer spending, thereby negatively affecting our profitability.

We are subject to extensive government regulation that could cause us to incur significant liabilities or restrict our business activities.

Regulatory requirements could cause us to incur significant liabilities and operating expenses and could restrict our business activities. We are subject to statutes and rules regulating, among other things, property management, fire safety in public places, certain developmental matters, building and site design, and matters concerning the protection of health and the environment. Our operating expenses may be increased by governmental regulations, such as fees and taxes that may be imposed. Any delay or refusal from government agencies to grant us necessary licenses, permits, and approvals could have an adverse effect on our operations, particularly, our renovation.

We may be unable to compete effectively in the local shopping center and retail industry.

Dalian local retail industry is fragmented and intensely competitive. We compete with several reputable multifunctional local shopping centers on the basis of price, variety of services, perceived value, customer service, atmosphere, location and overall shopping experience. We also compete with other restaurants and retail establishments for qualified franchisees, site locations and employees to work in a shopping center.

Many of our competitors have significantly greater financial and other resources than we do. Many of our competitors also have greater influence over their respective retail systems than we do because of their significantly higher percentage of company-owned shopping centers and/or ownership of franchise real estate, giving them a greater ability to implement operational initiatives and business strategies. Some of our competitors are local shopping centers that, in some cases, have a loyal customer base and strong brand recognition because of its long history. As our competitors expand their operations and as new competitors enter the industry, we expect competition to be more intensive. Increased competition could result in price reductions, decreases in profitability and loss of market share by us. In the event we are unable to compete effectively against other local competitors, our business, financial condition and results of operations could be materially and adversely affected.

| 12 |

A majority of our leases will expire within one year, and we may be unable to renew these leases or find new tenants on a timely basis, or at all.

A majority of the lease agreements with our tenants have a term of one year. As a result, we experience lease cycles in which a significant number of tenancies expire each year. These relatively short lease cycles expose us to rental market fluctuations. We may not be able to renew the lease agreements or find new tenants at rates equal to or higher than those of the expiring leases, or to find replacement tenants in time so as to minimize periods between leases. If the rental price for our underground shopping center decreases, or our existing tenants do not renew their lease agreements, or we are unable to find replacement tenants in time after the expiration of existing tenancies, our business, financial condition, results of operations and prospects could be materially and adversely affected.

Defaulting on bank loans could have a material adverse effect on our results of operations

As of December 31, 2016, we had total of $62,022,901 outstanding loans payable to Harbin Bank. The collaterals with Harbin Bank contains certain protective contractual provisions that limit our activities in order to protect the lender. The risk of default may increase in the event of an economic downturn or due to our failure to successfully execute our business plan. We have entered into guarantee or security agreements with the banks in connection with the bank loans, pursuant to which we have guaranteed or provided security including property mortgage, pledge of accounts receivable (including property management fees and rentals) and 80% equity interest of DVPD held by Sino Pride was pledged for all liabilities under the bank loans, as applicable. Defaulting on our bank loans could result in loss of our collateralized assets and cause a material adverse effect on our results of operations.

Our operating companies must comply with environmental protection laws that could adversely affect our profitability.

We are required to comply with the environmental protection laws and regulations promulgated by the national and local governments of the PRC. Some of these regulations govern the level of fees payable to government entities providing environmental protection services and the prescribed standards relating to construction. During the renovation and daily operation of our Victory Plaza, wastes are unavoidably generated. If we fail to comply with any of the environmental laws and regulations of the PRC, depending on the type and severity of the violation, we may be subject to, among other things, warnings from relevant authorities, imposition of fines, specific performance and/or criminal liability, forfeiture of profits made, or an order to close down our business operations and suspension of relevant permits.

The operating histories of our operating companies may not serve as adequate bases to judge our future prospects and results of operations.

The operating histories of DVPD and DVBM may not provide a meaningful basis for evaluating our business as we plan to renovate the Victory Plaza into a multifunctional shopping plaza to attract more diversified group of customers. We cannot guarantee that we can achieve profitability or that we will have net profit in the future. We will encounter risks and difficulties that companies who substantially adjust or expand their business frequently experience, including the potential failure to:

| ● | Obtain sufficient working capital to support our operation and renovation; | |

| ● | Manage our expanding operations and continue to meet customers’ demands; | |

| ● | Maintain adequate control of our expenses allowing us to realize anticipated income growth; | |

| ● | Implement, adapt and modify our business strategies as needed; | |

| ● | Anticipate and adapt to changing conditions in the commercial real estate rental and management industry resulting from changes in government regulations, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics. |

If we are not successful in addressing any or all of the foregoing risks, our business may be materially and adversely affected.

Our failure to effectively manage growth may cause a disruption of our operations resulting in the failure to generate revenue at the levels we expect.

In order to maximize potential growth in our current and potential markets, we believe that we must be able to attract new renters and customers to use the services provided by our shopping center to ensure the sustainable development capability of the company and to maintain our operations. This strategy may place a significant strain on our management and our operational, accounting, and information systems. We expect that we will need to continue to improve our financial controls, operating procedures, and management information systems. We will also need to effectively train, motivate, and manage our employees. Our failure to effectively manage our operations could prevent us from generating the revenues we expect and therefore have a material adverse effect on the results of our operations.

| 13 |

We may need additional employees to meet our operational needs.

Our future success also depends upon our ability to attract and retain highly qualified personnel. We may need to hire additional managers and employees with industry experience from time to time, and our success will be highly dependent on our ability to attract and retain skilled management personnel and other employees. There can be no assurance that we will be able to attract or retain highly qualified personnel. Competition for skilled personnel in the commercial real estate industries is significant. This competition may make it more difficult and expensive to attract, hire and retain qualified managers and employees.

We will incur significant costs as a public company in the United States.

We will incur significant costs associated with our public company reporting requirements, costs associated with newly applicable corporate governance requirements, including requirements under the Sarbanes-Oxley act of 2002 and other rules implemented by the SEC. We expect all of these applicable rules and regulations to significantly increase our legal and financial compliance costs and to make some activities more time consuming and costly. We also expect that these applicable rules and regulations may make it more difficult and more expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract or retain qualified individuals to serve on our board of directors or as executive officers. We cannot predict or estimate the amount of additional costs we may incur or the timing of such costs.

Our certificates, permits, and licenses related to our operations are subject to governmental control and renewal, and failure to obtain or renew such certificates, permits, and licenses will cause all or part of our operations to be terminated.

Our operations require licenses, permits and, in some cases, renewals of these licenses and permits from various governmental authorities in the PRC. Our ability to obtain, maintain, or renew such licenses and permits on acceptable terms is subject to change, as are, among other things, the regulations and policies of applicable governmental authorities.

If our qualification certificate of property management enterprise or our land use rights certificates are revoked or suspended or we are unable to renew the permits for any reason, we cannot assure you that our business operations will not be stopped and, accordingly, our financial performance would be adversely affected.

Our shopping center may be affected by fire or natural calamities. Our operations are also subject to the risk of power outages, equipment failures or labor disturbances and other business interruptions. We have limited insurance coverage and do not carry any business interruption insurance.

Our Shopping Center is currently underground. A fire, floods or other natural calamity may result in significant damage to our shopping center. Our operations are subject to risks of various business interruptions, including power outages, equipment failures or disturbances from labor unrest. If we are unable to obtain timely replacements of damaged equipment, or if we are unable to find an acceptable contract manufacturer in the event our shopping center are damaged by a catastrophic event, then major disruptions to our production would result, which would have significant adverse effect on our operations and financial results. Our property insurance may not be sufficient to cover damages to our Shopping Center, and we do not carry any business interruption insurance covering lost profits as a result of the disruption to our production.

We are subject to certain risks related to litigation filed by or against us, and adverse results may harm our business and operation.

We are currently involved in, and may in the future be subject to, claims, suits, government investigations, and proceedings arising from our business. As of November 30, 2017, to our knowledge, there were total of 453 litigations against us for unpaid rent by the leaseback owners and for the past due of purchasing-back property from current owner of properties. Total claims amounted to $22,295,450 (RMB 147,350,632). Historically, when DVPD sold property, it granted a purchase-back option to certain purchasers pursuant to which, such purchasers could request DVPD to buy back their properties at the original purchase prices during certain time frame. DVPD also leased back certain sold units and then sub-lease to third parties. These litigations are caused by our failure to buy back the properties when requested to or our failure to pay rents for certain lease-back units. Subsequently, certain units owned by DVPD have been frozen from transfer or disposition by the courts. DVPD has been restricted from free transfer, deposition, pledge of its 5% equity interest in DVBM during a period from March 2, 2017 to March 1, 2019. In addition, DVPD has been listed as a “dishonest debtor” by the courts. Once listed as a dishonest debtor, DVPD may been imposed with certain restrictions in connection with the commercial loans at banks’ discretion; purchase or transfer of properties and land use rights; and renovation, upgrade or renovation of properties. In addition, the bank accounts of DVPD are frozen by the courts which allows the inflow of cash to the bank accounts but prohibits the outflow of cash. The management is negotiating with these claimers actively and willing to settle these cases with a discounted payment amount. However, we cannot predict with certainty the cost of defense, the cost of prosecution, or the ultimate outcome of litigation and other proceedings filed by or against us, including remedies, damage awards, and penalties. Regardless of outcome, any such claims or actions require significant time, money, managerial and other resources, result in negative publicity, and harm our business and financial condition. See Historical Issue on page 35.

| 14 |

RISKS RELATING TO DOING BUSINESS IN CHINA

Labor laws in the PRC may adversely affect our results of operations.

On June 29, 2007, the PRC’s government promulgated the labor contract law of the PRC, which became effective on January 1, 2008 and was subsequently amended on December 28, 2012. The labor contract law imposes greater liabilities on employers and significantly affects the cost of an employer’s decision to reduce its workforce. Further, the law requires certain terminations be based upon seniority and not merit. In the event that we decide to significantly change or decrease our workforce, the labor contract law could adversely affect our ability to enact such changes in a manner that is most advantageous to our business or in a timely and cost-effective manner, thus materially and adversely affecting our financial condition and results of operations.

We may be exposed to liabilities under the foreign corrupt practices act and Chinese anti-corruption law.

In connection with this offering, we will become subject to the U.S. foreign corrupt practices act (“FCPA”), and other laws that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. persons and issuers as defined by the statute for the purpose of obtaining or retaining business. We are also subject to Chinese anti-corruption laws, which strictly prohibit the payment of bribes to government officials. We have operations, agreements with third parties, and make sales in China, which may experience corruption. Our activities in China create the risk of unauthorized payments or offers of payments by one of the employees, consultants of our company, because these parties are not always subject to our control. We are in the process of implementing an anticorruption program, which will prohibit the offering or giving of anything of value to governmental officials or third parties, directly or indirectly, for the purpose of obtaining or retaining business. In the meantime, we believe to date we have complied in all material respects with the provisions of the FCPA and Chinese anti-corruption laws. However, our existing safeguards and any future improvements may prove to be less than effective, and the employees, consultants of our company may engage in conduct for which we might be held responsible. Violations of the FCPA or Chinese anti-corruption laws may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results and financial condition. In addition, the government may seek to hold our company liable for successor liability FCPA violations committed by companies in which we invest or that we acquire.

The government in China has the right to take over part or all of our underground properties during times of war.

Among the approximately 137,500 square meters (1,480,038 square feet) of the total rental area of Victory Plaza, approximately 59,000 square meters (635,071 square feet) was designed for underground civil air defense shelter (the “Civil Air Defense Shelter”). The Civil Air Defense Shelter is allowed to be used for shopping place or garage during peace time as set forth in approvals by local air defense authority. However, the primary use of any civil air defense shelter is to protect civilians during times of war. In order to serve this purpose, the PRC government authorities, by law and regulation, reserve the right to take over the Civil Air Defense Shelter during times of war. If any military conflict or a war breaks out between China and other countries or regions, it is likely that the Civil Air Defense Shelter or other part of our underground Victory Plaza will be seized by the government in China as underground civil air defense shelters. Although the seizure of civil air defense shelters by the government authorities in China for use during times of war does not mean the government authorities permanently revoke our right to use, operate and profit from the facilities and we may continue the use and operation of our the Civil Air Defense Shelter after the war, our business would still be interrupted.

Uncertainties with respect to the PRC’s legal system could adversely affect us.

We conduct a substantial amount of our business through our subsidiaries in China. Our operations in China are governed by PRC laws and regulations. Our PRC subsidiaries are generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws and regulations applicable to the operative joint venture enterprises. The PRC legal system is based on statutes. Prior court decisions may be cited for reference but have limited precedential value.

| 15 |

Since 1979, PRC legislation and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, China has not developed a fully integrated legal system and recently enacted laws and regulations may not sufficiently cover all aspects of economic activities in China. In particular, because some of these laws and regulations are relatively new, and because of the limited volume of published decisions and their nonbinding nature, the interpretation and enforcement of these laws and regulations involve uncertainties. In addition, the PRC legal system is based in part on government policies and internal rules (some of which are not published on a timely basis or at all) that may have a retroactive effect. As a result, we may not be aware of our violation of these policies and rules until sometime after the violation. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention.

We are a holding company and we rely on funding for dividend payments from our subsidiaries, which are subject to restrictions under PRC laws.

We are a holding company incorporated in Nevada and we operate our core businesses through our subsidiaries in the PRC. Therefore, the availability of funds for us to pay dividends to our shareholders and to service our indebtedness depends upon dividends received from such PRC subsidiaries. The ability of our subsidiaries to pay dividends and make payments on intercompany loans or advances to their shareholders is subject to, among other things, distributable earnings, cash flow conditions, restrictions contained in the articles of association of our subsidiaries, joint-venture contracts, applicable laws and restrictions contained in the debt instruments of such subsidiaries. If our subsidiary incurs debt or losses, its ability to pay dividends or other distributions to us may be impaired. As a result, our ability to pay dividends and to repay our indebtedness will be restricted. PRC laws require that dividends be paid only out of the after-tax profit of our PRC subsidiary calculated according to PRC accounting principles, which differ in many aspects from generally accepted accounting principles in other jurisdictions. PRC laws also require enterprises established in the PRC to set aside part of their after-tax profits as statutory reserves. These statutory reserves are not available for distribution as cash dividends. In addition, restrictive covenants in bank credit facilities or other agreements that we or our subsidiary entered into or may enter into in the future may also restrict the ability of our subsidiaries to pay dividends to us. Further, starting from January 1, 2008, dividends paid by our PRC subsidiaries to their non-PRC parent companies will be subject to a 10% withholding tax, unless there is a tax treaty between the PRC and the jurisdiction in which the overseas parent company is incorporated, which specifically exempts or reduces such withholding tax. Pursuant to a double tax treaty between Hong Kong and the PRC, if the non-PRC parent company is a Hong Kong resident and directly holds a 25% or more interest in the PRC enterprise, such withholding tax rate may be lowered to 5%. These restrictions on the availability of our funding may impact our ability to pay dividends to our shareholders and to service our indebtedness.

In addition, the PRC government imposes controls on the convertibility of the renminbi, or “RMB” into foreign currencies and, in certain cases, the remittance of currency out of China. Shortages in the availability of foreign currency may restrict the ability of our PRC subsidiary to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from trade-related transactions can be made in foreign currencies without prior approval from State Administration of Foreign Exchange (“SAFE”) by complying with certain procedural requirements. However, approval from appropriate government authorities is required where RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may also, at its discretion, restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay dividends in foreign currencies to our security-holders.

Our business may be materially and adversely affected if any of our PRC subsidiaries declares bankruptcy or becomes subject to a dissolution or liquidation proceeding.

The enterprise bankruptcy law of the PRC, or the bankruptcy law, came into effect on June 1, 2007. The bankruptcy law provides that an enterprise will be liquidated if the enterprise fails to settle its debts as and when they fall due and if the enterprise’s assets are, or are demonstrably, insufficient to clear such debts.

Our PRC subsidiaries hold assets that are important to our business operations. If our PRC subsidiaries undergo a voluntary or involuntary liquidation proceeding, unrelated third-party creditors may claim rights to some or all of these assets, thereby hindering our ability to operate our business, which could materially and adversely affect our business, financial condition and results of operations.

| 16 |

According to SAFE’s provisions for administration of foreign exchange relating to inbound direct investment by foreign investors, effective on June 10, 2015, if our PRC subsidiaries undergo a voluntary or involuntary liquidation proceeding, prior approval from the safe for remittance of foreign exchange to our shareholders abroad is no longer required, but we still need to conduct a registration process with the SAFE designated commercial bank. It is not clear whether “registration” is a mere formality or involves the kind of substantive review process undertaken by SAFE designated commercial bank.

Fluctuations in exchange rates could adversely affect our business and the value of our securities.

Changes in the value of the RMB against the U.S. dollar and other foreign currencies are affected by, among other things, changes in China’s political and economic conditions. Any significant revaluation of the RMB may have a material adverse effect on our revenues and financial condition, and the value of, and any dividends payable on our shares in U.S. dollar terms. For example, to the extent that we need to convert U.S. dollars we receive from our Offering into RMB for our operations, appreciation of the RMB against the U.S. dollar would have an adverse effect on the RMB amount we would receive from the conversion. Conversely, if we decide to convert our RMB into U.S. dollars for the purpose of paying dividends on our Common Stock or for other business purposes, appreciation of the U.S. dollar against the RMB would have a negative effect on the U.S. dollar amount available to us.

Since July 2005, the RMB is no longer pegged to the U.S. dollar. Although the people’s bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, the RMB may appreciate or depreciate significantly in value against the U.S. dollar in the medium to long term. Moreover, it is possible that in the future, PRC authorities may lift restrictions on fluctuations in the RMB exchange rate and lessen intervention in the foreign exchange market.

Very limited hedging transactions are available in China to reduce our exposure to exchange rate fluctuations. To date, we have not entered into any hedging transactions. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited, and we may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert RMB into foreign currencies.

It may be difficult to effect service of process and enforcement of legal judgments upon our Company and our officers and directors because they reside outside the United States.

Our operations are based in China and all of our assets are located in China. In addition, a majority of our directors and officers reside in China. As a result, service of process on the Company and such foreign directors and officers may be difficult or impossible to effect within the United States. Moreover, China does not have treaties with the United States or many other countries providing for the reciprocal recognition and enforcement of the judgment of courts. As a result, recognition and enforcement in China of judgments of a court in any of these jurisdictions may be difficult or impossible.

PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident shareholders to penalties and limit our ability to inject capital into our PRC subsidiaries, limit our PRC subsidiaries’ ability to distribute profits to us, or otherwise adversely affect us.

The SAFE promulgated the notice on relevant issues relating to domestic resident’s investment and financing and roundtrip investment through special purpose vehicles (“SPV(s)”), or Notice 37, in July 2014 that requires PRC residents or entities to register with SAFE or its local branch in connection with their establishment or control of an offshore entity established for the purpose of overseas investment or financing. In addition, such PRC residents or entities must update their safe registrations when the offshore SPV undergoes material events relating to material change of capitalization or structure of the PRC resident itself (such as capital increase, capital reduction, share transfer or exchange, merger or spin off).On February 28, 2015, SAFE issued a notice according to which the aforesaid PRC residents or entities are no longer required to register with SAFE or its local branch, instead the aforesaid PRC residents or entities need to register with local banks. Failure by an individual to comply with the required SAFE registration and updating requirements described above may result in penalties up to RMB50, 000 imposed on such individual and restrictions being imposed on the foreign exchange activities of the PRC subsidiaries of such offshore SPV, including increasing the registered capital of, payment of dividends and other distributions to, and receiving capital injections for the offshore SPV. Failure to comply with Notice 37 may also subject relevant PRC residents or the PRC subsidiaries of such offshore SPV to penalties under PRC foreign exchange administration regulations for evasion of applicable foreign exchange restrictions. Our controlling shareholder Alex Brown (a.k.a “You Chang”) did not register with local SAFE branch or its delegated commercial bank when he acquired ownership of Sino Pride through his indirect holding of Victory Commercial Investment Ltd. in November 2016. Although Alex Brown was no longer a PRC nationality afterwards, we cannot assure you that our controlling shareholder will not be required under Notice 37 to register with local SAFE branch or its delegated commercial bank. These risks could in the future have a material adverse effect on our business, financial condition and results of operations.

| 17 |

Failure to comply with the individual foreign exchange rules relating to the overseas direct investment or the engagement in the issuance or trading of securities overseas by our PRC resident stockholders may subject such stockholders to fines or other liabilities.

Other than Notice 37, our ability to conduct foreign exchange activities in the PRC may be subject to the interpretation and enforcement of the implementation rules of the administrative measures for individual foreign exchange promulgated by safe in January 2007 (as amended and supplemented, the “Individual Foreign Exchange Rules”). Under the individual foreign exchange rules, any PRC individual seeking to make a direct investment overseas or engage in the issuance or trading of negotiable securities or derivatives overseas must make the appropriate registrations in accordance with safe provisions. PRC individuals who fail to make such registrations may be subject to warnings, fines or other liabilities.

We may not be fully informed of the identities of all our beneficial owners who are PRC residents. For example, because the investment in or trading of our shares will happen in an overseas public or secondary market where shares are often held with brokers in brokerage accounts, it is unlikely that we will know the identity of all of our beneficial owners who are PRC residents. Furthermore, we have no control over any of our future beneficial owners and we cannot assure you that such PRC residents will be able to complete the necessary approval and registration procedures required by the individual foreign exchange rules.

It is uncertain how the individual foreign exchange rules will be interpreted or enforced and whether such interpretation or enforcement will affect our ability to conduct foreign exchange transactions. Because of this uncertainty, we cannot be sure whether the failure by any of our PRC resident stockholders to make the required registration will subject our PRC subsidiaries to fines or legal sanctions on their operations, delay or restriction on repatriation of proceeds of this offering into the PRC, restriction on remittance of dividends or other punitive actions that would have a material adverse effect on our business, results of operations and financial condition.

Because our funds are held in banks that do not provide insurance, the failure of any bank in which we deposit our funds may affect our ability to continue to operate.

Banks and other financial institutions in the PRC do not provide insurance for funds held on deposit. As a result, in the event of a bank failure, we may not have access to funds on deposit. Depending upon the amount of money we maintain in a bank that fails, our inability to have access to our cash may impair our operations, and, if we are not able to access funds to pay our employees and other creditors, we may be unable to continue to operate.

If we are unable to obtain business insurance in the PRC, we may not be protected from risks that are customarily covered by insurance in the United States.

Business insurance is not readily available in the PRC. To the extent that we suffer a loss of a type that would normally be covered by insurance in the United States, such as product liability and general liability insurance, we would incur significant expenses in both defending any action and in paying any claims that result from a settlement or judgment. We have not obtained fire, casualty and theft insurance, and there is no insurance coverage for our raw materials, goods and merchandise, furniture or buildings in China. Any losses incurred by us will have to be borne by us without any assistance, and we may not have sufficient capital to cover material damage to, or the loss of, our Victory Plaza due to fire, severe weather, flood or other causes, and such damage or loss may have a material adverse effect on our financial condition, business and prospects.

Under the new enterprise income tax law, we may be classified as a “resident enterprise” of China. Such classification may result in unfavorable tax consequences to us and our non-PRC shareholders.

China passed a new enterprise income tax law, or the new EIT law, which became effective on January 1, 2008. Under the new EIT law, an enterprise established outside of China with de facto management bodies within China is considered a resident enterprise, meaning that it can be treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. The implementing rules of the new EIT law define de facto management as “substantial and overall management and control over the production and operations, personnel, accounting, and properties” of the enterprise. In addition, a circular issued by the state administration of taxation on April 22, 2009 clarified that dividends and other income paid by such resident enterprises will be considered to be the PRC’s source income and subject to the PRC’s withholding tax. This recent circular also subjects such resident enterprises to various reporting requirements with the PRC’s tax authorities.

| 18 |

Although substantially all of our management is currently located in the PRC, it remains unclear whether the PRC’s tax authorities would require or permit our overseas registered entities to be treated as PRC resident enterprises. We do not currently consider our company to be a PRC resident enterprise. However, if the PRC’s tax authorities determine that we are a resident enterprise for the PRC’s enterprise income tax purposes, a number of unfavorable PRC tax consequences may follow. First, we may be subject to the enterprise income tax at a rate of 25% on our worldwide taxable income as well as the PRC’s enterprise income tax reporting obligations. This would also mean that income such as interest on offering proceeds and non-China source income would be subject to the PRC’s enterprise income tax at a rate of 25%. Second, although under the new EIT law and its implementing rules, dividends paid to us from our PRC subsidiary would qualify as tax-exempt income, we cannot guarantee that such dividends will not be subject to a 10% withholding tax, as the PRC authorities responsible for enforcing the withholding tax have not yet issued guidance with respect to the processing of outbound remittances to entities that are treated as resident enterprises for the PRC’s enterprise income tax purposes. Finally, dividends paid to stockholders with respect to their shares of our Common Stock or any gains realized from transfer of such shares may generally be subject to the PRC’s withholding taxes on such dividends or gains at a rate of 10% if the shareholders are deemed to be non-resident enterprises or at a rate of 20% if the shareholders are deemed to be non-resident individuals. In addition, any gain realized on the transfer of shares of our common stock by such investors is also subject to PRC tax at a current rate of 10%, subject to any reduction or exemption set forth in relevant tax treaties, if such gain is regarded as income derived from sources within the PRC. If dividends payable to our non-PRC investors or gains from the transfer of our common stock by such investors are subject to PRC tax, the value of your investment in our common stock may decline significantly.

We and our shareholders face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies.

Pursuant to a notice, or Circular 698, issued by the State Administration of Taxation, where a non-resident enterprise conducts an “indirect transfer” by transferring the equity interests of a PRC resident enterprise indirectly via disposing of the equity interests of an overseas holding company, and such overseas holding company is located in a tax jurisdiction that: (1) has an effective tax rate less than 12.5%; or (2) does not tax foreign income of its residents, the non-resident enterprise, being the transferor, shall report to the relevant tax authority of the PRC resident enterprise such indirect transfer. Using a “substance over form” principle, the PRC tax authority may disregard the existence of the overseas holding company if it lacks a reasonable commercial purpose and was established for the purpose of reducing, avoiding or deferring PRC tax. As a result, gains derived from such indirect transfer may be subject to PRC enterprise income tax, currently at a rate of 10%. In 2015, the State Administration of Taxation issued a circular, known as Circular 7, which replaced or supplemented certain previous rules under Circular 698. Circular 7 sets out a wider scope of indirect transfer of PRC assets that might be subject to PRC enterprise income tax, and more detailed guidelines on the circumstances when such indirect transfer is considered to lack a bona fide commercial purpose and thus regarded as avoiding PRC tax. The conditional reporting obligation of the non-PRC investor under Circular 698 is replaced by a voluntary reporting by the transferor, the transferee or the underlying PRC resident enterprise being transferred. Furthermore, if the indirect transfer is subject to PRC enterprise income tax, the transferee has an obligation to withhold tax from the sale proceeds, unless the transferor reports the transaction to the PRC tax authority under Circular 7. Late payment of applicable tax will subject the transferor to default interest. Gains derived from the sale of shares by investors through a public stock exchange are not subject to the PRC enterprise income tax pursuant to Circular 7 where such shares were acquired in a transaction through a public stock exchange. Circular 698 was abolished by an announcement promulgated by the State Administration of Taxation in October 2017 and effective from December 1, 2017, or SAT Circular 37, which, among others, provides specific provisions on matters concerning withholding of income tax of non-resident enterprises at source.