ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED MAY 31, 2020

AUGUST 21, 2020

SUITE 501, 543 GRANVILLE STREET

VANCOUVER, B.C. V6C 1X8

METALLA ROYALTY & STREAMING LTD.

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED MAY 31, 2020

TABLE OF CONTENTS

- i -

INTRODUCTORY NOTES

Cautionary Note Regarding Forward-Looking Statements

This annual information form ("AIF") contains "forward-looking information" or "forward-looking statements" (collectively, "forward-looking statements") within the meaning of applicable securities legislation. The forward-looking statements are provided as of the date of this AIF and Metalla Royalty & Streaming Ltd. ("Metalla" or the "Company") does not intend to and does not assume any obligation to update forward-looking information, except as required by applicable law. For this reason and the reasons set forth below, investors should not place undue reliance on forward-looking statements.

All statements included herein that address events or developments that we expect to occur in the future are forward-looking statements. Generally, forward-looking statements can be identified by the use of forward-looking terminology such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "does not anticipate", or "believes", or variations of such words and phrases or statements that certain actions, events or results "may", "could", "would", "might" or "will be taken", "occur" or "be achieved".

The forward-looking statements are based on reasonable assumptions that have been made by Metalla as at the date hereof and are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Metalla to be materially different from those expressed or implied by such forward-looking statements, including but not limited to:

• risks related to epidemics, pandemics or other public health crises, including the novel coronavirus ("COVID-19") global health pandemic, and the spread of other viruses or pathogens, and the potential impact thereof on Metalla's business, operations and financial condition;

• risks related to commodity price fluctuations;

• the absence of control over mining operations from which Metalla will purchase precious metals pursuant to gold streams, silver streams and other agreements (collectively, "Streams" and each individually a "Stream") or from which it will receive royalty payments pursuant to net smelter returns ("NSR Royalties"), gross overriding royalties ("GOR Royalties") and other royalty agreements or interests (collectively, "Royalties" and each individually a "Royalty") and risks related to those mining operations, including risks related to international operations, government and environmental regulation, delays in mine construction and operations, actual results of mining and current exploration activities, conclusions of economic evaluations and changes in project parameters as plans are refined;

• risks related to exchange rate fluctuations;

• that payments in respect of Streams and Royalties may be delayed or may never be made;

• risks related to Metalla's reliance on public disclosure and other information regarding the mines or projects underlying its Streams and Royalties;

• that some Royalties or Streams may be subject to confidentiality arrangements that limit or prohibit disclosure regarding those Royalties and Streams;

• business opportunities that become available to, or are pursued by Metalla;

• that Metalla's cash flow is dependent on the activities of others;

• that Metalla has had negative cash flow from operating activities;

• that some Royalty and Stream interests are subject to rights of other interest-holders;

• risks related to Metalla's sole material asset, the Santa Gertrudis Property (as defined below);

• risks related to global financial conditions;

• that Metalla is dependent on its key personnel;

• risks related to Metalla's financial controls;

• dividend policy and future payment of dividends;

• competition;

• risks related to the operators of the properties in which Metalla holds, or may acquire, a Royalty or Stream or other interest, including changes in the ownership and control of such operators;

• that Metalla's Royalties and Streams may have unknown defects;

• that Metalla's Royalties and Streams may be unenforceable;

• risks related to conflicts of interest of Metalla's directors and officers;

• that Metalla may not be able to obtain adequate financing in the future;

- 2 -

• litigation;

• risks related to Metalla's current credit facility and financing agreements;

• title, permit or license disputes related to interests on any of the properties in which Metalla holds, or may acquire, a Royalty, Stream or other interest;

• interpretation by government entities of tax laws or the implementation of new tax laws;

• credit and liquidity risk;

• risks related to Metalla's information systems and cyber security;

• risks posed by activist shareholders;

• that Metalla may suffer reputational damage in the ordinary course of business;

• risks related to acquiring, investing in or developing resource projects;

• risks applicable to owners and operators of properties in which Metalla holds an interest;

• exploration, development and operating risks;

• risks related to climate change;

• environmental risks;

• that exploration and development activities related to mine operations are subject to extensive laws and regulations;

• that the operation of a mine or project is subject to the receipt and maintenance of permits from governmental authorities;

• risks associated with the acquisition and maintenance of mining infrastructure;

• that Metalla's success is dependent on the efforts of operators' employees;

• risks related to mineral resource and mineral reserve estimates;

• that mining depletion may not be replaced by the discovery of new mineral reserves;

• that operators' mining operations are subject to risks that may not be able to be insured against;

• risks related to land title;

• risks related to international operations;

• risks related to operating in countries with developing economies;

• risks associated with the construction, development and expansion of mines and mining projects;

• risks associated with operating in areas that are presently, or were formerly, inhabited or used by indigenous peoples;

• that Metalla is required, in certain jurisdiction, to allow individuals from that jurisdiction to hold nominal interests in Metalla's subsidiaries in that jurisdiction;

• the volatility of the stock market;

• that existing securityholders may be diluted;

• risks related to Metalla's public disclosure obligations;

• risks associated with future sales or issuances of debt or equity securities;

• that there can be no assurance that an active trading market for Metalla's securities will be sustained;

• risks related to the enforcement of civil judgments against Metalla; and

• risks relating to Metalla potentially being a passive foreign investment company within the meaning of U.S. federal tax laws,

as well as those factors discussed under the heading "Risk Factors" in this AIF.

Forward-looking statements included in this AIF include statements regarding:

- the completion of the Fosterville Transaction and the Exploration Royalty Portfolio Transaction (as defined below);

- our plans and objectives;

- our future financial and operational performance;

- expectations regarding the Streams of Metalla;

- royalty payments to be paid to Metalla by property owners or operators of mining projects pursuant to each Royalty;

- the future outlook of Metalla and the mineral reserves and resource estimates for the Santa Gertrudis gold property (the "Santa Gertrudis Property") and other properties with respect to which the Company has or proposes to acquire an interest;

- future gold and silver prices;

- 3 -

- the date upon which owners and operators of properties in which Metalla holds, or may acquire, an interest who have had their operations affected by COVID-19 will restart operations or resume planned operations;

- other potential developments relating to, or achievements by, the counterparties for our Stream and Royalty agreements, and with respect to the mines and other properties in which we have, or may acquire, a Stream or Royalty interest;

- estimates of future production, costs and other financial or economic measures;

- prospective transactions, growth and achievements;

- financing and adequacy of capital; and

- future payment of dividends.

Estimates of mineral resources and mineral reserves are also forward-looking statements because they involve estimates of mineralization that will be encountered in the future, and projections regarding other matters that are uncertain, such as future costs and commodity prices.

Forward-looking statements are based on a number of material assumptions, which management of Metalla believe to be reasonable, including, but not limited to, that Metalla will complete the Fosterville Transaction and the Exploration Royalty Portfolio Transaction, that owners and operators of properties in which Metalla holds, or may acquire, an interest who have had their operations affected by COVID-19 will restart their operations on the timetables currently proposed by such persons, the continuation of mining operations from which Metalla will purchase precious or other metals or in respect of which Metalla will receive Royalty payments, that commodity prices will not experience a material decline, mining operations that underlie Streams or Royalties will operate in accordance with disclosed parameters and achieve their stated production outcomes and such other assumptions as may be set out herein.

Although Metalla has attempted to identify important factors that could cause actual actions, events or results to differ materially from those contained in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such forward-looking statements. Accordingly, readers should not place undue reliance on forward-looking statements. Investors and readers of this AIF should also carefully review the risk factors set out in this AIF under the heading "Risk Factors".

Technical and Third-Party Information and Cautionary Note for United States Readers

Except where otherwise stated, the disclosure in this AIF relating to properties and operations in which Metalla holds Royalty, Stream or other interests, including the disclosure in this AIF under the heading "Material Assets" is based on information publicly disclosed by the owners or operators of these properties and information/data available in the public domain as at the date hereof, and none of this information has been independently verified by Metalla. Specifically, as a Royalty or Stream holder, Metalla has limited, if any, access to properties on which it holds Royalties, Streams, or other interests in its asset portfolio. The Company may from time to time receive operating information from the owners and operators of the mining properties, which it is not permitted to disclose to the public. Metalla is dependent on, (i) the operators of the mining properties and their qualified persons to provide information to Metalla, or (ii) on publicly available information to prepare disclosure pertaining to properties and operations on the properties on which the Company holds Royalty, Stream or other interests, and may have limited or no ability to independently verify such information. Although the Company does not have any knowledge that such information may not be accurate, there can be no assurance that such third-party information is complete or accurate. Some reported public information in respect of a mining property may relate to a larger property area than the area covered by Metalla's Royalty, Stream or other interest. Metalla's Royalty, Stream or other interests may cover less than 100% of a specific mining property and may only apply to a portion of the publicly reported mineral reserves, mineral resources and or production from a mining property.

As at the date of this AIF the Company considers its Royalty and Stream interests in the Santa Gertrudis Property to be its only material mineral property for the purposes of National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101"). Information included in this AIF with respect to the Santa Gertrudis Property has been prepared in accordance with the exemption set forth in section 9.2 of NI 43-101.

- 4 -

Unless otherwise noted, the disclosure contained in this AIF of a scientific or technical nature for the Santa Gertrudis Property is based on the technical report entitled "Technical Report, Updated Resource Estimate And Preliminary Economic Assessment On The Santa Gertrudis Gold Property, Sonora State, Mexico Latitude 30o 38' N Longitude 110o 33' W" having an effective date of August 22, 2014 which technical report was prepared for GoGold Resources Inc. ("GoGold"), and filed under GoGold's SEDAR profile on www.sedar.com, and information that has been provided by GoGold and/or has been sourced from their news releases with respect to the Santa Gertrudis Property.

Unless otherwise indicated, all of the mineral reserves and mineral resources disclosed in this AIF have been prepared in accordance with NI 43-101. Canadian standards for public disclosure of scientific and technical information concerning mineral projects differ significantly from the requirements of the Industry Guide 7 ("Guide 7") adopted by the United States Securities and Exchange Commission (the "SEC") under the U.S. Securities Act of 1933, as amended. In particular, and without limiting the generality of the foregoing, the terms "Mineral Reserve", "Proven Mineral Reserve" and "Probable Mineral Reserve" are Canadian mining terms as defined in accordance with NI 43-101 and CIM Standards. These definitions differ from the definitions in Guide 7, and therefore may not qualify as reserves under Guide 7 standards. Under Guide 7 standards, a "final" or "bankable" feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. Under Guide 7 standards, mineralization may not be classified as a "reserve" unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made.

In addition, the terms "Mineral Resource", "Measured Mineral Resource", "Indicated Mineral Resource" and "Inferred Mineral Resource" are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC subject to Guide 7. Accordingly, resource information contained herein may not be comparable to similar information disclosed by U.S. companies under Guide 7. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves or that they can be mined economically or legally. "Inferred Mineral Resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Historical results or feasibility models presented herein are not guarantees or expectations of future performance. It cannot be assumed that all, or any part, of an inferred mineral resource will ever be upgraded to a higher category. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or that it can be economically or legally mined. Further, while NI 43-101 permits companies to disclose economic projections contained in pre-feasibility studies and preliminary economic assessments, which are not based on "reserves", U.S. companies have not historically been permitted to disclose economic projections for a mineral property in their SEC filings prior to the establishment of "reserves". Disclosure of "contained ounces" in a resource is permitted disclosure under Canadian reporting standards; however, Guide 7 normally only permits issuers to report mineralization that does not constitute "reserves" by Guide 7 standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this AIF contains descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements of Guide 7 under the United States federal securities laws and the rules and regulations thereunder.

Charles Beaudry, M.Sc., P.Geo. and géo. for Metalla and a "Qualified Person" under NI 43-101 has reviewed and approved the written scientific and technical disclosure contained in this AIF.

Currency Presentation

All dollar amounts referenced as "C$", "CAD" or "CAD$" are references to Canadian dollars, all references to "US$", "USD" or "USD$" are references to United States dollars, and all dollar amounts referenced as "AUD$" or "A$" are references to Australian dollars.

The following table sets out the high and low rates of exchange for one U.S. dollar expressed in Canadian dollars in effect at the end of each of the following periods, the average rate of exchange for those periods, and the rate of exchange in effect at the end of each of those periods, each based on the rate published by the Bank of Canada.

- 5 -

| Year Ended May 31 | ||||||

| 2020 | 2019 | |||||

| Rate at end of period | C$1.3787 | C$1.3527 | ||||

| Average rate during period | C$1.3407 | C$1.3224 | ||||

| High rate for period | C$1.4496 | C$1.3642 | ||||

| Low rate for period | C$1.2970 | C$1.2803 | ||||

CORPORATE STRUCTURE

Metalla was incorporated on May 11, 1983 pursuant to the Company Act (British Columbia) under the name Cactus West Explorations Ltd. The Company's name was changed to Cimarron Minerals Ltd. and its share capital was consolidated on a five (old) for one (new) basis, on April 29, 1996. On May 1, 2000, the Company's name was changed to DiscFactories Corporation, and its share capital was consolidated on a two (old) for one (new) basis and the Company was continued into the federal jurisdiction under the Canada Business Corporations Act. On February 20, 2007, the Company completed a change of business transaction pursuant to which it changed its name from DiscFactories Corporation to Excalibur Resources Ltd. On January 11, 2010, its share capital was consolidated on an eight (old) for one (new) basis. On December 1, 2016 it changed its name from Excalibur Resources Ltd. to Metalla, and completed a share consolidation on a three (old) for one (new) basis. On November 16, 2017, Metalla continued under the Business Corporations Act (British Columbia) ("BCBCA").

On December 17, 2019 (the "Effective Date"), Metalla completed a share consolidation (the "Share Consolidation") on a one Common Share (new) to four Common Shares (old) basis. Unless otherwise indicated in this AIF, all references to Common Shares, Common Share purchase warrants, stock options or RSUs issued prior to the Effective Date (collectively, the "Consolidated Securities"), including the exercise price and/or conversion prices in respect to any of the Consolidated Securities, have been adjusted to reflect this Share Consolidation. Please refer to "General Development of the Business - Current Business of Metalla - 3 Year History - Share Consolidation" for more information regarding the Share Consolidation.

The Company's head office is located at 501-543 Granville Street, Vancouver, British Columbia, V6C 1X8, Canada. The Company's registered and records office is located at Suite 2800, 666 Burrard Street, Vancouver, British Columbia, V6C 2Z7, Canada.

The Company is a reporting issuer in British Columbia, Alberta, Manitoba, Ontario, Nova Scotia, and Newfoundland. As at the date of this AIF, the Company’s common shares (the “Common Shares”) are listed on the TSX Venture Exchange (the “TSX‑V”) under the symbol “MTA”, on the NYSE American LLC (“NYSE”) under the symbol “MTA”, and on the Frankfurt Exchange under the Symbol “X9C”.

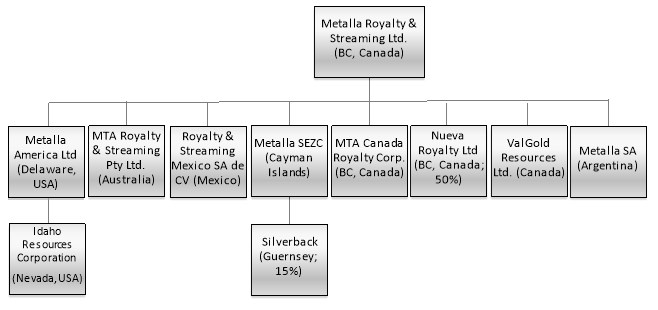

The Company has nine material subsidiaries: (i) MTA Canada Royalty Corp. which was incorporated under the laws of British Columbia; (ii) Valgold Resources Ltd. ("Valgold") which was incorporated under the laws of British Columbia; (iii) MTA Royalty & Streaming Pty Ltd. which was incorporated under the laws of Australia; (iv) Metalla S.A. which was incorporated under the laws of Argentina; (v) Royalty & Streaming Mexico, S.A. de C.V. which was incorporated under the laws of Mexico; (vi) Metalla SEZC which was incorporated under the laws of Cayman Islands; (vii) Metalla America Ltd. ("MTA America") which was incorporated under the laws of the State of Delaware; and (viii) Nueva Royalty Ltd. which was incorporated under the laws of British Columbia.

MTA America has one wholly owned subsidiary, Idaho Resources Corporation, which was incorporated under the laws of Nevada. Metalla SEZC has a 15% interest in Silverback Limited, a private Guernsey based company, which solely owns 100% of the New Luika Gold Mine silver Stream.

Inter-Corporate Relationships

The chart below illustrates the Company's material inter-corporate relationships as at the date hereof:

- 6 -

GENERAL DEVELOPMENT OF THE BUSINESS

Prior Business of Metalla

Prior to 2016, Metalla (operating as Excalibur Resources Ltd. at the time) was engaged in the business of exploration and development of mineral properties. Readers are referred to the public disclosure of Metalla and Excalibur Resources Ltd. for further information concerning the operations of Metalla prior to June 1, 2017.

Current Business of Metalla - 3 Year History

Acquisition of Royalty and Streaming Portfolio from Coeur

On July 31, 2017, Metalla purchased a portfolio of 3 Royalties and 1 Stream from Coeur Mining, Inc. (“Coeur”) in exchange for a total of 3,636,649 Common Shares and an unsecured convertible debenture in the principal amount of US$6,677,475.63 (the “Convertible Debenture”). The total consideration for the Royalty and Stream portfolio was US$13.0 million.

The Convertible Debenture included terms to automatically convert into Common Shares of Metalla at future financings or asset acquisitions to maintain Coeur's 19.9% interest until the outstanding principal was either converted in full or otherwise repaid. The Convertible Debenture was unsecured and bore interest at a rate of 5% per annum. The Convertible Debenture was fully converted on February 12, 2019.

The portfolio included the following:

• Endeavor Silver Stream - a silver Stream over the Endeavor Mine located in North‑central New South Wales, Australia and once the region’s largest zinc, lead and silver producer. Commissioned in 1983 as the Elura Mine, the site has been operated by CBH Resources Limited (“CBH Resources”) since 2003 at which time the site was renamed Endeavor. The Endeavor orebody is similar to others in the Cobar Basin in that it has the form of massive vertical pillars. Extraction of some 30 million tonnes of ore has occurred with remaining unextracted reserves. Metalla has the right to buy 100% of the silver production up to 20.0 million ounces (12.6 million ounces remaining under the contract) from the Endeavor Mine for an operating cost contribution of US$1.00 for each ounce of payable silver, indexed annually for inflation, plus a further increment of 50% of the silver price when the market price of silver exceeds US$7.00 per ounce.

- 7 -

• Joaquin Project - a 2.0% NSR Royalty on the Joaquin Property. The Joaquin Property was purchased by Pan American Silver Corp. ("Pan American") (NASDAQ:PAAS) for US$25 million in January 2017. The project is composed of seven contiguous claims, totaling 28,660 hectares. It is located in the Santa Cruz Province, Argentina, approximately 145 kilometers from Pan American's Manantial Espejo mine, where it is planned the Joaquin ore will be processed.

• Zaruma Gold Mine - a 1.5% NSR Royalty on the Zaruma Gold Mine which owned by Titan Minerals Ltd (ASX:TTM) and is located in the Zaruma-Portovelo Mining District of southern Ecuador, 3km north of the town of Zaruma. This district is a significant, high-grade goldfield, having produced over 5 million ounces of gold historically.

• Puchuldiza Project - a 1.5% NSR Royalty on the Puchuldiza Project in Chile. In May of 2019, due to a failure of Regulus Resources Inc. to maintain the mining concessions in good standing, Metalla acquired 9 mining concessions underlying the 1.5% NSR Royalty for C$100,000 and subsequently extinguished the 1.5% NSR Royalty. Metalla currently holds 5 of the concessions in good standing and allowed 4 of the concessions to lapse.

Please refer to “Secondary Bought Deal Offering of Coeur Common Shares” section below for more information regarding sale of Common Shares previously held by Coeur.

Akasaba West Royalty

On May 14, 2018, Metalla acquired a 2% NSR Royalty on the Akasaba West Property. The Akasaba West Property is a gold-copper deposit located in the Bourlamaque and Louvicourt Townships, Val d'Or, Quebec. The Akasaba West Property is owned and operated by Agnico Eagle Mines Limited ("Agnico") (NYSE:AEM). Agnico acquired the Akasaba West Property in 2014 and has continued previous permitting and development activities, with a view to commencing mining activities in 2020.

Agnico has the right to buy back 1% of the 2% NSR Royalty for US$7 million, and the Royalty will be payable after gold production has exceeded 210,000 ounces.

Completion of Arrangement with ValGold Resources Ltd. and acquisition of Garrison Royalty

On July 31, 2018, Metalla completed a plan of arrangement to acquire all outstanding common shares of ValGold which holds the Garrison Royalty and an exploration and evaluation project. Under the terms of the arrangement, shareholders of ValGold received 0.1667 Common Shares for each ValGold common share.

On the closing of this arrangement the following occurred:

• Metalla issued 2,414,993 Common Shares in exchange for common shares and in-the-money stock options of ValGold; and

• Outstanding Share purchase warrants of ValGold became exercisable to acquire up to 654,208 Common Shares at C$2.40 per Common Share, expiring October 6, 2019.

As a result of the acquisition of ValGold, Metalla acquired a 2% NSR Royalty on a significant portion of the Garrison Project previously 100% owned by Osisko Mining Inc. ("Osisko"), including the claims which were the subject of an NI 43-101 compliant resource estimate in 2014. The Garrison Project is situated directly on the prolific Destor-Porcupine Fault Zone, which is host to numerous gold mines. The Royalty covers the Garrcon, Jonpol, and eastern portion of the 903 deposit.

Osisko took over the Garrison Project in December 2015 when it acquired Northern Gold Mining Inc. and announced the start of a 20,000 metre drill program in July 2016. To-date, Osisko has drilled over 85,000 metres and made 12 announcements of drill results (the most recent on February 15, 2018) on all three main deposits on the Garrison Project and announced a mineral resource estimate for the Garrison Project on February 19, 2019.

- 8 -

On July 5, 2019, Osisko completed a plan of arrangement whereby the Garrison Project was transferred by spin out to O3 Mining Corporation.

Loan Agreements

On October 29, 2018, Metalla entered into three loan agreements with three arm’s length lenders (the “Three Lenders”) for aggregate principal amount of US$1,750,000 (the “Three Loans”). The proceeds from the Three Loans were used to pay, in part, the US$6 million cash portion of the acquisition price for the 2% NSR Royalty on the Santa Gertrudis Property (see sections titled Santa Gertrudis Royalty and Material Assets for further information). The terms of the Three Loans included interest at a rate of 5.0% per annum, calculated annually, and a term of twelve months. As an inducement for providing the Three Loans, Metalla agreed to provide the Three Lenders an origination discount of US$52,500, in total, and issue the Three Lenders an aggregate of 131,250 non-transferable Common Share purchase warrants (the “Loan Warrants”). Each Loan Warrant entitles the holder to acquire one Common Share at an exercise price of C$3.40 for a period of two years.

On December 5, 2018, Metalla entered into a fourth loan in the amount of US$250,000 with a arm’s length lender (the “Fourth Loan”). In connection with this increase, Metalla agreed to issue the arm’s length lender an aggregate of 18,750 non transferable Common Share purchase warrants (the “Broker Warrants”) with Broker Warrant entitling the holder to purchase one Common Share at an exercise price of C$3.40 for a period of two years.

On August 7, 2019, Metalla fully paid the amounts owing under the Three Loans and the Fourth Loan upon the initial drawdown of the Original Beedie Loan (see Establishment of the C$12,000,000 Convertible Loan Facility section below) and, as a result, no amounts remain outstanding under the Three Loans and the Fourth Loan.

Santa Gertrudis Royalty

In November 2017, GoGold sold the Santa Gertrudis Property to Agnico for US$80 million (C$105 million) in cash in and retained a 2% NSR Royalty. See Material Assets - Santa Gertrudis Property section for further information about the Santa Gertrudis Property including the mineral resource estimate in relation thereto.

On November 7, 2018, Metalla acquired the 2% NSR Royalty over the Santa Gertrudis Property located north of Hermosillo in Sonora, Mexico, for US$12 million, 1% of which can be bought back at any time for US$7.5 million. The Royalty was purchased from GoGold Resources Inc. (“GoGold”), the owner of the Royalty at the time of the transaction. Metalla paid US$6 million in cash and issued 2,530,769 Common Shares to GoGold for the Royalty.

COSE Royalty

On December 20, 2018, Metalla acquired a 1.5% NSR Royalty on certain mining rights located on the Cap‑Oeste Sur East property (“COSE”) located in the province of Santa Cruz, Argentina for a purchase price of US$1.5 million cash (partially funded by the Fourth Loan). Metalla also received a right of first refusal in favour of Metalla to acquire a future net smelter returns royalty that may be granted by, or received by, the seller (or an affiliate) on its Cap‑Oeste mine.

The COSE Property is a gold and silver project located in the province of Santa Cruz, Argentina that is 100% owned by Minera Triton Argentina S.A., a wholly-owned subsidiary of Pan American. The COSE Property is a fully-permitted mine that has been developed at a total cost of US$23.9 million, since Pan American acquired the property from Patagonia Gold for US$15 million in May 2017.

Completion of Private Placement

Metalla completed a private placement of 2,187,202 units at a price of C$3.12 per unit in two tranches on December 21, 2018 and January 4, 2019 for aggregate gross proceeds of C$6,824,070. Each unit consisted of one Common Share and one half of one Common Share purchase warrant (the "Private Placement Warrants"). Each Private Placement Warrant entitles the holder thereof to acquire one Common Share of the Company at a price of C$4.68 for a period of 24 months from the closing date of each tranche subject to acceleration (see Warrant Expiry Acceleration).

- 9 -

This offering was led by Haywood Securities Inc., on behalf of a syndicate of agents, including PI Financial Corp. and Canaccord Genuity Corp. The net proceeds from this private placement are being used to finance Royalty and Stream acquisitions and for general and working capital purposes.

Acquisition of Fifteen Mile Stream Royalty

On February 12, 2019, Metalla acquired a 1% NSR Royalty on Atlantic Gold Corporation's ("Atlantic Gold") Fifteen Mile Stream Project for US$4,000,000 pursuant to a royalty purchase agreement dated February 4, 2019 from a private vendor. The private vendor was paid US$2.2 million in cash and issued 654,750 Common Shares in consideration for the Royalty.

The Fifteen Mile Stream Project is a gold project located 57km northeast of Atlantic Gold's central milling facility at Touquoy and is readily accessible by highway. The Fifteen Mile Stream Project lies along the same geological trend as other related deposits - Touquoy, Beaver Dam and Cochrane Hill - and all are hosted within the same critical stratigraphy and structure, over a strike length of 80 km. The Royalty is in connection with two claims which cover the Egerton-Maclean, Hudson, 149 East Zone, and the majority of the Plenty deposit which collectively comprise the Fifteen Mile Stream Project located in Nova Scotia, Canada. The Royalty covers all products mined or otherwise recovered from the Fifteen Mile Stream Project.

On July 19, 2019, Atlantic Gold was acquired by St. Barbara Limited. ("St. Barbara"). On August 16, 2019, Metalla acquired an additional NSR Royalty in the Fifteen Mile Stream Project (see Additional Fifteen Mile Stream Royalty for more details).

Acquisition of Alamos Royalty Portfolio - First Closing

On April 1, 2019, Metalla entered into an asset purchase agreement with Alamos Gold Inc. (together with its affiliates, "Alamos") for the acquisition of a Royalty portfolio of up to 18 NSR Royalties or options to acquire NSR Royalties including, but not limited to, the following assets:

• El Realito Royalty - 2.0% NSR Royalty on the El Realito Property which is owned and operated by Agnico located adjacent to its operating La India Mine. El Realito is a satellite deposit located adjacent to Agnico’s operating La India Mine in Sonora, Mexico. Agnico can buy back 1.0% of the Royalty for US$4 million at any time and holds a 60‑day right of first refusal on the sale of the 2.0% Royalty.

• Wasamac Royalty - 1.5% NSR Royalty on the Wasamac Mine currently under development by Monarch Gold Corporation ("Monarch") located 15km west of Rouyn-Noranda in Quebec; Monarch has the right to buy back 0.5% of the NSR Royalty for a one-time payment of C$7.5 million at any time.

• La Fortuna Royalty Option - option to purchase a 1.0% NSR Royalty on the La Fortuna Mine currently under development by Minera Alamos Inc. located in Durango State, Mexico. Metalla has the option to purchase the 1% NSR Royalty from Alamos for US$0.6 million payable in cash or common shares at the option of Metalla for a period of two years.

• Beaufor Royalty - 1.0% NSR Royalty on the producing underground Beaufor Mine operated by Monarch, located 20km northeast of Val d’Or, Quebec, once Monarch has extracted 100,000 ounces of gold from the claims.

• San Luis Royalty - 1.0% NSR Royalty on the San Luis property owned by SSR Mining Inc. ("SSR") and located in the Ancash Department, central Peru.

The first closing occurred on April 17, 2019 and Metalla issued 2,054,752 Common Shares for the initial acquisition of 13 NSR Royalties and 2 options to purchase NSR Royalties. Certain Royalties in the portfolio were subject to rights of first refusal, consents, and future options at agreed to prices were to be acquired at a second or additional closings.

- 10 -

Beedie Convertible Loan Facility

On March 29, 2019, Metalla entered into a convertible loan facility (the "Original Beedie Loan") for up to C$12.0 million with Beedie Capital ("Beedie") to fund acquisitions of new Royalties and Streams. The Original Beedie Loan was funded by way of an initial advance of C$7.0 million within 90 days from closing of the Original Beedie Loan. The initial drawdown of C$7.0 million from the Original Beedie Loan occurred on August 7, 2019.

See Amendment, Conversion and Drawdown of Beedie Convertible Loan Facility below for further details about subsequent amendments, conversions and drawdowns under the Original Beedie Loan.

Alamos Royalty Portfolio - Second Closing

On June 20, 2019, Metalla entered into an amended and restated asset purchase agreement and completed a second closing for the purchase of the El Realito Royalty (which was subject to a 60 day right of first refusal by Agnico) and the Biricu Royalty. As consideration for the Biricu Royalty, Metalla issued 2,574 Common Shares.

Metalla also agreed to purchase from Alamos a 2.75% NSR Royalty on the Orion gold-silver project (that was not part of the existing Alamos Royalty portfolio) owned by Minera Frisco S.A.B. C.V. located in Nayarit, Mexico at a future third closing for 64,373 Common Shares.

Additional Fifteen Mile Stream Royalty

On August 16, 2019, Metalla acquired a 3.0% NSR Royalty on St. Barbara's Plenty deposit and Seloam Brook prospect, which forms part of St. Barbara's Fifteen Mile Stream Project, for C$2 million from a third-party in accordance with a purchase and sale agreement. As consideration for the transaction, Metalla made an upfront payment of C$0.5 million in cash, with an additional payment of up to C$1.5 million upon the exercise of the royalty payor's buy back right to purchase two-thirds of the 3.0% NSR Royalty for a period of five years.

Share Consolidation

Metalla completed a Share Consolidation on the basis of one new Common Share for every four Common Shares (1:4) effective as of the Effective Date, being December 17, 2020.

The Share Consolidation effected all securities of Metalla outstanding as of the Effective Date and, consequently, all Common Shares, Common Share purchase warrants, stock options and RSUs issued prior to the Effective Time, including the exercise price and/or conversion prices thereof, were adjusted on a 1:4 basis.

Listing on the NYSE

On January 8, 2020, Metalla commenced trading on the NYSE American LLC (the "NYSE") under the ticker symbol "MTA" and ceased trading on the over the counter venture market ("OTCQB").

Acquisition of NuevaUnion royalty portfolio

On February 18, 2020, Metalla, along with its joint venture partner Nova Royalty Corp. (formerly, BatteryOne Royalty Corp.) ("Nova" and, collectively with Metalla, the "Purchasers"), jointly acquired a 2.0% NSR Royalty on future gold production from a portion of the La Fortuna deposit and prospective exploration grounds forming part of the NuevaUnion project located in the Huasco Province in the Atacama region of Chile (collectively, the "NuevaUnion Project"). The NuevaUnion Project is jointly owned by Newmont Corporation ("Newmont") and Teck Resources Limited ("Teck"), and is one of the largest undeveloped copper-gold-molybenum projects in the world.

As consideration for the transaction, the Purchasers will pay a total of US$8 million to be satisfied in cash and common shares of the Purchasers. Metalla has agreed to pay 25% of the purchase price and Nova will pay 75% of the purchase price in proportion to the underlying commodity at the La Fortuna deposit. A total of US$3 million in cash was paid by the Purchasers on closing of the transaction and the balance of the purchase price is US$1 million in cash that is payable one year from the closing date along with an additional US$4 million that is payable equally in cash and common shares of the Purchasers upon the achievement of commercial production at the La Fortuna deposit (such common share price to be calculated based on a 10-day volume weighted average price as of the date prior to issuance or cash in certain circumstances) .

- 11 -

Under the joint venture arrangement, Metalla will be entitled to all payments under the NSR Royalty with respect to gold production and Nova will be entitled to all payments under the NSR Royalty with respect to copper production, and all other payments under the NSR Royalty will be split evenly between the Purchasers.

Filing of Base Shelf Prospectus and Prospectus Supplement

On May 1, 2020, Metalla filed a short form base shelf prospectus (the "Shelf Prospectus") with the securities regulatory authorities in each of the provinces of Canada and a corresponding registration statement on Form F-10 (the "Registration Statement") with the United States Securities and Exchange Commission under the Multijurisdictional Disclosure System established between Canada and the United States.

The Shelf Prospectus and the Registration Statement will enable the Company to make offerings of up to C$200 million of Common Shares, warrants, subscription receipts, units and share purchase contracts or a combination thereof of the Company from time to time, separately or together, in amounts, at prices and on terms to be determined based on market conditions at the time of the offering and as set out in an accompanying prospectus supplement, during the 25-month period that the Shelf Prospectus and Registration Statement remain effective.

On June 23, 2020, Metalla filed a prospectus supplement qualifying the distribution of 3,400,000 Common Shares (the "Offered Shares") to be sold by Coeur at a price of US$5.30 per Common Share by way of Secondary Offering (as defined below). See "Secondary Bought Deal Offering of Coeur Common Shares" for additional details regarding the Secondary Offering.

Acquisition of Idaho Resource Corporation

On May 22, 2020, Metalla acquired 100% of the issued and outstanding shares of Idaho Resources Corporation ("IRC"), a Nevada corporation, for an aggregate amount of US$4 million satisfied by the issuance of 357,121 Common Shares at a price of $7.88 per Common Share and US$2 million in cash.

IRC holds a 0.5% GOR Royalty on Nevada Gold Mine Corp.'s ("Nevada Gold") Anglo/Zeke claim block in Eureka County, Nevada, which is located on a trend to the southeast of the Cortez operations and Goldrush project owned by Nevada Gold. Nevada Gold is a joint venture between Barrick Gold Corporation ("Barrick") (61.5%) and Newmont (38.5%).

IRC also holds a 1.5% GOR Royalty covering NuLegacy Gold Corporation's ("NuLegacy") Red Hill project in Eureka County, Nevada, which is continuous to the southeast of the Anglo/Zeke claim block.

Subsequent Events to May 31, 2020

Acquisition of Wharf royalty

On June 30, 2020, Metalla acquired a 1.3875% NSR Royalty on the operating Wharf mine ("Wharf") owned by Coeur from various third-party sellers for a total purchase price of US$8.0 million. In conjunction with this transaction, Metalla agreed to sell a 0.3875% NSR Royalty to Coeur in consideration for the transfer of 421,554 Common Shares of Metalla held by Coeur, representing US$2.23 million in value based on a price of US$5.30 per Common Share.

As a result, Metalla acquired a net 1.0% royalty interest in the Wharf mine for a total consideration of US$5.77 million, consisting of US$1.0 million in cash and the issuance of 899,201 Common Shares.

- 12 -

Wharf has been in production since 1983 and is an open pit, heap leach operation located in the Northern Black Hills of South Dakota. Wharf was originally acquired by Coeur in February 2015 from Newmont Mining Corporation, formerly Goldcorp Inc. (“Newmont”) for cash consideration of approximately US$99.5 million.

Secondary Bought Deal Offering of Coeur Common Shares

On June 30, 2020, Metalla and Coeur completed a public offering of 3,910,000 Common Shares held by Coeur at a price of US$5.30 per Common Share for gross proceeds to Coeur of US$20,723,000 (the "Secondary Offering"), including 510,000 Common Shares offered as a result of the full exercise of the over-allotment option by the underwriters to the Secondary Offering.

The net proceeds of the Secondary Offering were paid directly to Coeur, and Metalla did not receive any proceeds from the Secondary Offering.

Prior to the completion of the Secondary Offering, Coeur owned 5,241,310 Common Shares, representing approximately 14.9% of the issued and outstanding Common Shares. Following the completion of the Secondary Offering and the repurchase by Coeur from Metalla of a 0.3875% royalty interest in Coeur's Wharf mine in exchange for 421,554 Common Shares previously held by Coeur (as described in the section “Acquisition of Wharf royalty” above), Coeur’s ownership of Metalla is now below reporting requirement thresholds for the purposes of applicable Canadian and U.S. securities laws.

Acquisition of Fosterville Royalty

On July 27, 2020, Metalla announced that it entered into a purchase and sale agreement with NuEnergy Gas Limited ("NuEnergy") to acquire an existing 2.5% NSR Royalty on the northern and southern portions of Kirkland Lake Gold Ltd.'s ("Kirkland Lake") operating Fosterville mine in Victoria, Australia (collectively, the "Fosterville Transaction").

In consideration for the 2.5% NSR Royalty, Metalla will pay NuEnergy A$2 million in cash and issue NuEnergy 467,730 Common Shares representing A$4 million in value based on the ten (10) trading day volume weighted average price of the Common Shares on the TSXV ("VWAP") on the date prior to announcing the transaction. The Fosterville Transaction is subject to customary closing conditions, including obtaining the requisite TSXV and NYSE approvals and Foreign Investment Review Board ("FIRB") approval, and is expected to close in October 2020.

Amendment, Conversion and Drawdown of Beedie Convertible Loan Facility

On July 29, 2020, Metalla announced that it had reached an agreement with Beedie to amend and restate the Original Beedie Loan (the "Amended and Restated Beedie Loan" and, collectively with the Original Beedie Loan, the "Beedie Loan Facility") pursuant to which (i) Beedie converted C$6.0 million of the outstanding C$7.0 million principal amount drawn under the Original Beedie Loan at a conversion price of C$5.56 per Common Share for a total of 1,079,136 Common Shares; (ii) the conversion price of the previously undrawn C$5.0 million tranche of the Original Beedie Loan was increased from C$5.56 to C$9.90 per Common Share; and (iii) the aggregate amount available under the Beedie Loan Facility was increased by an additional C$20 million. The second drawdown of $5.0 million pursuant to the Amended and Restated Beedie Loan occurred on August 6, 2020 at a conversion price of C$9.90 per Common Share.

The principal amount of the remaining C$1.0 million outstanding under the Original Beedie Loan (the "Initial Advance") will be convertible, at any time, at the option of Beedie, into Common Shares at a conversion price of C$5.56 per Common Share (the "Initial Advance Conversion Price"), representing a 25% premium to the 30-day VWAP per Common Share as of March 15, 2019. The principal amount of the $5.0 million drawdown under the Amended and Restated Beedie Loan (the "Second Advance") will be convertible at any time at the option of Beedie into Common Shares at a conversion price of C$9.90 per Common Share (the "Second Advance Conversion Price"), representing a 27% premium to the 30-day VWAP per Common Share as of July 28, 2020. Any future advances from the additional $20.0 million made available by Beedie will require a minimum drawdown of $2.5 million by Metalla with a conversion price based on a 20% premium to the 30-day VWAP of the Common Shares on the date of such advance.

- 13 -

Metalla may also elect to convert any or all of the principal amount outstanding on the Initial Advance and Second Advance if, for a period of thirty consecutive trading days on the TSXV, the 30-day VWAP of the Common Shares at the close of trading on such trading day equals or exceeds a 50% premium to the Initial Advance Conversion Price or the Second Advance Conversion Price.

The Beedie Loan Facility carries an interest rate of 8.0% on advanced funds and 1.5% on standby funds with principal repayment due on April 22, 2023. The Beedie Loan Facility is secured by certain assets of Metalla and can be repaid with no penalty at any time after the 12-month anniversary of each advance.

Warrant Expiry Acceleration

On August 6, 2020, Metalla announced that, in accordance with the terms of the Acceleration Warrants (as defined herein), it is electing to accelerate the expiry of certain outstanding Common Share purchase warrants of Metalla exercisable at $4.68 per Common Share and broker warrants exercisable at $3.12 per Common Share (collectively, the "Acceleration Warrants"). The Acceleration Warrants were issued pursuant to a brokered private placement of the Company that closed in two tranches on December 21, 2018 and January 4, 2019.

If all of the outstanding Acceleration Warrants are exercised, gross proceeds payable to Metalla will total approximately $2,342,870. The proceeds from the exercise of the Acceleration Warrants will be primarily used by the Company to continue to execute on its growth strategy, as well as for general corporate and working capital purposes.

Other Royalties

On August 18, 2020, Metalla entered into a purchase agreement to acquire up to four exploration-stage NSR Royalties in Australia (the "Exploration Royalty Portfolio Transaction") for cash consideration of $1.0 million. The Royalties are subject to a right of first refusal by each royalty payor and closing of the Exploration Royalty Portfolio Transaction is subject to customary closing conditions, including FIRB approval.

For a list of Royalty interests held by Metalla and not described above, see the chart below under the section Description of Business - Principal Product.

COVID-19

Metalla continues to monitor and assess the impacts of COVID-19 on its employees and business. At this time, all employees continue to work remotely. Metalla is closely monitoring the unpredictable impact of the COVID-19 pandemic on its portfolio of assets. On March 23, 2020, Pan American announced operations at its COSE and Joaquin mines in Argentina had been temporarily suspended in response to the COVID-19 pandemic; however on June 1, 2020, Pan American announced that underground mining at the Joaquin mine had resumed on May 2, 2020 and high-grade stockpiled ore was being hauled to the Manantial Espejo plant for processing, development work preparing the underground mine at COSE had resumed on May 4, 2020, and that Pan American expected to begin mining and hauling ore from COSE to the Manantial Espejo plant in the third quarter of 2020.

On March 30, 2020, the Mexican General Health Council declared a national health emergency and, on March 31, 2020, the Federal Health Ministry of Mexico issued extraordinary measures due to COVID-19 which resulted in the suspension of operations on the properties underlying the Santa Gertrudis and El Realito royalty assets held by Metalla. As part of the phased re-start of economic activities in Mexico, the Government of Mexico declared mining an essential industry on May 13, 2020 and also permitted the gradual re-start of mining operations beginning on May 18, 2020, in municipalities where there are no COVID-19 cases and which do not border municipalities with COVID-19 cases. Agnico has disclosed that exploration drilling resumed at the Santa Gertrudis Property on May 30, 2020 and that exploration drilling at El Realito has resumed as well.

- 14 -

DESCRIPTION OF THE BUSINESS

Metalla is a publicly traded precious metals royalty and streaming company listed on the TSX-V, NYSE and Frankfurt Exchange. Metalla's business model is focused on managing and growing its portfolio of Royalties and Streams. Metalla's long-term goal is to provide its shareholders with a model which provides:

- exposure to precious metals price optionality;

- a perpetual discovery option over large areas of geologically prospective lands which it acquires at no additional cost other than the initial investment;

- limited exposure to many of the risks associated with operating companies;

- free cash-flow and limited cash calls;

- high margins that can generate cash through the entire commodity cycle;

- diversity that is scalable, in which a large number of assets can be managed with a small stable overhead; and

- management focus on forward-looking growth opportunities rather than operational or development issues.

A royalty is a non-dilutive asset level perpetual interest in an underlying mineral project that, when in production, provides topline cash relative to the percentage of the royalty. Depending on the nature of a royalty interest, the laws applicable to it and the specific project, the royalty holder is generally not responsible for, and has no obligation to contribute to operating or capital costs or environmental liabilities. An NSR Royalty is generally based on the value of production or net proceeds received by an operator from a smelter or refinery for the minerals sold. These proceeds are usually subject to deductions or charges for transportation, insurance, smelting and refining costs as set out in the agreement governing the terms of the royalty.

Principal Product

In the past four years, Metalla has deployed over C$96 million, comprised of cash consideration, Common Shares, and other equity related structures issued to sellers, across 18 transactions amassing a portfolio of 50 Royalties and Streams. Metalla's portfolio provides exposure to established counterparties, including Agnico, Pan American, CBH, SSR, St. Barbara, Newmont, Teck, Barrick and many more.

The principal products of Metalla are: (i) precious metals that it has agreed to purchase pursuant to Stream agreements that it has entered into with mining companies; and (ii) Royalty payments pursuant to Royalty agreements acquired by Metalla or entered into with mining companies. Metalla is focused on precious metal streams and royalties for gold and silver.

The Company's sole material asset is its Royalty interest in the Santa Gertrudis Property.

The following table summarizes the Royalty and Stream interests that are owned by Metalla or are under contract to be acquired:

|

|

Property |

Operator |

Location |

Stage |

Metal(1) |

Terms |

|

1. |

Santa Gertrudis |

Agnico |

Sonora, Mexico |

Development |

Au |

2% NSR Royalty |

|

2. |

Wharf |

Coeur |

South Dakota |

Production |

Au |

1.0% Net Royalty |

|

3. |

Fosterville |

Kirkland Lake Gold |

Australia |

Production |

Au |

2.5% NSR Royalty(3) |

- 15 -

|

|

Property |

Operator |

Location |

Stage |

Metal(1) |

Terms |

|

4. |

Joaquin Mine |

Pan American |

Santa Cruz, Argentina |

Production |

Ag, Au |

2% NSR Royalty |

|

5. |

COSE Mine |

Pan American |

Santa Cruz, Argentina |

Production |

Ag, Au |

1.5% NSR Royalty |

|

6. |

New Luika |

Shanta Gold |

Lupa Goldfields, Tanzania |

Production |

Au |

Stream on 15% of Ag |

|

7. |

Endeavor Mine |

CBH Resources |

NSW Australia |

Care and Maintenance |

Zn, Pb, Ag |

Stream on 100% of Ag |

|

8. |

Fifteen Mile Stream (Hudson, Egerton-Maclean, 149 East Zone, Plenty deposit) |

St Barbara |

Nova Scotia |

Development |

Au |

1% NSR Royalty |

|

9. |

Fifteen Mile Stream (Plenty deposit and Seloam Brook prospect) |

St Barbara |

Nova Scotia |

Development |

Au |

3% NSR Royalty

|

|

10. |

NuevaUnion |

Newmont and Teck |

Chile |

Development |

Au, Cu, Mo |

2.0% NSR Royalty(4) |

|

11. |

Garrison Mine |

O3 Mining Corporation |

Kirkland Lake, ON |

Development |

Au |

2% NSR Royalty |

|

12. |

Hoyle Pond Extension |

Newmont Mining |

Timmins, Canada |

Development |

Au |

2% NSR, subject to 500Koz exemption |

|

13. |

Zaruma |

Titan Minerals |

Ecuador |

Development |

Au |

1.5% NSR Royalty |

|

14. |

Timmins West Extension |

Pan American Silver |

Timmins, Canada |

Development |

Au |

1.5% NSR Royalty (subject to a 0.75% buy back) |

|

15. |

Akasaba West |

Agnico Eagle |

Val d'Or, Canada |

Development |

Au, Cu |

2% NSR Royalty, payable after 210Koz Au (subject to a 1.0% buy back) |

- 16 -

|

|

Property |

Operator |

Location |

Stage |

Metal(1) |

Terms |

|

16. |

Aureus East Mine (Previously Dufferin) |

Aurelius Minerals Inc. |

Halifax, Canada |

Development |

Au |

1.0 % NSR Royalty |

|

17. |

El Realito |

Agnico Eagle |

Sonora, Mexico |

Development |

Au |

2.0 % NSR Royalty (subject to 1.0% buy back) |

|

18. |

La Fortuna |

Minera Alamos Inc. |

Durango, Mexico |

Development |

Au |

Option - 1.0 % NSR Royalty |

|

19. |

Wasamac |

Monarch |

Rouyn-Noranda, Quebec |

Development |

Au |

1.5% NSR Royalty |

|

20. |

Beaufor Mine |

Monarch |

Val d'Or, Quebec |

Development |

Au |

1.0% NSR Royalty, with 100,000 ounce exemption |

|

21. |

San Luis |

SSR Mining |

Peru |

Development |

Au |

1.0% NSR Royalty |

|

22. |

Anglo/Zeke |

Nevada Gold |

Nevada |

Exploration |

Au |

0.5% GOR Royalty |

|

23. |

Red Hill |

NuLegacy |

Nevada |

Exploration |

Au |

1.5% GOR Royalty |

|

24. |

TVZ Zone |

Newmont |

Timmins, Canada |

Exploration |

Au |

2% NSR Royalty |

|

25. |

DeSantis Mine |

Canadian Gold Miner |

Timmins, Canada |

Exploration |

Au |

1.5% NSR Royalty |

|

26. |

Bint Property |

Glencore |

Timmins, Canada |

Exploration |

Au |

2.0% NSR Royalty |

|

27. |

Colbert/Anglo |

Newmont Mining |

Timmins, Canada |

Exploration |

Au |

2.0% NSR Royalty |

|

28. |

Montclerg |

IEP |

Timmins, Canada |

Exploration |

Au |

1.0% NSR Royalty |

|

29. |

Pelangio Poirier |

Pelangio Exp. |

Timmins, Canada |

Exploration |

Au |

1.0% NSR Royalty |

|

30. |

DNA |

Kirkland Lake Gold |

Cochrane, Canada |

Exploration |

Au |

2.0% NSR Royalty |

|

31. |

Beaudoin |

Explor Resources |

Timmins, Canada |

Exploration |

Au, Ag |

0.4% NSR Royalty |

|

32. |

Grenfell |

Pelangio Exp. |

Kirkland Lake, Canada |

Exploration |

Au |

0.25% NSR Royalty |

|

33. |

Mirado Mine |

Orefinders |

Kirkland Lake, Canada |

Exploration |

Au |

1.0% NSR Royalty + Option |

- 17 -

|

|

Property |

Operator |

Location |

Stage |

Metal(1) |

Terms |

|

34. |

Solomon's Pillar |

Private Party |

Greenstone, Canada |

Exploration |

Au |

1.0% NSR Royalty |

|

35. |

Puchuldiza |

Not Applicable |

Chile |

Exploration |

Au |

1.5% NSR Royalty(2) |

|

36. |

Los Patos |

Private Party |

Venezuela |

Exploration |

Au |

1.5% NSR Royalty |

|

37. |

Big Island |

Voyageur Mineral Explorers Corp.(5) |

Flin Flon, Manitoba |

Exploration |

Au |

2.0% NSR Royalty |

|

38. |

Biricu |

Minaurum Gold Inc |

Guerrero, Mexico |

Exploration |

Au |

2.0% NSR Royalty |

|

39. |

Boulevard |

Independence Gold |

Yukon, Ontario |

Exploration |

Au |

1.0% NSR Royalty |

|

40. |

Camflo Northwest |

Monarch |

Val d'Or, Quebec |

Exploration |

Au |

1.0% NSR Royalty |

|

41. |

Edwards Mine |

Trillium Mining |

Wawa, Ontario |

Exploration |

Au |

1.25% NSR Royalty |

|

42. |

Goodfish Kirana |

Warrior Gold |

Kirkland Lake, Ontario |

Exploration |

Au |

1.0% NSR Royalty |

|

43. |

Kirkland-Hudson |

Kirkland Lake Gold |

Kirkland Lake, Ontario |

Exploration |

Au |

2.0% NSR Royalty |

|

44. |

Pucarana |

Buenaventura |

Peru |

Exploration |

Au |

Option - 1.8% NSR Royalty |

|

45. |

Capricho |

Pucara Resources |

Peru |

Exploration |

Au |

1.0% NSR Royalty |

|

46. |

Lourdes |

Pucara Resources |

Peru |

Exploration |

Au |

1.0% NSR Royalty |

|

47. |

Santo Tomas |

Pucara Resources |

Peru |

Exploration |

Au |

1.0% NSR Royalty |

|

48. |

Guadalupe/Pararin |

Pucara Resources |

Peru |

Exploration |

Au |

1.0% NSR Royalty |

|

49. |

Tower Mountain |

White Metal Resources Corp. |

Canada |

Exploration |

Au |

2.0% NSR Royalty |

|

50. |

Orion |

Minera Frisco |

Mexico |

Exploration |

Au, Ag |

2.75% NSR Royalty(3) |

- 18 -

Notes:

(1) "Au" means gold, "Ag" means silver, "Ph" means lead, "Zn" means Zinc, "Cu" means copper and "Mo" means Molybdenum,

(2) 1.5% Royalty has subsequently been extinguished upon acquisition of the underlying concessions by Metalla. See heading General Development of the Business - Current Business of Metalla - 3 Year History - Acquisition of Royalty and Streaming Portfolio from Coeur above.

(3) Not currently owned by Metalla. Under contract to be acquired, subject to customary closing conditions.

(4) Under the joint venture arrangement with Nova, Metalla will be entitled to all payments under the NSR Royalty with respect to gold production and Nova will be entitled to all payments under the NSR Royalty with respect to copper production, and all other payments under the NSR Royalty will be split evenly between the Purchasers.

(5) Formerly Copper Reef Mining Corporation prior to a name change announced on August 15, 2020.

Further details regarding the purchase agreements entered into by Metalla in respect of certain Stream and Royalty acquisition agreements with respect to development or production properties can be found under the heading General Development of the Business above.

Competitive Conditions

Metalla will compete with other companies that operate in the stream and royalty market segment to acquire Streams and Royalties. Metalla will also compete with companies that provide financing to mining companies. Metalla also competes with other precious metals focused companies for capital and human resources. See section Description of the Business - Risk Factors - Competition.

Components

Metalla expects to purchase or acquire Royalties or Streams as previously described above under the heading Description of the Business.

Employees

As at the date of this AIF, Metalla has a total of 3 full time and 5 part time employees. No management functions of Metalla are performed to any substantial degree by persons other than the directors and executive officers of the Company.

Foreign Operations

Metalla currently purchases or expects to purchase precious or other metals or receives or expects to receive payments under Royalties from mines or operations in Australia, Argentina, Mexico, Canada, Tanzania, Ecuador, Peru, and Chile. Metalla may in the future purchase precious metals or receive payments under Royalties from mines or operations in other countries. Changes in legislation, regulations or governments in such countries are beyond Metalla's control and could adversely affect the Company's business. The effect of these factors cannot be predicted with any accuracy by Metalla or its management. See section Description of the Business - Risk Factors - International Interests in this AIF.

RISK FACTORS

Investing in the securities of the Company is speculative and involves a high degree of risk due to the nature of our business and the present stage of its development. The following risk factors, as well as risks currently unknown to us, could materially and adversely affect our future business, operations and financial condition and could cause them to differ materially from the estimates described in forward-looking statements relating to the Company, or its business, property or financial results, contained herein, each of which could cause purchasers of our securities to lose part or all of their investment. The risks set out below are not the only risks we face; risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition, results of operations and prospects.

Investors should carefully consider all of the information disclosed in this AIF prior to investing in the securities of Metalla. In addition to the other information presented in this AIF, the following risk factors should be given special consideration when evaluating an investment in such securities. These risk factors could materially affect Metalla's future operating results and could cause actual events to differ materially from those described in forward-looking statements relating to Metalla. The risk factors described in this AIF are not the only risks that Metalla faces. Additional risks or uncertainties that Metalla does not have any knowledge of or are currently deemed as immaterial, could also materially adversely affect Metalla.

- 19 -

Risks Relating to Metalla

Public Health Crises, including the COVID-19 Pandemic, may Significantly Impact Metalla

Metalla's business, operations and financial condition could be materially adversely affected by public health crises, including epidemics, pandemics and/or other health crises, such as the outbreak of COVID-19. The current COVID-19 global health pandemic is significantly impacting the global economy and commodity and financial markets. The full extent and impact of the COVID-19 pandemic is unknown and to date has included extreme volatility in financial markets, a slowdown in economic activity, extreme volatility in commodity prices (including precious metals) and has raised the prospect of a global recession. The international response to COVID-19 has led to significant restrictions on travel, temporary business closures, quarantines, global stock market volatility and a general reduction in consumer activity, globally. Public health crises, such as the COVID-19 outbreak, can result in operating, supply chain and project development delays that can materially adversely affect the operations of third parties in which Metalla has an interest. Mining operations in which Metalla holds a Royalty or Stream interest ("Mining Operations") have been, and may in the future be, suspended for precautionary purposes or as governments declare states of emergency or other actions are taken in an effort to combat the spread of COVID-19. The re-initiation of operational suspensions at the COSE and Joaquin mines, or at the Santa Gertrudis Property, or the implementation of additional operational suspensions at one or more of the properties in which Metalla holds a Royalty, Stream or other interest and from which it receives or expects to receive significant revenue is suspended, may have a material adverse impact on Metalla's profitability, results of operations, financial condition and the trading price of Metalla's securities.

The risks to Metalla's business associated with COVID-19 include without limitation, the risk of breach of material contracts and customer agreements, risks to employee health and workforce productivity at Mining Operations, the possibility of increased insurance premiums, limitations on travel, the availability of industry experts and personnel, prolonged restrictive measures put in place in order to control an outbreak of contagious disease or other adverse public health developments globally and other factors that will depend on future developments beyond Metalla's control, which may have a material and adverse effect on Metalla's business, financial condition and results of operations. In addition, Metalla may experience business interruptions as a result of the re-initiation or initiation of suspensions or operational reductions at the mines in which Metalla has an interest, relating to the COVID-19 outbreak or such other events that are beyond the control of Metalla, which could in turn have a material adverse impact on Metalla's business, operating results, financial condition and the market for its securities. As at the date of this AIF, the duration of any business disruptions and related financial impact of the COVID-19 outbreak cannot be reasonably estimated.

Changes in Commodity Prices that underlie Royalty, Stream or Other Interests

The price of Metalla's Common Shares may be significantly affected by declines in commodity prices. The revenue derived by Metalla from its asset portfolio will be significantly affected by changes in the market price of commodities that underlie the Royalty, Stream or other investments or interests of Metalla. Metalla's revenue is particularly sensitive to changes in the price of gold and silver. Any future cash flow derived from silver Streams is dependent on the future price of silver. The price of gold, silver and other commodities fluctuates daily and are affected by factors beyond the control of Metalla, including levels of supply and demand, industrial development, inflation and interest rates, the U.S. dollar's strength and geo-political events. External economic factors that affect commodity prices can be influenced by changes in international investment patterns, monetary systems and political developments.

The Chinese market is a significant source of global demand for commodities. A sustained slowdown in China's growth or demand, or a significant slowdown in other markets, in either case, that is not offset by reduced supply or increased demand from other regions could have an adverse effect on the price and/or demand for the products in respect of which we have Streams, Royalties or other interests. The COVID-19 pandemic and efforts to contain it have had a significant effect on commodity prices and demand as well as broader impacts on the global economy. See also "Risk Factors - Risks Related to Mines and Mining Operations - Public Health Crises, including the COVID-19 Pandemic may Significantly Impact Metalla"

- 20 -

All commodities, by their nature, are subject to wide price fluctuations and future material price declines will result in a decrease in revenue and may cause a suspension or termination of production by relevant operators, which would result in a complete cessation of revenue from applicable Royalties, Streams or working interests. Even if Metalla works to ensure a diversification of commodities that underlie its Royalties, Streams and other interests, the commodity market trends are cyclical in nature and a general downturn in commodity prices could result in a significant decrease in overall revenue.

Fosterville and Exploration Royalty Portfolio Transactions

There is no certainty that the Fosterville Transaction or the Exploration Royalty Portfolio Transaction will be completed, or completed as announced, and any consequences of such non completion on Metalla may be difficult or impossible to predict.

Metalla Has No Control Over Mining Operations

Metalla is not directly involved in the operation of mines. The revenue Metalla may derive from its portfolio of Royalty and Stream assets and other interests based entirely on production from third-party mine owners and operators. Metalla is party to precious metal purchase agreements to purchase a certain percentage of precious metals or other metals produced by certain mines and operations and Metalla expects to receive payments under Royalty agreements based on production from certain mines and operations, however, Metalla will not have a direct interest in the operation or ownership of those mines and projects. The owners and operators generally will have the power to determine the manner in which the properties are exploited, including decisions to expand and continue or reduce, suspend or discontinue production from a property, to make decisions about the marketing of products extracted from the property and to make decisions to advance exploration efforts and conduct development of non producing properties. The interests of third-party owners and operators and those of Metalla in respect of a relevant project or property may not always be aligned. The inability of Metalla to control the operations for the properties in which it has a Royalty, Stream or other interest may result in a material adverse effect on the profitability of Metalla, the results of operations of Metalla and its financial condition. Except in a limited set of circumstances as may be specified in respect of a specific Stream, Royalty or other interest, Metalla will not receive compensation if a specific mine or operation fails to achieve or maintain production or if the specific mine or operation is closed or discontinued. In addition, a number Mining Operations are currently in exploration stage and may not commence commercial production and there can be no assurance that if such operations do commence production that they will achieve profitable and continued production levels. In addition, the owners or operators may take action contrary to policies or objectives of Metalla; be unable or unwilling to fulfill their obligations under their agreements with Metalla; have difficulty obtaining or be unable to obtain the financing necessary to move projects forward; or experience financial, operational or other difficulties, including insolvency, which could limit the owner or operator's ability to perform its obligations under arrangements with Metalla. Metalla is also subject to the risk that a specific mine or project may be put on care and maintenance or have its operations suspended, on both a temporary or permanent basis.

The owners or operators of the projects or properties in which Metalla holds a Royalty, Stream or other interest may from time to time announce transactions, including the sale or transfer of the projects or of the operator itself, over which Metalla has little or no control. If such transactions are completed it may result in a new operator controlling the project, who may or may not operate the project in a similar manner to the current operator which may positively or negatively impact Metalla. If any such transaction is announced, there is no certainty that any such transaction will be completed, or completed as announced, and any consequences of such non completion on Metalla may be difficult or impossible to predict.

Metalla is subject to the risk that Mining Operations may shut down on a temporary or permanent basis due to issues including but not limited to economic conditions, lack of financial capital, flooding, fire, pandemics (including the COVID-19 pandemic), weather related events, mechanical malfunctions, community or social related issues, social unrest, the failure to receive permits or having existing permits revoked, collapse of mining infrastructure including tailings ponds, expropriation and other risks. For example, in response to the COVID-19 pandemic and the resulting governmental laws and regulations, operations at each of the COSE and Joaquin mines, and the Santa Gertrudis Property, were suspended. These issues are common in the mining industry and can occur frequently. There is a risk that the carrying values of Metalla's assets may not be recoverable if the mining companies operating the Mining Operations cannot raise additional finances to continue to develop those assets. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in the Mining Operations becoming uneconomic resulting in their shutdown and closure. Metalla is not entitled to purchase gold, silver or other commodities, receive royalties or other economic benefit from the Mining Operations if no gold, silver or other commodities are produced from the Mining Operations.

- 21 -

Variations in Foreign Exchange Rates

Foreign exchange rates have seen significant fluctuation in recent years. A depreciation in the value of the Canadian Dollar against one or more of the currencies in which Metalla receives payments under the Royalties and Streams could have a material adverse effect on the profitability of Metalla, its results of operations and financial condition.

Metalla's consolidated revenue, expenses and financial position may be impacted by fluctuations in foreign exchange rates as payments in foreign currencies are translated into Canadian Dollars. Metalla has not hedged its exposure to currency fluctuations. Currency fluctuations in other international currencies in which Metalla receives payments under the Royalties and Streams could have an equal or greater effect including the payment of the Royalty on the COSE mine which may be made in either Argentinian Pesos or United States Dollars at the option of the payor.

Delay Receiving or Failure to Receive Payments