Integra Resources Corp.

ANNUAL INFORMATION FORM

For Fiscal Year Ended December 31, 2020

March 12, 2021

TABLE OF CONTENTS

| ADDITIONAL INFORMATION | 56 |

| Schedule "A" - Glossary | |

| Schedule "B" - Audit Committee Charter |

FORWARD LOOKING STATEMENTS

This annual information form ("AIF" or "Annual Information Form") of Integra Resources Corp. ("Integra" or the "Company") contains "forward-looking statements" or "forward-looking information" within the meaning of applicable Canadian and United States securities legislation (collectively, "forward-looking statements"). Forward-looking statements are included to provide information about management's current expectations and plans that allows investors and others to get a better understanding of the Company's operating environment, business operations and financial performance and condition.

Forward-looking statements relate, but are not limited, to: timing of completion of a technical report summarizing the results of the PFS; the development, operational and economic results of the PEA in the DeLamar Report, including cash flows, capital expenditures, development costs, extraction rates, life of mine cost estimates; estimation of Mineral Resources; magnitude or quality of mineral deposits; anticipated advancement of the DeLamar Project mine plan; future operations; future exploration prospects; the completion and timing of future development studies; future growth potential of DeLamar and future development plans; statements regarding planned exploration, drilling and development programs and expenditures; proposed exploration plans and expected results of exploration from the DeLamar Project; Integra's ability to obtain licenses, permits and regulatory approvals required to implement expected future exploration plans; changes in commodity prices and exchange rates; currency and interest rate fluctuations; and impact of COVID-19 on the timing of exploration work and development studies. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objections, assumptions or future events or performance (often, but not always, identified by words or phrases such as "expects", "is expected", "anticipates", "believes", "plans", "projects", "estimates", "assumes", "intends", "strategy", "goals", "objectives", "potential", "possible" or variations thereof or stating that certain actions, events, conditions or results "may", "could", "would", "should", "might" or "will" be taken, occur or be achieved (or the negative of any of these terms and similar expressions) are not statements of fact and may be forward-looking statements.

Forward-looking statements are necessarily based upon a number of factors and assumptions that, if untrue, could cause actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such statements. Forward-looking statements are based upon a number of estimates and assumptions that, while considered reasonable by the Company at this time, are inherently subject to significant business, economic and competitive uncertainties and contingencies that may cause the Company's actual financial results, performance, or achievements to be materially different from those expressed or implied herein. Some of the material factors or assumptions used to develop forward-looking statements include, without limitation, the future price of gold and silver, anticipated costs and the Company's ability to fund its programs, the Company's ability to carry on exploration and development activities, the timing and results of drilling programs, the discovery of additional Mineral Resources on the Company's mineral properties, the timely receipt of required approvals and permits, including those approvals and permits required for successful project permitting, construction and operation of projects, the costs of operating and exploration expenditures, the Company's ability to operate in a safe, efficient and effective manner, the Company's ability to obtain financing as and when required and on reasonable terms and the impact of COVID-19 and the resumption of business.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those expressed or implied. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Certain important factors that could cause actual results, performance or achievements to differ materially from those in the forward-looking statements include, among others: (i) access to additional capital; (ii) uncertainty and variations in the estimation of Mineral Resources; (iii) health, safety and environmental risks; (iv) success of exploration, development and operations activities; (v) delays in obtaining or failure to obtain governmental permits, or non-compliance with permits; (vi) delays in getting access from surface rights owners; (vii) the fluctuating price of gold and silver; (viii) assessments by taxation authorities; (ix) uncertainties related to title to mineral properties; (x) the Company's ability to identify, complete and successfully integrate acquisitions; and (xi) volatility in the market price of Company's securities.

This list is not exhaustive of the factors that may affect any of the Company's forward-looking statements. Although the Company believes its expectations are based upon reasonable assumptions and have attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. See the section entitled "The Business - Risk Factors" below for additional risk factors that could cause results to differ materially from forward-looking statements.

Investors are cautioned not to put undue reliance on forward-looking statements. The forward looking-statements contained herein are made as of the date of this Annual Information Form and, accordingly, are subject to change after such date. The Company disclaims any intent or obligation to update publicly or otherwise revise any forward-looking statements or the foregoing list of assumptions or factors, whether as a result of new information, future events or otherwise, except in accordance with applicable securities laws. Investors are urged to read the Company's filings with Canadian securities regulatory agencies, which can be viewed online under the Company's profile on SEDAR at www.sedar.com.

Cautionary Note to United States Investors with Respect to Mineral Resources

This AIF includes mineral reserves and mineral resources classification terms that comply with reporting standards in Canada and are made in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101"). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. These standards differ significantly from the requirements of the United States Securities and Exchange Commission (the "SEC") applicable to domestic United States reporting companies. Accordingly, information included in this AIF that describes the Company's mineral reserves and mineral resources estimates may not be comparable with information made public by United States companies subject to the SEC's reporting and disclosure requirements.

Non-GAAP Measures and Other Financial Measures

Alternative performance measures in this document such as "cash cost" and "AISC" are furnished to provide additional information. These non-GAAP performance measures are included in this AIF because these statistics are used as key performance measures that management uses to monitor and assess performance of the DeLamar Project, and to plan and assess the overall effectiveness and efficiency of mining operations. These performance measures do not have a standard meaning within IFRS and, therefore, amounts presented may not be comparable to similar data presented by other mining companies. These performance measures should not be considered in isolation as a substitute for measures of performance in accordance with IFRS.

INTRODUCTION

Currency and Other Information

Unless otherwise indicated, all references to "$" in this AIF are to Canadian dollars and all references to "US$" or "USD$" in this AIF are to U.S. dollars.

The following table reflects the low and high rates of exchange for one United States dollar, expressed in Canadian dollars, during the periods noted, the rates of exchange at the end of such periods and the average rates of exchange during such periods, based on the Bank of Canada daily exchange rates for 2018, 2019 and 2020.

|

|

Years Ended December 31, |

||

|

|

2020 |

2019 |

2018 |

|

Low for the period |

$1.2718 |

$1.2988 |

$1.2288 |

|

High for the period |

$1.4496 |

$1.3600 |

$1.3642 |

|

Rate at the end of the period |

$1.2732 |

$1.2988 |

$1.3642 |

|

Average |

$1.3446 |

$1.3269 |

$1.2957 |

On March 11, 2021, the Bank of Canada daily exchange rate was US$1.00 - $1.2561.

Scientific and Technical Information

Unless otherwise indicated, the scientific and technical information contained in this AIF relating to the DeLamar Project has been reviewed and approved by E. Max Baker (F.AusIMM), Vice President, Exploration, and Timothy Arnold (P.E.), COO, each of whom is a QP as defined in NI 43-101.

Consolidation

On July 9, 2020, Integra effected a 2.5 to 1 consolidation of its Common Shares (the "Consolidation"). Unless otherwise noted, all references to number of Common Shares, warrants and stock options, as well as strike price and price per Common Share information in this AIF reflect the Consolidation.

CORPORATE STRUCTURE

Name, Address and Incorporation

Integra was incorporated under the OBCA on April 15, 1997 as Berkana Digital Studios Inc. On December 4, 1998, the name of the Company was changed to Claim Lake Resource Inc. and on April 5, 2005, the Company completed a 2 for 1 consolidation and changed its name to Fort Chimo Minerals Inc. On January 1, 2009, the Company amalgamated with its wholly-owned subsidiary, Limestone Basin Exploration Ltd. The amalgamated company continued to operate as Fort Chimo Minerals Inc. On June 14, 2011, the Company completed a 5 to 1 consolidation and changed its name to Mag Copper Limited. The Company completed a 5 to 1 consolidation on September 2, 2015. In January 2017 and August 2017, the Company completed a 5 to 1 and 2.5 to 1 consolidation, respectively. On August 11, 2017, the Company changed its name to Integra Resources Corp.

On June 29, 2020, the Company completed the continuation (the "Continuation) of the Company from the Province of Ontario to the Province of British Columbia. As a result of the Continuation, the Business Corporations Act (Ontario) will no longer apply to the Company and the Company is subject to the Business Corporations Act (British Columbia) (the "BCBCA") as if it had been originally incorporated under the BCBCA. In connection with the Continuation, the articles and by-laws of the Company were replaced with notice of articles and articles. The notice of articles and articles are substantially similar to the former articles and by-laws of the Company. Changes include alterations to permit the Board to make certain changes to the capital structure of the Company; alterations to the advance notice requirements; alternations to the quorum requirement for the transaction of business at a Board meeting; alterations to the threshold to satisfy quorum to include 25% of the Common Shares entitled to be voted at the meeting; alterations to the record date for the purpose of dividend declaration; and alterations to the type of resolution required to remove a director before the expiration of his or her term.

On July 9, 2020, the Company completed the Consolidation.

The Company's head office is located at 1050 - 400 Burrard Street, Vancouver, BC V6C 3A6 and its registered office is located at 2200 HSBC Building, 885 West Georgia Street Vancouver, BC V6C 3E8.

The Company delisted from the Canadian Securities Exchange on November 6, 2017 and commenced trading on the TSX-V on November 7, 2017, under the trading symbol "ITR". In January 2018, the Company began trading in the United States on the OTCQB under the stock symbol "IRRZF" and subsequently graduated to the OTCQX on May 1, 2018. On July 31, 2020, the Company began trading on the NYSE American under the symbol "ITRG". The Company ceased trading on the OTCQX concurrently with the NYSE American listing. The Company continues to be listed on the TSX-V under the trading symbol "ITR".

Unless otherwise noted or inconsistent with the context, references to Integra or the Company in this AIF are references to Integra Resources Corp. and its subsidiaries.

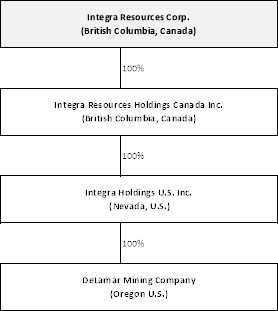

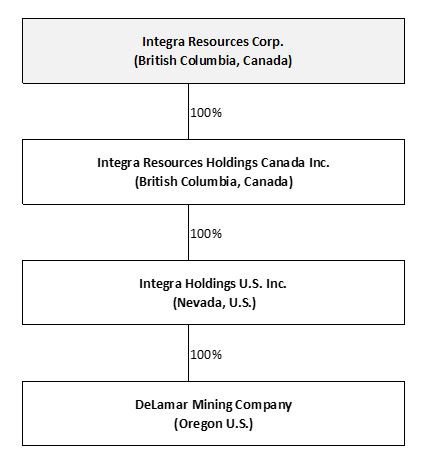

Intercorporate Relationships

The following diagram illustrates the intercorporate relationships among Integra and its subsidiaries, as well as the jurisdiction of incorporation of each entity.

GENERAL DEVELOPMENT OF THE BUSINESS

Overview

Integra Resources Corp. is a mineral resources company engaged in the acquisition, exploration and development of mineral properties in the Americas. The primary focus of the Company is the advancement of its DeLamar gold and silver project (the "DeLamar Project"), consisting of the neighbouring DeLamar Deposit and Florida Mountain Deposit in the heart of the historic Owyhee County mining district in south western Idaho.

Three Year History

2018

Exploration and Resource Estimates

In 2018, Integra undertook the first year of modern exploration at the DeLamar Project. In addition to completing over 20,000 m of drilling, the Company more than doubled its land package, completed 3 km of induced polarization surveys and commenced metallurgical test work.

In February 2018, Integra completed an updated Mineral Resource estimate for the DeLamar Project that included Mineral Resources from the Florida Mountain Area (the "2018 Technical Report"). This estimate added an additional 36,507,000 tonnes of Inferred Mineral Resources from the Florida Mountain Area grading 0.57 g/t gold and 14.12 g/t silver at a cut-off grade of 0.3 g/t AuEq, for 675,000 contained ounces of gold and 16.6 million contained ounces of silver, or 870,541 ounces AuEq.

Financing Transactions

On October 31, 2018, the Company closed an offering of 6,867,600 special warrants (the "Special Warrants") at an issue price of $0.80 per Special Warrant for gross proceeds of $5,494,080. The Company filed a short form prospectus and converted the Special Warrants into 6,867,600 free trading Common Shares, for no additional consideration, on November 15, 2018.

On November 6, 2018, the Company closed a brokered offering, which consisted of the issue of 14,375,000 Common Shares at an issue price of $0.80 per Common Share for gross proceeds of $11,500,000 under a short form prospectus.

Board Additions

The Company strengthened its Board in 2018 with the additions of Mr. George Salamis and Mr. Timo Jauristo in March 2018, and Ms. Anna Ladd-Kruger in December 2018.

2019

Director and Executive Appointments

The Company appointed Mr. Timothy D. Arnold as Vice President, Project Development, in January 2019. Mr. Arnold, a Reno-based, Professional Mining Engineer, comes to Integra with over 30 years of experience in mine project development, mine permitting and mine operational management on various projects in the western USA. Mr. Arnold was subsequently appointed COO in November 2019.

The former Idaho Governor C.L. "Butch" Otter joined the Company's Board in September 2019. Gov. Otter is a businessman who served as the 32nd Governor of Idaho from 2007 to 2019. Gov. Otter served as Lieutenant Governor from 1987 to 2001 and in the United States Congress from 2001 to 2007. Before devoting his career full-time to serving the people of Idaho in public office, Gov. Otter spent more than 30 years as a business leader including 12 years as President of the Idaho-based Simplot International.

Financings and Strategic Placement with Coeur Mining

On August 16, 2019, the Company closed an offering of 14,490,696 Special Warrants at an issue price of $0.86 per Special Warrant for gross proceeds of $12,461,999. The Company filed a short form prospectus and converted the Special Warrants into 14,490,696 free trading Common Shares, for no additional consideration, in August 2019.

On November 25, 2019, the Company closed a non-brokered offering with Coeur Mining, which consisted of the issue of 5,760,236 Common Shares at an issue price of $1.15 per Common Share for gross proceeds of approximately $6,624,270. In connection with the investment, Coeur Mining and Integra entered into the Coeur Investor Rights Agreement. The Coeur Investor Rights Agreement provides Coeur Mining with participation rights to maintain its pro rata Common Share ownership in Integra for two years and the right to appoint two members to a newly formed technical committee of Integra so long as Coeur Mining continues to own at least 2.4% of Integra's Common Shares.

On December 4, 2019, the Company closed a brokered offering, which consisted of the issue of 21,999,500 Common Shares (including exercised over-allotment option) at an issue price of $1.15 per Common Share for gross proceeds of approximately $25,300,000 under a short form prospectus.

Payment of Kinross Promissory Note

On November 5, 2019, the Company announced that it had paid the remaining $4,500,000 owed to Kinross USA pursuant to a secured promissory note. This payment represents payment in-full for all amounts owing under the secured promissory note and all obligations under the DeLamar Purchase Agreement with Kinross USA have been fully performed. As a result, Kinross USA released its security on 25% of the shares of DeLamar Mining Company.

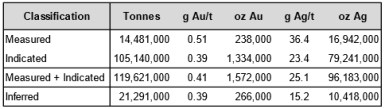

Updated Mineral Resource Estimate

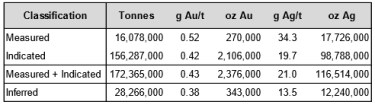

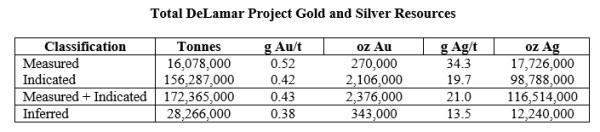

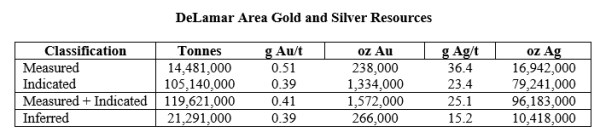

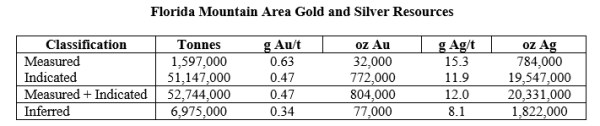

In June 2019, Integra completed an updated Mineral Resource estimate for the DeLamar Project, which includes the DeLamar and Florida Mountain Area deposits (the "2019 Technical Report").

Resource update highlights included:

- 3.9 Moz AuEq (2.4 Moz Au, and 116.5 Moz Ag) upgraded from Inferred into Measured and Indicated category ("M&I") with an average grade of 0.70 g/t AuEq (0.43 g/t Au, 21.0 g/t Ag) employing a 0.2 g/t AuEq cut-off for oxide/transitional Mineral Resources, and a 0.3 g/t AuEq cut-off for unoxidized Mineral Resources;

-

Global Inferred Mineral Resources updated to 501,000 oz AuEq (343,000 oz Au, 12,240,000 oz Ag) at an average grade of 0.55 g/t AuEq (0.38 g/t Au, 13.5 g/t Ag) employing a 0.2 g/t AuEq cut-off for oxide/transitional Mineral Resources, and a 0.3 g/t AuEq cut-off for unoxidized Mineral Resources;

-

Approximately 90% of the DeLamar Project global Mineral Resources were upgraded to an M&I category; and

-

All Mineral Resources are pit constrained with a low average overall strip ratio of 1.83:1 (2.05:1 for the DeLamar deposit, and 1.31:1 for the Florida Mountain Area deposit).

The Mineral Resources update incorporates approximately 30,000m in 93 drill holes of new infill and extensional drilling completed at the DeLamar Project since Integra acquired the DeLamar Project in November 2017, along with over 250,000m of drilling conducted by Kinross and its predecessors. The updated Mineral Resource shows a substantial conversion of Inferred Mineral Resources to M&I ounces. This reflects the data added to the DeLamar Project through the successful confirmatory drilling, comprehensive relogging of historical drill holes and continued compilation of historical geological information.

Please see "DeLamar Project - Mineral Resources" section below for further details on the updated Mineral Resource estimate for the DeLamar Project.

Preliminary Economic Assessment

In September 2019, Integra announced the results of a maiden PEA on the DeLamar Project. The PEA is based on the updated Mineral Resource estimate in the 2019 Technical Report.

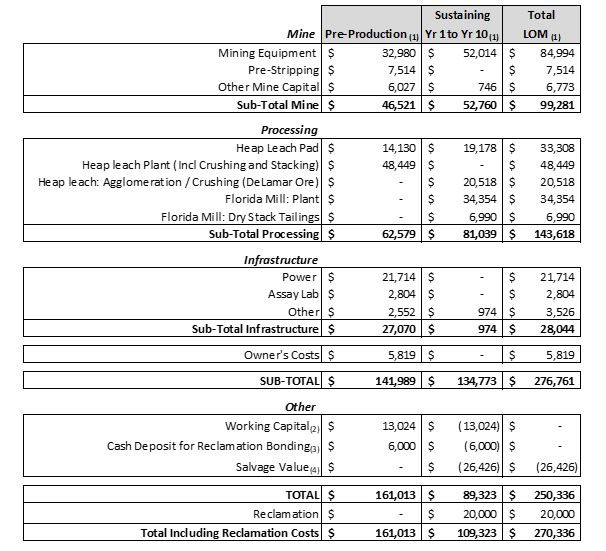

DeLamar Project PEA highlights included:

- 27,000 tpd open-pit/heap-leach production rate with an initial mine life of 10 years, sourcing oxide and transitional mineralization from both the Florida Mountain and DeLamar Area deposits;

-

2,000 tpd mill, commencing in year 3, sourcing unoxidized mineralization from Florida Mountain over a 6-year period;

-

Year 1 to 10 average annual production of 103,000 oz Au and 1,660,000 oz Ag (124,000 oz AuEq);

-

Year 2 to 6 average annual production of 126,000 oz Au and 1,796,000 oz Ag (148,000 oz AuEq);

-

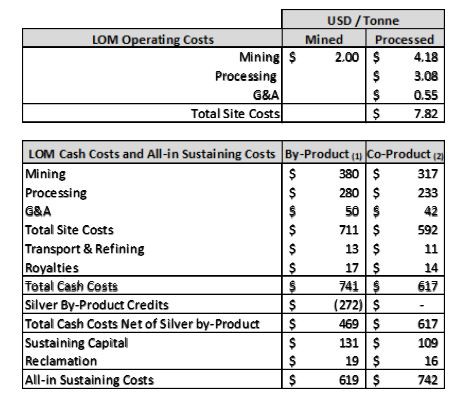

LOM total payable production of 1,031,000 oz Au and 16,603,000 oz Ag (1,239,000 oz AuEq);

-

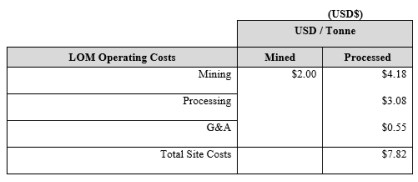

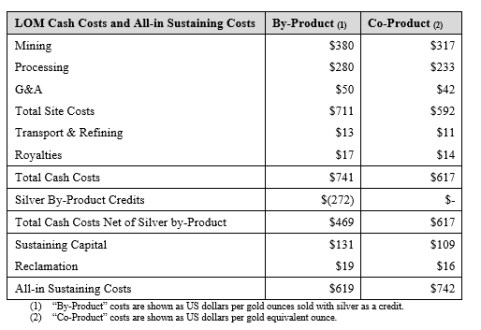

LOM AISC of US$619/oz net of silver by-product or US$742/oz on an Au Eq co-product basis;

-

A low LOM strip ratio of 1.09 to 1 (waste : mineralization);

-

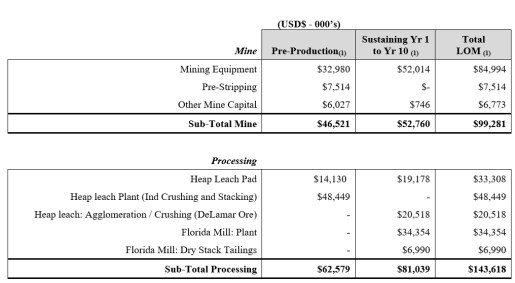

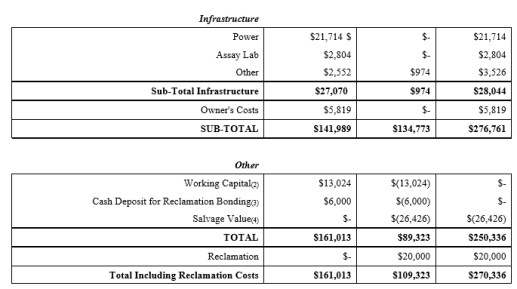

Low pre-production capex of US$161 million;

-

LOM capital expenditures (pre-production + sustaining capital) of US$277 million;

-

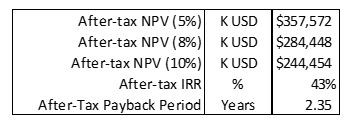

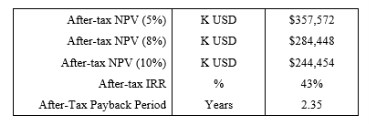

After-tax payback period of 2.4 years;

-

After-tax IRR of 43%;

-

After-tax NPV (5%) of US$358 million;

-

US$528 million after-tax LOM cumulative cash flow; and

-

Average annual after-tax free cash flow of US$61 million once in production.

Please see "DeLamar Project" section below for further details on the Company's PEA included in the "DeLamar Report".

Land Acquisitions

In January 2019, Integra announced that it had entered into an option agreement with Nevada Select Royalty Inc. ("Nevada Select"), a wholly owned subsidiary of Ely Gold Royalties Inc. ("Ely Gold") to acquire Nevada Select's interest in a State of Idaho Mineral Lease (the "State Lease") encompassing the War Eagle gold-silver Deposit ("War Eagle Property", "War Eagle Mountain" or "War Eagle") situated in the DeLamar District, southwestern Idaho. The War Eagle Property has a history of high-grade mining in the late 1800s/early 1900s as well as high-grade exploration drilling in the late 1980's. Upon exercise of the option, Nevada Select will transfer its right, title and interest in the State Lease, subject to a 1.0% NSR royalty on future production from the deposit payable to Ely Gold, to DMC. Under the option agreement, Integra will pay Nevada Select US$200,000 over a period of four years in annual payments.

In February 2019, Integra announced the acquisition of a highly prospective trend of multiple epithermal centers 6km to the northwest of the DeLamar Project, a trend now referred to as the "BlackSheep District" or "BlackSheep Area". The BlackSheep District to the northwest of DeLamar is comparable in geographical size to both the DeLamar and Florida Mountain Area deposits combined. As a result of its findings in the BlackSheep District, and in advance of a more substantial district scale exploration program, the Company has staked approximately 15 square km of additional claims.

Exploration and Development

The Company drilled approximately 22,250m from January 2019 through December 2019 at the DeLamar and Florida Mountain Area deposits and the War Eagle Property. Most of this drilling involved extracting core to support metallurgical testing, the results of which were used in the DeLamar Report. The Company's exploration program shifted to Mineral Resource expansion at Florida Mountain adjacent to the known Mineral Resource envelope as well as testing of the north-south mineralized trend. The Company also initiated an exploration program at the War Eagle Property. In addition to the drill program, the Company completed extensive geochemistry, geophysics, soil sampling and historical data review to delineate potential drill targets for Mineral Resource expansion and discovery at the DeLamar Project.

Corporate Social Responsibility

The Company continued to proactively engage local stakeholders with a series of formal and informal meetings focused primarily in Owyhee and Malheur Counties. The Company's goal with these meetings was to promote a long-lasting relationship built on clear and comprehensive disclosure between Integra and the neighbouring stakeholders, in order to maintain transparency and to encourage confidence in its business practices and ethics. Groups met included residents, businesses, ranch and landowners, elected officials and others.

Local initiatives participated in during 2019 included the Jordan Valley School Science Fair, the Owyhee County Historical Society Outpost Days, local school field trips, Owyhee Field Days, the Owyhee and Junior rodeos as well as the Spurs & Spikes Charity Fundraiser. Several site visits occurred over the course of the year, with stakeholders from Owyhee County, Malheur County and elected officials having an opportunity to observe Integra's operations and ask questions on the Company's plans for the future.

2020

Corporate

For the safety of all employees, the Company closed its corporate office (Vancouver, BC) in mid-March as a result of the COVID-19 global outbreak. Most corporate employees continue to work remotely from home, with some employees now working periodically at the office under safe COVID-19 protection protocols. One of the most impacted activities at the corporate level has been the ability to travel due to travel bans and safety risks. The Company has, however, remained extremely active on the investor relations and marketing fronts through virtual media forums both with investors and at multiple industry conferences.

On February 6, 2020, the Company announced that it had been approved for graduation from Tier 2 to Tier 1 issuer status on the TSX-V. The TSX-V classifies issuers into different tiers based on standards including historical financial performance, stage of development and financial resources. Tier 1 is the TSX-V's premier tier and is reserved for the TSX-V's most advanced issuers. As a result of the graduation to Tier 1 issuer status, the remaining 966,563 Common Shares previously held in escrow were released. The number of outstanding Common Shares did not change as a result of the escrow release.

On June 29, 2020, the Company completed the Continuation.

On July 9, 2020, the Company completed the Consolidation.

On July 31, 2020, the Common Shares commenced trading on the NYSE American under the symbol "ITRG". The Common Shares ceased to trade on the OTCQX concurrently with the NYSE American listing. The Company continues to list on the TSX-V under the symbol "ITR".

Financings

On August 21, 2020, the Company filed a final base shelf prospectus relating to the offering for sale from time to time of up to $100,000,000 of Common Shares, warrants, subscription receipts and units.

On September 14, 2020, the Company closed a brokered offering, which consisted of the issue of 6,785,000 Common Shares (including exercised over-allotment option) at an issue price of US$3.40 per Common Share for gross proceeds of approximately US$23,069,000 under a final prospectus supplement (the "Public Offering"). In connection with the Public Offering, the Company entered into an underwriting agreement with the underwriters of the Public Offering (the "Underwriting Agreement"). Pursuant to the Underwriting Agreement, the Company agreed to pay the underwriters 5.5% of the gross proceeds of the Public Offering, other than the issue of Common Shares to certain persons on a president's list and Coeur Mining, for which a 2.75% cash commission was paid. The Underwriting Agreement also included customary terms for transactions such as the Public Offering.

On December 30, 2020, the Company filed a prospectus supplement to qualify the distribution of up to US$25,000,000 of Common Shares by way of an at-the-market offering (the "ATM"). In connection with the ATM, the Company entered into an "at-the-market equity distribution agreement dated December 30, 2020 with the agent (the "Equity Distribution Agreement"). Pursuant to the Equity Distribution Agreement, the Company agreed to pay the agent 2.75% of the gross proceeds from the sale of Common Shares under the Equity Distribution Agreement. The Equity Distribution Agreement also included customary terms for transactions such as the ATM. Proceeds, if any, from the ATM are expected to fund additional exploration drilling and provide trading liquidity to United States capital markets.

Other

In July 2020, the Company led an effort with the Association for Mineral Exploration BC ("AMEBC") that raised over $100,000 within the British Columbia mining community to support foodbanks that serve rural, remote, and Indigenous communities.

In December 2020, Integra organized and co-sponsored a diversity & inclusion ("D&I") workshop amongst a group of roughly 25 mining executives, with instruction led by Brooks & Nelson. The goal of this workshop was to promote D&I training amongst Integra's leadership team, as well as extend the training to a group of industry leaders.

On December 3, 2020, the Company appointed Mr. Joshua Serfass to the position of Executive Vice President, Corporate Development and Investors Relations and Mr. Mark Stockton to the position of Vice President, Corporate Affairs and Sustainability. Earlier in 2020, the Company also hired a Senior Exploration Manager, Site Controller, Permitting Manager, and Engineering Manager.

Exploration

In mid-March 2020, for the safety of all employees, the Company suspended drilling and exploration activities. In mid-May 2020, the United States government declared mining an essential service; with comprehensive operational procedures in-place, which were specifically designed to mitigate the risk of disease transmission amongst essential site staff and crews, the Company resumed drilling. The Company continues to practice social distancing and complying with both Oregon and Idaho state government requirements regarding COVID-19. Though initially delayed due to COVID-19, all planned exploration drilling in 2020 was successfully executed.

Drilling

The Company completed a total of 14,517m of exploration drilling in 2020, including 9,091m at Florida Mountain, 3,674m at War Eagle, 1,083m at DeLamar, and 669m at BlackSheep.

Florida Mountain Drilling1

Integra drilled 20 drill holes at Florida Mountain specifically targeting high-grade shoots. Of those 20 drill holes, 13 intersected significant high-grade gold-silver mineralization in most cases well outside of the existing Mineral Resource boundaries under the DeLamar Report.

Integra's exploration team identified 7 high-grade vein structures, with an aggregate length of 7,000m that appear similar in size and orientation to the historically productive high-grade Trade Dollar - Black Jack vein system. Most historic underground production stemmed from the Trade Dollar - Black Jack vein, while the remaining 6 veins saw limited production up until mining operations ceased with the start of World War I.

Integra refined its understanding of the controls on high-grade vein mineralization at Florida Mountain in early 2020 and used this model to specifically target the higher-grade "shoots" within the several vein systems identified to date. Those higher-grade shoots are interpreted as being localized at the intersections of the North-Northwest and roughly East-West Trending fault/fracture systems. The high-grade shoots within those vein structures are localized at structural intersections, have strike length of up to 100m or more and down-dip extensions of several hundred meters, with widths of between 1m and 8m.

On February 24, 2020, the Company announced the final drill holes received from the 2019 Florida Mountain Deposit metallurgical sampling program, highlighting high-grade gold and silver outside of current resource boundary.

Florida Mountain exploration drilling highlight intercepts included:

- Drill hole IFM19-073: 40.39 g/t Au and 11.38 g/t Ag over 1.52m

- Drill hole IFM19-074: 9.73 g/t Au and 19.55 g/t Ag over 1.52m

On July 29, 2020, the Company announced drilling results from its first four drill holes of the 2020 program at Florida Mountain. The holes intersected significant high-grade gold and silver mineralization both within and outside of the existing NI 43-101 Mineral Resource boundary in the DeLamar Report. These drill results provide evidence that structurally-controlled high-grade veins exist below the current Mineral Resource estimate in the DeLamar Report and that further drill definition could potentially be interpreted and modelled as high-grade mill feed in future economic studies.

Florida Mountain exploration drilling highlight intercepts included:

- Drill Hole FME-20-076

→ 1.99 g/t Au and 24.17 g/t Ag (2.30 g/t AuEq) over 117.04m

-

Including 72.37 g/t Au and 82.00 g/t Ag (73.43 g/t AuEq) over 1.52m

-

Including 6.77 g/t Au and 68.62 g/t Ag (7.65 g/t AuEq) over 10.97m

___________________________________________

1Downhole thickness; true width varies depending on drill hole dip; most drill holes are aimed at intersecting the vein structures close to perpendicular therefore true widths are close to downhole widths (approximately 70% conversion ratio); Intervals reported are uncapped; Gold equivalent = g Au/t + (g Ag/t ÷ 77.70); For the intervals that were previously mined/stoped and were therefore unrecoverable and unverifiable, a grade of 0 g/t Au was inserted for compositing

→ 10.08 g/t Au and 1,233.77 g/t Ag (25.96 g/t AuEq) over 3.60m

-

Including 34.40 g/t Au and 4,075.40 g/t Ag (86.85 g/t AuEq) over 0.88m

-

6.37 g/t Au and 1,459 g/t Ag (25.14 g/t AuEq) over 1.52m

- Drill Hole FME-20-077

→ 1.63 g/t Au and 17.13 g/t Ag (1.85 g/t AuEq) over 113.69m

- Including 72.07 g/t Au and 63.16 g/t Ag (72.88 g/t AuEq) over 1.52m

On September 24, 2020, the Company announced drilling and geophysics results from Florida Mountain. Five drill holes intersected significant high-and-low-grade gold and silver mineralization both within and below the existing NI 43-101 Mineral Resource boundary in the DeLamar Report.

Florida Mountain exploration drilling highlight intercepts included:

- Drill Hole FME-20-084

→ 1.51 g/t Au and 102.12 g/t Ag (2.82 g/t AuEq) over 87.48m

-

Including 8.91 g/t Au and 607.55 g/t Ag (16.73 g/t AuEq) over 6.25m

-

Including 7.57 g/t Au and 652.54 g/t Ag (15.96 g/t AuEq) over 1.37m

- Drill Hole FME 20-80

- Including 6.77 g/t Au and 68.62 g/t Ag (7.65 g/t AuEq) over 10.97m

→ 11.75 g/t Au and 1,951.88 g/t Ag (36.87 g/t AuEq) over 1.68m

- Including 25.29 g/t Au and 3,841.14 g/t Ag (74.73 g/t AuEq) over 0.76m

- Drill Hole FME-20-081

→ 11.07 g/t Au and 1,480.13 g/t Ag (30.12 g/t AuEq) over 0.61m

On December 9, 2020, the Company announced further exploration results from the 2020 Florida Mountain exploration program.

Florida Mountain exploration drilling highlight intercepts included:

- Drill Hole FME-20-085 (within and below existing Mineral Resource estimate provided in the DeLamar Report)

→ 4.53 g/t Au and 262.67 g/t Ag (7.91 g/t AuEq) over 85.35m

- Including 11.74 g/t Au and 652.45 g/t Ag (20.14 g/t AuEq) over 30.48m

- Drill Hole FME-20-086 (50m beneath existing Mineral Resource estimate provided in the DeLamar Report)

→ 0.55 g/t Au and 18.16 g/t Ag (0.79 g/t AuEq) over 123.14m

-

Including 9.98 g/t Au and 16.43 g/t Ag (10.19 g/t AuEq) over 1.22m

- Drill Hole FME-20-087 (230m beneath existing Mineral Resource estimate provided in the DeLamar Report along the Alpine Vein)

→ 1.76 g/t Au and 347.37 g/t Ag (6.23 g/t AuEq) over 1.37m

- Drill Hole FME-20-088 (220m beneath the existing Mineral Resource estimate provided in the DeLamar Report along the Trade Dollar Vein)

→ 13.36 g/t Au and 13.04 g/t Ag (13.53 g/t AuEq) over 2.44m

- Drill Hole FME-20-091 (30m south of existing Mineral Resource estimate provided in the DeLamar Report)

→ 2.36 g/t Au and 2.38 g/t Ag (2.39 g/t AuEq) over 30.93 m

- Including 14.49 g/t Au and 9.94 g/t Ag (14.62 g/t AuEq) over 3.96 m

- Drill Hole FME-20-093 (250m south of existing Mineral Resource estimate provided in the DeLamar Report)

→ 8.61 g/t Au and 479.00 g/t Ag (14.78 g/t AuEq) over 1.61 m

War Eagle Drilling2

Drilling at War Eagle identified two parallel mineralized structures approximately 150m apart with strike lengths of over 500m. Those principal structures host high-grade gold and silver mineralization associated with quartz-pyrite veinlets within rhyolite breccias and brecciated volcano-sediments. The mineralization identified to date within the volcanics is considered to be within the diffuse cap which sits above the modelled high-grade veins within the underlying granite. The broad distribution of mineralization delineated by the soil geochemical anomalies indicates considerable lateral dispersion of mineralization within the permeable volcanic cap, possibly from a structure several hundred meters east of the known mineralized structures. All holes drilled in 2020 at War Eagle intersected these mineralized zones to varying degrees, highlighting the presence of high-grade gold silver concentrations in the form of 100m to 200m strike lengths in steeply plunging shoots.

On February 6, 2020, the Company announced drilling results from War Eagle, including 5.40 g/t Au and 45.85 Ag (5.99 g/t AuEq) over 3.05m at War Eagle in 150m step-out.

War Eagle exploration drilling highlight intercepts:

-

Drill hole IWE19-06: 5.40 g/t Au and 45.85 Ag (5.99 g/t AuEq) over 3.05m, located approximately 150m south of IWE19-01 and IWE19-02

-

Drill hole IWE19-04: 2.98 g/t Au and 7.27 g/t Ag (3.07 g/t AuEq) over 3.05m, located approximately 150m north of IWE19-01 and IWE19-02

-

Drill hole IWE19-05: 3.29 g/t Au and 155.57 g/t Ag (5.29 g/t AuEq) over 0.30m, located approximately 150m north of IWE19-01 and IWE19-02

___________________________________________

2Downhole thickness; true width varies depending on drill hole dip; most drill holes are aimed at intersecting the vein structures close to perpendicular therefore true widths are close to downhole widths (approximately 70% conversion ratio); Intervals reported are uncapped; Gold equivalent = g Au/t + (g Ag/t ÷ 77.70); For the intervals that were previously mined/stoped and were therefore unrecoverable and unverifiable, a grade of 0 g/t Au was inserted for compositing.

On November 19, 2020, the Company announced that it had intersected high-grade mineralization 400m north of 2019 drilling results in step-out drilling at War Eagle Mountain. This zone was first identified by soil geochemistry and confirmed by drilling in 2020. The structure is largely untested and extends at least 500m in a south-southeast direction.

War Eagle exploration drilling highlight intercepts:

- Drill Hole IWE-20-014

→ 24.20 g/t Au and 655.06 g/t Ag (32.63 g/t AuEq) over 7.62m

- Including 98.01 g/t Au and 2,782.13 g/t Ag (133.82 g/t AuEq) over 1.77m

- Drill Hole IWE-20-016

→ 1.19 g/t Au and 11.65 g/t Ag (1.34 g/t AuEq) over 30.63m

- Including 8.46 g/t Au and 9.11 g/t Ag (8.57 g/t AuEq) over 1.52m

- Drill Hole IWE-20-017

→ 21.85 g/t Au and 76.39 g/t Ag (22.84 g/t AuEq) over 1.52m

BlackSheep Drilling3

Exploration drilling began at BlackSheep in late 2020 with one drill rig expected to operate through the winter months. Two shallow drill holes were completed at the Georgianna target in 2020 to better define the structures controlling mineralization.

On February 18, 2021, the Company announced that the initial 4 drill holes (including 3 drill holes from the 2020 exploration program) from Georgianna, Milestone and Lucky Days targets within the BlackSheep District, intersected thick sections of low-sulphidation epithermal gold-silver mineralization, including several high-grade intercepts.

Drill highlights from the Georgianna targets, in the BlackSheep District, included:

- Drill hole IGE-20-002

→ 0.66 g/t Au and 117.25 g/t Ag (2.17 g/t AuEq) over 10.67m, including 1.48 g/t Au and 351.00 g/t Ag (5.99 g/t AuEq) over 3.05m

→ Broader low-grade intercepts include 0.30 g/t Au and 10.87 g/t Ag (0.44 g/t AuEq) over 41.76m

The Company intersected one of the highest-grade intercepts to date from the Milestone Deposit situated at the base of the existing resource and interpreted as indicating the location of the postulated higher-grade 'feeder zone' below, highlights included:

___________________________________________

3Downhole thickness; true width varies depending on drill hole dip; most drill holes are aimed at intersecting the vein structures close to perpendicular therefore true widths are close to downhole widths (approximately 70% conversion ratio); Intervals reported are uncapped; Gold equivalent = g Au/t + (g Ag/t ÷ 77.70); For the intervals that were previously mined/stoped and were therefore unrecoverable and unverifiable, a grade of 0 g/t Au was inserted for compositing.

- Drill hole IMS-20-015

→ 0.44 g/t Au and 77.60 g/t Ag (1.43 g/t AuEq) over 78.94 m

- Including 0.38 g/t Au and 488.00 g/t Ag (6.66 g/t AuEq) over 1.52 m;

- Including 0.28 g/t Au and 290.82 g/t Ag (4.02 g/t AuEq) over 1.68 m;

- Including 0.39 g/t Au and 288.00 g/t Ag (4.10 g/t AuEq) over 1.52 m;

- Including 1.12 g/t Au and 176.00 g/t Ag (3.39 g/t AuEq) over 1.83 m;

- Including 3.11 g/t Au and 172.00 g/t Ag (5.32 g/t AuEq) over 2.59 m.

Induced Polarization ("IP") Geophysics

A large geophysical anomaly to the west of Florida Mountain was defined with the 2020 IP Geophysical surveys in an area that has seen very limited historic drill testing. IP has proven to be a very effective tool for target generation in the DeLamar district because of the association of disseminated sulfide alteration with gold and silver mineralization. The IP data provided in the Company's September 24, 2020 news release delineated an anomaly 1,200m in length to the west of the NI 43-101 Mineral Resource estimate at Florida Mountain in the DeLamar Report in an area known as Blue Gulch. This strong geophysical anomaly coincides with an arsenic ("As") and Au soil geochemistry anomaly.

The BlackSheep IP survey was completed in July 2020. The data delineated two linear zones of chargeability and coincident resistivity at Georgianna, one of those features coincides with an outcropping vein in the Georgianna Pit. At Lucky Days, the IP delineated an extensive (300 x 200m) zone of chargeability coincident with outcropping stock-work vein mineralization similar in appearance to the mineralization at DeLamar.

Mapping and Sampling Program

On February 6, 2020, the Company announced that soil geochemical surveys at Florida Mountain delineated a 1,400m x 600m high intensity Au, Ag, As and Molybdenum ("Mo") anomaly directly to the east of the existing Florida Mountain Mineral Resource included in the DeLamar Report. The size of this anomaly is comparable to the main anomaly covering the existing Mineral Resource at Florida Mountain in the DeLamar Report and the area has limited historic drilling which together with the presence of historic workings indicate potential for both low-grade stockwork and high-grade veins in this area.

At War Eagle, a 1,000m x 200m Au and As anomaly was delineated approximately 300m east of the area drill tested in late 2019. A large complex Au/As soil anomaly, approximately the size of the footprint over DeLamar, was outlined in the BlackSheep area.

A rock chip sampling program was completed over the outcropping vein zone at Georgianna and Lucky Days areas in the southern half of BlackSheep. The sampling delineated a 300m x 100m zone of intense stockwork vein mineralization at the Lucky Days target also in BlackSheep. Please refer to the Company's news release dated September 24, 2020 for rock sampling results.

Development

Other than metallurgical drilling, the development activities in 2020 were not greatly impacted by the COVID-19 pandemic. The metallurgical drilling was eventually successfully completed in the calendar year 2020, with no effect on the metallurgical study timeline that will support the 2021 PFS.

Metallurgical Drilling4

The Company completed a total of 2,763 m of metallurgical core drilling in 2020.

The 2020 metallurgical drill program was designed to characterize gold and silver recovery variability within the oxide and transitional mineralization at the DeLamar Project. The program sought to further optimize processing options at the DeLamar and Florida Mountain Area, and to advance the Company's metallurgical knowledge as Integra moves toward a PFS on both deposits in 2021.

These results underscored the potential for high-grade in structures that have not been the target of significant modern exploration drilling, as well as the strong potential to increase the current Mineral Resource in the DeLamar Report as Integra aims to push all current drill holes beyond and below the existing Mineral Resource boundaries included in the DeLamar Report.

Results of note included:

- Drill Hole IDM-20-165

→ 17.45 g/t Au and 56.22 g/t Ag (18.18 g/t AuEq) over 2.29m

- Drill Hole IDM-20-172

→ 0.30 g/t Au and 61.30 g/t Ag (1.09 g/t AuEq) over 92.81m

Sampling and QA/QC Procedure

Thorough QA/QC protocols are followed on the DeLamar Project, including insertion of duplicate, blank and standard samples in the assay stream for all drill holes. The samples are submitted directly to AAL in Reno, Nevada for preparation and analysis. Analysis of gold is performed using fire assay method with atomic absorption ("AA") finish on a 1 assay ton aliquot. Gold results over 5 g/t are re-run using a gravimetric finish. Silver analysis is performed using ICP for results up to 100 g/t on a 5 acid digestion, with a fire assay, gravimetric finish for results over 100 g/t silver.

See "DeLamar Project - Sampling, Analysis and Data Verification" below with respect to the DeLamar Report.

Permitting

On August 20, 2020, the Company announced that it had signed a Memorandum of Understanding ("MOU") with the United States Bureau of Land Management ("BLM") to facilitate the hiring of a dedicated mineral specialist in the Marsing, Idaho BLM office that will oversee future permitting work for the DeLamar Project. In accordance with the MOU, Integra will reimburse the BLM for the costs of a dedicated mineral specialist project manager in the Marsing BLM office, who shall remain at all times independent of the Company. This BLM project manager responsible for the DeLamar Project permitting work will help the BLM manage increased workloads from current and anticipated future applications for mineral notices, operations plans/amendment approvals and environmental analyses resulting from the DeLamar Project. This funding effort is intended to increase the capacity of the local BLM office to work on DeLamar Project related applications and project requests on a priority basis, while not burdening the BLM with the cost of this increased workload.

___________________________________________

4Downhole thickness; true width varies depending on drill hole dip; most drill holes are aimed at intersecting the vein structures close to perpendicular therefore true widths are close to downhole widths (approximately 70% conversion ratio); Intervals reported are uncapped; Gold equivalent = g Au/t + (g Ag/t ÷ 77.70)

2020 saw significant efforts with respect to advancing the permitting process at the DeLamar Project. To enhance the process, Integra has maintained a focus from the outset on establishing positive partnerships with a wide selection of stakeholders. By focusing on these partnerships well in advance of submitting actionable documents to regulatory agencies, the Company intends to position itself in the best possible scenario to facilitate the permitting process in an efficient manner. Paramount to this process has been working with the BLM, the lead federal agency that the Company will engage with regarding permitting, in addition to Idaho state regulators. The MOU announced on August 20, 2020 streamlines the iterative permitting process, with the agreement allowing for an efficient communication framework between the Company and the BLM moving forward.

The ability to have initial plans reviewed for accuracy and conditionally approved by various regulatory agencies up front can add meaningful efficiencies in the permitting timeline. Being committed to transparent, straightforward, and accountable communication with stakeholders, Integra intends to facilitate a process in which the prospective mine plan being developed receives the appropriate acceptance from those stakeholders that any future development plans may impact. To this extent, actions in 2020 involving stakeholders at the regulator/agency level include:

-

Acceptance and preliminary approval of the Surface Water Sampling Program by Idaho Department of Environmental Quality ("IDEQ") and the Idaho Department of Water Resources ("IDWR");

-

Acceptance and preliminary approval of the Ground Water Drilling Plan and Sampling Program by IDEQ and IDWR; and

-

Acceptance and preliminary approval of both the Surface Water and Ground Water Sampling and Analysis Plans by IDEQ and IDWR.

Surface water and existing groundwater well sampling collected in the 2nd and 3rd quarter of 2020 have been completed. The first party air monitoring program contractor was selected and the site meteorological monitoring station became operational in early August, 2020.

Metallurgical Engineering

The 2020 engineering plans advanced steadily, building upon the concise plans outlined in the DeLamar Report. Importantly, efforts were focussed on adding Mineral Resources included in the Mineral Resource estimate in the DeLamar Report, but had yet to be included into the mine plan provided in the DeLamar Report. While the mainstay of the DeLamar Report focussed on heap-leaching (DeLamar and Florida Mountain Area oxide and transitional mineralization) and milling (Florida Mountain Area sulfide mineralization), much of the 2020 efforts were centered in the metallurgical properties of the DeLamar Area sulfide material and high-grade transitional material. Metallurgical test work on the DeLamar Area mineralization included:

- Detailed minerology;

- Sulfur and clay speciation;

- Further regrind and flotation test work;

- Albion processing test work, and other pre-oxidation methods; and

- Off-site processing of flotation concentrate at several locations in the US and Canada.

Pre-Feasibility Study

Over the course of 2020, the Company undertook several pre-feasibility and environmental baseline studies at the DeLamar Project, including geotechnical drilling and test work for pit slope design and stability.

On December 3, 2020, the Company announced the engagement of Mine Development Associates, a division of RESPEC ("MDA") as the lead consultant for the PFS at the DeLamar Project.

The PFS is projected to take approximately 10 months to complete, with results currently expected in the 4th quarter of 2021.

Social and Environmental

In response to the unprecedented circumstances surrounding the COVID-19 pandemic, several initiatives were undertaken in Idaho to support the local community during these extraordinary times. In partnership with the Jordan Valley Lions Club, Integra staff conducted weekly grocery supply trips to the Boise Valley, allowing the community's elderly and at-risk population the opportunity to stay home and avoid travelling to more populated centers. In addition, and in cooperation with several Idahoan companies through an initiative titled Curds & Kindness, Integra collaborated with Idaho's dairy farmers in redirecting their excess supply of dairy products to Idaho and Oregon food banks. The excess supply stems from the lack of demand in the restaurant industry, one of the many sectors that have been severely impacted by COVID-19.

Integra continues to implement strict operational measures in response to the COVID-19 pandemic, which restrict contact between employees and limits non-essential access to the DeLamar Project site. When deemed necessary, particularly following periods of higher travel within the community such as following breaks and holidays, site-wide testing of the entire employee-base has to date effectively allowed the Company to limit COVID-19 transmission on site.

Stakeholder meetings continued throughout the year where possible, either by video conference or in socially distanced settings as the Company continues to build relationships with surrounding communities that future operations may touch.

As part as its local initiatives, the Company extended a secured US$140,000 loan to a local business owner in August 2020 to complete the construction of a restaurant in Jordan Valley, the closest community to the DeLamar Project. This restaurant will be the sole restaurant serving the local community and the Company's employees and contractors.

As part of Integra's ESG commitment to prioritizing environmental stewardship at every stage of the project life cycle, the Company has engaged Warm Springs Consulting of Boise, Idaho, as the consulting/engineering firm to evaluate several sustainability-driven option studies that will potentially be incorporated into the anticipated PFS.

Water treatment operations followed their regular course at the DeLamar Project, with system updates to the water treatment facility completed and in operation, allowing for more efficient water filtration and less bi-product waste creation in the process.

No material environmental or health and safety incidents were reported in 2020.

Trends and Outlook

Although management has put in place all necessary measures to protect its employees' safety and to secure essential site activities, should the virus spread, or travel bans remain in place or should one of the Company's staff members or consultants become infected, the Company's ability to advance the DeLamar Project may be impacted. The Company continues to monitor the situation and the impact the virus may have on the DeLamar Project.

The head office of the Company (Vancouver, BC) will remain closed and employees will continue to work remotely from home until further notice.

As noted, the Company is working towards a PFS on the DeLamar Project, anticipated in the 4th quarter of 2021. In addition, the Company will continue its dual track strategy for 2021, consisting of exploration drilling designed to expand the Mineral Resource base and development study and permitting work designed to de-risk the DeLamar Project.

Corporate

On February 25, 2021, the Company announced the appointment of Carolyn Clark Loder to the Board.

Development

A key objective for 2021 will be to complete the PFS in the 4th quarter. To achieve this goal, extensive metallurgical test work will be carried out in the first half of the year to de-risk and improve project economics. There will also be a significant condemnation, geotechnical and groundwater drilling program in 2021. On the permitting front, surface, groundwater, geochemistry, wetlands, wildlife, aquatic, cultural and associated baseline studies, along with the management of these efforts, will extend throughout the year.

Current Pre-Feasibility Level Studies Aimed at Enhanced Silver Recoveries

Several key trade-off studies are currently under-way, aimed to define the cost-benefit of higher metal recoveries, specifically silver, in future development scenarios at the DeLamar Project.

Recent metallurgical test work since the DeLamar Report is being analyzed for opportunities to improve silver recovery. A deeper evaluation into the size sensitivity of both gold and silver recovery is underway, to be included in the PFS. This includes consideration of HPGR technology in the final stage of the crushing circuit for the heap leach process and/or implementation of a larger milling and agitated leach circuit for higher grade transitional mineralization, both of which would effectively produce finer crushed material with enhanced silver recovery potential.

Processing additional transitional mineralization through a mill circuit could potentially yield greater overall metal recovery, including silver, than through placement of crushed material on the leach pad.

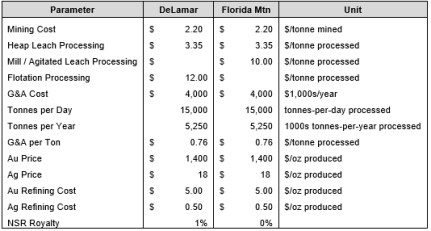

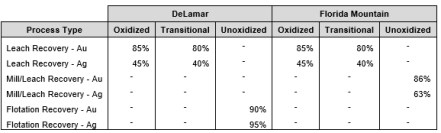

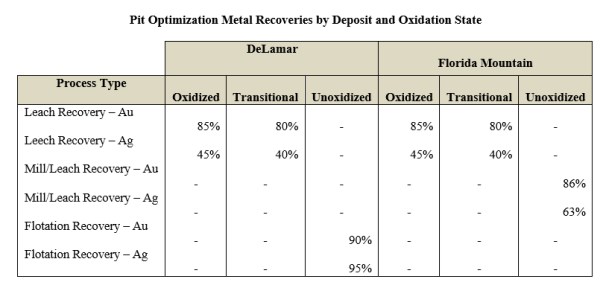

Florida Mountain unoxidized material is processed through the existing milling scenario in the DeLamar Report. Test work has shown that the unoxidized material from Florida Mountain is amenable to gravity concentration, followed by flotation of the gravity tails, with regrinding and agitated cyanide leaching of the flotation concentrate. Mill recoveries on this material in the DeLamar Report were 90% for gold and 80% for silver with a relatively course grind size of 212 µm. The Company is completing additional test work on the DeLamar deposit unoxidized mineralization which was not included in the DeLamar Report. This test work includes various pre-cyanidation treatments options, including fine grinding and pre-aeration, and will be reevaluated with current metal prices and better-defined costs.

Exploration

The 2021 exploration program is expected to comprise of 10,000 m of drilling along with additional IP surveys, soil sampling and geological mapping and prospecting. The drill program will focus on the following areas:

The Florida Mountain Deposit (4,000 m)

One of two exploration drill rigs on the DeLamar Project will operate at Florida Mountain through the winter months. Drilling at Florida Mountain will be dual-focused, including follow-up exploration on the high-grade shoots and structures below the existing resource and expanding the existing low-grade resource through drilling geochemical and geophysical anomalies to the east and west of the existing Mineral Resource in the DeLamar Report.

The Company has identified multiple high-grade gold-silver shoots at Florida Mountain. Integra's exploration team has modeled 7 high-grade vein structures that appear similar in size and orientation to the historically productive high-grade Trade Dollar - Black Jack vein system. Most historic underground production stemmed from the Trade Dollar - Black Jack vein, while the remaining 6 veins saw limited production up until mining operations ceased with the start of World War I. The identified vein zones have an aggregate strike length of over 7,000m. Within these vein zones are steeply dipping high-grade shoots with strike lengths of up to 200m and down dip extensions of up to 300m which are interpreted as having developed at structural intersections. Based on recent drill intercepts, the Company anticipates that the high-grade shoots are likely to have widths of between 1m and 8m.

Drilling is also planned to take place in the Florida Keys area, a large geochemical anomaly located immediately to the east of the resource that has seen limited drilling. The Florida Keys geochemical anomaly is of similar strength and size to the existing Mineral Resource estimate in the DeLamar Report footprint at the Florida Mountain Area deposit. The Company also intends to drill in Rich Gulch, a target located in a large zone of IP chargeability that was identified to the west of the Florida Mountain Area as part of a 2020 geophysical survey. Based on limited historic drilling and the presence of historic underground workings in this area the Company sees potential for both additional low-grade and high-grade underground mineralization.

War Eagle Mountain (2,000 m)

During the 2019 and 2020 drill programs at War Eagle, the Company intersected high-grade gold-silver mineralization within the volcanic unit overlying the entire area. In 2020, the Company identified a second high-grade shoot 400m to the north of the 2019 drill holes. This second structure is interpreted over a strike length of approximately 550m south-southeast and is largely untested. The geochemical soil anomaly that led the Company to this new structure is interpreted as being lateral leakage outward along the base of the latite flow, presumably emanating from the eastern most structure identified in the 2020 drill program.

Drilling in 2021 will continue to test these parallel structures at War Eagle. In addition, the Company plans on completing a detailed IP program to generate targets within a large geochemical anomaly to the east of the 2019 and 2020 drill holes locations.

BlackSheep and DeLamar (Henrietta Ridge) (4,000 m)

Exploration drilling at BlackSheep is underway with one drill rig expected to operate through the winter months. The drill campaign at BlackSheep will focus on the Georgianna and Lucky Days targets. BlackSheep is host to extensive areas of sinter and opaline silica cut by high-level epithermal veining and brecciation. Due to the shallow level of erosion at BlackSheep, very limited exploration drilling completed by previous operators was shown to be too shallow to properly evaluate the potential for high-grade vein style mineralization.

Two shallow drill holes have been completed at the Georgianna target to better define the structures controlling mineralization. Deeper, follow-up drill holes are planned at the Georgianna target for this year to test the productive zone at approximately 200m below the current surface.

The Company also plans on drilling the Henrietta Ridge target in 2021. Henrietta Ridge is located between the DeLamar deposit and the BlackSheep area. Historic drilling completed by previous operators along with geophysical surveys suggest mineralization from the DeLamar deposit extends along a northwest corridor from the current resource through Henrietta Ridge.

THE BUSINESS

General Overview

The primary focus of the Company is the advancement of its DeLamar Project, consisting of the neighboring DeLamar Area and Florida Mountain Area in the heart of the historic Owyhee County mining district in south western Idaho. The management team comprises the former executive team from Integra Gold Corp. ("Integra Gold").

Integra owns no producing properties and, consequently, has no current operating income or cash flow from the properties it holds, nor has it had any income from operations in the past three financial years. As a consequence, operations of Integra are primarily funded by equity financings.

Please see "General Development of the Business - Three-Year History" and "General Development of the Business - Trends and Outlook" sections above and "DeLamar Project" section below for further details on the DeLamar Project and development thereof.

Specialized Skills

Integra's business requires specialized skills and knowledge in the areas of geology, drilling, planning, implementation of exploration programs, compliance, engineering, metallurgy, economic studies, project development and permitting. To date, Integra has been able to locate and retain such professionals in Canada and the United States, and believes it will be able to continue to do so.

Competitive Conditions

Integra operates in a very competitive industry and competes with other companies, many of which have greater technical and financial facilities for the acquisition and development of mineral properties, as well as for the recruitment and retention of qualified employees and consultants.

Business Cycles

The precious metals sector is very volatile and cyclical. The sector specifically suffered significant declines from 2011 to 2019. During the same period the financial markets for mining in general, and mineral exploration and development in particular, were relatively weak. However, 2020 was a much stronger year for prices of gold and silver and for mining equities. Financial markets for mining have been relatively strong since. The price of gold reached a high in 2020, mostly fueled by the uncertainty created by the COVID-19 pandemic. Fundamentals that have traditionally supported a strong gold price are present, but there is no certainty that the prices of gold and silver will remain high and that the financial markets for mining will remain strong.

In addition to commodity price cycles and recessionary periods, exploration activity may also be affected by seasonal and irregular weather conditions in Idaho.

Environmental Protection Requirements

Integra's operations are subject to environmental regulations promulgated by government agencies from time to time. Environmental legislation provides for restrictions and prohibitions on spills, releases or emissions of various substances produced in association with certain mining industry operations, such as seepage from tailings disposal areas, and the use of cyanide which would result in environmental pollution. A breach of such legislation may result in imposition of fines and penalties. Certain types of operations may also require the submission and approval of environmental impact assessments.

Environmental legislation is evolving in a manner that means stricter standards, and enforcement, fines and penalties for non-compliance are more stringent. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies including its directors, officers and employees.

The cost of compliance with changes in governmental regulations has the potential to reduce the profitability of operations.

Employees

During fiscal 2020, Integra had thirty-six (36) full-time employees, with eight (8) based in Canada, one (1) employee based in Denver (Colorado), two (2) employees in Reno (Nevada), four (4) employee in Boise (Idaho), one (1) employee in Utah and twenty (20) employees on site in Idaho.

Foreign Operations

Mineral exploration and mining activities in the United States may be affected in varying degrees by government regulations relating to the mining industry. Any changes in regulations or shifts in political conditions may adversely affect Integra's business. Operations may be affected in varying degrees by government regulations with respect to restrictions on permitting, production, price controls, income taxes, expropriation of property, environmental legislation and mine safety.

Social and Environmental Policies

Integra has adopted a Code of Business Conduct and Ethics ("Code") that is intended to document the principles of conduct and ethics to be followed by employees, consultants, officers and directors of Integra. Its purpose is to:

-

promote honest and ethical conduct, including the ethical handling of actual or apparent conflicts of interest between personal and professional relationships;

-

promote avoidance of conflicts of interest, including disclosure to an appropriate person of any material transaction or relationship that reasonably could be expected to give rise to such a conflict;

-

promote full, fair, accurate, timely and understandable disclosure in reports and documents that Integra files with, or submits to, the securities regulators and in other public communications made by Integra;

-

promote compliance with applicable governmental laws, rules and regulations;

-

promote the prompt internal reporting to an appropriate person of violations of the Code;

-

promote accountability for adherence to the Code;

-

provide guidance to employees, officers and directors to help them recognize and deal with ethical issues;

-

provide mechanisms to report unethical conduct; and

-

help foster Integra's culture of honesty and accountability.

Integra expects all of its employees, officers and directors to comply at all times with the principles in the Code.

The Company also adopted a Safety, Environmental and Social Responsibility Policy to be followed by employees, consultants, officers and directors of Integra. Its purpose is to outline how Integra, together with its directors, officers, employees, consultants and contractors, will conduct its business in a safe and environmentally friendly manner and to the highest standards of corporate social responsibility.

Risk Factors

The Company is subject to a number of risks and uncertainties due to the nature of its business. The Company's exploration activities expose it to various financial and operational risks that could have a significant impact on its level of operating cash flows in the future. Readers are advised to study and consider risk factors stressed below.

The following are identified as the main risk factors affecting the Company.

Coronavirus (COVID-19) and Global Health Crisis

The COVID-19 global outbreak and efforts to contain it may have an impact on the Company's business. The Company continues to monitor the situation and the impact the virus may have on the DeLamar Project. Should the virus spread, travel bans remain in place or should one of the Company's team members or consultants become infected, the Company's ability to advance the DeLamar Project may be impacted. Similarly, the Company's ability to obtain financing and the ability of the Company's vendors, suppliers, consultants and partners to meet obligations may be impacted as a result of COVID-19 and efforts to contain the virus.

Exploration and Development

Resource exploration and development is a speculative business and involves a high degree of risk. There is no known body of commercial ore on the DeLamar Project. There is no certainty that the expenditures to be made by Integra in the exploration of the DeLamar Project or otherwise will result in discoveries of commercial quantities of minerals. The marketability of natural resources which may be acquired or discovered by Integra will be affected by numerous factors beyond the control of Integra, including, but not limited to, the COVID-19 pandemic. These factors include market fluctuations, the proximity and capacity of natural resource markets and processing equipment, government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in Integra not receiving an adequate return on invested capital.

Preliminary Economic Assessment

The PEA for the DeLamar Project is an early stage estimate that does not have sufficient certainty to constitute a pre-feasibility study or a feasibility study. Integra has not completed pre-feasibility or feasibility level work and analysis that would allow the Company to declare Proven or Probable Mineral Reserves at the DeLamar Project, and no assurance can be given that the Company will ever be in a position to declare a Proven or Probable Mineral Reserves at the DeLamar Project. In particular, the PEA for the DeLamar Project contains estimated capital costs and operating costs which are based on anticipated tonnage and grades of metal to be mined and processed, the expected recovery rates and other factors, none of which have been completed to date to a pre-feasibility study or a feasibility study level. Whether Integra completes a feasibility study on the DeLamar Project, and thereby delineates Proven or Probable Mineral Reserves, depends on a number of factors, including:

- the particular attributes of the deposit (including its size, grade, geological formation and proximity to infrastructure);

-

metal prices, which are highly cyclical;

-

government regulations (including regulations relating to taxes, royalties, land tenure, land use and permitting); and

-

environmental protection considerations.

We cannot determine at this time whether any of the estimates will ultimately be correct.

Financing Risks

Integra will require additional funding to conduct future exploration programs on the DeLamar Project and to conduct other exploration programs. If Integra's current exploration programs are successful, additional funds will be required for the development of an economic mineral body and to place it into commercial production. In addition, Integra has fixed payment obligations but no source of revenue. The DeLamar Project requires reclamation work of US$1,000,000 to US$1,800,000 per year for the foreseeable future, though this number is expected to decrease over time, all of which will need to be funded by Integra from available cash. The only sources of future funds presently available to Integra are the sale of equity capital, or the offering by Integra of an interest in its properties. There is no assurance that any such funds will be available to Integra on acceptable terms, on a timely basis or at all. Failure to obtain additional financing on a timely basis could cause Integra to reduce or terminate its proposed operations and otherwise could have a material adverse effect on its business.

Volatility of Commodity Prices

The development of the Company's properties is dependent on the future prices of gold and silver. As well, should any of the Company's properties eventually enter commercial production, the Company's profitability will be significantly affected by changes in the market prices of gold and silver. Precious metals prices are subject to volatile price movements, which can be material and occur over short periods of time and which are affected by numerous factors, all of which are beyond the Company's control. Such factors include, but are not limited to, interest and exchange rates, inflation or deflation, fluctuations in the value of the U.S. dollar and foreign currencies, global and regional supply and demand, speculative trading, the costs of and levels of precious metals production, and political and economic conditions. Such external economic factors are in turn influenced by changes in international investment patterns, monetary systems, the strength of and confidence in the U.S. dollar (the currency in which the prices of precious metals are generally quoted) and political developments. The effect of these factors on the prices of precious metals, and therefore the economic viability of the DeLamar Project, cannot be accurately determined. The prices of gold and silver have historically fluctuated widely, and future price declines could cause the development of (and any future commercial production from) the DeLamar Project to be impracticable or uneconomic. As such, the Company may determine that it is not economically feasible to commence commercial production, which could have a material adverse impact on the Company's financial performance and results of operations. In such a circumstance, the Company may also curtail or suspend some or all of its exploration activities.

Limitations on the Mineral Resource Estimates

The Mineral Resource estimates on the DeLamar Project are estimates only. No assurance can be given that any particular level of recovery of minerals will in fact be realized or that identified Mineral Resources will ever qualify as a commercially mineable (or viable) deposit which can be legally and economically exploited. In addition, the grade of mineralization which may ultimately be mined may differ from that indicated by drilling results and such differences could be material. Production can be affected by such factors as permitting regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations and work interruptions. The estimated Mineral Resources on the DeLamar Project should not be interpreted as assurances of commercial viability or of the profitability of any future operations. Moreover, all of the Mineral Resources are reported at an "inferred" level. Inferred Mineral Resources have a substantial degree of uncertainty as to their existence, and economic and legal feasibility. Accordingly, there is no assurance that Inferred Mineral Resources reported herein will ever be upgraded to a higher category. Investors are cautioned not to assume that part or all of an Inferred Mineral Resource exists, or is economically or legally mineable.

Reliance on Management

The success of the Company depends to a large extent upon its abilities to retain the services of its senior management and key personnel. The loss of the services of any of these persons could have a materially adverse effect on the Company's business and prospects. There is no assurance the Company can maintain the services of its directors, officers or other qualified personnel required to operate its business.

No History of Earnings

Integra has no history of earnings or of a return on investment, and there is no assurance that the DeLamar Project or any other property or business that Integra may acquire or undertake will generate earnings, operate profitably or provide a return on investment in the future. Integra has no capacity to pay dividends at this time and no plans to pay dividends for the foreseeable future.

Negative Operating Cash Flow

The Company is an exploration stage company and has not generated cash flow from operations. The Company is devoting significant resources to the development and acquisition of its properties, however there can be no assurance that it will generate positive cash flow from operations in the future. The Company expects to continue to incur negative consolidated operating cash flow and losses until such time as it achieves commercial production at a particular project. The Company currently has negative cash flow from operating activities.

Capital Resources