Integra Resources Corp.

Management's Discussion and Analysis

For the Three and Six-Month Periods Ended

June 30, 2020 and 2019

Expressed in Canadian Dollars

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

This portion of this quarterly report provides Management's Discussion and Analysis ("MD&A") of the financial condition and results of operations, to enable a reader to assess material changes in financial condition and results of operations as at, and for the three and six-month periods ended June 30, 2020, in comparison to the corresponding prior-year periods. The MD&A is intended to help the reader understand Integra Resources Corp. ("Integra", "we", "our" or the "Company"), our operations, financial performance and present and future business environment.

This MD&A has been prepared by management as at August 13, 2020 and should be read in conjunction with the unaudited interim condensed consolidated financial statements of Integra for the three and six-month periods ended June 30, 2020 and 2019 and the Company's audited consolidated financial statements for the years ended December 31, 2019 and 2018 prepared in accordance with International Financial Reporting Standards ("IFRS"). Further information on the Company can be found on SEDAR at www.sedar.com and the Company's website, www.integraresources.com.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if: (i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it important in making an investment decision; or (iii) it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

CORPORATE SUMMARYIntegra Resources Corp. is a mineral resources company engaged in the acquisition, exploration and development of mineral properties in the Americas. The primary focus of the Company is advancement of its DeLamar gold and silver project ("DeLamar Project"), consisting of the neighbouring DeLamar Deposit and Florida Mountain Deposit ("Florida Mtn" or "Florida Mountain") in the heart of the historic Owyhee County mining district in south western Idaho. The management team comprises the former executive team from Integra Gold Corp. The Company announced in September 2019 a positive Preliminary Economic Assessment and expect completing a Pre-Feasibility Study in 2021.

As at August 13, 2020, the directors and officers of the Company were:

George Salamis President, Director and CEO

Stephen de Jong Chairman and Director

Andrée St-Germain CFO and Corporate Secretary

Max Baker Vice President Exploration

Timothy Arnold Chief Operating Officer

David Awram Director

Timo Juristo Director

Anna Ladd-Kruger Director

C.L. "Butch" Otter Director

The Company's head office is located at 1050 - 400 Burrard Street, Vancouver, BC V6C 3A6 and its registered office is located at 2200 HSBC Building, 885 West Georgia Street Vancouver, BC V6C 3E8.

The Company trades on the TSX Venture, under the trading symbol "ITR" and trades in the United States on the NYSE American under the stock symbol "ITRG".

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

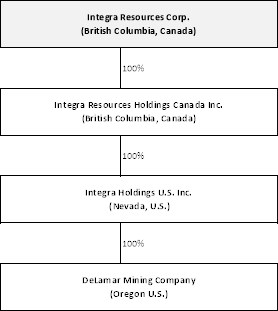

The following diagram illustrates the intercorporate relationships among Integra and its subsidiaries, as well as the jurisdiction of incorporation of each entity.

Q2 2020 IN REVIEW

Corporate

For the safety of all employees, the Company closed its corporate office (Vancouver, BC) in mid-March as a result of the COVID-19 global outbreak. All corporate employees have been working remotely from home since. The most significant impact of COVID-19 has been the cancelation of all travel. The Company has however remained extremely active on the marketing front, and has attended several virtual investors conferences, and held virtual meetings with investors. The Company also maintained a steady pace of exploration at their DeLamar exploration project in Idaho in addition to various feasibility-level studies during the course of Q2.

The Company held its Annual General and Special Meeting of shareholders ("AGSM") on June 16, 2020. A total of 26,452,596 common shares have been voted, representing 55.3% of the Company's outstanding shares. All of the directors were re-elected, and all other resolutions were approved by the Company's shareholders.

On June 29, 2020, the Company completed its continuation from Ontario to British Columbia. The continuation to British Columbia was approved at the Company's AGSM of shareholders on June 16, 2020. The Company's new registered and record office is located at 2200 HSBC Building, 885 West Georgia Street Vancouver, BC V6C 3E8.

Exploration

For the safety of all employees, the Company suspended drilling and exploration activities in mid-March. The U.S. Government has declared mining an essential service. With comprehensive operational procedures in-place, which were specifically designed to mitigate the risk of disease transmission amongst essential site staff and crews, the Company resumed drilling in mid-May.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

The Company completed a total of 1,234m of exploration core drilling this quarter, for a total of 2,318m this year.

On July 29, 2020, the Company announced drilling results from its first four drill holes at Florida Mtn, representing approximately 1,550 m of the 7,000 m exploration drill program at Florida Mtn. The holes intersected significant high-grade gold and silver mineralization both within and outside of the existing NI 43-101 resource boundary. These drill results provide evidence that structurally-controlled high-grade veins exist below the current resource and that further drill definition could potentially be interpreted and modelled as high-grade mill feed in future economic studies.

Florida Mnt exploration drilling highlight intercepts include:

- Drill Hole FME-20-076

- 1.99 grams per tonne ("g/t") gold ("Au") and 24.17 g/t silver ("Ag") (2.30 g/t gold equivalent ("AuEq")) over 117.04 m

• Including 72.37 g/t Au and 82.00 g/t Ag (73.43 g/t AuEq) over 1.52 m

• Including 6.77 g/t Au and 68.62 g/t Ag (7.65 g/t AuEq) over 10.97 m

- 10.08 g/t Au and 1,233.77 g/t Ag (25.96 g/t AuEq) over 3.60 m

• Including 34.40 g/t Au and 4,075.40 g/t Ag (86.85 g/t AuEq) over 0.88 m

- 6.37 g/t Au and 1,459 g/t Ag (25.14 g/t AuEq) over 1.52 m

- Drill Hole FME-20-077

- 1.63 g/t Au and 17.13 g/t Ag (1.85 g/t AuEq) over 113.69 m

• Including 72.07 g/t Au and 63.16 g/t Ag (72.88 g/t AuEq) over 1.52 m

The Company commenced its mapping and sampling program at Black Sheep in May and anticipates continuing until Q4.

Development

The Company completed a total of 1,307 m of metallurgical core drilling in the second quarter of 2020, for a total of 2,526 m this year. Various methods of metallurgical treatment of the sulfide mineralization at DeLamar are being researched at McClelland Labs. Initial benchtop comparisons of all metallurgical treatment options as compared to capital and operating will be carried out this year. Compositing of Florida Mtn drill core is being carried out for column testwork.

Drafts of the overall Framework Study Plan, Groundwater Baseline Study Plan and the Surface Water Baseline Study Plan were completed and submitted to the Bureau of Land Management ("BLM"), Idaho Department of Environmental Quality ("IDEQ") and Idaho Department of Water Resources ("IDWR") for review and comments. The Air Quality Baseline study was initiated with the submittal and acceptance by IDEQ. The Company anticipates the meteorological tower to be installed and operational in Q3. Baseline data collection plans for 2020 fieldwork for the existing and new surface water and existing groundwater wells commenced in Q2 and will continue in Q3. Significant communications with the BLM and State continue in preparation for submitting other plans in 2020.

Other than metallurgical drilling, the development activities during the second quarter of 2020 have not been greatly impacted by the COVID-19 pandemic to date.

Social and Environmental

In response to the unprecedented circumstances surrounding the COVID-19 pandemic, several initiatives are underway to support the local community during these unprecedented times. In partnership with the Jordan Valley Lions Club, Integra staff are conducting weekly grocery shopping trips to the Boise Valley, allowing the community's elderly and at-risk population the opportunity to stay home and avoid travelling to more populated centers. In addition, and in cooperation with several Idahoan companies through an initiative titled Curds & Kindness, Integra is working with Idaho's dairy farmers in redirecting their excess dairy supply to Idaho and Oregon food banks. The excess supply stems from the lack of demand in the restaurant industry, one of the many sectors that have been severely impacted by COVID-19.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

In British Columbia, Integra led an effort with the Association for Mineral Exploration BC ("AMEBC") that raised over $100,000 within the BC mining community to support foodbanks that serve rural, remote, and Indigenous communities. Stakeholder meetings have continued throughout the summer where possible, either by video conference or in socially distanced outdoor settings.

Water treatment operations followed their regular course, with several studies conducted looking to evaluate opportunities to increase efficiencies in the water treatment plant. Integra continues to implement strict operational measures in response to the COVID-19 pandemic, which restrict contact between employees.

No environmental or health and safety incidents were reported this quarter.

2020 OUTLOOK

Although management has put in place all necessary measures to protect its employees' safety and to secure essential site activities, should the virus spread, or travel bans remain in place or should one of the Company's staff members or consultants become infected, the Company's ability to advance the DeLamar Project may be impacted. The Company continues to monitor the situation and the impact the virus may have on the DeLamar Project.

The head offices (Vancouver, BC) will remain closed and employees will continue to work remotely from home until further notice.

The Company has adopted a dual track strategy for 2020, consisting of exploration drilling designed to expand the mineral resource base and development study and permitting work designed to de-risk the DeLamar Project.

Exploration

The Company's drill program in 2020 will focus strongly on exploration upside, in contrast to 2019's program which included a high proportion of necessary infill, metallurgical and confirmatory drilling in the lead up to the maiden PEA. In addition to rapidly advancing the DeLamar Project since its acquisition in late 2017, Integra has also quadrupled its land package to more than 27,000 acres. This additionally acquired exploration ground hosts multiple high-grade and bulk-tonnage low-grade targets identified through extensive airborne and induced polarization (IP) geophysics, soil geochemical sampling, historic data compilation, and other studies.

The planned 2020 exploration work programs on these targets include:

Florida Mountain Deposit:

Florida Mtn Drilling: Approximately 7,000 m Core Drilling Program (Started in May)

The first drill rig at Florida Mountain is conducting high-grade exploration into the vein system below Florida Mountain. In late July, a second diamond drill rig was added to the Florida Mountain campaign. While the majority of recent drill data gathered to date at Florida Mountain is within the shallow volcanics, compilation work conducted over the course of the winter on historic Trade Dollar - Black Jack underground stope measurements indicates greater continuity and higher gold and silver grades in the basement granite than within the overlying volcanics. Stratigraphically, from top to bottom at Florida Mountain, low-grade disseminated open-pitable resources occur almost entirely in overlying felsic volcanics. In contrast, high-grade underground stopes are located mainly within the underlying granite, which is the more favorable high-grade host rock. To date, only very limited drilling for high-grade mineralized shoots has been conducted within the underlying granites, which will now form the basis for many of the high-grade targets to be tested in the program commencing momentarily. Please refer to the "Q2 in Review" section above for drilling results from the first 1,500m of drilling at Florida Mtn.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Drilling on the eastern anomaly at Florida Mountain will also test the potential for additional high-grade veins at depth. Integra's exploration team identified four additional roughly parallel vein structures that are similar in size and orientation to the historically productive high-grade Trade Dollar - Black Jack vein system. These 4 additional vein structures are located below the eastern anomaly at Florida Mountain, east of the historic Trade Dollar - Black Jack vein system, and will be drilled in conjunction with this anomaly. The aggregate strike length of these recently interpreted veins is over 5,000 m and represents several significant high-grade targets.

Florida Mtn Induced Polarization (IP) Survey

The IP geophysical field crews are anticipated to move to Florida Mountain in late August to mid-September to conduct surveys designed to highlight possible expansions to the Florida Mountain sulphides, situated below the current oxide and transitional resource. As depicted in the current NI43-101 PEA released in Sept 2019, while most of the contemplated production plan calls for heap leaching of oxide and transitional resources at Florida Mountain and DeLamar, the development plan also includes the construction of a 2,000 tpd mill that will be designed to treat Florida Mountain sulphide mineralization. Test work conducted on Florida Mountain sulphide mineralization in 2019 demonstrates that a recovery of over 90% gold and 80% silver is to be expected from the milling and leaching of sulphide material from the Deposit.

War Eagle Mountain:

War Eagle Drilling: Approximately 4,000m Core Drilling Program Starting in Mid-August

War Eagle Mountain has produced several of the highest-grade drill results to date from the DeLamar Project. Located approximately 3 km from Florida Mountain Deposit, War Eagle's history is well documented as the one of the highest-grade mines in the Western US during the late 1800's and early 1900's. At War Eagle, Integra's drilling, together with a compilation of historical work, has identified that gold and silver occurs in several moderately to steeply plunging high-grade "shoots." These shoots are zones of higher-grade mineralization, developed due to local structural influences, within a more extensive, comparatively lower-grade zone.

The intent of this summer's 5,000 m RC drill program at War Eagle will be to complete close-spaced drilling on these mineralized shoots, tracing them to high-grade feeder veins in the basement granite where historic high-grade mining took place, and into areas where undrilled soil geochemical anomalies exist on extension.

Black Sheep Area:

Black Sheep Drilling: Approximately 1,500m Core Drilling Program Starting in October

The Black Sheep area is located northwest of the DeLamar Deposit and hosts multiple low-sulphidation epithermal centers within a vast 5 km x 5 km area that is largely undrilled and hosts similar geochemical and geophysical signatures to the DeLamar and Florida Mountain Deposits. Significant soil geochemical anomalies, along with IP anomalies, have delineated targets throughout Black Sheep, in specific areas including Georgiana, Twin Peaks, Statue and Spain Hills, Argentum and Lucky Days. Initial rock chip sampling conducted by Integra in 2018 and 2019 has returned gold assays typically ranging from 0.2 g/t to 4.5 g/t Au, and silver values in several assays greater than 4,000 g/t Ag. These target areas hosting the various soil geochemical anomalies have sizable signatures akin to DeLamar and Florida Mountain, the largest of which is approximately 2 km x 2 km.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Black Sheep Induced Polarization (IP) Survey

IP geophysics work has commenced in the Black Sheep area northwest of the DeLamar Deposit in June, during which time Integra's exploration team will advance the mapping of targets at Black Sheep before the drill testing that is currently scheduled in the fall.

Mapping and sampling program at Black Sheep is ongoing.

Development

The Company will continue to de-risk and advance the Project towards pre-feasibility and permitting on several other fronts. Various pre-feasibility level studies have been initiated on the Project and will continue throughout the year, including:

- Pre-feasibility level variability metallurgical test work designed to show gold-silver recovery within the oxide and transitional mineralization for the purposes of heap leaching;

- Extensive metallurgical testwork to better define detailed heap leach and unoxidized processing methods and provide engineering confidence levels for future technical studies;

- Various environmental baseline studies have been identified and will begin development of historical document review and developing a Plan of Study. Additional studies include Wetlands, Springs and Seeps, Cultural Resources, Fisheries, Vegetation and Geochemistry. These studies are designed to collect data which will support data needs for the National Environmental Policy Act ("NEPA") process;

- In July, Integra entered into a Memorandum of Understanding with the BLM to fund the hiring of a dedicated project manager with minerals specific and NEPA experience, to streamline the submittal and review process in support of site exploration and groundwater drilling;

- Initial BLM and State of Idaho engagement on work plans and outlining an expedited path forward for submitting a Plan of Operations to the BLM.

PROPERTIES

1. DeLamar Project, Idaho

The DeLamar Project consists of the neighbouring DeLamar Deposit and Florida Mountain Deposit.

The bulk of the information in this section is derived from the Technical Report and Preliminary Economic Assessment for the DeLamar and Florida Mountain Gold - Silver Project, dated October 22, 2019 (the "Report" or the "PEA") prepared by Michael M. Gustin, C.P.G., Steven I. Weiss, C.P.G., and Thomas L. Dyer, P.E., of Mine Development Associates ("MDA"), which has been filed with Canadian securities regulatory authorities and prepared pursuant to NI 43-101. The DeLamar Report is available for review under the Company's issuer profile on SEDAR at www.sedar.com. Mr. Gustin, Mr. Weiss and Mr. Dyer are Qualified Persons under NI 43-101.

Project Description, Location and Ownership

The DeLamar project consists of 748 unpatented lode, placer, and millsite claims, and 16 tax parcels comprised of patented mining claims, as well as certain leasehold and easement interests, that cover approximately 8,100 hectares in southwestern Idaho, about 80 kilometers southwest of Boise. The property is approximately centered at 43°00′48″N, 116°47′35″W, within portions of the historical Carson (Silver City) mining district, and it includes the formerly producing DeLamar mine last operated by Kinross. The total annual land-holding costs are estimated to be US$321,626. All mineral titles and permits are held by the DeLamar Mining Company ("DMC"), an indirect, 100% wholly owned subsidiary of Integra that was acquired from Kinross through a Stock Purchase Agreement in 2017.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

A total of 284 of the unpatented claims were acquired from Kinross, 101 of which are subject to a 2.0% net smelter returns royalty ("NSR") payable to a predecessor owner. This royalty is not applicable to the current project resources.

There are also six lease agreements covering 26 patented claims and one unpatented claim that require NSR payments ranging from 2.5% to 5.0%. One of these leases covers a small portion of the DeLamar area resources and one covers a small portion of the Florida Mountain area resources, with 5.0% and 2.5% NSRs applicable to maximums of US$50,000 and US$650,000 in royalty payments, respectively.

The property includes 1,355 hectares under six leases from the State of Idaho, which are subject to a 5.0% production royalty of gross receipts plus annual payments of US$23,252. One of these leases has been issued and five are pending issuance. The State of Idaho leases include very small portions of both the DeLamar and Florida Mountain resources.

Kinross has retained a 2.5% NSR royalty that applies to those portions of the DeLamar area claims that are unencumbered by the royalties outlined above (the "Kinross Royalty"). The Kinross Royalty was subsequently purchased by Maverix Metals Inc ("Maverix) on December 19, 2019. The Maverix royalty applies to more than 90% of the current DeLamar area resources, but this royalty will be reduced to 1.0% upon Maverix receiving total royalty payments of C$10,000,000.

DMC also owns mining claims and leased lands peripheral to the DeLamar project described above. These landholdings are not part of the DeLamar project, although some of the lands are contiguous with those of the DeLamar and Florida Mountain claims and state leases.

The DeLamar project historical open-pit mine areas have been in closure since 2003. Even though a substantial amount of reclamation and closure work has been completed to date at the site, there remain ongoing water-management activities and monitoring and reporting. A reclamation bond of US$2,817,329 remains with the Idaho Department of Lands ("IDL") and a reclamation bond of US$100,000 remains with the Idaho Department of Environmental Quality. A reclamation bond in the amount of US$51,500 has been placed with the U.S. Bureau of Land Management ("BLM") for exploration activities on public lands.

Exploration and Mining History

Total production of gold and silver from the DeLamar - Florida Mountain project area is estimated to be approximately 1.3 million ounces of gold and 70 million ounces of silver from 1891 through 1998, with an unknown quantity produced at the DeLamar mill in 1999, and recorded production may have occurred from 1876 to 1891. This includes an estimated 1.025 million ounces of gold and 51 million ounces of silver produced from the original De Lamar underground mine and the later DeLamar open-pit operations. At Florida Mountain, nearly 260,000 ounces of gold and 18 million ounces of silver were produced from the historical underground mines and late 1990s open-pit mining.

Mining activity began in the area of the DeLamar project when placer gold deposits were discovered in 1863 in Jordan Creek, just upstream from what later became the town site of De Lamar. During the summer of 1863, the first silver-gold lodes were discovered in quartz veins at War Eagle Mountain, to the east of Florida Mountain, resulting in the initial settlement of Silver City. Between 1876 and 1888, significant silver-gold veins were discovered and developed in the district, including underground mines at De Lamar Mountain and Florida Mountain. A total of 553,000 ounces of gold and 21.3 million ounces of silver were reportedly produced from the De Lamar and Florida Mountain underground mines from the late 1800s to early 1900s.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

The mines in the district were closed in 1914 and very little production took place until the gold and silver prices increased in the1930s. Placer gold was again recovered from Jordan Creek from 1934 to 1940, and in 1938 a 181 tonne-per-day flotation mill was constructed to process waste dumps from the De Lamar underground mine. The flotation mill reportedly operated until the end of 1942. Including Florida Mountain, the De Lamar - Silver City area is believed to have produced about 1 million ounces of gold and 25 million ounces of silver from 1863 through 1942.

During the late 1960s, the district began to undergo exploration for near-surface bulk-mineable gold-silver deposits, and in 1977 a joint venture operated by Earth Resources Company ("Earth Resources") began production from an open-pit milling and cyanide tank-leach operation at De Lamar Mountain, known as the DeLamar mine. In 1981, Earth Resources was acquired by the Mid Atlantic Petroleum Company ("MAPCO"), and in 1984 and 1985 the NERCO Mineral Company ("NERCO") successively acquired the MAPCO interest and the entire joint venture to operate the DeLamar mine with 100% ownership. NERCO was purchased by the Kennecott Copper Company ("Kennecott") in 1993. Two months later in 1993, Kennecott sold its 100% interest in the DeLamar mine and property to Kinross, and Kinross operated the mine, which expanded to the Florida Mountain area in 1994. Mining ceased in 1998, milling ceased in 1999, and mine closure activities commenced in 2003. Closure and reclamation were nearly completed by 2014, as the mill and other mine buildings were removed and drainage and cover of the tailings facility were developed.

Total open-pit production from the DeLamar project from 1977 through 1998, including the Florida Mountain operation, is estimated at approximately 750,000 ounces of gold and 47.6 million ounces of silver, with an unknown quantity produced at the DeLamar mill in 1999. From start-up in 1977 through to the end of 1998, open-pit production in the DeLamar area totaled 625,000 ounces of gold and about 45 million ounces of silver. This production came from pits developed at the Glen Silver, Sommercamp - Regan (including North and South Wahl), and North DeLamar areas. In 1993, the DeLamar mine was operating at a mining rate of 27,216 tonnes per day, with a milling capacity of about 3,629 tonnes per day. In 1994, Kinross commenced open-pit mining at Florida Mountain while continuing production from the DeLamar mine. The ore from Florida Mountain, which was mined through 1998, was processed at the DeLamar facilities. Florida Mountain production in 1994 through 1998 totaled 124,500 ounces of gold and 2.6 million ounces of silver.

Geological and Mineralization

The DeLamar project is situated in the Owyhee Mountains near the east margin of the mid-Miocene Columbia River - Steens flood-basalt province and the west margin of the Snake River Plain. The Owyhee Mountains comprise a major mid-Miocene eruptive center, generally composed of mid-Miocene basalt flows intruded and overlain by mid-Miocene rhyolite dikes, domes, flows and tuffs, developed on an eroded surface of Late Cretaceous granitic rocks.

The DeLamar mine area and mineralized zones are situated within an arcuate, nearly circular array of overlapping porphyritic and flow-banded rhyolite flows and domes that overlie cogenetic, precursor pyroclastic deposits erupted as local tuff rings. Integra interprets the porphyritic and banded rhyolite flows and latites as composite flow domes and dikes emplaced along regional-scale northwest-trending structures. At Florida Mountain, flow-banded rhyolite flows and domes cut through and overlie a tuff breccia unit that overlies basaltic lava flows and Late Cretaceous granitic rocks.

Gold-silver mineralization occurred as two distinct but related types: (i) relatively continuous, quartz-filled fissure veins that were the focus of late 19th and early 20th century underground mining, hosted mainly in the basalt and granodiorite and to a lesser degree in the overlying felsic volcanic units; and (ii) broader, bulk-mineable zones of closely-spaced quartz veinlets and quartz-cemented hydrothermal breccia veins that are individually continuous for only a few feet laterally and vertically, and of mainly less than 1.3 centimeters in width - predominantly hosted in the rhyolites and latites peripheral to and above the quartz-filled fissures. This second style of mineralization was mined in the open pits of the late 20th century DeLamar and Florida Mountain operations, hosted primarily by the felsic volcanic units.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

The fissure veins mainly strike north to northwest and are filled with quartz accompanied by variable amounts of adularia, sericite or clay, ± minor calcite. Vein widths vary from a few centimeters to several meters, but the veins persist laterally and vertically for as much as several hundreds of meters. Principal silver and gold minerals are naumannite, aguilarite, argentite, ruby silver, native gold and electrum, native silver, cerargyrite, and acanthite. Variable amounts of pyrite and marcasite with very minor chalcopyrite, sphalerite, and galena occur in some veins. Gold- and silver-bearing minerals are generally very fine grained.

The gold and silver mineralization at the DeLamar project is best interpreted in the context of the volcanic-hosted, low-sulfidation type of epithermal model. Various vein textures, mineralization, alteration features, and the low contents of base metals in the district are typical of shallow low-sulfidation epithermal deposits worldwide.

Drilling, Database and Data Verification

As of the effective date of this report, the resource database includes data from 2,718 holes, for a total of 306,078 meters, that were drilled by Integra and various historical operators at the DeLamar and Florida Mountain areas. The historical drilling was completed from 1966 to 1998 and includes 2,625 holes for a total of 275,790 meters of drilling. Most of the historical drilling was done using reverse-circulation ("RC") and conventional rotary methods; a total of 106 historical holes were drilled using diamond-core ("core") methods for a total of 10,845 meters. Approximately 74% of the historical drilling was vertical, including all historical conventional rotary holes.

Integra commenced drilling in 2018. As of the end of April 2019, Integra had drilled a total of 55 RC holes, 36 core holes, and 11 holes commenced with RC and finished with core tails, for a total of 33,573 meters in the DeLamar and Florida Mountain areas combined. All but one of the Integra holes were angled.

The historical portions of the current resource drill-hole databases for the DeLamar and Florida Mountain deposit areas were originally created by MDA using original DeLamar mine digital database files, and this information was subjected to various verification measures by both MDA and Integra. The Integra portion of the drill-hole databases was directly created by MDA using original digital analytical certificates in the case of the assay tables, or it was checked against original digital records in the case of the collar and down-hole deviation tables. Through these and other verification procedures summarized herein, the authors have verified that the DeLamar data as a whole are acceptable as used in this report.

Metallurgical Testing

Available results from ongoing metallurgical testing by Integra, at McClelland Laboratories (2018-2019) have been used to select preferred processing methods and estimate recoveries for oxide and transitional material types from both the DeLamar and Florida Mountain deposits, as well as unoxidized (sulfide) material type from the Florida Mountain deposit. Metallurgical testing has also been conducted on unoxidized (sulfide) material from the DeLamar deposit, but that testing has not yet progressed to the level required for processing of that material to be included in the PEA.

Samples used for this 2018-2019 testing, primarily composites of 2018 and 2019 drill core, were selected to represent the various material types contained in the current resources from both the DeLamar and Florida Mountain deposits. Composites were selected to evaluate effects of area, depth, grade, oxidation, lithology, and alteration on metallurgical response. In general, test results indicate that materials from each of the DeLamar and Florida Mountain deposits can most usefully be evaluated by considering the oxidation state (oxidized, transitional, or unoxidized).

Bottle-roll and column-leach cyanidation testing on drill core composites from both the DeLamar and Florida Mountain deposits and on bulk samples from the DeLamar deposit have shown that the oxide and transitional material types from both deposits can be processed by heap-leach cyanidation. Testing on drill core composites from the Florida Mountain deposit has shown that the unoxidized material from that deposit is not amenable to heap leach cyanidation but can be leached using cyanide after grinding. The Florida Mountain unoxidized material also responds well to bulk sulfide flotation treatment, and the resulting flotation concentrate is amenable to agitated cyanide leaching. Highest recoveries from the Florida Mountain unoxidized material were obtained by grinding, followed by gravity concentration and flotation of the gravity tailings, with regrind and agitated cyanidation of the flotation concentrate.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Available metallurgical test results indicate that gold recoveries in the range of 75% to 80%, and silver recoveries of about 30%, can be expected from the DeLamar oxide and transitional material types, by heap leaching at a crush size of 80% -13mm. Agglomeration pretreatment of this material is currently planned, because of the potential for processing of some materials with elevated clay content. Heap leach cyanide consumptions are expected to be reasonably low (about 0.3 - 0.4 kg NaCN/tonne).

In the case of the Florida Mountain oxide and transitional material types, gold recoveries of 85% to 90%, and silver recoveries of about 40%, are expected for heap leaching at an 80% -38mm feed size. Agglomeration pretreatment is not considered to be necessary for these material types. Heap leach cyanide consumptions are expected to be reasonably low (about 0.4 kg NaCN/tonne).

Planned processing of the Florida Mountain unoxidized material type includes grinding, followed by gravity concentration and flotation of the gravity tailings, with regrind and agitated cyanidation of the flotation concentrate. Expected recoveries are about 90% gold and 80% silver. Cyanide consumption for the concentrate leaching is expected to be equivalent to about 0.2 kg NaCN/tonne, on a mill feed basis.

In the case of the unoxidized material from the DeLamar deposit, 2018-2019 testing has shown that this material type is not amenable to heap-leach cyanidation and is highly variable with respect to response to grinding followed by agitated cyanidation. Reasons for the generally poor and highly variable grind-leach recoveries from this material type are poorly understood at present. Additional testing and mineralogy studies are in progress to gain a better understanding of the observed variability in recoveries. Further testing is also planned to better define what portion of the DeLamar unoxidized material type might be economically processed by simple grind-leach processing. Metallurgical testing has also shown that the DeLamar unoxidized material generally responds well to upgrading by gravity and flotation processing. Testing to evaluate subsequent processing of the resulting concentrate is in progress, but has not been completed as of the effective date of this report. It is expected that flotation concentrate produced from a significant portion of the DeLamar unoxidized materials will not be amenable to agitated leach (cyanidation). It is expected that for these flotation concentrates, some form of oxidative pre-treatment (such as pressure oxidation or roasting) will be required to maximize gold recovery by cyanidation. Alternatively, these concentrates could be shipped off site for toll processing.

Mineral Resources

Mineral resources have been estimated for both the Florida Mountain and DeLamar areas of the DeLamar project. The gold and silver resources were modeled and estimated by:

- evaluating the drill data statistically;

- creating low- (domain 100), medium- (domain 200) and high-grade (domain 300) mineral-domain polygons for both gold and silver on sets of cross sections spaced at 30-meter intervals;

- projecting the sectional mineral-domain polygons three-dimensionally to the drill data within each sectional window;

- slicing the three-dimensional mineral-domain polygons along 6-meter-spaced horizontal and vertical planes and using these slices to recreate the gold and silver mineral-domain polygons on level plans and long sections, respectively;

- coding a block model to the gold and silver domains for each of the two deposit areas using the level-plan and long-section mineral-domain polygons;

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

- analyzing the modeled mineralization geostatistically to aid in the establishment of estimation and classification parameters; and

- using inverse-distance to the third power to interpolate grades into models comprised of 6x6x6-meter blocks using the gold and silver mineral domains to explicitly constrain the grade estimations.

Parameters used in the estimation of gold and silver grades are summarized in Table 1.

Table 1 - Summary of DeLamar Area Grade Estimation Parameters

|

Estimation Pass - Au + Ag Domain |

Search Ranges (meters) |

Composite Constraints |

||||||

|

Major |

Semi-Major |

Minor |

Min |

Max |

Max/Hole |

|||

|

Pass 1 + 2 - Doman 100 |

60 |

60 |

30 |

2 |

12 |

4 |

||

|

Pass 1 + 2 - Doman 200 + 300 + 0 |

60 |

60 |

30 |

2 |

20 |

4 |

||

|

Pass 3 - Doman 0 + 100 + 200 +300 |

170 |

170 |

170 |

1 |

20 |

4 |

||

|

Restrictions on Search Ranges |

|||

|

Domain |

Search Restriction Threshold |

Search Restriction Distance |

Estimation Pass |

|

Au 100 |

>0.7 g Au/t |

40 meters |

1, 2 |

|

Au 300 |

>20 g Au/t |

35 meters |

1, 2, 3 |

|

Ag 300 |

>400 g Ag/t |

35 meters |

1, 2, 3 |

|

Au 0 |

>0.5 g Au/t |

6 meters |

1, 2, 3 |

|

Ag 0 |

>34.29 g Ag/t |

9 meters |

1, 2, 3 |

The estimation passes were performed independently for each of the mineral domains, so that only composites coded to a particular domain were used to estimate grade into blocks coded by that domain. The estimated grades for each gold and silver domain coded to a block were then coupled with the partial percentages of the those mineral domains in the block, as well as the outside, dilutionary, domain 0 grades and volumes, to enable the calculation of a single volume-averaged gold and a single volume-averaged silver grade for each block. These single resource block grades, and their associated resource tonnages, are therefore fully block-diluted using this methodology.

The search restrictions place limits on the maximum distances from a block that high-grade population composites can be 'found' and used in the interpolation of gold and/or silver grades into a block. To further avoid the smearing of outlier high grades that are sporadically present in the low-grade gold and silver domains, the maximum number of composites allowed for the estimation in Pass 1 and Pass 2 are less than that used for the higher-grade interpolations.

The gold and silver mineralization commonly exhibits multiple orientations, which led to the use of a number of search orientations to control both the DeLamar and Florida Mountain estimations.

Grade interpolation was completed using length-weighted 3.05-meter (10-foot) composites. The estimation passes were performed independently for each of the mineral domains, so that only composites coded to a particular domain were used to estimate grade into blocks coded to that domain. Blocks coded as having partial percentages of more than one gold and/or silver domain had multiple grade interpolations, one for each domain coded into the block for each metal. The estimated grades for each gold and silver domain coded to a block were coupled with the partial percentages of the those mineral domains in the block, as well as any outside, dilutionary, domain 0 grades and volumes, to enable the calculation of a single volume-averaged gold and a single volume-averaged silver grade for each block. These single final resource block grades, and their associated resource tonnages, are therefore fully block-diluted using this methodology.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

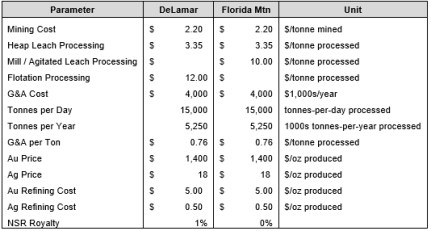

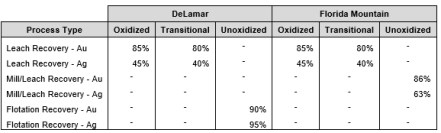

The DeLamar project mineral resources have been estimated to reflect potential open-pit extraction and processing by a combination of heap leaching, milling / agitated leaching, and flotation. To meet the requirement of the in-pit resources having reasonable prospects for eventual economic extraction, pit optimizations for the DeLamar and Florida Mountain deposit areas were run using the parameters summarized in Table 2 and Table 3.

Table 2 - Pit Optimization Cost Parameters (US$)

Table 3 - Pit-Optimization Metal Recoveries by Deposit and Oxidation State

The pit shells created using these optimization parameters were applied to constrain the project resources of both the DeLamar and Florida Mountain deposit areas. The in-pit resources were further constrained by the application of a gold-equivalent cutoff of 0.2 g/t to all model blocks lying within the optimized pits that are coded as oxidized or transitional, and 0.3 g/t for blocks coded as unoxidized. Gold equivalency, as used in the application of the resource cutoffs, is a function of metal prices (Table 2) and metal recoveries, with the recoveries varying by deposit and oxidation state (Table 3).

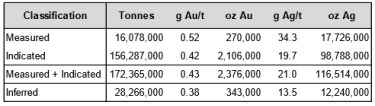

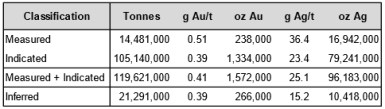

The total DeLamar project resources, which include the resources for both the DeLamar and Florida Mountain areas, are summarized in Table 4. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Table 4 - Total DeLamar Project Gold and Silver Resources

1. Mineral Resources are comprised of all oxidized and transitional model blocks at a 0.2 g AuEq/t cutoff and all unoxidized blocks at a 0.3 g AuEq/t that lie within optimized pits

2. The effective date of the resource estimations is May 1, 2019

3. Mineral resources that are not mineral reserves do not have demonstrated economic viability

4. Rounding may result in apparent discrepancies between tonnes, grade, and contained metal content

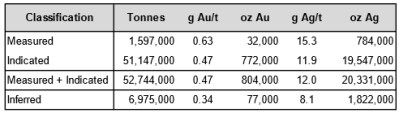

The gold and silver resources for the DeLamar and Florida Mountain areas are reported separately in Table 5 and Table 6, respectively.

Table 5 - DeLamar Deposit Gold and Silver Resources

1. Mineral Resources are comprised of all oxidized and transitional model blocks at a 0.2 g AuEq/t cutoff and all unoxidized blocks at a 0.3 g AuEq/t that lie within optimized pits

2. The effective date of the resource estimations is May 1, 2019

3. Mineral resources that are not mineral reserves do not have demonstrated economic viability

4. Rounding may result in apparent discrepancies between tonnes, grade, and contained metal content

Table 6 - Florida Mountain Deposit Gold and Silver Resources

1. Mineral Resources are comprised of all oxidized and transitional model blocks at a 0.2 g AuEq/t cutoff and all unoxidized blocks at a 0.3 g AuEq/t that lie within optimized pits

2. The effective date of the resource estimations is May 1, 2019

3. Mineral resources that are not mineral reserves do not have demonstrated economic viability

4. Rounding may result in apparent discrepancies between tonnes, grade, and contained metal content

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Mining Methods

The PEA considers open-pit mining of the DeLamar and Florida Mountain gold-silver deposits. Note that a PEA is preliminary in nature and includes Inferred mineral resources that are considered too speculative geologically to have the economic considerations applied that would enable them to be classified as mineral reserves. There is no certainty that the economic results of the PEA will be realized.

The methodology used for mine planning to define the economics for the PEA includes definition of economic parameters, pit optimization, creation of pit and waste rock facility designs, creation of production schedules, definition of personnel and equipment requirements, estimation of capital and operating costs, and performance of an economic analysis.

Pit optimization assumed processing of Florida Mountain and DeLamar oxide and transition resources as heap leach, and unoxidized Florida Mountain resources as milled using floatation followed by cyanidation of the concentrates on site. Leach material would be processed at 27,000 tonnes per day and mill material would be processed at 2,000 tonnes per day. Processing of the DeLamar material will require crushing and agglomeration prior to heap leaching.

The resulting pit optimizations were used as the basis for pit designs. The designs used an inner-ramp slope of 45°. DeLamar pit designs utilized five pit phases to establish a mining sequence and Florida Mountain pit designs were completed using three pit phases.

Waste management facility designs were created for the PEA to contain the waste material mined from both the DeLamar and Florida Mountain areas. Some waste material may also be stored in the form of backfill where and when space is available, although this has not been assumed for the PEA and therefore this is a potential opportunity for the project.

Production scheduling was completed with leaching starting with Florida Mountain material and DeLamar leach material being processed starting in year 5 at the same rate as Florida Mountain leach material. Florida Mountain unoxidized material will be stockpiled until the flotation mill is constructed. The start of the 2,000 tonne per day mill will be in year 3 and it will operate at a rate of 720,000 tonnes per year until unoxidized material is exhausted.

The total project mining rate is given a reasonable ramp-up that starts at 2,000 tonnes per day and increases to a life-of-mine maximum of 90,000 tonnes per day in later years.

The PEA has assumed owner mining in order to keep operating costs lower than it would be with contract mining. The production schedule was used along with additional efficiency factors, cycle times, and productivity rates to develop the first-principle hours required for primary mining equipment to achieve the production schedule. Mining anticipates 136-tonne capacity haul trucks loaded by hydraulic shovels. Personnel requirements have been estimated based on the number of people required to operate, supervise, maintain, and plan for operations to achieve the production schedule.

Processing and Recovery Methods

The PEA envisions the use of two process methods for the recovery of gold and silver:

1) Lower-grade oxide and transition materials from both DeLamar and Florida Mountain will be processed by crushed-ore cyanide heap leaching with stacking on a central heap leach by conveyor, followed by Merrill-Crowe zinc precipitation.

2) Higher-grade unoxidized material from Florida Mountain will be processed using grinding followed by gravity and flotation concentration, with the concentrates processed by regrinding, agitated-cyanide leaching, counter-current decantation ("CCD"), and Merrill-Crowe zinc precipitation. Flotation tailings will be thickened, filtered, and dry stacked at the tailings storage facility. Concentrate-leach tailings will be added to the heap-leach circuit for further recovery of gold and silver.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Both Florida Mountain and DeLamar oxide and transition ore types have been shown to be amenable to heap-leach processing following crushing. Material will be crushed in two stages to a nominal 100 millimeter size at a rate of 27,000 tonnes per day. Initially, for the Florida Mountain materials, the product of the secondary circuit will be a nominal size of 38 millimeters. Transitioning to DeLamar ore types will require the addition of a tertiary crushing circuit with tertiary screens and cone crushers operating in closed circuit to produce a nominal 13-millimeter product followed by cement agglomeration. Lime will be added to the crushed ore for pH control at a dosage of 1 kilogram/tonne. Cement will be added at 3 kilograms/tonne for agglomeration as required.

Crushed and prepared ore will be transferred to the heap-leach pad using overland conveyors and stacked on the heap using portable or grasshopper conveyors and a radial stacking system. Leach solution will be collected at the base on the heap leach and transferred to the Merrill-Crowe processing plant for recovery of precious metals by zinc precipitation. The zinc precipitate will be filtered, dried, and smelted to produce a precious metal doré product for shipment off site.

Gold and silver recoveries are expected to be 90% and 40%, respectively, for the Florida Mountain oxide heap-leach material. The DeLamar oxide recoveries used in this study are 80% for gold and 30% for silver. Cyanide consumptions for the oxide ore types are 0.4 kilograms/tonne and 0.3 kilograms/tonne for Florida Mountain and DeLamar, respectively.

Transition material gold recoveries are projected to be 85% for Florida Mountain and 75% for DeLamar. Silver recoveries for the transition material are projected to be 40% and 30% for Florida Mountain and DeLamar, respectively. Projected cyanide consumption is 0.4 kilograms per tonne for both the Florida Mountain and DeLamar transition material types.

Higher-grade Florida Mountain unoxidized material will be processed by crushing, grinding, gravity, and flotation concentration, followed by cyanide leaching of the concentrates using CCD and Merrill-Crowe precipitation. This circuit is scheduled to operate at a nominal production rate of 2,000 tonnes per day. For this process, the final crusher product will have a nominal particle size of 6 millimeters and will be fed to the ball mill via two belt feeders at a nominal ore production rate of 88 tonnes per hour. The ball mill discharge will be pumped to a set of two hydrocyclones, one operating and one standby, with the cyclone overflow reporting to the flotation conditioning tank. The cyclone underflow will report to a centrifugal gravity concentrator. Concentrator reject then reports back to the ball mill for additional grinding. The gravity concentrate will report to the concentrate regrind mill for subsequent processing in the leach circuit.

The flotation feed from the conditioning tank will report to the flotation circuit for sulfide concentration. The flotation concentrate will report to a regrind circuit where it will be ground to a nominal 37 µm before being leached in a conventional leach tank and CCD circuit. The flotation tailings are to be thickened and filtered with the filter cake reporting to the dry stacked tailings storage facility.

Leach solid residue and the pregnant leach solution are separated in the CCD circuit. The pregnant leach solution will report to the heap leach Merrill-Crowe circuit where it will be processed using zinc precipitation for the recovery of gold and silver. The leached residue will be thickened to 60% solids and added to the heap leach material before it is stacked on the heap, thus allowing for additional processing and mitigating the need for a cyanide-rated tailings storage facility.

Recoveries from the Florida Mountain milling/concentrator circuit are expected to be 90% for gold and 80% for silver. Sodium cyanide and lime consumptions are both expected at 0.2 kilograms per tonne of material feed.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Capital and Operating Costs

Table 7 summarizes the estimated life-of-mine ("LOM") capital costs for the project. The LOM total capital costs are estimated as US$270.3 million, including US$161.0 million in preproduction capital (including working capital) and US$109.3 million for sustaining capital (which includes US$20.0 million in reclamation costs).

Table 8 shows the estimated LOM operating costs for the project, which are estimated to be US$7.82 per tonne processed. This includes mining costs which are estimated to be US$2.00 per tonne mined. The total cash cost is estimated to be US$619 per ounce of gold equivalent and all-in sustaining costs are estimated to be US$742 per ounce of gold equivalent. See "Non-GAAP Measures" disclosure at the end of this MD&A.

Table 7 Capital Cost Summary (US$)

| Sustaining | Total | ||||||||

| Mine | Pre-Production (1) | Yr 1 to Yr 10 (1) | LOM (1) | ||||||

| Mining Equipment | $ | 32,980 | $ | 52,014 | $ | 84,994 | |||

| Pre-Stripping | $ | 7,514 | $ | - | $ | 7,514 | |||

| Other Mine Capital | $ | 6,027 | $ | 746 | $ | 6,773 | |||

| Sub-Total Mine | $ | 46,521 | $ | 52,760 | $ | 99,281 | |||

| Processing | |||||||||

| Heap Leach Pad | $ | 14,130 | $ | 19,178 | $ | 33,308 | |||

| Heap leach Plant (Incl Crushing and Stacking) | $ | 48,449 | $ | - | $ | 48,449 | |||

| Heap leach: Agglomeration / Crushing (DeLamar Ore) | $ | - | $ | 20,518 | $ | 20,518 | |||

| Florida Mill: Plant | $ | - | $ | 34,354 | $ | 34,354 | |||

| Florida Mill: Dry Stack Tailings | $ | - | $ | 6,990 | $ | 6,990 | |||

| Sub-Total Processing | $ | 62,579 | $ | 81,039 | $ | 143,618 | |||

| Infrastructure | |||||||||

| Power | $ | 21,714 | $ | - | $ | 21,714 | |||

| Assay Lab | $ | 2,804 | $ | - | $ | 2,804 | |||

| Other | $ | 2,552 | $ | 974 | $ | 3,526 | |||

| Sub-Total Infrastructure | $ | 27,070 | $ | 974 | $ | 28,044 | |||

| Owner's Costs | $ | 5,819 | $ | - | $ | 5,819 | |||

| SUB-TOTAL | $ | 141,989 | $ | 134,773 | $ | 276,761 | |||

| Other | |||||||||

| Working Capital(2) | $ | 13,024 | $ | (13,024 | ) | $ | - | ||

| Cash Deposit for Reclamation Bonding(3) | $ | 6,000 | $ | (6,000 | ) | $ | - | ||

| Salvage Value(4) | $ | - | $ | (26,426 | ) | $ | (26,426 | ) | |

| TOTAL | $ | 161,013 | $ | 89,323 | $ | 250,336 | |||

| Reclamation | $ | - | $ | 20,000 | $ | 20,000 | |||

| Total Including Reclamation Costs | $ | 161,013 | $ | 109,323 | $ | 270,336 |

(1) Capital costs include contingency and EPCM costs;

(2) Working capital is returned in year 11;

(3) Cash deposit = 30% of bonding requirement. Released once reclamation is completed;

(4) Salvage value for mining equipment and plant; and

(5) Reclamation costs listed here are treated as operating costs in the economic evaluation.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Table 8 Operating and Total Cost Summary (US$)

| USD / Tonne | ||||||

| LOM Operating Costs | Mined | Processed | ||||

| Mining | $ | 2.00 | $ | 4.18 | ||

| Processing | $ | 3.08 | ||||

| G&A | $ | 0.55 | ||||

| Total Site Costs | $ | 7.82 | ||||

| LOM Cash Costs and All-in Sustaining Costs | By-Product (1) | Co-Product (2) | ||||

| Mining | $ | 380 | $ | 317 | ||

| Processing | $ | 280 | $ | 233 | ||

| G&A | $ | 50 | $ | 42 | ||

| Total Site Costs | $ | 711 | $ | 592 | ||

| Transport & Refining | $ | 13 | $ | 11 | ||

| Royalties | $ | 17 | $ | 14 | ||

| Total Cash Costs | $ | 741 | $ | 617 | ||

| Silver By-Product Credits | $ | (272 | ) | $ | - | |

| Total Cash Costs Net of Silver by-Product | $ | 469 | $ | 617 | ||

| Sustaining Capital | $ | 131 | $ | 109 | ||

| Reclamation | $ | 19 | $ | 16 | ||

| All-in Sustaining Costs | $ | 619 | $ | 742 | ||

(1) By-Product costs are shown as US dollars per gold ounces sold with silver as a credit; and

(2) Co-Product costs are shown as US dollars per gold equivalent ounce.

Preliminary Economic Analysis

MDA has prepared this PEA for the DeLamar mining project, which includes operations at both the DeLamar and Florida Mountain deposits. A summary of the PEA results is shown in Table 9.

Table 9 Preliminary Economic Analysis Summary

|

After-tax NPV (5%) |

K USD |

$357,572 |

|

After-tax NPV (8%) |

K USD |

$284,448 |

|

After-tax NPV (10%) |

K USD |

$244,454 |

|

After-tax IRR |

% |

43% |

|

After-Tax Payback Period |

Years |

2.35 |

Note that a preliminary economic assessment is preliminary in nature and it includes Inferred mineral resources that are considered too speculative geologically to have the economic considerations applied that would enable them to be classified as mineral reserves. There is no certainty that the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Some economic highlights include:

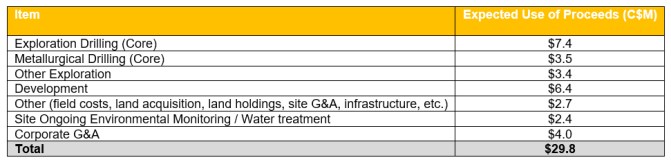

- Initial construction period is anticipated to be 18 months;

- After-tax net present value ("NPV") (5%) of US$358 million with a 43% after-tax internal rate of return ("IRR") using US$1,350 and US$16.90 per ounce gold and silver prices, respectively;

- After-tax payback period of 2.35 years;

- Year 2 to 6 gold equivalent production of 148,000 ounces (126,000 oz Au and 1,796,000 oz Ag); and

- Year 1 to 10 gold equivalent average production of 124,000 ounces (103,000 oz Au and 1,660,000 oz Ag);

- After-tax LOM cumulative cash flows of US$528 million; and

- Average annual after-tax free cash flow of US$61 million once in production.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

2. Black Sheep District, Idaho

On February 14, 2019, Integra announced the acquisition of a highly prospective trend of multiple epithermal centers 6 km to the northwest of the DeLamar Project, a trend now referred to as the Black Sheep District ("Black Sheep" or the "District"). The District was identified in part during site visits and research by renowned epithermal geologists Dr. Jeff Hedenquist and Dr. Richard Sillitoe. Dr. Sillitoe and Dr. Hedenquist, along with Integra's exploration team led by Dr. Max Baker, mapped the area and interpreted the District to have undergone very limited erosion since the mid-Miocene mineralization event, suggesting the productive zone of mineralization is potentially located approximately 200 m beneath the surface. Minimal historical exploration did encounter gold-silver in Black Sheep; however, historic drilling was shallow, less than 100 m vertical on average, and did not enter the theorized productive zone.

The Black Sheep District to the northwest of DeLamar is comparable in geographical size to both the DeLamar and Florida Mountain Deposits combined. The nature of the mineralization and alteration in Black Sheep includes extensive sinter deposits surrounding centers of hydrothermal eruption breccia vents associated with high-level coliform banded amorphous to chalcedonic silica with highly anomalous gold, silver arsenic, mercury, antimony and selenium values. In addition to some preliminary rock chip sampling, Integra completed an extensive soil geochemistry grid over the Black Sheep District showing highly anomalous gold and silver trends over significant lengths.

In the second half of 2019, the Company commenced an extensive regional exploration program at Black Sheep. This regional exploration program included:

- Additional rock-chip sampling and prospect scale mapping

- A regional airborne magnetic and radiometric survey

- Commissioning of the Idaho Geology Department to undertake 1:24,000 scale geological mapping of the DeLamar, Florida Mountain and Black Sheep Districts

- Induced polarization ("IP") survey currently underway

See "2020 Outlook" section above for 2020 exploration program.

3. War Eagle Property, Idaho

On January 21, 2019, Integra announced that, through its wholly owned subsidiary, DeLamar Mining Company, it entered into an option agreement with Nevada Select Royalty, Inc. ("Nevada Select"), a wholly owned subsidiary of Ely Gold Royalties, Inc to acquire Nevada Select's interest in a State of Idaho Mineral Lease encompassing the War Eagle gold-silver Deposit ("War Eagle") situated 3 km east of Integra's Florida Mountain Deposit.

In the War Eagle Mountain District, Integra had previously acquired the Carton Claim group comprising of six patented mining claims covering 45 acres and located 750 m north of the State Lease.

War Eagle Mountain has a rich history of high-grade gold-silver production dating back to the late 1800's. The War Eagle-Florida-DeLamar geological settings, all hosting low sulphidation epithermal gold-silver are genetically related to the same mineralization forming event that occurred roughly 16 million years ago. The local geology and ore mineralogy found within the low sulphidation epithermal veins on War Eagle Mountain are similar to the regimes found at DeLamar and Florida Mountain to the west. The key difference is the host rock. Historically mined gold and silver in high grade veins at War Eagle was predominately mined and hosted by late Cretaceous age granitic rock. It should be noted that historically, the veins of War Eagle Mountain were of far higher grade compared to any other mining operations in the district, including DeLamar and Florida Mountain. Past production on these high-grade vein systems has outlined strike lengths in excess of 1 km and depth extents of up to 750 meters or more.

The following table highlights several of the best intercepts drilled by previous explorers of War Eagle Mountain, as described in historic drill data tabulations.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

|

Drill Hole ID |

From (m) |

To |

Interval |

g/t AuEq(2) |

|

W14 incl |

131.06 131.06 |

213.36 134.11 |

82.30 3.05 |

4.07 32.04 |

|

W02 |

56.39 |

62.48 |

6.09 |

9.49 |

|

W03 |

175.26 |

182.88 |

7.62 |

9.28 |

|

W06 |

146.30 |

147.83 |

1.52 |

55.03 |

|

W40 |

68.58 |

92.96 |

24.38 |

8.45 |

|

W40 incl |

152.40 166.12 |

195.07 176.78 |

42.67 10.67 |

8.83 19.19 |

|

W51 |

124.97 |

132.59 |

7.62 |

8.04 |

1. The historic drill data reported in this release was developed by previous operators of the War Eagle Project prior to the introduction of NI43-101. Historic drill intersections are reported as drilled thicknesses. True widths of the mineralized intervals are estimated to be less than 75% of the reported widths. The historic drill data was sourced from historic reports by various operators' exploration and production data and reports. Integra Resources is providing this historic data for informational purposes only, and gives no assurance as to its reliability or relevance. Integra Resources has not completed any quality assurance program or applied quality control measures to the historic data. Accordingly, the historic data should not be relied upon.

2. Gold equivalent = g Au/t + (g Ag/t ÷ 85)

See "2020 Outlook" section above for 2020 exploration program.

SELECTED CONSOLIDATED FINANCIAL INFORMATION

The following table sets forth selected consolidation information of the Company as of June 30, 2020, December 31, 2019, and December 31, 2018, prepared in accordance with IFRS. The selected consolidated financial information should be read in conjunction with the Company's audited annual consolidated financial statements.

| Six-Months Ended June 30, 2020 $ |

Year Ended December 31, 2019 $ |

Year Ended December 31, 2018 $ |

|||||||

| Exploration and evaluation expenses | (5,259,331 | ) | (13,433,489 | ) | (9,512,437 | ) | |||

| Operating loss | (8,845,335 | ) | (20,281,662 | ) | (15,396,499 | ) | |||

| Other income (expense) | 493,760 | (1,371,387 | ) | 588,660 | |||||

| Net loss | (8,351,575 | ) | (21,653,049 | ) | (14,807,839 | ) | |||

| Net income (loss) per share | (0.18 | ) | (0.64 | ) | (0.63 | ) | |||

| Other comprehensive income (loss) | 940,548 | (861,523 | ) | (105,079 | ) | ||||

| Comprehensive loss | (7,411,027 | ) | (22,514,572 | ) | (14,912,918 | ) | |||

| Cash and cash equivalents | 26,122,941 | 31,323,346 | 15,420,540 | ||||||

| Restricted cash, long-term | 23,014 | 1,928,641 | 2,267,778 | ||||||

| Exploration and evaluation assets | 75,760,338 | 61,348,921 | 58,422,192 | ||||||

| Total assets | 105,854,990 | 97,714,711 | 78,827,015 | ||||||

| Total current liabilities | 5,604,869 | 4,445,062 | 8,587,843 | ||||||

| Total non-current liabilities | 56,178,545 | 42,710,061 | 40,660,609 | ||||||

| Working capital | 21,289,666 | 27,587,579 | 7,335,491 |

The current operating loss of $8,845,335 was mostly driven by exploration and evaluation expenses of $5,259,331 as well as head office expenses such as compensation, corporate development and marketing, office, professional fees, and stock-based compensation (non-cash) expenses. December 31, 2019 operating loss of $20,281,662 was mostly driven by exploration and evaluation expenses of $13,433,489 as well as head office expenses including compensation, corporate development and marketing, office, professional fees, and stock-based compensation expenses (non-cash). The change from 2018 to 2019 was mostly due to an increase in exploration and evaluation expenses.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

Other income (expense) of $493,760 (other income) in the current six-month period is mostly due to the foreign exchange gain and interest income, partially offset by reclamation accretion expenses. Other income (expense) of $1,371,387 (other expense) in the year ended December 31, 2019 was mostly due to the reclamation accretion expenses and foreign exchange losses, partly offset by the Company's interest and rent income. Other income (expense) of $588,660 (other income) in the year ended December 31, 2018 was mostly due to a foreign exchange gain partially offset by reclamation accretion expenses.

Other comprehensive income (loss) amounts are related to the foreign exchange translation adjustment.

Total assets in the current six-month period ended June 30, 2020 increased compared to the year ended December 31, 2019, mostly because of the exploration and evaluation assets increase, due to the reclamation adjustment, and property, plant and equipment additions. Total assets in the year ended December 31, 2019 increased when compared to the year ended December 31, 2018, mostly as a result of the cash increase due to the Company's 2019 financings. Working capital in the current six-month period slightly decreased comparing to the year ended December 31, 2019, mostly due to the exploration and development spending. Working capital increased significantly in the year ended December 31, 2019 comparing to the year ended December 31, 2018, due to the cash increase and current liabilities decrease (as the $4.5 million promissory note was paid in October 2019) in 2019. Working capital in the year ended December 31, 2018 was driven by the $17 million financing in the last quarter of 2018, cash expenditures spent on drilling, the Florida Mountain deposit acquisition, exploration expenses, and corporate general administration expenditures, and an increase in current liabilities (driven by the promissory note liability reclassification from non-current to current liabilities).

Total current liabilities decreased as of December 31, 2019 comparing to the year ended December 31, 2018, mostly due to the repayment of the promissory note in October 2019. Total non-current liabilities increased in the current six-month period ended June 30, 2020 comparing to the year ended December 31, 2019, mostly due to a change in reclamation liability (resulting from a change in discount rate and exchange rate in the current six-month period) and equipment financing liability incurred in the current six-month period. Total non-current liabilities increased in 2019 fiscal year, comparing to the year ended December 31, 2018, mostly due to a change in reclamation liability estimates.

The following table outlines the exploration and evaluation assets break-down:

| Total | |||

| Balance at December 31, 2018 | $ | 58,422,192 | |

| Land acquisitions/option payments | 64,940 | ||

| Claim Staking | 227,370 | ||

| Legal expenses | 25,303 | ||

| Title review and environment | 13,046 | ||

| Promissory note interest accretion expenses | 119,205 | ||

| Reclamation adjustment* | 5,241,860 | ||

| Depreciation** | (9,616 | ) | |

| Translation difference*** | (2,800,772 | ) | |

| Total | 61,303,528 | ||

| Advance minimum royalty | 45,393 | ||

| Balance at December 31, 2019 | 61,348,921 | ||

| Land acquisitions/option payments | 4,088 | ||

| Claim Staking | 20,803 | ||

| Legal expenses | 5,950 | ||

| Title review and environment | 9,289 | ||

| Reclamation adjustment* | 11,319,407 | ||

| Depreciation** | (5,031 | ) | |

| Translation difference*** | 3,023,045 | ||

| Total | 75,726,472 | ||

| Advance minimum royalty | 33,866 | ||

| Balance at June 30, 2020 | $ | 75,760,338 |

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

*Reclamation adjustment is the change in present value of the reclamation liability, due to changes to cost estimates, inflation rate, and or discount rate.

**A staff house building with a carrying value of US$187,150 (C$255,048) has been included in the DeLamar property. This building is being depreciated.

***December 31, 2018 closing balance of US$42,825,239 (C$58,422,192), translated to C$ with the December 31, 2019 exchange rate equals to $55,621,420, resulting in a $2,800,772 translation difference; December 31, 2019 closing balance of US$47,235,080 (C$61,348,921), translated to C$ with the June 30, 2020 exchange rate equals to $64,371,966, resulting in a $3,023,045 translation difference.

The following table outlines the exploration and evaluation expense break-down by properties for the six-month periods ended June 30, 2020 and 2019:

Exploration and Evaluation Expense Summary:

| June 30, 2020 |

DeLamar deposit |

Florida Mountain deposit |

Other deposits |

Joint expenses |

Total |

||||||||||

| Contract exploration drilling | $ | 317,008 | $ | 356,613 | $ | - | $ | - | $ | 673,621 | |||||

| Contract metallurgical drilling | 860,497 | - | - | - | 860,497 | ||||||||||

| Exploration drilling - other drilling labour & related costs | 288,297 | 219,953 | 15,011 | - | 523,261 | ||||||||||

| Metallurgical drilling - other drilling labour & related costs | 375,847 | - | - | - | 375,847 | ||||||||||

| Other exploration expenses* | - | - | 306,599 | 805,841 | 1,112,440 | ||||||||||

| Other development expenses** | - | - | - | 532,791 | 532,791 | ||||||||||

| Land*** | 96,714 | 41,912 | 29,456 | 4,518 | 172,600 | ||||||||||

| Permitting | - | - | - | 534,539 | 534,539 | ||||||||||

| Metallurgy test work | 248,925 | 75,459 | - | - | 324,384 | ||||||||||

| Technical reports and studies | - | - | - | 66,281 | 66,281 | ||||||||||

| Community engagement | - | - | - | 83,070 | 83,070 | ||||||||||

| Total | $ | 2,187,288 | $ | 693,937 | $ | 351,066 | $ | 2,027,040 | $ | 5,259,331 |

*Includes mapping, IP, sampling, payroll, exploration G&A expenses, consultants.

**Includes development G&A expenses and payroll.

***Includes compliance, consulting, property taxes, legal, etc. expenses.

| June 30, 2019 |

DeLamar deposit |

Florida Mountain deposit |

Other deposits |

Joint expenses |

Total |

||||||||||

| Contract exploration drilling | $ | 1,070,751 | $ | - | $ | - | $ | - | $ | 1,070,751 | |||||

| Contract metallurgical drilling | 1,028,563 | 84,541 | - | - | 1,113,104 | ||||||||||

| Exploration drilling - other drilling labour & related costs | 1,070,860 | - | - | - | 1,070,861 | ||||||||||

| Metallurgical drilling - other drilling labour & related costs | 461,665 | 34,938 | - | - | 496,603 | ||||||||||

| Other exploration expenses* | 22,112 | - | - | 242,663 | 264,775 | ||||||||||

| Land** | 70,476 | 8,260 | 10,020 | 44,638 | 133,394 | ||||||||||

| Metallurgy test work | - | - | - | 323,198 | 323,198 | ||||||||||

| Technical reports and studies | - | - | - | 431,802 | 431,802 | ||||||||||

| Community, safety & other | - | - | - | 84,133 | 84,133 | ||||||||||

| Total | $ | 3,724,427 | $ | 127,739 | $ | 10,020 | $ | 1,126,434 | $ | 4,988,620 |

*Includes mapping, IP, sampling, payroll, exploration G&A expenses, consultants.

**Includes compliance, consulting, property taxes, legal, etc. expenses.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

RESULTS OF OPERATIONS

SIX-MONTH PERIOD ENDED JUNE 30, 2020

Net loss for the six-month period ended June 30, 2020 was $8,351,575 and the comprehensive loss $7,411,027, compared to a net loss of $8,566,710 and a comprehensive loss of $9,244,930 for the comparative period in 2019.

Overall, operating expenses were slightly higher in the current six-month period mostly due to an increase in exploration and development expenses, stock-based compensation (non-cash expense), office and site administration, professional fees, and depreciation. The increase in expenses was partially off-set by a higher non-operating income in the current six-month period, mostly due to foreign exchange gain (versus an exchange loss in the comparative period) and lower accretion expenses. The variances between these two periods were primarily due to the following items:

- Exploration and evaluation expenses: the Company incurred $5,259,331 in exploration and development expenses during the six-month period ended June 30, 2020 (June 30, 2019 - $4,988,620). The difference is mostly due to compensation reclassification from the compensation and benefits expenses in the current six-month period.

- Compensation and benefits: these expenses amounted to $1,261,273 in the six-month period ended June 30, 2020 (June 30, 2019 - $1,168,327). The increase is mostly due to an increase in staff level, partially off-set by the reclassification of compensation expenses to the exploration and evaluation expenses in the current six-month period.

- Stock-based compensation: the Company incurred $923,015 in stock-based compensation in the current six-month period ended June 30, 2020 (June 30, 2019 - $660,540). The variance is due to the granting of options in 2020 and timing of vesting of options granted in 2019, 2018 and 2017.

- Office and site administration: the Company incurred $366,331 in expenses during the six-month period ended June 30, 2020 (June 30, 2019 - $279,833), mostly due to increased health and safety expenses, IT expenses, subscription and membership fees, sponsorship, and insurance expenses in the current period.

- Professional fees: for the six-month period ended June 30, 2020 totaled $280,592 (June 30, 2019 - $131,879). Professional fees include expenses such as legal, audit, accounting, tax, and miscellaneous consulting expenses. Professional fees were higher in the current period mostly due to increased legal fees resulting from increased corporate activity, such as the Company's continuation to BC, share consolidation and NYSE American listing.

- Corporate development and marketing: for the six-month period ended June 30, 2020 totaled $271,428 (June 30, 2019 - $314,471). The decrease was mostly due to a reduction in travel expenses due to COVID-19 travel restrictions in the current period.

- Depreciation expenses related to the right-of-use assets amounted to $175,842 in the six-month period ended June 30, 2020 (June 30, 2019 - $128,911). The increase is due to lease additions since Q2 2019.

- Depreciation expenses related to the property, plant and equipment amounted to $169,365 in the six-month period ended June 30, 2020 (June 30, 2019 - $88,756). The increase is due to equipment additions since Q2 2019.

|

MANAGEMENT’S DISCUSSION & ANALYSIS |

- Regulatory fees: for the six-month period ended June 30, 2020 totaled $138,158 (June 30, 2019 - $84,506). Regulatory fees, which include filing fees and transfer agent fees, were higher in the current period mostly due to increased corporate activity, such as the Company's continuation to BC, share consolidation and NYSE American listing.

- Other income (expense): amounted to $493,760 (other income) in the six-month period ended June 30, 2020, compared to $720,867 (other expenses) in the comparative period, mostly due to a foreign exchange gain of $718,557 (non-cash item) in 2020 versus an exchange loss of $203,653 in the comparative period, higher interest income in the current period, and lower accretion expenses in the current period.

THREE-MONTH PERIOD ENDED JUNE 30, 2020

Net loss for the three-month period ended June 30, 2020 was $5,234,608 and the comprehensive loss $6,134,610, compared to a net loss of $4,557,202 and a comprehensive loss of $4,873,929 for the comparative period in 2019.

Overall, operating expenses were slightly higher in the current three-month period mostly due to an increase in exploration and development expenses, stock-based compensation (non-cash item), office and site administration, professional and regulatory fees, and depreciation; other non-operating loss was also higher in the current three-month period, mostly due to the higher foreign exchange loss in the current period. The variances between these two periods were primarily due to the following items:

- Exploration and evaluation expenses: the Company incurred $2,846,257 in exploration and development expenses during the quarter ended June 30, 2020 (June 30, 2019 - $2,733,606). The difference is mostly due to compensation reclassification from the compensation and benefits expenses in the current three-month period.