UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

For the quarterly period ended

OR

For the transition period from to .

Commission File Number:

(Exact name of registrant as specified in its charter)

(State or Other Jurisdiction of Incorporation) | (IRS Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

| The |

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☒ | Smaller reporting company | |||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

As of August 9, 2023, the registrant had

LONGEVERON INC.

TABLE OF CONTENTS

i

PART I. FINANCIAL INFORMATION

Item 1. Condensed Financial Statements.

Longeveron Inc.

Condensed Balance Sheets

(In thousands, except share and per share data)

| June 30, 2023 | December 31, 2022 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Marketable securities | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Accounts and grants receivable | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Operating lease asset | ||||||||

| Other assets | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities and stockholders’ equity | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | $ | ||||||

| Accrued expenses | ||||||||

| Current portion of lease liability | ||||||||

| Estimated lawsuit liability | ||||||||

| Deferred revenue | ||||||||

| Total current liabilities | ||||||||

| Long-term liabilities: | ||||||||

| Lease liability | ||||||||

| Total long-term liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and contingencies (Note 9) | ||||||||

| Stockholders’ equity: | ||||||||

| Preferred stock, $ | ||||||||

| Class A Common Stock, $ | ||||||||

| Class B Common Stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Stock subscription receivable | ( | ) | ( | ) | ||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Total stockholders’ equity | ||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||

See accompanying notes to unaudited condensed financial statements.

1

Longeveron Inc.

Condensed Statements of Operations

(In thousands, except per share data)

(Unaudited)

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| Revenues | ||||||||||||||||

| Clinical trial revenue | $ | $ | $ | $ | ||||||||||||

| Grant revenue | ||||||||||||||||

| Total revenues | ||||||||||||||||

| Cost of revenues | ||||||||||||||||

| Gross profit | ||||||||||||||||

| Operating expenses | ||||||||||||||||

| General and administrative | ||||||||||||||||

| Research and development | ||||||||||||||||

| Selling and marketing | ||||||||||||||||

| Total operating expenses | ||||||||||||||||

| Loss from operations | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other income and (expenses) | ||||||||||||||||

| Non-operating lawsuit expense | ( | ) | ( | ) | ||||||||||||

| Other income and (expenses), net | ( | ) | ( | ) | ||||||||||||

| Total other income and (expenses), net | ( | ) | ( | ) | ||||||||||||

| Net loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||||

See accompanying notes to unaudited condensed financial statements.

2

Longeveron Inc.

Condensed Statements of Comprehensive Loss

(In thousands, except per share data)

(Unaudited)

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| Net loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Other comprehensive loss: | ||||||||||||||||

| Net unrealized (loss) gain on available-for-sale securities | ( | ) | ||||||||||||||

| Total comprehensive loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

See accompanying notes to unaudited condensed financial statements.

3

Longeveron Inc.

Condensed Statements of Stockholders’ Equity

(In thousands, except share amounts)

(Unaudited)

| Class A Common Stock | Class B Common Stock | Subscription | Additional Paid-In | Accumulated | Accumulated Other Comprehensive | Total Stockholder’s | ||||||||||||||||||||||||||||||

| Number | Amount | Number | Amount | Receivable | Capital | Deficit | Loss | Equity | ||||||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||

| Conversion of Class B common stock for Class A common stock | ( | ) | ||||||||||||||||||||||||||||||||||

| Class A Common Stock, issued for RSUs vested | ||||||||||||||||||||||||||||||||||||

| Class A Common Stock, held for taxes on RSUs vested | ( | ) | ( | ) | ( | ) | ||||||||||||||||||||||||||||||

| Equity-based compensation | - | - | ||||||||||||||||||||||||||||||||||

| Unrealized loss attributable to change in market value of available for sale investments | - | - | ||||||||||||||||||||||||||||||||||

| Net loss | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | Subscription | Additional Paid-In | Accumulated | Accumulated Other Comprehensive | Total Stockholder’s | ||||||||||||||||||||||||||||||

| Number | Amount | Number | Amount | Receivable | Capital | Deficit | Loss | Equity | ||||||||||||||||||||||||||||

| Balance at December 31, 2021 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | $ | |||||||||||||||||||||||||

| Conversion of Units into Class A and B common stock | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||

| Class A Common Stock, issued for RSUs vested | - | |||||||||||||||||||||||||||||||||||

| Class A Common Stock, held for taxes on RSUs vested | ( | ) | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Class A Common Stock Options Exercised | - | |||||||||||||||||||||||||||||||||||

| Equity-based compensation | - | - | ||||||||||||||||||||||||||||||||||

| Net loss | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | $ | |||||||||||||||||||||||||

See accompanying notes to unaudited condensed financial statements.

4

Longeveron Inc.

Condensed Statements of Stockholders’ Equity

(In thousands, except share amounts)

(Unaudited)

| Class A Common Stock | Class B Common Stock | Subscription | Additional Paid-In | Accumulated | Accumulated Other Comprehensive | Total Stockholder’s | ||||||||||||||||||||||||||||||

| Number | Amount | Number | Amount | Receivable | Capital | Deficit | Loss | Equity | ||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||

| Conversion of Class B common stock for Class A common stock | ( | ) | ||||||||||||||||||||||||||||||||||

| Class A Common Stock, issued for RSUs vested | - | |||||||||||||||||||||||||||||||||||

| Class A Common Stock, held for taxes on RSUs vested | ( | ) | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Equity-based compensation | - | - | ||||||||||||||||||||||||||||||||||

| Unrealized loss attributable to change in market value of available for sale investments | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||||

| Net loss | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | Subscription | Additional Paid-In | Accumulated | Accumulated Other Comprehensive | Total Stockholder’s | ||||||||||||||||||||||||||||||

| Number | Amount | Number | Amount | Receivable | Capital | Deficit | Loss | Equity | ||||||||||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | $ | |||||||||||||||||||||||||

| Conversion of Units into Class A and B common stock | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||

| Class A Common Stock, issued for RSUs vested | - | |||||||||||||||||||||||||||||||||||

| Class A Common Stock, held for taxes on RSUs vested | ( | ) | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Class A Common Stock Options Exercised | - | |||||||||||||||||||||||||||||||||||

| Equity-based compensation | - | - | ||||||||||||||||||||||||||||||||||

| Net loss | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | $ | |||||||||||||||||||||||||

See accompanying notes to unaudited condensed financial statements.

5

Longeveron Inc.

Condensed Statements of Cash Flows

(In thousands)

(Unaudited)

| Six months ended June 30, | ||||||||

| 2023 | 2022 | |||||||

| Cash flows from operating activities | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Depreciation and amortization | ||||||||

| Interest earned on marketable securities | ||||||||

| Equity issued for consulting services | ||||||||

| Equity-based compensation | ||||||||

| Non-operating lawsuit expense | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts and grants receivable | ( | ) | ||||||

| Prepaid expenses and other current assets | ( | ) | ( | ) | ||||

| Other assets | ( | ) | ||||||

| Accounts payable | ( | ) | ( | ) | ||||

| Deferred revenue | ( | ) | ||||||

| Estimated lawsuit liability | ( | ) | ||||||

| Accrued expenses | ( | ) | ||||||

| Lease asset and lease liability | ( | ) | ( | ) | ||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities | ||||||||

| Proceeds from the sale of marketable securities | ||||||||

| Acquisition of property and equipment | ( | ) | ( | ) | ||||

| Acquisition of intangible assets | ( | ) | ( | ) | ||||

| Net cash provided by investing activities | ||||||||

| Cash flows from financing activities | ||||||||

| Payments for taxes on RSUs vested | ( | ) | ( | ) | ||||

| Net cash used in financing activities | ( | ) | ( | ) | ||||

| Change in cash and cash equivalents | ( | ) | ( | ) | ||||

| Cash and cash equivalents at beginning of the period | ||||||||

| Cash and cash equivalents at end of the period | $ | $ | ||||||

| Supplement Disclosure of Non-cash Investing and Financing Activities: | ||||||||

| Vesting of RSUs into Class A Common Stock | $ | ( | ) | $ | ( | ) | ||

See accompanying notes to unaudited condensed financial statements.

6

Longeveron Inc.

Notes to the Condensed Financial Statements (Unaudited)

Three and Six Month Periods Ended June 30, 2023 and 2022

1. Nature of Business, Basis of Presentation, and Liquidity

Nature of business:

Longeveron was formed as a Delaware limited liability company on October 9, 2014, and was authorized to transact business in Florida on December 15, 2014. On February 12, 2021, Longeveron, LLC converted its corporate form (the “Corporate Conversion”) from a Delaware limited liability company (Longeveron, LLC) to a Delaware corporation, Longeveron Inc. (the “Company,” “Longeveron” or “we,” “us,” or “our”). The Company is a clinical stage biotechnology company developing cellular therapies for specific aging-related and life-threatening conditions and operates out of its leased facilities in Miami, Florida.

The Company’s product candidates are currently in development. There can be no assurance that the Company’s research and development will be successfully completed, that adequate protection for the Company’s intellectual property will be obtained, that any products developed will obtain necessary government regulatory approval or that any approved products will be commercially viable. Even if the Company’s product development efforts are successful, it is uncertain when, if ever, the Company will generate significant revenue from product sales. The Company operates in an environment of rapid technological change and substantial competition from, among others, existing pharmaceutical and biotechnology companies. In addition, the Company is dependent upon the services of its employees, partners and consultants.

The accompanying interim condensed balance sheet as of June 30, 2023, and the condensed statements of operations, statement of comprehensive loss, stockholders’ equity, and cash flows for the three and six months ended June 30, 2023 and 2022, are unaudited. The unaudited condensed financial statements have been prepared according to the rules and regulations of the Securities and Exchange Commission (“SEC”) and, therefore, certain information and disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”) have been omitted. In the opinion of management, the accompanying unaudited condensed financial statements for the periods presented reflect all adjustments which are normal and recurring, and necessary to fairly state the financial position, results of operations, and cash flows of the Company. These unaudited condensed financial statements and notes should be read in conjunction with the audited financial statements and notes thereto in the Company’s 2022 Annual Report on Form 10-K filed with the SEC on March 14, 2023.

Liquidity:

Since inception, the Company has primarily been engaged in organizational activities, including raising capital, and research and development activities. The Company does not yet have a product that has been approved by the U.S. Food and Drug Administration (“FDA”), and has only generated revenues from grants, clinical trials and contract manufacturing. The Company has not yet achieved profitable operations or generated positive cash flows from operations. The Company intends to continue its efforts to raise additional equity financing, develop its intellectual property, and secure regulatory approvals to commercialize its products. There is no assurance that profitable operations, if achieved, could be sustained on a continuing basis. Further, the Company’s future operations are dependent on the success of the Company’s efforts to raise additional capital, its research and commercialization efforts, regulatory approval, and, ultimately, the market acceptance of the Company’s approved products, if any. These financial statements do not include adjustments that might result from the outcome of these uncertainties.

The Company has incurred recurring losses from operations since its

inception, including a net loss of $

As of June 30, 2023, the Company had cash, and cash equivalents of

$

| ● | On June 27,2023 the Company filed a registration statement

with the SEC to conduct a tradeable subscription rights offering for up to $ |

7

| ● | the Company will attempt to use equity instruments to provide a portion of the compensation due to vendors and collaboration partners; |

| ● | the Company plans to pursue potential partnerships for pipeline programs, however, there can be no assurances that it can consummate such transactions; |

| ● | the Company will continue to support its Bahamas Registry to generate revenue; and |

| ● | since 2016 our clinical programs have received over $ |

The Company’s condensed financial statements do not include any adjustments to the assets carrying amount, to the expenses presented and to the reclassification of the condensed balance sheets items that could be necessary should the Company be unable to continue its operations.

2. Summary of Significant Accounting Policies

Basis of presentation:

The financial statements of the Company were prepared in accordance with accounting principles generally accepted in the U.S. (“U.S. GAAP”).

Certain reclassifications have been made to prior year financial statements to conform to classifications used in the current year. These reclassifications had no impact on net loss, stockholders’ equity or cash flows as previously reported.

Use of estimates:

The presentation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Accounting Standard Updates

A variety of proposed or otherwise potential accounting standards are currently under consideration by standard-setting organizations and certain regulatory agencies. Because of the tentative and preliminary nature of such proposed standards, management has not yet determined the effect, if any, that the implementation of such proposed standards would have on the Company’s condensed financial statements.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments - Credit Losses: Measurement of Credit Losses on Financial Instruments. The standard requires that credit losses be reported using an expected losses model rather than the incurred losses model that is currently used, and establishes additional disclosures related to credit risks. For available-for-sale debt securities with unrealized losses, these standards now require allowances to be recorded instead of reducing the amortized cost of the investment. These standards limit the amount of credit losses to be recognized for available-for-sale debt securities to the amount by which carrying value exceeds fair value and requires the reversal of previously recognized credit losses if fair value increases. The adoption of the standard as of January 1, 2023 did not have a material impact on the Company’s condensed financial statements; however, the Company did record net unrealized gains and losses in the condensed statement of comprehensive loss for the three and six month periods ended June 30, 2023.

Cash and cash equivalents:

The Company considers cash to consist of cash on hand and temporary investments having an original maturity of 90 days or less that are readily convertible into cash.

Marketable securities:

Marketable securities at June 30, 2023 and December 31, 2022 consisted

of marketable fixed income securities, primarily corporate bonds, as well as U.S. Government and agency obligations which are categorized

as trading securities and are thus marked to market and stated at fair value in accordance with ASC 820 Fair Value Measurement. These

investments are considered Level 1 and Level 2 investments within the ASC 820 fair value hierarchy. The fair value of Level 1 investments,

including cash equivalents, money funds and U.S. government securities, are substantially based on quoted market prices. The fair value

of corporate bonds is determined using standard market valuation methodologies, including discounted cash flows, matrix pricing and/or

other similar techniques. The inputs to these valuation techniques include but are not limited to market interest rates, credit

rating of the issuer or counterparty, industry sector of the issuer, coupon rate, call provisions, maturity, estimated duration and assumptions

regarding liquidity and estimated future cash flows. In addition to bond characteristics, the valuation methodologies incorporate

market data, such as actual trades completed, bids and actual dealer quotes, where such information is available. Accordingly, the estimated

fair values are based on available market information and judgments about financial instruments categorized within Level 1 and Level

2 of the fair value hierarchy. Interest and dividends are recorded when earned. Realized gains and losses on investments are

determined by specific identification and are recognized as incurred in the statement of operations. Changes in net unrealized gains

and losses are reported in other comprehensive loss and represent the change in the fair value of investment holdings during the reporting

period. Changes in net unrealized gains and losses were less than $

8

Accounts and grants receivable:

Accounts and grants receivable include amounts due from customers, granting institutions and others. The amounts as of June 30, 2023 and December 31, 2022 are certain to be collected, and no amount has been recognized for doubtful accounts. In addition, for the Clinical trial revenue, most participants pay in advance of treatment. Advanced grant funds and prepayments for the Clinical trial revenue are recorded to deferred revenue.

| June 30, 2023 | December 31, 2022 | |||||||

| National Institutes of Health – Grant | $ | $ | | |||||

| Total | $ | $ | ||||||

Deferred offering costs:

The Company recorded certain legal, professional and other third-party fees that were directly associated with in-process equity financings as deferred offering costs until the applicable equity financing was consummated. After consummation of an equity financing, these costs are recorded in stockholders’ equity as a reduction of proceeds generated as a result of the offering.

Property and equipment:

Property and equipment, including improvements that extend useful lives of related assets, are recorded at cost, while maintenance and repairs are charged to operations as incurred. Depreciation is calculated using the straight-line method based on the estimated useful lives of the assets. Leasehold improvements are amortized over the shorter of the estimated useful life of the asset or the original term of the lease. Depreciation expense is recorded in the research and development line of the condensed statements of operations as the assets are primarily related to the Company’s clinical programs.

Intangible assets:

Intangible assets include payments on license agreements with the Company’s co-founder and chief scientific officer (“CSO”) and the University of Miami (“UM”) (see Note 9) and legal costs incurred related to patents and trademarks. License agreements have been recorded at the value of cash consideration, common stock and membership units transferred to the respective parties when acquired.

Payments for license agreements are amortized using the straight-line

method over the estimated term of the agreements, which range from

Impairment of Long-Lived Assets:

The Company evaluates long-lived assets for impairment, including property and equipment and intangible assets, when events or changes in circumstances indicate that the carrying value of such assets may not be recoverable. Upon the occurrence of a triggering event, the asset is reviewed to assess whether the estimated undiscounted cash flows expected from the use of the asset plus the residual value from the ultimate disposal exceeds the carrying value of the asset. If the carrying value exceeds the estimated recoverable amounts, the asset is written down to the estimated fair value. Any resulting impairment loss is reflected on the condensed statements of operations. Upon evaluation, management determined that there was no impairment of long-lived assets during the three and six months ended June 30, 2023 and 2022.

Deferred revenue:

The unearned portion of advanced grant funds and prepayments for clinical

trial revenue, which will be recognized as revenue when the Company meets the respective performance obligations, has been presented

as deferred revenue in the accompanying condensed balance sheets. For the six months ended June 30, 2023 and 2022, the Company recognized

less than $

9

Revenue recognition:

The Company recognizes revenue when performance obligations related to respective revenue streams are met. For grant revenue, the Company considers the performance obligation met when the grant related expenses are incurred or supplies and materials are received. The Company is paid in tranches pursuant to terms of the related grant agreements, and then applies payments based on regular expense reimbursement submissions to grantors. There are no remaining performance obligations or variable consideration once grant expense reporting to the grantor is complete. For clinical trial revenue, the Company considers the performance obligation met when the participant has received the treatment. The Company usually receives prepayment for these services or receives payment at the time the treatment is provided, and there are no remaining performance obligations or variable consideration once the participant receives the treatment. For contract manufacturing revenue, the Company considers the performance obligation met when the contractual obligation and/or statement of work has been satisfied. Payment terms may vary depending on specific contract terms. There are no significant judgments affecting the determination of the amount and timing of revenue recognition.

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2023 | 2022 | 2023 | 2022 | |||||||||||||

| National Institute of Health - grant | $ | $ | $ | $ | ||||||||||||

| Clinical trial revenue | ||||||||||||||||

| MSCRF – TEDCO1 - grant | ||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||

| 1 | Maryland Stem Cell Research Fund (MSCRF) - Maryland Technology Development Corporation (TEDCO) |

The Company records cost of revenues based on expenses directly related to revenue. For Grants, the Company records allocated expenses for Research and development costs to a grant as a cost of revenues. For the Clinical trial revenue, directly related expenses for that program are expensed as incurred. These expenses are similar to those described under “Research and development expense” below.

Research and development expense:

Research and development costs are charged to expense when incurred in accordance with ASC 730 Research and Development. ASC 730 addresses the proper accounting and reporting for research and development costs. It identifies: 1) those activities that should be identified as research and development; 2) the elements of costs that should be identified with research and development activities, and the accounting for these costs; and 3) the financial statement disclosures related to them. Research and development costs include costs such as clinical trial expenses, contracted research and license agreement fees with no alternative future use, supplies and materials, salaries, share-based compensation, employee benefits, property and equipment depreciation and allocation of various corporate costs. The Company accrues for costs incurred by external service providers, including contract research organizations and clinical investigators, based on its estimates of service performed and costs incurred. These estimates include the level of services performed by the third parties, patient enrollment in clinical trials, administrative costs incurred by the third parties, and other indicators of the services completed. Based on the timing of amounts invoiced by service providers, the Company may also record payments made to those providers as prepaid expenses that will be recognized as expense in future periods as the related services are rendered.

Concentrations of credit risk:

Financial instruments which potentially subject the Company to credit risk consist principally of cash and cash equivalents, short-term investments and accounts and grants receivable. Cash and cash equivalents are held in U.S. financial institutions. At times, the Company may maintain balances in excess of the federally insured amounts.

Income taxes:

Prior to its Corporate Conversion, the Company was treated as a partnership for U.S. federal and state income tax purposes. Consequently, the Company passed its earnings and losses through to its members based on the terms of the Company’s Operating Agreement. Accordingly, no provision for income taxes is recorded in the financial statements for periods prior to the conversion.

10

Following the Corporate Conversion, the Company’s tax provision consists

of taxes currently payable or receivable, plus any change during the period in deferred tax assets and liabilities. The Company uses

the asset and liability method of accounting for income taxes. Under this method, deferred tax assets and liabilities are recognized

for the future tax consequences attributable to differences between the financial statement carrying amounts of assets and liabilities

and their respective tax basis. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable

income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and

liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. In addition, a valuation

allowance is established to reduce any deferred tax asset for which it is determined that it is more likely than not that some portion

of the deferred tax asset will not be realized. The Company’s tax provision was $

The Company recognizes the tax benefits from uncertain tax positions that the Company has taken or expects to take on a tax return. In the unlikely event an uncertain tax position exists in which the Company could incur income taxes, the Company would evaluate whether there is a probability that the uncertain tax position taken would be sustained upon examination by a taxing authority. Reserves for uncertain tax positions would then be recorded if the Company determined it is probable that either a position would not be sustained upon examination or a payment would have to be made to a taxing authority and the amount was reasonably estimable. As of June 30, 2023 and December 31, 2022, the Company does not believe it has any uncertain tax positions that would result in the Company having a liability to a taxing authority. It is the Company’s policy to expense any interest and penalties associated with its tax obligations when they are probable and estimable.

Equity-based compensation:

The Company accounts for equity-based compensation expense by the measurement and recognition of compensation expense for stock-based awards based on estimated fair values on the date of grant. The fair value of the stock options is estimated at the date of the grant using the Black-Scholes option-pricing model.

The Black-Scholes option-pricing model requires the input of highly subjective assumptions, the most significant of which are the expected share price volatility, the expected life of the option award, the risk-free rate of return, and dividends during the expected term. Because the option-pricing model is sensitive to changes in the input assumptions, different determinations of the required inputs may result in different fair value estimates of the options.

Neither the Company’s stock options nor its restricted stock

units (“RSUs”) trade on an active market. Volatility is a measure of the amount by which a financial variable, such as a

stock price, has fluctuated (historical volatility) or is expected to fluctuate (expected volatility) during a period. Given the Company’s

limited historical data, the Company utilizes the average historical volatility of similar publicly traded companies that are in the

same industry. The risk-free interest rate is the average U.S. treasury rate (having a term that most closely approximates the expected

life of the option) for the period in which the option was granted. The expected life is the period of time that the options granted

are expected to remain outstanding. Options granted have a maximum term of

3. Marketable securities

| Fair Value at June 30, 2023 | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| U.S. Treasury obligations | $ | $ | $ | $ | ||||||||||||

| U.S. government agencies | ||||||||||||||||

| Corporate and foreign bonds | ||||||||||||||||

| Money market funds(1) | ||||||||||||||||

| Accrued income | ||||||||||||||||

| Total marketable securities | $ | $ | $ | $ | ||||||||||||

| (1) |

11

| Fair Value at December 31, 2022 | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| U.S. Treasury obligations | $ | $ | $ | $ | ||||||||||||

| U.S. government agencies | ||||||||||||||||

| Corporate and foreign bonds | ||||||||||||||||

| Money market funds(1) | ||||||||||||||||

| Accrued income | ||||||||||||||||

| Total marketable securities | $ | $ | $ | $ | ||||||||||||

| (1) | Money market funds are included in cash and cash equivalents in the condensed balance sheet. |

As of June 30, 2023 and December 31, 2022, the Company reported accrued

interest receivable related to marketable securities of less than $

4. Property and equipment, net

| Useful Lives | June 30, 2023 | December 31, 2022 | ||||||||

| Leasehold improvements | | $ | $ | |||||||

| Furniture/Lab equipment | ||||||||||

| Computer equipment | ||||||||||

| Software/Website | ||||||||||

| Total property and equipment | ||||||||||

| Less accumulated depreciation and amortization | ||||||||||

| Property and equipment, net | $ | $ | ||||||||

Depreciation and amortization expense amounted to approximately $

5. Intangible assets, net

| Useful Lives | Cost | Accumulated Amortization | Total | |||||||||||

| License agreements | $ | $ | ( | ) | $ | |||||||||

| Patent Costs | ||||||||||||||

| Trademark costs | ||||||||||||||

| Total | $ | $ | ( | ) | $ | |||||||||

Major components of intangible assets as of December 31, 2022 are as follows:

| Useful Lives | Cost | Accumulated Amortization | Total | |||||||||||

| License agreements | $ | $ | ( | ) | $ | |||||||||

| Patent Costs | ||||||||||||||

| Trademark costs | ||||||||||||||

| Total | $ | $ | ( | ) | $ | |||||||||

12

Amortization expense related to intangible assets amounted to approximately

$

| Year Ending December 31, | Amount | |||

| 2023 (remaining six months) | $ | |||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| Thereafter | ||||

| Total | $ | |||

6. Leases

The Company records an operating lease asset and an operating lease

liability related to its operating leases (there are no finance leases). The Company’s corporate office lease expires in March

2027. As of June 30, 2023, the operating lease asset and operating lease liability were approximately $

| Year Ending December 31, | Amount | |||

| 2023 (remaining six months) | $ | |||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| Total | ||||

| Less: Interest | ||||

| Present value of operating lease liability | $ | |||

During each of the three month periods ended June 30, 2023 and 2022,

the Company incurred approximately $

7. Stockholders’ Equity

Class A Common Stock

On April 19, 2023, the Company finalized the Separation Agreement

effective June 9, 2023, for James Clavijo, the Company’s former Chief Financial Officer. In part for his agreement to a general

release the Company agreed to pay Mr. Clavijo $

On April 18, 2023, the Company finalized the Separation Agreement

dated March 31, 2023, for Dr. Christopher Min, the Company’s former Chief Medical Officer. In part for his agreement to a general

release the Company agreed to pay Dr. Min: $

RSUs are taxable upon vesting based on the market value on the date

of vesting. The Company is required to make mandatory tax withholding for the payment and satisfaction of income tax, social security

tax, payroll tax, or payment on account of other tax related to withholding obligations that arise by reason of vesting of an RSU. The

taxable income is calculated by multiplying the number of vested RSUs for each individual by the closing share price as of the vesting

date ($

On April 3, 2023, a total of

13

On April 3, 2023, a total of

On January 3, 2023, a total of

On November 16, 2022, the Company accounted for but had not issued

On October 3, 2022, a total of

On July 1, 2022, a total of

On June 22, 2022, a total of

On June 3, 2022, a total of

On April 4, 2022, a total of

On April 1, 2022, a total of 31,016 RSUs vested that previously had

been granted in connection with the Company’s IPO vested, of which 26,360 were held by Company employees. Based on the closing

price of $15.61 on April 1, 2022,

On April 1, 2022, a total of

On February 12, 2022, a total of

On January 3, 2022, a total of

14

During the six months ended June 30, 2022, stock options were exercised

for Class A Common Stock shares at an average exercise price of $

Class B Common Stock

In connection with the Corporate Conversion,

Holders of Class A Common Stock generally have rights identical to holders of Class B Common Stock, except that holders of Class A Common Stock are entitled to one vote per share and holders of Class B Common Stock are entitled to five (5) votes per share. The holders of Class B Common Stock may convert each share of Class B Common Stock into one share of Class A Common Stock at any time at the holder’s option. Class B Common Stock is not publicly tradeable.

During the six months ended June 30, 2023, stockholders exchanged

Warrants

As part of the IPO, the underwriter received warrants to purchase

As part of the 2021 PIPE Offering, the Company issued

8. Equity Incentive Plan

As part of the Company’s IPO, the Company adopted and approved the 2021 Incentive Award Plan, under which, the Company may grant equity incentive awards to eligible service providers in order to attract, motivate and retain the talent for which the Company competes.

On March 1, 2023, the Company granted Mr. Hashad a signing bonus of

On November

16, 2022, the Company accounted for but had not issued

On June 22, 2022, the Company granted $

On June 3, 2022, the Company granted a bonus to Mr. Clavijo and Mr.

Lehr in the form of RSUs. Mr. Clavijo and Mr. Lehr were granted

On April 4, 2022, the Company appointed K. Chris Min, M.D., Ph.D.

as its Chief Medical Officer. Dr. Min’s employment agreement provides an annual base salary of $

15

As of June 30, 2023 and December 31, 2022, the Company had

| Number of RSUs | ||||

| Outstanding (unvested) at December 31, 2022 | ||||

| RSU granted | ||||

| RSUs vested | ( | ) | ||

| RSU expired/forfeited | ( | ) | ||

| Outstanding (unvested) at June 30, 2023 | ||||

Stock Options

Stock options may be granted under the 2021 Incentive Plan. The exercise

price of options is set to equal the fair market value of the Company’s Class A Common Stock as of the grant date. Options historically

granted have generally become exercisable over four years and expire ten years from the date of grant. The 2021 Incentive Plan provides

for equity grants to be granted up to

The fair value of the options issued is estimated using the Black-Scholes

option-pricing model and using the following assumptions: a dividend yield of

As of June 30, 2023 and December 31, 2022, the Company has recorded

issued and outstanding options to purchase a total of

| Number of Stock Options | ||||

| Stock options vested (based on ratable vesting) | ||||

| Stock options unvested | ||||

| Total stock options outstanding at June 30, 2023 | ||||

For the year ended December 31, 2022:

| Number of Stock Options | ||||

| Stock options vested (based on ratable vesting) | ||||

| Stock options unvested | ||||

| Total stock options outstanding at December 31, 2022 | ||||

Number

of | Weighted Average Exercise Price | |||||||

| Outstanding at December 31, 2022 | $ | |||||||

| Options granted | $ | |||||||

| Options exercised | ||||||||

| Options expired/forfeited | ( | ) | $ | |||||

| Outstanding at June 30, 2023 | $ | |||||||

On March 1, 2023, the Company granted an award of

16

On December 21, 2022, the Company granted an award of

On November 16, 2022, the Company granted an award of

On September 6, 2022, the Company granted an award of

On June 3, 2022, the Company granted an award of

On March 14, 2022, the Company granted an award of

On January 6, 2022, the Company granted awards of

For the three months ended June 30, 2023 and 2022, the equity-based

compensation expense was $

As of June 30, 2023, the remaining unrecognized equity-based compensation

(which includes RSUs, PSUs and stock options) of approximately $

9. Commitments and Contingencies

Master Services Agreements:

As of June 30, 2023, the Company had three active

master services agreements with third parties to conduct its clinical trials and manage clinical research programs and clinical development

services on behalf of the Company. The Company expects these agreements or amended current agreements to have total expenditures of approximately

$

Consulting Services Agreements:

On November 20, 2014, the Company entered into a ten-year consulting

services agreement with Dr. Joshua Hare, its CSO. Under the agreement, the Company has agreed to pay the CSO $

Technology Services Agreement:

On March 27, 2015, the Company entered into a technology services

agreement with Optimal Networks, Inc. (a related company owned by Dr. Joshua Hare’s brother-in-law) for use of information technology

services. The Company agreed to issue the related party equity incentive units in the amount equal to

17

Exclusive Licensing Agreements:

UM Agreement

On November 20, 2014, the Company entered into an Exclusive License

Agreement with UM for the use of certain Aging-related Frailty MSC technology rights developed by our Chief Science Officer at UM. The

UM License is a worldwide, exclusive license, with right to sublicense, with respect to any and all know-how specifically related to

the development of the culture-expanded MSCs for Aging-related Frailty used at the IMSCs, all SOPs used to create the IMSCs, and all

data supporting isolation, culture, expansion, processing, cryopreservation and management of the IMSCs. The Company is required to pay

UM (i) a license issue fee of $

The milestone payment amendments shifted the triggering payments to

three payments of $

The Company has the right to terminate the UM License upon 60 days’

prior written notice, and either party has the right to terminate upon a breach of the UM License. To date, the Company has made payments

totaling $

CD271

On December 22, 2016, the Company entered into an exclusive license

agreement with an affiliated entity of Dr. Joshua Hare, JMH MD Holdings, LLC (“JMHMD”), for the use of CD271 cellular therapy

technology. The Company recorded the value of the cash consideration and membership units issued to obtain this license agreement as

an intangible asset.

Other Royalty

Under the grant award agreement with the Alzheimer’s Association, the Company may be required to make revenue sharing or distribution of revenue payments for products or inventions generated or resulting from this clinical trial program. The potential payments, although not currently defined, could result in a maximum payment of five times (5x) the award amount.

18

Contingencies – Legal

On September 13, 2021, the Company and certain of its directors and

officers were named as defendants in a securities lawsuit filed in the U.S. District Court for the Southern District of Florida and brought

on behalf of a purported class. The suit alleges there were materially false and misleading statements made (or omissions of required

information) in the Company’s initial public offering materials and in other disclosures during the period from our initial public

offering on February 12, 2021, through August 12, 2021, in violation of the federal securities laws. The action sought damages on behalf

of a proposed class of purchasers of the Company’s Common Stock during said period. On July 12, 2022, all parties preliminarily

agreed to settle the action for approximately $

10. Employee Benefits Plan

The Company sponsors a defined contribution employee benefit plan (the “Plan”) under the provisions of Section 401(k) of the Internal Revenue Code. The Plan covers substantially all full-time employees of the Company who have completed one year of service. Contributions to the Plan by the Company are at the discretion of the Board of Directors.

The Company contributed approximately $

11. Loss Per Share

Basic and diluted net loss per share have been computed using the weighted-average number of shares of common stock outstanding during the period. We have outstanding stock-based awards that are not used in the calculation of diluted net loss per share because to do so would be anti-dilutive.

| Six months ended June 30, | ||||||||

| 2023 | 2022 | |||||||

| RSUs | ||||||||

| PSUs | ||||||||

| Stock options | ||||||||

| Warrants | ||||||||

| Total | ||||||||

19

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

In this document, the terms “Longeveron,” “Company,” “we,” “us,” and “our” refer to Longeveron Inc. We have no subsidiaries.

This Quarterly Report on Form 10-Q (this “10-Q”) contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that reflect our current expectations about our future results, performance, prospects and opportunities. This 10-Q contains forward-looking statements that can involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this 10-Q, including statements regarding our future results of operations and financial position, business strategy, prospective products, product approvals, research and development costs, future revenue, timing and likelihood of success, plans and objectives of management for future operations, future capital raising, future results of anticipated products and prospects, plans and objectives of management are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” or “would” or the negative of these terms or other similar expressions, although not all forward-looking statements contain these words. Factors that could cause actual results to differ materially from those expressed or implied in any forward-looking statements contained in this report include, but are not limited to, statements about:

| ● | the ability of our clinical trials to demonstrate safety and efficacy of our product candidates, and other positive results; | |

| ● | the timing and focus of our ongoing and future preclinical studies and clinical trials, and the reporting of data from those studies and trials; | |

| ● | the size of the market opportunity for our product candidates, including our estimates of the number of patients who suffer from the diseases we are targeting; | |

| ● | the success of competing therapies that are or may become available; | |

| ● | the beneficial characteristics, safety, efficacy and therapeutic effects of our product candidates; | |

| ● | our ability to obtain and maintain regulatory approval of our product candidates; | |

| ● | our plans relating to the further development of our product candidates, including additional disease states or indications we may pursue; | |

| ● | our plans and ability to obtain or protect intellectual property rights, including extensions of existing patent terms where available and our ability to avoid infringing the intellectual property rights of others; | |

| ● | the need to hire additional personnel and our ability to attract and retain such personnel; | |

| ● | our estimates regarding expenses, future revenue, capital requirements and needs for additional financing; | |

| ● | our need to raise additional capital, the difficulties we may face in obtaining access to capital, and the dilutive impact it may have on our investors; | |

| ● | our financial performance and ability to continue as a going concern; and | |

| ● | the period over which we estimate our existing cash and cash equivalents will be sufficient to fund our future operating expenses and capital expenditure requirements. |

The forward-looking statements contained in this 10-Q are made on the basis of the views and assumptions of management regarding future events and business performance as of the date this 10-Q is filed with the Securities and Exchange Commission (the “SEC”). In addition, we operate in a highly competitive and rapidly changing environment; therefore, new risk factors can arise, and it is not possible for management to predict all such risk factors, nor to assess the impact of all such risk factors on our business or the extent to which any individual risk factor, or combination of risk factors, may cause results to differ materially from those contained in any forward-looking statement. We do not undertake any obligation to update these statements to reflect events or circumstances occurring after the date this 10-Q is filed. In addition, this discussion and analysis should be read in conjunction with our unaudited condensed financial statements and notes thereto included in this 10-Q and the audited condensed financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2022, filed with the SEC on March 14, 2023 (“2022 10-K”). Operating results are not necessarily indicative of results that may occur in future periods.

Overview and Recent Developments

Overview

We are a clinical stage biotechnology company developing regenerative medicines to address unmet medical needs. The Company’s lead investigational product is Lomecel-B™, an allogeneic medicinal signaling cell (MSC) formulation sourced from bone marrow of young, healthy adult donors. Lomecel-B™ has multiple potential mechanisms of action that promote tissue repair and healing with broad potential applications across a spectrum of disease areas. The underlying mechanism(s) of action that lead to the tissue repair programs include the stimulation of new blood vessel formation, modulation of the immune system, reduction in tissue fibrosis, and the stimulation of endogenous cells to divide and increase the numbers of certain specialized cells in the body.

20

We are currently pursuing three pipeline indications: Hypoplastic Left Heart Syndrome (HLHS), Aging-related Frailty, and Alzheimer’s disease (AD). Our mission is to advance Lomecel-B™ and other cell-based candidates into pivotal Phase 3 trials, with the goal of achieving regulatory approvals, subsequent commercialization, and broad use by the healthcare community.

Our HLHS program is focused on the potential clinical benefits of Lomecel-B™ as an adjunct therapeutic to standard-of-care HLHS surgery. HLHS is a rare and devastating congenital heart defect in which the left ventricle is severely underdeveloped. As such, babies born with this condition die shortly after birth without undergoing a complex series of reconstructive heart surgeries. Despite the life-saving surgical interventions, clinical studies show that only 50 to 60 percent of affected individuals survive to adolescence. We have early clinical state evidence supporting pro-vascular, pro-regenerative, and anti-inflammatory properties of Lomecel-B™ to improve heart function in HLHS patients. We have completed a Phase 1 open-label study (ELPIS)1 that supported the safety and tolerability of Lomecel-B™ for HLHS, when directly injected into the functional right ventricle during the second-stage standard-of-care surgery (adding minimal additional time to the surgical procedure). Preliminary data also suggested potential benefits on heart function. In addition, our early clinical stage data is favorable as compared to historical controls for survival and reduced need for heart transplants. Longeveron is currently conducting a controlled Phase 2a (ELPIS II)study which, if positive, could add to the clinical data suggesting the functional and clinical benefits of Lomecel-B™ in these patients.

Our other clinical programs focus on aging populations. Life-expectancy has substantially increased over the past century due to medical and public health advancements. However, this longevity increase has not been paralleled by healthspan – the period of time one can expect to live in relatively good health and independence. For many developed and developing countries, healthspan lags life-expectancy by over a decade. This has placed tremendous strain on healthcare systems in the management of aging-related ailments, and presents additional socioeconomic consequences due to patient decreased independence and quality-of-life. Since these strains continue to increase with demographic shifts towards an increasingly older population, improving healthspan has become a priority for health agencies, such as the National Institute on Aging (NIA) of the NIH, the Japanese Pharmaceuticals and Medical Devices Agency (PMDA), and the European Medicines Agency (EMA). As we age, we experience a decline in our own stem cells, a decrease in immune system function (known as “immunosenescence”), diminished blood vessel functioning, chronic inflammation (known as “inflammaging”), and other aging-related alterations that affect biological functioning. Our preliminary clinical data suggest that Lomecel-B™ can potentially address these problems through multiple mechanisms of action (MOAs) that simultaneously target key aging-related processes. Longeveron is currently engaged in clinical programs studying Lomecel-B™ for Alzheimer’s disease and Aging-related Frailty under INDs with the US FDA and under the PMDA in Japan, as well as using Lomecel-B™ in registry trials in The Bahamas.

Summary of Clinical Development Strategy

Our core mission is to become a world-leading regenerative medicine company through the development, approval, and commercialization of novel cell therapy products for unmet medical needs, with a focus on HLHS. Key elements of our current business strategy are as follows.

| ● | Execution of ELPIS II, a Phase 2 randomized controlled trial set forth in greater detail below, to measure the efficacy of Lomecel-B™ in HLHS. This trial is ongoing and is being conducted in collaboration with the National Heart, Lung, and Blood Institute (NHLBI) through grants from the NIH. |

| ● | Continue developing our international programs. Japan is our first non-U.S. territory in which we are conducting a randomized, double-blinded, placebo-controlled clinical trial to evaluate Lomecel-B™ for Aging-related Frailty. With successful completion of this trial and demonstration of safety, we intend to seek marketing approval under the Act on the Safety of Regenerative Medicine (ASRM). We also intend to explore conditional or full approval in Japan of Lomecel-B™ under the Pharmaceuticals and Medical Devices (PMD) Act for the treatment of Aging-related Frailty in the future, which will be guided by results from this trial and potentially others in our Frailty program. We may also explore other indications in Japan, and potentially pursue Aging-related Frailty and other indications in additional international locations for further development and commercialization. We also continue to successfully enroll in our Frailty and Cognitive Impairment registry trials in The Bahamas, and are launching an Osteoarthritis registry trial. |

| ● | Continue to pursue the therapeutic potential of Lomecel-B™ in Alzheimer’s disease (AD). We completed a Phase 1b study, which indicated the potential of Lomecel-B™ to preserve cognition in patients with mild AD through multiple potential mechanisms of action. Based on the outcomes of this trial, we are now conducting a Phase 2a randomized placebo-controlled trial (CLEAR MIND) to determine the safety and effects of up to four doses of Lomecel-B™ infused every 4 weeks in mild AD patients. This study entails a heavy focus on target engagement through multiple endpoints that include evaluation of fluid-based biomarkers, brain imaging, vascular function, and neurocognitive measures. |

| 1 | Sunjay Kaushal, MD, PhD, Joshua M Hare, MD, Jessica R Hoffman, PhD, Riley M Boyd, BA, Kevin N Ramdas, MD, MPH, Nicholas Pietris, MD, Shelby Kutty, MD, PhD, MS, James S Tweddell, MD, S Adil Husain, MD, Shaji C Menon, MBBS, MD, MS, Linda M Lambert, MSN-cFNP, David A Danford, MD, Seth J Kligerman, MD, Narutoshi Hibino, MD, PhD, Laxminarayana Korutla, PhD, Prashanth Vallabhajosyula, MD, MS, Michael J Campbell, MD, Aisha Khan, PhD, Eric Naioti, MSPH, Keyvan Yousefi, PharmD, PhD, Danial Mehranfard, PharmD, MBA, Lisa McClain-Moss, Anthony A Oliva, PhD, Michael E Davis, PhD. “Intramyocardial cell-based therapy with Lomecel-B™ during bidirectional cavopulmonary anastomosis for hypoplastic left heart syndrome: The ELPIS phase I trial” (2023) European Heart Journal Open, 2023. |

21

| ● | Expand our manufacturing capabilities to commercial-scale production. We operate a current good manufacturing practice (cGMP)-compliant manufacturing facility and produce our own product candidates for testing. We continue to improve and expand our capabilities with the goal of achieving cost-effective manufacturing that may potentially satisfy future commercial demand for potential Lomecel-B™ commercialization. |

| ● | Collaborative arrangements and out-licensing opportunities. We will be opportunistic and consider entering into co-development, out-licensing, or other collaboration agreements for the purpose of eventually commercializing Lomecel-B™ and other products domestically and internationally if appropriate approvals are obtained. |

| ● | Product candidate development pipeline through internal research and development, and in-licensing. Through our research and development program, and through strategic in-licensing agreements, or other business development arrangements, we intend to actively explore promising potential additions to our pipeline. |

| ● | Continue to expand our intellectual property portfolio. Our intellectual property is vitally important to our business strategy, and we take significant steps to develop this property and protect its value. Results from our ongoing research and development efforts are intended to add to our existing intellectual property portfolio. |

Clinical Development Pipeline in 2023

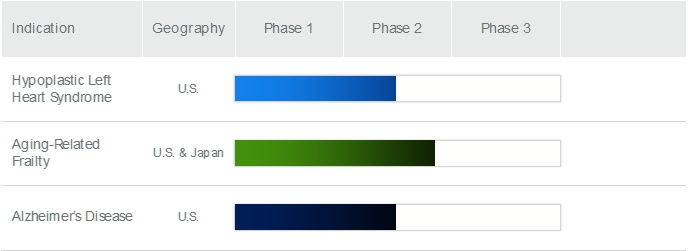

We are currently in clinical development of a single product, Lomecel-B™ for three potential indications (See Figure 1).

Figure 1: Lomecel-B™ clinical development pipeline

Hypoplastic Left Heart Syndrome (HLHS). The FDA granted Lomecel-B™ for the treatment of HLHS a Rare Pediatric Disease (RPD) Designation (on November 8, 2021), Orphan Drug Designation (ODD) (on December 2, 2021), and Fast Track Designation (on August 24, 2022). HLHS is a rare congenital heart condition that affects roughly 1,000 to 2,000 newborns annually in the US. HLHS babies are born with a severely underdeveloped left ventricle. To prevent certain death shortly after birth, these babies undergo a series of three heart surgeries that converts the normally 4-chamber heart into a 3-chamber one with a single ventricle (the right ventricle) supporting systemic circulation. Despite these life-saving surgeries, HLHS patients nevertheless still have high early mortality and morbidity rates due primarily to heart failure.

We are currently conducting an ongoing Phase 2 clinical trial (ELPIS II) under FDA IND 017677. ELPIS II is a multi-center, randomized, double-blind, controlled clinical trial designed to evaluate Lomecel-B™ as an adjunct therapy to the standard-of-care second-stage HLHS heart reconstructive surgery. The primary endpoint is to evaluate improvement in heart function after Lomecel-B™ treatment versus standard-of-care surgery alone (38 subjects total: 19 per arm). This trial is over 50% enrolled, and is funded in part by the NHLBI/NIH. While we cannot predict a specific time when the trial will be fully enrolled, the plan is to complete enrollment around mid-2024. |

22

ELPIS II is a next-step trial to our completed 10-patient open-label Phase 1 trial (ELPIS) under the same IND. This Phase 1 trial was designed to evaluate the safety and tolerability of Lomecel-B™ as an adjunct to the second-stage HLHS surgery, and to obtain preliminary evidence of Lomecel-B™ effect to support a next-phase trial. The primary safety endpoint was met: no major adverse cardiac events (MACE) or treatment-related infections during the first month post-treatment, and no triggering of stopping rules. Furthermore, fluid-based and imaging biomarker data supported multiple potential relevant mechanisms-of-action of Lomecel-B™, and the potential to improve post-surgical heart function. In addition to the 12-month follow-up evaluation on ELPIS, we continue to follow these patients on an annual basis. All 10 patients remain alive without the need for a heart transplant for 3.5 to 5.0 years since treatment with Lomecel-B™ (updated as of May 9, 2023), and five have already successfully undergone the third-stage surgery. Based on historical data, over 15% of patients would be expected to have received a heart transplant or have died within 3-years after the second-stage surgery, rising to nearly 20% by 5 years.

We are prosecuting a number of patent applications relating to the administration of mesenchymal stem cells for treating juvenile HLHS in Taiwan and the Bahamas.

Aging-related Frailty. Aging-related Frailty is a life-threatening geriatric condition that disproportionately increases risks for poor clinical outcomes from disease and injury. While the definition of Aging-related Frailty lacks consensus and would be a new indication from a regulatory standpoint, and while Aging-related Frailty has no approved pharmaceutical or biologic treatments, there are a number of companies now working to develop potential therapeutics for this unmet medical need. We will work with regulatory agencies, such as the U.S. FDA and Japan’s PMDA, to advance Lomecel-B™ as potentially the first approved drug for Aging-related Frailty. |

| ○ | We have previously completed two U.S. clinical trials under FDA IND 016644. One is a multicenter, randomized, placebo-controlled Phase 2b trial which showed that a single infusion of Lomecel-B™ significantly improved 6-Minute Walk Test (6MWT) distance 9 months after infusion, and also showed a dose-dependent increase in 6MWT distance 6 months after infusion. The second is a multicenter, randomized, placebo-controlled Phase 1/2 trial (“HERA Trial”) that showed that Lomecel-B™ was generally safe and well tolerated in patient with Aging-related Frailty, and showed that hemagglutinin inhibition (HAI) assay results in the Lomecel-B™ and placebo groups to influenza were not statistically different, indicating Lomecel-B™ does not suppress the immune system. | |

| ○ | Japan Clinical Trial: The Japanese PMDA has approved a Clinical Trial Notification (CTN), which is equivalent to a U.S. IND, allowing an Investigator-sponsored Phase 2 clinical study for Aging-related Frailty patients in Japan. This study is a 45-patient randomized placebo-controlled study with a primary objective of evaluating the safety of Lomecel-B™ in Japanese patients with Aging-related Frailty. Patient screening began in the 4th quarter of 2022, and the first patient was randomized in the first quarter of 2023. The goal of this study is to enable ASRM approval when combined with previous clinical results in non-Japanese patients.

We are prosecuting a number of patent applications relating to the administration of mesenchymal stem cells for Aging-related Frailty in Taiwan, the Bahamas and United States. |

|

Alzheimer’s disease. Alzheimer’s disease, a devastating neurologic disease leading to cognitive decline, has very limited therapeutic options. An estimated 6.7 million Americans age 65 and older have Alzheimer’s disease, and this number is projected to more than double by 2060. We have been testing Lomecel-B™ as a therapeutic with the possibility to slow the decline in cognitive function in patients with mild (i.e., early-stage) Alzheimer’s disease. Our completed and published Phase 1 clinical trial results suggest that Lomecel-B™ is safe in this population and does not cause Alzheimer Related Imaging Abnormality (ARIA), a serious complication of certain treatment strategies. Our early study also suggested the possibility of a therapeutic effect, and we are testing this possibility in a new Phase 2 clinical trial.

In the Phase 1 multicenter randomized placebo-controlled trial, patients received a single dose of Lomecel-B™ or placebo, and were evaluated for one year thereafter. The trial met its primary endpoint of safety (incidence of serious adverse events – SAEs – within one month of treatment), and supported the safety and tolerability of Lomecel-B™ through additional endpoint measures. Furthermore, through evaluation of blood-based and imaging biomarkers, neurocognitive assessments and quality-of-life measures, the trial provided insights into mechanisms of action of Lomecel-B™ for Alzheimer’s disease, as well as indications of potential to improve clinical outcomes2. | |

| 2 | Mark Brody, Marc Agronin, Brad J. Herskowitz, Susan Y. Bookheimer, Gary W. Small, Benjamin Hitchinson, Kevin Ramdas, Tyler Wishard, Katalina Fernández McInerney, Bruno Vellas, Felipe Sierra, Zhijie Jiang, Lisa McClain-Moss, Carmen Perez, Ana Fuquay, Savannah Rodriguez, Joshua M. Hare, Anthony A. Oliva Jr., Bernard Baumel. “Results and insights from a phase I clinical trial of Lomecel-B™ for Alzheimer’s disease” (2023) Alzheimer’s & Dementia: The Journal of the Alzheimer’s Association 19:261-273. |

23

The company is now conducting a next-step Phase 2a trial, CLEAR MIND, to evaluate multiple doses of Lomecel-B™ in patients with mild Alzheimer disease (ClinicalTrials.gov #NCT05233774). Each patient receives 4 treatments with Lomecel-B™, 4 treatments with placebo, or 1 treatment with Lomecel-B™ followed by 3 treatments with placebo, with each treatment delivered by intravenous (IV) infusion separated by 4 weeks. Patients are then followed for 9 months from the start of the first treatment. The primary objective is safety of multiple treatments with Lomecel-B™. This study also entails a rigorous evaluation of target engagement through endpoints that include evaluation of fluid-based biomarkers, brain imaging via magnetic resonance imaging (MRI), vascular function, and neurocognitive measures. Forty-nine (49) subjects have been enrolled and have received Lomacel-B™. The last patient visit is projected near the end of the third quarter of 2023, and topline CLEAR MIND results are expected around early October of 2023.

We are prosecuting a number of patent applications relating to the administration of allogenic mesenchymal stem cells for treating Alzheimer’s Disease in Hong Kong, South Africa, Singapore, Korea, New Zealand, Japan, Israel, Canada, Australia, the Bahamas, and the United States. |

| ○ | The Bahamas Registry Trials: We sponsor and operate Registry Trials in Nassau and Lyford Cay in The Bahamas, where participants may receive Lomecel-B™ for Aging-related Frailty and other indications, at the participant’s own expense. Lomecel-B™ is designated as an investigational product in The Bahamas. |

Impact of Macroeconomic Conditions

We have not to date been directly adversely impacted by the current banking sector volatility, and specifically the volatility being experienced within the regional banking sector volatility. However, we previously maintained deposits and marketable securities with a regional bank, and have made the determination, in light of such volatility and uncertainty, to transfer our deposits and marketable securities to a larger bank, so as to mitigate the likelihood of our experiencing a direct adverse impact from any ongoing or future volatility within the regional banking sector.

In addition, although we have experienced some supply constraints and marginal price increases, to date current macroeconomic conditions have not materially impacted our programs or our operations. We continue to monitor economic conditions in the U.S. and globally and expect to act proactively where possible to minimize the impact of continued inflation or supply constraints on materials and inventory needed for operations.

Components of Our Results of Operations

Revenue

We have generated revenue from three sources:

| ● | Grant awards. Extramural grant award funding, which is non-dilutive, has been a core strategy for supporting our ongoing clinical research. Since 2016 our clinical programs have received over $16.0 million in competitive extramural grant awards ($11.5 million which has been directly awarded to us and which are recognized as revenue when the performance obligations are met) from the NIH, Alzheimer’s Association, and Maryland Stem Cell Research Fund (MSCRF). |

| ● | The Bahamas Registry Trial. Participants in The Bahamas Registry Trial pay us a fee to receive Lomecel-B™, imported into The Bahamas, and administered at one of two private medical clinics in Nassau. While Lomecel-B™ is considered an investigational product in The Bahamas, under the approval terms received from the National Stem Cell Ethics Committee, we are permitted to charge a fee for participation in the Registry Trial. The fee is recognized as revenue, and is used to pay for the costs associated with manufacturing and testing of Lomecel-B™, administration, shipping and importation fees, data collection and management, biological sample collection and sample processing for biomarkers and other data, and overall management of the Registry, including personnel costs. Lomecel-B™ is considered an investigational treatment in The Bahamas and is not licensed for commercial sale. |

| ● | Contract development and manufacturing services. From time to time, we enter into fee-for-service agreements with third parties for our product development and manufacturing capabilities. |

Cost of Revenues

We record cost of revenues based on expenses directly related to revenue. For grants we record allocated expenses for research and development costs to a grant as a cost of revenues. For the clinical trial revenue, directly related expenses for that program are allocated and accrued as incurred. These expenses are similar to those described under “Research and Development Expenses” below.

Selling and Marketing Expenses

Selling and marketing expenses consist primarily of royalty and license fees associated with our agreements with the University of Miami as well as attending and sponsoring industry, investment, organization and medical conferences and events.

24

Research and Development Expenses

Research and development costs are charged to expense when incurred in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 730 Research and Development. ASC 730 addresses the proper accounting and reporting for research and development costs. It identifies: first, those activities that should be identified as research and development; second, the elements of costs that should be identified with research and development activities, and the accounting for these costs; and third, the financial statement disclosures related to them. Research and development include costs such as clinical trial expenses, contracted research and license agreement fees with no alternative future use, supplies and materials, salaries, share-based compensation, employee benefits, property and equipment depreciation and allocation of various corporate costs. We accrue for costs incurred by external service providers, including contract research organizations (CROs) and clinical investigators, based on estimates of service performed and costs incurred. These estimates include the level of services performed by the third parties, subject enrollment in clinical trials, administrative costs incurred by the third parties, and other indicators of the services completed. Based on the timing of amounts invoiced by service providers, we may also record payments made to those providers as prepaid expenses that will be recognized as expense in future periods as the related services are rendered.

We currently do not carry any inventory for our product candidates, as we have yet to receive regulatory approval and launch a product for commercial distribution. Historically our operations have focused on conducting clinical trials, product research and development efforts, and improving and refining our manufacturing processes, and accordingly, manufactured clinical doses of product candidates were expensed as incurred, consistent with the accounting for all other research and development costs. Once we begin commercial distribution, all newly manufactured approved products will be allocated either for use in commercial distribution, which will be carried as inventory and not expensed, or for research and development efforts, which will continue to be expensed as incurred.

We expect that our research and development expenses will increase in the future as we increase our headcount to support increased research and development activities relating to our clinical programs, as well as incur additional expenses related to our clinical trials.

General and Administrative Expenses

General and administrative expenses consist primarily of salaries and other related costs, including stock-based compensation, for personnel in our executive, finance, business development and administrative functions. General and administrative expenses also include public company related expenses; legal fees relating to corporate matters; insurance costs; professional fees for accounting, auditing, tax and consulting services; travel expenses; and facility-related expenses, which include direct depreciation costs and allocated expenses for rent and maintenance of facilities and other operating costs.

We expect that our general and administrative expenses will increase in the future as we increase our headcount to support the administrative activities related to being a public company, including costs of accounting, audit, legal, regulatory and tax-related services associated with maintaining compliance with Nasdaq and SEC requirements, director and officer insurance costs, and investor and public relations costs.

Other Income and Expenses

Interest income consists of interest earned on cash equivalents and marketable securities. We expect our interest income to fluctuate due to changes in the current cash and marketable securities balances. Other income consists of funds earned that are not part of our normal operations. In past years they have been primarily a result of tax refunds received for social security taxes as part of a research and development tax credit program.

Income Taxes