UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM

__________________________

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to

Commission file number:

__________________________

(Exact name of Registrant as specified in its charter) |

__________________________

| ||

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

| |

| ||

(Address of principal executive offices) |

| (Zip Code) |

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol |

| Name of the exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of the common stock held by non-affiliates of the registrant, based on the closing price of a share of common stock on June 30, 2023 as reported by the NYSE American on such date was approximately $

As of March 12, 2024, the registrant had

CATHETER PRECISION, INC.

TABLE OF CONTENTS

| 2 |

| Table of Contents |

CATHETER PRECISION, INC.

PART I

Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available. This section should be read in conjunction with our audited financial statements and related notes included in Part II, Item 8 of this report. The statements contained in this Annual Report on Form 10-K that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements can be identified by words such as “believe,” “anticipate,” “may,” “might,” “can,” “could,” “continue,” “depends,” “expect,” “expand,” “forecast,” “intend,” “predict,” “plan,” “rely,” “should,” “will,” “may,” “seek,” or the negative of these terms and other similar expressions, although not all forward-looking statements contain these words. You should read these statements carefully because they discuss future expectations, contain projections of future results of operations or financial condition, or state other “forward-looking” information. These statements relate to our future plans, objectives, expectations, intentions and financial performance and the assumptions that underlie these statements.

These forward-looking statements are subject to a number of risks, uncertainties, and assumptions, including, but not limited to, those described in “Risk Factors.” These forward-looking statements reflect our beliefs and views with respect to future events and are based on estimates and assumptions as of the date of this Annual Report on Form 10-K and are subject to risks and uncertainties. We discuss many of these risks in greater detail in the section entitled “Risk Factors” included in Part I, Item 1A and elsewhere in this report. Given these uncertainties, you should not place undue reliance on these forward-looking statements. We qualify all of the forward-looking statements in this Annual Report on Form 10-K by these cautionary statements. Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, whether as a result of new information, future events or otherwise.

This Annual Report on Form 10-K also contains estimates, projections and other information concerning our industry, our business, and the markets for certain diseases, including data regarding the estimated size of those markets. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained this industry, business, market, and other data from reports, research surveys, studies, and similar data prepared by market research firms and other third parties, industry, medical and general publications, government data, and similar sources.

| 3 |

| Table of Contents |

ITEM 1. BUSINESS

Overview

The registrant (together with our consolidated operating subsidiary, the “Company” or “Catheter”) was incorporated under the name “Ra Medical Systems, Inc.” as a Delaware corporation in July 2018. A predecessor had been incorporated in California in September of 2002, but was reincorporated in 2018 in connection with our initial public offering. The Company was initially formed to develop, commercialize and market an excimer laser-based platform for use in the treatment of vascular and dermatological immune-mediated inflammatory diseases, including the DABRA product line.

On January 9, 2023, the Company merged with Catheter Precision, Inc., or “Old Catheter”, a privately-held Delaware corporation (the “Merger”), and the business of Old Catheter became a wholly owned subsidiary of the Company, which today is our only operating subsidiary. Following the Merger, we discontinued the Company’s legacy lines of business and the use of any of its DABRA-related assets. For further information about these historical lines of business, see “Item 1. Business” of the Company’s Form 10-K for the fiscal year ended December 31, 2021. Since the Merger, we have shifted the focus of our operations to Old Catheter’s product lines. Accordingly, our current activities primarily relate to Old Catheter’s historical business which comprises the design, manufacture and sale of new and innovative medical technologies focused in the field of cardiac electrophysiology, or “EP.”

Our primary product is the VIVO System which is an anacronym for View into Ventricular Onset System(“VIVO” or “VIVO System”) which is a non-invasive imaging system that offers 3D cardiac mapping to help with localizing the sites of origin of idiopathic ventricular arrhythmias in patients with structurally normal hearts prior to EP procedures.

Our newest product, LockeT, is a suture retention device indicated for wound healing by distributing suture tension over a larger area in the patient in conjunction with a figure of eight suture closure. LockeT is intended to temporarily secure sutures and aid clinicians in locating and removing sutures efficiently.

Our product portfolio also includes the Amigo® Remote Catheter System, or Amigo, a robotic arm that serves as a catheter control device. Prior to 2018, Old Catheter marketed Amigo. We own the intellectual property related to Amigo, and this product is under consideration for future research and development of a generation 2 product.

Electrophysiology Market Overview

EP is one of healthcare’s largest sectors and rapidly growing. The EP market includes well known medical devices such as pacemakers, electrocardiogram, or ECG, systems and cardiac catheters, but also laboratory equipment such as intracardiac mapping systems and fluoroscopy systems (similar to x-ray in real time). The EP market includes large medical device companies such as Medtronic, Plc., Abbott Laboratories, Biosense-Webster (J&J) and Boston Scientific Corp. and is estimated to be $15.1 billion by 2028 (CAGR of 13.0%). Population growth, increasing rates of heart disease and the rising cost of healthcare are driving growth in the EP markets.

| 4 |

| Table of Contents |

Within the EP market, we focus our products on the catheter ablation market. The catheter ablation market was $3.2 billion in 2020 and estimated to grow to $6.4 billion in 2026. The catheter ablation market is growing at a faster rate (12.4% CAGR) than the EP market as a whole.

Within the last 10 years, ventricular ablation has become a fast-growing treatment option. Currently, there are about 80,000 ventricular ablations annually and VT ablations represent approximately 16% of ablations in the U.S. Currently, the market is underserved, and this number is expected to increase to over 250,000 procedures by 2026. The ventricular ablation market is expected to grow at a 21% CAGR through 2026, which is a faster rate than the global EP market and the catheter ablation market as a whole. The growth in the ventricular ablation market is driven by an aging population, advances in EP technology as well as updated physician guidelines. The Heart Rhythm Society, or HRS, Expert Consensus Statement on Catheter Ablation of Ventricular Arrhythmias, published in May 2019 recommends catheter ablation in preference to anti arrhythmic drugs or in the situation where anti arrhythmic therapy has failed or is not tolerated. The guidelines also recommend ablation for reducing recurrent VT and implantable cardioverter-defibrillator shocks.

Existing Treatments and Methods for Catheter Ablations

Traditionally, the first line of treatment for cardiac arrhythmias is medication. Unfortunately, this is not a permanent fix and most patients eventually need a catheter ablation.

Catheter Ablation Procedure Overview

An electrophysiologist stands next to the patient’s bed near the patient’s groin. A catheter or catheters are inserted into the femoral vein (located at the groin) and navigated into the right side of the heart. Depending on the type of arrhythmia, the catheter is inserted into the atrium or the ventricle. Once inserted, a diagnostic catheter is used in conjunction with an invasive (traditional) mapping system to create a map of the patient’s heart. This allows the physician to see the individual patient’s cardiac structures and size. Once the map is created, the physician begins to “pace map.” This process requires the physician to move the catheter from spot to spot to determine the electrical conduction at different areas to determine if the tissue in that area is responsible for the arrhythmia. Once the area is located, the physician will provide a form of energy (radiofrequency, cryo, etc.) to ablate the tissue in that spot.

Treatment Challenges for Ventricular Arrhythmias

Treatment of ventricular ablations with cardiac ablations is a relatively new treatment option. As a result, we believe that the patient population is underserved and is not as well understood, and the available techniques and technologies are limited when compared to the atrial ablation options.

| 5 |

| Table of Contents |

Ablation locations within the ventricle are very difficult to identify. Often, patients are highly symptomatic (dizzy, breathing difficulties, etc.) but the arrhythmia is infrequent. When this happens, it is hard to predict when the patient will be having an “active” arrhythmia. Because of this, the physician may not be able to identify the location even when using medication to induce the arrhythmia. Without confirmation during invasive mapping, the patient is removed from the electrophysiology lab without the ablation procedure being performed and the patient is required to return at a later date and try again for a successful outcome.

Even when a patient has frequent ventricular arrhythmias, the process of pace-mapping often takes 4 – 5 hours to identify the location for ablation, which can increase the likelihood of patient complications due to the extended time under anesthesia.

Lastly, many patients with untreated ventricular arrhythmias cannot tolerate anesthesia well, thus invasive mapping that takes a long time is not an option for them.

Treatment Challenges for Atrial Arrhythmias

Catheter ablation for atrial arrhythmias is more standardized and “advanced” than for ventricular ablations, thus less pace mapping is required. Instead, a procedure called Pulmonary Vein Isolation (“PVI”) is performed for atrial fibrillation, and a single line is ablated for atrial flutter. In pulmonary vein isolation, tiny scars are created in the left upper chamber of the heart in the area where the four lung (pulmonary) veins connect.

Despite steady improvement in the tools available to perform effective procedures, there is clear study evidence that catheter based atrial fibrillation treatment technology can become more effective. According to a study entitled “Long Term Outcomes of Catheter Ablation of Atrial Fibrillation: A Systematic Review and Meta- Analysis” published in the Journal of American Heart Association on March 18, 2013, which looked at multiple individual studies covering over 6,000 patients, “single procedure freedom from atrial fibrillation at long term follow up was 53.1%.” The same study found “with multiple procedures performed, the long-term success rate was 79.8%.” Ineffective treatment may result in patients undergoing two or more EP procedures to achieve relief from atrial fibrillation at an estimated cost in the range of $20,000 or more per procedure.

Specific reasons have not been proven for the lower success rate of initial ablation procedures. However, there is growing evidence that better results occur if the treating EP physician is able to make better lesions by maintaining stable contact force of the catheter against the heart wall, thereby reliably delivering the energy required to eliminate the abnormal rhythms. Variation in catheter contact force occurs as the physician attempts to manually position and hold the catheter tip in a stable position during cases lasting 2 to 3 hours in order to perform typically over 100 ablations of the cardiac anatomy.

Large multi-national medical device companies, such as Medtronic, Inc., Boston Scientific Corp., Abbott Laboratories, St. Jude Medical, Inc. and the Biosense Webster division of Johnson & Johnson, among others, continue to invest heavily to develop and introduce new devices and technologies to improve patient outcomes. Included among these are force-sensing catheters, including the Biosense SmartTouch TM catheter, which provide a continuous readout of the contact force between the catheter and the heart wall. Our Vivo System is focused on the controlled delivery of these catheter technologies to enhance both the performance of ablation procedures and the ease and safety for the physicians who perform them.

A recent peer-reviewed multicenter study sponsored by Biosense Webster, entitled “Paroxysmal AF Catheter Ablation with a Contact Force Sensing Catheter” published in 2014 found that catheter ablation success rates can be as high as 80% when the physician is able to maintain stable contact force within investigator selected working ranges. “When the CF (contact force) employed was between investigator selected working ranges > 80% of the time during therapy, outcomes were 4.25 times more likely to be successful.” Further, “stable CF during radiofrequency application increases the likelihood of twelve-month success.” However, it should be noted that, using manually controlled methods, the physicians in the study could only maintain optimal tissue contact in less than 30% of the patients studied.

In addition, another study, sponsored by St. Jude Medical, Inc. and published in 2015 showed similar findings using their recently FDA-approved contact-force sensing catheter, TOCCASTAR. In the TOCCASTAR study, 85.5% of ablation procedure patients were free of atrial fibrillation at one year after the procedure when optimal catheter tip contact force was maintained, versus only 67.7% when non-optimal contact force was achieved.

| 6 |

| Table of Contents |

VIVO Clinical Use and Studies

To date, VIVO has been used in more than 1,000 procedures, by more than 30 physicians in 10 countries. Initial clinical work was completed with the first-generation software, which resulted in FDA 510(k) Clearance in June 2019.

The U.S. multi-center study enrolled 51 patients from 5 centers. Of note, the Principal Investigator and center to have the highest enrollment was Johns Hopkins University in Baltimore, Maryland. This study was conducted to evaluate the accuracy of VIVO as compared to invasive mapping systems (current prevailing method for determining arrhythmia origins). VIVO met all study endpoints and correctly matched the predicted arrhythmia origin in 44/44 patients (100%; primary endpoint) and correctly matched paced sites in 225/226 locations (99.56%; secondary endpoint). In some instances, this study showed that VIVO has better predictability for arrhythmia origin than a physician’s manual review of a 12 lead ECG.

While conducting the initial clinical study for FDA submission, we developed generation 2 in parallel with a goal to have this version complete and ready to submit upon 510(k) clearance of generation 1. We successfully achieved this goal and received CE Mark and FDA 510(k) Clearance for generation 2 in 2020.

Additional clinical work has occurred with generation 2. Until recently, this data has been single center, physician-initiated research and has resulted in peer reviewed clinical science at electrophysiology conferences and in journals.

Three physicians, at different centers, in the UK conducted a feasibility study for Stereotactic Ablative Radiotherapy, or SABR, and published their data on nine patients. SABR is an ablation technique utilizing non-invasive methods akin to proton therapy for cancer treatment. To do a complete non-invasive ablation, accurately predicting the ablation location non-invasively is key to procedural success, and VIVO was utilized for this purpose. Non-invasive ablation is a new technique and requires additional data, but it is showing promise and has generated excitement within the EP community. If accepted for wide-spread treatment, this would allow for previously un-ablatable patients to receive lifesaving treatments.

In February 2023, a study from the Royal Brompton Hospital was published. This study enrolled 15 patients with 24 VTs (ventricular contractions) and PVCs (premature ventricular contractions). VIVO accurately identified VT and PVC origin in 23/24 (96%) and sub-localized in 100% of subjects. Acute success was achieved in 100% of cases. Standard ECG algorithms, conducted by 3 physicians in blind trials, only identified the correct chamber in 50-88% of the patients and sub-localized within the right ventricular outflow tract (septum v free wall) in 37 – 58% of subjects. Of note, six patients had previously attended for nine attempted ablations collectively, which were either unsuccessful or aborted owing to lack of spontaneously occurring clinical PVCs. One patient had previously reported for four separate attempts without PVCs and ablations were aborted, but collection of a single beat allowed VIVO to create an analysis map and provide the physician with information to complete the ablation for all these patients. In addition, this study showed a 27% reduction in procedure time when using VIVO as compared to a historical cohort. This study concluded that VIVO can accurately identify arrhythmia origin with an accuracy that is superior to that of established ECG algorithms.

In April 2022, one physician from the Netherlands presented an abstract at EHRA (European Heart Rhythm Association), focused on using VIVO as a way to screen patients prior to the ablation procedure. This study of 15 patients concludes that using VIVO pre-procedurally may enable the physician to determine procedure success rates and prevent unnecessary ablation procedures. This data will need to be further studied in larger numbers but determining success in advance of the procedure would improve ablation therapy, which has a high failure rate and thus requires additional ablation procedures.

In October 2021 the first patient was enrolled in the VIVO EU Registry. This registry aims to gather data about how VIVO is used in real-world settings, outside of a rigorous clinical study. The registry will enroll 125 patients across Europe and the UK and collect information about different workflows and applications for VIVO. Enrollment of 125 patients was completed in June 2023. The study requires 12 month follow-up and data collection is planned for completion in Q3 2024.This data serves multiple purposes including fulfilling European regulatory requirements for on-going data collection, publication of multi-center data, and future development of studies and improvements to the VIVO technology.

| 7 |

| Table of Contents |

Currently, there is an ongoing physician initiated study at Coventry hospital in the UK. This study will enroll 50 patients with Re-entrant Ventricular Tachycardia. These patients have hearts that are not structurally normal and scarred tissue is present in the ventricle. This data will be used for publication and to support an FDA submission to expand the current labeling of the existing product.

Our Products

VIVO™ System

Our lead product, VIVO, is an FDA-cleared and CE marked product that utilizes non-invasive inputs to locate the origin of ventricular arrhythmias. VIVO has been used in more than 1,000 procedures in leading U.S. and European hospitals under a limited commercial launch that commenced in the third quarter of 2021. A full scale commercial launch commenced in Q1 2023 in conjunction with the expansion of a direct sales force in the US.

VIVO is a non-invasive imaging system that offers 3D cardiac mapping to help with localizing the sites of origin of idiopathic ventricular arrhythmias in patients with structurally normal hearts prior to electrophysiology procedures. The VIVO system has achieved a CE Mark allowing it to be commercialized in the European Union and has been placed at several hospitals in Europe. FDA 510(k) Clearance in the United States was received in June 2019.

The VIVO software is provided on an off the shelf laptop, and the system includes a 3D camera. In addition, the system can only be used with a disposable component, the VIVO Positioning Patches, which are required for each procedure.

|

|

|

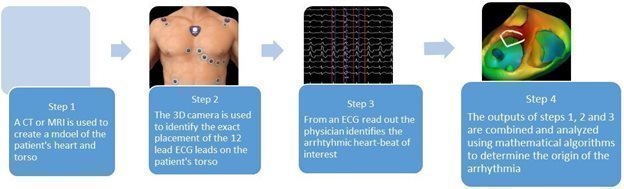

The VIVO software contains proprietary algorithms that are based on standard EP principles. However, the accuracy of the algorithms is improved because it does not use generalized assumptions and instead, uses patient specific information. VIVO uses standard clinical inputs such as a CT or MRI and a 12 lead ECG, both of which are routinely gathered for most EP procedures, allowing VIVO to seamlessly integrate into the workflow. A 3D photograph is obtained of the patient’s torso after the ECG leads are in place and all of these clinical inputs are combined to generate a 3D map of the patient’s heart with a location of the earliest onset of the ventricular arrhythmia.

| 8 |

| Table of Contents |

VIVO Workflow

LockeT

LockeT, a suture retention device, is a sterile, Class I product that was registered with the FDA in February 2023, at which time we began initial shipments to distributors. In May 2023, Catheter submitted LockeT for CE Mark approval. CE Mark approval is expected in the second half of 2024, at which time initial international shipments to distributors will begin. LockeT is indicated for wound healing by distributing suture tension over a larger area in the patient in conjunction with a figure of eight suture closure and is intended to temporarily secure sutures and aid clinicians in locating and removing sutures efficiently.

|

|

|

| 9 |

| Table of Contents |

Clinical studies for LockeT began during 2023. The three phases of the current studies are planned to show the product’s effectiveness and benefits, including faster wound closure, earlier ambulation, potentially leading to early hospital discharge, and lower costs for the healthcare provider and/or insurance payor. This data is intended to provide crucial data for marketing and to expand our indications for use with the FDA. See License and Other Agreements below.

The Phase I - First in Man Feasibility Study was completed in 2023 and showed the device works for its intended purpose, that there were no safety events and gathered initial data to support Phase II submission to Institutional Review Board (IRB). The results were submitted to the Journal of American Academy of Cardiologists in January 2024.

Phase II received IRB approval in late 2023 and is anticipated to be completed by June 2024. This phase will compare manual compression (standard of care) to LockeT in a one-to-one randomized study of 100 patients and assess improved time to hemostasis and ambulation when using LockeT versus manual compression.

Phase III IRB approval is in process and will compare LockeT to one or more competitive products in a one-to-one randomized study of 100 patients and will include cost comparisons and assess risk of hematoma when using LockeT versus those competitive products. We anticipate this phase to be completed in early 2025.

Our Previously Marketed DABRA Product

Prior to the Merger, we manufactured and marketed DABRA, a portable excimer laser console with proprietary, single-use catheters for the minimally invasive endovascular treatment of vascular blockages resulting from lower extremity vascular disease in both above and below the knee lesions.

The DABRA catheter transmitted energy from the laser to the vascular blockage. The laser energy traveled through the catheter and ablated the blockage, reducing it to chemicals that were found naturally in the bloodstream. The catheters were specifically designed for use with our excimer laser. The DABRA catheter used a liquid-filled plastic tubing allowing for the efficient and precise delivery of the laser energy.

Subsequent to the Merger, we no longer manufactured or marketed DABRA.

Our Solutions

Adoption of our VIVO System by electrophysiologists is expected to enhance their ability to diagnose and treat cardiac arrhythmias.

Non-invasive mapping prior to the ablation procedure provides a solution for patients that could not be ablated previously. First, many patients with VT do not tolerate anesthesia well. By providing a non-invasive solution to determine the ablation location, physicians are better able to understand where the arrhythmia originates and how easily one can access the ablation location, minimizing the amount of time that the patient may need to be anesthetized, and allowing many patients the ability to have an ablation that otherwise could not. Second, many patients are highly symptomatic, but do not have PVCs often. In these situations, the patients are often brought in for ablation procedures only to have no arrhythmia and sent home time and time again. In these instances, the physicians can monitor the patient prior to hospitalization and obtain information about the arrythmia. In this way, the patient can still proceed to an ablation procedure without having PVCs on the day of surgery.

Non-invasive mapping also enables planning prior to the start of the procedure. This enables the physicians to better understand where they are targeting, which enables them to make advanced decisions about where they are navigating the catheter and which catheter(s) they are using, reducing both procedure time and cost.

Surgery patients who are offered the LockeT device are expected to benefit from faster wound closure, more comfort than manual compression and earlier ambulation, potentially leading to early hospital discharge and lower costs for the healthcare provider and/or insurance payor.

| 10 |

| Table of Contents |

Our Strategy

Our goal is to become a leading medical imaging company in the field of cardiac electrophysiology, and we are dedicated to developing and delivering electrophysiology products to provide patients, hospitals, and physicians with novel technologies and solutions to improve the lives of patients with cardiac arrhythmias. We aim to establish VIVO as an integral tool used by cardiac electrophysiologists during ablation treatment of ventricular arrhythmias by reducing procedure time and patient complications and increasing procedural success.

Customers

Our primary customers are hospitals providing cardiac electrophysiology lab procedures. We believe there are 2,000 to 3,000 EP labs in the U.S. and a similar number of labs outside of the U.S. performing approximately 600,000 ablation procedures annually. During fiscal 2023, we had two individual customers that represented approximately 32% and 20% of our total revenues, respectively, and four customers (including the two just described) that in the aggregate represented approximately 72% of our total revenues.

Sales and Marketing

Today, we use a mix of distribution partners (Europe), independent sales agents (U.S.) specializing in EP products, and direct employees providing clinical support and product specialization. In the U.S., the VIVO System and patches are currently sold by direct employees and independent sales agents who call on electrophysiologists, lab staff and hospital administrators. This sales team qualifies appropriate prospective customers, and with support from our direct clinical specialists they conduct product demonstrations, and support customer training and case usage. In Europe, our products are sold through distributors, supported by three full time contracted employees.

In addition, in both the U.S. and Europe, we have entered into a co-marketing agreement with Stereotaxis, or STX. The goal is to leverage the compatibility of VIVO with their robotic system. STX customers are the same customers for VIVO, and VIVO provides their customers with an added tool to reduce procedure time. Pursuant to the agreement, STX can perform promotional activity at any hospital globally that has a Stereotaxis Robotic Magnetic Navigation System, referred to herein as a robotic hospital, and where VIVO has appropriate regulatory clearances. In addition, STX will act as a spot distributor for us at mutually agreed upon hospitals where the VIVO System is included as a line item within an STX quote. In exchange for its marketing, distribution and support activity, Stereotaxis receives a payment equal to 45% of the revenue generated from VIVO at robotic hospitals. After the initial sale of VIVO products to customers by Stereotaxis, we will be responsible for selling additional VIVO-related products to the customers but will continue to owe the 45% payment to Stereotaxis with respect to any such sales. The agreement has a term that runs through December 31, 2025, provided however, that the agreement will automatically extend for successive two-year terms unless either party provides the other written notice of termination at least one year prior to the next-scheduled termination date. Stereotaxis will continue to be entitled to receive the 45% payments described above for a period of six months following termination of the agreement.

We continue to hire additional clinical support and direct sales representation as we continue the full VIVO product launch that began in 2023. They are experienced in the electrophysiology field and will identify and target prospective customers to educate, and demonstrate our products, leading to adoption and purchase of our technology. We will continue to use direct clinical specialists to provide training and ongoing clinical support.

In the future, we intend to market our products in the U.S. and certain international markets using a combination of a direct sales force and independent distributors. This may require us to make a significant investment building our U.S. commercial infrastructure and sales force and in recruiting and training our sales representatives and clinical specialists for U.S. commercialization of VIVO. This is a lengthy process that requires recruiting appropriate sales representatives, establishing a commercial infrastructure in the United States, and training our sales representatives, and will require significant ongoing investment by us. Following initial training, our sales representatives typically require lead time in the field to grow their network of accounts, coordinate their sales efforts with each hospital’s capital budgeting and acquisition cycle and produce sales results. Successfully recruiting and training a sufficient number of productive sales representatives is required to achieve growth at the rate we desire.

| 11 |

| Table of Contents |

Marketing and market development activities will target increasing our product usage and expanding the applications of VIVO into the physician clinic and not just hospitals by employing a reimbursement specialist to provide reimbursement for VIVO in different settings.

Outside the U.S., we will continue to foster additional key partner relationships with distributors who will market, sell and support its products.

In addition, we believe there are opportunities to offer additional complementary products through our sales and marketing channels that would enhance the productivity of our sales force and provide additional scale to revenue, better covering fixed operating costs.

Manufacturing and Availability of Raw Materials

VIVO manufacturing, inventory and product fulfillment is housed in our approximate 2,000 square feet facility in Fort Mill, South Carolina. This facility currently has one full-time employee who oversees manufacturing, quality objectives, and order fulfillment. The VIVO system includes VIVO software, loaded onto an off-the-shelf laptop, which we equip with a 3D camera. We purchase laptops and cameras that have been manufactured by third parties. Disposable VIVO Positioning Patches are also required for use of the system, and the manufacture of the patches is outsourced. We also outsource updating and troubleshooting of the software, as needed, to a third party software engineering company from time to time. LockeT manufacturing, inventory and product fulfillment has been subcontracted to the company who is also providing research and development of the product.

Competition

The medical device industry is highly competitive, subject to rapid change and significantly affected by new product introductions and other activities of industry participants. We face potential competition from major medical device companies worldwide, many of which have longer, more established operating histories, and significantly greater financial, technical, marketing, sales, distribution, and other resources. Our overall competitive position is dependent upon a number of factors, including product performance and reliability, manufacturing cost, and customer support. Our primary competitors in the cardiac electrophysiology space include known medical devices such as pacemakers, electrocardiogram, or ECG, systems and cardiac catheters, but also laboratory equipment such as intracardiac mapping systems and fluoroscopy systems (similar to x-ray in real time). The EP market includes large medical device companies such as Medtronic, Plc., Abbott Laboratories, Biosense-Webster (J&J) and Boston Scientific Corp. LockeT’s direct competitors include Abbott’s Perclose device, Haemonetic’s VASCADE device and Inari Medical’s FlowStasis device.

Reimbursement

At this time, there is no reimbursement for VIVO. Ablation procedures are reimbursed using one current procedural technology, or CPT, code, which varies depending on the type and complexity of the procedure. The range of reimbursement for ablations varies within regions but can be as much as $20,000 or more.

We currently intend, in the future, to hire a reimbursement specialist to guide us through the process of obtaining a CPT code specifically for VIVO. Although a new Category III CPT codes is approved and available starting July 1, 2024, Category III codes, which are temporary, do not have a payment rate established, and payment is at the discretion of payors; further, payors generally require a high level of clinical data through long-term patient studies to demonstrate that a treatment produces favorable results in a cost-effective manner relative to other treatments, in order to be willing to provide reimbursement based on Category III codes. Successful execution of our current commercialization and build out for VIVO will be needed in order to move Category III codes to permanent Category I codes.

Research and Development

The major focus of our research and development team is to leverage our existing technology platform for new applications and improvements to our existing applications, including multiple engineering efforts to improve our current products. Future research and development efforts will involve continued enhancements to and cost reductions for VIVO and LockeT. We will also explore the development of other products that can be derived from our core technology platform and intellectual property. Our research and development team works together with our commercial team to set development priorities based on communicated customer needs. The feedback received from our customers is reviewed and evaluated for incorporation into new products.

| 12 |

| Table of Contents |

In the future we intend to develop a generation 3 of VIVO. This version would have expanded indications to include ischemic heart disease and improve usability by the hospital staff. It would also contain more automaticity, potentially reducing our need for clinical support.

Resources Material to Our Business

Patents and Proprietary Technology

Patents

We have a number of patents covering our intellectual property, both in the U.S., as well in a number of international countries. We consider the U.S. to be the most important market for our products, and hence, the most important country for the filing of patents. Any foreign filings are merely replicates of the U.S. filings. For the U.S., we have the following patent positions for the different product areas:

| · | VIVO – We have two U.S. patents granted on the original VIVO concept, which have been licensed from a third party. We consider the primary component to be the ideas around utilizing a 3D camera to identify the exact location of the body surface electrodes. These two patents expire in 2038. An additional two applications have been granted, which disclosed ideas around merging of the heart models to other heart images and expire in 2038 and 2040. An additional three applications were published, all filed in 2021, covering the idea of determining the thickness of the wall of the ventricle, covering the concept of the rendering of a heart model and likely outcomes of an EP procedure. An additional application was filed in September 2023 and is not yet published. |

|

|

|

| · | LockeT – Suture Retention Device - We have four published U.S. patent applications. These cover the basic concept, methods of use and the design of the conceived device. |

|

|

|

| · | AMIGO – We have twenty issued U.S. patents. The first patent, filed in 2006 and expiring in 2031, covers the basic idea, with a three way motor, a remote control, a sled device, and a docking station for a catheter. The more detailed ideas behind the original concept were covered in three patents filed between 2011 and 2013 and expiring in 2026. Additional concepts and methods were filed with six patents between 2010 and 2013, with expirations between 2029 and 2031. We consider the most relevant of the intellectual property to be the guiding track with opposing flexible guides to hold the catheter stable as it is advanced, the form and function of the controller handle, and the introducer interface of the arm to the introducer. An additional ten patents, filed between 2013 and 2017, and expiring in 2034 to 2037, are patents covering ideas not used in the original commercial device, but potential ideas for future embodiments. |

License and Other Agreements

PEACS, NV Software and Technology License Agreement

On May 1, 2016, we entered into a certain Software and Technology License Agreement with PEACS, NV, a Netherlands company, or the License Agreement, for the exclusive worldwide license of the underlying technology to its VIVO product, including intellectual property rights and patent applications pertaining thereto. The license was for use of the technology for the field of use defined as “the localization of the origin of cardiac activation for the electrophysiology treatment and/or detection of cardiac arrhythmias.” The License Agreement called for us to pay for the prosecution and maintenance of patents to protect the technology.

In May 2021, the License Agreement was modified to modify the field of use to specifically exclude the use of clinical applications for the implanting of atrial or ventricular pacemakers, including bi-ventricular pacemakers.

| 13 |

| Table of Contents |

LockeT Royalty Agreement

In February 2022, we agreed to an assignment and royalty agreement, or the Royalty Agreement, for the LockeT device. Pursuant to the Royalty Agreement, we agreed to pay a royalty fee of 5% on net sales up to $1 million. Thereafter, if a patent for the LockeT device is obtained from the U.S. Patent and Trademark Office, we will pay a royalty fee of 2% of net sales up to a total of $10 million in royalties. In addition, at the time of the Merger, additional royalty rights with respect to LockeT device were granted to certain holders, or the Noteholders, of Old Catheter’s outstanding convertible promissory notes in exchange for forgiveness of the interest that had accrued under those notes but remained unpaid, pursuant to the terms of certain Debt Settlement Agreements. The Debt Settlement Agreements provided for the Noteholders to receive, in the aggregate, approximately 12% of the net sales, if any, of the LockeT device, commencing upon the first commercial sale through December 31, 2035.

Trademarks

We own or have rights to trademarks that we use in connection with the operation of our business. We own or have rights to trademarks for Ra Medical Systems and Catheter Precision and their logos, as well as other trademarks such as AMIGO. In February 2024 we filed a trademark for LockeT.

Trade Secrets

We also have relied upon trade secrets, know-how and technological innovation, and may in the future rely upon licensing opportunities, to develop and maintain its competitive position. We have protected our proprietary rights through a variety of methods, including confidentiality agreements and proprietary information agreements with suppliers, employees, consultants and others who may have access to proprietary information.

Government Regulations

Governmental authorities in the U.S. (at the federal, state, and local levels) and abroad extensively regulate, among other things, the research and development, testing, manufacture, quality control, clinical research, approval, labeling, packaging, storage, record-keeping, promotion, advertising, distribution, post-approval monitoring and reporting, marketing, and export and import of products such as those we market and are developing. See Item 1.A. Risk Factors—Risks Related to Government Regulation.

United States Medical Device Regulation

In the U.S., medical devices are subject to extensive regulation by the Food and Drug Administration (“FDA”), pursuant to the Food, Drug and Cosmetic Act, or FDCA, and its implementing regulations, and certain other federal and state statutes and regulations. The laws and regulations govern, among other things, the design, manufacture, storage, recordkeeping, approval, labeling, promotion, post-approval monitoring and reporting, distribution and import and export of medical devices. Failure to comply with applicable requirements may subject a device and/or its manufacturer to a variety of administrative sanctions, such as FDA refusal to approve pending pre-market approval (“PMA”), applications or premarket notification submissions (commonly referred to as “510(k)s),” issuance of warning letters or untitled letters, product recalls, import detentions, civil monetary penalties, and/or judicial sanctions, such as product seizures, injunctions, and criminal prosecution.

The FDCA classifies medical devices into one of three categories based on the risks associated with the device and the level of control necessary to provide reasonable assurance of safety and effectiveness. Class I devices are deemed to be low risk and are subject to the fewest regulatory controls. Class II devices provide intermediate levels of risk. They are subject to general controls and must also comply with special controls. Class III devices are generally the highest risk devices and are subject to the highest level of regulatory control to provide reasonable assurance of the device’s safety and effectiveness. Class III devices must typically be approved by the FDA before they are marketed. LockeT is a sterile, Class I product and was registered with the FDA in February of 2023. It does not require FDA marketing authorization. VIVO is an FDA-cleared Class II product.

Establishments that manufacture devices are required to register their establishments with the FDA and provide the FDA a list of the devices that they handle at their facilities.

| 14 |

| Table of Contents |

The FDA conducts market surveillance and periodic visits, both announced and unannounced, to inspect or re-inspect equipment, facilities, laboratories and processes to confirm regulatory compliance. These inspections may include the manufacturing facilities of subcontractors. Following an inspection, the FDA may issue a report, known as a Form 483, listing instances where the manufacturer has failed to comply with applicable regulations and/or procedures or, if observed violations are severe and urgent, a warning letter. If the manufacturer does not adequately respond to a Form 483 or warning letter, the FDA (with assistance from the Justice Department in certain cases) make take enforcement action against the manufacturer or impose other sanctions or consequences, which may include:

| · | injunctions or consent decrees; |

|

|

|

| · | civil monetary penalties; |

|

|

|

| · | recall, detention or seizure of our products; |

|

|

|

| · | operating restrictions, partial or total shutdown of production facilities; |

|

|

|

| · | refusal of or delay in granting requests for 510(k) clearance, de novo classification, or premarket approval of new products or modified products; |

|

|

|

| · | withdrawing 510(k) clearances, de novo classifications, or premarket approvals that are already granted; |

|

|

|

| · | refusal to grant export approval or export certificates or devices; and |

|

|

|

| · | criminal prosecution. |

Pre-Market Authorization and Notification

While most Class I and some Class II devices can be marketed without prior FDA authorization, most medical devices can be legally sold within the U.S. only if the FDA has: (i) approved a PMA application prior to marketing, generally applicable to most Class III devices; (ii) cleared the device in response to a premarket notification, or 510(k) submission, generally applicable to Class I and II devices; or (iii) authorized the device to be marketed through the de novo process, generally applicable for novel Class I or II devices. Some devices that have been classified as Class III are regulated pursuant to the 510(k) requirements because the FDA has not yet called for PMAs for these devices.

510(k) Notification

Product marketing in the U.S. for most Class II and limited Class I devices typically follows a 510(k) pathway. To obtain 510(k) clearance, a manufacturer must submit a premarket notification demonstrating that the proposed device is substantially equivalent to a legally marketed device, referred to as the predicate device. A predicate device may be a previously 510(k) cleared device or a device that was in commercial distribution before May 28, 1976 for which the FDA has not yet called for submission of PMA applications, or a product previously granted de novo authorization. The manufacturer must show that the proposed device has the same intended use as the predicate device, and it either has the same technological characteristics, or it is shown to be equally safe and effective and does not raise different questions of safety and effectiveness as compared to the predicate device.

There are three types of 510(k)s: traditional; special, for certain device modifications; and abbreviated, for devices that conform to a recognized standard. The special and abbreviated 510(k)s are intended to streamline review. The FDA intends to process special 510(k)s within 30 days of receipt and abbreviated 510(k)s within 90 days of receipt. Though the FDA has a goal to clear a traditional 510(k) within 90 days of receipt, the clearance pathway for traditional 510(k)s can take substantially longer.

After a device receives 510(k) clearance, any modification that could significantly affect its safety or effectiveness, or that would constitute a major change in its intended use, requires a new 510(k) clearance or could require a PMA. The FDA requires each manufacturer to make this determination in the first instance, but the FDA can review any such decision. If the FDA disagrees with a manufacturer’s decision not to seek a new 510(k) clearance for the modified device, the agency may retroactively require the manufacturer to seek 510(k) clearance or PMA. The FDA also can require the manufacturer to cease marketing and/or recall the modified device until 510(k) clearance or PMA is obtained.

| 15 |

| Table of Contents |

VIVO was cleared by the FDA via a traditional 510(k) with supporting clinical data. This data was collected via a clinical study enrolling 51 subjects and took approximately 12 months to gather. In order to expand the indications for use of the current VIVO product with the FDA to include ischemic hearts, data collection via the Coventry study to support a new 510(k) submission will be required. It is expected that future generations of VIVO will require similar data collection and 510(k) submission to receive separate FDA clearance.

Because the LockeT device is a Class I product, it did not require clinical data or a formal submission process. After completing validation testing and compiling a Device History File, LockeT was added to our listing of registered devices. The regulatory pathway for future LockeT devices will depend on the intended use and desired labeling claims and the requirements for clinical data.

De Novo Classification

Devices of a new type that the FDA has not previously classified based on risk are automatically classified into Class III by operation of section 513(f) (1) of the FDCA, regardless of the level of risk they pose. To avoid requiring PMA review of low- to moderate-risk devices classified in Class III by operation of law, Congress enacted section 513(f)(2) of the FDCA. This provision allows the FDA to classify a low- to moderate-risk device not previously classified into Class I or II through the de novo classification pathway. The FDA evaluates the safety and effectiveness of devices submitted for review under the de novo classification pathway and devices determined to be Class II through this pathway can serve as predicate devices for future 510(k) applicants. The de novo classification pathway can require clinical data and is generally more burdensome than the 510(k) pathway and less burdensome than the PMA pathway.

Pre-Market Approval

A product not eligible for 510(k) clearance or de novo classification must follow the PMA pathway, which requires proof of the safety and effectiveness of the device to the FDA’s satisfaction.

Results from adequate and well-controlled clinical trials are required to establish the safety and effectiveness of a Class III PMA device for each indication for which FDA approval is sought. After completion of the required clinical testing, a PMA including the results of all preclinical, clinical, and other testing, and information relating to the product’s marketing history, design, labeling, manufacture, and controls, is prepared and submitted to the FDA.

The PMA process is generally more expensive, rigorous, lengthy, and uncertain than the 510(k) premarket notification process and de novo classification process and requires proof of the safety and effectiveness of the device to the FDA’s satisfaction. As part of the PMA review, the FDA will typically inspect the manufacturer’s facilities for compliance with Quality System Regulations, or QSR, requirements, which impose elaborate testing, control, documentation and other quality assurance procedures. The FDA’s review of a PMA application typically takes one to three years but may last longer. The FDA will often convene an independent advisory panel to review the submission. If the FDA’s evaluation of the PMA application is favorable, the FDA will issue a PMA for the approved indications, which can be more limited than those originally sought by the manufacturer. The PMA can include post-approval conditions that the FDA believes necessary to ensure the safety and effectiveness of the device including, among other things, restrictions on labeling, promotion, sale and distribution. Failure to comply with the conditions of approval can result in material adverse enforcement action, including the loss or withdrawal of the approval and/or placement of restrictions on the sale of the device until the conditions are satisfied.

Even after approval of a PMA, a new PMA or PMA supplement may be required in the event of a modification to the device, its labeling or its manufacturing process. Supplements to a PMA often require the submission of the same type of information required for an original PMA, except that the supplement is generally limited to that information needed to support the proposed change from the product covered by the original PMA.

Clinical Trials

A clinical trial is almost always required to support a PMA application and de novo classification and is sometimes required for a premarket notification. For significant risk devices, the FDA regulations require that human clinical investigations conducted in the U.S. be approved under an Investigational Device Exemption (“IDE”), which must become effective before clinical testing may commence. A nonsignificant risk device does not require FDA approval of an IDE. In some cases, one or more smaller IDE studies may precede a pivotal clinical trial intended to demonstrate the safety and efficacy of the investigational device. A 30-day waiting period after the submission of each IDE is required prior to the commencement of clinical testing in humans. If the FDA disapproves the IDE within this 30-day period, the clinical trial proposed in the IDE may not begin. In addition, even if the 30-day waiting period expires without objection by the FDA, the FDA can impose a clinical hold if safety issues arise.

| 16 |

| Table of Contents |

An IDE application must be supported by appropriate data, such as animal and laboratory test results, showing that it is safe to test the device in humans and that the testing protocol is scientifically sound. The IDE application must also include a description of product manufacturing and controls, and a proposed clinical trial protocol. The FDA typically grants IDE approval for a specified number of patients to be treated at specified study centers. During the study, the sponsor must comply with the FDA’s IDE requirements for investigator selection, trial monitoring, reporting, and record keeping. The investigators must obtain patient informed consent, follow the investigational plan and study protocol, control the disposition of investigational devices, and comply with reporting and record keeping requirements. Prior to granting PMA, the FDA typically inspects the records relating to the conduct of the study and the clinical data supporting the PMA application for compliance with IDE requirements.

Clinical trials must be conducted: (i) in compliance with federal regulations; (ii) in compliance with good clinical practice, or GCP, an international standard intended to protect the rights and health of patients and to define the roles of clinical trial sponsors, investigators, and monitors; and (iii) under protocols detailing the objectives of the trial, the parameters to be used in monitoring safety, and the effectiveness criteria to be evaluated. Pivotal clinical trials supporting premarket applications for devices are typically conducted at geographically diverse clinical trial sites and are designed to permit the FDA to evaluate the overall benefit-risk relationship of the device and to provide adequate information for the labeling of the device when considering whether a device satisfies the statutory standard for commercialization. Clinical trials, for significant and nonsignificant risk devices, must be approved by an institutional review board, or IRB—an appropriately constituted group that has been formally designated to review and monitor biomedical research involving human subjects and which has the authority to approve, require modifications in, or disapprove research to protect the rights, safety, and welfare of the human research subject.

The FDA may order the temporary, or permanent, discontinuation of a clinical trial at any time, or impose other sanctions, if it believes that the clinical trial either is not being conducted in accordance with the FDA requirements or presents an unacceptable risk to the clinical trial patients. An IRB may also require the clinical trial it has approved to be halted, either temporarily or permanently, for failure to comply with the IRB’s requirements, or may impose other conditions or sanctions.

Although the QSR does not fully apply to investigational devices, the requirement for controls on design and development does apply. The sponsor also must manufacture the investigational device in conformity with the quality controls described in the IDE application and any conditions of IDE approval that the FDA may impose with respect to manufacturing. Investigational devices may only be distributed for use in an investigation and must bear a label with the statement: “CAUTION-Investigational device. Limited by Federal law to investigational use.”

Post-Market Requirements

After a device is placed on the market, numerous regulatory requirements apply. These include: the QSR requirements, labeling regulations, the medical device reporting regulations (which require that manufacturers report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if it were to recur), and reports of corrections and removals regulations (which require manufacturers to report recalls or removals and field corrections to the FDA if initiated to reduce a risk to health posed by the device or to remedy a violation of the FDCA). Failure to properly identify reportable events or to file timely reports, as well as failure to address observations to FDA’s satisfaction, can subject us to warning letters, recalls, or other sanctions and penalties.

Advertising, marketing and promotional activities for devices are also subject to FDA oversight and must comply with the statutory standards of the FDCA, and the FDA’s implementing regulations. The FDA’s oversight authority review of marketing and promotional activities encompasses, but is not limited to, direct-to-consumer advertising, healthcare provider-directed advertising and promotion, sales representative communications to healthcare professionals, promotional programming and promotional activities involving electronic media. The FDA also regulates industry-sponsored scientific and educational activities that make representations regarding product safety or efficacy in a promotional context.

| 17 |

| Table of Contents |

Manufacturers of medical devices are permitted to promote products solely for the uses and indications set forth in the approved or cleared product labeling. A number of enforcement actions have been taken against manufacturers that promote products for “off-label” uses (i.e., uses that are not described in the approved or cleared labeling), including actions alleging that claims submitted to government healthcare programs for reimbursement of products that were promoted for “off-label” uses are fraudulent in violation of the Federal False Claims Act or other federal and state statutes and that the submission of those claims was caused by off-label promotion. The failure to comply with prohibitions on “off-label” promotion can result in significant monetary penalties, revocation or suspension of a company’s business license, suspension of sales of certain products, product recalls, civil or criminal sanctions, exclusion from participating in federal healthcare programs, or other enforcement actions. In the United States, allegations of such wrongful conduct could also result in a corporate integrity agreement with the U.S. government that imposes significant administrative obligations and costs, as has occurred in the past with respect to our legacy products that we no longer market.

The Federal Trade Commission, or FTC, also oversees the advertising and promotion of our products (other than labeling) pursuant to its broad authority to police deceptive advertising for goods or services within the U.S. The FDA and FTC work together to regulate different aspects of activities by medical product manufacturers, consistent with the inter-agency Memorandum of Understanding. Under the Federal Trade Commission Act, or FTCA, the FTC is empowered, among other things, to (a) prevent unfair methods of competition and unfair or deceptive acts or practices in or affecting commerce; (b) seek monetary redress and other relief for conduct injurious to consumers; and (c) gather and compile information and conduct investigations relating to the organization, business, practices, and management of entities engaged in commerce. In the context of performance claims for products such as our devices and services, compliance with the FTC Act includes ensuring that there is scientific data to substantiate the claims being made, that the advertising is neither false nor misleading, and that any user testimonials or endorsements we or our agents disseminate related to the devices or services comply with disclosure and other regulatory requirements.

Violations of the FDCA or FTCA relating to the inappropriate promotion of approved products may lead to investigations alleging violations of federal and state healthcare fraud and abuse and other laws, including state consumer protection laws.

For a PMA or Class II 510(k) or de novo devices, the FDA also may require post-marketing testing, surveillance, or other measures to monitor the effects of an approved or cleared product. The FDA may place conditions on a PMA-approved device that could restrict the distribution or use of the product. In addition, quality-control, manufacture, packaging, and labeling procedures must continue to conform to QSRs and other applicable regulatory requirements after approval and clearance, and manufacturers are subject to periodic inspections by the FDA. Accordingly, manufacturers must continue to expend time, money, and effort in the areas of production and quality-control to maintain compliance with QSRs. If the FDA believes we or any of our contract manufacturers or regulated suppliers are not in compliance with these requirements and patients are being subjected to serious risks, the agency can shut down our manufacturing operations, require recalls of our medical device products, refuse to approve new marketing applications, initiate legal proceedings to detain or seize products, enjoin future violations, or assess civil and criminal penalties against us or our officers or other employees.

European Economic Area (EEA) Regulation

The EEA recognizes a single medical device approval (the CE Mark) which allows for distribution of an approved product throughout the EEA without additional general applications in each country. Individual EEA members, however, reserve the right to require additional labeling or information to address particular patient safety issues prior to allowing marketing. Third parties called “Notified Bodies” award the CE Mark. These Notified Bodies are approved and subject to review by the “Competent Authorities” of their respective countries. Our Notified Bodies perform periodic on-site inspections to independently review our compliance with systems and regulatory requirements. A number of countries outside of the EEA accept the CE Mark in lieu of marketing submissions as an addendum to that country’s application process. We have a CE Mark for the VIVO System. Beginning July 1, 2023, the United Kingdom requires its own medical device approval (UKCA). VIVO is currently registered with UK’s Medicines and Healthcare products Regulatory Agency to market the VIVO system in the UK. Since July 1, 2023, VIVO bears the UKCA symbol as required by the UK Medical Devices Regulations 2002 (SI 2002 No 618, as amended) (“MDR”) to continue UK distributions. MDR requirements now include on-going collection of clinical data to include in annual reports to ensure state of the art technology and safety requirements are met. We are currently collecting data via a multi-center (and country) European Registry. This registry concluded enrollment in June 2023 and is anticipated to complete data collection and study activities in September 2024.

| 18 |

| Table of Contents |

LockeT is currently undergoing MDR review and approval via the Notified Body. CE Mark is anticipated in August 2024.

Other Healthcare Laws

Our business operations and current and future arrangements with healthcare professionals, consultants, customers and patients, expose us to broadly applicable state, federal, and foreign fraud and abuse and other healthcare laws and regulations. These laws constrain the business and financial arrangements and relationships through which we conduct our operations, including how we research, market, sell and distribute our products. Such laws include, but are not limited to:

| · | the U.S. federal Anti-Kickback Statute, which prohibits, among other things, persons and entities from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in cash or in kind, to induce or reward, or in return for, either the referral of an individual for, or the purchase, order or recommendation of, any good or service, for which payment may be made under a U.S. healthcare program such as Medicare and Medicaid. A person or entity does not need to have actual knowledge of the U.S. federal Anti-Kickback Statute or specific intent to violate it in order to have committed a violation. In addition, the government may assert that a claim including items or services resulting from a violation of the U.S. federal Anti-Kickback Statute constitutes a false or fraudulent claim for purposes of the federal civil False Claims Act; |

|

|

|

| · | U.S. federal civil and criminal false claims laws and civil monetary penalties laws, including the federal civil False Claims Act, which, among other things, impose criminal and civil penalties, including through civil whistleblower or qui tam actions, against individuals or entities for knowingly presenting, or causing to be presented, to the U.S. government, claims for payment or approval that are false or fraudulent, knowingly making, using or causing to be made or used, a false record or statement material to a false or fraudulent claim, or from knowingly making a false statement to avoid, decrease or conceal an obligation to pay money to the U.S. government. Persons and entities can be held liable under these laws if they are deemed to “cause” the submission of false or fraudulent claims by, for example, providing inaccurate billing or coding information to customers or promoting a product off-label; |

|

|

|

| · | the U.S. Health Insurance Portability and Accountability Act of 1996, or HIPAA, which imposes criminal and civil liability for, among other things, knowingly and willfully executing, or attempting to execute, a scheme to defraud any healthcare benefit program, or knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false statement, in connection with the delivery of, or payment for, healthcare benefits, items or services. Similar to the U.S. federal Anti-Kickback Statute, a person or entity does not need to have actual knowledge of the health care fraud statute implemented under HIPAA or specific intent to violate it in order to have committed a violation; |

|

|

|

| · | in addition, HIPAA, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009, or HITECH Act, and its implementing regulations, imposes obligations, including mandatory contractual terms, with respect to safeguarding the privacy, security and transmission of individually identifiable health information without appropriate authorization by covered entities subject to the rule, such as health plans, healthcare clearinghouses and certain healthcare providers as well as their business associates that perform certain services for or on their behalf involving the use or disclosure of individually identifiable health information; |

|

|

|

| · | the U.S. Physician Payments Sunshine Act, which requires applicable manufacturers of drugs, devices, biologics and medical supplies for which payment is available under Medicare, Medicaid or the Children’s Health Insurance Program (with certain exceptions) to report annually to the government information related to payments or other “transfers of value” made to physicians (defined to include doctors, dentists, optometrists, podiatrists and chiropractors), non-physician healthcare professionals (defined to include physician assistants, nurse practitioners, clinical nurse specialists, certified registered nurse anesthetists and anesthesiologist assistants, and certified nurse-midwives) and teaching hospitals, as well as information regarding ownership and investment interests held by the physicians described above and their immediate family members; and |

|

|

|

| · | analogous state and non-U.S. laws and regulations, such as state anti-kickback and false claims laws, which may apply to our business practices, including, but not limited to, research, distribution, sales and marketing arrangements and claims involving healthcare items or services reimbursed by non-governmental third-party payors, including private insurers, or by the patients themselves; state laws that require pharmaceutical and device companies to comply with the industry’s voluntary compliance guidelines and the relevant compliance guidance promulgated by the U.S. government, or otherwise report or restrict payments that may be made to healthcare providers and other potential referral sources; state laws and regulations that require manufacturers to report information related to payments and other transfers of value to physicians and other healthcare providers or marketing expenditures and pricing information; and state and non-U.S. laws governing the privacy and security of health information in some circumstances, many of which differ from each other in significant ways and often are not preempted by HIPAA, thus complicating compliance efforts. |

| 19 |

| Table of Contents |

In particular, activities and arrangements in the healthcare industry are subject to extensive laws and regulations intended to prevent fraud, waste and other abusive practices. These laws and regulations may restrict or prohibit a wide range of activities or other arrangements related to the development, marketing or promotion of products, including pricing and discounting of products, provision of customer incentives, provision of reimbursement support, other customer support services, provision of sales commissions or other incentives to employees and independent contractors and other interactions with healthcare practitioners, other healthcare providers and patients.

Because of the breadth of these laws and the narrow scope of the statutory or regulatory exceptions and safe harbors available, our business activities could be challenged under one or more of these laws. Relationships between medical product manufacturers and health care providers are an area of heightened scrutiny by the government.

Government expectations and industry best practices for compliance continue to evolve and past activities may not always be consistent with current industry best practices. Further, there is a lack of government guidance as to whether various industry practices comply with these laws, and government interpretations of these laws continue to evolve, all of which creates compliance uncertainties. Any non-compliance could result in regulatory sanctions, criminal or civil liability and serious harm to our reputation. It is not always possible to identify and deter misconduct, and the precautions we take to detect and prevent this activity may not be effective in preventing such conduct, mitigating risks, or reducing the chance of governmental investigations or other actions or lawsuits stemming from a failure to comply with these laws or regulations.

If a government entity opens an investigation into possible violations of any of these laws (which may include the issuance of subpoenas), we would have to expend significant resources to defend ourselves against the allegations. Defending against any such actions can be costly, time-consuming and may require significant financial and personnel resources. Therefore, even if we are successful in defending against any such actions that may be brought against us, our business may be impaired. If any of the above occur, it could adversely affect our ability to operate our business and our results of operations.