NEXA RESOURCES S.A. (“NEXA”) RESULTS FOR THE THREE-MONTH ENDED MARCH 31, 2018

THIS EARNINGS RELEASE DATED AS OF APRIL 30, 2018 SHOULD BE READ IN CONJUNCTION WITH THE UNAUDITED CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS OF NEXA AND THE NOTES THERETO AS AT AND FOR THE THREE-MONTH PERIOD ENDED MARCH 31, 2018. THIS DOCUMENT CONTAINS FORWARD-LOOKING STATEMENTS. PLEASE REFER TO THE CAUTIONARY LANGUAGE UNDER THE HEADING “CAUTIONARY STATEMENT ON FORWARD-LOOKING STATEMENTS”.

|

Conference Call |

Investor Relations Team |

|

Wednesday, May 2, 2018 — 10am (ET) |

Leandro Cappa (Head of IR): leandro.cappa@nexaresources.com |

|

USA: +1-866-807-9684 |

Diogo Rocha: diogo.rocha@nexaresources.com |

|

Canada: +1-866-450-4696 |

Henry Aragon: henry.aragon@nexaresources.com |

|

Brazil: 0800-8910015 |

Luiz Perez: luiz.perez@nexaresources.com |

|

International: +1-412-317-5415 |

Cristiene Costa: cristiene.costa@nexaresources.com |

|

Documents: www.nexaresources.com/investors |

ir@nexaresources.com |

Contact: ir@nexaresources.com

|

Index |

|

|

About Nexa |

4 |

|

Outlook Nexa 1Q18 |

8 |

|

Market Overview |

11 |

|

Business Performance |

15 |

|

CAPEX |

28 |

|

Financial Results |

31 |

|

Result by Segment |

34 |

|

Liquidity, Indebtedness and Rating |

36 |

|

Capital Resources |

38 |

|

Related Party Transactions |

39 |

|

Financial Instruments and Derivatives |

39 |

|

Risk Management |

40 |

|

Critical Accounting Policies and Estimates |

41 |

|

Use of Non-IFRS Financial Measures |

43 |

|

CAUTIONARY STATEMENT ON FORWARD-LOOKING STATEMENTS |

43 |

|

Appendix |

45 |

About Nexa

Nexa Resources is a large-scale, low-cost integrated zinc producer with over 60 years of experience developing and operating mining and smelting assets in Latin America. The Company owns and operates five long-life underground polymetallic mines, three located in the Central Andes of Peru (Cerro Lindo, El Porvenir and Atacocha) and two located in the state of Minas Gerais in Brazil (Vazante and Morro Agudo). Two of the Company’s mines, Cerro Lindo and Vazante, are among the 10 largest zinc mines in the world, and combined with the Company’s other mining operations, place the Company among the top five producers of mined zinc globally in 2017, according to Wood Mackenzie. Nexa also operates three smelting assets, two in Brazil located in the state of Minas Gerais (Juiz de Fora and Três Marias) and one in Peru (Cajamarquilla). Nexa produces substantial amounts of copper, lead, silver and gold as by-products, which reduce our overall cost to produce mined zinc.

Nexa Resources S.A. (NYSE: NEXA, TSX: NEXA) (formerly VM Holding S.A.) (“Nexa Resources”, “Nexa”, or the “Company”) started to trade its common shares on the New York Stock Exchange (“NYSE”) and the Toronto Stock Exchange (“TSX”) under the ticker symbol “NEXA” on October 27, 2017.

Corporate Structure

Highlights

Mining Performance:

· Zinc equivalent(3) metal production in Nexa’s mining operations totaled 134.0kton(4) in 1Q18, slightly lower compared to 135.2kton in the same period of the previous year, representing a 0.9% reduction. The 4.1% increase (123 ktons) in the volume of treated ore, especially in El Porvenir, and the increase in copper and silver grades (3 bp and 2bp respectively) offset part of the reduction in zinc grades.

· The production by metal in 1Q18 totaled 87.2kton of zinc, 10.7kton of copper, 12.3kton of lead, 1,884koz of silver and 7.4koz of gold compared to 92.3kton of zinc, 9.4kton of copper, 11.8kton of lead, 1,706koz of silver and 8.0koz of gold in 1Q17.

· Per mine production on a zinc equivalent basis, during 1Q18, the Peruvian Cerro Lindo mine accounted for 43% of the total production, followed by Vazante, El

(1) Nexa Resources holds a direct 0.17% equity interest in Nexa Peru and an indirect 80.06% equity interest through Nexa Resources Cajamarquilla. A 15.79% equity interest is publicly floated and the remaining 3.97% of equity interest pertains to treasury shares.

(2) Nexa owns 100% of Pollarix ordinary shares and 33.3% of the total capital.

(3) Consolidated mining production in kton of zinc equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton (US$1.31/lb); copper: US$6,166/ton (US$2.80/lb); lead: US$2,317/ton (US$1.05/lb); silver: US$17/oz; and gold: US$1,257/oz. Each ton is equivalent to 2,204.62 pounds.

(4) kton refers to one thousand metric tons.

Porvenir, Atacocha and Morro Agudo mines, accounting for 27%, 18%, 9% and 4%, respectively.

· Cash cost net of by-products credits was US$0.22/lb (or US$483.7/ton), a significant reduction of 42.7% in 1Q18 compared to 1Q17. Higher by-products credits and lower zinc treatment charges were the main drivers of this decrease.

· All-in sustaining cost net of by-products credits (“AISC”(5)) also decreased in 1Q18, amounting to US$0.37/lb (or US$805.4/ton), 27.8% lower than in 1Q17.

Smelting Performance:

· Metallic zinc sales in 1Q18 were 5.1% higher than in 1Q17, totaling 137.3kton supported by higher production in the quarter. Production and sales in the first half of 2017 were impacted by heavy rains and floods in Peru compared to a normalized smelting performance this quarter.

· Cash cost net of by-products credits increased by 30.3%, to US$1.43/lb (or US$3,163.4/ton) in 1Q18 compared to 1Q17, mostly due to higher raw material costs driven by higher zinc prices and lower treatment charges. Our cash cost net of by-products credits is measured in respect to zinc.

· AISC(5) increased by 26.1% in 1Q18, amounting to US$1.51/lb (or US$3,327.3/ton).

Projects and Operations Developments:

· Aripuanã (greenfield)

· In April, 2018, Aripuanã was granted the Preliminary Environmental License which certifies that the project complies with the environmental standard requirements of projects with such characteristics.

· Project currently on FEL3 (feasibility study). As of March 31, 2018 the FEL3 is 58% completed and is expected to be completed in the second half of 2018.

Financial Performance:

· Net revenues of US$676.2 million in 1Q18, 23.1% higher than in 1Q17, supported by higher metal prices and higher sales volumes from our smelters.

· Adjusted EBITDA of US$191.2 million in 1Q18 compared to US$144.1 in 1Q17 a 32.7% increase.

· Adjusted EBITDA margin of 28.3% in 1Q18 compared to 26.2% in 1Q17.

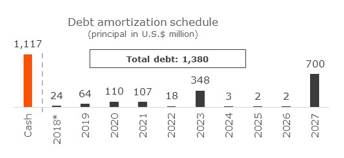

· Net Debt/Adj. EBITDA of 0.37x as of March 31, 2018.

· Average maturity of the total debt(6) of 6.6 years at an average cost of 5.0% as of March 31, 2018, with only 24% of total debt maturing within the next 5 years.

· Cash and cash equivalents added to the financial investments position of US$1.12 billion on March 31, 2018.

(5) Zinc all-in sustaining cost net of by-products credits, in US$/lb. We updated our AISC calculations to include sustaining capital expenditures (“CAPEX”) and also health, safety and environment, tailing dams and other non-expansion related CAPEX. For AISC reconciliation, please see pages 54-57.

(6) Our total debt refers to short and long term loans and financing (principal only).

|

US$ million |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Net Revenues |

|

676.2 |

|

736.7 |

|

549.3 |

|

23.1 |

% |

|

Adjusted EBITDA(1) |

|

191.2 |

|

222.5 |

|

144.1 |

|

32.7 |

% |

|

Adj. EBITDA Margin(1) |

|

28.3 |

% |

30.2 |

% |

26.2 |

% |

210 |

bp |

|

Net Income |

|

62.8 |

|

24.0 |

|

55.2 |

|

13.6 |

% |

|

Avg # of outstanding shares (in ‘000) |

|

133,320 |

|

127,527 |

|

112,821 |

|

18.2 |

% |

|

EPS (in US$) (2) |

|

0.41 |

|

0.10 |

|

0.44 |

|

-5.0 |

% |

|

Net Debt |

|

261.4 |

|

225.0 |

|

144.1 |

|

0.0 |

% |

|

Net Debt / Adj. EBITDA |

|

0.37 |

|

0.34 |

|

0.32 |

|

N/A |

|

|

CAPEX |

|

33.0 |

|

66.9 |

|

30.7 |

|

7.6 |

% |

|

Zn Eq Mining Production (3) |

|

134.0 |

|

154.1 |

|

135.2 |

|

-0.9 |

% |

|

Mining Cash Cost(4) |

|

0.22 |

|

0.16 |

|

0.38 |

|

-42.7 |

% |

|

Mining AISC(5) |

|

0.37 |

|

0.38 |

|

0.51 |

|

-27.8 |

% |

|

Metal Sales(6) |

|

146.4 |

|

155.0 |

|

139.5 |

|

5.0 |

% |

|

Smelting Cash Cost(5) |

|

1.43 |

|

1.34 |

|

1.10 |

|

30.3 |

% |

|

Smelting AISC(5) |

|

1.51 |

|

1.48 |

|

1.20 |

|

26.1 |

% |

(1) See “Use of Non-IFRS Financial Measures” below for further information

(2) Reflects revised EPS data for prior periods. See “Restatement of Earnings Per Share” below for further information.

(3) Consolidated mining production in kton of Zinc Equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: Zinc: US$2,896/ton; Copper: US$6,166/ton; Lead: US$2,317/ton; Silver: US$17/oz; Gold: US$1,257/oz.

(4) Zinc cash cost net of by-products credits, in US$/lb.

(5) Zinc AISC net of by-products credits, in US$/lb. We revised our AISC calculations in order to include not only sustaining CAPEX but also health, safety and environment/tailing dams and other non-expansion related capex.

(6) Consolidated sales of metallic zinc and zinc oxide (in kton of product volume).

Share Premium

The share premium is a capital reserve account of the net equity of a Luxembourg company and can be distributed to the Company’s shareholders. On February 15, 2018, the Board of Directors approved a share premium distribution in cash of approximately US$0.60 per ordinary share to shareholders of the Company of record at the close of business on March 14, 2018 and paid a total aggregate amount of US$80 million on March 28, 2018.

Corporate Highlights

On April 30, 2018 we filed our annual report on Form 20-F for the fiscal year ended December 31, 2017 and published a report with updated information relating to mineral reserves and resources as of December 31, 2017 (“2017 YE MRMR Update”). Such report discloses estimated contained metal in the Proven and Probable Mineral Reserve categories estimated as of December 31, 2017 in accordance with the 2014 CIM (Canadian Institute of Mining. Metallurgy and Petroleum) Definition Standards, whose definitions are incorporated by reference in National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) totaling an aggregate of contained metal in reserves of 3,897.2 thousand tonnes of zinc, 430.8 thousand tonnes of copper, 592.6 thousand tonnes of lead, 3,468,642 kilograms of silver and 2,919 kilograms of gold, representing an increase of 8.7% for zinc, 5.6% for copper, 6.6% for lead, 7.9% for silver and a 5.4% decrease in gold, in comparison to information provided in our previous 2017 publicly available technical reports on SEDAR (www.sedar.com) and on EDGAR

(www.sec.gov).

Earnings Per Share

Earnings per share (“EPS”) in 1Q18 were US$0.41 compared to US$0.44 in 1Q17, a -5.0% decrease. We have identified an error in the calculation of EPS in our earnings reports and financial statements for prior periods. All EPS data in this report for prior periods has been corrected. For additional information, see “Restatement of Earnings Per Share” below.

Outlook 1Q18

We are reiterating our annual guidance for mining production, smelting sales, CAPEX and OPEX related to exploration and project development for the 2018 fiscal year as we reported on February 15, 2018. Below we discuss each guidance and the performance of each indicator in the 1Q18.

Mining Production

The mining production in the 1Q18 reached 134.0 ktons in zinc equivalent terms which is 101% of the volume planned for the quarter despite the fact that Cerro Lindo production lagged behind on the same terms, as it has taken longer than expected for us to reach higher grade areas. The better performance in Vazante and El Porvenir offset this effect.

|

Metal Contained (in |

|

2017 |

|

1Q18 |

|

2018 estimated |

| ||||

|

Zinc (kton) |

|

375.4 |

|

87.2 |

|

370 |

|

— |

|

390 |

|

|

Lead (kton) |

|

52.6 |

|

12.3 |

|

55 |

|

— |

|

60 |

|

|

Copper (kton) |

|

44.2 |

|

10.7 |

|

39 |

|

— |

|

42 |

|

|

Silver (koz) |

|

7,946 |

|

1,884 |

|

7,600 |

|

— |

|

8,000 |

|

|

Gold (koz) |

|

32.5 |

|

7.4 |

|

17 |

|

— |

|

19 |

|

Main assumptions behind the annual guidance are: (i) the increase in total treated ore by more than 6%; (ii) lower grades, especially in the Cerro Lindo mine, in line with expectations; and (iii) planned operational dilution reduction in Vazante.

Metal Sales

Smelting metallic zinc sales totaled 137.3 ktons in the quarter while zinc oxide sales reached 9.1 ktons. During the 1Q18 our smelters ran at capacity while the roasters performance increased as expected and the weather conditions during the start of the rainy season allowed us to operate within our planned schedule and focus our efforts on cost efficiency and enhancing our safety standards.

|

Smelting sales |

|

2017 |

|

1Q18 |

|

2018 estimated |

| ||||

|

Zinc Metal (kton) |

|

555.4 |

|

137.3 |

|

560 |

|

— |

|

580 |

|

|

Zinc Oxide (kton) |

|

38.5 |

|

9.1 |

|

37 |

|

— |

|

39 |

|

|

Total |

|

593.9 |

|

146.4 |

|

597 |

|

— |

|

619 |

|

The main assumptions for the annual smelting sales are: (i) the increase in the performance of the roasters in each of the Company’s smelters; and (ii) regular production through 2018, with weather conditions assumed to be in line with historical average, compared to 2017 which experienced atypical rains and floods in Peru during the first quarter.

Capital expenditures (“CAPEX”)

Total capital expenditures were US$20.0 million below budget for 1Q18, as certain necessary approvals were delayed. We invested US$33.0 million during the quarter.

|

Capex per segment (US$mm) |

|

2017 actual |

|

1Q18 actual |

|

2018 estimated |

|

|

Mining |

|

107.1 |

|

20.0 |

|

172 |

|

|

Smelter |

|

81.0 |

|

10.1 |

|

108 |

|

|

Others |

|

9.5 |

|

2.9 |

|

0 |

|

|

Total |

|

197.6 |

|

33.0 |

|

280 |

|

|

Capex per category (US$mm) |

|

2017 actual |

|

1Q18 actual |

|

2018 estimated |

|

|

Expansion/Greenfield |

|

48.8 |

|

9.6 |

|

90 |

|

|

Modernization |

|

21.4 |

|

1.0 |

|

20 |

|

|

Sustaining |

|

59.4 |

|

9.4 |

|

68 |

|

|

HS&E/Tailing dams |

|

62.1 |

|

11.2 |

|

92 |

|

|

IT/Others |

|

5.9 |

|

1.7 |

|

10 |

|

|

Total |

|

197.6 |

|

33.0 |

|

280 |

|

Main projects for 2018 and related CAPEX for the year are:

· Vazante’s life of mine extension (US$43 million);

· Implementation of dry stack tailings at Vazante (US$22 million);

· FEL 3 and potential commencement of execution of Aripuanã project in Brazil (US$20 million); and

· Process conversion at the Cajamarquilla Smelter from the Goethite process to the Jarosite process (US$20 million) which is expected to increase zinc recovery at the plant.

Expenses related to Project Development and Exploration(1)

In 1Q18, we spent US$13.4 million in mineral exploration on our greenfield, brownfield and open field projects. The project development expenses amounted to US$3.3 million in 1Q18.

As the Company advances with its exploration and drilling campaigns and moves forward on the development of its pipeline of projects, the expenses estimated for 2018 are

expected to increase, thus impacting our margins since early-stage projects are charged to “Other Operating Expenses”.

|

US$ million |

|

2017 actual |

|

1Q18 actual |

|

2018 estimated |

|

|

Mineral exploration |

|

77.7 |

|

13.4 |

|

86.2 |

|

|

Project development |

|

16.6 |

|

3.3 |

|

53.6 |

|

|

Total |

|

94.3 |

|

16.7 |

|

139.8 |

|

(1) Includes explorations, expansion, modernization, R&D, health, safety and environment and others.

(2) Exploration and project development expenses consider several stages of development, from mineral potential definition, R&D, and subsequent scoping and pre-feasibility studies (FEL1 and FEL2).

Market Overview

Zinc

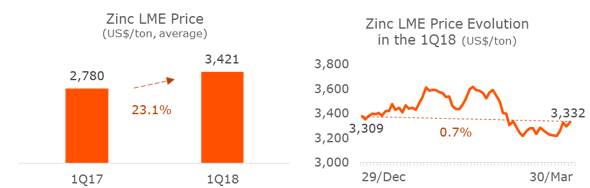

The average LME(1) price for zinc in 1Q18 was US$3,421/ton, 23.1% higher than the average price in the same quarter of 2017. The price at the end of March 2018 was US$3,332/ton, 0.7% higher when compared to US$3,309/ton at the end of 4Q17.

Source: Bloomberg

In the beginning of March, President Trump announced tariffs on U.S. imports of aluminum (+10%), steel (+25%) and Chinese goods (+25%), creating concerns of a trade war. This decision triggered a sell-off in equity markets and served to lend momentum to a sell-off in zinc, which was already underway. Also in the beginning of March, LME stocks reported an additional 77kt of metallic zinc, which specialists believe came from shadow stocks. This also brought LME prices down due to concerns that the amount of metal available through shadow stocks could be higher than previously believed.

Although market analysts forecast an increase in concentrate output in H2 2018, this does not seem enough to replace the reduction of concentrate and metal LME stocks seen in recent years.

On the demand side, perspectives for China in 2018 are strong primarily for the real estate and manufacturing sectors. In the U.S., trade tariffs raise question marks for the American market and how zinc will be affected by this new scenario. The Eurozone, on the other hand, maintains a good pace and GDP growth for 2018 should remain high.

(1) The London Metal Exchange (LME) publishes a set of daily reference prices that are used by industrial and financial participants for referencing, hedging, physical settlement, contract negotiations, margining and portfolio evaluations. As they are based on some of the most liquid trading sessions of the day, we believe LME prices are good indicators of where the market is at any point in time. Source: LME

Copper

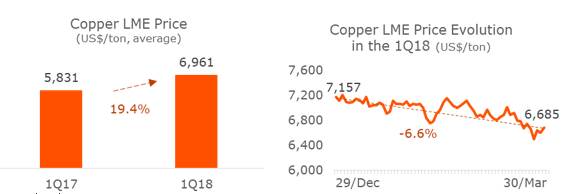

The average LME copper price in 1Q18 was US$6,961/ton, up 19.4% when compared to the same quarter of 2017. The price closed 1Q18 at US$6,685/ton, down 6.6% from US$7,157/ton at the end of 4Q17.

Source: Bloomberg

The risk of strikes due to collective labor negotiations in Chile in 2018, which supported the rally in prices throughout the second half of 2017, appears to be easing with new labor contracts now being agreed. Chilean labor talks are progressing well, so the likelihood of significant tonnage disruption is diminishing, depressing prices further.

During 1Q18 the better-than-expected Chinese macro data lent some support to LME prices. Industrial output recorded a faster-than-expected 7.2% increase in January/February, compared to the same period a year earlier and exceeded estimates of an increase of 6.1%. On the other hand, official Chinese refined copper production rose by 10.3% YoY in the first two months of the year, reflecting fewer copper smelter maintenances so far in 2018.

Another point that had impacted copper prices was President Trump’s announcement of across-the-board tariffs. Although copper is not directly impacted, expectations of another year of solid global economic growth were dented and the prospect of a wider trade war between China and the U.S. has hit investor confidence.

Total LME stocks have risen significantly to 388kt, up by 93% since the start of the year (201kt) and 28% compared with the high of 302kton in 4Q17.

Lead

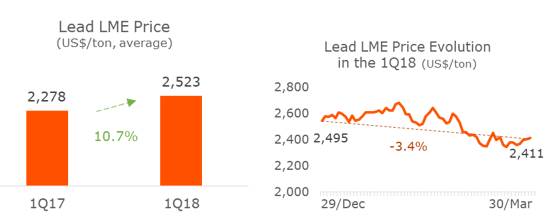

The average LME lead price in 1Q18 was US$2,523/ton, 10.7% higher than the average price in 1Q17. The price closed the 1Q18 at US$2,411/ton, down 3.4% from US$2,495/ton at the end of 4Q17. The decrease in prices is driven mainly by new expectations of increase in supply and concerns over a demand reduction.

Source: Bloomberg

The better-than-expected Chinese performance in the first two months of 2018 - industrial production recorded a 7.2% increase - and the expectations of a more robust demand for the year was dampened by the tariff announcement by the U.S. president. This raised the prospect of retaliatory actions from the Chinese, with its potential to harm overall global economic growth, sending metal prices downwards.

From stocks side, the delivery of 9.8kt of refined lead into the LME warehouses at the beginning of March also added momentum to the overall fall in price. This was in addition to the 12.9kt that came in to LME at the end of February. Notwithstanding, LME stocks continued a declining behavior during 1Q18, closing March at 129kt, a reduction of 9% when compared to the beginning of January, that closed at 142kt.

Foreign Exchange

Continuing 2017’s decline, the U.S. dollar started 2018 on a weaker note supported by rising concerns over a global trade-war, after the U.S. announcement of tariffs on steel and aluminum, as well as Chinese manufactured goods, an expectation of progress in renegotiations of the North America Free Trade Agreement (NAFTA) and the Federal Reserve forecast of three rate hikes during the year, not four as the market expected.

The average exchange rate for the Brazilian Real in the first quarter of 2018 was 3.24/US$, 3.1% higher than the average in the same period in 2017, due to the delay in approval of the welfare reform that seems to be a low priority, and the political uncertainty surrounding the Brazilian electoral scenario, with the anti-corruption Operation “Car Wash” increasingly impacting possible presidential candidates and allies resulting in concerns with the market about the outcome of the October elections.

The average exchange rate for Peruvian soles in the first quarter of 2018 was 3.24/US$, 1.5% lower than the average in the same period in 2017, due primarily to the resignation of president Pedro Pablo Kuczynski that fueled expectations of higher political stability in Peru.

Business Performance

Information relating to mineral reserves and resources

On April 30, 2018 we filed both our annual report on Form 20-F for the fiscal year ended December 31, 2017 and the 2017 YE MRMR Update. We reported an aggregate of contained metal in reserves estimates as at December 31, 2017 of 3,897.2 thousand tonnes of zinc, 430.8 thousand tonnes of copper, 592.6 thousand tonnes of lead, 3,468,642 kilograms of silver and 2,919 kilograms of gold, representing an increase of 8.7% for zinc, 5.6% for copper, 6.6% for lead, 7.9% for silver and a 5.4% decrease in gold, in comparison to information provided in our previous publicly available technical reports.

An increase in reserves estimates aggregate tonnage at Cerro Lindo in Peru (3.3 million tonnes or 6.2%) and Vazante in Brazil (3.1 million tonnes or 20.6%) resulted from a successful exploration program that increased the resource base combined with the improvement in operational conditions, such as mine recovery in Cerro Lindo. In the case of Atacocha in Peru, the reserves estimate increase in aggregate tonnage (3.0 million tonnes or 17.6%) resulted from the granting of permits in respect of our open pit operation (Tajo San Gerardo), which expanded the pit limits. Reserves estimates net increase was 8.9 million tonnes compared to our previously disclosed estimates dated as of June 30, 2017.

The report also includes mineral reserves and/or mineral resources estimates for our El Porvenir mine in Peru and Morro Agudo mine in Brazil and our greenfield projects — Aripuanã and Caçapava do Sul in Brazil and Shalipayco, Magistral, Hilarión, Pukaqaqa and Florida Canyon in Peru.

The 2017 YE MRMR Update contains descriptions of our mineral reserves and mineral resources estimates prepared in accordance with NI 43-101, and may not be comparable to similar information prepared in accordance with Industry Guide 7 that is presented in our annual report on Form 20-F.

The annual report on Form 20-F and the 2017 YE MRMR Update report are available on our website (www.nexaresources.com), on SEDAR (www.sedar.com) and on EDGAR (www.sec.gov).

Mining Production Volumes and Cash Cost by Assets

|

Consolidated |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. 1Q17 |

|

|

Treated Ore (kton ROM) |

|

3,149 |

|

3,351 |

|

3,026 |

|

4.1 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

Zinc grade (%) |

|

3.19 |

|

3.50 |

|

3.48 |

|

-29 |

bp |

|

Copper grade (%) |

|

0.42 |

|

0.40 |

|

0.39 |

|

3 |

bp |

|

Lead grade (%) |

|

0.50 |

|

0.58 |

|

0.52 |

|

-2 |

bp |

|

Silver grade (oz/t)(2) |

|

0.88 |

|

0.96 |

|

0.86 |

|

2 |

bp |

|

Gold grade (oz/t) |

|

0.00 |

|

0.01 |

|

0.01 |

|

1 |

bp |

|

|

|

|

|

|

|

|

|

|

|

|

Zn Content (kton) |

|

87.2 |

|

102.0 |

|

92.3 |

|

-5.5 |

% |

|

Cerro Lindo |

|

27.8 |

|

44.6 |

|

39.3 |

|

-29.3 |

% |

|

Vazante(2) |

|

35.5 |

|

34.8 |

|

34.3 |

|

3.6 |

% |

|

El Porvenir |

|

15.4 |

|

13.9 |

|

9.5 |

|

62.2 |

% |

|

Atacocha |

|

4.1 |

|

3.9 |

|

3.8 |

|

7.8 |

% |

|

Morro Agudo |

|

4.4 |

|

4.9 |

|

5.4 |

|

-19.0 |

% |

|

Cu Content (kton) |

|

10.7 |

|

10.9 |

|

9.4 |

|

13.4 |

% |

|

Pb Content (kton) |

|

12.3 |

|

15.0 |

|

11.8 |

|

4.1 |

% |

|

Ag Content (koz)(2) |

|

1,884 |

|

2,271 |

|

1,706 |

|

10.4 |

% |

|

Au Content (koz) |

|

7.4 |

|

8.0 |

|

8.0 |

|

-7.8 |

% |

|

Zn Eq production(1) |

|

134.0 |

|

154.1 |

|

135.2 |

|

-0.9 |

% |

|

Cerro Lindo |

|

57.1 |

|

77.9 |

|

67.1 |

|

-14.9 |

% |

|

Vazante |

|

36.1 |

|

35.5 |

|

34.9 |

|

3.5 |

% |

|

El Porvenir |

|

23.8 |

|

22.5 |

|

15.7 |

|

51.4 |

% |

|

Atacocha |

|

11.6 |

|

12.3 |

|

10.9 |

|

7.0 |

% |

|

Morro Agudo |

|

5.3 |

|

5.9 |

|

6.6 |

|

-19.6 |

% |

(1) Consolidated mining production in kton of zinc equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton; copper: US$6,166/ton; lead: US$2,317/ton; silver: US$17/oz; and gold: US$1,257/oz.

(2) Silver volumes now include the silver in lead concentrate from Vazante, which was not considered in previous reports. The differences are: 218,975 oz of silver in 2015, 224,353 oz of silver in 2016 and 355,496 oz of silver in 2017.

Production: The zinc equivalent production in Nexa’s mining operations totaled 134.0kton in 1Q18, slightly lower compared to 135.2kton in the same period of the previous year representing a 0.9% reduction. The 4.1% (123 ktons) increase in treated ore volume and the increase in copper and silver grades offset part of the reduction in zinc grades.

Cerro Lindo zinc equivalent production in 1Q18 was 14.9% or 10.0 kton lower compared to 1Q17 mainly due to lower grades. This reduction was partially offset by a 51.4% or 8.1 kton higher production in El Porvenir, mainly due to higher treated ore in the same period combined with better grades at the mine.

|

Consolidated cash cost |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 |

|

|

Cash cost net of by-products credits in US$/ton |

|

483.5 |

|

349.4 |

|

843.7 |

|

-42.7 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

0.22 |

|

0.16 |

|

0.38 |

|

-42.7 |

% |

|

AISC in US$/ton |

|

805.7 |

|

828.2 |

|

1,116.0 |

|

-27.8 |

% |

|

AISC in US$/lb |

|

0.37 |

|

0.38 |

|

0.51 |

|

-27.8 |

% |

Cash cost: We updated our AISC calculations to include sustaining CAPEX and also health, safety and environment, tailing dams and other non-expansion related CAPEX.

The cash cost net of by-products credits decreased by 42.7% when comparing US$0.22/lb (or US$483.7/ton) in 1Q18 and US$0.38/lb (or US$843.7/ton) in 1Q17. Higher by-products credits and lower zinc treatment charges pushed the total cash cost net of by-products down.

AISC also decreased, reaching US$0.37/lb (or US$805.7/ton) in 1Q18 when compared to US$0.51/lb (or US$1,116.0/ton) in 1Q17, driven mostly by cash cost reductions but partially offset by higher sustaining CAPEX and corporate expenses.

For a reconciliation of AISC, please refer to the appendix section “All-in Sustaining Cost — Mining”.

Cerro Lindo, Peru

The Cerro Lindo mine is an underground mine located in Peru, wholly-owned by our subsidiary Nexa Peru, which began operating in 2007. In July 2017, an expansion project was completed at the concentrate plant that treats ore at Cerro Lindo, increasing its processing capacity to 21kton of ore per day. Cerro Lindo’s estimated proven and probable mineral reserves represents a mine life of approximately eight years in accordance to the most recent 2017 YE MRMR Update as of December 31, 2017.

|

Cerro Lindo, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. 1Q17 |

|

|

Treated Ore (kton ROM) |

|

1,712 |

|

1,876 |

|

1,713 |

|

0.0 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

Zinc grade (%) |

|

1.79 |

|

2.57 |

|

2.51 |

|

-72 |

bp |

|

Copper grade (%) |

|

0.69 |

|

0.67 |

|

0.64 |

|

5 |

bp |

|

Lead grade (%) |

|

0.21 |

|

0.32 |

|

0.29 |

|

-8 |

bp |

|

Silver grade (oz/t) |

|

0.63 |

|

0.73 |

|

0.70 |

|

-7 |

bp |

|

Gold grade (oz/t) |

|

0.00 |

|

0.00 |

|

0.00 |

|

0 |

bp |

|

|

|

|

|

|

|

|

|

|

|

|

Zn Content (kton) |

|

27.8 |

|

44.6 |

|

39.3 |

|

-29.3 |

% |

|

Cu Content (kton) |

|

10.5 |

|

10.8 |

|

9.2 |

|

13.7 |

% |

|

Pb Content (kton) |

|

2.7 |

|

4.8 |

|

3.8 |

|

-29.4 |

% |

|

Ag Content (koz) |

|

770 |

|

1,024 |

|

803 |

|

-4.1 |

% |

|

Au Content (koz) |

|

0.9 |

|

1.2 |

|

1.1 |

|

-19.6 |

% |

|

Zn Eq production(1) |

|

57.1 |

|

77.9 |

|

67.1 |

|

-14.9 |

% |

(1) Mining production in kton of Zinc Equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton; copper: US$6,166/ton; lead: US$2,317/ton; silver: US$17/oz; and gold: US$1,257/oz.

Production: The zinc equivalent production in Cerro Lindo was 57.1 kton in 1Q18, 14.9% lower when compared to 67.1 kton in 1Q17. Copper grades increased from 0.64% in 1Q17 to 0.69% in 1Q18, but it was not enough to offset the lower zinc grades of 1.79% in 1Q18 compared to 2.51% in 1Q17. The mining plan for Cerro Lindo already indicated a reduction in zinc grades, but it was intensified by a delay in reaching some higher grades areas that were planned to operate during 1Q18.

Projects:

· Construction of the new waste disposal (Botadero Pahuaypite) aims the continuity of operations in the Cerro Lindo Unit according with the mine plan. In 1Q18, we finished the feasibility study (FEL3) and the project is under final internal approval. The Environmental Impact Assessment modification to include this new disposal area was approved by the government in March 2018. This is a prerequisite for the construction license, which has already been submitted and is forecasted to be approved in July 2018. NEXA estimates a total CAPEX for this implementation in the order of US$9.4 million with the start of operation of the new deposit in January 2019.

· Replacement of the seawater pipeline from the desalination plant on the coast to the mine. The goal of this project is to extend the life of the pumping lines, reducing the working pressure by increasing the diameter and improving the availability of water flow. The project will be carried out in three stages: (1)

replacement of the critical sections (11.3 km) by the end of 2018 and (2) other sections along 2019, totaling an additional 23.6km. In 1Q18, the Feasibility Study (FEL3) was completed and the project is under NEXA´s internal approval process. The total CAPEX is estimated at US$11.8 million.

|

Cash cost Cerro Lindo, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

-501.5 |

|

-430.9 |

|

211.5 |

|

N/A |

|

|

Cash cost net of by-products credits in US$/lb |

|

-0.23 |

|

-0.20 |

|

0.10 |

|

N/A |

|

Cash cost: Cash cost net of by-products decreased from US$0.10/lb (or US$211.5/ton) in the 1Q17 to a negative US$0.23/lb (or US$501.5/ton) in the 1Q18 reflecting not only higher prices but also larger volumes of copper produced as a by-product.

Vazante, Brazil

The Vazante mine is an underground mine located in Minas Gerais State in Brazil. It is wholly-owned by our subsidiary Nexa Recursos Minerais, and began operating in 1969. The current concentration processing capacity is 4.1kton of ore per day. This mine’s estimated proven and probable mineral reserves represents a mine life of approximately twelve years in accordance to the 2017 YE MRMR Update as of December 31, 2017.

|

Vazante, Brazil |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. 1Q17 |

|

|

Treated Ore (kton ROM) |

|

313 |

|

343 |

|

310 |

|

1.1 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

Zinc grade (%) |

|

13.62 |

|

12.66 |

|

13.09 |

|

53 |

bp |

|

Lead grade (%) |

|

0.30 |

|

0.32 |

|

0.32 |

|

-2 |

bp |

|

Silver grade (oz/t)(2) |

|

0.54 |

|

0.46 |

|

0.62 |

|

-8 |

bp |

|

|

|

|

|

|

|

|

|

|

|

|

Zn Content (kton) |

|

35.5 |

|

34.8 |

|

34.3 |

|

3.6 |

% |

|

Pb Content (kton) |

|

0.20 |

|

0.26 |

|

0.23 |

|

-16.0 |

% |

|

Ag Content (koz)(2) |

|

74.9 |

|

82.9 |

|

74.1 |

|

1.0 |

% |

|

Zn Eq production(1) |

|

36.1 |

|

35.5 |

|

34.9 |

|

3.5 |

% |

(1) Mining production in kton of Zinc Equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton; copper: US$6,166/ton; lead: US$2,317/ton; silver: US$17/oz; and gold: US$1,257/oz.

(2) Silver volumes now include the silver in lead concentrate from Vazante, which was not considered in previous reports. The differences are: 218,975 oz of silver in 2015, 224,353 oz of silver in 2016 and 355,496 oz of silver in 2017.

Production: The zinc equivalent production in Vazante was 36.1kton in 1Q18, 3.5% higher when compared to 1Q17 due to higher grades of 13.62% vs. 13.09% in 1Q17 and stable treated ore volumes of 313kton compared to 310 kton in 1Q17.

Projects:

· Dry Stacking Disposal consists on the installation of a filtration tailings plant with press filters to dry dispose the material in piles, replacing the conventional tailings disposal directly into dam. During 1Q18, the project advanced into construction with key highlights including the engagement of Ausenco to develop the detail engineering, purchase orders for long lead time items (filters, thickener and belt

conveyors) and the kick-off meeting with the civil and electromechanical erection company.

· Vazante mine deepening project: One of our key brownfield projects is the Vazante Mine Deepening Project, which we expect to extend the mine life of Vazante mine from 2022 until 2027. This project began in 2013 and is forecasted to end in 2022. In 1Q18, we reached 64% physical progress focusing on the Pumping Station EB140 where we completed the pumping room excavation and held the kick-off meeting with the civil and electromechanical assembly company for Pumping Station EB140. The project has contributed 27% of Vazante’s zinc production in 2017 and reached 52% in 1Q18.

|

Cash cost Vazante, Brazil |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

827.4 |

|

850.8 |

|

1,076.4 |

|

-23.1 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

0.38 |

|

0.39 |

|

0.49 |

|

-23.1 |

% |

Cash cost: Cash cost net of by-products decreased 23.1% comparing 1Q17 to the 1Q18, from US$0.49/lb (or US$1,076.4/ton) to US$0.38/lb (or US$827.4/ton).

El Porvenir, Peru

The El Porvenir mine is an underground mine located in Peru. It is wholly-owned by our subsidiary Nexa Peru and began operating in 1949. The current concentration processing capacity is 6.5kton of ore per day. This mine’s estimated proven and probable mineral reserves represent a mine life of approximately ten years in accordance to the 2017 YE MRMR Update as of December 31, 2017.

|

El Porvenir, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. 1Q17 |

|

|

Treated Ore (kton ROM) |

|

535 |

|

516 |

|

381 |

|

40.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

Zinc grade (%) |

|

3.20 |

|

3.04 |

|

2.86 |

|

34 |

bp |

|

Copper grade (%) |

|

0.16 |

|

0.13 |

|

0.14 |

|

2 |

bp |

|

Lead grade (%) |

|

0.96 |

|

1.07 |

|

0.98 |

|

-2 |

bp |

|

Silver grade (oz/t) |

|

1.82 |

|

2.08 |

|

1.98 |

|

-16 |

bp |

|

Gold grade (oz/t) |

|

0.01 |

|

0.02 |

|

0.02 |

|

1 |

bp |

|

|

|

|

|

|

|

|

|

|

|

|

Zn Content (kton) |

|

15.4 |

|

13.9 |

|

9.5 |

|

62.2 |

% |

|

Cu Content (kton) |

|

0.2 |

|

0.1 |

|

0.2 |

|

0.0 |

% |

|

Pb Content (kton) |

|

4.1 |

|

4.3 |

|

2.8 |

|

47.4 |

% |

|

Ag Content (koz) |

|

614 |

|

671 |

|

475 |

|

29.3 |

% |

|

Au Content (koz) |

|

2.4 |

|

2.4 |

|

1.8 |

|

33.1 |

% |

|

Zn Eq production(1) |

|

23.8 |

|

22.5 |

|

15.7 |

|

51.4 |

% |

(1) Mining production in kton of Zinc Equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton; copper: US$6,166/ton; lead: US$2,317/ton; silver: US$17/oz; and gold: US$1,257/oz.

Production: In El Porvenir, zinc equivalent production was 51.4% higher, totaling 23.8kton in the 1Q18 compared to 15.7kton in 1Q17, mainly due to stabilization of new operational safety standards that negatively impacted production in the beginning of 2017 and higher zinc grades.

Main Projects for the Pasco complex (El Porvenir and Atacocha):

The El Porvenir and Atacocha mines that form the Pasco mining complex are currently undergoing an operational integration process. This complex integration involves shared tailings, storage facility and shared underground infrastructure among other benefits.

· Elevation of El Porvenir tailings dam level: this project is being undertaken to assure sustainability to the operations of Atacocha and El Porvenir Units. During 1Q18, we have concluded an initial stage of this project expending a total of US$16.9 million, 5% below the project’s original estimate. We started studies to further elevate the tailings dam by 2Q19. We are also working on a rain water channel, which aims to meet the environmental constraints aligned with the best sustainability practices of our organization.

· Waste disposal: The focus is on the construction of the new waste disposal for the continuous operation of San Gerardo’s open pit in Atacocha. In 1Q18, the first phase of construction has reached 67% physical progress with CAPEX

estimated at US$8.4MM and completion scheduled for 3Q18. The second phase is under Feasibility Study (FEL3) that is more than 44% complete, with the project expected to start construction in 3Q18 and completion by 3Q19.

|

Cash cost El Porvenir, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

1,267.9 |

|

1,183.1 |

|

1,766.9 |

|

-28.2 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

0.58 |

|

0.54 |

|

0.80 |

|

-28.2 |

% |

Cash cost: El Porvenir’ cash cost net of by-products decreased from US$0.80/lb (US$ 1,766.9/ton) to US$0.58/lb (US$ 1,267.9/ton), a 28.2% reduction, primarily due to an increase in zinc produced and an increase in by-products off-setting an increase in costs due to a significant increase in tons mined and milled.

Atacocha, Peru

The Atacocha mine is an underground and open pit mine located in Peru. It is 67% owned by Nexa Peru and began operating in 1938. The current concentration processing capacity is 4.5kton of ore per day. This mine’s estimated proven and probable mineral reserves represent a mine life of approximately twelve years estimated in accordance with the 2017 YE MRMR Update as of December 31, 2017.

|

Atacocha, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. 1Q17 |

|

|

Treated Ore (kton ROM) |

|

368 |

|

382 |

|

353 |

|

4.3 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

Zinc grade (%) |

|

1.42 |

|

1.32 |

|

1.37 |

|

5 |

bp |

|

Copper grade (%) |

|

0.10 |

|

0.10 |

|

0.07 |

|

3 |

bp |

|

Lead grade (%) |

|

1.28 |

|

1.32 |

|

1.14 |

|

14 |

bp |

|

Silver grade (oz/t) |

|

1.49 |

|

1.60 |

|

1.32 |

|

17 |

bp |

|

Gold grade (oz/t) |

|

0.02 |

|

0.02 |

|

0.02 |

|

0 |

bp |

|

|

|

|

|

|

|

|

|

|

|

|

Zn Content (kton) |

|

4.1 |

|

3.9 |

|

3.8 |

|

7.8 |

% |

|

Cu Content (kton) |

|

0.02 |

|

0.02 |

|

0.02 |

|

N/A |

|

|

Pb Content (kton) |

|

4.1 |

|

4.4 |

|

3.4 |

|

18.1 |

% |

|

Ag Content (koz) |

|

424.8 |

|

493.1 |

|

354.4 |

|

19.9 |

% |

|

Au Content (koz) |

|

4.1 |

|

4.4 |

|

5.1 |

|

-19.8 |

% |

|

Zn Eq production(1) |

|

11.6 |

|

12.3 |

|

10.9 |

|

7.0 |

% |

(1) Mining production in kton of Zinc Equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton; copper: US$6,166/ton; lead: US$2,317/ton; silver: US$17/oz; and gold: US$1,257/oz.

Production: At Atacocha, zinc equivalent production increased by 7.0% to 11.6kton in 1Q18 when compared to 10.9kton in 1Q17. The higher zinc equivalent volume was driven by a 4.3% increase in treated ore (15kton) combined with higher grades for all metals.

Main Projects for the Pasco complex (El Porvenir and Atacocha): Please see the El Porvenir section above for further details.

|

Cash cost Atacocha, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

287.0 |

|

-563.3 |

|

1,063.1 |

|

-73.0 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

0.13 |

|

-0.26 |

|

0.48 |

|

-73.0 |

% |

Cash cost: Atacocha cash cost net of by-products decreased from US$0.48/lb (US$1,063.1/ton) to US$0.13/lb (US$287.0/ton), a 73.0% reduction when comparing 1Q18 with 1Q17 primarily due to an increase in by-products credits due to higher non-zinc metals production and higher metals prices and high zinc sales.

Morro Agudo, Brazil

The Morro Agudo complex, located in the Minas Gerais State of Brazil, includes an underground and an open pit mine. It is wholly-owned by our subsidiary Nexa Recursos Minerais and began operating in 1988. The current concentration processing capacity is 3.40kton of ore per day. As of June 30, 2017, this mine’s mineral estimated resources presented a potential mine life of approximately 11 years at a preliminary economic assessment level of study.

|

Morro Agudo, Brazil |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. 1Q17 |

|

|

Treated Ore (kton ROM) |

|

220 |

|

236 |

|

270 |

|

-18.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

Zinc grade (%) |

|

2.18 |

|

2.22 |

|

2.18 |

|

0 |

bp |

|

Lead grade (%) |

|

0.63 |

|

0.67 |

|

0.71 |

|

-8 |

bp |

|

|

|

|

|

|

|

|

|

|

|

|

Zn Content (kton) |

|

4.4 |

|

4.9 |

|

5.4 |

|

-19.0 |

% |

|

Pb Content (kton) |

|

1.2 |

|

1.3 |

|

1.5 |

|

-21.9 |

% |

|

Zn Eq production(1) |

|

5.3 |

|

5.9 |

|

6.6 |

|

-19.6 |

% |

(1) Mining production in kton of Zinc Equivalent calculated by converting copper, lead, silver and gold contents to a zinc equivalent grade at 2017 average benchmark prices. The prices used for this conversion are: zinc: US$2,896/ton; copper: US$6,166/ton; lead: US$2,317/ton; silver: US$17/oz; and gold: US$1,257/oz.

Production: The Morro Agudo zinc equivalent production was 19.6% lower in the 1Q18 when compared to the same period of 2017, 5.3kton and 6.6kton respectively, impacted by lower treated ore and lower grades.

|

Cash cost Morro Agudo, Brazil |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

2,154.5 |

|

1,887.2 |

|

1,637.0 |

|

31.6 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

0.98 |

|

0.86 |

|

0.74 |

|

31.6 |

% |

Cash cost: Morro Agudo cash cost net of by-products increased from US$0.74/lb (US$1,637.0) in the 1Q17 to US$0.98/lb (US$ 2,154.5/ton) in the 1Q18, a 31.6% increase in the period negatively impacted by lower zinc production and sales and a decrease in by-products revenue.

Smelting Volumes and Cash Cost by Assets

|

Consolidated |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Metallic zinc Sales (kton) |

|

137.3 |

|

145.3 |

|

130.6 |

|

5.1 |

% |

|

Global Recovery |

|

94.4 |

% |

95.0 |

% |

94.3 |

% |

3 |

bp |

|

Zinc oxide Sales (kton) |

|

9.1 |

|

9.7 |

|

8.9 |

|

2.7 |

% |

Sales: Sales of metallic zinc in 1Q18 were 5.1% higher than in 1Q17, totaling 137.3kton supported by higher production. As discussed in previous quarters, production and sales in the first half of 2017 were impacted by heavy rains and floods in Peru.

Cash cost: We updated our AISC calculations to include sustaining CAPEX and also health, safety and environment, tailing dams and other non-expansion related CAPEX.

|

Consolidated cash cost |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

3,163.4 |

|

2,946.8 |

|

2,427.4 |

|

30.3 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

1.43 |

|

1.34 |

|

1.10 |

|

30.3 |

% |

|

AISC in US$/ton |

|

3,327.3 |

|

3,268.4 |

|

2,639.2 |

|

26.1 |

% |

|

AISC in US$/lb |

|

1.51 |

|

1.48 |

|

1.20 |

|

26.1 |

% |

Cash cost: cash cost net of by-products credits increased by 30.3% to US$1.43/lb (or US$3,163.4/ton) in 1Q18 when compared to US$1.10/lb (or US$2,427.4/ton) in the same period of the previous year, mostly due to higher raw material costs driven by higher zinc prices and lower treatment charges, partially offset by higher by-products’ credits (mainly sulfuric acid and copper sulfate); and lower sustaining CAPEX with the main modernization projects that started in 2017 nearing final phase.

For a reconciliation of AISC, please refer to the appendix section “All-in Sustaining Cost — Smelting”.

Cajamarquilla, Peru

The Cajamarquilla smelter, which is wholly-owned by Nexa, is located in Peru and began operating in 1981. It is currently the largest zinc smelter in Latin America and the seventh largest globally, according to Wood Mackenzie data from 2017. Cajamarquilla uses roast-leach-electrowinning technology, with a nominal production capacity of 335kton per year. It sold 79.0kton in 1Q18, 8.7% higher than in 1Q17 that was impacted by heavy rains and floods.

|

Cajamarquilla, Peru |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Metallic zinc sales (kton) |

|

79.0 |

|

84.2 |

|

72.7 |

|

8.7 |

% |

|

Global Recovery |

|

95.0 |

% |

96.3 |

% |

94.7 |

% |

28 |

bp |

Main Projects:

· Conversion to Jarosite process: the conversion will allow for the recovery of a greater percentage of zinc, estimated to increase average recoveries from 94% to 97% at the plant. Total CAPEX for the conversion is estimated to be US$44.9 million, and the project is expected to be completed by 3Q19. Amec Foster Wheeler completed feasibility studies on the project and Asturiana de Zinc, a globally recognized independent consultant, performed crosschecks and recommendations for the process route. In 1Q18, the project execution highlights include the conclusion of the procurement process for detailed engineering, awarding SNC Lavalin as the main consultant and Asturiana de Zinc as the process consultant. Additionally, we are finalizing the purchase process for certain long lead time items.

|

Cash cost Cajamarquilla |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

3,087.0 |

|

2,849.6 |

|

2,502.0 |

|

23.4 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

1.40 |

|

1.29 |

|

1.13 |

|

23.4 |

% |

Cash cost: Cajamarquilla cash cost net of by-products increased from US$1.13/lb (US$2,502.0/ton) to US$1.40/lb (US$3,087.0/ton) in 1Q18, a 23.4% increase in the comparison with the same quarter of the previous year.

Três Marias, Brazil

The Três Marias smelter, which is wholly-owned by the subsidiary Nexa Recursos Minerais, is located in Minas Gerais State in Brazil and began operating in 1969. Três Marias processes zinc silicate concentrate from Nexa’s Vazante mine and zinc sulfide concentrate from Nexa’s Morro Agudo mine and uses roast-leach-electrowin technology, with a nominal production capacity of 190kton per year. It sold 40.1kton of metallic zinc in 1Q18, 5.6% higher than in 1Q17.

|

Três Marias, Brazil |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

| |

|

Metallic zinc sales (kton) |

|

40.1 |

|

42.0 |

|

38.0 |

|

5.6 |

% | |

|

Global Recovery |

|

94.2 |

% |

94.7 |

% |

94.9 |

% |

-70 |

bp | |

|

Zinc oxide (kton) |

|

9.1 |

|

9.7 |

|

8.9 |

|

2.7 |

% | |

|

|

|

|

|

|

|

|

|

|

| |

|

Cash cost Três Marias |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

| |

|

Cash cost net of by-products credits in US$/ton |

|

3,294.0 |

|

3,089.2 |

|

2,333.1 |

|

41.2 |

% | |

|

Cash cost net of by-products credits in US$/lb |

|

1.49 |

|

1.40 |

|

1.06 |

|

41.2 |

% | |

Cash cost: Três Marias cash cost net of by products increased by 41.2% when comparing the 1Q17 level of US$1.06/lb (US$2,333.1/ton) to US$1.49/lb (US$3,294.0/ton) in the 1Q18.

Juiz de Fora, Brazil

The Juiz de Fora smelter, which is wholly-owned by our subsidiary Nexa Recursos Minerais, is located in Minas Gerais State in Brazil and began operating in 1980. This smelter uses roast-leach-lectrowin and Waelz Furnace technologies, with a nominal production capacity of 89kton per year. It sold 18.2kton in 1Q18, 8.8% lower than 1Q17.

|

Juiz de Fora, Brazil |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Metallic zinc sales (kton) |

|

18.2 |

|

19.1 |

|

19.9 |

|

-8.8 |

% |

|

Global Recovery |

|

92.4 |

% |

90.40 |

% |

92.0 |

% |

40 |

bp |

|

Cash cost Juiz de Fora |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 vs. |

|

|

Cash cost net of by-products credits in US$/ton |

|

3,212.3 |

|

2,549.1 |

|

2,447.6 |

|

31.2 |

% |

|

Cash cost net of by-products credits in US$/lb |

|

1.46 |

|

1.16 |

|

1.11 |

|

31.2 |

% |

Cash cost: Juiz de Fora cash cost net of by-products increased by 31.2% from US$1.11/lb (US$2,447.6/ton) to US$1.46/lb (US$3,212.3/ton) in the comparison between the 1Q18 and 1Q17.

CAPEX

|

|

|

|

US$ million |

|

1Q18 |

|

2017 |

|

|

Mining |

|

20.0 |

|

107.1 |

|

|

Cerro Lindo |

|

0.5 |

|

7.5 |

|

|

El Porvenir |

|

4.7 |

|

19.9 |

|

|

Atacocha |

|

2.1 |

|

5.9 |

|

|

Vazante |

|

11.2 |

|

55.3 |

|

|

Morro Agudo |

|

1.6 |

|

18.6 |

|

|

Smelting |

|

10.1 |

|

81.0 |

|

|

CJM |

|

2.2 |

|

20.0 |

|

|

Três Marias |

|

5.7 |

|

43.5 |

|

|

Juiz de Fora |

|

2.1 |

|

17.5 |

|

|

Other |

|

2.9 |

|

9.5 |

|

|

|

|

|

|

|

|

|

Expansion |

|

9.6 |

|

48.8 |

|

|

Non-Expansion |

|

23.3 |

|

148.8 |

|

|

|

|

|

|

|

|

|

Total |

|

33.0 |

|

197.6 |

|

|

|

|

|

|

|

|

|

US$ million |

|

1Q18 |

|

2017 |

|

|

Modernization |

|

1.0 |

|

21.4 |

|

|

Sustaining |

|

9.4 |

|

59.4 |

|

|

HSE |

|

11.2 |

|

62.1 |

|

|

Other |

|

1.7 |

|

5.9 |

|

|

Non-Expansion |

|

23.3 |

|

148.8 |

|

Total capital expenditures (CAPEX(7)) was US$33.0 million in the first quarter of 2018, and consisted mainly of higher investments in the tailings dams of the Três Marias smelter in Brazil. The CAPEX was US$20.0 million below budget for 1Q18, as certain necessary approvals were delayed. Of our total CAPEX, 29% was directed towards brownfield expansion projects in 1Q18, respectively, which is aligned with Nexa’s strategy of growing its mining business.

The main expansion project impacting CAPEX in 1Q18 is the ongoing deepening of the Vazante mine. Other brownfield mining projects, including the development of the

(7) Total capital expenditure (CAPEX) is the sum of acquisitions of property, plant and equipment and acquisition of intangible assets, as published in the consolidated statement of cash flows.

Ambrosia trend at the Company’s Morro Agudo mine, are also included in expansion CAPEX. Current expenditures in early-stage mining projects are considered expenses in operating results (see “Operational Results — Other Operating Results”) and totaled US$16.7 million in 1Q18.

Non-expansion projects accounted for 71% of total CAPEX in 1Q18. Main non-expansion projects are related to environmental, health and safety investments, sustaining and investments in tailings dams.

Greenfields

In addition to our mines and smelters, we have interests in five greenfield mining projects in Peru (Shalipayco, Magistral, Hilarión, Pukaqaqa and Florida Canyon Zinc) and two in Brazil (Aripuanã and Caçapava do Sul).

Aripuanã project

On April 25, we announced that the environmental authorities of the State of Mato Grosso, Brazil (SEMA/MT) granted the Preliminary Environmental License (“LP”) for our Aripuanã project after the approval by the Environmental State Council (CONSEMA).

The LP certifies that the project complies with the environmental standard requirements of projects with such characteristics and it is one important milestone for the implementation of the Aripuanã project.

The Aripuanã project is owned by Mineração Dardanelos Ltda., a joint venture between Nexa (which holds a 62.3% interest), Compañia Minera Milpo S.A.A., which is currently changing its corporate name to Nexa Resources Perú S.A.A., a subsidiary of Nexa (which holds a 7.7% interest) and Mineração Rio Aripuanã Ltda., a subsidiary of Karmin Exploration Inc. (which holds the remaining 30%).

Aripuanã is an underground polymetallic project containing zinc, lead and copper, with an estimated mine life of 24 years and an expected start of production in 2020. The project is located in the State of Mato Grosso, Brazil, exhibiting characteristics of a Volcanogenic Massive Sulfide, or VMS. As set out in the preliminary economic assessment (“PEA”), the estimated aggregate capital expenditures required for this project is US$354 million. It is currently estimated that the Aripuanã project, when and if it is fully developed and begins operation, could produce an annual average of approximately 51.0 thousand tonnes of zinc in concentrate, 20.0 thousand tonnes of lead in concentrate, 4.0 thousand tonnes of copper in concentrate and also 1.0 million ounces of silver and 25.0 thousand ounces of gold contained in the zinc, lead and copper concentrates. The PEA disclosed the details of the possible development of an operation with 5,000 tpd ore mining and processing capacity.

Outlook: The pre-feasibility study stage was completed during 2017, and Nexa approved the project to move forward to the feasibility study stage. Currently, the feasibility study development (FEL3) has advanced accordingly, reaching 58% completion at the end of March 2018 and is expected to be submitted to Nexa’s Board of Directors for approval consideration during the second half of 2018. In 2017, an

exploration program of more than 26,600 meter infill drilling was completed focused on mineral resources conversion and identification of mineralized deposits. Other applicable licenses and permits in Brazil such as the Installation License (LI) and Operating License (LO) are still pending.

Magistral and Pukaqaqa

Magistral and Pukaqaqa projects are progressing through pre-feasibility study (FEL 2). In 1Q18 we completed a drilling program for further metallurgical testwork, awarded engineering to Ausenco for Magistral’s FEL 2 and to JRI for Pukaqaqa’s FEL 2, and concluded tailings dam solution trade off studies.

Shalipayco

During 2018, we expect to finalize a scoping study (FEL1) in compliance with our investment policies, allowing pre-feasibility level drilling to commence in late 2018. Several alternatives for the business case are under early stages of study.

Financial Results

Consolidated

|

US$ million |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

1Q18 |

|

|

Net Revenues |

|

676.2 |

|

736.7 |

|

549.3 |

|

23.1 |

% |

|

Cost of sales |

|

-485.0 |

|

-502.4 |

|

-411.5 |

|

17.8 |

% |

|

Raw materials and consumed used |

|

-321.1 |

|

-321.3 |

|

-263.1 |

|

22.0 |

% |

|

Employee benefit expenses |

|

-43.8 |

|

-54.1 |

|

-43.9 |

|

-0.1 |

% |

|

Depreciation, amortization and depletion |

|

-68.9 |

|

-68.9 |

|

-67.8 |

|

1.6 |

% |

|

Services, miscellaneous |

|

-25.2 |

|

-36.2 |

|

-17.8 |

|

41.8 |

% |

|

Other expenses |

|

-26.0 |

|

-22.0 |

|

-18.9 |

|

37.1 |

% |

|

SG&A |

|

-46.7 |

|

-42.9 |

|

-40.8 |

|

-19.8 |

% |

|

Selling (1) |

|

-3.6 |

|

-4.9 |

|

-3.3 |

|

8.2 |

% |

|

General & administrative |

|

-43.1 |

|

-38.0 |

|

-37.5 |

|

14.9 |

% |

|

Other Income and expenses, net |

|

-22.9 |

|

-39.1 |

|

-21.8 |

|

5.2 |

% |

|

Project expenses |

|

-16.7 |

|

-42.5 |

|

-8.1 |

|

107.0 |

% |

|

Mining obligations |

|

-1.7 |

|

-2.4 |

|

-1.6 |

|

8.3 |

% |

|

Net operating hedge loss |

|

0.3 |

|

-6.8 |

|

-4.7 |

|

N/A |

|

|

Judicial provision |

|

-4.2 |

|

0.3 |

|

-1.9 |

|

123.8 |

% |

|

Others |

|

-0.6 |

|

12.4 |

|

-5.5 |

|

-89.5 |

% |

|

Net Financial Results |

|

-29.0 |

|

-90.0 |

|

4.1 |

|

N/A |

|

|

Financial income |

|

8.8 |

|

4.8 |

|

10.2 |

|

-14.4 |

% |

|

Financial expenses |

|

-29.9 |

|

-25.1 |

|

-22.4 |

|

33.4 |

% |

|

Foreign exchange gains (loss), net |

|

-7.9 |

|

-69.7 |

|

16.3 |

|

N/A |

|

|

Depreciation, amortization and depletion |

|

70.0 |

|

70.1 |

|

68.9 |

|

1.5 |

% |

|

Adjusted EBITDA |

|

191.2 |

|

222.5 |

|

144.1 |

|

32.7 |

% |

|

Adj. EBITDA Margin |

|

28.3 |

% |

30.2 |

% |

26.2 |

% |

210 bp |

|

|

Income Tax |

|

-29.8 |

|

-38.3 |

|

-24.0 |

|

24.5 |

% |

|

Net Income for the period |

|

62.8 |

|

24.0 |

|

55.2 |

|

13.6 |

% |

|

Attributable to Nexa shareholders |

|

55.1 |

|

12.2 |

|

49.1 |

|

12.2 |

% |

|

Attributable to non-controlling interests |

|

7.6 |

|

11.8 |

|

6.1 |

|

24.6 |

% |

|

Avg # of outstanding shares (in ‘000) |

|

133,320 |

|

127,527 |

|

112,821 |

|

18.2 |

% |

|

EPS (in US$) (2) |

|

0.41 |

|

0.10 |

|

0.44 |

|

-5.0 |

% |

Note: The information related to each of the eight most recently completed quarters is available at the appendix. A reconciliation of Adjusted EBITDA is available on at the end of this section.

(1) Freight costs were reclassified from selling expenses to cost of sales in 1Q18 and previous quarters due to the adoption of IFRS 15.

(2) Reflects corrected EPS for prior periods. See “Restatement of Earnings Per Share” below for further information.

Net Revenues totaled US$676.2 million in 1Q18, an increase of 23.1%, or US$126.9 million, when compared to US$549.3 million in 1Q17 due primarily to higher base metals prices in the global market. The average LME zinc price was 23.1% higher than the average in the same quarter of 2017. Copper and lead LME prices also increased by 19.4% and 10.7%, respectively.

Cost of sales increased by 17.8% in the 1Q18, totaling US$485.0 million compared to US$411.5 million in the 1Q17, due primarily to higher concentrate prices that impact our smelting operation. As mentioned in previous quarters, the process revisions made in order to reinforce safety conditions in the Company’s mines happened through the second half of 2017, impacting costs since then.

SG&A expenses totaled US$46.7 million in the 1Q18, compared to US$40.8 million in 1Q17. The 1Q18 total is composed of US$3.6 million in selling expenses and US$43.1 million in general and administrative (G&A) expenses. G&A expenses increased by 14.9%, or US$5.6 million mainly due to provisions regarding profit sharing bonuses in Peru and increase in management services.

Expenses under Other operating results totaled US$22.9 million in 1Q18 compared to US$21.8 million in 1Q17. This increase is mainly explained by: (i) an increase of US$8.6 million in the expenses associated with early stage projects; (ii) a provision recognized in the 1Q18 of US$3.8 million related to a legal dispute with an energy supplier in Peru; and (iii) a decrease of US$4.9 million in others.

Net financial results amounted to a loss of US$29.0 million in 1Q18, compared to a gain of US$4.1 million in 1Q17, a negative variation of US$33.1 million explained by: (i) non-cash foreign exchange variation of US$24.2 million, mainly as a result of the impact of intercompany foreign exchange variation on U.S. dollar-denominated loans made by Nexa Resources to Nexa Recursos Minerais S.A. (which has BRL as its functional currency) in a total amount of US$1,113.4 million, as of March 31, 2018. During 1Q18, the 3.1% depreciation of the BRL against the U.S. dollar resulted in a foreign exchange loss of US$7.9 million while in 1Q17 it had appreciated 19.4% generating an foreign exchange gain of US$16.3 million at that time; and (ii) an increase of US$6.4 million in interest on loans and financing as we issued US$700 million in unsecured bonds in May 2017 with a coupon of 5.375% p.a.

Income tax expenses amounted to US$29.8 million in 1Q18, representing an effective tax rate of 32.2%. The effective tax rate for the same period of 2017 was 30.3%.

Net income attributable to Nexa’s shareholders totaled US$55.1 million in 1Q18, an increase of 12.2% or US$6.0 million when compared to US$49.1 million in 1Q17, a consequence of the impacts mentioned above.

Adjusted EBITDA(8) totaled US$191.2 million in 1Q18, a 32.7% or US$47.2 million increase when compared to the same quarter of the previous year, mostly as a result of increased metal prices positively impacting net revenues as explained above.

The following table presents a reconciliation of Adjusted EBITDA to Net income.

|

US$ million |

|

1Q18 |

|

4Q17 |

|

1Q17 |

|

|

Adjusted EBITDA |

|

191.2 |

|

222.5 |

|

144.1 |

|

|

Gain (loss) on sales of investments |

|

0.3 |

|

0.0 |

|

0.0 |

|

|

|

|

|

|

|

|

|

|

|

EBITDA |

|

191.6 |

|

222.5 |

|

144.1 |

|

|

Results of investees |

|

0.0 |

|

0.1 |

|

0.0 |

|

|

Deprec., amort. and depletion |

|

-70.0 |

|

-70.1 |

|

-68.9 |

|

|

Net financial results |

|

-29.0 |

|

-90.0 |

|

4.1 |

|

|

Income tax |

|

-29.8 |

|

38.3 |

|

-24.0 |

|

|

Net Income |

|

62.8 |

|

100.7 |

|

55.2 |

|

(8) Non-IFRS financial measure. See “Use of Non-IFRS Financial Measures” section for further information.

Result by Segment

Segments information are reported in accordance with IFRS 8 - ‘Operating Segments’, and the information presented to the Board of Directors (“Directors”) and CEO on the performance of each segment is derived from the accounting records, adjusted for reallocations between segments, non-recurring effects, transfer pricing adjustments, extraordinary revenues or expenses not allocated in a specific segment. Revenues from the mining segment set out below reflect zinc concentrates production from the Vazante and Morro Agudo mines in Brazil that is transferred at cost to the Três Marias smelter. As a result, zinc concentrates production from our Vazante and Morro Agudo mines has its margin embedded in the Três Marias smelter financial results. A total of US$208.4 million in revenues from the mining segment was eliminated on consolidation comprised of US$90.6 million related to transfer-pricing adjustments and US$117.8 million related to intersegment elimination. For more information, please refer to explanatory note 30 of our Financial Statements.