UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| |

OR | |

|

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Date of event requiring this shell company report

For the transition period from to

Commission file number:

(Exact Name of Registrant as Specified in Its Charter) |

|

Not Applicable |

(Translation of Registrant’s Name Into English) |

|

(Jurisdiction of Incorporation or Organization) |

People’s Republic of |

|

(Address of Principal Executive Offices) People’s Republic of Telephone: +86- Email: |

(Name, Telephone, Email and/or Facsimile Number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

None

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Class A ordinary shares, par value US$0.0001 per share | ||||

(Title of Class) | ||||

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None |

(Title of Class) |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2023, there were

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐Yes ☒

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

☒ | Emerging growth company |

If an emerging growth company that prepare its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

International Financial Reporting Standards as issued | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to

follow. Item 17 ◻ Item 18 ◻

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ☐ Yes ☐ No

TABLE OF CONTENTS

i

INTRODUCTION

Except where the context otherwise requires and for purposes of this annual report only:

| ● | “ADSs” refers to our American depositary shares, each of which represents 20 Class A ordinary shares. Except as otherwise indicated, all ADS and per ADS data in this annual report give retroactive effect to the change in the ratio of ADSs to Class A ordinary shares from two ADSs to five Class A ordinary shares to one ADS to 20 Class A ordinary shares, or the ADS Ratio, which became effective on October 30, 2020; |

| ● | “China” or “PRC” refers to the People’s Republic of China; |

| ● | “Class A ordinary shares” refers to our Class A ordinary shares, par value US$0.0001 per share; |

| ● | “Class B ordinary shares” refers to our Class B ordinary shares, par value US$0.0001 per share; |

| ● | “Restructuring” refers to a corporate restructuring we completed in 2018 in order to strengthen our positioning as an independent open platform (for more information, see “Item 4. Information on the Company—A. History and Development of the Company”). As part of the Restructuring, all business operations previously operated by RONG360 prior to the Restructuring except for the digital lending business was transferred from RONG360 to us; |

| ● | “RONG360” means RONG360 Inc., a Cayman Islands exempted company, its subsidiaries and its consolidated variable interest entity, but, prior to the Restructuring, exclude Jianpu Technology Inc., its subsidiaries and its consolidated variable interest entities; |

| ● | “shares” or “ordinary shares” refers to our Class A and Class B ordinary shares, par value US$0.0001 per share; |

| ● | “VIE” refers to variable interest entity, and “the VIEs” refer to Beijing Rongdiandian Information Technology Co., Ltd., or RDD, Beijing Kartner Information Technology Co., Ltd., or KTN, Beijing Guangkezhixun Information Technology Co., Ltd., or GKZX, and Beijing Tianyi Chuangshi Technology Co., Ltd., or TCT; and |

| ● | “we,” “us,” “our company” and “our” refer to Jianpu Technology Inc., a Cayman Islands exempted company with limited liabilities, and its subsidiaries. We conduct operations in China through (i) our subsidiaries in mainland China and (ii) the VIEs with which we have maintained contractual arrangements and their subsidiaries in China. The description in this annual report on Form 20-F of our operations in China prior to the Restructuring excludes the digital lending business that was previously operated by and continued to be carried out by RONG360 after the Restructuring. |

For financial service providers, we generally consider each separate legal entity as one provider. For example, nationwide banks operate with multiple legal entities at provincial and local levels, and each entity has autonomy over product features and credit policies. Accordingly, we treat each legal entity as one financial service provider.

Our reporting currency is the Renminbi because our business is mainly conducted in China and substantially all of our revenues are denominated in Renminbi. This annual report contains translations of Renminbi amounts into U.S. dollars at specific rates solely for the convenience of the reader. The conversion of Renminbi into U.S. dollars in this annual report is based on the exchange rate set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report were made at a rate of RMB7.0999 to US$1.00, the exchange rate in effect on December 29, 2023 set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, the rates stated below, or at all.

The mainland China government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade.

1

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that involve risks and uncertainties. All statements other than statements of current or historical facts are forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

You can identify these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “likely to” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to, statements about:

| ● | our goals and strategies; |

| ● | our future business development, financial condition and results of operations; |

| ● | expected changes in our revenues, costs or expenditures; |

| ● | our expectations regarding demand for and market acceptance of our services; |

| ● | our expectation regarding the impact of any communicable diseases on our business, financial condition and results of operations; |

| ● | prospects for and competition in our industry, and |

| ● | government policies and regulations relating to us, and their future development. |

You should read this annual report and the documents that we refer to in this annual report with the understanding that our actual future results may be materially different from and worse than what we expect. Other sections of this annual report include additional factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements.

You should not rely upon forward-looking statements as predictions of future events. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

This annual report on Form 20-F also contains statistical data and estimates that we obtained from industry publications and reports generated by third-party providers of market intelligence, including the size, growth rates and other data relating to the financial services market in China. Although we have not independently verified the data, we believe that the publications and reports are reliable. The market data contained in this annual report involves a number of assumptions, estimates and limitations. The financial services market in China and its components may not grow at the rates projected by market data, or at all. The failure of these markets to grow at the projected rates may have a material adverse effect on our business and the market price of our ADSs. If any one or more of the assumptions underlying the market data turns out to be incorrect, actual results may differ from the projections based on these assumptions. In addition, projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Item 3. Key Information—D. Risk Factors” and elsewhere in this annual report. You should not place undue reliance on these forward-looking statements.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this annual report and the documents that we refer to in this annual report and have filed as exhibits to the registration statement, of which this annual report is a part, completely and with the understanding that our actual future results may be materially different from what we expect.

2

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Our Holding Company Structure and Contractual Arrangements with the VIEs

Jianpu Technology Inc. is not an operating company in China but a Cayman Islands holding company with no equity ownership in the VIEs. We conduct our operations in China through (i) our subsidiaries in mainland China and (ii) the VIEs with which we have maintained contractual arrangements and their subsidiaries in China. The laws and regulations of mainland China impose restrictions on foreign direct investment in companies involved in the value-added telecommunication services. Therefore, we operate such business or may operate certain other businesses which are also subject to foreign investment restrictions in mainland China through Beijing Rongdiandian Information Technology Co., Ltd., or RDD, Beijing Kartner Information Technology Co., Ltd., or KTN, Beijing Guangkezhixun Information Technology Co., Ltd., or GKZX, and Beijing Tianyi Chuangshi Technology Co., Ltd., or TCT, which we refer to collectively as “the VIEs” in this annual report, and rely on contractual arrangements among our subsidiaries in mainland China, the VIEs and their respective nominee shareholders to control the business operations of the VIEs. Such structure is used to provide investors with exposure to foreign investment in China-based companies where laws and regulations in mainland China prohibit or restrict direct foreign investment in operating companies. Revenues, excluding intercompany revenues, contributed by the VIEs accounted for 18.1%, 18.5% and 22.5% of our total revenues for the year ended December 31, 2021, 2022 and 2023, respectively. As used in this annual report, “we,” “us,” “our company” and “our” refer to Jianpu Technology Inc., a Cayman Islands exempted company with limited liabilities, and its subsidiaries. The description in this annual report of our operations in China prior to the Restructuring excludes the digital lending business that was previously operated by and continued to be carried out by RONG360 after the Restructuring. Holders of our ADSs hold equity interest in Jianpu Technology Inc., our Cayman Islands holding company, and do not have direct or indirect equity interest in the VIEs, and they may never directly hold equity interests in the VIEs in China.

We do not have any equity interests in the VIEs and the contractual agreements with the VIEs are not equivalent to equity ownership in their business. We have entered into a series of contractual arrangements, including exclusive purchase option agreements, exclusive business cooperation agreements, equity pledge agreements and powers of attorneys, with the VIEs and their shareholders. In particular, through the exclusive purchase option agreements, the shareholders of the VIEs irrevocably grant our subsidiaries in mainland China exclusive options to purchase all or part of the shareholders’ equity interests in the VIEs and all or part of the assets of the VIEs to the extent permitted under mainland China law. Through the equity pledge agreements, the shareholders of the VIEs pledge all of their equity interests in the VIEs to guarantee their and the VIEs’ performance of their obligations under the contractual arrangements. Pursuant to the powers of attorneys, the shareholders of the VIEs appoint our subsidiaries in mainland China as their attorneys-in-fact to exercise all shareholder rights in the VIEs. Through the exclusive business cooperation agreements, our subsidiaries in mainland China have the exclusive right to provide the VIEs with technical, consulting and other services needed for the business of the VIEs and are entitled to receive a service fee from the VIEs in return. Despite the lack of equity ownership, as a result of these contractual arrangements, we are regarded as the primary beneficiary of the VIEs for accounting purposes, which is not akin to a parent-subsidiary relationship, and we consolidate the VIEs in accordance with U.S. GAAP as required by Accounting Standards Codification Topic 810, Consolidation. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—The shareholders of the VIEs may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition” and “Item 4 Information on the Company—C. Organizational Structure—Contractual Arrangements with the VIEs.”

3

However, the contractual arrangements may not be as effective as direct ownership in providing us with control over the VIEs, and we may incur substantial costs to enforce the terms of the arrangements. In addition, these agreements have not been tested in Chinese courts. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—We rely on contractual arrangements with the VIEs and their shareholders to exercise control over a significant part of our business, which may not be as effective as direct ownership in providing operational control” and “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—The shareholders of the VIEs may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.”

There are also substantial uncertainties regarding the interpretation and application of current and future laws, regulations and rules in mainland China regarding the status of the rights of our Cayman Islands holding company with respect to its contractual arrangements with the VIEs and their shareholders. It is uncertain whether any new laws or regulations in mainland China relating to variable interest entity structures will be adopted or if adopted, what they would provide. If we or the VIEs are found to be in violation of any existing or future laws or regulations in mainland China, or fail to obtain or maintain any of the required permits or approvals, the regulatory authorities in mainland China would have certain discretion to take actions in dealing with such violations or failures. Our holding company, our subsidiaries in mainland China, the VIEs and our investors face uncertainty about potential future actions by the mainland China government that could affect the enforceability of the contractual arrangements with the VIEs and, consequently, significantly affect the financial performance of the VIEs and our company as a whole. The regulatory authorities in mainland China could disallow the VIE structure, which would likely result in a material change in our operations and cause the value of our securities to significantly decline or become worthless. For a detailed description of the risks associated with our corporate structure, please refer to risks disclosed under “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure.”

We face various legal and operational risks and uncertainties related to doing business in China that could result in a material change in our operations and/or the value of our ADSs. Substantially all of our current business operations are conducted in China through our subsidiaries in mainland China and the VIEs and their subsidiaries, and we are subject to complex and evolving laws and regulations in mainland China. The mainland China government has issued statements and conducted regulatory actions relating to areas such as the use of variable interest entities in certain industries, approvals, filings or other administrative requirements on offshore offerings, anti-monopoly regulatory actions, and oversight on cybersecurity and data privacy. The mainland China government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit our and the VIEs’ ability to conduct business and/or significantly limit or completely hinder our ability to offer or continue to offer securities to investors, accept foreign investments or list on a United States or other foreign exchange. Implementation of industry-wide regulations in this nature may cause the value of our securities to significantly decline or be worthless. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The mainland China government’s significant oversight and discretion over our business operation could result in a material adverse change in our operations and the value of our ADSs.”

For example, the PRC Data Security Law and the PRC Personal Information Protection Law promulgated in 2021 posed additional challenges to our cybersecurity and data privacy compliance. The Cybersecurity Review Measures issued by the Cyberspace Administration of China and several other governmental authorities in mainland China in December 2021, as well as the Regulations on the Administration of Cyber Data Security (Draft for Comments) published by the Cyberspace Administration of China for public comments in November 2021, imposed potential additional restrictions on China-based overseas issuers like us. If future implementing rules of the Cybersecurity Review Measures and the enacted version of these drafted regulations mandate clearance of cybersecurity review and other specific actions to be taken by issuers like us, we face uncertainties as to whether these additional procedures can be completed by us timely, or at all, which may subject us to governmental enforcement actions and investigations, fines, penalties or suspension of our non-compliant operations, and materially and adversely affect our business and results of operations and the price of our ADSs. For additional details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Our Business—Our business generates and processes a certain amount of data, and we are required to comply with laws and other applicable laws in mainland China relating to privacy and cybersecurity. The improper use or disclosure of data could have a material and adverse effect on our business and prospects.”

4

In addition, on February 17, 2023, the China Securities Regulatory Commission, or the CSRC, promulgated the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies and five supporting guidelines, which took effect from March 31, 2023, requiring Chinese domestic companies’ overseas offerings and listings of equity securities be filed with the CSRC. These measures clarify the scope of overseas offerings and listings by Chinese domestic companies which are subject to the filing and reporting requirements thereunder, and provide, among other things, that Chinese domestic companies that have already directly or indirectly offered and listed securities in overseas markets prior to the effectiveness of these measures shall fulfill their filing obligations and report required information to the CSRC within three working days after conducting a follow-on securities offering, and follow the reporting requirements within three working days upon the occurrence and public disclosure of any specified circumstances including (i) change of control; (ii) investigations or sanctions imposed by overseas securities regulatory agencies or other competent authorities; (iii) change of listing status or transfer of listing segment; and (iv) voluntary or mandatory delisting. In addition, where there is any material change in the main business of an issuer after its overseas offering and listing beyond the scope of business stated in the filing documents, such issuer shall follow the reporting requirements within three working days after occurrence of the changes. In connection with our delisting in March 2024 from the New York Stock Exchange (see “Item 4. Information on the Company—A. History and Development of the Company”), or the NYSE, we have completed our reporting procedures with the CSRC as required by the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies. Uncertainties still exist regarding the interpretation, implementation and enforcement of the measures under the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies and its supporting guidelines. Any future offerings or equivalent activities we conduct may be subject to the filing and reporting requirements under these measures. We cannot assure you that we will be able to complete the required filings or other regulatory procedures in a timely manner, or at all, in connection with our future overseas offering or listing activities. We also cannot guarantee that new rules or regulations promulgated in the future will not impose any additional requirement on us or otherwise tighten the regulations on mainland China companies seeking overseas offering or listing. If we fail to complete the filing or other required procedures for any future offshore offering or listing or equivalent activities, the operations of the VIEs and our subsidiaries in mainland China may face penalties by the CSRC or other regulatory authorities in mainland China, which may include a warning and a fine between RMB1 million to RMB10 million, which could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our ADSs. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The filing with the CSRC or other requirements from the CSRC or other government authorities in mainland China may be required in connection with our offshore offerings under mainland China law, and, if required, we cannot predict whether or for how long we will be able to complete such filing or other required procedures.”

Furthermore, the mainland China regulators have promulgated new anti-monopoly and competition laws and regulations and strengthened the enforcement under these laws and regulations. There remain uncertainties as to whether these laws, regulations and guidelines will have a material impact on our business, financial condition, results of operations and prospects. We cannot assure you that our business operations comply with such regulations and authorities’ requirements in all respects. If any non-compliance is raised by the authorities and determined against us, we may be subject to fines and other penalties.

Risks and uncertainties arising from the legal system in mainland China, including the above-mentioned risks and uncertainties regarding the enforcement of laws and evolving rules and regulations in mainland China, could result in a material adverse change in our operations and the value of our ADSs. For more details, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Changes and developments in the PRC legal system and the interpretation and enforcement of PRC laws, rules and regulations may subject us to uncertainties.”

These risks, if materialized, could result in a material adverse change in our operations and the value of our ADSs, significantly limit or completely hinder our ability to continue to offer securities to investors, or cause the value of such securities to significantly decline or be worthless. For a detailed description of risks related to doing business in China, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

5

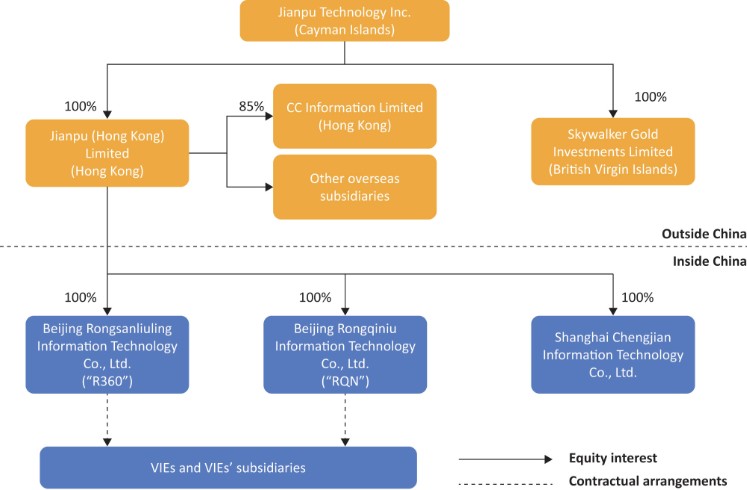

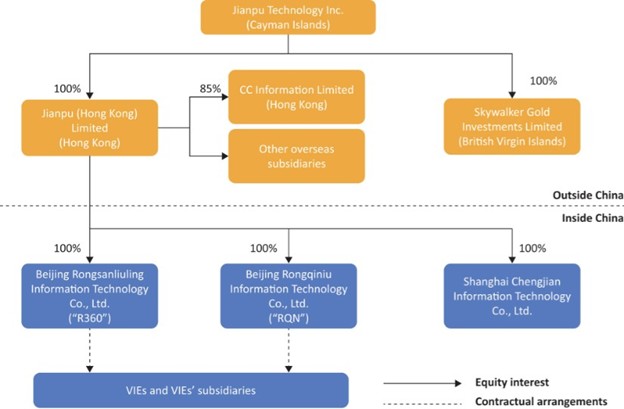

The following diagram illustrates the principal entities in our corporate structure as of the date of this annual report:

Note:

| (1) | The VIEs include RDD, KTN, GKZX and TCT. Shareholders of RDD and their respective shareholdings in RDD and relationship with our company are (i) Jiayan Lu (40%), our director and co-founder; (ii) Huijing Ye (40%), family member of one of our co-founders; and (iii) Caofeng Liu (20%), our director, chief technology officer and co-founder. Shareholders of KTN and their respective shareholdings in KTN and relationship with our company are (i) Hui Li (60%), our employee; and (ii) Yang Liu (40%), our employee. Shareholders of GKZX and their respective shareholdings in GKZX and relationship with our company are (i) Xiang Zhu (5%), our employee; and (ii) Deyou Zhou (95%), our employee. The shareholding structure of GKZX was updated in both 2021 and 2022. Concurrently with each completion of equity transfer in GKZX, the previous contractual arrangements we entered into with GKZX’s then previous shareholders that provided us with effective control over GKZX were terminated and a new set of contractual arrangements with the same terms were entered into with GKZX’s then current shareholders. Shareholders of TCT and their respective shareholdings in TCT and relationship with our company are (i) Xiaoqing Hu (51%), our employee; and (ii) Yuexuan Gao (49%), our employee. The VIEs’ major subsidiary includes RDD’s subsidiary, Shanghai Anguo Insurance Brokerage Co., Ltd. |

6

Permissions Required from the Mainland China Authorities for Our Operations and the Operations of the VIEs and Securities Issuances to Foreign Investors

Due to the restriction of foreign investment in providing value-added telecommunication services in mainland China, including internet information provision services, we rely on the contractual arrangements with RDD, one of the VIEs, to provide such services. RDD has obtained a value-added telecommunication services license for internet information services, known as an ICP License, issued by the Beijing Telecommunication Administration in July 2017. Any challenge to the validity of these arrangements may significantly disrupt our business, subject us to sanctions including revoking the business licenses and/or ICP License or other operating licenses of such entities, compromise enforceability of our contractual arrangements, or have other adverse effects on us. See “Item 3. Key Information—D. Risk Factors—Risks Related to Our Corporate Structure—If the mainland China government deems that our contractual arrangements with the VIEs do not comply with mainland China regulatory restrictions on foreign investment in relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations.”

In addition, we operate insurance brokerage business through Shanghai Anguo Insurance Brokerage Co., Ltd., which holds an insurance brokerage business license. The insurance brokerage business is a highly regulated industry in mainland China, and the National Financial Regulatory Administration has extensive authority to supervise and regulate the insurance industry in mainland China and has been enhancing its supervision over this industry in recent years. New laws, regulations and regulatory requirements have been promulgated and implemented from time to time in this industry. If any non-compliance incidents in our insurance brokerage business operation are identified, we may be required to take certain rectification measures in accordance with applicable laws and regulations, or we may be subject to other administrative penalties. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We may be adversely affected by the complexity and changes in mainland China’s regulation of internet-related businesses and companies and other businesses we and the VIEs are or will be engaged in.”

Furthermore, for issuances of securities to foreign investors, under the laws, regulations and regulatory rules in mainland China, as of the date of this annual report, we (i) have not received any requirement from competent governmental authorities in mainland China to obtain permissions from the CSRC, (ii) have not received any requirement from competent governmental authorities in mainland China to go through cybersecurity review by the Cyberspace Administration of China, and (iii) have not received or were denied such requisite permissions by any mainland China authority. Meanwhile, the mainland China government has indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers.

There are uncertainties with respect to how the mainland China government will regulate foreign investment in providing value-added telecommunication services in mainland China, insurance brokerage business operation and overseas securities offerings and listings in general, as well as the interpretation and implementation of any related regulations. If we, our subsidiaries in mainland China or the VIEs (i) do not receive or maintain required permissions or approvals or do not complete required filings, (ii) inadvertently conclude that such permissions, approvals or filings are not required, or (iii) are required to obtain or fulfill such permissions, approvals or filings in the future when applicable laws, regulations or interpretations change but we fail to obtain or fulfill such necessary approvals, permits or filings in a timely manner, or at all, we may be subject to penalties, including fines, suspension of business and revocation of required licenses, our ability to continue to offer securities to investors may also be significantly limited or completely hindered, and the value of our securities may significantly decline or become worthless. For more detailed information, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The filing with the CSRC or other requirements from the CSRC or other government authorities in mainland China may be required in connection with our offshore offerings under mainland China law, and, if required, we cannot predict whether or for how long we will be able to complete such filing or other required procedures.”

7

The Holding Foreign Companies Accountable Act

Pursuant to the Holding Foreign Companies Accountable Act, as amended by the Consolidated Appropriations Act, 2023, or the HFCAA, if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspections by the Public Company Accounting Oversight Board, or the PCAOB, for two consecutive years, the SEC will prohibit our shares or the ADSs from being traded on a national securities exchange or in the over-the-counter trading market in the United States. On December 16, 2021, the PCAOB issued a report to notify the SEC of its determination that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong, including our auditor. In May 2022, the SEC conclusively listed us as a Commission-Identified Issuer under the HFCAA following the filing of our annual report on Form 20-F for the fiscal year ended December 31, 2021. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. As of the date of this annual report, the PCAOB has not issued any new determination that it is unable to inspect or investigate completely registered public accounting firms headquartered in any jurisdiction. For this reason, we do not expect to be so identified after we file this annual report on Form 20-F for the fiscal year ended December 31, 2023. On December 29, 2022, the Consolidated Appropriations Act, 2023, was signed into law, which amended the HFCAA (i) to reduce the number of consecutive non-inspection years required for triggering the prohibitions under the HFCAA from three years to two, and (ii) so that any foreign jurisdiction could be the reason why the PCAOB does not have complete access to inspect or investigate a company’s auditor. As it was originally enacted, the HFCAA applied only if the PCAOB’s inability to inspect or investigate was due to a position taken by an authority in the foreign jurisdiction where the relevant public accounting firm is located. As a result of the Consolidated Appropriations Act, 2023, the HFCAA now also applies if the PCAOB’s inability to inspect or investigate the relevant accounting firm is due to a position taken by an authority in any foreign jurisdiction. The denying jurisdiction does not need to be where the accounting firm is located. Each year, the PCAOB will determine whether it can inspect and investigate completely audit firms in mainland China and Hong Kong, among other jurisdictions. If the PCAOB determines in the future that it no longer has full access to inspect and investigate completely accounting firms in mainland China and Hong Kong and we continue to use an accounting firm headquartered in one of these jurisdictions to issue an audit report on our financial statements filed with the SEC, we would be identified as a Commission-Identified Issuer following the filing of the annual report on Form 20-F for the relevant fiscal year. Furthermore, whether the PCAOB will continue to conduct inspections and investigations completely to its satisfaction of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainty and depends on a number of factors out of our, and our auditor’s, control, including positions taken by authorities of the PRC or any other foreign jurisdiction. If authorities in the PRC or another foreign jurisdiction were to take a position at any time in the future that would prevent the PCAOB from continuing to inspect or investigate completely registered public accounting firms headquartered in mainland China or Hong Kong, and if such lack of inspection were to extend for the requisite period of time under the HFCAA, our securities will be prohibited from being traded on U.S. markets. There can be no assurance that we would not be identified as a Commission-Identified Issuer for any future fiscal year, and if we were so identified for two consecutive years, we would become subject to the prohibition on trading under the HFCAA. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—The PCAOB had historically been unable to inspect our auditor in relation to their audit work performed for our financial statements and the inability of the PCAOB to conduct inspections of our auditor in the past has deprived our investors with the benefits of such inspections” and “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—Our ADSs may be prohibited from trading in the United States under the HFCAA in the future if the PCAOB is unable to inspect or investigate completely auditors located in China. The prohibition of trading in the ADSs, or the threat of the trading being prohibited, may materially and adversely affect the value of your investment.”

Cash Flows through Our Organization

Jianpu Technology Inc. is a holding company with no material operations of its own. We conduct our operations in China primarily through our subsidiaries in mainland China and the VIEs. As a result, although other means are available for us to obtain financing at the holding company level, Jianpu Technology Inc.’s ability to pay dividends to the shareholders and to service any debt it may incur depend upon dividends paid by our subsidiaries in mainland China and service fees paid by the VIEs. If our existing subsidiaries in mainland China or any newly formed ones incur debt on their own behalf in the future, the instruments governing their debt may restrict their ability to pay dividends to Jianpu Technology Inc. In addition, our wholly foreign-owned subsidiaries in China are permitted to pay dividends to Jianpu Technology Inc. only out of their retained earnings, if any, as determined in accordance with the accounting standards and regulations in mainland China. Further, our subsidiaries in mainland China and the VIEs are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. For more details, see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Holding Company Structure.”

8

Under laws and regulations in mainland China, our subsidiaries in mainland China and the VIEs are subject to certain restrictions with respect to paying dividends or otherwise transferring any of their net assets to us. Remittance of dividends by a wholly foreign-owned enterprise out of China is also subject to examination by the banks designated by State Administration of Foreign Exchange, or the SAFE. The amounts restricted include the paid-up capital and the statutory reserve funds of our subsidiaries in mainland China and the net assets of the VIEs in which we have no legal ownership, totaling RMB133.3 million, RMB142.3 million and RMB73.6 million (US$10.4 million) as of December 31, 2021, 2022 and 2023, respectively. For risks relating to the fund flows of our operations in China, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We may rely on dividends and other distributions on equity paid by our subsidiaries in mainland China to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries in mainland China to make payments to us could have a material and adverse effect on our ability to conduct our business.”

Under mainland China law, Jianpu Technology Inc. may provide funding to our subsidiaries in mainland China only through capital contributions or loans, and to the VIEs only through loans, subject to satisfaction of applicable government registration and approval requirements. For risks relating to the fund flows of our operations in China, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China—We may rely on dividends and other distributions on equity paid by our subsidiaries in mainland China to fund any cash and financing requirements we may have, and any limitation on the ability of our subsidiaries in mainland China to make payments to us could have a material and adverse effect on our ability to conduct our business.”

In the years ended December 31, 2021, 2022 and 2023, Jianpu Technology Inc. extended loans with outstanding principal amount of nil, RMB40.4 million and RMB14.5 million (US$2.0 million), respectively, to our intermediate holding companies and subsidiaries, and received repayments of RMB25.1 million, RMB51.9 million and RMB9.6 million (US$1.4 million), respectively. In the years ended December 31, 2021, 2022 and 2023, the VIEs received RMB1.0 million, nil and nil, respectively, as capital investment (in the form of loans extended to nominee shareholders from our subsidiaries in mainland China) or as loans from our subsidiaries in mainland China. The VIEs may transfer cash to our subsidiaries in mainland China by paying service fees according to the contractual arrangements. For the years ended December 31, 2021, 2022 and 2023, no service fees were paid by the VIEs to our subsidiaries in mainland China.

Jianpu Technology Inc. has not declared or paid any cash dividends, nor has any present plan to pay any cash dividends on our ordinary shares in the foreseeable future. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business. See “Item 8. Financial Information—A. Consolidated Statements and Other Financial Information-Dividend Policy.” For the Cayman Islands, mainland China and United States federal income tax considerations of an investment in our ADSs, see “Item 10. Additional Information—E. Taxation.”

For purposes of illustration, the following discussion reflects the hypothetical taxes that might be required to be paid within mainland China, assuming that: (i) we have taxable earnings, and (ii) we determine to pay a dividend in the future:

| Tax calculation (1) |

| |

Hypothetical pre-tax earnings(2) |

| 100 | % |

Tax on earnings at statutory rate of 25%(3) |

| (25) | % |

Net earnings available for distribution |

| 75 | % |

Withholding tax at standard rate of 10%(4) |

| (7.5) | % |

Net distribution to Parent/Shareholders |

| 67.5 | % |

Notes:

(1) | For purposes of this example, the tax calculation has been simplified. The hypothetical book pre-tax earnings amount, not considering timing differences, is assumed to equal taxable income in mainland China. |

9

(2) | Under the terms of the contractual arrangements with the VIEs, our subsidiaries in mainland China may charge the VIEs for services provided to the VIEs. These service fees shall be recognized as expenses of the VIEs, with a corresponding amount as service income by our subsidiaries in mainland China and eliminate in consolidation. For income tax purposes, our subsidiaries and the VIEs in mainland China file income tax returns on a separate company basis. The service fees paid are recognized as a tax deduction by the VIEs and as income by our subsidiaries in mainland China and are tax neutral. |

(3) | Certain of our subsidiaries qualify for a 15% preferential income tax rate in mainland China. However, such rate is subject to qualification, is temporary in nature, and may not be available in a future period when distributions are paid. For purposes of this hypothetical example, the table above reflects a maximum tax scenario under which the full statutory rate would be effective. |

(4) | The PRC Enterprise Income Tax Law imposes a withholding income tax of 10% on dividends distributed by a foreign invested enterprise, or FIE, to its immediate holding company outside of mainland China. A lower withholding income tax rate of 5% is applied if the FIE’s immediate holding company is registered in Hong Kong or other jurisdictions that have a tax treaty arrangement with mainland China, subject to a qualification review at the time of the distribution. For purposes of this hypothetical example, the table above assumes a maximum tax scenario under which the full withholding tax would be applied. |

The table above has been prepared under the assumption that all profits of the VIEs will be distributed as fees to our subsidiaries in mainland China under tax neutral contractual arrangements. If, in the future, the accumulated earnings of the VIEs exceed the service fees paid to our subsidiaries in mainland China (or if the current and contemplated fee structure between the intercompany entities is determined to be non-substantive and disallowed by Chinese tax authorities), the VIEs could make a non-deductible transfer to our subsidiaries in mainland China for the amounts of the stranded cash in the VIEs. This would result in such transfer being non-deductible expenses for the VIEs but still taxable income for the subsidiaries in mainland China. Such a transfer and the related tax burdens would reduce our after-tax income to approximately 50.6% of the pre-tax income. Our management believes that there is only a remote possibility that this scenario would happen.

10

Financial Information Related to the VIEs

The following table presents the condensed consolidating schedule of financial position for Jianpu Technology Inc., its wholly-owned subsidiaries, or the WFOEs, that are the primary beneficiaries of the VIEs under U.S. GAAP, or the Primary Beneficiaries of VIEs, its other subsidiaries that are not the Primary Beneficiaries of the VIEs, or the Other Subsidiaries, and the VIEs and their subsidiaries that we consolidate as of the dates presented.

As of December 31, 2023 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Consolidating Schedule of Financial Position |

|

|

|

|

|

|

|

|

|

|

|

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

Current assets: |

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

| 4,681 |

| 244,201 |

| 65,413 |

| 30,274 |

| — |

| 344,569 |

Time deposits |

| — |

| 31,949 |

| — |

| — |

| — |

| 31,949 |

Restricted cash and time deposits |

| — |

| 278,359 |

| — |

| — |

| — |

| 278,359 |

Accounts receivable, net |

| — |

| 71,064 |

| 37,894 |

| 52,863 |

| — |

| 161,821 |

Amount due from related parties |

| 13,488 |

| (44,090) |

| — |

| 30,757 |

| — |

| 155 |

Amount due from subsidiaries and VIEs(1) |

| — |

| 67,309 |

| 64,110 |

| 6,895 |

| (138,314) |

| — |

Prepayments and other current assets |

| 2,094 |

| 10,575 |

| 14,305 |

| 13,235 |

| — |

| 40,209 |

Total current assets |

| 20,263 |

| 659,367 |

| 181,722 |

| 134,024 |

| (138,314) |

| 857,062 |

Non-current assets: |

|

|

|

|

|

| ||||||

Property and equipment, net |

| — |

| 163 |

| 2,239 |

| 9,345 |

| — |

| 11,747 |

Intangible assets, net |

| 1,485 |

| 2,782 |

| 262 |

| 12,633 |

| — |

| 17,162 |

Restricted cash and time deposits |

| 26,042 |

| — |

| — |

| 8,804 |

| — |

| 34,846 |

Amount due from subsidiaries and VIEs(1) |

| 1,371,941 |

| — |

| 39,906 |

| — |

| (1,411,847) |

| — |

Other non-current assets |

| — |

| 7,960 |

| 1,340 |

| 1,684 |

| — |

| 10,984 |

Total non-current assets |

| 1,399,468 |

| 10,905 |

| 43,747 |

| 32,466 |

| (1,411,847) |

| 74,739 |

Total assets |

| 1,419,731 |

| 670,272 |

| 225,469 |

| 166,490 |

| (1,550,161) |

| 931,801 |

|

|

|

|

|

|

|

|

|

|

| ||

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

| |

Current liabilities: |

|

|

|

|

|

|

|

|

|

|

|

|

Short-term borrowings |

| — |

| 95,081 |

| 141,131 |

| — |

| — |

| 236,212 |

Accounts payable |

| 418 |

| 19,000 |

| 64,788 |

| 22,255 |

| — |

| 106,461 |

Advances from customers |

| — |

| 817 |

| 43,727 |

| 1,598 |

| — |

| 46,142 |

Tax payable |

| — |

| 198 |

| 2,178 |

| 7,928 |

| — |

| 10,304 |

Amount due to related parties |

| — |

| — |

| 10,623 |

| — |

| — |

| 10,623 |

Amount due to subsidiaries(1) |

| — |

| 6,895 |

| 3,527 |

| 127,892 |

| (138,314) |

| — |

Deficit in subsidiaries(2) |

| 943,614 |

| 113,950 |

| 225 |

| — |

| (1,057,789) |

| — |

Deficit in VIEs(3) |

| — |

| — |

| 4,735 |

| — |

| (4,735) |

| — |

Accrued expenses and other current liabilities |

| 7,341 |

| 5,266 |

| 68,710 |

| 8,224 |

| — |

| 89,541 |

Total current liabilities |

| 951,373 |

| 241,207 |

| 339,644 |

| 167,897 |

| (1,200,838) |

| 499,283 |

Non-current liabilities: |

|

|

|

|

|

| ||||||

Deferred tax liabilities |

| — |

| 209 |

| — |

| 3,196 |

| — |

| 3,405 |

Amount due to subsidiaries(1) |

| 39,906 |

| 1,371,941 |

| — |

| — |

| (1,411,847) |

| — |

Other non-current liabilities |

| 11,551 |

| — |

| — |

| 132 |

| — |

| 11,683 |

Total non-current liabilities |

| 51,457 |

| 1,372,150 |

| — |

| 3,328 |

| (1,411,847) |

| 15,088 |

Total liabilities |

| 1,002,830 |

| 1,613,357 |

| 339,644 |

| 171,225 |

| (2,612,685) |

| 514,371 |

Total Jianpu’s shareholders’ equity/(deficit) |

| 416,901 |

| (943,614) |

| (114,175) |

| (4,735) |

| 1,062,524 |

| 416,901 |

Non-controlling interests |

| — |

| 529 |

| — |

| — |

| — |

| 529 |

Total shareholders’ equity/(deficit) |

| 416,901 |

| (943,085) |

| (114,175) |

| (4,735) |

| 1,062,524 |

| 417,430 |

Total liabilities and shareholders’ equity/(deficit) |

| 1,419,731 |

| 670,272 |

| 225,469 |

| 166,490 |

| (1,550,161) |

| 931,801 |

11

| ||||||||||||

As of December 31, 2022 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Consolidating Schedule of Financial Position |

|

|

|

| ||||||||

ASSETS |

|

|

|

|

|

|

|

| ||||

Current assets: |

|

|

|

|

|

|

|

| ||||

Cash and cash equivalents |

| 19,518 |

| 269,148 | 24,332 | 33,541 |

| — |

| 346,539 | ||

Restricted cash and time deposits |

| — |

| 297,634 | — | — |

| — |

| 297,634 | ||

Accounts receivable, net |

| — |

| 120,287 | 24,967 | 44,411 |

| — |

| 189,665 | ||

Amount due from related parties |

| 13,818 |

| (41,368) | — | 27,703 |

| — |

| 153 | ||

Amount due from subsidiaries and VIEs(1) |

| — |

| 34,685 | 99,638 | 6,895 |

| (141,218) | — | |||

Prepayments and other current assets |

| 1,629 |

| 18,823 | 14,697 | 11,388 |

| — | 46,537 | |||

Total current assets |

| 34,965 |

| 699,209 | 163,634 | 123,938 |

| (141,218) |

| 880,528 | ||

Non-current assets: |

|

|

|

|

|

|

|

| ||||

Property and equipment, net |

| — |

| 227 | 2,323 | 10,028 |

| — |

| 12,578 | ||

Intangible assets, net |

| 1,460 |

| 2,640 | 454 | 13,785 |

| — |

| 18,339 | ||

Restricted cash and time deposits |

| 25,879 |

| — | 9,180 | 5,000 |

| — |

| 40,059 | ||

Amount due from subsidiaries and VIEs(1) | 1,347,219 | — | 39,906 | — | (1,387,125) | — | ||||||

Other non-current assets |

| — |

| 5,866 | 930 | 3,962 |

| — |

| 10,758 | ||

Total non-current assets |

| 1,374,558 |

| 8,733 | 52,793 | 32,775 |

| (1,387,125) |

| 81,734 | ||

Total assets |

| 1,409,523 |

| 707,942 | 216,427 | 156,713 |

| (1,528,343) |

| 962,262 | ||

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

| ||||

Current liabilities: |

|

|

|

|

|

|

|

| ||||

Short-term borrowings |

| — |

| 85,556 | 167,925 | — |

| — |

| 253,481 | ||

Accounts payable |

| 606 |

| 22,466 | 54,221 | 19,436 |

| — |

| 96,729 | ||

Advances from customers |

| — |

| 2,505 | 42,850 | 1,565 |

| — |

| 46,920 | ||

Tax payable |

| — |

| 475 | 717 | 8,470 |

| — |

| 9,662 | ||

Amount due to related parties |

| — |

| — | 12,828 | 706 |

| — |

| 13,534 | ||

Amount due to subsidiaries(1) |

| — |

| 6,895 | 3,527 | 130,796 |

| (141,218) | — | |||

Deficit/(investment) in subsidiaries(2) |

| 924,085 |

| 131,707 | (6,413) | — |

| (1,049,379) | — | |||

Deficit in VIEs(3) | — | — | 14,613 | — | (14,613) | — | ||||||

Accrued expenses and other current liabilities |

| 2,742 |

| 28,532 | 51,453 | 6,144 |

| — |

| 88,871 | ||

Total current liabilities |

| 927,433 |

| 278,136 | 341,721 | 167,117 |

| (1,205,210) |

| 509,197 | ||

Non-current liabilities: |

|

|

|

|

|

|

|

| ||||

Deferred tax liabilities |

| — |

| 215 | — | 3,429 |

| — |

| 3,644 | ||

Amount due to subsidiaries(1) | 39,906 | 1,347,219 | — | — | (1,387,125) | — | ||||||

Other non-current liabilities |

| 12,316 |

| — | — | 780 |

| — |

| 13,096 | ||

Total non-current liabilities |

| 52,222 |

| 1,347,434 | — | 4,209 |

| (1,387,125) |

| 16,740 | ||

Total liabilities |

| 979,655 |

| 1,625,570 | 341,721 | 171,326 |

| (2,592,335) |

| 525,937 | ||

Total Jianpu’s shareholders’ equity/(deficit) |

| 429,868 |

| (924,085) | (125,294) | (14,613) |

| 1,063,992 | 429,868 | |||

Non-controlling interests |

| — |

| 6,457 | — | — |

| — |

| 6,457 | ||

Total shareholders’ equity/(deficit) |

| 429,868 |

| (917,628) | (125,294) | (14,613) |

| 1,063,992 |

| 436,325 | ||

Total liabilities and shareholders’ equity/(deficit) |

| 1,409,523 |

| 707,942 | 216,427 | 156,713 |

| (1,528,343) |

| 962,262 | ||

12

The following tables present the condensed consolidating schedules of results of operations and cash flows for Jianpu Technology Inc., the Primary Beneficiaries of VIEs, the Other Subsidiaries, and the VIEs and their subsidiaries that we consolidate as of the dates presented.

For the Year Ended December 31, 2023 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Condensed Consolidating Schedule of Results of Operations | ||||||||||||

Third-party revenues |

| — |

| 393,107 |

| 436,207 |

| 240,099 |

| — |

| 1,069,413 |

Inter-company revenues(4) |

| — |

| 29,223 |

| 117,054 |

| 224,919 |

| (371,196) |

| — |

Third-party costs and expenses |

| (18,610) |

| (241,293) |

| (439,533) |

| (422,502) |

| — |

| (1,121,938) |

Inter-company costs and expenses(5) |

| — |

| (204,367) |

| (133,639) |

| (33,190) |

| 371,196 |

| — |

Income/(Loss) from subsidiaries(6) |

| (9,819) |

| 766 |

| (97) |

| — |

| 9,150 |

| — |

Income from VIEs(7) |

| — |

| — |

| 9,762 |

| — |

| (9,762) |

| — |

Others |

| 1,657 |

| 12,675 |

| 10,915 |

| 204 |

| — |

| 25,451 |

Income/(Loss) before income tax |

| (26,772) |

| (9,889) |

| 669 |

| 9,530 |

| (612) |

| (27,074) |

Income tax benefits/(expenses) |

| — |

| (204) |

| — |

| 232 |

| — |

| 28 |

Net income/(loss) |

| (26,772) |

| (10,093) |

| 669 |

| 9,762 |

| (612) |

| (27,046) |

Less: net loss attributable to non-controlling interests |

| — |

| (274) |

| — |

| — |

| — |

| (274) |

Net income/(loss) attributable to Jianpu’s shareholders |

| (26,772) |

| (9,819) |

| 669 |

| 9,762 |

| (612) |

| (26,772) |

For the Year Ended December 31, 2022 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Condensed Consolidating Schedule of Results of Operations | ||||||||||||

Third-party revenues |

| — |

| 493,639 |

| 313,454 |

| 182,582 |

| — |

| 989,675 |

Inter-company revenues(4) |

| — |

| 11,319 |

| 180,074 |

| 262,936 |

| (454,329) |

| — |

Third-party costs and expenses |

| (13,079) |

| (262,163) |

| (417,674) |

| (448,782) |

| — |

| (1,141,698) |

Inter-company costs and expenses(5) |

| — |

| (266,602) |

| (159,449) |

| (28,278) |

| 454,329 |

| — |

Loss from subsidiaries(6) |

| (120,953) |

| (111,373) |

| (10,090) |

| — |

| 242,416 |

| — |

Loss from VIEs(7) |

| — |

| — |

| (26,084) |

| — |

| 26,084 |

| — |

Others |

| 9,725 |

| 3,651 |

| (1,694) |

| 5,172 |

| — |

| 16,854 |

Loss before income tax |

| (124,307) |

| (131,529) |

| (121,463) |

| (26,370) |

| 268,500 |

| (135,169) |

Income tax benefits |

| — |

| 632 |

| — |

| 286 |

| — |

| 918 |

Net loss |

| (124,307) |

| (130,897) |

| (121,463) |

| (26,084) |

| 268,500 |

| (134,251) |

Less: net loss attributable to non-controlling interests |

| — |

| (9,944) |

| — |

| — |

| — |

| (9,944) |

Total comprehensive loss attributable to Jianpu Technology Inc. | (124,307) | (120,953) | (121,463) | (26,084) | 268,500 | (124,307) | ||||||

Accretion of mezzanine equity | — | (7,353) | — | — | — | (7,353) | ||||||

Net loss attributable to Jianpu’s shareholders |

| (124,307) |

| (128,306) |

| (121,463) |

| (26,084) |

| 268,500 |

| (131,660) |

13

For the Year Ended December 31, 2021 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Condensed Consolidating Schedule of Results of Operations | ||||||||||||

Third-party revenues |

| — |

| 406,082 |

| 253,427 |

| 145,538 |

| — |

| 805,047 |

Inter-company revenues(4) |

| — |

| 15,560 |

| 285,740 |

| 266,617 |

| (567,917) |

| — |

Third-party costs and expenses |

| (22,424) |

| (196,934) |

| (401,197) |

| (442,995) |

| — |

| (1,063,550) |

Inter-company costs and expenses(5) |

| — |

| (268,058) |

| (266,617) |

| (33,242) |

| 567,917 |

| — |

Loss from subsidiaries(6) |

| (178,242) |

| (193,920) |

| (3,813) |

| — |

| 375,975 |

| — |

Loss from VIEs(7) |

| — |

| — |

| (62,494) |

| — |

| 62,494 |

| — |

Others |

| 881 |

| 54,422 |

| (2,779) |

| 1,303 |

| — |

| 53,827 |

Loss before income tax |

| (199,785) |

| (182,848) |

| (197,733) |

| (62,779) |

| 438,469 |

| (204,676) |

Income tax benefits |

| — |

| 297 |

| — |

| 285 |

| — |

| 582 |

Net loss |

| (199,785) |

| (182,551) |

| (197,733) |

| (62,494) |

| 438,469 |

| (204,094) |

Less: net loss attributable to non-controlling interests |

| — |

| (4,309) |

| — |

| — |

| — |

| (4,309) |

Net loss attributable to Jianpu’s shareholders |

| (199,785) |

| (178,242) |

| (197,733) |

| (62,494) |

| 438,469 |

| (199,785) |

For the Year Ended December 31, 2023 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Condensed Consolidating Schedules of Cash Flows |

|

|

|

|

|

|

|

|

|

|

|

|

Net cash (used in)/provided by operating activities carried outside our group |

| (10,204) |

| 274,295 |

| 54,140 |

| (313,965) |

| — |

| 4,266 |

Net cash (used in)/provided by operating activities carried within our group(8) |

| — |

| (295,920) |

| (18,582) |

| 314,502 |

| — |

| — |

Net cash (used in)/ provided by operating activities |

| (10,204) |

| (21,625) |

| 35,558 |

| 537 |

| — |

| 4,266 |

Purchases of intangible assets, property and equipment |

| — |

| — |

| (2,057) |

| — |

| — |

| (2,057) |

Proceeds from sale of property and equipment |

| — |

| 1,737 |

| 13 |

| — |

| — |

| 1,750 |

Cash paid for long-term investments |

| — |

| (2,524) |

| — |

| — |

| — |

| (2,524) |

Cash net flow from deconsolidations of subsidiaries, net of cash disposed |

| — |

| (6,222) |

| 18,000 |

| — |

| — |

| 11,778 |

Purchase of restricted time deposits | (1,340) | (7,676) | — | (1,000) | — | (10,016) | ||||||

Withdrawal of restricted time deposits | 1,637 | — | — | — | — | 1,637 | ||||||

Loans repaid from other subsidiaries(9) |

| 9,582 |

| — |

| — |

| — |

| (9,582) |

| — |

Investments and loans extended to subsidiaries and VIEs(10) |

| (14,534) |

| (6,940) |

| — |

| — |

| 21,474 |

| — |

Net cash (used in)/provided by investing activities |

| (4,655) |

| (21,625) |

| 15,956 |

| (1,000) |

| 11,892 |

| 568 |

Receipt of loans extended by owner(11) |

| — |

| 14,534 |

| — |

| — |

| (14,534) |

| — |

Repayment of loans extended to owner(9) |

| — |

| (9,582) |

| — |

| — |

| 9,582 |

| — |

Receipt as investment or capital increase(12) |

| — |

| — |

| 6,940 |

| — |

| (6,940) |

| — |

Proceeds from employees exercising stock options |

| 33 |

| — |

| — |

| — |

| — |

| 33 |

Proceeds from short-term borrowings |

| — |

| 95,081 |

| 160,931 |

| — |

| — |

| 256,012 |

Repayment of short-term borrowings |

| — |

| (85,556) |

| (187,725) |

| — |

| — |

| (273,281) |

Net cash (used in)/provided by financing activities |

| 33 |

| 14,477 |

| (19,854) |

| — |

| (11,892) |

| (17,236) |

14

For the Year Ended December 31, 2022 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Condensed Consolidating Schedules of Cash Flows | ||||||||||||

Net cash (used in)/ provided by operating activities carried outside our group |

| (14,635) |

| 240,009 |

| 45,420 |

| (425,389) |

| — |

| (154,595) |

Net cash (used in)/provided by operating activities carried within our group(8) |

| — |

| (314,725) |

| (128,240) |

| 442,965 |

| — |

| — |

Net cash (used in)/ provided by operating activities |

| (14,635) |

| (74,716) |

| (82,820) |

| 17,576 |

| — |

| (154,595) |

Proceeds from maturity of short-term investments |

| — |

| 32,101 |

| — |

| — |

| — |

| 32,101 |

Purchases of short-term investments |

| — |

| (30,000) |

| — |

| — |

| — |

| (30,000) |

Purchases of intangible assets, property and equipment |

| — |

| (212) |

| (1,594) |

| — |

| — |

| (1,806) |

Proceeds from sale of property and equipment |

| — |

| 53 |

| 138 |

| — |

| — |

| 191 |

Purchase of restricted time deposits |

| — |

| (45,486) |

| — |

| — |

| — |

| (45,486) |

Loans repaid from other subsidiaries(9) |

| 51,919 |

| — |

| — |

| — |

| (51,919) |

| — |

Investments and loans extended to subsidiaries and VIEs(10) |

| (40,362) |

| (59,808) |

| — |

| — |

| 100,170 |

| — |

Cash net flow from deconsolidations of subsidiaries, net of cash disposed | 19,005 | (30,453) | 16,996 | (474) | — | 5,074 | ||||||

Net cash provided by/(used in) investing activities |

| 30,562 |

| (133,805) |

| 15,540 |

| (474) |

| 48,251 |

| (39,926) |

Receipt of loans extended by owner(11) |

| — |

| 40,362 |

| — |

| — |

| (40,362) |

| — |

Repayment of loans extended to owner(9) |

| — |

| (51,919) |

| — |

| — |

| 51,919 |

| — |

Receipt as investment or capital increase(12) |

| — |

| — |

| 59,808 |

| — |

| (59,808) |

| — |

Proceeds from employees exercising stock options |

| 143 |

| — |

| — |

| — |

| — |

| 143 |

Proceeds from short-term borrowings |

| — |

| 85,556 |

| 167,925 |

| — |

| — |

| 253,481 |

Repayment of short-term borrowings |

| — |

| — |

| (181,853) |

| — |

| — |

| (181,853) |

Purchase of additional shares held by noncontrolling interests shareholder |

| — |

| (8,702) |

| — |

| — |

| — |

| (8,702) |

Net cash provided by financing activities |

| 143 |

| 65,297 |

| 45,880 |

| — |

| (48,251) |

| 63,069 |

15

For the Year Ended December 31, 2021 | ||||||||||||

Primary | VIEs and | |||||||||||

Other | Beneficiaries | their | Eliminating | Consolidated | ||||||||

| Parent |

| subsidiaries |

| of VIEs |

| subsidiaries |

| adjustments |

| Totals | |

in RMB thousands | ||||||||||||

Condensed Consolidating Schedules of Cash Flows |

|

|

|

|

|

|

|

|

|

|

|

|

Net cash (used in)/provided by operating activities carried outside our group |

| (28,745) |

| 233,884 |

| (43,497) |

| (456,230) |

| — |

| (294,588) |

Net cash (used in)/provided by operating activities carried within our group(8) |

| — |

| (287,666) |

| (142,663) |

| 430,329 |

| — |

| — |

Net cash used in operating activities |

| (28,745) |

| (53,782) |

| (186,160) |

| (25,901) |

| — |

| (294,588) |

Proceeds from maturity of short-term investments and restricted investment |

| — |

| — |

| 153,650 |

| 9,620 |

| — |

| 163,270 |

Purchases of short-term investments and restricted investment |

| — |

| — |

| (169,600) |

| (20) |

| — |

| (169,620) |

Purchases of intangible assets, property and equipment |

| — |

| (212) |

| (2,818) |

| (112) |

| — |

| (3,142) |

Proceeds from sale of property and equipment |

| — |

| 59 |

| 15 |

| 56 |

| — |

| 130 |

Cash paid for long-term investments |

| — |

| (3,000) |

| — |

| — |

| — |

| (3,000) |

Cash received for long-term investments |

| — |

| 59,559 |

| — |

| 1,000 |

| — |

| 60,559 |

Placement of time deposits |

| — |

| — |

| (10,000) |

| — |

| — |

| (10,000) |

Transfer to restricted time deposits |

| — |

| (1,688) |

| — |

| — |

| — |

| (1,688) |

Loans repaid from Other subsidiaries(9) |

| 25,094 |

| — |

| — |

| — |

| (25,094) |

| — |

Investments and loans extended to subsidiaries and VIEs(10) |

| — |

| (65,172) |

| — |

| — |

| 65,172 |

| — |

Net cash provided by/(used in) investing activities |

| 25,094 |

| (10,454) |

| (28,753) |

| 10,544 |

| 40,078 |

| 36,509 |

Receipt of loans extended by owner(11) |

| — |

| — |

| — |

| 1,000 |

| (1,000) |

| — |

Repayment of loans extended to owner (9) |

| — |

| (25,094) |

| — |

| — |

| 25,094 |

| — |

Receipt as investment or capital increase(12) |

| — |

| — |

| 64,172 |

| — |

| (64,172) |

| — |

Proceeds from employees exercising stock options |

| 4 |

| — |

| — |

| — |

| — |

| 4 |

Proceeds from short-term borrowings |

| — |

| — |

| 297,542 |

| — |

| — |

| 297,542 |

Repayment of short-term borrowings |

| — |

| — |

| (274,166) |

| — |

| — |

| (274,166) |

Net cash provided by/(used in) financing activities |

| 4 |

| (25,094) |

| 87,548 |

| 1,000 |

| (40,078) |

| 23,380 |

Notes:

(1) | It represents the elimination of intercompany balances among Jianpu Technology Inc., the Primary Beneficiaries of VIEs, the Other Subsidiaries, and the VIEs and their subsidiaries that we consolidate. |

(2) | It represents the elimination of the deficit or investment among Jianpu Technology Inc., the Primary Beneficiaries of VIEs, the Other Subsidiaries that we consolidate. |

(3) | It represents the elimination of the deficit or investment in the VIEs and their subsidiaries by the Primary Beneficiaries of VIEs. |

(4) | Inter-company revenues of (i) marketing services provided by the VIEs to the Primary Beneficiaries of VIEs and other subsidiaries, and (ii) technical support and personnel outsourcing among VIEs and their subsidiaries, the Primary Beneficiaries of VIEs and other subsidiaries due to infrastructure sharing were eliminated at the consolidated level. |

(5) | Inter-company costs and expenses corresponding to intercompany revenues were eliminated at the consolidated level. |