UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark one)

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended

Or

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from __________ to __________

Commission file number

(Exact name of Registrant as specified in its charter)

|

|

|

|

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Trading Symbol(s) |

|

Name of Each Exchange on Which Registered |

|

|

|

|

|

The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

☒ |

Smaller reporting company |

|

|

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive proxy statement relating to its 2021 annual meeting of stockholders (the “2021 Proxy Statement”) are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. The 2021 Proxy Statement will be filed with the Securities and Exchange Commission (the “SEC”) within 120 days after the end of the fiscal year to which this report relates.

This Annual Report on Form 10-K contains forward-looking statements which are made pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements may be identified by such forward-looking terminology as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology. Our forward-looking statements are based on a series of expectations, assumptions, estimates and projections about our company, are not guarantees of future results or performance and involve substantial risks and uncertainty. We may not actually achieve the plans, intentions or expectations disclosed in these forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in these forward-looking statements. Our business and our forward-looking statements involve substantial known and unknown risks and uncertainties, including the risks and uncertainties inherent in our statements regarding:

| ● | the impacts of COVID-19, or other future pandemics on our business, results of operations, financial position and cash flows; | |

| ● | our ability to effectively manage our growth and maintain and improve our corporate culture; | |

| ● | the potential benefits of and our ability to maintain our relationships with ridesharing companies, and establish or maintain future collaborations or strategic relationships or obtain additional funding; | |

| ● | our marketing capabilities and strategy; | |

| ● |

our ability to maintain a cost-effective insurance program; |

|

| ● | our industry is in early stages of growth | |

| ● | our anticipated investments in new products and offerings, and the effect of these investments on our results of operations; | |

| ● | our ability to retain the continued service of our key professionals and to identify, hire and retain additional qualified professionals; | |

| ● | our competitive position, and developments and projections relating to our competitors and our industry; | |

| ● | our estimates regarding expenses, future revenue, capital requirements and needs for additional financing; and | |

| ● | our ability to comply with existing, modified, or new laws and regulations applying to our business. |

All of our forward-looking statements are as of the date of this Annual Report on Form 10-K only. In each case, actual results may differ materially from such forward-looking information. We can give no assurance that such expectations or forward-looking statements will prove to be correct. An occurrence of, or any material adverse change in, one or more of the risk factors or risks and uncertainties referred to in this Annual Report on Form 10-K or included in our other public disclosures or our other periodic reports or other documents or filings filed with or furnished to the SEC could materially and adversely affect our business, prospects, financial condition and results of operations. Except as required by law, we do not undertake or plan to update or revise any such forward-looking statements to reflect actual results, changes in plans, assumptions, estimates or projections or other circumstances affecting such forward-looking statements occurring after the date of this Annual Report on Form 10-K, even if such results, changes or circumstances make it clear that any forward-looking information will not be realized. Any public statements or disclosures by us following this Annual Report on Form 10-K that modify or impact any of the forward-looking statements contained in this Annual Report on Form 10-K will be deemed to modify or supersede such statements in this Annual Report on Form 10-K.

This Annual Report on Form 10-K may include market data and certain industry data and forecasts, which we may obtain from internal company surveys, market research, consultant surveys, publicly available information, reports of governmental agencies and industry publications, articles and surveys. Industry surveys, publications, consultant surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but the accuracy and completeness of such information is not guaranteed. While we believe that such studies and publications are reliable, we have not independently verified market and industry data from third-party sources.

| -ii- |

Throughout this Annual Report on Form 10-K, the “Company,” “HyreCar,” “we,” “us,” and “our” refers to HyreCar Inc. and “our board of directors” or our “Board” refers to the board of directors of HyreCar Inc.

Overview

HyreCar Inc. was formed as a corporation in the State of Delaware on November 24, 2014. Our founders identified the need for a car-sharing platform for individuals who wanted to drive for ride-sharing companies such as Uber Technologies Inc. (“Uber”) and Lyft, Inc. (“Lyft”), but whose automobiles could not meet the standards imposed by the ride-sharing companies. For example, Uber maintains strict guidelines regarding the types of cars a driver can use. Although guidelines relating to cars can differ by state, in general the use of two door coupes, motorcycles and cars that are 12 years or older are excluded. Our founders, before deciding to purchase qualifying sedans that met Uber’s strict guidelines, first inquired as to whether there were any rental options available from Uber that would allow them to drive for the ride-sharing platform. To their surprise, there were no rental options available, other than a shadow industry of individuals renting cars to one another.

HyreCar is a car-sharing marketplace that allows car owners (collectively, “Owners”) to rent their idle cars to ride-sharing service drivers (collectively, “Drivers”). By sourcing vehicles from individual Owners, part-time Drivers may more easily enter and exit the market and our business model allows us to satisfy fluctuating transportation demand in cities around the United States by matching Owners and Drivers. In 2019 we began to diversify our vehicle supply to include commercial owners of vehicles including car dealerships and fleet owners to help increase activity levels.

Our business is based on a proprietary car-sharing marketplace developed to (i) onboard Owners and Drivers, (ii) facilitate the matching of Owners and Drivers and (iii) log rental activity for Owners and Drivers. All transactions related to the rental (including, but not limited to, background checks, rentals, deposits and insurance costs) are run securely through the HyreCar platform. Drivers and Owners access their rental or car dashboards through a unique login. Drivers can initiate, terminate or extend a rental through the platform while Owners can manage their car or fleet of cars through the platform.

We believe we have a competitive advantage with our commercial automobile insurance policy that covers both Owners and Drivers. The policy is specifically designed to cover the period of time in which a Driver is operating an Owner’s vehicle while not actively operating a vehicle on a ride-sharing platform, such as Uber or Lyft. During the periods when Drivers are actively operating on a ride-sharing platform, the insurance subordinates to the state mandated insurance provided by the third party ride-sharing business. To our knowledge, we are the only provider of this car-matching service utilizing this unique insurance product.

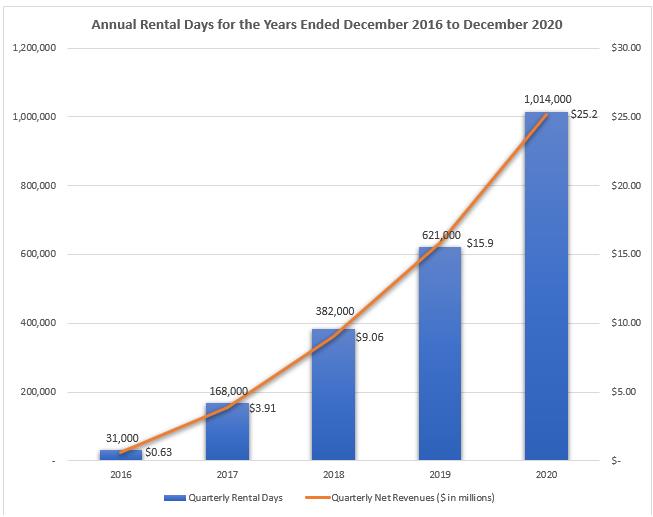

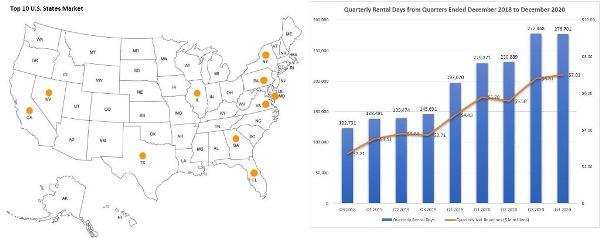

To date, the majority of our growth has been from the dealer sales efforts to build sustainable vehicle supply focused on key markets through the United States. Our car supply has changed from mostly individuals which is where we initially sourced, but now with more of our car supply and rental days coming from the commercial side of the business – consisting primarily of dealers and large fleet owners. We have seen a particular emphasis on states in the southern portion of the United States in late 2019, and now the majority of our daily rental days come from certain states including Georgia, California, New York, Pennsylvania, and Texas. We have also increased driver leads matched in those same key markets, which has been achieved through organic search traffic and paid search advertising. Going forward we will direct advertising dollars strategically because we believe that online channels and offline brand awareness will provide substantial opportunities for growth.

Impact of COVID-19 to our Business

In March 2020, COVID-19 began spreading rapidly throughout the world, prompting governments and businesses to take unprecedented measures in response. Such measures included restrictions on travel and business operations, temporary closures of businesses, and quarantines and shelter-in-place orders. The full extent of the future impact of the COVID-19 pandemic on the Company’s operational and financial performance is currently uncertain and will depend on many factors outside the Company’s control, including, without limitation, the extent, trajectory and duration of the pandemic, the availability of effective treatments and vaccines, and the imposition of further protective public safety measures nationlly or in the markets in which we operate. Refer to Part I, Item 1A of the of this Form 10-K under the heading “Risk Factors,” for more information.

| -1- |

Industry and Market Opportunities

Our company was founded to capitalize on a combination of two growth markets: ridesharing (an industry led by Uber and Lyft) and car-sharing (an industry led by companies such as Turo, Inc. and ZipCar, Inc.). Our customers are the Drivers that use our car-sharing platform to rent a car and then use that car to make money driving for either Uber or Lyft. Finding enough cars and drivers to meet demand has been a problem for ride-sharing companies. Recently we have expanded our target marketing to drivers who provide delivery services with companies like Instacart and Postmates.

The transportation industry represents a massive market. In the United States alone, consumer expenditures on transportation were approximately $1.1 trillion and $1.3 trillion in 2020 and 2019, respectively. Transportation was the second largest household expenditure after housing and was almost twice as large as healthcare and three times as large as entertainment. We believe we are still in the relatively early phases of potentially capturing part of the opportunity in the industry. In 2019, ridesharing accounted for just seven percent of total vehicle miles travelled in the United States and in a 2016 survey, 57% of U.S. respondents who used sharing services said that well-priced and convenient offerings could cause them to give up ownership altogether.

We have added over 38,000 Drivers, matching them with Owner vehicles that have been used on the Uber and Lyft platforms over the past several years. During the years ended December 31, 2020 and 2019, we added approximately 14,000 and 11,000 new Drivers, respectively, into cars so that they could drive for Uber and Lyft. These numbers represent an equivalent 127.3% growth rate in new drivers onto the HyreCar platform year over year.

Ride-sharing Industry (Uber and Lyft)

The growth in ridesharing over the past few years has kicked off a transportation revolution. Smart phones are now used as ride hailing apps, transactions are processed through online platforms and transportation as a service is becoming more and more personalized. The industry has experienced tremendous traction. According to a July 2016 post on TechCrunch, it took Uber six years, to December 2015, to complete a billion rides and by the end of 2020, Uber announced that it had completed its two-billionth ride.

Transportation Network Companies (“TNCs”) like Uber and Lyft have reported high demand from Drivers but many of these Drivers do not own a car that qualifies for their platforms. Uber reported that it had 3.9 million drivers and Lyft reported that it had 1.9 million drivers in North America at the end of 2018. In 2016, a spokesperson for Uber estimated that approximately 10% to 15% of their potential drivers/partners do not own a qualifying car. Further, Lyft estimates that there are approximately 60,000 people in the city of Chicago alone that want to drive for their platform, but do not currently own a qualifying car, and General Motors also estimates that there are approximately 160,000 potential drivers in the DC Metro area, Baltimore, Chicago and Boston who do not own a qualifying car.

Accordingly, TNCs are actively taking steps to satisfy their driver demand by setting up programs designed to get eligible drivers into qualified cars, including such programs as the Enterprise/Uber partnership, the Lyft Express Driver partnership with Hertz and Pep Boys and the General Motor’s Maven program. These programs serve as a validation that there is a healthy market to pair eligible drivers with qualified cars.

Food and Package Industry (Instacart and Grubhub)

With the growth in food, package and grocery delivery services such as Instacart, Postmates, Uber Eats and Grubhub, Hyrecar expects driver demand for services like HyreCar to continue into 2021. With expected revenues for all food delivery companies to top $123B in 2020 and expectations to increase to $164B by 2024. Drivers participating into the Gig economy are diversifying their sources of income across many different TNCs and delivery services. Over 61% of all HyreCar drivers are active drivers for both rideshare and delivery service companies. The package and food delivery companies have seen tremendous demand in the first quarter of 2020, and expect continued growth into 2021 as more and more households move away from traditional in store purchase to online and mobile purchases for the same goods.

Car-sharing Industry

Shared mobility market began to rapidly develop around 2010-2011 when the total number of its users exceeded one million. In 2017, there were already around 10 million people using this type of service, and according to a study by Frost & Sullivan, by 2025 their numbers will reach 36 million, maintaining the annual growth rate of 16.4%. Global Market Insights forecasts the value of the global car sharing market in 2024 at $11 billion. At present, the leading shared mobility markets are the U.S. and Western Europe, while experts predict that Asia will experience the fastest growth in this field. HyreCar is attempting to capitalize on this opportunity as demand from traditional taxi and public transportation options is transferred to shared transportation. Further, growth is expected from this opportunity as the accelerating trend of the mass ease-of-use and availability of shared transportation permanently shifts some driving habits away from personal vehicle ownership. Evidence of this decline, while not yet a national trend, can be seen in large cities as vehicle ownership is beginning to decline. Longer term, we envision a potential impact on the auto industry as a whole from a subset of people permanently changing their driving habits and selling their cars entirely in favor of using shared transportation.

| -2- |

Competition

We believe the key differentiator between HyreCar and our competitors is our asset light model, which allows us to connect excess car inventory to drivers without actually owning or managing the vehicles. This allows our prices to be competitive with other vehicle solutions because we do not have the monthly vehicle overhead or infrastructure costs that our competitors may have. Other advantages include the following:

|

|

1. |

Pay-As-You-Go: Drivers using our platform are not locked into lengthy lease agreements, monthly contracts or subscription fees. Our payment model is upfront and transparent. While our competitors engage in auto-debiting payment for the rented vehicle from the Drivers’ accounts, regardless of their current account balance, under our platform Drivers pay for the term of rental up-front, extend if they are financially able, and return the rented vehicle whenever they need with no “strings” attached. We are the only company providing this type of fluid and frictionless car transaction for Uber and Lyft drivers. |

|

|

2. |

Convenience: In some cases, drivers are renting a car from a local supplier or even their neighbor. They walk down the street, take the keys and go. With Hertz, FlexDrive, Fair or Avis, only one or two retail outlets participate in the Uber and Lyft programs. |

|

|

3. |

Flexibility: The ability to use the same car for both rideshare companies plus food delivery is an important reason why many drivers choose our platform. Coupled with a comprehensive protection program that includes insurance, drivers are attracted to this unique service not offered by our competition. |

Among vehicle solutions for ride-sharing rentals, are Avis, FlexDrive, Getaround and HyreCar. These car rental companies are similar in one way: they operate in the U.S. and provide cars drivers to rent and drive on the Uber or Lyft platform. However, their business models vary widely.

Hertz (OTC:HTZGQ) and Fair.com (“Fair”) were competitors with vehicle supply partnerships with Uber, but both floundered in 2020. Hertz declared bankruptcy mid-year and following Uber’s spring 2019 initial public offering, Fair was offering promotional weekly rates to Uber drivers, which presented a competitive threat in certain marketing, particularly in California. The partnership ended in February 2020 when Uber announced it was ending this “Fair Go” partnership, and as a result Fair has exited the weekly rental business .

A comparative analysis of markets, pricing limitations and age requirements are as follows:

|

|

|

|

|

|

|

Markets |

Nationwide |

30+ Cities |

26+ Cities |

9+ Cities |

|

Rental Length and Age Requirement |

2-Day Minimum / 21+ |

24-Hour Minimum / 25+ |

7-Day Minimum / 25+ | 1-Hour Minimum / 21+ |

|

Service Limitation |

No Limits |

Uber Only |

Lyft Only |

Uber Only |

|

Deposit |

$99 in some states based on driver risk |

None |

$250 |

$150 |

|

Average Weekly Rates** |

Owners set pricing on the platform, around $200 per week with incentives |

$209 per week plus $0.10 - $0.30 per mile (depends on location, taxes and fees) |

$209 per week (disqualified from Express Pay and driver bonuses) |

$5 per hour + 3% Booking fee of trip price + $0.5 per mile daily trip mileage overages |

|

All-In Cost* |

$311 |

$340 |

$390 |

$498 |

* Includes insurance, weekly cost assumes 1,000 miles driven per week, assumes maximum 12-hour rental per day, assumes $0.10 per mile plus 15% taxes and fees applied to advertised competitor pricing.

** Assumes $150 per week in driver bonuses.

| -3- |

Our Strengths

Using our website platform or mobile applications (iOS and Android), vehicle Owners can post their cars to our marketplace and Drivers can browse car inventory prior to rental. Once a Driver finds a car, he or she creates a profile, enters his or her personal information and credentials (including, address, city, state, a copy of applicable state issued driver’s license, Uber or Lyft credentials and social security number) and submits a credit card for payment. We then perform a criminal background check, DMV driving record check, Homeland Security Watch-list and Sex Offender database check. HyreCar’s screening criteria is stricter than Uber and Lyft’s background check and we are focused on maintaining a safe user experience and ensuring that all transactions between owners and drivers are processed through a secure web platform. The attraction and vetting of qualified gig economy drivers is a primary reason why commercial automobile businesses around the country are increasingly working with the Company.

Why Drivers Use Our Service

|

|

● |

Attractive Economics: Drivers’ ability to earn income by driving for multiple ride-sharing or delivery services simultaneously. |

|

|

● |

Pay-As-You-Go: Drivers are not locked into long-term lease agreements or monthly payments or even subscription fees. |

|

|

● |

Convenience: Drivers can quickly pick up the car from a location close by. Typically getting behind the wheel in under 48 hours. |

|

|

● |

Transparency and Trust: No hidden fees and only Car Owners who have been properly vetted are permitted to use the platform. |

|

|

● |

Customer Experience: Application of game-design elements (i.e. gamification) of the platform keeps Drivers engaged. |

Why Owners Use Our Service

Data from a national survey of driving behavior indicates that private vehicles are in use 5% or less during any given day, or about one hour per day. Given the excess capacity of vehicle hours, higher vehicle utilization rates, and lower vehicle ownership rates, we expect a consumer shift towards acceptance of car-sharing. Based on the results of the survey, we believe our platform is advantageous for the following reasons:

|

|

● |

Passive Income: We often match Owners with long term Drivers, which provides the Owners with a steady source of passive income resulting from our re-booking process. |

|

|

● |

Insurance: Physical damage and liability policies fill the gaps left by personal and ride-sharing policies. |

|

|

● |

Review of Drivers: Drivers must pass our extensive background checks which even exceed the Uber and Lyft background checks. |

Insurance Coverage

A key component to our business is our commercial auto insurance coverage. The two-sided nature of our platform means that we need to insure both the Driver and the Owner. Prior to any rental the Driver and Owner are provided an insurance ID card that lists the driver’s name and the vehicle identification number. Insurance is typically generated for the rental until the Owner confirms drop-off of the rented vehicle by the Driver. The vehicle pick-up and drop-off is all managed through our platform. An Owner takes pictures of his or her vehicle prior to pressing the “Confirm Pick-up” button on the HyreCar mobile app. After the rental is completed, the Owner presses the “Confirm Drop-off” button on the HyreCar mobile app and the rental ends.

| -4- |

AON is our insurance broker utilizing their Digital Economy Practice for consulting and insurance placement activities. AON is the leading global professional services firm providing advice and solutions in risk, retirement and health. We moved our annual automobile insurance policy to Apollo for the policy year June 2020 to June 2021 under improved terms and conditions.

For insurance purposes a vehicle rental is broken into four distinct driving periods. Period 0 is when the Driver has picked a vehicle up from the Owner and is driving with the Uber or Lyft app turned-off. Period 1 is when the Driver has the Uber or Lyft app turned-on but has not yet accepted a fare. Period 2 is when the Driver has accepted a fare and is on the way to pick-up a passenger. Period 3 is when a passenger is in the vehicle. The HyreCar policy is specifically written to cover periods in which the Drivers are operating HyreCar vehicles OFF the Uber or Lyft platform (period 0). During the periods when Drivers are operating ON the Uber or Lyft platform (periods 1, 2 and 3), the HyreCar liability insurance subordinates to state mandated insurance provided by Uber and Lyft. This enables us to keep insurance costs and liability low by leveraging state mandated insurance policies provided by the TNCs.

Business Structure and Strategy

We operate out of our corporate office in Los Angeles, California. Our technology platform allows for a relatively small staff compared to the size and reach of our business. For example, our platform matches drivers and owners in certain states and key markets with no physical presence in those states, with the exception of California. Our business structure is divided into three distinct departments: General and Administrative, Sales and Marketing and Research and Development.

Sales and Marketing are vital to our future profitability and growth. Most of our customers need to be sold into a car because they are initially reluctant to pay upfront fees. Early interactions with our customers indicated that if customers were walked through the process once by a member of our sales and marketing team, the customers were more inclined to use and continue to use our services for a longer period of time. As we have streamlined our technology stack, user experience, and strengthened our brand in the industry, consuming rental vehicles through our applications has become a much more seamless process. We have found that a segment of our user base can seamlessly flow through our reservation journey with very few touch points. Due to this we have transitioned the majority of our sales staff into drivers success agents who facilitate the rental process, provide guidance on best places rideshare drivers are making the most income, and generally more of a customer support role.

The Driver Success Team is currently 28 employees, including 2 managers, which are divided into different specialties based on points in the reservation flow. For example, to onboard drivers to the platform we have an outsource group that has a sole focus to get drivers into and through our driver vetting process or background check. After that there is a team of driver success agents who facilitate the driver to rent the vehicle, troubleshoot any issues with the vehicle supplier, generate insurance and inspection documents and make sure that the driver can upload the rental vehicle to their rideshare platform. The Owner team is comprised of agents who are very familiar with the nuances of operating a fleet of vehicles on the HyreCar platform. The Owner sales team’s primary objective is to get Owners to list their cars on the platform. To compliment and tie together the Owner and driver teams, we have built a utilization team with the core focus to facilitate both the driver and owners sides of the marketplace to optimize vehicle utilization for all HyreCar Owners. To underpin the supply side of the marketplace, there is also a specialized group of dealerships and mini fleet sales representatives who present the Platform solution to B2B Owners. As the driver success team has become more efficient as we have scaled, we do not expect the need to add headcount as rapidly through 2021 in order for us to continue to achieve forecasted revenue growth rates.

Leveraging headcount more efficiently is a key assumption that we believe drives profitability. The ability to grow topline revenue without significant increases to operating expense is achieved through a combination of marketing, sales, support and technology. Attribution of organic bookings is directly related to the quality of marketing leads generated and user interface/experience enhancements (UI/UX) per technology development. HyreCar has invested in a partnership with a leading SEO firm to continue maximizing organic rankings on Google search pages. Additionally, new market automation tools have allowed HyreCar to communicate directly with its drivers with specially curated messaging to increase awareness of available vehicles and incentive programs for each target DMA and market segment. The company’s expectation is that both aspects contribute to low operating expense growth in relation to revenue, which in-turn, the company believes, will lead to higher gross profit in 2021.

We currently operate with one technology development team in the United States, including multiple full-time developers based out of our home office in Los Angeles. These teams are tasked with maintaining the current codebase and website, and incrementally adding enhancement to the Owner and Driver application and website to support our expansion into institutional car supply nationally.

| -5- |

Support and operations underpin the company. New Dealer onboarding, insurance claims management, owner payment resolutions, Driver payment resolutions, collections, chat support, email support, phone support, late rentals, car recovery, Driver verifications, insurance generation and insurance verification all work together to create what we believe is a “best in class” customer service experience. Currently, we have 12 in-house customer support staff in our Los Angeles office as well as 20 independent contractors located in the Central Time Zone through our outsourced partner who we added in mid-2019. Our plan is to focus our domestic customer support team on being client-facing for larger commercial accounts and scale by outsourcing as we continue to grow. We believe that customer service is critical to our goal of bringing new Drivers/Owners onto the platform and retaining those customers who have already utilized our services.

Revenue Model

We generate revenue by taking a fee out of each rental processed on our platform. Each rental transaction represents a Driver renting a car from an Owner. Drivers pay a daily rental rate set by the Car Owner, plus a 10% HyreCar Driver Fee and direct daily insurance costs. Owners receive their daily rental rate minus a 15-25% HyreCar Owner Fee. For example, as of December 31, 2020, the average daily rental rate of a HyreCar vehicle nationally is approximately $36.00 (“Daily Rental Rate”), plus a 10% HyreCar Driver fee ($3.60) and daily direct insurance fee of $13.00, totaling $52.60 in total daily gross billings is paid by the Driver via a credit card transaction. On average approximately 80% of the daily rental or $28.80 is transferred to the Owner via our merchant processing partner. HyreCar earns revenues from the two revenue share fees and the insurance totaling approximately $24.16 per day. Accordingly, the GAAP reportable revenue recognized by HyreCar is $24.16 in this example transaction, as detailed in the following table:

|

Daily Gross Revenue Example |

|

Daily Net (GAAP) Revenue Example |

||||||||

|

|

|

|

|

|

|

|

|

|

||

|

National Average Daily Rental Rate |

|

$ |

36.00 |

|

|

HyreCar Owner Fee (~21% Average) |

|

$ |

7.56 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Driver Fee |

|

$ |

3.60 |

|

|

HyreCar Driver Fee (10% rate) |

|

$ |

3.60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daily Insurance Fee |

|

$ |

13.00 |

|

|

Insurance Fee (100% of fee) |

|

$ |

13.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daily Gross Billing Paid by Driver |

|

$ |

52.60 |

|

|

Daily Average Net Revenue |

|

$ |

24.16 |

|

Gross billings is an important measure by which we evaluate and manage our business. We define gross billings as the amount billed to Drivers, without any adjustments for amounts paid to Owners or refunds. It is important to note that gross billings is a non-GAAP measure and as such, is not recorded in our consolidated financial statements as revenue. However, we use gross billings to asses our business growth, scale of operations and our ability to generate gross billings is strongly correlated to our ability to generate revenues. Gross billings may also be used to calculate net revenue margin, defined as the company’s GAAP reportable revenue over gross billings. Using the definition of net revenue margin and the example above, HyreCar’s net revenue margin is equal to approximately 45.2% ($25,231,741 HyreCar’s GAAP revenue over $55,761,917 Total Gross Billings). A breakout of revenue components is provided in the section of this Annual Report on Form 10-K titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the footnotes to our audited consolidated financial statements.

Marketing Plan

Our marketing team periodically reviews keyword searches using Google Analytics. Thirty keywords and phrases were chosen and analyzed, allowing the team to determine in which cities the persons searching for the keywords and phrases were located. For example, approximately 400,000 people in Los Angeles googled key words like, “rent a car for Uber,” “Uber,” and “Uber Leasing.” Overlaying our customer demographics with the Google search results created a Driver/Owner affinity population of approximately 25 million potential customers, with the bulk of the 25 million concentrated in 16 core geographic locations. Our key geographies currently consist of ten key metropolitan statistical areas (MSA) based on the driver demand for ridesharing and delivery activity as part of the gig economy with large population bases. As we built out the institutional car supply through year ended December 31, 2020, our historical car supply constraints were largely addressed. Further, we have started focusing more locally on approximately ten key metropolitan markets in certain states. Currently more than 75% of our car supply comes from commercial versus individual sources and for the fourth quarter of 2020 more than 75% of our rental days come from a few key states including California, Florida, Georgia, New York, Pennsylvania, Texas and Maryland.

| -6- |

Insurance Opportunity

A large percentage of our cost of revenues is direct insurance and claims expense, which we pay to the insurance company. The premiums are broken into two categories, liability insurance and physical damage. The unique nature of our insurance enables us to keep insurance costs and liability low by leveraging state mandated insurance policies provided by the Transportation Network Companies.

In addition to self-insurance, the company is also working with AON to develop new and innovative insurance products. The company is reviewing alternative insurance opportunities including a new type of owner “lay-up” insurance and higher insurance level for fleet vehicle owners on the HyreCar platform. Lay-up insurance replaces the need for an owner’s personal auto insurance policy and would represent significant cost savings when compared to other insurance options available in the market today. Offering this type of insurance product benefits the company in multiple verticals, including reduced insurance claim expense, greater customer retention and stickiness to the HyreCar platform.

Regulation

The California Public Utilities Commission (“CPUC”) was the first state regulatory body to impose rules and guidelines for ridesharing in the United States. The CPUC designated Uber and Lyft as “transportation network companies” or TNCs. The CPUC guidelines became the standard for all states across the U.S. Most states have adopted some form of the guidelines. California is one of the strictest states when it comes to regulating the TNCs. Our insurance works within the California guidelines which make it easily adoptable by future state mandates outside of California.

Changes in government regulation of our business have the potential to materially alter our business practices or our operational results. Depending on the jurisdiction, those changes may come about through the issuance of new laws and regulations or changes in the interpretation of existing laws and regulations by a court, regulatory body or governmental official. Sometimes those changes may have not just prospective but also retroactive effect; this is particularly true when a change is made through reinterpretation of laws or regulations that have been in effect for some time. Moreover, changes in regulation that may seem neutral on their face may have either more or less impact on us than on ride-sharing businesses, depending on the circumstances. Potential changes in law or regulation that may affect us relate to insurance intermediaries, customer privacy, data security and rate regulation.

In addition, our operations also could be affected by any limitation in the fuel supply or by any imposition of mandatory allocation or rationing regulations. We are not aware of any current proposal to impose such a regime in the U.S. or internationally. Such a regime could, however, be quickly imposed if there was a serious disruption in the fuel supply for any reason, including an act of war, terrorist incident or other problem, such as the devastation caused by hurricane Harvey, affecting the petroleum supply, refining, distribution or pricing.

Employees

As of December 31, 2020, we employ 86 full-time personnel primarily in our headquarters location in downtown Los Angeles, California, although our team has largely been remote since March 2020 due to COVID-19 limitations.

Our Corporate Information

We were incorporated as a Delaware corporation on November 24, 2014. Our principal executive offices are located at 355 South Grand Avenue, Suite 1650, Los Angeles, California 90071, and our telephone number is (888) 688-6769.

Available Information

Our website address is www.hyrecar.com. The contents of, or information accessible through, our website are not part of this Annual Report on Form 10-K, and our website address is included in this document as an inactive textual reference only. We make our filings with the SEC, including our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports, available free of charge on our website as soon as reasonably practicable after we file such reports with, or furnish such reports to, the SEC. The public may read and copy the materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Additionally, the SEC maintains an internet site that contains reports, proxy and information statements and other information. The address of the SEC’s website is www.sec.gov. The information contained in the SEC’s website is not intended to be a part of this filing.

| -7- |

You should carefully consider the risks described below, as well as general economic and business risks and the other information in this Annual Report on Form 10-K. The occurrence of any of the events or circumstances described below or other adverse events could have a material adverse effect on our business, results of operations and financial condition and could cause the trading price of our common stock to decline. Additional risks or uncertainties not presently known to us or that we currently deem immaterial may also harm our business.

Risks Related to Our Business and Our Industry

Our limited operating history makes it difficult to evaluate our current business and prospects and may increase the risks associated with your investment.

We were founded in 2014. Our limited operating history makes it difficult to evaluate our current business and prospects and plan for and model our future growth. We have encountered and will continue to encounter risks and uncertainties frequently encountered by rapidly growing companies in developing markets. If our assumptions regarding these risks and uncertainties are incorrect or change in response to changes in the ridesharing or car-sharing market, our results of operations and financial results could differ materially from our plans and forecasts. Although we have experienced periods of rapid growth since our inception, there is no assurance that such growth will continue. Any success we may experience in the future will depend in large part on our ability to, among other things:

|

|

● |

maintain and expand our customer base and the ways in which customers use our platform; |

|

|

● |

expand revenue from existing customers through increased or broader use of our platform; |

|

|

● |

improve the performance and capabilities of our platform through research and development; |

|

|

● |

effectively expand our business domestically and internationally, which will require that we rapidly expand our sales force and fill key management positions; and |

|

|

● |

successfully compete with other companies that currently provide, or may in the future provide, solutions like ours. |

If we are unable to achieve our key objectives, including the objectives listed above, our business and results of operations will be adversely affected, and the value of our securities could decline.

The COVID-19 pandemic has disrupted and harmed, and is expected to continue to disrupt and harm, our business, financial condition and results of operations. We are unable to predict the extent to which the pandemic and related impacts will continue to adversely impact our business, financial condition and results of operations and the achievement of our strategic objectives.

Our business, operations and financial performance have been negatively impacted by the COVID-19 pandemic and related public health responses, such as travel bans, travel restrictions and shelter-in-place orders. The pandemic and these related responses have caused, and are expected to continue to cause, decreased demand for our platform relative to pre-COVID-19 demand, the global slowdown of economic activity (including a decrease in demand for a broad variety of goods and services), disruptions in global supply chains, and significant volatility and disruption of financial markets.

The COVID-19 pandemic has subjected our operations, financial performance and financial condition to a number of risks, including, but not limited to those discussed below:

|

|

● |

Declines in travel as a result COVID-19, including commuting, local travel, and business and leisure travel, has resulted in decreased demand for our platform which has decreased our anticipated revenue growth trajectory. During certain periods in the past, these factors have led to a decrease in earning opportunities for drivers on our platform. Changes in travel trends and behavior arising from COVID-19 may continue to develop or persist over time and further contribute to this adverse effect. |

|

|

● |

Changes in driver behavior arising from COVID-19 have led to reduced levels of driver availability on our platform. To the extent that driver availability is limited, our service levels may be negatively impacted, which may adversely affect our business, financial condition and results of operation. |

| -8- |

|

|

● |

The responsive measures to the COVID-19 pandemic have caused us to modify our business practices by having employees work remotely or holding virtual meetings. We may in the future be required to or choose voluntarily to take actions for the health and safety of our workforce, whether in response to government orders or based on our own determinations of what is in the best interests of our employees or users of our platform. The effects of the pandemic, including remote working arrangements for employees, may also impact our financial reporting systems and internal control over financial reporting, including our ability to ensure information required to be disclosed in our reports under the Securities Exchange Act of 1934, as amended, is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms and that such information is accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate, to allow for timely decisions regarding required disclosure. To the extent these measures result in decreased productivity, harm our company culture, adversely affect our ability to maintain internal controls, or otherwise negatively affect our business, our financial condition and results of operations could be adversely affected. |

Our results of operations vary and are unpredictable from period-to-period, which could cause the trading price of our common stock to decline.

Our results of operations have historically varied from period-to-period and we expect that our results of operations will continue to do so for a variety of reasons, many of which are outside of our control and difficult to predict. Because our results of operations may vary significantly from quarter-to-quarter and year-to-year, the results of any one period should not be relied upon as an indication of future performance. We have presented many of the factors that may cause our results of operations to fluctuate in this “Risk Factors” section. Fluctuations in our results of operations may cause such results to fall below our financial guidance or other projections, or the expectations of analysts or investors, which could cause the trading price of our common stock to decline.

The ridesharing market and the market for our service offerings are still in relatively early stages of growth and if such markets do not continue to grow, grow more slowly than we expect or fail to grow as large as we expect, our business, financial condition and results of operations could be adversely affected.

The ridesharing market has grown rapidly since we launched our car-sharing marketplace in 2014, but it is still relatively new, and it is uncertain to what extent market acceptance will continue to grow, if at all. Our success will depend to a substantial extent on the willingness of people to widely-adopt car-sharing and ride-sharing generally. We cannot be certain whether the COVID-19 pandemic will negatively impact the willingness of drivers or passengers to participate in ridesharing. If the public does not perceive ridesharing as beneficial, or chooses not to adopt them as a result of concerns regarding public health or safety, affordability or for other reasons, whether as a result of incidents on Lyft or Uber or similar platforms, the COVID-19 pandemic, or otherwise, then the market for our offerings may not further develop, may develop more slowly than we expect or may not achieve the growth potential we expect. Additionally, from time to time we may re-evaluate the markets in which we operate, and we have discontinued and may in the future discontinue operations in certain markets as a result of such evaluations. Any of the foregoing risks and challenges could adversely affect our business, financial condition and results of operations.

Our business is subject to a wide range of laws and regulations, many of which are evolving, and failure to comply with such laws and regulations could harm our business, financial condition and results of operations.

We are subject to a wide variety of laws in the United States and other jurisdictions. Laws, regulations and standards governing issues such as transportation network companies (“TNCs”), ridesharing, food and package delivery, worker classification, labor and employment, anti-discrimination, payments, gift cards, whistleblowing and worker confidentiality obligations, product liability, defects, maintenance and repairs, personal injury, text messaging, subscription services, intellectual property, consumer protection, taxation, privacy, data security, competition, unionizing and collective action, arbitration agreements and action waiver provisions, terms of service, mobile application accessibility, autonomous vehicles, bike and scooter sharing, insurance, vehicle rentals, money transmittal, non-emergency medical transportation, environmental health and safety, background checks, public health, anti-corruption, anti-bribery, and delivery of goods including (but not limited to) medical supplies, perishable foods and prescription drugs are often complex and subject to varying interpretations, in many cases due to their lack of specificity. As a result, their application in practice may change or develop over time through judicial decisions or as new guidance or interpretations are provided by regulatory and governing bodies, such as federal, state and local administrative agencies.

| -9- |

Recent financial, political and other events have increased the level of regulatory scrutiny on larger companies, technology companies in general and companies engaged in dealings with independent contractors, such as ridesharing and delivery companies. Regulatory bodies may enact new laws or promulgate new regulations that are adverse to our business, or, due to changes in our operations and structure or partner relationships as a result of changes in the market or otherwise, they may view matters or interpret laws and regulations differently than they have in the past or in a manner adverse to our business. For example, Assembly Bill 5 (as codified in part at Cal. Labor Code sec. 2750.3) codified and extended an employment classification test in Dynamex Operations West, Inc. v. Superior Court, which established a new standard for determining employee or independent contractor status. The passage of this bill led to additional challenges to the independent contractor classification of drivers using the Lyft and Uber platforms. Subsequently, voters in California voted on Proposition 22, a state ballot initiative that provides a framework for drivers utilizing platforms such as Lyft to maintain their status as independent contractors under California law. Based on the unofficial results published by the California Secretary of State indicating that Proposition 22 was approved, Lyft filed a petition for rehearing of our appeal with the California Court of Appeal on November 6, 2020.

The results of Proposition 22 in California may cause us to alter our operations and incur additional costs.

The recent passage of Proposition 22 in California may impact how TNCs provide different earning opportunities to drivers in California. We expect that this transition will require additional costs as TNCs transition drivers to this new model, including the logistics of providing the additional earning opportunities, and as a result may result in potential changes to the pricing or method by which customers utilize these services, and in turn the services we offer. The change in model may also affect our ability to attract and retain drivers and vehicle owners in this market. To the extent similar classification models are adopted in other jurisdictions, we may face similar costs and challenges.

Changes in tax treatment of companies engaged in e-commerce may adversely affect the commercial use of our sites and our financial results.

Due to the global nature of the Internet, it is possible that various states might attempt to impose additional or new regulation on our business or levy additional or new sales, income or other taxes relating to our activities. Tax authorities at the federal, state and local levels are currently reviewing the appropriate treatment of companies engaged in e-commerce and digital services. New or revised international, federal, state or local tax regulations or court decisions may subject us or our customers to additional sales, income and other taxes. For example, on June 21, 2018, the U.S. Supreme Court rendered a 5-4 majority decision in South Dakota v. Wayfair Inc., 17-494 where the Court held, among other things, that a state may require an out-of-state seller with no physical presence in the state to collect and remit sales taxes on goods the seller ships to consumers in the state, overturning existing court precedent. Other new or revised taxes and, in particular, digital taxes, sales taxes, VAT and similar taxes could increase the cost of doing business online and decrease the attractiveness of selling products services over the Internet. New taxes and rulings could also create significant increases in internal costs necessary to capture data and collect and remit taxes. Any of these events could have a material adverse effect on our business, financial condition and operating results.

Our revenue growth rate and financial performance in recent periods may not be indicative of future performance and such revenue growth rate or growth in demand for our offerings may slow over time.

We have grown rapidly over the last several years, and therefore, our recent revenue growth rate and financial performance should not be considered indicative of our future performance. We have experienced a decline in ur anticipated revenue growth trajectory due to decreased demand in the second quarter for our car-sharing platform in light of the COVID-19 pandemic, and we expect that our revenue growth rate and financial performance in future quarters will continue to be harmed while responsive measures to COVID-19, such as travel bans and restrictions and shelter-in-place orders, remain in place. You should not rely on our revenue for any previous quarterly or annual period as any indication of our revenue or revenue growth in future periods. As we grow our business, our revenue growth rates will slow in future periods due to a number of reasons, which may include impacts of the COVID-19 pandemic on our business, slowing demand for our offerings, increasing competition, a decrease in the growth of our overall market or market saturation, increasing regulatory costs and challenges and resulting changes to our business model and our failure to capitalize on growth opportunities.

| -10- |

If we fail to effectively manage our growth, our business, financial condition and results of operations could be adversely affected.

Our ability to manage our growth and business operations effectively and to integrate new employees, technologies and acquisitions into our existing business will require us to continue to expand our operational and financial infrastructure and to continue to retain, attract, train, motivate and manage employees. Continued growth could strain our ability to develop and improve our operational, financial and management controls, enhance our reporting systems and procedures, recruit, train and retain highly skilled personnel and maintain user satisfaction. Additionally, if we do not effectively manage the growth of our business and operations, the quality of our offerings could suffer, which could negatively affect our reputation and brand, business, financial condition and results of operations.

Any actual or perceived security or privacy breach could interrupt our operations, harm our brand and adversely affect our reputation, brand, business, financial condition and results of operations.

Our business involves the collection, storage, processing and transmission of our users’ personal data and other sensitive data. An increasing number of organizations, including large online and off-line merchants and businesses, other large Internet companies, financial institutions and government institutions, have disclosed breaches of their information security systems and other information security incidents, some of which have involved sophisticated and highly targeted attacks. In addition, users on our platform could have vulnerabilities on their own mobile devices that are entirely unrelated to our systems and platform, but could mistakenly attribute their own vulnerabilities to us. Further, breaches experienced by other companies may also be leveraged against us. For example, credential stuffing attacks are becoming increasingly common and sophisticated actors can mask their attacks, making them increasingly difficult to identify and prevent. Certain efforts may be state-sponsored or supported by significant financial and technological resources, making them even more difficult to detect.

Changes in laws or regulations relating to privacy, data protection or the protection or transfer of personal data, or any actual or perceived failure by us to comply with such laws and regulations or any other obligations relating to privacy, data protection or the protection or transfer of personal data, could adversely affect our business.

We receive, transmit and store a large volume of personally identifiable information and other data relating to the users on our platform. Numerous local, municipal, state, and federal laws and regulations address privacy, data protection and the collection, storing, sharing, use, disclosure and protection of certain types of data, including the California Online Privacy Protection Act, the Personal Information Protection and Electronic Documents Act, the U.S. Federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, Section 5(c) of the Federal Trade Commission Act, the California Consumer Privacy Act, or CCPA, and the California Privacy Rights Act, or CPRA, which becomes operative on January 1, 2023. These laws, rules and regulations evolve frequently and their scope may continually change, through new legislation, amendments to existing legislation and changes in enforcement, and may be inconsistent from one jurisdiction to another. For example, the CPRA will require new disclosures to California consumers and affords such consumers new data rights and abilities to opt-out of certain sharing of personal information. The CPRA provides for fines of up to $7,500 per violation, which can be applied on a per-consumer basis. Aspects of the CPRA and its interpretation and enforcement remain unclear. The effects of this legislation potentially are far-reaching, however, and may require us to further modify our data processing practices and policies and incur additional compliance-related costs and expenses. The CPRA and other changes in laws or regulations relating to privacy, data protection and information security, particularly any new or modified laws or regulations that require enhanced protection of certain types of data or new obligations with regard to data retention, transfer or disclosure, could greatly increase the cost of providing our offerings, require significant changes to our operations or even prevent us from providing certain offerings in jurisdictions in which we currently operate and in which we may operate in the future.

Operating as a public company requires us to incur substantial costs and requires substantial management attention. In addition, certain members of our management team have limited experience managing a public company.

As a public company, we incur substantial legal, accounting and other expenses that we did not incur as a private company. For example, we are subject to the reporting requirements of the Exchange Act, the applicable requirements of the Sarbanes-Oxley Act, the Dodd-Frank Wall Street Reform and Consumer Protection Act, the rules and regulations of the SEC and the listing standards of the Nasdaq Global Select Market. For example, the Exchange Act requires, among other things, we file annual, quarterly and current reports with respect to our business, financial condition and results of operations. We are also required to maintain effective disclosure controls and procedures and internal control over financial reporting. Compliance with these rules and regulations has increased and will continue to increase our legal and financial compliance costs, and increase demand on our systems. In addition, as a public company, we may be subject to stockholder activism, which can lead to additional substantial costs, distract management and impact the manner in which we operate our business in ways we cannot currently anticipate. As a result of disclosure of information in filings required of a public company, our business and financial condition will become more visible, which may result in threatened or actual litigation, including by competitors.

| -11 |

We rely on third-party background check providers to screen potential drivers, and if such providers fail to provide accurate information, or if providers are unable to complete background checks because of court closures or other unforeseen government shutdown, or we do not maintain business relationships with them, our business, financial condition and results of operations could be adversely affected.

We rely on third-party background check providers such as Checkr to screen the records of potential drivers to help identify those that are not qualified to utilize our platform pursuant to applicable law or our internal standards. Our business has and may continue to be adversely affected to the extent we cannot attract or retain qualified drivers as a result of such providers being unable to complete certain background checks because of court closures or other government shutdown related to the COVID-19 pandemic, or to the extent that they do not meet their contractual obligations, our expectations or the requirements of applicable law or regulations. If any of our third-party background check providers terminates its relationship with us or refuses to renew its agreement with us on commercially reasonable terms, we may need to find an alternate provider, and may not be able to secure similar terms or replace such partners in an acceptable time frame. If we cannot find alternate third-party background check providers on terms acceptable to us, we may not be able to timely onboard potential drivers, and as a result, our platform may be less attractive to qualified drivers. Further, if the background checks conducted by our third-party background check providers do not meet our expectations or the requirements under applicable laws and regulations, unqualified drivers may be permitted to provide rides on our platform, and as a result, our reputation and brand could be adversely affected and we could be subject to increased regulatory or litigation exposure.

We could be subject to claims from TNC or delivery drivers or third parties that are harmed whether or not our platform is in use, which could adversely affect our business, brand, financial condition and results of operations.

We are regularly subject to claims, lawsuits, investigations and other legal proceedings relating to injuries to, or deaths of, TNC and delivery drivers or third-parties, as applicable, that are attributed to us through our offerings. We may also be subject to claims alleging that we are directly or vicariously liable for the acts of the drivers on our platform or for harm related to the actions of drivers, TNC riders, or third parties, or the management and safety of our platform and our assets, including in light of the COVID-19 pandemic and related public health measures issued by various jurisdictions, including travel bans, restrictions, social distancing guidance, and shelter-in-place orders. We may also be subject to personal injury claims whether or not such injury actually occurred as a result of activity on our platform. For example, third parties have in the past asserted legal claims against us in connection with personal injuries related to the actions of a driver or rider who may have previously utilized our platform, but was not at the time of such injury. Regardless of the outcome of any legal proceeding, any injuries to, or deaths of, any TNC riders, drivers or third parties could result in negative publicity and harm to our brand, reputation, business, financial condition and results of operations.

We may require additional capital, which may not be available on terms acceptable to us or at all.

We evaluate financing opportunities from time to time, and our ability to obtain financing will depend, among other things, on our development efforts, business plans and operating performance and the condition of the capital markets at the time we seek financing. Additionally, COVID-19 may impact our access to capital and make additional capital more difficult or available only on terms less favorable to us. We cannot be certain that additional financing will be available to us on favorable terms, or at all. If we are unable to obtain adequate financing or financing on terms satisfactory to us, when we require it, our ability to continue to support our business growth and to respond to business challenges could be significantly limited, and our business, financial condition and results of operations could be adversely affected.

We have had operating losses each year and quarterly period since our inception and may not achieve or maintain profitability in the future.

We have incurred operating losses each year and every quarterly period since inception. For the years ended December 31, 2020 and 2019, our operating loss was $15,252,689 and $12,689,558 respectively. We expect our operating expenses to decrease in the future as we curtail expenditures by scaling back certain sales and marketing and research and development expenses. Our revenue growth may slow or our revenue may decline for a number of other reasons, including reduced demand for our services, economic weakness, global macroeconomic shocks such as the recent coronavirus outbreak, increased competition, a decrease in the growth or size of the ride-sharing or car-sharing market or any failure to capitalize on growth opportunities. Any failure to increase our revenue as we grow our business could prevent us from achieving or maintaining profitability. If we are unable to meet these risks and challenges as we encounter them, our business, financial condition and results of operations may suffer.

| -12- |

If we do not respond appropriately, the evolution of the automotive industry towards autonomous vehicles and mobility on demand services could adversely affect our business.

The automotive industry is increasingly focused on the development of advanced driver assistance technologies, with the goal of developing and introducing a commercially viable, fully automated driving experience. The high development cost of active safety and autonomous driving technologies may result in a higher risk of exposure to the success of new or disruptive technologies different than those being developed by us. There has also been an increase in consumer preferences for mobility on demand services, such as car and ridesharing, as opposed to automobile ownership, which may result in a long-term reduction in the number of vehicles per capita. These evolving areas have also attracted increased competition from entrants outside the traditional automotive industry. If we do not continue to innovate to develop or acquire new and compelling products and service offerings that capitalize upon new technologies in response to consumer preferences, this could have an adverse impact on our results of operations.

If we do not effectively expand and train our direct sales force, we may be unable to add new customers or increase sales to our existing customers, and our business will be adversely affected.

We continue to be substantially dependent on our direct sales force to obtain new customers and increase sales with existing customers. There is significant competition for sales personnel with the skills and technical knowledge that we require. Our ability to achieve significant revenue growth will depend, in large part, on our success in recruiting, training and retaining sufficient numbers of sales personnel to support our growth. New hires require significant training and may take significant time before they achieve full productivity. Our recent hires and planned hires may not become productive as quickly as we expect, and we may be unable to hire or retain sufficient numbers of qualified individuals in the markets where we do business or plan to do business. In addition, because we continue to grow rapidly, a large percentage of our sales force is new to our company. If we are unable to hire and train a sufficient number of effective sales personnel, or the sales personnel we hire are not successful in obtaining new customers or increasing sales to our existing customer base, our business will be adversely affected.

Unfavorable global economic, business, or political conditions could adversely affect our business, financial condition or results of operations.

Our results of operations could be adversely affected by general conditions in the global economy and in the global financial markets, including conditions that are outside of our control, including the impact of health and safety concerns, such as those relating to the current COVID-19 coronavirus (“COVID-19”) pandemic. The recent global financial crisis in connection with the COVID-19 pandemic has caused extreme volatility and disruptions in the capital and credit markets. A severe or prolonged economic downturn could result in a variety of risks to our business, including weakened demand for our platform and our ability to raise additional capital when needed on acceptable terms, if at all. Any of the foregoing could harm our business and we cannot anticipate all the ways in which the current economic climate and financial market conditions could adversely impact our business.

We have no formal contracts with either Uber or Lyft and our current relationships with either of these companies could change in the future, which could adversely affect our revenues.

Although we have deployed drivers and cars to the systems of both Uber and Lyft since our operations began in 2015, there is currently no formal contractual relationship in place with either company. We have an arrangement with Lyft that allows us to activate our Drivers through Lyft’s sign-up portal; however, this is an oral arrangement that has not been memorialized in a written agreement. Consequently, each of these relationships could be discontinued at any time. In addition, virtually all of our revenue is generated by cars and drivers operating on both the Uber or Lyft platform and therefore this concentration represents a high degree of risk to us and to potential investors.

The ride-sharing and delivery models may not continue to grow, which would adversely affect our business.

Our business and future growth is significantly dependent on the continued success of each of Uber, Lyft, Instacart and other software-based systems that have come into the marketplace to compete with standard taxicab transportation organizations.

While the effect of those companies has been to decrease the cost and therefore increase the utilization of ride-sharing, there can be no assurance that consumer utilization of these systems will continue to grow, or that competition and the resulting price pressure will not undermine the viability of these types of systems, thereby adversely affecting our business.

| -13- |

Our unique peer to peer structure could be duplicated and our inability to accurately predict user behavior could negatively impact our sales business.

Although to date neither Uber nor Lyft have endeavored to develop a peer-to-peer system to match drivers and car owners as we are doing, there can be no assurance that either one of these companies or other competitors subsequently entering the marketplace will not endeavor to do so, and there can be no assurance that such competition will not have a negative impact on our business.

Furthermore, although several attempts to match up fleets of cars owned by operators with Uber and Lyft drivers have failed, there can be no assurance that other entities will not enter the marketplace on this basis with economic and logistical models that solve the problems that caused this failure.

The market forecasts included in this Annual Report on Form 10-K may prove to be inaccurate, and even if the markets in which we operate achieve growth, we cannot assure you our business will grow at similar rates, if at all.

Growth forecasts are subject to significant uncertainty and are based on assumptions and estimates, which may not prove to be accurate. Forecasts relating to the expected growth in the ride-sharing market, including the forecasts or projections referenced in this Annual Report, may prove to be inaccurate. Even if the ride-sharing market experiences the forecasted growth, we may not grow our business at similar rates, or at all. Our growth is subject to many factors, including our success in implementing our business strategy, which is subject to many risks and uncertainties. Accordingly, the forecasts of market growth included in this Annual Report should not be taken as indicative of our future growth.

We rely on third-party insurance policies to insure auto-related risks. If insurance coverage is insufficient for the needs of our business or our insurance providers are unable to meet their obligations, we may not be able to mitigate the risks facing our business, which could adversely affect our business, financial condition and results of operations.

We procure third-party insurance policies which provide coverage for both Owners and Drivers on our platform. If the amount of one or more auto-related claims were to exceed our applicable aggregate coverage limits, we may bear the excess liability. Insurance providers have raised premiums and deductibles for many businesses and may do so in the future. As a result, our insurance and claims expense could increase. Our business, financial condition and results of operations could be adversely affected if (i) cost per claim, premiums or the number of claims significantly exceeds our historical experience and coverage limits, (ii) we experience a claim in excess of coverage limits, (iii) our insurance providers fail to pay insurance claims, or (iv) we experience a claim for which coverage is not provided.

We rely on third-party background check providers to screen potential drivers, and if such providers fail to provide accurate information, or if providers are unable to complete background checks because of court closures or other unforeseen government shutdown, or we do not maintain business relationships with them, our business, financial condition and results of operations could be adversely affected.