UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

For the transition period from ______ to ______

Commission

file number

(Exact name of registrant as specified in charter)

| (State or jurisdiction of Incorporation or organization) | I.R.S. Employer Identification No. |

| (Address of principal executive offices) | (Zip code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||

| The |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller Reporting Company | ||

| Emerging Growth Company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate

by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act) Yes ☐ No

The

aggregate market value of the voting stock and non-voting common equity held by non-affiliates of the registrant as of the last business

day of the registrant’s most recently completed second fiscal quarter ended June 30, 2021 was $

Number

of shares of common stock outstanding as of March 28, 2022 was

Documents Incorporated by Reference: None.

Table of Contents

i

CAUTIONARY NOTE ON FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Any statements in this Annual Report on Form 10-K about our expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as “believe,” “will,” “expect,” “anticipate,” “estimate,” “intend,” “plan” and “would.” For example, statements concerning financial condition, possible or assumed future results of operations, growth opportunities, industry ranking, plans and objectives of management, markets for our common stock and future management and organizational structure are all forward-looking statements. Forward-looking statements are not guarantees of performance. They involve known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to differ materially from any results, levels of activity, performance or achievements expressed or implied by any forward-looking statement.

Any forward-looking statements are qualified in their entirety by reference to the risk factors discussed throughout this Annual Report on Form 10-K. Some of the risks, uncertainties and assumptions that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include, but are not limited to:

| ● | our business strategies; | |

| ● | the timing of regulatory submissions; | |

| ● | our ability to obtain and maintain regulatory approval of our existing product candidates and any other product candidates we may develop, and the labeling under any approval we may obtain; | |

| ● | risks relating to the timing and costs of clinical trials and the timing and costs of other expenses; | |

| ● | risks related to market acceptance of products; | |

| ● | intellectual property risks; | |

| ● | risks associated to our reliance on third party organizations; |

| ● | our competitive position; |

| ● | our industry environment; |

| ● | our anticipated financial and operating results, including anticipated sources of revenues; |

| ● | assumptions regarding the size of the available market, benefits of our products, product pricing and timing of product launches; |

| ● | management’s expectation with respect to future acquisitions; |

| ● | statements regarding our goals, intentions, plans and expectations, including the introduction of new products and markets; and |

| ● | our cash needs and financing plans. |

The foregoing list sets forth some, but not all, of the factors that could affect our ability to achieve results described in any forward-looking statements. You should read this Annual Report on Form 10-K and the documents that we reference herein and have filed as exhibits to the Annual Report on Form 10-K, completely and with the understanding that our actual future results may be materially different from what we expect. You should assume that the information appearing in this Annual Report on Form 10-K is accurate as of the date hereof. Because the risk factors referred to on page 13 of Annual Report on Form 10-K, could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by us or on our behalf, you should not place undue reliance on any forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of the information presented in this Annual Report on Form 10-K, and particularly our forward-looking statements, by these cautionary statements.

ii

RISK FACTOR SUMMARY

Our business is subject to significant risks and uncertainties that make an investment in us speculative and risky. Below we summarize what we believe are the principal risk factors but these risks are not the only ones we face, and you should carefully review and consider the full discussion of our risk factors in the section titled “Risk Factors,” together with the other information in this Annual Report on Form 10-K. If any of the following risks actually occurs (or if any of those listed elsewhere in this Annual Report on Form 10-K occur), our business, reputation, financial condition, results of operations, revenue, and future prospects could be seriously harmed. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business.

Risk Related to our Financial Position and Need for Capital

| ● | We have generated no revenue from commercial sales and our future profitability is uncertain. If we fail to obtain the capital necessary to fund our operations, we will be unable to continue or complete our product development. |

Risk Related to Product Development, Regulatory Approval, Manufacturing and Commercialization

| ● | The marketing approval process is lengthy, time consuming and inherently unpredictable, and if we are ultimately unable to obtain marketing approval for the product candidates we intend to develop, our business may be substantially harmed. |

| ● | We may encounter substantial delays in completing our clinical studies which in turn will require additional costs, or we may fail to demonstrate adequate safety and efficacy to the satisfaction of applicable regulatory authorities. If we are not able to obtain any required regulatory approvals for our product candidates, we will not be able to commercialize our product candidates and our ability to generate revenue will be limited. |

| ● | Conducting successful clinical studies may require the enrollment of large numbers of patients, and suitable patients may be difficult to identify and recruit. |

| ● | We rely on and intend to rely on third parties to conduct our clinical trials, to assist us with pre-clinical development and for manufacturing and marketing of our proposed product candidates. If we are not able to secure favorable arrangements with such third parties, or such third parties do not perform as contractually required or expected, we may not be able to obtain regulatory approval for or commercialize our products and our business and financial condition could be harmed. |

| ● | Even if our product candidates are approved by regulatory authorities, if we or our suppliers fail to comply with ongoing U.S. Food and Drug Administration regulations or if we experience unanticipated problems with our products, these products could be subject to restrictions or withdrawal from the market. |

| ● | Our revenue stream will depend upon third-party reimbursement. |

| ● | Our products will face significant competition, and if they are unable to compete successfully, our business will suffer. |

| ● | If we fail to comply with healthcare regulations, we could face substantial enforcement actions, including civil and criminal penalties and our business, operations and financial condition could be adversely affected. |

iii

Risk Related to our Intellectual Property Rights

| ● | Our business depends upon us securing and protecting critical intellectual property. |

| ● | We rely upon licenses granted to us by various licensors, and if such licensors do not adequately defend such licenses, our business may be harmed. |

| ● | Patent positions in our industry are highly uncertain and involve complex legal and factual questions. |

Risk Related to our Company

| ● | We have expanded and may continue to expand, our business through the acquisition of rights to new drug candidates that could disrupt our business, harm our financial condition and may also dilute current shareholders’ ownership interests in our Company. |

| ● | If a product liability claim is successfully brought against us for uninsured liabilities, or such claim exceeds our insurance coverage, we could be forced to pay substantial damage awards that could materially harm our business. |

| ● | Any international operations we undertake may subject us to risks inherent with operations outside of the United States. |

| ● | Our Amended and Restated Bylaws provide that the Eighth Judicial District Court of Clark County, Nevada will be the sole and exclusive forum for certain disputes which could limit shareholders’ ability to obtain a favorable judicial forum for disputes with us or our directors, officers, employees or agents. |

General Risk Factors

| ● | Market and economic conditions may negatively impact our business, financial condition and share price. |

| ● | Future sales and issuances of our securities could result in additional dilution of the percentage ownership of our shareholders and could cause our share price to fall. |

| ● | We do not intend to pay cash dividends on our shares of common stock so any returns will be limited to the value of our shares. |

| ● | If we are unable to maintain listing of our securities on The Nasdaq Capital Market or any stock exchange, our stock price could be adversely affected and the liquidity of our stock and our ability to obtain financing could be impaired. |

iv

PART I

Throughout this Annual Report on Form 10-K, the “Company,” “Hoth,” “we,” “us,” and “our” refers to Hoth Therapeutics, Inc., individually, or as the context requires, collectively with its subsidiary, Hoth Therapeutics Australia Pty Ltd.

ITEM 1. BUSINESS

Overview

We are a clinical-stage biopharmaceutical company focused on developing new generation therapies for unmet medical needs. We are focused on developing (i) a topical formulation for treating side effects from drugs used for the treatment of cancer; (ii) a treatment for mast-cell derived cancers and anaphylaxis; and (iii) a treatment and/or prevention for Alzheimer’s or other neuroinflammatory diseases. We also have preclinical assets being developed for (i) atopic dermatitis (also known as eczema); (ii) a treatment for asthma and allergies using inhalational administration; (iii) a treatment for lung diseases resulting from bacterial infections; and (iv) a treatment for inflammatory bowel diseases. We are also developing a diagnostic device via a mobile device.

Primary Development:

HT-001

On February 1, 2020, we entered into a patent license agreement with The George Washington University (“GW”) pursuant to which GW granted us a license to certain patent rights to, among other things, make, use, offer and sell certain licensed products throughout the world with respect to HT-001 which we intend to potentially use for treating dermatological side effects from epidermal growth factor receptor (“EGFR”) inhibitors, and potentially other drugs used for the treatment of cancer. HT-001 is a topical formulation under development for the treatment of patients with rash and skin disorders associated with initial and repeat courses of tyrosine kinase EGFR inhibitor therapy. EGFR inhibitors are used for the treatment of cancers with EGFR up-regulation (such as non-small cell lung cancer, pancreatic cancer, breast cancer and colon cancer); however, EGFR inhibitors are often associated with dose-limiting skin toxicities that can result in the interruption or reduction of treatment. HT-001 is targeted to treat these EGFR-induced skin disorders to allow patients to achieve the best potential outcomes of EGFR therapy. HT-001 has achieved positive results in its initial pre-clinical studies conducted at GW. In December 2020, we submitted a pre-IND meeting request to the FDA with respect to HT-001 as a concomitant therapy with EGFR inhibitors. In preparation for such pre-IND meeting, we prepared and submitted to the FDA our IND-opening clinical trial plan in January 2021, which includes two phase 2 trials conducted in patients. Based on the FDA’s feedback, we intend to advance our IND-enabling activities for HT-001 as planned. We have engaged Worldwide Clinical Trials (“Worldwide”) as our clinical research organization to provide clinical management, data management, biostatistical, medical monitoring, pharmacovigilance, and other related services to support the CLEER1 Phase 2a clinical trial in the United States.

We believe that the key elements for our market success with respect to HT-001 include:

| ● | To our knowledge, there are currently no drugs approved for the treatment of skin toxicities associated with EFGR inhibitor therapy and 49-100% of patients develop skin toxicities during EGFR inhibitory therapy; |

| ● | The main active ingredient of HT-001 is already approved in oral and IV dosage forms which supports pursuit of the 505(b)(2) regulatory pathway to reduce development time and cost; |

| ● | To our knowledge, there are no current topical formulations available using HT-001’s active ingredient so we believe that there is no direct market competition; and |

| ● | We have the potential to pursue other indications such as chronic pruritus, atopic dermatitis and other skin toxicities that develop from anti-cancer therapies using the HT-001 formulation. |

1

HT-KIT

We have obtained from North Carolina State University an exclusive, worldwide, royalty bearing license to certain intellectual property to, among other things, discover, develop, make, have made, use and sell certain licensed products and sell, use and practice certain licensed services with respect to cancer and anaphylaxis; this is being developed as HT-KIT. The HT-KIT drug is designed to more specifically target the receptor tyrosine kinase KIT in mast cells, which is required for the proliferation, survival and differentiation of bone marrow-derived hematopoietic stem cells. Mutations in the KIT pathway have been associated with several human cancers, such as gastrointestinal stromal tumors and mast cell-derived cancers (mast cell leukemia and mast cell sarcoma). Based on the initial proof-of-concept success, we intend to initially target mast cell neoplasms for development of HT-KIT, which is a rare, aggressive cancer with poor prognosis.

The same target, KIT, also plays a key role in mast cell-mediated anaphylaxis, a serious allergic reaction that is rapid in onset and may cause death. Anaphylaxis typically occurs after exposure to an external allergen that results in an immediate and severe immune response. We also intend to pursue the anaphylaxis indication for HT-KIT in parallel to cancer treatment.

On December 21, 2021, we submitted an Orphan Drug Designation (“ODD”) request to the U.S. Food and Drug Administration (“FDA”) for HT-KIT for the treatment of mastocytosis, and on March 10, 2022, we received ODD for HT-KIT for the treatment of mastocytosis. Drugs intended to treat orphan diseases (rare diseases that affect less than 200,000 people in the U.S.) are eligible to apply for ODD, which provides benefits such as 7 year marketing exclusivity and tax incentives to the sponsor during development and after approval.

HT-ALZ

On February 23, 2021, we filed a provisional patent application with the United States Patent and Trademark Office for the use of the active ingredient of HT-001 to treat and prevent Alzheimer’s disease and other neuroinflammatory diseases.

We intend to develop HT-ALZ for use in patients following the Section 505(b)(2) regulatory pathway of the FDA rules. Section 505(b)(2) of the Federal Food, Drug, and Cosmetic Act (“FDCA”) was enacted to enable sponsors to seek New Drug Application (“NDA”) approval for novel repurposed drugs without the need for such sponsors to undertake time consuming and expensive pre-clinical safety studies and Phase 1 safety studies. Proceeding under this regulatory pathway, we will be able to rely upon publicly available data with respect to our active ingredient in our NDA submission to the FDA for marketing approval.

On June 7, 2021, we entered into a sponsored research agreement with The Washington University to investigate the effects of HT-ALZ on behavioral and pathological markers of Alzheimer’s disease and to determine if HT-ALZ can improve learning and memory in an animal model of Alzheimer’s disease. Our study will also determine if behavior is improved utilizing HT-ALZ in blocking NK-1Rs. The study commenced in August 2021 and we expect preclinical results in 2022.

The BioLexa Platform

We have obtained an exclusive license from the University of Cincinnati to make, use, have made, import, offer for sale, and sell products based upon or involving the use of (i) topical compositions comprising a zinc chelator and gentamicin and (ii) zinc chelators to inhibit biofilm formation (the “BioLexa Platform” or “BioLexa”). The license enables us to develop the platform for any indications in humans.

The BioLexa Platform is a proprietary, patented, drug compound platform for the treatment of eczema. It combines an FDA approved zinc chelator with one or more approved antibiotics in a topical dosage form to address unchecked eczema flare-ups by preventing the formation of infectious biofilms and the resulting clogging of sweat ducts.

2

The technology is based on scientific research into the mechanism of Staphylococcus biofilm formation conducted by Andrew B. Herr, PhD at the University of Cincinnati. Dr. Herr conducted multiple in-vitro experiments, or experiments conducted in a controlled environment outside of a living organism, demonstrating that chelation of zinc can prevent Staphylococcus bacteria from forming complex colonies called a biofilm. Biofilms are used by bacteria as a defense mechanism against the host immune response and antibiotics. Prevention of the biofilm formation leaves the bacteria in their planktonic, or single cell state and susceptible to host immune defenses and antibiotic therapy. Dr. Herr’s in-vitro work demonstrating that zinc is an enabler for staph-biofilm formation led to the design and implementation of a series of in-vivo experiments, or experiments conducted using living organisms. These experiments were conducted at the University of Miami using a minipig wound infection model and intended to demonstrate that the combination of zinc removal, or chelation, and broad spectrum antibiotic therapy was more effective than either approach on its own. These positive results supported development of the BioLexa Platform for multiple indications with staph-biofilms as the causative agent.

We intend to develop the BioLexa Platform for use in patients following the Section 505(b)(2) regulatory pathway of the FDA rules. Section 505(b)(2) of the Federal Food, Drug and Cosmetic Act (“FDCA”) was enacted to enable sponsors to seek New Drug Application (“NDA”) approval for novel repurposed drugs without the need for such sponsors to undertake time consuming and expensive pre-clinical safety studies and Phase 1 safety studies. Proceeding under this regulatory pathway, we will be able to rely upon publicly available data with respect to gentamicin and zinc chelator in our NDA submission to the FDA for marketing approval.

In September 2018, we attended the first of a series of meetings with the FDA to review the requirements for submission and activation of an investigational new drug application (“IND”) with respect to the BioLexa Platform for use in eczema. We prepared and presented to the FDA our proposed first in human clinical trial plan for the treatment of eczema in patients over the age of one year old, and the FDA provided us with general guidance with respect to specific animal studies, dosing schedules and suggested human safety studies before we commence clinical trials in pediatric or adult patients. The FDA requested that safety and efficacy of BioLexa be established in adults prior to investigating pediatric and adolescent patients. Therefore, we planned to conduct our first clinical trial for BioLexa in Australia in order to enroll both adult and adolescents to support future clinical development.

On December 9, 2020, we received approval from the Belberry Human Research Ethics Committee (“HREC”) in Australia to conduct our clinical trial of BioLexa, and we have engaged Novotech (Australia) Pty Limited (“Novotech”) as our local clinical research organization in Australia to provide clinical management, data management, biostatistical, medical monitoring, pharmacovigilance, and other related services to support the first in human clinical trial of BioLexa. Phase 1 of the trial was initiated in 2021 and is expected to conclude in 2022.

We believe that the key elements for our market success with respect to BioLexa include:

| ● | the proprietary formulation of two FDA-approved drugs to treat bacterial proliferation which may reduce development time and costs by giving us the ability to rely on safety and efficacy data from the two approved drugs; | |

| ● | our proprietary formulation is not a topical corticosteroid, and provides a novel mechanism of action and potentially a preferred safety profile as a market differentiator; and | |

| ● | the literature set forth below reaffirms the critical role that S. aureus plays in the development of atopic dermatitis flare-ups within the international medical community, supporting the targeted mechanism of action of BioLexa.

Shi et al, “MRSA Colonization is Associated with Decreased Skin Commensal Bacteria in Atopic Dermatitis,” Invest Dermatol. 2018.

Blicharz, et al, “Staphylococcus aureus: an underestimated factor in the pathogenesis of atopic dermatitis?,” Adv Dermatol Allergol 2019. |

3

Preclinical Development

HT-003

On July 30, 2020 (the “Isoprene Effective Date”), we entered into a Sublicense Agreement (the “Isoprene Sublicense Agreement”) with Isoprene Pharmaceuticals, Inc. (“Isoprene”) pursuant to the commercial evaluation sublicense and option agreement dated March 8, 2019 by and among us, the University of Maryland, Baltimore and Isoprene. Pursuant to the Isoprene Sublicense Agreement, Isoprene granted us an exclusive sublicense to certain intellectual property (i) to make, have made, use, sell, offer to sell and import certain licensed products, (ii) in connection therewith, to use certain inventions and licensed materials and (iii) to practice certain patent rights for the treatment of dermatological conditions or diseases, referred to as HT-003. The retinoic acid metabolism blocking agents (“RAMBAs”) have the potential to be developed as a platform for multiple inflammatory-based indications. Accordingly, we entered into a Sublicense Agreement with Isoprene on July 2, 2021 pursuant to the option agreement dated December 22, 2020 to expand the therapeutic indication of the sublicensed RAMBAs from Isoprene to include inflammatory bowel diseases, including Crohn’s disease and ulcerative colitis.

Retinoids, which include Vitamin A (retinol) and its analogues (both synthetic and metabolites), play a critical role in cell signaling and biological processes, including regulation of immune cells and inflammation, signaling pathways that control normal skin maintenance, embryonic development and cell growth/differentiation/repair. Deficiencies in retinoids and their active metabolites have been implicated in a wide variety of diseases. In the skin, retinol deficiency leads to hyperkeratosis and keratinizing metaplasia that is observed in skin disorders like psoriasis and acne. Vitamin A and retinoic acid also play a crucial role in regulating cell proliferation, differentiation, and apoptosis and therefore, altered metabolism of retinoids has been suspected as playing a potential role in tumorigenesis. Accordingly, retinoids have been approved in the U.S. for treatment of acne and psoriasis as well as other therapeutic indications such as acute promyelocytic leukemia and cutaneous T-cell lymphoma; however, the therapeutic use of exogenous retinoids has been limited due to negative effects associated with high systemic concentrations. A new therapeutic approach to increase intracellular retinoic acid (the active metabolite of retinol) potentially without causing negative side effects of exogenous retinoic acid is to use inhibitors of RAMBAs, which prolong the presence of retinoic acid. HT-003 is a novel RAMBA under investigation for topical treatment in acne and psoriasis applications.

In December 2019, we entered into a research collaboration agreement with Weill Cornell Medicine for the completion of pre-clinical studies investigating the mechanism of action of HT-003 that was renewed in January 2021 as a result of positive preclinical results. Dr. Jonathan Zippin, M.D., Ph.D., FAAD, Associate Professor of Dermatology at Weill Cornell Medicine and our Senior Scientific Advisor, is the principal investigator for such pre-clinical studies.

Preclinical proof-of-concept studies began in the first quarter of 2021 for the investigation of RAMBAs for treatment of inflammatory bowel diseases, including Crohn’s disease and ulcerative colitis.

HT-004

On November 20, 2019, we entered into a license agreement with North Carolina State University (“NC State”) pursuant to which NC State granted us an exclusive license to, among other things, develop, make, use, offer and sell certain licensed products throughout the world with respect to HT-004 for treating allergic diseases. HT-004 is a potential disease-modifying agent that uses exon-skipping oligonucleotide-targeted methods to reduce mast cell responses to immunoglobulin E (IgE)-directed antigens, which is one of the key mechanisms in the pathophysiology of asthma, atopic dermatitis and other allergic diseases. HT-004 is currently under investigation for the treatment of asthma and allergies using inhalational administration.

Preclinical proof-of-concept data was generated in October 2020 supporting efficacy of HT-004 after inhalational delivery in a mouse model. Critical proof-of-concept studies in a humanized mouse model are planned to be conducted in 2022. These studies are being conducted by our Scientific Advisory Board member, Dr. Glenn Cruse, at NC State.

We believe that the key elements for our market success with respect to HT-004 include:

| ● | To our knowledge, there are currently no disease-modifying agents for asthma or allergy diseases; |

| ● | The active pharmaceutical ingredient in HT-004 is a novel molecular class that we believe would prevent generic competition after commercialization; |

| ● | HT-004 is being developed for inhalational administration by either inhaler or nebulizer for easy access at home by patients; and |

| ● | HT-004 is applicable for both adult and pediatric patient populations with asthma and/or allergies. |

4

HT-006

On December 22, 2020, we entered into a non-exclusive commercial evaluation license agreement with the U.S. Army Medical Research and Development Command (“USAMRDC”), as amended, pursuant to which USAMRDC granted us a non-exclusive commercial evaluation license to HT-006 for the treatment of lung diseases resulting from bacterial infections. We will initially target treatment of serious bacterial infections of the lung, such as hospital-acquired pneumonia (“HAP”) and ventilator-associated pneumonia (“VAP”). Given the indication, we intend to develop HT-006 for inhalational administration.

Both HAP and VAP are considered life-threatening diseases for which current treatment options are limited or not effective against multi-drug resistance bacteria. As such, we intend to pursue streamlined development opportunities under the FDA’s program for “antibacterial therapies for patients with an unmet medical need for the treatment of serious bacterial diseases.” This streamlined program allows for the use of nonclinical animal studies to reduce clinical studies required for approval.

HT-002

On May 18, 2020, we entered into an Exclusive License Agreement with the Virginia Commonwealth University Intellectual Property Foundation (“VCU”) pursuant to which VCU granted us an exclusive, royalty bearing license to HT-002, a novel peptide developed by researchers at VCU that may be used to slow the transmission of SARS-CoV-2 (the “VCU Peptide”) and a non-exclusive royalty bearing, worldwide license with respect to certain licensed technical information patents to make, have made, use, offer to sell, sell and import certain licensed products and perform certain licensed services. On June 29, 2020, we entered into a Sponsored Project Agreement (“VCU SPA”) with VCU for the development of a potential COVID-19 treatment using the VCU Peptide. The VCU SPA was amended on April 28, 2021 to extend the period of research and to add additional scope of investigation to include the variants of SARS-CoV-2.

Proof-of-Concept preclinical studies are expected to be completed in 2022.

Direct Detect Breath Diagnostic Device

On August 7, 2020, we entered into a Patent License Agreement (“GW Patent License Agreement”) with GW pursuant to which GW granted us an exclusive, worldwide, royalty bearing license to certain intellectual property that can be used to develop a device designed to detect the presence of viruses. Specifically, the GW Patent License Agreement permits us to make, have made, use, import, offer for sale and sell certain licensed products in the field of virus sensing and detection. We have engaged a company to develop a platform prototype and, once developed, we will select target analytes for further development.

5

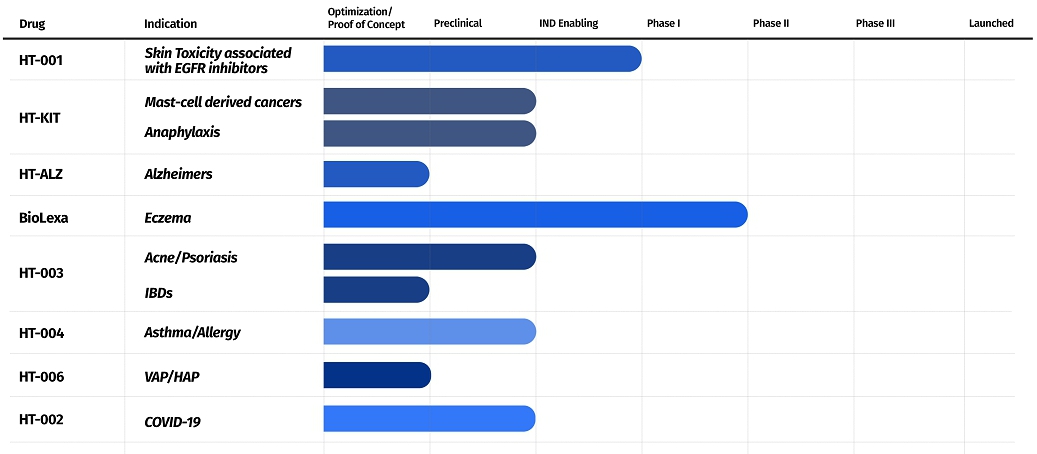

Product Development Pipeline

The following table summarizes our product development pipeline.

Other Interests

We have interests in certain other assets being developed by third parties. Specifically, in December 2021, we entered into a license agreement with Zylö Therapeutics, Inc. (“Zylö”) with respect to the development of HT-005. We had previously entered into a sublicense agreement with Zylö pursuant to which we had advanced the development of HT-005 for patients with lupus. (See Note 6 to the consolidated financial statements for a discussion of our agreement with Zylö). In addition, in March 2020, we entered into a Royalty and Development Agreement (the “Voltron Agreement”) with Voltron Therapeutics, Inc. with respect to the development of potential product candidates for the prevention of COVID-19. (See Note 6 to the consolidated financial statements for a discussion of our agreement with Voltron).

Competition

The biopharmaceutical industry utilizes rapidly advancing technologies and is characterized by intense competition. There is also a strong emphasis on intellectual property and proprietary products. In the segment of the biopharmaceutical industry, competition from different sources including major biopharmaceutical companies, academic institutions, government agencies, and public and private research institutions will continue. Many of our competitors have significantly greater financial resources and expertise in product candidate development and may have progressed further toward approval and marketing. In addition, smaller or early-stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large and established companies.

Manufacturing and Supply

We do not have any manufacturing capability and therefore we currently rely on and intend to continue to rely on contract manufacturing organizations to produce our product candidates in accordance with regulatory requirements.

Commercialization

Our success depends not only on the successful development and approval of our products candidates but also on the commercialization of our potential products. If and when our product candidates receive regulatory approval, we intend to engage third-parties such as pharmaceutical and biotechnology companies for the commercialization of our products.

Intellectual Property Portfolio

Our goal is to obtain, maintain and enforce patent protection for our products, formulations, processes, methods and other proprietary technologies, preserve our trade secrets, and operate without infringing on the proprietary rights of other parties, both in the U.S. and in other countries. Our policy is to actively seek the broadest intellectual property protection possible for our products, proprietary information and proprietary technology through a combination of contractual arrangements and patents, both in the U.S. and elsewhere in the world. In addition, we intend to actively pursue product life-cycle management initiatives to extend our market exclusivity.

6

We intend to cement our market exclusivity in conjunction with our formulation-development partners through additional patents based on the pharmaceutical and clinical characteristics of our product candidates in the proprietary formulation and through the introduction of line extensions such as combination drugs and new formulations.

In addition to any granted patents, our products may be eligible for market exclusivity to run concurrently with the term of the patent for three and a half years in the U.S. pursuant to the Hatch-Waxman Act and pediatric exclusivity guideline and up to ten years of market exclusivity in the E.U. which includes eight years of data exclusivity and two years of market exclusivity from the date we file an NDA or the European equivalent referred to as Marketing Authorization Application.

We currently have licenses to six U.S. patents and one pending U.S. patent application, and we have licenses to three patents issued in Europe and Australia and five pending patent applications in foreign jurisdictions including Europe, Brazil, Canada and Hong Kong. Hoth also holds two pending U.S. patent applications and one pending PCT patent application.

In addition to patents, we rely on trade secrets and know-how and continuing technological innovation to develop and maintain our competitive position. However, trade secrets and know-how can be difficult to protect. We take measures to protect and maintain the confidentiality of proprietary information in order to protect aspects of the business that are not amenable to, or that we do not consider appropriate for, patent protection. We require employees, consultants, outside scientific partners, sponsored researchers and other advisors to execute confidentiality agreements with us on or prior to the commencement of employment or consulting relationships with us.

Government Regulations

Governmental authorities in the U.S. and other countries extensively regulate the research, development, testing, manufacture, labeling, promotion, advertising, distribution and marketing of pharmaceutical products, including biological products, and medical devices, such as those being developed by us. In the U.S., the FDA regulates such products under the FDCA and the Public Health Services Act and implements related regulations. Failure to comply with applicable FDA requirements, both before and after approval, may subject us to administrative and judicial sanctions, such as a delay in approving or refusal by the FDA to approve pending applications, warning letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions and/or criminal prosecution.

U.S. Food and Drug Administration Regulations

United States Drug Development

In the United States, the FDA regulates drugs (including biological products, such as vaccines), medical devices and combinations of drugs and devices, or combination products, under the FDCA and its implementing regulations. These products are also subject to other federal, state and local statutes and regulations. The process of obtaining regulatory approvals and the subsequent compliance with appropriate federal, state, local and foreign statutes and regulations requires the expenditure of substantial time and financial resources. Failure to comply with the applicable U.S. requirements at any time during the product development process, approval process or after approval, may subject an applicant to administrative or judicial sanctions. These sanctions could include, among other actions, the FDA’s refusal to approve pending applications, withdrawal of an approval, a clinical hold, untitled or warning letters, requests for voluntary product recalls or withdrawals from the market, product seizures, total or partial suspension of production or distribution injunctions, fines, refusals of government contracts, restitution, disgorgement, or civil or criminal penalties. Any agency or judicial enforcement action could have a material adverse effect on us.

7

The process required by the FDA before a drug may be marketed in the United States generally involves the following:

| ● | completion of extensive pre-clinical laboratory tests, animal studies and formulation studies in accordance with applicable regulations, including the FDA’s Good Laboratory Practice regulations; |

| ● | submission to the FDA of an IND, which must become effective before human clinical trials may begin; |

| ● | performance of adequate and well-controlled human clinical trials in accordance with an applicable IND and other clinical study related regulations, referred to as good clinical practice (“GCP”), to establish the safety and efficacy of the proposed drug for its proposed indication; |

| ● | submission to the FDA of an NDA or biologics license application (“BLA”); |

| ● | satisfactory completion of an FDA pre-approval inspection of the manufacturing facility or facilities at which the product, or components thereof, are produced to assess compliance with the FDA’s current good manufacturing practice (“cGMP”) requirements; |

| ● | potential FDA audit of the clinical trial sites that generated the data in support of the NDA or BLA; and |

| ● | FDA review and approval of the NDA or BLA prior to any commercial marketing or sale. |

Human clinical trials are typically conducted in three sequential phases that may overlap or be combined:

| ● | Phase 1. The product is initially introduced into a small number of healthy human subjects or patients and tested for safety, dosage tolerance, absorption, metabolism, distribution and excretion and, if possible, to gain early evidence on effectiveness. In the case of some products for severe or life-threatening diseases, especially when the product is suspected or known to be unavoidably toxic, the initial human testing may be conducted in patients. |

| ● | Phase 2. Involves clinical trials in a limited patient population to identify possible adverse effects and safety risks, to preliminarily evaluate the efficacy of the product for specific targeted diseases and to determine dosage tolerance and optimal dosage and schedule. |

| ● | Phase 3. Clinical trials are undertaken to further evaluate dosage, clinical efficacy and safety in an expanded patient population at geographically dispersed clinical trial sites. These clinical trials are intended to establish the overall risk/benefit relationship of the product and provide an adequate basis for product labeling. |

Post-approval trials, sometimes referred to as Phase 4 clinical trials, may be conducted after initial marketing approval. These studies are used to gain additional experience from the treatment of patients in the intended therapeutic indication. In certain instances, the FDA may mandate the performance of Phase 4 trials. Phase 1, Phase 2 and Phase 3 clinical trials may not be completed successfully within any specified period, if at all. The FDA or the clinical trial sponsor may suspend or terminate a clinical trial at any time on various grounds, including a finding that the research subjects or patients are being exposed to an unacceptable health risk. Similarly, an Institutional Review Board (“IRB”), which oversees the conduct of clinical trials, can suspend or terminate approval of a clinical trial at its institution if the clinical trial is not being conducted in accordance with the IRB’s requirements or if the product has been associated with unexpected serious harm to patients. Additionally, some clinical trials are overseen by an independent group of qualified experts organized by the clinical trial sponsor, known as a data safety monitoring board or committee. This group provides authorization for whether a trial may move forward at designated check points based on access to certain data from the study. The clinical trial sponsor may also suspend or terminate a clinical trial based on evolving business objectives and/or competitive climate.

8

FDA Review Process

The results of product development, pre-clinical studies and clinical trials, along with descriptions of the manufacturing process, analytical tests conducted on the drug, proposed labeling and other relevant information, are submitted to the FDA as part of an NDA for a new drug, or BLA for a biological product, requesting approval to market the product. The submission of an NDA or BLA is subject to the payment of a substantial user fee, and the sponsor of an approved NDA or BLA is also subject to an annual program user fee; although a waiver of such fee may be obtained under certain limited circumstances.

The FDA reviews all NDAs submitted before it accepts them for filing and may request additional information rather than accepting an NDA for filing. Under the goals and policies agreed to by the FDA under the Prescription Drug User Fee Act (“PDUFA”), the FDA’s goal to complete its substantive review of a standard NDA and respond to the applicant is ten months from the receipt of the NDA. The FDA does not always meet its PDUFA goal dates, and the review process is often significantly extended by FDA requests for additional information or clarification and may go through multiple review cycles.

The review and evaluation of an NDA or BLA by the FDA is extensive and time consuming and may take longer than originally planned to complete, and we may not receive a timely approval, if at all.

Before approving an NDA, the FDA will conduct a pre-approval inspection of the manufacturing facilities for the new product to determine whether they comply with cGMPs. The FDA will not approve the product unless it determines that the manufacturing processes and facilities are in compliance with cGMP requirements and adequate to assure consistent production of the product within required specifications. In addition, before approving an NDA, the FDA may also audit data from clinical trials to ensure compliance with GCP requirements.

There is no assurance that the FDA will ultimately approve a product for marketing in the United States, and we may encounter significant difficulties or costs during the review process. If a product receives marketing approval, the approval may be significantly limited to specific diseases and dosages or the indications for use may otherwise be limited, which could restrict the commercial value of the product. Further, the FDA may require that certain contraindications, warnings or precautions be included in the product labeling or may condition the approval of the NDA or BLA on other changes to the proposed labeling, development of adequate controls and specifications, or a commitment to conduct post-market testing or clinical trials and surveillance to monitor the effects of approved products. For example, the FDA may require Phase 4 clinical trials to further assess drug safety and effectiveness and may require testing and surveillance programs to monitor the safety of approved products that have been commercialized. The FDA may also place other conditions on approvals, including the requirement for a risk evaluation and mitigation strategy (“REMS”), to assure the safe use of the drug.

Section 505(b)(2) Regulatory Approval Pathway

Section 505(b)(2) of the FDCA provides an alternate regulatory pathway for approval of a new drug by allowing the FDA to rely on data not developed by the applicant. Specifically, Section 505(b)(2) permits the submission of an NDA where one or more of the investigations relied upon by the applicant for approval was not conducted by or for the applicant and for which the applicant has not obtained a right of reference. The applicant may rely upon published literature and/or the FDA’s findings of safety and effectiveness for an approved drug already on the market. Approval or submission of a 505(b)(2) application, like those for abbreviated new drugs (“ANDAs”), may be delayed because of patent and/or exclusivity rights that apply to the previously approved drug.

A 505(b)(2) application may be submitted for a new chemical entity (“NCE”) when some part of the data necessary for approval is derived from studies not conducted by or for the applicant and when the applicant has not obtained a right of reference.

Section 505(b)(2) applications also may be entitled to marketing exclusivity if supported by appropriate data and information. Three-year new data exclusivity may be granted to the 505(b)(2) application if one or more clinical investigations conducted in support of the application, other than bioavailability/bioequivalence studies, were essential to the approval and conducted or sponsored by the applicant. Five years of marketing exclusivity may be granted if the application is for an NCE, and pediatric exclusivity is likewise available.

9

Orange Book Listing and Paragraph IV Certification

For NDA submissions, including those under Section 505(b)(2), applicants are required to list with the FDA certain patents with claims that cover the applicant’s product. Upon approval, each of the patents listed in the application is published in Approved Drug Products with Therapeutic Equivalence Evaluations, commonly referred to as the Orange Book. Any applicant who subsequently files an ANDA or 505(b)(2) NDA that references a drug listed in the Orange Book must certify to the FDA that (1) no patent information on the drug product that is the subject of the application has been submitted to the FDA; (2) such patent has expired; (3) the date on which such patent expires; or (4) such patent is invalid or will not be infringed upon by the manufacture, use or sale of the drug product for which the application is submitted. This last certification is known as a Paragraph IV Certification.

If an applicant has provided a Paragraph IV Certification to the FDA, the applicant must also send notice of the Paragraph IV Certification to the holder of the NDA for the approved drug and the patent owner once the application has been accepted for filing by the FDA. The NDA holder or patent owner may then initiate a patent infringement lawsuit in response to notice of the Paragraph IV Certification. The filing of a patent infringement lawsuit within 45 days of the receipt of a Paragraph IV Certification prevents the FDA from approving the ANDA or 505(b)(2) application until the earlier of 30 months from the date of the lawsuit, the applicant’s successful defense of the suit, or expiration of the patent.

United States Medical Device Regulation

Medical devices, including diagnostic test devices, also are subject to extensive and rigorous regulation by the FDA under the FDCA, as well as other federal and state regulatory bodies in the United States, and laws and regulations of foreign authorities in other countries. FDA requirements specific to medical devices are wide ranging and govern, among other things, the design, development and manufacturing, human clinical trials, preclearance or approval, advertising and promotion, and product import and export. Unless an exemption applies, medical devices distributed in the United States must receive either premarket clearance under Section 510(k) of the FDCA or premarket approval of a premarket application (“PMA”). During the COVID-19 public health emergency, the FDA has authorized COVID-19 diagnostic tests under its Emergency Use Authorization authority. Medical devices are classified into one of three classes—Class I, Class II, or Class III—depending on the degree or risk associated with each medical device and the extent of control needed to ensure safety and effectiveness. Medical devices deemed to pose relatively low risk are placed in either Class I or II. Class II devices generally require the manufacturer to submit a premarket notification under Section 510(k) of the FDCA requesting permission for commercial distribution. Devices deemed by the FDA to pose the greatest risk, such as life-sustaining, life-supporting or implantable devices are placed in Class III requiring PMA approval.

Reimbursement

Potential sales of any of our product candidates, if approved, will depend, at least in part, on the extent to which such products will be covered by third-party payors, such as government health care programs, commercial insurance and managed healthcare organizations. These third-party payors are increasingly limiting coverage and/or reducing reimbursements for medical products and services. A third-party payor’s decision to provide coverage for a drug product does not imply that an adequate reimbursement rate will be approved. Further, one payor’s determination to provide coverage for a drug product does not assure that other payors will also provide coverage for the drug product. In addition, the U.S. government, state legislatures and foreign governments have continued implementing cost-containment programs, including price controls, restrictions on reimbursement and requirements for substitution of generic products. Adoption of price controls and cost-containment measures, and adoption of more restrictive policies in jurisdictions with existing controls and measures, could further limit our future revenues and results of operations. Decreases in third-party reimbursement or a decision by a third-party payor to not cover a product candidate, if approved, or any future approved products could reduce physician usage of our products, and have a material adverse effect on our sales, results of operations and financial condition.

In the United States, the Medicare Part D program provides a voluntary outpatient drug benefit to Medicare beneficiaries for certain products. We do not know whether our product candidates, if approved, will be eligible for coverage under Medicare Part D, but individual Medicare Part D plans offer coverage subject to various factors such as those described above. Furthermore, private payors often follow Medicare coverage policies and payment limitations in setting their own coverage policies.

10

Orphan Drug Designation

Under the Orphan Drug Act, the FDA may grant orphan designation to a drug or biologic intended to treat a rare disease or condition, which is a disease or condition that affects fewer than 200,000 individuals in the United States, or more than 200,000 individuals in the United States for which there is no reasonable expectation that the cost of developing and making available in the United States a drug or biologic for this type of disease or condition will be recovered from sales in the United States for that drug or biologic. Orphan drug designation must be requested before submitting an NDA or BLA. After the FDA grants orphan drug designation, the generic identity of the therapeutic agent and its potential orphan use are disclosed publicly by the FDA. The orphan drug designation does not convey any advantage in, or shorten the duration of, the regulatory review or approval process.

If a product that has orphan drug designation subsequently receives the first FDA approval for the disease for which it has such designation, the product is entitled to orphan drug exclusive approval (or exclusivity), which means that the FDA may not approve any other applications, including a full NDA or BLA, to market the same drug for the same indication for seven years, except in limited circumstances, such as a showing of clinical superiority to the product with orphan drug exclusivity. Orphan drug exclusivity does not prevent the FDA from approving a different drug or biologic for the same disease or condition, or the same drug or biologic for a different disease or condition. Among the other benefits of orphan drug designation are tax credits for certain research and a waiver of the application user fee.

A designated orphan drug may not receive orphan drug exclusivity if it is approved for a use that is broader than the indication for which it received orphan designation. In addition, exclusive marketing rights in the United States may be lost if the FDA later determines that the request for designation was materially defective or if the manufacturer is unable to assure sufficient quantities of the product to meet the needs of patients with the rare disease or condition.

Healthcare Laws and Regulations

Sales of our product candidates, if approved, or any other future product candidate will be subject to healthcare regulation and enforcement by the federal government and the states and foreign governments in which we might conduct our business. The healthcare laws and regulations that may affect our ability to operate include the following:

| ● | The federal Anti-Kickback Statute makes it illegal for any person or entity to knowingly and willfully, directly or indirectly, solicit, receive, offer, or pay any remuneration that is in exchange for or to induce the referral of business, including the purchase, order, lease of any good, facility, item or service for which payment may be made under a federal healthcare program, such as Medicare or Medicaid. The term “remuneration” has been broadly interpreted to include anything of value. | |

| ● | Federal false claims and false statement laws, including the federal civil False Claims Act, prohibits, among other things, any person or entity from knowingly presenting, or causing to be presented, for payment to, or approval by, federal programs, including Medicare and Medicaid, claims for items or services, including drugs, that are false or fraudulent. | |

| ● | Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) created additional federal criminal statutes that prohibit among other actions, knowingly and willfully executing, or attempting to execute, a scheme to defraud any healthcare benefit program, including private third-party payors or making any false, fictitious or fraudulent statement in connection with the delivery of or payment for healthcare benefits, items or services. |

| ● | HIPAA, as amended by the Health Information Technology for Economic and Clinical Health Act of 2009 and their implementing regulations, impose obligations on certain types of individuals and entities regarding the electronic exchange of information in common healthcare transactions, as well as standards relating to the privacy and security of individually identifiable health information. | |

| ● | The federal Physician Payments Sunshine Act requires certain manufacturers of drugs, devices, biologics and medical supplies for which payment is available under Medicare, Medicaid or the Children’s Health Insurance Program, with specific exceptions, to report annually to the Centers for Medicare & Medicaid Services information related to payments or other transfers of value made to physicians and teaching hospitals, as well as ownership and investment interests held by physicians and their immediate family members. |

11

Also, many states have similar laws and regulations, such as anti-kickback and false claims laws that may be broader in scope and may apply regardless of payor, in addition to items and services reimbursed under Medicaid and other state programs. Additionally, we may be subject to state laws that require pharmaceutical companies to comply with the federal government’s and/or pharmaceutical industry’s voluntary compliance guidelines, state laws that require drug manufacturers to report information related to payments and other transfers of value to physicians and other healthcare providers or marketing expenditures, as well as state and foreign laws governing the privacy and security of health information, many of which differ from each other in significant ways and often are not preempted by HIPAA.

Additionally, to the extent that our product is sold in a foreign country, we may be subject to similar foreign laws.

Australia

Our first clinical trial for BioLexa will be conducted in Australia. The TGA and the National Health and Medical Research Council set the GCP requirements for clinical research in Australia, and compliance with these codes is mandatory. Australia has also adopted international codes, such as those promulgate by the International Council for Harmonization of Technical Requirements for Registration of Pharmaceuticals for Human Use (“ICH”). The ICH guidelines must be followed across all areas of clinical research, including those related to pharmaceutical quality, nonclinical and clinical data requirements and trial designs. The basic requirements for preclinical data to support a first-in-human trial under ICH guidelines are applicable in Australia. Requirements related to adverse event reporting in Australia are similar to those required in other major jurisdictions.

Clinical trials conducted using “unapproved therapeutic goods” in Australia, being those which have not yet been evaluated by the TGA for quality, safety and efficacy must occur pursuant to either the Clinical Trial Notification Scheme (“CTN Scheme”) or the Clinical Trial Exemption Scheme (“CTX Scheme”). In each case, the trial is supervised by a HREC, an independent review committee set up under guidelines of the Australian National Health and Medical Research Council that ensures the protection of rights, safety and well-being of human subjects involved in a clinical trial. A HREC does this by reviewing, approving and providing continuing examination of trial protocols and amendments, and of the methods and material to be used in obtaining and documenting informed consent of the trial subjects. A HREC reviews the scientific validity of the trial design, the balance of risk versus harm of the therapeutic good, the ethical acceptability of the trial process, and approves the trial protocol. The HREC is also responsible for monitoring the conduct of the trial.

The CTN Scheme broadly involves:

| ● | completion of preclinical laboratory and animal testing; |

| ● | submission to a HREC, of all material relating to the proposed clinical trial, including the trial protocol; |

| ● | the institution or organization at which the trial will be conducted, referred to as the “Approving Authority”, giving final approval for the conduct of the trial at the site, having regard to the advice from the HREC; and |

| ● | the investigator submitting a ‘Notification of Intent to Conduct a Clinical Trial’ form (“CTN Form”) to the TGA. The CTN form must be signed by the sponsor, the principal investigator, the chairman of the HREC and a person responsible from the Approving Authority. The TGA does not review any data relating to the clinical trial however CTN trials cannot commence until the trial has been notified to the TGA. |

Under the CTX Scheme:

| ● | a sponsor submits an application to conduct a clinical trial to the TGA for evaluation and comment; and |

| ● | a sponsor must forward any comments made by the TGA Delegate to the HREC(s) at the sites where the trial will be conducted. |

A sponsor cannot commence a trial under the CTX Scheme until written advice has been received from the TGA regarding the application and approval for the conduct of the trial has been obtained from an ethics committee and the institution at which the trial will be conducted.

12

The Therapeutic Goods Act 1989 (the Act) requires that medical products, including pharmaceuticals, imported into, supplied in, or exported from Australia be included in the Australian Register of Therapeutic Goods (“ARTG”). In order to obtain registration of the product on the ARTG:

| ● | Sponsors must provide a product application containing adequate nonclinical data as well as data from adequate and well-controlled clinical trials that demonstrate the safety and efficacy of the therapeutic product; |

| ● | Sponsors also must provide information demonstrating that the manufacture and quality of the therapeutic product complies with the principles of cGMP; |

| ● | TGA then evaluates the application data, taking into account recommendations from an advisory committee, such as the Advisory Committee on Medicines, which makes recommendations to the TGA as to whether or not to grant approval to include the therapeutic product in the ARTG; and |

| ● | TGA must decide to include the therapeutic product on the ARTG. |

Employees

As of March 28, 2022, we employed a total of 4 full-time employees, 1 employee consultant, and 1 part-time employee. We are not a party to any collective bargaining agreements. We believe that we maintain good relations with our employees.

Our Corporate Information

We were incorporated as a Nevada corporation on May 16, 2017. Our principal executive offices are located at 1 Rockefeller Plaza, Suite 1039, New York, New York 10020 and our telephone number is (646) 756-2997.

Available Information

Our website address is www.hoththerapeutics.com. The contents of, or information accessible through, our website are not part of this Annual Report on Form 10-K, and our website address is included in this document as an inactive textual reference only. We make our filings with the U.S. Securities and Exchange Commission (“SEC”), including our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports, available free of charge on our website as soon as reasonably practicable after we file such reports with, or furnish such reports to, the SEC. The public may read and copy the materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Additionally, the SEC maintains an internet site that contains reports, proxy and information statements and other information. The address of the SEC’s website is www.sec.gov. The information contained in the SEC’s website is not intended to be a part of this filing.

ITEM 1A. RISK FACTORS

An investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors and the other information in this Annual Report on Form 10-K before investing in our common stock. Our business and results of operations could be seriously harmed by any of the following risks. The risks set out below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results. If any of the following events occur, our business, financial condition and results of operations could be materially adversely affected. In such case, the value and trading price of our common stock could decline, and you may lose all or part of your investment.

13

Risks Related to Our Financial Position and Need for Capital

We have generated no revenue from commercial sales to date and our future profitability is uncertain.

We were incorporated in May 2017 and have a limited operating history and our business is subject to all of the risks inherent in the establishment of a new business enterprise. Our likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered in connection with development and expansion of a new business enterprise. Since inception, we have incurred losses and expect to continue to operate at a net loss for at least the next several years as we commence our research and development efforts, conduct clinical trials and develop manufacturing, sales, marketing and distribution capabilities. Our net losses for the years ended December 31, 2021 and 2020 were $14,313,705 and $7,197,816, respectively, and our accumulated deficit as of December 31, 2021 and 2020 was $33,727,163 and $19,413,458, respectively. There can be no assurance that the products under development by us will be approved for sale in the U.S. or elsewhere. Furthermore, there can be no assurance that if such products are approved they will be successfully commercialized, and the extent of our future losses and the timing of our profitability are highly uncertain. If we are unable to achieve profitability, we may be unable to continue our operations.

If we fail to obtain the capital necessary to fund our operations, we will be unable to continue or complete our product development and you will likely lose your entire investment.

We will need to continue to seek capital from time to time to continue development of our product candidates. We cannot provide any assurances that any revenues that we may generate in the future will be sufficient to fund our ongoing operations. We believe that we will need to raise substantial additional capital to fund our operations and the development and commercialization of our product candidates.

Our business or operations may change in a manner that may consume available funds more rapidly than anticipated and substantial additional funding may be required to maintain operations, fund expansion, commercialize our product candidates, develop new or enhanced products, acquire complementary products, business or technologies or otherwise respond to competitive pressures and opportunities, such as a change in the regulatory environment or a change in preferred treatment modalities. In addition, we may need to accelerate the growth of our sales capabilities and distribution beyond what is currently envisioned, and this would require additional capital. However, we may not be able to secure funding on favorable terms, if at all.

If we cannot raise adequate funds to satisfy our capital requirements, we may have to delay, scale back or eliminate our research and development activities, clinical studies or operations. We may also be required to obtain funds through arrangements with collaborators, which arrangements may require us to relinquish rights to certain intellectual property, technologies or products that we otherwise would not consider relinquishing, including rights to future product candidates or certain major geographic markets. This could result in sharing revenues which we might otherwise retain for ourselves. Any of these actions may harm our business, financial condition and results of operations.

The amount of capital we may need depends on many factors, including the progress, timing and scope of our product development programs; the progress, timing and scope of our pre-clinical studies and clinical trials; the time and cost necessary to obtain regulatory approvals; the time and cost necessary to further develop manufacturing processes and arrange for contract manufacturing; our ability to enter into and maintain collaborative, licensing and other commercial relationships; and our partners’ commitment of time and resources to the development and commercialization of our products.

Even if we can raise additional funding, we may be required to do so on terms that are dilutive to you.

The capital markets have been unpredictable in the recent past for unprofitable companies such as ours. The amount of capital that a company such as ours is able to raise often depends on variables that are beyond our control. As a result, we may not be able to secure financing on terms attractive to us, or at all. If we are able to consummate a financing arrangement, the amount raised may not be sufficient to meet our future needs. If adequate funds are not available on acceptable terms, or at all, our business, including our results of operations, financial condition and our continued viability will be materially adversely affected.

14

Risks Related to Product Development, Regulatory Approval, Manufacturing and Commercialization

We are dependent upon the clinical success of our licensed products and technologies. If we are unable to generate revenues from our licensed products and technologies, our ability to create shareholder value may be limited.

We do not currently generate revenues from any of our product candidates, and we may not be successful in obtaining regulatory approvals to commence our clinical trials. If we do not obtain such approvals, the time in which we expect to commence clinical programs for our product candidates will be extended and such extension may increase our expenses and our need for additional capital. Moreover, there is no guarantee that our clinical trials will be successful or that we will continue clinical development in support of an approval from the regulatory agencies for any indication. We note that most drug candidates never reach the clinical stage and even those that do commence clinical development have only a small chance of successfully completing clinical development and gaining regulatory approval. Therefore, our business currently depends entirely on the successful development, regulatory approval and commercialization of our product candidates, which may never occur.

Although we have entered into the Voltron Agreement pursuant to which we and HaloVax intend to jointly develop products to prevent COVID-19, no assurance can be given as to when, if ever, we will be able to develop any products for such purpose and if developed that such products will be successfully commercialized.

In March 2020, we entered into the Voltron Agreement pursuant to which we and HaloVax will work to jointly develop potential products candidates to prevent COVID-19; however, no assurance can be given as to when, if ever, we will be able to develop any products for such purpose. Furthermore, we are subject to risks including, but not limited to, the following with respect to the development of a treatment for COVID-19:

| ● | the Emergency Use Authorization marketing approval processes of the FDA are lengthy, time consuming and inherently unpredictable, and we cannot guarantee that we will ever have a marketable product; |

| ● | we may encounter substantial delays in completing our clinical studies which in turn will require additional costs, or we may fail to demonstrate adequate safety and efficacy to the satisfaction of applicable regulatory authorities; |

| ● | conducting successful clinical studies may require the enrollment of large numbers of patients, and suitable patients may be difficult to identify and recruit; |

| ● | to be commercially successful, physicians must be persuaded that using our products are effective alternatives to other existing therapies and treatments; |

| ● | we may depend on third parties for manufacturing our proposed product candidates and any conflicts with such partners could delay or prevent the development or commercialization of such product candidates; |

| ● | if third-party contract manufacturers upon whom we rely to formulate and manufacture our product candidates do not perform, fail to manufacture according to our specifications or fail to comply with strict regulations, our clinical studies could be adversely affected and the development of our product candidates could be delayed or terminated or we could incur significant additional expenses; |

| ● | adverse events involving our products may lead the FDA to delay or deny clearance for our products or result in product recalls that could harm our reputation, business and financial results; and |

| ● | if we fail to comply with healthcare regulations, we could face substantial enforcement actions, including civil and criminal penalties and our business, operations and financial condition could be adversely affected. |

If our joint venture with HaloVax, LLC (“HaloVax”) is not successful or if we fail to realize the benefits we anticipate from such joint venture, we may not be able to capitalize on the full market potential of our potential products.

In March 2020, we entered into the Voltron Agreement to form a joint venture entity named HaloVax to jointly develop potential product candidates for the prevention of the COVID-19. Pursuant to the terms of the Voltron Agreement we are entitled to receive sales-based royalties at low single digit percentages. In addition, in 2020, we purchased 6% of HaloVax’s outstanding membership interests and shall contribute proceeds of the development of products to prevent COVID-19. If and to the extent we and HaloVax are unable to develop potential product candidates for the prevention of COVID-19, we will not be entitled to any sale-based royalties and the value of our ownership interest in HaloVax could decline in which case we may lose all or part of our investment in HaloVax.

15

While Voltron has agreed to cooperate and use commercially reasonable efforts to exchange information and resources that will lead to the development activities and established a Joint Development Committee consisting of seven members, two of which were selected by us, to plan, review, coordinate and oversee the performance of the development activities and timelines with respect to development activities, we have limited contractual rights to direct its activities. Moreover, we will not have any other control with respect to the operations of HaloVax. Therefore, HaloVax will have a greater influence with respect to its commercialization efforts and other operations. In general, our joint venture with HaloVax subjects us to a number of related risks including that:

| ● | we may not receive sales-based royalties pursuant to the terms of the Voltron Agreement; |

| ● | we may not be successful in the development of any product candidates; |

| ● | HaloVax may not commit sufficient resources to the marketing and distribution of our products; |

| ● | HaloVax may infringe the intellectual property rights of third parties, which may expose us to litigation and other potential liability; |

| ● | disputes may arise between us and HaloVax that result in the delay or termination of the commercialization of our products or product candidates or that result in costly litigation or arbitration that diverts management attention and resources including, but not limited to, disputes with respect to commercializing products upon terms mutually agreeable or beneficial to us and HaloVax; |

| ● | any products, if developed, will be sold or licensed on terms that are beneficial to us; |