0001711291false2022FYP3YP3Y3P1Yhttp://fasb.org/us-gaap/2022#OtherAssetsMiscellaneous3http://fasb.org/us-gaap/2022#OtherAssetsMiscellaneoushttp://fasb.org/us-gaap/2022#OtherAssetsMiscellaneousP5Y33.3300017112912022-01-012022-12-3100017112912022-06-30iso4217:USD00017112912023-03-03xbrli:shares00017112912022-12-3100017112912021-12-310001711291us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2022-12-310001711291us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2021-12-31iso4217:USDxbrli:shares0001711291curo:InterestAndFeesRevenueMember2022-01-012022-12-310001711291curo:InterestAndFeesRevenueMember2021-01-012021-12-310001711291curo:InterestAndFeesRevenueMember2020-01-012020-12-310001711291curo:InsurancePremiumsAndCommissionsMember2022-01-012022-12-310001711291curo:InsurancePremiumsAndCommissionsMember2021-01-012021-12-310001711291curo:InsurancePremiumsAndCommissionsMember2020-01-012020-12-310001711291curo:OtherRevenueMember2022-01-012022-12-310001711291curo:OtherRevenueMember2021-01-012021-12-310001711291curo:OtherRevenueMember2020-01-012020-12-3100017112912021-01-012021-12-3100017112912020-01-012020-12-310001711291us-gaap:CommonStockMember2019-12-310001711291us-gaap:TreasuryStockMember2019-12-310001711291us-gaap:AdditionalPaidInCapitalMember2019-12-310001711291us-gaap:RetainedEarningsMember2019-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-3100017112912019-12-310001711291us-gaap:RetainedEarningsMember2020-01-012020-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001711291us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001711291us-gaap:CommonStockMember2020-01-012020-12-310001711291us-gaap:TreasuryStockMember2020-01-012020-12-310001711291us-gaap:CommonStockMember2020-12-310001711291us-gaap:TreasuryStockMember2020-12-310001711291us-gaap:AdditionalPaidInCapitalMember2020-12-310001711291us-gaap:RetainedEarningsMember2020-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-3100017112912020-12-310001711291us-gaap:RetainedEarningsMember2021-01-012021-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001711291us-gaap:CommonStockMember2021-01-012021-12-310001711291us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001711291us-gaap:TreasuryStockMember2021-01-012021-12-310001711291us-gaap:CommonStockMember2021-12-310001711291us-gaap:TreasuryStockMember2021-12-310001711291us-gaap:AdditionalPaidInCapitalMember2021-12-310001711291us-gaap:RetainedEarningsMember2021-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001711291us-gaap:RetainedEarningsMember2022-01-012022-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001711291us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001711291us-gaap:CommonStockMember2022-01-012022-12-310001711291us-gaap:TreasuryStockMember2022-01-012022-12-310001711291us-gaap:CommonStockMember2022-12-310001711291us-gaap:TreasuryStockMember2022-12-310001711291us-gaap:AdditionalPaidInCapitalMember2022-12-310001711291us-gaap:RetainedEarningsMember2022-12-310001711291us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001711291curo:ShareRepurchaseAgreementWithFaulkner2017DynastyTrustMembersrt:AffiliatedEntityMember2021-01-012021-12-310001711291curo:AdAstraMember2022-01-012022-12-310001711291curo:AdAstraMember2021-01-012021-12-310001711291curo:AdAstraMember2020-01-012020-12-310001711291curo:FlexitiMember2022-01-012022-12-310001711291curo:FlexitiMember2021-01-012021-12-310001711291curo:FlexitiMember2020-01-012020-12-310001711291curo:HeightsFinanceMember2022-01-012022-12-310001711291curo:HeightsFinanceMember2021-01-012021-12-310001711291curo:HeightsFinanceMember2020-01-012020-12-310001711291curo:FirstHeritageCreditMember2022-01-012022-12-310001711291curo:FirstHeritageCreditMember2021-01-012021-12-310001711291curo:FirstHeritageCreditMember2020-01-012020-12-310001711291curo:SPVAndSPEFacilitiesMember2022-01-012022-12-310001711291curo:SPVAndSPEFacilitiesMember2021-01-012021-12-310001711291curo:SPVAndSPEFacilitiesMember2020-01-012020-12-310001711291curo:SeniorSecuredRevolvingLoanFacilityMember2022-01-012022-12-310001711291curo:SeniorSecuredRevolvingLoanFacilityMember2021-01-012021-12-310001711291curo:SeniorSecuredRevolvingLoanFacilityMember2020-01-012020-12-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMember2021-12-31xbrli:pure0001711291curo:SeniorSecuredNotesDue2025Member2022-01-012022-12-310001711291curo:SeniorSecuredNotesDue2025Member2021-01-012021-12-310001711291curo:SeniorSecuredNotesDue2025Member2020-01-012020-12-310001711291curo:SeniorSecuredNotesDue2028Memberus-gaap:SeniorNotesMember2021-12-310001711291curo:SeniorSecuredNotesDue2028Member2022-01-012022-12-310001711291curo:SeniorSecuredNotesDue2028Member2021-01-012021-12-310001711291curo:SeniorSecuredNotesDue2028Member2020-01-012020-12-31curo:location0001711291curo:UnitedStatesSegmentMember2022-12-31curo:state0001711291curo:CanadaDirectLendingMember2022-12-31curo:province0001711291country:CA2022-12-31curo:territory0001711291curo:CanadaPOSLendingMember2022-12-31curo:storecuro:partner0001711291curo:FirstHeritageCreditMember2022-07-132022-07-130001711291curo:HeightsMember2021-12-272021-12-270001711291curo:FlexitiMember2021-03-102021-03-100001711291curo:FlexitiMembersrt:MaximumMember2021-03-100001711291curo:AdAstraMember2020-01-030001711291curo:AdAstraMember2020-01-032020-01-030001711291curo:USLegacyDirectLendingBusinessMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2022-07-080001711291curo:USLegacyDirectLendingBusinessMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2022-07-082022-07-080001711291curo:USLegacyDirectLendingBusinessMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2022-01-012022-09-300001711291curo:USLegacyDirectLendingBusinessMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2022-07-012022-09-300001711291curo:PreviousLagPeriodMembercuro:KatapultMember2021-06-012021-06-010001711291curo:PreviousLagPeriodMembercuro:KatapultMember2021-01-012021-03-310001711291curo:InstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:HeightsInsuranceProgramMember2022-12-310001711291curo:FundingFacilitiesMember2022-12-310001711291curo:AutoTitleLoanMemberus-gaap:ConsumerPortfolioSegmentMember2022-01-012022-12-310001711291us-gaap:FurnitureAndFixturesMembersrt:MinimumMember2022-01-012022-12-310001711291us-gaap:FurnitureAndFixturesMembersrt:MaximumMember2022-01-012022-12-310001711291srt:MinimumMemberus-gaap:LeaseholdImprovementsMember2022-01-012022-12-310001711291us-gaap:LeaseholdImprovementsMembersrt:MaximumMember2022-01-012022-12-310001711291srt:MinimumMemberus-gaap:ComputerSoftwareIntangibleAssetMember2022-01-012022-12-310001711291us-gaap:ComputerSoftwareIntangibleAssetMembersrt:MaximumMember2022-01-012022-12-310001711291srt:MinimumMember2022-01-012022-12-310001711291srt:MaximumMember2022-01-012022-12-310001711291stpr:CA-ONus-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001711291us-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMemberstpr:TX2022-01-012022-12-310001711291stpr:CA-ONus-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2021-01-012021-12-310001711291us-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMemberstpr:TX2021-01-012021-12-310001711291us-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMemberstpr:TX2020-01-012020-12-310001711291stpr:CAus-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2020-01-012020-12-310001711291stpr:CA-ONus-gaap:SalesRevenueNetMemberus-gaap:GeographicConcentrationRiskMember2020-01-012020-12-310001711291curo:HeightsAndFirstHeritageMember2022-12-310001711291stpr:CA-ONcuro:LoansReceivableBenchmarkMemberus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001711291stpr:TNcuro:LoansReceivableBenchmarkMemberus-gaap:GeographicConcentrationRiskMember2022-01-012022-12-310001711291curo:LoansReceivableBenchmarkMemberus-gaap:GeographicConcentrationRiskMemberstpr:TX2022-01-012022-12-310001711291curo:MerchantConcentrationRiskMemberus-gaap:SalesRevenueNetMembercuro:LFLMember2022-01-012022-12-310001711291curo:MerchantConcentrationRiskMemberus-gaap:AccountsReceivableMembercuro:LFLMember2022-01-012022-12-310001711291srt:ScenarioForecastMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2023-01-010001711291srt:ScenarioForecastMembersrt:CumulativeEffectPeriodOfAdoptionAdjustmentMember2023-01-012023-01-010001711291curo:KatapultMembercuro:CurrentLagPeriodMember2021-01-012021-03-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2022-01-012022-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2021-01-012021-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2020-01-012020-12-310001711291curo:TotalInstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2022-01-012022-12-310001711291curo:TotalInstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2021-01-012021-12-310001711291curo:TotalInstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2020-01-012020-12-310001711291us-gaap:ConsumerPortfolioSegmentMember2022-01-012022-12-310001711291us-gaap:ConsumerPortfolioSegmentMember2021-01-012021-12-310001711291us-gaap:ConsumerPortfolioSegmentMember2020-01-012020-12-310001711291curo:InsuranceRevenueMemberus-gaap:UnallocatedFinancingReceivablesMember2022-01-012022-12-310001711291curo:InsuranceRevenueMemberus-gaap:UnallocatedFinancingReceivablesMember2021-01-012021-12-310001711291curo:InsuranceRevenueMemberus-gaap:UnallocatedFinancingReceivablesMember2020-01-012020-12-310001711291curo:OtherRevenueMemberus-gaap:UnallocatedFinancingReceivablesMember2022-01-012022-12-310001711291curo:OtherRevenueMemberus-gaap:UnallocatedFinancingReceivablesMember2021-01-012021-12-310001711291curo:OtherRevenueMemberus-gaap:UnallocatedFinancingReceivablesMember2020-01-012020-12-310001711291curo:CreditServicesOrganizationProgramsMember2022-01-012022-12-310001711291curo:CreditServicesOrganizationProgramsMember2021-01-012021-12-310001711291curo:CreditServicesOrganizationProgramsMember2020-01-012020-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2022-12-310001711291curo:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2022-12-310001711291us-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2022-12-310001711291curo:RevolvingLOCMemberus-gaap:FinancingReceivables1To29DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivables1To29DaysPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivables1To29DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:RevolvingLOCMemberus-gaap:FinancingReceivables30To59DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:TotalInstallmentCompanyOwnedMemberus-gaap:FinancingReceivables30To59DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivables30To59DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivables60To89DaysPastDueMembercuro:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivables60To89DaysPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivables60To89DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:RevolvingLOCMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancialAssetPastDueMembercuro:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancialAssetPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancialAssetPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291country:CAcuro:SinglePayMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2021-12-310001711291curo:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2021-12-310001711291us-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2021-12-310001711291curo:RevolvingLOCMemberus-gaap:FinancingReceivables1To29DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivables1To29DaysPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivables1To29DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:RevolvingLOCMemberus-gaap:FinancingReceivables30To59DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:TotalInstallmentCompanyOwnedMemberus-gaap:FinancingReceivables30To59DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivables30To59DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivables60To89DaysPastDueMembercuro:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivables60To89DaysPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivables60To89DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:RevolvingLOCMemberus-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancingReceivablesEqualToGreaterThan90DaysPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancialAssetPastDueMembercuro:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancialAssetPastDueMembercuro:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:FinancialAssetPastDueMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:TotalInstallmentCompanyOwnedMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:SinglePayMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291country:CAcuro:SinglePayMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:TotalInstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:UnallocatedFinancingReceivablesMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291us-gaap:UnallocatedFinancingReceivablesMemberus-gaap:ConsumerPortfolioSegmentMember2022-01-012022-12-310001711291curo:TotalInstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:UnallocatedFinancingReceivablesMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:RevolvingLOCMemberus-gaap:ConsumerPortfolioSegmentMember2020-12-310001711291curo:TotalInstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2020-12-310001711291us-gaap:UnallocatedFinancingReceivablesMemberus-gaap:ConsumerPortfolioSegmentMember2020-12-310001711291us-gaap:ConsumerPortfolioSegmentMember2020-12-310001711291us-gaap:UnallocatedFinancingReceivablesMemberus-gaap:ConsumerPortfolioSegmentMember2021-01-012021-12-310001711291curo:InstallmentMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2022-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMemberus-gaap:FinancialAssetNotPastDueMember2021-12-310001711291us-gaap:FinancialAssetPastDueMembercuro:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291us-gaap:FinancialAssetPastDueMembercuro:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2021-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2022-01-012022-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2021-01-012021-12-310001711291curo:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2020-01-012020-12-310001711291curo:OpenEndMembercuro:CreditServicesOrganizationProgramsMemberus-gaap:ConsumerPortfolioSegmentMember2022-12-31curo:loancuro:facility0001711291curo:UnitedStatesSegmentMember2020-12-310001711291curo:CanadaDirectLendingMember2020-12-310001711291curo:CanadaPOSLendingMember2020-12-310001711291curo:UnitedStatesSegmentMember2021-01-012021-12-310001711291curo:CanadaDirectLendingMember2021-01-012021-12-310001711291curo:CanadaPOSLendingMember2021-01-012021-12-310001711291curo:UnitedStatesSegmentMember2021-12-310001711291curo:CanadaDirectLendingMember2021-12-310001711291curo:CanadaPOSLendingMember2021-12-310001711291curo:UnitedStatesSegmentMember2022-01-012022-12-310001711291curo:CanadaDirectLendingMember2022-01-012022-12-310001711291curo:CanadaPOSLendingMember2022-01-012022-12-3100017112912022-10-012022-12-31curo:Unit0001711291curo:CanadaPOSLendingMembercuro:FlexitiMember2021-12-310001711291curo:CanadaPOSLendingMembercuro:FlexitiMember2021-01-012021-12-310001711291curo:UnitedStatesSegmentMembercuro:HeightsMember2021-12-272021-12-270001711291curo:UnitedStatesSegmentMembercuro:HeightsFinanceMember2022-12-3100017112912022-07-012022-09-3000017112912022-01-012022-09-300001711291curo:UnitedStatesSegmentMember2022-07-132022-07-130001711291us-gaap:TradeNamesMember2022-12-310001711291us-gaap:TradeNamesMember2021-12-310001711291curo:MerchantRelationshipsMember2022-01-012022-12-310001711291curo:MerchantRelationshipsMember2022-12-310001711291curo:MerchantRelationshipsMember2021-12-310001711291us-gaap:CustomerRelationshipsMember2022-01-012022-12-310001711291us-gaap:CustomerRelationshipsMember2022-12-310001711291us-gaap:CustomerRelationshipsMember2021-12-310001711291us-gaap:ComputerSoftwareIntangibleAssetMember2022-01-012022-12-310001711291us-gaap:ComputerSoftwareIntangibleAssetMember2022-12-310001711291us-gaap:ComputerSoftwareIntangibleAssetMember2021-12-310001711291us-gaap:TradeNamesMember2022-01-012022-12-310001711291us-gaap:TradeNamesMember2022-12-310001711291us-gaap:TradeNamesMember2021-12-310001711291us-gaap:SoftwareDevelopmentMember2022-12-310001711291us-gaap:SoftwareDevelopmentMember2021-12-310001711291curo:CashMoneyTradeNameMember2022-12-310001711291us-gaap:OtherIntangibleAssetsMembersrt:MinimumMember2022-01-012022-12-310001711291us-gaap:OtherIntangibleAssetsMembersrt:MaximumMember2022-01-012022-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001711291curo:FlexitiMember2021-01-012021-03-310001711291curo:FlexitiMember2021-03-3100017112912021-03-310001711291curo:FlexitiMember2022-07-012022-07-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Member2022-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel1Membercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel3Membercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291curo:HeightsRevolvingCreditFacilityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsRevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsRevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsRevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsRevolvingCreditFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291curo:FirstHeritageCreditRevolvingCreditFacilityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FirstHeritageCreditRevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FirstHeritageCreditRevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FirstHeritageCreditRevolvingCreditFacilityMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291curo:FlexitiSPVFacilityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMembercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Membercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Membercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Membercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Member2021-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel1Membercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:FairValueInputsLevel2Member2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel3Membercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:SeniorNotesMembercuro:SecuredNotesDue2028Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291curo:USSPVFacilityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:USSPVFacilityMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:USSPVFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:USSPVFacilityMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:USSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMembercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel1Membercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel2Membercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMemberus-gaap:FairValueInputsLevel3Membercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:CanadaSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291curo:FlexitiSPVFacilityMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSPVFacilityMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:CarryingReportedAmountFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:FlexitiSecuritizationMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:CarryingReportedAmountFairValueDisclosureMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsFinanceSPVMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsFinanceSPVMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsFinanceSPVMemberus-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EstimateOfFairValueFairValueDisclosureMembercuro:HeightsFinanceSPVMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2019-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2019-12-310001711291us-gaap:EquityMethodInvestmentsMember2019-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-01-012020-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310001711291us-gaap:EquityMethodInvestmentsMember2020-01-012020-12-310001711291curo:CommonStockWarrantsAndPreferredStockMemberus-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-01-012020-12-310001711291curo:CommonStockWarrantsAndPreferredStockMemberus-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310001711291curo:CommonStockWarrantsAndPreferredStockMemberus-gaap:EquityMethodInvestmentsMember2020-01-012020-12-310001711291us-gaap:CommonStockMemberus-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-01-012020-12-310001711291us-gaap:CommonStockMemberus-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310001711291us-gaap:CommonStockMemberus-gaap:EquityMethodInvestmentsMember2020-01-012020-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001711291us-gaap:EquityMethodInvestmentsMember2020-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-01-012021-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2021-01-012021-12-310001711291us-gaap:EquityMethodInvestmentsMember2021-01-012021-12-310001711291us-gaap:CommonStockMemberus-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-01-012021-12-310001711291us-gaap:CommonStockMemberus-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2021-01-012021-12-310001711291us-gaap:CommonStockMemberus-gaap:EquityMethodInvestmentsMember2021-01-012021-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2021-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001711291us-gaap:EquityMethodInvestmentsMember2021-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-01-012022-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2022-01-012022-12-310001711291us-gaap:EquityMethodInvestmentsMember2022-01-012022-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-12-310001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001711291us-gaap:EquityMethodInvestmentsMember2022-12-310001711291curo:KatapultMember2021-06-092021-06-090001711291curo:KatapultMember2021-04-012021-06-300001711291us-gaap:EquityMethodInvestmentsMemberus-gaap:FairValueMeasurementsNonrecurringMember2022-10-012022-12-310001711291curo:KatapultMember2021-10-012021-12-3100017112912021-06-09curo:boardSeat0001711291curo:KatapultMember2022-12-310001711291curo:SeniorSecuredNotesDue2028Memberus-gaap:SeniorNotesMember2022-12-310001711291curo:CorporateDebtMember2022-12-310001711291curo:CorporateDebtMember2021-12-310001711291us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembercuro:HeightsMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:HeightsMember2022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:HeightsMember2021-12-310001711291us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembercuro:FirstHeritageCreditMember2022-01-012022-12-310001711291curo:FirstHeritageCreditMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-12-310001711291curo:FirstHeritageCreditMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2021-12-310001711291curo:FlexitiSPVFacilityMember2022-12-310001711291curo:FlexitiSPVFacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-12-31iso4217:CAD0001711291curo:FlexitiSPVFacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2021-12-310001711291curo:FlexitiSecuritizationMembercuro:CanadianDollarOfferedRateCDORMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMembercuro:FlexitiSecuritizationMemberus-gaap:RevolvingCreditFacilityMember2022-12-310001711291us-gaap:LineOfCreditMembercuro:FlexitiSecuritizationMemberus-gaap:RevolvingCreditFacilityMember2021-12-310001711291curo:CanadianDollarOfferedRateCDORMembercuro:CanadaSPVFacilityMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CanadaSPVFacilityMember2022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CanadaSPVFacilityMember2021-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:LondonInterbankOfferedRateLIBORMembercuro:BasisSpreadScenarioOneMember2022-01-012022-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2021-12-310001711291curo:USSPVFacilityMemberus-gaap:LondonInterbankOfferedRateLIBORMembercuro:BasisSpreadScenarioOneMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMembercuro:USSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-12-310001711291us-gaap:LineOfCreditMembercuro:USSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2021-12-310001711291curo:CuroCanadaRevolvingCreditFacilityMemberus-gaap:PrimeRateMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CuroCanadaRevolvingCreditFacilityMember2022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CuroCanadaRevolvingCreditFacilityMember2021-12-310001711291us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembercuro:SeniorSecuredRevolvingLoanFacilityMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:SeniorSecuredRevolvingLoanFacilityMember2022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:SeniorSecuredRevolvingLoanFacilityMember2021-12-310001711291curo:FundingDebtMember2022-12-310001711291curo:FundingDebtMember2021-12-310001711291curo:FlexitiSecuritizationMember2022-07-070001711291us-gaap:RevolvingCreditFacilityMembercuro:CuroCanadaRevolvingCreditFacilityMember2022-12-200001711291curo:SeniorSecuredNotesDue2028Memberus-gaap:SeniorNotesMember2021-07-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMember2018-08-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMember2021-09-300001711291curo:SeniorSecuredNotesDue2028Memberus-gaap:SeniorNotesMember2021-09-300001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMember2021-07-012021-09-300001711291curo:HeightsRevolvingCreditFacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-07-150001711291us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembercuro:HeightsRevolvingCreditFacilityMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-07-150001711291curo:HeightsRevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMembercuro:FirstHeritageCreditRevolvingCreditFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-07-130001711291us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:LineOfCreditMembercuro:FirstHeritageCreditRevolvingCreditFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-07-130001711291us-gaap:LineOfCreditMembercuro:FirstHeritageCreditRevolvingCreditFacilityMember2022-01-012022-12-310001711291curo:FlexitiSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-09-280001711291curo:FlexitiSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-09-290001711291curo:FlexitiSPVFacilityMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CanadaSPVFacilityMember2018-08-310001711291us-gaap:RevolvingCreditFacilityMembercuro:CanadaSPVFacilityMember2022-12-3100017112912022-03-310001711291us-gaap:LineOfCreditMembercuro:CanadaSPVFacilityMember2022-01-012022-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:RevolvingCreditFacilityMember2022-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:LondonInterbankOfferedRateLIBORMembercuro:BasisSpreadScenarioOneMember2019-12-012019-12-310001711291curo:HeightsFinanceSPVMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-07-1500017112912022-07-152022-07-150001711291curo:USSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2020-04-300001711291curo:USSPVFacilityMemberus-gaap:LondonInterbankOfferedRateLIBORMembercuro:BasisSpreadScenarioOneMember2020-04-012020-04-300001711291us-gaap:LineOfCreditMembercuro:USSPVFacilityMember2022-01-012022-12-310001711291curo:USSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-07-082022-07-080001711291us-gaap:LineOfCreditMemberus-gaap:LetterOfCreditMembercuro:SeniorSecuredRevolvingLoanFacilityMember2022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:LetterOfCreditMembercuro:SeniorSecuredRevolvingLoanFacilityMember2022-01-012022-12-310001711291us-gaap:LondonInterbankOfferedRateLIBORMembercuro:SeniorSecuredRevolvingLoanFacilityMember2022-01-012022-12-310001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CuroCanadaRevolvingCreditFacilityMember2022-12-200001711291us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembercuro:CuroCanadaRevolvingCreditFacilityMember2022-12-210001711291curo:FlexitiSPVFacilityMemberus-gaap:RevolvingCreditFacilityMember2022-10-110001711291curo:FlexitiSPVFacilityMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMember2022-12-310001711291curo:FlexitiSPVFacilityMemberus-gaap:InterestRateSwapMember2022-01-012022-12-310001711291curo:FlexitiSecuritizationMemberus-gaap:RevolvingCreditFacilityMember2022-07-070001711291curo:FlexitiSecuritizationMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMember2022-12-310001711291curo:FlexitiSecuritizationMemberus-gaap:InterestRateSwapMember2022-01-012022-12-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodOneMember2022-01-012022-12-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:DebtInstrumentRedemptionPeriodTwoMemberus-gaap:SeniorNotesMember2022-01-012022-12-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodThreeMember2022-01-012022-12-310001711291curo:SeniorSecuredNotesDue2025Memberus-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodFourMember2022-01-012022-12-3100017112912020-12-012020-12-310001711291curo:ShareholderDerivativeLawsuitsMember2020-07-31curo:lawsuit0001711291curo:ShareholderDerivativeLawsuitsWithFFLDefendantsMember2020-07-3100017112912022-10-272022-10-270001711291srt:ProFormaMemberus-gaap:CanadaRevenueAgencyMember2022-01-012022-12-310001711291us-gaap:ForeignCountryMember2022-12-310001711291us-gaap:ForeignCountryMember2020-12-310001711291us-gaap:CanadaRevenueAgencyMember2022-12-310001711291us-gaap:StateAndLocalJurisdictionMember2022-12-310001711291curo:A2010IncentivePlanMember2010-12-310001711291curo:A2017IncentivePlanMember2017-12-310001711291curo:StockOptionsMember2022-01-012022-12-3100017112912019-01-012019-12-310001711291us-gaap:PerformanceSharesMembersrt:MinimumMember2022-01-012022-12-310001711291us-gaap:PerformanceSharesMembersrt:MaximumMember2022-01-012022-12-310001711291us-gaap:PerformanceSharesMember2022-01-012022-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2022-01-012022-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2019-12-310001711291us-gaap:PerformanceSharesMember2019-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2019-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001711291us-gaap:PerformanceSharesMember2020-01-012020-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2020-01-012020-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2020-12-310001711291us-gaap:PerformanceSharesMember2020-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2020-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001711291us-gaap:PerformanceSharesMember2021-01-012021-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2021-01-012021-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2021-12-310001711291us-gaap:PerformanceSharesMember2021-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2021-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001711291us-gaap:RestrictedStockUnitsRSUMember2022-12-310001711291us-gaap:PerformanceSharesMember2022-12-310001711291curo:RestrictedStockUnitsRSUsPerformanceBasedMember2022-12-310001711291curo:UnrelatedThirdPartyMember2022-01-012022-12-310001711291curo:UnrelatedThirdPartyMember2021-01-012021-12-310001711291curo:UnrelatedThirdPartyMember2020-01-012020-12-310001711291curo:RelatedPartyMember2022-01-012022-12-310001711291curo:RelatedPartyMember2021-01-012021-12-310001711291curo:RelatedPartyMember2020-01-012020-12-310001711291curo:UnrelatedThirdPartyMember2022-12-310001711291curo:RelatedPartyMember2022-12-3100017112912020-02-2900017112912021-05-3100017112912022-02-0400017112912022-03-012022-03-0100017112912022-04-2800017112912022-05-232022-05-2300017112912022-08-0300017112912022-08-262022-08-2600017112912021-01-2900017112912021-03-022021-03-0200017112912021-05-0300017112912021-05-272021-05-2700017112912021-07-2800017112912021-08-192021-08-1900017112912021-10-2700017112912021-11-222021-11-220001711291curo:UnitedStatesSegmentMember2020-01-012020-12-310001711291curo:CanadaDirectLendingMember2020-01-012020-12-310001711291curo:CanadaPOSLendingMember2020-01-012020-12-310001711291curo:FirstHeritageCreditMember2022-05-182022-05-180001711291curo:FirstHeritageCreditMember2022-07-130001711291curo:FirstHeritageCreditMemberus-gaap:TradeNamesMember2022-07-130001711291curo:FirstHeritageCreditMemberus-gaap:TradeNamesMember2022-07-132022-07-130001711291curo:FirstHeritageCreditMemberus-gaap:CustomerRelationshipsMember2022-07-130001711291curo:FirstHeritageCreditMemberus-gaap:CustomerRelationshipsMember2022-07-132022-07-130001711291curo:FirstHeritageCreditMember2022-12-310001711291curo:HeightsMember2021-12-27curo:branch0001711291curo:HeightsMember2022-01-012022-12-3100017112912022-01-012022-03-310001711291curo:HeightsMember2022-10-012022-12-310001711291curo:HeightsMember2022-12-310001711291curo:HeightsMember2021-12-282022-12-310001711291curo:FlexitiMember2021-03-100001711291curo:FlexitiMember2021-03-102021-12-310001711291curo:FlexitiMember2021-12-310001711291curo:FlexitiMember2021-03-112021-12-310001711291curo:FlexitiMembercuro:DevelopedTechnologyMember2022-12-310001711291curo:FlexitiMembercuro:DevelopedTechnologyMember2022-01-012022-12-310001711291curo:FlexitiMembercuro:MerchantRelationshipsMember2022-12-310001711291curo:FlexitiMembercuro:MerchantRelationshipsMember2022-01-012022-12-310001711291curo:FlexitiMemberus-gaap:CustomerRelationshipsMember2022-12-310001711291curo:FlexitiMemberus-gaap:CustomerRelationshipsMember2022-01-012022-12-310001711291curo:FlexitiMember2022-12-310001711291curo:FlexitiMembersrt:MinimumMember2021-03-100001711291curo:AdAstraMember2019-01-012019-12-310001711291curo:USLegacyDirectLendingBusinessMemberus-gaap:DiscontinuedOperationsDisposedOfBySaleMember2022-01-012022-12-310001711291curo:USLegacyDirectLendingBusinessMember2022-01-012022-12-310001711291curo:USLegacyDirectLendingBusinessMember2021-01-012021-12-310001711291srt:AffiliatedEntityMembersrt:MinimumMembercuro:AdAstraMember2022-01-012022-12-310001711291srt:AffiliatedEntityMembercuro:AdAstraMembersrt:MaximumMember2022-01-012022-12-310001711291srt:AffiliatedEntityMembercuro:AdAstraMembercuro:CommissionsforCollectionActivitiesMember2022-01-012022-12-310001711291us-gaap:LeaseholdImprovementsMember2022-12-310001711291us-gaap:LeaseholdImprovementsMember2021-12-310001711291us-gaap:FurnitureAndFixturesMember2022-12-310001711291us-gaap:FurnitureAndFixturesMember2021-12-310001711291curo:DeferredCompensationAgreementPeriodOneMember2022-01-012022-12-310001711291curo:DeferredCompensationAgreementPeriodTwoMember2022-01-012022-12-310001711291curo:RegisteredRetirementSavingsPlanMember2022-01-012022-12-310001711291curo:RegisteredRetirementSavingsPlanMember2022-01-012022-12-310001711291curo:DefinedContributionPlanPeriodOneMembercuro:RegisteredRetirementSavingsPlanMember2022-01-012022-12-310001711291curo:DefinedContributionPlanPeriodTwoMembercuro:RegisteredRetirementSavingsPlanMember2022-01-012022-12-310001711291curo:A2021RegisteredRetirementSavingsPlanMembercuro:ContactCenterEmployeesMember2022-01-012022-12-310001711291curo:A2021RegisteredRetirementSavingsPlanMembercuro:ContactCenterEmployeesMember2022-01-012022-12-310001711291curo:A2021RegisteredRetirementSavingsPlanMembercuro:CorporateEmployeesMember2022-01-012022-12-310001711291curo:A2021RegisteredRetirementSavingsPlanMembercuro:CorporateEmployeesMember2022-01-012022-12-310001711291curo:A2021RegisteredRetirementSavingsPlanMember2022-01-012022-12-31curo:contract0001711291curo:RegisteredRetirementSavingsPlanMember2021-01-012021-12-310001711291curo:RegisteredRetirementSavingsPlanMember2020-01-012020-12-310001711291curo:A401kRetirementSavingsPlanMember2022-01-012022-12-310001711291curo:Tier1Membercuro:A401kRetirementSavingsPlanHeightsMember2022-01-012022-12-310001711291curo:Tier2Membercuro:A401kRetirementSavingsPlanHeightsMember2022-01-012022-12-310001711291curo:A401kRetirementSavingsPlanMember2022-01-012022-12-310001711291curo:A401kRetirementSavingsPlanMember2021-01-012021-12-310001711291curo:A401kRetirementSavingsPlanMember2020-01-012020-12-310001711291us-gaap:EmployeeSeveranceMember2022-01-012022-12-310001711291us-gaap:FacilityClosingMember2022-01-012022-12-310001711291curo:UNITEDSTATESANDCANADAMember2022-01-012022-12-310001711291curo:LaborAndRelatedExpenseMemberus-gaap:EmployeeSeveranceMember2022-10-062022-12-310001711291curo:LaborAndRelatedExpenseMemberus-gaap:FacilityClosingMember2022-10-062022-12-310001711291curo:LaborAndRelatedExpenseMember2022-10-062022-12-310001711291us-gaap:CostOfSalesMemberus-gaap:EmployeeSeveranceMember2022-10-062022-12-310001711291us-gaap:CostOfSalesMemberus-gaap:FacilityClosingMember2022-10-062022-12-310001711291us-gaap:CostOfSalesMember2022-10-062022-12-310001711291us-gaap:EmployeeSeveranceMemberus-gaap:OtherOperatingIncomeExpenseMember2022-10-062022-12-310001711291us-gaap:FacilityClosingMemberus-gaap:OtherOperatingIncomeExpenseMember2022-10-062022-12-310001711291us-gaap:OtherOperatingIncomeExpenseMember2022-10-062022-12-310001711291us-gaap:EmployeeSeveranceMember2022-10-062022-12-310001711291us-gaap:FacilityClosingMember2022-10-062022-12-3100017112912022-10-062022-12-3100017112912022-10-050001711291country:US2021-01-012021-12-310001711291stpr:IL2021-01-012021-12-310001711291stpr:OR2021-01-012021-12-310001711291stpr:CO2021-01-012021-12-310001711291stpr:WA2021-01-012021-12-310001711291stpr:TX2021-01-012021-12-310001711291stpr:CA2021-01-012021-12-310001711291stpr:LA2021-01-012021-12-310001711291stpr:NV2021-01-012021-12-310001711291stpr:TN2021-01-012021-12-310001711291country:US2021-04-012021-06-300001711291country:US2021-07-012021-09-300001711291curo:CorporateDistrictAndOtherExpensesMember2021-01-012021-12-310001711291us-gaap:CostOfSalesMember2021-01-012021-12-310001711291curo:U.KSegmentMemberus-gaap:DiscontinuedOperationsDisposedOfByMeansOtherThanSaleMember2020-01-012020-12-310001711291curo:RepurchaseProgram2022Member2022-02-280001711291curo:RepurchaseProgram2021Member2021-05-310001711291curo:RepurchaseProgram2021Member2022-12-310001711291curo:RepurchaseProgram2021Member2022-10-012022-12-310001711291curo:RepurchaseProgram2021Member2022-01-012022-12-310001711291curo:ShareRepurchaseAgreementWithFaulkner2017DynastyTrustMembersrt:AffiliatedEntityMember2021-11-012021-11-300001711291curo:ShareRepurchaseAgreementWithFaulkner2017DynastyTrustMembersrt:AffiliatedEntityMember2021-11-300001711291curo:RepurchaseProgram2021Member2021-07-012021-09-300001711291curo:RepurchaseProgram2020Member2020-02-290001711291us-gaap:LineOfCreditMemberus-gaap:SubsequentEventMemberus-gaap:RevolvingCreditFacilityMembercuro:CuroCanadaRevolvingCreditFacilityMember2023-01-06

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2022

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________to__________

Commission File Number: 1-38315

CURO GROUP HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 90-0934597 |

(State or other jurisdiction

Of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

200 W Hubbard Street, 8th Floor, Chicago, IL | | 60654 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (312) 470-2000

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common stock, $0.001 par value per share | CURO | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | Accelerated filer | ☒ |

| Non-accelerated filer | ☐ | | | |

| Smaller reporting company | ☒ | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of 23,535,837 shares of the registrant’s common stock, par value $0.001 per share, held by non-affiliates on June 30, 2022 was approximately $130,153,179.

As of March 3, 2023 there were 40,835,943 shares of the registrant’s Common Stock, $0.001 par value per share, outstanding.

Documents Incorporated by Reference:

Certain information required by Part III of this Annual Report on Form 10-K is incorporated herein by reference to the Proxy Statement for the registrant’s 2023 Annual Meeting of Stockholders, which is expected to be filed pursuant to Regulation 14A within 120 days after the end of the registrant’s fiscal year ended December 31, 2022.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

YEAR ENDED DECEMBER 31, 2022

INDEX

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Page |

| |

| | | | | | | |

|

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | | | | | |

|

Item 5. | | |

Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | | | | | | |

|

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | | | | | |

|

| Item 15. | Exhibits, Financial Statement Schedules | |

| Item 16. | | |

| | |

GLOSSARY

Terms and abbreviations used throughout this report are defined below.

| | | | | | | | |

| Term or abbreviation | | Definition |

| | |

| | |

| | |

| | |

| 2021 Form 10-K | | Annual Report on Form 10-K for the year ended December 31, 2021, filed with the SEC on March 7, 2022 |

| 7.50% Senior Secured Notes | | 7.50% Senior Secured Notes, issued in July 2021 for $750.0 million, which mature in August 2028 |

| 8.25% Senior Secured Notes | | 8.25% Senior Secured Notes, issued in August 2018 for $690.0 million, which were extinguished during the third quarter of 2021 |

| Ad Astra | | Ad Astra Recovery Services, Inc., a wholly-owned subsidiary of the Company, which, prior to acquisition in January 2020, was our exclusive provider of third-party collection services for the legacy Direct Lending U.S. business. The Company ceased operations of Ad Astra in January 2023. |

| ABL | | Asset-Backed Lending |

| Adjusted EBITDA | | EBITDA plus or minus certain non-cash and other adjusting items; Refer to "Supplemental Non-GAAP Financial Information" for additional details |

| ALL | | Allowance for loan losses |

| | |

| AOCI | | Accumulated other comprehensive income (loss) |

| ASC | | Accounting Standards Codification |

| ASU | | Accounting Standards Update |

| Average gross loans receivable | | Utilized to calculate product yield and NCO rates; calculated as average of beginning of quarter and end of quarter gross loans receivable |

| BNPL | | Buy-Now-Pay-Later |

| bps | | Basis points |

| C$ | | Canadian dollar |

| CAB | | Credit Access Business |

| Canada SPV | | A four-year revolving credit facility with capacity up to C$400.0 million |

| | |

| Curo Canada Revolving Credit Facility | | C$5.0 million revolving credit facility (formerly known as Cash Money Revolving Credit Facility), maintained by CURO Canada. This facility was terminated in January 2023. |

| CDOR | | Canadian Dollar Offered Rate |

| CECL | | In June 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments. This ASU requires an impairment model (known as the current expected credit loss (“CECL”) model) that is based on expected rather than incurred losses, with an anticipated result of more timely loss recognition. This guidance will be effective for us on January 1, 2023. |

| | |

| | |

| | |

| CODM | | Chief Operating Decision Maker |

| | |

| | |

| Community Choice Financial | | Community Choice Financial Inc., a consumer financial services company based in Dublin, Ohio, which we sold our Legacy U.S. Direct Lending Business to on July 8, 2022 |

| CSO | | Credit services organization |

| | |

| Curo Canada | | Curo Canada Corp, a wholly-owned Canadian subsidiary of the Company, formerly known as Cash Money Cheque Cashing Inc. |

| Curo Receivables Finance II, LLC | | A U.S. bankruptcy remote special purpose vehicle and an indirect wholly-owned subsidiary of the Company |

| | |

| | |

| EBITDA | | Earnings Before Interest, Taxes, Depreciation and Amortization |

| Exchange Act | | Securities Exchange Act of 1934, as amended |

| | |

| FASB | | Financial Accounting Standards Board |

| FinServ | | FinServ Acquisition Corp., a publicly traded special purpose acquisition company |

| FinTech | | Financial Technology; the term used to describe any technology that delivers financial services through software, such as online banking, mobile payment apps or cryptocurrency |

| First Heritage | | First Heritage Credit, LLC, a wholly-owned U.S. subsidiary of the Company, which we acquired in July 2022 |

| First Heritage SPV | | A revolving credit facility, entered into concurrent with the acquisition of First Heritage, with capacity up to $225.0 million |

| Flexiti | | Flexiti Financial Inc., a wholly-owned Canadian subsidiary of the Company, which we acquired in March 2021 |

| Flexiti Securitization | | A non-recourse revolving credit facility, entered into on December 9, 2021, with capacity up to C$526.5 million |

| | | | | | | | |

| Term or abbreviation | | Definition |

| Flexiti SPV | | A revolving credit facility, entered into concurrent with the acquisition of Flexiti, with capacity up to C$535.0 million |

| Form 10-K | | This report on Form 10-K for the year ended December 31, 2022 |

| Gross Combined Loans Receivable | | Gross loans receivable plus loans originated by third-party lenders which are Guaranteed by the Company. As a result of the sale of the Legacy U.S. Direct Lending business on July 8, 2022, the Company no longer guarantees loans originated by third-party lenders through CSO programs |

| Guaranteed by the Company | | Loans originated by third-party lenders through the CSO program which we historically guaranteed but did not include in the Consolidated Financial Statements. All balances in connection with the CSO programs were disposed of on July 8, 2022 with the divestiture of the Legacy U.S. Direct Lending Business. |

| Heights Finance | | SouthernCo, Inc., a Delaware corporation d/b/a Heights Finance, a wholly-owned U.S. subsidiary of

the Company, which we acquired in December 2021 |

| Heights Finance SPV | | A non-recourse revolving credit facility, entered into concurrent with the acquisition of Heights Finance, with capacity up to $350.0 million. This facility was extinguished on July 15, 2022 when we entered into a new non-recourse revolving warehouse facility, see "Heights SPV." |

| Heights SPV | | A revolving credit facility, entered into to replace the incumbent lender's facility and finance future loans originated by Heights Finance, with capacity up to $425.0 million |

| ICFR | | Internal control over financial reporting |

| Katapult | | Katapult Holdings, Inc. a lease-to-own platform for online, brick and mortar and omni-channel retailers. |

| Legacy U.S. Direct Lending Business | | The Legacy U.S. Direct Lending Business historically operated under the Speedy Cash, Rapid Cash and Avio Credit brands. We sold the Legacy U.S. Direct Lending Business to Community Choice Financial on July 8, 2022. |

| LFL | | LFL Group, Canada's largest home furnishings retailer. |

| LIBOR | | London Inter-Bank Offered Rate |

| MDR | | Merchant discount revenue |

| NCO | | Net charge-off; total charge-offs less total recoveries |

| | |

| POS | | Point-of-sale |

| | |

| | |

| ROU | | Right of use |

| RSU | | Restricted Stock Unit |

| SEC | | U.S. Securities and Exchange Commission |

| Senior Revolver | | Senior Secured Revolving Loan Facility with borrowing capacity of $40.0 million as of December 31, 2022 |

| Sequential | | The change from one quarter to the next fiscal quarter |

| SOFR | | Secured Overnight Financing Rate |

| SPAC | | Special Purpose Acquisition Company |

| | |

| SPE | | Special Purpose Entity |

| SPV | | Special Purpose Vehicle |

| SRC | | Smaller Reporting Company as defined by the SEC |

| TDR | | Troubled Debt Restructuring. Debt restructuring for which a concession is granted to the borrower as a result of economic or legal reasons related to the borrower's financial difficulties |

| | |

| UDAAP | | Unfair, deceptive, or abusive acts and practices |

| U.K. Subsidiaries | | Collectively, Curo Transatlantic Limited and SRC Transatlantic Limited. These wholly-owned subsidiaries were placed into administration in February 2019. |

| U.S. | | United States of America |

| | |

| U.S. GAAP | | Accounting principles generally accepted in the U.S. |

| U.S. SPV | | An asset-backed revolving credit facility with capacity up to $200.0 million if certain conditions are met. This facility was extinguished on July 7, 2022. |

| VIE | | Variable Interest Entity; our wholly-owned, bankruptcy-remote special purpose subsidiaries |

FORWARD LOOKING STATEMENTS

This Form 10-K contains forward-looking statements. These forward-looking statements include projections, estimates and assumptions about various matters, including future financial and operational performance and may be identified by words such as "guidance," "estimate," "anticipate," "believe," "forecast," "step," "plan," "predict," "focused," "project," "is likely," "is possible," "expect," "anticipate," "intend," "should," "will," 'may," "confident," "trend" and variations of such words and similar expressions. The matters discussed in these forward-looking statements are based on management's beliefs, assumptions, current expectations and estimates and projections, and are subject to risk, uncertainties and other factors that could cause actual results to differ materially from those made, projected or implied in the forward-looking statements. Except as required by applicable law and regulations, we undertake no obligation to update any forward-looking statements or other statements we may make in the following discussion or elsewhere in this document even though these statements may be affected by events or circumstances occurring after the forward-looking statements or other statements were made. Please see the section titled “Risk Factors” below for a discussion of the uncertainties, risks and assumptions associated with our business.

PART I

The terms "CURO," "we," "our," "us" and "Company" include CURO Group Holdings Corp. and all of its direct and indirect subsidiaries as a combined entity, except where otherwise stated.

This report references third-party reports and studies solely for informational purposes only. Investors and market participants should not place undue reliance on such references, and the underlying reports and studies are not part of this report.

ITEM 1. BUSINESS

Company Overview

We are a tech-enabled, omni-channel consumer finance company serving a full spectrum of non-prime, near-prime and prime consumers in portions of the U.S. and Canada. CURO was founded over 25 years ago to meet the growing needs of consumers looking for alternative access to credit. We continuously update our products and technology platform to offer a variety of convenient, accessible financial and loan services. We design our customer experience to allow consumers to apply for, update and manage their loans in the channels they prefer—in branch, and via mobile device or over the phone. Our high customer satisfaction scores speak to our ability to anticipate and exceed customers’ needs.

In the U.S., we operate under several principal brands, including "Covington Credit," "Heights Finance," "Quick Credit," "Southern Finance" and "First Heritage." In Canada, we operate under “Cash Money” and “LendDirect” direct lending brands and the "Flexiti" POS/BNPL brand. As of December 31, 2022, we operated our direct lending and online services in eight Canadian provinces and one Canadian territory. Our point-of-sale operations are available at over 8,400 retail locations and over 3,500 merchant partners across 10 provinces and two territories. Until the sale of our Legacy U.S. Direct Lending Business in July 2022, we also operated under brands that included "Speedy Cash," "Rapid Cash" and "Avio Credit." We also offered demand deposit accounts in the U.S. under the "Revolve Finance" brand, and credit card programs under the "First Phase" brand, until the fourth quarter of 2022. As of December 31, 2022, our store network consisted of 496 locations across 13 U.S. states.

Recent Business Developments

Flexiti Acquisition

On March 10, 2021, we acquired Flexiti, an emerging growth Canadian POS/BNPL provider, which provided us instant capability and scale opportunity in Canada's credit card and POS financing markets. Flexiti offers the customers of its retail partners a variety of promotional financing offers on big-ticket purchases such as furniture, appliances, jewelry and electronics.

Heights Finance Acquisition

On December 27, 2021, we acquired Heights Finance, a consumer finance company that provides Installment loans and offers customary opt-in insurance and other financial products in the U.S. The acquisition of Heights Finance accelerated our strategic transition toward longer term, higher balance and lower credit risk products, and provided us with access to a larger addressable market while mitigating regulatory risk.

Divestiture of Legacy U.S. Direct Lending Business

On July 8, 2022, we sold our Legacy U.S. Direct Lending Business, which operated under the "Speedy Cash", "Rapid Cash" and "Avio Credit" brands, to Community Choice Financial.

First Heritage Acquisition

On July 13, 2022, we purchased First Heritage, a consumer lender that provides near-prime installment loans and customary opt-in insurance and other financial products in the U.S. This acquisition furthered our strategic shift to broaden our presence in the near-prime consumer lending market in the U.S.

These transactions were foundational to our strategic transition into longer term, higher balance and lower rate credit products. Refer to Note 14, "Acquisitions and Divestiture" for additional details regarding the divestiture of our Legacy U.S. Direct Lending Business and the acquisitions of First Heritage, Heights Finance and Flexiti.

2022 Restructuring and Expense Saving Initiatives

In October 2022, we began restructuring actions to increase our operating efficiency by reducing our global workforce and closing 89 stores across the U.S. and Canada. These actions were aimed at reducing duplicative corporate functions and stores with overlapping customer populations as a result of our recent acquisitions. Refer to Note 21, "Restructuring and Store Closures" for additional details regarding these initiatives.

Regulatory Developments

Our Products and Services

Overview of Loan Product Revenue

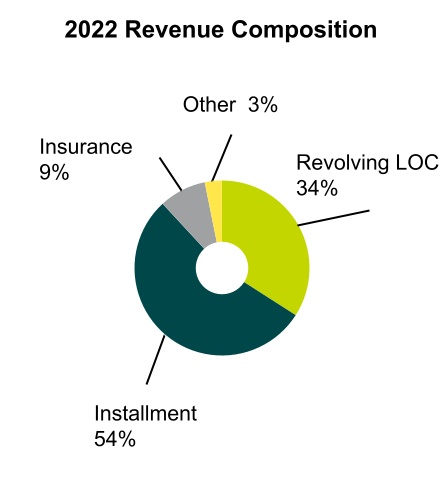

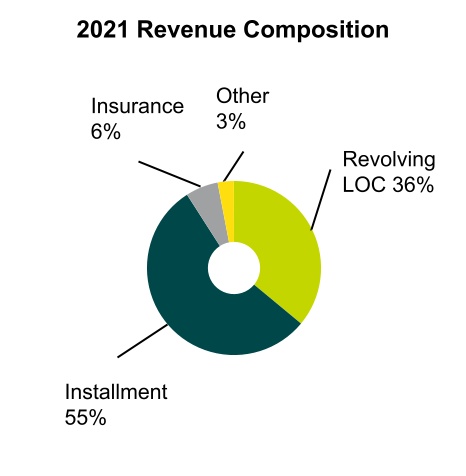

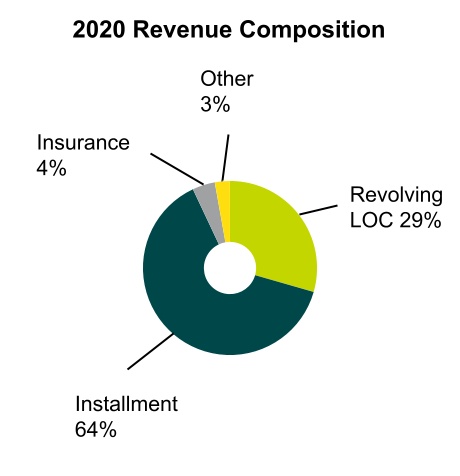

The following charts depict the revenue contribution, including CSO fees, of our products and services:

Our direct lending operations include a broad range of direct-to-consumer finance products focusing on revolving LOC, installment loans, insurance and other ancillary products, serving our customers' diversified needs as they address credit and related financial needs. The acquisitions of Heights Finance and First Heritage enable us to expand the geographic reach of our Installment products in the U.S. Through our acquisition of Flexiti in March 2021, we diversified our products, now offering POS financing options for consumers in Canada. We also provide a number of ancillary financial products such as optional credit protection, demand deposit accounts, proprietary general-purpose credit cards, check cashing and money transfer services. Our products are licensed and governed by enabling federal and state legislation in the U.S. and federal and provincial regulations in Canada. For additional details regarding recent regulatory developments, see "Regulatory Environment and Compliance" below.

Installment Loans

Installment loan products range from unsecured, short-term loans in Canada whereby a customer receives cash in exchange for a post-dated personal check or a pre-authorized debit from the customer’s bank account, to fixed-term, fully amortizing loans with a fixed payment amount due each period during the term of the loan in both U.S. and Canada. Certain Installment loans are secured by a clear vehicle title or security interest in the vehicle. The customer receives the benefit of immediate cash and retains possession of the vehicle while the loan is outstanding. Payments are due bi-weekly or monthly to match the customer's pay cycle. Customers may prepay without penalty or fees. Loans offered by Heights Finance and First Heritage are considered Installment loans, and can be unsecured or secured. Installment loans comprised 53.5%, 54.9% and 63.6% of our consolidated revenue during the years ended December 31, 2022, 2021 and 2020, respectively.

Revolving LOC Loans

Revolving LOC loans are lines of credit without a specified maturity date. Customers in good standing may draw against their line of credit, repay with minimum, partial or full payment and redraw as needed. We earn interest on the outstanding loan balances. Customers may prepay without penalty or fees. Typically, customers do not initially draw the full amount of their credit limits. Canada Direct Lending Revolving LOC loans comprised 93.8%, 94.2% and 91.8% of our total Canada Direct Lending loans as of December 31, 2022, 2021 and 2020, respectively. As of December 31 2022, Revolving LOC loans also included the Flexiti POS financing products, which are included in our Canada POS Lending segment and allow us to offer BNPL products as well as Flexiti branded credit cards at merchant locations. Canada POS Lending Revolving LOC gross loans receivable increased $374.3 million, or 81.5% from December 31, 2021. For the years ended December 31, 2022, 2021 and 2020, revolving loans revenues were $345.8 million, $294.6 million and $249.5 million, respectively.

Insurance Premiums and Commissions

We offer consumers a number of insurance products, including Credit Life and Disability, Involuntary Unemployment, Personal Property Collateral and Collateral Protection Plans. These products are optional and not a condition of the loan. We do not sell insurance to non-borrowers. We own a captive insurance company in the U.S. that reinsures a portion of our insurance sales. We earn revenue from the sale of optional credit protection insurance, which we recognize ratably over the term of the loan. Credit protection insurance is available to consumers on certain Revolving LOC and Installment products. For the years ended December 31, 2022, 2021 and 2020, insurance revenues were $88.5 million, $49.4 million and $35.6 million, respectively.

Other

Other products we offer include general-purpose credit cards, ancillary financial products including check cashing, prepaid cards, demand deposit and money transfer services. We offer memberships for car club, home and auto related services. We have no direct risk of loss on these membership plans. Check cashing, demand deposit and money transfer product lines in the U.S.ended with the divestiture of the Legacy U.S. Direct Lending Business and are now only offered by Canada Direct Lending. Revenues from consumer products include credit card revenue, check cashing and miscellaneous fees such as administrative fees, annual membership fees, over limit fees and deferral fees.

For the years ended December 31, 2022, 2021 and 2020, other revenues were $32.0 million, $24.7 million and $23.7 million, respectively.

CSO Programs

Through our CSO programs, we acted as a CSO/CAB on behalf of customers in accordance with applicable state laws. We offered Installment loans with a maximum term of 180 days through CSO programs in stores and online in the state of Texas. As a CSO, we earned revenue by charging the customer a CSO fee for arranging an unrelated third party to make a loan to that customer.

CSO loans were made by a third-party lender, and thus we did not include them in our Consolidated Balance Sheets as loans receivable; instead, we included fees receivable in “Prepaid expenses and other” in our Consolidated Balance Sheets.