UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended September 30, 2021

OR

For the transition period from _________to__________

Commission File Number 1-38315

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction Of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (316 ) 772-3801

Former name, former address and former fiscal year, if changed since last report: No Changes

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | ||||||||||||

| Non-accelerated filer | ☐ | |||||||||||||

| Smaller reporting company | Emerging growth company | |||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of October 29, 2021 there were 40,452,336 shares of the registrant’s Common Stock, $0.001 par value per share, outstanding.

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

FORM 10-Q

THIRD QUARTER ENDED September 30, 2021

INDEX

| Page | |||||||||||||||||||||||

Item 1. | Financial Statements (unaudited) | ||||||||||||||||||||||

| September 30, 2021 (unaudited) and December 31, 2020 | |||||||||||||||||||||||

Three and nine months ended September 30, 2021 and 2020 (unaudited) | |||||||||||||||||||||||

Three and nine months ended September 30, 2021 and 2020 (unaudited) | |||||||||||||||||||||||

Three and nine months ended September 30, 2021 and 2020 (unaudited) | |||||||||||||||||||||||

| Item 2. | |||||||||||||||||||||||

| Item 3. | |||||||||||||||||||||||

| Item 4. | |||||||||||||||||||||||

| Item 1. | |||||||||||||||||||||||

| Item 1A. | |||||||||||||||||||||||

| Item 2. | |||||||||||||||||||||||

| Item 3. | |||||||||||||||||||||||

| Item 4. | |||||||||||||||||||||||

| Item 5. | |||||||||||||||||||||||

| Item 6. | |||||||||||||||||||||||

2

PART I. FINANCIAL INFORMATION

GLOSSARY

Terms and abbreviations used throughout this report are defined below.

| Term or abbreviation | Definition | |||||||

| 2017 Final CFPB Rule | The final rule issued by the CFPB in 2017 regarding Payday, Vehicle Title and Certain high Cost Installment loans | |||||||

| 2019 Proposed Rule | The subsequent CFPB rulemaking process which proposed to rescind the mandatory underwriting provisions of the 2017 Final CFPB Rule | |||||||

| 2020 Form 10-K | Annual Report on Form 10-K for the year ended December 31, 2020, filed with the SEC on March 5, 2021 | |||||||

| 7.50% Senior Secured Notes | 7.50% Senior Secured Notes, issued in July 2021 for $750.0 million, which mature in August 2028 | |||||||

| 8.25% Senior Secured Notes | 8.25% Senior Secured Notes, issued in August 2018 for $690.0 million, which we extinguished during the third quarter of 2021 | |||||||

| Ad Astra | Ad Astra Recovery Services, Inc., a wholly-owned subsidiary of the Company, which, prior to acquisition in January 2020, was our exclusive provider of third-party collection services for the U.S. business | |||||||

| Adjusted EBITDA | EBITDA plus or minus certain non-cash and other adjusting items; Refer to "Supplemental Non-GAAP Financial Information" for additional details | |||||||

| ALL | Allowance for loan losses | |||||||

| Allowance coverage | Allowance for loan losses as a percentage of gross loans receivable | |||||||

| AOCI | Accumulated Other Comprehensive Income (Loss) | |||||||

| ASC | Accounting Standards Codification | |||||||

| ASU | Accounting Standards Update | |||||||

| Average gross loans receivable | Utilized to calculate product yield and NCO rates; calculated as average of beginning of quarter and end of quarter gross loans receivable | |||||||

| BNPL | Buy-Now-Pay-Later | |||||||

| bps | Basis points | |||||||

| C$ | Canadian dollar | |||||||

| CAB | Credit Access Business | |||||||

| CARES Act | Coronavirus Aid, Relief, and Economic Security Act enacted by the U.S. Federal government on March 27, 2020 in response to the COVID-19 pandemic | |||||||

| CURO Canada | CURO Canada Corp, a wholly-owned Canadian subsidiary of the Company, formerly known as Cash Money Cheque Cashing Inc. | |||||||

| Cash Money Revolving Credit Facility | C$10.0 million revolving credit facility with Royal Bank of Canada, maintained by CURO Canada | |||||||

| CDOR | Canadian Dollar Offered Rate | |||||||

| CFPB | Consumer Financial Protection Bureau | |||||||

| CFSA | Community Financial Services Association | |||||||

| CFTC | CURO Financial Technologies Corp., a wholly-owned subsidiary of the Company | |||||||

| CODM | Chief Operating Decision Maker | |||||||

| Condensed Consolidated Financial Statements | The condensed consolidated financial statements presented in this Form 10-Q | |||||||

| CSO | Credit services organization | |||||||

| EBITDA | Earnings Before Interest, Taxes, Depreciation and Amortization | |||||||

| Exchange Act | Securities Exchange Act of 1934, as amended | |||||||

| FASB | Financial Accounting Standards Board | |||||||

| FinServ | FinServ Acquisition Corp., a publicly traded special purpose acquisition company (trading symbol FSRV) | |||||||

| FinTech | Financial Technology; the term used to describe any technology that delivers financial services through software, such as online banking, mobile payment apps or cryptocurrency | |||||||

| Flexiti | Flexiti Financial Inc., a wholly-owned Canadian subsidiary of the Company, which we acquired on March 10, 2021 | |||||||

| Form 10-Q | This report on Form 10-Q for the quarter September 30, 2021 | |||||||

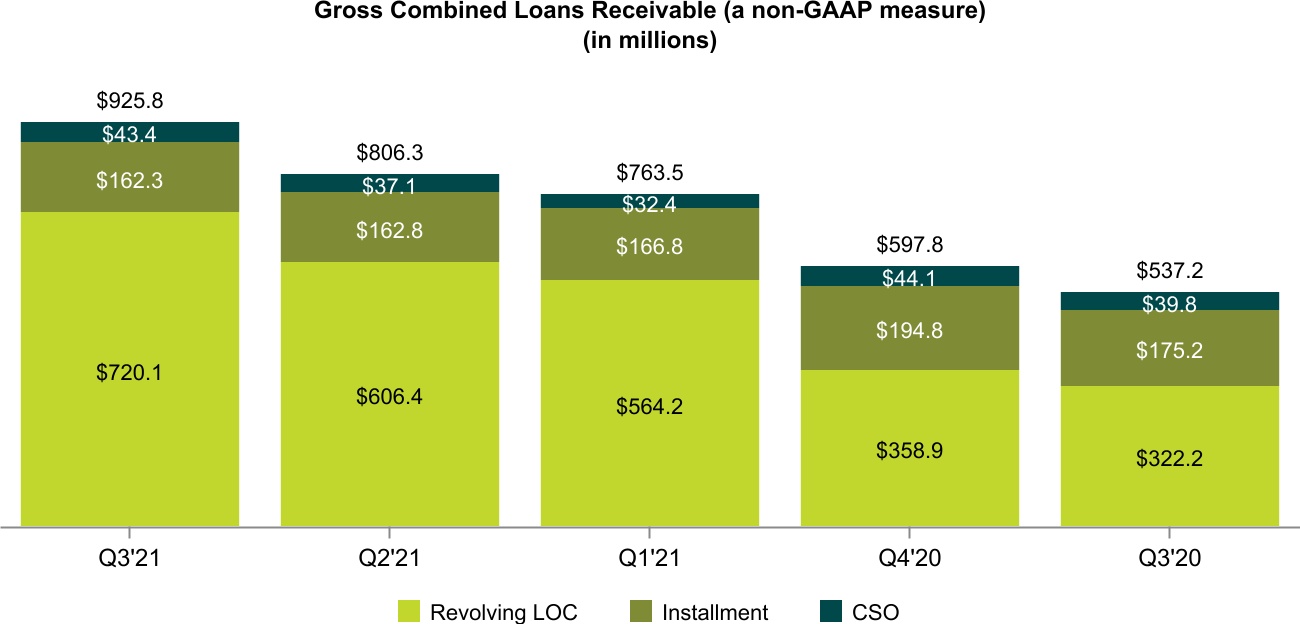

| Gross Combined Loans Receivable | Gross loans receivable plus loans originated by third-party lenders which are Guaranteed by the Company | |||||||

| Guaranteed by the Company | Loans originated by third-party lenders through the CSO program which we guarantee but are not included in the Condensed Consolidated Financial Statements | |||||||

3

| Term or abbreviation | Definition | |||||||

| Katapult | Katapult Holdings, Inc. a lease-to-own platform for online platform for online, brick and mortar and omni-channel retailers. | |||||||

| LFL | LFL Group, Canada's largest home furnishings retailer. | |||||||

| LIBOR | London Inter-Bank Offered Rate | |||||||

| MDR | Merchant discount revenue | |||||||

| NCO | Net charge-off; total charge-offs less total recoveries | |||||||

| NOL | Net operating loss | |||||||

| Non-Recourse Canada SPV Facility | A four-year revolving credit facility with Waterfall Asset Management, LLC, with capacity up to C$250.0 million | |||||||

| Non-Recourse Flexiti SPE Facility | A revolving credit facility, entered into concurrent with the acquisition of Flexiti, with capacity up to C$500.0 million | |||||||

| Non-Recourse U.S. SPV Facility | A four-year, asset-backed revolving credit facility with Atalaya Capital Management with capacity up to $200.0 million if certain conditions are met | |||||||

| POS | Point-of-sale | |||||||

| ROU | Right of use | |||||||

| RSU | Restricted Stock Unit | |||||||

| SEC | Securities and Exchange Commission | |||||||

| Senior Revolver | Senior Secured Revolving Loan Facility with borrowing capacity of $50.0 million | |||||||

| Sequential | The change from one quarter to the next quarter | |||||||

| SPAC | Special Purpose Acquisition Company | |||||||

| SPE | Special Purpose Entity | |||||||

| SPV | Special Purpose Vehicle | |||||||

| SRC | Smaller Reporting Company as defined by the SEC | |||||||

| TDR | Troubled Debt Restructuring. Debt restructuring in which a concession is granted to the borrower as a result of economic or legal reasons related to the borrower's financial difficulties | |||||||

| U.S. | United States of America | |||||||

| U.S. GAAP | Generally accepted accounting principles in the United States | |||||||

| Verge Credit loans | Loans originated and funded by a third-party bank | |||||||

| VIE | Variable Interest Entity; our wholly-owned, bankruptcy-remote special purpose subsidiaries | |||||||

4

ITEM 1. FINANCIAL STATEMENTS

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except share data)

| September 30, 2021 (unaudited) | December 31, 2020 | ||||||||||

| ASSETS | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Restricted cash (includes restricted cash of consolidated VIEs of $ | |||||||||||

Gross loans receivable (includes loans of consolidated VIEs of $ | |||||||||||

Less: Allowance for loan losses (includes allowance for loan losses of consolidated VIEs of $ | ( | ( | |||||||||

Loans receivable, net | |||||||||||

| Income taxes receivable | |||||||||||

Prepaid expenses and other (includes prepaid expenses and other of consolidated VIEs of $ | |||||||||||

| Property and equipment, net | |||||||||||

| Investments in Katapult | |||||||||||

| Right of use asset - operating leases | |||||||||||

| Deferred tax assets | |||||||||||

| Goodwill | |||||||||||

| Intangibles, net | |||||||||||

| Other assets | |||||||||||

| Total Assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||||||

| Liabilities | |||||||||||

Accounts payable and accrued liabilities (includes accounts payable and accrued liabilities of consolidated VIEs of $ | $ | $ | |||||||||

| Deferred revenue | |||||||||||

| Lease liability - operating leases | |||||||||||

| Contingent consideration related to acquisition | |||||||||||

Accrued interest (includes accrued interest of consolidated VIEs of $ | |||||||||||

| Liability for losses on CSO lender-owned consumer loans | |||||||||||

Debt (includes debt and issuance costs of consolidated VIEs of $ | |||||||||||

| Other long-term liabilities | |||||||||||

| Deferred tax liabilities | |||||||||||

| Total Liabilities | |||||||||||

| Commitments and contingencies (Note 12) | |||||||||||

| Stockholders' Equity | |||||||||||

Preferred stock - $ | |||||||||||

Common stock - $ | |||||||||||

Treasury stock, at cost - | ( | ( | |||||||||

| Paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Total Stockholders' Equity | |||||||||||

| Total Liabilities and Stockholders' Equity | $ | $ | |||||||||

See accompanying Notes to unaudited Condensed Consolidated Financial Statements.

5

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

(unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Revenue | $ | $ | $ | $ | |||||||||||||||||||

| Provision for losses | |||||||||||||||||||||||

| Net revenue | |||||||||||||||||||||||

| Cost of providing services | |||||||||||||||||||||||

| Salaries and benefits | |||||||||||||||||||||||

| Occupancy and office | |||||||||||||||||||||||

| Other costs of providing services | |||||||||||||||||||||||

| Advertising | |||||||||||||||||||||||

| Total cost of providing services | |||||||||||||||||||||||

| Gross margin | |||||||||||||||||||||||

| Operating expense (income) | |||||||||||||||||||||||

| Corporate, district and other expenses | |||||||||||||||||||||||

| Interest expense | |||||||||||||||||||||||

| Loss (income) from equity method investment | ( | ( | ( | ||||||||||||||||||||

| Gain from equity method investment | ( | ||||||||||||||||||||||

| Total operating expense | |||||||||||||||||||||||

| Other expense | |||||||||||||||||||||||

| Loss on extinguishment of debt | |||||||||||||||||||||||

| Total other expense | |||||||||||||||||||||||

| (Loss) income from continuing operations before income taxes | ( | ||||||||||||||||||||||

| (Benefit) provision for income taxes | ( | ( | |||||||||||||||||||||

| Net (loss) income from continuing operations | ( | ||||||||||||||||||||||

| Income from discontinued operations, before income tax | |||||||||||||||||||||||

| Income tax expense related to disposition | |||||||||||||||||||||||

| Net income from discontinued operations | |||||||||||||||||||||||

| Net (loss) income | $ | ( | $ | $ | $ | ||||||||||||||||||

| Basic (loss) earnings per share: | |||||||||||||||||||||||

| Continuing operations | $ | ( | $ | $ | $ | ||||||||||||||||||

| Discontinued operations | |||||||||||||||||||||||

| Basic (loss) earnings per share | $ | ( | $ | $ | $ | ||||||||||||||||||

| Diluted (loss) earnings per share: | |||||||||||||||||||||||

| Continuing operations | $ | ( | $ | $ | $ | ||||||||||||||||||

| Discontinued operations | |||||||||||||||||||||||

| Diluted (loss) earnings per share | $ | ( | $ | $ | $ | ||||||||||||||||||

| Weighted average common shares outstanding: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

See accompanying Notes to unaudited Condensed Consolidated Financial Statements.

6

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

(in thousands)

(unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Net (loss) income | $ | ( | $ | $ | $ | ||||||||||||||||||

| Other comprehensive (loss) income: | |||||||||||||||||||||||

| Foreign currency translation adjustment, net of tax | ( | ( | ( | ||||||||||||||||||||

| Other comprehensive (loss) income | ( | ( | ( | ||||||||||||||||||||

| Comprehensive (loss) income | $ | ( | $ | $ | $ | ||||||||||||||||||

See accompanying Notes to unaudited Condensed Consolidated Financial Statements.

7

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(dollars in thousands, unaudited)

| Nine Months Ended September 30, | |||||||||||

| 2021 | 2020 | ||||||||||

| Cash flows from operating activities | |||||||||||

| Net income from continuing operations | $ | $ | |||||||||

Adjustments to reconcile net income to net cash provided by continuing operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Provision for loan losses | |||||||||||

| Amortization of debt issuance costs and bond discount | |||||||||||

| Loss on extinguishment of debt | |||||||||||

| Deferred income tax (benefit) expense | ( | ||||||||||

| Loss on disposal of property and equipment | |||||||||||

| Income from equity method investment | ( | ( | |||||||||

| Gain from equity method investment | ( | ||||||||||

| Change in fair value of contingent consideration | |||||||||||

| Share-based compensation | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accrued interest on loans receivable | |||||||||||

| Prepaid expenses and other assets | ( | ||||||||||

| Accounts payable and accrued liabilities | ( | ||||||||||

| Deferred revenue | ( | ||||||||||

| Income taxes receivable | ( | ||||||||||

| Accrued interest | ( | ( | |||||||||

| Other long-term liabilities | ( | ||||||||||

| Net cash provided by continuing operating activities | |||||||||||

| Net cash provided by discontinued operating activities | |||||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities | |||||||||||

| Purchase of property, equipment and software | ( | ( | |||||||||

Loans receivable originated or acquired | ( | ( | |||||||||

Loans receivable repaid | |||||||||||

| Proceeds from (Investment in) Katapult | ( | ||||||||||

Acquisition of Ad Astra, net of acquiree's cash received | ( | ||||||||||

| Acquisition of Flexiti, net of acquiree's cash received | ( | ||||||||||

Net cash used in investing activities (1) | ( | ( | |||||||||

| Cash flows from financing activities | |||||||||||

| Proceeds from Non-Recourse SPV and SPE facilities | |||||||||||

| Payments on Non-Recourse SPV and SPE facilities | ( | ( | |||||||||

| Debt issuance costs paid | ( | ( | |||||||||

| Proceeds from credit facilities | |||||||||||

| Payments on credit facilities | ( | ( | |||||||||

Extinguishment of | ( | ||||||||||

Proceeds from issuance of | |||||||||||

| Payments of call premiums from early debt extinguishments | ( | ||||||||||

| Proceeds from exercise of stock options | |||||||||||

| Payments to net settle restricted stock units vesting | ( | ( | |||||||||

| Repurchase of common stock | ( | ( | |||||||||

| Dividends paid to stockholders | ( | ( | |||||||||

Net cash provided by (used in) financing activities (1) | ( | ||||||||||

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | ( | ( | |||||||||

| Net increase in cash, cash equivalents and restricted cash | |||||||||||

| Cash, cash equivalents and restricted cash at beginning of period | |||||||||||

| Cash, cash equivalents and restricted cash at end of period | $ | $ | |||||||||

8

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(dollars in thousands, unaudited)

See accompanying Notes to unaudited Condensed Consolidated Financial Statements.

SUPPLEMENTAL CASH FLOW INFORMATION

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported within the unaudited Condensed Consolidated Balance Sheets as of September 30, 2021 and 2020 to the cash, cash equivalents and restricted cash used in the Statement of Cash Flows (in thousands):

| September 30, | ||||||||||||||

| 2021 | 2020 | |||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

Restricted cash (includes restricted cash of consolidated VIEs of $ | ||||||||||||||

| Total cash, cash equivalents and restricted cash used in the Statement of Cash Flows | $ | $ | ||||||||||||

9

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND NATURE OF OPERATIONS

Nature of Operations

The terms “CURO" and the “Company” refer to CURO Group Holdings Corp. and its direct and indirect subsidiaries as a combined entity, except where otherwise stated.

The Company is a tech-enabled, omni-channel consumer finance company serving a full spectrum of non-prime consumers in the U.S and non-prime and prime consumers in Canada. Effective with its acquisition of Flexiti on March 10, 2021, CURO provides a BNPL solution for customers in Canada.

Basis of Presentation

The Company has prepared the accompanying unaudited Condensed Consolidated Financial Statements in accordance with U.S. GAAP and the accounting policies described in its 2020 Form 10-K. Interim results of operations are not necessarily indicative of results that might be expected for future interim periods or for the year ending December 31, 2021.

Following the acquisition of Flexiti, the Company reports Flexiti operations as the "Canada POS Lending" segment throughout this Form 10-Q. Refer to Note 11, "Segment Reporting" for further information.

While certain information and note disclosures normally included in annual financial statements prepared in accordance with U.S. GAAP have been condensed or omitted, the Company believes that the disclosures are adequate to enable a reasonable understanding of the information presented. Additionally, the Company will continue to take advantage of the scaled disclosure requirements permitted by the SEC for. SRCs for the quarter-to-date and year-to-date periods presented. SRC status is determined on an annual basis as of the last business day of the most recently completed second fiscal quarter. The Company qualified as an SRC until June 30, 2021, but after that date, the Company no longer qualified as an SRC and thus will begin to report as a non-SRC beginning with the first quarter of 2022.

Principles of Consolidation

The unaudited Condensed Consolidated Financial Statements reflect the accounts of CURO and its direct and indirect subsidiaries, including Flexiti, which was acquired on March 10, 2021, and Ad Astra, which was acquired on January 3, 2020. Refer to Note 15, "Acquisitions" for further disclosures related to these acquisitions. Intercompany transactions and balances have been eliminated in consolidation.

10

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Change in Accounting Principle Related to Equity Method Investment in Katapult

Katapult is an e-commerce focused, FinTech company offering an innovative lease financing solution to consumers and enabling essential transactions at the merchant POS. CURO first invested in Katapult in 2017 as the Company identified multiple catalysts for Katapult's future success: an innovative e-commerce POS business model, a focus on the large and under-penetrated non-prime financing market and a clear and compelling value proposition for merchants and consumers. The Company accounts for its investment in Katapult under the equity method of accounting as of September 30, 2021. Refer to Note 8, "Fair Value Measurements" for further disclosures regarding the accounting for the Company's investment in Katapult.

Historically, the Company reported income and loss from its equity method investment in Katapult on a two-month reporting lag. The merger between Katapult and FinServ in June 2021 triggered a change in Katapult's control environment and reporting structure to coincide with SEC reporting requirements. As a result, during the first quarter of 2021 the Company applied a change in accounting principle to reflect the Company's share of Katapult's historical and ongoing results from a two-month reporting lag to a one-quarter reporting lag. The Company believes this change in accounting principle is preferable as it provides the Company with the ability to present the results of its equity method investment after Katapult’s results are publicly available and related internal controls have been completed. The Company has not retrospectively applied the change in accounting principle because the impact on the financial statements was immaterial for all periods presented.

Continuing Impacts of COVID-19

The COVID-19 pandemic continues to cause significant uncertainty and impacts. Macroeconomic conditions, in general, and the Company's operations, specifically, have been significantly affected by COVID-19. Government responses to the pandemic, either through the form of mandated lockdowns or a variety of stimulus programs to mitigate the impact of the pandemic, suppressed loan demand in 2020 and into the first quarter of 2021. For details regarding the effect COVID-19 had on the Company's operations in 2020, the Company's response to mitigate the impact of the pandemic and the U.S. and Canadian federal and local responses to the pandemic, refer to the 2020 Form 10-K. During the second quarter of 2021, the runoff of additional federal stimulus programs in the U.S. resulted in the stabilization of the Company's U.S. loan portfolio and resulted in moderately higher NCO and past-due trends, though still at relatively low levels compared to pre-COVID-19 trends. For further information regarding the impact the pandemic had on loan balances as of September 30, 2021, refer to Note 3, "Loans Receivable and Revenue."

Goodwill

The annual impairment review for goodwill consists of performing a qualitative assessment to determine whether it is more likely than not that a reporting unit’s fair value is less than its carrying amount, as a basis for determining whether or not further testing is required. The Company may elect to bypass the qualitative assessment and proceed directly to the two-step process, for any reporting unit in any period. The Company can resume the qualitative assessment for any reporting unit in any subsequent period. If the Company determines, on the basis of qualitative factors, that it is more likely than not that the fair value of the reporting unit is less than the carrying amount, the Company will then apply a two-step process of (i) determining the fair value of the reporting unit and (ii) comparing it to the carrying value of the net assets allocated to the reporting unit. When performing the two-step process, if the fair value of the reporting unit exceeds its carrying value, no further analysis or write-down of goodwill is required. In the event the estimated fair value of a reporting unit is less than the carrying value, the Company would recognize an impairment loss equal to such excess, which could significantly and adversely impact reported results of operations and stockholders’ equity.

11

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

During the fourth quarter of 2020, the Company performed a quantitative assessment for the U.S. and Canada Direct Lending reporting units. Management concluded that the estimated fair values of these two reporting units were greater than their respective carrying values. During the three and nine months ended September 30, 2021, the Company did not identify triggering events that indicate an impairment existed and did no

Recently Adopted Accounting Pronouncements

ASU 2020-01

In January 2020, the FASB issued ASU 2020-01, Investments-Equity Securities (Topic 321), Investments-Equity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic 815) (ASU 2020-01). ASU 2020-01 clarifies the interaction of the accounting for equity securities under Topic 321, the accounting for equity method investments in Topic 323 and the accounting for certain forward contracts and purchased options in Topic 815. The Company adopted ASU 2020-01 as of January 1, 2021, which did not have a material impact on the unaudited Condensed Consolidated Financial Statements.

ASU 2019-12

In December 2019, the FASB issued ASU 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes (Topic 740). The ASU intends to simplify various aspects related to accounting for income taxes and removes certain exceptions to the general principles in Topic 740. Additionally, the ASU clarifies and amends existing guidance to improve consistent application of its requirements. The Company adopted ASU 2019-12 as of January 1, 2021, which did not have a material impact on the Company's unaudited Condensed Consolidated Financial Statements.

Recently Issued Accounting Pronouncements Not Yet Adopted

ASU 2016-13

In June 2016, the FASB issued ASU 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, and subsequent amendments to the guidance: ASU 2018-19 in November 2018, ASU 2019-04 in April 2019, ASU 2019-05 in May 2019, ASU 2019-10 and -11 in November 2019 and ASU 2020-02 in February 2020. The amended standard changes how entities will measure credit losses for most financial assets and certain other instruments that are not measured at fair value through net income. The standard will replace the current “incurred loss” approach with an “expected loss” model for instruments measured at amortized cost. The amendment will affect loans, debt securities, trade receivables, net investments in leases, off-balance sheet credit exposures, reinsurance receivables and any other financial assets not excluded from the scope that have the contractual right to receive cash.

ASU 2019-10 amends the mandatory effective date for ASU 2016-13. As a result, ASU 2016-13 and related amendments are effective for fiscal years beginning after December 15, 2022 for entities that qualified as an SRC as of June 30, 2019, such as the Company. ASU 2016-13 and its amendments should be applied on either a prospective transition or modified-retrospective approach depending on the subtopic. Early adoption is permitted. The Company is evaluating its alternatives with respect to the available accounting methods under ASU 2016-13, including the fair value option. If the fair value option is not utilized, adoption of ASU 2016-13 will increase the allowance for credit losses, with a resulting negative adjustment to retained earnings on the date of adoption. The Company deferred the adoption of ASU 2016-13 as permitted under ASU 2019-10. The Company is currently assessing the impact that adoption of ASU 2016-13 will have on its financial statements.

12

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

ASU 2020-04 and subsequent amendments

In March 2020, the FASB issued ASU 2020-04, Reference Rate Reform - Facilitation of the Effects of Reference Rate Reform on Financial Reporting. This ASU provides temporary optional expedients and exceptions to U.S. GAAP guidance on contract modifications and hedge accounting to ease the financial reporting burdens of the upcoming market transition from LIBOR and other interbank offered rates to alternative reference rates, such as the Secured Overnight Financing Rate. Entities can elect not to apply certain modification accounting requirements to contracts affected by this reference rate reform, if certain criteria are met. An entity that makes this election would not have to remeasure the contracts at the modification date or reassess a previous accounting determination. Entities also can elect various optional expedients that would allow them to continue applying hedge accounting for hedging relationships affected by reference rate reform if certain criteria are met. The guidance is effective upon issuance and generally can be applied through December 31, 2022. The FASB also issued ASU 2021-01, Reference Rate Reform (Topic 848): Scope in January 2021. It clarifies that certain optional expedients and exceptions in Topic 848 apply to derivatives that are affected by the discounting transition. The amendments in this ASU affect the guidance in ASU 2020-04 and are effective in the same timeframe as ASU 2020-04. The Company does not expect the adoption of these ASUs to have a material impact on its financial statements.

NOTE 2 - VARIABLE INTEREST ENTITIES

As of September 30, 2021, the Company had three credit facilities whereby certain loans receivable were sold to VIEs to collateralize debt incurred under each facility. See Note 5, "Debt" for additional details on the Non-Recourse U.S. SPV Facility, entered into in April 2020, the Non-Recourse Canada SPV Facility, entered into in August 2018, and the Non-Recourse Flexiti SPE Facility, entered into concurrent with the Company's acquisition of Flexiti in March 2021.

The carrying amounts of consolidated VIEs' assets and liabilities were as follows (in thousands):

| September 30, 2021 | December 31, 2020 | |||||||||||||

| Assets | ||||||||||||||

| Restricted cash | $ | $ | ||||||||||||

| Loans receivable, net | ||||||||||||||

Intercompany receivable(1) | ||||||||||||||

| Prepaid expenses and other | ||||||||||||||

| Deferred tax assets | ||||||||||||||

| Total Assets | $ | $ | ||||||||||||

| Liabilities | ||||||||||||||

| Accounts payable and accrued liabilities | $ | $ | ||||||||||||

| Deferred revenue | ||||||||||||||

| Accrued interest | ||||||||||||||

| Debt | ||||||||||||||

| Total Liabilities | $ | $ | ||||||||||||

| (1) Intercompany receivable VIE balances eliminate upon consolidation. | ||||||||||||||

NOTE 3 – LOANS RECEIVABLE AND REVENUE

13

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

The following table summarizes revenue by product (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||||||||||||

| Revolving LOC | $ | $ | $ | $ | ||||||||||||||||||||||

| Unsecured Installment | ||||||||||||||||||||||||||

| Secured Installment | ||||||||||||||||||||||||||

| Single-Pay | ||||||||||||||||||||||||||

| Total Installment | ||||||||||||||||||||||||||

| Ancillary | ||||||||||||||||||||||||||

Total revenue(1) | $ | $ | $ | $ | ||||||||||||||||||||||

(1) Includes revenue from CSO programs of $ | ||||||||||||||||||||||||||

The following tables summarize loans receivable by product and the related delinquent loans receivable (in thousands):

| September 30, 2021 | |||||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Single-Pay(1) | Total Installment - Company Owned | Total | ||||||||||||||||||||||||

| Current loans receivable | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||

| Delinquent loans receivable | |||||||||||||||||||||||||||||

| Total loans receivable | |||||||||||||||||||||||||||||

| Less: allowance for losses | ( | ( | ( | ( | ( | ( | |||||||||||||||||||||||

| Loans receivable, net | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||

(1) Of the $ | |||||||||||||||||||||||||||||

| September 30, 2021 | ||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Total Installment - Company Owned | Total | ||||||||||||||||||||||

| Delinquent loans receivable | ||||||||||||||||||||||||||

| 0-30 days past due | $ | $ | $ | $ | $ | |||||||||||||||||||||

| 31-60 days past due | ||||||||||||||||||||||||||

| 61 + days past due | ||||||||||||||||||||||||||

| Total delinquent loans receivable | $ | $ | $ | $ | $ | |||||||||||||||||||||

| December 31, 2020 | |||||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Single-Pay(1) | Total Installment - Company Owned | Total | ||||||||||||||||||||||||

| Current loans receivable | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||

| Delinquent loans receivable | |||||||||||||||||||||||||||||

| Total loans receivable | |||||||||||||||||||||||||||||

| Less: allowance for losses | ( | ( | ( | ( | ( | ( | |||||||||||||||||||||||

| Loans receivable, net | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||

(1) Of the $ | |||||||||||||||||||||||||||||

14

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| December 31, 2020 | ||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Total Installment - Company Owned | Total | ||||||||||||||||||||||

| Delinquent loans receivable | ||||||||||||||||||||||||||

| 0-30 days past due | $ | $ | $ | $ | $ | |||||||||||||||||||||

| 31-60 days past due | ||||||||||||||||||||||||||

| 61 + days past due | ||||||||||||||||||||||||||

| Total delinquent loans receivable | $ | $ | $ | $ | $ | |||||||||||||||||||||

The following tables summarize loans Guaranteed by the Company under CSO programs and the related delinquent receivables (in thousands):

| September 30, 2021 | ||||||||||||||

| Unsecured Installment | Secured Installment | Total Installment - Guaranteed by the Company | ||||||||||||

| Current loans receivable Guaranteed by the Company | $ | $ | $ | |||||||||||

| Delinquent loans receivable Guaranteed by the Company | ||||||||||||||

| Total loans receivable Guaranteed by the Company | ||||||||||||||

| Less: Liability for losses on CSO lender-owned consumer loans | ( | ( | ( | |||||||||||

| Loans receivable Guaranteed by the Company, net | $ | $ | $ | |||||||||||

| September 30, 2021 | ||||||||||||||

| Unsecured Installment | Secured Installment | Total Installment - Guaranteed by the Company | ||||||||||||

| Delinquent loans receivable | ||||||||||||||

| 0-30 days past due | $ | $ | $ | |||||||||||

| 31-60 days past due | ||||||||||||||

| 61+ days past due | ||||||||||||||

| Total delinquent loans receivable | $ | $ | $ | |||||||||||

| December 31, 2020 | ||||||||||||||

| Unsecured Installment | Secured Installment | Total Installment - Guaranteed by the Company | ||||||||||||

| Current loans receivable Guaranteed by the Company | $ | $ | $ | |||||||||||

| Delinquent loans receivable Guaranteed by the Company | ||||||||||||||

| Total loans receivable Guaranteed by the Company | ||||||||||||||

| Less: Liability for losses on CSO lender-owned consumer loans | ( | ( | ( | |||||||||||

| Loans receivable Guaranteed by the Company, net | $ | $ | $ | |||||||||||

| December 31, 2020 | ||||||||||||||

| Unsecured Installment | Secured Installment | Total Installment - Guaranteed by the Company | ||||||||||||

| Delinquent loans receivable | ||||||||||||||

| 0-30 days past due | $ | $ | $ | |||||||||||

| 31-60 days past due | ||||||||||||||

| 61 + days past due | ||||||||||||||

| Total delinquent loans receivable | $ | $ | $ | |||||||||||

15

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

The following tables summarize activity in the ALL and the liability for losses on CSO lender-owned consumer loans in total (in thousands):

| Three Months Ended September 30, 2021 | |||||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Single-Pay | Total Installment | Other | Total | |||||||||||||||||||||||

| Allowance for loan losses: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Recoveries | |||||||||||||||||||||||||||||

| Net charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Provision for losses | |||||||||||||||||||||||||||||

| Effect of foreign currency translation | ( | ( | ( | ( | ( | ||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Liability for losses on CSO lender-owned consumer loans: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Increase in liability | |||||||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Three Months Ended September 30, 2020 | |||||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Single-Pay | Total Installment | Other | Total | |||||||||||||||||||||||

| Allowance for loan losses: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Recoveries | |||||||||||||||||||||||||||||

| Net charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Provision for losses | |||||||||||||||||||||||||||||

| Effect of foreign currency translation | |||||||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Liability for losses on CSO lender-owned consumer loans: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Increase in liability | |||||||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

16

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Nine Months Ended September 30, 2021 | |||||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Single-Pay | Total Installment | Other | Total | |||||||||||||||||||||||

| Allowance for loan losses: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Recoveries | |||||||||||||||||||||||||||||

| Net charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Provision for losses | |||||||||||||||||||||||||||||

| Effect of foreign currency translation | ( | ( | |||||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Liability for losses on CSO lender-owned consumer loans: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Decrease in liability | ( | ( | ( | ( | |||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Nine Months Ended September 30, 2020 | |||||||||||||||||||||||||||||

| Revolving LOC | Unsecured Installment | Secured Installment | Single-Pay | Total Installment | Other | Total | |||||||||||||||||||||||

| Allowance for loan losses: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Recoveries | |||||||||||||||||||||||||||||

| Net charge-offs | ( | ( | ( | ( | ( | ( | ( | ||||||||||||||||||||||

| Provision for losses | |||||||||||||||||||||||||||||

| Effect of foreign currency translation | ( | ( | ( | ( | ( | ||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Liability for losses on CSO lender-owned consumer loans: | |||||||||||||||||||||||||||||

| Balance, beginning of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

| Decrease in liability | ( | ( | ( | ( | |||||||||||||||||||||||||

| Balance, end of period | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||

As of September 30, 2021, Revolving LOC and Installment loans classified as nonaccrual were $5.1 million and $6.1 million, respectively. As of December 31, 2020, Revolving LOC and Installment loans classified as nonaccrual were $4.4 million and $6.2 million, respectively. The Company's loans receivable inherently considers nonaccrual loans in its estimate of the ALL as delinquencies are a primary input into the Company's roll rate-based model.

TDR Loans Receivable

In certain circumstances, the Company modifies the terms of its loans receivable for borrowers. Under U.S. GAAP, a modification of loans receivable terms is considered a TDR if the borrower is experiencing financial difficulty and the Company grants a concession to the borrower it would not have otherwise granted under the terms of the original agreement. In response to COVID-19 in 2020, the Company established an enhanced Customer Care Program, which enables its team members to provide relief to customers in various ways, ranging from due date changes, interest or fee forgiveness, payment waivers or extended payment plans, depending on a customer’s individual circumstances. The Company modifies loans only if it believes the customer has the ability to pay under the restructured terms. The Company continues to accrue and collect interest on these loans in accordance with the restructured terms.

17

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

The Company records its ALL related to TDRs by discounting the estimated cash flows associated with the respective TDR at the effective interest rate immediately after the loan modification and records any difference between the discounted cash flows and the carrying value as an allowance adjustment. A loan that has been classified as a TDR remains so classified until the loan is paid off or charged off. A TDR is charged off consistent with the Company's policies for the related loan product. For additional information on the Company's loss recognition policy, see the 2020 Form 10-K.

The table below presents TDRs that are related to the Customer Care Program implemented in response to COVID-19, included in both gross loans receivable and the impairment included in the ALL (in thousands):

As of September 30, 2021 | As of December 31, 2020 | ||||||||||

| Current TDR gross receivables | $ | $ | |||||||||

| Delinquent TDR gross receivables | |||||||||||

| Total TDR gross receivables | |||||||||||

| Less: Impairment included in the allowance for loan losses | ( | ( | |||||||||

| Less: Additional allowance | ( | ( | |||||||||

| Outstanding TDR receivables, net of impairment | $ | $ | |||||||||

The tables below present loans modified and classified as TDRs during the periods presented (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||||||||||||

| Pre-modification TDR loans receivable | $ | $ | $ | $ | ||||||||||||||||||||||

| Post-modification TDR loans receivable | ||||||||||||||||||||||||||

| Total concessions included in gross charge-offs | $ | $ | $ | $ | ||||||||||||||||||||||

There were $2.9 million and $5.1 million of loans classified as TDRs that were charged off and included as a reduction in the ALL during the three months ended September 30, 2021 and 2020, respectively, and $11.0 million and $6.0 million during the nine months ended September 30, 2021 and 2020, respectively. The Company had commitments to lend additional funds of approximately $2.1 million to customers with available and unfunded Revolving LOC loans classified as TDRs as of September 30, 2021.

The table below presents the Company's average outstanding TDR loans receivable, interest income recognized on TDR loans and number of TDR loans for the periods presented (dollars in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||||||||||||

| Average outstanding TDR loans receivable | $ | $ | $ | $ | ||||||||||||||||||||||

| Interest income recognized | ||||||||||||||||||||||||||

| Number of TDR loans | ||||||||||||||||||||||||||

NOTE 4 – CREDIT SERVICES ORGANIZATION

The CSO fee receivables were $5.2 million and $5.0 million at September 30, 2021 and December 31, 2020, respectively, and are reflected in "Prepaid expenses and other" in the unaudited Condensed Consolidated Balance Sheets. The Company bears the risk of loss through its guarantee to purchase customer loans that are charged-off. The terms of these loans range up to six months . See Note 1, "Summary of Significant Accounting Policies and Nature of Operations" of the 2020 Form 10-K for further details of the Company's accounting policy.

As of September 30, 2021 and December 31, 2020, the incremental maximum amount payable under all such guarantees was $35.3 million and $36.6 million, respectively. This liability is not included in the Company's unaudited Condensed Consolidated Balance Sheets. If the Company is required to pay any portion of the total amount of the loans it has guaranteed, it will attempt to recover the entire amount or a portion from the applicable customers. The Company holds no collateral in respect of the guarantees. The Company estimates a liability for losses associated with the guaranty provided to the CSO lenders, which was $7.0 million and $7.2 million at September 30, 2021 and December 31, 2020, respectively. This liability is reflected in "Liability for losses on CSO lender-owned consumer loans" in the unaudited Condensed Consolidated Balance Sheets.

18

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

NOTE 5 – DEBT

Debt consisted of the following (in thousands):

| September 30, 2021 | December 31, 2020 | |||||||||||||

| $ | $ | |||||||||||||

| Non-Recourse U.S. SPV Facility | ||||||||||||||

| Non-Recourse Canada SPV Facility | ||||||||||||||

| Non-Recourse Flexiti SPE Facility | ||||||||||||||

| Debt | $ | $ | ||||||||||||

In July 2021, the Company issued $750.0 million of 7.50 % Senior Secured Notes which mature on August 1, 2028. Interest on the notes is payable semiannually, in arrears, on February 1 and August 1. In connection with the 7.50 % Senior Secured Notes, financing costs of $15.5 million were capitalized, net of amortization, and included in the unaudited Condensed Consolidated Balance Sheets as a component of "Debt." These costs are amortized over the term of the 7.50 % Senior Secured Notes as a component of interest expense.

In August 2018, the Company issued $690.0 million of 8.25 % Senior Secured Notes maturing on September 1, 2025. In connection with the 8.25 % Senior Secured Notes, the Company capitalized financing costs of $13.9 million, which were being amortized over the term of the 8.25 % Senior Secured Notes as a component of interest expense.

During the third quarter of 2021, the 8.25 % Senior Secured Notes were extinguished using proceeds from the 7.50 % Senior Secured Notes described above. The early extinguishment of the 8.25 % Senior Secured Notes resulted in a loss of $40.2 million.

Non-Recourse U.S. SPV Facility

In April 2020, CURO Receivables Finance II, LLC, a wholly-owned subsidiary of the Company, entered into the Non-Recourse U.S. SPV Facility with Midtown Madison Management LLC, as administrative agent, and Atalaya Asset Income Fund VI LP, as the initial lender. As of September 30, 2021, the Non-Recourse U.S. SPV Facility provided for $200.0 million of borrowing capacity.

As of September 30, 2021, the effective interest rate on the Company's borrowings was one-month LIBOR plus 6.25 %. The borrower pays the lenders a monthly commitment fee at an annual rate of 0.50 % on the unused portion of the commitments. The Company is currently evaluating the impact of the upcoming transition from LIBOR to an alternative reference rate.

As of September 30, 2021, outstanding borrowings under the Non-Recourse U.S. SPV Facility were $44.9 million, net of deferred financing costs of $4.5 million. For further information on the Non-Recourse U.S. SPV Facility, refer to Note 2, "Variable Interest Entities."

The Non-Recourse U.S. SPV Facility matures on April 8, 2024.

19

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Non-Recourse Canada SPV Facility

In August 2018, CURO Canada Receivables Limited Partnership, a wholly-owned subsidiary of the Company, entered into the Non-Recourse Canada SPV Facility with Waterfall Asset Management, LLC. The Non-Recourse Canada SPV Facility currently provides for C$175.0 million of borrowing capacity and the ability to expand such capacity up to C$250.0 million. As of September 30, 2021, the effective interest rate was three-month CDOR plus 6.75 %. The borrower also pays a 0.50 % per annum commitment fee on the unused portion of the commitments. The Non-Recourse Canada SPV Facility matures on September 2, 2023.

As of September 30, 2021, outstanding borrowings under the Non-Recourse Canada SPV Facility were $96.8 million, net of deferred financing costs of $1.0 million. For further information on the Non-Recourse Canada SPV Facility, refer to Note 2, "Variable Interest Entities."

Non-Recourse Flexiti SPE Facility

In March 2021, concurrently with the acquisition of Flexiti, Flexiti Financing SPE Corp., a wholly-owned Canadian subsidiary of the Company, refinanced and increased its Non-Recourse Flexiti SPE Facility to C$500.0 million, with a maturity on March 10, 2024. As of September 30, 2021, the effective interest rate was three-month CDOR plus 4.40 %. The borrower also pays a 0.50 % to 1.00 % per annum commitment fee on the unused portion of the commitments.

As of September 30, 2021, outstanding borrowings under the Non-Recourse Flexiti SPE Facility were $255.7 million, net of deferred financing costs of $4.2 million. For further information on the Non-Recourse Flexiti SPE Facility, refer to Note 2, "Variable Interest Entities."

Senior Revolver

The Company maintains the Senior Revolver that provides $50.0 million of borrowing capacity, including up to $5.0 million of standby letters of credit, for a one-year term, renewable for successive terms following annual review. The current term expires June 30, 2022. The Senior Revolver accrues interest at one-month LIBOR plus 5.00 %. The Senior Revolver is syndicated among four banks. The Company is currently evaluating the impact of the upcoming transition from LIBOR to an alternative reference rate.

The Senior Revolver is guaranteed by all subsidiaries that guarantee the 7.50 % Senior Secured Notes, and is secured by a lien on substantially all assets of CURO and the guarantor subsidiaries that are senior to the lien securing the 7.50 % Senior Secured Notes.

The revolver was undrawn at September 30, 2021 and December 31, 2020.

Cash Money Revolving Credit Facility

CURO Canada maintains the Cash Money Revolving Credit Facility, a C$10.0 million revolving credit facility with Royal Bank of Canada, which provides short-term liquidity for the Company's Canadian direct lending operations. As of September 30, 2021, the borrowing capacity under the Cash Money Revolving Credit Facility was C$9.9 million, net of C$0.1 million in outstanding stand-by letters of credit.

The Cash Money Revolving Credit Facility is collateralized by substantially all of CURO Canada’s assets and contains various covenants that require, among other things, that the aggregate borrowings outstanding under the facility not exceed the borrowing base, as well as restrictions on the encumbrance of assets and the creation of indebtedness. Borrowings under the Cash Money Revolving Credit Facility bear interest per annum at the prime rate of a Canadian chartered bank plus 1.95 %.

The Cash Money Revolving Credit Facility was undrawn at September 30, 2021 and December 31, 2020.

NOTE 6 – SHARE-BASED COMPENSATION

20

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

RSUs

As of September 30, 2021, the Company has granted three types of RSUs: time-based, market-based and, in connection with the Flexiti acquisition, performance-based.

Grants of time-based RSUs are valued at the grant date based on the closing market price of the Company's common stock and are expensed using the straight-line method over the service period. Time-based RSUs typically vest over a three-year period.

Grants of market-based RSUs are valued using the Monte Carlo simulation pricing model. The market-based RSUs granted to date vest after three years if the Company's total stockholder return over the three-year performance period meets a specified target relative to other companies in its selected peer group. Expense recognition for market-based RSUs occurs over the service period using the straight-line method.

Upon closing of the Flexiti acquisition in March 2021, the Company granted performance-based RSUs to certain Flexiti employees. Grants of performance-based RSUs are valued at the grant date based on the closing market price of the Company's common stock. The performance-based RSUs vest over two years if Flexiti achieves specified internal targets, including revenue less NCOs and loan originations metrics. Expense recognition for performance-based RSUs occurs ratably over the service period if it is probable that the targets will be achieved as of each period end. If such results are not probable, no share-based compensation expense is recognized and any previously recognized share-based compensation expense is reversed.

Unvested shares of RSUs generally are forfeited upon termination of employment, or failure to achieve the required performance condition, if applicable.

A summary of the activity of time-based, market-based and performance-based unvested RSUs as of September 30, 2021 and changes during the nine months ended September 30, 2021 is presented in the following table:

| Number of RSUs | |||||||||||||||||

| Time-Based | Market-Based | Performance-Based | Weighted Average Grant Date Fair Value per Share | ||||||||||||||

| December 31, 2020 | $ | ||||||||||||||||

| Granted | |||||||||||||||||

| Vested | ( | ||||||||||||||||

| Forfeited | ( | ( | |||||||||||||||

| September 30, 2021 | $ | ||||||||||||||||

Share-based compensation expense for the three months ended September 30, 2021 and 2020, which includes compensation costs from stock options and RSUs, was $4.0 million and $3.4 million, respectively, and during the nine months ended September 30, 2021 and 2020 was $10.1 million and $9.9 million, respectively. Share-based compensation expense is included in the unaudited Condensed Consolidated Statements of Operations as a component of "Corporate, district and other expenses."

NOTE 7 – INCOME TAXES

The Company's effective income tax rate was 24.9 % and 3.0 % for the nine months ended September 30, 2021 and 2020, respectively.

The effective income tax rate for the nine months ended September 30, 2021, was lower compared to the blended federal and state/provincial statutory rate of approximately 26 %, primarily as a result of proportionally more net income in lower-tax rate jurisdictions, driven by the $146.9 million gain on the Katapult merger in the second quarter of 2021 and the $40.2 million loss on extinguishment of debt in the third quarter of 2021. Additionally, the effective tax rate also includes (i) the release of a valuation allowance of $0.4 million due to the Company's share of Katapult's income, (ii) tax benefits related to share-based compensation of $0.2 million, (iii) $1.3 million of tax expense related to the non-deductible transaction costs and the change in fair value of contingent consideration, (iv) $0.3 million tax expense of additional Texas accrual for 2020 due to the settlement of 2013 to 2019 Texas returns and (v) a tax benefit of $0.9 million for the recognition of the research and development tax credit.

The lower effective income tax rate for the nine months ended September 30, 2020 was primarily due to a tax benefit from the CARES Act. The CARES Act, among other things, allows NOLs incurred in 2018, 2019 and 2020 to be carried back to each of the five preceding taxable years to generate a refund of previously paid Federal income taxes. The Company recorded an income tax

21

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

NOTE 8 – FAIR VALUE MEASUREMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. The Company is required to use valuation techniques that are consistent with the market approach, income approach and/or cost approach. Inputs to valuation techniques refer to the assumptions that market participants would use in pricing the asset or liability based on observable market data obtained from independent sources, or unobservable, meaning those that reflect the Company's own judgment about the assumptions market participants would use in pricing the asset or liability based on the best information available for the specific circumstances. Accounting standards establish a three-level fair value hierarchy based upon the assumptions (inputs) used to price assets or liabilities. The hierarchy requires the Company to maximize the use of observable inputs and minimize the use of unobservable inputs.

The three levels of inputs used to measure fair value are listed below.

Level 1 – Inputs are unadjusted quoted prices in active markets for identical assets or liabilities that the Company has access to at the measurement date.

Level 2 – Inputs include quoted market prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability and inputs that are derived principally from or corroborated by observable market data by correlation or other means (market corroborated inputs).

22

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Financial Assets and Liabilities Carried at Fair Value

The table below presents the assets and liabilities that were carried at fair value on the unaudited Condensed Consolidated Balance Sheets at September 30, 2021 (in thousands):

| Estimated Fair Value | |||||||||||||||||

| Carrying Value September 30, 2021 | Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Financial assets: | |||||||||||||||||

| Cash Surrender Value of Life Insurance | $ | $ | $ | $ | $ | ||||||||||||

| Financial liabilities: | |||||||||||||||||

| Non-qualified deferred compensation plan | $ | $ | $ | $ | $ | ||||||||||||

| Contingent consideration related to acquisition | |||||||||||||||||

Contingent consideration related to acquisition

In connection with the acquisition of Flexiti during the first quarter of 2021, the Company recorded a liability for contingent consideration based on the achievement of revenue less NCOs and loan origination targets over the two years following closing of the acquisition that could result in additional cash consideration up to $32.8 million to Flexiti's former stockholders. The fair value of the liability is estimated using the option-based income approach using a Monte Carlo simulation model discounted back to the reporting date. The significant unobservable inputs (Level 3) used to estimate the fair value included the expected future tax benefits associated with the acquisition, the probability that the risk adjusted-revenue and origination targets will be achieved and discount rates. The contingent consideration measured at fair value using unobservable inputs increased from the initial measurement of $20.6 million as of March 31, 2021 to $24.1 million as of September 30, 2021. For additional information on Flexiti and the related contingent consideration, refer to Note 15, "Acquisitions."

The table below presents the assets and liabilities that were carried at fair value on the unaudited Condensed Consolidated Balance Sheets at December 31, 2020 (in thousands):

| Estimated Fair Value | |||||||||||||||||

| Carrying Value December 31, 2020 | Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Financial assets: | |||||||||||||||||

| Cash Surrender Value of Life Insurance | $ | $ | $ | $ | $ | ||||||||||||

| Financial liabilities: | |||||||||||||||||

| Non-qualified deferred compensation plan | $ | $ | $ | $ | $ | ||||||||||||

Financial Assets and Liabilities Not Carried at Fair Value

The table below presents the assets and liabilities that were not carried at fair value on the unaudited Condensed Consolidated Balance Sheets at September 30, 2021 (in thousands):

| Estimated Fair Value | |||||||||||||||||

| Carrying Value September 30, 2021 | Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Financial assets: | |||||||||||||||||

| Cash and cash equivalents | $ | $ | $ | $ | $ | ||||||||||||

| Restricted cash | |||||||||||||||||

| Loans receivable, net | |||||||||||||||||

| Financial liabilities: | |||||||||||||||||

Liability for losses on CSO lender-owned consumer loans | $ | $ | $ | $ | $ | ||||||||||||

| Non-Recourse U.S. SPV facility | |||||||||||||||||

| Non-Recourse Canada SPV facility | |||||||||||||||||

| Non-Recourse Flexiti SPE facility | |||||||||||||||||

23

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

The table below presents the assets and liabilities that were not carried at fair value on the unaudited Condensed Consolidated Balance Sheets at December 31, 2020 (in thousands):

| Estimated Fair Value | |||||||||||||||||

| Carrying Value December 31, 2020 | Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Financial assets: | |||||||||||||||||

| Cash and cash equivalents | $ | $ | $ | $ | $ | ||||||||||||

| Restricted cash | |||||||||||||||||

| Loans receivable, net | |||||||||||||||||

| Financial liabilities: | |||||||||||||||||

| Liability for losses on CSO lender-owned consumer loans | $ | $ | $ | $ | $ | ||||||||||||

| Non-Recourse U.S. SPV facility | |||||||||||||||||

| Non-Recourse Canada SPV facility | |||||||||||||||||

Loans Receivable, Net

Loans receivable are carried on the unaudited Condensed Consolidated Balance Sheets net of the ALL. The unobservable inputs used to calculate the carrying values include quantitative factors, such as current default trends. Also considered in evaluating the accuracy of the models are changes to the loan portfolio mix, the impact of new loan products, changes to underwriting criteria or lending policies, new store development or entrance into new markets, changes in jurisdictional regulations or laws, recent credit trends and general economic conditions. The carrying value of loans receivable approximates their fair value. Refer to Note 3, "Loans Receivable and Revenue" for additional information. Loans receivable acquired as part of the Flexiti acquisition, which represent $82.3 million of the $809.8 million, are carried at gross contractual balance less unamortized fair value discount and ALL. For additional information on the determination of the fair value discount, refer to Note 15, "Acquisitions."

CSO Program

In connection with CSO programs, the Company guarantees consumer loan payment obligations to unrelated third-party lenders for loans that the Company arranges for consumers on the third-party lenders’ behalf. The Company is required to purchase from the lender charged-off loans that it has guaranteed. Refer to Note 3, "Loans Receivable and Revenue" and Note 4, Credit Services Organization" for additional information.

The fair value disclosure for the 7.50 % Senior Secured Notes as of September 30, 2021 and 8.25 % Senior Secured Notes as of December 31, 2020 were based on observable market trading data. The fair values of the Non-Recourse U.S. SPV Facility, Non-Recourse Canada SPV Facility and Non-Recourse Flexiti SPE Facility were based on the cash needed for their respective final settlements.

24

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Investment in Katapult

The table below presents the Company's investment in Katapult (in thousands):

| Equity Method Investment | Measurement Alternative (1) | Total Investment in Katapult | ||||||||||||||||||

| Balance at December 31, 2019 | $ | $ | — | $ | ||||||||||||||||

| Equity method (loss) - Q1 2020 | ( | — | ( | |||||||||||||||||

| Balance at March 31, 2020 | — | |||||||||||||||||||

| Equity method income - Q2 2020 | ||||||||||||||||||||

| Balance at June 30, 2020 | ||||||||||||||||||||

| Equity method income - Q3 2020 | ||||||||||||||||||||

| Accounting policy change for certain securities from equity method investment to measurement alternative | ( | |||||||||||||||||||

| Purchases of common stock warrants and preferred shares | ||||||||||||||||||||

| Balance at September 30, 2020 | ||||||||||||||||||||

| Equity method income - Q4 2020 | ||||||||||||||||||||

| Purchases of common stock | ||||||||||||||||||||

| Balance at December 31, 2020 | ||||||||||||||||||||

| Equity method income - Q1 2021 | ||||||||||||||||||||

| Balance at March 31, 2021 | ||||||||||||||||||||

| Equity method income - Q2 2021 | ||||||||||||||||||||

Conversion of investment(2) | ( | ( | ||||||||||||||||||

| Balance at June 30, 2021 | ||||||||||||||||||||

| Equity method loss - Q3 2021 | ( | $ | ( | |||||||||||||||||

| Balance at September 30, 2021 | $ | $ | $ | |||||||||||||||||

| Classification as of December 31, 2020 | Level 3, not carried at fair value | Level 3, carried at measurement alternative | ||||||||||||||||||

| Classification as of September 30, 2021 | Level 3, not carried at fair value | N/A | ||||||||||||||||||

(1) The Company elected to measure this equity security without a readily determinable fair value equal to its cost minus impairment. If the Company identifies an observable price change in orderly transactions for same or similar investment in Katapult, it will measure the equity security at fair value as of the date that the observable transaction occurred. | ||||||||||||||||||||

(2) On June 9, 2021, Katapult completed its merger with FinServ. Immediately prior to the merger, the Company first converted all of its preferred stock and exercised all common stock warrants, and then exchanged all shares of Katapult common stock for $ | ||||||||||||||||||||

Prior to September 2020, the Company owned 42.5 % of the outstanding shares (excluding unexercised options) of Katapult, comprised of multiple classes of equity, including preferred stock and certain common stock warrants, which met the accounting criteria for in-substance common stock at the time of their acquisition. This financial asset was not carried at fair value. The Company accounted for this investment under the equity method, and recognized a proportionate share of Katapult’s income or loss on a two-month lag.

In September 2020, the Company acquired common stock warrants and preferred shares of Katapult from existing shareholders for $11.2 million in cash. This transaction resulted in the reevaluation of the accounting for all of the Company’s holdings in Katapult. The Company determined that its holdings of certain common stock warrants qualified as in-substance common stock and were required to be accounted for using the equity method. The Company’s holdings in preferred stock and certain other common stock warrants did not meet the criteria for in-substance common stock and therefore were carried at cost minus impairment under the measurement alternative. As a result, the Company (i) reclassified $12.5 million from an equity method investment to cost minus impairment under the measurement alternative, (ii) recorded a purchase of common stock warrants for $4.0 million determined to be in-substance common stock within its equity method investment and (iii) recorded a purchase of preferred stock for $7.2 million that was accounted for under the measurement alternative.

In October and November 2020, the Company acquired common stock of Katapult from existing shareholders for an aggregate $1.6 million. The Company recorded this purchase within its equity method investment.

25

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

During the first quarter of 2021, the Company changed the two-month reporting lag to a one-quarter reporting lag, as discussed in Note 1, "Summary of Significant Accounting Policies and Nature of Operations." The Company recorded a loss of $1.6 million for the three months ended September 30, 2021 and income of $0.7 million for the nine months ended September 30, 2021, based on its share of Katapult’s earnings for the respective periods.

On June 9, 2021, Katapult completed its merger with FinServ. As a result, the Company received $146.9 million in cash and 18.9 million shares of common stock of the resulting public company, Katapult (NASDAQ: KPLT), which are subject to a six-month trading restriction. The Company recorded a related net gain of $135.4 million on its equity method investment in Katapult during the second quarter of 2021. Additionally, as part of the merger, CURO received 3.0 million earn-out warrants and holds two of the seven board of director seats for Katapult. For further information regarding the merger between Katapult and FinServ and its impact on CURO, refer to the description immediately following the table above.

Both the equity method investment and the previously recognized investment measured at cost minus impairment are presented within "Investments in Katapult" on the unaudited Condensed Consolidated Balance Sheet.

26

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

NOTE 9 – STOCKHOLDERS' EQUITY

The following table summarizes the changes in stockholders' equity for the three and nine months ended September 30, 2021 and 2020 (in thousands, except Common Stock data):

| Common Stock | Treasury Stock, at cost | Paid-in capital | Retained Earnings (Deficit) | AOCI (1) | Total Stockholders' Equity | ||||||||||||||||||||||||||||||||||||

| Shares Outstanding | Par Value | ||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2020 | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

| Net income from continuing operations | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Dividends | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||

| Share based compensation expense | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Proceeds from exercise of stock options | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Common stock issued for RSUs vesting, net of shares withheld and withholding paid for employee taxes | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

| Net income from continuing operations | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Dividends | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||

| Share based compensation expense | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Proceeds from exercise of stock options | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Repurchase of common stock | ( | — | ( | — | — | — | ( | ||||||||||||||||||||||||||||||||||

| Common stock issued for RSUs vesting, net of shares withheld and withholding paid for employee taxes | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||

| Balance at June 30, 2021 | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

| Net loss from continuing operations | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Dividends | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||

| Share based compensation expense | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Proceeds from exercise of stock options | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Repurchase of common stock | ( | — | ( | — | — | — | ( | ||||||||||||||||||||||||||||||||||

| Common stock issued for RSUs vesting, net of shares withheld and withholding paid for employee taxes | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||

| Balance at September 30 2021 | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

(1) Accumulated other comprehensive income (loss) | |||||||||||||||||||||||||||||||||||||||||

27

CURO GROUP HOLDINGS CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Common Stock | Treasury Stock, at cost | Paid-in capital | Retained Earnings (Deficit) | AOCI (1) | Total Stockholders' Equity | ||||||||||||||||||||||||||||||||||||