UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

for

the quarterly period ended

or

for the transition period from to .

Commission

file number:

SPONSORED BY GOLD CORPORATION AND EXCHANGE TRADED CONCEPTS, LLC

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

c/o Exchange Traded Concepts, LLC

(Address of principal executive offices) (Zip Code)

(

(Registrant’s telephone number, including area code)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Perth Mint Physical Gold ETF Shares | AAAU | NYSE Arca |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | ☐ | ☒ | |

| Non-Accelerated Filer | ☐ | Smaller Reporting Company | |

| Emerging Growth Company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.). ☐ Yes

The

registrant had

Perth Mint Physical Gold ETF

Table of Contents

i

Part I. FINANCIAL INFORMATION.

Item 1. Unaudited Financial Statements.

Perth Mint Physical Gold ETF

Index to Unaudited Financial Statements

1

Perth Mint Physical Gold ETF

Statements of Assets and Liabilities

| September 30, 2020 | December 31, 2019 | |||||||

| (unaudited) | ||||||||

| Assets | ||||||||

| Investment in gold, at fair value (cost $ | $ | $ | ||||||

| Total Assets | ||||||||

| Liabilities | ||||||||

| Custodial Sponsor Fee payable | ||||||||

| Total Liabilities | ||||||||

| Net Assets | $ | $ | ||||||

| Shares issued and outstanding (unlimited number of shares authorized, par value) | ||||||||

| Net asset value per share | $ | | $ | |||||

See notes to unaudited financial statements.

2

Perth Mint Physical Gold ETF

Schedules of Investments

| September 30, 2020 (unaudited) | ||||||||||||||||

| Ounces | Cost | Fair Value | % of Net Assets | |||||||||||||

| Investment in gold, at fair value | $ | $ | % | |||||||||||||

| Total Investments | $ | $ | % | |||||||||||||

| Liabilities in excess of other assets | ( | ) | ( | )% | ||||||||||||

| Net Assets | $ | % | ||||||||||||||

| December 31, 2019 | ||||||||||||||||

| Ounces | Cost | Fair Value | % of Net Assets | |||||||||||||

| Investment in gold, at fair value | $ | $ | % | |||||||||||||

| Total Investments | $ | $ | % | |||||||||||||

| Liabilities in excess of other assets | ( | ) | ( | )% | ||||||||||||

| Net Assets | $ | % | ||||||||||||||

See notes to unaudited financial statements.

3

Perth Mint Physical Gold ETF

Statements of Operations

| Three

Months Ended September 30, 2020 | Three

Months Ended September 30, 2019 | Nine

Months Ended September 30, 2020 | Nine

Months Ended September 30, 2019 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Investment Income | ||||||||||||||||

| Expenses | ||||||||||||||||

| Custodial Sponsor Fee | $ | $ | ||||||||||||||

| Total expenses | ||||||||||||||||

| Net investment (loss) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized and unrealized gain (loss) | ||||||||||||||||

| Net realized gain (loss) on gold bullion distributed for redemptions | ( | ) | ( | ) | ||||||||||||

| Net realized gain (loss) on gold transferred to pay expenses | ( | ) | ( | ) | ( | ) | ||||||||||

| Net change in unrealized appreciation (depreciation) on: | ||||||||||||||||

| Investment in gold | ||||||||||||||||

| Net realized and unrealized gain (loss) from operations | ||||||||||||||||

| Net Income | $ | $ | $ | $ | ||||||||||||

| Net income per share | $ | | $ | $ | $ | |||||||||||

| Average number of shares (in 000s) | ||||||||||||||||

See notes to unaudited financial statements.

4

Perth Mint Physical Gold ETF

Statements of Changes in Net Assets

| Three Months Ended September 30, 2020 | Three Months Ended September 30, 2019 | Nine Months Ended September 30, 2020 | Nine Months Ended September 30, 2019 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Net Assets - beginning of period | $ | $ | $ | $ | ||||||||||||

| Creations | ||||||||||||||||

| Redemptions | ( | ) | ( | ) | ||||||||||||

| Net creations (redemptions) | ( | ) | ||||||||||||||

| Net investment (loss) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized gain (loss) from gold bullion distributed for redemptions | ( | ) | ( | ) | ||||||||||||

| Net realized gain (loss) from gold transferred to pay expenses | ( | ) | ( | ) | ( | ) | ||||||||||

| Net change in unrealized appreciation (depreciation) on investments in gold | ||||||||||||||||

| Net Assets - end of period | $ | $ | $ | $ | ||||||||||||

See notes to unaudited financial statements.

5

Perth Mint Physical Gold ETF

Financial Highlights

| Three Months Ended September 30, 2020 | Three Months Ended September 30, 2019 | Nine Months Ended September 30, 2020 | Nine Months Ended September 30, 2019 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Per Share Performance (for a share outstanding throughout each period) | ||||||||||||||||

| Net asset value per share, beginning of period | $ | $ | $ | $ | ||||||||||||

| Net investment gain (loss)(a) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized and unrealized gain (loss) on investment in gold | ||||||||||||||||

| Change in net assets from operations | ||||||||||||||||

| Net asset value per share, end of period | $ | $ | ||||||||||||||

| Market value per share, beginning of period(b) | $ | $ | ||||||||||||||

| Market value per share, end of period(b) | $ | $ | ||||||||||||||

| Total Return, at net asset value(c) | % | % | % | % | ||||||||||||

| Total Return, at market value(c) | % | % | % | % | ||||||||||||

| Net assets ($000’s) | $ | $ | $ | $ | ||||||||||||

| Ratios to average net assets(d) | ||||||||||||||||

| Net investment gain (loss) | ( | )% | ( | )% | ( | )% | ( | )% | ||||||||

| Total expenses | ( | )% | ( | )% | ( | )% | ( | )% | ||||||||

| (a) | |

| (b) | |

| (c) | |

| (d) |

See notes to unaudited financial statements.

6

Perth Mint Physical Gold ETF

Notes to Unaudited Financial Statements

1. ORGANIZATION

Perth

Mint Physical Gold ETF (the “Trust”) is a trust formed on

Gold Corporation, trading as the Perth Mint, is a Western Australian Government-owned statutory body corporation established under the Gold Corporation Act 1987 (Western Australia) (the “Gold Corporation Act”). Under section 22 of the Gold Corporation Act, the payment of the cash equivalent of gold due, payable and deliverable by the Custodial Sponsor (including gold held by the Custodial Sponsor for the benefit of the Trust) is guaranteed by the Treasurer of Western Australia, in the name and on behalf of the Crown in right of the State of Western Australia (the “Government Guarantee”). The Government Guarantee is subject to the claims-paying ability of the Government of Western Australia.

Physical

gold that the Trust holds includes London Bars (as defined in the Trust Agreement) and other gold products having a gold purity

of at least

Virtu Financial BD LLC is the initial Authorized

Participant and contributed

The primary objective of the Trust is to provide investors with an opportunity to invest in gold through the shares the Trust issues and have the gold securely stored by the Custodial Sponsor. An additional objective of the Trust is for the shares to reflect the performance of the price of gold less the expenses of the Trust’s operations. The Trust is not actively managed. The shares trade on the NYSE Arca Marketplace (“NYSE Arca”) under the symbol “AAAU.”

The

Trust’s fiscal year-end is December 31.

On September 29, 2020, the Sponsors entered into an agreement to transfer their respective roles to Goldman Sachs Asset Management,

L.P. (the “Goldman Sachs Transaction”). Upon closing of the Goldman Sachs Transaction, Goldman Sachs Asset Management,

L.P. will serve as the new sponsor of the Trust, which will combine the roles of the Custodial Sponsor and the Administrative

Sponsor.

At

the closing of the Goldman Sachs Transaction, Gold Corporation will resign as the Custodian of the Trust’s gold bullion

(in its role as Custodian of the Trust) and a new third-party custodian will be appointed, at which point the payment of the cash

equivalent of gold due, payable and deliverable on behalf of the Trust will no longer be guaranteed under the Government Guarantee.

It is also expected that, immediately after the closing of the Goldman Sachs Transaction, investors will no longer be able to

take delivery of the physical gold bullion in exchange for the shares such investors own. It is also anticipated that the Trust

will be renamed at the closing of the Goldman Sachs Transaction to Goldman Sachs Physical Gold ETF.

7

The statements of assets and liabilities and schedules of investments at September 30, 2020 and the statements of operations and

of changes in net assets for the periods ended September 30, 2020 and 2019, have been prepared on behalf of the Trust and are

unaudited. In the opinion of management of the Administrative Sponsor of the Trust, all adjustments (which include normal recurring

adjustments) necessary to present fairly the financial position and results of operations for the period ended September 30, 2020

have been made.

2. SIGNIFICANT ACCOUNTING POLICIES

In preparing financial statements in conformity with accounting principles generally accepted in the United States (“GAAP”), management of the Administrative Sponsor makes estimates and assumptions that affect the reported amounts of assets, liabilities and disclosures of contingent assets and liabilities at the date of the financial statements, as well as the reported amount of revenue and expenses reported during the period. Actual results could differ from these estimates.

The following is a summary of significant accounting policies followed by the Trust.

2.1. Basis of Presentation

The Administrative Sponsor has determined that the Trust falls within the scope of Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 946, Financial Services - Investment Companies, and has concluded that for reporting purposes, the Trust is classified as an Investment Company (as defined in ASC 946). The Trust is not registered as an investment company under the Investment Company Act of 1940 and is not required to register under such act.

2.2. Valuation of Gold

The Trust follows the provisions of ASC 820, Fair Value Measurements (“ASC 820”). ASC 820 provides guidance for determining fair value and requires increased disclosure regarding the inputs to valuation techniques used to measure fair value. ASC 820 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Gold is held by the Custodial Sponsor, as custodian on behalf of the Trust, at Gold Corporation’s vaulting facilities, generally in Perth, Australia or such other locations where the Custodial Sponsor may maintain vaulting facilities from time to time. Gold is initially and subsequently recognized at its fair value, based on the London Bullion Market Association (“LBMA”) PM Gold Price.

The LBMA PM Gold Price is set at 3:00 p.m. London time via an auction independently operated and administered by ICE Benchmark Administration (“IBA”). The price is set in U.S. dollars per fine troy ounce (“fine ounce”).

On each business day that the NYSE Arca is open for regular trading, as promptly as practicable after 4:00 p.m. New York time, the Trustee will value the gold held by the Trust and will determine the Net Asset Value of the Trust. The Net Asset Value of the Trust is the aggregate value of gold and other assets, if any, of the Trust (other than any amounts credited to the Trust’s reserve account, if any) and cash, if any, less liabilities of the Trust, which include estimated accrued but unpaid fees, expenses and other liabilities. All gold is valued based on its fine ounce content, calculated by multiplying the weight of gold by its purity. The same methodology is applied independent of the type of gold held by the Trust; similarly, the value of up to 430 fine ounces of unallocated gold the Trust may hold is calculated by multiplying the number of fine ounces with the price of gold determined by the Trustee as follows: the Trustee values the gold held by the Trust based on the LBMA PM Gold Price, or the LBMA AM Gold Price, if such day’s LBMA PM Gold Price is not available. If no LBMA PM Gold Price is available for the day, the Trustee will value the Trust’s gold based on the most recently announced LBMA PM Gold Price or LBMA AM Gold Price. If the Custodial Sponsor determines that such price is inappropriate to use, it shall identify an alternate basis for evaluation to be employed by the Trustee. The Custodial Sponsor may instruct the Trustee to use a different publicly available price that the Custodial Sponsor determines to fairly represent the commercial value of the Trust’s gold.

Neither

the Trustee nor the Sponsors are liable to any person for the determination that the most recently announced LBMA PM Gold Price

(or other benchmark price) is not appropriate as a basis for evaluation of the gold held or receivable by the Trust or for any

determination as to the alternative basis for evaluation, provided that such determination is made in good faith. Once the value

of gold has been determined, the Trustee will subtract all estimated accrued but unpaid fees, expenses and other liabilities of

the Trust from the total value of gold and any other assets of the Trust (other than any amounts credited to the Trust’s

reserve account), including cash, if any. The resulting figure is the Net Asset Value of the Trust. The Trustee will also determine

the Net Asset Value per share by dividing the Net Asset Value of the Trust by the number of shares outstanding as of the close

of trading on the NYSE Arca (which includes the net number of any shares deemed created or redeemed on such evaluation day). There

were

8

ASC 820 establishes a hierarchy that prioritizes inputs to valuation techniques used to measure fair value. The three levels of inputs are:

Level 1: Unadjusted quoted prices in active markets for identical assets or liabilities that the Trust has the ability to access.

Level 2: Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments and similar data.

Level 3: Unobservable inputs for the asset or liability to the extent that relevant observable inputs are not available, representing the Trust’s own assumptions about the assumptions that a market participant would use in valuing the asset or liability, and that would be based on the best information available.

The Trustee categorizes the Trust’s investment in gold as a Level 1 asset within the ASC 820 hierarchy.

2.3. Expenses, Realized Gains and Losses

The

Trust’s only ordinary recurring fee is expected to be the fee paid to the Custodial Sponsor, which will accrue daily at

an annualized rate equal to

2.4. Gold Receivable and Payable

Gold receivable or payable represents the quantity of gold covered by contractually binding orders for the creation or redemption of shares respectively, where the gold has not yet been transferred to or from the Trust’s account. Generally, ownership of the gold is transferred within two business days of the trade date.

2.5. Creations and Redemptions of Shares

The

Trust issues and redeems shares in one or more blocks of at least

Orders

to create or redeem Baskets may be placed only by Authorized Participants. An Authorized Participant must: (1) be a registered

broker-dealer or other securities market participant, such as a bank or other financial institution, which, but for an exclusion

from registration, would be required to register as a broker-dealer to engage in securities transactions, (2) be a participant

in DTC, and (3) have an agreement with Gold Corporation, as the Trust’s custodian, or a LBMA gold clearing bank approved

by Gold Corporation establishing an account or have an existing account meeting certain standards. To become an Authorized Participant,

a person must enter into an Authorized Participant Agreement with the Administrative Sponsor and the Trustee. The Authorized Participant

Agreement provides the procedures for the creation and redemption of Baskets and for the delivery of the gold required for such

creations and redemptions. The Authorized Participant Agreement and the related procedures attached thereto may be amended by

the Trustee and the Administrative Sponsor, without the consent of any investor or Authorized Participant. A transaction fee of

$

Authorized Participants who make deposits with the Trust in exchange for Baskets will receive no fees, commissions or other form of compensation or inducement of any kind from either a Sponsor or the Trust, and no such person has any obligation or responsibility to a Sponsor or the Trust to affect any sale or resale of shares.

Changes in the shares during the three months ended September 30, 2020 are:

| Balance at June 30, 2020 | ||||

| Creations | ||||

| Redemptions | ( | ) | ||

| Balance at September 30, 2020 |

9

Changes in the shares during the nine months ended September 30, 2020 are:

| Balance at December 31, 2019 | ||||

| Creations | ||||

| Redemptions | ( | ) | ||

| Balance at September 30, 2020 |

2.6. Organizational Costs

The costs of the Trust’s organization are borne directly by the Custodial Sponsor. The Trust is not obligated to reimburse the Custodial Sponsor for these costs.

2.7. Income Taxes

The Trust is classified as a “grantor trust” for United States federal income tax purposes. As a result, the Trust itself is not subject to United States federal income tax. Instead, the Trust’s income, gain, losses, and expenses will “flow through” to the shareholders, and the Trustee reports these to the Internal Revenue Service on that basis.

The Administrative Sponsor evaluates tax positions taken or expected to be taken in the course of preparing the Trust’s tax returns to determine whether the tax positions are “more-likely-than-not” to be sustained by the applicable tax authority. Tax positions not deemed to meet that threshold would be recorded as an expense in the current year. The Trust is required to analyze all open tax years. Open tax years are those years that are open for examination by the relevant income taxing authority. As of September 30, 2020, the 2018 and 2019 tax years are open for examination. There is no examination in progress at period end.

2.8. New Accounting Pronouncement

In August 2018, the FASB issued Accounting Standards Update 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”). The update provides guidance that eliminates, adds and modifies certain disclosure requirements for fair value measurements. ASU 2018-13 is effective for annual periods beginning after December 15, 2019 and interim periods therein. As a result of adopting ASU 2018-13, the Trust no longer discloses the amounts and reasons of the transfer of assets and liabilities between Level 1 and Level 2 of the Fair Value Hierarchy.

3. INVESTMENT IN GOLD

The following represents the changes in ounces of gold and the respective fair value during the three months ended September 30, 2020:

| Amount in ounces | Amount in US$ | |||||||

| Balance at June 30, 2020 | $ | |||||||

| Creations | ||||||||

| Redemptions | ( | ) | ( | ) | ||||

| Net realized gain (loss) from gold bullion distributed for redemptions | ( | ) | ||||||

| Transfer of gold to pay expenses | ( | ) | ( | ) | ||||

| Net realized gain (loss) from gold transferred to pay expenses | ( | ) | ||||||

| Change in unrealized appreciation (depreciation) on investment in gold | ||||||||

| Balance at September 30, 2020 | $ | |||||||

The following represents the changes in ounces of gold and the respective fair value during the nine months ended September 30, 2020:

| Amount in ounces | Amount in US$ | |||||||

| Balance at December 31, 2019 | $ | |||||||

| Creations | ||||||||

| Redemptions | ( | ) | ( | ) | ||||

| Net realized gain (loss) from gold bullion distributed for redemptions | ( | ) | ||||||

| Transfer of gold to pay expenses | ( | ) | ( | ) | ||||

| Net realized gain (loss) from gold transferred to pay expenses | ( | ) | ||||||

| Change in unrealized appreciation (depreciation) on investment in gold | ||||||||

| Change in unrealized appreciation (depreciation) on unsettled creations (redemptions) | ||||||||

| Balance at September 30, 2020 | $ | |||||||

10

4. RELATED PARTIES – CUSTODIAL SPONSOR, ADMINISTRATIVE SPONSOR, TRUSTEE, CUSTODIAN AND MARKETING FEES

A

fee is paid to the Custodial Sponsor as compensation for services performed under the Trust Agreement. In exchange for the Custodial

Sponsor’s fee, the Custodial Sponsor has agreed to assume and be responsible for the payment of the following expenses,

up to a maximum amount equal to the greater of $

From time to time, the Custodial Sponsor may waive all or a portion of the Custodial Sponsor Fee at its discretion. The Custodial Sponsor is under no obligation to continue a waiver after the end of a stated period, and, if such waiver is not continued, the Custodial Sponsor Fee will thereafter be paid in full. Presently, the Custodial Sponsor does not intend to waive any of its fees.

Affiliates of the Trustee may from time to time act as Authorized Participants or purchase or sell gold or Trust shares for their own account, as agent for their customers and for accounts over which they exercise investment discretion.

Investors may exchange their shares for gold by delivering their shares to Gold Corporation. The procedures for exchanging shares for gold are set forth in the Trust’s prospectus. Gold Corporation may decline to approve an investor’s application for an exchange of shares for gold for any reason, in its sole discretion. Further, Gold Corporation may suspend or reject the exchange of shares for gold during any period while regular trading on the NYSE Arca is suspended or restricted, in which an emergency exists that makes it reasonably impracticable to deliver, dispose of, or evaluate gold, or for such other period as Gold Corporation may deem necessary or advisable including due to the inability to transport gold or the lack of liquidity in the market. The delivery of gold in exchange for shares shall be suspended in the event Gold Corporation resigns as the Custodial Sponsor or if Gold Corporation is otherwise unable or unwilling to accept applications from investors to take delivery of gold.

5. CONCENTRATION OF RISK

The Trust’s sole business activity is the investment in gold bullion. Several factors could affect the price of gold: (i) global gold supply and demand, which is influenced by such factors as forward selling by gold producers, purchases made by gold producers to unwind gold hedge positions, central bank purchases and sales, and production and cost levels in major gold-producing countries, and new production projects; (ii) investors’ expectations regarding future inflation rates; (iii) currency exchange rate volatility; (iv) interest rate volatility; and (v) political, economic, global or regional incidents. In addition, there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price of gold declines, the Sponsors expect the value of an investment in the shares to decline proportionately. Each of these events could have a material effect on the Trust’s financial position and results of operations.

11

6. INDEMNIFICATION

The Trust Agreement provides that the Trustee, its directors, officers, employees, shareholders, agents and affiliates (as defined under the Securities Act of 1933, as amended) shall be indemnified from the Trust and held harmless against any loss, liability or expense (including the reasonable fees and expenses of counsel) arising out of or in connection with the performance of its obligations under the Trust Agreement and under each other agreement entered into by the Trustee in furtherance of the administration of the Trust (including the Custody Agreement and any Authorized Participant Agreement, including the Trustee’s indemnification obligations under these agreements), or otherwise by reason of the Trustee’s acceptance or administration of the Trust to the extent such loss, liability or expense was incurred without (i) gross negligence, bad faith, willful misconduct or willful malfeasance on the part of such indemnified party in connection with the performance of its obligations under the Trust Agreement or any such other agreement, or any actions taken in accordance with the provisions of this Agreement or any such other agreement, or (ii) reckless disregard on the part of such indemnified party of its obligations and duties under the Trust Agreement or any such other agreement. Each indemnified party shall be indemnified from the Trust and held harmless against any loss, liability or expense (including the reasonable fees and expenses of counsel) arising out of or in connection with any services Gold Corporation may, directly or indirectly, separately offer or provide to any beneficial owner. Such indemnities shall include payment from the Trust of the reasonable costs and expenses incurred by such indemnified party in investigating or defending itself against any such loss, liability or expense or any claim therefor, provided that such indemnified party shall repay to the Trust the amount of any such reasonable costs and expenses paid by the Trust to the extent it may be ultimately determined that such indemnified party was not entitled to be indemnified under the Trust Agreement because clause (i) or clause (ii) of the sentence preceding the prior sentence applied. Any amounts payable to an indemnified party may be payable in advance or shall be secured by a lien on the Trust’s assets.

Each Sponsor and its members, managers, directors, officers, employees, agents and affiliates shall be indemnified from the Trust and held harmless against any loss, liability or expense (including the reasonable fees and expenses of counsel) arising out of or in connection with the performance of its obligations under the Trust Agreement and under each other agreement entered into by such Sponsor in furtherance of the administration of the Trust (including Authorized Participant Agreements to which the Administrative Sponsor is a party, including the Administrative Sponsor’s indemnification obligations thereunder) or any actions taken in accordance with the provisions of the Trust Agreement, to the extent such loss, liability or expense was incurred without (i) gross negligence, bad faith, willful misconduct or willful malfeasance on the part of such indemnified party in connection with the performance of its obligations under the Trust Agreement or any such other agreement or any actions taken in accordance with the provisions of the Trust Agreement, or any such other agreement or (ii) reckless disregard on the part of such indemnified party of its obligations and duties under the Trust Agreement, or any such other agreement. Each Sponsor (in the case of the Custodial Sponsor, in its capacity as Custodial Sponsor) and its members, managers, directors, officers, employees, agents and affiliates shall be indemnified from the Trust and held harmless against any loss, liability or expense (including the reasonable fees and expenses of counsel) arising out of or in connection with any services Gold Corporation may, directly or indirectly, separately offer or provide to any beneficial owner. Such indemnities shall include payment from the Trust of the reasonable costs and expenses incurred by such indemnified party in investigating or defending itself against any such loss, liability or expense or any claim therefor, provided that such indemnified party shall repay to the Trust the amount of any such reasonable costs and expenses paid by the Trust to the extent it may be ultimately determined that such indemnified party was not entitled to be indemnified under the Trust Agreement because clause (i) or clause (ii) of this paragraph applied. Any amounts payable to an indemnified party may be payable in advance or shall be secured by a lien on the Trust's assets.

In addition, the Trustee or a Sponsor may, in its sole discretion, undertake any action that it may deem necessary or desirable in respect of the Trust Agreement and in such event, the reasonable legal expenses and costs and other disbursements of any such actions shall be expenses and costs of the Trust and the Trustee or such Sponsor, as the case may be, shall be entitled to reimbursement by the Trust. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred.

12

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

This information should be read in conjunction with the financial statements and notes included in Item 1 of Part I of the Trust’s Quarterly Report on Form 10-Q for the quarterly period ended September 30, 2020 (this “Form 10-Q”). This Form 10-Q contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and such forward-looking statements involve risks and uncertainties. All statements (other than statements of historical fact) included in this Form 10-Q that address activities, events or developments that may occur in the future, including such matters as future gold prices, gold sales, costs, objectives, changes in commodity prices and market conditions (for gold and the shares), the Trust’s operations (including the effects thereon related to the coronavirus (“COVID-19”) pandemic), the Sponsors’ plans and references to the Trust’s future success and other similar matters are forward-looking statements. Words such as “could,” “would,” “may,” “expect,” “intend,” “estimate,” “predict,” and variations on such words or negatives thereof, and similar expressions that reflect our current views with respect to future events and Trust performance, are intended to identify such forward-looking statements. These forward-looking statements are only predictions, subject to risks and uncertainties that are difficult to predict and many of which are outside of our control, and actual results could differ materially from those discussed. Forward-looking statements involve risks and uncertainties that could cause actual results or outcomes to differ materially from those expressed therein. We express our estimates, expectations, beliefs, and projections in good faith and believe them to have a reasonable basis. However, we make no assurances that management’s estimates, expectations, beliefs, or projections will be achieved or accomplished. These forward-looking statements are based on assumptions about many important factors that could cause actual results to differ materially from those in the forward-looking statements. Such factors are discussed in: Part I, Item 1A. Risk Factors of the Trust’s Annual Report on Form 10-K for the year ended December 31, 2019 (the “2019 Form 10-K”); Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of the 2019 Form 10-K; Part I, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Form 10-Q; Part II, Item 1A. Risk Factors of this Form 10-Q, and other parts of this Form 10-Q. We do not intend to update any forward-looking statements even if new information becomes available or other events occur in the future, except as required by the federal securities laws.

Organization and Trust Overview

Perth Mint Physical Gold ETF (the “Trust”) was formed pursuant to the Depository Trust Agreement (the “Trust Agreement”) on July 26, 2018 under New York State law. The Trust issues Perth Mint Physical Gold ETF Shares (the “shares”), which represent units of fractional undivided beneficial interest in the Trust. The Trust’s primary objective is to provide investors with an opportunity to invest in gold through the shares the Trust issues and have the gold securely stored by Gold Corporation (the “Custodial Sponsor”). An additional objective of the Trust is for the shares to reflect the performance of the price of gold less the expenses of the Trust’s operations. The Trust is not actively managed. The Custodial Sponsor and Exchange Traded Concepts, LLC (the “Administrative Sponsor” and, together with the Custodial Sponsor, the “Sponsors”) are the Trust’s sponsors. Gold Corporation also serves as the custodian of the Trust’s gold bullion. References to the “Custodian” throughout this Form 10-Q refer to Gold Corporation in its capacity as Custodian of the Trust’s gold bullion instead of its capacity as Custodial Sponsor. The Bank of New York Mellon is the trustee of the Trust (the “Trustee”).

Gold Corporation, trading as the Perth Mint, is a Western Australian Government-owned statutory body corporate established under the Gold Corporation Act 1987 (Western Australia) (the “Gold Corporation Act”). Under Section 22 of the Gold Corporation Act, the payment of the cash equivalent of gold due, payable and deliverable by the Custodial Sponsor (including gold held by the Custodial Sponsor for the benefit of the Trust) is guaranteed by the Treasurer of Western Australia, in the name and on behalf of the Crown in right of the State of Western Australia (the “Government Guarantee”). The Government Guarantee is subject to the claims-paying ability of the Government of Western Australia.

Physical gold that the Trust holds includes London Bars (as defined in the Trust Agreement) and other gold products having a gold purity of at least 99.5% (including but not limited to coins, cast bars and minted bars). The Custodial Sponsor’s policy is to hold 100% of the gold held on behalf of the Trust in physical gold. The Trust issues shares in blocks of at least 25,000 shares called “Baskets” in exchange for gold from certain registered broker-dealers or other securities market participants (the “Authorized Participants”), which is then allocated as physical gold and safely stored by the Custodian. When the Trust was launched, a Basket was the equivalent of 50,000 shares. On June 1, 2019, the Trust revised the definition of a Basket pursuant to the Depository Trust Agreement to consist of at least 25,000 shares. The Trust issues and redeems Baskets on an ongoing basis at net asset value (“NAV” or “Net Asset Value”) to and from Authorized Participants who have entered into a contract with the Administrative Sponsor and the Trustee. Investors may request to take delivery of physical gold in exchange for their shares, at their option, by submitting their shares to the Custodial Sponsor in exchange for physical gold.

The Trust’s only ordinary recurring fee is the fee paid to the Custodial Sponsor, which accrues daily at an annualized rate equal to 0.18% of the daily NAV of the Trust, payable in gold monthly in arrears (the “Custodial Sponsor Fee”). In exchange for the Custodial Sponsor Fee, the Custodial Sponsor has agreed to assume and be responsible for the payment of most of the expenses incurred by the Trust, up to a maximum amount equal to the greater of $500,000 per annum and the amount that is equal to 0.15% of the average total value of the gold held by the Trust, as determined by the Trustee on each business day, plus the value of all other assets of the Trust (other than any amount credited to the Trust’s reserve account), including cash, if any.

The Trust’s shares trade on the NYSE Arca Marketplace (the “NYSE Arca”) under the symbol “AAAU.” The market price of the shares may be different from the NAV per share.

13

Goldman Sachs Transaction

On September 29, 2020, the Sponsors entered into an agreement to transfer their respective roles to Goldman Sachs Asset Management, L.P. (the “Goldman Sachs Transaction”). Upon closing of the Goldman Sachs Transaction, Goldman Sachs Asset Management, L.P. will serve as the new sponsor of the Trust, which will combine the roles of the Custodial Sponsor and the Administrative Sponsor.

At the closing of the Goldman Sachs Transaction, Gold Corporation will resign as the Custodian of the Trust’s gold bullion (in its role as Custodian of the Trust) and a new third-party custodian will be appointed, at which point the payment of the cash equivalent of gold due, payable and deliverable on behalf of the Trust will no longer be guaranteed under the Government Guarantee. It is also expected that, immediately after the closing of the Goldman Sachs Transaction, investors will no longer be able to take delivery of the physical gold bullion in exchange for the shares such investors own. It is also anticipated that the Trust will be renamed at the closing of the Goldman Sachs Transaction to Goldman Sachs Physical Gold ETF.

Valuation of Gold and Computation of Net Asset Value

The Trustee determines the NAV of the Trust on each day that the NYSE Arca is open for regular trading, as promptly as practical after 4:00 p.m. New York time. The NAV of the Trust is the aggregate value of gold and other assets, if any, of the Trust (other than any amounts credited to the Trust’s reserve account, if any) and cash, if any, less liabilities of the Trust, which include estimated accrued but unpaid fees, expenses and other liabilities. In determining the Trust’s NAV, the Trustee values the gold held by the Trust based on the afternoon London gold price per troy ounce of gold for delivery in London through a member of the London Bullion Market Association (“LBMA”) authorized to effect such delivery, as calculated and administered by independent service provider(s) and published by the LBMA on its website or by its successor that publicly displays prices (the “LBMA PM Gold Price”), or, if such day’s afternoon price is not available, the morning LBMA Gold Price (the “LBMA AM Gold Price”). If no LBMA Gold Price is available for the day, the Trustee will value the Trust’s gold based on the most recently announced LBMA PM Gold Price or LBMA AM Gold Price. If the Custodial Sponsor determines that such price is inappropriate to use, it shall identify an alternate basis for evaluation to be employed by the Trustee. The Custodial Sponsor may instruct the Trustee to use a different publicly available price, which the Custodial Sponsor determines to fairly represent the commercial value of the Trust’s gold.

Results of Operations

Three and Nine Months Ended September 30, 2020 and 2019

For the three months ended September 30, 2020, 5,800,000 shares (232 Baskets) were created in exchange for 65,518.2 ounces of gold, and 99.7 ounces of gold were sold to pay expenses. For the nine months ended September 30, 2020, 15,225,000 shares (609 Baskets) were created in exchange for 151,754.8 ounces of gold, and 219.6 ounces of gold were sold to pay expenses. The Trust’s NAV per share ended the period at $18.80 compared to $17.62 at June 30, 2020 and $15.19 at December 31, 2019. The increase in NAV per share was due to a higher price of gold of $1,886.90 at period end, which represented an increase of 6.72% from $1,768.10 at June 30, 2020 and an increase of 23.89% from $1,523.00 at December 31, 2019.

For the three months ended September 30, 2019, 1,650,000 shares (66 Baskets) were created in exchange for 16,470 ounces of gold, and 43.4 ounces of gold were sold to pay expenses. For the nine months ended September 30, 2019, 4,150,000 shares (166 Baskets) were created in exchange for 41,441 ounces of gold, and 112.8 ounces of gold were sold to pay expenses. The Trust’s NAV per share ended the period at $14.82, compared to $14.07 at June 30, 2019 and $12.81 at December 31, 2018. The increase in NAV per share was due to a higher price of gold of $1,485.30 at period end, which represented an increase of 5.42% from $1,409.00 at June 30, 2019, and 15.89% from $1,281.65 at December 31, 2018.

At September 30, 2020, the Custodial Sponsor held 258,295.7 ounces of gold on behalf of the Trust in its vault, with a market value of $487,378,111 (cost: $402,056,316) based on the LBMA PM Gold Price at period end.

At September 30, 2019, the Custodial Sponsor held 110,790.5 ounces of gold on behalf of the Trust in its vault, with a market value of $164,557,189 (cost: $141,430,618) based on the LBMA PM Gold Price at period end.

The change in net assets from operations for the three months ended September 30, 2020 was $22,793,340, which was due to (i) the Custodial Sponsor Fee of $(212,831) and (ii) a net realized and unrealized gain of $23,006,171 from operations, which in turn resulted from a net realized loss on gold transferred to pay expenses of $(786) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $24,031,732. Other than the Custodial Sponsor Fee, the Trust had no expenses during the three months ended September 30, 2020.

14

The change in net assets from operations for the three months ended September 30, 2019 was $6,980,329, which was due to (i) the Custodial Sponsor Fee of $(68,564) and (ii) a net realized and unrealized gain of $7,048,893 from operations, which in turn resulted from a net realized loss on gold transferred to pay expenses of $(108) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $7,049,001. Other than the Custodial Sponsor Fee, the Trust had no expenses during the three months ended September 30, 2019.

The change in net assets from operations for the nine months ended September 30, 2020 was $57,254,507, which was due to (i) the Custodial Sponsor Fee of $(432,632) and (ii) a net realized and unrealized gain of $57,687,139 from operations, which in turn resulted from a net realized gain on gold distributed for redemptions of $105,511, a net realized loss on gold transferred to pay expenses of $(2,478) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $57,795,128. Other than the Custodial Sponsor Fee, the Trust had no expenses during the nine months ended September 30, 2020.

The change in net assets from operations for the nine months ended September 30, 2019 was $18,038,196, which was due to (i) the Custodial Sponsor Fee of $(164,694) and (ii) a net realized and unrealized gain of $18,202,890 from operations, which in turn resulted from a net realized gain on gold transferred to pay expenses of $831 and a net change in unrealized appreciation/depreciation on investments in gold bullion of $18,202,059. Other than the Custodial Sponsor Fee, the Trust had no expenses during the nine months ended September 30, 2019.

Liquidity and Capital Resources

The Trust is not aware of any trends, demands, commitments, events or uncertainties that are reasonably likely to result in material changes to its liquidity needs. The Trust’s only ordinary recurring fee is the Custodial Sponsor Fee, which accrues daily at an annualized rate equal to 0.18% of the daily NAV of the Trust, and is payable in gold monthly in arrears. The Custodial Sponsor Fee was the only ordinary expense of the Trust during the period covered by this Form 10-Q.

The Trustee will, when directed by the Custodial Sponsor, and, in the absence of such direction may, in its discretion, sell gold in such quantity and at such times as may be necessary to permit payment in cash of the Trust’s extraordinary expenses not assumed by the Custodial Sponsor. At September 30, 2020 and 2019, the Trust did not have any cash balances.

Off-Balance Sheet Arrangement

As of September 30, 2020, the Trust did not have any off-balance sheet arrangements.

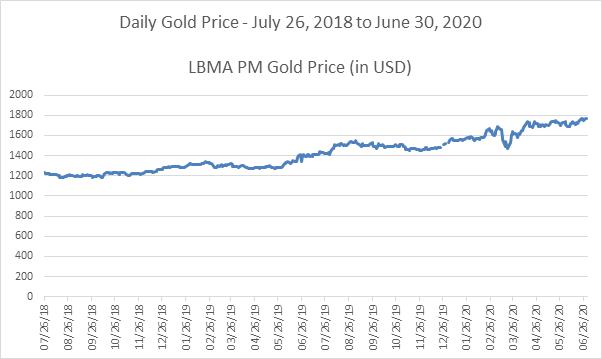

Analysis of Movements in the Price of Gold

As movements in the price of gold are expected to directly affect the price of the Trust’s shares, it is important for investors to understand and follow movements in the price of gold. Past movements in the gold price are not indicators of future movements.

The following chart shows movements in the price of gold based on the LBMA PM Gold Price in U.S. dollars per ounce over the period from July 26, 2018 (the first date the Trust’s shares began trading on the NYSE Arca) to September 30, 2020.

15

The average, high, low and end-of-period gold prices for the period from October 1, 2019 through September 30, 2020, based on the LBMA PM Gold Price were:

| Period | Average | High | Date | Low | Date | End of period | Last business day(1) | |||||||||||||||||||

| October 1, 2019 to December 31, 2019 | $ | 1,480.96 | $ | 1,517.10 | Oct. 3, 2019 | $ | 1,452.05 | Nov. 12, 2019 | $ | 1,514.75 | Dec. 30, 2019(2) | |||||||||||||||

| January 1, 2020 to March 31, 2020 | $ | 1,582.80 | $ | 1,683.65 | Mar. 6, 2020 | $ | 1,474.25 | Mar. 19, 2020 | $ | 1,608.95 | Mar. 31, 2020 | |||||||||||||||

| April 1, 2020 to June 30, 2020 | $ | 1,711.13 | $ | 1,771.60 | June 29, 2020 | $ | 1,576.55 | Apr. 1, 2020 | $ | 1,768.10 | June 30, 2020 | |||||||||||||||

| July 1, 2020 to September 30, 2020 | $ | 1,908.56 | $ | 2,067.15 | Aug. 6, 2020 | $ | 1,771.05 | July 1, 2020 | $ | 1,886.90 | Sept. 30, 2020 | |||||||||||||||

| (1) | The end of period gold price is the LBMA PM Gold Price on the last business day of the period. This is in accordance with the Trust Agreement and the basis used for calculating the NAV of the Trust. |

| (2) | The last business day of the period was December 31, 2019; however, no LBMA PM Gold Price was recorded. Last LBMA PM Gold Price for the period was recorded on December 30, 2019. |

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

The Trust is a passive investment vehicle. It is not actively managed. The Trust’s primary objective is to provide investors with an opportunity to invest in gold through the shares the Trust issues and have the gold securely stored by the Custodial Sponsor. Accordingly, fluctuations in the price of gold will affect the value of the Trust’s shares.

Item 4. Controls and Procedures.

Disclosure Controls and Procedures

The duly authorized officers of the Administrative Sponsor, performing functions equivalent to those a principal executive officer and principal financial officer of the Trust would perform if the Trust had any officers, have evaluated the effectiveness of the Trust’s disclosure controls and procedures, and have concluded that the disclosure controls and procedures of the Trust were effective as of the end of the period covered by this report. Such disclosure controls and procedures are designed to provide reasonable assurance that information required to be disclosed in the reports that the Trust files or submits under the Securities Exchange Act of 1934, as amended, are recorded, processed, summarized and reported, within the time period specified in the applicable rules and forms, and that such information is accumulated and communicated to the duly authorized officers of the Administrative Sponsor performing functions equivalent to those a principal executive officer and principal financial officer of the Trust would perform if the Trust had any officers, and to the Audit Committee of the Administrative Sponsor, as appropriate, to allow timely decisions regarding required disclosure.

Internal Control over Financial Reporting

There has been no change in the internal control over financial reporting that occurred during the three months ended September 30, 2020 that has materially affected, or is reasonably likely to materially affect, the Trust’s internal control over financial reporting.

16

Part II. OTHER INFORMATION.

Item 1. Legal Proceedings.

The Trust is not aware of any existing or pending legal proceedings against it, nor is it involved as a plaintiff in any proceeding or pending litigation.

Item 1A. Risk Factors.

The operations of the Trust are subject to numerous risks and uncertainties. As a result, the risks and uncertainties discussed in Part I, Item 1A. Risk Factors in the Trust’s 2019 Form 10-K should be carefully considered. There have been no material changes in the assessment of the Trust’s risk factors from those set forth in the Trust’s 2019 Form 10-K, except as stated below.

The effects of a global public health crisis, including the ongoing COVID-19 pandemic, could adversely affect the Sponsors and their service providers, as well as the value of our shares and the price of gold.

Pandemics and other global public health crises may cause a curtailment of business activities that may potentially affect the ability of the Sponsors and their service providers to operate. The COVID-19 pandemic or a similar public health threat could adversely affect the Trust by causing operating delays and disruptions, market disruption and shutdowns (including as a result of government regulation and prevention measures). For instance, the suspension of operations of mines, refineries and vaults that extract, produce or store gold, restrictions on travel that delay or prevent the transportation of gold, and an increase in demand for gold may disrupt supply chains for gold, which could cause secondary market spreads to widen and compromise our ability to settle transactions on time. Any inability of the Trust to issue or redeem our shares or the Custodian or any sub-custodian to receive or deliver gold as a result of the outbreak will negatively affect the Trust’s operations. In addition, market disruptions and other volatility related to global public health crises can significantly affect the price of gold and, consequently, the value of our shares.

The duration of the COVID-19 outbreak and its effects cannot be determined with certainty. A prolonged outbreak could result in an increase of the costs of the Trust, affect liquidity in the market for gold as well as the correlation between the price of our shares and the net asset value of the Trust, any of which could adversely affect the value of our shares. In addition, the outbreak could also impair the information technology and other operational systems upon which the Trust’s service providers, including the Sponsors, the Trustee and the Custodian, rely, and could otherwise disrupt the ability of employees of the Trust’s service providers to perform essential tasks on behalf of the Trust. Governmental and quasi-governmental authorities and regulators throughout the world have in the past responded to major economic disruptions with a variety of fiscal and monetary policy changes, including, but not limited to, direct capital infusions into companies, new monetary programs and lower interest rates. An unexpected or quick reversal of these policies, or the ineffectiveness of these policies, is likely to increase volatility in the market for gold, which could adversely affect the price of our shares.

Further, the outbreak could interfere with or prevent the operation of the electronic auction hosted by IBA to determine the LBMA Gold Price, which the Trustee uses to value the gold held by the Trust and calculate the Net Asset Value of the Trust. The outbreak could also cause the closure of futures exchanges, which could eliminate the ability of Authorized Participants to hedge purchases of Baskets, increasing trading costs of our shares and resulting in a sustained premium or discount in our shares. Each of these outcomes would negatively impact the Trust.

If the Goldman Sachs Transaction is completed, the Trust will no longer have the protections of the Government Guarantee, which would affect the Trust’s ability to satisfy a claim.

At the closing of the Goldman Sachs Transaction, Gold Corporation will resign as the Custodian of the Trust’s gold bullion (in its role as Custodian of the Trust) and a new third-party custodian will be appointed, at which point the payment of the cash equivalent of gold due, payable and deliverable on behalf of the Trust will no longer be subject to the Government Guarantee. As such, the Trust would not be able to file a claim to recover any loss from the government of Western Australia from any failure by the Trust’s new custodian to exercise in due care in the safekeeping of the Trust’s gold, which would affect the Trust’s ability to satisfy a claim.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

a) None.

b) Not applicable.

c) The Trust does not purchase shares directly from its shareholders. In connection with its redemption of Baskets held by Authorized Participants, the Trust redeemed 24 Baskets (comprising 600,000 shares) during the three months ended September 30, 2020. The following table summarizes the redemptions by Authorized Participants during the period:

| Period | Total Number of Shares Redeemed | Average Price Per Share | ||||||

| 7/1/20 to 7/31/20 | - | $ | - | |||||

| 8/1/20 to 8/31/20 | - | $ | - | |||||

| 9/1/20 to 9/30/20 | 600,000 | $ | 18.53 | |||||

| Total | 600,000 | |||||||

17

Item 3. Defaults Upon Senior Securities.

None.

Item 4. Mine Safety Disclosures.

None.

Item 5. Other Information.

None.

Item 6. Exhibits.

See the Exhibit Index below, which is incorporated by reference herein.

EXHIBIT INDEX

18

Signatures

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned in the capacities* indicated thereunto duly authorized.

EXCHANGE TRADED CONCEPTS, LLC

Administrative Sponsor of Perth Mint Physical Gold ETF

| By: | /s/ J. Garrett Stevens* | |

| J. Garrett Stevens Chief Executive Officer (Principal Executive Officer) |

Date: November 6, 2020

* The registrant is a trust and the person is signing in his capacity as an officer of Exchange Traded Concepts, LLC, the Administrative Sponsor of the Registrant.

19