Table of Contents

Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the quarterly period ended |

Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

| Large Accelerated Filer | ☐ | Accelerated Filer | ☐ | |||

Non-Accelerated Filer |

☒ | Smaller Reporting Company | ||||

| Emerging Growth Company | ||||||

Table of Contents

Goldman Sachs Physical Gold ETF

Table of Contents

Table of Contents

Part I. FINANCIAL INFORMATION.

Item 1. Unaudited Financial Statements.

Goldman Sachs Physical Gold ETF

Index to Unaudited Financial Statements

| Documents |

Page | |||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

| 7 | ||||

1

Table of Contents

September 30, 2022 (unaudited) |

December 31, 2021 |

|||||||

Assets |

||||||||

Investment in gold, at fair value (cost $ |

$ | $ | ||||||

Total assets |

||||||||

Liabilities |

||||||||

Sponsor fee payable |

||||||||

Total liabilities |

||||||||

Net Assets |

$ | $ | ||||||

Shares issued and outstanding ( number of shares authorized, |

||||||||

Net asset value per Share |

$ | $ | ||||||

Ounces |

Cost |

Fair Value |

% of Net Assets |

|||||||||||||

Investment in gold, at fair value |

$ | $ | % | |||||||||||||

Total Investments |

$ | $ | % | |||||||||||||

Liabilities in excess of other assets |

( |

) | ( |

)% | ||||||||||||

Net Assets |

$ | % | ||||||||||||||

Ounces |

Cost |

Fair Value |

% of Net Assets |

|||||||||||||

Investment in gold, at fair value |

$ | $ | % | |||||||||||||

Total Investments |

$ | $ | % | |||||||||||||

Liabilities in excess of other assets |

( |

) | ( |

)% | ||||||||||||

Net Assets |

$ | % | ||||||||||||||

Three Months Ended September 30, 2022 (unaudited) |

Three Months Ended September 30, 2021 (unaudited) |

Nine Months Ended September 30, 2022 (unaudited) |

Nine Months Ended September 30, 2021 (unaudited) |

|||||||||||||

| Expenses |

||||||||||||||||

| Sponsor fee |

$ | ( |

) | $ | ( |

) | $ | ( |

) | $ | ( |

) | ||||

| |

|

|

|

|

|

|

|

|||||||||

| Total expenses |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net investment (loss) |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net realized and unrealized gain (loss) |

||||||||||||||||

| Net realized gain (loss) on gold bullion distributed for redemptions |

( |

) | ||||||||||||||

| Net realized gain (loss) on gold transferred to pay expenses |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net realized gain (loss) |

( |

) | ( |

) | ||||||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net change in unrealized appreciation (depreciation) on investment in gold |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net realized and unrealized gain (loss) from operations |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

| |

|

|

|

|

|

|

|

|||||||||

| Net Income (Loss) |

$ | ( |

) | $ | ( |

) | $ | ( |

) | $ | ( |

) | ||||

| |

|

|

|

|

|

|

|

|||||||||

| Net income (loss) per share |

$ | ( |

) | $ | ( |

) | $ | ( |

) | $ | ( |

) | ||||

| |

|

|

|

|

|

|

|

|||||||||

| Average number of shares |

||||||||||||||||

| |

|

|

|

|

|

|

|

|||||||||

Three Months Ended September 30, 2022 (unaudited) |

Three Months Ended September 30, 2021 (unaudited) |

Nine Months Ended September 30, 2022 (unaudited) |

Nine Months Ended September 30, 2021 (unaudited) |

|||||||||||||

Net Assets, beginning of period |

$ | $ | $ | $ | ||||||||||||

Creations |

||||||||||||||||

Redemptions |

( |

) | ( |

) | ( |

) | ||||||||||

Net creations (redemptions) |

( |

) | ( |

) | ||||||||||||

Net investment loss |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

Net realized gain (loss) |

( |

) | ( |

) | ||||||||||||

Net change in unrealized appreciation (depreciation) on investments in gold |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

Net Assets, end of period |

$ | $ | $ | $ | ||||||||||||

Three Months Ended September 30, 2022 (unaudited) |

Three Months Ended September 30, 2021 (unaudited) |

Nine Months Ended September 30, 2022 (unaudited) |

Nine Months Ended September 30, 2021 (unaudited) |

|||||||||||||

Per Share Performance (for a share outstanding throughout each period) |

||||||||||||||||

Net asset value per share, beginning of period |

$ | $ | $ | $ | ||||||||||||

Net investment loss (a) |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

Net realized and unrealized gain (loss) on investment in gold |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

Change in net assets from operations |

( |

) | ( |

) | ( |

) | ( |

) | ||||||||

Net asset value per share, end of period |

$ | $ | $ | $ | ||||||||||||

Market value per share, beginning of period |

$ | $ | $ | $ | ||||||||||||

Market value per share, end of period |

$ | $ | $ | $ | ||||||||||||

Total Return, at net asset value (b) |

( |

)% | ( |

)% | ( |

)% | ( |

)% | ||||||||

Total Return, at market value (b) |

( |

)% | ( |

)% | ( |

)% | ( |

)% | ||||||||

Net assets ($000’s) |

$ | $ | $ | $ | ||||||||||||

Ratios to average net assets (c) |

||||||||||||||||

Net investment loss |

( |

)% | ( |

)% | ( |

)% | ( |

)% | ||||||||

Total expenses |

( |

)% | ( |

)% | ( |

)% | ( |

)% | ||||||||

| (a) | Calculated using average shares outstanding. |

| (b) | Total Return, at net asset value (“NAV”) is calculated assuming an initial investment made at the NAV at the beginning of the period, reinvestment of any dividends and distributions at NAV during the period, and redemption of Shares on the last day of the period. Total Return, at NAV includes adjustments in accordance with U.S. GAAP and as such, the NAV for financial reporting purposes and the returns based upon those NAVs may differ from the NAVs and returns for shareholder transactions. Total Return, at market value is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all dividends and distributions at market value during the period and redemption of Shares at the market value on the last day of the period. Total returns for periods less than one full year are not annualized. |

| (c) | Annualized. |

Three Months Ended |

||||||||

September 30, 2022 |

September 30, 2021 |

|||||||

| Beginning Share Balance |

||||||||

| Creations (representing |

||||||||

| Redemptions (representing |

( |

) | ||||||

| |

|

|

|

|||||

| Ending Share Balance |

||||||||

Nine Months Ended |

||||||||

September 30, 2022 |

September 30, 2021 |

|||||||

| Beginning Share Balance |

||||||||

| Creations (representing |

||||||||

| Redemptions (representing |

( |

) | ( |

) | ||||

| |

|

|

|

|||||

| Ending Share Balance |

||||||||

Amount in ounces |

Amount in US$ |

|||||||

| Balance at June 30, 2022 |

$ | |||||||

| Creations |

||||||||

| Redemptions |

( |

) | ( |

) | ||||

| Net realized gain (loss) from gold bullion distributed for redemptions |

( |

) | ||||||

| Transfer of gold to pay expenses |

( |

) | ( |

) | ||||

| Net realized gain (loss) from gold transferred to pay expenses |

( |

) | ||||||

| Change in unrealized appreciation (depreciation) on investment in gold |

( |

) | ||||||

| |

|

|

|

|||||

| Balance at September 30, 2022 |

$ | |||||||

Amount in ounces |

Amount in US$ |

|||||||

| Balance at December 31, 2021 |

$ | |||||||

| Creations |

||||||||

| Redemptions |

( |

) | ( |

) | ||||

| Net realized gain (loss) from gold bullion distributed for redemptions |

||||||||

| Transfer of gold to pay expenses |

( |

) | ( |

) | ||||

| Net realized gain (loss) from gold transferred to pay expenses |

( |

) | ||||||

| Change in unrealized appreciation (depreciation) on investment in gold |

( |

) | ||||||

| |

|

|

|

|||||

| Balance at September 30, 2022 |

$ | |||||||

Table of Contents

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

This information should be read in conjunction with the financial statements and notes included in Item 1 of Part I of this Form 10-Q. This Form 10-Q contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and such forward-looking statements involve risks and uncertainties. All statements (other than statements of historical fact) included in this Form 10-Q that address activities, events or developments that may occur in the future, including such matters as future gold prices, gold sales, costs, objectives, changes in commodity prices and market conditions (for gold and the shares), the Trust’s operations, the Sponsors’ plans and references to the Trust’s future success and other similar matters are forward-looking statements. Words such as “could,” “would,” “may,” “expect,” “intend,” “estimate,” “predict,” and variations on such words or negatives thereof, and similar expressions that reflect our current views with respect to future events and Trust performance, are intended to identify such forward-looking statements. These forward-looking statements are only predictions, subject to risks and uncertainties that are difficult to predict and many of which are outside of our control, and actual results could differ materially from those discussed. Forward-looking statements involve risks and uncertainties that could cause actual results or outcomes to differ materially from those expressed therein. We express our estimates, expectations, beliefs, and projections in good faith and believe them to have a reasonable basis. However, we make no assurances that management’s estimates, expectations, beliefs, or projections will be achieved or accomplished. These forward-looking statements are based on assumptions about many important factors that could cause actual results to differ materially from those in the forward-looking statements. Such factors are discussed in: Part I, Item 1A. Risk Factors of the Trust’s Annual Report on Form 10-K for the year ended December 31, 2021 (“2021 Form 10-K”); Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of the 2021 Form 10-K; Part I, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Form 10-Q, and other parts of this Form 10-Q. We do not intend to update any forward-looking statements even if new information becomes available or other events occur in the future, except as required by the federal securities laws.

Organization and Trust Overview

Goldman Sachs Physical Gold ETF (the “Trust”) is organized as a New York trust. The Trust is governed by the provisions of the First Amended and Restated Depositary Trust Agreement (as amended from time to time, the “Trust Agreement”) executed after the close of business on December 11, 2020 by Goldman Sachs Asset Management, L.P. (the “Sponsor”) and The Bank of New York Mellon (the “Trustee”). The Trust issues Goldman Sachs Physical Gold ETF Shares (the “Shares”), which represent units of fractional undivided beneficial interest in the Trust. The Trust commenced operations on July 26, 2018.

The Sponsor of the Trust is Goldman Sachs Asset Management, L.P., a Delaware limited partnership. Goldman Sachs Asset Management, L.P. is an indirect, wholly-owned subsidiary of The Goldman Sachs Group, Inc. (“GS Group Inc.”) and an affiliate of Goldman Sachs & Co. LLC.

The Trustee is generally responsible for the day-to-day administration of the Trust, including keeping the Trust’s operational records. JPMorgan Chase Bank, N.A., London branch (the “Custodian”) serves as the Custodian for the Trust’s gold bullion. The Custodian is responsible for holding the Trust’s gold, as well as receiving and converting allocated and unallocated gold on behalf of the Trust.

Physical gold that the Trust holds consists of gold bullion that meets the specifications for “good delivery” gold bars (“London Good Delivery Standards”), including the specifications for weight, dimension, fineness (or purity), identifying marks and appearance of gold bars, set forth in the good delivery rules promulgated by the London Bullion Market Association (“LBMA”). The Trust issues the Shares in blocks of at least 25,000 shares called “Baskets” in exchange for gold from certain registered broker-dealers or other securities market participants (the “Authorized Participants”), which is then allocated as physical gold and stored by the Custodian. The Trust issues and redeems Baskets on an ongoing basis at net asset value (“NAV” or “Net Asset Value”) to and from Authorized Participants who have entered into a contract with the Sponsor and the Trustee. As of September 30, 2022, each of Virtu Americas LLC and Goldman Sachs & Co. LLC has signed an Authorized Participant Agreement with the Sponsor and the Trustee, and may create and redeem Baskets.

The Trust’s investment objective is for the Shares to reflect the performance of the price of gold less the expenses of the Trust’s operations. The Trust is not actively-managed. The Shares trade on the Cboe BZX Exchange, Inc. (“Cboe BZX Exchange”) under the symbol “AAAU.” Effective February 3, 2022, the listing of the Trust was transferred from NYSE Arca to Cboe BZX Exchange.

The Trust’s fiscal year-end is December 31.

Valuation of Gold and Computation of Net Asset Value

On each business day that the Cboe BZX Exchange is open for regular trading, as promptly as practicable after 4:00 p.m. New York City time, the Trustee values the gold held by the Trust and determines the Net Asset Value of the Trust, as described below.

12

Table of Contents

The Net Asset Value of the Trust is the aggregate value of gold and other assets, if any, of the Trust (other than amounts credited to the Trust’s reserve account, if any) including cash, if any, less liabilities of the Trust, which include estimated accrued but unpaid fees, expenses and other liabilities. The reserve account, if established, will be a separate non-interest bearing account with the Trustee or such other banking institution specified by the Sponsor, or if the Sponsor fails so to specify, as selected by the Trustee, in the name, and for the benefit, of the Trust, subject only to draft or order by the Trustee acting pursuant to the terms of the Trust Agreement. The Trustee will hold in such account all cash that it has credited to such account to reflect the reserves for taxes or other governmental charges and other contingent liabilities payable out of the Trust that the Trustee has determined from time to time to be required by GAAP. The Trustee determines the Net Asset Value per Share by dividing the Net Asset Value of the Trust by the number of the Shares outstanding as of the close of trading on the Cboe BZX Exchange (which includes the net number of any Shares deemed created or redeemed on such evaluation day).

All gold is valued based on its fine troy ounce (“Fine Ounce”) content, calculated by multiplying the weight of gold by its purity. The same methodology is applied independent of the type of gold held by the Trust; similarly, the value of up to 430 Fine Ounces of unallocated gold the Trust may hold is calculated by multiplying the number of Fine Ounces with the price of gold determined by the Trustee. The Trustee values the gold held by the Trust based on the LBMA Gold Price PM. The LBMA Gold Price PM is set at 3:00 p.m. London time via an auction independently operated and administered by ICE Benchmark Administration (“IBA”). The price is set in U.S. dollars per Fine Ounce. If no LBMA Gold Price PM is available for the required day, the Trustee uses the LBMA Gold Price AM. If no LBMA Gold Price PM or LBMA Gold Price AM is available for the day, the Trustee values the Trust’s gold based on the most recently announced LBMA Gold Price PM or LBMA Gold Price AM. If the Sponsor determines that such price is inappropriate to use, it must identify an alternate basis for evaluation to be employed by the Trustee. The Sponsor may instruct the Trustee to use a different price which is reasonably available to the Trustee at no cost to the Trustee that the Sponsor determines to represent fairly the commercial value of the Trust’s gold.

The Trustee’s estimation of accrued but unpaid fees, expenses and liabilities is conclusive upon all persons interested in the Trust, and no revision or correction in any computation made under the Trust Agreement is required by reason of any difference in amounts estimated from those actually paid.

The Sponsor and the investors may rely on any evaluation or determination of any amount made by the Trustee, and, except for any determination by the Sponsor as to the price to be used to evaluate gold, the Sponsor has no responsibility for the evaluation’s accuracy. The determinations the Trustee makes are made in good faith upon the basis of, and the Trustee will not be liable for any errors contained in, information reasonably available to it. The Trustee is not liable to the Sponsor, Authorized Participants, investors or any other person for errors in judgment. However, the preceding liability exclusion will not protect the Trustee against any liability resulting from bad faith or gross negligence in the performance of its duties.

Results of Operations

Three and Nine Months Ended September 30, 2022 and 2021

For the three months ended September 30, 2022, 4,900,000 shares (196 Baskets) were created in exchange for 48,646.5 ounces of gold, 13,880,000 shares (555 Baskets) were redeemed in exchange for 137,799.9 ounces of gold, and 141.3 ounces of gold were sold to pay expenses. For the nine months ended September 30, 2022, 26,650,000 shares (1,066 Baskets) were created in exchange for 264,757.9 ounces of gold, 25,980,000 shares (1,039 Baskets) were redeemed in exchange for 257,995.2 ounces of gold, and 425.9 ounces of gold were sold to pay expenses. The Trust’s NAV per share ended the period at $16.59 compared to $18.04 at June 30, 2022 and $18.09 at December 31, 2021. The change in the NAV per share was due to a change in the price of gold to $1,671.75 at period end, which represented a decrease of (7.99)% from $1,817.00 at June 30, 2022 and a decrease of (8.15)% from $1,820.10 at December 31, 2021.

At September 30, 2022, the Custodian held 239,448.7 ounces of gold on behalf of the Trust in its vault, with a market value of $400,298,339 (cost: $447,396,288) based on the LBMA PM Gold Price at period end.

At September 30, 2021, the Custodian held 228,243.1 ounces of gold on behalf of the Trust in its vault, with a market value of $397,782,021 (cost: $400,109,939) based on the LBMA PM Gold Price at period end.

The change in net assets from operations for the three months ended September 30, 2022 was $(41,568,663), which was due to (i) the Sponsor Fee of $(225,175) and (ii) a net realized and unrealized loss of $(41,343,488) from operations, which in turn resulted from a net realized loss on gold distributed for redemptions of $(4,334,332), a net realized loss on gold transferred to pay expenses of $(29,400) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $(36,979,756). Other than the Sponsor Fee, the Trust had no expenses during the three months ended September 30, 2022.

The change in net assets from operations for the three months ended September 30, 2021 was $(5,089,113), which was due to (i) the Sponsor Fee of $(172,760) and (ii) a net realized and unrealized loss of $(4,916,353) from operations, which in turn resulted from a net realized loss on gold transferred to pay expenses of $(2,352) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $(4,914,001). Other than the Sponsor Fee, the Trust had no expenses during the three months ended September 30, 2021.

13

Table of Contents

The change in net assets from operations for the nine months ended September 30, 2022 was $(43,644,019), which was due to (i) the Sponsor Fee of $(780,094) and (ii) a net realized and unrealized loss of $(42,863,925) from operations, which in turn resulted from a net realized gain on gold distributed for redemptions of $19,888,824, a net realized loss on gold transferred to pay expenses of $(64,667) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $(62,688,082). Other than the Sponsor Fee, the Trust had no expenses during the nine months ended September 30, 2022.

The change in net assets from operations for the nine months ended September 30, 2021 was $(35,512,329), which was due to (i) the Sponsor Fee of $(503,341) and (ii) a net realized and unrealized loss of $(35,008,988) from operations, which in turn resulted from a net realized gain on gold distributed for redemptions of $47,462,394, a net realized loss on gold transferred to pay expenses of $(38,462) and a net change in unrealized appreciation/depreciation on investments in gold bullion of $(82,432,920). Other than the Sponsor Fee, the Trust had no expenses during the nine months ended September 30, 2021. Liquidity and Capital Resources

The Trust is not aware of any trends, demands, commitments, events or uncertainties that are reasonably likely to result in material changes to its liquidity needs. In exchange for the Sponsor Fee, the Sponsor has agreed to assume and be responsible for the payment of most of the expenses incurred by the Trust, up to a maximum amount equal to the greater of $500,000 per annum and the amount that is equal to 0.15% of the average total value of the gold held by the Trust, as determined by the Trustee on each business day, plus the value of all other assets of the Trust (other than any amount credited to the Trust’s reserve account), including cash, if any. As such, the only ordinary expense of the Trust during the period covered by this report was the Sponsor Fee. The Sponsor Fee accrues daily based on the prior business day’s NAV and is payable in cash from the Trust Property or the sale of gold in accordance with the Trust Agreement.

The Trustee will, when directed by the Sponsor, and, in the absence of such direction may, in its discretion, sell gold in such quantity and at such times as may be necessary to permit payment in cash of the Trust’s extraordinary expenses not assumed by the Sponsor. At September 30, 2022 and 2021, the Trust did not have any cash balances.

Off-Balance Sheet Arrangement

At September 30, 2022 and 2021, the Trust did not have any off-balance sheet arrangements.

14

Table of Contents

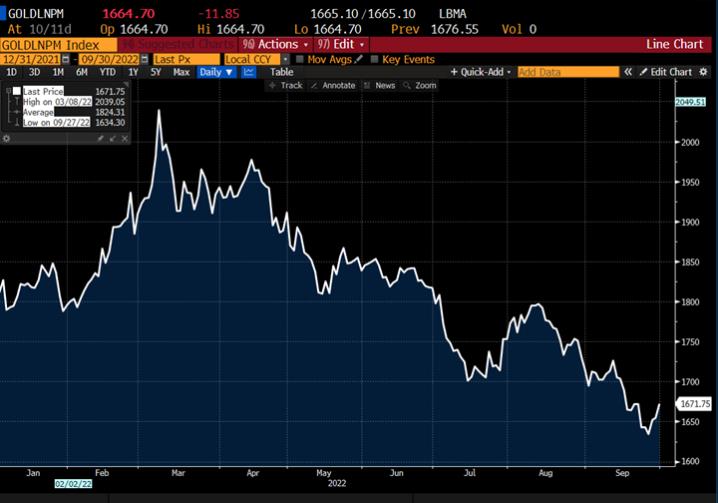

Analysis of Movements in the Price of Gold

As movements in the price of gold are expected to directly affect the price of the Trust’s shares, it is important for investors to understand and follow movements in the price of gold. Past movements in the gold price are not indicators of future movements.

The following chart shows movements in the price of gold based on the LBMA PM Gold Price in U.S. dollars per ounce over the period from December 31, 2021 to September 30, 2022.

Source: Bloomberg, LBMA Gold Price PM USD, December 31, 2021 – September 30, 2022

15

Table of Contents

The average, high, low and end-of-period gold prices for each quarterly period from July 1, 2021 through September 30, 2022, based on the LBMA PM Gold Price were:

| Period |

Average | High | Date | Low | Date | End of period |

Last business day(1) | |||||||||||||||||

| July 1, 2022 to September 30, 2022 |

$ | 1,728.91 | $ | 1,808.40 | Jul. 4, 2022 | $ | 1,634.30 | Sep. 27, 2022 | $ | 1,671.75 | Sep. 30, 2022 | |||||||||||||

| April 1, 2022 to June 30, 2022 |

$ | 1,871.76 | $ | 1,976.75 | Apr. 13, 2022 | $ | 1,809.50 | May 16, 2022 | $ | 1,817.00 | Jun. 30, 2022 | |||||||||||||

| January 1, 2022 to March 31, 2022 |

$ | 1,876.05 | $ | 2,039.05 | Mar. 08, 2022 | $ | 1,788.15 | Jan. 28, 2022 | $ | 1,942.15 | Mar. 31, 2022 | |||||||||||||

| October 1, 2021 to December 31, 2021 |

$ | 1,794.88 | $ | 1,872.25 | Nov. 16, 2021 | $ | 1,748.25 | Oct. 6, 2021 | $ | 1,820.10 | (2) | Dec. 31, 2021 | ||||||||||||

| (1) | The end of period gold price is the LBMA PM Gold Price on the last business day of the period. This is in accordance with the Trust Agreement and the basis used for calculating the NAV of the Trust. |

| (2) | December 31, 2021 was the last day of the fiscal year; however, no LBMA PM Gold Price was recorded on that date. The price provided represents the LBMA AM Gold Price on December 31, 2021, the last price recorded for the fiscal year. |

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

The Trust is a passive investment vehicle. It is not actively managed. The Trust’s investment objective is for the Shares to reflect the performance of the price of gold less the expenses of the Trust’s operations. Accordingly, fluctuations in the price of gold will affect the value of the Trust’s shares.

Item 4. Controls and Procedures.

Conclusion Regarding the Effectiveness of Disclosure Controls and Procedures

The Trust maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in its Exchange Act reports is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms, and that such information is accumulated and communicated to the duly authorized officers of the Sponsor, who perform functions similar to those the principal executive officer and principal financial officer of the Trust would perform if the Trust had officers, to allow timely decisions regarding required disclosure.

Under the supervision and with the participation of such duly authorized officers of the Sponsor, the Sponsor conducted an evaluation of the Trust’s disclosure controls and procedures, as defined under Exchange Act Rule 13a-15(e), as of September 30, 2022. Based on this evaluation, the duly authorized officers of the Sponsor, who perform functions similar to those the principal executive officer and principal financial officer of the Trust would perform if the Trust had officers concluded that the Trust’s disclosure controls and procedures were effective as of September 30, 2022.

Changes in Internal Control over Financial Reporting

There was no change in the Trust’s internal control over financial reporting that occurred during the Trust’s most recently completed fiscal quarter ended September 30, 2022 that has materially affected, or is reasonably likely to materially affect, these internal controls.

Part II. OTHER INFORMATION.

Item 1. Legal Proceedings.

Not applicable.

Item 1A. Risk Factors.

The operations of the Trust are subject to numerous risks and uncertainties. As a result, the risks and uncertainties discussed in Part I, Item 1A. Risk Factors in the 2021 Form 10-K should be carefully considered. Except as set forth below, there have been no material changes in the assessment of the Trust’s risk factors from those set forth in the 2021 Form 10-K.

16

Table of Contents

The value of the Shares fluctuates based upon the price of the gold held by the Trust. Fluctuations in the price of gold could materially adversely affect an investment in the Shares, which creates the potential for losses, regardless of the period of time the Shares are held

The Shares are intended to track the performance of the price of gold. The value of the Shares relates directly to the value of the gold owned by the Trust. Therefore, the value of the Shares will fluctuate with the price of gold. The Trust does not actively manage the gold it holds and does not use any hedging techniques to attempt to reduce the risk of losses resulting from price decreases. The price of gold has fluctuated widely over the past several years. This exposes an investment in Shares to potential losses. Several factors may affect the price of gold and, as a result, the value of the Shares, including the following:

| • | global supply and demand, which is influenced by factors including: (1) forward selling by gold producers; (2) purchases made by gold producers to unwind gold hedge positions; (3) central bank purchases and sales; (4) production and cost levels in major gold-producing countries; and (5) new production projects; |

| • | investors’ expectations regarding future inflation rates; |

| • | currency exchange rate volatility; |

| • | interest rate volatility; and |

| • | unexpected political, economic, global or regional incidents, including the recent Russian invasion of Ukraine. |

In February 2022, Russia launched a large-scale invasion of Ukraine. These steps have increased tensions between its neighbors and Western countries. These developments may continue for some time and create uncertainty in the region. Russia’s actions have induced the United States and other countries to impose economic sanctions and may result in additional sanctions in the future. Such sanctions and other similar measures could cause volatility in precious metals prices and have a significant impact on Trust performance and the value of an investment in the Shares. On March 7, 2022, the LBMA suspended six Russian gold and silver refiners from its Good Delivery List. As a result, while existing gold bars from these refiners are considered acceptable, new gold bars are not. Following an announcement at the G7 Summit to collectively ban the import of Russian gold, the UK passed regulations which prohibit the direct or indirect (i) import of gold that originated in Russia, (ii) acquisition of gold that originated in Russia or is located in Russia and (iii) supply or delivery of gold that originated in Russia, all after July 21, 2022. Similarly, US regulations prohibit the import of gold of Russian origin into the United States on or after June 28, 2022 and EU regulations prohibit the direct or indirect import, purchase or transfer of gold if it originates in Russia and has been exported from Russia after July 22, 2022.

Investors should be advised that there is no assurance that gold will maintain its long-term value in terms of U.S. dollar value in the future. In the event that the price of gold declines, the value of an investment in the Shares is expected to decline proportionately.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

a) None.

b) Not applicable.

c) Although the Trust does not purchase shares directly from its shareholders, in connection with its redemption of Baskets, the Trust redeemed 555 Baskets (13,880,000 Shares) during the fiscal quarter ended September 30, 2022 as set forth in the table below:

| Period |

Total Number of Shares Redeemed |

Average Price Per Share |

||||||

| 7/1/22 to 7/31/22 |

230,000 | $ | 17.12 | |||||

| 8/1/22 to 8/31/22 |

7,580,000 | $ | 17.66 | |||||

| 9/1/22 to 9/30/22 |

6,070,000 | $ | 16.90 | |||||

|

|

|

|||||||

| Total |

13,880,000 | |||||||

|

|

|

|||||||

Item 3. Defaults Upon Senior Securities.

Not applicable.

Item 4. Mine Safety Disclosures.

Not applicable.

17

Table of Contents

Item 5. Other Information.

None.

Item 6. Exhibits.

See the Exhibit Index below, which is incorporated by reference herein.

18

Table of Contents

EXHIBIT INDEX

19

Table of Contents

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned in the capacities* indicated thereunto duly authorized.

GOLDMAN SACHS ASSET MANAGEMENT, L.P.

Sponsor of Goldman Sachs Physical Gold ETF

| By: | /s/ Michael Crinieri* | |

| Michael Crinieri | ||

| Global Head of Exchange Traded Funds | ||

| (Principal Executive Officer) |

| By: | /s/ Joseph DiMaria* | |

| Joseph DiMaria | ||

| Managing Director | ||

| (Principal Financial and Accounting Officer) |

Date: November 4, 2022

| * | The Registrant is a trust and the persons are signing in their capacities as Managing Directors of Goldman Sachs Asset Management, L.P., the Sponsor of the Registrant. |

20