UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________

FORM 10-K

_______________________________________________

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-38730

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) (Zip Code) | ||||||||

(203) 837 - 2000 | + | |||||||

| (Registrant's telephone number, including area code) | ||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Trading Symbol(s) | Name of each exchange on which registered: | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

___________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," " smaller reporting company, " and "emerging growth company" in Rule 12b-2 of the Exchange Act.

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☑ No ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of the voting and non-voting common stock held by non-affiliates as of June 30, 2022, was approximately $143 billion (based on the closing sale price of the stock on that date as reported on the New York Stock Exchange).

At January 31, 2023, 492,160,806 ordinary shares of €0.001 nominal value per share of the Registrant were outstanding.

Documents incorporated by reference:

LINDE PLC

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended December 31, 2022

TABLE OF CONTENTS

| Page | ||||||||

| Part I | ||||||||

| Item 1: | ||||||||

| Item 1A: | ||||||||

| Item 1B: | ||||||||

| Item 2: | ||||||||

| Item 3: | ||||||||

| Item 4: | ||||||||

| Part II | ||||||||

| Item 5: | ||||||||

| Item 6: | ||||||||

| Item 7: | ||||||||

| Item 7A: | ||||||||

| Item 8: | ||||||||

| Item 9: | ||||||||

| Item 9A: | ||||||||

| Item 9B: | ||||||||

| Item 9C: | ||||||||

| Part III | ||||||||

| Item 10: | ||||||||

| Item 11: | ||||||||

| Item 12: | ||||||||

| Item 13: | ||||||||

| Item 14: | ||||||||

| Part IV | ||||||||

| Item 15: | ||||||||

| Item 16: | ||||||||

2

FORWARD-LOOKING STATEMENTS

This document contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are identified by terms and phrases such as: anticipate, believe, intend, estimate, expect, continue, should, could, may, plan, project, predict, will, potential, forecast, and similar expressions. They are based on management’s reasonable expectations and assumptions as of the date the statements are made but involve risks and uncertainties. These risks and uncertainties include, without limitation: the performance of stock markets generally; developments in worldwide and national economies and other international events and circumstances, including trade conflicts and tariffs; changes in foreign currencies and in interest rates; the cost and availability of electric power, natural gas and other raw materials; the ability to achieve price increases to offset cost increases; catastrophic events including natural disasters, epidemics, pandemics such as COVID-19, and acts of war and terrorism; the ability to attract, hire, and retain qualified personnel; the impact of changes in financial accounting standards; the impact of changes in pension plan liabilities; the impact of tax, environmental, healthcare and other legislation and government regulation in jurisdictions in which the company operates; the cost and outcomes of investigations, litigation and regulatory proceedings; the impact of potential unusual or non-recurring items; continued timely development and market acceptance of new products and applications; the impact of competitive products and pricing; future financial and operating performance of major customers and industries served; the impact of information technology system failures, network disruptions and breaches in data security; and the effectiveness and speed of integrating new acquisitions into the business. These risks and uncertainties may cause actual future results or circumstances to differ materially from accounting principles generally accepted in the United States of America, International Financial Reporting Standards or adjusted projections, estimates or other forward-looking statements.

Linde plc assumes no obligation to update or provide revisions to any forward-looking statement in response to changing circumstances. The above listed risks and uncertainties are further described in Item 1A (Risk Factors) in this report, which should be reviewed carefully. Please consider Linde plc’s forward-looking statements in light of those risks.

3

Linde plc and Subsidiaries

PART I

ITEM 1. BUSINESS

General

Linde plc is a public limited company formed under the laws of Ireland with its principal offices in the United Kingdom and United States. Linde is the largest industrial gas company worldwide and is a major technological innovator in the industrial gases industry. Its primary products in its industrial gases business are atmospheric gases (oxygen, nitrogen, argon, and rare gases) and process gases (carbon dioxide, helium, hydrogen, electronic gases, specialty gases, and acetylene etc). The company also designs and builds equipment that produces industrial gases and offers customers a wide range of gas production and processing services such as olefin plants, natural gas plants, air separation plants, hydrogen and synthesis gas plants and other types of plants.

Linde serves a diverse group of industries including healthcare, chemicals and energy, manufacturing, metals and mining, food and beverage, and electronics.

Linde’s sales were $33,364 million, $30,793 million, and $27,243 million for 2022, 2021, and 2020, respectively. Refer to Item 7, Management's Discussion and Analysis, for a discussion of consolidated sales and Note 18 to the consolidated financial statements for additional information related to Linde’s reportable segments.

Industrial Gases Products and Manufacturing Processes

Atmospheric gases are the highest volume products produced by Linde. Using air as its raw material, Linde produces oxygen, nitrogen and argon through several air separation processes of which cryogenic air separation is the most prevalent. Rare gases, such as krypton, neon and xenon, are also produced through cryogenic air separation. As a pioneer in the industrial gases industry, Linde is a leader in developing a wide range of proprietary and patented applications and supply systems technology. Linde also led the development and commercialization of non-cryogenic air separation technologies for the production of industrial gases. These technologies open important new markets and optimize production capacity for the company by lowering the cost of supplying industrial gases. These technologies include proprietary vacuum pressure swing adsorption (“VPSA”) and membrane separation to produce gaseous oxygen and nitrogen, respectively.

Process gases, including carbon dioxide, hydrogen, helium, specialty gases and acetylene are produced by methods other than air separation.

Hydrogen is produced from a range of feedstocks using an array of different technologies. Despite hydrogen being an invisible molecule, colors are often used to designate and differentiate between the production processes used to produce the molecule. The majority of hydrogen currently produced by Linde is what is termed gray hydrogen and is derived from natural gas or methane, using steam methane reformation technology. Linde has multiple technologies to produce blue and green hydrogen, which are both considered types of clean energy. Blue hydrogen is produced by capturing the carbon emissions from the hydrogen plant and either utilizing them in a way that stops them from being emitted or sequestering them in the subsurface for the long term. Green hydrogen is produced by electrolysis using renewable energy or from the steam methane reforming of biomethane. Low carbon intensity, high-purity hydrogen is also produced by purifying and recovering by-product hydrogen sources from the chemical and petrochemical industries.

Helium is sourced from certain helium-rich natural gas streams in the United States, with additional supplies being acquired from outside the United States. Carbon monoxide can be produced by either steam methane reforming or auto-thermal reforming of natural gas or other feed streams such as naphtha. Acetylene is primarily sourced as a chemical by-product, but may also be produced from calcium carbide and water. Most carbon dioxide is purchased from by-product sources, including chemical plants, refineries and industrial processes or is recovered from carbon dioxide wells. Carbon dioxide is processed in Linde’s plants to produce commercial and food-grade carbon dioxide.

Industrial Gases Distribution

There are three basic distribution methods for industrial gases: (i) on-site or tonnage; (ii) merchant or bulk liquid; and (iii) packaged or cylinder gases. These distribution methods are often integrated, with products from all three supply modes coming from the same plant. The method of supply is generally determined by the lowest cost means of meeting the customer’s needs, depending upon factors such as volume requirements, purity, pattern of usage, and the form in which the product is used (as a gas or as a cryogenic liquid).

On-site. Customers that require the largest volumes of product (typically oxygen, nitrogen and hydrogen) and that have a relatively constant demand pattern are supplied by cryogenic and process gas on-site plants. Linde constructs plants on or

4

adjacent to these customers’ sites and supplies the product directly to customers by pipeline. On-site product supply contracts generally are total requirement contracts with terms typically ranging from 10-20 years and containing minimum purchase requirements and price escalation provisions. Many of the cryogenic on-site plants also produce liquid products for the merchant market. Therefore, plants are typically not dedicated to a single customer. Advanced air separation processes allow on-site delivery to customers with smaller volume requirements.

Merchant. The merchant business is generally associated with distributable liquid oxygen, nitrogen, argon, carbon dioxide, hydrogen and helium. The deliveries generally are made from Linde’s plants by tanker trucks to storage containers at the customer's site which are usually owned and maintained by Linde and leased to the customer. Due to distribution cost, merchant oxygen and nitrogen generally have a relatively small distribution radius from the plants at which they are produced. Merchant argon, hydrogen and helium can be shipped much longer distances. The customer agreements used in the merchant business are usually three to seven-year requirement contracts.

Packaged Gases. Customers requiring small volumes are supplied products in metal containers called cylinders, under medium to high pressure. Packaged gases include atmospheric gases, carbon dioxide, hydrogen, helium, acetylene and related products. Linde also produces and distributes in cylinders a wide range of specialty gases and mixtures. Cylinders may be delivered to the customer’s site or picked up by the customer at a packaging facility or retail store. Packaged gases are generally sold under one to three-year supply contracts and through purchase orders.

Engineering

Linde’s Engineering business has a global presence, with its focus on market segments such as air separation, hydrogen, synthesis, olefin and natural gas plants. The company utilizes its extensive process engineering know-how in the planning, design and construction of highly efficient turnkey plants for the production and processing of gases. With its state-of-the-art sustainable technologies Engineering also helps customers avoid, capture and utilize CO2 emissions. Its technology portfolio covers the entire value chain for production, liquefaction, storage, distribution and application of hydrogen which supports the transition to clean energy. Its digital services and solutions increase plant efficiency and performance.

Linde's plants are used in a wide variety of fields: in the petrochemical and chemical industries, in refineries and fertilizer plants, to recover air gases, to produce synthesis gases, to treat natural gas and to produce noble gases. The Engineering business either supplies plant components directly to the customer or to the industrial gas business of Linde which operates the plants under a long-term gases supply contract.

Inventories – Linde carries inventories of merchant and cylinder gases and hardgoods to supply products to its customers on a reasonable delivery schedule. On-site plants and pipeline complexes have limited inventory. Inventory obsolescence is not material to Linde’s business.

Customers – Linde is not dependent upon a single customer or a few customers.

International – Linde is a global enterprise with approximately 68% of its 2022 sales outside of the United States. The company also has majority or wholly owned subsidiaries that operate in approximately 45 European, Middle Eastern and African countries (including Germany, the United Kingdom (U.K.), France, Sweden, and the Republic of South Africa); approximately 20 Asian and South Pacific countries (including China, Australia, India, South Korea and Thailand); and approximately 20 countries in North and South America (including Canada, Mexico and Brazil).

The company also has equity method investments operating in Europe, Asia, Africa, the Middle East, and North America.

Linde’s non-U.S. business is subject to risks customarily encountered in non-U.S. operations, including fluctuations in foreign currency exchange rates, import and export controls, and other economic, political and regulatory policies of local governments. Also, see Item 1A. “Risk Factors” and Item 7A. “Quantitative and Qualitative Disclosures About Market Risk.”

Seasonality – Linde’s business is generally not subject to seasonal fluctuations to any significant extent.

Research and Development – Linde’s research and development is directed toward development of gas processing, separation and liquefaction technologies, and clean energy technologies; improving distribution of industrial gases and the development of new markets and applications for these gases. This results in the development of new advanced air separation, hydrogen, synthesis gas, natural gas, adsorption and chemical process technologies; novel clean energy and carbon management solutions; as well as the frequent introduction of new industrial gas applications. Research and development is primarily conducted at Munich, Germany, Tonawanda, New York, Burr Ridge, Illinois and Shanghai, China.

5

Patents and Trademarks – Linde owns or licenses a large number of patents that relate to a wide variety of products and processes. Linde’s patents expire at various times over the next 20 years. While these patents and licenses are considered important to its individual businesses, Linde does not consider its business as a whole to be materially dependent upon any one particular patent, or patent license, or family of patents. Linde also owns a large number of trademarks, of which the "Linde" trademark is the most significant.

Raw Materials and Energy Costs – Energy is the single largest cost item in the production and distribution of industrial gases. Most of Linde’s energy requirements are in the form of electricity, natural gas and diesel fuel for distribution. The company mitigates electricity, natural gas, and hydrocarbon price fluctuations contractually through pricing formulas, surcharges, and cost pass–through and tolling arrangements.

The supply of energy has not been a significant issue in the geographic areas where the company conducts business. However, energy availability and price is unpredictable and may pose unforeseen future risks.

For carbon dioxide, carbon monoxide, helium, hydrogen and specialty gases, raw materials are largely purchased from outside sources. Linde has contracts or commitments for, or readily available sources of, most of these raw materials; however, their long-term availability and prices are subject to market conditions.

Competition – Linde participates in highly competitive markets in industrial gases and engineering, which are characterized by a mixture of local, regional and global players, all of which exert competitive pressure on the parties. In locations where Linde has pipeline networks, which enable the company to provide reliable and economic supply of products to larger customers, Linde derives a competitive advantage.

Competitors in the industrial gases industry include global and regional companies such as L’Air Liquide S.A., Air Products and Chemicals, Inc., Messer Group GmbH, Mitsubishi Chemical Holdings Corporation (through Taiyo Nippon Sanso Corporation) as well as an extensive number of small to medium size independent industrial gas companies which compete locally as producers or distributors. In addition, a significant portion of the international gases market relates to customer-owned plants.

Employees – The company sources talent from an ever-changing and competitive environment. The ability to source and retain qualified and committed employees is a prerequisite for the company’s success, and represents a general risk for Linde.

The Board of Directors ("Board") has established a strategic business objective to maintain world-class standards in talent management. Executive variable compensation is assessed annually based on performance in financial measures as well as in several strategic non-financial areas, including talent management. The Human Capital Committee assists the Board in its oversight of Linde’s compensation policies and programs, particularly in regard to reviewing executive compensation for Linde’s executive officers. The Human Capital Committee also periodically reviews the company’s management development and succession programs, diversity policies and objectives, and the associated programs to achieve those objectives. The global head of Human Resources reports to the Chief Executive Officer ("CEO"). A global leader of Diversity and Inclusion reports to the head of Human Resources.

Linde has aligned diversity and inclusion with its business strategies and implemented diversity action planning into business process and performance management. Diversity and inclusion are line management responsibilities and Linde seeks competitive advantage through proactive management of its talent pipeline and recruiting processes. Linde provides equal employment opportunity, and recruits, hires, promotes and compensates people based solely on their performance and ability.

Employees receive a competitive salary and variable compensation components based on performance and job level. Linde has collective bargaining agreements with unions at numerous locations throughout the world. Additional benefits are offered such as occupational pensions and contributions towards health insurance or medical screening, reflecting regional conditions and local competition. Senior managers participate directly in the company’s growth in value through the Long Term Incentive Plan of Linde plc. From time to time, Linde may introduce special compensation schemes to recognize or reward specific individuals such as the one implemented in 2020 for global front-line employees. Linde also invests in professional development of its employees through formal and on-the-job training.

As of December 31, 2022, Linde had 65,010 employees worldwide comprised of approximately 28 percent women and 72 percent men.

Environment – Information required by this item is incorporated herein by reference to the section captioned “Management’s Discussion and Analysis – Environmental Matters” in Item 7 of this 10-K.

6

Available Information – The company makes its periodic and current reports available, free of charge, on or through its website, www.linde.com, as soon as practicable after such material is electronically filed with, or furnished to, the Securities and Exchange Commission ("SEC"). Investors may also access from the company website other investor information such as press releases and presentations. Information on the company’s website is not incorporated by reference herein. In addition, the public may read and copy any materials filed with the SEC free of charge at the SEC’s website, www.sec.gov, that contains reports, proxy information statements and other information regarding issuers that file electronically.

Executive Officers – The following Executive Officers have been elected by the Board of Directors and serve at the pleasure of the Board. It is expected that the Board will elect officers annually following each annual meeting of shareholders.

Sanjiv Lamba, 58, was appointed Chief Executive Officer of Linde effective March 1, 2022. Prior to being appointed CEO, he was Chief Operating Officer starting in January 2021 and after serving as Executive Vice President, APAC, beginning in October 2018. Previously, Mr. Lamba was appointed a Member of the Executive Board of Linde AG in 2011, responsible for the Asia, Pacific segment of the Gases Division, for Global Gases Businesses Helium & Rare Gases, Electronics as well as Asia Joint Venture Management. Mr. Lamba started his career 1989 with BOC India in Finance where he progressed to become Director of Finance before being appointed as Managing Director for BOC’s India’s business in 2001. Throughout his years with BOC/Linde, he worked in various roles across a number of different geographies including Germany, the U.K., Singapore and India.

Guillermo Bichara, 48, is Executive Vice President and Chief Legal Officer. He previously served as Praxair’s Vice President and General Counsel. Mr. Bichara joined the company in 2006, first as Director of Legal Affairs at Praxair Mexico before being promoted to Vice President and General Counsel of Praxair Asia. He subsequently had responsibility for Europe, Mexico and corporate transactions before being promoted to Associate General Counsel and Assistant Secretary. Mr. Bichara previously held roles at Cemex and various global law firms.

Sean Durbin, 52, became Executive Vice President, EMEA in April 2021. Previously, he served as Senior Vice President, Global Functions beginning in July 2020. Durbin joined Praxair, Inc. in 1993 and served in various roles across operations, engineering, project management, business development and sales. In recent years, he has held leadership positions including Business President, Region Europe South from 2019 to 2020, and President, Praxair Canada Inc. from 2013 to 2019.

Kelcey E. Hoyt, 53, became the Chief Accounting Officer of Linde in October 2018. Prior to this, she served as Vice President and Controller of Praxair, Inc. beginning in August 2016. Prior to becoming Controller, she served as Praxair’s Director of Investor Relations since 2010. She joined Praxair in 2002 and served as Director of Corporate Accounting and SEC Reporting through 2008, and later served as Controller for various divisions within Praxair’s North American Industrial Gas business. Previously, she was in audit at KPMG, LLP.

Juergen Nowicki, 59, was appointed Executive Vice President and CEO, Linde Engineering in April 2020. Prior to this, he was Senior Vice President, Commercial, Linde Engineering. Mr. Nowicki joined Linde in 1991 as an Internal Auditor and held various positions in Finance and Controlling. In 2002, he was appointed CFO Linde Gas North America, USA, and was named Head of Finance and Control for The Linde Group in 2006. Nowicki assumed the role of Managing Director, Linde Engineering in 2011.

John Panikar, 55, was appointed Executive Vice President, APAC of Linde effective in January 2021. Previously, he served as President UK & Africa of Linde since October 2018. From 2014 to 2018, Mr. Panikar was President of Praxair Asia. He began his career with Praxair in 1991 as an Applications Engineer. Over the years, Mr. Panikar held increasingly responsible positions including Manager of Site Services and Equipment, Business Development Director for Praxair Asia, Managing Director of Praxair India, VP, South Region, North American Industrial Gases and President, Praxair Distribution, Inc.

David P. Strauss, 64, is Executive Vice President and Chief Human Resources Officer. He previously served as Praxair’s Chief Human Resources Officer. Mr. Strauss joined Linde in 1990 as an Applications Engineer before being promoted to lead the electronics materials business. He subsequently served as Vice President of Safety, Health and Environment.

Matthew J. White, 50, became Executive Vice President and Chief Financial Officer of Linde in October 2018. He previously served as the Senior Vice President and Chief Financial Officer of Praxair, Inc. since January 1, 2014. Prior to

7

this, Mr. White was President of Praxair Canada from 2011 to 2014. He joined Praxair in 2004 as finance director for the company’s largest business unit, North American Industrial Gases. In 2008, he became Vice President and Controller of Praxair, Inc., then was named Vice President and Treasurer in 2010. Before joining Praxair, White was vice president, finance, at Fisher Scientific and before that he held various financial positions, including group controller, at GenTek, a manufacturing and performance chemicals company.

8

ITEM 1A. RISK FACTORS

Due to the size and geographic reach of the company’s operations, a wide range of factors, many of which are outside of the company’s control, could materially affect the company’s future operations and financial performance. Management believes the following risks may significantly impact the company:

Weakening economic conditions in markets in which Linde does business may adversely impact its financial results and/or cash flows.

Linde serves a diverse group of industries across more than 80 countries, which generally leads to financial stability through various business cycles. However, a broad decline in general economic or business conditions in the industries served by its customers could adversely affect the demand for Linde’s products and impair the ability of its customers to satisfy their obligations to Linde, resulting in uncollected receivables and/or unanticipated contract terminations or project delays. For example, global political and economic uncertainty could reduce investment activities of Linde’s customers, which could adversely affect Linde’s business.

In addition, many of Linde’s customers are in businesses that are cyclical in nature, such as the chemicals, metals and energy industries. Downturns in these industries may adversely impact Linde during these cycles. Additionally, such conditions could impact the utilization of Linde’s manufacturing capacity which may require it to recognize impairment losses on tangible assets such as property, plant and equipment, as well as intangible assets such as goodwill, customer relationships or intellectual property.

Increases in the cost of energy and raw materials and/or disruption in the supply of these materials could result in lost sales or reduced profitability.

Energy is the single largest cost item in the production and distribution of industrial gases. Most of Linde’s energy requirements are in the form of electricity, natural gas and diesel fuel for distribution. Linde attempts to minimize the financial impact of variability in these costs through the management of customer contracts and reducing demand through operational productivity and energy efficiency. Large customer contracts typically have escalation and pass-through clauses to recover energy and feedstock costs. Such attempts may not successfully mitigate cost variability, which could negatively impact Linde’s financial condition or results of operations. The supply of energy has not been a significant issue in the geographic areas where Linde conducts business. However, regional energy conditions are unpredictable and may pose future risk.

For carbon dioxide, carbon monoxide, helium, hydrogen and specialty gases, raw materials are largely purchased from outside sources. Where feasible, Linde sources several of these raw materials, including carbon dioxide, hydrogen and calcium carbide, as chemical or industrial byproducts. In addition, Linde has contracts or commitments for, or readily available sources of, most of these raw materials; however, their long-term availability and prices are subject to market conditions. A disruption in supply of such raw materials could impact Linde’s ability to meet contractual supply commitments.

Linde’s international operations are subject to the risks of doing business abroad and international events and circumstances may adversely impact its business, financial condition or results of operations.

Linde has substantial international operations which are subject to risks including devaluations in currency exchange rates, transportation delays and interruptions, political and economic instability and disruptions, restrictions on the transfer of funds, trade conflicts and the imposition of duties and tariffs, import and export controls, changes in governmental policies, labor unrest, possible nationalization and/or expropriation of assets, changes in U.S. and non-U.S. tax policies and compliance with governmental regulations. These events could have an adverse effect on the international operations of Linde in the future by reducing the demand for its products, decreasing the prices at which it can sell its products, reducing the revenue from international operations or otherwise having an adverse effect on its business.

Currency exchange rate fluctuations and other related risks may adversely affect Linde's results.

Because a significant portion of Linde's revenue is denominated in currencies other than its reporting currency, the U.S. dollar, changes in exchange rates will produce fluctuations in revenue, costs and earnings and may also affect the book

9

value of assets and liabilities and related equity. Although the company from time to time utilizes foreign exchange forward contracts to hedge these exposures, its efforts to minimize currency exposure through such hedging transactions may not be successful depending on market and business conditions. As a result, fluctuations in foreign currency exchange rates could adversely affect Linde’s financial condition, results of operations or cash flows.

Macroeconomic factors may impact Linde’s ability to obtain financing or increase the cost of obtaining financing which may adversely impact Linde’s financial results and/or cash flows.

Volatility and disruption in the U.S., European and global credit and equity markets, from time to time, could make it more difficult for Linde to obtain financing for its operations and/or could increase the cost of obtaining financing. In addition, Linde’s borrowing costs can be affected by short- and long-term debt ratings assigned by independent rating agencies which are based, in significant part, on its performance as measured by certain criteria such as interest coverage and leverage ratios. A decrease in these debt ratings could increase the cost of borrowing or make it more difficult to obtain financing.

An impairment of goodwill or intangible assets could negatively impact the company's financial results.

As of December 31, 2022, the net carrying value of goodwill and other indefinite-lived intangible assets was $26 billion and $2 billion, respectively, primarily as a result of the business combination and the related acquisition method of accounting applied to Linde AG. In accordance with generally accepted accounting principles, the company periodically assesses these assets to determine if they are impaired. Significant negative industry or economic trends, disruptions to business, unexpected significant changes or planned changes in use of the assets, divestitures and sustained market capitalization declines may result in recognition of impairments to goodwill or other indefinite-lived assets. Any charges relating to such impairments could have a material adverse impact on Linde's results of operations in the periods recognized.

Catastrophic events could disrupt the operations of Linde and/or its customers and suppliers and may have a significant adverse impact on the results of operations.

The occurrence of catastrophic events or natural disasters such as extreme weather, including hurricanes and floods; health epidemics; pandemics, such as COVID-19; and acts of war or terrorism, could disrupt or delay Linde’s ability to produce and distribute its products to customers and could potentially expose Linde to third-party liability claims. In addition, such events could impact Linde’s customers and suppliers resulting in temporary or long-term outages and/or the limitation of supply of energy and other raw materials used in normal business operations. Linde evaluates the direct and indirect business risks, consults with vendors, insurance providers and industry experts, makes investments in suitably resilient design and technology, and conducts regular reviews of the business risks with management. Despite these steps, however, these situations are outside Linde’s control and may have a significant adverse impact on its financial results.

The inability to attract and retain qualified personnel may adversely impact Linde’s business.

If Linde fails to attract, hire and retain qualified personnel, it may not be able to develop, market or sell its products or successfully manage its business. Linde is dependent upon a highly skilled, experienced and efficient workforce to be successful. Much of Linde’s competitive advantage is based on the expertise and experience of key personnel regarding marketing, technology, manufacturing and distribution infrastructure, systems and products. The inability to attract and hire qualified individuals or the loss of key employees in very skilled areas could have a negative effect on Linde’s financial results.

If Linde fails to keep pace with technological advances in the industry or if new technology initiatives do not become commercially accepted, customers may not continue to buy Linde’s products and results of operations could be adversely affected.

Linde’s research and development is directed toward developing new and improved methods for the production and distribution of industrial gases, the design and construction of plants and toward developing new markets and applications for the use of industrial and process gases. This results in the introduction of new applications and the development of new advanced process technologies. As a result of these efforts, Linde develops new and proprietary technologies and employs necessary measures to protect such technologies within the global geographies in which Linde operates. These technologies help Linde to create a competitive advantage and to provide a platform to grow its business. If Linde’s research and

10

development activities do not keep pace with competitors or if Linde does not create new technologies that benefit customers, future results of operations could be adversely affected.

Risks related to pension benefit plans may adversely impact Linde’s results of operations and cash flows.

Pension benefits represent significant financial obligations that will be ultimately settled in the future with employees who meet eligibility requirements. Because of the uncertainties involved in estimating the timing and amount of future payments and asset returns, significant estimates are required to calculate pension expense and liabilities related to Linde’s plans. Linde utilizes the services of independent actuaries, whose models are used to facilitate these calculations. Several key assumptions are used in the actuarial models to calculate pension expense and liability amounts recorded in the consolidated financial statements. In particular, significant changes in actual investment returns on pension assets, discount rates, or legislative or regulatory changes could impact future results of operations and required pension contributions.

Operational risks may adversely impact Linde’s business or results of operations.

Linde’s operating results are dependent on the continued operation of its production facilities and its ability to meet customer contract requirements and other needs. Insufficient or excess capacity threatens Linde’s ability to generate competitive profit margins and may expose Linde to liabilities related to contract commitments. Operating results are also dependent on Linde’s ability to complete new construction projects on time, on budget and in accordance with performance requirements. Failure to do so may expose Linde’s business to loss of revenue, potential litigation and loss of business reputation.

Also inherent in the management of Linde’s production facilities and delivery systems, including storage, vehicle transportation and pipelines, are operational risks that require continuous training, oversight and control. Material operating failures at production, storage facilities or pipelines, including fire, toxic release and explosions, or the occurrence of vehicle transportation accidents could result in loss of life, damage to the environment, loss of production and/or extensive property damage, all of which may negatively impact Linde’s financial results.

Linde may be subject to information technology system failures, network disruptions and breaches in data security.

Linde relies on information technology systems and networks for business and operational activities, and also stores and processes sensitive business and proprietary information in these systems and networks. These systems are susceptible to outages due to fire, flood, power loss, telecommunications failures, viruses, break-ins and similar events, or breaches of security.

Linde has taken steps to address these risks and concerns by implementing advanced security technologies, internal controls, network and data center resiliency and recovery process. Despite these steps, however, our information technology systems have in the past been and in the future will likely be subject to increasingly sophisticated cyber attacks. Operational failures and breaches of security from such attempts could lead to the loss or disclosure of confidential information or personal data belonging to Linde or our employees and customers or suppliers. These failures and breaches could result in business interruption or malfunction and lead to legal or regulatory actions that could result in a material adverse impact on Linde’s operations, reputation and financial results. To date, such attempts have not had any significant impact on Linde's operations or financial results.

The inability to effectively integrate acquisitions or collaborate with joint venture partners could adversely impact Linde’s financial position and results of operations.

Linde has evaluated and expects to continue to evaluate, a wide array of potential strategic acquisitions and joint ventures. Many of these transactions, if consummated, could be material to its financial condition and results of operations. In addition, the process of integrating an acquired company, business or group of assets may create unforeseen operating difficulties and expenditures. Although historically Linde has been successful with its acquisition strategy and execution, the areas where Linde may face risks include:

•the need to implement or remediate controls, procedures and policies appropriate for a larger public company at companies that prior to the acquisition lacked these controls, procedures and policies;

•diversion of management time and focus from operating existing business to acquisition integration challenges;

11

•cultural challenges associated with integrating employees from the acquired company into the existing organization;

•the need to integrate each company’s accounting, management information, human resources and other administrative systems to permit effective management;

•difficulty with the assimilation of acquired operations and products;

•failure to achieve targeted synergies and cost reductions; and

•inability to retain key employees and business relationships of acquired companies.

Foreign acquisitions and joint ventures involve unique risks in addition to those mentioned herein, including those related to integration of operations across different cultures and languages, currency risks and the particular economic, political and regulatory risks associated with specific countries.

Also, the anticipated benefit of potential future acquisitions may not materialize. Future acquisitions or dispositions could result in the incurrence of debt, contingent liabilities or amortization expenses, or impairments of goodwill, any of which could adversely impact Linde’s financial results.

Linde is subject to a variety of international laws and government regulations and changes in, or failure to comply with, these laws or regulations could have an adverse impact on the company’s business, financial position and results of operations.

Linde is subject to regulations in the following areas, among others:

•environmental protection, including climate change and energy efficiency laws and policies;

•U.S. and non-U.S. tax laws and currency controls;

•safety;

•securities laws applicable in the United States, the European Union, Germany, Ireland, and other jurisdictions;

•trade and import/export restrictions, as well as economic sanctions laws;

•antitrust matters;

•data protection;

•global anti-bribery laws, including the U.S. Foreign Corrupt Practices Act; and

•healthcare regulations.

Changes in these or other regulatory areas may impact Linde’s profitability and may give rise to new or increased compliance risks: it may become more complex and costly to ensure compliance, and the level of sanctions in the event of non-compliance may rise. Noncompliance with such laws and regulations could result in penalties or sanctions, cancellation of marketing rights or restrictions on participation in, or even exclusion from, public tender proceedings, all of which could have a material adverse impact on Linde’s financial results and/or reputation.

Such changes may also restrict Linde’s ability to compete effectively in the marketplace. Changes to regulations in the areas of environmental protection and climate change, for example, may impact customer and competitor behavior driving structural changes in key end markets. While Linde will work to mitigate these risks through the pursuit of strategic alliances and investment in applications technologies to capture new growth areas, given the uncertainty about the type and scope of new regulations, it is difficult to predict how such changes and their impact on market behavior will ultimately impact Linde’s business. However, such changes could have a material adverse impact on Linde's results of operations.

Doing business globally requires Linde to comply with anti-corruption, trade, compliance and economic sanctions and similar laws, and to implement policies and procedures designed to ensure that its employees and other intermediaries comply with the applicable restrictions. These restrictions include prohibitions on the sale or supply of certain products, services and any other economic resources to embargoed or sanctioned countries, governments, persons and entities. Compliance with these restrictions requires, among other things, screening of business partners. Despite its commitment to legal compliance and corporate ethics, the company cannot ensure that its policies and procedures will always protect it from intentional, reckless or negligent acts committed by employees or agents under the applicable laws. If Linde fails to comply with laws governing the conduct of international operations, Linde may be subject to criminal and civil penalties and other remedial measures, which could materially adversely affect its reputation, business and results of operations.

12

The outcome of litigation or governmental investigations may adversely impact the company’s business or results of operations.

Linde’s subsidiaries are party to various lawsuits and governmental investigations arising in the ordinary course of business. Adverse outcomes in some or all of the claims pending may result in significant monetary damages or injunctive relief that could adversely affect Linde’s ability to conduct business. Linde and its subsidiaries may in the future become subject to further claims and litigation, which is impossible to predict. The litigation and other claims Linde faces are subject to inherent uncertainties. Legal or regulatory judgments or agreed settlements might give rise to expenses which are not covered, or are not fully covered, by insurance benefits and may also lead to negative publicity and reputational damage. An unfavorable outcome or determination could cause a material adverse impact on the company’s results of operations.

Potential product defects or inadequate customer care may adversely impact Linde’s business or results of operations.

Risks associated with products and services may result in potential liability claims, the loss of customers or damage to Linde’s reputation. Principal possible causes of risks associated with products and services are product defects or an inadequate level of customer care when Linde is providing services.

Linde is exposed to legal risks relating to product liability in the countries where it operates, including countries such as the United States, where legal risks (in particular through class actions) have historically been more significant than in other countries. The outcome of any pending or future products and services proceedings or investigations cannot be predicted and legal or regulatory judgments or agreed settlements may give rise to significant losses, costs and expenses.

The manufacturing and sale of products as well as the construction and sale of plants by Linde may give rise to risks associated with the production, filling, storage, handling and transport of raw materials, goods or waste. Industrial gases are potentially hazardous substances and medical gases and the related healthcare services must comply with the relevant specifications in order to not adversely affect the health of patients treated with them.

Linde’s products and services, if defective or not handled or performed appropriately, may lead to personal injuries, business interruptions, environmental damages or other significant damages, which may result, among other consequences, in liability, losses, monetary penalties or compensation payments, environmental clean-up costs or other costs and expenses, exclusion from certain market sectors deemed important for future development of the business and loss of reputation. All these consequences could have a material adverse effect on Linde’s business and results of operations.

U.S. civil liabilities may not be enforceable against Linde.

Linde is organized under the laws of Ireland and substantial portions of its assets are located outside of the United States. In addition, certain directors and officers of Linde and its subsidiaries reside outside the United States. As a result, it may be difficult for investors to effect service of process within the United States upon Linde or such persons, or to enforce outside the United States judgments obtained against such persons in U.S. courts in any action, including actions predicated upon the civil liability provisions of the U.S. federal securities laws. In addition, it may be difficult for investors to enforce, in original actions brought in courts in jurisdictions located outside the United States, rights predicated upon the U.S. federal securities laws.

A judgment for the payment of money rendered by a court in the United States based on civil liability would not be automatically enforceable in Ireland. There is no treaty between Ireland and the United States providing for the reciprocal enforcement of foreign judgments. The following requirements must be met before the foreign judgment will be deemed to be enforceable in Ireland (i) the judgment must be for a definite sum, (ii) the judgment must be final and conclusive; and (iii) the judgment must be provided by a court of competent jurisdiction.

An Irish court will also exercise its right to refuse judgment if the foreign judgment (i) was obtained by fraud; (ii) violated Irish public policy; (iii) is in breach of natural justice; or (iv) if the judgment is irreconcilable with an earlier foreign judgment.

In addition, there is doubt as to whether an Irish court would accept jurisdiction and impose civil liability on Linde or such persons in an original action predicated solely upon the U.S. federal securities laws brought in a court of competent jurisdiction in Ireland against Linde or such member, officer or expert, respectively.

13

Changes in tax laws or policy could adversely impact the company’s financial position or results of operations.

Linde and its subsidiaries are subject to the tax rules and regulations in the U.S., Germany, Ireland, the U.K. and other countries in which they operate. Those tax rules and regulations are subject to change on a prospective or retroactive basis. Under current economic and political conditions tax rates and policies in any jurisdiction, including the U.S., the U.K. and the EU, are subject to significant changes which could result in a significant change to Linde's current and deferred income tax. In particular, since Linde is currently treated as U.K. tax resident, any potential changes in the tax rules applying to U.K. tax-resident companies would directly affect Linde.

A change in Linde’s tax residency could have a negative effect on the company’s future profitability and may trigger taxes on dividends or exit charges. If Linde ceases to be resident in the U.K. and becomes resident in another jurisdiction, it may be subject to U.K. exit charges, and/or could become liable for additional tax charges in the other jurisdiction. If Linde were to be treated as resident in more than one jurisdiction, it could be subject to duplicative taxation. Furthermore, although Linde is incorporated in Ireland and is not expected to be treated as a domestic corporation for U.S. federal income tax purposes, it is possible that the IRS could challenge this result or that changes in U.S. federal income tax law could alter this result. If the IRS successfully asserted such a position or the law were to change, significant adverse tax consequences may result for Linde, the company and Linde’s shareholders.

Changes in tax laws may result in higher tax expense and tax payments. In addition, changes in tax legislation and uncertainty about the tax environment in some regions may restrict Linde's opportunity to enforce its respective rights under the law. Linde also operates in countries with complex tax regulations which could be interpreted in different ways. Linde and its subsidiaries are subject to audits by taxing authorities in various jurisdictions or other review actions by the relevant financial or tax authorities. The ultimate tax outcome may differ from the amounts recorded in Linde’s or its subsidiaries’ financial statements and may materially affect their respective financial results for the period when such determination is made.

Following the Reorganization, New Linde will seek Irish High Court approval for the creation of distributable reserves. New Linde expects this will be forthcoming, but cannot guarantee this, and until distributable reserves of New Linde are created, New Linde will be unable to make distributions by way of dividends, share repurchases or otherwise under Irish law.

Under Irish law, dividends may only be paid and share repurchases and redemptions must generally be funded only out of “distributable reserves,” which New Linde will not have immediately following the Reorganization. The creation of distributable reserves of New Linde involves a reduction in New Linde’s undenominated share capital which requires the approval of the Irish High Court. The approval of the Irish High Court is expected within eight weeks following the Reorganization becoming effective. This approval is the same process successfully followed by Linde immediately after the Linde AG – Praxair, Inc. merger in 2018. New Linde is not aware of any reason why the Irish High Court would not approve the creation of distributable reserves in this manner; however, the issuance of the required order is a matter for the discretion of the Irish High Court. In the event that distributable reserves of New Linde are not created, no distributions by way of dividends, share repurchases or otherwise will be permitted under Irish law until such time as New Linde has created sufficient distributable reserves from its business activities, except that New Linde will be able to pay any dividends declared by the company prior to the Reorganization becoming effective.

14

ITEM 1B. UNRESOLVED STAFF COMMENTS

Linde has received no written SEC staff comments regarding any of its Exchange Act reports which remain unresolved.

ITEM 2. PROPERTIES

Linde's principal executive offices are located in leased office space in Woking, United Kingdom and owned office space in Danbury, Connecticut. Linde also owns principal administrative office space in Tonawanda, New York, United States and Pullach, Germany.

Due to the nature of Linde’s industrial gas products, it is generally uneconomical to transport them distances greater than a few hundred miles from the production facility. As a result, Linde operates a significant number of production facilities spread globally throughout a number of geographic regions.

The following is a description of production facilities for Linde by segment. No significant portion of these assets was leased at December 31, 2022. Generally, these facilities are utilized and are sufficient to meet the company's manufacturing needs.

Americas

The Americas segment operates production facilities primarily in the U.S., Canada, Mexico and Brazil, approximately 350 of which are mainly cryogenic air separation plants, hydrogen plants and carbon dioxide plants. There are five major pipeline complexes in North America located in northern Indiana, Houston, along the Gulf Coast of Texas, Detroit and Louisiana. Also located throughout the Americas are noncryogenic air separation plants, packaged gas facilities and other smaller plant facilities.

EMEA

The EMEA segment has production facilities primarily in Germany, France, Sweden, the Republic of South Africa, and the U.K. which include approximately 275 cryogenic air separation plants and carbon dioxide plants. Also located throughout Europe are noncryogenic air separation plants, pipelines, hydrogen, packaged gas facilities and other smaller plant facilities.

APAC

The APAC segment has production facilities located primarily in China, Australia, India, South Korea and Thailand, approximately 230 of which are cryogenic air separation plants and carbon dioxide plants. Also located throughout Asia are noncryogenic air separation plants, pipelines, hydrogen, packaged gas and other production facilities.

Engineering

The Engineering business designs and constructs turnkey process plants for third-party customers as well as for the gases businesses in many locations worldwide, such as air separation, hydrogen, synthesis, olefin and natural gas plants. Plant components are produced in owned factories in Tacherting, Germany; Hesinque, France; New York and Oklahoma, United States; and Dalian, China.

ITEM 3. LEGAL PROCEEDINGS

Information required by this item is incorporated herein by reference to the section captioned “Notes to Consolidated Financial Statements – 17. Commitments and Contingencies” in Item 8 of this 10-K.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable.

15

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Linde plc shares trade on the New York Stock Exchange (“NYSE”) and the Frankfurt Stock Exchange (“FSE”) under the ticker symbol “LIN”. At December 31, 2022 there were 7,319 shareholders of record.

On January 18, 2023, shareholders approved the company’s proposal for an intercompany reorganization that will result in the delisting of its ordinary shares from the Frankfurt Stock Exchange. Following the completion of legal and regulatory approvals, Linde anticipates that the intercompany reorganization and delisting process will be completed, and its ordinary shares will be delisted from the Frankfurt Stock Exchange, on or about March 1, 2023.

Purchases of Equity Securities – Certain information regarding purchases made by or on behalf of the company or any affiliated purchaser (as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934, as amended) of its ordinary shares during the three months ended December 31, 2022 is provided below:

| Period | Total Number of Shares Purchased (Thousands) | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (1) (Thousands) | Approximate Dollar Value of Shares that May Yet be Purchased Under the Program (2) (Millions) | |||||||||||||||||||

| October 2022 | 677 | $ | 287.57 | 677 | $ | 5,832 | |||||||||||||||||

| November 2022 | 1,323 | $ | 316.05 | 1,323 | $ | 5,414 | |||||||||||||||||

| December 2022 | 138 | $ | 333.88 | 138 | $ | 5,368 | |||||||||||||||||

| Fourth Quarter 2022 | 2,138 | $ | 308.18 | 2,138 | 5,368 | ||||||||||||||||||

(1)On February 28, 2022 the company's board of directors approved the repurchase of $10.0 billion of its ordinary shares ("2022 program") which could take place from time to time on the open market (and could include the use of 10b5-1 trading plans), subject to market and business conditions. The 2022 program has a maximum repurchase amount of 15% of outstanding shares, beginning on March 1, 2022 and expires on July 31, 2024.

(2) As of December 31, 2022, the company repurchased $4.6 billion of its ordinary shares pursuant to the 2022 ` program. As of December 31, 2022, $5.4 billion of share repurchases remain authorized under the 2022 program.

16

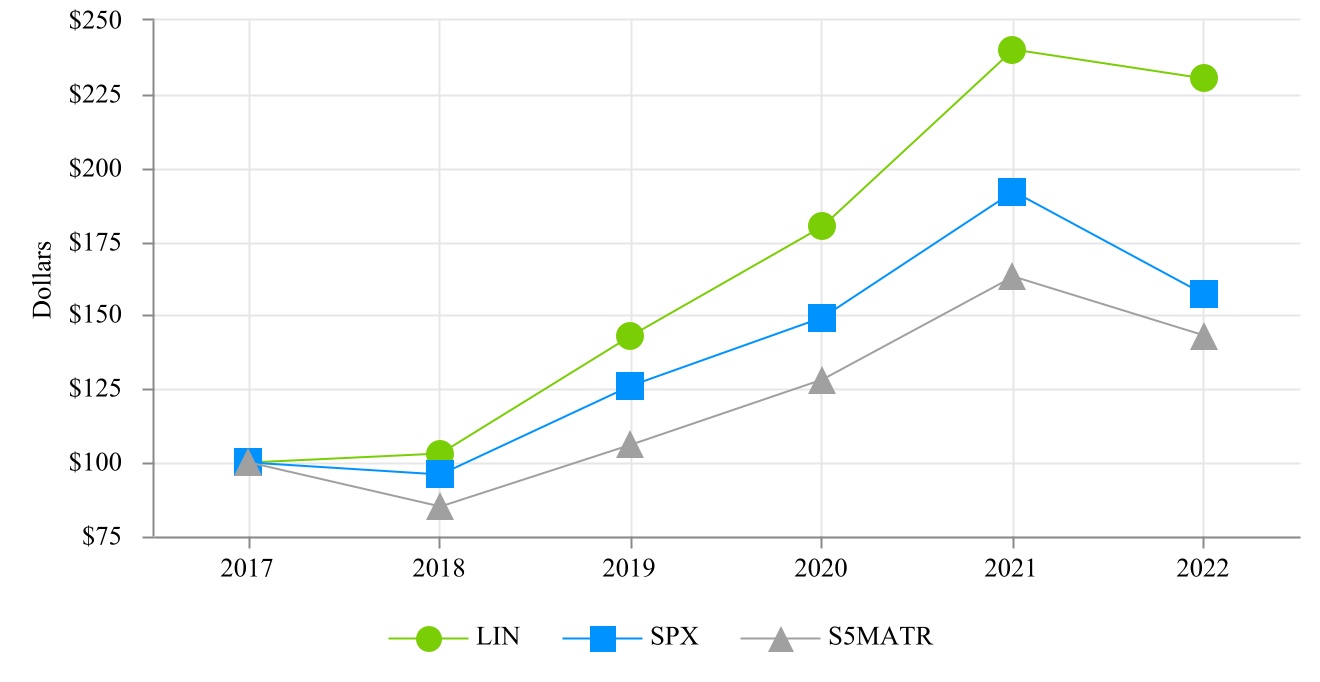

Peer Performance Table – The graph below compares the most recent five-year cumulative returns of the common stock of Praxair, the company's predecessor, through October 31, 2018 and Linde's ordinary shares for periods subsequent to October 31, 2018 with those of the Standard & Poor’s 500 Index ("SPX") and the S5 Materials Index ("S5MATR") which covers 29 companies, including Linde. The figures assume an initial investment of $100 on December 31, 2017 and that all dividends have been reinvested.

| 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |||||||||||||||

| LIN | $100 | $103 | $143 | $180 | $240 | $230 | ||||||||||||||

| SPX | $100 | $96 | $126 | $149 | $192 | $157 | ||||||||||||||

| S5MATR | $100 | $85 | $106 | $128 | $163 | $143 | ||||||||||||||

ITEM 6. RESERVED

Not applicable.

17

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion of the company’s financial condition and results of operations should be read together with its consolidated financial statements and notes to the consolidated financial statements included in Item 8 of this Form 10-K.

| Page | |||||

| Business Overview | |||||

| Executive Summary – Financial Results & Outlook | |||||

| Consolidated Results and Other Information | |||||

| Segment Discussion | |||||

| Liquidity, Capital Resources and Other Financial Data | |||||

| Off-Balance Sheet Arrangements | |||||

| Critical Accounting Estimates | |||||

| New Accounting Standards | |||||

| Fair Value Measurements | |||||

| Non-GAAP Financial Measures | |||||

| Supplemental Guarantee Information | |||||

18

BUSINESS OVERVIEW

The company's primary products in its industrial gases business are atmospheric gases (oxygen, nitrogen, argon, rare gases) and process gases (carbon dioxide, helium, hydrogen, electronic gases, specialty gases, acetylene). The company also designs, engineers, and builds equipment that produces industrial gases and offers its customers a wide range of gas production and processing services such as olefin plants, natural gas plants, air separation plants, hydrogen and synthesis gas plants and other types of plants.

Linde’s industrial gas operations are managed on a geographical basis and in 2022 86% of sales were generated by Linde's three geographic segments (Americas, EMEA and APAC) and the remaining 14% are related largely to the Engineering segment, and to a lesser extent Other (see Note 18 to the consolidated financial statements for operating segment details).

Linde serves a diverse group of industries including healthcare, chemicals and energy, manufacturing, metals and mining, food and beverage, and electronics. The diversity of end-markets supports financial stability for Linde in varied business cycles.

Linde generates most of its revenues and earnings in the following geographies where the company has its strongest market positions and where distribution and production operations allow the company to deliver the highest level of service to its customers at the lowest cost.

| North and South America ("Americas") | Europe, Middle East and Africa (“EMEA”) | Asia and Pacific (“APAC”) | ||||||||||||

| United States | Germany | China | ||||||||||||

| Brazil | United Kingdom | Australia | ||||||||||||

| Mexico | Eastern Europe | South Korea | ||||||||||||

| Canada | India | |||||||||||||

The company manufactures and distributes its industrial gas products through networks of thousands of production plants, pipeline complexes, distribution centers and delivery vehicles. Major pipeline complexes are primarily located in the United States and China. These networks are a competitive advantage, providing the foundation of reliable product supply to the company’s customer base. The majority of Linde’s business is conducted through long-term contracts which provide stability in cash flow and the ability to pass through changes in energy and feedstock costs to customers. The company has growth opportunities in all major geographies and in diverse end-markets such as healthcare, chemicals and energy, manufacturing, metals and mining, food and beverage, and electronics.

19

EXECUTIVE SUMMARY – FINANCIAL RESULTS & OUTLOOK

2022 Year in review

•Sales of $33,364 million were 8% above 2021 sales of $30,793 million. Higher pricing across all geographic segments contributed 7% to sales. Cost pass-through increased sales by 6% with minimal impact on operating profit. Volume increased sales by 1%. Currency translation decreased sales by 5%, largely in EMEA and APAC. Divestitures decreased sales by 1%.

•Reported operating profit of $5,369 million was 8% above 2021. Adjusted operating profit of $7,904 million was 10% above 2021. The increase in the reported operating profit was primarily due to higher pricing, productivity initiatives and lower depreciation and amortization driven by merger related assets, which more than offset Russia-Ukraine conflict and other charges and the adverse impacts of inflation and currency in the year. The increase in adjusted operating profit increase was primarily due to higher pricing and productivity initiatives, which more than offset the adverse impacts of inflation and currency in the year.*

•Income from continuing operations of $4,147 million and diluted earnings per share from continuing operations of $8.23 increased from $3,821 million and $7.32, respectively in 2021. Adjusted income from continuing operations of $6,195 million and adjusted diluted earnings per share from continuing operations of $12.29 were 11% and 15%, respectively above 2021 adjusted amounts.*

•Cash flow from operations of $8,864 million was $861 million below 2021. The decrease was driven by higher working capital requirements, including lower inflows from contract liabilities from engineering customer advanced payments, partially offset by higher net income adjusted for non cash charges. Capital expenditures were $3,173 million; dividends paid were $2,344 million; net purchases of ordinary shares of $5,132 million; and debt borrowings, net were $4,475 million.

*A reconciliation of the adjusted amounts can be found in the "Non-GAAP Financial Measures" section in this MD&A.

2023 Outlook

Linde provides quarterly updates on operating results, material trends that may affect financial performance, and financial guidance via earnings releases and investor teleconferences. These materials are available on the company’s website, www.linde.com, but are not incorporated herein.

20

CONSOLIDATED RESULTS AND OTHER INFORMATION

The discussion that follows includes a comparison of our results of operations and liquidity and capital resources for the years ended December 31, 2022 and 2021. For the discussion comparing the years ended December 31, 2021 and 2020, refer to Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, of our Form 10-K for the year ended December 31, 2021.

The following table provides summary information for 2022 and 2021. The reported amounts are GAAP amounts from the Consolidated Statements of Income. The adjusted amounts are intended to supplement investors' understanding of the company's financial information and are not a substitute for GAAP measures.

(Millions of dollars, except per share data) Year Ended December 31, | 2022 | 2021 | Variance | ||||||||||||||

| Reported Amounts | |||||||||||||||||

| Sales | $ | 33,364 | $ | 30,793 | 8 | % | |||||||||||

| Cost of sales, exclusive of depreciation and amortization | $ | 19,450 | $ | 17,543 | 11 | % | |||||||||||

| As a percent of sales | 58.3 | % | 57.0 | % | |||||||||||||

| Selling, general and administrative | $ | 3,107 | $ | 3,189 | (3) | % | |||||||||||

| As a percent of sales | 9.3 | % | 10.4 | % | |||||||||||||

| Depreciation and amortization | $ | 4,204 | $ | 4,635 | (9) | % | |||||||||||

| Russia-Ukraine conflict and other charges (a) | $ | 1,029 | $ | 273 | — | ||||||||||||

| Operating Profit | $ | 5,369 | $ | 4,984 | 8 | % | |||||||||||

| Operating margin | 16.1 | % | 16.2 | % | |||||||||||||

| Interest expense – net | $ | 63 | $ | 77 | (18) | % | |||||||||||

| Net pension and OPEB cost (benefit), excluding service cost | $ | (237) | $ | (192) | 23 | % | |||||||||||

| Effective tax rate | 25.9 | % | 24.7 | % | |||||||||||||

| Income from equity investments | $ | 172 | $ | 119 | 45 | % | |||||||||||

| Noncontrolling interests from continuing operations | $ | (134) | $ | (135) | (1) | % | |||||||||||

| Income from continuing operations | $ | 4,147 | $ | 3,821 | 9 | % | |||||||||||

| Diluted earnings per share from continuing operations | $ | 8.23 | $ | 7.32 | 12 | % | |||||||||||

| Diluted shares outstanding | 504,038 | 521,875 | (3) | % | |||||||||||||

| Number of employees | 65,010 | 72,327 | (10) | % | |||||||||||||

| Adjusted Amounts (b) | |||||||||||||||||

| Operating profit | $ | 7,904 | $ | 7,176 | 10 | % | |||||||||||

| Operating margin | 23.7 | % | 23.3 | % | |||||||||||||

| Income from continuing operations | $ | 6,195 | $ | 5,579 | 11 | % | |||||||||||

| Diluted earnings per share from continuing operations | $ | 12.29 | $ | 10.69 | 15 | % | |||||||||||

| Other Financial Data (b) | |||||||||||||||||

| EBITDA from continuing operations | $ | 9,745 | $ | 9,738 | — | % | |||||||||||

| As percent of sales | 29.2 | % | 31.6 | % | |||||||||||||

| Adjusted EBITDA from continuing operations | $ | 10,873 | $ | 10,179 | 7 | % | |||||||||||

| As percent of sales | 32.6 | % | 33.1 | % | |||||||||||||

________________________

(a)See Note 3 to the consolidated financial statements.

(b)Adjusted amounts and Other Financial Data are non-GAAP performance measures. A reconciliation of reported amounts to adjusted amounts can be found in the "Non-GAAP Financial Measures" section of this MD&A.

21

Results of Operations

The following table provides a summary of changes in consolidated sales:

| 2022 vs. 2021 | ||||||||

| % Change | ||||||||

| Factors Contributing to Changes - Sales | ||||||||

| Volume | 1 | % | ||||||

| Price/Mix | 7 | % | ||||||

| Cost pass-through | 6 | % | ||||||

| Currency | (5) | % | ||||||

| Acquisitions/divestitures | (1) | % | ||||||

| Engineering | — | % | ||||||

| 8 | % | |||||||

2022 Compared With 2021

Sales

Linde sales increased $2,571 million, or 8%, for the 2022 year versus 2021. Higher pricing across all geographic segments contributed 7% to sales. Cost pass-through, representing the contractual billing of energy cost variances primarily to onsite customers, increased sales by 6%, with minimal impact on operating profit. Volume growth in all end markets, except healthcare, and startups increased sales by 1%. Currency translation decreased sales by 5%, largely in EMEA and APAC, driven by the weakening of the Euro, Chinese yuan, British pound and Australian dollar against the U.S. dollar. The impact of divestitures decreased sales by 1%.

Cost of sales, exclusive of depreciation and amortization

Cost of sales, exclusive of depreciation and amortization, increased $1,907 million, or 11%, for the year primarily due to inflation and higher volumes, partially offset by productivity gains and currency effects. Cost of sales, exclusive of depreciation and amortization, was 58.3% and 57.0% of sales, respectively, in 2022 compared to 2021. The increase as a percentage of sales was due primarily to higher cost pass-through to customers.

Selling, general and administrative expenses

Selling, general and administrative expense ("SG&A") decreased $82 million, from $3,189 in 2021 to $3,107 million in 2022. SG&A was 9.3% of sales in 2022 versus 10.4% in 2021. Currency impacts decreased SG&A by approximately $127 million in 2022. Excluding currency impacts, underlying SG&A increased primarily due to higher costs.

Depreciation and amortization

Reported depreciation and amortization expense decreased $431 million, or 9% versus 2021. The decrease is primarily due to lower depreciation and amortization of assets acquired in the merger and currency impacts.

On an adjusted basis, depreciation and amortization expense decreased $49 million, or 2%, versus 2021. Currency impacts decreased depreciation and amortization by $123 million in 2022. Excluding currency impacts, underlying depreciation and amortization increased including new project start ups.

Russia-Ukraine conflict and other charges

Russia-Ukraine conflict and other charges were $1,029 million and $273 million for 2022 and 2021, respectively. The charge for 2022 relates primarily to the deconsolidation and impairment of Russian subsidiaries resulting from the ongoing war in Ukraine and related sanctions recorded as of June 30, 2022. 2021 charges relate to cost reduction program and other charges, primarily severance (see Note 3 to the condensed consolidated financial statements).

On an adjusted basis, these benefits and costs have been excluded in both periods.

Operating profit

Reported operating profit increased $385 million in 2022, or 8%. On an adjusted basis, operating profit increased $728 million, or 10%, for 2022 versus 2021.

On a reported basis, operating profit increased $385 million, or 8% in 2022. The increase was primarily due to higher pricing, volumes, savings from productivity initiatives, and lower depreciation and amortization driven by merger related

22

assets. These increases more than offset the adverse impacts of inflation and currency in the year as well as the Russia-Ukraine conflict and other charges of $1,029 million. Cost reduction programs and other charges was $273 million in 2021.

On an adjusted basis, which excludes the impacts of purchase accounting as well as Russia-Ukraine conflict and other charges, operating profit increased $728 million, or 10%. Operating profit growth was driven by higher pricing, volumes and productivity initiatives, which more than offset the effects of inflation and currency during the period. A discussion of operating profit by segment is included in the segment discussion that follows.

Interest expense - net

Reported interest expense – net in 2022 decreased $14 million, or 18%, versus 2021. On an adjusted basis interest expense decreased $32 million, or 25% in 2022 as compared to 2021.

On both a reported and adjusted basis, the decrease year over year was driven primarily by higher interest income on cash deposits, partially offset by higher borrowing costs on short-term debt.

Net pension and OPEB cost (benefit), excluding service cost

Reported net pension and OPEB cost (benefit), excluding service cost were benefits of $237 million and $192 million in 2022 and 2021, respectively. The increase in benefit primarily relates to lower amortization of deferred losses, partially offset by higher interest cost reflective of the higher discount rate environment year-over-year (see Note 16 to the consolidated financial statements).

Effective tax rate

The reported effective tax rate ("ETR") for 2022 was 25.9% versus 24.7% in 2021. The increase in the rate is primarily related to the net tax expense resulting from the deconsolidation and impairment of the company’s business in Russia in 2022. 2021 included a deferred income tax charge related to the revaluation of net deferred tax liabilities for a tax rate increase in the United Kingdom (see Note 5 to the consolidated financial statements).

On an adjusted basis, the ETR for 2022 was 24.2% versus 24.1% in 2021.

Income from equity investments

Reported income from equity investments for 2022 was $172 million as compared to $119 million in 2021. On an adjusted basis, income from equity investments for 2022 was $247 million versus $231 million in 2021.

On a reported basis, the year-over-year increase in income from equity investments was due to a $35 million impairment charge taken in the third quarter of 2021 related to a joint venture in the APAC segment.

On an adjusted basis, the year-over-year increase in income from equity investments was primarily driven by the overall performance of investments in APAC.

Noncontrolling interests from continuing operations

At December 31, 2022, noncontrolling interests from continuing operations consisted primarily of noncontrolling shareholders’ investments in APAC (primarily in China).

Reported noncontrolling interests from continuing operations decreased $1 million, from $135 million in 2021 to $134 million in 2022.

Adjusted noncontrolling interests from continuing operations increased $6 million in 2022 as compared to 2021.

Income from continuing operations

Reported income from continuing operations increased $326 million, or 9%. On an adjusted basis, which excludes the impacts of purchase accounting and Russia-Ukraine conflict and other charges, income from continuing operations increased $616 million, or 11%, in 2022 versus 2021. On both a reported and adjusted basis, the increase was driven by higher operating profit.

Diluted earnings per share from continuing operations