UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED | |||||||||||

| or | |||||||||||

| TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||||||

Commission File Number: 001-39933

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |||||||

| (Address of principal executive office) | (Zip Code) | (Registrant’s telephone number, Including area code) | ||||||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. o Yes x No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | ||||||||

x | Smaller Reporting Company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that audited the registrant's financial statements. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). o Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter on June 30, 2022 was $40,366,306 .

As of March 16, 2023, the registrant had 10,771,991 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| Item No. | Page No. | |||||||

| Item 16. | ||||||||

F-1 | ||||||||

2

Cautionary Information about Forward-Looking Statements

This Annual Report on Form 10-K ("Form 10-K" or this "Report") contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act") and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), including statements related to: future events; challenges we may face; growth strategy; expansion and future operations; the ability to recognize backlog as revenue; financial position; estimated or projected revenues, losses, costs, gross profit, earnings or other financial items; business strategy, prospects, plans and objectives of management; anticipated or pending investigations, legal claims, proceedings or litigation that may involve or affect us; implementation of ESG initiatives; industry-specific trends, events or regulations and the impact of those trends, events and regulations on us or our financial performance; and updates to regulations and the impact of those regulations on us. All statements other than statements of historical fact may be forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as "seek," "anticipate," "plan," "continue," "estimate," "expect," "may," "will," "project," "predict," "potential," "targeting," "intend," "could," "might," "should," "believe," "outlook" and variations of such words or their negative and similar expressions. Forward-looking statements should not be read as a guarantee of future performance or results and may not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on management’s belief, based on currently available information, as to the outcome and timing of future events

Important factors known to us that could cause such material differences are identified in this Report, including the factors described in Part I, Item 1A, "Risk Factors," and other cautionary statements described in this Report on Form 10-K. These factors are not necessarily all of the important factors that could cause actual results or events to differ materially from those expressed in the forward-looking statements. Other unknown or unpredictable factors could also cause actual results or events to differ materially from those expressed in the forward-looking statements. We undertake no obligation to correct or update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any future disclosures we make on related subjects in future reports to the Securities and Exchange Commission ("SEC").

PART I

ITEM 1. BUSINESS

Background

urban-gro, Inc. (together with its wholly owned subsidiaries, collectively "urban-gro," "we," "us," or "the Company") was originally formed on March 20, 2014, as a Colorado limited liability company. In March 2017, we converted to a Colorado corporation and exchanged shares of our common stock for every member interest issued and outstanding on the date of conversion. On October 29, 2020, we reincorporated as a Delaware corporation. On December 31, 2020, we effected a 1-for-6 reverse stock split with respect to our common stock. All information in this Report gives effect to this reverse stock split, including restating prior period reported amounts. On February 12, 2021, we completed an uplisting to the Nasdaq Stock Market under the ticker symbol UGRO.

Overview

urban-gro is an integrated professional services and construction design-build firm. Our business focuses primarily on providing fee-based knowledge-based services as well as the value-added reselling of equipment. We derive income from our ability to generate revenue from our clients through the billing of our employees’ time spent on client projects. We offer value-added architectural, engineering, systems procurement and integration, and construction design-build solutions to customers operating in the controlled environment agriculture ("CEA") and industrial and other commercial ("Commercial") sectors. Our evolution, both organically and through the acquisition of engineering, architecture, and construction management firms has enabled us to successfully diversify into the commercial sectors of the clients we serve, as well as the capabilities we offer, which we believe has helped insulate our business from any one sector. Even with this successful diversification, our main focus and value-add has always been and remains in providing solutions to our CEA clients, where we have experience and expertise in designing, engineering, building, and integrating complex environmental equipment systems into indoor CEA cultivation and retail facilities, and then providing ongoing maintenance, training, and support services to those same facilities.

We aim to work with our clients from inception of their project in a way that provides value throughout the life of their facility. Clients, regardless of sector they are in, engage us to deliver their vision because of our experience and expertise, and because our integrated, design-build solutions offer a value-add approach to design, engineering, procurement, construction-management, construction, and equipment integration, providing a single point of accountability across all aspects of a project.

3

For our CEA clients in particular, we create high-performance indoor cultivation facilities to grow specialty crops, including cannabis as well as produce such as leafy greens, vegetables, herbs and berries. We also provide design-build solutions for our CEA clients' retail facilities. We help our clients achieve operational efficiency and economic advantages through a full spectrum of professional services and programs focused on facility optimization and environmental health which establish facilities that allow clients to manage, operate and perform at the highest level throughout their entire cultivation lifecycle once they are up and running. For these CEA clients, our team provides services to meet the most stringent regulatory environments, whether they are energy efficiency goals, Good Agricultural and Collection Practices (GACP), or Good Manufacturing Practice ("GMP") and/or European Medicine Agency EU GMP ("EU/GMP") certification.

While we have successfully diversified our target markets across several commercial sectors, the majority of our clients are commercial CEA cultivators. We believe a key differentiation point that clients value is the depth of our employees’ and Company’s experience. As of December 31, 2022, we employed 152 full time employees, approximately two-thirds of which are considered experts in their areas of focus. Our team includes Designers (Architects, Interior Designers, Cultivation Space Planners), Engineers (Mechanical, Electrical, Plumbing, Controls, and Fire Protection), Construction Managers (Project Managers and Supervisors), and horticulturists. As a company, we have worked on over 1000 CEA projects, and believe that the experience of our team and Company provides clients with the confidence that will proactively keep them from making common costly mistakes during the design and build process that would impact operational stages. Our expertise translates into clients saving time, money, and resources through expertise that they can leverage without having to add headcount to their own operations. We provide this experience in addition to offering a platform of the highest quality equipment systems that can be integrated holistically into our clients’ facilities.

Our Solutions

Since commencing business in March 2014, we have expanded our ongoing operations across North America and Europe while diversifying our services offerings organically and through acquisitions into full design-build solutions by adding design, engineering, construction, and construction-management services, introducing new equipment solutions, products and services, and successfully diversifying into several additional commercial sectors beyond cannabis-focused CEA, including produce-focused CEA; or vertical farming, healthcare, industrial, commercial packaged goods ("CPG"), and retail. We are a trusted partner and adviser to our clients and provide value to our clients regardless of the sector in which they sit or solution for which they are utilizing us.

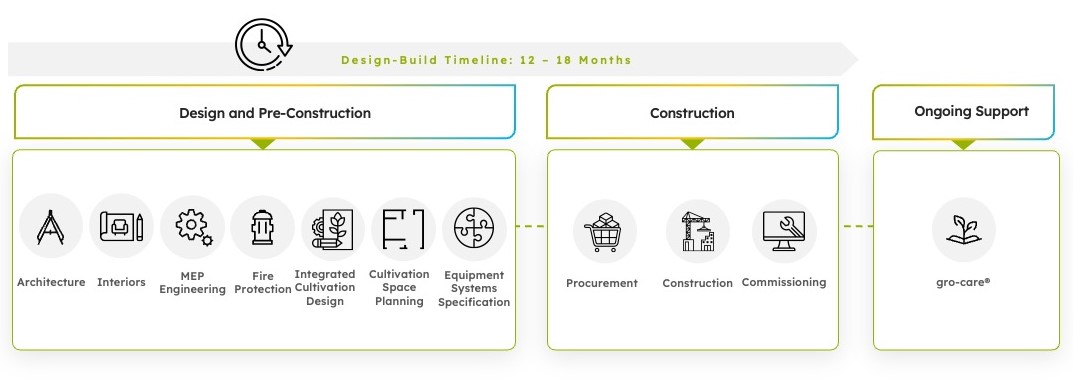

As is detailed in the Project Delivery Comparison chart below, in the CEA sector, the advantages of the urban-gro design-build model vs the traditional owner-contracted model are clear. There is a single responsible party for our clients' needs from conception through operational start. This results in greater efficiencies throughout the design-build process and a faster speed to launch. Additionally, our experience and expertise within our sectors help to prevent costly mistakes for our clients.

4

Outlined below is an example of a complete end-to-end design-build project that demonstrates how we provide value to our clients over time.

Our design-build solution, when focused on indoor CEA, offers an integrated suite of in-house services and equipment systems that generally fall within the following categories:

•Service Solutions:

•Architectural Design, Engineering, and Construction Services – A comprehensive collection of services including:

i.Pre-Construction Services

ii.Cultivation Space Programming ("CSP")

iii.Architectural Design and Interior Design

iv.Engineering

v.Integrated Cultivation Design ("ICD")

vi.Owner's Representative Services / Construction Management ("CM")

vii.General Contracting ("GC")

•Additional Service Offerings including:

i.Facility and Equipment Commissioning Services

ii.gro-care® Crop and Asset Protection Services including Training Services, Equipment Maintenance Services, Asset Protection Program, and an Interactive Online Operating Support System ("OSS") for gro-care® and client document delivery and project management

iii.Property Condition Assessment ("PCA")

5

•Integrated Equipment Systems Solutions:

•Design, Source, and Integration of Complex Environmental Equipment Systems including Heating, Ventilation, and Air Conditioning ("HVAC") solutions, Environmental Controls, Fertigation, and Irrigation Distribution

•Value-Added Reselling ("VAR") of Cultivation Equipment Systems

•Strategic Vendor Relationships with Premier Manufacturers

Service Solutions

Architectural Design, Engineering, and Construction Services

We generate revenue by providing our clients with design-build service offerings that include architectural, interior, and engineering design, construction and construction management, as well as services for the operational stages of the facility. Our in-house architectural, interior design, engineering, construction and cultivation design services integrate design with pre-construction services and thereby reduce project schedule and capital investments.

Pre-Construction Services include providing a forecast summary of what it will take to get a high-performance facility built, giving initial indication and detailed analysis of budget, timeline/schedule, and potential large decision impacts including value analysis and value engineering options. The integration of Pre-Construction Services can expedite project completion, lower initial project costs, and help reduce costly change orders.

CSP is an early-stage engagement with stakeholders that provides an optimized basis of design including the interaction of people, plants, and processes. The output of CSP provides an optimized analysis of spatial needs based on stipulated criteria and can accelerate construction and regulatory approval paths, save stakeholders money and time, and enable a process-driven decision-making approach.

Architectural Design is the implementation of a defined process from development of vision to built environment. Architecture includes the integration and coordination of all project required disciplines such as civil, landscape, structural, mechanical, plumbing and electrical engineering, fire protection, security, interior design, and other specialty disciplines. Our services are built around an integrated design process focused on the collaborative development of client-driven solutions. Specific to the CEA industry, our team’s understanding of the relationship between people, plants, and process helps clients maximize profits and efficiencies while minimizing capital investments, and operational and maintenance costs.

Interior Design involves branding and development of the interior aesthetic vision. Our collaborative and integrated approach from our award-winning team begins with inspiration boards focused on understanding the client’s aesthetic desires. Interior design is holistic and thereby includes all aspects of the building interiors from full branding to the selection and design of all finishes and interior systems. Common discussions beyond aesthetics include the cost, durability, and maintainability of systems presented.

Mechanical, Electrical, and Plumbing ("MEP") engineering design focuses on the entire building, not just the cultivation space, which in turn eliminates the "gap" between cultivation systems and the building systems. We provide engineered construction contract documents for mechanical, HVAC, plumbing and electrical systems required for the building permits necessary to obtain a Certificate of Occupancy. Our team evaluates client capabilities, needs, desires, and budget in development of recommended systems through a client-focused collaborative process culminating in the delivery of high-performance and low-maintenance systems.

ICD creates cultivation space-focused design layouts that integrate climate control, fertigation, benching, air flow, and lighting. Our ICD team’s deep understanding of cultivation systems provides the foundation for ensuring optimal space utilization as they utilize an integrated and collaborative design process focused on understanding, vetting, and implementing the client’s vision. Products utilized in the ICD’s basis-of-design ensures the integration of high-quality systems and product performance. These detailed ICD plans are taken through the construction document stage and are leveraged by our clients to efficiently solicit contractor bids.

Construction and Construction Management provides all the additional necessary parts to deliver our clients' projects, from the initial estimate and bid process, to subcontractor selection, and management of all construction details. Our skilled project managers, specialized within our clients' sectors, maintain knowledgeable open lines of communication with both clients, onsite superintendents, and internal and external construction partners to manage expectations, costs and schedules.

6

Our Additional Service Offerings

Our Facility and Equipment Commissioning Services provide a cultivation-level view of the complex system made up by each piece of equipment and ensures systems are running properly. Many of the current service options available to CEA cultivation clients are isolated to vendors providing post-sale service for a single piece of equipment. Our team confirms contractors and specialty trades are installing systems to the design intent allowing for rapid installation, continuous process improvement, and increased revenue for our clients.

gro-care® is a highly differentiated service offering that provides a combination of CEA cultivation facility commissioning and an asset protection program through training, equipment maintenance, on-demand support, standard operating procedures ("SOP"), and a client-specific OSS that acts as an online hub for clients’ ongoing services. Combined, this solution focuses on the troubleshooting, tuning, and support of a myriad of cultivation systems and equipment while further providing guidance for client interactions with tradespeople working on HVAC, electrical, and plumbing in the facility on an ongoing basis.

Our PCA offering provides value to all clients regardless of sector, but also adds unique value for our clients in the CEA sector. PCA includes researching historical records of the building as related to code issues, field documentation of existing conditions, a report of findings with materials systems categorized by condition, and a capital expenditure report for correction of any deficiencies. For our clients in the CEA sector, our PCA offering provides analysis of components specifically within CEA facilities, both with an eye towards critical cultivation and manufacturing systems as well as helping clients understand a facility's ability to meet any state regulations that may have evolved such as adherence to standards such as Current Good Manufacturing Practices ("cGMP"), EU-GMP, and/or World Health Organization guidelines on GACP. PCA provides necessary data for clients to understand options for optimizing operational performance, understanding deficiencies, and property preparing for necessary capital expenditures.

Integrated Equipment Solutions

While our engineers play an integral part in the design of most of the complex equipment systems that are then integrated into a CEA facility, we also provide consultative reselling of more common solutions that we integrate into the overall design. For CEA, the environmental goal is to maintain a stable and consistent vapor pressure deficit ("VPD") according to the client’s priorities through environmental control of relative humidity and temperature during all stages of growth. There are four main variables in CEA that affect plant growth (and can impact VPD): (i) water and nutrients; (ii) environmental control; (iii) CO2; and (iv) lighting. The complex equipment systems that we design and procure for our clients play an important role in helping control and maintain the cultivation facility's environment for plants.

Design, Source, and Integration of Complex Environmental Equipment Systems

Complex Environment Systems for CEA include environmental controls, fertigation and irrigation distribution, a complete line of water treatment and wastewater reclamation systems, and HVAC equipment systems.

As related to systems and equipment, the most significant and influential variable within a CEA facility is the ability to control and maintain the cultivation environment. This is accomplished through the integration of mechanical systems (HVAC), lighting, air movement systems, irrigation systems, and environmental controls. Maintaining a consistent desired temperature and humidity level within the cultivation spaces ensures less stress on plants. urban-gro designs these systems to fit within our clients' budgets and provides our clients' facilities a more stable environment to maximize plant health and yields, minimize crop loss, minimize utility costs, save on capital equipment, and maximize sustainability.

Value-Added Reselling of Cultivation Equipment Systems

We act as an experienced vendor providing VAR to our clients when selling vetted best-in-class commercial horticulture lighting solutions, rolling and automated container benching systems, specialty fans, fertigation/irrigation systems, environmental control systems, and microbial mitigation and odor reduction systems. The acquired knowledge of how each of these systems work in combination with and in tangent to the overall ecosystem is a significant benefit that our engineers and product experts offer to our clients. Not only are many competing products reviewed in each category with the intention of vetting the best solution, but we also continually search out and review competing technologies to ensure that only the best-in-class equipment systems are integrated into our projects. As such, we believe it will be imperative to maintain and to continue to develop close relationships with both existing and new leading technology and manufacturing providers.

Today, we typically do not sell any cultivation equipment systems individually as a one-time sale. The majority of equipment sales are sold as part of a larger all-encompassing project solution that spans over a 12 to 24 month period and includes design, engineering, and the sale of both custom complex and more standard equipment systems.

7

Strategic Vendor Relationships with Premier Manufacturers

We work closely with leading technology and manufacturing providers to deliver an integrated solution designed to achieve the stated objectives of our clients. We pride ourselves as being equipment agnostic – meaning we do not have allegiances to any single manufacturer – we offer the solution that will best meet the design and budget constraints of our clients and design, engineer, and integrate whatever equipment fits the client's needs.

Revenues and Gross Profit Margins

As our business has evolved and diversified into design-build offerings, our margin profiles have changed. Professional service revenues for engineering design services contracts can be hundreds of thousands of dollars, depending on the spectrum of services desired by the client and the size of the facility. Construction design-build contracts can run in the tens of millions of dollars depending on the overall size of the facility. Equipment revenues for customized equipment systems can be millions of dollars, depending on the size of the cultivation facilities, the complexity and types of systems purchased by the client, and the number of systems purchased by the client. Sales of other products are typically of a recurring nature each month to a client and can be in the tens of thousands of dollars.

Targeted gross profit margins for each of the Company’s revenue categories are as follows:

•Professional services - greater than forty percent;

•Construction design-build services - greater than six percent;

•Customized equipment systems - greater than ten percent; and

•Other products revenues - greater than fifteen percent.

Gross profit margins are highly dependent on the complexity and size of the project.

Our Clients

We primarily market and sell our solutions to clients in the CEA and Commercial sectors. In the CEA sector, our clients include operators and facilitators in both the cannabis and produce markets in the United States, Canada, and Europe. In the Commercial sector, we work with leading food and beverage consumer packaged goods companies in the United States, and clients in healthcare, higher education, and hospitality.

Environment, Social, and Governance

We are continuously striving to develop, maintain, and build upon our environmental, social, and governance ("ESG") practices and credentials. We greatly value ESG considerations as they enable us to better identify material risks and growth potential, leading to better-informed decisions and business outcomes with the goal of maximizing value creation for our shareholders.

To this end, the urban-gro Board of Directors ("Board") recently established an ESG committee as part of our Board. In addition, we have engaged with the services of an independent consulting solution to help educate us and guide us as we develop our ESG roadmap and work towards establishing our priorities in this space. While we engage in those activities, we continue to support ESG in the following ways:

•Environment: As a professional services design-build firm, and a leader in the CEA space, urban-gro has a continuing commitment to Environmental Sustainability in order to help form a better, healthier world for our and future generations. In general, we are aligned with industry best practices around CEA, which include a focus on water conservation and reuse, reducing the carbon footprint of the production and distribution process, and increasing the efficiency of harvests. Utilizing the expertise of our employees, we have assisted in the creation of over 500 CEA facilities worldwide and counting with Leadership in Energy and Environmental Design ("LEED") certified and/or GMP facilities in a variety of commercial sectors focused on reducing waste, water consumption, and carbon consumption. We believe we present a strong opportunity for investors looking for companies focused on providing a more sustainable world for generations to come. As technological advancement continues, we plan to work with our partners to create even more earth-friendly cultivation sites within the CEA sector and projects within other sectors. We are actively exploring opportunities to lower energy use for our customers including but not limited to: active energy management, efficiency measures in HVAC, and innovations in lighting.

8

•Social: We strive to hire and promote from underrepresented communities in order to become a diverse organization which we believe will bring strength and value to our organization and our shareholders. In addition, we currently are members of and work with the following organizations:

◦Charities: We have been a supporter of Teens for Food Justice ("TFFJ") which is catalyzing a youth-led movement to end food insecurity in one generation through high-capacity, school-based hydroponic farming. We have helped build out and commission their first in-classroom vertical farm in the Denver area located near our headquarters and have committed our team’s time to mentoring students and helping further TFFJ’s goals in addition to working with them on future vertical farms.

◦Associations and Organizations: We are currently members of good standing in several industry organizations and trade groups such as the New England Healthcare Engineer Society ("NEHES"), the Georgia City-County Management Association ("GCMA"), The Georgia Chapter of APPA ("GAPPA"), American Hort, Association for Vertical Farming, the American Society of Heating, Refrigerating, and Air-Conditioning Engineers ("ASHRAE"), the National Cannabis Industry Association ("NCIA") and the National Cannabis Roundtable ("NCR"). Those last two groups, as a part of their work and being born out of the cannabis industry, are dedicated to sensible regulation, criminal justice reform, social equity and community reinvestment.

•Governance: We have several approaches we utilize to guide us for a successful governance program to ensure that our stakeholders’ best interests are acted upon:

◦Board Composition: We have a strong and diverse Board made up of leaders from a variety of fields that help guide our overall efforts. We publish our Board Diversity Matrix on our website at ir.urban-gro.com as well as within our proxy materials each year.

◦Board Committees: We currently utilize four Board committees:

•The Audit Committee which is focused on internal controls, risk management, and multi-discipline oversight enabled by its charter and structure;

▪The Compensation Committee which is focused on compensation principles, policies, and practices for all employees;

▪The Nominating and Corporate Governance Committee which oversees the Company's corporate governance practices and procedures; and

▪The Environmental, Social, and Governance Committee, recently created, which is overseeing the Company's approach to ESG practices and procedures.

◦Guiding Policies: In addition to the above committee charters, we have a Code of Business Ethics and Conduct as well as a Whistleblower Policy which can be found on our website.

◦Cybersecurity: We utilize external consultants to help inform cybersecurity best practices, employ cybersecurity software that is preventative and detective for our infrastructure, and require and provide consistent ongoing training for all employees.

Growth Strategy

Our employees and the application of their acquired knowledge are our most valuable assets as an organization. Our growth strategy involves leveraging this considerable strength as a basis for growth across three pillars of focus and exploration. These three pillars allow us to continue to provide value to our current and future clients:

1.Leverage our Sector Diversification and In-House Capability Offerings

2.Focus on Design-Build Solution

3.Expansion of Geographical Reach

9

1. Leverage our Sector Diversification and In-House Capability Offerings

Our vision is to be the global leading provider for purpose-built turnkey indoor CEA facilities. To that end, we have and continue to seek to diversify our service capabilities to provide value to our clients through acting as a single point of responsibility in our turnkey design-build, approach. While we will continue to expand our services organically, we began this journey through the acquisition of engineering, architecture, and construction management firms over the last 18-month period. This in-house service capability diversification also brought with it a diversified client base that included clients from sectors outside of CEA. We expect to continue to compete successfully in all of these sectors as we believe it helps us attract the best talent, weather the downturns of any one sector, and continue to find growth and future returns for our shareholders.

We believe that acting as a single point of responsibility as a provider of turnkey design-build solutions, especially one with the depth and breadth of experience within all sectors that we've served, we can get our clients to market more quickly and more efficiently than others.

We intend to continue to leverage all our service capabilities within our design-build delivery model, across sectors, to grow the services and value we are providing to our clients. As an example, some clients may currently only be engaged with us for architectural design - we plan to leverage our in-house model and take advantage of every opportunity to cross sell our other services such as engineering; or construction management or general contracting, to provide further value to our clients and grow our revenues and margin dollars.

2. Focus on Design-Build Solution

As written previously, through both organic and inorganic means, we have diversified our in-house service capabilities so that we are able to provide full turnkey design-build solutions to our clients. These design-build projects allow us to engage with a client at the conception of a project and act as a single point of responsibility to provide value throughout and beyond the project lifecycle. These design-build projects are also much larger from a revenue and project complexity perspective - instead of working on 100s of projects, our goal will be to grow through working on a smaller number of projects of a much larger size, allowing us to capture greater revenue and more margin dollars and overall, provide greater value to our clients. We expect these larger projects will also provide us with the foresight to more accurately forecast our future quarterly business performance.

3. Expansion of Geographical Reach

While continuing to focus on building out our solution set and expanding our client base in all sectors, and more specifically establishing our end-to-end solution as the industry standard for CEA indoor cultivation in the U.S. market, we also plan to continue to expand our reach within Europe.

After completing approximately 18 months of due diligence in the European market, in Q3 of 2022, we hired a Netherlands-based Managing Director, with experience and expertise in horticulture and pre-harvest and post-harvest equipment automation, to lead our Europe, Middle East, and Africa ("EMEA") market expansion. After opening an office in Dordrecht, Netherlands shortly thereafter, we began to build our European team, including investing in hiring in-market as well as relocating a previously U.S. based Company Vice President with vast experience in CEA cultivation design to the region.

We are focused on securing and providing value to clients in the CEA sector, and continue to develop and iterate on our marketing and outreach plans, including taking part in trade shows, speaking engagements, and business development travel to areas in Europe with existing clients as well as other developing markets. We have thus far signed several engagements with CEA clients in multiple countries and look to continue our growth through this geographic expansion.

Our Competition

We believe that our experience and expertise combined with our complex end-to-end design-build solutions places us as a growing leader in the indoor-CEA sector. Within that CEA sector, we do face competition from companies that offer some, but not all, portions of an all-encompassing design-build facility solution. We compete for projects with other smaller and mid-sized companies that focus solely on architectural and interior design, engineering, construction, or product sales. For services, we see these competitors as offering similar specific area solutions, though not integrated nor as in depth on fertigation design. For product sales, we currently view our competition to be focused on predominantly commodity "off-the-shelf" items like lighting and other cultivation staple products, both pre-startup and post-startup. This competition comes from traditional wholesale horticulture dealers, online retailers, and some manufacturers who sell direct.

10

Greenhouse manufacturers and European systems integrators may increasingly seek to offer comprehensive product and service solutions to compete with our integrated solution, but they are primarily focused on the greenhouse industry, and not on indoor-CEA facilities. European systems integrators in particular are experienced and have a strong operating history in traditional horticulture and provide specialized, intensive, and large-scale solutions that revolve around greenhouse projects. Instead of competing with these integrators, we find ourselves working with them and combining synergies to work on projects together.

For our clients from non-CEA sectors such as Industrial, Food and Beverage CPG, Healthcare, Education, and Civic, we believe we face more competition from those who offer some, but not all, portions of a design-build facility solution but also those who employ the design-build methodology. We believe we compete successfully here because while the overall design-build projects come at higher revenues and margin dollars, the projects from non-CEA on which we typically engage are of a size that we believe is smaller than our design-build competitors are set up to take on. In addition, the majority of our non-CEA client base is developed from long-term relationships that provide our Company with a strategic advantage.

Regulation

As it relates to our business conducted in the legalized cannabis-focused CEA segment, the regulations for each region are detailed as follows.

U.S. Regulations

While we do not generate any revenue from the direct sale of cannabis products, we have historically, and may continue to, offer our solutions to indoor cultivators that are engaged in various aspects of the cannabis industry. Tetrahydrocannabinol ("THC"), one of the main active chemicals in cannabis, is a Schedule I controlled substance and is illegal under federal law. Even in those states in which the use of cannabis has been legalized, its use remains a violation of federal laws.

A Schedule I controlled substance is defined as a substance that has no currently accepted medical use in the United States, a lack of safety for use under medical supervision and a high potential for abuse. The Department of Justice defines Schedule I controlled substances as "the most dangerous drugs of all the drug schedules with potentially severe psychological or physical dependence." If the federal government decides to enforce the Controlled Substances Act with respect to cannabis, persons that are charged with distributing, possessing with intent to distribute, or growing cannabis could be subject to fines and terms of imprisonment, the maximum being life imprisonment and a $50 million fine. Any such change in the federal government’s enforcement of current federal laws could cause significant financial damage to us. While we do not intend to harvest, distribute or sell cannabis, we may be irreparably harmed by a change in enforcement by the federal or state governments.

Since the use of THC is illegal under federal law, most federally chartered banks will not accept deposit funds from businesses involved with cannabis. Consequently, businesses involved in the cannabis industry generally bank with state-chartered banks and credit unions who provide banking to the industry.

Although cultivation and distribution of cannabis for medical use is permitted in many states, subject to compliance with applicable state and local laws, rules, and regulations, THC is illegal under federal law. Strict enforcement of federal law regarding cannabis could result in material adverse effects on our business and revenues. Though the cultivation and distribution of cannabis containing THC remains illegal under federal law, H.R. 83, enacted by Congress on December 16, 2014, provides that none of the funds made available to the DOJ pursuant to the 2015 Consolidated and Further Continuing Appropriations Act may be used to prevent states from implementing their own laws that authorize the use, distribution, possession, or cultivation of medical cannabis. While this appropriations measure has remained in effect from 2016 through 2022, continued re-authorization cannot be guaranteed. If this appropriations rider is no longer in effect, the risk of federal enforcement and override of state cannabis laws would increase. However, state laws do not supersede the prohibitions set forth in the federal drug laws.

In order to participate in either the medical or adult use sides of the cannabis industry, all businesses must obtain licenses from the state and local jurisdictions. In addition, in most jurisdictions, all owners and employees must obtain an occupational license to be permitted to own or work in a facility. Applicants for licenses undergo a background investigation, including a criminal record check for all owners and employees.

Laws and regulations affecting the medical cannabis industry are constantly changing, which could detrimentally affect our existing and proposed operations. Local, state and federal medical cannabis laws and regulations are broad in scope and subject to evolving interpretations, which could require us to incur substantial costs associated with compliance or alter our business plan. In addition, violations of these laws, or allegations of such violations, could disrupt our business and result in a material adverse effect on our operations. Regulations may be enacted in the future that may be directly applicable to our business. We cannot predict the nature of any future laws, regulations, interpretations or applications, nor can we determine what effect additional governmental regulations or administrative policies and procedures, when and if promulgated, could have on our business.

11

Canadian Regulations

Summary of the Cannabis Act

In 2001, Canada began the legislative path towards the eventual legalization and regulation of recreational and medical cannabis. The laws in Canada have been revised since then and in 2018, the Cannabis Act came into effect and legalized adult recreational use of cannabis across Canada. The Cannabis Act regulates the production, distribution and sale of cannabis and related oil extracts in Canada for both recreational and medical purposes. Under the Cannabis Act, Canadians who are authorized by their health care practitioner to use medical cannabis have the option of purchasing cannabis from one of the producers licensed by Health Canada and are also able to register with Health Canada to produce a limited amount of cannabis for their own medical purposes or to designate a registered individual to produce cannabis on their behalf for such purposes.

Pursuant to the Cannabis Act, subject to provincial regulations, individuals over the age of 18 are able to purchase fresh cannabis, dried cannabis, cannabis oil, and cannabis plants or seeds and are able to legally possess up to 30 grams of dried cannabis, or the equivalent amount in fresh cannabis or cannabis oil. The Cannabis Act also permits households to grow a maximum of four cannabis plants. In addition, the Cannabis Act provides provincial and municipal governments the authority to prescribe regulations regarding retail and distribution, as well as the ability to alter some of the existing baseline requirements of the Cannabis Act, such as increasing the minimum age for purchase and consumption.

Provincial and territorial governments in Canada have made varying announcements on the proposed regulatory regimes for the distribution and sale of cannabis for adult-use purposes. For example, Québec, New Brunswick, Nova Scotia, Prince Edward Island, Yukon and the Northwest Territories have chosen the government-regulated model for distribution, whereas Saskatchewan and Newfoundland and Labrador have opted for a private sector approach. Alberta, Ontario, Manitoba, Nunavut and British Columbia, have announced plans to pursue a hybrid approach of public and private sale and distribution.

In connection with this framework for regulating cannabis in Canada, the federal government introduced new penalties under its criminal code, including penalties for the illegal sale of cannabis, possession of cannabis over the prescribed limit, and production of cannabis beyond personal cultivation limits.

In 2018, the Canadian federal government published new regulations and amended existing regulations to support the Cannabis Act. These regulations outline the rules for the legal cultivation, processing, research, analytical testing, distribution, sale, importation and exportation of cannabis and hemp in Canada, including the various classes of licenses that can be granted, and set standards for cannabis and hemp products. They also include stringent security requirements for all federally licensed production sites. The regulations maintain a distinct system for access to cannabis.

Intellectual Property

The success of our business depends, in part, on our ability to maintain and protect our proprietary technologies, information, processes and know-how. We rely primarily on patent, trademark, copyright and trade secret laws in the U.S. and similar laws in other countries, confidentiality agreements and procedures and other contractual arrangements to protect our technology and confidential information. Our patents are limited to certain sensors that we obtain from third party manufacturers that do not contribute materially to our sales or profitability. Our trademarks are solely for branding purposes, although we no longer sell any goods or services under the Soleil brand. As of the date of this Report, the following summarizes the status of our registrations, pending applications, and issued U.S. patents:

12

Trademarks

We have received the following trademark registrations:

| Trademark | Jurisdiction | Registration Number | Registration Date | Status | ||||||||||||||||||||||

| URBAN-GRO | United States | 4618322 | October 07, 2014 | Registered | ||||||||||||||||||||||

| URBAN-GRO | United Kingdom | 3266415 | January 19, 2018 | Registered | ||||||||||||||||||||||

| URBAN-GRO | European Union | 017391806 | October 31, 2018 | Registered | ||||||||||||||||||||||

| URBAN-GRO | WIPO | 1548013 | July 08, 2020 | Registered | ||||||||||||||||||||||

| URBAN-GRO | United Kingdom | UK0081548013 | July 08, 2020 | Registered | ||||||||||||||||||||||

| URBAN-GRO | Canada (Madrid) | A0098111 | July 08, 2020 | Registered | ||||||||||||||||||||||

| URBAN-GRO | European Union (Madrid) | A0098111 | July 08, 2020 | Registered | ||||||||||||||||||||||

| URBAN-GRO | United States | 97213742 | February 7, 2023 | Registered | ||||||||||||||||||||||

| SOLEIL | United States | 5209707 | May 23, 2017 | Registered | ||||||||||||||||||||||

| SOLEIL | United Kingdom | 3266410 | March 09, 2018 | Registered | ||||||||||||||||||||||

| SOLEIL | Canada | 1083969 | October 07, 2020 | Registered | ||||||||||||||||||||||

| SOLEIL | European Union | 017391781 | September 11, 2018 | Registered | ||||||||||||||||||||||

| SOLEIL | United Kingdom | UK00917391781 | September 08, 2018 | Registered | ||||||||||||||||||||||

| OPTI-DURA | United States | 5770091 | June 04, 2019 | Registered | ||||||||||||||||||||||

| OPTI-DURA | Canada | TMA1070145 | January 20, 2020 | Registered | ||||||||||||||||||||||

| GRO-CARE | European Union | 1560748 | August 24, 2020 | Registered | ||||||||||||||||||||||

| GRO-CARE | European Union | 017391806 | October 29, 2019 | Registered | ||||||||||||||||||||||

| GRO-CARE | United Kingdom | UK00917391806 | October 29, 2018 | Registered | ||||||||||||||||||||||

| GRO-CARE | Canada (Madrid) | A0099548 | August 24, 2020 | Registered | ||||||||||||||||||||||

| GRO-CARE | WIPO | A0099548 | August 24, 2020 | Registered | ||||||||||||||||||||||

We have applied for and are awaiting receipt of the following trademark registrations:

| Trademark | Jurisdiction | Application Number | Filing Date | Status | ||||||||||||||||||||||

| URBAN-GRO | Canada | 1930075 | November 13, 2018 | Pending | ||||||||||||||||||||||

| URBAN-GRO | United States | 88898690 | May 03, 2020 | Pending | ||||||||||||||||||||||

| URBAN-GRO | United States | 97213778 | January 11, 2022 | Pending | ||||||||||||||||||||||

| GRO-CARE | United States | 88898692 | May 03, 2020 | Pending | ||||||||||||||||||||||

Patents

| Title | Jurisdiction | Application Number | Filing Date | Patent Number and Issue Date | Status | |||||||||||||||||||||||||||

| Sensor bus architecture for modular sensor systems | United States | 15/626,085 | June 17, 2017 | 10,499,123 (December 3, 2019) | Issued Expire in 2037 | |||||||||||||||||||||||||||

| Modular sensor architecture for soil and water analysis at various depths from the surface | United States | 15/626,079 | June 17, 2017 | 10,405,069 (September 3, 2019) | Issued Expire in 2037 | |||||||||||||||||||||||||||

| Modular sensor architecture for soil and water analysis at various depths from the surface | United States | 16/519,800 | July 23, 2019 | 10,955,402 (March 23, 2021) | Issued Expire in 2037 | |||||||||||||||||||||||||||

13

We rely on trade secret protection and confidentiality agreements to safeguard our interests with respect to proprietary know-how that is not patentable and processes for which patents are difficult to enforce. We believe that many elements of our design and engineering processes involve proprietary know-how, technology or data that are not covered by patents or patent applications, including technical processes, test equipment designs, algorithms and procedures.

Our policy is for our employees to enter into confidentiality and proprietary information agreements with us to address intellectual property protection issues and require our employees to assign to us all of the inventions, designs and technologies they develop during the course of employment with us. However, we might not have entered into such agreements with all applicable personnel, and such agreements might not be self-executing. Moreover, such individuals could breach the terms of such agreements.

We attempt to protect our intellectual property via the deployment of non-disclosure agreements with both prospective clients and business partners as well as licensees; however, these non-disclosure agreements may not prevent a third party from infringing upon our rights.

Human Capital

As of December 31, 2022, we employed 152 employees, all of which were full-time employees. This is an increase of 66 employees (77%) from December 31, 2021. Our employees are critical to our continued success. With approximately two-thirds of our employees considered experts, we view our employees and the depth and breadth of their experience and expertise as our competitive advantage. As such, we strive to provide an environment where urban-gro employees can have a fulfilling and productive career. We offer industry-leading employee benefits and programs to ensure the diverse needs of our employees and their families are met, including access to healthcare choices, continued growth opportunities for career development, and resources such as 401(k) plans and counseling to support their financial well-being.

The table below summarizes the change in full-time employee headcount that has occurred by quarter for the years ended December 31, 2022 and 2021:

| 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||

| Fourth Quarter | Third Quarter | Second Quarter | First Quarter | Fourth Quarter | Third Quarter | Second Quarter | First Quarter | ||||||||||||||||||||||||||||||||||||||||

Beginning of period headcount | 115 | 121 | 98 | 86 | 77 | 51 | 46 | 40 | |||||||||||||||||||||||||||||||||||||||

| Net change in headcount | 13 | (6) | 3 | 12 | 9 | 6 | 5 | 6 | |||||||||||||||||||||||||||||||||||||||

| 2WR acquisition | 0 | 0 | 0 | 0 | 0 | 20 | 0 | 0 | |||||||||||||||||||||||||||||||||||||||

| Emerald acquisition | 0 | 0 | 20 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||||||||||

| DVO acquisition | 24 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||||||||||

| Ending of period headcount | 152 | 115 | 121 | 98 | 86 | 77 | 51 | 46 | |||||||||||||||||||||||||||||||||||||||

Available Information

Our internet address is www.urban-gro.com and our investor relations internet address is ir.urban-gro.com. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports can be found on our investor relations website, free of charge, as soon as reasonably practical after we electronically file such material with, or furnish it to, the SEC. Information contained on our website is not incorporated by reference into this Form 10-K. The SEC maintains a public website, www.sec.gov, which contains reports, proxy and information statements, and other information regarding issuers that that file electronically with the SEC.

ITEM 1A. RISK FACTORS

An investment in our common stock involves a high degree of risk. You should carefully consider the following risks and all of the other information contained in this report before deciding whether to invest in our common stock. If any of the following risks are realized, our business, financial condition and results of operations could be materially and adversely affected. In that event, the trading price of our common stock could decline and you could lose all or part of your investment in our common stock. Additional risks of which we are not presently aware or that we currently believe are immaterial may also harm our business and results of operations. Some statements in this report, including such statements in the following risk factors, constitute forward-looking statements. See the section entitled Cautionary Information about Forward-Looking Statements in Part I of this Report.

14

Risks Related to Our Operations

We have a relatively limited history of operations, a history of losses, and our future earnings, if any, and cash flows may be volatile, resulting in uncertainty about our prospects generally.

We were initially organized as a limited liability company in the State of Colorado on March 20, 2014. In March 2017, we converted into a corporation and on February 12, 2021, we completed an uplisting to the Nasdaq Stock Market under the ticker symbol UGRO. The following is a summary of our recent historical operating performance:

•During the year ended December 31, 2022, we generated revenue of $67.0 million and incurred a net loss of $15.3 million.

•During the year ended December 31, 2021, we generated revenue of $62.1 million and incurred a net loss of $0.9 million.

•During the year ended December 31, 2020, we generated revenue of $25.8 million and incurred a net loss of $5.1 million.

•During the year ended December 31, 2019, we generated revenue of $24.2 million and incurred a net loss of $8.3 million.

Our lack of a significant history and the evolving nature of the market in which we operate make it likely that there are risks inherent to our business that are yet to be recognized by us or others, or not fully appreciated, and that could result in us suffering further losses. As a result of the foregoing, and concerns regarding the economic impact from the coronavirus disease of 2019 ("COVID-19"), an investment in our securities necessarily involves uncertainty about the stability of our operating results, cash flows and, ultimately, our prospects generally.

We had negative cash flow from operations for the fiscal years ended December 31, 2022 and December 31, 2021.

We had negative cash flow from operations of $12.6 million for the fiscal year ended December 31, 2022 and $1.6 for the fiscal year ended December 31, 2021. To the extent that we have negative cash flow from operations in future periods, we may need to allocate a portion of our cash reserves to fund such negative cash flow. We may also be required to raise additional funds through the issuance of equity or debt securities. We may not be able to generate positive cash flow from our operations and additional capital or other types of financing may not be available when needed or on terms favorable to us.

Our architecture, engineering, design, and construction management services have been used and may continue to be contracted for use in emerging industries that may be subject to quickly changing and inconsistent laws, regulations, practices and perceptions.

Although the demand for our architecture, engineering, design, and construction management services may be negatively impacted depending on how laws, regulations, administrative practices, judicial interpretations, and consumer perceptions develop, we cannot reasonably predict the nature of such developments or the effect, if any, that such developments could have on our business. We will continue to encounter risks and uncertainty relating to our operations that may be difficult to overcome.

We may continue to incur losses in the near future, which may impact our ability to implement our business strategy and adversely affect our financial condition.

While we are focused significantly on controlling our operating expenses by managing variable expenses, employee count, and marketing activities in order to become cash flow positive, these measures may adversely affect our future operating results if we are unable to support the business effectively. In turn, this would have a negative impact on our financial condition and potentially our share price.

We may not become profitable or generate sufficient profits from operations in the future. If our revenues do not continue to grow or our gross profits deteriorate substantially, we are likely to continue to experience losses in future periods. Collectively, this may impact our ability to implement our business strategy and adversely affect our financial condition. This potentially would have a negative impact on our share price.

15

We may become subject to additional regulation of CEA facilities.

Our engineering and design services are focused on facilities that grow a wide variety of crops that are subject to regulation by the United States Food and Drug Administration and other federal, state or foreign agencies. Changes to any regulations and laws that could complicate the engineering of these CEA facilities, such as waste water treatment and electricity-related mandates, make it possible that potential related enforcement could decrease the demand for our services, and in turn negatively impact our revenues and business opportunities.

Competition in our industry is intense.

There are many competitors in the horticulture industry, including many who offer somewhat categorically similar equipment solutions and services as those offered by us. In the future other companies may enter this arena by developing solutions that directly compete with us. We anticipate the presence as well as entry of other companies in this market space and acknowledge that we may not be able to establish, or if established to maintain, a competitive advantage. Some of these companies have longer operating histories, greater name recognition, larger client bases and significantly greater financial, technical, sales and marketing resources. This may allow them to respond more quickly than us to market opportunities. It may also allow them to devote greater resources to the marketing, promotion and sale of their products and/or services. These competitors may also adopt more aggressive pricing policies and make more attractive offers to existing and potential clients, employees, strategic partners, distribution channels and advertisers. Increased competition is likely to result in price reductions, reduced gross margins and a potential loss of market share.

The COVID-19 pandemic could continue to materially adversely affect our business, financial condition, results of operations, cash flows and day-to-day operations.

The outbreak of COVID-19, a novel strain of coronavirus first identified in China, which has spread across the globe including the U.S., had an adverse impact on our operations and financial condition by causing temporary delays in our projects. The response to coronavirus by federal, state and local governments resulted in significant market and business disruptions across many industries and affected businesses of all sizes. This pandemic also caused significant stock market volatility and further tightened capital access for most businesses. Given that the COVID-19 pandemic and its disruptions are of an unknown duration, they could have an adverse effect on our liquidity and profitability.

We continue to monitor the status of COVID-19. While it seems like the negative effects of the virus have largely dissipated, if a new variant or other new development cause a substantial increase of cases, it could disrupt the businesses of our customers and suppliers, which, in turn, could negatively impact market demand, interfere with our ability to timely service the needs of our clients and prospects, cause contract cancellations, scope reductions and delays, and interfere with our ability to procure equipment and raw materials from our suppliers. Any of these effects could thereby negatively impact our business, financial condition, results of operations or prospects.

We depend upon third-party suppliers for the equipment solutions that we sell.

We depend on outside manufacturers for the equipment solutions that we sell. For the year ended December 31, 2022, one vendor, Fluence Bioengineering, Inc. ("Fluence"), a provider of lighting systems, was particularly important to our integrated sales solutions. We use Fluence as one of the LED lighting systems options in our designs and then act as VAR and sell these systems to our clients as part of our overall package. While we believe that there are sufficient sources of supply available, if the third-party suppliers, such as Fluence, were to cease production or otherwise fail to supply us with products in sufficient quantities on a timely basis and we were unable to contract on acceptable terms for these equipment type products with alternative suppliers, our ability to sell these solutions would be materially adversely affected. If a sole source supplier was to go out of business, we may be unable to find a replacement for such source in a timely manner or at all. If a sole source supplier were to be acquired by a competitor, that competitor may elect not to sell to us in the future. Any inability to secure required products or to do so on appropriate terms could have a materially adverse impact on the business, financial condition, results of operations or prospects of urban-gro.

We have historically depended on a small number of clients for a substantial portion of our revenue. If we fail to retain or expand our client relationships, or if a significant client were to terminate its relationship with us or reduce its purchases, our revenue could decline significantly.

During the year ended December 31, 2022, three clients represented 40% of total revenue. During the year ended December 31, 2021 one client represented 46% of total revenue. Although we have been able to successfully generate substantial sales to different clients over time, we may not be able to continue to do this in the future. Our operating results for the foreseeable future could continue to depend on substantial sales to a small number of clients. Our clients have no purchase commitments and may cancel, change or delay purchases with little or no notice or penalty. As a result of this, our revenue could fluctuate materially and could be materially and disproportionately impacted by purchasing decisions of any client. Clients who represented a substantial portion of our

16

historical revenue may decide to purchase products and services from other providers in the future, which could cause our revenue to decline materially and negatively impact our financial condition and results of operations. If we are unable to diversify our client base, we will continue to be susceptible to risks associated with client concentration.

A portion of our business depends on our clients obtaining appropriate licenses from various licensing agencies.

A portion of our business depends on our clients obtaining appropriate licenses from various licensing agencies. Any or all licenses necessary for our clients to operate their businesses may not be obtained, retained or renewed. If a licensing body were to determine that one of our clients had violated applicable rules and regulations, there is a risk the license granted to that client could be revoked, which could adversely affect future sales to that client and our operations. Our existing clients may not be able to retain their licenses going forward and new licenses may not be granted to existing and new market entrants.

System security risks, data protection breaches, cyber-attacks and systems integration issues could disrupt our internal operations or services provided to clients.

Experienced computer programmers and hackers may be able to penetrate our network security and misappropriate or compromise our confidential information or that of third parties, create system disruptions or cause shutdowns. Computer programmers and hackers also may be able to develop and deploy viruses, worms, and other malicious software programs that attack or otherwise exploit any security vulnerabilities of the products that we may sell in the future. Such disruptions could adversely impact our ability to fulfill orders and interrupt other processes. Delayed sales, lower profits, or lost clients resulting from these disruptions could adversely affect our financial results, stock price and reputation.

We may be forced to litigate to defend our intellectual property rights, or to defend against claims by third parties against urban-gro relating to intellectual property rights.

We may be forced to litigate to enforce or defend our intellectual property rights, to protect our trade secrets or to determine the validity and scope of other parties’ proprietary rights. Any such litigation could be very costly and could distract our management from focusing on operating our business. The existence and/or outcome of any such litigation could harm our business.

We may not be able to successfully identify, consummate or integrate acquisitions or to successfully manage the impacts of such transactions on our operations.

Part of our business strategy includes pursuing synergistic acquisitions. We have expanded, and plan to continue to expand, our business by making strategic acquisitions and regularly seeking suitable acquisition targets to enhance our growth. Material acquisitions, dispositions and other strategic transactions involve a number of risks, including: (i) the potential disruption of our ongoing business; (ii) the distraction of management away from the ongoing oversight of our existing business activities; (iii) incurring indebtedness; (iv) the anticipated benefits and cost savings of those transactions not being realized fully, or at all, or taking longer to realize than anticipated; (v) an increase in the scope and complexity of our operations; and (vi) the loss or reduction of control over certain of our assets.

The pursuit of acquisitions may pose certain risks to us. We may not be able to identify acquisition candidates that fit our criteria for growth and profitability. Even if we are able to identify such candidates, we may not be able to acquire them on terms or financing satisfactory to us. We will incur expenses and dedicate attention and resources associated with the review of acquisition opportunities, whether or not we consummate such acquisitions.

Additionally, even if we are able to acquire suitable targets on agreeable terms, we may not be able to successfully integrate their operations with ours. Achieving the anticipated benefits of any acquisition will depend in significant part upon whether we integrate such acquired businesses in an efficient and effective manner. We may not be able to achieve the anticipated operating and cost synergies or long-term strategic benefits of our acquisitions within the anticipated timing or at all. The benefits from any acquisition will be offset by the costs incurred in integrating the businesses and operations. We may also assume liabilities in connection with acquisitions to which we would not otherwise be exposed. An inability to realize any or all of the anticipated synergies or other benefits of an acquisition as well as any delays that may be encountered in the integration process, which may delay the timing of such synergies or other benefits, could have an adverse effect on our business, results of operations and financial condition.

17

Risks Related to the Legal Cannabis Industry

To date, the majority of our revenues have come from providing architecture and engineering design services and selling equipment systems into facilities prior to the facility becoming operational. The majority of our revenues to date have been generated from clients that operate in the legal cannabis industry.

We are broadening our market reach beyond the legal cannabis industry and are placing a substantial sales effort on expansion into the rapidly growing non-cannabis CEA vertical farming sector as well as the Commercial sector. However, on a historic basis, the majority of our clients to whom we provide facility architecture and engineering design services and sell equipment systems prior to the facility becoming operational have primarily been in the legal cannabis industry. In addition to selling directly to these clients, we also sell our equipment solutions to third parties, such as general contractors and other intermediaries, like equipment leasing companies. The majority of these solutions have been resold into the legal cannabis industry. A significant decrease in demand in the legal cannabis industry could have a material adverse effect on our revenues and the success of our business.

The cannabis industry in the U.S. is an emerging industry and has only been legalized in some states while remaining illegal in others and under U.S. federal law. Federal Prohibition makes it difficult to accurately forecast the demand for our solutions in this specific industry. Losing clients from this industry may have a material adverse effect on our revenues and the success of our business.

The legal cannabis industry is not mature in the United States and has been legalized in only some states and remains illegal in others and under U.S. federal law, making it difficult to accurately forecast demand for our solutions. Revenues could materially decline if the U.S. Department of Justice ("DOJ") enforces federal law against the industry and some of our clients are negatively impacted.

The legal cannabis industry in the U.S. remains in state of flux, and many aspects of this industry’s development and evolution cannot be accurately predicted. Therefore, losing any clients could have a material adverse effect on our business. While we have attempted to identify our business risks in the legal cannabis industry, investors should carefully consider that there are other risks that cannot be foreseen or are not described in this Report, which could materially and adversely affect our business and financial performance.

There is heightened scrutiny by Canadian regulatory authorities related to the cannabis industry.

Our existing operations in the United States, and any future operations or investments, may become the subject of heightened scrutiny by regulators and other authorities in Canada. As a result, we may be subject to significant direct and indirect interaction with public officials. This heightened scrutiny may in turn lead to the imposition of certain restrictions on our ability to operate or invest in the United States.

On February 8, 2018, following discussions with the Canadian Securities Administrators and recognized Canadian securities exchanges, the TMX Group announced the signing of the TMX Memorandum of Understanding ("MOU") with Aequitas NEO Exchange Inc., the Canadian Securities Exchange ("CSE"), the Toronto Stock Exchange, and the TSX Venture Exchange ("TSXV"). The MOU outlines the parties’ understanding of Canada’s regulatory framework applicable to the rules, procedures, and regulatory oversight of the exchanges and Canadian Depository for Securities Limited ("CDS") as it relates to issuers with cannabis-related activities in the United States. The MOU confirms, with respect to the clearing of listed securities, that CDS relies on the exchanges to review the conduct of listed issuers. As a result, there is no CDS ban on the clearing of securities of issuers with cannabis-related activities in the United States. However, this approach to regulation may not continue in the future. If such a ban were to be implemented, and our shares were listed on a Canadian exchange, it would have a material adverse effect on the ability of holders of our securities to make and settle trades.

As cannabis remains illegal under United States federal law, we may have to stop providing equipment systems and services to companies who are engaged in cannabis cultivation and other cannabis-related activities.

Cannabis, which is referred to as "Marijuana" in the Controlled Substances Act, is currently classified as a Schedule I controlled substance under the Controlled Substances Act and is illegal under United States federal law. It is illegal under United States federal law to grow, cultivate, sell or possess cannabis for any purpose or to assist or conspire with those who do so. Additionally, 21 U.S.C. 856 makes it illegal to "knowingly open, lease, rent, use, or maintain any place, whether permanently or temporarily, for the purpose of manufacturing, distributing, or using any controlled substance." Even in those states in which the use of cannabis has been authorized under state law, its use remains a violation of federal law. Since federal law criminalizing the use of cannabis is not preempted by state laws that legalize its use, strict enforcement of federal law regarding cannabis may result in the inability of our clients that are involved in the cannabis industry to proceed with their operations, which would adversely affect our operations.

18

Our solutions are used by legal and licensed cannabis growers. While we are not aware of any threatened or current federal or state law enforcement actions against any supplier of equipment that might be used for cannabis cultivation, law enforcement authorities, in their attempt to regulate the illegal use of cannabis, may seek to bring an action or actions against us under the Controlled Substances Act for assisting or conspiring with persons engaged in the cultivation of cannabis.

There is also a risk that our activities could be deemed to be facilitating the selling or distribution of cannabis in violation of the Controlled Substances Act. Although federal authorities have not focused their resources on such tangential or secondary violations of the Controlled Substances Act, nor have they threatened to do so, with respect to the sale of equipment that might be used by legal and licensed cannabis cultivators, or with respect to any supplies marketed to participants in the medical and recreational cannabis industry, if the federal government were to change its practices, or were to expend its resources investigating and prosecuting providers of equipment that could be usable by participants in the medical or recreational cannabis industry, such actions could have a materially adverse effect on our operations and the sales of our products and services.

As a company with clients operating in the legal cannabis industry, we face many particular and evolving risks associated with that industry, including uncertainty of United States federal enforcement and the need to renew temporary safeguards.

The "FinCEN Memo" dated February 14, 2014, de-prioritizes enforcement of the Bank Secrecy Act against financial institutions and cannabis related businesses which utilize them. This memorandum appears to be a standalone document and is presumptively still in effect. At any time, however, the Department of the Treasury, Financial Crimes Enforcement Network, could elect to rescind the FinCEN Memo. This would make it more difficult for our clients and potential clients to access the U.S. banking systems and conduct financial transactions, which would adversely affect our operations.