UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE | ||||

| SECURITIES EXCHANGE ACT OF 1934 | ||||

| For the fiscal year ended December 31, 2017 | ||||

| OR | ||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE | ||||

| SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________ to ____________

Commission file number: 000-54288

COSMOS GROUP HOLDINGS INC.

(Exact name of registrant as specified in its charter)

| NEVADA | 22-3617931 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) | |

|

Rooms1705-6, 17th Floor, Tai Yau Building, No. 181 Johnston Road Wanchai, Hong Kong |

N/A | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: +852 3188 9363

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☒ No ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ (Do not check if a smaller reporting company) | Smaller reporting company ☒ |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Approximate aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 2017, based upon the closing sale price reported by the Over-the-Counter Bulletin Board on that date: US$9,796,929.25.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

| Common Stock | Outstanding at March 19, 2018 | |

| Common Stock, US$0.001 par value per share | 21,492,933 shares | |

DOCUMENTS INCORPORATED BY REFERENCE: None

| i |

Forward Looking Statements

This Form 10-K contains “forward-looking” statements including statements regarding our expectations of our future operations. For this purpose, any statements contained in this Form 10-K that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the foregoing, words such as “may,” “will,” “expect,” “believe,” “anticipate,” “estimate,” or “continue” or comparable terminology are intended to identify forward-looking statements. These statements by their nature involve substantial risks and uncertainties, and actual results may differ materially depending on a variety of factors, many of which are not within our control.

These risks and uncertainties include international, national, and local general economic and market conditions; our ability to sustain, manage, or forecast growth, our ability to successfully make and integrate acquisitions, new product development and introduction, existing government regulations and changes in, or the failure to comply with, government regulations, adverse publicity, competition, the loss of significant customers or suppliers, fluctuations and difficulty in forecasting operating results, change in business strategy or development plans, business disruptions, the ability to attract and retain qualified personnel, the ability to protect technology, and the risk of foreign currency exchange rate. Although the forward-looking statements in this report reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by them. In light of these risks and uncertainties, you are cautioned not to place undue reliance on these forward-looking statements. Except as required by law, we undertake no obligation to announce publicly revisions we make to these forward-looking statements to reflect the effect of events or circumstances that may arise after the date of this report. All written and oral forward-looking statements made subsequent to the date of this report and attributable to us or persons acting on our behalf are expressly qualified in their entirety by this section.

ITEM 1. DESCRIPTION OF BUSINESS.

OVERVIEW

We are a Hong Kong based specialty commercial logistic company and vehicle sales and leasing company. Our specialty commercial logistic company operates through Lee Tat Transportation Int’l Limited, our wholly owned Hong Kong subsidiary (“Lee Tat”), and provides timely and reliable logistics and delivery services to commercial clients located in Hong Kong. We offer service to the cable supply industry in Hong Kong, and expect to provide small parcel delivery service in cities near Shanghai in the near future. Lee Tat was organized as a private limited liability company on August 11, 2014, in Hong Kong. We acquired Lee Tat on May 12, 2017.

In October 2017, we held a soft launch of our vehicle sales and leasing business in Guangdong, China, with the intent to commence a vehicle leasing business in China through Asia Cosmos Group (Hong Kong) Limited, our wholly owned Hong Kong subsidiary, and Foshan Cosmos Xi Yue Car Rental Co. Ltd., a wholly foreign-owned enterprise incorporated in China. Based on the positive feedback from our marketing efforts, we began providing group car buying services, adopting a discount sale strategy to stand out in the auto market.

We expect to continue exploring market opportunities in the auto markets in China and America, especially the synergy and application with big data in the near future. We anticipate that our vehicle sales business, which is expected to include an O2O platform solution, will provide membership based vehicles sales, resale platform, maintenance and related ancillary services and benefits.

| 1 |

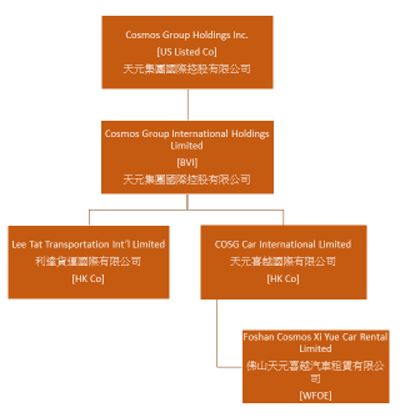

Our corporate organization chart is below.

We reported a net (loss) income of $(127,642) and $19,166 for the years ended December 31, 2017 and 2016, respectively. As of December 31, 2017, our current assets and current liabilities were $370,248 and $545,386, respectively. We had current assets of $47,863 and current liabilities of $75,130 as of December 31, 2016. Our auditors have prepared our financial statements for the years ended December 31, 2017 and 2016 assuming that we will continue as a going concern. Our continuation as a going concern is dependent upon improving our profitability and the continuing financial support from our stockholders. Our sources of capital in the past have included the sale of equity securities, which include common stock sold in private transactions and short-term and long-term debts.

We are organized under the laws of the State of Nevada as a holding company that conducts its business through a number of subsidiaries organized under the laws of foreign jurisdictions such as Hong Kong and the British Virgin Islands. This may have an adverse impact on the ability of U.S. investors to enforce a judgment obtained in U.S. Courts against these entities, or to effect service of process on the officers and directors managing the foreign subsidiaries.

History

We were incorporated in the state of Nevada on August 14, 1987, under the name Shur De Cor, Inc. and engaged in developing certain mining claims. In April 1999, Shur De Cor merged with Interactive Marketing Technology, a New Jersey corporation that was engaged in the business of developing and direct marketing of consumer products. As the surviving company, Shur De Cor changed its name to Interactive Marketing Technology, Inc. Shur De Cor's then management resigned and the management of Interactive New Jersey became the Company’s management. The prior management of Shur De Cor retained Shur De Cor’s business and assets. After that acquisition, the Company, through a wholly owned subsidiary, IMT's Plumber, Inc., produced, marketed, and sold a licensed product called the Plumber's Secret, which was discontinued in fiscal 2001. In May 2002, the Company ceased to actively pursue its product development and marketing business and actively sought to either acquire a third party, merge with a third party or pursue a joint venture with a third party in order to re-enter its former business of development and direct marketing of proprietary consumer products in the United States and worldwide.

| 2 |

On November 17, 2004, the Company acquired MPL, a company organized under the laws of the British Virgin Islands, and its subsidiaries in accordance with the terms of a Share Exchange Agreement executed by the parties (the “2004 Agreement”). In connection with the acquisition, the Company issued an aggregate of 109,623,006 shares of its common stock to Imperial International Limited, a company incorporated under the laws of the British Virgin Islands (“Imperial”), the sole shareholder of MPL, in exchange for 100% of the issued and outstanding shares of MPL capital stock (the "2004 Share Exchange"). Upon completion of the share exchange, MPL became the Company's wholly owned subsidiary and the Company’s former owner transferred control of the Company to Imperial. The Company relied on Rule 506 of Regulation D of the Securities Act of 1933, as amended (the "Act"), in regard to the shares that we issued pursuant to the 2004 Share Exchange. The Company treated this transaction as a qualified "business combination" as defined by Rule 501(d). The Company relied on the exemption from registration pursuant to Section 4(2) of, and or Regulation D promulgated under, the Act in issuing the Company’s securities.

In connection with the 2004 Share Exchange, the Company: (i) changed its name from Interactive Marketing Technology, Inc. to China Artists Agency, Inc. ("China Artists"); (ii) obtained a new stock symbol, "CAAY", and CUSIP Number, effective on December 21, 2004; (iii) increased its authorized common stock to 200,000,000 shares; (iv) effectuated a 1 for 1.69 reverse stock split; and (v) spun off the Company’s existing business into a separate public company, All Star Marketing, Inc., a Nevada corporation ("All Star"). All Star was formed as a wholly owned subsidiary of the Company. The Spin-off was satisfied by means of a pro-rata share dividend to the Company's shareholders of record as of December 10, 2004. The purpose of the Spin-Off was to allow the subsidiary to operate as a separate public company and raise working capital through the sale of its own equity. This allowed the Company’s management to focus on its business, while at the same time, allowing the spun-off company to have greater exposure by trading as an independent public company. Additionally, the shareholders and the market would then more easily identify the results and performance of the Company as a separate entity from that of All Star. In August 2005, the Company changed its name to China Entertainment Group, Inc. and, effective August 9, 2005, obtained a new stock symbol "CGRP", and CUSIP Number.

Because the Company failed to generate revenues in its new business, prior management commenced litigation in the Superior Court for Los Angeles County California which action was removed to the United States District Court for the Central District of California Case No. CV07-1068 GHK. On January 30, 2008, the parties entered into a Settlement Agreement and Conditional Release (the “Settlement Agreement”), pursuant to which, among other things, the Company’s former management reacquired control of the Company and all assets related to the Chinese entertainment business were transferred out of the Company. The Company, under its former management, once again entered the business of locating products to develop and mass market. These efforts did not prove fruitful and the Company, while continuing its product development business, also began to seek another business to acquire.

Effective July 22, 2010, the Company merged with Safe and Secure TV Channel, LLC, a Delaware limited liability company (the “Merger”). In connection with the Merger, the management of the Company resigned and was replaced by the management and principals of Safe and Secure TV Channel, LLC. The holders of interests in Safe and Secure TV Channel, LLC exchanged their interests for approximately 50.2% of the issued and outstanding stock of the Company. In September 2010, the Company effectuated a 9.85 for one stock split to shareholders of record as of August 23, 2010. After the Merger, the Company became a television network and multimedia information and distribution company focused on serving the homeland security and emergency preparedness industry.

On February 15, 2016, the Company sold to Asia Cosmos Group Limited, a private limited liability company incorporated under the laws of British Virgin Islands (“ACOSG”), 10,000,000 shares of its common stock at a per share price of $0.027. ACOSG’s sole shareholder is Miky Wan. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to ACOSG.

In connection with the private placement to ACOSG, a change of control occurred and Bryan Glass resigned from his position as President, Secretary, Treasurer and Chairman of the Company. Miky Wan was appointed to serve as Chief Executive Officer, Chief Operating Officer, President and Director, effective February 19, 2016. Peter Tong, our Chief Financial Officer, Secretary and director continued in his positions with the Company. Calvin K.W. Lai, Anthony H.H. Chan, Jenher Jeng, Alice K.M. Tang, Connie Y.M. Kwok were appointed to serve on our Board of Directors effective February 19, 2016. Effective February 26, 2016, the Company changed its name to Cosmos Group Holdings Inc. and filed a Certificate of Amendment to such effect with the Nevada Secretary of State. The name change and the related stock symbol change to “COSG” were approved by the Financial Industry Regulatory Authority on March 31, 2016. The Company also increased the number of its authorized common stock, par value $0.001, from 90,000,0000 shares to 500,000,000 and its preferred stock, par value $0.001, from 10,000,000 to 30,000,000 shares. After the private placement, the Company shifted its business plan to focus on acquiring undervalued companies including those in the Greater China region.

| 3 |

On September 27, 2016, Peter Tong and Calvin Lai resigned from all of their positions with the Company. Connie Y.M. Kwok was appointed to serve as the Secretary and Miky Wan, our Chief Executive Officer, was appointed to serve as the interim Chief Financial Officer.

On January 13, 2017, the Company sold 200,000,000 shares of its common stock to ACOSG at a per share price of $0.001 per share for aggregate consideration of US $200,000. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to ACOSG.

Acquisition of Lee Tat, Our Logistics Business

On May 12, 2017, we acquired all of the issued and outstanding shares of Lee Tat from Mr. Koon Wing CHEUNG, Lee Tat’s sole shareholder, in exchange for 219,222,938 shares of our issued and outstanding common stock. In connection with the Lee Tat acquisition, Miky Wan resigned from her positions as Chief Executive Officer and Chief Operating Officer and Koon Wing CHEUNG and Yongwei HU were appointed to serve as our Chief Executive Officer and Chief Operating Officer, respectively, and also as our directors. In addition, Anthony H.H. CHAN and Alice K. M. TANG resigned from their positions as directors, and Zhigang LIAO and Weiming CHEN were appointed to fill the vacancies created by their resignations. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to the shareholders of Lee Tat.

Vehicle Sales and Leasing Business

During the fourth quarter of 2017, we engaged in two months of research and promotional activity in the China auto market. On October 27, 2017, we held a soft launch event for our car sales and leasing business in the City of Foshan and obtained a nonbinding intent of cooperation from Xi Yue Yi Car Rental Co, a car sales and leasing service provider. We commenced our auto sales business in November 2017 through Asia Cosmos Group (Hong Kong) Limited, our wholly owned Hong Kong subsidiary, and Foshan Cosmos Xi Yue Car Rental Co. Ltd a wholly foreign-owned enterprise incorporated in China. Based upon the positive feedback received from our marketing efforts, especially with respect to our discount sales strategy, we decided to restructure our group of companies and especially of Asia Cosmos Group (Hong Kong) Limited on November 30, 2017, to Giant Merit Development Holdings Limited, an offshore entity, to better take advantage of this valuable independent sector.

We expect to continue exploring market opportunities in the auto markets in China and America, especially the synergy and application with big data in the near future. We anticipate that our vehicle sales business, which is expected to include a O2O platform solution, will provide membership based vehicles sales, resale platform, maintenance and related ancillary services and benefits. We believe the vehicle sales and leasing business could be a high growth market, especially if implemented through our ecosystem.

Effective February 6, 2018, we engaged in a 1:20 reverse split of our common stock so that each twenty shares of issued and outstanding common stock were exchanged for one share.

Market Overview

The Logistics Market

According to The Statistics Portal in 2017, China is the world's largest express delivery market, with total parcel volume of 31 billion in 2016, approximately 1.5 times the total parcel volume of the United States. The logistics industry in China is at an earlier stage of development compared to the United States, and the majority of players focus on one particular logistics sub-segment, such as express delivery, or a limited number of logistics service categories.

The express delivery market is in turn driven by China's fast growing e-commerce market, which has created a strong demand for reliable and express delivery services. According to iResearch, China’s e-commerce Gross Merchandise Value (GMV) totaled 20.2 trillion Yuan in 2016, increasing by 23.1% compared with 2015. Online shopping with growth rate of 23.9% and local life O2O with growth of 28.2% were important roles which fueled the development of e-commerce in 2016. Some leading Chinese e-commerce platforms, such as Alibaba and JD.com, have completed millions of online sale and purchase transactions. In addition, "micro-merchants" who promote and sell their merchandise on social networking and other mobile platforms have also become an emerging key growth driver of the express delivery industry in China.

| 4 |

According to the iResearch Report, China's express delivery service providers generally fall into the following two major categories:

A. "Network partner" model.

A majority of China's private domestic express delivery service providers operate under the "network partner" model, which is a subcontracting business model. The top four domestic express delivery companies that operate under this model, namely ZTO Express, STO Express, YTO Express and Yunda Express, are commonly referred to as the "Tongda Operators". Market shares of these four companies in 2017 in terms of parcel volume were 14.4%, 10.4%, 14.3% and 10.3%, respectively, according to the iResearch Report. These players typically operate a logistics network by focusing on the build-out and operations of the core sorting hubs and line-haul transportation assets while relying on network partners to carry out pickup and last-mile deliveries. As a result of these unique characteristics, the Tongda Operators have the ability to rapidly scale up and expand their networks to meet the demands from the fast-growing e-commerce industry while limiting their capital expenditures.

B. "Direct" model.

EMS (a subsidiary of China Post) and SF Express are examples of Chinese express delivery operators that have adopted the "direct" model. Under this model, operators offer a spot to spot delivery service by its own operation team. Market shares of EMS and SF Express in 2017 in terms of parcel volume were 5.7% and 7.7%, respectively, according to the iResearch Report.

We believe the network partner model is best suited to support the enormous growth of the e-commerce industry in China. This model enables the express delivery companies to serve a fragmented merchant and consumer base and seasonal demand of the e-commerce industry.

In addition to robust economic and e-commerce growth, the growth of China’s express delivery companies is supported by favorable government policies that stimulate infrastructure development in rural areas which allows for increased penetration of express delivery services. We believe that the express delivery industry will also have new growth opportunities in the cross-border e-commerce market as well as adjacent logistics markets including less-than-truckload business.

Our Business

Logistics Business

Lee Tat Transportation Int’l Limited was originally formed as a sole proprietorship in August 11, 1995, and was incorporated on August 11, 2014. Prior to our acquisition, Lee Tat was wholly owned by Koon Wing CHEUNG, its Chief Executive Officer and Chief Financial Officer. Lee Tat initially provided express delivery for commercial clients, delivering small goods to factories and offices in Hong Kong. In 2016, Lee Tat’s conducted its business solely in Hong Kong.

In 2005 in response to the relocation of many local factories to mainland China, we began to focus on providing express delivery and logistic services to local cable and data equipment suppliers, delivering goods to their customers such as construction companies. Hong Kong is a well-developed city with respect to wireless and telecom communication. Because the useful life of cable is 5-10 years and data equipment is 3 years, there is a high demand for equipment replacement. As most of the repairing work happens in night-time, many small and medium cable suppliers outsource to logistic companies to deliver their products to their customers. We currently serve up to 70% of cable suppliers and cable trading companies in Hong Kong and deliver cable wire material to different contracting sites.

We provide our delivery services through direct delivery (Direct Model) and through our network of subcontractors (Network Model) as well as other custom value-added logistics services. In Hong Kong, we direct deliver small goods and primarily work with six network business sub-contractors to find the most competitive partner to deliver our client’s cable products. The lifecycle of a typical delivery is briefly described below.

Work flow of a typical delivery

Step 1: Parcel Pickup.

| 5 |

Our courier team collects the parcel from the sender once it receives a delivery order. Unless the sender chooses pay-at-arrival service, our pickup team collects the delivery service fee from the sender at the time of pickup. The pickup team collects and sends the parcels to our centralized control sorting hub in Suzhou twice per day. Typically, parcels that are picked up before 9 a.m. will be shipped to the hub on the same day. Through each waybill, we assign a unique tracking number and corresponding barcode to each parcel. The waybills, coupled with our automated systems, allow us to track the status of each individual parcel throughout the entire pickup, sorting and delivery process.

Step 2: Parcel Sorting and Transportation.

Upon receipt of parcels shipped from various pickup outlets within its coverage area, the sorting hub sorts, further packs and dispatches the parcels to the destination by the courier team. Barcodes on each waybill attached to the parcels are scanned as they go through each sorting and transportation gateway allowing us to track the progress of each parcel.

Step 3: Parcel Delivery.

Parcels are then delivered to the recipients by our network delivery team. Once the recipient signs on the waybill to confirm receipt, a full service cycle is completed and the settlement of delivery service fee promptly ensues on our network payment settlement system.

Pricing determination

Pricing of our services is based on our operating costs, service requested, fees assessed by our network partners, market conditions and competition. We participate in a fee sharing arrangement in which the pickup and delivery outlets share the delivery service fees of each delivery order. When we deliver through our network partners, we allocate a portion of the services fees, or network transit fees, to our network partners for express delivery services. The fee typically consists of a fixed amount for a waybill attached to each parcel and a variable per parcel amount based on parcel weight and route. Historically, delivery service fees charged by our network partners have experienced declines due in part to market competition. Based on the market conditions and our cost base, we may evaluate and adjust our service pricing from time to time. The average revenue of a typical parcel delivery is US$102.

We leverage our subcontractor network to reduce costs and generate fees. Before initiating deliveries through our network partners, we are able to search through our system to compare and find the most competitive pricing for pick up and last mile deliveries. This arrangement allows us to control our per parcel costs. Because our network is transparent, our delivery subcontractors are able to directly connect with other member logistic service suppliers. When these third parties directly connect, we benefit through fee rebates provided by our network partner, Suzhou Hexie Yuantong Logistic Company Limited. We facilitate these connections by providing information and guidance on valuation of the transferred business with participation by both sides.

In light of the competitive nature of our market, we believe that our success will depend upon the reliability and quality of services provided and cost management. As a general matter, we strive to maintain high quality services and meet customer satisfaction. We believe that we have established systems and procedures to achieve service standardization and quality control over the services provided by us and our network partners. We constantly monitor and seek to improve on a series of key service quality indicators such as delivery delay rate, complaint rate and damaged parcel rate. Further, we believe that our focus on the cable and data equipment industry provides a competitive advantage that has enabled us to provide valued added services to better able to meet the specific needs of our customers.

Termination of China Expansion

Effective May 1, 2017, and expiring April 30, 2022, we agreed to provide certain logistics and delivery services to Shanghai Yunda Cargo Company Limited (“Yunda”), in accordance with the terms of that certain Lee Tat Transportation Service Contract, of the Transportation Service Contract. Pursuant to the agreement, Yunda agreed to provide to us not less than RMB 12 million (US $1.76 million) of revenue from cargo business per year. We expected to provide cross-border delivery and logistics services in Shanghai and nearby cities pursuant to the terms of the Transportation Service Contract.

We began operations in China in July 2017. We initially anticipated providing door-to-door cross-border and domestic logistics service for small goods deliveries through subcontractors and network partners to reach and serve fragmented and geographically dispersed merchants at a minimized fixed operation cost. After a quarter trial period, management concluded that the business operations in Suzhou and Shanghai were not cost efficient, and that the profit margins could not meet our expectations. While we are still a party to the Transportation Service Contract, we are reassessing our business analysis of this business relationship.

| 6 |

The foregoing description of the Transportation Service Contract is qualified in its entirety by reference to the Transportation Service Contract, which is filed as Exhibit 10.1 to this Registration Statement and incorporated herein by reference.

During the course of our business, we have collected data relating to consumer behavior. We hope to develop a proprietary database and provide data analytics regarding consumer behavior in the commercial logistics and vehicle sales and leasing industries. We believe that we can leverage this database and accompanying analytics to refine our product and services offerings as well as provide relevant industry knowledge.

Vehicle Sales and Leasing Business

On October 27, 2017, we held a soft launch event for our car sales and leasing business in the City of Foshan and received a nonbinding intent of cooperation from Xi Yue Yi Car Rental Co, a car sales and leasing service provider. After a two month research and soft launch, we established our auto sales business in November 2017 through Asia Cosmos Group (Hong Kong) Limited, our wholly owned Hong Kong subsidiary, and Foshan Cosmos Xi Yue Car Rental Co. Ltd, a wholly foreign-owned enterprise incorporated in China. Based upon the positive feedback received from our marketing efforts, especially with respect to our discount sales strategy, we decided to restructure our group of companies and especially of Asia Cosmos Group (Hong Kong) Limited on November 30, 2017, to Giant Merit Development Holdings Limited, an offshore entity, to better take advantage of this valuable independent sector.

We expect to continue to explore the opportunity of the auto market in China and America, especially the synergy and application with big data in the near future. We hope to establish a vehicle sales and related business, which will provide membership based vehicles sales, resale platform, maintenance and related ancillary services and benefits. We expect to offer members of our vehicle sales and leasing business the opportunity to purchase vehicles, vehicle insurance, vehicle repair services and other perks and benefits at a discounted price. We hope to offer memberships at the corporate and individual levels. We expect a standard to extend for an eighteen-month period, and contract fees will vary based upon the make and number of vehicles selected. Membership fees will be nonrefundable and payable in full upon the commencement of membership.

We expect a member to receive his vehicle directly from the dealer during the seventh month of his membership. During the membership period, a member will be entitled to take advantage of our perks and benefits such as discounted insurance and repair service pricing. Any loss or damage to the vehicle during the membership period will be borne by the member. Upon the expiration of the eighteen-month period, the member will be entitled to retain his vehicle.

In order to provide our members with competitive vehicle pricing and an attractive package of benefits, we are in the process of negotiating bulk pricing arrangements with local car dealers, repair service shops, insurance brokers and other related service providers.

We may organically develop our vehicle sales and leasing business segment or acquire an existing auto service enterprise with an experienced operation team. In the interim, we expect to focus on the marketing research and the development of our business plan.

Sales and Marketing.

We expect to continue to focus on providing express delivery and logistic services to cable and data equipment suppliers in Hong Kong and mainland China. We anticipate focusing on business to business marketing, cold callings or attending local chamber of commerce events to obtain customers. We are in the process of focusing and consolidating our Hong Kong and Shanghai operations. We expect to sustain and consolidate the existing business in Hong Kong. Our branch in Hong Kong will also support our Shanghai client (Yunda) and the Suzhou office for cross border logistic and delivery. We expect our Suzhou team to continue operations with a focus on developing business in Foshan, with our Suzhou business partner servicing the actual deliveries.

Major Customers.

All of our major customers are located in Hong Kong. During the year ended December 31, 2017, and 2016, the following customers accounted for 10% or more of our total net revenues:

| Year ended December 31, 2017 | December 31, 2017 | |||||||||||

| Revenues | Percentage of revenues | Accounts receivable | ||||||||||

| Peaceman Cable Engineering Limited | $ | 295,534 | 38% | $ | – | |||||||

| Hip Tung Cables Company Limited | 183,390 | 24% | – | |||||||||

| TOTAL | 478,924 | 62% | – | |||||||||

| 7 |

| Year ended December 31, 2016 | December 31, 2016 | |||||||||||

| Revenues | Percentage of revenues | Accounts receivable | ||||||||||

| Peaceman Cable Engineering Limited | $ | 172,971 | 39% | $ | 32,777 | |||||||

| Hip Tung Cables Company Limited | 84,926 | 19% | – | |||||||||

| TOTAL | 257,897 | 58% | 32,777 | |||||||||

We have a delivery operations team in Hong Kong consisting of two trucks, two drivers, and six network partners that pick up stocks for us and complete the delivery process. Generally, we are not a party to any long-term agreements with our customers. From time to time, we may enter into long term contracts similar to the Transportation Service with major customers and subcontract the performance of the performance of the contract to corresponding network partner according to the price and area.

Major Network Partners.

All of our major vendors are located in Hong Kong. For the year ended December 31, 2017, one vendor, Po Won Transport Company Limited represented more than 10% of the Company’s operating cost. This vendor accounted for 14% of the Company’s operating cost amounting to $48,246 with $0 of accounts payable.

For the year ended December 31, 2016, one vendor, Tak Lee Transportation Company represented more than 10% of the Company’s operating cost. This vendor accounted for 23% of the Company’s operating cost amounting to $26,862 with $0 of accounts payable.

Seasonality.

Our logistics business is highly dependent upon the e-commerce industry in Hong Kong and China. In Hong Kong and China, we experience peak demand for our services during the double eleven festival and the Chinese New Year celebrations.

Insurance.

We maintain certain insurance in accordance customary industry practices in Hong Kong. Under Hong Kong law it is a requirement that all employers in the city must purchase Employee's Compensation Insurance to cover their liability in the event that their staff suffers an injury or illness during the normal course of their work. Lee Tat maintains Employee’s Compensation Insurance, vehicle insurance and third party risks insurance for the business purposes.

INTELLECTUAL PROPERTY AND PATENTS

We expect to rely on, trade secrets, copyrights, know-how, trademarks, license agreements and contractual provisions to establish our intellectual property rights and protect our brand and services. These legal means, however, afford only limited protection and may not adequately protect our rights. Litigation may be necessary in the future to enforce our intellectual property rights, protect our trade secrets or determine the validity and scope of the proprietary rights of others. Litigation could result in substantial costs and diversion of resources and management attention.

In addition, the laws of Hong Kong and the PRC may not protect our brand and services and intellectual property to the same extent as U.S. laws, if at all. We may be unable to fully protect our intellectual property rights in these countries.

We intend to seek the widest possible protection for significant product and process developments in our major markets through a combination of trade secrets, trademarks, copyrights and patents, if applicable. We anticipate that the form of protection will vary depending upon the level of protection afforded by the particular jurisdiction. We expect that our revenue will be derived principally from our operations in Hong Kong and China where intellectual property protection may be limited and difficult to enforce. In such instances, we may seek protection of our intellectual property through measures taken to increase the confidentiality of our findings.

| 8 |

We intend to register trademarks as a means of protecting the brand names of our companies and products. We intend protect our trademarks against infringement and also seek to register design protection where appropriate.

We rely on trade secrets and unpatentable know-how that we seek to protect, in part, by confidentiality agreements. We expect that, where applicable, we will require our employees to execute confidentiality agreements upon the commencement of employment with us. We expect these agreements to provide that all confidential information developed or made known to the individual during the course of the individual's relationship with us is to be kept confidential and not disclosed to third parties except in specific limited circumstances. The agreements will also provide that all inventions conceived by the individual while rendering services to us shall be assigned to us as the exclusive property of our company. There can be no assurance, however, that all persons who we desire to sign such agreements will sign, or if they do, that these agreements will not be breached, that we would have adequate remedies for any breach, or that our trade secrets or unpatentable know-how will not otherwise become known or be independently developed by competitors.

COMPETITION

We operate in a highly competitive and fragmented industry that is sensitive to price and service. We compete with leading domestic express delivery companies including SF Express, STO Express, YTO Express, Yunda Express and EMS. We also compete with international logistics companies such as federal express and DHL. We may in the future compete against major e-commerce platforms, such as Alibaba and JD.com, if they elect to build or further develop in-house delivery capabilities to serve their logistics needs. Some of our current and prospective competitors have greater financial resources, broader product and service offerings, longer operating histories, larger customer base and greater brand recognition, or they are controlled or subsidized by foreign governments, which enable them to raise capital and enter into strategic relationships more easily. We believe that we compete on the basis of a number of factors, including business model, operational capabilities, pricing and service quality.

EMPLOYEES

Our Chief Executive Officer, Mr. Cheung, and one driver are the sole employees of the Company. In the next twelve months, we expect to engage approximately ten full time employees at our Suzhou logistic hub or Foshan in China, and 2 full time administration staff in Hong Kong for an aggregate of 15 employees as set forth below:

| Marketing operator | 4 | |||

| Logistic team | 6 | |||

| Administration Staff | 5 | |||

| Total | 15 |

We are required to contribute to the MPF for all eligible employees in Hong Kong between the ages of eighteen and sixty-five. We are required to contribute a specified percentage of the participant’s income based on their ages and wage level. For the years ended December 31, 2017 and 2016, the MPF contributions by us were $7,701 and $7,028, respectively. We have not experienced any significant labor disputes or any difficulties in recruiting staff for our operations.

GOVERNMENT AND INDUSTRY REGULATIONS

Hong Kong

Our business is located in Hong Kong are subject to the laws and regulations of Hong Kong governing businesses concerning, in particular labor, occupational safety and health, contracts, tort and intellectual property. Furthermore, we need to comply with the rules and regulations of Hong Kong governing the data usage and regular terms of service applicable to our potential customers or clients. As the information of our potential customers or clients is preserved in Hong Kong, we need to comply with the Hong Kong Personal Data (Privacy) Ordinance.

The Employment Ordinance is the main piece of legislation governing conditions of employment in Hong Kong since 1968. It covers a comprehensive range of employment protection and benefits for employees, including Wage Protection, Rest Days, Holidays with Pay, Paid Annual Leave, Sickness Allowance, Maternity Protection, Statutory Paternity Leave, Severance Payment, Long Service Payment, Employment Protection, Termination of Employment Contract, Protection Against Anti-Union Discrimination. In addition, every employer must take out employees’ compensation insurance to protect the claims made by employees in respect of accidents occurred during the course of their employment.

| 9 |

An employer must also comply with all legal obligations under the Mandatory Provident Fund Schemes Ordinance, (CAP485). These include enrolling all qualifying employees in MPF schemes and making MPF contributions for them. Except for exempt persons, employer should enroll both full-time and part-time employees who are at least 18 but under 65 years of age in an MPF scheme within the first 60 days of employment. The 60-day employment rule does not apply to casual employees in the construction and catering industries. Pursuant to the said Ordinance, we are required to make MPF contributions for our Hong Kong employees once every contribution period (generally the wage period within 1 month). Employers and employees are each required to make regular mandatory contributions of 5% of the employee’s relevant income to an MPF scheme, subject to the minimum and maximum relevant income levels. For a monthly-paid employee, the minimum and maximum relevant income levels are HK$7,100 and HK$30,000 respectively.

Mainland China

Our logistics operations are and future vehicle sales and leasing operations will be located in China and subject to the general laws in China governing businesses including labor, occupational safety and health, general corporations, intellectual property and other similar laws.

Employment Contracts

The Employment Contract Law was promulgated by the National People’s Congress’ Standing Committee on June 29, 2007 and took effect on January 1, 2008. The Employment Contract Law governs labor relations and employment contracts (including the entry into, performance, amendment, termination and determination of employment contracts) between domestic enterprises (including foreign-invested companies), individual economic organizations and private non-enterprise units (collectively referred to as the “employers”) and their employees.

a. Execution of employment contracts

Under the Employment Contract Law, an employer is required to execute written employment contracts with its employees within one month from the commencement of employment. In the event of contravention, an employee is entitled to receive double salary for the period during which the employer fails to execute an employment contract. If an employer fails to execute an employment contract for more than 12 months from the commencement of the employee’s employment, an employment contract would be deemed to have been entered into between the employer and employee for a non-fixed term.

b. Right to non-fixed term contracts

Under the Employment Contract Law, an employee may request for a non-fixed term contract without an employer’s consent to renew. In addition, an employee is also entitled to a non-fixed term contract with an employer if he has completed two fixed term employment contracts with such employer; however, such employee must not have committed any breach or have been subject to any disciplinary actions during his employment. Unless the employee requests to enter into a fixed term contract, an employer who fails to enter into a non-fixed term contract pursuant to the Employment Contract Law is liable to pay the employee double salary from the date the employment contract is renewed.

c. Compensation for termination or expiry of employment contracts

Under the Employment Contract Law, employees are entitled to compensation upon the termination or expiry of an employment contract. Employees are entitled to compensation even in the event the employer (i) has been declared bankrupt; (ii) has its business license revoked; (iii) has been ordered to cease or withdraw its business; or (iv) has been voluntarily liquidated. Where an employee has been employed for more than one year, the employee will be entitled to such compensation equivalent to one month’s salary for every completed year of service. Where an employee has employed for less than one year, such employee will be deemed to have completed one full year of service.

d. Trade union and collective employment contracts

Under the Employment Contract Law, a trade union may seek arbitration and litigation to resolve any dispute arising from a collective employment contract; provided that such dispute failed to be settled through negotiations. The Employment Contract Law also permits a trade union to enter into a collective employee contract with an employer on behalf of all the employees.

Where a trade union has not been formed, a representative appointed under the recommendation of a high-level trade union may execute the collective employment contract. Within districts below county level, collective employment contracts for industries such as those engaged in construction, mining, food and beverage and those from the service sector, etc., may be executed on behalf of employees by the representatives from the trade union of each respective industry. Alternatively, a district-based collective employment contract may be entered into.

As a result of the Employment Contract Law, all of our employees have executed standard written employment agreements with us. We have not experienced any significant labor disputes or any difficulties in recruiting staff for our operations.

| 10 |

Foreign Exchange Control and Administration

Foreign exchange in China is primarily regulated by:

| • | The Foreign Currency Administration Rules (1996), as amended; and |

| • | The Administration Rules of the Settlement, Sale and Payment of Foreign Exchange (1996), or the Administration Rules. |

Under the Foreign Currency Administration Rules, if documents certifying the purposes of the conversion of RMB into foreign currency are submitted to the relevant foreign exchange conversion bank, the RMB will be convertible for current account items, including the distribution of dividends, interest and royalties payments, and trade and service-related foreign exchange transactions. Conversion of RMB for capital account items, such as direct investment, loans, securities investment and repatriation of investment, however, is subject to the approval of SAFE or its local counterpart.

Under the Administration Rules for the Settlement, Sale and Payment of Foreign Exchange, foreign-invested enterprises may only buy, sell and/or remit foreign currencies at banks authorized to conduct foreign exchange business after providing valid commercial documents and, in the case of capital account item transactions, obtaining approval from SAFE or its local counterpart.

As an offshore holding company with a PRC subsidiary, we may (i) make additional capital contributions to our PRC subsidiaries, (ii) establish new PRC subsidiaries and make capital contributions to these new PRC subsidiaries, (iii) make loans to our PRC subsidiaries or consolidated affiliated entities, or (iv) acquire offshore entities with business operations in China in offshore transactions. However, most of these uses are subject to PRC regulations and approvals. For example:

| • | capital contributions to our PRC subsidiaries, whether existing or newly established ones, must be approved by the Ministry of Commerce or its local counterparts; |

| • | loans by us to our PRC subsidiaries, each of which is a foreign-invested enterprise, to finance their activities cannot exceed statutory limits and must be registered with SAFE or its local branches; and |

| • | loans by us to our consolidated affiliated entities, which are domestic PRC entities, must be approved by the National Development and Reform Commission and must also be registered with SAFE or its local branches. |

On August 29, 2008, SAFE issued the Circular on the Relevant Operating Issues Concerning the Improvement of the Administration of the Payment and Settlement of Foreign Currency Capital of Foreign-Invested Enterprises, or SAFE Circular 142. Pursuant to SAFE Circular 142, RMB resulting from the settlement of foreign currency capital of a foreign-invested enterprise must be used within the business scope as approved by the applicable government authority and cannot be used for domestic equity investment, unless it is otherwise approved. Documents certifying the purposes of the settlement of foreign currency capital into RMB, including a business contract, must also be submitted for the settlement of the foreign currency. In addition, SAFE strengthened its oversight of the flow and use of RMB capital converted from foreign currency registered capital of a foreign-invested company. The use of such RMB capital may not be altered without SAFE’s approval, and such RMB capital may not be used to repay RMB loans if such loans have not been used. Violations of SAFE Circular 142 could result in severe monetary fines or penalties. We expect that our use of RMB funds have been, and will be, within the approved business scope of our PRC subsidiary. We believe that our PRC subsidiary is permitted to conduct its castor seeds distribution operations and provide consulting services to castor farmers. However, we may not be able to use such RMB funds to make equity investments in the PRC through our PRC subsidiaries. There are no costs associated with applying for registration or approval of loans or capital contributions with or from relevant PRC governmental authorities, other than nominal processing charges. Under PRC laws and regulations, the PRC governmental authorities are required to process such approvals or registrations or deny our application within a prescribed time period, which is usually less than 90 days. The actual time taken, however, may be longer due to administrative delays. We cannot assure you that we will be able to obtain these government registrations or approvals on a timely basis, if at all, with respect to our operations in China. If we fail to receive such registrations or approvals, our ability to use the proceeds from our funds to capitalize our PRC operations may be negatively affected, which could materially and adversely affect our liquidity and ability to fund and expand our business.

| 11 |

The value of the Renminbi against the US dollar and other currencies may fluctuate and is affected by, among other things, changes in China’s political and economic conditions. Historically, the conversion of Renminbi into foreign currencies, including US dollars, has been based on rates set by the People’s Bank of China. On July 21, 2005, the PRC government changed its policy of pegging the value of the Renminbi to the US dollar. Under the new policy, the Renminbi will be permitted to fluctuate within a band against a basket of certain foreign currencies. There remains significant international pressure on the PRC government to adopt a substantial liberalization of its currency policy, which could result in a further and more significant appreciation in the value of the Renminbi against the US dollar.

The fluctuation of the Renminbi against the US dollar and other currencies may have an impact on our figures in our consolidated financial information presented elsewhere in this prospectus.

Dividend Distributions

The principal regulations governing dividend distributions of wholly foreign-owned enterprises include:

| • | the Companies Law (2005); |

| • | the Wholly Foreign-Owned Enterprise Law (2000); and |

| • | the Wholly Foreign-Owned Enterprise Law Implementing Rules (2001). |

Under these regulations, wholly foreign-owned enterprises in the PRC may pay dividends only out of their accumulated profits as determined in accordance with PRC accounting standards and regulations. In addition, these wholly foreign-owned enterprises are required to set aside at least 10% of their respective accumulated profits each year, if any, to fund certain reserve funds, until the aggregate amount of such fund reaches 50% of its registered capital. At the discretion of these wholly foreign-owned enterprises, they may allocate a portion of their after-tax profits based on PRC accounting standards to staff welfare and bonus funds. These reserve funds and staff welfare and bonus funds are not distributable as cash dividends.

Any wholly foreign owned enterprise of COSG will be regulated by the laws governing foreign-invested enterprises in the PRC. Accordingly, it will be required to allocate 10% of its after-tax profits based on PRC accounting standards each year to their general reserves until the accumulated amount of such reserves has exceeded 50% of its registered capital, after which no further allocation is required to be made. These reserve funds, however, may not be distributed to equity owners except in accordance with PRC laws and regulations. In addition, due to the failure of these laws and regulations to define or interpret the terms “non-profit,” “for-profit” or “for the purpose of making a profit” as they relate to our business, we cannot assure you that the PRC government authorities will not request our subsidiary to use its after-tax profits for its own development and restrict our subsidiary’s ability to distribute their after-tax profits to us as dividends.

On March 16, 2007, the National People’s Congress approved and promulgated the PRC Enterprise Income Tax Law, or “EIT Law,” which took effect on January 1, 2008. Pursuant to the new EIT law and its implementing regulations, dividends payable by a foreign-invested enterprise to its foreign enterprise (but not individual) investors will be subject to a 10% withholding tax if the foreign investors are considered as non-resident enterprises without any establishment or place of business within China or if the dividends payable have no connection with the establishment or place of business of the foreign investors within China, to the extent that the dividends are deemed China sourced income, unless any such foreign investor’s jurisdiction of incorporation has a tax treaty with China that provides for a different withholding arrangement. Hong Kong, where Lee Tat is incorporated, has such a tax treaty with China.

In addition, as clarified by a notice jointly promulgated by the Ministry of Finance and the State Administration of Taxation of the PRC on February 22, 2008, distribution of accumulated profits of foreign-invested enterprises will be subject to withholding tax.

CORPORATE INFORMATION

Our principal executive and registered offices are located at Rooms 1705-06, 17th Floor, Tai Yau Building, No. 181 Johnston Road, Wanchai, Hong Kong., telephone number +852 3643 1111. Our operations are based at 2/F and Roof, 52 Chan Uk Po, Sheung Shui, New Territories, Hong Kong. Our telephone number at the operational address is +852 2673 3760.

| 12 |

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

ITEM 1B. Unresolved Staff Comments.

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

Our corporate and executive office is located at Rooms 1705-6, 17th Floor, Tai Yau Building, No. 181 Johnston Road, Wanchai, Hong Kong, telephone number +852 3643 1111. Our Hong Kong operations hub is located at 2/F and Roof, 52 Chan Uk Po, Sheung Shui, New Territories, Hong Kong. Both of these locations are provided to us on a rent-free basis from our executive officers. We believe that our existing facilities are adequate to meet our current requirements. We do not own any real property.

There are no material pending legal proceedings to which we are a party or to which any of our property is subject, nor are there any such proceedings known to be contemplated by governmental authorities. None of our directors, officers or affiliates is involved in a proceeding adverse to our business or has a material interest adverse to our business.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

| 13 |

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

(a) Market Information

The following table sets forth the high and low closing sale prices for the periods presented as reported on the Over the Counter Bulletin Board. There is no established public trading market for our securities and a regular trading market may not develop, or if developed, may not be sustained.

| Price Range | ||||||||

| High | Low | |||||||

| Fiscal 2017 | ||||||||

| First quarter | US$ | 2.00 | US$ | 0.30 | ||||

| Second quarter | 1.59 | 0.15 | ||||||

| Third quarter | 0.56 | 0.10 | ||||||

| Fourth quarter | 0.10 | 0.10 | ||||||

| Fiscal 2016 | ||||||||

| First quarter | US$ | 1.00 | US$ | 0.22 | ||||

| Second quarter | 0.69 | 0.30 | ||||||

| Third quarter | 0.65 | 0.20 | ||||||

| Fourth quarter | 1.20 | 0.05 | ||||||

Our common stock is quoted on the Over the Counter Bulletin Board under the symbol COSG. As of March 20, 2018, the closing bid price of our securities was US$32.00.

(b) Approximate Number of Holders of Common Stock

As of March 19, 2018, there were approximately 132 shareholders of record of our common stock. Such number does not include any shareholders holding shares in nominee or “street name”.

(c) Dividends

Holders of our common stock are entitled to receive such dividends as may be declared by our board of directors. We paid no dividends during the periods reported herein, nor do we anticipate paying any dividends in the foreseeable future.

(d) Equity Compensation Plan Information

There are no options, warrants or convertible securities outstanding.

(e) Recent Sales of Unregistered Securities

The information set forth below describes our issuance of securities without registration under the Securities Act of 1933, as amended, during the year ended December 31, 2017, that were not previously disclosed in a Quarterly Report on Form 10-Q or in a Current Report on Form 8-K: None.

ITEM 6. Selected Financial Data.

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

| 14 |

ITEM 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

This discussion summarizes the significant factors affecting the operating results, financial condition, liquidity and cash flows of the Company and its subsidiaries for the fiscal years ended December 31, 2017 and 2016. The discussion and analysis that follow should be read together with the section entitled “Forward Looking Statements” and our consolidated financial statements and the notes to the consolidated financial statements included elsewhere in this annual report on Form 10-K.

Except for historical information, the matters discussed in this section are forward looking statements that involve risks and uncertainties and are based upon judgments concerning various factors that are beyond the Company’s control. Consequently, and because forward-looking statements are inherently subject to risks and uncertainties, the actual results and outcomes may differ materially from the results and outcomes discussed in the forward-looking statements. You are urged to carefully review and consider the various disclosures made by us in this report.

Currency and exchange rate

Unless otherwise noted, all currency figures quoted as “U.S. dollars”, “dollars” or “US$” refer to the legal currency of the United States. References to “HKD” are to the Hong Kong Dollar, the legal currency of Hong Kong. References to “RMB” are to the Renminbi, the legal currency of China. Throughout this report, assets and liabilities of the Company’s subsidiaries are translated into U.S. dollars using the exchange rate on the balance sheet date. Revenue and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive income within the statement of stockholders’ equity.

Overview

We are a Hong Kong based specialty commercial logistic company and vehicle sales and leasing company. Our specialty commercial logistic company operates through Lee Tat Transportation Int’l Limited, our wholly owned Hong Kong subsidiary (“Lee Tat”), and provides timely and reliable logistics and delivery services to commercial clients located in Hong Kong. We offer service to the cable supply industry in Hong Kong, and expect to provide small parcel delivery service in cities near Shanghai in the near future. Lee Tat was organized as a private limited liability company on August 11, 2014, in Hong Kong. We acquired Lee Tat on May 12, 2017.

We were incorporated in the state of Nevada on August 14, 1987, under the name Shur De Cor, Inc. and engaged in developing certain mining claims. In April 1999, Shur De Cor merged with Interactive Marketing Technology, a New Jersey corporation that was engaged in the business of developing and direct marketing of consumer products. As the surviving company, Shur De Cor changed its name to Interactive Marketing Technology, Inc. Shur De Cor's then management resigned and the management of Interactive New Jersey became the Company’s management. The prior management of Shur De Cor retained Shur De Cor’s business and assets. After that acquisition, the Company, through a wholly owned subsidiary, IMT's Plumber, Inc., produced, marketed, and sold a licensed product called the Plumber's Secret, which was discontinued in fiscal 2001. In May 2002, the Company ceased to actively pursue its product development and marketing business and actively sought to either acquire a third party, merge with a third party or pursue a joint venture with a third party in order to re-enter its former business of development and direct marketing of proprietary consumer products in the United States and worldwide.

On November 17, 2004, the Company acquired MPL, a company organized under the laws of the British Virgin Islands, and its subsidiaries in accordance with the terms of a Share Exchange Agreement executed by the parties (the “2004 Agreement”). In connection with the acquisition, the Company issued an aggregate of 109,623,006 shares of its common stock to Imperial International Limited, a company incorporated under the laws of the British Virgin Islands (“Imperial”), the sole shareholder of MPL, in exchange for 100% of the issued and outstanding shares of MPL capital stock (the "2004 Share Exchange"). Upon completion of the share exchange, MPL became the Company's wholly owned subsidiary and the Company’s former owner transferred control of the Company to Imperial. The Company relied on Rule 506 of Regulation D of the Securities Act of 1933, as amended (the "Act"), in regard to the shares that we issued pursuant to the 2004 Share Exchange. The Company treated this transaction as a qualified "business combination" as defined by Rule 501(d). The Company relied on the exemption from registration pursuant to Section 4(2) of, and or Regulation D promulgated under, the Act in issuing the Company’s securities.

| 15 |

In connection with the 2004 Share Exchange, the Company: (i) changed its name from Interactive Marketing Technology, Inc. to China Artists Agency, Inc. ("China Artists"); (ii) obtained a new stock symbol, "CAAY", and CUSIP Number, effective on December 21, 2004; (iii) increased its authorized common stock to 200,000,000 shares; (iv) effectuated a 1 for 1.69 reverse stock split; and (v) spun off the Company’s existing business into a separate public company, All Star Marketing, Inc., a Nevada corporation ("All Star"). All Star was formed as a wholly owned subsidiary of the Company. The Spin-off was satisfied by means of a pro-rata share dividend to the Company's shareholders of record as of December 10, 2004. The purpose of the Spin-Off was to allow the subsidiary to operate as a separate public company and raise working capital through the sale of its own equity. This allowed the Company’s management to focus on its business, while at the same time, allowing the spun-off company to have greater exposure by trading as an independent public company. Additionally, the shareholders and the market would then more easily identify the results and performance of the Company as a separate entity from that of All Star. In August 2005, the Company changed its name to China Entertainment Group, Inc. and, effective August 9, 2005, obtained a new stock symbol "CGRP", and CUSIP Number.

Because the Company failed to generate revenues in its new business, prior management commenced litigation in the Superior Court for Los Angeles County California which action was removed to the United States District Court for the Central District of California Case No. CV07-1068 GHK. On January 30, 2008, the parties entered into a Settlement Agreement and Conditional Release (the “Settlement Agreement”), pursuant to which, among other things, the Company’s former management reacquired control of the Company and all assets related to the Chinese entertainment business were transferred out of the Company. The Company, under its former management, once again entered the business of locating products to develop and mass market. These efforts did not prove fruitful and the Company, while continuing its product development business, also began to seek another business to acquire.

Effective July 22, 2010, the Company merged with Safe and Secure TV Channel, LLC, a Delaware limited liability company (the “Merger”). In connection with the Merger, the management of the Company resigned and was replaced by the management and principals of Safe and Secure TV Channel, LLC. The holders of interests in Safe and Secure TV Channel, LLC exchanged their interests for approximately 50.2% of the issued and outstanding stock of the Company. In September 2010, the Company effectuated a 9.85 for one stock split to shareholders of record as of August 23, 2010. After the Merger, the Company became a television network and multimedia information and distribution company focused on serving the homeland security and emergency preparedness industry.

On February 15, 2016, the Company sold to Asia Cosmos Group Limited, a private limited liability company incorporated under the laws of British Virgin Islands (“ACOSG”), 10,000,000 shares of its common stock at a per share price of $0.027. ACOSG’s sole shareholder is Miky Wan. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to ACOSG.

In connection with the private placement to ACOSG, a change of control occurred and Bryan Glass resigned from his position as President, Secretary, Treasurer and Chairman of the Company. Miky Wan was appointed to serve as Chief Executive Officer, Chief Operating Officer, President and Director, effective February 19, 2016. Peter Tong, our Chief Financial Officer, Secretary and director continued in his positions with the Company. Calvin K.W. Lai, Anthony H.H. Chan, Jenher Jeng, Alice K.M. Tang, Connie Y.M. Kwok were appointed to serve on our Board of Directors effective February 19, 2016. Effective February 26, 2016, the Company changed its name to Cosmos Group Holdings Inc. and filed a Certificate of Amendment to such effect with the Nevada Secretary of State. The name change and the related stock symbol change to “COSG” were approved by the Financial Industry Regulatory Authority on March 31, 2016. The Company also increased the number of its authorized common stock, par value $0.001, from 90,000,0000 shares to 500,000,000 and its preferred stock, par value $0.001, from 10,000,000 to 30,000,000 shares. After the private placement, the Company shifted its business plan to focus on acquiring undervalued companies including those in the Greater China region.

On September 27, 2016, Peter Tong and Calvin Lai resigned from all of their positions with the Company. Connie Y.M. Kwok was appointed to serve as the Secretary and Miky Wan, our Chief Executive Officer, was appointed to serve as the interim Chief Financial Officer.

On January 13, 2017, the Company sold 200,000,000 shares of its common stock to ACOSG at a price of $0.001 per share for aggregate consideration of US $200,000. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to ACOSG.

| 16 |

Acquisition of Lee Tat, Our Logistics Business

On May 12, 2017, we acquired all of the issued and outstanding shares of Lee Tat from Mr. Koon Wing CHEUNG, Lee Tat’s sole shareholder, in exchange for 219,222,938 shares of our issued and outstanding common stock. In connection with the Lee Tat acquisition, Miky Wan resigned from her positions as Chief Executive Officer and Chief Operating Officer and Koon Wing CHEUNG and Yongwei HU were appointed to serve as our Chief Executive Officer and Chief Operating Officer, respectively, and also as our directors. In addition, Anthony H.H. CHAN and Alice K. M. TANG resigned from their positions as directors, and Zhigang LIAO and Weiming CHEN were appointed to fill the vacancies created by their resignations. The Company relied on the exemption from registration pursuant to Section 4(2) of, and Regulation D and/or Regulation S promulgated under the Act in selling the Company’s securities to the shareholders of Lee Tat.

On October 27, 2017, we held a soft launch event for our car sales and leasing business in the City of Foshan and obtained a nonbinding intent of cooperation from Xi Yue Yi Car Rental Co, a car sales and leasing service provider. We commenced our auto sales business in November 2017 through Asia Cosmos Group (Hong Kong) Limited, our wholly owned Hong Kong subsidiary, and Foshan Cosmos Xi Yue Car Rental Co. Ltd. a wholly foreign-owned enterprise incorporated in China. Based upon the positive feedback received from our marketing efforts, especially with respect to our discount sales strategy, we decided to restructure our group of companies and especially of Asia Cosmos Group (Hong Kong) Limited on November 30, 2017, to Giant Merit Development Holdings Limited, an offshore entity, to better take advantage of this valuable independent sector.

We expect to continue exploring market opportunities in the auto markets in China and America, especially the synergy and application with big data in the near future. We anticipate that our vehicle sales business, which is expected to include a O2O platform solution, will provide membership based vehicles sales, resale platform, maintenance and related ancillary services and benefits. We believe the vehicle sales and leasing business could be a high growth market, especially if implemented through our ecosystem.

Effective February 6, 2018, we engaged in a 1:20 reverse split of our common stock so that each twenty shares of issued and outstanding common stock were exchanged for one share.

Comparison of the fiscal years ended December 31, 2017 and December 31, 2016

As of December 31, 2017, we suffered from a working capital deficit of $36,140. Our continuation as a going concern is dependent upon improving our profitability and the continuing financial support from our stockholders or other capital sources. Management believes that the continuing financial support from the existing shareholders and external financing will provide the additional cash to meet our obligations as they become due.

These consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets and liabilities that may result in the Company not being able to continue as a going concern.

The following table sets forth certain operational data for the years indicated:

| Fiscal Years Ended December 31, | ||||||||

| 2017 | 2016 | |||||||

| Revenues | $ | 773,468 | $ | 443,797 | ||||

| Cost of revenue | (510,204 | ) | (289,404 | ) | ||||

| Gross profit | 263,264 | 154,393 | ||||||

| General and administrative expenses | (374,090 | ) | (131,110 | ) | ||||

| Income from operation | (110,826 | ) | 23,283 | |||||

| Other expense, net | (2,106 | ) | (2,153 | ) | ||||

| Income tax expense | (14,710 | ) | (1,964 | ) | ||||

| Net (loss) income | (127,642 | ) | 19,166 | |||||

| 17 |

Revenue. We generated revenues of $773,468 and $443,797 for the fiscal years ended December 31, 2017 and 2016. The increase in revenue is attributable to our increase in the market share of the logistic service for cable supplying industry in Hong Kong and our contract with Shanghai Yunda Cargo Limited. On a going forward basis, we expect revenue to Increase once we begin our vehicles sales business.

During the years ended December 31, 2017, and 2016, the following customers accounted for 10% or more of our total net revenues:

| Year ended December 31, 2017 | December 31, 2017 | |||||||||||

| Revenues | Percentage of revenues | Trade accounts receivable | ||||||||||

| Peaceman Cable Engineering Limited | $ | 295,534 | 38% | – | ||||||||

| Hip Tung Cables Company Limited | 183,390 | 24% | – | |||||||||

| TOTAL | 478,924 | 62% | – | |||||||||

| Year ended December 31, 2016 | December 31, 2016 | |||||||||||

| Revenues | Percentage of revenues | Trade accounts receivable | ||||||||||

| Peaceman Cable Engineering Limited | $ | 172,971 | 39% | 32,777 | ||||||||

| Hip Tung Cables Company Limited | 84,926 | 19% | – | |||||||||

| TOTAL | 257,897 | 58% | 32,777 | |||||||||

Cost of Revenue. Cost of revenue as a percentage of net revenue was approximately 66%, or $510,204, for the fiscal year ended December 31, 2017. Cost of revenue as a percentage of net revenue was approximately 65%, or $289,404, for the fiscal year ended December 31, 2016.

Gross Profit. We achieved a gross profit of $263,264 and $154,393 for the fiscal years ended December 31, 2017, and 2016, respectively. The increase in gross profit is primarily attributable to the growth of our business in Hong Kong and our contract with Shanghai Yunda Cargo Limited.

General and Administrative Expenses (“G&A”). We incurred G&A expenses of $374,090 and $131,110 for the fiscal years ended December 31, 2017, and 2016, respectively. The increase in G&A is primarily attributable to costs associated with implementing our business plan of expansion.

G&A as a percentage of net revenue was approximately 48% and 30% for the fiscal years ended December 31, 2017 and 2016, respectively. As a general matter, we expect our G&A to increase in the foreseeable future as we expand our business operations.

Other Expense, net. We incurred net other expenses of $2,106 for the fiscal year ended December 31, 2017, as compared to net other expenses of $2,153 for the fiscal year ended December 31, 2016. Our net other expenses for the years ended December 31, 2017 and 2016 consisted primarily of interest expenses.

Income Tax Expense. We recorded income tax expenses of $14,710 and $1,964 for the fiscal years ended December 31, 2017 and 2016. Even though we increased our revenues, our income tax expense decreased as the expenses of associated with the outsourcing of transportation offset the effect of the revenue increase.

Liquidity and Capital Resources

As of December 31, 2017, we had cash and cash equivalents of $99,583, purchase deposit of $194.852 and net loss of $127,642.

| 18 |