UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2017

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From ________ to _________

Commission file number: 000-55791

________________________________________________

VICI PROPERTIES INC.

(Exact name of registrant as specified in its charter)

________________________________________________

Maryland | 81-4177147 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

8329 W. Sunset Road, Suite 210 Las Vegas, Nevada 89113

(Address of Principal Executive Offices) (Zip Code)

Registrant’s telephone number, including area code: (702) 820-3800

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of each class | Name of each exchange on which registered | |

Common stock, $0.01 par value | New York Stock Exchange | |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | o | Accelerated filer | o |

Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | o |

Emerging growth company | o | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

As of June 30, 2017 (the last day of the registrant’s most recently completed second fiscal quarter), the registrant’s common stock was not listed on any exchange or over-the-counter market. The registrant’s common stock was first publicly traded on the OTC Markets Group, Inc.’s “Grey Market” on October 18, 2017 and began trading on the New York Stock Exchange on February 1, 2018. As of February 28, 2018, the aggregate market value of the common stock held by non-affiliates of the registrant was approximately $7.23 billion.

As of February 28, 2018, the registrant had 370,128,832 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2018 annual meeting of stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K. Such proxy statement, or an amendment to this Annual Report on Form 10-K, will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the calendar year to which this report relates.

TABLE OF CONTENTS | Page | |

PART I

In this Annual Report on Form 10-K, the words “VICI,” “VICI REIT,” “Company,” “we,” “our,” and “us” refer to VICI Properties Inc., unless otherwise stated or the context requires otherwise.

We refer to (i) our Consolidated Financial Statements as our “Financial Statements,” (ii) our Consolidated Statement of Operations as our “Statement of Operations,” and (iii) our Consolidated Balance Sheets as our “Balance Sheet.” References to numbered “Notes” refer to Notes to our Consolidated Financial Statements included in Item 8.

“CEOC” refers to Caesars Entertainment Operating Company, Inc., a Delaware corporation, and its subsidiaries, prior to the October 6, 2017 (the “Formation Date”), and following the Formation Date, CEOC, LLC, a Delaware limited liability company and its subsidiaries. CEOC is a subsidiary of Caesars.

“Caesars” or “CEC” refers to Caesars Entertainment Corporation and its subsidiaries. “CRC” refers to Caesars Resort Collection, LLC, a Delaware limited liability company which is a subsidiary of Caesars.

“VICI PropCo” refers to VICI Properties 1 LLC, a Delaware limited liability company, which through its subsidiaries owns the real estate assets transferred by CEOC to VICI on the Formation Date and “CPLV” refers to the Caesars Palace Las Vegas facility located on the Las Vegas Strip, which was owned by CEOC prior to the Formation Date and whose related real estate assets were transferred by CEOC to us on the Formation Date.

“HLV” refers to the real estate of Harrah’s Las Vegas Hotel & Casino facility located on the Las Vegas Strip which we purchased from a subsidiary of CRC on December 22, 2017.

“HLV Lease Agreement” refers to the lease agreement for the Harrah’s Las Vegas facilities. “CPLV Lease Agreement” refers to

the lease agreement for Caesars Palace Las Vegas; “Joliet Lease Agreement” refers to the lease agreement for the facilities in Joliet, Illinois; and the“Non-CPLV Lease Agreement” refers to the lease agreement for regional properties other than the facilities in Joliet, Illinois (together, the “Formation Lease Agreements”). “Lease Agreements” refers collectively to the CPLV Lease Agreement, the Non-CPLV Lease Agreement, the Joliet Lease Agreement and the HLV Lease Agreement, unless the context otherwise requires.

ITEM 1. | Business |

Overview of the Company

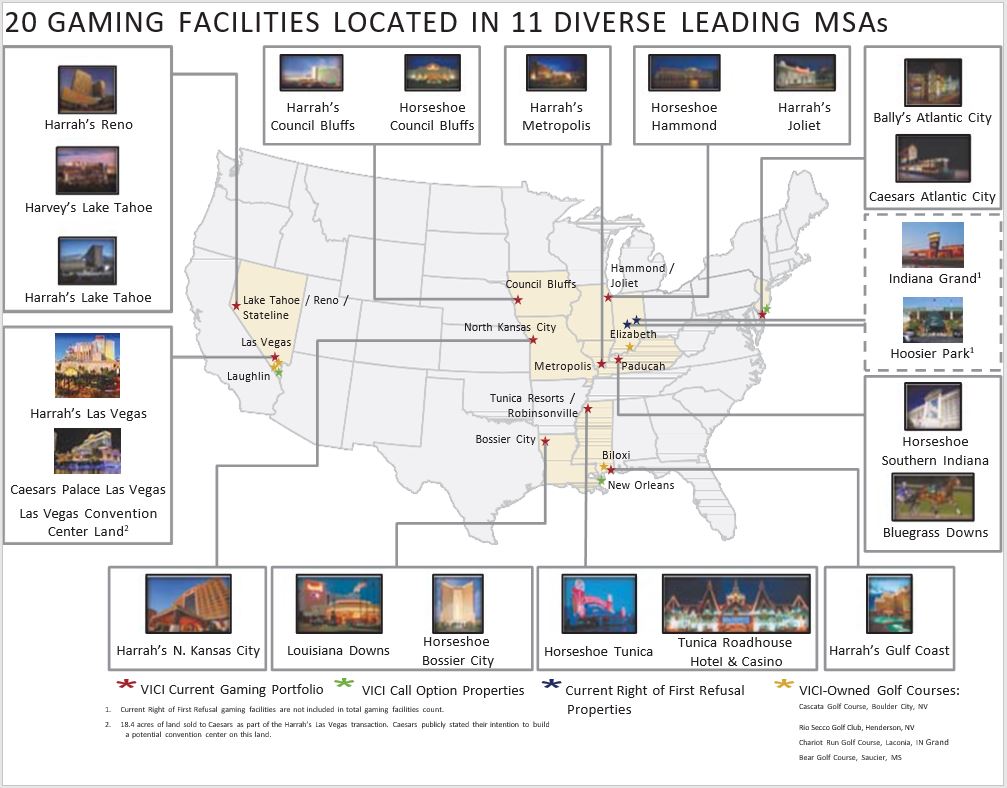

We are an owner and acquirer of experiential real estate assets across leading gaming, hospitality, entertainment and leisure destinations. Our national, geographically diverse portfolio consists of 20 market-leading properties, including Caesars Palace Las Vegas and Harrah’s Las Vegas, two of the most iconic entertainment facilities on the Las Vegas Strip. Our entertainment facilities are leased to leading brands that seek to drive consumer loyalty and value with guests through superior services, experiences, products and continuous innovation. Across more than 36 million square feet, our well-maintained properties are located in nine states, contain nearly 14,500 hotel rooms and feature over 150 restaurants, bars and nightclubs. Our portfolio also includes approximately 34 acres of undeveloped land adjacent to the Las Vegas Strip that is leased to Caesars, which we may look to monetize as appropriate. We also own and operate four championship golf courses located near certain of our properties, two of which are in close proximity to the Las Vegas Strip. As a growth focused public real estate company, we expect our relationship with our partners will position us for the acquisition of additional properties across leisure and hospitality.

In December 2017, we acquired from an affiliate of Caesars and then leased back the real estate assets of Harrah’s Las Vegas for approximately $1.14 billion, and we simultaneously sold to Caesars approximately 18.4 acres of undeveloped land located behind the LINQ Hotel & Casino and Harrah’s Las Vegas for $73.6 million (the “Eastside Property”). Simultaneous with this transaction, VICI PropCo entered into a new credit facility (the “VICI PropCo Credit Facility”), comprised of a $2.2 billion senior secured term loan B facility (the “Term Loan B Facility”) and a $400.0 million senior secured revolving credit facility (the “Revolving Credit Facility”), and we used the proceeds from the Term Loan B Facility and drawings under the Revolving Credit Facility to refinance a portion of our outstanding long-term debt.

Our portfolio is competitively positioned and well-maintained. Pursuant to the terms of the Lease Agreements, which require Caesars to invest in our properties, and in line with its commitment to build guest loyalty, we anticipate Caesars will continue to make strategic value-enhancing investments in our properties over time, helping to maintain their competitive position. In addition,

1

given our scale and deep industry knowledge, we believe we are well-positioned to execute highly complementary single-asset and portfolio acquisitions to augment growth.

We intend to elect and qualify to be taxed as a REIT for U.S. Federal income tax purposes commencing with our taxable year ended December 31, 2017. We believe our election of REIT status combined with the income generation from the Lease Agreements will enhance our ability to make distributions to our stockholders, providing investors with current income as well as long-term growth.

Recent Developments

On February 5, 2018, the Company completed an initial public offering of 69,575,000 shares of common stock (which included 9,075,000 shares of common stock related to the overallotment option exercised by the underwriters in full) at an offering price of $20.00 per share for gross proceeds of $1,391.5 million, resulting in net proceeds of approximately $1,307.0 million after commissions and expenses. The Company utilized a portion of the net proceeds from the stock offering to: (a) pay down $300.0 million of indebtedness outstanding under the Revolving Credit Facility; (b) redeem $268.4 million in aggregate principal amount of the Second Lien Notes at a redemption price of 108% plus accrued and unpaid interest to the date of the redemption; and (c) repay $100.0 million of the Term Loan B Facility.

Our Competitive Strengths

We believe the following strengths effectively position us to execute our business and growth strategies:

Leading portfolio of high-quality experiential gaming, hospitality, entertainment and leisure assets.

Our portfolio features Caesars Palace Las Vegas and Harrah’s Las Vegas and market-leading regional properties with significant scale. Our properties are well-maintained and leased to leading brands, such as Caesars, Horseshoe, Harrah’s and Bally’s. These brands seek to drive loyalty and value with guests through superior service and products and continuous innovation. Our portfolio benefits from its strong mix of demand generators, including casinos, guest rooms, restaurants, entertainment facilities, bars and nightclubs and convention space. We believe our properties are well-insulated from incremental competition as a result of high replacement costs, as well as regulatory restrictions and long-lead times for new development. The high quality of our properties appeals to a broad base of customers, stimulating traffic and visitation.

Our portfolio is anchored by our Las Vegas properties, Caesars Palace Las Vegas and Harrah’s Las Vegas, which are located at the center of the Strip. We believe Las Vegas is one of the most attractive travel destinations in the United States, with a record 42.9 million visitors in 2016, according to the Las Vegas Convention and Visitors Authority. We believe Las Vegas is a market characterized by steady economic growth and high consumer and business demand with limited new supply. Our Las Vegas properties, which are two of the most iconic entertainment facilities in Las Vegas, feature gaming entertainment, large-scale hotels, extensive food and beverage options, state-of-the-art convention facilities, retail outlets and entertainment showrooms. Our Las Vegas properties continue to benefit from positive macroeconomic trends, including, according to Caesars’ publicly available information, record visitation levels in 2016 and strong convention attendance, hotel occupancy and average daily rates, among other key indicators.

Our portfolio also includes market-leading regional resorts that we believe are benefiting from significant invested capital over recent years. The regional properties we own include award-winning land-based and dockside casinos, hotels and entertainment facilities that are market leaders within their respective regions. The properties operate primarily under the Caesars, Harrah’s, Horseshoe and Bally’s trademark and brand names, which, in many instances, have market-leading brand recognition.

Under the terms of the Lease Agreements, the tenants are required to continue to invest in the properties, which we believe will enhance the value of our properties.

Our properties feature diversified sources of revenue on both a business and geographic basis.

Our portfolio includes 20 geographically diverse casino resorts that serve numerous Metropolitan Statistical Areas (“MSAs”) nationally. This diversity reduces our exposure to adverse events that may affect any single market. This also allows our tenants to derive revenue from an economically diverse set of customers who work in a variety of industries. Additionally, although the Lease Agreements are with subsidiaries of Caesars, Caesars generates revenue from a diverse set of services that it offers its customers. These include gaming, food and beverage, entertainment, hospitality and other sources of revenue. We believe that this

2

geographic diversity and the diversity of revenue sources that our tenants derive from our leased properties improves the stability of rental revenue.

Our long-term Lease Agreements provide a highly predictable base level of rent with embedded growth potential.

Our properties are 100% occupied pursuant to our long-term triple-net Lease Agreements with subsidiaries of Caesars, providing us with a predictable level of rental revenue to support future cash distributions to our stockholders. In October 2017, we entered into the Formation Lease Agreements and in December 2017, we entered into the HLV Lease Agreement.

Caesars is generally not permitted to remove individual properties from the Non-CPLV Lease Agreement and has the right, following certain casualty events or condemnations, to terminate the respective Lease Agreement with respect to affected properties. All of our casino resort properties are established assets with extensive operating histories. Based on historical performance of the properties, we expect that the properties will generate sufficient revenues for Caesars’ subsidiaries to pay to us all rent due under the Lease Agreements.

We believe our relationship with Caesars, including our contractual agreements with it and its applicable subsidiaries, will continue to drive significant benefits and mutual alignment of strategic interests in the future.

Caesars or CRC guarantees the payment obligations of our tenants under the Lease Agreements.

All of our existing properties are leased to subsidiaries of Caesars. Caesars guarantees the payment obligations of our tenants under the Formation Lease Agreements and CRC, a subsidiary of Caesars, guarantees the payment obligations of our tenant under the HLV Lease Agreement. In addition to the properties leased from us, Caesars operates numerous other casino resorts, collectively comprising a nationally-recognized portfolio of brands, including Caesars, Harrah’s, Horseshoe and Bally’s, and operates its portfolio of properties (including the properties that are leased from us) using the Total Rewards® customer loyalty program. Core to Caesars’ cross market strategy, the Total Rewards® program is designed to encourage Caesars’ customers to direct a larger share of their entertainment spending to Caesars.

Experienced management team and independent board of directors with robust corporate governance

We have an experienced management team that has been actively engaged in the leadership, acquisition and investment aspects of the hospitality, gaming, entertainment and real estate industries throughout their careers. Our Chief Executive Officer, Edward Pitoniak, and President and Chief Operating Officer, John Payne, are industry veterans with an average of 30 years of experience in the REIT industry and experiential real estate companies, during which time they were able to drive controlled growth and diversification of significant real estate and gaming portfolios. Mr. Pitoniak’s service as an independent board member of public companies provides him with a unique and meaningful management perspective and will enable him to work as a trusted steward with our independent board of directors as a trusted steward of our extensive portfolio. Our independent board of directors, which is made of highly skilled and seasoned real estate, gaming and corporate professionals, was established to ensure that there was no overlap between our tenants and the companies with which our directors are affiliated. In addition, our board of directors is not staggered, with each of our directors subject to re-election annually. Robust corporate governance in the best interests of our stockholders is of central importance to the management of our company, as we have a separate Chairman of the Board and Chief Executive Officer and all members of our audit and finance committee qualify as an “audit committee financial expert” as defined by the SEC. Directors are elected in uncontested elections by the affirmative vote of a majority of the votes cast, and stockholder approval is required prior to, or in certain circumstances within twelve months following, the adoption by our board of a stockholder rights plan.

Tenants

As of December 31, 2017, all of our properties with the exception of the TRS golf courses were leased to Caesars.

Caesars is a leading owner and operator of gaming, entertainment and leisure properties. Caesars maintains a diverse brand portfolio with a wide range of options that appeal to a variety of gaming, travel and entertainment consumers. As of December 31, 2017, Caesars operates 48 properties, consisting of 20 owned and operated properties, eight properties that it manages on behalf of third parties and 20 properties that it leases from us. Caesars or CRC guarantee the lease payment obligations of the properties leased from us.

The historical audited and unaudited financial statements of Caesars (which are not included or incorporated by reference in this Annual Report on Form 10-K), as the parent and guarantor of CEOC, our significant lessee, have been filed with the Securities

3

and Exchange Commission (“SEC”). Caesars files annual, quarterly and current reports and other information with the SEC. Please call the SEC at 1-800-SEC-0330 for further information on the public reference rooms. Caesars’ SEC filings are also available to the public from the SEC’s web site at www.sec.gov. We make no representation as to the accuracy or completeness of the information regarding Caesars that is available through the SEC’s website or otherwise made available by Caesars or any third party, and none of such information is incorporated by reference in this Annual Report on Form 10-K.

Our Relationship with Caesars

We are independent from Caesars. Although we currently lease all our gaming facilities to subsidiaries of Caesars, we anticipate diversifying our portfolio over time.

We believe we have a mutually beneficial relationship with Caesars, a leading owner and operator of gaming, entertainment and leisure properties. Our long-term triple-net Lease Agreements with subsidiaries of Caesars provide us with a highly predictable revenue stream with embedded growth potential. We believe our geographic diversification limits the effect of changes in any one market on our overall performance. We are focused on driving long-term total returns through managing assets and allocating capital diligently, maintaining a highly productive tenant base, capitalizing on strategic development and redevelopment opportunities, and optimizing our capital structure to support opportunistic growth.

To govern the ongoing relationship between us and Caesars and our respective subsidiaries, we entered into various agreements with Caesars and/or its subsidiaries as described herein. The summaries presented below are not complete and are qualified in their entirety by reference to the full text of the applicable agreements, which are included as exhibits to this Annual Report on Form 10-K.

Overview of our Lease Agreements

We derive substantially all of our revenues from rental revenue from the leases of our properties to certain subsidiaries of Caesars pursuant to the Lease Agreements, each of which are “triple-net” leases, pursuant to which the tenant bears responsibility for all property costs and expenses associated with ongoing maintenance and operation, including utilities, property taxes and insurance.

Our leases provide for an initial term of 15 years, followed by four 5-year renewal options exercisable by the tenants, provided that for certain facilities the aggregate lease term, including renewals, may be cut back to the extent it would otherwise exceed 80% of the remaining useful life of the applicable leased property, solely at the option of the tenants. Caesars does not have any purchase option under the Lease Agreements, except with respect to the HLV Lease Agreement if we engage in certain transactions with entities deemed to be competitors, or the landlord under the lease otherwise becomes a competitor of Caesars.

Under the CPLV Lease Agreement entered into on October 6, 2017, rent is $165.0 million for the first seven years, subject to an annual escalator commencing in the second year of the lease term. Beginning in the eighth year, a portion of the rent amount will be designated as variable rent and will be adjusted periodically, with the balance of the rent amount designated as base rent and continuing to be subject to the annual escalator. At each renewal term, the base rent amount will be set at fair market value for the rent but will not be less than the amount of base rent due from the tenant in the immediately preceding year nor will the base rent increase by more than 10% compared to the immediately preceding year.

Under each of the Non-CPLV Lease Agreement and Joliet Lease Agreement entered into on October 6, 2017, rent is $433.3 million and $39.6 million, respectively, for the first seven years, subject to an annual escalator commencing in the sixth year of the lease term. With respect to the Joliet Lease Agreement, we are entitled to receive 80% of the rent thereunder pursuant to the operating agreement of our joint venture, Harrah’s Joliet Landco LLC. Beginning in the eighth year, a portion of each rent amount will be designated as variable rent and will be adjusted periodically, with the balance of the rent amount designated as base rent and continuing to be subject to the annual escalator. At each renewal term, each base rent amount will be set at fair market value for the rent but will not be less than the amount of base rent due from the applicable tenant in the immediately preceding year nor will such base rent increase by more than 10% compared to the immediately preceding year.

Under the HLV Lease Agreement entered into on December 22, 2017, rent is $87.4 million for each of the first seven years of the lease term, subject to an annual escalator commencing in the second year of the lease term (subject to satisfaction of an EBITDAR to rent ratio commencing in the sixth year of the lease term). Beginning in the eighth year, a portion of the rent amount will be designated as variable rent and will be adjusted periodically. At each renewal term, the base rent amount will be set at fair market value for the rent but will not be less than the amount of base rent due from the tenant in the immediately preceding year nor will

4

the base rent increase by more than 10% compared to the immediately preceding year. The payment obligations under the HLV Lease Agreement are guaranteed by CRC under the Guaranty of the Lease.

The Lease Agreements provide for portions of the rent to be designated as variable rent with periodic variable rent resets following the seventh year and tenth year of the leases and at the commencement of each renewal term based on the tenant’s net revenue from the facilities at such time.

In each calendar year, CEOC must satisfy both of the following requirements (A) under the Non-CPLV Lease Agreement and Joliet Lease Agreement, expend a minimum of $100.0 million in capital expenditures (which may include certain expenditures incurred by a certain CEOC affiliate or with respect to certain other CEOC assets), which amount may be decreased under certain circumstances, such as removal of property from a Formation Lease Agreement due to casualty or condemnation or disposition of a material property, by an amount in proportion to the EBITDAR of the property being removed or disposed of, and (B) for each of the properties covered by the Formation Lease Agreements, expend an amount equal to at least 1% of actual net revenue (from the prior year) generated by the properties, as applicable, on capital expenditures that constitute installation or restoration and repair or other improvements of items with respect to the leased properties.

In addition, every rolling period of three years, CEOC must satisfy both of the following requirements: (A) under the Non-CPLV Lease Agreement and Joliet Lease Agreement, expend a minimum of $495.0 million in capital expenditures (which may include certain expenditures incurred by a certain CEOC affiliate or with respect to certain other CEOC assets), and (B) expend a minimum of $350.0 million in capital expenditures excluding capital expenditures for any services entity, foreign subsidiaries and unrestricted subsidiaries of CEOC, gaming equipment, corporate shared services and properties not included in the Formation Lease Agreements. These amounts, in each case, may be decreased under the same circumstances with respect to the annual requirement. Further, with respect to the requirement to expend a minimum of $350.0 million in capital expenditures, such capital expenditures will be allocated as follows: (i) $84.0 million to the facilities covered by the CPLV Lease Agreement; (ii) $255.0 million to the facilities covered by the Non-CPLV Lease Agreement and the Joliet Lease Agreement; and (iii) the balance to facilities covered by any Formation Lease Agreement in such proportion as CEOC may elect.

The HLV Lease Agreement requires the tenant thereunder to spend (x) $171 million in capital expenditures for the period commencing January 1, 2017 and ending December 31, 2021, and, (y) commencing in 2022, annually, 1% of the actual net revenue generated during the immediately prior year from such property on capital expenditures that constitute installation, restoration, repair, maintenance or replacement of physical improvements or other physical items with respect to the leased property under the HLV Lease Agreement.

In addition to customary default remedies, if CEOC does not spend the full amount of the minimum capital expenditures as required under the applicable Formation Lease Agreement, we have the right to seek the remedy of specific performance to require CEOC to spend any such unspent amount or deposit such amounts in a reserve account. CEOC’s obligations to spend the minimum capital expenditures will constitute monetary obligations included in Caesars’ obligations as guarantor with respect to these Formation Lease Agreements.

Caesars Guaranty

Pursuant to the Management and Lease Support Agreements, Caesars guarantees the payment and performance of all monetary obligations of CEOC and/or its subsidiaries under the Formation Lease Agreements and of the “User” under the Golf Course Use Agreement, subject to the following terms: (i) Caesars will be liable for the full amounts of the monetary obligations owed by our tenants and/or its subsidiaries in respect of the Formation Lease Agreements and of the “User” under the Golf Course Use Agreement (not merely for any deficiency amount), unless and until irrevocably paid in full; (ii) Caesars will have no obligation to make a payment with respect to the leases unless an event of default is continuing under the applicable Formation Lease Agreement; (iii) if an event of default under a Formation Lease Agreement occurs, Caesars will have no obligation to make a payment (other than payments in respect of such damages to which we are entitled due to a termination pursuant to the Formation Lease Agreements and enforcement costs), unless Caesars was given notice of the applicable default (or event or circumstance that is or would become a default) of our tenant and/or its subsidiaries under the CPLV Lease Agreement, the Non-CPLV Lease Agreement or Joliet Lease Agreement, as applicable, and, with respect to monetary defaults, did not cure such default within the period set forth in the agreements; (iv) Caesars’ and the Managers’ obligations with respect to each Management and Lease Support Agreement (including, without limitation, Caesars’ guaranty obligations with respect to a Formation Lease Agreement) will terminate in the event the applicable Formation Lease Agreement is terminated by us expressly in writing (or with our express written consent), except to the extent of any accrued and unpaid guaranty obligations through the date of such termination and such damages to which we are entitled due to such termination pursuant to the Formation Lease Agreements; and (v) Caesars’ obligations with respect to each

5

Management and Lease Support Agreement (including, without limitation, Caesars’ guaranty obligations with respect to a Formation Lease Agreement) will also terminate in the event (x) the Management and Lease Support Agreement is terminated by us, CEOC and/or its subsidiaries, the Manager and Caesars expressly in writing (or the parties’ express written consent), (y) a replacement Lease Agreement and Management and Lease Support Agreement are entered into by us, Caesars and/or its affiliates upon certain bankruptcy-related events (or if we elect in writing not to enter into such replacement agreements or such replacement agreements are not entered into as a direct and proximate result of our acts or failure to act in accordance with the Management and Lease Support Agreement provisions in respect of replacing such agreements) or (z) we terminate a Manager for cause (as defined in the Management and Lease Support Agreements) and an arbitrator appointed in accordance with the Management and Lease Support Agreements determines that cause did not exist. Notwithstanding the foregoing, Caesars’ guaranty obligations will continue (i) to the extent of any accrued and unpaid guaranty obligations through the date of termination of the guaranty and such damages to which we are entitled due to such termination pursuant to the Formation Lease Agreements and enforcement costs, (ii) during a two-year post-termination transition period during which the applicable Manager continues to act as manager and (iii) in all respects if the Managers are terminated for cause (as defined in the Management and Lease Support Agreements). Except as provided above, Caesars’ guaranty obligations under the Management and Lease Support Agreements will not terminate for any reason.

Collateral

Caesars’ guaranty of the Formation Leases is not currently collateralized. However, in the event that CEOC’s first lien debt is (i) guaranteed by Caesars and such guaranty is secured by Caesars’ or certain of its subsidiaries’ assets, or (ii) secured by Caesars’ or certain of its subsidiaries’ assets, then, unless the collateral is limited to the equity interests in CEOC, the collateral securing any such first lien debt of CEOC shall also serve as collateral for Caesars’ guaranty obligations pursuant to the Management and Lease Support Agreements on a pari passu basis with such CEOC first lien debt under the security agreement and any other related instruments securing CEOC’s first lien debt or the Caesars guaranty in respect of CEOC’s first lien debt (or any Caesars guaranty in respect of any refinancing thereof) in order to provide a security interest in all collateral thereunder to secure Caesars’ obligations under the Management and Lease Support Agreements. Such security interest will automatically be released upon the earlier to occur of (i) the termination of the security interest granted by Caesars or its subsidiaries securing CEOC’s first lien debt (or Caesars’ guaranty thereof) and (ii) (x) the date on which Caesars’ guaranty obligations under the Management and Lease Support Agreements have been irrevocably paid or (y) to the extent Caesars’ guaranty obligation under the Management and Lease Support Agreement is terminated by the express terms of the Management and Lease Support Agreements, twelve months after such termination. Such security interest would be a “silent” security interest that provides us with a secured claim against Caesars while any such Caesars debt guaranty or pledge of assets remains in effect, but we will have no voting, enforcement or default related rights with respect to such debt guaranty or collateral, unless and until the earlier of (x) the occurrence of a default in respect of any of Caesars’ guaranty obligations with respect to the Lease Agreements, or (y) the occurrence of an event of default that would cause the holders of CEOC’s first lien debt to take enforcement action in respect of the security interest in Caesars’ or its subsidiaries’ assets, in which case we would have all rights afforded to a secured creditor with respect such assets of Caesars and its subsidiary, including all rights available to holders of CEOC’s first lien debt. We would be a party to such security agreement and all related instruments that provide for such rights. The collateral that secures Caesars’ guaranty obligations will be the same collateral that secures any such Caesars debt guaranty obligations at any time, and Caesars’ guaranty obligations will be secured by such collateral on a pari passu basis with such Caesars debt guaranty obligations for so long as and at any time that such debt guaranty obligations are secured. Caesars will cause the parties benefitting from any security interest in Caesars’ or certain of its subsidiaries’ assets to enter into an intercreditor agreement containing, among other things, provisions governing the pari passu coverage of such collateral provisions and the “waterfall” by which any proceeds of, or collections on, the collateral will be distributed as between CEOC’s first lien debt and the lease guaranty obligations.

Caesars Covenants

The Management and Lease Support Agreements contain customary terms and waivers of all suretyship and other defenses by Caesars and include a covenant by Caesars requiring that (a) a sale of certain material assets by Caesars be for fair market value consideration, on arm’s-length terms in certain cases, with the approval of Caesars’ board of directors, and (b) non-cash dividends by Caesars are permitted only to the extent such dividends would not reasonably be expected to result in Caesars’ inability to perform its guaranty obligations under the Management and Lease Support Agreements

In addition, until October 6, 2023, or, if earlier, (x) on the date on which Caesars’ guaranty obligations under the Management and Lease Support Agreements have been irrevocably paid or (y) to the extent Caesars’ guaranty obligation under the Management and Lease Support Agreements are terminated by the express terms of the Management and Lease Support Agreements, twelve months after such termination, Caesars may not directly or indirectly (i) declare or pay, or cause to be declared or paid, any dividend,

6

distribution, any other direct or indirect payment or transfer (in each case, in cash, stock, other property, a combination thereof or otherwise) with respect to any of Caesars’ capital stock or other equity interests, (ii) purchase or otherwise acquire or retire for value any of Caesars’ capital stock or other equity interests, or (iii) engage in any other transaction with any direct or indirect holder of Caesars’ capital stock or other equity interests, which is similar in purpose or effect to those described above. However, Caesars will be permitted to execute such transactions if (a) Caesars’ equity market capitalization after giving effect to such dividend, distribution, or other transaction is at least $5.5 billion, (b) the amount of such dividend, distribution, or other transaction (together with any and all other such dividends and distributions and other transactions made under this clause (b) but excluding, any dividends, distributions or other transactions to be made under clause (c) or (d) below in such fiscal year), does not exceed, in the aggregate, (x) 25% of the net proceeds, up to a cap of $25 million in any fiscal year, from the disposition of assets by Caesars and its subsidiaries and (y) $100 million from other sources in any fiscal year, (c) Caesars’ equity market capitalization after giving effect to such dividend, distribution, or other transaction is at least $4.5 billion and such dividend, distribution or other transaction made under this clause (c) (excluding, any dividends, distributions or other transactions made under clause (b) above or clause (d) below in such fiscal year) is less than or equal to $125 million per annum and is funded solely by asset sale proceeds or (d) solely with respect to a transaction described in clause (a) above, the aggregate amount of such transactions (excluding transactions made under clause (b) or (c) above) is not more than $199.5 million. Similarly, until October 6, 2023, or earlier, (x) the date on which Caesars’ guaranty obligations under the Management and Lease Support Agreements have been irrevocably paid or (y) to the extent Caesars’ guaranty obligation under the Management and Lease Support Agreements are terminated by the express terms of the Management and Lease Support Agreements, twelve months after such termination, except in the case of the exceptions set forth under clauses (a) and (c) above, any net proceeds from the disposition of assets by Caesars or its subsidiaries in excess of $25 million that are directly or indirectly distributed to, or otherwise received by, Caesars in any fiscal year will not be used to fund any restricted payment of Caesars described above in clauses (i) through (iii) above.

Amended and Restated Right of First Refusal Agreement

We entered into an amended and restated right of first refusal agreement with Caesars (the “Amended and Restated Right of First Refusal Agreement”), which contains a right of first refusal in our favor, pursuant to which we have the right to own (and cause to be leased to, and managed by, Caesars (or its affiliate or affiliates)) any domestic gaming facility located outside of Greater Las Vegas, proposed to be acquired or developed by Caesars (and/or its subsidiaries) that is not (i) then subject to a pre-existing lease, management agreement or other contractual restriction that was not entered into in contemplation of such acquisition or development and which (x) was entered into on arms’-length terms and (y) would not be terminated upon or prior to such transaction, (ii) a transaction for which the opco/propco structure would be prohibited by applicable laws, rules or regulations or which would require governmental consent, approval, license or authorization (unless already received), (iii) any transaction that does not consist of owning or acquiring a fee or leasehold interest in real property, (iv) a transaction in which Caesars and/or its subsidiaries will not own at least 50% of, or control, the entity that will own the gaming facility, (v) a transaction in which one or more third parties will own or acquire, in the aggregate, a beneficial economic interest of at least 30% in the applicable gaming facility, and such third parties are unable, or make a bona fide, good faith refusal, to enter into the opco/propco structure, (vi) a transaction in which Caesars or its subsidiaries proposes to acquire a then-existing gaming facility from Caesars or its subsidiaries, and (vii) a transaction with respect to any asset remaining in CEOC after the formation transactions. The Amended and Restated Right of First Refusal further provides us, subject to certain exclusions, the right to acquire (and lease to Caesars) any of the properties that Caesars has recently agreed to acquire from Centaur Holdings, LLC, should Caesars determine to sell any such properties. If we decline to exercise our right of first refusal, the Non-CPLV and Joliet Lease Agreements will provide for the establishment of a variable rent floor applicable to any non-CPLV facility with respect to which the new facility is located within a 30-mile radius of such facility leased thereunder and outside of Greater Las Vegas. If we exercise such right, we and Caesars (or its designee) will structure such transaction in a manner that allows the subject property to be owned by us and leased to Caesars (or its designee). In such event, Caesars (or its designee) will enter into a lease with respect to the subject property whereby (i) rent thereunder will be established based on formulas consistent with the EBITDAR coverage ratio (determined based on the prior 12 month period) with respect to the Lease Agreement then in effect and (ii) such other terms as are agreed by the parties.

The Amended and Restated Right of First Refusal Agreement also contains a right of first refusal in favor of Caesars, pursuant to which Caesars will have the right to lease and manage any domestic gaming facility located outside of Greater Las Vegas, proposed to be acquired by us that is not: (i) any asset that is then subject to a pre-existing lease, management agreement or other contractual restriction that was not entered into in contemplation of such acquisition and which (x) was entered into on arms’ length terms and (y) would not be terminated upon or prior to closing of such transaction, (ii) any transaction for which the opco/propco structure would be prohibited by applicable laws, rules or regulations or which would require governmental consent, approval, license or authorization (unless already received), (iii) any transaction structured by the seller as a sale-leaseback, (iv) any transaction in which we and/or our affiliates will not own at least 50% of, or control, the entity that will own the gaming facility, and (v) any

7

transaction in which we or our affiliates propose to acquire a then-existing gaming facility from ourselves or our affiliates. If Caesars (or its designee) exercises such right, we and Caesars (or its designee) will structure such transaction in a manner that allows the subject property to be owned by us and leased to Caesars (or its designee). In such event, Caesars (or its designee) will enter into a lease with respect to the additional property whereby (i) rent thereunder will be established based on formulas consistent with the adjusted EBITDA coverage ratio (as set forth in the Amended and Restated Right of First Refusal Agreement) with respect to the lease then in effect and (ii) such other terms as are agreed by the parties.

In the event that the foregoing rights are not exercised by us or Caesars and CEOC, as applicable, each party will have the right to consummate the subject transaction without the other’s involvement, provided the same is on terms no more favorable to the counterparty than those presented to us or Caesars and CEOC, as applicable, for consummating such transaction.

The rights of first refusal will not apply if (A) the Management and Lease Support Agreements have been terminated or have expired by their terms or with our consent, (B) Caesars (or a subsidiary thereof) is no longer managing the facilities, or (C) a change of control occurs with respect to either Caesars or us.

Call Right Agreements

We entered into certain call right agreements (the “Call Right Agreements”), which provide our Operating Partnership with the opportunity to acquire Harrah’s Atlantic City, Harrah’s New Orleans and Harrah’s Laughlin (“Option Properties”) from Caesars, as applicable. Our Operating Partnership can exercise the call rights within five years from the Formation Date by delivering a request to the applicable owner of the property containing evidence of our ability to finance the call right. The purchase price for each property will be 10 multiplied by the initial property lease rent for the respective property, with the initial property lease rent for each property being the amount that causes the ratio of (x) EBITDAR of the property for the most recently ended four quarter period for which financial statements are available to (y) the initial property lease rent to equal 1.67.

Upon such election, if the owner of the property determines that (i) the sale of the property would not be permitted under a debt agreement under which at least $100.0 million of indebtedness (individually or in the aggregate) is outstanding, (ii) the consummation of the call right would not be approved by the applicable gaming authorities or (iii) the property is not for any other reason deliverable to our Operating Partnership, the owner may propose one or more replacement properties and the material terms of the purchase and if such proposal is at least as economically beneficial to us as the exercise of the call right, the parties must proceed with the sale of that property and any dispute with respect to the same (including whether such proposal was a qualifying proposal) will be submitted to arbitration.

If the exercise of the call right is not permissible because a debt agreement does not permit the sale and such limitation is not resolved within one year from exercise of the right and the owner has not made an alternative proposal, or has made an alternative proposal that is not at least as economically beneficial to us as the exercise of the call right, the owner must pay us an amount equal to the value of our loss, which, as of the Formation Date, was equal to $114.0 million, $84.0 million and $62.0 million for Harrah’s Atlantic City, Harrah’s New Orleans and Harrah’s Laughlin, respectively. These amounts will increase at a rate of 8.5% per annum, with annual compounding for the period from the date of each agreement until the date on which payment of the value loss amount is made.

If the exercise of the call right is not permissible due to a reason other than because of a debt limitation (including that the sale was not approved by the gaming authorities or the failure to obtain the consent of a landlord) and the owner has not made an alternative proposal, or has made an alternative proposal that is not at least as economically beneficial to us as the exercise of the call right, then the parties must use commercially reasonable efforts to resolve the issue until the earlier of (A) one year from the date of the exercise of the call right or (B) the date on which the parties determine that there is no reasonable chance that the issue will be resolved. If the applicable issue making the transaction impermissible is not resolved by the foregoing described deadline, the owner must use commercially reasonable efforts to sell the property to an alternative purchaser for the fair market value of the property. Upon the closing of any such alternative transaction, the net cash proceeds of the sale of the property will be allocated (i) first, to owner in an amount not to exceed the purchase price that would otherwise be determined in accordance with the applicable Call Right Agreement and (ii) any excess of such amount, to us (subject to any necessary approvals from applicable gaming authorities required for owner to pay, and us to receive, such funds).

If the exercise of the call right is permissible, the parties will use good faith, commercially reasonable efforts, for a period of ninety days following the delivery of the election notice to negotiate and enter into a sale agreement and conveyance and ancillary documents with respect to the applicable property together with a leaseback agreement.

8

Put-Call Agreement

HLV Owner and certain subsidiaries of Caesars entered into a put-call agreement (the “Put-Call Agreement”) which provides for (i) a put right in favor of Caesars, which, if exercised, would result in the sale by Caesars to HLV Owner and simultaneous leaseback by HLV Owner to Caesars of a convention center (the “Eastside Convention Center Property”) that Caesars may construct on the Eastside Property (the “Put Right”), (ii) if Caesars exercises the put right and, among other things, the sale of the Eastside Convention Center Property to HLV Owner does not close for certain reasons more particularly described in the agreement, then a repurchase right in favor of Caesars, which, if exercised, would result in the sale by HLV Owner to Caesars of HLV (the “HLV Repurchase Right”) and (iii) a call right in favor of HLV Owner, which, if exercised, would result in the sale by Caesars to HLV Owner and simultaneous leaseback by HLV Owner to Caesars of the Eastside Convention Center Property (the “Call Right”). The Put Right may be exercised by Caesars during the period of time commencing on January 1, 2024 and ending on December 31, 2024. If applicable, the HLV Repurchase Right may be exercised by Caesars during a one year period commencing on the date upon which the closing under the Put Right transaction does not occur and ending on the day immediately preceding the first anniversary thereof. The purchase price for HLV would be an amount equal to 13 times the rent due under the HLV Lease Agreement for the most recently ended four consecutive fiscal quarter period for which financial statements are available as of the date of Caesars’ election to execute the HLV Repurchase Right. If applicable, the Call Right may be exercised by HLV Owner during the period of time commencing on January 1, 2027 and ending on December 31, 2027. The purchase price for the Eastside Convention Center Property is equal to thirteen times the rent due in connection with the leaseback thereof which will be determined pursuant to the formulas set forth in the Put-Call Agreement. The Put-Call Agreement also provides that the closing of the applicable transaction(s) would occur approximately 180 days after the entering into of the purchase and sale agreement. Simultaneously with the execution of the Put-Call Agreement: (x) CRC entered into a Guaranty, whereby CRC guaranteed Caesars’ obligations to pay certain liquidated damages amounts and perform certain obligations in connection with the construction of the convention center, and (y) VICI Properties 1 LLC, a Delaware limited liability company (“VICI 1”), entered into a Guaranty, whereby VICI 1 guaranteed HLV Owner’s obligations to pay certain liquidated damages amounts.

Golf Course Use Agreement

Pursuant to the Golf Course Use Agreement, VICI Golf granted to CEOC and CES (collectively, the “users”) certain priority rights and privileges with respect to access and use of the following golf course properties: Rio Secco (Henderson, Nevada), Cascata (Boulder City, Nevada), Chariot Run (Laconia, Indiana) and Grand Bear (Saucier, Mississippi). Pursuant to the Golf Course Use Agreement, the users are granted specific rights and privileges to the golf courses, including (i) preferred access to tee times for guests of users’ casinos and/or hotels located within the same markets as the golf courses, (ii) preferred rates for guests of users’ casinos and/or hotels located within the same markets as the golf courses, and (iii) availability for golf tournaments and events at preferred rates and discounts. In addition, VICI Golf is required to reserve a certain number of tee times for users’ guests on any and all dates as well as make commercially reasonable efforts to place users’ guests once the aforementioned reserved tee times have been utilized and at all other times when tee time inventory is limited. Pursuant to the Golf Course Use Agreement, the users are required to use commercially reasonable efforts to refer to VICI Golf a minimum number of complimentary golf rounds per month at each of the golf courses. Payments under the Golf Course Use Agreement are comprised of a $10.0 million annual membership fee, $3.0 million of use fees and approximately $1.1 million of minimum rounds fees. The membership fee is subject to increase or decrease, as applicable, whenever rent under the Non-CPLV Lease Agreement is adjusted in accordance with the terms of the Non-CPLV Lease Agreement. The adjusted membership fee will be calculated based on the proportionate increase or decrease, as applicable, in rent under the Non-CPLV Lease Agreement. The use fees and minimum round fees are subject to an annual escalator equal to the greater of 2% and the increase in the Consumer Price Index from the prior year beginning at the times provided under the Golf Course Use Agreement.

Tax Matters Agreement

We have entered into a tax matters agreement (the “Tax Matters Agreement”), which addresses matters relating to the payment of taxes and entitlement to tax refunds by Caesars, CEOC, the Operating Partnership and us, and allocates certain liabilities, including providing for certain covenants and indemnities, relating to the payment of such taxes, receipt of such refunds, and preparation of tax returns relating thereto. In general, the Tax Matters Agreement provides for the preparation and filing by Caesars of tax returns relating to CEOC and for the preparation and filing by us of tax returns relating to us and our operations. To the extent that any matters contained in any tax return prepared by Caesars relate to our taxes, we have the right to review and comment on such items and, similarly, to the extent that any matters contained in any tax return prepared by us relate to CEOC’s taxes, Caesars has the right to review and comment on such items. Under the Tax Matters Agreement, Caesars has agreed to indemnify us for any taxes allocated to CEOC which we are required to pay pursuant to our tax returns and we have agreed to indemnify Caesars for any

9

taxes allocated to us which Caesars or CEOC is required to pay pursuant to a Caesars or CEOC tax return. We have the right to participate in the contest of any matters relating to any Caesars or CEOC tax return that relate to matters for which we have indemnification responsibilities, and Caesars will have the right to participate in the contest of any matters relating to any of our tax returns that relate to matters for which Caesars has indemnification responsibilities.

The Tax Matters Agreement sets forth the parties’ intent that certain transactions entered into as part of the Plan of Reorganization qualify as tax-free under the Code. The Tax Matters Agreement provides that Caesars, CEOC and we will not take certain actions which may be inconsistent with certain facts presented and representations made relating to the foregoing intended tax treatment without obtaining a supplemental ruling from the IRS or, if mutually agreed, an opinion of a nationally recognized law or accounting firm that such actions will not affect the foregoing intended tax treatment. The parties agreed generally not to file tax returns or take any other action (or refrain from taking action) in a manner inconsistent with the foregoing intended tax treatment. Under the Tax Matters Agreement, Caesars has agreed to indemnify us for taxes attributable to acts or omissions taken by Caesars and we have agreed to indemnify Caesars for taxes attributable to our acts or omissions, in each case that cause a failure of the transactions entered into as part of the Plan of Reorganization to qualify for the intended tax treatment described above.

Our Properties

10

The following table summarizes the properties that we own as of December 31, 2017. Our properties are diversified across a range of primary uses, including gaming, hotel, convention, dining, entertainment, retail, golf course and other resort amenities and activities.

MSA / Property | Location | Approx. Structure Sq Ft (000’s) | Hotel Rooms | ||||

Las Vegas—Destination Gaming | |||||||

Caesars Palace Las Vegas | Las Vegas, NV | 8,579 | 3,980 | ||||

Harrah’s Las Vegas | Las Vegas, NV | 4,100 | 2,530 | ||||

Cascata Golf Course | Boulder City, NV | 37 | N/A | ||||

Rio Secco Golf Course | Henderson, NV | 30 | N/A | ||||

San Francisco / Sacramento | |||||||

Harvey’s Lake Tahoe | Lake Tahoe, NV | 1,670 | 740 | ||||

Harrah’s Reno | Reno, NV | 1,371 | 930 | ||||

Harrah’s Lake Tahoe | Stateline, NV | 1,057 | 510 | ||||

Philadelphia | |||||||

Caesars Atlantic City | Atlantic City, NJ | 3,632 | 1,140 | ||||

Bally’s Atlantic City | Atlantic City, NJ | 2,547 | 1,250 | ||||

Chicago | |||||||

Horseshoe Hammond | Hammond, IN | 1,716 | N/A | ||||

Harrahs Joliet (1) | Joliet, IL | 1,011 | 200 | ||||

Dallas | |||||||

Horseshoe Bossier City | Bossier City, LA | 1,419 | 600 | ||||

Harrah’s Louisiana Downs | Bossier City, LA | 1,118 | N/A | ||||

Kansas City | |||||||

Harrah’s North Kansas City | North Kansas City, MO | 1,435 | 390 | ||||

Memphis | |||||||

Horseshoe Tunica | Robinsonville, MS | 1,008 | 510 | ||||

Tunica Roadhouse | Tunica Resorts, MS | 225 | 130 | ||||

Omaha | |||||||

Harrah’s Council Bluffs | Council Bluffs, IA | 790 | 250 | ||||

Horseshoe Council Bluffs | Council Bluffs, IA | 632 | N/A | ||||

Nashville | |||||||

Harrah’s Metropolis | Metropolis, IL | 474 | 260 | ||||

New Orleans | |||||||

Harrah’s Gulf Coast | Biloxi, MS | 1,031 | 500 | ||||

Grand Bear Golf Course | Saucier, MS | 5 | N/A | ||||

Louisville, KY | |||||||

Horseshoe Southern Indiana | Elizabeth, IN | 2,510 | 500 | ||||

Bluegrass Downs | Paducah, KY | 184 | N/A | ||||

Chariot Run Golf Course | Laconia, IN | 5 | N/A | ||||

Total | 24 | 36,586 | 14,420 | ||||

(1) Owned by Harrah’s Joliet LandCo LLC, a joint venture of which VICI PropCo is the 80% owner and the managing member. | |||||||

11

Las Vegas

Caesars Palace Las Vegas

Caesars Palace is a hotel and casino resort located in Las Vegas, Nevada. It was opened in 1966 and features six hotel towers uniquely designed to address the varied demands of our diverse customer base, 124,181 square feet of casino space including over 1,400 slot and table gaming units, a 14,187 square foot high limit casino area, a 4,557 square foot high limit slots area and a 24-hour poker room, approximately 300,000 square feet of meeting, convention and ballroom facilities, the 4,300-seat Colosseum entertainment venue, the 81,300 square foot OMNIA Nightclub, over 20 restaurants, lounges and bars, approximately 702,000 square feet of retail space, approximately 40,450 square feet of spa facilities and five swimming pools spanning eight acres.

Harrah’s Las Vegas

Harrah’s Las Vegas is a hotel and casino resort located in Las Vegas, Nevada. It was constructed in 1973 and features 90,600 square feet of casino space, 1,210 slot machines and 90 gaming tables. The property has 2,530 rooms and suites, 1,600 of which have been renovated over the past two years, 16 restaurants and bars, retail shopping, spa services and 24,000 square feet of meeting space.

San Francisco/Sacramento

Harrah’s Lake Tahoe

Harrah’s Lake Tahoe is a hotel and casino resort located on Lake Tahoe in Stateline, Nevada. It consists of a 45,136 square foot casino with nearly 900 slot and table-gaming units, a 510 room hotel and 18,000 square feet of meeting and event space. The property features eleven restaurants, shopping and nightlife venues and amenities, such as a spa and salon.

Harvey’s Lake Tahoe

Harvey’s Lake Tahoe is a hotel and casino resort located on Lake Tahoe in Stateline, Nevada. It consists of a 44,200 square foot casino, including over 800 slot and table-gaming units, a 740 room hotel and 19,000 square feet of meeting and event space. The property features nine restaurants, nightlife venues and amenities, such as an outdoor pool.

Harrah’s Reno

Harrah’s Reno is a hotel and casino resort located in Reno, Nevada. It consists of a 40,200 square foot casino, including over 650 slot and table-gaming units, a 930 room hotel and 21,765 square feet of meeting and event space. The property features six restaurants, nightlife venues and amenities, such as a spa and salon and an outdoor pool.

Philadelphia

Bally’s Atlantic City

Bally’s Atlantic City is a hotel and casino resort located along the Boardwalk in Atlantic City, New Jersey. It was opened in 1979 and consists of a 121,624 square foot casino, including over 1,900 slot and table-gaming units, a 1,251 room hotel, 63,589 square feet of convention center space, eight restaurants, four lounges and bars, shopping venues and a spa with indoor pool.

Caesars Atlantic City

Caesars Atlantic City is a hotel and casino resort located in Atlantic City, New Jersey. It was opened in 1979 and consists of an 115,225 square foot casino, including over 1,900 slot and table-gaming units, a 1,141 room hotel, 28,590 square feet of convention center space, a 1,100 seat concert venue, a 10,000 square foot multi-level nightclub, over 15 lounges and bars, a spa and an indoor/outdoor rooftop pool. The property also features 15 restaurants and shopping and entertainment venues and amenities.

Chicago

Harrah’s Joliet

Harrah’s Joliet is a hotel and casino resort located in the Chicagoland area of Illinois owned by a joint venture of which VICI PropCo is the 80% owner and managing member. It consists of a 39,000 square foot casino, including over 1,000 slots and table-

12

gaming units, a 200 room hotel, four restaurants and 6,110 square feet of meeting and event space. The property also features nightlife offerings.

Horseshoe Hammond

Horseshoe Hammond is a casino resort located in Hammond, Indiana. It consists of a 121,479 square foot casino, including over 2,600 slot and table-gaming units and a 2,500 seat concert venue. The property features seven restaurants as well as nightlife offerings.

Dallas

Harrah’s Louisiana Downs

Louisiana Downs is a “racino” located in Bossier City, Louisiana. It consists of a 12,000 square foot casino, including over 800 slot units and a race track. The property features five casual restaurants and three bars onsite.

Horseshoe Bossier City

Horseshoe Bossier City is a hotel and casino resort located in Bossier City, Louisiana. It consists of a 28,100 square foot casino, including over 1,400 slot and table-gaming units, a 604 room hotel and 21,594 square feet of meeting and event space. The property features seven restaurants, nightlife venues and amenities, such as a spa and an outdoor pool, and is adjacent to the Louisiana Boardwalk outlets.

Kansas City

Harrah’s North Kansas City

Harrah’s North Kansas City is a hotel and casino resort located in North Kansas City, Missouri. It consists of a 60,100 square foot casino, including over 1,300 slot and table-gaming units, a 390 room hotel and 12,800 square feet of meeting and event space. The property features four restaurants as well as nightlife venues.

Memphis

Horseshoe Tunica

Horseshoe Tunica is a hotel and casino resort located in Robinsonville, Mississippi. It consists of a 63,000 square foot casino, including nearly 1,200 slot and table-gaming units, a 505 room hotel and 2,079 square feet of meeting and event space. The property features six restaurants and entertainment venues and amenities, such as a spa and outdoor pool.

Tunica Roadhouse

Tunica Roadhouse is a hotel and casino resort located in Tunica Resorts, Mississippi. It consists of a 33,000 square foot casino, including over 700 slot and table-gaming units, a 130 room hotel and 10,200 square feet of meeting and event space. The property features entertainment venues and amenities, such as a spa and outdoor pool.

Omaha

Harrah’s Council Bluffs

Harrah’s Council Bluffs is a hotel and casino resort located in Council Bluffs, Iowa, across the Missouri River from Omaha, Nebraska. It consists of a 25,000 square foot casino, including over 500 slot and table gaming units, a 250 room hotel, three restaurants and 5,731 square feet of meeting and event space. The property also features nightlife offerings.

Horseshoe Council Bluffs

Horseshoe Council Bluffs is a casino resort located in Council Bluffs, Iowa. It consists of a 78,800 square foot casino, including over 1,400 slot and table-gaming units. The property features three restaurants as well as nightlife offerings.

13

Nashville

Harrah’s Metropolis

Harrah’s Metropolis is a hotel and casino resort located in Metropolis, Illinois. It consists of a 23,669 square foot casino, including over 850 slot and table-gaming units and a 260 room hotel. The property features three restaurants as well as nightlife offerings.

New Orleans

Harrah’s Gulf Coast

Harrah’s Gulf Coast is a hotel and casino resort located in Biloxi, Mississippi, which replaced the former Grand Casino Biloxi which was destroyed by Hurricane Katrina. It was opened in 2006 and consists of a 31,300 square foot casino, including over 500 slot and table-gaming units and a 500 room hotel. The property features five restaurants, a 16,000 square foot spa and salon and an outdoor pool. The Great Lawn, a festival-style green space, features a 10.5 acre outdoor concert space along the waterfront. The resort also has access via the Golf Course Use Agreement, to the Grand Bear Golf Course described below.

Louisville

Bluegrass Downs

Bluegrass Downs is a live harness horse racing track located in Paducah, Kentucky.

Horseshoe Southern Indiana

Horseshoe Southern Indiana is a hotel and casino resort located in Elizabeth, Indiana. It consists of an 86,600 square foot casino, including over 1,700 slot and table-gaming units, a 503 room hotel and 24,000 square feet of convention center space. The property features eight restaurants and entertainment venues and amenities, such as a spa and local golf course.

Golf Courses

We own and operate four golf courses, located near some of our properties, two of which are close to Caesars Palace and Harrah’s Las Vegas. Cascata was built in 2000 by golf course architect Rees Jones. It is located southeast of Las Vegas, in Boulder City, Nevada, approximately 25 miles from the Strip, and includes a clubhouse with a restaurant, golf shop, and event space. Rio Secco, designed by Rees Jones, opened in 1997 and is located in the south Las Vegas foothills, in Henderson, Nevada, approximately 14 miles from the Strip. The course operates the Butch Harmon School of Golf and includes a clubhouse with a restaurant, golf shop and event space.

Chariot Run is a Bill Bergin-designed, equestrian-themed, bent-grass course. It opened in 2002 and is located 12 miles from the Horseshoe Southern Indiana Casino. The course includes a clubhouse with a dining room, pro shop and event space. Grand Bear is an 18-hole course set over 650 acres of rolling land in the piney woods of the DeSoto National Forest. The course, designed by Jack Nicklaus, is considered one of the top courses in the Southern United States and is a short drive from the Harrah’s Gulf Coast casino. The course includes a clubhouse with a restaurant and golf shop.

Segment Information

Please see the accompanying consolidated financial statements and notes thereto included elsewhere in this Annual Report on Form 10-K for financial information about the Company's reportable segments.

Competition

We compete for real property investments with other REITs, gaming companies, investment companies, private equity and hedge fund investors, sovereign funds, lenders and other investors. In addition, revenues from our properties are dependent on the ability of our tenants, currently subsidiaries of Caesars, and operators to compete with other gaming operators. The operators of our properties compete on a local and regional basis for customers. The gaming industry is characterized by a high degree of competition among a large number of participants, including riverboat casinos, dockside casinos, land-based casinos, video lottery, sweepstakes and poker machines not located in casinos, Native American gaming, emerging varieties of Internet gaming and other forms of gaming in the United States.

14

As a landlord, we compete in the real estate market with numerous developers and owners of properties. Some of our competitors are significantly larger, have greater financial resources and lower costs of capital than we have, have greater economies of scale and have greater name recognition than we do. Increased competition will make it more challenging to identify and successfully capitalize on acquisition opportunities that meet our investment objectives. Our ability to compete is also impacted by national and local economic trends, availability of investment alternatives, availability and cost of capital, construction and renovation costs, existing laws and regulations, new legislation and population trends.

Employees

Approximately 140 employees were employed by us at December 31, 2017. These employees are employed either at our Operating Partnership or at our taxable REIT subsidiary, VICI Golf LLC (“VICI Golf”) or their respective subsidiaries.

Governmental Regulation and Licensing

The ownership, operation and management of gaming and racing facilities are subject to pervasive regulation. Each of our gaming and racing facilities is subject to regulation under the laws, rules, and regulations of the jurisdiction in which it is located. Gaming laws and regulations generally require gaming industry participants to:

• | ensure that unsuitable individuals and organizations have no role in gaming operations; |

• | establish and maintain responsible accounting practices and procedures; |

• | maintain effective controls over their financial practices, including establishment of minimum procedures for internal fiscal affairs and the safeguarding of assets and revenues; |

• | maintain systems for reliable record keeping; |

• | file periodic reports with gaming regulators; and |

• | ensure that contracts and financial transactions are commercially reasonable, reflect fair market value and are arms-length transactions. |

Gaming laws and regulations impact our business in two respects: (1) our ownership of land and buildings in which gaming activities are operated by subsidiaries of Caesars (or other tenants) pursuant to the Lease Agreements (or other lease agreements); and (2) the operations of subsidiaries of Caesars (or other tenants). Further, many gaming and racing regulatory agencies in the jurisdictions in which our tenants operate require us and our affiliates to apply for and maintain a license as a key business entity or supplier because of our status as landlord.

Our businesses and the business of Caesars (or other tenants) are also subject to various Federal, state and local laws and regulations in addition to gaming regulations. These laws and regulations include, but are not limited to, restrictions and conditions concerning alcoholic beverages, environmental matters, employees, health care, currency transactions, taxation, zoning and building codes and marketing and advertising. Such laws and regulations could change or could be interpreted differently in the future, or new laws and regulations could be enacted. Material changes, new laws or regulations, or material differences in interpretations by courts or governmental authorities could adversely affect our operating results.

Violations of Gaming Laws

If we, our subsidiaries or the tenants of our properties violate applicable gaming laws, our gaming licenses could be limited, conditioned, suspended or revoked by gaming authorities, and we and any other persons involved could be subject to substantial fines. Further, a supervisor or conservator can be appointed by gaming authorities to operate our gaming properties, or in some jurisdictions, take title to our gaming assets in the jurisdiction, and under certain circumstances, earnings generated during such appointment could be forfeited to the applicable jurisdictions. Violations of laws in one jurisdiction could result in disciplinary action in other jurisdictions. Finally, the loss of our gaming licenses could result in an event of default under our certain of our indebtedness, and cross-default provisions in our debt agreements could cause an event of default under one debt agreement to trigger an event of default under our other debt agreements. As a result, violations by us of applicable gaming laws could have a material adverse effect on us.

15

Review and Approval of Transactions

Substantially all material loans, leases, sales of securities and similar financing transactions by us and our subsidiaries must be reported to and in some cases approved by gaming authorities. Neither we nor any of our subsidiaries may make a public offering of securities without the prior approval of certain gaming authorities. Changes in control through merger, consolidation, stock or asset acquisitions, management or consulting agreements, or otherwise are subject to receipt of prior approval of gaming authorities. Entities seeking to acquire control of us or one of our subsidiaries must satisfy gaming authorities with respect to a variety of stringent standards prior to assuming control.

Insurance

The Lease Agreements require the tenants to maintain, with financially sound and reputable insurance companies (and in certain cases subject to the right of the tenants to self-insure), insurance (subject to customary deductibles and retentions) in such amounts and against such risks as are customarily maintained by similarly situated companies engaged in the same or similar businesses operating in the same or similar locations. The Lease Agreements provide that the amount and type of insurance that the tenants have in effect as of the commencement of the leases will satisfy for all purposes the requirements to insure the properties. However, such insurance coverage may not be sufficient to fully cover our losses.

Environmental Matters

Our properties are subject to environmental laws regulating, among other things, air emissions, wastewater discharges and the handling and disposal of wastes, including medical wastes. Certain of the properties we own utilize above or underground storage tanks to store heating oil for use at the properties. Other properties were built during the time that asbestos-containing building materials were routinely installed in residential and commercial structures. The Lease Agreements generally obligate our tenants to comply with applicable environmental laws and to indemnify us if its noncompliance results in losses or claims against us, and we expect that any future leases will include the same provisions for other operators. A tenant’s failure to comply could result in fines and penalties or the requirement to undertake corrective actions which may result in significant costs to the operator and thus adversely affect their ability to meet their obligations to us.

Pursuant to U.S. Federal, state and local environmental laws and regulations, a current or previous owner or operator of real property may be required to investigate, remove and/or remediate a release of hazardous substances or other regulated materials at, or emanating from, such property. Further, under certain circumstances, such owners or operators of real property may be held liable for property damage, personal injury and/or natural resource damage resulting from or arising in connection with such releases. Certain of these laws have been interpreted to be joint and several unless the harm is divisible and there is a reasonable basis for allocation of responsibility. We also may be liable under certain of these laws for damage that occurred prior to our ownership of a property or at a site where we sent wastes for disposal. The failure to properly remediate a property may also adversely affect our ability to lease, sell or rent the property or to borrow funds using the property as collateral.

In connection with the ownership of our current properties and any properties that we may acquire in the future, we could be legally responsible for environmental liabilities or costs relating to a release of hazardous substances or other regulated materials at or emanating from such property. We are not aware of any environmental issues that are expected to have a material impact on the operations of any of our properties

Intellectual Property