Exhibit

99.1

SIERRA METALS INC.

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2019

DATED: MARCH 30, 2020

Corporate Office:

161 Bay Street, Suite 4260

Toronto, Ontario

M5J 2S1

Table

of Contents

| Preliminary Notes |

1 |

| Corporate Structure |

4 |

| General Development of the Business |

5 |

| Description of the Business |

13 |

| Material Mineral Properties |

21 |

| Updated Mineral Resource and Mineral Reserve Information |

48 |

| Risk Factors |

52 |

| Dividends and Distributions |

63 |

| Description of Capital Structure |

63 |

| Market for Securities |

63 |

| Escrowed Securities |

64 |

| Directors and Officers |

64 |

| Audit Committee Information |

68 |

| Legal Proceedings and Regulatory Actions |

70 |

| Interest of Management and Others in Material Transactions |

71 |

| Transfer Agent and Registrar |

71 |

| Material Contracts |

71 |

| Interest of Experts |

72 |

| Additional Information |

72 |

ANNUAL INFORMATION FORM DATED MARCH 30, 2020

SIERRA METALS INC. (“Sierra”, “Sierra

Metals” or the “Company”)

Preliminary Notes

Effective Date of Information

The date of this Annual Information Form (the

“AIF”) is March 30, 2020. Except as otherwise indicated, the information contained herein is as at December

31, 2019.

Documents Incorporated by Reference

The information provided in this AIF is supplemented

by disclosure contained in the documents listed below which are incorporated by reference into this AIF. These documents must be

read together with the AIF in order to provide full, true and plain disclosure of all material facts relating to Sierra Metals.

The documents listed below are not contained within or attached to this document. The documents may be accessed on SEDAR at www.sedar.com

under the Company’s profile.

| Document |

Effective Date/

Period Ended |

Date Filed on

SEDAR website |

Document Category on the SEDAR Website |

| NI 43-101 Technical Report on Resources and Reserves, Yauricocha Mine, Yauyos Province, Peru (the “Yauricocha Technical Report”). |

October 31, 2019 |

February 3, 2020 |

Technical Report |

| NI 43-101 Preliminary Economic Assessment (“PEA”) for the Bolivar Mine, Mexico (the “Bolivar Technical Report”) |

October 31, 2017 |

August 23, 2018 |

Technical Report |

| NI 43-101 PEA for the Cusi Mine, Chihuahua State, Mexico (the “Cusi Technical Report”) |

August 31, 2017 |

August 2, 2018 |

Technical Report |

Cautionary Statement – Forward Looking

Information

This AIF contains “forward looking information”

within the meaning of Canadian securities laws related to the Company and its operations, and in particular, the anticipated developments

in the Company’s operations in future periods, the Company’s planned exploration activities, the adequacy of the Company’s

financial resources and other events or conditions that may occur in the future. Statements concerning mineral reserve and resource

estimates may also be considered to constitute forward-looking statements to the extent that they involve estimates of the mineralization

that will be encountered if and when the properties are developed or further developed. These statements relate to analyses and

other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management.

These forward-looking statements include, but

are not limited to: future production of silver, gold, lead, copper and zinc (collectively, the “metals”); future

cash costs per ounce or pound of the metals; the price of the metals; the effects of domestic and foreign laws, regulations and

government policies and actions affecting the Company’s operations or potential future operations; future successful development

of the Yauricocha mine in Yauyos Province, Peru (the “Yauricocha Mine”), the Bolivar mine in Chihuahua, Mexico

(the “Bolivar Mine”) and the Cusihuiriachic property in Chihuahua, Mexico (the “Cusi

Mine”) and other exploration and development projects; the sufficiency of the Company’s current working capital,

anticipated operating cash flow or the Company’s ability to raise necessary funds; estimated production rates for the metals

produced by the Company; timing of production; the estimated cost of sustaining capital; ongoing or future development plans and

capital replacement, improvement or remediation programs; the estimates of expected or anticipated economic returns from the Company’s

mining projects; future sales of the metals, concentrates or other future products produced by the Company; the SIB (as defined

herein) and the Company’s plans and expectations for its properties and operations.

Forward-looking information is subject to a

variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking

information, including, without limitation, risks inherent in the mining industry including environmental hazards, industrial

accidents, unusual or unexpected geological formations, floods, labour disruptions, explosions, cave-ins, weather conditions and

criminal activity; commodity price fluctuations; higher operating and/or capital costs; lack of available infrastructure; the

possibility that future exploration, development or mining results will not be consistent with the Company’s expectations;

risks associated with the estimation of mineral resources and the geology, grade and continuity of mineral deposits and the inability

to replace reserves; fluctuations in the price of commodities used in the Company’s operations; risks related to foreign

operations; changes in laws or policies, foreign taxation, delays or the inability to obtain necessary governmental permits; risks

relating to outstanding borrowings; issues regarding title to the Company’s properties; risks related to environmental regulation;

litigation risks; risks related to uninsured hazards; the impact of competition; volatility in the price of the Company’s

securities; global financial risks; inability to attract or retain qualified employees; potential conflicts of interest; risks

related to a controlling group of shareholders; dependence on third parties; differences in U.S. and Canadian reporting of mineral

reserves and resources; claims under U.S. securities laws; potential dilutive transactions; foreign currency risks; risks related

to business cycles; liquidity risks; reliance on internal control systems; credit risks; risks relating to climate change and

risks relating to coronavirus (COVID-19) (“COVID-19”).

Any statements that express or involve discussions

with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance

(often, but not always, using words or phrases such as “expects”, “anticipates”, “plans”, “projects”,

“estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”,

“potential” or variations thereof, or stating that certain actions, events or results “may”, “could”,

“would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these

terms and similar expressions) are not statements of historical fact and may be forward-looking information. Forward-looking information

is subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to

differ from those expressed or implied by the forward-looking information, including, without limitation: uncertainty of production

and cost estimates for the Yauricocha Mine, the Bolivar Mine and the Cusi Mine; uncertainty of production at the Company’s

exploration and development properties; risks and uncertainties associated with developing and exploring new mines including start-up

delays; risks and hazards associated with the business of mineral exploration, development and mining (including operating in foreign

jurisdictions, environmental hazards, industrial accidents, unusual or unexpected geological or structure formations, pressures,

cave-ins and flooding); risks and uncertainties relating to the interpretation of drill results and the geology, grade and continuity

of the Company’s mineral deposits; risks related to the Company’s ability to obtain adequate financing for the Company’s

planned development activities and to complete further exploration programs; fluctuations in spot and forward markets for the metals

and certain other commodities; risks related to general economic conditions, including recent market and world events and conditions;

inadequate insurance, or inability to obtain insurance, to cover these risks and hazards; relationships with and claims by

local communities and indigenous populations; diminishing quantities or grades of mineral reserves as properties are mined; challenges

to, or difficulty maintaining, the Company’s title to properties and continued ownership thereof; risks related to the Company’s

covenants with respect to the Corporate Facility (as hereinafter defined); changes in national and local legislation, taxation,

controls or regulations and political or economic developments or changes in Canada, Mexico, Peru or other countries where they

may carry on business; risks related to the delay in obtaining or failure to obtain required permits, or non-compliance with permits

the Company has obtained; increased costs and restrictions on operations due to compliance with environmental laws and regulations;

regulations and pending legislation governing issues involving climate change, as well as the physical impacts of climate change;

risks related to reclamation activities on the Company’s properties; uncertainties related to title to the Company’s

mineral properties and the surface rights thereon, including the Company’s ability to acquire, or economically acquire, the

surface rights to certain of the Company’s exploration and development projects; the Company’s ability to successfully

acquire additional commercially mineable mineral rights; risks related to currency fluctuations (such as the Canadian dollar, the

United States dollar, the Peruvian sol and the Mexican peso); increased costs affecting the mining industry, including occasional

high rates of inflation; increased competition in the mining industry for properties, qualified personnel and management; risks

related to some of the Company’s directors’ and officers’ involvement with other natural resource companies;

the Company’s ability to attract and retain qualified personnel and management to grow the Company’s business; risks

related to estimates of deferred tax assets and liabilities; risks related to claims and legal proceedings and the Company’s

ability to maintain adequate internal control over financial reporting.

This list is not exhaustive of the factors that

may affect any of the Company’s forward-looking information. Forward looking information includes statements about the future

and are inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially

from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors, including,

without limitation, those referred to in this AIF under the heading “Risk Factors”. The Company’s statements

containing forward-looking information are based on the beliefs, expectations and opinions of management on the date the statements

are made, and the Company does not assume any obligation to update forward-looking information if circumstances or management’s

beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one

should not place undue reliance on forward-looking information.

Classification of Mineral Reserves and Resources

In this AIF, the definitions of proven and probable

mineral reserves, and measured, indicated and inferred mineral resources are those used by the Canadian provincial securities regulatory

authorities and conform to the definitions utilized by the Canadian Institute of Mining, Metallurgy and Petroleum, as the CIM Definition

Standards on Mineral Resources and Mineral Reserves adopted by the CIM Council, as amended.

Cautionary Note to U.S. Investors concerning

Estimates of Mineral Reserves and Measured, Indicated and Inferred Mineral Resources

This AIF has been prepared in accordance

with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States

securities laws. The terms “mineral reserve”, “proven mineral reserve” and “probable mineral

reserve” are Canadian mining terms as defined in accordance with the Canadian Securities Administrators’ National

Instrument 43-101 – Standards of Disclosure for Mineral Projects

(“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum as the CIM Definition Standards

on Mineral Resources and Mineral Reserves adopted by the CIM Council, as amended. These definitions differ from the definitions

in SEC Industry Guide 7 under the United States Securities Act of 1933, as amended. Under SEC Industry Guide 7 standards, a “final”

or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in

any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the

appropriate governmental authority.

In addition, the terms “mineral resource”,

“measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are

defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and

are normally not permitted to be used in reports and registration statements filed with the United States Securities and Exchange

Commission (the “SEC”). Investors are cautioned not to assume that any part or all mineral deposits in these

categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as

to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part

of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral

resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to

assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Disclosure of “contained

ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers

to report mineralization that does not constitute “reserves” by SEC Industry Guide 7 standards as in place tonnage

and grade without reference to unit measures.

Accordingly, information contained in this AIF

contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject

to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Currency Information

All currency references in this AIF are in United

States dollars unless otherwise indicated. References to “Canadian dollars” or the use of the symbol “C$”

refers to Canadian dollars.

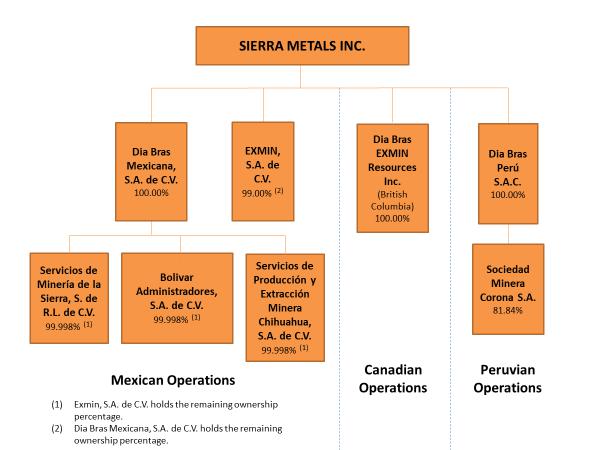

Corporate Structure

Name, Address and Incorporation

The Company was incorporated under the Canada

Business Corporations Act (the “CBCA”) on April 11, 1996 under the corporate name “Line Islands Exploration

Inc.”. The articles were amended by a certificate of amendment dated December 9, 1999 changing the corporate name to “Dia

Bras Exploration Inc.” The Company changed its name to “Sierra Metals Inc.” by a certificate of amendment dated

December 5, 2012. On June 19, 2014, the Company’s articles were further amended to provide that meetings of shareholders

may be held in (i) Canada, (ii) the United States of America or (iii) any city, municipality or other country in which the Company

is doing business.

The registered principal office of Sierra Metals

is located at 161 Bay Street, Suite 4260, Toronto, Ontario, Canada M5J 2S1. The head office of the Company’s Mexican subsidiaries

is located at Calle Blas Cano de los Rios No 500, Colonia San Felipe, C.P 31203, Chihuahua, Chihuahua, Mexico. The head office of the Company’s

Peruvian subsidiaries is located at Av. Pedro de Osma, 450 Barranco, Lima, Peru.

Intercorporate Relationships

The Company carries on a significant portion

of its business through a number of direct and indirect subsidiaries, as follows:

General Development of the Business

Three-Year History and Recent Developments

2017

Peru

On May 1, 2017, the Company announced the discovery

of a new high-grade oxide zone, referred to as the Esperanza North zone, which is located between the Esperanza zone and the Cachi-Cachi

Mine at the Yauricocha Mine. Drill results were also announced on this date, which demonstrate the extension of the high-grade

sulfide zone, referred to as the Cuye-Mascota zone, discovered in November 2016.

On October 26, 2017, the Company announced it

had updated its Mineral Reserve Estimate for the Yauricocha Mine showing estimated Mineral Reserves of 8,917,000 tonnes averaging

48.3 g/t silver, 1.2% copper, 0.8% lead, 2.4% zinc and 0.5 g/t gold, representing a 134% increase over the previous Mineral Reserve

Estimate.

On December 19, 2017, the Company announced

drilling results demonstrating new limestone replacement mineralization at the Cuye Zone extension located within the Central Mine

at Yauricocha.

Mexico

On February 27, 2017, the Company announced the discovery

of new high-grade silver intercepts occurring in the Santa Rosa de Lima complex located within the Cusi Mine operational area.

The discovery came as part of a reinterpretation of the Hydrothermal model and a drilling campaign consisting of 15,000 meters

which began in December 2016.

On March 6, 2017, the Company announced the results

of the initial drill program at the Bolivar Mine which continued to define high grade silver-gold and polymetallic mineralization

within the La Sidra vein. The mineralized zone extended to over 500 meters in length and 300 meters in depth and was still open

along strike and down dip.

Drilling programs also continued at Bolivar West with

future plans to drill Bolivar North West (skarn ore deposit area) in order to define high grade copper with coincident strong chargeability

and within resistivity zones detected during a completed 400 Hectare Titan 24 Induced Polarization (IP) survey conducted by Quantec

Geosciences of Toronto, Canada.

On April 17, 2019, the Company filed a NI 43-101 Technical

Report on Resources for the Cusi Mine in Mexico. The report provided support for total indicated mineral resources of 1,990,000

tonnes averaging 237 g/t silver, 0.53% lead, 0.53% zinc, 0.16 g/t gold, 283 g/t AgEq and 18.3 Moz AgEq; and total inferred mineral

resources of 1,200,000 tonnes averaging 305 g/t silver, 0.51% lead, 0.64% zinc, 0.14 g/t gold, 354 g/t AgEq and 13.7 Moz AgEq.

On April 19, 2017, the Company filed a NI 43-101 Technical

Report on Resources and Reserves for the Bolivar Mine in Mexico. The report provided support for total indicated mineral resources

of 9,335,000 tonnes averaging 18.1 g/t silver, 0.90% copper and 0.30 g/t gold, 1.23% CuEq; total inferred mineral resources of

9,055,000 tonnes averaging 17.9 g/t silver, 0.86% copper and 0.33 g/t gold, 1.20% CuEq; and total probable mineral reserves of

4,327,000 tonnes averaging 17.5 g/t silver, 0.85% copper and 0.31g/t gold, 1.18% Cu Eq.

On September 5, 2017, the Company announced assay results

from a completed definition drilling program at the Bolivar West zone, adjacent to the operations at the Bolivar Mine. The exploration

programs identified skarn ore deposits in the form of mantos in the area, extending for eight kilometers. The brownfield drilling

program was designed with a target of increasing the grades being mined at the Bolivar Mine and defining further mineral resources.

On October 4, 2017, the Company announced the initial

results of a drilling program designed to test the anomalies of the Titan 24 Geophysical Survey on the Bolivar Mine. The Titan

24 survey was completed to follow up on geophysical, geological and geochemical anomalies identified. The Titan 24 Geophysical

survey was carried out to assist in mapping the extent of the mantos and structures containing copper and copper/zinc skarn mineralization

for drill targeting in the immediate vicinity of the mine.

On December 29, 2017 the Company announced that it

had updated its Mineral Resource Estimate for the Cusi Mine. The updated Mineral Resource Estimate was the result of drilling programs

completed between January 2014 and August 2017. The update disclosed the following:

| · | Total Measured and Indicated Resources increased 129% to 4,557,000 tonnes from 1,990,000 tonnes

previously reported; and Total Inferred Resources increased 36% to 1,633,000 tonnes from 1,200,000 tonnes previously reported; |

| · | Total Measured Mineral Resources of 362,000 tonnes averaging 225g/t silver, 0.55% lead, 0.68% zinc,

0.13 g/t gold for a total 268 g/t Ag Eq; |

| · | Total Indicated Mineral Resources of 4,195,000 tonnes averaging 217 g/t silver, 0.64% lead, 0.66%

zinc, 0.21 g/t gold and 267 g/t AgEq; and |

| · | Total Inferred Mineral Resources of 1,633,000 tonnes averaging 158 g/t silver, 0.54% lead, 0.84%

zinc, 0.16 g/t gold and 207 g/t AgEq. |

Financing and Corporate Activities

Spin-off of Cautivo Mining Inc.

On August 8, 2017, the Company completed the

distribution of all of the common shares (the “Cautivo Shares”) of its wholly owned subsidiary, Cautivo Mining

Inc. (“Cautivo”) and listing of the Cautivo Shares on the Canadian Securities Exchange. The Cautivo Shares were

distributed to holders of the Company’s common shares (the “Common Shares”) of record as of 4:59 p.m.

(Toronto time) on July 26, 2017 as a return of capital, reducing the Company’s shareholdings in Cautivo from 100% to nil.

Management Changes

On March 29, 2017, the Company announced that

Mark Brennan tendered his resignation as President and Chief Executive Officer of the Company and on April 6, 2017, the Company

announced the appointment of Igor Gonzales as President and Chief Executive Officer, effective May 1, 2017.

U.S. Listing and ATM Offering

On May 18, 2017, the Company announced the filing of

a preliminary short form base shelf prospectus with the securities regulatory authorities in each of the provinces of British Columbia,

Alberta and Ontario, and a corresponding registration statement on Form F-10 (the “Registration Statement”)

with the SEC in accordance with the Multijurisdictional Disclosure System established between Canada and the

United States. A final short form base shelf prospectus (the “Shelf Prospectus”) was subsequently filed on June

29, 2017, providing for the offerings for sale of up to C$75 million of Common Shares, warrants, units and subscription receipts

or a combination thereof, from time to time, separately or together, in amounts, at prices and on terms to be determined based

on market conditions at the time of the sale and as set forth in an accompanying prospectus supplement. The Registration Statement

was declared effective by the SEC on July 7, 2017.

On July 6, 2017, the Company announced that its Common

Shares were approved for listing on the NYSE American Stock Exchange (the “NYSE American”) and were expected

to begin trading under the symbol “SMTS” beginning on July 11, 2017.

On October 10, 2017, the Company announced that it

entered into an Open Market Sale AgreementSM (the “Sales Agreement”) with Jefferies LLC, H.C. Wainwright

& Co., LLC, Scotia Capital (USA) Inc. and Noble Capital Markets, Inc. (collectively, the “Agents”), pursuant

to which the Company was permitted, at its discretion and from time to time during the term of the Sales Agreement, sell, through

the Agents, acting as agent and/or principal, such number of Common Shares as would result in aggregate gross proceeds to the Company

of up to US$55 million (the “ATM Offering”). Sales of Common Shares through the Agents, acting as agent, were

to be made through “at the market” issuances on the NYSE American at the market price prevailing at the time of each

sale. On October 10, 2017, the Company also filed a prospectus supplement for the ATM Offering pursuant to the Sales Agreement.

No Common Shares under such offering were offered or sold in Canada. The Sales Agreement expired on July 29, 2019, and as of such

date, the Company had not issued or sold any Common Shares pursuant to such agreement.

2018

Peru

On June 27, 2018, the Company reported the results

of a PEA for the Yauricocha Mine, yielding a 486% return on investment and after-tax net present value (“NPV”)

of US$393 million at an 8% discount rate. The PEA was compiled under NI 43-101 standards by Mining Plus Peru SAC.

On October 1, 2018, the Company confirmed the

discovery of a new style of mineralization (copper-molybdenum porphyry). The results were from testing of the geophysical anomalies

in the quartz monzonite intrusive, in the eastern part of the mineralized area. This area is known as the Central Mine which is

located between the Cuye and Esperanza zones. Prior evidence of copper-molybdenum porphyry mineralization had been observed on

surface within the monzonite intrusive and had previously been sampled by Rio Tinto Zinc. Subsequently, drill core was sampled

at 10-meter intervals over the entire hole length and the Company obtained 122 samples. A hole was drilled from the Klepetko Tunnel

to test the priority anomaly located in the monzonite intrusive as this zone had high conductivity within the Intrusive. A copper-molybdenum

mineralized porphyry was discovered.

Mexico

On May 22, 2018, the Company announced an update

to its Mineral Reserve and Resource Estimate for the Bolivar Mine. Total Probable Mineral Reserves for the Bolivar Mine were 7,925,000

tonnes averaging 19 g/t silver, 0.86% copper and 0.25 g/t gold, 1.14% CuEq representing an 83% increase to the previous Probable

Mineral Reserve Estimate. Total Indicated Mineral Resources were 13,267,000 tonnes averaging 22.5 g/t silver, 1.04% copper and

0.29 g/t gold, 1.37% CuEq representing a 42% increase to the previous Indicated Mineral Resource estimate. Total Inferred Mineral

Resources were 8,012,000 tonnes averaging 22 g/t silver, 0.96% copper and 0.30 g/t gold, 1.35% CuEq representing an 11.5% decrease

to the previous Inferred Mineral Resource Estimate.

On June 6, 2018, the Company announced the results

of an infill drilling program evaluating the continuity and characteristics of geophysical anomalies that were previously tested

as part of a recent Titan 24 Geophysical Survey and deemed high value targets at the Bolivar Mine. Drilling has identified and

defined a new zone named Cieneguita, which is an extension of the Bolivar northwest structure and is situated in close proximity

to the Bolivar northwest zone with similar characteristics. The Company completed a successful infill drilling program on those

previously tested areas, which resulted in a new structure being defined demonstrating the continuity of the previously defined

wide high-grade copper structures.

On June 18, 2018, the Company reported the results

of the Cusi Technical Report, yielding a 75% internal rate of return and after-tax NPV of US$92 million at an 8% discount rate.

The Cusi Technical Report was compiled under NI 43-101 standards by Mining Plus Peru SAC and was filed on SEDAR on August 2, 2018.

On June 29, 2018, the Company announced that

the development program at the Cusi Mine has confirmed a wide, high-grade silver stockwork zone located within the Santa Rosa

de Lima vein complex. This mineralized zone extends to over 100 meters in length, 40 meters in width and 70 meters in height.

On July 9, 2018, the Company reported the results

of the Bolivar Technical Report, yielding a 550% return on investment and after-tax NPV of US$214 million at an 8% discount rate.

The Bolivar Technical Report was compiled under NI 43-101 standards by Mining Plus Peru SAC and was filed on SEDAR on August 23,

2018.

Financing and Corporate Activities

Initiation of Normal Course Issuer Bid

On December 11, 2018, the Company announced that its

board of directors (the “Board”) approved a share repurchase program in the form of a normal course issuer bid

(the “NCIB”) in the open market through the facilities of the Toronto Stock Exchange (the “TSX”)

and other Canadian marketplaces/alternative trading systems. Pursuant to the NCIB, the Company proposed to repurchase for cancellation

up to 1,500,000 Common Shares, which represented approximately 0.92% of the issued and outstanding Common Shares as at December

11, 2018.

Under the NCIB, the Company was permitted

to purchase up to 1,500,000 Common Shares through the facilities of the TSX and other Canadian marketplaces/alternative trading

systems during the 12-month period commencing on December 17, 2018 and ending on or before December 16, 2019. Any Common Share

purchases made pursuant to the NCIB were to be at the prevailing market price at the time of the transaction, purchased in accordance

with the policies of the TSX and conducted by CIBC Capital Markets (“CIBC”). In accordance with TSX rules, any

daily purchases made under the NCIB were limited to a maximum of 4,214 Common Shares, which represented 25% of the average daily

trading volume of 16,858 Common Shares on the TSX for the six months ended November 30, 2018. However, the Company was permitted

to make one block purchase per calendar week which exceeded the daily repurchase restriction, up to and including the maximum annual

aggregate limit of 1,500,000 Common Shares.

2019

Peru

On February 13, 2019, the Company announced

that Sociedad Minera Corona, S.A. (“Minera Corona”), one of its Peruvian subsidiaries, received approval from

SENACE (National Environmental Certification Service), whom are the agency responsible for the evaluation of natural resources

and production projects in Peru, with respect to its recent Environmental Impact Assessment (“EIA”) study for

the expansion of the tailings deposition facility at the Yauricocha Mine. With this approval for the EIA study, the Company became

in a position to proceed to obtain a construction permit for the next phase of the tailings deposition facility, and commence planning

for an expanded waste rock facility. Once those steps have been completed, the Company will be able to complete a final submission

of its Informe Técnico Sustentatorio document (“ITS”)

(English translation: Supporting Technical Report), which is required for any potential expansion of the Yauricocha Mine.

On March 21, 2019, the Company announced that

employees who were members of the Union of the Mine and Metallurgical Workers of Minera Corona, representing approximately 66%

of the employees at the Yauricocha Mine, initiated a strike action in protest of contractor changes made as part of regular operations

at the Yauricocha Mine. The Company suspended all mining and milling activities for the safety of all employees as of March 19,

2019. The Peruvian Ministry of Labour, upon receiving notification by the Union of its intent to strike, indicated that the strike

could not proceed. Once the strike had materialized, they deemed the strike as illegal under current legislation. On April 12,

2019, the Company announced the resolution of the strike action at the Yauricocha Mine.

On June 27, 2019, the Company announced the

receipt of its permit to construct the expansion of the tailing dam facility as well as its permit for the surface drilling program

at the Yauricocha Mine.

On December 19, 2019, the Company announced

an updated Mineral Reserve and Resource Estimate at the Yauricocha Mine. The updated Mineral Reserve and Resource Estimate disclosed

the following:

| · | Mineral Reserves of 8,439,000 tonnes averaging 46.5 g/t silver, 1.1% copper, 0.8% lead, 3.1% zinc

and 0.5 g/t gold representing a 5.4% overall tonnage decrease to the previous Reserve Estimate, however, Proven Mineral Reserves

increased 45% with Probable Mineral Reserves decreasing 18% as compared to the previous Reserve Estimate. |

| · | Total Proven and Probable Contained Metal decreased by 8.9% silver, 10.9% copper, 4.6% lead, increased

by 20.1% zinc, and decreased by 8.9% gold as compared to the previous Reserve Estimate. |

| · | Measured and Indicated Mineral Resources of 12,651,000 tonnes averaging 51.5 g/t silver, 1.3% copper,

0.9% lead, 3.0% zinc and 0.6 g/t gold representing a 4% tonnage decrease from the previous resource tonnage estimate, however,

Measured Mineral Resources increased 18% with Indicated Mineral Resources decreasing 11% as compared to the previous Resource Estimate. |

| · | Total Measured and Indicated Contained Metal reduced by 21% silver, 15% copper, 7% lead, increased

by 8% zinc, and reduced by 12% gold as compared to the previous Resource Estimate. |

| · | Total Inferred Mineral Resources of 6,501,000 tonnes averaging 39.1 g/t silver, 1.5% copper, 0.6%

lead, 1.7% zinc and 0.5 g/t gold compared from the previous Resource Estimate, representing a 2% tonnage decrease to the overall

Inferred Resource Estimate. |

| · | Total Inferred Contained Metal reduced by 11% silver, 26% copper, increase by 32% lead, reduced

by 23% zinc and 9% gold as compared to the previous Resource Estimate. |

Mexico

On January 9, 2019, the Company reported

that its expansion plans were on track at the Bolivar Mine. In July 2018, the Company had announced the results of a PEA at Bolivar

to achieve a sustainable and staged increase in mine production and mill throughput from 3,000 tonnes per day (“tpd”)

to 3,600 tpd in Q1-2019, and to 5,000 tpd by mid-2020. Completion of the expansion included the installation of a refurbished mill,

an electrical substation with 1250 KVA of capacity, a secondary crusher and a hydrocyclone cluster that allowed for finer grind

size optionality.

On April 3, 2019, the Company announced positive results

from a drilling program designed to test the continuity and characteristics of geophysical anomalies identified in a recent Titan

24 Geophysical Survey. The areas drilled had been deemed as high-value targets within the Bolivar West zone, located at the Bolivar

Mine. Drilling identified and defined a new zone named West Extension to the Bolivar West zone which is an extension of the Bolivar

West structure and is within close proximity to the Bolivar West zone with similar characteristics.

On June 3, 2019, the Company announced that it had

agreed to repurchase a royalty on the Cusi Mine from Minera Cusi SA de CV, for US$4.0 million. The royalty agreement required the

Company to pay a 3% royalty on the net revenues generated by the mine, less transportation costs, for the life of the Cusi Mine.

The Company already paid US$2.5 million upon signing the repurchase contract on May 10, 2019 and is required to pay a further US$1.5

million on May 10, 2021.

On December 31, 2019, the Company announced an update

to its Mineral Resource Estimate at the Bolivar Mine. The updated Mineral Resource Estimate disclosed the following:

| · | Total Indicated Mineral Resources are 11.63 million tonnes averaging 0.95% copper, 18.1 g/t silver

and 0.24 g/t gold or 1.17% CuEq which represents a 12% overall tonnage decrease from the previous Indicated Resource Estimate,

but which includes depletions since the previous Resource Update. Metal grades were also reduced by 9% for copper, 20% for silver

and 17% for gold. |

| · | Total Inferred Mineral Resources are 16.69 million tonnes averaging 0.93% copper, 16.8 g/t silver

and 0.30 g/t gold or 1.16% CuEq which represents a 108% overall tonnage increase from the previous Inferred Resource Estimate.

Metal grades were reduced by 3% for copper, 25% for silver and 29% for gold. |

The Company is planning to release another

updated Mineral Resource and Reserve Estimate, which will include additional drilling and information from a litho-structural

model, by March 31, 2020, followed by a NI 43-101 technical report to be filed within 45 days of this update.

Financing and Corporate Activities

Repayment of FIFOMI Loan in Mexico

During February 2019, the Company repaid the remaining

US$1,657,000 owed on Dia Bras Mexicana S.A. de C.V. (“Dia Bras Mexicana”)’s loan from FIFOMI. Dia Bras

Mexicana is a wholly-owned subsidiary of Sierra Metals. This repayment, prior to the loan’s maturity date, did not result

in any financial penalties and was within the terms of the agreement.

Closing of New Senior Secured US$100 Million Corporate

Credit Facility

The Company, together with Dia Bras Peru S.A.C. and

Dia Bras Mexicana, as co-obligors, entered into a new six-year senior secured corporate credit facility (“Corporate Facility”)

dated March 8, 2019, as amended on July 11, 2019, with Banco de Credito del Peru, as lender, and Banco de Credito del Peru, as

administrative agent and agent of guarantees, that provides funding of up to US$100 million. The Corporate Facility provides the

Company with additional liquidity and will provide the financial flexibility to fund future capital projects in Mexico as well

as corporate working capital requirements. The Company also used a portion of the proceeds of the Corporate Facility to repay old

debt balances.

The key terms of the Corporate Facility are as follows:

| · | Term: 6-year term maturing March 2025 |

| · | Principal Repayment Grace Period: 2 years |

| · | Principal Repayment Period: 4 years |

| · | Interest Rate: 3.15% + LIBOR 3M |

The Corporate Facility is subject to customary covenants,

including consolidated net leverage and interest coverage ratios and customary events of default.

Changes to the Board

On April 4, 2019, the Company announced the appointment

of Ricardo Arrarte to the Board. Mr. Arrarte filled the vacancy created by the resignation of Philip Renaud.

On July 15, 2019, the Company announced

the appointment of Koko Yamamoto to the Board. Ms. Yamamoto was also appointed to the audit committee of the Board (the “Audit

Committee”) and would serve as its Chair.

Automatic Share Purchase Plan and NCIB Amendment

On April 15, 2019, the Company announced that, in connection

with its NCIB, it had entered into an automatic share purchase plan (the “ASPP”) with CIBC, the Company’s

designated broker for the NCIB.

The ASPP permitted CIBC to purchase Common Shares at

times when the Company ordinarily would not be active in the market due to insider trading rules and its own internal trading blackout

periods. Purchases were only to be made by CIBC based upon parameters set out by the Company prior to the commencement of any such

blackout period and in accordance with the terms of the ASPP. Outside of these blackout periods, Common Shares would continue to

be purchased at the Company’s discretion, subject to the rules of the TSX and applicable securities laws. The Company’s

NCIB commenced on December 17, 2018 and remained active until December 16, 2019.

On September 18, 2019, the Company announced its intention

to amend the NCIB to increase the number of Common Shares which the Company was permitted to repurchase for cancellation thereunder

from 1,500,000 Common Shares to 2,500,000 Common Shares. Other than the increase to the maximum number of Common Shares purchasable

by the Company pursuant to the NCIB, no other amendments had been made to the NCIB. The Company purchased a total of 2,012,654

Common Shares under the NCIB.

Management Changes

On August 1, 2019, the Company announced the mutually

agreed upon departure of Gordon Babcock, its Chief Operating Officer. Mr. Babcock’s responsibilities were taken over by Alonso

Lujan, Vice President Exploration and Country Manager Mexico, and James Leon, Country Manager Peru.

2020

On January 8, 2020, the Company announced that, as

a result of entering into a new phase as a generator of free cash flow, it was in a position to start returning capital to its

shareholders. In this regard, the Board approved a plan to return up to US$30 million to shareholders in the coming year. In furtherance

of this plan, the Company announced its intention to launch a substantial issuer bid (the “SIB”) pursuant to

which the Company would offer to repurchase for cancellation up to US$15 million in value of Common Shares from shareholders for

cash. The SIB was intended to proceed by way of a modified Dutch auction and would be funded with available cash on hand.

In the first quarter of 2020, metal prices

have weakened further due to the impact of COVID-19. While the Company now expects lower cash flows at least in the first half

of the year, the extent and duration of the impacts of COVID-19 on the metal prices and the operations of the Company are still

unknown at this time. Due to the highly uncertain economic situation as a result of COVID-19 and its impact on the Company’s

operations and metal prices, the Company has decided to postpone the contemplated SIB.

On February 3, 2020, the Company filed the Yauricocha

Technical Report.

On February 6, 2020, the Company announced the settlement

of the P&R Litigation (as defined herein). The accord was executed in The Second District Court (the “Court”)

in the state of Chihuahua, Mexico. The declaration of the termination of P&R Litigation was issued by the Court on February

6, 2020. This settlement ends all claims against and litigation against the Company and Dia Bras Mexicana from P&R. The impact

of the settlement amount paid on the Company’s financial condition and operating results is not significant. For further

details on the P&R Litigation, see “Legal Proceedings and Regulatory Actions – Legal Proceedings”.

On March 17, 2020, the Company announced that the Peruvian government

had declared a 15-day state of emergency to contain the advancement of COVID-19, which restricts travel within the country and

requires citizens to remain at home with the exception of grocery, banks and medical. On March 26, 2020, the Peruvian government

extended the state of emergency for an additional 13 days until April 12, 2020. As such, all mining activities and permitting submissions

in Peru have also been halted. This will result in a delay in all permits being issued. Pursuant to this declaration, the Company

has also ceased its mining operations at the Yauricocha Mine, with the exception of emergency staff as permitted by the government.

Due to the uncertainty of the effect that the COVID-19 pandemic could have on the Company’s operations and financial condition,

and due to rapidly changing developments, the Company is currently implementing proactive and reactive mitigation measures to minimize

any potential impacts that COVID-19 may have on its employees, communities, operations, supply chain and finances. This also includes

preserving capital and deferring capital programs, where appropriate, in order to improve liquidity. The Company is maintaining

its guidance due to the operating flexibility of its Yauricocha Mine and the current normal operation of its Mexican mines. Should

any material changes occur, the Company would update its guidance promptly, and expects to provide a more comprehensive update

with more data points on metal prices and operating developments as part of the Q1 2020 reporting process.

Description of the Business

General

Summary

Sierra Metals is a diversified Canadian mining

company focused on the production, exploration and development of precious and base metals in Peru and Mexico. The Company’s

strategic focus is to continue being a profitable, low-cost, mid-tier precious and base metals producer. The Company plans to

continue growing its production base through exploration investments within its properties. The Company has high returns on invested

capital and strong cash flow generation as key priorities.

The Company has mining properties at several

stages of development and manages its business on the basis of the geographical location of its mining projects. The Peruvian operation

(Peru) includes the Yauricocha Mine and its near-mine concessions. The Mexican Operation (Mexico) includes the Bolivar and Cusi

mines both located in the Chihuahua State, Mexico, their near-mine concessions and the Mexican exploration and early stage properties.

Sierra Metals is fully committed to disciplined

and responsible growth and has Safety and Health and Environmental Policies in place to support this commitment. The Company’s

corporate responsibility objectives are to prevent pollution, minimize the impact operations may cause to the environment and practice

progressive rehabilitation of areas impacted by its activities. The Company aims to operate in a socially responsible and sustainable

manner, and to follow international guidelines in Mexico and Peru. The Company plans to focus on social programs with the local

communities in Mexico and Peru on an ongoing basis.

The Company produces zinc, copper and lead concentrates

with gold and silver by-products from its polymetallic circuit at the Yauricocha Mine; copper concentrates at the Bolivar Mine;

and a silver-lead concentrate at the Cusi Mine. These concentrates are sold to international metal traders who in turn sell and

deliver these products to different clients around the world.

The breakdown of revenue from metals payable

by product for 2017, 2018 and 2019 is as follows:

| By Revenue (%) |

2017 |

2018 |

2019 |

| Silver |

15% |

16% |

19% |

| Copper |

31% |

37% |

38% |

| Lead |

14% |

11% |

12% |

| Zinc |

38% |

35% |

26% |

| Gold |

2% |

1% |

6% |

Peru – Yauricocha Mine

Mining at Yauricocha is completed by various

extraction methods, principally sublevel caving and overhand cut and fill stoping. Ore is transported via underground rail to the

on-site Chumpe mill for processing. The Chumpe mill processes ores produced by Yauricocha using crushing, grinding and flotation.

Polymetallic ore is processed and treated in a polymetallic circuit.

Mexico – Bolivar Mine

At the Bolivar Mine, mining is done by room-and-pillar

and sublevel stoping methods. Extracted ore is trucked 5 kilometers to the Company’s Piedras Verdes mill, which is a conventional

flotation processing plant rated at 5,000 tpd depending on the work index.

Mexico – Cusi Mine

Mining at the Cusi Mine is completed by cut

and fill method. Mined development rock is trucked 37 km via flat, paved roads to the Company’s Malpaso mill, which is a

conventional flotation processing plant. The plant has three ball mills: (1) 8´ x 14´ mill, with capacity of 28 tph;

(2) 8´ x 7´ mill, with capacity of 13 tph; and (3) 7´ x 10´ mill, with capacity of 9 tph. Total capacity

between the three mills is 50 tph, or 1,200 tpd.

Exploration Properties

Of the several exploration properties in Mexico

held by the Company, two have had work done by the Company and are considered properties of merit: Bacerac and Batopilas. The others,

such as Arechuyvo and Maguarchic, have not had work performed on them because they are considered to be of lower priority for allocation

of resources such as personnel and funds.

Specialized Skill and Knowledge

Most aspects of the Company’s business

require specialized skills and knowledge. Such skills and knowledge include the areas of geology, mining, metallurgy, engineering,

environmental issues, permitting, social issues, and accounting. The Company has adequate employees with experience in these specialized

areas to meet its current needs.

Cycles

The mining and exploration industry is cyclical

in nature. The mining industry is subject to commodity pricing, which is in turn affected by other economic indicators and worldwide

cycles. The pricing cycles that the mining industry experiences affect the overall environment in which the Company conducts its

business. For example, if commodity pricing is low, Sierra’s access to capital may be restricted. Continuing periods of low

commodity prices or economic stalls could also affect the economic potential of the Company’s current properties and may

affect its ability to, among other things: (i) capitalize on financing, including equity financing, to fund its ongoing operations

and exploration and development activities; and (ii) continue exploration or development activities on its properties.

Furthermore, weather cycles may affect the Company’s

ability to conduct exploration activities at its mines, including the Yauricocha Mine, Bolivar Mine and Cusi Mine. More specifically,

drilling and other exploration activities may be restricted during periods of adverse weather conditions or winter seasons as a

result of weather related factors, including inclement weather, snow covering the ground, frozen ground and restricted access due

to snow, ice, or other weather related factors.

Competitive Conditions

The mining and exploration industry is

competitive in all aspects. The Company competes with other mining companies, many of whom have greater financial resources,

operational experience or technical capabilities than Sierra, in connection with the acquisition of properties producing, or

capable of producing, precious metals. In addition, the Company also competes for the recruitment and retention of qualified

employees and consultants.

Changes to Contracts

The Company does not anticipate that its business

will be materially affected in the current financial year by the renegotiation or termination of any contracts or sub-contracts.

Metal Price Volatility

The profitability of the Company’s operations

may be significantly affected by changes in the market price of the precious and base metals that it produces. The economics of

producing precious and base metals are affected by many factors, including the cost of operations, variations in the grade of

ore mined and the price of the precious and base metals. Depending on the price of precious and base metals that it produces,

the Company may determine that it is impractical to commence or continue commercial production. The price of precious and base

metals fluctuates widely and is affected by numerous industry factors beyond the Company’s control, such as the demand for

precious and base metals, forward selling by producers and central bank sales and purchases of precious and base metals. The price

of gold and silver is also affected by macro-economic factors, such as expectations for inflation, interest rates, the world supply

of mineral commodities, the stability of currency exchange rates and global or regional political and economic situations. Such

external economic factors are in turn influenced by changes in international investment patterns, monetary systems and political

systems and developments. The price of precious and base metals has fluctuated widely in recent years, and future serious price

declines could cause commercial production to be uneconomic.

Any significant drop in the price of precious

and base metals adversely impacts the Company’s revenues, profitability and cash flows. In addition, sustained low gold price

may:

| · | reduce production revenues as a result of cutbacks caused by the cessation of mining operations

involving deposits or portions of deposits that have become uneconomic at prevailing prices; |

| · | cause the cessation or deferral of new mining projects; |

| · | decrease the amount of capital available for exploration activities; |

| · | reduce existing reserves by removing ore from reserves that cannot be economically mined at prevailing

prices; or |

| · | cause the write-off of an asset whose value is impaired by low metal prices. |

There can be no assurance that the price of precious and base metals will remain stable or that such prices will be at a level

that will prove feasible to begin development of its properties, or commence or continue commercial production, as applicable.

Environmental Protection

The Company is currently in material compliance

with all applicable environmental regulations applicable to its exploration, development, construction and operating activities.

The financial and operational effects of environmental protection requirements on capital expenditures, earnings and expenditures

during the fiscal year ended December 31, 2019 were not material.

Employees

As at December 31, 2019, the Company and its

subsidiaries had 784 employees in Peru, 654 employees in Mexico, and 7 employees in Canada.

Social or Environmental Policies

The Company has built strong relationships with

the communities in which it operates and is committed to complying in all material respects with all environmental laws and regulations

applicable to its activities.

Foreign Operations

Doing Business in Peru

Peru is a democratic republic governed by an elected

government which is headed by a president who serves for a five-year term.

In Peru, the General Mining Law allows mining companies

to obtain clear and secure title to mining concessions. The surface land rights are distinct from the mining concessions. The government

retains ownership of mineral resources, but the titleholder of the concessions retains ownership of extracted mineral resources.

Peruvian law requires that all operators of mines in Peru have an agreement with the owners of the land surface above the mining

rights or to establish an easement upon such surface for mining purposes. Mining concessions allow for both exploration and for

exploitation.

Mining rights in Peru can be transferred by their private

holders with no restrictions or requirements other than to register the transaction with the Public Mining Register and the Ministry

of Energy and Mines. The only exception to this rule is that foreigners cannot acquire or possess mining concessions within 50

kilometers of the border, unless an exception based on public necessity or national interest is granted by the President of Peru

by means of a Supreme Decree.

The sale of mineral products is also unrestricted,

so there is no obligation to satisfy the internal market before exporting products. Pursuant to environmental laws applicable to

the mining sector, holders of mining activities are required to file and obtain approval for an EIA, which incorporates technical,

environmental and social matters, before being authorized to commence operations.

The Environmental Evaluation and Oversight Agency (“OEFA”)

monitors environmental compliance. OEFA has the authority to carry out audits and levy fines on companies if they fail to comply

with prescribed environmental standards. The following main permits are generally needed for a project: Start-Up Authorization;

Certificate for the Inexistence of Archaeological Remains (CIRA); EIA; Mine Closure Plan; Beneficiation Concession; Water Usage

Permits and Rights over surface lands.

Companies incorporated in Peru are subject to income

tax on their worldwide taxable income, while foreign companies that are located in Peru and non-resident entities are taxed on

income from Peruvian sources only. The current corporate income tax rate is 29.5%.

In general terms, mining companies in Peru are subject

to the general corporate income tax regime. If the taxpayer has elected to sign a Stability Agreement, an additional 2% premium

is applied on the regular corporate income tax rate. The Company has not signed a Stability Agreement. Also, 50% of income tax

paid by a mine to the Central Government is remitted as “Canon” by the Central Government back to the regional and

local authorities of the area where the mine is located.

In Peru, the current dividend tax rate of 5% is imposed

on distributions of profits to non-residents and domiciled individuals by resident companies and by branches, permanent establishments

and agencies of foreign companies. This rate applies to dividends that correspond to profits generated since January 1, 2017. Profits

generated up to December 31, 2014 are subject to a withholding tax rate of 4.1%, and profits generated between January 1, 2015

and December 31, 2016 are subject to a withholding tax at a rate of 6.8%, even if the relevant profits are distributed in future

years.

Peru’s transfer-pricing rules apply to cross-border

and domestic transactions between related parties and to all transactions with residents in tax-haven jurisdictions. The transfer-pricing

rules also apply to transactions with residents in non-cooperating jurisdictions, as well as transactions with residents whose

revenue or income is subject to a preferential tax regime.

In Peru, the Boar will be responsible for approving

the entity’s tax planning. This obligation cannot be delegated.

Peru has entered into double tax treaties with Brazil,

Canada, Chile, Korea (South), Mexico, Portugal and Switzerland. It has also entered into an agreement to avoid double taxation

with the other members of the “Comunidad Andina” (Bolivia, Colombia and Ecuador).

As of 2004, holders of mining concessions are required

to pay the government a Mining Royalty as consideration for the exploitation of metallic and non-metallic minerals. Payment of

mining royalties shall be completed on a quarterly basis and is calculated based on the greater of either: (a) an amount determined

in accordance with a statutory scale of tax rates based on a company’s operating profit margin and applied to the company’s

operating profit; and (b) 1% of the company’s net sales, in each case during the applicable quarter. The royalty rate applicable

to the company’s profit is based on its operating profit margin according to a statutory scale of rates that range between

1% and 12%. Mining royalty payments are deductible as expenses for income tax purposes in the fiscal year in which such payments

are made.

The Special Mining Tax (“SMT”) is

a tax imposed in parallel with the Mining Royalty described above. The SMT is applied on operating margin profit based on a sliding

scale, with progressive marginal rates ranging from 2.0% to 8.4%. The tax liability arises and becomes payable on a quarterly basis.

The SMT applies on the operating margin profit derived from sales of metallic mineral resources, regardless of whether the mineral

producer owns or leases the mining concession. SMT payments are deductible as expenses for income tax purposes in the fiscal year

in which such payments are made.

Doing Business in Mexico

Mexico is a federal presidential representative democratic

republic, where the President is both head of state and head of government. The current government of Mexico is guided by the 1917

constitution. The President is the head of the executive branch, the commander-in-chief of the armed forces and also the head of

state. The President of Mexico is elected by an absolute majority of the federal entities. Mexico’s President is elected

for six years and cannot be re-elected. The President is mandated to appoint and dismiss cabinet ministers and nearly all other

officials of the executive.

The

mining industry in Mexico is controlled by the Secretaría de Economía through the Subsecretaría de Minería,

which is officially located and administered from Chihuahua City, with offices in Mexico City. In Mexico, mining activities

include extraction activities independent from petroleum, natural gas and radioactive minerals, and certain non-metallic minerals

such as construction and ornament materials, some of which are not subject to the mining legislation. In addition to the extraction

activities, mining, smelting and refining activities are also considered as part of the mining industry, which are jointly known

as mining-metallurgic activities. Mining concessions in Mexico may only be obtained

by Mexican nationals or Mexican companies incorporated under Mexican law (which could be wholly owned by foreign investors). The

construction of processing plants requires further governmental approvals (e.g. Federal, local and municipal permits).

In

Mexico, surface land rights are distinct from the mining concessions. The holder of a mining concession is granted the exclusive

right to explore and develop a designated area. Mining concessions are granted for 50 years from the date of their registration

with the Public Registry of Mining to the concession holder as a matter of law, if all regulations have been complied with. During

the final five years of this period, the concession holder may apply for one additional 50-year period, which shall be granted

provided all other concession terms have been complied with. Mining rights in Mexico can be transferred by their private holders

with no restrictions or requirements other than to register the transaction with the Public Registry of Mining and that the assignee

is qualified to hold a concession (i.e. a Mexican national or a Mexican company incorporated under Mexican law having mining activities

as its main corporate purpose). Securities can be imposed to mining concessions. The instrument formalizing the corresponding

security shall be also registered before the Mining Public Registry.

Concessionaires must perform work each year that

begins within ninety days of the concession being granted. Concessionaires must file proof of the work performed every year by

the end of May. Non-compliance with these requirements is cause for cancellation only after the authority communicates in writing

to the concessionaire any such default, granting the concessionaire a specified time frame in which to remedy the default.

In Mexico, there are no limitations on the total

amount of mining concessions or on the amount of land that may be held by an individual or a company. Excessive accumulation of

concessions is regulated indirectly through the duties levied on the property and the production and exploration requirements as

outlined below.

Three different fees or royalties applicable to the

mining activity in Mexico exist as per the Federal Fees Law (LFD). Such fees are as follows:

Special mining fee:

This fee shall be calculated at a 7.5%

rate over the positive difference resulting from subtracting the deductions allowed in the Mexican Income Tax Law (MITL) from the

income resulting from the revenue of the mining activity.

However, for the purposes of calculating

the basis of this fee, the LFD does not allow to take into account several expenses that may be incurred by the mining taxpayers.

Such expenses involve investments not related to mining prospecting and exploration, as well as tax losses not yet amortized and

incurred in previous fiscal years.

Mining concessionaires and assignees shall

be exempted from the payment of this fee exclusively for the use, enjoyment, or exploitation of coal gas deposits.

Additional mining fee:

This fee shall be incurred based on the

maximum rate of the mining fee set forth in Article 263 of the LFD per concession’s hectare. Usually, this fee is nominal.

Extraordinary mining fee:

This fee shall be calculated at a 0.5%

rate over the income resulting from the sale of gold, silver, and platinum, without any deduction.

Control over Subsidiaries

Corporate Governance

The Company has implemented a system of corporate

governance, internal controls over financial reporting, and disclosure controls and procedures that apply at all levels of the

Company and its subsidiaries. These systems are overseen by the Board and implemented by the Company’s senior management.

The relevant features of these systems are set forth below.

The Company’s corporate structure has been

designed to ensure that the Company controls, and/or has a measure of direct oversight over, the operations of its subsidiaries.

The Company, as the ultimate shareholder, has internal policies and systems in place which provide it with visibility into the

operations of its subsidiaries, including its subsidiaries operating in emerging markets, and the Company’s management team

is responsible for monitoring the activities of the subsidiaries.

The Company, directly or indirectly, controls

the appointments of all of the directors and senior officers of its subsidiaries. The directors of the Company’s subsidiaries

are ultimately accountable to the Company as the shareholder appointing him or her, and the Board and senior management of the

Company. As well, the annual budget, capital investment and exploration program in respect of the Company’s mineral properties

are established by the Company.

Further, signing officers for subsidiary foreign

bank accounts are either employees of the Company or employees of the subsidiaries. In accordance with the Company’s internal

policies, all subsidiaries must notify the Company’s corporate treasury department of any changes in their local bank accounts

including requests for changes to authority over the subsidiaries’ foreign bank accounts. Monetary limits are established

internally by the Company as well as with the respective banking institution. Annually, authorizations over bank accounts are reviewed

and revised as necessary. Changes are communicated to the banking institution by the Company and the applicable subsidiary to ensure

appropriate individuals are identified as having authority over the bank accounts.

Strategic Direction

While the mining operations of each of the Company’s

subsidiaries are managed locally, the Board is responsible for the overall stewardship of the Company and, as such, supervises

the management of the business and affairs of the Company. More specifically, the Board is responsible for reviewing the strategic

business plans and corporate objectives, and approving acquisitions, dispositions, investments, capital expenditures and other

transactions and matters that are material to the Company including those of its material subsidiaries.

Internal Control Over

Financial Reporting

The Company prepares its consolidated financial

statements on an annual basis in accordance with International Financial Reporting Standards (“IFRS”) as issued

by the International Accounting Standards Board and on a quarterly basis in accordance with IFRS as applicable to interim financial

reports including International Accounting Standard 34, Interim Financial Reporting. This requires financial information and disclosures

from its subsidiaries. The Company implements internal controls over the preparation of its financial statements and other financial

disclosures to provide reasonable assurance that its financial reporting is reliable and that the quarterly and annual financial

statements are being prepared in accordance with the relevant reporting framework and securities laws.

The responsibilities of the Board include oversight

of the Company’s internal control systems including those systems to identify, monitor and mitigate business risks as well

as compliance with legal, ethical and regulatory requirements.

Regional Experience

The directors and executive officers of the

Company have significant experience conducting business in Peru and/or Mexico, including (i) international corporate finance and

mergers and acquisitions experience in Peru and/or Mexico, (ii) planning, supervising and managing experience with mining operations

in Peru and/or Mexico, (iii) executive officers and/or directors with experience with other publicly-listed mining companies with

operations in Peru and/or Mexico, and (iv) visiting the Company’s projects in Peru and Mexico on a regular basis. Further,

Alberto Arias (Director), Dionisio Romero (Director), Jose Vizquerra Benavides (Director), Ricardo Arrarte (Director), Igor Gonzales

(Chief Executive Officer), Ed Guimaraes (Chief Financial Officer), Alonso Lujan (Vice President, Exploration) and Rajesh Vyas (Corporate

Controller) are all either fluent or proficient in Spanish.

Material

Mineral Properties

The Company has three material projects described

below. To satisfy the reporting requirements of National Instrument 51-102F2 with respect to the Company’s material mineral

projects, the Company has opted, as permitted by the Instrument, to reproduce the summaries from the technical reports on the respective

material properties and to incorporate by reference each such technical report into this AIF.

Yauricocha Mine, Peru

The Company owns 81.84% of Minera Corona, which

in turn owns 100% of the Yauricocha Mine.

Yauricocha Technical Report

The following is the summary section of the

Yauricocha Technical Report, prepared by SRK Consulting (Canada) Inc. (“SRK”), and signed by Qualified

Persons Andre M. Deiss, BSc. (Hons), Pri.Nat.Sci, MSAIMM, SRK Principal Consultant (Resource Geology); Carl Kottmeier,

B.A.Sc., P. Eng, MBA, SRK Principal Consultant (Mining); Daniel H. Sepulveda, BSc, SME-RM, SRK Associate Consultant

(Metallurgy); Dan Mackie, M.Sc., B.Sc., PGeo, SRK Principal Consultant (Hydrogeologist); and Jarek Jakubec, C. Eng. FIMMM,

SRK Practice Leader/Principal Consultant (Mining, Geotechnical). The full text of the Yauricocha Technical Report is

available for viewing on SEDAR at www.sedar.com and is incorporated by reference in

this AIF. Defined terms and abbreviations used herein and not otherwise defined shall have the meanings ascribed to such

terms in the Yauricocha Technical Report.

“1 Executive

Summary

This report was prepared as a Canadian National

Instrument 43-101 (NI 43-101) Technical Report on Resources and Reserves (Technical Report) for Sierra Metals Inc. (Sierra Metals),

previously known as Dia Bras Exploration, Inc., on the Yauricocha Mine (Yauricocha or Project), which is located in the eastern

part of the Department of Lima, Peru. The purpose of this report is to present the Mineral Resource and Reserve estimates, operating

and capital costs, description of the mining methods used, the processing plant, and the related surface and underground infrastructure.

The Consultants preparing this technical report

are specialists in the fields of geology, exploration, Mineral Resource and Mineral Reserve estimation and classification, underground

mining, geotechnical, environmental, permitting, metallurgical testing, mineral processing, processing design, capital and operating

cost estimation, and mineral economics.

| 1.1 | Property Description and Ownership |

The Yauricocha Mine is in the Alis district,

Yauyos province, department of Lima approximately 12 km west of the Continental Divide and 60 km south of the Pachacayo railway

station. The active mining area within the mineral concessions is located at coordinates 421,500 m east by 8,638,300 m north on

UTM Zone 18L on the South American 1969 Datum, or latitude and longitude of 12.3105⁰ S and 75.7219⁰ W. It is geographically

in the high zone of the eastern Andean Cordillera, and within one of the major sources of the River Cañete which discharges

into the Pacific Ocean. The mine is at an average altitude of 4,600 masl (Gustavson, 2015).

The current operation is an underground polymetallic

sulfide and oxide operation, providing material for the nearby Chumpe process facility. The mine has been operating continuously

under Sociedad Minera Corona S.A. (SMCSA or Minera Corona) ownership since 2002 and has operated historically since 1948. Sierra

Metals, Inc. purchased 82% of SMCSA in 2011.

| 1.2 | Geology and Mineralization |

The Yauricocha Mine features several mineralized

bodies, which have been emplaced along structural trends, with the mineralization itself related to replacement of limestones by

hydrothermal fluids related to nearby intrusions. The mineralization varies widely in morphology, from large, relatively wide,

tabular style (manto) deposits to narrow, sub-vertical chimneys. The mineralization features economic grades of silver (Ag), copper

(Cu), lead (Pb) and zinc (Zn), with local gold (Au) to a lesser degree. The majority of the deposits are related to the regional

high-angle NW-trending Yauricocha fault or the NE trending and less well-defined Cachi-Cachi structural trend. The mineralization

generally presents as polymetallic sulfides but is locally oxidized to significant depths or is associated with Cu-rich bodies.

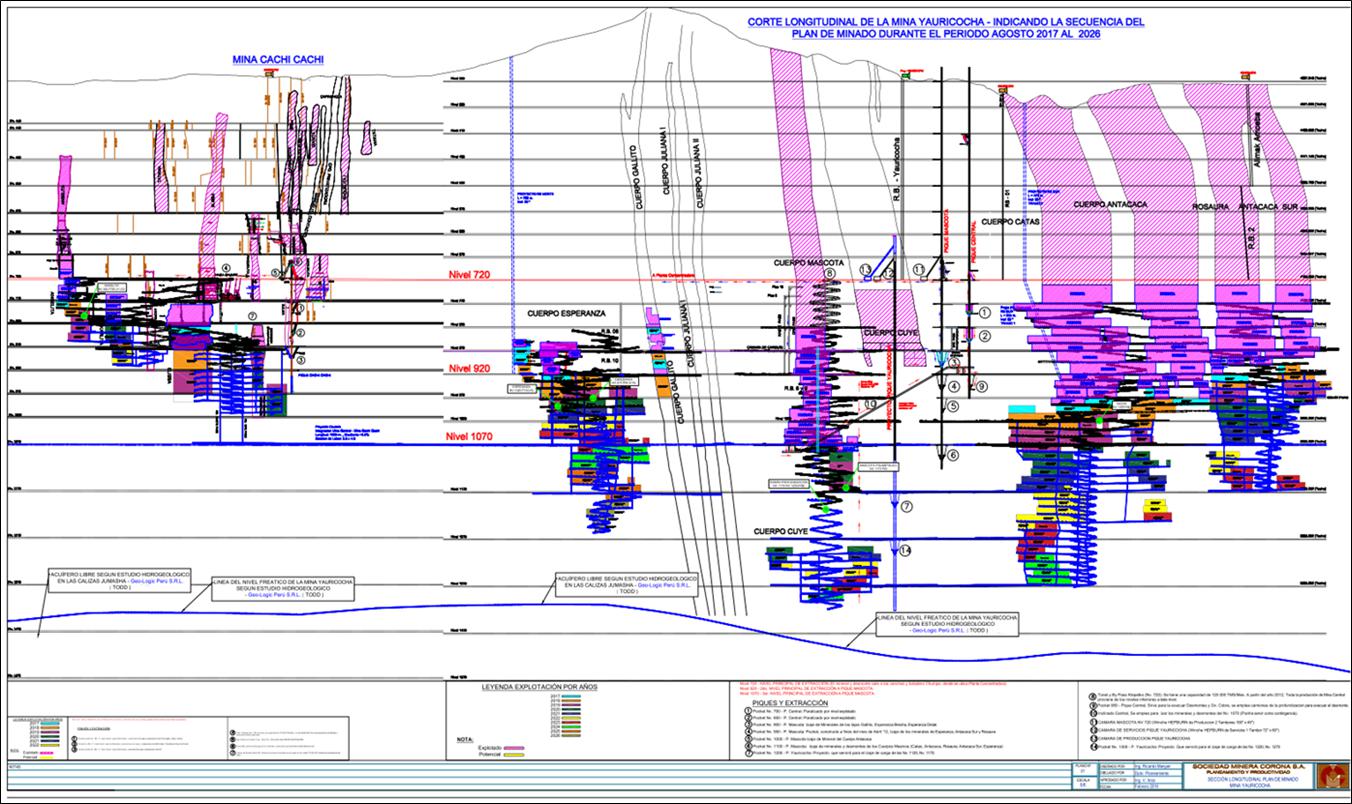

The Yauricocha Mine is concurrently undertaking

exploration, development and operations. Exploration is ongoing within the mine claim and is supported predominantly by drilling

and exploration drifting. The mine is also currently producing multiple types of metal concentrates from several underground mine

areas.

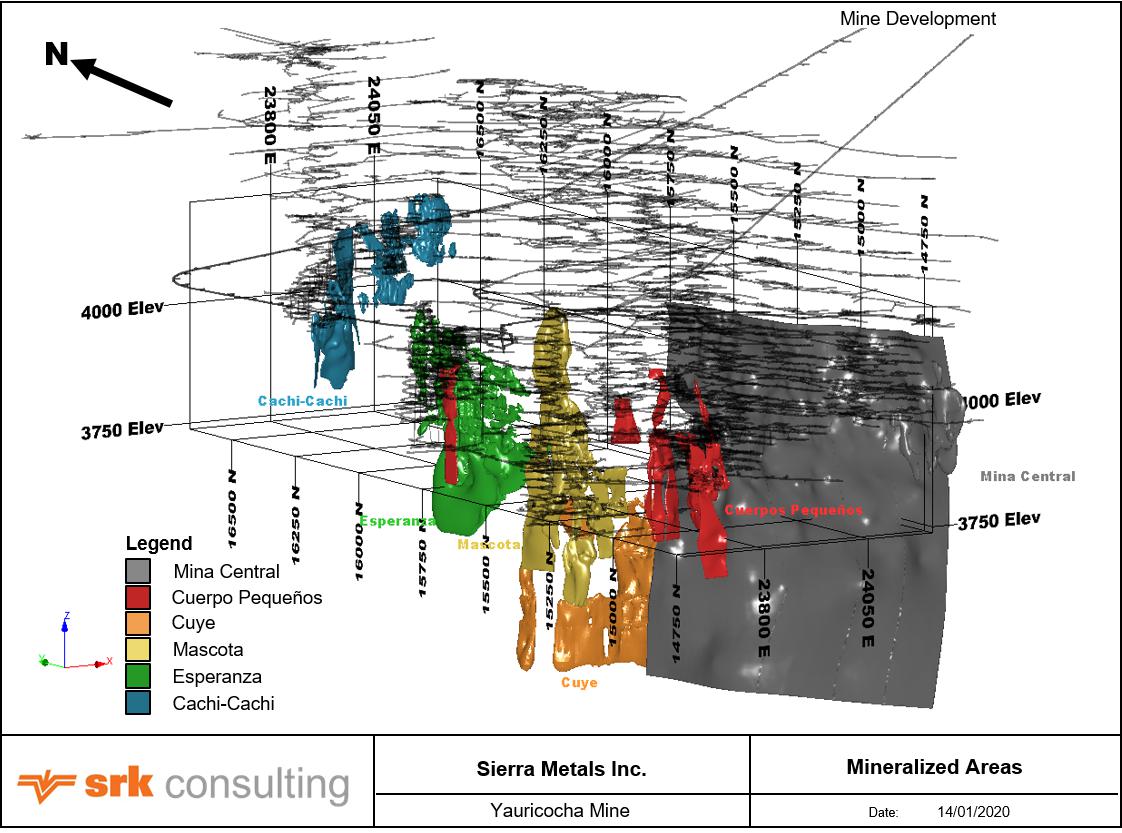

| 1.4 | Mineral Resource Estimate |

The understanding of the geology and mineralization,

as reported in the Resource Statement for Yauricocha is based on a combination of geologic mapping, drilling and development sampling

that guides the ongoing mine design. SRK has reviewed the methods and procedures for these data collection methods and notes that

they are generally reasonable and consistent with industry best practice. The validation and verification of data and information

supporting the Mineral Resource estimation has historically been deficient, but strong efforts are being made to modernize and

validate the historic information using current, aggressive Quality Assurance / Quality Control (QA/QC) methods and more modern

practices for drilling and sampling. SRK notes that most of the remaining resources in areas such as Mina Central and Cachi-Cachi

(Figure 1-1) are supported by modern data validation and QA/QC, and that new areas like Esperanza feature extensive QA/QC and

third-party analysis.

Figure 1-1: Modelled Mineralized areas Estimated

at Yauricocha Mine

SRK notes that the geological modeling procedures

currently implemented by the Yauricocha geologists are significantly different than that used in previous years and are now based

on implicit modeling through Seequent Leapfrog® Geo 3D geology modeling software. This is consistent with industry best practice,

and SRK notes that there have been advances in the detail and extent of geological modeling for most of the orebodies.

The procedures and methods supporting the Mineral

Resource estimation have been developed in conjunction with Minera Corona geological personnel. The resource estimations presented

herein have been conducted by SRK as independent consultants using supporting data generated by the site. In general, the geologic

models are defined by the site geologists using manual and implicit 3D modeling techniques and are based on information from drilling

and development. These models are used to constrain block models, which are flagged with bulk density, mine area, depletion, etc.

Grade is estimated into these block models using both drilling and channel samples, applying industry-standard estimation methodology.

Mineral Resources were estimated in Datamine Studio RMTM software and are categorized in a manner consistent with industry

best practice. Mineral Resources are reported above reasonable unit value cut-off’s applicable per mineralization type and

the expected mining method.