UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

EXCHANGE ACT OF 1934

For the Fiscal Year Ended

Or

EXCHANGE ACT OF 1934

Commission file number:

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| (Address of Principal Executive Offices) | (Zip Code) |

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to

file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405

of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Smaller reporting

company | Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. Yes ☐ No

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐

No

As of June 30, 2021, the last business day of the registrant’s most recently completed second fiscal quarter, the registrant’s securities were not publicly traded. The registrant’s common stock began trading on The Nasdaq Stock Market LLC on November 10, 2020.

The registrant had

DOCUMENTS INCORPORATED BY REFERENCE

The definitive proxy statement relating to the registrant’s Annual Meeting of Stockholders to be filed within 120 days of the registrant’s fiscal year ended December 31, 2021 and is incorporated by reference in Part III to the extent described therein.

TABLE OF CONTENTS

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

We make forward-looking statements under the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in other sections of this Form 10-K. In some cases, you can identify these statements by forward-looking words such as “may,” “might,” “should,” “would,” “could,” “expect,” “plan,” “anticipate,” “intend,” “believe,” “estimate,” “predict,” “potential” or “continue,” and the negative of these terms and other comparable terminology. These forward-looking statements, which are subject to known and unknown risks, uncertainties and assumptions about us, may include projections of our future financial performance based on our growth strategies and anticipated trends in our business. These statements are only predictions based on our current expectations and projections about future events. There are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements.

While we believe we have identified material risks, these risks and uncertainties are not exhaustive. Other sections of this Form 10-K may describe additional factors that could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible to predict all risks and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

Although we believe the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, level of activity, performance or achievements. Moreover, neither we nor any other person assumes responsibility for the accuracy or completeness of any of these forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. We are under no duty to update any of these forward-looking statements after the date of this Form 10-K to conform our prior statements to actual results or revised expectations, and we do not intend to do so.

We caution you not to place undue reliance on the forward-looking statements, which speak only as of the date of this Form 10-K in the case of forward-looking statements contained in this Form 10-K.

You should not rely upon forward-looking statements as predictions of future events. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. We qualify all of our forward-looking statements by these cautionary statements. Although we believe that the expectations reflected in the forward looking-statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Therefore, you should not rely on any of the forward-looking statements. In addition, with respect to all of our forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

SPECIAL NOTE REGARDING COMPANY REFERENCES

In this annual report on Form 10-K, and unless the context otherwise requires, the “Company,” “we,” “us” and “our” refer to Bluejay Diagnostics, Inc. and its wholly-owned subsidiary Bluejay Spinco, LLC, taken as a whole.

ii

PART I

ITEM 1. BUSINESS

Overview

We are a late-stage pre-revenue company focused on improving patient outcomes through a more cost efficient, rapid, near patient product for triage, diagnosis and monitoring of disease progression. We believe there is a market need for an on-site and rapid diagnostic system that can be employed for testing and monitoring. Our diagnostic system, which we refer to as “Symphony,” is an exclusively licensed, patented, low-cost, system that consists of a small footprint instrument and single-use indication specific test cartridges, that we believe, if cleared, authorized, or approved by the U.S. Food and Drug Administration (“FDA”), can provide a solution to this market need rapidly and with laboratory quality results in approximately 24 minutes, in the clinic, Intensive Care Unit (“ICU”), Emergency Room (“ER”) and in other hospital and clinical setting settings where rapid and reliable results are required. Currently, testing is generally performed in a laboratory, and the transportation and logistics of transporting the samples to the lab and obtaining the result takes between 8-48 hours. Our platform is a sample-to-result system that has been shown in a clinical study to provide results in approximately 24 minutes. Our business model is to generate revenue from the sale of the table-top Symphony instrument, and from the sale of single-use indication specific cartridges that are used by the Symphony instrument for the diagnostic test. Once the test material (generally a small volume blood sample) is transferred to a single-use indication specific Symphony cartridge, no additional sample preparation or pre-processing is required. Based on the results of the clinical study described below, we believe Symphony may be able to eliminate the time required for transportation and logistics, and may be able to eliminate the number of operational ‘touch-points’ from ‘sample-to-result’ from six to two.

Our technology is the result of more than 12 years of development by our development partner and investor, Toray Industries, Inc. (“Toray”). For the past three years, Toray has used the technology successfully in Japan by selected clinical institutions for measurement of Interleukin-6 (“IL-6”) in rheumatoid arthritis to monitor disease progression. Based in part on this extensive development, we believe we are now positioned to complete the last stages of development needed for commercialization in the US.

In a 2016 study conducted in Japan (the “Japan Study”), which was sponsored by Toray, it was shown that the Symphony system (known as the RAY-FAST system in Japan) can provide accurate results within 24 minutes. The Japan Study was conducted at the University of Yamanashi Hospital in Yamanashi, Japan to evaluate the accuracy and efficacy of the Symphony system in rheumatoid arthritis patients. The results of the study were published in Cytokine, “Development of a quick serum IL-6 measuring system in rheumatoid arthritis” (Volume 95. July 2017). In the Japan Study, 150 blood samples were collected from 76 rheumatoid arthritis patients, of which 16 samples were lower than the detection limit of the Symphony system. The Japan Study then examined the correlation between the results from the Symphony system and the chemiluminescent enzyme immunoassay (CLEIA) method. The serum IL-6 concentrations measured by the Symphony system were positively correlated with those measured by the CLEIA method. The correlation between the Symphony system and CLEIA method for IL-6 was r = 0.941 (the closer the r-value is to 1, the more closely the two variables are related). As such, the Japan Study concluded that the Symphony system was as accurate as CLEIA methods. In addition, the Japan Study confirmed the time required for the measurement of the IL-6 concentration to be 24 minutes.

Our first diagnostic test in development is for triage of sepsis in patients utilizing IL-6 as the target biomarker. According to a report by Market Data Forecast (February 2020), the total market for IL-6 testing for sepsis triage was $934 million in 2020 and is estimated to reach $1.4 billion by 2025 growing at a CAGR of 8.5%. IL-6 has important roles in both innate and adaptive immunity. It is an inflammatory biomarker, also considered as a ‘first-responder,’ that is elevated in patients with infection, sepsis, and septicemia. Reports have shown IL-6 concentrations correlate with severity of sepsis, progression of cancer, rheumatoid arthritis and many other severe conditions as defined by clinical and laboratory parameters. IL-6 is a clinically established biomarker for assessment of severity of infection and inflammation across many disease indications. IL-6 appears early in the blood circulation as a ‘first responder’ during infection or inflammation. One factor that is a challenge for healthcare professionals to overcome is the amount of time it takes to determine if a patient is septic. It usually takes about several hours to receive the lab results of a patient who may be in a very critical state, and the risk of dying increases every hour a patient is not treated for sepsis. We believe early measurement of IL-6 can enable physicians to make better therapeutic and treatment decisions. Due to its clinical significance hospital systems and centralized testing labs routinely utilize IL-6 testing.

1

The importance of IL-6 testing has been further highlighted during the COVID-19 pandemic, and IL-6 concentrations in blood have been found to be elevated in patients with COVID-19-associated systemic inflammation and hypoxic respiratory failure.

We are further developing a pipeline of diagnostic tests for Symphony including triage of myocardial infarction (“MI”), congestive heart failure (“CHF”), neutropenic sepsis in cancer, and other disease diagnostic indications using the same Symphony platform. We intend to pursue the general diagnostic marketplace following a sufficient clinical trial to support a 510(k) submission with the FDA, with the initial indication as a general diagnostic test for sepsis in triage of patients. We do not currently have any regulatory clearance for our Symphony products and our Symphony products will need to receive regulatory authorization from FDA, in order to be marketed as a diagnostic product in the United States.

Our operations to date have been funded primarily through sales of preferred stock and convertible notes. We expect to incur increasing expenses over the next two years to develop additional diagnostic tests, to expand our sales and marketing infrastructure, and our research and development activities. We believe the proceeds from our Initial Public Offering (“IPO”) on November 10, 2021 will be sufficient to reach commercialization.

We were incorporated under the laws of Delaware on March 20, 2015. Our headquarters are located in Acton, Massachusetts.

Symphony Advantages

We believe there is a fast-growing market for near-patient, low-cost diagnostic platforms that are used for time-sensitive patient testing in life-threatening situation in hospitals, Long-Term Acute Care facilities (“LTACs”), intensive-care units (“ICUs”) and clinics to replace legacy testing formats and processes. We believe our platform is well positioned to meet this need. Based on the results of the Japan Study, we believe Symphony may be able to provide results within approximately 24 minutes. In addition, based on the results of the Japan Study, we believe Symphony may be able to reduce test result time from days to minutes and to provide results that appear to be as accurate as those performed in a laboratory, allowing for more frequent testing, which we believe may lead to shortened hospital stays and improved patient outcomes, all of which also leads to reduced patient care costs.

Symphony is an automated diagnostic system, consisting of a fluorescence immuno-analyzer which uses a single-use diagnostic test cartridge with reagents integrated in the cartridge. Symphony utilizes a ‘sample-to-result’ format, which means that once a specimen is taken from the patient, it is placed in the cartridge and then the cartridge is placed inside the analyzer where the test is run without further technician intervention or additional reagent. This reduces test complexity and eliminates the need for highly trained and expensive laboratory technicians to run the tests. Our platform is designed to enable simple, rapid, and cost-effective analysis from a single clinical sample, which will allow LTACs, hospitals and clinics that traditionally could not afford more expensive or complex diagnostic testing platforms to modernize their laboratory testing and provide better patient testing at an affordable cost in time sensitive, life-threatening situations. We believe our on-site testing may also help avoid potential penalties often imposed on LTACs by insurance companies for failure to monitor for potential sepsis.

Based on the results of the Japan Study, we believe Symphony IL-6 can make a significant impact with turn-around time. As the whole blood samples do not need to be pre-processed, this medical device can be run at the patient’s bedside, effectively eliminating the extended turn-around time for lab results.

If incorporated in the hospital workflow, this medical device can provide assistance with monitoring patients post-surgery, and monitoring patients admitted in the emergency room who are suspected to have acute symptoms of sepsis.

2

We believe our technology can provide the following advantages over traditional diagnostic systems:

| ● | Ease of Use. Symphony is a sample-to-results system. No sample preparation or pre-processing is required. Once the samples are placed inside the cartridge and the cartridge is placed in the analyzer, the technician does not need to monitor the test and can complete other unrelated tasks. |

| ● | Cost Savings. We believe that the Symphony system and our expected pricing strategy will make it possible for LTACs, clinics and many types of hospitals that have cost constraints to adopt in-house testing. Our customers will be able to either purchase the analyzer or lease it at an affordable price through a third-party leasing company. A typical Symphony test would cost approximately $80 (the cost of the single-use cartridge to the health-care facility) compared to the approximately $275 per test charged by a third-party lab, excluding overhead and transportation cost. |

| ● | Time Savings. Saving pre-processing time for samples reduces time to test results by approximately 1-2 hours depending on the pre-processing required for a particular assay system. Furthermore, as current tests can only be performed in a laboratory, the transportation and logistics of transporting the samples to the lab and obtaining the result takes between 8-48 hours. Based on the results of the Japan Study, we believe Symphony may be able to eliminate the time required for transportation and logistics and may be able to eliminate the number of operational ‘touch-points’ from ‘sample-to-result’ from six to two. |

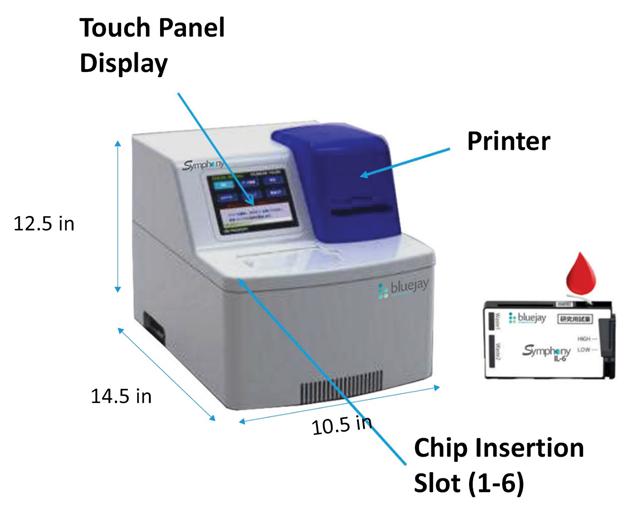

| ● | Space Savings. Symphony’s significantly smaller tabletop design (14.5 inches by 10.5 inches), compared to the 100-200 square feet of space required by other diagnostic systems, will make it possible for many healthcare providers to perform in-house testing where there is limited available laboratory space. |

| ● | Versatile Platform with the Capability to Deliver a Broad Test Menu. Our Symphony platform has the potential for broad application across a number of areas in near-patient diagnostic testing. The same analyzer can be utilized for all of our planned future diagnostic tests. |

| ● | Throughput and Multiple Testing Capability. Our platform has been designed to provide the ability to analyze up to six distinct targets or six different patient samples simultaneously within approximately 24 minutes. This functionality will allow any organization to run multiple tests or panels on a single analyzer. |

Our Market

According to research published by Allied Market Research (Global Invitro Diagnostics Market, 2020-2027), the global in vitro diagnostics market was $67.1 billion in 2019; projected to reach $91.1 billion by 2027, a compound annual growth rate (“CAGR”) of 4.8% over 7 years driven by prevalence of chronic diseases including cancer, autoimmune diseases, and other inflammatory conditions. We believe the Symphony sample-to-result platform is well suited to address a subset of this market, including sepsis, cardio-metabolic diseases, cancer and other diseases that require time-sensitive, near-patient testing.

According to a report by Market Data Forecast (February 2020), the total market for IL-6 testing for sepsis triage was $934 million in 2020 and is estimated to reach $1.4 billion by 2025 growing at a CAGR of 8.51%. Our platform is designed to provide on-site and rapid test results, with no pre-processing of the blood, and as such, we intend to pursue the following markets for triage:

| ● | Sepsis Triage using IL-6. According to the CDC, each year, at least 1.7 million adults in America develop sepsis and nearly 270,000 Americans die as a result of sepsis. In the United States, 1 in 3 patients who dies in a hospital has sepsis. In addition, in 2016, according to the National Center for Health Statistics, 8.3 million people were served by LTACs. A major responsibility of these LTAC facilities is to monitor sepsis. We estimate the potential total market for sepsis triage testing in LTACs is approximately $2–$3 billion annually. Septic shock and multi-organ failure were the most common cause of death in COVID-19 patients, often due to suppurative pulmonary infection. |

| ● | Chest Pain Triage using hsTNT and NT-proBNP. According to a Washington Post article in April 2019, there are 7.6 million people in the United States each year who visit or are admitted to the hospital with chest pain. Research suggests that about 50% of those patients are admitted for further observation and care of potential heart disease, and that approximately 3.6 million people annually needed cardiac triage. Two major biomarkers that are assessed to diagnose and monitor cardiac irregularities are hsTNT and NT-proBNP. These clinically established biomarkers generated approximately $4.6 billion in revenue in 2019 and will continue to grow with a CAGR of 11.2% through 2027. We are developing diagnostic tests for triage situations, using these cardiac biomarkers (hsTNT and NT pro-BNP), which were approximately a $3.6 billion market in 2020 and are estimated to be $5.5 billion by 2025, a CAGR of 8.9% (report by Markets and Markets, January 2021). |

3

The CDC National Center for Health Statistics estimates that the market for the diagnostic cardiac triage tests will increase by more than 20% per year over the next several years. Many factors are driving the growth of these markets, particularly the accelerating adoption of near-patient testing inside hospitals, LTACs and ICUs. According to the 2021 edition of American Hospital Association Hospital Statistics, there were approximately 6,090 hospitals in the United States in 2019, approximately 5,000 of which are considered community hospitals. According to outside research, fewer than half of these facilities have the capabilities, technology and products for near-patient diagnoses for triage of either sepsis or cardiac conditions. We believe these facilities are candidates for our diagnostic platform.

Our Business Model

Our goal is to become a leading provider of sample-to-result, ‘near-patient’ diagnostic testing in infectious, inflammatory and metabolic diseases by leveraging the strengths of our Symphony platform. We intend to market the use of Symphony by targeting our sales and marketing to LTACs, clinics, and community hospitals in the United States. We believe that the format of our low-cost, ‘near-patient’ platform will be attractive to these institutions which may not otherwise have the financial resources, laboratory space, or trained personnel to justify the purchase of a diagnostic solution. Our business model relies on the following:

| ● | Attractive Financing Model. We intend to provide our customers the ability to lease our analyzer at an affordable cost through third-party financial institutions. As such, our business model will not require a significant capital outlay by health care facility customers and, by moving testing in-house, will create a profit center for the facility. |

| ● | Recurring Revenue. We intend to sell our customers disposable, single-use diagnostic test cartridges. Our single-use test cartridges will create a growing and recurring revenue stream for us as we sell more systems, as adoption and utilization increase, and as we develop tests for additional indications. We expect the sale of test cartridges to generate the majority of our revenue. |

| ● | Expand our Menu of Diagnostic Products. If adoption increases, we believe the average customer use of the Symphony platform will begin to increase. As we expand our test menu, we believe we will be able to increase our annual revenue per customer through the resulting increase in utilization. To that end, we are in development on a broad menu of diagnostic tests that we believe will satisfy growing medical needs and present attractive commercial opportunities. |

| ● | Increase our revenue and reduce our cost of sales through a ‘waterfall’ sales strategy. Our proprietary test cartridges and Symphony analyzers are manufactured through our agreements with Toray and Sanyoseiko Co., Ltd. (“Sanyoseiko”), thus reducing the manufacturing cost structure. They currently build our Symphony system and test cartridges and currently purchase materials at high per unit cost due to low purchase volumes. We believe that by focusing our initial sales efforts on multi-location institutions, increased adoption and utilization of Symphony may lead to increasing sales within a relatively small customer base. We believe sales within those institutions may lower our salesforce costs. We believe the increased unit sales of our Symphony and cartridges will not only increase revenue, but will also allow us to reduce manufacturing costs and improve gross margins enhancing our ability to provide a lower cost solution to customers. |

Our Symphony Platform

Symphony

The Symphony platform is an innovative and proprietary technology platform that in the Japan Study appeared to provide rapid and accurate measurements of key diagnostic biomarkers found in whole blood. Symphony is compact and portable as compared with current laboratory diagnostic platforms that we believe, based on the Japan Study, provide comparable sensitivity. In the Japan Study, Symphony appeared to provide lab-quality results in a near-patient setting. Symphony is designed for usability; all sample preparation and reagents are integrated into the disposable Symphony Cartridges. Symphony only needs a few hundred femtograms (10-10 grams) of the target to provide quantitation directly from whole blood. Therefore, Symphony only requires a few drops of blood to generate a result in approximately 24 minutes.

4

Symphony is comprised of the Symphony Fluorescence Immuno-analyzer and the Symphony Cartridge Library, shown in Figure 1. The Symphony analyzer orchestrates whole blood processing, biomarker isolation, and immunoassay preparation using non-contact centrifugal force. All necessary reagents and components are integrated into the Symphony Cartridges. Utilizing precision microchannel technology and high specificity antibodies, whole blood is processed, and the biomarker is isolated within the Symphony Cartridge. Intermitted centrifugation cycles enable complex fluid movements, enabling sequential reagent additions and independent reaction steps inside the hermitically sealed Symphony Cartridge. At the conclusion of the test, the Symphony analyzer measures the fluorescence signature correlating to a highly sensitive quantitation of the biomarker.

Figure 1. Photograph of the Symphony Fluorescence Immuno-analyzer and a Symphony IL-6 Cartridge. Barcode reader (not pictured) is included to streamline clinical workflow.

Although our first commercial offering will be focused on the detection and quantitation of IL-6, we believe the flexibility of our technology will allow us to deploy new biomarkers for additional indications. Every Symphony Cartridge inserted in the analyzer has a unique code which programs the Symphony to perform the specific test. This unique feature will enable the release of new tests without the need for system redesigns or updates. Furthermore, this automated feature will eliminate the need for system recalibrations for every product lot, further streamlining the clinical workflow and enhancing usability.

5

The Symphony IL-6 test principle employs direct sandwich Enzyme Linked Immunosorbent Assay (“ELISA”) for the quantitation of human IL-6 by fluorescence enzyme immunoassay (“FEIA”), as shown in Figure 2. Within the single-use Symphony IL-6 Cartridge, the assay separates plasma from whole blood and forms complexes through reaction of any IL-6 present in the sample with highly specific IL-6 binding antibodies. After the IL-6 sandwich is formed, a fluorescent substrate is enzymatically decomposed to generate fluorescent molecules. The fluorescence intensity is measured and converted to IL-6 concentration, and the entire process is enclosed within the Symphony IL-6 Cartridge and is controlled and measured by the Symphony Fluorescence Immuno-analyzer.

Figure 2. Overview of the Symphony IL-6 test principle.

The Symphony Test Cartridge

To perform a Symphony test, the test operator adds three drops of blood to the Symphony Cartridge. The volume does not have to be precise because the cartridge is able to work with a range of 0.1 — 0.2 cc, which can be visualized with a fill-gauge on the Symphony Cartridge as shown in Figure 3. After scanning in the patient ID, the Symphony Cartridge is inserted into the Symphony and the test proceeds automatically. Up to six Symphony Cartridges can be tested simultaneously, enabling up to six different patients or six different biomarkers to be tested at once on a single machine. In approximately 24 minutes, the measurement results are produced, and a clinical decision can be made.

The disposable cartridge contains the reagents required to run the applicable test. The three steps of the test (sample preparation, chemical reaction, and detection) are performed in chambers present on the cartridge. All waste is collected in a chamber in the cartridge significantly reducing the risk of lab contamination that is often cited as a concern of molecular diagnostic testing. After the test is completed and the result is obtained, the cartridge is disposed of with the hospital’s other medical waste.

6

Figure 3. Photograph of the Symphony IL-6 Cartridge loaded with a whole blood specimen.

Manufacturing

We plan to manufacture both our devices and cartridges through Contract Manufacturing Organizations (“CMOs”). We have contracts with Toray to manufacture our cartridges and Sanyoseiko to manufacture both our devices and cartridges. Pursuant to our agreement with Toray, we are required to use Toray to manufacture test cartridges for a period of three years. We believe both companies are well-known and well-established global manufacturing companies with capabilities to scale up, re-design and supply our devices and cartridges globally when needed. Therefore, we believe we will have the capability to supply globally, when required. Both Toray and Sanyoseiko facilities are located in Japan.

We outsource our manufacturing due to a number of factors; including,

| ● | The cost of initiating and scaling in-house manufacturing is capital intensive, |

| ● | It would take significant time to establish our own manufacturing facilities, |

| ● | It would take significant time to obtain necessary certifications by regulatory authorities; and |

| ● | There would be a significant personnel and maintenance costs to maintain production in compliance with regulations. |

In the first quarter of 2021, we established Sanyoseiko as our large-scale contract manufacturing organization. Toray will continue to develop, validate and manufacture our current IL-6 cartridges and other cartridges in our product pipeline as our pilot-manufacturing partner.

Regulatory Strategy

We license the technology for Symphony from Toray. Our license grants us exclusive world-wide use with the exception of Japan. Toray started developing the Symphony (known as RAY-FAST in Japan) to complement one of its sepsis related products for blood purification during sepsis. Development of RAY-FAST begin in 2006. For the past 3-4 years, RAY-FAST has been used successfully in Japan by selected clinical institutions for measurement of IL-6 in rheumatoid arthritis to monitor disease progression for the purpose of clinical validation, efficacy, monitoring potential adverse conditions reporting, robustness, durability and customer feedback on usability.

Our initial regulatory pathway is to label and distribute Symphony as an Research Use Only, or RUO product in the U.S. An RUO product is an in-vitro diagnostic device that is in the laboratory research phase of development. RUO devices are not authorized for use in clinical or diagnostic applications. However, it is possible that certain laboratories may choose to independently utilize the RUO Symphony as part of their own Laboratory Developed Test, or LDT. An LDT is a type of in vitro diagnostic test that is designed, manufactured and used within a single laboratory. In parallel, we are pursuing 510(k) clearance from FDA to use Symphony for in vitro diagnostic use.

7

Symphony IL-6

Our Symphony IL-6 product candidate is intended for early and rapid identification of sepsis during Emergency Department (“ED”), critical care triage, and neutropenic sepsis in oncology patients. Our Symphony IL-6 product candidate is also intended for monitoring disease progression during such treatment regimen.

We are conducting a multi-center clinical study at The University of Texas, Southwestern Medical Center (William P. Clements Jr. University Hospital (CUH) and Zale Lipshy Pavilion Hospital) and Parkland Memorial Hospital under a single protocol. Our clinical study will involve:

| ● | A reference range study. For the reference range study, 120 subjects will be enrolled to achieve at a minimum 100 qualified data points for the statistical analysis. The reference range (2.5th to 97.5th centile) will be estimated using parametric methods. Parametric methods will be used to calculate the 95% confidence intervals for the reference limits. Nonparametric estimates of the reference limits with confidence intervals will be computed as a sensitivity analysis. |

| ● | A cutoff value study. For the cutoff value study, 96 subjects will be enrolled to achieve at a minimum 80 qualified data points for the statistical analysis. For the cutoff value study, the Receiver Operating Characteristic (“ROC”) curve will be estimated. The ideal cutoff, which gives a point on the ROC curve that is closest to the (0.1) point, will be selected based on the results from this study. |

| ● | A cutoff validation study. For the cutoff validation study, 48 patients will be enrolled into the study to achieve at a minimum 40 qualified data points. Clinical sensitivity, clinical specificity, positive predictive value, negative predictive value, and corresponding 95% confidence intervals will be calculated using the cutoff value determined from the cutoff value study. |

In parallel to these studies, we intend to capture the necessary analytical data required for FDA submission. These studies will be performed using patient samples with natural IL-6 and will be performed in accordance with the Clinical & Laboratory Standards Institute (“CLSI”) guidelines.

We plan to start clinical studies at other clinical sites to support additional indications and possibly additional FDA premarket submissions. In addition to ICUs, we plan to add both adult and pediatric oncology patients. We plan to perform blood collections by both venipuncture and capillary collection, which includes both finger stick and heel stick, in our studies so we can support these indications for use.

Blood collection for pediatric patients is often faced with many challenges due to their limited supply of blood and the difficulty of performing venipuncture collections. We believe the small amount of blood needed for Symphony will be very attractive for pediatric healthcare. Furthermore, we have planned in our clinical studies to include finger stick and heel stick blood collection to further reduce the clinical burden of performing tests in pediatric patients.

We submitted a pre-submission application to the FDA presenting our study design and the data from our first set of studies. We will use their feedback, if necessary, to modify the ongoing studies and to construct the FDA clearance application. We plan to submit our FDA clearance application at the end of the third quarter of 2022.

The importance of IL-6 testing has been further highlighted during the COVID-19 pandemic, and IL-6 concentrations in blood have been found to be heightened in patients with COVID-19-associated systemic inflammation and hypoxic respiratory failure. If clinical studies are successful, our Symphony IL-6 product candidate could also be used with confirmed COVID-19 illness to aid in determining the risk of intubation with mechanical ventilation, in conjunction with clinical findings and the results of other laboratory testing. In our ongoing clinical studies, we have performed prospective Symphony IL-6 tests on the whole blood of 90 subjects admitted to either William P. Clements Jr. University Hospital, Zale Lipshy Pavilion Hospital, or Parkland Memorial Hospital with confirmed COVID-19, confirmed by an FDA Emergency Use Authorization, or EUA PCR SARS-CoV-2 test. Once completed, we believe our planned study design can be used to apply for an EUA for use with confirmed COVID-19 illness to aid in determining the risk of intubation with mechanical ventilation, in conjunction with clinical findings and the results of other laboratory testing. There is no assurance that we will be successful in obtaining EUA for this indication.

8

Symphony hsTNT/I and NT-proBNP

We have two other product candidates that are in development: (i) hsTNT/I for myocardial injury or myocardial infarction (MI) and (ii) NT-proBNP for cardiac heart failure (“CHF”). These product candidates will follow a similar regulatory pathway as identified for our Symphony IL-6 product candidate which we believe will result in obtaining 510(k) clearance for diagnostic use.

For the clinical trial, we plan to have both retrospective samples and prospective subjects to power the study to have a statistically significant result. For retrospectively collected samples, we will utilize clinical information recorded during the original sample collection. For prospectively collected samples, clinical information will be collected initially during admission or ER triage, and will be considered as baseline samples. Clinical information will also be collected on discharge, shift or admission to ICU. Our clinical plan also allows us to monitor ER or admitted patients during their treatment regimen.

Sales and Marketing

Initially, we plan to have four major sales territories; Northeast, Northwest, Central (South central and North central) and West (North west and South west). These territories will be served and supported by territory sales managers and technical sales support managers. A centralized sales and technical support team will support the regional groups. We intend to focus our initial sales efforts on the large institutions, hospitals, and LTACs that operate multiple facilities and therefore might purchase multiple units. This ‘Waterfall’ strategy, focusing on sales within those institutions, may lower salesforce costs.

Our sales representatives will typically have experience in molecular diagnostic testing and a network of customer contacts within their respective territories. We will utilize our teams’ knowledge along with market research databases to target and qualify our customers. We intend to execute a variety of sales campaigns and strategies to meet the buying criteria of the different customer segments we intend to pursue.

In the United States, our sales cycle will typically include customer evaluations, a decision to use our platform and then validation of our platform. Upon successful validation a hospital or reference lab may choose to become a customer. The analyzer will be available to the customer by purchase or third-party lease for their use with our diagnostic test. The customer will buy our proprietary test cartridge from us and utilize one disposable test cartridge each time they run a diagnostic test.

We have deployed the Symphony and test cartridges in the United States in selected medical institutions and LTAC facilities for evaluation. Our goal is to convert these facilities into paying customers if we receive FDA authorization.

Customers

Our initial focus is on the following types of customers:

Medical Institution and Hospitals with Intensive Care Unit (ICUs): ICUs treat patients with severe or life-threatening illnesses and injuries, which require constant care, close supervision from life support equipment and medication to ensure normal bodily functions. ICUs are staffed by highly trained physicians, nurses and respiratory therapists who specialize in caring for critically ill patients. ICUs are also distinguished from general hospital wards by a higher staff-to-patient ratio and access to advanced medical resources and equipment that is not routinely available elsewhere. The types of patients typically seen in ICUs are those with acute and advanced respiratory distress syndrome, septic shock, and patients requiring support for an acute reversible failure of one or more organs.

Long-term Acute Care facilities (LTACs): LTACs are facilities that specialize in the treatment of patients with serious medical conditions that require care on an on-going basis but no longer require intensive care or extensive diagnostic procedures. These patients are typically discharged from the intensive care units and require more care than they can receive in a rehabilitation center, skilled nursing facility, or at home. The types of patients typically seen in LTACs include those requiring prolonged ventilator use or weaning, ongoing dialysis for chronic renal failure, intensive respiratory care, multiple IV medications or transfusions, and complex wound care/care for burns.

Outpatient Clinics: A clinic (or outpatient or ambulatory care clinic) is a health care facility that is primarily focused on the care of outpatients. Clinics can be privately operated or publicly managed and funded. They typically cover the primary care needs of populations in local communities. Typical large outpatient clinics house general medical practitioners such as doctors and nurses to provide ambulatory care and some acute care services including patient triage for sepsis and cardiac patients. The types of patient care they perform include blood tests, triage with chest pain complaints, triage with septic shock, biopsies, chemotherapy, colonoscopy, CT scan, mammograms, minor surgical procedures, radiation treatments, ultrasound imaging and x-rays.

9

License Agreement

We have an exclusive license with Toray for the entire world, excluding Japan, to use their patents and know-how related to Symphony and the detection cartridges for the manufacturing, marketing and sale of the products (as defined in the agreement). We also have a nonexclusive license for the same purposes in Japan. The term of this license agreement extends until the expiration of all the patents associated with the licensed patent rights, which are between 2029 and 2036. If we do not generate commercial sales within five years of the date of the license, Toray has the right to terminate the agreement or make it non-exclusive. In addition, we are required to make commercially reasonable efforts to obtain market approval for the products in the United States and the European Union by October 2023. Pursuant to the agreement, we are required to use Toray to manufacture the sample cartridges. The agreement terminates upon expiration of the last of the patents included in the license.

In connection with entering into the agreement, we paid Toray $240,000 in licensing fees. We are required to pay a 15% royalty fee for the period that any underlying patents exist or for 5 years after the first sale for the licensing of this technology based on a percentage of our “Net Sales” of products using these technologies (as defined in the license agreement) with a minimum royalty of $60,000 for the initial year that royalties are payable increasing to a minimum of $100,000 thereafter.

Intellectual Property, Proprietary Technology

We do not currently hold any patents directly. We rely on a combination either directly or through our license agreement with Toray of patent, copyright, trade secret, trademark, confidentiality agreements, and contractual protection to establish and protect our proprietary rights. We have licensed U.S. Patent Nos. 8,409,447 (“the ‘447 patent”) and 8,821,813 (“the ‘813 patent”). The ‘447 patent is valid through at least February 2029 and is generally directed to a separation chip and a method for separating an insoluble component from a suspension with the separation chip. The ‘813 patent is valid through at least March 2028 and is generally directed to a liquid-feeding chip, a liquid feeding method and analysis method. We have also licensed use or process patents covering the inventions and/or subject matter of the ‘447 and ‘813 patents in various international territories including Japan, Canada, China, Europe and South Korea, which are valid through at least February 2027.

These measures may not be adequate to safeguard the technology underlying our products. For example, employees, consultants and others who participate in the development of our products may breach their agreements with us regarding our intellectual property, and we may not have adequate remedies for the breach. We also may not be able to effectively protect our intellectual property rights in some foreign countries, as many countries do not offer the same level of legal protection for intellectual property as the United States. Furthermore, for a variety of reasons, we may decide not to file for patent, copyright or trademark protection outside of the United States. Our trade secrets could become known through other unforeseen means. Notwithstanding our efforts to protect our intellectual property, our competitors may independently develop similar or alternative technologies or products that are equal or superior to our technology. Our competitors may also develop similar products without infringing on any of our intellectual property rights or design around our proprietary technologies. Furthermore, any efforts to enforce our proprietary rights could result in disputes and legal proceedings that could be costly and divert attention from our business. We could also be subject to third-party claims that we require additional licenses for our products, and such claims could interfere with our business. If our products infringe the intellectual property rights of others, we could face costly litigation, which could cause us to pay substantial damages and limit our ability to sell some or all of our products. Even if our products were determined not to infringe the intellectual property rights of others, we could incur substantial costs in defending any such claims.

Competition

Our primary competition is laboratory size equipment including the Roche Cobas®, Siemens ADVIA Centaur® and Beckman Coulter Access 2®.

10

Our competitors have substantially greater financial, technical, research and other resources and larger, more established marketing, sales and distribution organizations than we do. Our competitors also offer broader product lines and have greater brand recognition than we do. Moreover, our existing and new competitors may make rapid technological developments that may result in our technologies and products becoming obsolete before we recover the expenses incurred to develop them or before they generate significant revenue. We may encounter potential customers that, due to existing relationships with our competitors, are committed to or prefer the products offered by these competitors. There can be no assurance that competitors, many of which have made substantial investments in competing technologies, will not prevent, limit or interfere with our ability to make, use or sell our products either in the United States or in international markets.

Government Regulation

The design, development, manufacture, testing and sale of our diagnostic products are subject to regulation by numerous governmental authorities, principally the FDA, and corresponding state and foreign regulatory agencies.

FDA Regulation

Research Use Only Technologies

Symphony will initially be commercialized as an RUO tool in the United States. RUO products belong to a separate regulatory classification under a long-standing FDA regulation. From an FDA perspective, products that are intended for research use only and are labeled as RUO are not regulated by the FDA as in vitro diagnostic devices and are therefore not subject to the regulatory requirements discussed below for clinical diagnostic products. Thus, RUO products may be used or distributed for research use without first obtaining FDA clearance, authorization or approval. The products must bear the statement: “For Research Use Only. Not for Use in Diagnostic Procedures.” RUO products cannot make any claims related to safety, effectiveness or diagnostic utility, and they cannot be intended by the manufacturer for human clinical diagnostic use. Accordingly, a product labeled RUO but intended or promoted for clinical diagnostic use may be viewed by the FDA as false or misleading and thereby adulterated and misbranded products under the Federal Food, Drug, and Cosmetic Act (“FDCA”) and subject to FDA enforcement action. The FDA’s 2013 Guidance for Industry and Food and Drug Administration Staff on “Distribution of In Vitro Diagnostic Products Labeled for Research Use Only or Investigational Use Only,” explains that the FDA will consider the totality of the circumstances surrounding distribution and use of an RUO product, including how the product is marketed and to whom, when determining its intended use. Merely including a labeling statement that a product is intended for research use only will not necessarily exempt the device from the FDA’s 510(k) clearance, premarket approval, or other requirements, if the circumstances surrounding the distribution of the product indicate that the manufacturer intends its product to be used for clinical diagnostic use. These circumstances may include written or verbal marketing claims or links to articles regarding a product’s performance in clinical applications, a manufacturer’s provision of technical support for clinical validation or clinical applications, or solicitation of business from clinical laboratories, all of which could be considered evidence of intended uses that conflict with RUO labeling. If the FDA disagrees with a company’s RUO status for its product, the company may be subject to FDA enforcement activities, including, without limitation, removal of the product, or requiring the company to seek clearance, authorization or approval for the products.

Medical Devices

Generally, in vitro diagnostic products we develop must be cleared by the FDA before they are marketed in the United States. Before and after approval, authorization, or clearance in the United States, our products are subject to extensive regulation by the FDA, as well as by other regulatory bodies. FDA regulations govern, among other things, the development, testing, manufacturing, labeling, safety, storage, recordkeeping, market clearance, authorization or approval, advertising and promotion, import and export, marketing and sales, and distribution of medical devices, including in vitro diagnostic devices (“IVDs”). IVDs are a type of medical device and include reagents and instruments used in the diagnosis or detection of diseases, conditions or infections, including, without limitation, the presence of certain chemicals or other biomarkers. Predictive, prognostic and screening tests can also be IVDs.

In the United States, medical devices are subject to varying degrees of regulatory control and are classified in one of three classes depending on the extent of controls the FDA determines are necessary to reasonably ensure their safety and effectiveness:

| ● | Class I: general controls, such as labeling and adherence to quality system regulations; |

| ● | Class II: special controls, premarket notification (often referred to as a 510(k)), specific controls such as performance standards, patient registries, post-market surveillance, additional controls such as labeling and adherence to quality system regulations; and |

| ● | Class III: special controls and approval of a premarket approval (“PMA”) application. |

11

After a medical device is placed on the market, numerous regulatory requirements apply. These include:

| ● | compliance with the FDA’s QSR, which requires manufacturers to follow stringent design, testing, control, documentation, record maintenance, including maintenance of complaint and related investigation files, and other quality assurance controls during the manufacturing process; |

| ● | labeling regulations, which prohibit the promotion of products for uncleared, or unapproved uses, or “off-label” uses, and impose other restrictions on labeling; and |

| ● | obligations to investigate and report to the FDA adverse events, including deaths, or serious injuries that may have been or were caused by a medical device and malfunctions in the device that would likely cause or contribute to a death or serious injury if it were to recur. |

Failure to comply with applicable regulatory requirements can result in enforcement action by the FDA, which may include sanctions, including but not limited to, warning letters; fines, injunctions, and civil penalties; recall or seizure of the device; operating restrictions, partial suspension or total shutdown of production; refusal to grant 510(k) clearance, de novo authorization, or approval of a PMA application for new devices; withdrawal of clearance, authorization, or approval; and civil or criminal prosecution.

Premarket Authorization and Notification

While most Class I and some Class II devices can be marketed without prior FDA authorization, most medical devices can be legally sold within the U.S. only if the FDA has: (i) approved a PMA application prior to marketing, generally applicable to Class III devices; or (ii) cleared the device in response to a premarket notification, or 510(k) submission, generally applicable to Class II and some Class I devices. Some devices that have been classified as Class III are regulated pursuant to the 510(k) requirements because FDA has not yet called for PMAs for these devices. Other less common regulatory pathways to market medical devices include Emergency Use Authorization or the EUA process which is only available during public health emergencies, humanitarian device exception (“HDE”) or a product development protocol (“PDP”).

510(k) Notification

Product development in the U.S. for most Class II and limited Class I devices typically follows a 510(k) pathway. To obtain 510(k) clearance, a manufacturer must submit a premarket notification demonstrating that the proposed device is substantially equivalent to a legally marketed device, referred to as the predicate device. A predicate device may be a previously 510(k) cleared device or a device that was in commercial distribution before May 28, 1976 for which the FDA has not yet called for submission of PMA applications. The manufacturer must show that the proposed device has the same intended use as the predicate device, and it either has the same technological characteristics, or it is shown to be equally safe and effective and does not raise different questions of safety and effectiveness as compared to the predicate device.

There are three types of 510(k)s: traditional; special, for devices that are modified and the modification needs a new 510(k) but the modification does not affect the intended use or alter the fundamental scientific technology of the device; and abbreviated, for devices that conform to a recognized standard. The special and abbreviated 510(k)s are intended to streamline review. The FDA intends to process special 510(k)s within 30 FDA days of receipt, and abbreviated 510(k)s within 90 FDA days of receipt. The clearance pathway for traditional 510(k)s can, however, take from four to 12 months, or even longer if FDA has questions during the review.

After a device receives 510(k) clearance, any modification that could significantly affect its safety or effectiveness, or that would constitute a major change in its intended use, requires a new 510(k) clearance or could require a de novo authorization approval of a PMA application. The FDA requires each manufacturer to make this determination in the first instance, but the FDA can review any such decision. If the FDA disagrees with a manufacturer’s decision not to seek a new 510(k) clearance, the agency may retroactively require the manufacturer to seek 510(k) clearance, de novo authorization, or PMA approval. The FDA also can require the manufacturer to cease marketing and/or recall the modified device until 510(k) clearance, de novo authorization, or PMA approval is obtained.

During the review of a 510(k) submission, the FDA may request more information or additional studies and may decide the indications for which we seek clearance should be limited. In addition, laws and regulations and the interpretation of those laws and regulations by the FDA may change in the future. We cannot foresee what effect, if any, such changes may have on us.

12

De Novo Classification

Devices of a new type that FDA has not previously classified based on risk are automatically classified into Class III by operation of section 513(f)(1) of the FDCA, regardless of the level of risk they pose. To avoid requiring PMA review of low- to moderate-risk devices classified in Class III by operation of law, Congress enacted section 513(f)(2) of the FDCA. This provision allows FDA to classify a low- to moderate-risk device not previously classified into Class I or II. After de novo authorization, an authorized device may be used as a predicate for future devices going through the 510(k) process.

PMA Application

A product not eligible for 510(k) clearance or de novo authorization must follow the PMA approval pathway, which requires proof of the safety and effectiveness of the device to the FDA’s satisfaction.

Results from adequate and well-controlled clinical trials are required to establish the safety and effectiveness of a Class III PMA device for each indication for which FDA approval is sought. After completion of the required clinical testing, a PMA including the results of all preclinical, clinical, and other testing, and information relating to the product’s marketing history, design, labeling, manufacture, and controls, is prepared and submitted to the FDA.

The PMA approval process is generally more expensive, rigorous, lengthy, and uncertain than the 510(k) premarket notification process and requires proof of the safety and effectiveness of the device to the FDA’s satisfaction. As part of the PMA review, the FDA will typically inspect the manufacturer’s facilities for compliance with the QSR requirements, which impose elaborate testing, control, documentation and other quality assurance procedures. The FDA’s review of a PMA application typically takes one to three years, but may last longer. If the FDA’s evaluation of the PMA application is favorable, the FDA will issue a PMA for the approved indications, which can be more limited than those originally sought by the manufacturer. The PMA can include post-approval conditions that the FDA believes necessary to ensure the safety and effectiveness of the device including, among other things, restrictions on labeling, promotion, sale and distribution. Failure to comply with the conditions of approval can result in material adverse enforcement action, including the loss or withdrawal of the approval and/or placement of restrictions on the sale of the device until the conditions are satisfied.

Even after approval of a PMA, a new PMA or PMA supplement is required in the event of a modification to the device, its labeling or its manufacturing process. Supplements to a PMA often require the submission of the same type of information required for an original PMA, except that the supplement is generally limited to that information needed to support the proposed change from the product covered by the original PMA.

EUA Process

The program for authorizations of products through an Emergency Use Authorization (“EUA”) is established when the Secretary of Health and Human Services declares a public health emergency. This process remains in effect only as long the declared public health emergency is in effect. An EUA authorization is granted by FDA using similar analytical and clinical validation metrics similar to what may be required for 510(k), PMA or de novo authorizations but are based on a reduced amount of data. The process to obtain an EUA typically consists of two phases, an initial Pre-EUA submission that is used to identify and resolve any significant problems that would preclude issuance of an EUA and a final EUA submission. The final EUA submission addresses the details that the FDA will require to demonstrate that the Symphony IL-6 test will have acceptable analytical and clinical performance. FDA has granted EUA for the Roche Elecsys IL-6 test, the Siemens ADVIA Centaur IL-6 test and the Beckman Coulter Access IL-6 test. FDA publishes summaries of the testing performed to support these EUAs, which will serve as guidance as we prepare our EUA. There are no required timelines for review and authorization of an EUA. Moreover, FDA has prioritized those IVD EUA that the agency will review to include molecular and antigen tests that may be used at the POC or completely at home; the manufacturer has the capacity to scale up to a production of >500,00 tests per week within 3 months of authorization; or tests that are from or supported by US government stakeholder, e.g. BARDA or NIH’s RADx program. For serology tests, FDA intends to focus on quantitative and neutralizing antibody tests. There is no guarantee that the Symphony IL-6 assay will be a priority for FDA review.

13

Clinical Trials of Medical Devices

Clinical trials are almost always required to support a PMA, are often required for a de novo authorization, and are sometimes required for 510(k) clearance. Clinical trials may also be conducted or continued to satisfy post-approval requirements for devices with PMAs. Clinical studies of unapproved or uncleared medical devices or devices being studied for uses for which they are not approved or cleared (investigational devices) must be conducted in compliance with FDA requirements. If an investigational device could pose a significant risk to patients, the sponsor company must submit an Investigational Device Exemption (“IDE”) application to the FDA prior to initiation of the clinical study. An IDE application must be supported by appropriate data, such as animal and laboratory test results, showing it is safe to test the device on humans and the testing protocol is scientifically sound. The IDE will automatically become effective 30 days after receipt by the FDA unless the FDA notifies the company the investigation may not begin. Clinical studies of investigational devices may not begin until an institutional review board (“IRB”) has approved the study.

During any study, the sponsor must comply with the applicable portions of FDA’s IDE requirements. These requirements include investigator selection, trial monitoring, adverse event reporting, and record keeping. The investigators must obtain patient informed consent, rigorously follow the investigational plan and study protocol, control the disposition of investigational devices, and comply with reporting and record keeping requirements.

A nonsignificant risk device does not require FDA approval of an IDE; however, the clinical trial must still be conducted in compliance with various requirements of FDA’s IDE regulations and be approved by an IRB at the clinical trials sites. We, the FDA, or the IRB at each institution at which a clinical trial is being conducted may suspend a clinical trial at any time for various reasons, including a belief the subjects are being exposed to an unacceptable risk. During the approval, authorization, or clearance process, the FDA may inspect the records relating to the conduct of one or more investigational sites participating in the study supporting the application.

Even if a trial is completed, the results of clinical testing may not demonstrate the safety and effectiveness of the device, may be equivocal or may otherwise not be sufficient to obtain approval, authorization, or clearance of the product.

Sponsors of applicable clinical trials of devices are required to register with www.clinicaltrials.gov, a public database of clinical trial information. Information related to the device, patient population, phase of investigation, study sites and investigators and other aspects of the clinical trial is made public as part of the registration.

Although the QSR does not fully apply to investigational devices, the requirement for controls on design and development does apply. The sponsor also must manufacture the investigational device in conformity with the quality controls described in the IDE application and any conditions of IDE approval that the FDA may impose with respect to manufacturing.

Post-Approval Regulation of Medical Devices

After a device is cleared, authorized, or approved for marketing, numerous and pervasive regulatory requirements continue to apply. These include:

| ● | the FDA QSR, which applies to manufacturers, developers, and contract manufacturers, and governs, among other things, how manufacturers design, test manufacture, exercise quality control over, and document manufacturing of their products; |

| ● | establishment registration and device listing |

| ● | corrections and removal reporting regulations, which require that manufactures report to FDA field corrections or removals if undertaken to reduce a risk to health posed by a device or to remedy a violation of the FDCA that may present a risk to health; |

| ● | labeling and claims regulations, which prohibit the promotion of products for unapproved or “off-label” uses and impose other restrictions on labeling; and |

| ● | the Medical Device Reporting regulation, which requires reporting to the FDA of certain adverse experience associated with use of the product. |

14

We will continue to be subject to inspection by the FDA to determine our compliance with regulatory requirements. If the FDA finds a violation, it can institute a wide variety of enforcement actions, ranging from a public warning letter to more severe sanctions such as:

| ● | fines, injunctions, and civil penalties; |

| ● | recall or seizure of products; |

| ● | operating restrictions, partial suspension or total shutdown of production; |

| ● | refusing requests for 510(k) clearance or PMA approval of new products; |

| ● | withdrawing 510(k) clearance or PMA approvals already granted; and |

| ● | criminal prosecution. |

QSR Requirements

Manufacturers of medical devices are required to comply with FDA quality system requirements set forth the QSR. The QSR requires, among other things, establishment of a quality system and processes for design and development and manufacturing controls as well as the corresponding maintenance of records and documentation. Certain adverse events and malfunctions with the product must be reported to the FDA and could result in the imposition of marketing restrictions through labeling changes or in product withdrawal. Product approvals, authorizations, or clearances may be withdrawn if compliance with regulatory requirements is not maintained or if problems concerning safety or effectiveness of the product occurs following the approval, authorization, or clearance. We will use contract manufacturers to manufacture our products for the foreseeable future. We will, therefore, be dependent on their compliance with these requirements to market our products. We work closely with our contract manufacturers to assure our products are in strict compliance with these regulations.

Export Regulations

Medical devices that are legally marketed in the United States may be exported anywhere in the world without prior FDA notification or approval. Devices that have not been approved or cleared in the United States must follow the export provisions of the FDCA. Depending on which section of the FDCA we may export under, we may need to request an export permit letter or export certificate, or we may need to submit a simple notification. Export certificates may be requested by foreign customers or foreign governments to provide proof of the products’ status as regulated by the FDA. The export certificate is prepared by FDA and contains information about a product’s regulatory or marketing status in the United States.

Clinical Laboratory Improvement Amendments of 1988

The use of our products is also affected by the Clinical Laboratory Improvement Amendments of 1988 (“CLIA”) and related federal and state regulations, which provide for regulation of laboratory testing. Any customers using our products for clinical use in the United States will be regulated under CLIA, which establishes quality standards for all laboratory testing to ensure the accuracy, reliability and timeliness of patient test results regardless of where the test was performed. In particular, these regulations mandate that clinical laboratories must be certified by the federal government or a federally approved accreditation agency, or must be located in a state that has been deemed exempt from CLIA requirements because the state has in effect laws that provide for requirements equal to or more stringent than CLIA requirements. Moreover, these laboratories must meet quality assurance, quality control and personnel standards, and they must undergo proficiency testing and inspections. The CLIA standards applicable to clinical laboratories are based on the complexity of the method of testing performed by the laboratory, which range from “waived” to “moderate complexity” to “high complexity.”

Laboratory-developed tests.

The FDA considers LDTs to be tests that are designed, developed, validated and used within a single laboratory. The FDA historically has taken the position that it has the authority to regulate such tests as medical devices under the FDC Act but has for the most part exercised enforcement discretion and has not required clearance, authorization, or approval of LDTs prior to marketing. Rather, in place of premarket clearance or approval and other medical device general and special controls, the agency has relied on the certification of the laboratory under CLIA to ensure the quality and validity of the tests.

15

Under present FDA enforcement discretion, most LDTs currently do not require premarket clearance or approval. Instead, LDTs are generally subject to CLIA regulations, provided that:

| 1. | the tests must be developed and validated by a laboratory certified by CLIA as capable of performing high complexity tests; |

| 2. | the developed LDT may be requested only on the order of a physician or other licensed health care provider; |

| 3. | the technological characteristics of the LDT are not so complex or potentially misunderstood by users such that the technology alone creates a significant health risk to patients; |

| 4. | the LDT is not marketed directly to consumers; and |

| 5. | the LDT does not present a specific patient or population risk such that FDA determines that enforcement discretion is not warranted or appropriate. |

Foreign Government Regulation

We intend to market our products in European and other select international markets. The regulatory pre-market requirements for molecular devices vary from country to country. Some countries impose product standards, packaging requirements, labeling requirements and import restrictions on devices. Each country has its own tariff regulations, duties and tax requirements. Failure to comply with applicable foreign regulatory requirements may subject us to fines, suspension or withdrawal of regulatory approvals, product recalls, seizure of products, operating restrictions and criminal prosecution. For products sold in the European Economic Area, we have self-declared a Declaration of Conformity under the relevant sections of the applicable European Community standards and other normative documents.

Fraud and Abuse Regulations

We are subject to numerous federal and state health care anti-fraud laws, including the federal anti-kickback statute and False Claims Act that are intended to reduce waste, fraud and abuse in the health care industry. These laws are broad and subject to evolving interpretations. They prohibit many arrangements and practices that are lawful in industries other than health care, including certain payments for consulting and other personal services, some discounting arrangements, the provision of gifts and business courtesies, the furnishing of free supplies and services, and waivers of payments. In addition, many states have enacted or are considering laws that limit arrangements between medical device manufacturers and physicians and other health care providers and require significant public disclosure concerning permitted arrangements. These laws are vigorously enforced against medical device manufacturers and have resulted in manufacturers paying significant fines and penalties and being subject to stringent corrective action plans and reporting obligations. If we are ever accused of violating them, we could be forced to expend significant resources on investigation, remediation and monetary penalties.

Patient Protection and Affordable Care Act

Our operations will be affected by the federal Patient Protection and Affordable Care Act of 2010, as modified by the Health Care and Education Reconciliation Act of 2010, which we refer to as the Health Care Act. Among other things, the Health Care Act requires manufacturers to report to HHS detailed information about financial arrangements with physicians, teaching hospitals and certain other categories of health care providers. These reporting provisions preempt state laws that require reporting of the same information, but not those that require reports of different or additional information. Failure to comply subjects the manufacturer to significant civil monetary penalties.

Health Insurance Coverage and Reimbursement

Our ability to successfully commercialize our product candidates will depend in part on the extent to which governmental authorities, private health insurers and other third-party payors provide coverage for and establish adequate reimbursement levels for our product candidates.

16

In the United States, third-party payors continue to implement initiatives that restrict the use of certain technologies to those that meet certain clinical evidentiary requirements. In addition to uncertainties surrounding coverage policies, there are periodic changes to reimbursement. Third-party payors regularly update reimbursement amounts and also from time to time revise the methodologies used to determine reimbursement amounts. This includes annual updates to payments to physicians, hospitals and ambulatory surgery centers for procedures during which our products are used.

Employees

As of December 31, 2021, we have nine full-time employees. We also contract with several consultants and contractors performing public relations, investor relations, and accounting functions. None of our employees are represented by labor unions or covered by collective bargaining agreements.

Available Information

Our principal executive offices are located at 360 Massachusetts Avenue, Suite 203, Acton, MA 01720 and our telephone number is (844) 327-7078. Our website address is www.bluejaydx.com. We make available free of charge through the Investors Relations section of our website our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the U.S. Securities and Exchange Commission. We include our website address in this report only as an inactive textual reference and do not intend it to be an active link to our website. The contents of our website are not incorporated into this report.

ITEM 1A. RISK FACTORS

Risk Factor Summary

The following summary highlights the material risks that may affect our business, operating results, financial condition and prospects, as more fully described in the pages that follow this summary.

Risks Related to Our Financial Condition and Capital Requirements

We are subject to the risks associated with new businesses.