UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| For the fiscal year ended December 31, 2019 |

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| For the transition period from ___________ to ___________ |

|

| |

| Commission File No. 001-34864 |

| TGS International Ltd. |

| (Exact Name of Registrant as Specified in its Charter) |

| Nevada |

| N/A |

| (State or Other Jurisdiction of Incorporation) |

| (I.R.S. Employer Identification Number) |

Suite 1023, 10/F., Ocean Centre

5 Canton Rd., Tsim Sha Tsui

Kowloon, Hong Kong

(Address of principal executive offices) (zip code)

(852)2116-3863

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Exchange Act:

| Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

| Common Stock |

| TGSI |

| OTC Markets – Pink Sheets |

Securities registered under Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-K (ss.229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” and “emerging grown company,” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

|

| Emerging Growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based upon the average bid and asked price of the registrant’s common stock on June 28, 2019, the last business day of the Company’s second fiscal quarter, was $4,101,839.

As of March 20, 2020, the number of shares outstanding of the registrant’s common stock was 14,858,328.

DOCUMENTS INCORPORATED BY REFERENCE

None.

|

|

| 2 |

|

|

FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K (the “Report”) and other reports (collectively the “Filings”) filed by the registrant from time to time with the Securities and Exchange Commission (the “SEC”) contain or may contain forward looking statements and information that are based upon beliefs of, and information currently available to, the registrant’s management as well as estimates and assumptions made by the registrant’s management. When used in the filings the words “anticipate,” “believe,” “estimate,” “expect,” “future,” “intend,” “plan” or the negative of these terms and similar expressions as they relate to the registrant or the registrant’s management identify forward looking statements. Such statements reflect the current view of the registrant with respect to future events and are subject to risks, uncertainties, assumptions and other factors (including the risks contained in the section of this Report entitled “Risk Factors”) relating to the registrant’s industry, the registrant’s operations and results of operations and any businesses that may be acquired by the registrant. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

Although the registrant believes that the expectations reflected in the forward looking statements are reasonable, the registrant cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, the registrant does not intend to update any of the forward-looking statements to conform these statements to actual results. The following discussion should be read in conjunction with the registrant’s financial statements and the related notes thereto included in this Report.

In this Report, “we,” “our,” “us,” “TGS International Ltd.” or the “Company” sometimes refers collectively to TGS International Ltd. and its subsidiaries and affiliated companies.

General Overview

The Company was established on December 1, 2016 in Nevada, USA. On September 14, 2018, the Company and Arcus Mining Holdings Limited (“Arcus”) entered into a Share Exchange Agreement, dated September 14, 2018 (the “Share Exchange Agreement”), with Chi Kin Loo, Billion Plus Limited, First Fortune Investment Limited, Great Win Limited and Master Value Holdings Limited (the “Selling Stockholders”), pursuant to which the Selling Stockholders agreed to sell all of their ordinary shares of Arcus to the Company in exchange for an aggregate of 7,000,000 shares of common stock of the Company. Arcus, through its wholly owned subsidiaries, is engaged in the exploration, mining, processing and sale of fluorite in Mongolia.

Arcus currently owns three fluorite projects through its subsidiaries. Its official mining licenses in Mongolia are shown below:

Details of Three Fluorite Projects transferred to the Company by Arcus

| Mining Project | Fluorite Reserves | Covered Area | License No. | Expiration Date | Current Status |

| Altan Ovoo (Mine A) | To be explored

| 39.35 hectares (97.24 acres) | MV-009918 | December 29, 2034 | In exploration stage. Trial production has been in place since 2019. |

| Oosmonskogo 1 (Mine B) | To be explored

| 98.37 hectares (243.08 acres) | MV-016819 | April 28, 2041 | In exploration stage since 2015. Trial production has been in place since 2018. |

| Oosmonskogo 2 (Mine C) | To be explored | 300.96 hectares (743.69 acres) | MV-017305 | April 23, 2043 | Ready for exploration. |

According to the staged exploration results, there are abundant resources as well as a large potential to expand the resource base of the mines, laying a solid foundation for the sustainable development of the Company.

| 3 |

|

|

| Table of Contents |

Arcus strives to create more value through efficiency in mining. The initial expected annual production capacity of fluorite (“CaF2”) for 2020 and 2021 is described below:

| Type |

| Metallurgical Grade |

| Acid Grade | ||

| CaF2 Content |

| 50% |

| 80% to 90% |

| 97% |

| Estimated Capacity in 2020 |

| 30,000 tons |

| 6,000 tons |

| 22,000 tons |

| Estimated Capacity in 2021 |

| 35,000 tons |

| 6,000 tons |

| 12,000 tons |

| Final Product |

| Granule |

| Granule/Powder |

| Powder |

Arcus intends to start producing 97% Acid Grade powder products and further increase the production of the metallurgical grade products in 2020.

Nevertheless, there are several areas where Arcus expects to outperform the market:

|

| · | Abundant fluorite resources for a long-term sustainable business; and |

|

|

|

|

|

| · | Experience in mine construction, mining and marketing of fluorite. |

In summary, the Company intends to make full use of Mongolia’s fluorite resource advantages and market under the guidance of our experienced management team.

Arcus Company Background

The founders and the management of Arcus have extensive experience in the mining industry in Africa, China, Russia and Mongolia. Their industrial experience includes exploration, mining and mineral investment. With extensive experience in the manufacture and sale of fluorite and related products, Arcus believes the Company will be able to produce the raw material needed for various high standard industrial products, including the manufacture of acid grade fluorite, metallurgical grade fluorite and more.

To meet ever-changing demands from customers, Arcus established a management team comprised of several experienced persons in the industry, as well as financial and marketing experts from international and local markets. The mines use advanced production equipment to produce high-quality products for the market.

In 2014, the Mongolian Parliament waived several restrictions on issuing new minerals exploration licenses and introduced a series of new regulations to encourage foreign investments in the Mongolian mining sector. Arcus is well positioned to take advantage of new opportunities in this promising business environment.

| 4 |

|

|

| Table of Contents |

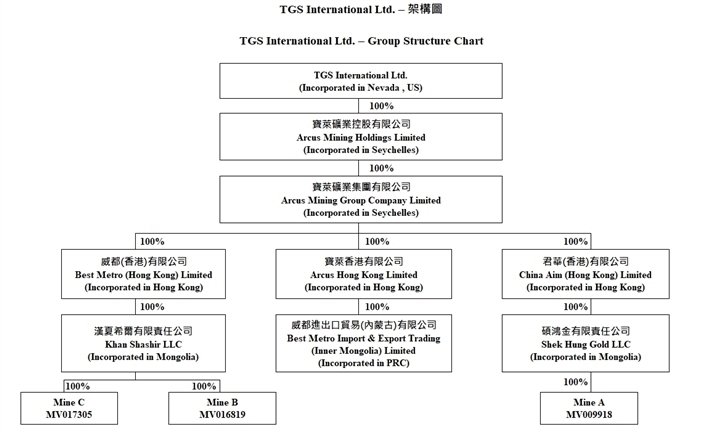

Arcus Company Structure

Arcus indirectly holds three fluorite projects in Mongolia through its wholly owned subsidiaries incorporated in Hong Kong, namely Best Metro (Hong Kong) Limited, China Aim (Hong Kong) Limited, which in turn wholly own Mongolian based fluorite mining companies Khan Shashir LLC (“Khan Shashir”), Shek Hung Gold LLC (“Shek Hung”) respectively. Arcus Hong Kong Limited wholly own the PRC based Best Metro Import & Export Trading (Inner Mongolia) Limited as a trading arm.

The demand for metallurgical grade fluorite in China and other Asian countries currently exceeds supply, and current market conditions are expected to continue for the foreseeable future, creating excellent opportunities for the Company. Inherent uncertainties in the mining industry as well as the changing legal and political environment in Mongolia potentially bring additional business risks, as detailed under “Risk Factors” below.

Shek Hung currently owns a project called Altan Ovoo, while Khan Shashir owns the mines Oosmonskogo 1 and Oosmonskogo 2.

Mining Licenses

The three fluorite projects in Mongolia are Altan Ovoo (“Mine A”), Oosmonskogo 1 (“Mine B”) and Oosmonskogo 2 (“Mine C”).

The three projects have all been issued official mining licenses. The mining licenses allow the right to conduct mining activities throughout the license areas and to construct structures within the license areas that are related to its mining activities.

Mine A is located in Uulbayan soum, Sukhbaatar province, 530 kilometers (“km”) from Ulaanbaatar, the capital of Mongolia. Mine A’s mining license, reference number MV-009918, is valid until December 29, 2034. Mine A covers an area of 39.35 hectares (97.24 acres).

Mine B is located in the Bayan-Ovoo soum, Khentii province, 440 km from Ulaanbaatar. Mine B’s license, reference number MV-016819, is valid until April 28, 2041. Mine B covers an area of 98.37 hectares (243.08 acres).

Mine C is adjacent to Mine B. Mine C’s license, reference number MV-017305, is valid until April 23, 2043. Mine C covers an area of 300.96 hectares (743.69 acres).

| 5 |

|

|

| Table of Contents |

The location map of Mines A, B and C are shown below:

Resources and Reserves

After years of exploration, a significant potential for high grade fluorite resources for Mine A and Mine B has been positively demonstrated.

The historic exploration of Mine A and Mine B can be divided into three phrases:

|

| · | An investigation conducted by the former Soviet Union governmental agencies in the last century; |

|

|

|

|

|

| · | An investigation conducted by an independent consultant from the United States in 2012; and |

|

|

|

|

|

| · | An investigation conducted by SRK Consulting in 2014, a leading mining consulting services provider. |

Arcus’ own geological team will continue to search for other resources through continued exploration in the areas surrounding existing deposits.

Mine A

Phase 1: Investigation conducted by former Soviet Union government agencies in 1980’s

The former Soviet Union politically governed Mongolia between 1925 and 1991. Its governmental agencies performed the first systematic exploration on Mine A between 1985 and 1987. Only one vein was located, east-trending with a strike length of 600 to 700 meters. The major work performed included drilling and digging six trenches three to four meters deep along the vein.

Phase 2: Investigation conducted by an independent surveyor in 2012

Since the date of the report by the Soviet Union governmental agencies, 27 new holes were drilled (2,916 m) underneath the trenches excavated in the 1980s to investigate the resource in Mine A. Most holes were drilled vertically or at an angle of 60° to the north, as the vein dips approximately 45° to the south.

Phase 3: Investigation conducted by SRK Consulting

Considering the advice from the independent explorer on the possibility of re-drilling some core holes to increase output of Mine A and Mine B, Arcus formally engaged SRK Consulting to perform a formal survey on both mines.

In late 2014, a specialist from SRK Consulting visited both Mine A and Mine B. SRK Consulting collected 43 extra drill core samples in Mine A during its visit. The finding by SRK Consulting is at a better grade with an average CaF2 of 34%.

| 6 |

|

|

| Table of Contents |

Mine B

Phase 1: Investigation conducted by former Soviet Union government agencies in 1930s to 1950s

Former Soviet Union governmental agencies performed the first systemic exploration on Mine B in 1937 and continued until approximately 1950. The main vein located was north-striking. It was traced by trenching and defined to be at least 400 meters in length in the 1940’s.

Major work performed in Phase 1 included:

|

| 1. | Over 160 trenches dug along the vein surface, which are now mostly deteriorated; |

|

| 2. | Over 35 vertical drill holes; and |

|

| 3. | A 35-meter underground tunnel along the main vein zone. |

Phase 2: Investigation conducted by an independent surveyor in 2012

The Company has drilled 9 vertical core holes with an aggregate length of 877 meters in 2011 to update information on Mine B. Based on the samples obtained from the 9 vertical core holes drilled and assays of 4 drill hole cores in the Soviet Union period.

Phase 3: Investigation conducted by SRK Consulting

During the site visit to Mine B, the specialist consultant from SRK Consulting observed that most of the fluorite ores in Mine B have a grade of more than 90% CaF2 and could be used for ornamental and lapidary purposes.

Based on the samples taken by SRK Consulting, the average grade of CaF2 is 67%.

Mine C

No exploration or resource estimate has been done on Mine C, but initial surface investigations suggest that the resource of Mine B may extend onto the license of Mine C.

Future development

The Company is planning to continue with a second round of exploration in Mine A and Mine B and start a first round of exploration in Mine C. The primary objective would be to gain a better understanding of the geological structure to assist in mine planning and to upgrade the identified inferred resource to the indicated resource category.

According to SRK Consulting, the drill holes in Mine A do not provide consistent coverage of all areas. Therefore, another round of exploration would allow a more detailed understanding of the resource allocation and help upgrade much of the inferred resource into the indicated resource category. Full feasibility studies for Mine A and Mine B will be prepared once it’s the right time. These feasibility studies will be conducted by external specialist consultants together with Arcus’ experienced team.

Mine C is adjacent to Mine B, and given the large cover area of Mine C, we are optimistic regarding the resources of Mine C. Based on preliminary estimates by the geologists, it is possible that the resource of Mine C could be greater than that of Mine B. Conducting a thorough exploration of the resource will allow better planning on mining Mine C and ensure sustainability of the Company’s growth.

Operations

Both Mine A and Mine B were in the exploration stage in 2019. Revenue generated during the year were $101,222 by Mine A and $181,635 by Mine B. We expected to further extend the operation of Mine A and Mine B in the second quarter of 2020.

There are two types of products available from Mine B, metallurgical and acid grade fluorite. Metallurgical grade fluorite is sold mainly to steel manufacturers for use as flux in steel production. Acid grade fluorite which is used to manufacture hydrofluoric acid, a feedstock for many different chemical processes. At the moment, there is only metallurgical grade fluorite available from Mine A.

The Company ran trial productions at Mine A and Mine B in 2019. Below is the summary of revenue for 2019 from the trial productions.

| Type of Finished Products |

| Grade Mined |

| Quantities (In tons) |

|

| Mining Recovery |

|

| Average Price (USD) |

| |||

| Metallurgical Fluorite |

| Concentration 50% |

|

| 4,418 |

|

|

| 95 | % |

|

| 22.91 |

|

| Metallurgical Fluorite |

| Concentration 65% |

|

| 2,221 |

|

|

| 95 | % |

|

| 81.78 |

|

| 7 |

|

|

| Table of Contents |

Workflow of Operations

The operation at Mine A and Mine B of the Company involves several steps as shown below:

Mine Preparation

Preparing a mine involves investigation, exploration, evaluation and the construction of necessary infrastructures and utilities facilities, among other tasks.

Both Mine A and Mine B are now equipped with the necessary facilities, but the infrastructure in Mine B is more comprehensive. The basic facilities information of Mine A and Mine B is shown below:

|

| Mine A | Mine B |

| Water Resources | Drilled water wells | Drilled water wells |

| Electricity Resources | Local wind turbine generators | Bayan-Ovoo soum electrical power grid |

| Mining Method | Open pit mining | Underground mining |

| Shafts | Not applicable | 4 in production |

Water Resources

It is probable that there is sufficient water from drilled wells for mining and processing operations in Mine A and Mine B. Several such wells have been completed at both Mine A and Mine B. All the water will be recycled, but in the dry climate, evaporation is high.

Electricity Resources

Mine B is currently connected to the Bayan-Ovoo soum electrical power grid. Power generation in Mine A is currently supported by a set of wind turbines. Both Mine A and Mine B have sufficient power to meet daily usage, and each has two sets of contingent diesel generators.

Infrastructures

At Mine B, the construction of offices, living quarters and explosive stores has been completed. Of the four shafts built in Mine B, one shaft and the other shaft has been excavated with a 150 meter long and 180 meter long development drive in the fluorite ore respectively. There was no vertical development in 2019. Construction on excavating an underground tunnel to connect the four shafts is completed in 2019.

Mining activities are halted for the winter break, which takes place between January and March every year. Since mining activities are conducted underground, which is more dependent on the weather condition, the winter break for the mining activities is one month longer than the winter break for the production line. We have adopted open-pit mining at Mine A which is different from Mine B. Although mining activities are subject to weather, open-pit mining is more flexible so we decided to suspend the mining activities at Mine A in mid-February instead of late November 2019 as we did with Mine B. Production of both Mine A and Mine B is to be continued after the winter break and is expected to commence in the second quarter of 2020.

Mine A is planned as an open pit mine because the mineralization outcrops on the surface are relatively easy to begin mining. Four temporary offices and storage containers have been set up at Mine A. Since the resource in Mine A is large, management plans to develop Mine A in stages. Mining of the open pit has been commenced in 2019, while the deeper ores will be subjected to further exploration.

Mine A is originally planned to produce fluorite powder. However, in order to cope with our business development, the management decided to put the construction of refinery at Mine A on hold for now. Once it is the suitable time for further expanding our business, the management may resume the plan of the construction of refinery at Mine A.

| 8 |

|

|

| Table of Contents |

Mining

A strategic open pit exploration at Mine A has been started in 2019. The refinery operations described below apply only to Mine B but can serve as a general reference regarding the future production of Mine A. Starting from year 2019, we have outsourced the mining activities to subcontractors.

Refining

The Company will not outsource its core fluorite processing to third parties but rather work together with the strategic partners. Major fluorite processing of metallurgical grade fluorite includes gravity separation, which refines the fluorite granules, followed by sorting the granules by sizes in accordance with a customer’s needs.

The major machines employed in Mine B are the shakers and the jiggers. A jigger is a vertical container where a pulsing action divides ores into different layers according to their densities. When sorted by a shaker, ore is placed on a horizontal water surface, and the shaker applies longitudinal forces. As ores of different densities respond to longitudinal forces, they are sorted accordingly. Both shakers and jiggers are common tools in conducting gravity selection, but jiggers mainly divide coarse ores into different size groups (30 mm - 80 mm) and shakers mainly refine smaller ores (3 mm – 10 mm or 1 mm – 3 mm).

Sales and Marketing

From 2015 throughout 2019, the mines have still been in exploration stage so the Company decided to sell metallurgical grade fluorite within the territory of Mongolia to avoid incurring cross-border freight and transportation. The Company would like to further expand its production in the second quarter of 2020. Some of the ultimate target customers include foreign steel manufacturers.

Customers

The Company intends to develop a pool of customers to reduce its distribution risk. The Company’s targeted customer base is set forth below:

|

| · | Korean steel manufacturers; |

|

|

|

|

|

| · | Chinese steel manufacturers; |

|

|

|

|

|

| · | Other foreign steel manufacturers (e.g., Japanese, Indian, American, etc.); |

|

|

|

|

|

| · | Online sales platforms; |

|

|

|

|

|

| · | Fluorochemical companies, mainly in China due to large demand; |

|

|

|

|

|

| · | Chinese and other foreign aluminum manufacturers. |

The Market for Fluorite in Mongolia

Fluorite and its Applications

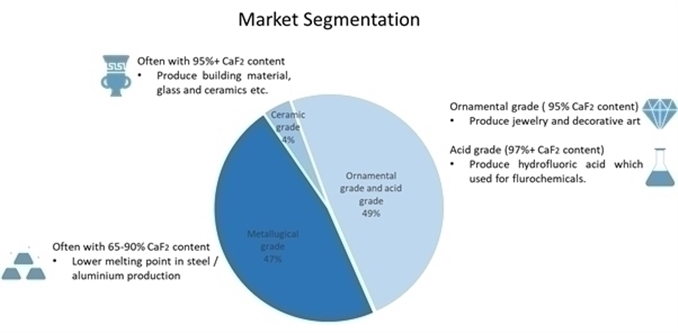

Fluorite, commercially termed as fluorspar, is a transparent halide mineral of various colors, composed primarily of calcium fluoride (CaF2). Fluorite is the dominant source for the chemical element fluorine. Due to its unique chemical properties, fluorine is largely irreplaceable in its use. The major applications of fluorite and the corresponding requirement of content percentage are summarized below:

Most of the world demand for fluorite is for acid-grade fluorite, which is used to manufacture hydrofluoric acid, a feedstock for many different chemical processes. The second greatest demand is for metallurgical grade fluorite, used as flux in steel and aluminum production. A small portion is produced as ceramic grade fluorite for the manufacture of ceramics and enamels due to the high content percentage requirement.

| 9 |

|

|

| Table of Contents |

Competition

There are a number of listed companies that are primarily focused on mining fluorite. We have presented them in the table set forth below.

| Comparable company | Mexichem | China King Resources | Do-Fluoride |

| Country | Mexico | China | China |

| Exchange Listed | Mexico | Shanghai | Shenzhen |

| Location of fluorite deposit | Mexico | China | China |

Patents, Trademarks, Licenses, Franchises, Concessions and Royalty Agreements

Licenses

The three projects owned by the Company all hold official mining licenses from the Mineral Resources and Petroleum Authority of Mongolia. The mining licenses allow the holder the right to conduct mining activities throughout the license areas and to construct structures within the license areas that are related to its mining activities.

Mine A is located in Uulbayan soum, Sukhbaatar province, 530 kilometers from Ulaanbaatar, the capital of Mongolia. Mine A’s mining license, reference number MV-009918, is valid until December 29, 2034. Mine A covers an area of 39.35 hectares (97.24 acres).

Mine B is located in the Bayan-Ovoo soum, Khentii province, 440 kilometers from Ulaanbaatar. Mine B’s license, reference number MV-016819, is valid until April 28, 2041. Mine B covers an area of 98.37 hectares (243.08 acres).

Mine C is adjacent to Mine B. Mine C’s license, reference number MV-017305, is valid until April 23, 2043. Mine C covers an area of 300.96 hectares (743.69 acres).

Government Approval and Regulation of the Company’s Principal Products or Services

The Mineral Law of Mongolia governs our operations. The Company endeavors to ensure the safe and lawful operation of its facilities in its operations and the distribution of its products and believes it is in compliance in all material respects with applicable laws and regulations.

Employees

The Company currently has approximately 100 employees.

Principal Executive Offices

Our principal executive office is located at Suite 1023, 10/F., Ocean Centre, 5 Canton Rd., Tsim Sha Tsui, Kowloon, Hong Kong.

Risks Related to our Business

Our limited operating history makes it difficult to evaluate our future prospects and results of operations.

The Company is in the process of developing its mines and bringing its fluorite products to the market. Accordingly, we have a limited operating history. You should consider our future prospects in light of the risks and uncertainties experienced by early stage companies in evolving geographical areas such as Mongolia. Some of these risks and uncertainties relate to our ability to:

|

| · | offer products of sufficient quality to attract and retain a larger customer base; |

|

|

|

|

|

| · | attract additional customers and increase spending per customer; |

|

|

|

|

|

| · | increase awareness of our products and continue to develop customer loyalty; |

|

|

|

|

|

| · | respond to competitive market conditions; |

|

|

|

|

|

| · | respond to changes in our regulatory environment; |

|

|

|

|

|

| · | maintain effective control of our costs and expenses; |

|

|

|

|

|

| · | raise sufficient capital to sustain and expand our business; and |

|

|

|

|

|

| · | attract, retain and motivate qualified personnel. |

If we are unsuccessful in addressing any of these risks and uncertainties, our business may be materially and adversely affected.

| 10 |

|

|

| Table of Contents |

Our operating results may fluctuate, which makes our results difficult to predict and could cause our results to fall short of expectations.

Our operating results may fluctuate as a result of a number of factors, many outside of our control. As a result, comparing our operating results on a period-to-period basis may not be meaningful, and you should not rely on our past results as an indication of our future performance. Our quarterly, year-to-date and annual expenses as a percentage of our revenues may differ significantly from our historical or projected rates. Our operating results in future quarters may fall below expectations. Any of these events could cause our stock price to fall. Each of the risk factors listed in this section and the following factors may affect our operating results:

|

| · | Our ability to continue to attract customers; |

|

|

|

|

|

| · | Our ability to generate revenue from the products we offer; |

|

|

|

|

|

| · | The amount and timing of operating costs and capital expenditures related to the maintenance and expansion of our businesses; and |

|

|

|

|

|

| · | Our focus on long-term goals over short-term results. |

Because our business is changing and evolving, our historical operating results may not be useful to you in predicting our future operating results.

Our business operations may be adversely affected by present or future governmental regulations or political changes.

Mongolia, the country where the Company’s mines are situated, is currently undergoing rapid development. Our operations may be affected by changes to Mongolian regulation of the mining sector or changing levels of political involvement in mining.

The Mongolian Parliament passed an amendment to the Minerals Law on July 1, 2014 to ease certain restrictions on the mining industry and also to give some incentives to foreign mining companies and investors. These changes have clarified many areas of the law and settled issues around government interests in mines of national or strategic importance. These changes have brought potential benefits to the Company. Visits paid by Chinese president Xi Jinping to Mongolia have indicated Chinese support for strengthening cooperation between Mongolian and Chinese entities in the future. Corresponding lobbying by the Chinese government may help ensure that the Mongolian government respects the rights of foreign mining companies investing in Mongolia.

Our business operations may be adversely affected by the recent COVID-19

Due to the current outbreak of novel coronavirus that was first reported from Wuhan, China, on December 31, 2019 and since then, the government of Mongolia officially announced on January 31, 2020 that it will close all ports of entry from and into China with immediate effect until March 2, 2020. However, The Embassy of the PRC in Mongolia further announced on February 19, 2020 that all ports of entry from and into China will be closed until March 30, 2020. We expect that such temporary closures might result in a delay in the resumption of our exploratory work and production in the newly set up refinery at Mine A and Mine B respectively. However, we have started the preparation work for arranging working visas for the Chinese workers in advance and will hire more Mongolian workers in case all ports of entry from and into China are not open before we resume our work at both Mine A and Mine B so as to minimize the effect of the delay.

Taking the recent worldwide outbreak and development of the COVID-19 into account, the management worried the development of 2020 but we have been strictly prudent towards the epidemic. We will keep tracking the measures of different governments, especially the Chinese and Mongolian Government, are going to implement so to determine what the Company will do in order to minimize the negative effect of the COVID-19 on our business. The management will strengthen all necessary measures and make special arrangement so to protect our workers from the COVID-19 after the winter break as well as sticking to our expected performance in 2020.

Deviations between inferred resources and actual mineable resources may have an adverse effect on the Company’s results.

Actual mine output usually deviates to a certain extent when compared to the inferred resource, as every estimation model is based on certain assumptions made in the calculation. In order to enhance estimation accuracy and maximize output quantity and quality, the Company engaged SRK Consulting, a leading mining consultant company, to conduct a detailed resource and reserve assessment. However, there can be no assurance as to the accuracy of SRK Consulting’s estimate.

Adverse weather conditions may limit the periods during which the Company may conduct its operations or may cause a disruption in its utilities or the delivery of its products to its customers.

Due to the severe weather in Mongolia during the winter, we have scheduled a regular winter break between January and March for mining activities and processing every year. However, it is possible that severe weather conditions may occur outside their normal range in some years, which would hinder the Company’s mining and production operations and require the extension of the scheduled winter break. Severe weather may also cause a disruption in the Company’s essential utilities. Although the production lines will be roofed to minimize the impact of severe weather and the Company will maintain a backstock of ore to reduce the chances of production suspension from interruptions in mining, there can be no assurance that these measures will be adequate to compensate for the effects of especially severe weather. As a further precaution, we will also maintain a sufficient inventory level in our Baganuur warehouse to secure a continuous supply to customers during the winter, but there can be no assurance that our rail and trucking transportation methods will not be disrupted by weather events.

We may suffer losses resulting from industry-related accidents.

Despite the safety precautions taken by the Company in its mining operations, there can be no assurance that we will not suffer losses resulting from industry-related accidents. To minimize the occurrence of industrial incidents, we regularly monitor mine site construction in order to identify and implement practical protective measures.

| 11 |

|

|

| Table of Contents |

We may not be successful in implementing important strategic initiatives, which may have a material adverse impact on our business and financial results.

There is no assurance that we will be able to implement important strategic initiatives in accordance with our expectations, which may result in a material adverse impact on our business and financial results. These strategic initiatives are designed to drive long-term stockholder value and improve our results of operations.

We face significant competition, and if we do not compete successfully against new and existing competitors, we may lose our market share, and our profitability may be adversely affected.

Increased competition could reduce our profitability and result in a loss of market share. Some of our existing and potential competitors may have competitive advantages, such as significantly greater financial, marketing or other resources, and may successfully mimic and adopt our business models. We cannot assure you that we will be able to successfully compete against new or existing competitors.

Failure to manage our growth could strain our management, operational and other resources, which could materially and adversely affect our business and prospects.

We intend to expand our operations and plan to expand as rapidly as possible. The continued growth of our business will result in, substantial demand on our management, operational and other resources. In particular, the management of our growth will require, among other things:

|

| · | increased sales and sales support activities; |

|

|

|

|

|

| · | improved administrative and operational systems; |

|

|

|

|

|

| · | enhancements to our information technology system; |

|

|

|

|

|

| · | stringent cost controls and sufficient working capital; |

|

|

|

|

|

| · | strengthening of financial and management controls; and |

|

|

|

|

|

| · | hiring and training of new personnel. |

As we continue this effort, we may incur substantial costs and expend substantial resources. We may not be able to manage our current or future operations effectively and efficiently or compete effectively in new markets we enter. If we are not able to manage our growth successfully, our business and prospects would be materially and adversely affected.

Attracting skilled personnel are essential to growing our business.

We face competition for attracting skilled personnel. If we fail to attract and retain qualified personnel to meet current and future needs, this could slow our ability to grow our business, which could result in a decrease in market share.

We may need additional capital and we may not be able to obtain it at acceptable terms, or at all, which could adversely affect our liquidity and financial position.

We may need additional cash resources due to changed business conditions or other future developments. If these sources are insufficient to satisfy our cash requirements, we may seek to sell additional equity or debt securities or obtain a credit facility. The incurrence of indebtedness would result in increased debt service obligations and could result in operating and financing covenants that would restrict our operations and liquidity.

Our ability to obtain additional capital on acceptable terms is subject to a variety of uncertainties, including:

|

| · | investors’ perception of, and demand for, our securities; |

|

| · | conditions of the U.S. and other capital markets in which we may seek to raise funds; |

|

| · | our future results of operations, financial condition and cash flow; |

|

| · | Mongolian governmental regulation; and |

|

| · | economic, political and other conditions in Mongolia. |

We do not have a majority of independent directors serving on our board of directors, which could present the potential for conflicts of interest.

We do not have a majority of independent directors serving on our board of directors. In the absence of a majority of independent directors, our executive officers could establish policies and enter into transactions without independent review and approval thereof. This could present the potential for a conflict of interest between us and our stockholders, generally, and the controlling officers, stockholders or directors. However, we are going to invite different professionals as our independent directors gradually. An independent director was added in April 2019.

| 12 |

|

|

| Table of Contents |

We have limited insurance coverage.

The insurance industry in China is still at an early stage of development. Insurance companies in China offer limited insurance products. We have determined that the risks of disruption or liability from our business, the loss or damage to our property, including our facilities, equipment and office furniture, the cost of insuring for these risks, and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. As a result, we do not have any business liability, disruption, litigation or property insurance coverage for our operations in China except for insurance on some company owned vehicles. Any uninsured occurrence of loss or damage to property, or litigation or business disruption may result in the incurrence of substantial costs and the diversion of resources, which could have an adverse effect on our operating results.

Similarly, although it has been 80 years since the introduction of insurance in Mongolia, the penetration of insurance is still low and its development is still immature which the insurance industry is still yet to be up to international standard. As a result, we do not have any business liability, disruption, litigation or property insurance coverage for our operations in Mongolia except for insurance on some company owned vehicles. Any uninsured occurrence of loss or damage to property, or litigation or business disruption may result in the incurrence of substantial costs and the diversion of resources, which could have an adverse effect on our operating results.

If we are unable to establish appropriate internal financial reporting controls and procedures, it could cause us to fail to meet our reporting obligations, result in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence in our reported financial information and have a negative effect on the market price for shares of our common stock.

Effective internal controls are necessary for us to provide reliable financial reports and effectively prevent fraud. We maintain a system of internal control over financial reporting, which is defined as a process designed by, or under the supervision of, our principal executive officer and principal financial officer, or persons performing similar functions, and effected by our board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

As a public company, we have significant additional requirements for enhanced financial reporting and internal controls. We are required to document and test our internal control procedures in order to satisfy the requirements of SOX 404, which requires annual management assessments of the effectiveness of our internal controls over financial reporting and a report by our independent registered public accounting firm addressing these assessments. The process of designing and implementing effective internal controls is a continuous effort that requires us to anticipate and react to changes in our business and the economic and regulatory environments and to expend significant resources to maintain a system of internal controls that is adequate to satisfy our reporting obligations as a public company.

We cannot assure you that we will not, in the future, identify areas requiring improvement in our internal control over financial reporting. We cannot assure you that the measures we will take to remediate any areas in need of improvement will be successful or that we will implement and maintain adequate controls over our financial processes and reporting in the future as we continue our growth. If we are unable to establish appropriate internal financial reporting controls and procedures, it could cause us to fail to meet our reporting obligations, result in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence in our reported financial information and have a negative effect on the market price for shares of our common stock.

Lack of experienced officers of publicly-traded companies may hinder our ability to comply with Sarbanes-Oxley Act.

It may be time consuming, difficult and costly for us to develop and implement the internal controls and reporting procedures required by the Sarbanes-Oxley Act. We may need to hire additional financial reporting, internal controls and other finance staff or consultants in order to develop and implement appropriate internal controls and reporting procedures. If we are unable to comply with the Sarbanes-Oxley Act’s internal controls requirements, we may not be able to obtain the independent auditor certifications that Sarbanes-Oxley Act requires publicly-traded companies to obtain.

We incur increased costs as a result of being a public company.

As a public company, we incur significant legal, accounting and other expenses that we did not incur as a private company. In addition, the Sarbanes-Oxley Act, as well as new rules subsequently implemented by the SEC, has required changes in corporate governance practices of public companies. We expect these new rules and regulations to increase our legal, accounting and financial compliance costs and to make certain corporate activities more time-consuming and costly. In addition, we incur additional costs associated with our public company reporting requirements. We are currently evaluating and monitoring developments with respect to these new rules, and we cannot predict or estimate that there is a high probability of additional costs we may incur or the timing of such costs.

| 13 |

|

|

| Table of Contents |

Risks Relating to Our Securities

There may not be sufficient liquidity in the market for our securities in order for investors to sell their securities.

There is currently only a limited public market for our common stock, which is listed on the Over-the-Counter (“OTC”) Pink Sheets, and there can be no assurance that a trading market will develop further or be maintained in the future.

The market price of our common stock may be volatile.

The market price of our common stock has been and will likely continue to be highly volatile, as is the stock market in general, and the market for OTC Pink Sheet quoted stocks in particular. Some of the factors that may materially affect the market price of our common stock are beyond our control, such as changes in financial estimates by industry and securities analysts, conditions or trends in the industry in which we operate or sales of our common stock. These factors may materially adversely affect the market price of our common stock, regardless of our performance. In addition, the public stock markets have experienced extreme price and trading volume volatility. This volatility has significantly affected the market prices of securities of many companies for reasons frequently unrelated to the operating performance of the specific companies. These broad market fluctuations may adversely affect the market price of our common stock.

Our common stock may be considered a “penny stock” and may be difficult to sell.

The SEC has adopted regulations which generally define a “penny stock” to be an equity security that has a market price of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to specific exemptions. The market price of our common stock is less than $5.00 per share and, therefore, it may be designated as a “penny stock” according to SEC rules. This designation requires any broker or dealer selling these securities to disclose certain information concerning the transaction, obtain a written agreement from the purchaser and determine that the purchaser is reasonably suitable to purchase the securities. These rules may restrict the ability of brokers or dealers to sell our common stock and may affect the ability of investors to sell their shares.

The market for penny stocks has experienced numerous frauds and abuses, which could adversely impact investors in our stock.

OTC Pink Sheet securities are frequent targets of fraud or market manipulation, both because of their generally low prices and because OTC Pink Sheet reporting requirements are less stringent than those of the stock exchanges or NASDAQ.

Patterns of fraud and abuse include:

|

| · | Control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer; |

|

| · | Manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; |

|

| · | “Boiler room” practices involving high pressure sales tactics and unrealistic price projections by inexperienced sales persons; |

|

| · | Excessive and undisclosed bid-ask differentials and markups by selling broker-dealers; and |

|

| · | Wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the inevitable collapse of those prices with consequent investor losses. |

Our management is aware of the abuses that have occurred historically in the penny stock market.

We have not paid dividends in the past and do not expect to pay dividends in the foreseeable future and any return on investment may be limited to the value of our stock.

We have never paid any cash dividends on our common stock and do not anticipate paying any cash dividends on our common stock in the foreseeable future and any return on investment may be limited to the value of our stock. We plan to retain any future earnings to finance growth.

Item 1B. Unresolved Staff Comments

None.

The Company’s corporate headquarters is located at Suite 1023, 10/F., Ocean Centre, 5 Canton Rd., Tsim Sha Tsui, Kowloon, Hong Kong. We believe that our existing mining and processing facilities in Mongolia, which are described above, are well maintained and in good operating condition, and will be sufficient for our production goals for the next year.

There are no pending legal proceedings to which the Company is a party or in which any director, officer or affiliate of the Company, any owner of record or beneficially of more than 5% of any class of voting securities of the Company, or security holder is a party adverse to the Company or has a material interest adverse to the Company. The Company’s property is not the subject of any pending legal proceedings.

Item 4. Mine and Safety Disclosure

Not applicable.

| 14 |

|

|

| Table of Contents |

Market Information

Our common stock is currently traded on the OTC Pink Sheets under the trading symbol “TGSI”. There is a limited trading market in our securities.

Our transfer agent is VStock Transfer, LLC, 18 Lafayette Place, Woodmere, NY, 11598, telephone: (212) 828-8436, fax: (646) 536-3179.

Holders

As of March 20, 2020, there were 35 holders of record of our common stock and 14,858,328 shares of our common stock were issued and outstanding.

Dividends

We have not declared or paid any cash dividends since inception. We intend to retain future earnings, if any, for use in the operation and expansion of our business and do not intend to pay any cash dividends in the foreseeable future. There are no restrictions in our articles of incorporation or bylaws that prevent us from declaring dividends.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

In 2019, the Company issued a subscription package (the “Second Subscription Package”) of up to $825,000, consisting of 330,000 common shares and 66,000 warrants exercisable at $3.00 to purchase common shares within three years from the respective issuance dates, to accredited investors. The Company also issued the placement agent 33,000 common shares at a price of $3.70 per common share for services rendered.

In 2019, there were four convertible bond agreements entered into between the Company, Arcus and third party investors. Three of the bonds matured in 2019 and were settled by issuing 141,782 common shares at a price stated in the respective agreements, representing loans of HK$4 million and interest expenses of HK$8,333, for a total of HK$4,008,333 (equivalent to US$513,888). In November 2019, one convertible bond agreement was signed including a HK$1.5 million (equivalent to US$192,308) loan bearing interest of 5% per annum for six months. The convertible bond will mature on May 25, 2020 with a conversion price of $3.60 per share.

The shares issued in connection with the transactions were issued pursuant to an exemption from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”), pursuant Section 4(a)(2) of the Securities Act and Regulation S promulgated thereunder.

Equity Compensation Plans

We do not have in effect any compensation plans under which our equity securities are authorized for issuance and we do not have any outstanding stock options.

Purchases of Equity Securities by the Company

We did not purchase any of our shares of common stock or other securities during the fiscal year ended December 31, 2019.

Item 6. Selected Financial Data

As a “smaller reporting company”, we are not required to provide the information required by this Item.

| 15 |

|

|

| Table of Contents |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

FORWARD LOOKING STATEMENTS

This annual report contains forward-looking statements. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our audited financial statements are stated in United States Dollars ($) and are prepared in accordance with United States Generally Accepted Accounting Principles. The following discussion should be read in conjunction with our financial statements and the related notes to the consolidated financial statements included elsewhere in this Form 10-K. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed below and elsewhere in this annual report.

In this annual report, unless otherwise specified, all dollar amounts are expressed in United States dollars and all references to “common stock” refer to the common stock in our capital stock.

As used in this annual report, the terms “we”, “us”, “our” or the “Company” mean TGS International Ltd., a Nevada corporation, and our subsidiaries, unless otherwise indicated.

General Overview

TGS International Ltd. was established on December 1, 2016 in Nevada, USA. On September 14, 2018, TGS International Ltd. and Arcus entered into a Share Exchange Agreement, dated September 14, 2018, with Chi Kin Loo, Billion Plus Limited, First Fortune Investment Limited, Great Win Limited and Master Value Holdings Limited, pursuant to which the Selling Stockholders agreed to sell all of their ordinary shares of Arcus to the Company in exchange for an aggregate of 7,000,000 shares of common stock of TGS International Ltd.

We are a mining company focused on both fluorite mining operations in Mongolia (3 mines in total, Mining license numbers: MV-016819, MV-017305 and MV-009918) and sales of fluorite across Mongolia and China. During 2015 to 2017, we were setting up infrastructure at Mine B and appointed SRK Consulting China Limited for resource exploration for Mine A and Mine B. The only production at Mine B started in 2018 and has been ongoing since that time.

In 2019, there were a few unpredictable events, including delay in exploratory work at Mine B due to the tightened working visa application procedure by the Mongolian Government, delay in explosives delivery due to the temporary suspension of the only two explosive factories in Mongolia, which have brought about significant postponement of our exploratory work. Therefore, the production forecast for 2019 was not reached. Nonetheless, the management has devoted all their effort to minimize any impact on the Company. For instance, workers were instructed to work on the foundation of the refinery and other on-site infrastructures until the explosives arrived at our mine.

We have suspended the work at Mine B since November 25, 2019 due to the annual winter break and expect to resume our work in early April 2020, depending on the weather and overall situation. All workers working at Mine B were sent home the same day. Right before the winter break, there were 2,221 tons of output from Mine B in the last quarter of 2019.

Although open pit mining is adopted at Mine A, as the weather has become more frigid, we have put the exploratory work at Mine A on hold since mid-February 2020 to make sure the workers are safe and sound. The output in the last quarter of 2019 is 4,418 tons. We would like to take advantage of adopting open pit mining at Mine A so as to resume the exploratory work earlier once the winter break comes to an end and boost the production, presumably in early April 2020.

The construction of the refinery at Mine B was completed in late November 2019. However, the power supply upgrade at Mine B is still in progress and we hope to get it done in early April 2020 to put the refinery into use as early as possible. This is a strategic cooperation with Yantai Fulin Mining Machinery Co., Ltd (“Fulin”) which provided construction funds in advance to the construction and installation of the refinery. We expect that the production and the sales would have a certain increase in 2020 as well as the profits. During 2019, we have upgraded the infrastructures at Mine B as well as building the refinery at Mine B. The cost, therefore, was unavoidably much larger than the last year’s. With the experienced engineers and construction teams provided by Fulin, our strategic partner, we could get the construction of the refinery completed in merely six months. The refinery is basically ready. Once we get the power supply upgrade done in April 2020, the entire refinery could be put into trial in late April or early May 2020.

As what we have known that the operation of the refinery and the production line is straightforward and simple with approximately 3 steps – breaking apart and grinding, flotation separation, and drying out the acid grade fluorite, the end product. We expect to increase manpower to accelerate the exploration at Mine B by the end of the second quarter of 2020 to escalate production. The fluorite with higher grading could be sold to the market directly while the fluorite with lower grading could be used as the raw materials for producing acid grade fluorite. The management are confident in the overall development and sales of the Company.

Mine C is still intact and we have not had any development there because we would like to prioritize and focus the use of our resources for the development of Mine A and Mine B. Once we have sufficient resources, we would start exploring and developing Mine C, for example, getting SRK Consulting China Limited for resource exploration as the first step, to maximize the value of the Company.

| 16 |

|

|

| Table of Contents |

There were a total of four convertible bond agreements entered into between the Company, a subsidiary of the Company, Arcus Mining Holdings Limited (“Arcus”), and third party investors during 2019. On August 30 2019, a convertible bond agreement was entered into between the Company, Arcus and a third party investor including a HK$1 million (equivalent to US$128,205) loan bearing interest of 2.5% per annum for one month. The convertible bond matured and was converted into 34,722 shares of the Company’s common stock on September 29, 2019 with a conversion price of $3.70 per share.

On October 25, 2019, a convertible bond agreement was entered into between the Company, Arcus and a third party investor including a HK$2 million (equivalent to US$256,410) loan bearing interest of 2.5% per annum for one month. The convertible bond matured and was converted into 71,373 shares of the Company’s common stock on November 27, 2019 with a conversion price of $3.60 per share.

On November 4, 2019, a convertible bond agreement was entered into between the Company, Arcus and a third party investor including a HK$1 million (equivalent to US$128,205) loan bearing interest of 2.5% per annum for one month. The convertible bond matured and was converted into 35,687 shares of the Company’s common stock on December 3, 2019 with a conversion price of $3.60 per share.

On November 26, 2019, a convertible bond agreement was entered into between the Company, Arcus and a third party investor including a HK$1.5 million (equivalent to US$192,308) loan, bearing interest of 5% per annum for six months. The convertible bond will mature on May 25, 2020 with a conversion price of $3.60 per share.

As of December 31, 2019, a loan of $132,423 was borrowed from an unrelated party. The loan is unsecured, has no collateral or guarantee and carries interest at 11.61% per annum and repayable on December 31, 2029.

Subsequent to the year ended December 31, 2019, there were four convertible bond agreements entered into between the Company, Arcus and third party investors. On January 2, 2020 a convertible bond agreement was signed including a HK$1.5 million (equivalent to US$192,308) loan bearing interest of 2.5% per annum for one month. The convertible bond matured and was converted into 53,236 shares of the Company’s common stock on February 1, 2020 with a conversion price of $3.62 per share.

On January 14, 2020, a convertible bond agreement was signed including a HK$400,000 (equivalent to US$51,282) loan bearing interest of 2.5% per annum for one month. The convertible bond matured and was converted into 14,196 shares of the Company’s common stock on February 13, 2020 with a conversion price of $3.62 per share.

On February 24, 2020, a convertible bond agreement was signed including a HK$200,000 (equivalent to US$25,641) loan bearing interest of 2.5% per annum for one month. The convertible bond will mature on March 25, 2020 with a conversion price of $3.62 per share.

On February 29, 2020, a convertible bond agreement was signed including a HK$500,000 (equivalent to US$64,103) loan bearing interest of 2.5% per annum for one month. The convertible bond will mature on March 30, 2020 with a conversion price of $3.62 per share.

Apart from the exploration and infrastructure work at Mine A and Mine B, the Company might consider further fund raising activities through the capital markets and from stockholders with the aim of speeding up the development of the Company.

Results of Operations

Comparison of Years Ended December 31, 2019 and December 31, 2018

Revenue

Revenue consisted mainly of fluorspar products generated from production at our mines. In 2019, we had total revenue of $282,857, as compared to revenue of $274,238 during 2018. The percentage of such increase was approximately 3% as a result of the increase in average price of metallurgical fluorite.

Commission income

Commission income was recognized when the Company purchased minerals from suppliers and received payments from the customers on selling minerals. The Company has been determined as an agent for the ultimate customers in these transactions and the revenue is recorded net of the related fulfillment costs as commission income. The Company had commission income of $393,566 in 2018 and nil commission income in 2019.

Cost of goods sold

Cost of goods sold included raw material costs. The total cost of goods sold decreased from $10,544 in 2018 to nil in 2019. The significant decrease was mainly due to no raw material costs in 2019.

Exploration cost

Exploration costs are expensed as incurred and included labor and benefits, construction service fee, mining overhead, including food, supplies, utilities and lubricants related to mine exploration. Exploration costs increased significantly from $421,508 in 2018 to $737,248 in 2019. The percentage of such increment was approximately 75% and was mainly due to our focus on the mining infrastructure project resulted in the increase of construction service fee, mining supplies and utilities during the year.

Selling and distribution cost

Selling and distribution costs included transportation and handling costs related to the movement of finished goods from mines to customer designated locations, security fee, royalty and custom tax. Selling and distribution costs increased significantly from $56,697 in 2018 to $105,279 in 2019. The percentage of such increment was approximately 86% and was mainly due to the increase in royalty and custom tax.

| 17 |

|

|

| Table of Contents |

Administrative expenses

Administrative expenses included salaries and benefits, consulting, audit, tax, legal, insurance, rent and utilities, and other general operating expenses.

Administrative expenses increased significantly from $1,342,830 in 2018 to $1,645,900 in 2019. The percentage of such increment was approximately 23% and is mainly due to the commission expenses related to subscription package, increase in staff salaries and increase of rental expense by additional staff accommodation in 2019.

Other income

Other income increased significantly from $34,083 in 2018 to $195,576 in 2019. The percentage of such increment was approximately 474% as a result of a waiver of consultancy fee in 2019 and a write back of receipt in advance due to the dissolution of our customer.

Interest expenses

Interest expenses mainly included other loan interest, related party loan interest and bond interest arising from convertible bonds.

Interest expenses decreased from $83,548 in 2018 to $76,824 in 2019. The percentage of such reduction was approximately 8% as a result of the repayment of related party loans of HK$3 million (equivalent to US$382,945), in which HK$2 million (equivalent to US$255,297) was settled by issuance of shares and HK$1 million (equivalent to US$127,648) was settled by cash.

Net loss

As a result of the factors described above, we had a net loss of $2,115,716 for the year ended December 31, 2019 as compared to a net loss of $1,241,452 for the year ended December 31, 2018. The net loss resulted mainly from the decrease in the commission income and increase in cost on mining infrastructure project. This was within our management expectation since our mine is still under trial production and we expect to further increase the productions in 2020.

Liquidity and Capital Resources

Cash and cash equivalents are short-term, highly liquid investments with original maturities of three months or less. As of December 31, 2019 and 2018, the Company’s cash was $106,850 and $98,121, respectively. There were no cash equivalents.

Factors affecting our liquidity include (i) net cash used in operating activities that consists of (a) cash required to fund the mining sites operating activities and continued expansion of our mining sites and (b) our working capital needs, which include advanced payments for several mining supplies and repair and maintenance, payment of our operating expenses; and (ii) net cash used in investing activities that consists of the investments in purchasing new and additional property, plant and equipment for mining sites. To date, we have financed our liquidity needs primarily through advances from stockholders, proceeds from related parties and unrelated party loans, proceeds from issuance of common stock and the proceeds from issuance of convertible bonds.

We expect to continue to make capital expenditures to keep pace with the expansion of the production and scale of operations of our mining sites, which we expect to fund in part with the proceeds from issuance of convertible bonds and other loans in the future. We expect that the proceeds from the above and our existing cash and cash equivalents will be used to fund working capital and for capital expenditures and other general corporate purposes, such as partnering arrangements, or reduction of debt obligations. However, there can be no assurance that we will be able obtain financing, if at all or upon terms that will be acceptable to us.

Cash Flows

As of December 31, 2019, we had $106,850 in cash and cash equivalents, compared to $98,121 on December 31, 2018.

Net cash used in operating activities

Our net cash used in operating activities increased to $1,228,886 in 2019 from $888,079 in 2018. Net cash used in operating activities for the year ended December 31, 2019 primarily reflected our net loss of $2,115,716 and the add-back of non-cash items, mainly consisting of depreciation of property, plant and equipment of $51,898, stock compensation expenses of $122,100, amortization of non-cash interest expenses and bond discount related to convertible bonds of $13,732, exchange difference of $246,346, and deduct of non-cash items, mainly consisting of write back of receipt in advance of $160,542 and waiver of consultancy fee of $34,556, and changes in operating assets and liabilities primarily consisting of an increase in accounts receivable of $60,314, an increase of other receivables of $394,560, an increase of deposits and prepayments of $56,795, decrease in accrued charges of $40,022 and offset by an increase of trade and other payables of $1,196,364 and increase in provision for asset retirement obligations of $3,179.

Net cash used in investing activities

Our net cash used in investing activities increased to $976,818 in 2019 from $38,379 in 2018. This was mainly due to acquisition of property, plant and equipment at mine sites.

Net cash provided by financing activities

Our net cash provided by financing activities increased to $2,216,864 in 2019 from $989,312 in 2018. This was mainly the result of advances from stockholders and directors, proceed from unrelated party loan, issuance of common stock and convertible bonds in 2019.

| 18 |

|

|

| Table of Contents |

Future Financings

We anticipate continuing to rely on related party and unrelated party loans, convertible bonds or equity sales of our common stock in order to continue to fund our business operations. We believe this will enable us to meet our cash needs for the next 12 months. Issuances of additional shares will result in dilution to our existing stockholders. Importantly, there is no assurance that we will achieve any additional sales of our equity securities or arrange for debt or other financing (whether from related parties or otherwise) to fund our planned business activities.

Except for the convertible bonds and loans from others, we presently do not have any other arrangements or commitments for additional financing for the expansion of our operations, and no potential lines of credit or sources of financing are currently available for the purpose of proceeding with our plan of operations.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, and capital expenditures or capital resources that are material to stockholders.

Critical Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States (“GAAP”) requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported period. The critical accounting policies we employ in the preparation of our consolidated financial statements are those which involve impairment of long-lived assets, intangible assets and income taxes.

Going Concern

The Company incurred an operating loss of $2,115,716 for the year ended December 31, 2019, and as of that date, the Company’s current liabilities exceeded its current assets by $1,555,450. Notwithstanding the operating loss incurred for the year ended December 31, 2019 and the net current liabilities as of December 31, 2019, the accompanying consolidated financial statements have been prepared on a going concern basis. Since the Company is currently in the exploration stage, it is still in the capital investing period. The Company’s business forecast indicates that the Company will have positive cash inflow after the commencement of formal production in 2021. Management believes the Company will have sufficient working capital to meet its financing requirements for the next 12 months based on the financial support of certain stockholders, issuance of new convertible bonds, proceeds from unrelated party loans and upon their experience and their assessment of the Company’s projected performance, production ability and product market.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Not applicable.

Item 8. Financial Statements and Supplementary Data

Our Consolidated Financial Statements, together with the report of our independent registered public accounting firm, begin on page 20 of this Annual Report and are incorporated herein by reference.

| 19 |

|

|

| Table of Contents |

Report of Independent Registered Public Accounting Firm

To the Stockholders and the Board of Directors of TGS International Ltd.

Opinion on the Consolidated Financial Statements

We have audited the accompanying consolidated balance sheets of TGS International Ltd. and subsidiaries (collectively, the “Company”) as of December 31, 2019 and 2018, and the related consolidated statements of operations and comprehensive loss, changes in stockholders’ equity, and cash flows for each of the two years in the period ended December 31, 2019, and the related notes (collectively referred to as the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Company as of December 31, 2019 and 2018, and the consolidated results of its operations and its cash flows for each of the two years in the period ended December 31, 2019, in conformity with accounting principles generally accepted in the United States of America.

Material Uncertainty related to Going Concern

The accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern. As discussed in Note 1 to the consolidated financial statements, the Company has suffered an operating loss of $2,115,716 for the year ended December 31, 2019, and as of that date, the Company’s current liabilities exceeded its current assets by $1,555,450, which raise substantial doubt about its ability to continue as a going concern. Management's plans in regard to these matters are also described in Note 1. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s consolidated financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.