As filed with the Securities and Exchange Commission on September 19, 2023

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM F-3

REGISTRATION STATEMENT

UNDER THE

SECURITIES ACT OF 1933

| FARMMI, INC. |

| (Exact name of registrant as specified in its charter) |

| Cayman Islands |

| Not Applicable |

| (State or other jurisdiction |

| (I.R.S. Employer |

| of incorporation or organization) |

| Identification No.) |

Fl 1, Building No. 1, 888 Tianning Street, Liandu District

Lishui, Zhejiang Province

People’s Republic of China 323000

+86-0578-82612876 — telephone

(Address, including zip code, and telephone number, including area code, of registrant’s

principal executive offices)

CT Corporation System

28 Liberty St.

New York, NY 10005

+1-212-894-8940 — telephone

(Name, address including zip code, and telephone number, including area code, of agent for

service)

With a copy to:

Anthony W. Basch, Esq.

Kaufman & Canoles, P.C.

Two James Center, 14th Floor

1021 East Cary Street

Richmond, Virginia 23219

+1-804-771-5700 — telephone

+1-888-360-9092 — facsimile

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement as determined by the registrant.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box: ☐

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a registration statement pursuant to General Instruction I.C. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ☐

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.C. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated September 19, 2023

PROSPECTUS

FARMMI, INC.

21,052,629 Ordinary Shares

This prospectus relates to the resale, from time to time, by the selling shareholders (the “Selling Shareholders”) identified in this prospectus under the caption “Selling Shareholders” of 21,052,629 of our ordinary shares (the “Shares”), par value $0.025 per share. We are not selling any ordinary shares under this prospectus and will not receive any proceeds from the sale of the Shares by the Selling Shareholders. We have agreed to bear all of the expenses incurred in connection with the registration of the Shares.

The Selling Shareholders may sell the Shares offered by this prospectus from time to time on terms to be determined at the time of sale through ordinary brokerage transactions or through any other means described in this prospectus under the caption “Plan of Distribution.” The Shares may be sold at fixed prices, at market prices prevailing at the time of sale, at prices related to prevailing market price or at negotiated prices.

Our ordinary shares are listed on the Nasdaq Capital Market under the symbol “FAMI.” On September 18, 2023, the closing price of our ordinary shares was $0.265 per share.

We are not a Chinese operating company but a Cayman Islands holding company with operations conducted by our subsidiaries and consolidated affiliated entities (“VIEs”) established in People’s Republic of China (“PRC” or “China”), Hong Kong Special Administrative Region of the People’s Republic of China (“HKSAR” or “Hong Kong”), the U.S., and Canada. Therefore, investing in our securities being offered pursuant to this prospectus involves unique and a high degree of risk. You should carefully read and consider the risk factors beginning on page 15 of this prospectus, and the risk factors described in the documents incorporated by reference into this prospectus for more information before you make your investment decision.

The securities offered in this offering are of the off-shore holding company Farmmi, Inc. (the “Company”), which owns equity interests, directly or indirectly, of the operating subsidiaries. Subsidiaries conduct a vast majority of our operations in China and the holding company does not conduct operations in China. We also operate online and e-commerce product sales in China through VIEs and rely on contractual arrangements among our PRC subsidiaries, VIEs and their nominee shareholder for the limited online sale operations. Unless otherwise stated, as used in this prospectus and in the context of describing our operations and consolidated financial information, “Farmmi” “we,” “us,” “Company,” or “our,” refers to Farmmi, Inc., a Cayman Islands holding company. “PRC Subsidiaries” refer to our subsidiaries incorporated in mainland China, “Hong Kong Subsidiaries” refer to our subsidiaries incorporated in Hong Kong, and “North America Subsidiaries” refer to subsidiaries incorporated in the U.S. and in Canada. We will also refer to all of our subsidiaries, “Subsidiaries”. “VIEs” refer to our affiliated entities incorporated in mainland China and the financial results of the VIEs are consolidated into our financial statements for accounting purposes, but we do not own any equity interest in the VIEs.

| i |

| Table of Contents |

We are also subject to legal and operational risks associated with being based in and having the majority of the company’s operations in PRC. The Chinese government may intervene or influence the operation of our PRC operating entities and exercise significant oversight and discretion over the conduct of their business and may intervene in or influence their operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or the value of our ordinary shares. Further, any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly released the Opinions on Severely Cracking Down on Illegal Securities Activities According to Law, or the Opinions. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection requirements, etc. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future.

On February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the relevant system and rules for the management of overseas listing records, which was implemented on March 31, 2023. A total of six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”) and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement, misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the listing and trading of our ordinary shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required. Further, we believe, as of the date of this prospectus, none of the circumstances prohibiting the overseas offering and listing by domestic companies established in mainland China as listed above applies to us, and we can offer and continue to offer our ordinary shares on Nasdaq.

In accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we had been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our Mainland China Subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our Mainland China Subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

| ii |

| Table of Contents |

Further, on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which has come into effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators, any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws and regulations. Any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected of committing a crime. As of the date of this prospectus, we believe that we and our subsidiaries have not provided or publicly disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. We intend to strictly comply with the Confidentiality Provisions and other relevant PRC laws and regulations in our offering and listing on Nasdaq in future.

However, any failure of us or our mainland China subsidiaries to fully comply with the Listing Records Rules and/or the Confidentiality Provisions, may significantly limit or completely hinder our ability to offer or continue to offer our ordinary shares on Nasdaq, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our ordinary shares to significantly decline in value or become worthless. See “Risk Factor — Risks Related to Doing Business in China — The approval of, filing or other procedures with the CSRC or other Chinese regulatory authorities may be required in connection with issuing securities to foreign investors under PRC law, and, if required, we cannot predict whether we will be able, or how long it will take us, to obtain such approval or complete such filing or other procedures.

We or our Subsidiaries may also be subject to PRC laws relating to the use, sharing, retention, security and transfer of confidential and private information, such as personal information and other data. On November 14, 2021, the Cyberspace Administration of China (“CAC”) released the Regulations on the Network Data Security Management (Draft for Comments), or the Data Security Management Regulations Draft, to solicit public opinion and comments till December 13, 2021, which has not been promulgated as of the date of this prospectus. Pursuant to the Data Security Management Regulations Draft, data processors holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. Data processing activities refers to activities such as the collection, retention, use, processing, transmission, provision, disclosure, or deletion of data. According to the latest amended Cybersecurity Review Measures, which was promulgated on November 16, 2021, and became effective on February 15, 2022, an online platform operator holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. As of the date of this prospectus, we have not been informed by any PRC governmental authority of any requirement that we or our Subsidiaries file for approval for this offering. We don’t believe that we or any of our Subsidiaries will be subject to either the amended Cybersecurity Review Measures or the Data Security Management Regulations Draft since none of us hold more than one million users/users’ individual information. However, it is uncertain how the above-mentioned new laws or regulations will be enacted, interpreted or implemented, and whether it will affect us. Since the regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our Subsidiaries’ daily business operation, their ability to accept foreign investments, and our ability to continue to list or offer securities on an U.S. exchange.

On February 7, 2021, the Anti-Monopoly Committee of the State Council promulgated the Anti-monopoly Guidelines for the Platform Economy Sector, or the Anti-monopoly Guideline, aiming to improve anti-monopoly administration on online platforms. The Anti-monopoly Guideline, operating as the compliance guidance under the then-existing PRC anti-monopoly regulatory regime for platform economy operators, specifically prohibits certain acts of the platform economy operators that may have the effect of eliminating or limiting market competition, such as concentration of undertakings.

| iii |

| Table of Contents |

The PRC anti-monopoly regulatory regime started with the Anti-Monopoly Law promulgated by the Standing Committee of the National People’s Congress of China (“SCNPC”) on August 30, 2007 and effective on August 1, 2008, which requires that transactions which are deemed concentrations and involve parties with specified turnover thresholds must be cleared by the Ministry of Commerce of China (“MOFCOM”) before they can be completed. In addition, on February 3, 2011, the General Office of the State Council promulgated a Notice on Establishing the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, or Circular 6, which officially established a security review system for mergers and acquisitions of domestic enterprises by foreign investors. Further, on August 25, 2011, MOFCOM promulgated the Regulations on Implementation of Security Review System for the Merger and Acquisition of Domestic Enterprises by Foreign Investors, or the MOFCOM Security Review Regulations, which became effective on September 1, 2011, to implement Circular 6. Under Circular 6, a security review is required for mergers and acquisitions by foreign investors having “national defense and security” concerns and mergers and acquisitions by which foreign investors may acquire the “de facto control” of domestic enterprises with “national security” concerns. Under the MOFCOM Security Review Regulations, MOFCOM will focus on the substance and actual impact of the transaction when deciding whether a specific merger or acquisition is subject to security review. If MOFCOM decides that a specific merger or acquisition is subject to security review, it will submit it to the Inter-Ministerial Panel, an authority established under the Circular 6 led by the NDRC, and MOFCOM under the leadership of the State Council, to carry out the security review. The regulations prohibit foreign investors from bypassing the security review by structuring transactions through trusts, indirect investments, leases, loans, control through contractual arrangements or offshore transactions.

As a holding company, we may rely upon dividends paid to us by our subsidiaries in the PRC to pay dividends and to finance any debt we may incur. As of the date of this prospectus, we have never declared or paid any cash dividends on our Ordinary Shares. We anticipate that we will retain any earnings to support operations and to finance the growth and development of our business. Therefore, we do not expect to pay cash dividends in the foreseeable future. Any future determination relating to our dividend policy will be made at the discretion of our Board of Directors and will depend on a number of factors, including future earnings, capital requirements, financial conditions and future prospects and other factors the Board of Directors may deem relevant.

Under Cayman Islands law, a Cayman Islands company may pay a dividend out of either its profit or share premium account, but a dividend may not be paid if this would result in the company being unable to pay its debts as they fall due in the ordinary course of business. According to our Third Amended and Restated Articles of Association, dividends can be declared and paid out of funds lawfully available to us, which include the share premium account. Dividends, if any, shall be declared and paid according to the amounts paid up on the shares on which the dividend is paid. All dividends, if any, shall be paid in proportion to the number of shares a shareholder holds during any portion or portions of the period in respect of which the dividend is paid.

Current PRC regulations permit our subsidiary in mainland China to pay dividends to the Company only out of its accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. Under our current corporate structure, we rely on dividend payments or other distributions from our subsidiaries to fund any cash and financing requirements we may have, including the funds necessary to pay dividends and other cash distributions to our shareholders or to service any debt we may incur. If any subsidiary incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to us. In addition, under PRC laws and regulations, each of our Chinese subsidiaries is required to set aside a portion of their net income each year to fund a statutory surplus reserve until such reserve reaches 50% of its registered capital. This reserve is not distributable as dividends. As a result, our PRC subsidiaries are restricted in their ability to transfer a portion of its net assets to us in the form of dividends, loans or advances. Further, the PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. If we are unable to receive funds from our subsidiaries, we may be unable to pay cash dividends on our ordinary shares.

| iv |

| Table of Contents |

Cash dividends, if any, on our ordinary shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10%. A 10% PRC withholding tax is applicable to dividends payable to investors that are non-resident enterprises. Any gain realized on the transfer of ordinary shares by such investors is also subject to PRC tax at a current rate of 10% which in the case of dividends will be withheld at source if such gain is regarded as income derived from sources within the PRC.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC resident enterprise. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including without limitation that (a) the Hong Kong resident enterprise must be the beneficial owner of the relevant dividends; and (b) the Hong Kong resident enterprise must directly hold no less than 25% share ownership in a PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot be certain that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by our PRC subsidiaries to our Hong Kong subsidiaries. As of the date of this prospectus, we have not applied for the tax resident certificate from the relevant Hong Kong tax authority. Our Hong Kong subsidiaries intend to apply for the tax resident certificate when our subsidiaries in mainland China plan to declare and pay dividends to their Hong Kong parent companies.

As an offshore holding company, we will be permitted under PRC laws and regulations to provide funding from the proceeds of our offshore fund-raising activities to our subsidiaries in China only through loans or capital contributions, subject to the satisfaction of the applicable government registration and approval requirements. Before providing loans to our PRC subsidiaries, we will be required to make filings about details of the loans with the State Administration of Foreign Exchange of the PRC (the “SAFE”) in accordance with relevant PRC laws and regulations. Our PRC subsidiaries that receive the loans are only allowed to use the loans for the purposes set forth in these laws and regulations. Under regulations of the SAFE, Renminbi is not convertible into foreign currencies for capital account items, such as loans, repatriation of investments and investments outside of China, unless the prior approval of the SAFE is obtained and prior registration with the SAFE is made. In addition, in accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we have been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our mainland China subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our mainland China subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

Under PRC law, we may provide funding to our PRC subsidiaries only through capital contributions or loans, and only through loans to our consolidated affiliated entities, subject to satisfaction of applicable government registration and approval requirements.

We have not declared or paid any cash dividends, nor do we have any present plan to pay any cash dividends on our ordinary shares in the foreseeable future. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business.

As of the date of this prospectus, we do not anticipate any difficulties on our ability to transfer cash between subsidiaries. We have not installed any cash management policies that dictate the amount of such funds and how such funds are transferred.

Our ordinary shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the Holding Foreign Companies Accountable Act (the “HFCAA”) if the PCAOB determines it is unable to inspect or investigate completely our auditors for two consecutive years. Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. Our auditor, YCM CPA Inc., headquartered in Irvine, California, has been inspected by the PCAOB on a regular basis. Our auditor was not among the PCAOB-registered public accounting firms headquartered in the PRC or Hong Kong that were subject to PCAOB’s determination. On December 15, 2022, the PCAOB removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. Notwithstanding the foregoing, in the future, if it is determined that the PCAOB is unable to inspect or investigate our auditor completely, or if there is any regulatory change or step taken by PRC regulators that does not permit our auditor to provide audit documentations to the PCAOB for inspection or investigation, or the PCAOB expands the scope of the Determination so that we are subject to the HFCAA, as the same may be amended, you may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected or investigated by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditor’s audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities, including trading on the national exchange or “over-the-counter” markets, may be prohibited under the HFCAA.

Investing in our ordinary shares involves risks. See “Risk Factors” beginning on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is ____ , 2023.

| v |

| Table of Contents |

| 1 |

| Table of Contents |

You should rely only on the information contained or incorporated by reference in this prospectus or any prospectus supplement. We have not authorized any person to provide you with different or additional information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement, as well as information we have previously filed with the SEC and incorporated by reference, is accurate as of the date on the front of those documents only. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus is part of a registration statement that we filed with the Securities and Exchange Commission, or SEC. You should read carefully both this prospectus and any prospectus supplement together with additional information described below under the caption “Where You Can Find More Information,” before making an investment decision. We have incorporated exhibits into this registration statement. You should read the exhibits carefully for provisions that may be important to you.

Industry data and other statistical information used in this prospectus, any applicable prospectus supplement, any related free writing prospectus and any document incorporated by reference into this prospectus are based on independent publications, reports by market research firms or other published independent sources. Some data are also based on our good faith estimates, derived from our review of internal surveys and the independent sources listed above. Although we believe these sources are reliable, we have not independently verified the information.

You should rely only on the information contained or incorporated by reference in this prospectus or any prospectus supplement. We have not authorized any person to provide you with different or additional information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement, as well as information we have previously filed with the SEC and incorporated by reference, is accurate as of the date on the front of those documents only. Our business, financial condition, results of operations and prospects may have changed since those dates.

The Selling Shareholder may sell our ordinary shares to underwriters who will sell the securities to the public at a fixed offering price or at varying prices determined at the time of sale. The applicable prospectus supplement will contain the names of the underwriters, dealers or agents, if any, together with the terms of offering and the compensation of those underwriters, dealers or agents. Any underwriters, dealers or agents participating in the offering may be deemed “underwriters” within the meaning of the Securities Act.

All references to “RMB,” “Renminbi” and “¥” are to the legal currency of China and all references to “USD,” “U.S. dollars,” “dollars,” and “$” are to the legal currency of the United States.

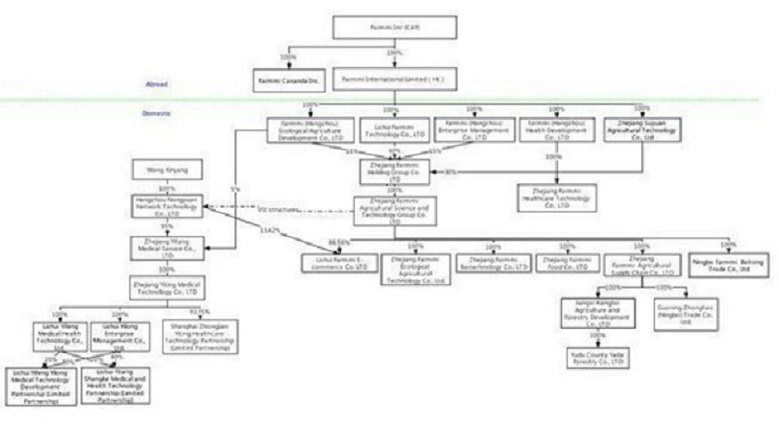

Our Company - Overview

We are not a Chinese operating company but a Cayman Islands holding company with most of the operations conducted by our Subsidiaries established in PRC.

In addition, we also sell our products through online and e-commerce channels. PRC laws and regulations restrict and impose conditions on foreign investment in internet based, value-added telecommunication services, mobile application services and certain other businesses. Accordingly, we operate our online and e-commerce sales in China mainly through our consolidated affiliated entities and rely on contractual arrangements among our PRC subsidiaries, consolidated affiliated entities and their nominee shareholder to control the business operations. Those affiliated entities are consolidated for accounting purposes, but are not entities in which our Cayman holding company, or our investors, own equity. Such structure and the contractual arrangements are designed to enable Farmmi to have power to direct significant activities of those entities and to receive economic benefits from these entities where PRC law prohibits, restricts or imposes conditions on direct foreign investment in such entities.

| 2 |

| Table of Contents |

Our consolidated affiliated entities have been treated as Variable Interest Entities under the Statement of Financial Accounting Standards Board Accounting Standards Codification 810 Consolidation and we are regarded as the primary beneficiary of our consolidated affiliated entities, or VIEs. Accordingly, we treat our VIEs as our consolidated entities under U.S. GAAP and we consolidate the financial results of our VIEs in our consolidated financial statements in accordance with U.S. GAAP.

Our subsidiaries, our VIEs and the shareholder of VIEs have entered into a series of contractual agreements. These contractual arrangements enable us to: (a) receive the economic benefits that could potentially be significant to our consolidated affiliated entities in consideration for the services provided by our subsidiaries; (b) exercise effective control over our consolidated affiliated entities; and (c) hold an exclusive option to purchase all or part of the equity interests in our VIEs when and to the extent permitted by PRC law. The contractual arrangements among our subsidiaries, our VIEs and their shareholder generally include shareholder voting rights proxy agreements, exclusive equity purchase option agreements, technologies, management and consulting services agreements, and equity interest pledge agreements. As a result of the contractual arrangements, we have effective control over and are considered the primary beneficiary of these affiliated companies, and we have consolidated the financial results of these companies in our consolidated financial statements.

The contractual arrangements may not be as effective as direct ownership in providing us with control over our consolidated affiliated entities and we may incur substantial costs to enforce the terms of the arrangements. Uncertainties in the PRC legal system may limit our ability, as a Cayman holding company, to enforce these contractual arrangements. Our corporate structure is subject to risks associated with our contractual arrangements with our VIEs. Investors may never directly hold equity interests in our VIEs. If the PRC government finds that the agreements that establish the structure for operating our business do not comply with PRC laws and regulations, or if these regulations or their interpretations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. See “Risk Factor — Risks Relating to Doing Business in China.”

PRC laws and regulations governing business operations are sometimes vague and uncertain, and therefore, these risks may result in a material change in the operations of our PRC Subsidiaries and Hong Kong Subsidiaries, significant depreciation of the value of our ordinary shares, or a complete hindrance of our ability to offer or continue to offer our securities to investors and cause the value of such securities to significantly decline or be worthless. The Chinese government may intervene or influence the operations of our PRC operating entities at any time and may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in the operations of our PRC operating entities and/or the value of our ordinary shares. Further, any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. See “Prospectus Summary — Permission Required from the PRC Authorities for the Company’s Operation and to Issue Our Ordinary Shares to Foreign Investors”; “Risk Factor — The approval of, filing or other procedures with the CSRC or other Chinese regulatory authorities may be required in connection with issuing securities to foreign investors under PRC law, and, if required, we cannot predict whether we will be able, or how long it will take us, to obtain such approval or complete such filing or other procedures.

Our ordinary shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the HFCAA if the Public Company Accounting Oversight Board of the United States (“PCAOB”) determines it is unable to inspect or investigate completely our auditors for two consecutive years.

In recent years, U.S. regulatory authorities have continued to express their concerns about challenges in their oversight of financial statement audits of U.S.-listed companies with significant operations in China. As part of a continued regulatory focus in the United States on access to audit and other information, the Holding Foreign Companies Accountable Act, or the HFCAA, was enacted on December 18, 2020. The HFCAA includes requirements for the SEC to identify issuers whose audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely because of a restriction imposed by a non-U.S. authority in the auditor’s local jurisdiction. The HFCAA also requires that, to the extent that the PCAOB has been unable to inspect an issuer’s auditor for three consecutive years since 2021, the SEC shall prohibit its securities registered in the United States from being traded on any national securities exchange or over-the-counter markets in the United States.

| 3 |

| Table of Contents |

Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On August 26, 2022, the CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”), governing inspections and investigations of audit firms based in China and Hong Kong. On December 15, 2022, the PCAOB determined that it was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and vacated its previous Determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination. On December 29, 2022, the Accelerating Holding Foreign Companies Accountable Act was signed into law as part of the “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”), reducing the number of consecutive non-inspection years required for triggering the prohibitions under the HFCA Act from three years to two. Our current auditor, YCM CPA Inc., headquartered in Irvine, California, is a firm registered with the PCAOB and is required by the laws of the U.S. to undergo regular inspections by the PCAOB to assess its compliance with the laws of the U.S. and professional standards. YCM CPA Inc. has been subjected to PCAOB inspections. Notwithstanding the foregoing, in the future, if it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, or if there is any regulatory change or step taken by PRC regulators that does not permit our auditors to provide audit documentations to the PCAOB for inspection or investigation, you may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected or investigated by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditors’ audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities, including trading on the national exchange or “over-the-counter” markets, may be prohibited under the HFCAA. See “Risk Factors—Trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act if the PCAOB determines that it cannot inspect or investigate completed our auditors for two consecutive years” for more information.

Permission Required from the PRC Authorities for the Company’s Operation and to Issue Our Ordinary Shares to Foreign Investors

We conduct our business in China through our subsidiaries, and prior to August 2021, also through our VIEs in China. Our operations in China are governed by PRC laws and regulations. We are required to obtain certain permissions from the PRC authorities to operate, issue securities to foreign investors, and transfer certain data. The PRC government has exercised, and may continue to exercise, substantial influence or control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be undermined if our PRC subsidiaries are not able to obtain or maintain approvals to operate in China. The central or local governments could impose new, stricter regulations or interpretations of existing regulations that could require additional expenditures, and efforts on our part to ensure our compliance with such regulations or interpretations. To operate our general business activities currently conducted in mainland China, each of our PRC subsidiaries is required to obtain a business license from the local counterpart of the State Administration for Market Regulation, or SAMR. Each of our PRC subsidiaries has obtained a valid business license from the local SAMR, and no application for any such license has been denied. Our PRC subsidiaries are also required to obtain certain licenses and permits, including but not limited to the following material licenses and permits: Farmmi Food and Farmmi Biotech are required to obtain food business licenses pursuant to the PRC Food Safety Law. As of the date of this prospectus, as advised by our PRC legal counsel, Zhejiang Zhengbiao Law Firm, we and our PRC subsidiaries have received all requisite permits, approvals and certificates from the PRC government authorities to conduct our business operations in China. To our knowledge, no permission or approval has been denied or revoked. However, given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by government authorities, we cannot be certain that relevant policies in this regard will not change in the future, which may require us or our subsidiaries to obtain additional licenses, permits, filings or approvals for conducting our business in the PRC. If we or our subsidiaries do not receive or maintain required permissions or approvals, or inadvertently conclude that such permissions or approvals are not required, we may be subject to governmental investigations or enforcement actions, fines, penalties, suspension of operations, or be prohibited from engaging in relevant business or conducting securities offering, and these risks could result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless.

| 4 |

| Table of Contents |

In connection with our previous issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this prospectus, we and our PRC subsidiaries, (i) are not required to obtain permissions from the China Securities Regulatory Commission, or the CSRC, (ii) are not required to go through cybersecurity review by the Cyberspace Administration of China, or the CAC, and (iii) have not received or were denied such requisite permissions by any PRC authority. However, the PRC government has recently indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers.

On February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the relevant system and rules for the management of overseas listing records, which will be implemented from March 31, 2023. A total of six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”) and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement, misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the listing and trading of our ordinary shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required. Further, we believe, as of the date of this prospectus, none of the circumstances prohibiting the overseas offering and listing by domestic companies established in mainland China as listed above applies to us, and we can offer and continue to offer our ordinary shares on Nasdaq.

In accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we had been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our Mainland China Subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our Mainland China Subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

| 5 |

| Table of Contents |

Further, on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which will come into effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators, any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws and regulations. Once effective, any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected of committing a crime. As of the date of this prospectus, we believe that we and our subsidiaries have not provided or publicly disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. We intend to strictly comply with the Confidentiality Provisions and other relevant PRC laws and regulations in our offering and listing on Nasdaq in future.

However, any failure of us or our mainland China subsidiaries to fully comply with the Listing Records Rules and/or the Confidentiality Provisions, once effective, may significantly limit or completely hinder our ability to offer or continue to offer our ordinary shares on Nasdaq, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our ordinary shares to significantly decline in value or become worthless.

On July 10, 2021, the CAC published a revised draft revision to the Cybersecurity Review Measures for public comment, or the Revised Cybersecurity Measures. Under these measures, an operator having more than one million users shall be subject to cybersecurity review before listing abroad. The cybersecurity review will evaluate the risk of critical information infrastructure, core data, important data, or a large amount of personal information being influenced, controlled or maliciously used by foreign governments after going public overseas. The procurement of network products and services, data processing activities and overseas listing should also be subject to cybersecurity review if they concern or potentially pose risks to national security. According to the effective Cybersecurity Review Measures, online platform/website operators of certain industries may be identified as critical information infrastructure operators by the CAC, once they meet standard as stated in the National Cybersecurity Inspection Operation Guide, and such operators may be subject to cybersecurity review. On December 28, 2021, the CAC, the National Development and Reform Commission (“NDRC”), and other government agencies jointly issued the final version of the Revised Measures for Cybersecurity Review, or the Measures, which took effect on February 15, 2022 and replaced the previously issued Revised Cybersecurity Review Measures. Under the Measures, an “online platform operator” in possession of personal data of more than one million users must apply for a cybersecurity review if it intends to list its securities on a foreign stock exchange. The operators of critical information infrastructure and the online platform operators (collectively, the “Operators”) carrying out data processing activities that affect or may affect national security, shall conduct a cybersecurity review, and any online platform operator who controls more than one million users’ personal information must go through a cybersecurity review by the cybersecurity review office if it seeks to be listed in a foreign country. Pursuant to the Measures, we believe we are not subject to the cybersecurity review by the CAC, given that (i) we possess personal information of a relatively small number of users in our business operations as of the date of this prospectus, significantly less than one million users; and (ii) data processed in our business does not have a bearing on national security and thus shall not be classified as core or important data by the PRC authorities. We don’t believe that we are an Operator within the meaning of the Measures, nor do we control more than one million users’ personal information, and as such, we should not be required to apply for a cybersecurity review under the Revised Measures. Further, an expert interpretation of the Measures published at the CAC’s website on February 17, 2022 indicated no application review is required for operators that have been listed abroad before the implementation of the Revised Cybersecurity Measures. However, the Measures were just recently released and there is a general lack of guidance and substantial uncertainties exist with respect to their interpretation and implementation. For example, certain terms used in the Measures are not defined and require further clarification on their meaning. Whether the data processing activities carried out by traditional enterprises (such as food, medicine, manufacturing, and merchandise sales enterprises) are subject to such review and the scope of the review remain to be further clarified by the regulatory authorities in the subsequent implementation process.

| 6 |

| Table of Contents |

The PRC government recently initiated a series of regulatory actions and statements to regulate business operations in China, including adopting new measures to extend the scope of cybersecurity reviews, cracking down on illegal activities in the securities market, and expanding the efforts in anti-monopoly enforcement. The PRC government is increasingly focused on data security. In July 2021, the CAC opened cybersecurity probes into several U.S.-listed technology companies focusing on anti-monopoly regulation, and how companies collect, store, process and transfer data. On November 14, 2021, the CAC published the Draft Regulations on Network Data Security Management in November 2021 for public comments, which among other things, stipulates that a data processor listed overseas must conduct an annual data security review by itself or by engaging a data security service provider and submit the annual data security review report for a given year to the municipal cybersecurity department before January 31 of the following year. If the Draft Regulations on Network Data Security Management are enacted in the current form, we, as an overseas listed company, would be required to carry out an annual data security review and comply with the relevant reporting obligations. As of the date of this prospectus, the draft regulations have been released for public comment only and have not been formally adopted. The final provisions and the timeline for its adoption are subject to changes and uncertainties. We have been closely monitoring the regulatory development in China, particularly regarding the requirements of approvals, annual data security review or other procedures that may be imposed on us. If any approval, review or other procedure is in fact required, we cannot assure our investors that we will be able to obtain such approval or complete such review or other procedure timely or at all. For any approval that we may be able to obtain, it could nevertheless be revoked and the terms of its issuance may impose restrictions on our operations and/or securities offerings. The PRC regulatory requirements with respect to cybersecurity and data security are constantly evolving and can be subject to varying interpretations and significant changes, resulting in uncertainties about the scope of our responsibilities in that regard. Failure to comply with these cybersecurity and data privacy requirements in a timely manner, or at all, may subject us to government enforcement actions and investigations, fines, penalties, suspension or disruption of our operations.

Because we are relying on advice of our PRC counsel with regard to PRC laws, there is uncertainty inherent in relying on an opinion of counsel in connection with whether we are required to obtain permissions from a governmental agency that is required to approve of our operations and/or listings. In the event that an government approval is required, we cannot assure our investor that we will be able to receive clearance in a timely manner, or at all. Any failure of us to fully comply with new regulatory requirements may significantly limit or completely hinder our ability to offer or continue to offer our ordinary shares, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our shares to significantly decline in value or become worthless.

For more detailed information, see “Risk Factors–Risks Relating to Doing Business in China.”

Dividend Distributions and Cash Transfer among Farmmi and the Subsidiaries

As a holding company, we may rely upon dividends paid to us by our subsidiaries in the PRC to pay dividends and to finance any debt we may incur. As of the date of this prospectus, we have never declared or paid any cash dividends on our Ordinary Shares. We anticipate that we will retain any earnings to support operations and to finance the growth and development of our business. Therefore, we do not expect to pay cash dividends in the foreseeable future. Any future determination relating to our dividend policy will be made at the discretion of our Board of Directors and will depend on a number of factors, including future earnings, capital requirements, financial conditions and future prospects and other factors the Board of Directors may deem relevant.

Under Cayman Islands law, a Cayman Islands company may pay a dividend out of either its profit or share premium account, but a dividend may not be paid if this would result in the company being unable to pay its debts as they fall due in the ordinary course of business. According to our Third Amended and Restated Articles of Association, dividends can be declared and paid out of funds lawfully available to us, which include the share premium account. Dividends, if any, shall be declared and paid according to the amounts paid up on the shares on which the dividend is paid. All dividends, if any, shall be paid in proportion to the number of shares a shareholder holds during any portion or portions of the period in respect of which the dividend is paid.

| 7 |

| Table of Contents |

Current PRC regulations permit our subsidiary in mainland China to pay dividends to the Company only out of its accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. Under our current corporate structure, we rely on dividend payments or other distributions from our subsidiaries to fund any cash and financing requirements we may have, including the funds necessary to pay dividends and other cash distributions to our shareholders or to service any debt we may incur. If any subsidiary incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to us. In addition, under PRC laws and regulations, each of our Chinese subsidiaries is required to set aside a portion of their net income each year to fund a statutory surplus reserve until such reserve reaches 50% of its registered capital. This reserve is not distributable as dividends. As a result, our PRC subsidiaries are restricted in their ability to transfer a portion of its net assets to us in the form of dividends, loans or advances. Further, the PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. If we are unable to receive funds from our subsidiaries, we may be unable to pay cash dividends on our ordinary shares.

Cash dividends, if any, on our ordinary shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10%. A 10% PRC withholding tax is applicable to dividends payable to investors that are non-resident enterprises. Any gain realized on the transfer of ordinary shares by such investors is also subject to PRC tax at a current rate of 10% which in the case of dividends will be withheld at source if such gain is regarded as income derived from sources within the PRC.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC resident enterprise. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including without limitation that (a) the Hong Kong resident enterprise must be the beneficial owner of the relevant dividends; and (b) the Hong Kong resident enterprise must directly hold no less than 25% share ownership in a PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot be certain that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by our PRC subsidiaries to our Hong Kong subsidiaries. As of the date of this prospectus, we have not applied for the tax resident certificate from the relevant Hong Kong tax authority. Our Hong Kong subsidiaries intend to apply for the tax resident certificate when our subsidiaries in mainland China plan to declare and pay dividends to their Hong Kong parent companies.

As an offshore holding company, we will be permitted under PRC laws and regulations to provide funding from the proceeds of our offshore fund-raising activities to our subsidiaries in China only through loans or capital contributions, subject to the satisfaction of the applicable government registration and approval requirements. Before providing loans to our PRC subsidiaries, we will be required to make filings about details of the loans with the State Administration of Foreign Exchange of the PRC (the “SAFE”) in accordance with relevant PRC laws and regulations. Our PRC subsidiaries that receive the loans are only allowed to use the loans for the purposes set forth in these laws and regulations. Under regulations of the SAFE, Renminbi is not convertible into foreign currencies for capital account items, such as loans, repatriation of investments and investments outside of China, unless the prior approval of the SAFE is obtained and prior registration with the SAFE is made. In addition, in accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we have been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our mainland China subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our mainland China subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

| 8 |

| Table of Contents |

Under PRC law, we may provide funding to our PRC subsidiaries only through capital contributions or loans, and only through loans to our consolidated affiliated entities, subject to satisfaction of applicable government registration and approval requirements.

We have not declared or paid any cash dividends, nor do we have any present plan to pay any cash dividends on our ordinary shares in the foreseeable future. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business.

As of the date of this prospectus, we do not anticipate any difficulties on our ability to transfer cash between subsidiaries. We have not installed any cash management policies that dictate the amount of such funds and how such funds are transferred.

The Holding Foreign Companies Accountable Act (“HFCAA”)

Our ordinary shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the HFCAA if the Public Company Accounting Oversight Board of the United States (“PCAOB”) determines it is unable to inspect or investigate completely our auditors for two consecutive years.

In recent years, U.S. regulatory authorities have continued to express their concerns about challenges in their oversight of financial statement audits of U.S.-listed companies with significant operations in China. As part of a continued regulatory focus in the United States on access to audit and other information, the Holding Foreign Companies Accountable Act, or the HFCAA, was enacted on December 18, 2020. The HFCAA includes requirements for the SEC to identify issuers whose audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely because of a restriction imposed by a non-U.S. authority in the auditor’s local jurisdiction. The HFCAA also requires that, to the extent that the PCAOB has been unable to inspect an issuer’s auditor for three consecutive years since 2021, the SEC shall prohibit its securities registered in the United States from being traded on any national securities exchange or over-the-counter markets in the United States.

Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On August 26, 2022, the CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”), governing inspections and investigations of audit firms based in China and Hong Kong. On December 15, 2022, the PCAOB determined that it was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and vacated its previous Determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination. On December 29, 2022, the Accelerating Holding Foreign Companies Accountable Act was signed into law as part of the “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”), reducing the number of consecutive non-inspection years required for triggering the prohibitions under the HFCA Act from three years to two. Our current auditor, YCM CPA Inc., headquartered in Irvine, California, is a firm registered with the PCAOB and is required by the laws of the U.S. to undergo regular inspections by the PCAOB to assess its compliance with the laws of the U.S. and professional standards. YCM CPA Inc. has been subjected to PCAOB inspections. Notwithstanding the foregoing, in the future, if it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, or if there is any regulatory change or step taken by PRC regulators that does not permit our auditors to provide audit documentations to the PCAOB for inspection or investigation, you may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected or investigated by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditors’ audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities, including trading on the national exchange or “over-the-counter” markets, may be prohibited under the HFCAA.

| 9 |

| Table of Contents |

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS; CAUTIONARY LANGUAGE