Exhibit 99.2

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our company’s financial condition and results of operations should be read in conjunction with our consolidated financial statements and the related notes included elsewhere in this report. This discussion contains forward-looking statements that involve risks and uncertainties. Actual results and the timing of selected events could differ materially from those anticipated in these forward-looking statements as a result of various factors.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements. All statements contained in this report other than statements of historical fact, including statements regarding our future results of operations and financial position, our business strategy and plans, and our objectives for future operations, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” and similar expressions are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in the “Risk Factors” section. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

Business Overview

We currently produce and/or sell the following categories of agricultural products: Shiitake mushrooms, Mu Er mushrooms, other edible fungi and other agricultural products. We do not grow fungi, but purchase dried edible fungi from third party suppliers, mainly from family farms, and two co-operatives representing family farms, Jingning Liannong Trading Co. Ltd. (“JLT”) and Qingyuan Nongbang Mushroom Industry Co., Ltd. (“QNMI”), with whom we have worked with for many years. JLT and QNMI are two companies in Lishui area where our facilities are located. They are co-operatives representing family farms which plant and provide edible fungi. JLT and QNMI themselves do not have any facilities and do not process any fungi. They are established to share resources such as procurement information and to enjoy the advantage of economy of scale. After we select and filter the dried edible fungi for specific size and quality from our suppliers, we may further dehydrate them again, as deemed necessary, to ensure the uniform level of dryness of our products. We then package the fungi products for sale. The only products we process and package are edible fungi, which are processed and packaged at our own processing facilities. For other agricultural products, such as rice and edible oil, we purchase them from third-party suppliers, and sell these products at our online store Farmmi Liangpin Market. Mainly through distributors, we offer gourmet dried mushrooms to domestic and overseas retail supermarkets, produce distributors and foodservice distributors and operators. We have become an enterprise with advanced processing equipment and business management experience, and we pride ourselves on consistently producing quality mushrooms and serving our customers with a high level of commitment.

Currently, we estimate that approximately 93% of our products are sold in China to domestic distributors and the remaining 7% are sold internationally, including USA, Japan, Canada and other countries, through distributors. In addition, in order to enhance our e-commerce marketing presence, we developed our own e-commerce websites www.farmmi.com and www.farmmi88.com. We are also testing a few offline stores in Hangzhou to expand our brand presence and grow revenue.

Growth Strategy

Increasing our market share — the premium quality of our products has been long recognized by our customers. People’s increasing awareness of healthy dietary will likely lead to increased demand of our products. Our development plan mainly focuses on developing high-quality agricultural products market. Through our continued efforts of building e-commerce platform, expansion to international market, and building stable relationship with suppliers, we expect to expand our product lines and improve our brand awareness and customer loyalty, to meet the demands of market and customers, and improve our sales performance.

Expansion of our sources of supply, productivity and sales network — to meet the increasing demand, we emphasize cooperation with major suppliers as well as small family farms to ensure the quantity and quality of raw materials. While expanding supply resource, we also plan to increase our processing capability and upgrade production facilities to increase productivity. In addition to our present sales network, we intend to invest more in our online stores, continue to train our employees, upgrade relevant information technology and supply chain system, with the goal of making an integrated sales network with an international approach.

Securing high quality raw materials with competitive price — to meet the increasing demand for our products, we have been increasing our cooperation with major suppliers, with whom we have been working together for many years, to secure the quality and quantity of our raw materials. We also have dedicated teams that constantly visit and communicate with the family farm suppliers, to monitor the quality and quantity of raw materials. By working closely with our suppliers throughout the planting seasons, we have been providing such suppliers technical support to secure the stable supply of our raw materials. With our deep understanding of the edible fungi market, we have been able to purchase raw materials of premium quality at favorable prices. Edible fungi can be stored for a long time after simple processing, therefore we have been purchasing edible fungi when we expect their purchase price to increase, and store them to fulfill future sales orders. This strategy has been proven effective and will continue to be used by us as a cost control method.

Factors Affecting Our Results of Operations

Government Policy May Impact our Business and Operating Results

We have not seen any impact of unfavorable government policy upon our business in recent years. However, our business and operating results will be affected by China’s overall economic growth and government policies. Unfavorable changes in government policies could affect the demand for our products and could materially and adversely affect our results of operations. Our edible fungi products are currently eligible for certain favorable government tax incentive and other incentives, any future changes in the government’s policy upon edible fungi industry may have a negative effect on our operations.

| 2 |

Price Inelasticity of Raw Materials May Reduce Our Profit

As a processor of edible fungi, we rely on a continuous and stable supply of edible fungi raw materials to ensure our operation and expansion. The price of edible fungi may be inelastic when we wish to purchase supplies, resulting in an increase in raw material prices and thus reduce our profit. In addition, although we compete primarily the high-end market which puts more emphasize on the flavor, texture and quality of our products, we risk losing customers by increasing our selling prices.

Competition in Edible Fungi Industry

Although we have a lot of competitive advantages, such as premium product quality, stable and experienced factory employees, favorable production locations within proximity of significant mushroom planting bases and strong relationships with our significant suppliers, we face a series of challenges.

Our products face competition from a number of companies operating in the vicinity. One of the largest competitors has high sales volume, which enables this competitor to purchase and sell edible fungi at a relatively lower price. Another major competitor has much larger plants and warehouses than we have and its main product is Mu Er mushrooms with different sorts and qualities. Competition from these two major competitors may prevent us from increasing our revenue.

On the other hand, although we believe we distinguish our Company from competitors on the basis of product quality, the edible fungi industry is fragmented and subject to relatively low barriers of entry. Many of our competitors can provide products at relatively lower prices to increase their supplies which may affect our profit margins as we seek to compete with them.

At last, we have devoted significant resources to build and develop our online stores, Farmmi Jicai and Farmmi Liangpin Market. We plan to expand these two online stores. While this strategy may offer new opportunities to our Company, it is also a new venture and is impacted by many other factors. Farmmi Jicai and Farmmi Liangpin Market are not well known by consumers yet, and we do not have rich experience in e-commerce operation. As a result, we have no guarantee that we will be successful in this new expansion. If we do not manage our expansion effectively, our business prospects could be impaired.

Economy and Politics

Our results of operations have been adversely affected, to the extent that the COVID-19 or any other epidemic harms the Chinese and global economy in general. Any potential impact to our results will depend on, to a large extent, future developments and new information that may emerge regarding the duration and severity of the COVID-19 and the actions taken by government authorities and other entities to contain the COVID-19 or treat its impact, almost all of which are beyond our control.

Our ability to be successful in China depends in part on our awareness of trends in politics that may affect our company, including, for example, government initiatives that would either encourage or discourage programs and companies that produce healthy foods or efforts to increase export of agricultural products. In addition, we must be aware of political situations in destination countries of our products, particularly if such countries take action to stifle importation of food products from abroad.

| 3 |

Trend Information

We have noted the existence of the following trends since October 2019, all of which are likely to affect our business to the extent they continue in the future:

China’s edible fungi industry is growing, both in absolute terms and in market share.

Through its development of enoki mushroom industrialization technology in the 1960s, Japan became the world leader in mushroom farming. As other countries’ fungi farming technology improved, China began to supplant Japan and now became the largest worldwide edible mushroom producer. China’s growth has outpaced worldwide production growth rates. While China’s growth rates in the past much higher than world growth rates, it appears to be moving from rapid expansion to a more mature industry. As China’s mushroom industry is moving from rapid expansion to a more mature stage, we expect the effect of industry growth on promoting our sales volume will decrease.

The COVID-19 has had a significant impact on our operations since January 2020 and could adversely affect our business and financial results for the remaining months of the 2020 fiscal year.

Our sales volume of Shiitake mushroom for the six months ended March 31, 2020 was approximately 591 tons. This number represents a decrease of 71 tons compared with 662 tons sales volume for the same period of fiscal 2019. In the meanwhile, our sales volume of Mu Er for the six months ended March 31, 2020 was approximately 476 tons. This number represents an increase of 57 tons compared with 476 tons sales volume for the same period of fiscal 2019. On an overall basis, our sales volume of Shiitake mushroom and Mu Er was 1,067 tons for the six months ended March 31, 2020, a decrease of 14 tons as compared with 1,081 tons sales volume for the same period of fiscal 2019. The decreased sales of Shiitake mushroom and Mu Er was primarily due to the reduced economic activities caused by the pandemic of COVID-19. We expect such decrease should be temporary, and the sales may recover in the near future upon resumption and increase in economic activities as the spread of the disease has gradually been under control in China. However, COVID-19 could still adversely affect our business and financial results for the remaining months of fiscal year 2020. Although we do not expect a continued decline in sales in long term, the extent of the impact of COVID-19 on the our results of operations and financial condition will depend on future developments, including the duration and spread of the outbreak and the impact on our customers, which are still uncertain and cannot be reasonably estimated at this point of time.

| 4 |

Our aggregate employee salaries have been decreasing.

During the period of October 2019 to July 2020, our monthly salary expense was as follows:

The decrease in monthly employee salaries of January was mainly due to the Chinese New Year Holiday, when some employees took extended unpaid leaves during the holiday period. The decrease in monthly employee salaries of February and March was mainly due to the lock-down, travel restrictions and quarantine imposed by the Chinese government as a result of the COVID-19 pandemic. Monthly salaries after March decreased due mainly to reduction of sales volume as a major portion of salaries are commissions directly related to sales volume.

Raw material costs have been on the downward trends.

With our deep understanding of the edible fungi market, constant market research, and communication with our suppliers, we have been able to obtain favorable price for premium raw materials. With increased sales orders we receive, we need to purchase additional raw materials to meet the new demand. We expect the raw material costs in fiscal year 2020 will be decreasing, fluctuating between 1% and 5% comparing with fiscal year 2019.

| 5 |

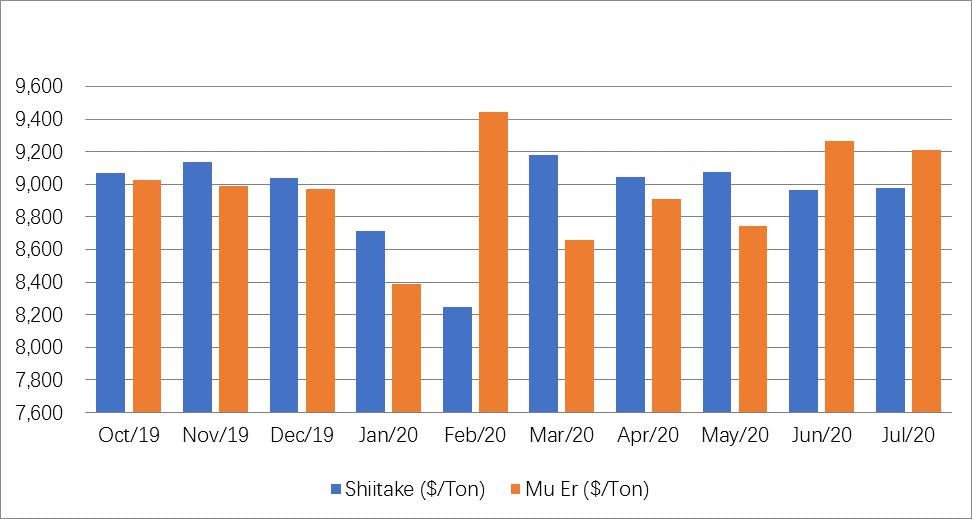

During the period from October 2018 to July 2020, the average monthly unit price per ton for Shiitake and Mu Er we purchased were as follows:

We anticipate that for fiscal year 2020, the average unit price of Shiitake and Mu Er we purchase will be about $9,214 per ton and $9,285 per ton, respectively. We expect our gross margin will be slightly lower in fiscal year 2020 than in fiscal year 2019.

We expect the agriculture industry in China to become increasingly reliant on Internet sales.

Government initiatives such as the concept of “Internet+” articulated by Premier Li Keqiang beginning in 2015, reflect the government’s push to incorporate Internet and other information technology in conventional industries. One of the specific applications of this concept has been “Internet + Agriculture”, which reflects the increased use of technology both in the growing and sales sides of farming.

In addition, we have seen shifts of Chinese consumers to purchase products — including food products like ours — online. We have been building our online store Farmmi Liangpin Market (now called Farmmi Jicai) in response to this trend, and this online store mainly targets on small wholesale clients, such as restaurants and retailers. Since its launch in December 2016, our online sales have been increasing rapidly. In September 2018, we started another Farmmi Liangpin Market online store, which mainly facing individual customers and started to generate revenue since October 2018. Besides selling edible mushrooms, this store also sells other agricultural products, such as rice, edible oil and other local specialty food products from different provinces of China.

| 6 |

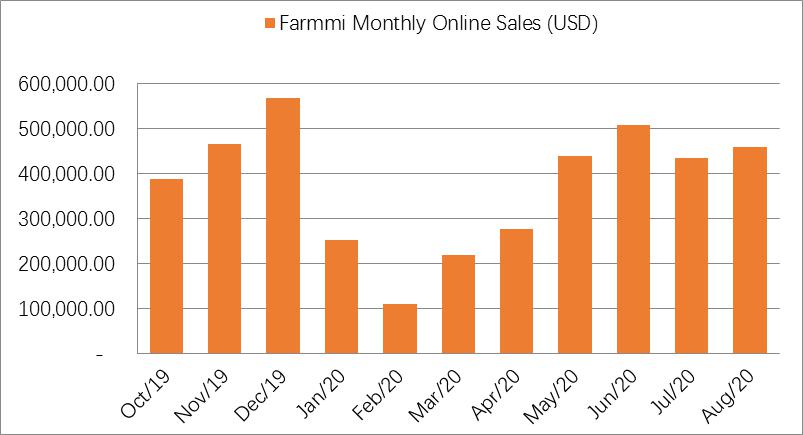

During the six months ended March 31, 2020, our online sales accounted for 14.75% of our total sales. For the six months ended March 31, 2020, our aggregate online sales were $2,002,500, a decrease by 35.37% compared with online sales for the same period in 2019, and the average monthly online sales were $333,750. The following chart shows our online sales for each month from October 2019 to August 2020:

The online sales during the six months ended March 31, 2020 decreased as compared to the same period of last year. The significant decrease in monthly online sales from January 2020 to March 2020 was mainly attributable to the reduced economic activities due to the lockdown and travel restriction imposed by the Chinese government as a result of the COVID-19 pandemic.

Increased sales to China Forest.

China Forest, one of the biggest edible fungi exporters in China, has been one of our major customers since 2016. Our sales to China Forest for the six months ended March 31, 2020 totaled $10,409,681, an increase of 10.44% from $9,425,737 for the same period in 2019, mainly due to the increased sales volume of Mu Er. Our sales of Mu Er to China Forest for the six months ended March 31, 2020 were 421 tons, an increase of 28.29% from 328 tons for the same period in 2019. However, our sales of Shiitake mushroom to China Forest for the six months ended March 31, 2020 totaled 439 tons, a decrease of 2.12% from 448 tons for the same period in 2019.

| 7 |

Critical Accounting Policies and Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities, revenues and expenses, and related disclosures in the financial statements. Critical accounting policies are those accounting policies that may be material due to the levels of subjectivity and judgment necessary to account for highly uncertain matters or the susceptibility of such matters to change, and that have a material impact on financial condition or operating performance. While we base our estimates and judgments on our experience and on various other factors that we believe to be reasonable under the circumstances, actual results may differ from these estimates under different assumptions or conditions. We believe the following critical accounting policies used in the preparation of our financial statements require significant judgments and estimates. For additional information relating to these and other accounting policies, see Note 2 to our unaudited condensed consolidated financial statements included elsewhere in this report.

Use of Estimates

In preparing the consolidated financial statements in conformity with US GAAP, management makes estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the dates of the consolidated financial statements, as well as the reported amounts of revenues and expenses during the reporting year. Significant items subject to such estimates and assumptions include the useful lives of property, plant and equipment; allowances pertaining to the allowance for doubtful accounts and advances to suppliers; the valuation of inventories; the valuation of beneficial conversion feature of the convertible notes; and the valuation of deferred tax assets.

Revenue Recognition

We recognized revenue following Accounting Standards Update (“ASU”) 2014-09 Revenue from Contracts with Customers (“ASC Topic 606”). In accordance with ASC 606, to determine revenue recognition for contracts with customers, we perform the following five steps: (i) identify the contract(s) with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies the performance obligation.

We recognize revenue when we transfer our goods and services to customers in an amount that reflects the consideration to which we expect to be entitled in such exchange. All of our contracts have a single performance obligation satisfied at a point in time and the transaction price is stated in the contract, usually as a price per ton. We evaluate whether it is appropriate to record the gross amount of product sales and related costs or the net amount earned as commissions. In accordance with ASC 606, when we act as a principal, that we obtain control of the specified goods before they are transferred to the customers, the revenues should be recognized in the gross amount of consideration to which it expects to be entitled in exchange for the specified goods transferred.

The contract liabilities are recorded on the unaudited condensed consolidated balance sheets as advances from customers as of March 31, 2020 and September 30, 2019. For the six months ended March 31, 2020 and 2019, there was no revenue recognized from performance obligations related to prior periods.

We do not have any contract assets since revenue is recognized when control of the promised goods is transferred and the payment from customers is not contingent on a future event.

Refer to Note 15 — Segment reporting for details of revenue segregation of our Unaudited Condensed Consolidated Financial Statements.

Accounts Receivable

Accounts receivable are presented net of allowance for doubtful accounts. We maintain allowance for doubtful accounts for estimated losses. We review our accounts receivable on a periodic basis and make general and specific allowances when there is doubt as to the collectability of individual balances. In evaluating the collectability of individual receivable balances, we consider various factors, including the age of the balance, customer’s payment history, its current credit-worthiness and current economic trends. Accounts are written off after efforts at collection prove unsuccessful. As of March 31, 2020 and September 30, 2019, no allowance for doubtful accounts was recorded because all accounts receivable are fully realizable.

Inventory, net

We value our inventory at the lower of cost, determined on a weighted average basis, or net realizable value. We review our inventory periodically to determine if any reserves are necessary for potential obsolescence or if the carrying value exceeds net realizable value. We recorded inventory reserve of $223,037 and nil as of March 31, 2020 and September 30, 2019, respectively.

| 8 |

Recent accounting pronouncements

In June 2016, the FASB issued Accounting Standards Update (“ASU”) 2016-13, Financial Instruments-Credit Losses (Topic 326), which requires entities to measure all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts. This replaces the existing incurred loss model and is applicable to the measurement of credit losses on financial assets measured at amortized cost. ASU 2016-13 was subsequently amended by Accounting Standards Update 2018-19, Codification Improvements to Topic 326, Financial Instruments — Credit Losses, Accounting Standards Update 2019-04 Codification Improvements to Topic 326, Financial Instruments — Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments, and Accounting Standards Update 2019-05, Targeted Transition Relief. For public entities, ASU 2016-13 and its amendments is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019. For all other entities, this guidance and its amendments will be effective for fiscal years beginning after December 15, 2022, including interim periods within those fiscal years. As an emerging growth company, we plan to adopt this guidance effective October 1, 2023. We are currently evaluating the impact of our pending adoption of ASU 2016-13 on our consolidated financial statements.

In August 2018, the FASB Accounting Standards Board issued ASU No. 2018-13, “Fair Value Measurement (Topic 820): Disclosure Framework Changes to the Disclosure Requirements for Fair Value Measurement” (“ASU 2018-13”). ASU 2018-13 modifies the disclosure requirements on fair value measurements. ASU 2018-13 is effective for all entities for fiscal years and interim periods within those fiscal years beginning after December 15, 2019, with early adoption permitted for any removed or modified disclosures. The removed and modified disclosures will be adopted on a retrospective basis and the new disclosures will be adopted on a prospective basis. The Company will adopt this guidance effective October 1, 2020. The Company is currently evaluating the impact of its pending adoption of this guidance on its consolidated financial statements but does not expect this guidance will have a material impact on its consolidated financial statements.

In December 2019, the FASB issued ASU No. 2019-12, Income Taxes (Topic 740)—Simplifying the Accounting for Income Taxes. ASU 2019-12 is intended to simplify accounting for income taxes. It removes certain exceptions to the general principles in Topic 740 and amends existing guidance to improve consistent application. ASU 2019-12 is effective for fiscal years beginning after December 15, 2020 and interim periods within those fiscal years, with early adoption permitted. The Company will adopt this guidance effective October 1, 2021. The Company is currently evaluating the impact of its pending adoption of this guidance on its consolidated financial statements but does not expect this guidance will have a material impact on its consolidated financial statements.

In February 2020, the FASB issued ASU 2020-02, “Financial Instruments – Credit Losses (Topic 326) and Leases (topic 842) Amendments to SEC Paragraphs Pursuant to SEC Staff Accounting Bulletin No. 119 and Update to SEC Section on Effective Date Related to Accounting Standards Update No. 2016-02, Leases (topic 842)”. This ASU provides guidance regarding methodologies, documentation, and internal controls related to expected credit losses. This ASU is effective for interim and annual periods beginning after December 15, 2019, and early adoption is permitted. The Company will adopt this guidance effective October 1, 2020. The Company is currently evaluating the impact of its pending adoption of this guidance on its consolidated financial statements but does not expect this guidance will have a material impact on its consolidated financial statements.

The Company does not believe other recently issued but not yet effective accounting standards, if currently adopted, would have a material effect on the unaudited condensed consolidated financial position, statements of operations and cash flows.

| 9 |

Results of Operations for the Six Months Ended March 31, 2020 and 2019

Overview

The following table summarizes our results of operations for the six months ended March 31, 2020 and 2019:

| Six Months Ended March 31, | Variance | |||||||||||||||

| 2020 | 2019 | Amount | % | |||||||||||||

| Revenue | $ | 13,580,782 | $ | 14,388,187 | $ | (807,405 | ) | (5.61 | )% | |||||||

| Cost of revenues | (11,470,717 | ) | (11,845,025 | ) | (374,308 | ) | (3.16 | )% | ||||||||

| Gross profit | 2,110,065 | 2,543,162 | (433,097 | ) | (17.03 | )% | ||||||||||

| Selling and distribution expenses | (142,382 | ) | (281,213 | ) | (138,831 | ) | (49.37 | )% | ||||||||

| General and administrative expenses | (828,414 | ) | (876,746 | ) | (48,332 | ) | (5.51 | )% | ||||||||

| Income from operations | 1,139,269 | 1,385,203 | (245,934 | ) | (17.75 | )% | ||||||||||

| Interest income | 141 | 451 | (310 | ) | (68.74 | )% | ||||||||||

| Interest expense | (1,290,039 | ) | (1,527,302 | ) | (237,263 | ) | (15.53 | )% | ||||||||

| Other income (expense) net | 110,966 | (1,583 | ) | 112,549 | 7,109.85 | % | ||||||||||

| Loss before income taxes | (39,663 | ) | (143,231 | ) | 103,568 | (72.31 | )% | |||||||||

| Provision for income taxes | (24,144 | ) | (27,860 | ) | (3,716 | ) | (13.34 | )% | ||||||||

| Net loss | $ | (63,807 | ) | $ | (171,091 | ) | $ | (107,284 | ) | (62.71 | )% | |||||

| 10 |

Revenues

Currently, we have three main types of revenue streams deriving from our three major product categories: Shiitake, Mu Er and other edible fungi and other agricultural products.

The following table sets forth the breakdown of our revenues for the six months ended March 31, 2020 and 2019, respectively:

| Six Months Ended March 31, | Variance | |||||||||||||||||||||||

| 2020 | % | 2019 | % | Amount | % | |||||||||||||||||||

| Shiitake | $ | 7,346,174 | 54.09 | % | $ | 8,346,344 | 58.01 | % | $ | (1,000,170 | ) | (11.98 | )% | |||||||||||

| Mu Er | 5,762,752 | 42.43 | % | 5,167,414 | 35.91 | % | 595,338 | 11.52 | % | |||||||||||||||

| Other edible fungi and other agricultural products | 471,857 | 3.47 | % | 874,429 | 6.08 | % | (402,572 | ) | (46.04 | )% | ||||||||||||||

| Total | $ | 13,580,782 | 100.00 | % | $ | 14,388,187 | 100.00 | % | $ | (807,405 | ) | (5.61 | )% | |||||||||||

Total revenues for the six months ended March 31, 2020 decreased by $807,405, or 5.61%, to $13,580,782 from $14,388,187 for the same period of last year.

Revenue from sales of Shiitake decreased by $1,000,170 or 11.98%, to $7,346,174 for the six months ended March 31, 2020 from $8,346,344 for the same period of last year, mainly due to the decreased sales volume, from 662 tons for the six months ended March 31, 2019 to 591 tons for the six months ended March 31, 2020, which resulted in a decrease of $885,891 in revenue from sales of Shiitake. The decrease in sales volume of Shiitake was caused by the reduced customer orders related to travel restriction imposed by the Chinese government due to the COVID-19 pandemic. Also, the average unit sales price for Shiitake reduced from $12,608 per ton for the six months ended March 31, 2019 to $12,425 per ton for the six months ended March 31, 2020, which resulted in a decrease of $114,279 in revenue from sales of Shiitake. The decrease in the average unit sales price of Shiitake was a result of our adjusted business strategy to stimulate customer orders to maintain the sales level.

Revenue from sales of Mu Er increased by $595,338, or 11.52%, to $5,762,752 for the six months ended March 31, 2020 from $5,167,414 for the same period of last year, mainly due to the increased sales volume. Sales volume of Mu Er increased to 476 tons for the six months ended March 31, 2020 from 419 tons for the same period of last year, which resulted in an increase of $698,188 in revenue from sales of Mu Er. The volume increase was partially offset by a lower average selling price from $12,333 per ton for the six months ended March 31, 2019 to $12,103 per ton for the six months ended March 31, 2020, which resulted in a decrease of $102,850 in revenue from sales of Mu Er. The increase in sales volume of Mu Er was caused by the increase in market demand for Mu Er. Average unit sales price of Mu Er decreased by 1.86%, which changed in line with the price of raw materials. As a result of the increased competition amongst the local suppliers. the Company was able to purchase raw materials from suppliers at lower prices during the six months ended March 31, 2020.

Revenue from sales of other edible fungi and other agricultural products decreased by $402,572, or 46.04%, to $471,857 for the six months ended March 31, 2020 from $874,429 for the same period of last year. The decrease was mainly attributed to the decrease in sales volume from 28 tons for the six months ended March 31, 2019 to 18 tons for the six months ended March 31, 2020, which resulted in a decrease of $289,874 in revenue from sales of other edible fungi and other agricultural products. The decrease in sales volume of other edible fungi and other agricultural products was caused by the stay-at-home order and travel restriction imposed by the Chinese government due to the COVID-19 pandemic. Further, the decrease in average unit sales price from $31,230 per ton for the six months ended March 31, 2019 to $26,322 per ton for the six months ended March 31, 2020, which resulted in a decrease of $112,698 in revenue from sales of other edible fungi and other agricultural products. The decrease in average unit sales price was in line with the decrease in price of raw materials.

| 11 |

Cost of Revenues

The following table sets forth the breakdown of the Company’s cost of revenue for the six months ended March 31, 2020 and 2019, respectively:

| Six Months Ended March 31, | Variance | |||||||||||||||||||||||

| 2020 | % | 2019 | % | Amount | % | |||||||||||||||||||

| Shiitake | $ | 6,289,207 | 54.86 | % | $ | 6,885,006 | 58.12 | % | $ | (595,799 | ) | (8.65) | % | |||||||||||

| Mu Er | 4,805,731 | 41.92 | % | 4,295,736 | 36.27 | % | 509,995 | 11.87 | % | |||||||||||||||

| Other edible fungi and other agricultural products | 369,237 | 3.22 | % | 664,283 | 5.61 | % | (295,046 | ) | (44.42) | % | ||||||||||||||

| Total | $ | 11,464,175 | 100.00 | % | $ | 11,845,025 | 100.00 | % | $ | (380,850 | ) | (3.22 | )% | |||||||||||

Cost of revenues decreased by $380,850, or 3.22%, to $11,464,175 for the six months ended March 31, 2020 from $11,845,025 for the same period of last year.

Cost of revenues of Shiitake decreased by $595,799 or 8.65%, to $6,289,207 for the six months ended March 31, 2020 from $6,885,006 for the same period of last year. The decrease was primarily attributable to the decrease in sales volume from 662 tons for the six months ended March 31, 2019 to 591 tons for the six months ended March 31, 2020, which resulted in a decrease of $744,505 in cost of revenue of Shiitake. The decrease was partially offset by an increase in average unit cost of Shiitake from $10,400 per ton for the six months ended March 31, 2019 to $10,638 per ton for the six months ended March 31, 2020, which resulted in an increase of $148,706 in cost of revenue of Shiitake. The increase in average unit cost was caused by allowance for inventory reserve, due to the stay-at-home order and travel restriction imposed by the Chinese government resulted from the COVID-19 pandemic. Therefore, certain Shiitake was not sold as planned and was aged near or over 18 months, and full allowance was made for these Shiitake in the amount of $223,037.

Cost of revenue of Mu Er increased by $509,995 or 11.87% to $4,805,731 for the six months ended March 31, 2020 from $4,295,736 for the same period of last year. The increase was primarily attributable to the increase in sales volume from 419 tons for the six months ended March 31, 2019 to 476 tons for the six months ended March 31, 2020, which resulted in an increase of $581,317 in cost of revenue of Mu Er. The increase was partially offset by a decrease in average unit cost of Mu Er from $10,252 per ton for the six months ended March 31, 2019 to $10,093 per ton for the six months ended March 31, 2020, which resulted in a decrease of $71,322 in cost of revenue of Mu Er.

Cost of revenue of other edible fungi and agricultural products decreased by $295,046, or 44.42%, to $369,237 for the six months ended March 31, 2020 from $664,283 for the same period of last year. The decrease was primarily attributable to the decrease in sales volume from 28 tons for the six months ended March 31, 2019 to 18 tons for the six months ended March 31, 2020, which resulted in a decrease of $223,239 in cost of revenue of other edible fungi and agricultural products. Further, the decrease was attributable to the decrease in average unit cost of other edible fungi and agricultural products from $23,724 per ton for the six months ended March 31, 2019 to $20,597 per ton for the six months ended March 31, 2020, which resulted in a decrease of $71,808 in cost of revenue of other edible fungi and agricultural products.

| 12 |

Gross Profit

The following table sets forth the breakdown of the Company’s gross profit for the six months ended March 31, 2020 and 2019, respectively:

| Six Months Ended March 31, | Variance | |||||||||||||||||||||||

| 2020 | % | 2019 | % | Amount | % | |||||||||||||||||||

| Shiitake | $ | 1,056,967 | 49.94 | % | $ | 1,461,338 | 57.46 | % | $ | (404,371 | ) | (27.67) | % | |||||||||||

| Mu Er | 957,020 | 45.21 | % | 871,678 | 34.28 | % | 85,342 | 9.79 | % | |||||||||||||||

| Other edible fungi and other agricultural products | 102,620 | 4.85 | % | 210,146 | 8.26 | % | (107,526 | ) | (51.17) | % | ||||||||||||||

| Total | $ | 2,116,607 | 100.00 | % | $ | 2,543,162 | 100.00 | % | $ | (426,555 | ) | (16.77) | % | |||||||||||

Overall gross profit decreased by $426,555 or 16.77%, to $2,116,607 for the six months ended March 31, 2020 from $2,543,162 for the same period of fiscal 2019. Gross profit from sales of Shiitake decreased by $404,371 or 27.67, to $1,056,967 for the six months ended March 31, 2020 from $1,461,338 for the same period of last year. Gross profit from sales of Mu Er increased by $85,342 or 9.79% to $957,020 for the six months ended March 31, 2020 from $871,678 for the same period of last year. Gross profit from sales of other edible fungi and agricultural products decreased by $107,526 or 51.17%, to $102,620 for the six months ended March 31, 2020 from $210,146 for the same period of last year. The decreased gross profit was caused by decreased sales for the six months ended March 31, 2020, as compared to the prior period, and a one-time inventory allowance of approximately $0.2 million for the six months ended March 31, 2020.

Overall gross margin decreased by 2.09 percentage points to 15.59% for the six months ended March 31, 2020 from 17.68% for the same period of last year. Overall average unit margin decrease from $2,293 for the six months ended March 31, 2019 to $1,950 for the six months ended March 31, 2020. The decrease in overall gross margin was caused by the allowance for inventory reserve, as mentioned above.

Selling and Distribution Expenses

Selling and distribution expenses decreased by $138,831, or 49.37%, to $142,382 for the six months ended March 31, 2020 from $281,213 for the same period of last year. The decrease was primarily due to a decrease of $35,000 in shipping expenses caused by the decrease in sales volume for the six months ended March 31, 2020, as compared to the same period of last year. Further, the decrease was due to a decrease of $100,000 in advertising and marketing expenses as the Company had already spent on the promotion for the Company’s online platforms last year.

General and Administrative Expenses

General and administrative expenses decreased by $48,332, or 5.51%, to $828,414 for the six months ended March 31, 2020 from $876,746 for the same period of last year. The decrease was primarily attributable to the reduction of headcounts which reduced salaries and related expenses.

Interest Expense

Interest expense was $1,290,039 for the six months ended March 31, 2020, as compared to $1,527,302 for the same period of last year. The decrease in interest expense was primarily attributable to the decreased amortization of debt issuance costs and decreased interest expense incurred for the convertible notes during the six months ended March 31, 2020.

Provision for Income Taxes

For the six months ended March 31, 2020 and 2019, our income tax expense was $24,144 and $27,860, respectively. Overall, the Company is in a loss position, the tax expense was primarily attributable to certain PRC entities that have taxable income from operations, the loss position was primarily incurred by overseas entities as a result of interest expenses of convertible notes.

| 13 |

A total net income of $1.69 million and $1.5 million was exempt from income tax for the six months ended March 31, 2020 and 2019, respectively. The aggregate amount of our tax holiday was approximately $0.42 million and $0.37 million for the six months ended March 31, 2020 and 2019, respectively. From April 1, 2020 to December 31, 2020, we expect to enjoy the tax exemption for 95% of our taxable income. The summary is below:

| Exempted Net Income | Tax holiday | ||||

| October 1, 2015 – September 30, 2016 | RMB7.8 million (approximately $1.2 million) |

RMB1.87 million (approximately $0.28 million) | |||

| October 1, 2016 – September 30, 2017 | RMB23.71 million (approximately $3.5 million) |

RMB5.9 million (approximately $0.87 million) | |||

| October 1, 2017 – September 30, 2018 | RMB25.38 million (approximately $3.9 million) |

RMB6.3 million (approximately $0.97 million) | |||

| October 1, 2018 – September 30, 2019 | RMB24.72 million (approximately $3.6 million) |

RMB6.2 million (approximately $0.90 million) | |||

| October 1, 2019 – March 31, 2020 | RMB11.82 million (approximately $1.69 million) |

RMB2.9 million (approximately $0.42 million) |

Net Loss

As a result of the factors described above, our net loss was $63,807 for the six months ended March 31, 2020, a decrease of $107,284 from net loss of $171,091 for the same period of fiscal year 2019.

Liquidity and Capital Resources

We are a holding company incorporated in the Cayman Islands. We may need dividends and other distributions on equity from our PRC subsidiaries to satisfy our liquidity requirements. Current PRC regulations permit our PRC subsidiaries to pay dividends to us only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, our PRC subsidiaries are required to set aside at least 10% of their respective accumulated profits each year, if any, to fund certain reserve funds until the total amount set aside reaches 50% of their respective registered capital. Our PRC subsidiaries may also allocate a portion of its after-tax profits based on PRC accounting standards to employee welfare and bonus funds at their discretion. These reserves are not distributable as cash dividends.

Further, although instruments governing the current debts incurred by our PRC subsidiaries do not have restrictions on their abilities to pay dividends or make other payments to us, the lender may impose such restriction in the future. As a result, our ability to distribute dividends largely depends on earnings from our PRC subsidiaries and their ability to pay dividends out of earnings. Management believes that our current cash, cash flows provided by operating activities, and access to loans will be sufficient to meet our working capital needs for at least the next 12 months. We intend to continue to carefully execute our growth plans and manage market risk.

| 14 |

As of March 31, 2020 and September 30, 2019, we had cash in the amount of $5,100,133 and $135,125, respectively. Total current assets as of March 31, 2020 amounted to $31,005,440, an increase of $1,300,412 compared to $29,705,028 at September 30, 2019. The increase in total current assets at March 31, 2020 compared to September 30, 2019 was mainly due to the increase in cash. Current liabilities amounted to $ 6,702,902 at March 31, 2020, in comparison to $8,145,080 at September 30, 2018. This decrease of current liabilities was mainly attributable to the decrease in convertible notes payable.

Although management believes that the cash generated from operations will be sufficient to meet our normal working capital needs for at least the next twelve months, our ability to repay our current obligations will depend on the future realization of our current assets. Management has considered the historical experience, the economy, trends in the agricultural product industry, the expected collectability of accounts receivable and the realization of the inventories as of March 31, 2020. Based on the above considerations, management is of the opinion that we have sufficient funds to meet our working capital requirements and debt obligations as they become due. However, there is no assurance that management will be successful in our plan. There are a number of factors that could potentially arise which might result in shortfalls to what is anticipated, such as the demand for our products, economic conditions, the competition in the industry, and our bank and suppliers being able to provide continued support. If the future cash flow from operations and other capital resources is insufficient to fund our liquidity needs, we may be forced to obtain additional debt or equity capital, or refinance all or a portion of our debt.

Indebtedness. As of March 31, 2020, we have $1,834,300 of short-term bank loans and $1,879,688 convertible notes payable. Beside these loans and convertible notes payable, we did not have any finance leases or purchase commitments, guarantees or other material contingent liabilities.

Off-Balance Sheet Arrangements. We have not entered into any financial guarantees or other commitments to guarantee the payment obligations of any third parties. In addition, we have not entered into any derivative contracts that are indexed to our own shares and classified as shareholders’ equity, or that are not reflected in our consolidated financial statements. Furthermore, we do not have any retained or contingent interest in assets transferred to an unconsolidated entity that serves as credit, liquidity or market risk support to such entity. Moreover, we do not have any variable interest in any unconsolidated entity that we provide financing, liquidity, market risk or credit support to or engages in hedging or research and development services with us.

Capital Resources. The primary drivers and material factors impacting our liquidity and capital resources include our ability to generate sufficient cash flows from our operations and renew commercial bank loans, as well as proceeds from equity and debt financing, to ensure our future growth and expansion plans. On February 21, 2018, we announced the closing of our initial public offering of 1,680,000 Ordinary Shares at a price to the public of $4.00 per share for a total of $6,720,000 in gross proceeds. As of March 31, 2020, we had total assets of $31.7 million, which includes cash of $5.1 million, accounts receivable of $9.0 million, advance to suppliers of $11.7 million, due from related parties of $3.6 million and inventory of $0.7 million, working capital of $24.3 million, and total equity of $24.8 million.

Working Capital. Total working capital as of March 31, 2020 amounted to $24,302,538, compared to $21,559,948 as of September 30, 2019.

Capital Needs. Our capital needs include our daily working capital needs and capital needs to finance the development of our business. We have established effective collection procedures of our accounts receivable, and have been able to realize or receive the refund of the advances to suppliers in the past. Our management believes that income generated from our current operations can satisfy our daily working capital needs over the next 12 months. We may also raise additional capital through public offerings or private placements to finance our business development and to consummate any merger or acquisition, if necessary.

| 15 |

Cash Flows

The following table provides detailed information about our net cash flows for the six months ended March 31, 2020 and 2019:

|

For the six months ended March 31, |

||||||||

| 2020 | 2019 | |||||||

| Net provided by (used in) operating activities | $ | 5,686,467 | $ | (5,916,038 | ) | |||

| Net cash used in investing activities | (246,726 | ) | (104,110 | ) | ||||

| Net cash (used in) provided by financing activities | (453,757 | ) | 6,707,429 | |||||

| Effect of exchange rate changes on cash and restricted cash | (39,666 | ) | 225,773 | |||||

| Net increase in cash and restricted cash | 4,946,318 | 913,054 | ||||||

| Cash and restricted cash, beginning of period | 753,815 | 5,525,165 | ||||||

| Cash and restricted cash, end of period | $ | 5,700,133 | $ | 6,438,219 | ||||

Operating Activities

Net cash provided by operating activities was $5,686,467 for the six months ended March 31, 2020. This was an increase of $11,602,505 compared to net cash used in operating activities of $5,916,038 for the six months ended March 31, 2019. The increase in net cash provided by operating activities was primarily attributable to an increase of $4,944,245 in accounts receivable and an increase of $2,428,891 in advances to suppliers.

Investing Activities

For the six months ended March 31, 2020, net cash used in investing activities amounted to $246,726 as compared to net cash used in investing activities of $104,110 for the same period of 2019. The increase of $142,616 was primarily due to an increase of $158,242 in purchase of property, plant and equipment.

Financing Activities

Net cash used in financing activities amounted to $453,757 for the six months ended March 31, 2020, as compared to net cash provided by financing activities of $6,707,429 for the same period in 2019. The decrease of $7,161,186 in net cash provided by financing activities was mainly due to an increase of $7,500,000 in gross proceeds from the issuance of convertible notes in prior period and a decrease of $716,318 in direct costs disbursed from Initial Public Offering proceeds in prior period.

Commitments and Contractual Obligations

The following table presents the Company’s material contractual obligations as of March 31, 2020:

| Less than 1 | More than 5 | |||||||||||||||||||

| Contractual Obligations | Total | year | 1-3 years | 3-5 years | years | |||||||||||||||

| Short-term bank loans | $ | 1,834,300 | $ | 1,834,300 | $ | - | $ | - | $ | - | ||||||||||

| Operating lease obligations | 379,277 | 56,892 | 113,784 | 113,784 | 94,817 | |||||||||||||||

| Total | $ | 2,213,577 | $ | 1,891,192 | $ | 113,784 | $ | 113,784 | $ | 94,817 | ||||||||||

| 16 |