UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-K

ANNUAL FINANCIAL REPORT PURSUANT TO REGULATION A

For the fiscal year ended December 31, 2018

MOGULREIT II, Inc.

(Exact name of issuer as specified in its charter)

Commission File Number: 024-10713

|

Maryland |

|

81-5263630 |

|

(State or other jurisdiction |

|

(I.R.S. Employer |

|

of incorporation or organization) |

|

Identification No.) |

|

|

|

|

|

10780 Santa Monica Blvd, Suite 140 |

|

|

|

Los Angeles, CA |

|

90025 |

|

(Full mailing address of |

|

(Zip code) |

|

principal executive offices) |

|

|

(877) 781-7153

(Issuer’s telephone number, including area code)

Common Stock, par value $0.01 per share

(Title of each class of securities issued pursuant to Regulation A)

Part II.

STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

We make statements in this Annual Report on Form 1-K (the “Annual Report”) that are forward-looking statements within the meaning of the federal securities laws. The words “believe,” “estimate,” “expect,” “anticipate,” “intend,” “plan,” “seek,” “may,” “continue,” “could,” “might,” “potential,” “predict,” “should,” “will,” “would,” and similar expressions or statements regarding future periods or the negative of these terms are intended to identify forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any predictions of future results, performance or achievements that we express or imply in this Annual Report or in the information incorporated by reference into this Annual Report.

The forward-looking statements included in this Annual Report are based upon our current expectations, plans, estimates, assumptions and beliefs that involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements. Factors which could have a material adverse effect on our operations and future prospects include, but are not limited to:

|

· |

our ability to effectively deploy the proceeds raised in our offering of shares of our common stock pursuant to Regulation A promulgated under the Securities Act of 1933, as amended (the “Securities Act”); |

|

· |

our ability to attract and retain members to the Realty Mogul Platform; |

|

· |

risks associated with breaches of our data security; |

|

· |

changes in economic conditions generally and the real estate and securities markets specifically; |

|

· |

expected rates of return provided to investors; |

|

· |

the ability of Realty Mogul Commercial Capital, Co. (“RMCC”), which in its loan servicing capacity, may be referred to as an RM Lender, and which in its loan originating capacity, may be referred to as an RM Originator, to source, originate and service our loans and other assets, and the quality and performance of these assets; |

|

· |

our ability to hire and retain competent individuals who will provide services to us and appropriately staff our operations; |

|

· |

legislative or regulatory changes impacting our business or our assets (including changes to the laws and regulation governing the taxation of real estate investment trusts (“REITs”) and our ability to offer our shares of common stock to the public pursuant to Regulation A and related exemption from state securities law registration requirements for “covered securities,” as defined in Section 18 of the Securities Act; |

|

· |

changes in business conditions and the market value of our assets, including changes in interest rates, prepayment risk, operator or borrower defaults or bankruptcy, and generally the increased risk of loss if our investments fail to perform as expected; |

|

· |

our ability to implement effective conflicts of interest policies and procedures among the various real estate investment opportunities sponsored by Realty Mogul, Co.; |

|

· |

our ability to access sources of liquidity when we have the need to fund repurchases of shares of our common stock in excess of the proceeds from the sales of shares of our common stock in our continuous offering and the consequential risk that we may not have the resources to satisfy share repurchase requests; |

1

|

· |

our failure to qualify and maintain our status as a REIT for U.S. federal income tax purposes; |

|

· |

our compliance with applicable local, state and federal laws, including the Investment Advisers Act of 1940, as amended, (the “Advisers Act”), the Investment Company Act of 1940, as amended (the “Investment Company Act”) and other laws; and |

|

· |

changes to U.S. generally accepted accounting principles (“GAAP”). |

Any of the assumptions underlying forward-looking statements could be inaccurate. You are cautioned not to place undue reliance on any forward-looking statements included in this Annual Report. All forward-looking statements are made as of the date of this Annual Report and the risk that actual results will differ materially from the expectations expressed in this Annual Report will increase with the passage of time. Except as otherwise required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements after the date of this Annual Report, whether as a result of new information, future events, changed circumstances or any other reason. In light of the significant uncertainties inherent in the forward-looking statements included in this Annual Report, the inclusion of such forward-looking statements should not be regarded as a representation by us or any other person that the objectives and plans set forth in this Annual Report will be achieved.

2

Item 1. Business

The Company

MogulREIT II, Inc. is a Maryland corporation formed on January 13, 2017 to own and manage a diversified portfolio of preferred equity and joint venture equity investments in multifamily properties located in target markets throughout the United States. The use of the terms “MogulREIT II,” the “Company,” “we,”, “us,” or “our” in this Annual Report refer to MogulREIT II, Inc., unless the context indicates otherwise. We have elected to be taxed as a REIT under the Internal Revenue Code of 1986, as amended (the “Code”), commencing with our taxable year ended December 31, 2017.

We operate under the direction of the board of directors, the members of which are accountable to us and our stockholders as fiduciaries. The current board members are Jilliene Helman, Flynann Janisse and Louis W. Weeks III. Ms. Janisse and Mr. Weeks are independent directors. We are externally managed by RM Adviser, LLC (“Manager”), which is an affiliate of the Company’s sponsor, RM Sponsor, LLC (“Sponsor”). Our Manager and our Sponsor are each wholly-owned subsidiaries of Realty Mogul, Co. Our Manager manages our day-to-day operations. Our Manager also provides asset management, investor relations and other administrative services on our behalf with the goal of maximizing our operating cash flow and preserving our capital.

On August 23, 2017, our offering of shares of common stock (the “Offering”) was qualified by the Securities and Exchange Commission (“SEC”), and we commenced operations on September 18, 2017. We are offering up to $50,000,000 in shares of our common stock including any shares of our common stock that may be sold pursuant to our distribution reinvestment plan. As of December 31, 2018, we had issued 1,279,398 shares of our common stock in the Offering for gross offering proceeds of $12,793,975. We expect to continue to offer shares of our common stock in the Offering until we raise the maximum amount being offered, unless the Offering is terminated by our board of directors at an earlier time. See Item 2 “Management’s Discussion and Analysis of Financial Condition and Results of Operation—Overview” for more information concerning the current status of the Offering.

We have used, and intend to continue using substantially all of the net proceeds from the Offering to invest in and manage a diversified portfolio of preferred equity and joint venture equity investments in multifamily properties located in target markets throughout the Unites States.

As of December 31, 2018, our portfolio was comprised of approximately $77,000,000 in real estate investments that, in the opinion of our Manager, meets our investment objectives. We intend to make preferred equity and joint venture equity investments in apartment communities that have demonstrated consistently high occupancy and income levels across market cycles as well as multifamily properties that offer value added opportunities with appropriate risk-adjusted returns and opportunity for value appreciation.

Investment Strategy

We have used and intend to continue using substantially all of the proceeds of the Offering to make preferred equity and joint venture equity investments in multifamily properties, including independent senior-living communities, located in target markets throughout the United States. We intend to invest in apartment communities that have demonstrated consistently high occupancy and income levels across market cycles as well as multifamily properties that offer value added opportunities with appropriate risk-adjusted returns and opportunity for value appreciation. We will invest in the following types of assets: equity or preferred equity interests in companies whose primary business is to own and operate one or more specified multifamily projects.

We believe that the near and intermediate-term market for investment in multifamily communities is compelling from a risk-return perspective. Millennials and Baby Boomers, the two largest demographic groups comprising roughly half of the total population in the United States, are increasingly choosing to live in a variety of rental housing. The Company plans to provide rental housing for these multi-generational groups as they age through their housing needs. With home ownership is at its lowest rate since 1967 combined with the demographic and economic factors that favor renting, we believe that a multifamily investment policy targeted to provide rental housing options is appropriately timed for this market. We believe that our investment strategy, combined with the experience and expertise of our Manager’s management team, will provide opportunities to invest in assets with attractive risk-adjusted returns.

3

Our Manager, through its affiliates, intends to structure, underwrite and originate many of the properties in which we will invest as this provides for the best opportunity to control our borrower and partner relationships and optimize the terms of our investments. Our affiliates’ underwriting process, which our management team has successfully developed over their extensive real estate careers in a variety of market conditions and implemented at Realty Mogul, Co., will involve comprehensive financial, structural, operational and legal due diligence of our borrowers and partners in order to optimize pricing and structuring and mitigate risk. We believe the current and future market environment provides a wide range of opportunities to generate compelling investments with strong risk-return profiles for our stockholders.

Investment Objectives

Our primary investment objectives are to realize capital appreciation in the value of our investments over the long term and to pay attractive and stable cash distributions to stockholders.

Competition

There are numerous REITs with asset acquisition objectives similar to ours, and others may be organized in the future, which may increase competition for the investments suitable for us. Competitive variables include market presence and visibility, size of investments offered and underwriting standards. To the extent that a competitor is willing to risk larger amounts of capital in a particular transaction or to employ more liberal underwriting standards when evaluating potential investments than we are, our investment volume and profit margins for our investment portfolio could be impacted. Our competitors also may be willing to accept lower returns on their investments and may succeed in buying the assets that we have targeted for acquisition. Although we believe that we are well positioned to compete effectively in each facet of our business, there is enormous competition in our market sector and there can be no assurance that we will compete effectively or that we will not encounter increased competition in the future that could limit our ability to conduct our business effectively.

Risk Factors

We face risks and uncertainties that could affect us and our business as well as the real estate industry generally. These risks are outlined under the heading “Risk Factors” contained in our Offering Circular dated August 24, 2018, and qualified by the SEC on August 24, 2018, as supplemented (the “Offering Circular”), which may be accessed on the SEC’s EDGAR (Electronic Data Gathering, Analysis, and Retrieval) system and may be updated from time to time by our future filings under Regulation A. In addition, new risks may emerge at any time, and we cannot predict such risks or estimate the extent to which they may affect our financial performance. These risks could result in a decrease in the value of shares of our common stock.

4

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

MogulREIT II, Inc. is a Maryland corporation formed on January 13, 2017 to own and manage a diversified portfolio of preferred equity and joint venture equity investments in multifamily properties located in target markets throughout the United States. We are externally managed by our Manager, which is an affiliate of our Sponsor. Both our Manager and our Sponsor are wholly-owned subsidiaries of Realty Mogul, Co. Although our Manager manages our day-to-day operations, we operate under the direction of our board of directors, majority of whom are independent directors. Our affiliate, RM Technologies, LLC operates an online investment platform, www.realtymogul.com. With the exception of offering our shares through select RIA partners, our shares are being offered in the Offering exclusively through this platform. We commenced operations on September 18, 2017.

Pursuant to the Offering, we are offering and will continue to offer up to $50,000,000 in shares of our common stock, including any shares that may be sold pursuant to our distribution reinvestment plan. As of April 26, 2019, we had raised total gross offering proceeds of approximately $16,389,117 from settled subscriptions and issued an aggregate of 1,638,911 shares of our common stock, with additional subscriptions for an aggregate of 10,550 shares of our common stock, representing additional potential gross offering proceeds of approximately $105,500, that have been accepted by us but not settled. Assuming the settlement for all subscriptions received, as of April 26, 2019, approximately $33,505,382 in shares of our common stock remained available for sale to the public pursuant to the Offering. We have used and intend to continue using substantially all of the net proceeds from the Offering (after paying or reimbursing organization and offering expenses) to invest in and manage a diverse portfolio of preferred equity and joint venture equity investments in multifamily properties located in target markets throughout the United States.

Our Investments

During the year ended December 31, 2018, we entered into the following investments.

Acquisition of Plano Multifamily Portfolio–Plano, TX

On January 9, 2018, we acquired a $1,000,000 joint-venture limited partnership equity investment related to the acquisition and renovation of two garden-style apartment communities in Plano, Texas. We acquired the investment for a purchase price of $1,000,000, which was funded with a loan from Realty Mogul Commercial Capital, Co.

Acquisition of Tuscany at Westover Hills–San Antonio, TX

On January 31, 2018, we acquired a $1,000,000 joint-venture limited partnership equity investment related to the acquisition of a Class B apartment complex in San Antonio, Texas. We acquired the investment for a purchase price of $1,000,000, which was funded with a loan from Realty Mogul Commercial Capital, Co.

Acquisition of Villas del Mar–Fort Worth, TX

On February 28, 2018, we acquired a $1,000,000 joint-venture limited partnership equity investment related to the acquisition of an apartment complex in Fort Worth, Texas. We acquired the investment for a purchase price of $1,000,000, which was funded with a loan from Realty Mogul Commercial Capital, Co.

Acquisition of Ashland Apartments–Chicago, IL

On June 22, 2018, we acquired a $1,440,000 preferred equity investment related to the acquisition of an apartment complex in Chicago, Illinois. We acquired the investment for a purchase price of $1,440,000, which was funded with a loan from Realty Mogul Commercial Capital, Co.

Acquisition of Avon Place Apartments–Avon, CT

On November 1, 2018, we acquired a $3,500,000 joint-venture limited partnership equity investment related to the acquisition and renovation of an apartment complex in Avon, Connecticut. The investment was anticipated to be funded in two tranches – an initial investment of $2,634,000 (“Avon Initial Investment”), which was funded at acquisition and an

5

additional investment of $866,000 (the “Avon Additional Investment”), which will be funded within 60 days’ notice from the real estate company. The Avon Initial Investment was made on November 1, 2018 and was funded with a loan from Realty Mogul Commercial Capital, Co. On December 26, 2018, $162,590 of the Avon Additional Investment amount was funded.

See the section entitled “Recent Developments” below for a discussion on distributions declared subsequent to December 31, 2018.

Distributions

Our board of directors has declared and paid, and we expect that our board of directors will continue to declare and pay, distributions quarterly in arrears. Stockholders who are record holders with respect to declared distributions will be entitled to such distributions until such time as the stockholders have had their shares repurchased by us. Although our goal is to fund the payment of distributions solely from cash flow from operations, we may pay distributions from other sources, including the net proceeds of the Offering, borrowings in anticipation of future operating cash flow and the issuance of additional securities, and we have no limit on the amounts we may pay from such other sources. In addition, on December 15, 2017, our board of directors authorized a special daily cash distribution of $0.0057682365 per share of the Company’s common stock to stockholders of record as of the close of business on each day of the period commencing on December 17, 2017 and ending on December 31, 2017 (the “Special Distribution Period”), which was payable to stockholders of record as of the close of business on each day of the Special Distribution Period.

Our board of directors has declared quarterly distributions for stockholders of record as of the close of business on the last day of each quarter, as shown in the table below:

|

Distribution Period for Daily Record Dates |

Date of Authorization |

Payment Date (1) |

Cash Distribution Amount per Share of Common Stock |

Annualized Yield |

|

12/17/2017 – 12/31/2017 |

12/15/2017 |

1/15/2018 |

$0.0057682365 |

2.1%(2) |

|

1/30/2018 – 3/31/2018 |

12/22/2017 |

4/13/2018 |

$0.0012328767 |

4.5%(2) |

|

4/1/208 – 6/30/2018 |

3/21/2018 |

7/16/2018 |

$0.0012328767 |

4.5%(2) |

|

7/1/2018 – 9/30/2018 |

6/20/2018 |

10/15/2018 |

$0.0012328767 |

4.5%(2) |

|

10/1/2018 – 12/31/2018 |

9/18/2018 |

1/15/2019 |

$0.0012328767 |

4.5%(2) |

(1) Dates presented are the dates on which the distributions were scheduled to be distributed; actual distribution dates may vary.

(2) Annualized yield represents the annualized yield amount of each distribution calculated on an annualized basis at the then current rate, assuming a $10.00 per share purchase price.

During the years ended December 31, 2018 and December 31, 2017, we paid distributions of approximately $302,258 and $0, respectively, including approximately $206,273 and $0, respectively, through the issuance of shares pursuant to the distribution reinvestment plan. Our distributions for the year ended December 31, 2018, including shares issued pursuant to the distribution reinvestment plan, were funded by cash flows from operations. Our distributions for the period ended December 31, 2017, including shares issued pursuant to the distribution reinvestment plan, were funded by cash flows from financing activities.

See the section entitled “Recent Developments” below for a discussion on distributions declared subsequent to December 31, 2018.

Share Repurchase Program

We have adopted a share repurchase program in order to provide our stockholders with some liquidity that may enable them to sell their shares of common stock to us in limited circumstances. The Board may, in its sole discretion, amend, suspend, or terminate the share repurchase program at any time. Reasons we may amend, suspend or terminate the share repurchase program include (i) to protect our operations and our remaining stockholders, (ii) to prevent an undue burden on our liquidity, (iii) to preserve our status as a REIT, (iv) following any material decrease in our NAV, or (v) for any other reason.

During the year ended December 31, 2018, we received repurchase requests for 250 shares of common stock, and we repurchased 250 of such shares, or 100%. During the period from January 13, 2017 (inception) to December 31, 2017, we did not receive any repurchase requests. A valid repurchase request is one that complies with the applicable

6

requirements and guidelines of our current share repurchase program. The share repurchases were funded with cash flows from operations.

Sources of Operating Revenue and Cash Flow

Our revenue is mainly generated from rental income and tenant reimbursements from our investments.

Profitability and Performance Metrics

We calculate funds from operations (“FFO”) and adjusted funds from operations (“AFFO”) to evaluate the profitability and performance of our business. See “─ Non-GAAP Financial Measures” below for a description of these metrics. Our investing and management activities related to commercial real estate are all considered a single reportable business segment for financial reporting purposes. All of the investments we have made to date have been in domestic commercial real estate assets with similar economic characteristics, and we evaluate the performance of all of our investments using similar criteria.

Market Outlook and Recent Trends

|

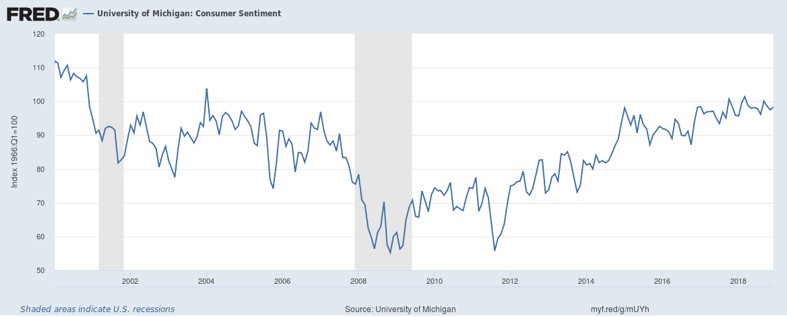

On a macroeconomic level, we still see strong economic indicators for commercial real estate. Though we believe the U.S. economy is in the late stages of its recovery, we believe that there is still further growth in the near to intermediate-term. In November 2017, consumer confidence reached its highest level in 17 years and has remained at historically high levels through November 2018. The index has remained over 90 for almost two years. According to the University of Michigan, who created the survey, the last time the index has remained at these levels for this period of time was the 1997-2000 timeframe. While we believe consumer confidence trails the market rather than precedes it, we believe that positive consumer confidence bodes well for near-term investing.

|

|

|

Despite the extreme volatility in Q4 2018, equities are still at high historic levels, evidenced by the S&P 500 Index and the Dow Jones Industrial Average. The fourth quarter 2018 was challenging for the S&P 500, and the index experienced dramatic losses. As of December 31, 2018, the S&P 500 index was down almost 7% for the year. The volatility in the equities market may be largely the result of investor fear that we are nearing the peak of a market cycle. |

|

7

|

Job growth has remained strong, and unemployment rates are at historically low levels at 3.9% as of December 2018. We believe that this is one of the most important macroeconomic indicators for real estate and is one of the foundations of our positive near-term outlook. |

|

|

|

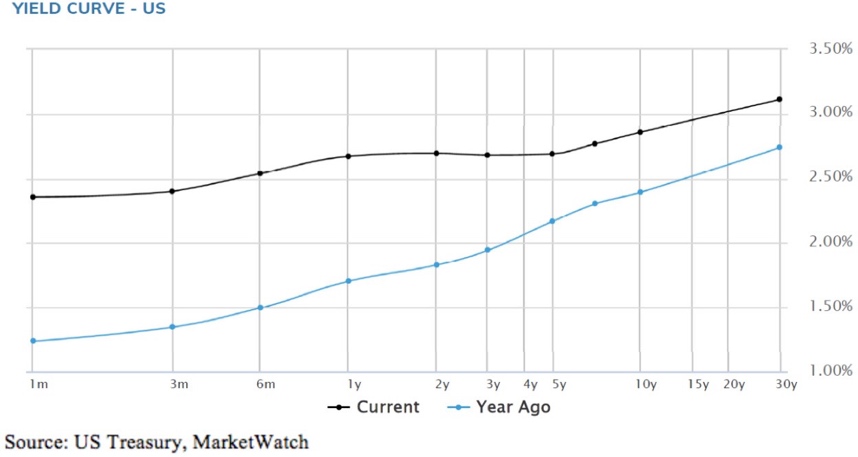

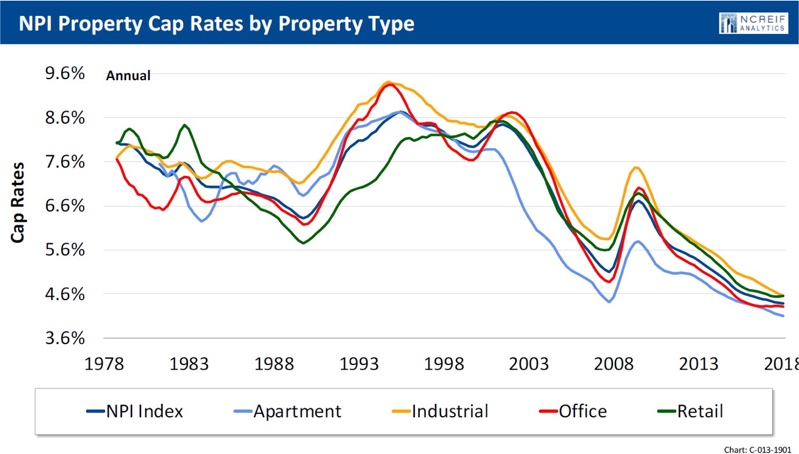

After years of predictions of substantial movement in interest rates, the Federal Reserve finally viewed the economy stable enough to begin to raise interest rates in the past 18 months. The corresponding chart shows movement in the yield curve over the past 12 months. In a rising interest rate environment, one might expect to see cap rates rise with interest rates as valuations decrease due to the increased financing costs; however, as interest rates have risen over the past two years, cap rates have remained at historically low levels. According to CBRE’s Cap Rate Survey for H2 2018, although there was a slight uptick from Q2 2018 to Q4 2018, cap rates were broadly unchanged. |

|

|

Though current pricing indicates that we are in a seller’s market overall, we believe that our prudent underwriting and flexibility to make investments in any asset class, any geography and any tier in the capital stack leaves us poised to take advantage of the near and intermediate-term opportunities.

We believe that the following market conditions, which are by-products of the economy, credit market and regulatory environment should create a favorable investment environment.

8

|

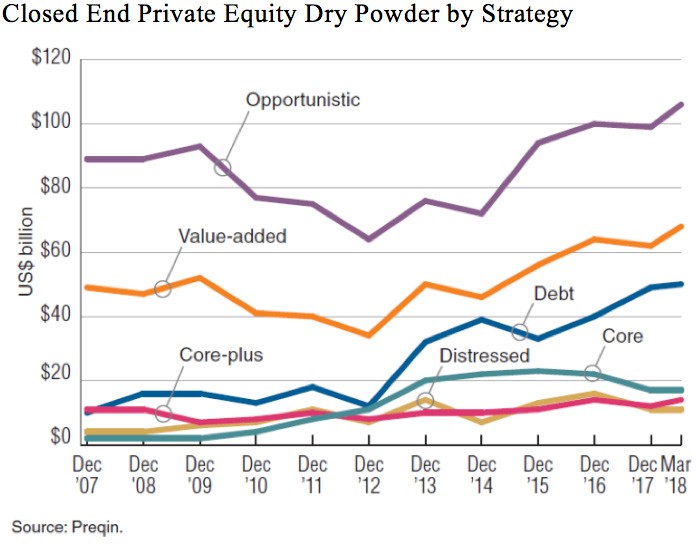

Concentration of fundraising among the largest private equity funds has increased the difficulty for real estate companies to raise equity or mezzanine investments of less than $10,000,000. One of the responses to the 2008 recession, according to Prequin Global Private Equity Report, has been growth in the average size of investment funds, whereby large investors have been investing more of their capital with managers that have extensive track records, and are therefore, by nature, raising much larger funds. In 2014, funds of a size equivalent to $1.5 billion or more accounted for 58% of all private equity capital raised while first-time managers only accounted for 7% of capital raised. The average fund size hit a record of greater than $600,000,000. Larger funds consequently focus on larger deals in order to deploy their capital fully and effectively.

Further, the changing economic landscape may provide dislocation in market and create opportunities in non-core sections of the real estate markets. After years of anticipation of future rises in interest rates, the Federal Reserve has finally felt comfortable with the economy to begin raising rates. For the most part, these rises were already priced into commercial real estate valuations. However, the rising interest rate environment creates uncertainty which can lead to opportunity, especially in the segments of the market which are not flush with increasing levels of institutional capital. |

|

9

|

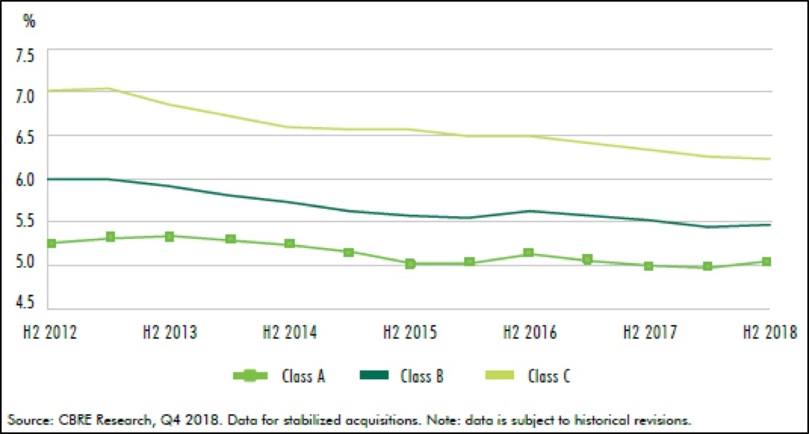

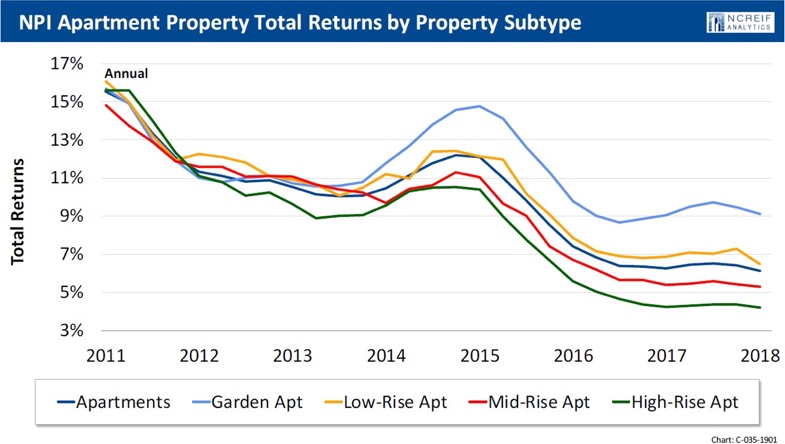

More specifically, for non-core, suburban multifamily, as depicted in the chart to the right, cap rates have decreased steadily since 2012. Similarly, per NCREIF’s Year-End Indices Review, in 2018, apartment buildings had the lowest cap rates of all asset classes. We believe that this trend can be attributed in part to the market viewing multifamily as a defensive asset class, especially in the context of what is now the longest economic expansion in the history of the United States. Tenant risk for multifamily buildings, as opposed to retail and office buildings, is typically spread amongst a larger tenant base; thus, if one tenant vacates, a multifamily property generally can more easily absorb such loss. According to NCREIF’s 2018 report, garden-style apartments had the highest total returns across the multifamily asset class while high-rise buildings performed the worst. |

|

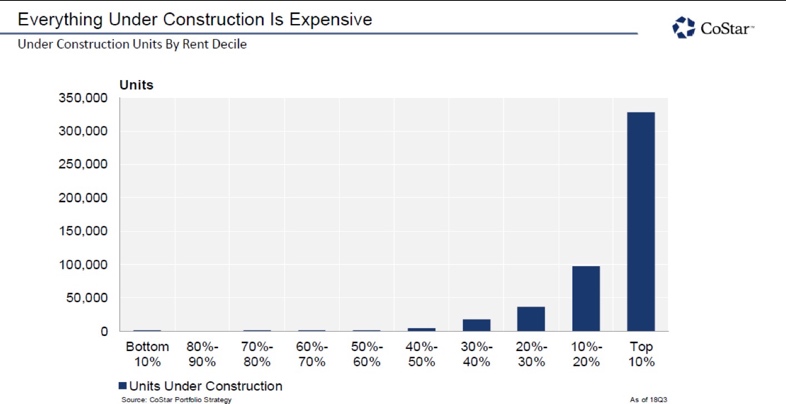

|

Since construction related to garden-style multifamily projects is typically conducted on a much smaller scale compared to mid and high-rise buildings, the low initial capital outlay may help increase overall garden-style property returns. Furthermore, garden properties are typically located in suburban areas, and the smaller suburban markets may inhibit gluts of supply, thus driving rent growth. According to CoStar, as of Q3 2018, over 300,000 units that are under construction are being built in areas that fall into the highest rent bracket. Again, this trend may explain why suburban, workforce housing has experienced high returns as most of the new supply has been in the top of the market. |

|

10

|

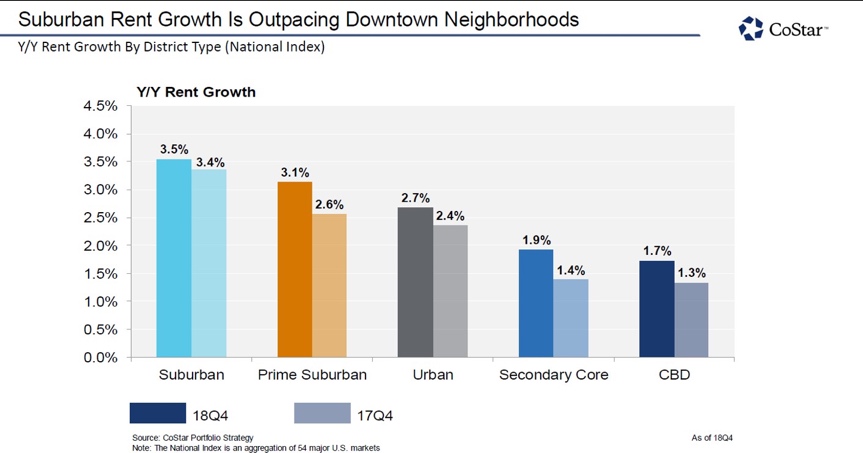

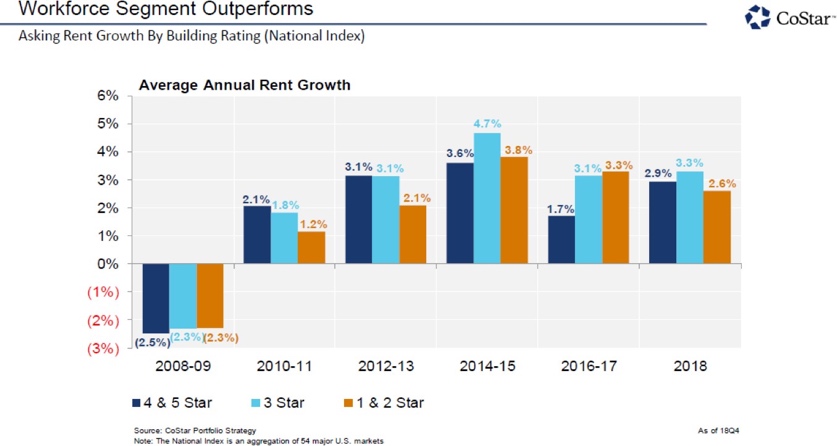

As one might expect from the above insights, according to CoStar, in Q4 2018, suburban multifamily assets had over double the rent growth as CBD multifamily assets, with the strongest rent growth in Class B product, which is typically affordable, workforce housing. |

|

We believe that the non-core areas of commercial real estate present investors with attractive risk adjusted return opportunities. We are encouraged by the success of suburban, low-rise multifamily product over the past decade. With a population that is trending towards rentals as opposed to home ownership as well as strong rent growth in the suburban multifamily markets due to minimal new construction, we have continued confidence in MogulREIT II’s strategy of acquiring equity investments in this asset class.

Critical Accounting Policies

The preparation of financial statements in accordance with GAAP requires management to use judgment in the application of accounting policies, including making estimates and assumptions. Such judgments are based on our management’s experience, our historical experience, the experience of our Manager’s affiliates, and the industry. We consider these policies critical because we believe that understanding these policies is critical to understanding and evaluating our reported financial results. Additionally, these policies may involve significant management judgments and assumptions, or require estimates about matters that are inherently uncertain. These judgments will affect the reported amounts of assets and liabilities and our disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting periods. With different estimates or assumptions, materially different amounts could be reported in our financial statements. Additionally, other companies may utilize different estimates that may impact the comparability of our results of operations to those of companies in similar businesses.

Accounting for Acquisition of Real Estate

Prior to January 1, 2018, the Company recorded acquired real estate investments that are consolidated as business combinations when the real estate is occupied, at least in part, at acquisition. Costs directly related to the acquisition of such investments have been expensed as incurred. The purchase consideration included cash paid, the fair value of equity

11

or other assets issued, and the fair value of any assumed debt. The Company assessed the fair value of assumed debt based on estimated cash flow projections that utilized appropriate discount rates and available market information. Such inputs were categorized as Level 3 in the fair value hierarchy. The difference between the fair value and the stated principal of assumed debt was amortized using the effective interest method basis over the terms of the respective debt obligation.

The Company allocated the fair value of the purchase consideration to the fair value of land, buildings, site improvements and intangible assets including in-place leases at the acquisition date. The Company estimated the fair value of the assets using market-based, cost-based, and income-based valuation techniques.

Effective January 1, 2018, the Company adopted the provisions of Accounting Standard Update 2017-01, which provides that if substantially all the fair value of the gross assets is concentrated in any individual asset, the acquisition is treated as an asset acquisition as opposed to a business combination. Under an asset acquisition, costs directly related to the acquisition are capitalized as part of the purchase consideration. The fair value of the purchase consideration is then allocated based on the relative fair value of the assets. The estimates of the fair value of the purchase consideration and the fair value of the assets acquired is consistent with the techniques used in a business combination.

Variable Interest Entities and Voting Interest Entities

A variable interest entity (“VIE”) is an entity that lacks one or more of the characteristics of a voting interest entity. A VIE is defined as an entity in which equity investors do not have the characteristics of a controlling financial interest or do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. The determination of whether an entity is a VIE includes consideration of various factors. These factors include review of the formation and design of the entity, its organizational structure including decision-making ability and relevant financial agreements, and analysis of the forecasted cash flows of the entity. We make an initial determination upon acquisition of a VIE, and reassess the initial evaluation of an entity as a VIE upon the occurrence of certain events.

A VIE must be consolidated only by its primary beneficiary, which is defined as the party who, along with its affiliates and agents has both the: (i) power to direct the activities that most significantly impact the VIE’s performance; and (ii) obligation to absorb the losses of the VIE or the right to receive the benefits from the VIE, which could be significant to the VIE. We determine whether we are the primary beneficiary of a VIE by considering various factors, including, but not limited to: which activities most significantly impact the VIE’s economic performance and which party controls such activities; the amount and characteristics of its investment; the obligation or likelihood for us or other interests to provide financial support; consideration of the VIE’s purpose and design, including the risks the VIE was designed to create and pass through to its variable interest holders and the similarity with and significance to the business activities of our interest and the other interests. We reassess our determination of whether we are the primary beneficiary of a VIE each reporting period. Significant judgments related to these determinations include estimates about the future performance of investments held by VIEs and general market conditions. The maximum risk of loss related to our investments is limited to our recorded investment in such entities, if any.

A voting interest entity (“VOE”) is an entity in which equity investors have the characteristics of a controlling financial interest and has sufficient equity at risk to finance its activities. A controlling financial interest exists if limited partners with equity at risk are able to exercise substantive kick-out rights or are able to exercise substantive participation rights. Under the VOE model, generally, only a single limited partner that is able to exercise substantial kick-out rights will consolidate the entity.

As of December 31, 2018 and 2017, the Company held investments in three and zero entities, respectively, which were evaluated under the VIE model and were not consolidated because the Company was not determined to be the primary beneficiary. These investments are carried on the equity method because of the Company’s significant influence.

As of December 31, 2018 and 2017, the Company held investments in three and two entities, respectively, which were evaluated under the VOE model and are consolidated because the Company is able to exercise substantial kick-out rights and substantive participation rights.

12

Commercial Real Estate Debt Investments

Credit Quality Monitoring

The Company’s preferred equity investments that earn interest based on debt-like terms are typically secured by interests in entities that have interests in real estate. The Company evaluates its debt investments at least quarterly and differentiates the relative credit quality principally based on: (i) whether the borrower is currently paying contractual guaranteed preferred equity payments in accordance with its contractual terms; and (ii) whether the Company believes the borrower will be able to perform under its contractual terms in the future, as well as the Company’s expectations as to the ultimate recovery of principal at maturity. The Company considered an investment for which it expects to receive full payment of contractual principal and interest payments as “performing.” As of December 31, 2018, the investment is considered to be performing and no allowance for loan loss has been recorded. In the event that an investment is deemed other than performing, the Company will evaluate the instrument for any required impairment.

Fair Value

Fair value is the exchange price that would be received for an asset or paid to transfer a liability (exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. There are three levels of inputs that may be used to measure fair values:

Level 1 — Quoted prices (unadjusted) for identical assets or liabilities in active markets that the entity has the ability to access as of the measurement date.

Level 2 — Significant other observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data.

Level 3 — Significant unobservable inputs that reflect a company’s own assumptions about the assumptions that market participants would use in pricing an asset or liability.

Fair Value Option

Accounting Standards Codification (“ASC”) 825 “Fair Value Option for Financial Assets and Financial Liabilities” (“ASC 825”) provides a fair value option election that allows companies to irrevocably elect fair value as the initial and subsequent measurement attribute for certain financial assets and liabilities. ASC 825 permits the fair value option election on an instrument by instrument basis at initial recognition. We have decided not to make this election.

Revenue Recognition

Rental income is recognized as rentals become due. Rental payments received in advance are deferred until earned. All leases between the Company and tenants of the property are operating leases and are one year or less.

For certain properties, in addition to contractual base rent, the tenants pay their share of utilities to the Company. The income and expenses associated with these properties are generally recorded on a gross basis when the Company is the primary obligor. For the year ended December 31, 2018 and December 31, 2017, the Company recorded reimbursements of expenses of approximately $499,000 and $111,000, respectively, which are reported as tenant reimbursements in the accompanying consolidated statements of operations.

Tenant fees, such as application fees, administrative fees, late fees, and other revenues from tenants are recorded when amounts become due.

Impairment and Allowance for Doubtful Accounts

The Company reviews its real estate portfolio on a quarterly basis to ascertain if there are any indicators of impairment to the value of any of its real estate assets, including deferred costs and intangibles, to determine if there is any need for an impairment charge. In reviewing the portfolio, the Company examines one or more of the following: the type of asset, the current financial statements or other available financial information of the asset, and the economic

13

situation in the area in which the asset is located. For each real estate asset owned for which indicators of impairment exist, management performs a recoverability test by comparing the sum of the estimated undiscounted future cash flows attributable to the asset to its carrying amount. If the aggregate undiscounted cash flows are less than the asset's carrying amount, an impairment loss is recorded to the extent that the estimated fair value is less than the asset's carrying amount. The estimated fair value is determined using a discounted cash flow model of the expected future cash flows through the useful life of the property. The analysis includes an estimate of the future cash flows that are expected to result from the real estate investment's use and eventual disposition. These cash flows consider factors such as expected future operating income, trends and prospects, the effects of leasing demand, competition and other factors.

For the year ended December 31, 2018 and the period ended December 31, 2017, the Company determined that three was no impairment of long-lived assets.

The Company maintains an allowance for doubtful accounts for estimated losses resulting from the inability of a tenant to make required rent payments. At December 31, 2018 and December 31, 2017, respectively, there was $52,350 and zero balance in the allowance for doubtful accounts, respectively.

Results of Operations

Revenue

The year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017 resulted in a net loss attributable to MogulREIT II of approximately $1,587,000 and $674,000, respectively. Net loss was primarily attributable to rental and tenant reimbursements income, which was partially offset by an equity in earnings loss, less general and administrative expenses, depreciation and amortization, and real estate taxes, utilities and maintenance expenses and other operating expenses over the operating period.

Rental Income, net

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, we earned net rental income of approximately $5,012,000 and $933,000, respectively.

Tenant Reimbursements

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, we earned tenant reimbursements of approximately $499,000 and $111,000, respectively.

Expenses

Depreciation and Amortization

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, we incurred depreciation and amortization expenses of approximately $2,100,000 and $462,000, respectively.

General and Administrative Expenses

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, we incurred general and administrative expenses of approximately $1,256,000 and $234,000, respectively, which includes professional fees, organizational costs and other costs associated with running our business.

Real Estate Expenses

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, we incurred real estate expenses of approximately $1,666,000 and $312,000, respectively.

14

Liquidity and Capital Resources

We require capital to fund our investment activities and operating expenses. Our capital sources may include net proceeds from the Offering, cash flow from operations and borrowings under credit facilities.

We are dependent upon the net proceeds from the Offering to conduct our proposed operations. We currently obtain the capital required to purchase real estate-related investments and conduct our operations from the proceeds of the Offering and any future offerings we may conduct, from secured or unsecured financings from banks and other lenders and from any undistributed funds from our operations. As of December 31, 2018, we had made seven investments with a net investment value of approximately $76,000,000 and had cash of approximately $1,600,000. We anticipate that proceeds from the Offering will provide sufficient liquidity to meet future funding commitments one year from the date the financial statements are available to be issued.

If we raise substantially less than $50,000,000 in gross offering proceeds, we will make fewer investments resulting in less diversification in terms of the type, number and size of investments we make and the value of an investment in us will fluctuate more with the performance of the specific assets we acquire. Further, we will have certain fixed operating expenses, including certain expenses as a publicly offered REIT, regardless of whether we are able to raise substantial funds in this Offering. Our inability to raise substantial funds would increase our fixed operating expenses as a percentage of gross income, reducing our net income and limiting our ability to make distributions.

We expect to selectively employ leverage to enhance total returns to our stockholders. Our targeted portfolio-wide leverage after we have acquired an initial substantial portfolio of diversified investments is up to 75% of the fair market value or expected fair market value (for a value-add acquisition) of our assets; provided, however, we may exceed this limit for certain temporary bridge financings. During the period when we are acquiring our initial portfolio, we may employ greater leverage on individual assets (that will also result in greater leverage of the initial portfolio) in order to quickly build a diversified portfolio of assets. As of December 31, 2018, we had no outstanding borrowings other than those owed to related parties.

In addition to making investments in accordance with our investment objectives, we expect to use our capital resources to make certain payments to our Manager. During our organization and offering stage, these payments will include payments for reimbursement of certain organization and offering expenses. We expect aggregate organization and offering expenses to be approximately $1,500,000 or, if we raise the maximum offering amount, approximately 3% of gross offering proceeds. If the Offering is not successfully completed, we will not be obligated to pay the remaining offering and organizational costs owed to our Manager. Real estate sponsors may make payments to our Sponsor or its affiliates in connection with the selection or purchase of investments. We will pay the Manager a quarterly asset management fee of one-fourth of 1.25%, which, until September 30, 2018, was based on our net offering proceeds as of the end of each quarter, and thereafter was based on the average investment value of our assets. During our acquisition stage, we also expect to make payments to our Manager in connection with the purchase of investments of up to 3% of the contract purchase price of each asset and for costs incurred by our Manager in providing services to us. When assets are disposed of, we expect to make payments to our Manager of up to 2% of the contract sales prices of each property sold.

15

Cash Flow

The following presents our cash flows for the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017 (in thousands):

|

|

|

|

|

|

For the Period from |

||

|

|

|

|

|

|

January 13, 2017 |

||

|

|

|

For the Year |

|

|

(inception) |

||

|

|

|

ended |

|

|

through |

||

|

|

|

December 31, |

|

|

December 31, |

||

|

Cash provided by (used in) |

|

2018 |

|

|

2017 |

||

|

Operating activities: |

|

$ |

802 |

|

|

$ |

(282) |

|

Investing activities: |

|

|

(31,494) |

|

|

|

(23,977) |

|

Financing activities: |

|

|

31,120 |

|

|

|

25,428 |

|

Net increase in cash and cash equivalents |

|

|

428 |

|

|

|

1,169 |

|

Cash and cash equivalents, beginning of period |

|

|

1,169 |

|

|

|

— |

|

Cash and cash equivalents, end of period |

|

$ |

1,597 |

|

|

$ |

1,169 |

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, net cash provided by (used in) operating activities was approximately $802,000 and $(282,000), respectively, and related to net operating income excluding equity in losses of investees and net operating loss, respectively, on real estate investments.

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, net cash used in investing activities was approximately $31,494,000 and $23,977,000, respectively, and related to the acquisition of new real estate, investment in equity method investees and investment in a debt securities instrument.

For the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, net cash provided by financing activities was approximately $31,120,000 and $25,428,000, respectively, and related to new proceeds from the issuance of shares of our common stock pursuant to the Offering, proceeds from the issuance of debt and capital contributions from noncontrolling interests, net of syndication costs.

Off-Balance Sheet Arrangements

Funding Commitment

As of December 31, 2018, we had a future funding commitment of $703,410 related to the Avon Place equity investment.

Related Party Arrangements

For further details, please see “Note 8 ─ Related Party Arrangements” in Item 7 “Financial Statements” below.

Recent Developments

Avon Place

On January 16, 2019, MogulREIT II completed the sale of $500,000 of the Avon Initial Investment to an affiliated entity, and MogulREIT II used such proceeds to pay down a portion of the loan from RealtyMogul Commercial Capital, Co. After such transfer, the total investment as of January 16, 2019 is $2,296,590.

16

Offering Proceeds

As of April 26, 2019, we had raised total gross offering proceeds of approximately $16,389,117 from settled subscriptions and issued an aggregate of 1,638,911 shares of our common stock, with additional subscriptions for an aggregate of 10,550 shares of our common stock, representing additional potential gross offering proceeds of approximately $105,500, that have been accepted by us but not settled. Assuming the settlement for all subscriptions received, as of April 26, 2019, approximately $33,505,382 in shares of our common stock remained available for sale to the public pursuant to the Offering.

Distributions

On December 20, 2018, our board of directors authorized a daily cash distribution of $0.0012328767 per share of the Company’s common stock to stockholders of record as of the close of business on each day of the period commencing January 1, 2019 and ending on March 31, 2019. The distribution was scheduled to be paid on or about April 15, 2019. The aggregate amount of cash distributed and distributions reinvested related to the distribution period was $156,203 and $108,220, respectively.

Non-GAAP Financial Measures

Our Manager believes that funds from operations, or FFO, and adjusted funds from operations, or AFFO, each of which are non-GAAP measures, are additional appropriate measures of the operating performance of a REIT and of our company in particular. We compute FFO in accordance with the standards established by the National Association of Real Estate Investment Trusts, or NAREIT, as net income or loss (computed in accordance with GAAP), excluding gains or losses from sales of depreciable properties, the cumulative effect of changes in accounting principles, real estate-related depreciation and amortization, and after adjustments for unconsolidated/uncombined partnerships and joint ventures. FFO, as defined by NAREIT, is a computation made by analysts and investors to measure a real estate company’s cash flow generated by operations.

We calculate AFFO by subtracting from (or adding to) FFO:

|

· |

the amortization or accrual of various deferred costs; and |

|

· |

an adjustment to reverse the effects of unrealized gains/(losses). |

Our calculation of AFFO differs from the methodology used for calculating AFFO by certain other REITs and, accordingly, our AFFO may not be comparable to AFFO reported by other REITs. Our management utilizes FFO and AFFO as measures of our operating performance, and believes they are also useful to investors, because they facilitate an understanding of our operating performance after adjustment for certain non-cash expenses. Additionally, FFO and AFFO serve as measures of our operating performance because they facilitate evaluation of our company without the effects of selected items required in accordance with GAAP that may not necessarily be indicative of current operating performance and that may not accurately compare our operating performance between periods. Furthermore, although FFO, AFFO and other supplemental performance measures are defined in various ways throughout the REIT industry, we also believe that FFO and AFFO may provide us and our investors with an additional useful measure to compare our financial performance to certain other REITs.

Neither FFO nor AFFO is equivalent to net income or cash generated from operating activities determined in accordance with GAAP. Furthermore, FFO and AFFO do not represent amounts available for management’s discretionary use because of needed capital replacement or expansion, debt service obligations or other commitments or uncertainties. Neither FFO nor AFFO should be considered as an alternative to net income as an indicator of our operating performance or as an alternative to cash flow from operating activities as a measure of our liquidity.

17

Our unaudited FFO and AFFO calculations for the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, are as follows:

|

|

|

|

|

For the Period from |

||

|

|

|

|

|

January 13, 2017 |

||

|

|

|

For the Year |

|

(inception) |

||

|

|

|

ended |

|

through |

||

|

|

|

December 31, |

|

December 31, |

||

|

|

|

|

2018 |

|

2017 |

|

|

|

|

(in thousands) |

|

(in thousands) |

||

|

GAAP net income attributable to MogulREIT II, Inc. |

|

$ |

(1,587) |

|

$ |

(674) |

|

Add: depreciation and amortization of properties |

|

|

1,328 |

|

|

234 |

|

Adjustments for noncontrolling interests |

|

|

(573) |

|

|

(92) |

|

Adjustments for equity method investments |

|

|

302 |

|

|

— |

|

Funds from operations (“FFO”) applicable to common stock |

|

|

(530) |

|

|

(532) |

|

Add: amortization of lease intangibles |

|

|

749 |

|

|

228 |

|

Add: amortization of deferred financing costs and discount |

|

|

177 |

|

|

23 |

|

Add: real estate acquisition costs |

|

|

— |

|

|

636 |

|

Adjustments for noncontrolling interests |

|

|

(326) |

|

|

(393) |

|

Adjustments for equity method investments |

|

|

253 |

|

|

— |

|

Adjusted funds from operations (“AFFO”) applicable to common stock |

|

$ |

323 |

|

$ |

(38) |

Item 3. Directors and Officers

Although our Manager manages our day-to-day operations, we operate under the direction of the board of directors, the members of which are accountable to us and our stockholders as fiduciaries. We currently have three directors, two of whom are independent directors.

In accordance with our charter, a majority of our independent directors generally must approve corporate actions or policies that directly relate to the following:

|

· |

any transfer or sale of our Sponsor’s initial investment in the Company; provided, however, our Sponsor may not sell its initial investment while it remains our Sponsor, but our Sponsor may transfer the shares to an affiliate; |

|

· |

the duties of our directors, including ratification of our charter, the written policies on investments and |

borrowing, the monitoring of administrative procedures, investment operations and our performance and the

performance of our Manager;

|

· |

the management agreement; |

|

· |

liability and indemnification of our directors, Manager and affiliates; |

|

· |

fees, compensation and expenses, including organization and offering expenses, acquisition fees and |

acquisition expenses, disposition fees, total operating expenses, real estate commissions on the resale of

property, incentive fees, and Manager compensation;

|

· |

any change or modification of our statement of investment objectives; |

|

· |

real property appraisals; |

|

· |

our borrowing policies; |

|

· |

annual and special meetings of stockholders; |

|

· |

election of our directors; and |

|

· |

our distribution reinvestment plan. |

As of the date of this Annual Report, our executive officers and directors are as follows:

|

Name |

|

Age* |

|

Position |

|

Jilliene Helman |

|

32 |

|

Chief Executive Officer, Chief Financial Officer, President, Treasurer, Secretary and Director |

|

Flynann Janisse |

|

50 |

|

Independent Director |

|

Louis S. Weeks III |

|

66 |

|

Independent Director |

*As of April 25, 2019

18

Jilliene Helman has served as our Chief Executive Officer, President, Treasurer and Secretary since January 2017, and Chief Executive Officer and Secretary of our Manager since March 2016. Since May 2012, Ms. Helman has served as the Chief Executive Officer and a director of Realty Mogul, Co., where she is responsible for Realty Mogul, Co.’s strategic direction and operations. In this capacity, she has approved over $350 million of investments with property values worth over $1 billion. From July 2008 to September 2012, Ms. Helman served in a variety of capacities at Union Bank, including as a Management Training Associate; an Assistant Vice President, Sales Development Manager; and Vice President, Corporate Risk Management. Ms. Helman held these positions across the wealth management, finance and risk management departments of Union Bank. Ms. Helman is a Certified Wealth Strategist and holds Series 7, Series 63 and Series 24 licenses. Ms. Helman has a Bachelor of Science in Business Administration degree from Georgetown University.

Flynann Janisse has served as one of our independent directors since July 2017. Ms. Janisse has served as the Executive Director of Rainbow Housing Assistance Corporation (Rainbow), President and Executive Director of Equality Community Housing Corporation, and President and Chairman of the board of directors of Placet Development Corporation. Ms. Janisse supports the national operations of an award-winning Resident Services Division of Rainbow and the asset management for an extensive affordable housing portfolio. Prior to joining Rainbow, Ms. Janisse served as Director of Property Management at Community Services of Arizona, a fully-integrated management company specializing in the management of multifamily, service-enriched affordable housing. Ms. Janisse has extensive experience in managing market rate (REIT), Section 42 Tax Credit, Project Section 8, and HUD and RD-financed housing communities. As an Advisory board of directors member for Novogradac’s Journal of Tax Credits, Ms. Janisse provides industry knowledge through publications reaching over 45,000 readers and serves as a judge for their industry Development of Distinction Awards at the Tax Credit Developers Conference recognizing excellence and ingenuity in the development of tax credit projects across the country using the LIHTC program. With 27 years of experience in asset management with an emphasis on the development and implementation of social service programs for service-enriched affordable housing, she has assembled a team of professionals to serve the mission of Rainbow with integrity and passion.

Louis S. Weeks III has served as one of our independent directors since July 2017. Mr. Weeks is the Founder and Principal at Seabury Coxe Advisors, LLC, consultants in financing and investing in commercial real estate. The firm is located in Baltimore, MD and is active nationally with projects and clients in New York, Philadelphia, Hartford and Los Angeles. For more than 35 years, Mr. Weeks has been involved in commercial real estate investments and finance. He spent 26 years at Columbia National Real Estate Finance, a 75-year old Mortgage Banking firm in Baltimore, MD founded by James W. Rouse. His various roles including 10 years as the firm’s Managing Partner and CEO. He was responsible for the Company’s overall operations, production, servicing, and finance. Over the years, Mr. Weeks has arranged debt and equity for clients totaling over $3.0 billion. Mr. Weeks’ early career was spent in the banking industry in New York City with Manufacturers Hanover Trust and BankersTrust Co. He has been an active member of the local chapters of NAIOP, ULI, ICSC, MBA and Baltimore Downtown Partnership and served on numerous local community board of directors. Mr. Weeks graduated from Skidmore College as a Periclean Scholar with a degree in Philosophy and attended Pratt Institute as a candidate for a Masters of Architecture degree.

Compensation of Directors

We pay to each of our independent directors a retainer of 1,000 shares of our common stock per year, plus an additional retainer of 500 shares of our common stock to the chairman of the audit committee. All directors will receive reimbursement of reasonable out-of-pocket expenses incurred in connection with attendance at each meeting of the board of directors. Independent directors are not reimbursed by us, our Sponsor, our Manager or any of their affiliates for spouses’ expenses to attend events (if any) to which spouses are invited. If a non-independent director is also an employee of the Company or our Manager or its affiliates, we will not pay compensation for services rendered as a director.

Our Manager

Our Manager manages our day-to-day affairs, and implements our investment strategy. Our Manager and its officers are not required to devote all of their time to our business and are only required to devote such time to our affairs as their duties require.

19

Executive Officers of our Manager

As of the date of this Annual Report, the executive officers of our Manager and their positions and offices are as follows:

|

Name |

|

Age* |

|

Position |

|

Jilliene Helman |

|

32 |

|

Chief Executive Officer, Chief Financial Officer and Secretary |

|

Eric Levy |

|

32 |

|

Portfolio Manager |

|

William Wenke |

|

36 |

|

General Counsel |

*As of April 25, 2019

Biographical information for Ms. Helman is provided above.

Eric Levy has served as Portfolio Manager since January 2019. Mr. Levy has served as an Assistant Vice President, Asset Management of Realty Mogul, Co. since October 2017. Mr. Levy is responsible for portfolio and asset management for debt and equity assets held by MogulREIT I, LLC and MogulREIT II, Inc. From April 2013 to September 2017, Mr. Levy served as Strategic Projects Manager at World Class Capital Group, a national real estate investment firm focused on acquiring, developing and managing real estate with over $1.2 billion in assets under management. In that role, he led the asset management of over 2.3 million square feet of retail and office properties, oversaw capital improvement plans for over 4.5 million square feet of self-storage facilities, managed portfolio-wide investor reporting and investor relationships, and helped to develop the operational infrastructure of the company. From August 2010 to March 2013, Mr. Levy served as Senior Paralegal – M&A, Real Estate, Credit at Willkie, Farr & Gallagher, an international law firm. Mr. Levy has more than eight years of experience in commercial real estate. Mr. Levy has a Bachelor of Arts degree from the University of Wisconsin-Madison.

William Wenke has served as General Counsel since January 2019. Since February 2018, Mr. Wenke has served as the Vice President, Legal of Realty Mogul, Co., where he is responsible for managing all legal and regulatory matters. From August 2016 to August 2017, Mr. Wenke was the Associate General Counsel at Westwood Financial, a fully integrated asset management, property management, leasing, brokerage and investment firm. From October 2013 to October 2015, Mr. Wenke served as Senior Counsel, Compliance and Legal for Blackstone Group subsidiary Invitation Homes, a private equity fund investing in a real estate portfolio with assets under management in excess of $12.3 billion, where he focused on forming and refining best practices and legal guidelines in preparation for the company’s $1.54 billion initial public offering (“IPO”) (NYSE: INVH). From October 2011 to August 2013, Mr. Wenke was the Assistant Vice President, Legal and Compliance Counsel, and Assistant Secretary of American Homes 4 Rent, an internally managed single-family homes REIT, where he provided representation for over $3 billion in capital transactions, including an over $700 million IPO (NYSE: AMH), additional offerings, and acquisitions. Earlier in his career, Mr. Wenke practiced as a litigation fellow at the American Civil Liberties Union. Mr. Wenke has a Bachelor of Arts degree from Emory University, a Robert Traurig-Greenberg Traurig Master of Laws in Real Property Development from the University of Miami School of Law, and a Juris Doctor from the University of Miami School of Law.

Compensation of the Executive Officers of our Manager

We do not currently have any employees nor do we currently intend to hire any employees who will be compensated directly by us. As described above, certain of the executive officers of Realty Mogul, Co. also serve as executive officers of our Manager. Each of these individuals receives compensation for his or her services, including services performed for us on behalf of our Manager, from Realty Mogul, Co. As executive officers of our Manager, these individuals will manage our day-to-day affairs, oversee the review, selection and recommendation of investment opportunities, service acquired investments and monitor the performance of these investments to ensure that they are consistent with our investment objectives. Although we will indirectly bear some of the costs of the compensation paid to these individuals, through fees we pay to our Manager, we do not intend to pay any compensation directly to these individuals.

Item 4. Security Ownership of Management and Certain Securityholders

The following table sets forth the beneficial ownership of shares of our common stock as of April 30, 2019, for each person or group that holds more than 5% of shares of our common stock, for each executive officer and director and

20

for the executive officers and directors of our Manager as a group. To our knowledge, each person that beneficially owns shares of our common stock has sole voting and disposition power with regard to such shares.

Unless otherwise indicated below, each person or entity has an address in care of our principal executive offices at 10780 Santa Monica Blvd., Suite 140, Los Angeles, CA 90025.

|

|

|

Number of |

|

|

|

|

|

|

Shares |

|

Percent of All |

|

|

|

|

Beneficially |

|

Shares as of |

|

|

Name of Beneficial Owner(1) |

|

Owned |

|

April 30, 2019 |

|

|

RM Sponsor, LLC (2)(3) |

|

10,000 |

|

0.6102 |

% |

|

Jilliene Helman |

|

— |

|

— |

|

|

Flynann Janisse |

|

1,000 |

|

0.0610 |

|

|

Louis S. Weeks III |

|

1,500 |

|

0.0915 |

|

|

All executive officers and directors as a group (4 persons) |

|

12,500 |

|

0.7627 |

% |

|

(1) |

Under SEC rules, a person is deemed to be a “beneficial owner” of a security if that person has or shares “voting power,” which includes the power to dispose of or to direct the disposition of such security. A person also is deemed to be a beneficial owner of any securities which that person has a right to acquire within 60 days. Under these rules, more than one person may be deemed to be a beneficial owner of the same securities and a person may be deemed to be a beneficial owner of securities as to which he or she has no economic or pecuniary interest. |

|

(2) |

After the completion of this offering, RM Sponsor, LLC will own less than 0.02% of our common stock, assuming we sell the maximum offering amount, including shares sold pursuant to our distribution reinvestment plan. |

|

(3) |

All voting and investment decisions with respect to shares of our common stock that are held by RM Sponsor, LLC are controlled by its manager, Jilliene Helman. Ms. Helman disclaims beneficial ownership of such shares. |

Item 5. Interest of Management and Others in Certain Transactions

For information responsive to this Item, please see “Note 8 ─ Related Party Arrangements” in Item 7 “Financial Statements” below.

Item 6. Other Information

None.

21

Item 7. Financial Statements

MogulREIT II, Inc.

Index

|

|

Page |

|

F-2 |

|

|

|

|

|

F-3 |

|

|

|

|

|

F-4 |

|

|

|

|

|

F-5 |

|

|

|

|

|

F-6 |

|

|

|

|

|

F-7 to F-18 |

F-1

Independent Auditor's Report

To the Stockholders

MogulREIT II, Inc.

We have audited the accompanying consolidated financial statements of MogulREIT II, Inc., which comprise the consolidated balance sheets as of December 31, 2018 and 2017, and the related consolidated statements of operations, stockholders' equity and cash flows for the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017, and the related notes to the financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of MogulREIT II, Inc. as of December 31, 2018 and 2017, and its results of operations and its cash flows for the year ended December 31, 2018 and the period from January 13, 2017 (inception) through December 31, 2017 in accordance with accounting principles generally accepted in the United States of America.

/s/ CohnReznick LLP

Bethesda, Maryland

April 30, 2019

F-2

MogulREIT II, Inc.

As of December 31, 2018 and 2017

(Amounts in thousands, except share and per share data)

|

|

|

As of December 31, |

|

As of December 31, |

||

|

|

|

2018 |

|

2017 |

||

|

ASSETS |

|

|

|

|

|

|

|

Real estate investments, at cost |

|

|

|

|

|

|

|

Land |

|

$ |

22,538 |

|

$ |

15,592 |

|

Buildings and improvements |

|

|

51,309 |

|

|

31,641 |

|

Total real estate investments, at cost |

|

|

73,847 |

|

|

47,233 |

|

Less accumulated depreciation |

|

|

(1,562) |

|

|

(234) |

|

Real estate investments, net |

|

|

72,285 |

|

|

46,999 |

|

Investment in real estate, equity method |

|

|

2,076 |

|

|

— |

|

Investment in debt instrument, at amortized cost |

|

|

1,440 |

|

|

— |

|

Cash and cash equivalents |

|

|

1,597 |

|

|

1,169 |

|

Restricted cash |

|

|

396 |

|

|

48 |

|

Rent receivable, net |

|

|

89 |

|

|

16 |

|

Unamortized intangible lease asset, net |

|

|

132 |

|

|

484 |

|

Stock subscription receivable |

|

|

64 |

|

|

— |

|

Deferred offering costs, net |

|

|

422 |

|

|

318 |

|

Prepaid expenses |

|

|

73 |

|

|

63 |

|

Escrow, deposits and other assets |

|

|

341 |

|

|

228 |

|

Total Assets |

|

$ |

78,915 |

|

$ |

49,325 |

|

|

|

|

|

|

|

|

|

LIABILITIES AND EQUITY |

|

|

|

|

|

|

|

Liabilities: |

|

|

|

|

|

|

|

Mortgages payable, net of $405 and $93 of deferred financing costs and $208 and $338 discount |

|

$ |

53,708 |

|

$ |

34,372 |

|

Accounts payable and accrued expenses |

|

|

623 |

|

|

504 |

|

Deferred offering costs payable |

|

|

806 |

|

|

342 |

|

Loans payable - related party |

|

|

2,209 |

|

|

3,295 |

|

Dividends payable |

|

|

137 |

|

|

33 |

|

Other liabilities |

|

|

373 |

|

|

175 |

|

Total Liabilities |

|

|

57,856 |

|

|

38,721 |

|

|

|

|

|

|

|

|

|

Equity: |

|

|

|

|

|

|

|