00016991362023FYfalseP1YP1M100016991362023-01-012023-12-3100016991362023-06-30iso4217:USD0001699136us-gaap:CommonClassAMember2024-02-27xbrli:shares0001699136us-gaap:CommonClassBMember2024-02-2700016991362023-12-3100016991362022-12-31iso4217:USDxbrli:shares0001699136us-gaap:CommonClassAMember2022-12-310001699136us-gaap:CommonClassAMember2023-12-310001699136us-gaap:CommonClassBMember2022-12-310001699136us-gaap:CommonClassBMember2023-12-310001699136us-gaap:ProductMember2023-01-012023-12-310001699136us-gaap:ProductMember2022-01-012022-12-310001699136us-gaap:ProductMember2021-01-012021-12-310001699136whd:RentalRevenueMember2023-01-012023-12-310001699136whd:RentalRevenueMember2022-01-012022-12-310001699136whd:RentalRevenueMember2021-01-012021-12-310001699136us-gaap:ProductAndServiceOtherMember2023-01-012023-12-310001699136us-gaap:ProductAndServiceOtherMember2022-01-012022-12-310001699136us-gaap:ProductAndServiceOtherMember2021-01-012021-12-3100016991362022-01-012022-12-3100016991362021-01-012021-12-310001699136us-gaap:CommonClassAMember2023-01-012023-12-310001699136us-gaap:CommonClassAMember2022-01-012022-12-310001699136us-gaap:CommonClassAMember2021-01-012021-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2020-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-12-310001699136us-gaap:AdditionalPaidInCapitalMember2020-12-310001699136us-gaap:RetainedEarningsMember2020-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001699136us-gaap:NoncontrollingInterestMember2020-12-3100016991362020-12-310001699136us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2021-01-012021-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-01-012021-12-310001699136us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001699136us-gaap:RetainedEarningsMember2021-01-012021-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2021-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-12-310001699136us-gaap:AdditionalPaidInCapitalMember2021-12-310001699136us-gaap:RetainedEarningsMember2021-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001699136us-gaap:NoncontrollingInterestMember2021-12-3100016991362021-12-310001699136us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-01-012022-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-01-012022-12-310001699136us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001699136us-gaap:RetainedEarningsMember2022-01-012022-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-12-310001699136us-gaap:AdditionalPaidInCapitalMember2022-12-310001699136us-gaap:RetainedEarningsMember2022-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001699136us-gaap:NoncontrollingInterestMember2022-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2023-01-012023-12-310001699136us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001699136us-gaap:NoncontrollingInterestMember2023-01-012023-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2023-01-012023-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001699136us-gaap:RetainedEarningsMember2023-01-012023-12-310001699136us-gaap:CommonStockMemberus-gaap:CommonClassAMember2023-12-310001699136us-gaap:CommonClassBMemberus-gaap:CommonStockMember2023-12-310001699136us-gaap:AdditionalPaidInCapitalMember2023-12-310001699136us-gaap:RetainedEarningsMember2023-12-310001699136us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001699136us-gaap:NoncontrollingInterestMember2023-12-310001699136us-gaap:RevenueFromContractWithCustomerMemberus-gaap:CustomerConcentrationRiskMemberwhd:OneCustomerMember2023-01-012023-12-31xbrli:pure0001699136us-gaap:RevenueFromContractWithCustomerMemberus-gaap:CustomerConcentrationRiskMemberwhd:OneCustomerMember2021-01-012021-12-310001699136us-gaap:CostOfGoodsProductLineMemberwhd:SupplierOneMemberus-gaap:SupplierConcentrationRiskMember2023-01-012023-12-310001699136us-gaap:BuildingAndBuildingImprovementsMembersrt:MinimumMember2023-12-310001699136us-gaap:BuildingAndBuildingImprovementsMembersrt:MaximumMember2023-12-310001699136us-gaap:MachineryAndEquipmentMembersrt:MinimumMember2023-12-310001699136us-gaap:MachineryAndEquipmentMembersrt:MaximumMember2023-12-310001699136whd:ReelsAndSkidsMembersrt:MinimumMember2023-12-310001699136whd:ReelsAndSkidsMembersrt:MaximumMember2023-12-310001699136srt:MinimumMemberwhd:VehiclesUnderFinanceLeaseMember2023-12-310001699136whd:VehiclesUnderFinanceLeaseMembersrt:MaximumMember2023-12-310001699136whd:RentalEquipmentMembersrt:MinimumMember2023-12-310001699136whd:RentalEquipmentMembersrt:MaximumMember2023-12-310001699136us-gaap:FurnitureAndFixturesMember2023-12-310001699136whd:ComputerAndSoftwareMembersrt:MinimumMember2023-12-310001699136whd:ComputerAndSoftwareMembersrt:MaximumMember2023-12-310001699136us-gaap:LandMember2023-12-310001699136us-gaap:LandMember2022-12-310001699136us-gaap:BuildingAndBuildingImprovementsMember2023-12-310001699136us-gaap:BuildingAndBuildingImprovementsMember2022-12-310001699136us-gaap:MachineryAndEquipmentMember2023-12-310001699136us-gaap:MachineryAndEquipmentMember2022-12-310001699136whd:ReelsAndSkidsMember2023-12-310001699136whd:ReelsAndSkidsMember2022-12-310001699136whd:VehiclesUnderFinanceLeaseMember2023-12-310001699136whd:VehiclesUnderFinanceLeaseMember2022-12-310001699136whd:RentalEquipmentMember2023-12-310001699136whd:RentalEquipmentMember2022-12-310001699136us-gaap:FurnitureAndFixturesMember2022-12-310001699136whd:ComputerAndSoftwareMember2023-12-310001699136whd:ComputerAndSoftwareMember2022-12-310001699136us-gaap:ConstructionInProgressMember2023-12-310001699136us-gaap:ConstructionInProgressMember2022-12-310001699136whd:FlexSteelMember2023-02-282023-02-280001699136whd:FlexSteelMember2023-02-2800016991362023-02-280001699136whd:FlexSteelMember2023-12-310001699136whd:FlexSteelMember2022-12-310001699136whd:FlexSteelMember2023-10-012023-12-310001699136whd:FlexSteelMember2023-03-012023-12-310001699136whd:FlexSteelMember2023-01-012023-12-310001699136whd:FlexSteelMember2022-01-012022-12-310001699136whd:PressureControlSegmentMember2022-12-310001699136whd:SpoolableTechnologiesMember2022-12-310001699136whd:PressureControlSegmentMember2023-01-012023-12-310001699136whd:SpoolableTechnologiesMember2023-01-012023-12-310001699136whd:PressureControlSegmentMember2023-12-310001699136whd:SpoolableTechnologiesMember2023-12-310001699136us-gaap:CustomerRelationshipsMember2023-12-310001699136us-gaap:TechnologyBasedIntangibleAssetsMember2023-12-310001699136us-gaap:TradeNamesMember2023-12-310001699136us-gaap:OrderOrProductionBacklogMember2023-12-310001699136whd:IdentifiableIntangibleAssetsAcquiredMember2023-12-310001699136whd:IdentifiableIntangibleAssetsAcquiredMember2023-01-012023-12-310001699136us-gaap:RevolvingCreditFacilityMembersrt:SubsidiariesMember2018-08-012018-08-310001699136us-gaap:RevolvingCreditFacilityMemberwhd:CactusWellheadLlcAndItsSubsidiariesMemberus-gaap:LineOfCreditMember2022-07-250001699136whd:CactusWellheadLlcAndItsSubsidiariesMemberus-gaap:LineOfCreditMember2022-07-250001699136whd:AmendedABLCreditFacilityMemberus-gaap:SecuredDebtMember2023-02-280001699136whd:AmendedABLCreditFacilityMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMember2023-02-280001699136whd:AmendedABLCreditFacilityMemberus-gaap:LetterOfCreditMemberus-gaap:LineOfCreditMember2023-02-280001699136us-gaap:RevolvingCreditFacilityMemberwhd:CactusWellheadLlcAndItsSubsidiariesMemberus-gaap:LineOfCreditMember2023-02-280001699136us-gaap:SecuredDebtMemberus-gaap:LineOfCreditMemberwhd:TheCreditFacilityMember2023-02-280001699136us-gaap:RevolvingCreditFacilityMemberus-gaap:LineOfCreditMemberwhd:TheCreditFacilityMember2023-02-280001699136us-gaap:BaseRateMemberus-gaap:RevolvingCreditFacilityMembersrt:SubsidiariesMembersrt:MinimumMember2023-01-012023-12-310001699136us-gaap:BaseRateMemberus-gaap:RevolvingCreditFacilityMembersrt:SubsidiariesMembersrt:MaximumMember2023-01-012023-12-310001699136us-gaap:RevolvingCreditFacilityMemberwhd:SecuredOvernightFinancingRateMembersrt:SubsidiariesMembersrt:MinimumMember2023-01-012023-12-310001699136us-gaap:RevolvingCreditFacilityMemberwhd:SecuredOvernightFinancingRateMembersrt:SubsidiariesMembersrt:MaximumMember2023-01-012023-12-310001699136us-gaap:RevolvingCreditFacilityMembersrt:SubsidiariesMembersrt:MaximumMember2023-01-012023-12-310001699136whd:CreditAgreementMemberus-gaap:RevolvingCreditFacilityMembersrt:SubsidiariesMemberus-gaap:LineOfCreditMember2023-12-310001699136us-gaap:RevolvingCreditFacilityMembersrt:SubsidiariesMember2023-01-012023-12-310001699136us-gaap:RevolvingCreditFacilityMember2023-12-310001699136whd:SecuredOvernightFinancingRateMember2023-01-012023-12-310001699136whd:SecuredOvernightFinancingRateSixMonthMember2023-01-012023-12-310001699136whd:SecuredOvernightFinancingRateOneMonthMember2023-01-012023-12-310001699136whd:SecuredOvernightFinancingRateThreeMonthMember2023-01-012023-12-310001699136whd:DeferredTaxAssetInvestmentInSubsidiaryMember2022-01-012022-12-310001699136whd:DeferredTaxAssetInvestmentInSubsidiaryMember2022-12-310001699136whd:DeferredTaxAssetAccruedForeignTaxesAndStateCreditsMember2023-12-310001699136us-gaap:DomesticCountryMember2023-12-310001699136us-gaap:StateAndLocalJurisdictionMember2023-12-310001699136us-gaap:EmployeeStockMemberwhd:LongTermIncentivePlanMember2023-01-012023-12-310001699136us-gaap:EmployeeStockMemberwhd:LongTermIncentivePlanMember2022-01-012022-12-310001699136us-gaap:EmployeeStockMemberwhd:LongTermIncentivePlanMember2021-01-012021-12-310001699136us-gaap:EmployeeStockMember2023-01-012023-12-310001699136us-gaap:EmployeeStockMember2022-01-012022-12-310001699136us-gaap:EmployeeStockMember2021-01-012021-12-310001699136us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001699136us-gaap:RestrictedStockUnitsRSUMember2022-12-310001699136us-gaap:RestrictedStockUnitsRSUMember2023-12-310001699136us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001699136us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001699136whd:PerformanceSharesThreeYearPerformancePeriodMember2023-01-012023-12-310001699136us-gaap:PerformanceSharesMembersrt:MinimumMember2023-01-012023-12-310001699136us-gaap:PerformanceSharesMembersrt:MaximumMember2023-01-012023-12-310001699136us-gaap:PerformanceSharesMember2023-01-012023-12-310001699136us-gaap:PerformanceSharesMember2022-12-310001699136us-gaap:PerformanceSharesMember2023-12-310001699136us-gaap:PerformanceSharesMember2022-01-012022-12-310001699136us-gaap:PerformanceSharesMember2021-01-012021-12-310001699136srt:MinimumMember2023-01-012023-12-310001699136srt:MaximumMember2023-01-012023-12-310001699136srt:MaximumMember2023-12-3100016991362018-02-122018-02-120001699136whd:CactusLlcMember2023-01-012023-12-310001699136whd:CactusLlcMember2022-01-012022-12-310001699136us-gaap:CommonClassBMember2023-01-012023-12-310001699136whd:AdditionalOfferingMemberus-gaap:CommonClassAMember2023-01-012023-01-310001699136whd:AdditionalOfferingMemberus-gaap:CommonClassAMember2023-01-310001699136us-gaap:AdditionalPaidInCapitalMember2023-01-012023-01-310001699136whd:FlexSteelMemberwhd:KeyEmployeeMember2023-01-012023-12-310001699136whd:CactusCompaniesMemberus-gaap:CommonClassBMember2023-12-310001699136whd:CCUnitsRedeemedForClassCommonStockMemberus-gaap:CommonClassAMember2023-12-310001699136whd:CwUnitsRedeemedForClassCommonStockMemberus-gaap:CommonClassAMember2018-02-012023-12-310001699136whd:March2021SecondaryOfferingMember2021-01-012021-12-310001699136whd:June2021CadentRedemptionMember2021-01-012021-12-310001699136whd:September2021CadentRedemptionMember2021-01-012021-12-310001699136whd:OtherCWRedemptionsMember2021-01-012021-12-310001699136whd:OtherCWRedemptionsMember2022-01-012022-12-310001699136whd:OtherCWRedemptionsMember2023-01-012023-12-310001699136whd:CWUnitHolderRedemptionMemberus-gaap:CommonClassBMember2023-01-012023-12-310001699136whd:CWUnitHolderRedemptionMemberus-gaap:CommonClassBMember2022-01-012022-12-310001699136whd:CWUnitHolderRedemptionMemberus-gaap:CommonClassBMember2021-01-012021-12-310001699136whd:CactusWellheadLlcAndItsSubsidiariesMember2023-01-012023-12-310001699136whd:CactusWellheadLlcAndItsSubsidiariesMember2022-01-012022-12-310001699136whd:CactusWellheadLlcAndItsSubsidiariesMember2021-01-012021-12-310001699136whd:March2021SecondaryOfferingMemberus-gaap:CommonClassAMember2021-03-092021-03-090001699136whd:March2021SecondaryOfferingMemberus-gaap:CommonClassAMember2021-03-090001699136whd:March2021SecondaryOfferingMemberus-gaap:CommonClassAMember2021-03-122021-03-120001699136whd:March2021SecondaryOfferingMemberus-gaap:OtherNonoperatingIncomeExpenseMember2021-03-122021-03-120001699136whd:SecondaryOfferingMemberus-gaap:OtherNonoperatingIncomeExpenseMember2021-03-120001699136whd:CactusLLCMemberwhd:CwUnitHoldersOtherThanCactusIncMember2021-06-172021-06-170001699136whd:CactusLLCMemberwhd:CwUnitHoldersOtherThanCactusIncMemberus-gaap:CommonClassAMember2021-06-172021-06-170001699136whd:CactusLLCMemberwhd:CwUnitHoldersOtherThanCactusIncMember2021-09-132021-09-130001699136whd:CactusLLCMemberwhd:CwUnitHoldersOtherThanCactusIncMemberus-gaap:CommonClassAMember2021-09-132021-09-130001699136whd:ShareRepurchaseProgramMember2023-06-060001699136whd:ShareRepurchaseProgramMemberus-gaap:CommonStockMember2023-01-012023-12-310001699136whd:ShareRepurchaseProgramMemberus-gaap:CommonStockMember2023-12-310001699136us-gaap:FairValueInputsLevel2Member2023-12-310001699136us-gaap:FairValueInputsLevel2Member2022-12-310001699136us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:FairValueMeasurementsRecurringMemberwhd:EarnOutLiabilityMemberus-gaap:FairValueInputsLevel2Member2023-12-310001699136us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:FairValueMeasurementsRecurringMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:MeasurementInputRiskFreeInterestRateMembersrt:MinimumMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:MeasurementInputRiskFreeInterestRateMemberwhd:EarnOutLiabilityMembersrt:MaximumMember2023-12-310001699136whd:MeasurementInputExpectedRevenueVolatilityMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:MeasurementInputDiscountRateMembersrt:MinimumMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:MeasurementInputDiscountRateMemberwhd:EarnOutLiabilityMembersrt:MaximumMember2023-12-310001699136whd:CreditDiscountRateMembersrt:MinimumMemberwhd:EarnOutLiabilityMember2023-12-310001699136us-gaap:FairValueInputsLevel3Memberwhd:EarnOutLiabilityMember2023-02-280001699136us-gaap:FairValueInputsLevel3Memberwhd:EarnOutLiabilityMember2023-03-012023-12-310001699136us-gaap:FairValueInputsLevel3Memberwhd:EarnOutLiabilityMember2023-12-3100016991362023-03-012023-12-31whd:segment0001699136whd:PressureControlSegmentMember2022-01-012022-12-310001699136whd:PressureControlSegmentMember2021-01-012021-12-310001699136whd:SpoolableTechnologiesMember2022-01-012022-12-310001699136whd:SpoolableTechnologiesMember2021-01-012021-12-310001699136whd:PressureControlSegmentMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001699136whd:PressureControlSegmentMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001699136whd:PressureControlSegmentMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310001699136whd:SpoolableTechnologiesMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001699136whd:SpoolableTechnologiesMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001699136whd:SpoolableTechnologiesMemberus-gaap:OperatingSegmentsMember2021-01-012021-12-310001699136us-gaap:OperatingSegmentsMember2023-01-012023-12-310001699136us-gaap:OperatingSegmentsMember2022-01-012022-12-310001699136us-gaap:OperatingSegmentsMember2021-01-012021-12-310001699136us-gaap:CorporateNonSegmentMember2023-01-012023-12-310001699136us-gaap:CorporateNonSegmentMember2022-01-012022-12-310001699136us-gaap:CorporateNonSegmentMember2021-01-012021-12-310001699136us-gaap:FairValueInputsLevel3Member2023-12-310001699136whd:PressureControlSegmentMemberus-gaap:OperatingSegmentsMember2023-12-310001699136whd:PressureControlSegmentMemberus-gaap:OperatingSegmentsMember2022-12-310001699136whd:PressureControlSegmentMemberus-gaap:OperatingSegmentsMember2021-12-310001699136whd:SpoolableTechnologiesMemberus-gaap:OperatingSegmentsMember2023-12-310001699136whd:SpoolableTechnologiesMemberus-gaap:OperatingSegmentsMember2022-12-310001699136whd:SpoolableTechnologiesMemberus-gaap:OperatingSegmentsMember2021-12-310001699136us-gaap:OperatingSegmentsMember2023-12-310001699136us-gaap:OperatingSegmentsMember2022-12-310001699136us-gaap:OperatingSegmentsMember2021-12-310001699136us-gaap:CorporateNonSegmentMember2023-12-310001699136us-gaap:CorporateNonSegmentMember2022-12-310001699136us-gaap:CorporateNonSegmentMember2021-12-310001699136us-gaap:GeographicConcentrationRiskMemberus-gaap:SalesRevenueNetMemberus-gaap:GeographicDistributionDomesticMember2021-01-012021-12-310001699136us-gaap:GeographicConcentrationRiskMemberus-gaap:SalesRevenueNetMemberus-gaap:GeographicDistributionDomesticMember2022-01-012022-12-310001699136us-gaap:GeographicConcentrationRiskMemberus-gaap:SalesRevenueNetMemberus-gaap:GeographicDistributionDomesticMember2023-01-012023-12-310001699136us-gaap:GeographicConcentrationRiskMemberwhd:TangibleLongLivedAssetsMemberus-gaap:GeographicDistributionDomesticMember2022-01-012022-12-310001699136us-gaap:GeographicConcentrationRiskMemberwhd:TangibleLongLivedAssetsMemberus-gaap:GeographicDistributionDomesticMember2021-01-012021-12-310001699136us-gaap:GeographicConcentrationRiskMemberwhd:TangibleLongLivedAssetsMemberus-gaap:GeographicDistributionDomesticMember2023-01-012023-12-3100016991362023-01-012023-02-270001699136us-gaap:RelatedPartyMember2022-01-012022-12-310001699136us-gaap:RelatedPartyMember2021-01-012021-12-310001699136us-gaap:RelatedPartyMember2023-01-012023-12-310001699136us-gaap:RelatedPartyMember2023-12-310001699136us-gaap:RelatedPartyMember2022-12-310001699136us-gaap:RelatedPartyMembersrt:MaximumMember2023-01-012023-12-310001699136srt:SubsidiariesMember2023-01-012023-12-310001699136srt:SubsidiariesMember2022-01-012022-12-310001699136srt:SubsidiariesMember2021-01-012021-12-3100016991362023-10-012023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-38390

Cactus, Inc.

(Exact name of registrant as specified in its charter)

| | | | | |

| Delaware | 35-2586106 |

(State or other jurisdiction

of incorporation or organization) | (I.R.S. Employer

Identification No.) |

| |

920 Memorial City Way, Suite 300 Houston, Texas | 77024 |

| (Address of principal executive offices) | (Zip code) |

(713) 626-8800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Class A Common Stock, par value $0.01 | | WHD | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☑ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes ☐ No ☑

As of June 30, 2023, the aggregate market value of the common stock of the registrant held by non-affiliates of the registrant was $2.7 billion.

As of February 27, 2024, the registrant had 65,322,730 shares of Class A common stock, $0.01 par value per share, and 14,033,979 shares of Class B common stock, $0.01 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Registrant’s Definitive Proxy Statement for the 2024 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Report relates.

TABLE OF CONTENTS

| | | | | | | | |

| |

| | |

| | | |

| | | |

| | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | | |

| | | |

| | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | | |

| | | |

| | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| | | |

| | | |

| Item 15. | | |

| Item 16. | | |

| | | |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10‑K (this “Annual Report”) contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). When used in this Annual Report, the words “attempt,” “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project” and similar expressions are intended to identify forward‑looking statements, although not all forward‑looking statements contain such identifying words. These forward‑looking statements are based on our current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. When considering forward‑looking statements, you should keep in mind the risk factors and other cautionary statements described under the heading “Item 1A. Risk Factors” included in this Annual Report and other cautionary statements contained herein. These forward‑looking statements are based on management’s current belief, based on currently available information, as to the outcome and timing of future events.

Important factors that could cause actual results to differ materially from those contained in the forward‑looking statements include, but are not limited to:

•demand for our products and services, which is affected by, among other things, the price of crude oil and natural gas;

•the number of active drilling and workover rigs, pad sizes, drilling and completion efficiencies, lateral lengths, well productivity, well counts and availability of takeaway and storage capacity;

•changes in the number of drilled but uncompleted wells (“DUCs”);

•competition and capacity within the oilfield services industry;

•disparities in activity levels between private operators and large publicly-traded exploration and production (“E&P”) companies;

•the financial health of our customers and our credit risk of customer non-payment;

•availability and cost of raw materials, components and imported items;

•changes in inland and ocean shipping costs as well as transit times, particularly due to Red Sea-related disruptions;

•the impact of inflation, high interest rates and a possible recession;

•availability and cost of skilled and qualified workers and our ability to recruit and retain employees and managers;

•potential liabilities such as warranty and product liability claims arising out of the installation, use or misuse of our products;

•our financial strategy, operating cash flows, liquidity and capital required for our business, including our ability to obtain and repay debt-financing and to pay dividends;

•our ability to retain, expand and create new relationships with major customers or suppliers;

•consolidation among our customers;

•laws and regulations, including environmental regulations, that may increase our costs or our customers’ costs, limit the demand for our products and services or restrict our operations;

•disruptions in political, regulatory, economic and social conditions domestically or internationally including increasing tensions and military activity throughout the Middle East;

•the severity and duration of global pandemics or other health crises, such as the outbreak of COVID-19, and the extent of their impact on our business, including employee absenteeism;

•the impact of actions taken by the Organization of Petroleum Exporting Countries and other oil and gas producing countries (“OPEC+”) affecting the supply of oil and gas;

•the impact of planned and possible future releases from and replenishments to the Strategic Petroleum Reserve;

•the impact of LNG regasification and storage capacity on associated natural gas demand and potential delays in approvals of new natural gas export terminals;

•the significance of future liabilities under the Tax Receivable Agreement (the “TRA”) we entered into in connection with our initial public offering;

•a failure of our information technology infrastructure or any significant breach of security;

•potential uninsured claims and litigation against us;

•currency exchange rate fluctuations associated with our international operations;

•our ability to successfully integrate FlexSteel and realize the expected benefits of the transaction in an efficient and effective manner; and

•our ability to expand internationally.

We caution you that these forward‑looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident to the operation of our business. These risks include but are not limited to the risks described in this Annual Report under “Item 1A. Risk Factors.” Should one or more of the risks or uncertainties described in this Annual Report occur, or should underlying assumptions prove incorrect, our actual results could differ materially from those expressed in any forward‑looking statements.

All forward‑looking statements, expressed or implied, included in this Annual Report are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward‑looking statements that we or persons acting on our behalf may issue. Except as otherwise required by applicable law, we disclaim any duty to update any forward‑looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this Annual Report.

PART I

Item 1. Business

General

Cactus, Inc. (“Cactus Inc.”) was incorporated on February 17, 2017 as a Delaware corporation for the purpose of completing an initial public offering of equity, which was completed on February 12, 2018 (our “IPO”). We began operating in August 2011 following the formation of Cactus Wellhead, LLC (“Cactus LLC”) in part by Scott Bender and Joel Bender, who have owned or operated wellhead manufacturing businesses since the late 1970s.

Cactus Inc. and its consolidated subsidiaries (the “Company,” “we,” “us,” “our” and “Cactus”) are primarily engaged in the design, manufacture, sale and rental of highly engineered pressure control and spoolable pipe technologies. Our products are sold and rented principally for onshore unconventional oil and gas wells and are utilized during the drilling, completion and production phases of our customers’ wells. We also provide field services for all of our products and rental items to assist with the installation, maintenance and handling of the equipment. Additionally, we offer repair and refurbishment services as appropriate. We operate through service centers and pipe yards located in the United States, Canada and Australia. We also provide rental and service operations in the Middle East and other select international markets. We also have manufacturing and production facilities in Bossier City, Louisiana, Baytown, Texas and Suzhou, China. Our corporate headquarters are located in Houston, Texas.

FlexSteel Acquisition

On February 28, 2023, we completed the acquisition of the FlexSteel business (the “Merger”) through a merger with HighRidge Resources, Inc. and its subsidiaries (“HighRidge”). The purpose of the Merger was to effect the acquisition of the operations of FlexSteel Holdings, Inc. and its subsidiaries. We completed the acquisition on a cash-free, debt-free basis and paid total cash consideration of $621.5 million which included final adjustments for closing working capital, cash on hand and indebtedness adjustments as set forth in the related merger agreement (the “Merger Agreement”). In addition to the upfront consideration, there is a potential future earn-out payment of up to $75 million to be paid no later than the third quarter of 2024, if certain revenue growth targets are met by the FlexSteel business. We funded the upfront purchase price using a combination of $165.6 million of net proceeds received from a public offering of shares of our Class A common stock completed in January 2023, borrowings under the Amended ABL Credit Facility (as defined in Note 6 in the notes to the Consolidated Financial Statements) totaling $155.0 million and available cash on hand. See Note 3 in the notes to the Consolidated Financial Statements for additional information related to the acquisition.

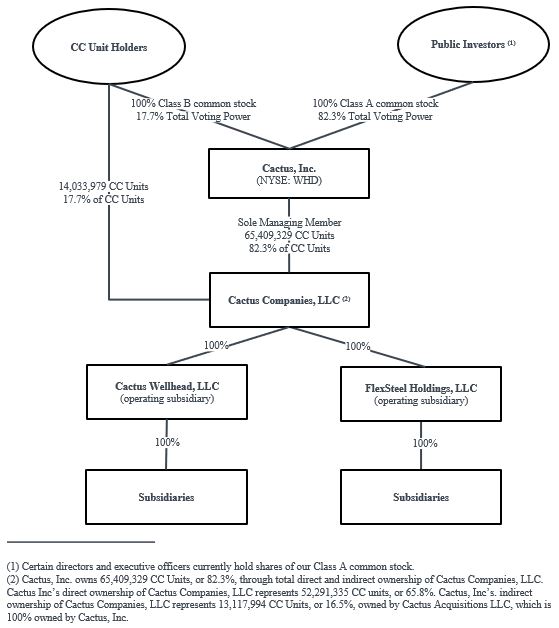

CC Reorganization and Current Ownership Structure

On February 27, 2023, in order to facilitate the Merger with HighRidge, an internal reorganization (the “CC Reorganization”) was completed in which Cactus Companies, LLC (“Cactus Companies”), a wholly-owned subsidiary of Cactus Inc., acquired all of the outstanding units representing limited liability ownership interests in Cactus LLC (“CW Units”), the operating subsidiary of Cactus Inc., in exchange for an equal number of units representing limited liability company interests in Cactus Companies (“CC Units”). Subsequent to the Merger, FlexSteel Holdings, Inc. was converted into a limited liability company and is now named FlexSteel Holdings, LLC (“FlexSteel”). Cactus Inc. contributed HighRidge to Cactus Acquisitions LLC (“Cactus Acquisitions”), a newly created entity, whereby HighRidge was converted into a limited liability company. Lastly, Cactus Acquisitions contributed FlexSteel to Cactus Companies.

Cactus Inc. is a holding company whose only material asset is a direct and indirect equity interest consisting of CC Units following the completion of the CC Reorganization (which were CW Units from the IPO until the CC Reorganization). Cactus Inc. was the sole managing member of Cactus LLC upon completion of our IPO until the CC Reorganization and became the sole managing member of Cactus Companies upon completion of the CC Reorganization. In connection with the CC Reorganization, Cactus Inc., Cactus Acquisitions and the remaining owners of CC Units entered into the Amended and Restated Limited Liability Company Operating Agreement of Cactus Companies (the “Cactus Companies LLC Agreement”), which contains substantially the same terms and conditions as the Second Amended and Restated Limited Liability Company Operating Agreement of Cactus LLC (the “Cactus Wellhead LLC Agreement”), which was the limited liability company operating agreement of Cactus LLC prior to the CC Reorganization. Cactus Inc. was responsible for all operational, management and administrative decisions relating to Cactus LLC’s business for the period from completion of our IPO until the CC Reorganization and for the Cactus Companies’ business for periods after the CC Reorganization.

From the completion of our IPO until the CC Reorganization, pursuant to the Cactus Wellhead LLC Agreement, owners of CW Units were entitled to redeem their CW Units for shares of Cactus Inc.’s Class A common stock, par value $0.01 per share (“Class A common stock”) on a one-for-one basis, which would have resulted in a corresponding increase in Cactus Inc.’s membership interest in Cactus LLC and an increase in the number of shares of Class A common stock outstanding. After the CC Reorganization, we refer to the owners of CC Units, other than Cactus Inc. (along with their permitted transferees), as “CC Unit Holders.” From the completion of our IPO until the CC Reorganization, CW Unit Holders owned one share of our Class B common stock, par value $0.01 per share (“Class B common stock”) for each CW Unit such CW Unit Holder owned and, upon the completion of the CC Reorganization, such CW Unit Holders ceased to be holders of CW Units and, instead, became holders of a number of CC Units equal to the number of CW Units such CW Unit Holders held immediately prior to the completion of the CC Reorganization. Following the completion of the CC Reorganization, CC Unit Holders own one share of our Class B common stock for each CC Unit such CC Unit Holder owns and Cactus Companies is the sole member of Cactus LLC. Pursuant to the Cactus Companies LLC Agreement, owners of CC Units are entitled to redeem their CC Units for shares of Cactus Inc.’s Class A common stock on a one-for-one basis, which would result in a corresponding increase in Cactus Inc.’s membership interest in Cactus Companies and an increase in the number of shares of Class A common stock outstanding.

Since our IPO, 46.5 million CC Units (including CW Units prior to the CC Reorganization) and a corresponding number of shares of Class B common stock have been redeemed in exchange for shares of Class A common stock. Holders of Class A common stock and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law or our amended and restated certificate of incorporation. Cactus WH Enterprises, LLC (“Cactus WH Enterprises”) is the largest CC Unit Holder. Cactus WH Enterprises is a Delaware limited liability company owned by Scott Bender, Joel Bender, Steven Bender and certain other employees. As of December 31, 2023, Cactus Inc. owned 82.3% and CC Unit Holders owned 17.7% of Cactus Companies, which was based on 65.4 million shares of Class A common stock issued and outstanding and 14.0 million shares of Class B common stock issued and outstanding. Cactus WH Enterprises held approximately 15.8% of our voting power as of December 31, 2023.

The following diagram indicates our simplified ownership structure as of December 31, 2023:

Our Products and Services

Following the acquisition of FlexSteel, we have two operating segments consisting of Pressure Control and Spoolable Technologies. See discussion below of each operating segment.

Pressure Control

The Pressure Control segment designs, manufactures, sells and rents a range of wellhead and pressure control equipment under the Cactus Wellhead brand. Products are sold and rented principally for onshore unconventional oil and gas wells and are utilized during the drilling, completion and production phases of our customers’ wells. In addition, we provide field services for all of our products and rental items to assist with the installation, maintenance and handling of the equipment.

We operate through service centers in the United States, which are strategically located in the key oil and gas producing regions, and in Eastern Australia. These service centers support our field services and provide equipment assembly and repair services. We also provide rental and service operations in the Middle East. Pressure Control manufacturing and production facilities are located in Bossier City, Louisiana and Suzhou, China.

Demand for our product sales in the Pressure Control segment is driven primarily by the number of new wells drilled, as each new well requires a wellhead and, after the completion phase, a production tree. Demand for our rental items is driven primarily by the number of well completions as we rent frac trees to oil and gas operators to assist in hydraulic fracturing. To a lesser extent, rental demand is also driven by drilling activity as we rent tools used in the installation of wellheads. Field service and other revenues are closely correlated with revenues from product sales and rentals, as items sold or rented almost always have an associated service component.

Spoolable Technologies

The Spoolable Technologies segment designs, manufactures, and sells spoolable pipe and associated end fittings under the FlexSteel brand. Our customers use these products primarily as production, gathering and takeaway pipelines to transport oil, gas or other liquids. In addition, we also provide field services and rental items to assist our customers with the installation of these products. We support our field service operations through service centers and pipe yards located in oil and gas regions throughout the United States and Western Canada. We also provide equipment and services in select international markets. The Spoolable Technologies manufacturing facility is located in Baytown, Texas.

Demand for our product sales in the Spoolable Technologies segment is driven primarily by the number of wells being placed into production after the completions phase as customers use our spoolable pipe and associated fittings to bring wells more rapidly onto production. Rental and field service and other revenues are closely correlated with revenues from product sales, as items sold usually have an associated rental and service component.

Our Revenues

Our revenues are derived from three sources: products, rentals, and field service and other. Product revenues are derived from the sale of wellhead systems, production trees and spoolable pipe and fittings. Rental revenues are primarily derived from the rental of equipment used during the completion process, the repair of such equipment and the rental of equipment or tools used to install wellhead equipment or spoolable pipe. Field service and other revenues are primarily earned when we provide installation and other field services for both product sales and equipment rental.

For the year ended December 31, 2023, we derived 74% of our total revenues from the sale of our products, 10% from rentals and 16% from field service and other. In 2022, we derived 66% of our total revenues from the sale of our products, 14% from rentals and 20% from field service and other. In 2021, we derived 64% of our total revenues from the sale of our products, 14% from rentals and 22% from field service and other. We have predominantly domestic operations and sales but also generate revenues in Australia, Canada and other select international markets.

Most of our sales are made on a call out basis pursuant to agreements, wherein our clients provide delivery instructions for goods and/or services as their operations require. Such goods and services are most often priced in accordance with a preapproved price list. The actual pricing of our products and services is impacted by a number of factors including competitive pricing pressure, the value perceived by our customers, the level of utilized capacity in the oil service sector, cost of manufacturing the product, cost of providing the service and general market conditions. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - Recent Developments and Trends” for a discussion of trends in market demand.

Costs of Conducting Our Business

The principal elements of cost of sales for our products are the direct and indirect costs to manufacture and supply our products, including labor, materials, machine time, tariffs and duties, freight and lease expenses related to our facilities. The principal elements of cost of sales for rentals are the direct and indirect costs of manufacturing and supplying rental equipment, including depreciation, repairs specifically performed on such rental equipment and freight. The principal elements of cost of sales for field service and other are labor, equipment depreciation and repair, equipment and vehicle lease expenses, fuel and supplies. Selling, general and administrative expenses (“SG&A”) are comprised of costs such as sales and marketing, engineering and product development, general corporate overhead, business development, compensation, employment benefits, insurance, information technology, safety and environmental, legal and professional.

Suppliers and Raw Materials

Forgings, castings, tube and bar stock represent the principal raw materials used in the manufacture of our Pressure Control products and rental equipment. In addition, we require accessory items (such as elastomers, ring gaskets, studs and nuts) and machined components. The principal raw materials used by our Spoolable Technologies segment include tube, bar stock, steel strip and high density polyethylene. We purchase a majority of our raw materials from vendors primarily located in the United States, China, India, Australia and the United Kingdom. We do not believe that we are overly dependent on any individual vendor to supply our required materials or services. The materials and services essential to our business are normally readily available and, where we use one or a few vendors as a source of any particular materials or services, we believe that we can, within a reasonable period of time, make satisfactory alternative arrangements in the event of an interruption of supply from any vendor. We believe our materials and services vendors have the capacity to meet additional demand should we require it, although at potentially higher costs and with extended deliveries.

Manufacturing

Our manufacturing and production facilities within our Pressure Control operating segment are located in Bossier City, Louisiana and Suzhou, China. Although both facilities can produce our full range of products, our Bossier City facility has advanced production capabilities and is designed to support time-sensitive and rapid turnaround of made-to-order equipment, while our facility in China is optimized for longer lead time orders and outsources its machining requirements. The facilities are licensed to the latest American Petroleum Institute (“API”) 6A specification for wellheads and valves and API Q1 and ISO 9001:2015 quality management systems. The Bossier City facility also has the ability to perform frac rental equipment remanufacturing. Our production facility in China is configured to efficiently produce our range of pressure control products and components for less time-sensitive, higher-volume orders. The Suzhou facility assembles and tests finished and semi-finished machined components before shipment to the United States, Australia and other international locations. Our Suzhou subsidiary is wholly-owned, and its facility is staffed by Cactus employees, which we believe is a key factor in sustaining high quality and dependable deliveries.

Our manufacturing facility within our Spoolable Technologies operating segment is located in Baytown, Texas. Using proprietary-designed manufacturing equipment, we produce pipe products in accordance with industry standards. Additionally, our Baytown facility utilizes advanced Computer Numeric Control machines dedicated to the precision manufacturing of the FlexSteel connectors. Our Baytown facility is licensed to the latest API 15S specification for spoolable reinforced plastic line pipe, API 17J specification for unbonded flexible pipe and adheres to certified API Q1 and ISO 9001:2015 quality management systems.

Trademarks and Patents

Trademarks are important to the marketing of our products. The Company has numerous trademarks registered with the U.S. Patent and Trademark Office as well as foreign trademark offices and has also applied for registration of several other trademarks, which are still pending. Once registered, our trademarks can be renewed every 10 years as long as we are using them in commerce. We also seek to protect our technology through the use of patents, which affords us 20 years of protection of our proprietary inventions and technology, although we do not deem patents to be critical to our success. We have been awarded U.S. patents and patents in foreign jurisdictions while still having additional patent applications pending. We also rely on trade secret protection for our confidential and proprietary information. To protect our information, we customarily enter into confidentiality agreements with our employees and suppliers. There can be no assurance, however, that others will not independently obtain similar information or otherwise gain access to our trade secrets.

Cyclicality

We are substantially dependent on conditions in the oil and gas industry, including the level of exploration, development and production activity of, and the corresponding capital spending by, oil and natural gas companies. The level of exploration, development and production activity is directly affected by trends in oil and natural gas prices, which have historically been volatile, and by the availability of capital and the associated capital spending discipline exercised by customers. Declines, as well as anticipated declines, in oil and gas prices could negatively affect the level of these activities and capital spending, which could adversely affect demand for our products and services and, in certain instances, result in the cancellation, modification or rescheduling of existing and expected orders and the ability of our customers to pay us for our products and services. These factors could have an adverse effect on our revenue and profitability.

Seasonality

Our business is not significantly impacted by seasonality, although our fourth quarter has historically been impacted by holidays and our customers’ budget cycles. This can lead to lower activity in our three revenue categories as well as lower margins, particularly in field services due to reduced labor utilization.

Customers

We serve over 300 customers representing private operators, publicly-traded independents, majors and other companies with operations in the key U.S. oil and gas producing basins as well as in Australia, Canada, the Middle East and other international locations. One customer represented approximately 10% of total revenues during the year ended December 31, 2023. No customer represented 10% or more of our total revenues during the year ended December 31, 2022, whereas one customer represented 12% of total revenues during the year ended December 31, 2021.

Competition

The markets in which we operate are highly competitive. In the Pressure Control segment, we believe we are one of the largest suppliers of wellheads used in the United States. We compete with Vault, divisions of SLB and TechnipFMC and a large number of other companies. We believe the rental market for frac stacks and related flow control equipment is more fragmented than the wellhead product market and do not believe any individual company represents more than 20% of the U.S. market. In the Spoolable Technologies segment, we compete with companies who offer spoolable products, including Baker Hughes, Mattr, NOV and select other companies, and also companies who offer traditional steel line pipe, including Tenaris, Vallourec, and a large number of other line pipe manufacturers and distributors.

We believe the competitive factors in the markets we serve include technical features, equipment availability, work force competency, efficiency, safety record, reputation, continuity of management and price. Additionally, projects are often awarded on a bid basis, which tends to create a highly competitive environment. While we seek to be competitive in our pricing, we believe many of our customers elect to work with us based on product performance, features, safety and availability, as well as the quality of our people, equipment and services. We seek to differentiate ourselves from our competitors by delivering the highest‑quality services and equipment possible, coupled with superior execution and operating efficiency in a safe working environment.

Environmental, Health and Safety Regulation

We are subject to stringent governmental laws and regulations, both in the United States and other countries, pertaining to protection of the environment and occupational safety and health. Compliance with environmental legal requirements in the United States at the federal, state or local levels may require acquiring permits to conduct regulated activities, incurring capital expenditures to limit or prevent emissions, discharges and any unauthorized releases, and complying with stringent practices to handle, recycle and dispose of certain wastes. These laws and regulations include, among others:

•the Federal Water Pollution Control Act (the “Clean Water Act”);

•the Clean Air Act;

•the Comprehensive Environmental Response, Compensation and Liability Act;

•the Resource Conservation and Recovery Act;

•the Occupational Safety and Health Act; and

•national and local environmental protection laws in Australia, China, Canada and the Middle East.

New, modified or stricter enforcement of environmental laws and regulations could be adopted or implemented that significantly increase our compliance costs, pollution mitigation costs, or the cost of any remediation of environmental contamination that may become necessary, and these costs could be material. Our customers are also subject to most, if not all, of the same laws and regulations relating to environmental protection and occupational safety and health in the United States and in foreign countries where we operate. Consequently, to the extent these environmental compliance costs, pollution mitigation costs or remediation costs are incurred by our customers, those customers could elect to delay, reduce or cancel drilling, exploration or production programs, which could reduce demand for our products and services and, as a result, have a material adverse effect on our business, financial condition, results of operations, or cash flows. Consistent with our quality assurance and Health, Safety & Environment (“HSE”) principles, we have established proactive environmental and worker safety policies in the United States and foreign countries for the management, handling, recycling or disposal of chemicals and gases and other materials and wastes resulting from our operations. Substantial fines and penalties can be imposed and orders or injunctions limiting or prohibiting certain operations may be issued in connection with any failure to comply with laws and regulations relating to worker health and safety.

Licenses and Certifications. Our manufacturing facility in Bossier City, Louisiana, our production facility in Suzhou, China and our service center in Brendale, Australia are currently licensed by the API to monogram manufactured products in accordance with API 6A, 21st Edition product specification for both wellheads and valves while the quality management system is certified to API Q1, 9th Edition and ISO 9001:2015. Cactus has also developed an API Q2 program specific to our Pressure Control service business. We have and are implementing the API Q2 Quality Management System at select service locations to reduce well site non-productive time, improve service tool reliability and enhance customer satisfaction and retention.

Our manufacturing facility in Baytown, Texas also holds API licenses, allowing us to monogram our FlexSteel products in strict accordance with industry-leading standards. Specifically, we adhere to the API 15S 3rd Edition product specification for spoolable reinforced plastic line pipe and the API 17J 4th Edition product specification for unbonded flexible pipe. The FlexSteel quality management system is certified to API Q1, 9th Edition, and ISO 9001:2015. We also hold product conformity certifications for our Spoolable Technologies segment from ICONTEC, covering Latin and South American standards for API 15S and 17J, and ABNT, endorsing Brazilian production conformity to API 15S and 17J.

The API licenses and certifications expire every three years and are renewed upon successful completion of annual audits. Our current API licenses and certifications for our Pressure Control segment are published on our website under the “Quality Assurance & Control” section at www.CactusWHD.com. The current licenses and certifications for our Spoolable Technologies segment can be found under the “HSEQ” section of our FlexSteel website at www.flexsteelpipe.com. API’s standards are subject to revision, however, and there is no guarantee that future amendments or substantive changes to the standards would not require us to modify our operations or manufacturing processes to meet the new standards. Doing so may materially affect our operational costs. We also cannot guarantee that changes to the standards would not lead to the rescission of our licenses should we be unable to make the changes necessary to meet the new standards. Loss of our API licenses could materially affect demand for these products.

Hydraulic Fracturing. Most of our customers utilize hydraulic fracturing in their operations. Environmental concerns have been raised regarding the potential impact of hydraulic fracturing and the resulting wastewater disposal on underground water supplies and seismic activity. These concerns have led to several regulatory and governmental initiatives in the United States to restrict the hydraulic fracturing process, which could have an adverse impact on our customers’ completions or production activities. Although we do not conduct hydraulic fracturing, certain of our products are used in hydraulic fracturing. Increased regulation and attention given to the hydraulic fracturing process could lead to greater opposition to oil and gas production activities using hydraulic fracturing techniques. Since 2021, the Texas Railroad Commission, which regulates the state’s oil and gas industry, has suspended the use of deep wastewater disposal wells in certain areas of oil-producing counties in West Texas. The suspensions are intended to mitigate earthquakes thought to be caused by the injection of waste fluids, including saltwater, that are a byproduct of hydraulic fracturing into disposal wells. The bans require oil and gas production companies to find other options to handle the wastewater, which may include piping or trucking it longer distances to other locations not under the bans. In addition, the Texas Railroad Commission has overseen the development of well-operator-led response plans to reduce injection volumes in other portions of West Texas in order to reduce seismicity in these areas. The adoption of new laws or regulations at the federal, state, local or foreign level imposing reporting obligations on, or otherwise limiting, delaying or banning, the hydraulic fracturing process or other processes on which hydraulic fracturing and subsequent hydrocarbon production relies, such as water disposal, could make it more difficult to complete oil and natural gas wells. Further, it could increase our customers’ costs of compliance and doing business, and otherwise adversely affect the hydraulic fracturing services for which they contract, which could negatively impact demand for our products.

Climate Change. State, national and foreign governments and agencies continue to evaluate, and in some instances adopt, climate-related legislation and other regulatory initiatives that would restrict emissions of greenhouse gases. Changes in environmental requirements related to greenhouse gases, climate change and alternative energy sources may negatively impact demand for our services. For example, oil and natural gas exploration and production may decline as a result of environmental requirements, including land use policies responsive to environmental concerns. While the United States Department of the Interior (“DOI”) announced in April 2022 that it would resume oil and gas leasing on public lands, there was an 80% reduction in the number of acres offered and an increase in the royalties companies must pay. In August 2023, the DOI proposed a scaled back offshore lease sale for certain areas in the Gulf of Mexico due to concerns related to an endangered whale population in the area. The exclusion of certain lease blocks from the sale was successfully challenged in court, and the DOI was ordered to hold the lease sale at its original scale. This decision was upheld by the U.S. Court of Appeals for the Fifth Circuit on November 14, 2023, and the sale went forward as scheduled on December 20, 2023. The topic of oil and gas leasing on public land remains politically fraught. In addition, the Biden administration has indicated that it is delaying consideration of new natural gas export terminals in the United States and to the extent that these developments or other initiatives to reform federal leasing practices result in the development of additional restrictions on drilling, limitations on the availability of leases, or restrictions on the ability to obtain required permits, it could impact our customers’ opportunities and reduce demand for our products and services in the aforementioned areas.

Because our business depends on the level of activity in the oil and natural gas industry, existing or future laws, regulations, treaties or international agreements related to greenhouse gases and climate change, may reduce demand for oil and natural gas and could have a negative impact on our business. Likewise, such restrictions may result in additional compliance obligations that could have a material adverse effect on our business, consolidated results of operations and consolidated financial position. In addition, our business could be impacted by initiatives to address greenhouse gases and climate change and incentives to conserve energy or use alternative energy sources. For example, the Inflation Reduction Act of 2022 (the “Inflation Reduction Act”) appropriates significant federal funding for the development of renewable energy, clean hydrogen, clean fuels, electric vehicles and supporting infrastructure and carbon capture and sequestration, amongst other provisions. In addition, the Inflation Reduction Act imposes the first ever federal fee on the emission of greenhouse gases (“GHG”) through a methane emissions charge. The Inflation Reduction Act amends the federal Clean Air Act to impose a fee on the emission of methane from sources required to report their GHG emissions to the EPA, including those sources in the onshore petroleum and natural gas production categories. These developments could further accelerate the transition of the U.S. economy away from the use of fossil fuels towards lower- or zero-carbon emissions alternatives, which could reduce demand for our products and services and negatively impact our business.

Insurance and Risk Management

We rely on customer indemnifications and third‑party insurance as part of our risk mitigation strategy. However, our customers may be unable to satisfy indemnification claims against them. In addition, we indemnify our customers against certain claims and liabilities resulting or arising from our provision of goods or services to them. Our insurance may not be sufficient to cover any particular loss or may not cover all losses. We carry a variety of insurance coverages for our operations, and we are partially self‑insured for certain claims, in amounts that we believe to be customary and reasonable. Historically, insurance rates have been subject to various market fluctuations that may result in less coverage, increased premium costs, or higher deductibles or self‑insured retentions.

Our insurance includes coverage for commercial general liability, damage to our real and personal property, damage to our mobile equipment, pollution liability, workers’ compensation and employer’s liability, auto liability, foreign package policy, commercial crime, fiduciary liability employment practices, cargo, excess liability, and directors and officers’ insurance. We also maintain a partially self-insured medical plan that utilizes specific and aggregate stop loss limits. Our insurance includes various coverage limitations, policy limits and deductibles or self‑insured retentions, which must be met prior to, or in conjunction with, any recovery.

Human Capital Management

As of December 31, 2023, we employed almost 1,600 people worldwide, of which over 100 were employed outside of the United States, mainly in Australia and China. We are not a party to any collective bargaining agreements and have not experienced any strikes or work stoppages. We consider our relations with our workforce to be good. Our success is highly dependent on our ability to attract, retain and motivate a diverse population of talented employees at all levels of our organization, including the individuals who comprise our global workforce, executive officers and other key personnel. To thrive in a highly competitive industry, we have formulated essential strategies, objectives, and metrics for recruitment and retention. These factors play a significant role in our comprehensive business management approach and our high levels of retention of key managers and associates.

Recruiting. Our talent strategy prioritizes the attraction, recognition, development, and retention of high-performing individuals. To find qualified candidates, we encourage and reward employee referrals, utilize several social media platforms, participate in regional job fairs and establish partnerships with educational organizations throughout the United States. Furthermore, we collaborate with local workforce commissions to ensure that we attract a diverse and highly capable pool of candidates in all regions where we operate.

Training and Development. We are dedicated to our employees’ training and development, especially those in field, plant and branch operations. We offer extensive internal training programs that prioritize and monitor their technical and safety skills. Our internal training focuses on safety, corporate and personal responsibility, product knowledge, behavioral development and ethical conduct. Our career development plans are designed to enable individuals to acquire the necessary technical knowledge to perform their jobs with utmost safety and precision. External training courses are attended by employees with specialized skills, knowledge or certifications as needed for their ongoing success and professional development. We believe our continued focus on training and development translates into a safer work environment, opportunities to promote within the organization, improved employee morale and increased employee retention.

Diversity and Inclusion. We believe that diversity and inclusion are integral to our success and essential to fostering innovation and sustainable growth. We are dedicated to cultivating a workplace that embraces differences and ensures everyone feels valued, respected and empowered to contribute their unique perspectives. We are committed to creating and maintaining a workplace culture that is diverse, inclusive, and free from discrimination. This commitment extends across all aspects of our business, from hiring and promotion practices to employee development and supplier relationships. Our workforce comprises a diverse associate group, with approximately 14% women and approximately 46% of our workforce representing a minority population.

Compensation and Benefits. We offer comprehensive compensation and benefits programs designed to address the needs of our employees and their families. Along with competitive salaries and wages, our benefits programs (which may vary by country) include annual bonuses, retirement plans such as a 401(k) plan, healthcare and insurance benefits, health savings accounts partially funded by the Company, standard flexible spending accounts, personal legal services insurance, company-sponsored long and short term disability, accident and critical illness, paid time off, family leave, partially paid maternity and paternity leave, family care resources and employee assistance programs, among others. We also offer tuition reimbursement in certain circumstances to support our employees’ continued growth and development. Additionally, we use targeted equity-based grants with vesting conditions to facilitate the retention of key personnel.

Health and Safety. Our health and safety programs are designed around global standards with appropriate variations addressing the multiple jurisdictions and regulations, specific hazards and unique working environments of our manufacturing and production facilities, service centers and headquarters. We require each location to conduct regular safety evaluations to verify that expectations for safety program procedures and training are being met. We also engage in third-party conformity assessments of our HSE processes to determine adherence to our HSE management system and to global health and safety standards. We monitor our Occupational Safety and Health Administration Total Recordable Incident Rate (“TRIR”) to assess our operation’s health and safety performance. TRIR is defined as the number of incidents per 100 full-time employees that have resulted in a recordable injury or illness in the pertinent period. During fiscal year 2023, our Pressure Control segment reported a TRIR of 1.19, which compares to 1.35 in 2022, with no work-related fatalities in either year. Our Spoolable Technologies segment reported a TRIR of 0.98 for fiscal year 2023 with no work-related fatalities. Based on the most recent statistics available from the International Association of Drilling Contractors, our TRIR statistics are in line with the industry average.

We are committed to the health, safety and wellness of our employees. We provide our employees and their families access to various flexible and convenient health and wellness programs. These programs include benefits that offer protection and security to have peace of mind concerning events that may require time away from work or impact their financial well-being. These tools also support their physical and mental health by providing resources to improve or maintain their health status.

Executive Officers and Directors

The following tables set forth certain information regarding our Executive Officers and Directors as of February 27, 2024:

Information About Our Executive Officers

| | | | | | | | |

| Name | | Position |

| Scott Bender | | Chief Executive Officer, Chairman of the Board and Director |

| Joel Bender | | President and Director |

| Steven Bender | | Chief Operating Officer |

| Stephen Tadlock | | Executive Vice President, Chief Executive Officer of the Spoolable Technologies segment and Treasurer |

| Alan Keifer | | Interim Chief Financial Officer |

| William Marsh | | Executive Vice President, General Counsel and Corporate Secretary |

| Donna Anderson | | Vice President and Chief Accounting Officer |

Information About Our Board of Directors

| | | | | | | | |

| Name | | Position |

| Scott Bender | | Chief Executive Officer, Chairman of the Board and Director of Cactus, Inc. |

| Joel Bender | | President and Director of Cactus, Inc. |

| Melissa Law | | President of Global Operations for Tate & Lyle |

| Michael McGovern | | Executive Chairman of the board of directors of Superior Energy Services, Inc. |

| John (Andy) O’Donnell | | Former Vice President and executive officer of Baker Hughes Incorporated |

| Gary Rosenthal | | Partner, The Sterling Group, L.P. |

| Bruce Rothstein | | Former Member and co-founder of Cadent Energy Partners LLC |

| Alan Semple | | Director of Teekay Corporation |

| Tym Tombar | | Managing Director and Co-Founder of Arcadius Capital Partners |

Available Information

Our principal executive offices are located at 920 Memorial City Way, Suite 300, Houston, TX 77024, and our telephone number at that address is (713) 626‑8800. Our website address is www.CactusWHD.com. Our periodic reports and other information filed with or furnished to the SEC, including our Form 10-Ks, Form 10-Qs and Form 8-Ks, as well as amendments to such filings, are available free of charge through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this Annual Report and does not constitute a part of this Annual Report.

Item 1A. Risk Factors

Investing in our Class A common stock involves risks. You should carefully consider the information in this Annual Report, including the matters addressed under “Cautionary Statement Regarding Forward‑Looking Statements,” and the following risks before making an investment decision. Our business, results of operations and financial condition could be materially and adversely affected by any of these risks. Additional risks or uncertainties not currently known to us, or that we deem immaterial, may also have an effect on our business, results of operations and financial condition. The trading price of our Class A common stock could decline due to any of these risks, and you may lose all or part of your investment.

Risks Related to the Oilfield Services Industry and Our Business

Demand for our products and services depends on oil and gas industry activity and customer expenditure levels, which are directly affected by trends in the demand for and price of crude oil and natural gas and availability of capital.

Demand for our products and services depends primarily upon the general level of activity in the oil and gas industry, including the number of drilling rigs in operation, the number of oil and gas wells being drilled, the depth, lateral length and

drilling conditions of these wells, the volume of production, the number of well completions and the level of well remediation activity, the number of wells put into production and the corresponding capital spending by oil and gas companies. Oil and gas activity is in turn heavily influenced by, among other factors, current and anticipated oil and natural gas prices locally and worldwide, which have historically been volatile. Declines, as well as anticipated declines, in oil and gas prices could negatively affect the level of these activities and capital spending, which could adversely affect demand for our products and services and, in certain instances, result in the cancellation, modification or rescheduling of existing and expected orders and the ability of our customers to pay us for our products and services. These factors could have an adverse effect on our results of operations, financial condition and cash flows.

The oil and gas industry is cyclical and has historically experienced periodic downturns, which have been characterized by diminished demand for our products and services and downward pressure on the prices we charge. These downturns cause many E&P companies to reduce their capital budgets and drilling activity. Any future downturn or expected downturn could result in a significant decline in demand for oilfield services and adversely affect our business, results of operations and cash flows.

U.S. drilling and completion activity could be adversely affected by any significant constraints in equipment, labor or takeaway capacity in the regions in which we operate.

U.S. drilling and completion activity may be impacted by, among other things, the availability and cost of ancillary equipment and services, pipeline capacity, and material and labor shortages. Should significant changes in activity occur, there could be concerns over availability of the equipment, materials and labor required to drill and complete a well, together with the ability to move the produced oil and natural gas to market. Should significant constraints develop that materially impact the efficiency and economics of oil and gas producers, U.S. drilling and completion activity could be adversely affected. This would have an adverse impact on the demand for the products we sell and rent, which could have a material adverse effect on our business, results of operations and cash flows.

We may be unable to employ a sufficient number of skilled and qualified workers to sustain or expand our current operations.

The delivery of our products and services requires personnel with specialized skills and experience. Our ability to be productive and profitable will depend upon our ability to attract and retain skilled workers. In addition, our ability to expand our operations depends in part on our ability to increase the size of our skilled labor force. The demand for skilled workers is high and the cost to attract and retain qualified personnel has remained elevated. During industry downturns, skilled workers may leave the industry, reducing the availability of qualified workers when conditions improve. In addition, a significant increase in the wages paid by competing employers both within and outside of our industry could result in increases in the wage rates that we must pay. If we are not able to employ and retain skilled workers, our ability to respond quickly to customer demands or strong market conditions may inhibit our growth, which could have a material adverse effect on our business, results of operations and cash flows.

Our business is dependent on the continuing services of certain of our key managers and employees.

We depend on key personnel. The loss of key personnel could adversely impact our business. The loss of qualified employees or an inability to retain and motivate additional highly‑skilled employees required for the operation and expansion of our business could hinder our ability to successfully maintain and expand our market share. During the fourth quarter of 2023, our Chief Financial Officer (“CFO”) assumed responsibility for the Chief Executive Officer position in our Spoolable Technologies operating segment (the FlexSteel business) and was replaced with an interim CFO. While the Company intends to appoint a new CFO during 2024, the changes in executive leadership could cause disruption to our business operations.

Political, regulatory, economic and social disruptions in the countries in which we conduct business and globally could adversely affect our business or results of operations.

In addition to our facilities in the United States, we operate a production facility in China and have facilities in Australia and Canada that sell and rent equipment as well as provide parts, repair services and field services associated with installation. Additionally, we provide rental and field service operations in the Middle East. Instability and unforeseen changes in any of the markets in which we conduct business could have an adverse effect on the demand for, or supply of, our business, results of operations and cash flows.

We are dependent on a relatively small number of customers in a single industry. The loss of an important customer could adversely affect our results of operations and financial condition.