UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

For

the fiscal year ended

or

Commission

File Number:

(Exact Name of Registrant as Specified in Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification Number) |

(Address of Principal Executive Offices, Zip Code)

Registrant’s

telephone number, including area code: (

Securities registered under Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered under Section 12(g) of the Act: None.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act

during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has

been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant

to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | |

| Non-accelerated filer | ☐ | Smaller reporting company | |

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

The

aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of June 30, 2020,

the last business day of the registrant’s last completed second quarter, based upon the closing price of the common stock

of $9.60 on such date, is $

As

of March 5, 2021, there were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement relating to its 2021 annual meeting of shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

All statements in this Annual Report on Form 10-K that address events, developments or results that we expect or anticipate may occur in the future are “forward-looking statements” within the meaning of Section 27A of the Securities Act, Section 21E of the Exchange Act and the Private Securities Litigation Reform Act of 1995. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “project,” “forecast,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “seeks,” “scheduled,” or “will,” and similar expressions are intended to identify forward-looking statements. These statements relate to future periods, future events or our future operating or financial plans or performance, are made on the basis of management’s current views and assumptions with respect to future events, including management’s current views regarding the likely impacts of the COVID-19 pandemic. Any forward-looking statement is not a guarantee of future performance and actual results could differ materially from those contained in the forward-looking statement. We operate in a changing environment where new risks emerge from time to time and it is not possible for us to predict all risks that may affect us, particularly those associated with the COVID-19 pandemic, which has had wide-ranging and continually evolving effects. The forward-looking statements, as well as our prospects as a whole, are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in the forward-looking statements. These risks and uncertainties include, without limitation:

| ● | our ability to recognize the anticipated benefits of the Business Combination (as defined below), including with respect to financial and business performance, and our ability to produce accurate projections and metrics related thereto, which may be affected by, among other things, competition and the ability of the combined business to grow and manage growth profitably; |

| ● | costs related to the Business Combination; |

| ● | the impact of health epidemics, including the COVID-19 pandemic, on our business and the actions we may take in response thereto; |

| ● | changes in our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects and plans; |

| ● | the outcome of actual or potential litigation, complaints, product liability claims, or regulatory proceedings, and the potential adverse publicity related thereto; |

| ● | the implementation, market acceptance and success of our business model, expansion plans, opportunities and initiatives, including the market acceptance of our planned products and services; |

| ● | competition and our ability to counter competition, including changes to Google’s algorithm; |

| ● | developments and projections relating to our competitors and industry; |

| ● | our expectations regarding our ability to obtain and maintain intellectual property protection and not infringe on the rights of others; |

| ● | our future capital requirements, our ability to raise capital and utilize sources of cash; |

| ● | our ability to obtain funding for our operations; |

| ● | changes in applicable laws or regulations; and |

| ● | the possibility that we may be adversely affected by other economic, business, and/or competitive factors. |

See also the section titled “Risk Factors” (refer to Part I, Item 1A of this report), and subsequent reports and registration statements filed from time to time with the Securities and Exchange Commission (the “SEC”), for further discussion of certain risks and uncertainties that could cause actual results and events to differ materially from our forward-looking statements. Readers of this report are cautioned not to rely on these forward-looking statements, since there can be no assurance that these forward-looking statements will prove to be accurate. Forward-looking statements speak only as of the date they are made, and we expressly disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any further disclosures we make on related subjects in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. This cautionary note is applicable to all forward-looking statements contained in this report.

ii

RISK FACTORS SUMMARY

Our business, financial condition, and operating results may be affected by a number of factors, whether currently known or unknown. Any one or more of such factors could directly or indirectly cause our actual results of operations and financial condition to vary materially from past or anticipated future results of operations and financial condition. Any of these factors, in whole or in part, could materially and adversely affect our business, financial condition, results of operations, and stock price. We have provided a summary of some of these risks below, with a more detailed explanation of the risks applicable to us in Part I, Item 1A. “Risk Factors” and elsewhere in this report.

| ● | Our business is subject to risks arising from epidemic diseases, such as the COVID-19 pandemic. |

| ● | Our recent growth rates may not be sustainable or indicative of our future growth, which will depend on: (i) our customers’ experience, (ii) the economy and disposable income of our customers, (iii) our product offering, product pricing and fulfillment, (iv) shipping speed and cost optimization, (v) our competitive position in the aftermarket parts supply, (vi) changes in search engine algorithms affecting our website’s search engine optimization, and (vii) vendor supplies and vendor performance. |

| ● | We are primarily dependent on negative working capital to finance our business, and any adverse change in the availability of negative working capital, due to any factor, including a decrease in revenues or a reduction and/or withdrawal of credit terms from our key vendors, could severely impact the liquidity of the Company and its operations. |

| ● | Our business operates on thin operating margins, and even small changes in our operating scale, revenue growth rate, product costs, advertisement costs, customer traffic patterns, search engine algorithms, or selling and administrative overhead costs, or any one-time exceptional expense, could have a material impact on our profitability. If we fail to manage our growth or our cost effectively, our business, financial conditions and results of operations could be materially and adversely affected. |

| ● | We may be unable to accurately forecast net sales and appropriately plan our expenses in the future. |

| ● | We depend on search engines and other online sources to attract visitors to our digital commerce platform, and if we are unable to attract these visitors and convert them into customers in a cost-effective manner, our business, financial condition and results of operations will be harmed. |

| ● | If we are unable to manage the challenges associated with its international operations, the growth of our business could be limited, and our business could suffer. |

| ● | Our growth strategy is dependent upon our ability to expand our “iD” branded store in industries outside automotive parts and accessories and to expand beyond our core “do-it-yourself” (“DIY”) customer base into “business to business” and “do-it-for-me” (“DIFM”) customers, and these expansion efforts may fail. |

| ● | We are highly dependent upon key product vendors. Sales of products sourced from our top ten product vendors represented approximately 33.4% of our total revenue during the fiscal year ended December 31, 2020. Our ability to source products from product vendors in amounts and on terms acceptable to the Company is dependent upon factors that are beyond our control. |

| ● | We source a majority of our private label products, and our product vendors acquire a majority of their products, from manufacturers and distributors located in Taiwan and China. We do not have any long-term contracts or exclusive agreements with our foreign product vendors that would ensure our ability to source the types and quantities of products we desire at acceptable prices and in a timely manner or that would allow us to rely on customary indemnification protection with respect to any third-party claims similar to some of our U.S. product vendors. |

| ● | We may not be able to properly enforce our agreements with contractors, service providers or product vendors in international markets. |

| ● | We face intense competition and operate in an industry with limited barriers to entry, and some of our competitors may have greater resources than us and may be better positioned to capitalize on the growing online automotive aftermarket parts and accessories market. |

iii

| ● | Any failure to maintain the privacy and security of information, including personally identifiable information relating to our customers, employees and vendors, whether as a result of cybersecurity attacks on our information systems or otherwise, could damage our reputation, result in litigation or other legal actions against us, cause us to incur substantial additional costs, and materially adversely affect our business, financial condition and results of operations. |

| ● | System failures, including failures due to natural disasters or other catastrophic events, could prevent access to our digital commerce platform, which could reduce our net sales and harm its reputation. |

| ● | If we are unable to protect our intellectual property rights, our reputation and brand could be impaired and we could lose customers. |

| ● | Claims of intellectual property infringement by parts manufacturers, distributors or retailers to the validity of aftermarket parts and accessories or related marketing materials could adversely affect our business. |

| ● | We are subject to environmental laws, rules, and regulations, which may adversely impact our operations, and the failure to comply could result in harm to our reputation and could lead to fines and other penalties, including restrictions on the importation of our products into, or the sale of its products in, one or more jurisdictions until compliance is achieved. |

| ● | Our business could be adversely affected by an ongoing legal proceeding with certain stockholders, and because we are involved in litigation from time to time and is subject to numerous laws and governmental regulations, we could incur substantial judgments, fines, legal fees and other costs as well as reputational harm. |

| ● | We will incur significantly increased expenses and administrative burdens as a public company, which could have an adverse effect on our business, financial condition and results of operations. |

| ● | We depend on third-party delivery services to deliver products to our customers on a timely and consistent basis, and any deterioration in our relationship with any one of these third parties or increases in the fees that they charge could harm our reputation and adversely affect our business and financial condition. |

| ● | Shipping is a critical part of our business and any changes in, or disruptions to, our shipping arrangements could adversely affect our business, financial condition, and results of operations. Further, customers’ increasing demands for free shipping of products could adversely impact the growth of our business. |

| ● | We rely on our bandwidth and data center providers and other third parties to provide products to our customers, and any failure or interruption in the services provided by these third parties could disrupt our business and cause us to lose customers. |

| ● | Demand for the products we sell may be affected by the number of older vehicles in service. Vehicles seven years old or older are generally no longer under the original vehicle manufacturers’ warranties and tend to need more maintenance and repair than newer vehicles. |

| ● | Demand for the products we sell may be affected by the number of miles vehicles are driven annually. Higher vehicle mileage increases the need for maintenance and repair. Mileage levels may be affected by gas prices, ride sharing, the COVID-19 pandemic and related restrictions to slow its spread and other factors. |

| ● | If commodity prices such as fuel, plastic and steel increase, our margins may be negatively impacted. |

iv

PART I

Item 1. Business

The following discussion reflects, and “we,” “us,” “our” the “Company” and “PARTS iD” generally refer to, the business of Onyx Enterprises Int’l, Corp. prior to giving effect to the Business Combination and PARTS iD, Inc. after giving effect to the Business Combination, as the context indicates, unless the context otherwise refers to Legacy Acquisition Corp.

Introductory Note

On November 20, 2020 (the “Closing Date”), PARTS iD, Inc., a Delaware corporation (f/k/a Legacy Acquisition Corp. (“Legacy”)) (the “Company” or “PARTS iD”), consummated the previously announced business combination pursuant to that certain Business Combination Agreement, dated September 18, 2020 (the “Business Combination Agreement”), by and among the Company, Excel Merger Sub I, Inc., a Delaware corporation and an indirect wholly owned subsidiary of the Company and directly owned subsidiary of Merger Sub 2 (“Merger Sub 1”), Excel Merger Sub II, LLC, a Delaware limited liability company and direct wholly owned subsidiary of the Company (“Merger Sub 2”), Onyx Enterprises Int’l, Corp., a New Jersey corporation (“Onyx”), and Shareholder Representative Services LLC, a Colorado limited liability company, solely in its capacity as the stockholder representative pursuant to the terms of Section 11.16 of the Business Combination Agreement.

At the closing of the transactions contemplated by the Business Combination Agreement (the “Closing”), (a) Merger Sub 1 merged with and into Onyx (the “First Merger”), with Onyx surviving as a direct wholly-owned subsidiary of Merger Sub 2, and (b) promptly following the First Merger, Onyx, as the surviving company of the First Merger, merged with and into Merger Sub 2 (the “Second Merger”). Upon the consummation of the Second Merger, Merger Sub 2 was the surviving company and Onyx ceased to exist, and Merger Sub 2 became a direct, wholly owned subsidiary of the Company (collectively with the other transactions described in the Business Combination Agreement, the “Business Combination”). On the Closing Date, (i) Legacy changed its name from Legacy Acquisition Corp. to PARTS iD, Inc. and listed its shares of Class A common stock, par value $0.0001 per share (the “Class A Common Stock”) on the NYSE under the symbol “ID” and (ii) Merger Sub 2 changed its name to PARTS iD, LLC (“PARTS iD, LLC”).

Available Information

Our website address is www.partsidinc.com. Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, as well as any amendments to those reports, are available free of charge through our website as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. In addition, our code of ethics, audit committee charter, compensation committee charter, nominating and corporate governance committee charter and strategy, technology and risk management committee charter are available free of charge on our website. The public may read materials we file with the SEC, including reports, proxy and information statements, and other information, on the Internet site maintained by the SEC. The address of that site is www.sec.gov.

The above references to our website and the SEC’s website do not constitute incorporation by reference of the information contained on the websites and such information should not be considered part of this document.

Overview

PARTS iD, Inc. is a technology-driven, digital commerce company focused on creating custom infrastructure and unique user experiences within niche markets. The Company was founded in 2008 with a vision of creating a one-stop digital commerce destination for the automotive parts and accessories market. Management believes that the Company has since become a market leader and proven brand-builder, fueled by its commitment to delivering an engaging shopping experience; comprehensive, accurate and varied product offerings; and continued digital commerce innovation.

At its core, the Company’s technology solution is a data and information platform that enables and facilitates a differentiated digital commerce experience within complex product markets, as opposed to a pure digital commerce or electronics retailer. The deep technology platform that we have built integrates software engineering with catalog management, data intelligence, mining and analytics, along with user interface development that utilizes distinctive rules-based parts fitment software capabilities. In order to handle the ever-growing need for accurate automotive product and parts data, the Company has utilized cutting-edge computational and software engineering techniques, including Bayesian classification, to enhance and improve data records and product information and also deliver an engaging user experience. The technology platform also offers the Company fungibility, which was demonstrated by the fact that it was able to launch seven new verticals in August 2018.

1

Through the journey of building a comprehensive and complex product portfolio with over 17 million SKUs, as well as building an end-to-end digital commerce platform, the Company has developed a platform for both digital commerce and fulfillment, relying on insights gleaned from nearly 14 billion data points related to vehicle parts, a virtual shipping network comprising over 2,500 locations, nearly 5,000 active brands, and machine-learning algorithms for complex fitment industries such as vehicle parts and accessories.

While the Company’s platform has been initially focused on automotive parts and accessories, management believes the Company’s platform is scalable and can be applied to other complex, multi-dimensional fitment, product portfolio industries, in addition to the seven new parts and accessories verticals — semi truck, motorcycle, powersports, RV/camper, boating, recreation and tools — that we launched in August 2018.

The Company has positioned these verticals under its existing “iD” brand and believes this will drive brand loyalty among customers and reputation among vendors, ultimately increasing online traffic, brand visibility, and customer orders for adjacent markets. The Company has since experienced growth in revenue related to the new verticals, our original equipment (“OE”) business, and our repair parts business.

Customer service is a key aspect of the experience the Company offers to its customers throughout their buying journey. The Company has specialized customer support teams which assist customers in navigating through the platform, addressing any technical questions, order tracking and completing the order.

Digital Commerce Platform

The Company’s digital commerce platform was developed in-house from inception as a solution for industries with data limitations and parts fitment complexities, all while making processes simpler and more efficient. A core differentiator of the Company’s digital commerce platform is its purpose-built and proprietary data catalog developed over more than a decade by collecting, analyzing and refining data regarding original equipment manufacturer, or OEM, vehicles and aftermarket products and customer feedback to define a universe of accurate Year-Make-Model, or YMM, values. Management believes this functionality creates a unique user experience path that drives purchase intelligence and increases consumer confidence and trust.

2

The Company’s in-house data catalog houses nearly 14 billion data points for automobiles and the Company’s other seven verticals. This data catalog is designed to tie vehicles with parts that fit their specific YMM, including the variations of sub-model, engine size, transmission type and drivetrain type, as well as to recommend complementary products, such as tools required to install purchased parts and accessories. To build its catalog, the Company aggregates data from multiple sources, cross-pollinates this data to address any gaps in data sets, enriches the catalog using its proprietary internal data, then applies artificial intelligence to make further improvements. Through this process, the Company’s data catalog is able to: (i) determine the exact parts fitment for a product by its parameters, even if certain fitment details are originally missing in manufacturers’ data feeds; and (ii) rapidly incorporate new SKUs as they become available. Because its data catalog is continually expanding with each customer interaction, the Company also is able to offer better purchase recommendations, increase up-sell opportunities, improve the efficiency of its fulfillment operations, and lower errors and mistakes in orders. These economic and commercial advantages result in a fly-wheel effect that increases operating leverage and momentum. Because the cost of operating the Company’s data catalog is largely fixed, the Company has been able to expand its customer offerings into adjacent categories at relatively low incremental costs. The Company’s in-house catalog and deep understanding of fitment data helps offer a personalized and tailored experience to its diverse customer base of DIY, DIFM and PRO (mechanics) customers. For example, the Company can offer its DIFM consumers the ability to research and choose from a wide variety of tires, and in the same transaction select a tire installation center (2,117 locations available as of February 28, 2021) near them and schedule an appointment. The Company is committed to providing an enhanced customer experience and becoming a one-stop shop and seamless solution for all vehicle enthusiast needs.

Product Vendors

The Company provides its product vendors with access to its large customer base and e-commerce market. The Company’s 1000+ product vendors can leverage the Company’s disruptive technology, enhanced fitment data, deep understanding of the market and large customer database to sell and position their innovative product catalog instantly. Product vendors can benefit from the Company’s engaging shopping experience, advanced 3D imagery, in-depth product description, reviews, installation guides and other tailored content offered by the Company’s platform, complemented by specialized customer service.

Fulfillment Operations

The Company’s virtual, proprietary and capital-efficient fulfillment model manages our sales volume while carrying minimal inventory, which is primarily associated with its private label products. The Company’s platform, which incorporates live or frequently updated inventory feeds from our product vendors, provides stock-on-hand for more than 17 million products across nearly 5,000 brands. The Company’s fulfillment model decides which product vendor to source from while the sale is made based on a proprietary algorithm, which incorporates factors such as availability of inventory, customer proximity, shipping cost and profitability.

This decentralized, data-driven approach allows the Company to increase delivery speed through more than 2,500 shipping points from its U.S. vendor network.

Products

The Company primarily sells automotive parts and accessories, including a wide range of goods from automobile accessories, wheels and tires, performance parts, lighting and repair parts. In addition, the Company launched seven new verticals in August 2018 and, in 2020, the value of the orders received from these new verticals grew to approximately 10% of the Company’s total order value. These seven new verticals offer parts and accessories for semi-trucks, motorcycles, powersports (including ATVs, snowmobiles and personal watercraft), RVs/campers, boats, recreation (including outdoor sports and camping gear) and tools using the same proprietary platform.

The Company primarily sources its products from industry leading brands and product vendors located in the U.S., except that its private label products are largely sourced from foreign product vendors. Regarding sales of products sourced from our product vendors, no single product vendor accounted for more than 10% of the Company’s total revenue for the year ended December 31, 2020. The Company’s inventory on hand, which largely relates to private label products, has generally remained below $1.0 million in value. As of December 31, 2020 and December 31, 2019, the sale value of customers’ unshipped and undelivered orders were $16.2 million and $8.6 million, respectively.

Private Label Product. The Company’s private label business uses proprietary data to identify, import and sell higher margin products that are in demand on its platform. Management believes that by selecting and pairing a superior import product with its purpose-built and proprietary data catalog, consumers are provided the option to purchase a high-quality product at a reasonable cost. Private label revenue was less than 10% of the Company’s total revenue for the year ended December 31, 2020.

3

Branded Product. The Company has developed and implemented application-programming interfaces with the majority of its drop-ship product vendors that allow it to electronically transmit orders, check inventory availability, and receive the shipment tracking information and share it with its customers. These processes allow the Company to offer nearly 5,000 brands on an inventory-free basis, thereby reducing carrying costs and improving margins.

Industry and Market Opportunity

The Company’s management believes the U.S. aftermarket automotive market is massive, fragmented, and ripe for disruption as overall consumer preferences are increasingly shifting to online transactions. Although the ultimate impacts of the COVID-19 pandemic remain uncertain and consumer demand for automobile parts and accessories may be impacted in a recessionary environment, a recent survey published by Capgemini SE, a consulting corporation, found that 46% of U.S. adults surveyed plan to use their cars more often and public transportation less often in the future. Additionally, the pandemic is accelerating trends of online shopping more broadly as consumers seek to avoid physical retail locations.

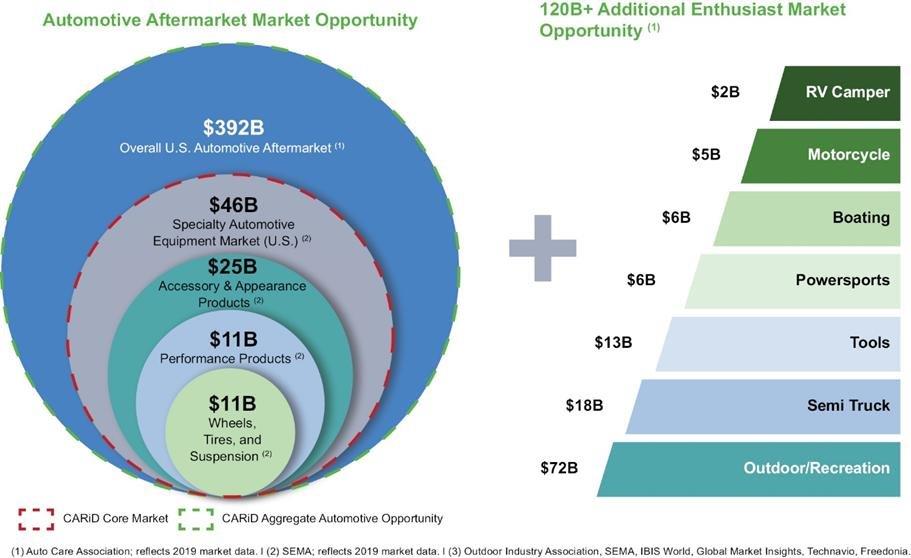

In 2020, the domestic automotive aftermarket market opportunity was estimated to be approximately $392 billion. The Company has historically focused on the $46 billion specialty automotive equipment market, but is seeking to accelerate its growth through automotive repairs, targeted international expansion and the addition of new verticals. The Company’s other product verticals present an aggregate market opportunity exceeding $120 billion in 2020.

Marketing

Management believes its customers’ core need is to find the right parts that fit their vehicle at the best price and are delivered on time. Our marketing strategies are designed around customer acquisition and retention which includes paid and non-paid advertising. Our paid advertising primarily includes search engine marketing, display, paid social media, connected TV (CTV) and paid partnerships. Our non-paid advertising efforts include search engine optimization, non-paid social media and e-mail marketing.

4

The Company currently drives traffic to its platform primarily with search engines; 77% of the Company’s traffic and 66% of its revenue in 2020 was acquired in this manner. Once on the platform, customers are presented with the Company’s proprietary marketing and product content that is created via in-house, multi-step image and video processing. Automated image refinement and the Company’s creative design team work to ensure consistency and quality across all content, including the product images presented to customers on the Company’s platform. Product pages on the Company’s platform present customers with multiple, customized product choices, plus cross-sell and up-sell opportunities, as well as training materials, product comparison information, installation instructions and customer reviews. Customers have the option to shop and explore on the Company’s platform in multiple ways, including by part number, brand or product category.

Competition

The parts and accessories industries in which the Company sells its products are competitive and fragmented, and products are distributed through multi-tiered and overlapping channels. The Company competes with both online and offline sellers that offer parts and accessories, repair parts and OEM parts to either the DIY or the DIFM consumer groups. Current or potential competitors include (i) online retailers, including both niche retailers of uncommon, highly specialized products and general retailers of a larger number of broadly available products; (ii) national parts retailers such as Advance Auto Parts, AutoZone, NAPA and O’Reilly Auto Parts; (iii) internet-based marketplaces such as Amazon.com and eBay.com; (iv) discount stores and mass merchandisers; (v) local independent retailers; (vi) wholesale parts distributors and (vii) manufacturers, product vendors and other distributors selling online directly to consumers. The Company faces significant competition from these and other retailers in the United States and abroad. The majority of these competitors are, and will be, substantially larger than the Company, and have substantially greater resources and operating histories. There can be no assurance that the Company will be able to keep pace with the technological or product developments of its competitors. These companies also compete with the Company in recruiting and retaining highly qualified technical and professional personnel and consultants.

Competitive factors in the markets the Company serves include fitment data and related intelligence, technology, customer experience, customer service, range of product offerings, product availability, product quality, price and shipping speed. Management believes its custom-built tech-stack for the complex, multi-dimensional automotive parts and accessories industry, which offers nearly 5,000 brands and more than 17 million unique SKUs, provides it with a unique competitive advantage.

Intellectual Property

The Company owns a number of trade names, service marks and trademarks, including “iD,” “CARiD,” “BOATiD,” “MOTORCYCLEiD,” “CAMPERiD,” “POWERSPORTSiD,” “TOOLSiD,” “TRUCKiD,” “RECREATIONiD” and more, for use in connection with its business. In addition, the Company owns and has registered trademarks for certain of its private label brands. Management believes these trade names, service marks and trademarks are important to the Company’s sales and marketing strategy.

5

Environmental Matters

The Company is subject to various federal, state and local laws and governmental regulations relating to the operation of its business, including those governing the use and transportation of hazardous substances and emissions-related standards, established by the United States Environmental Protection Agency (the “EPA”), and similar state-level regulators, including the California Air Resources Board (“CARB”).

While the Company has processes in place to ensure that products are sold in compliance with the requirements imposed by the EPA and similar state-level regulators, all verification processes have inherent limitations. The Company has been, is currently, and may in the future be the subject of regulatory proceedings initiated by the EPA, CARB or other applicable regulatory bodies, and the results of such proceedings are uncertain. For additional information, see Note 6 of Notes to Consolidated Financial Statements.

Although management believes that the Company is in substantial compliance with currently applicable environmental laws, rules, and regulations, it is unable to predict the ultimate impact of adopted or future laws, rules, and regulations on its business, properties or products. Such laws, rules, or regulations may cause the Company to incur significant expenses to achieve or maintain compliance, may require it to modify its product offerings, may adversely affect the price of or demand for some of its products, and may ultimately affect the way the Company conducts its operations. Failure to comply with these current or future laws, rules, or regulations could result in harm to the Company’s reputation and/or could lead to fines and other penalties, including restrictions on the importation of the Company’s products into, or the sale of its products in, one or more jurisdictions until compliance is achieved.

Seasonality

The Company’s revenue is relatively evenly distributed throughout the year, although sales typically spike during the spring months upon the distribution to the general public by the IRS of income tax refunds and during the winter holiday season. While the Company expects to be able to maintain sales growth through seasonality, it recognizes that future revenues may be affected by these seasonal trends as well as cyclical trends affecting the overall economy, especially the automotive parts and accessories industry.

Employees

As of December 31, 2020, the Company employed 108 full-time employees, all in the United States. None of the Company’s employees are represented by a labor union, and management believes that the Company’s relations with its employees are good.

Certain call center, development, and back-office services are provided by independent contractors in Ukraine, Belarus, Philippines and Costa Rica.

6

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

The following table sets forth certain information with respect to our executive officers as of March 5, 2021.

| Name | Age | Title | ||

| Antonino Ciappina | 39 | Chief Executive Officer | ||

| Kailas Agrawal | 63 | Chief Financial Officer | ||

| Ajay Roy | 38 | Chief Operating Officer | ||

| Mark Atwater | 61 | Vice President of Vendor Relations |

Antonino Ciappina served as Onyx’s Interim General Manager from July 2020 until the Closing of the Business Combination in November 2020 and has served as the Company’s Chief Executive Officer since the Closing. Upon joining Onyx in January 2020, Mr. Ciappina served as Chief Marketing Officer and directed efforts related to marketing, customer acquisition and retention, pricing optimization, advertising, creative services, market research, analytics and public relations for the portfolio of iD brands. Prior to joining Onyx, Mr. Ciappina served in various digital marketing and e-commerce positions, most recently as Senior Director, E-Commerce & Digital Marketing at Foot Locker from May 2018 to December 2019, as Vice President, E-Commerce & Digital Marketing at Firestar Diamond Group from June 2017 to May 2018 and as Director, Digital Marketing & Customer Acquisition at The Children’s Place from April 2015 to June 2017. Mr. Ciappina earned his Bachelor of Science degree in Business Administration, Marketing and International Business from Montclair State University.

Kailas Agrawal served as Onyx’s Chief Financial Officer from January 2018 until the Closing of the Business Combination in November 2020 and has served as the Company’s Chief Financial Officer since the Closing. Prior to joining Onyx, Mr. Agrawal served as Chief Financial Officer at In Colour Capital (during this period, he functioned as the Chief Financial Officer of Onyx), an independent principal investment group, from January 2016 to December 2017 and as Principal Financial Consultant with KSS Consulting, Inc. from May 2014 to December 2015. Additionally, Mr. Agrawal has gained international experience while serving in various positions for multiple organizations across the United States, Canada, and India, including as Regional Chief Financial Officer of Minacs Worldwide, Inc. Mr. Agrawal’s experience spans numerous industries such as information technology services, food distribution, real estate, agricultural processing and manufacturing. Mr. Agrawal earned a designation as a Chartered Accountant from the Institute of Chartered Accountants of India in addition to obtaining a Bachelor of Commerce from the University of Mumbai.

Ajay Roy served as Onyx’s Chief Operating Officer from October 2019 until the Closing of the Business Combination in November 2020 and has served as the Company’s Chief Operating Officer since the Closing. Prior to joining Onyx, Mr. Roy served as Senior Vice President of Operations at Moda Operandi, Inc., an online fashion retailer, from September 2018 to August 2019 and General Manager of Global Supply Chain and Operations at Wayfair, Inc., an online furniture and home-goods retailer, from August 2017 to August 2018. Additionally, Mr. Roy gained extensive management experience while serving as Vice President of ToolsGroup, Inc., a global provider of service-driven supply chain planning and demand analytics software, from 2013 to August 2017 and as a Management Consultant with Deloitte Consulting. Mr. Roy earned his Master’s in Business Administration from SP Jain School of Management and a Bachelor of Engineering in Computer Engineering from the MS Ramaiah Institute of Technology.

Mark Atwater served as Onyx’s Vice President of Vendor Relations from October 2016 until the Closing of the Business Combination in November 2020 and has served as the Company’s Vice President of Vendor Relations the Closing. As Vice President of Vendor Relations, Mr. Atwater is responsible for the leadership of the Vendor Relations Department, management of Onyx’s vendor partners, pricing strategy, new product category development and carrier logistics. Since joining Onyx in 2011, Mr. Atwater has served in a variety of positions including General Manager and Director of Vendor Relations. Prior to joining Onyx, while serving in a variety of positions in the automotive industry, Mr. Atwater obtained experience in negotiating, purchasing, logistics and distribution, warehouse management, retail store management, automotive sales and e-commerce sales.

7

Item 1A. Risk Factors

Our business, financial condition and results of operations could be materially adversely affected by a number of factors. In addition to the factors discussed elsewhere in this report, the following risks and uncertainties could materially harm our business, financial condition or results of operations, including causing our actual results to differ materially from those projected in any forward-looking statements. The following list of significant risk factors is not all-inclusive or necessarily in order of importance. Additional risks and uncertainties not presently known to us, or that we currently deem immaterial, also may materially adversely affect us in future periods. You should carefully consider these risks and uncertainties before investing in our securities.

Risks Related to the COVID-19 Pandemic

The global COVID-19 pandemic could harm the Company’s business, results of operations, financial condition and liquidity.

The global spread of COVID-19 and related measures to contain its spread (such as government-mandated business closures and shelter-in-place guidelines) have created significant volatility, uncertainty and economic disruption. Although the COVID-19 pandemic and related measures to contain its spread have not adversely affected the Company’s results of operations to date, they have adversely affected certain components of the Company’s business, including by increasing cancellations (which can result in an increase in advertisement costs) and shipping times. The extent to which the COVID-19 pandemic impacts the Company’s business, results of operations, financial condition and liquidity in the future will depend on numerous evolving factors that it cannot predict, including the duration and scope of the pandemic; any resurgence of the pandemic; governmental, business and individuals’ actions that have been and continue to be taken in response to the pandemic; the impact of the pandemic on national and global economic activity, unemployment levels and financial markets; the potential for shipping difficulties, including slowed deliveries to customers; the potential for increased cancellations by customers; and the ability of consumers to pay for products. Although consumer demand for and the inventory of the Company’s products have remained stable, the COVID-19 pandemic has generally resulted in a decrease in consumer spending with respect to the wider economy, which in the future could have an adverse impact on the Company through reduced consumer demand for or inventory of its products. Additionally, the COVID-19 pandemic has caused the Company to require employees to work remotely for an indefinite period of time, which could negatively impact its business and harm productivity and collaboration. If there is a prolonged impact of COVID-19, it could adversely affect the Company’s business, results of operations, financial condition and liquidity, perhaps materially. The future impact of COVID-19 and these containment measures cannot be predicted with certainty and may increase the Company’s borrowing costs, if any, and other costs of capital and otherwise adversely affect its business, results of operations, financial condition and liquidity, and the Company cannot assure that it will have access to external financing at times and on terms it considers acceptable, or at all, or that it will not experience other liquidity issues going forward.

To the extent the COVID-19 pandemic adversely affects the Company’s business, results of operations, financial condition or liquidity, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section.

Risks Related to the Company’s Business and Industry

The Company depends on search engines and other online sources to attract visitors to its digital commerce platform, and if the Company is unable to attract these visitors and convert them into customers in a cost-effective manner, its business and results of operations will be harmed.

The Company’s success depends on its ability to attract customers in a cost-effective manner. The Company’s investments in marketing may not effectively reach potential consumers or those consumers may not decide to buy from it or the volume of consumers that purchase from it may not yield the intended return on investment. In order to drive traffic to its digital commerce platform, the Company relies on relationships with providers of online services, search engines, shopping comparison sites and marketplace sites to provide content, advertising banners and other links. In particular, the Company relies on Google as an important marketing channel, and if Google changes its algorithms or if competition increases for advertisements on Google or the Company’s other marketing channels, the Company may be unable to cost-effectively attract customers to its products. During the year ended December 31, 2020, 51.1% of the Company’s revenue was directly attributable to organic and paid traffic from Google.

8

In addition, many of the parties with whom the Company has online-advertising arrangements could provide advertising services to other companies, including retailers with whom the Company competes. As competition for online advertising has increased, the cost for these services has also increased. With the growing awareness of the importance of digital commerce channels, many of the Company’s competitors are investing to acquire customers at a much higher cost and with a much lower profitability threshold, including through free shipping and other loss leaders. A significant increase in the cost of the marketing channels, including a change in the proportion of paid and free traffic upon which the Company relies, could adversely impact its ability to attract customers in a cost-effective manner and harm its business and results of operations. Further, while the Company uses promotions as a way to drive sales, these promotional activities may not drive sales and may adversely affect its gross margins.

Similarly, if any free search engine, price comparison and shopping engine, or marketplace site on which the Company relies begins charging fees for listing or placement, or if one or more of the search engines, price comparison and shopping engines, marketplace sites or other online sources on which the Company relies for purchased listings increases their fees, or modifies or terminates its relationship with the Company, including by restricting certain categories of products, the Company’s expenses could rise, it could lose customers, and traffic to its digital commerce platform could decrease. Moreover, if the use of price comparison and shopping engines by consumers continues to increase in popularity, the Company may face increased pricing pressure or suffer reduced sales as consumers are more readily able to price compare among online shopping platforms.

The Company’s recent growth rates may not be sustainable or indicative of its future growth.

The Company experienced significant growth in recent periods. This rate of growth may not be sustainable or indicative of the Company’s future rate of growth. The Company believes that its continued growth will depend upon the success of its multiple initiatives and continuation of higher traffic and conversion rates, which primarily depend on (i) customer experiences, (ii) the economy and customers’ disposable income, (iii) the Company’s product offerings, product pricing and fulfillment, (iv) shipping speed and cost optimization, (v) the Company’s competitive position in the aftermarket parts supply, (vi) changes in search engine algorithms affecting the Company’s website’s search engine optimization, and (vii) vendor supplies and vendor performance.

If the Company is unable to manage the challenges associated with its international operations, the growth of its business could be limited and its business could suffer.

The Company maintains international business operations in Ukraine, Belarus, the Philippines and Costa Rica. This international operation includes development and maintenance of the Company’s websites and call center and back-office support services. The Company is subject to a number of risks and challenges that specifically relate to its international operations. The Company’s international operations may not be successful if it is unable to meet and overcome these challenges, which could limit the growth of its business and may have an adverse effect on its business and operating results. These risks and challenges include:

| ● | difficulties and costs of staffing and managing foreign operations, including any impairment to its relationship with contractors, including the lead contractor of the Company’s Ukraine operations, as well as service providers controlled by that lead contractor; |

| ● | changes in operating costs charged by the Company’s Ukrainian service providers, who are controlled by the Company’s lead contractor in Ukraine; |

| ● | increasing competition with respect to technology resources in Ukraine, leading to higher costs and higher attrition; |

| ● | restrictions imposed by local labor practices and laws on its business and operations; |

| ● | exposure to different business practices and legal standards; |

| ● | unexpected changes in regulatory requirements; |

| ● | the imposition of government controls and restrictions; |

| ● | political, social and economic instability and the risk of war, terrorist activities or other international incidents; |

| ● | the failure of telecommunications and connectivity infrastructure; |

9

| ● | natural disasters and public health emergencies, including the ongoing COVID-19 pandemic; and |

| ● | potentially adverse tax consequences, including the possible imposition of increased withholding taxes or the re-classification of contractors as employees under local law. |

The Company’s growth strategy is dependent upon its ability to expand its “iD” branded store in industries outside automotive parts and accessories and to expand beyond its core DIY customer base into “business to business” and DIFM customers.

While the Company’s digital commerce platform initially focused solely on automotive parts and accessories, management believes its platform is scalable. Accordingly, management believes that its application to other complex product portfolio industries, including the seven parts and accessories verticals launched in August 2018 under the “iD” brand (i.e., semi-truck, motorcycle, powersports, RV/camper, boating, recreation and tools), will continue to drive brand loyalty among customers and reputation among vendors and increase customer orders from adjacent markets. However, the Company can provide no assurance that this strategy will continue to be successful. In future periods, the Company’s parts and accessories verticals may fail to attract new customers or appeal to the Company’s existing customers of automotive products, or the customers of each vertical may be more segmented than the Company expects, thereby limiting its ability to develop cross-vertical brand loyalty. The Company may also struggle to populate its new verticals with a comprehensive assortment of products, which management believes is important to attract and retain customers. Additionally, within the automotive parts and accessories space, the Company’s growth strategy is focused on expanding beyond its core DIY customer base by increasing business-to-business sales and sales to DIFM customers. These prospective customers may not be receptive to the Company’s marketing efforts, product offerings, or current speed of fulfillment or shipping, or may remain committed to using their existing product vendors. If for these or other reasons the Company is unable to continue to execute its growth strategy, its results of operations and financial conditions could be adversely affected.

Purchasers of aftermarket automotive parts and accessories may not choose to shop online, which would prevent the Company from acquiring new customers who are necessary to the growth of its business.

The online market for automotive parts and accessories is less developed than the online market for many other business and consumer products and currently represents only a small part of the overall automotive parts and accessories market. The Company’s success will depend in part on its ability to attract new customers and to convert customers who have historically purchased automotive parts and accessories through traditional retail and wholesale operations. Specific factors that could discourage or prevent prospective customers from purchasing from the Company include:

| ● | concerns about buying automotive parts and accessories without face-to-face interaction with sales personnel; |

| ● | the inability to physically handle, examine and compare products; |

| ● | delivery time associated with internet orders; |

| ● | concerns about the security of online transactions and the privacy of personal information; |

| ● | delayed shipments or shipments of incorrect or damaged products; |

| ● | increased shipping costs; |

| ● | the inconvenience associated with returning or exchanging items purchased online; and |

| ● | limited or no installation options or support for many products purchased online. |

If the online market for automotive parts and accessories does not gain widespread acceptance, the Company’s sales may decline and its business and financial results may suffer.

10

If demand for the Company’s products slow, then its business may be materially adversely affected.

Demand for the products the Company sells may be affected by a number of factors it cannot control, including:

| ● | the number of older vehicles in service. Vehicles seven years old or older are generally no longer under the original vehicle manufacturers’ warranties and tend to need more maintenance and repair than newer vehicles. |

| ● | the economy. In periods of declining economic conditions, consumers may reduce their discretionary spending by deferring vehicle maintenance or repair. Additionally, such conditions may affect the Company’s customers’ ability to obtain credit. During periods of expansionary economic conditions, more of the Company’s DIY customers may pay others to repair and maintain their vehicles instead of working on their own vehicles, or they may purchase new vehicles. |

| ● | the weather. Milder weather conditions may lower the failure rates of automotive parts, while extended periods of rain and winter precipitation may cause the Company’s customers to defer maintenance and repair on their vehicles. Further, drastic weather storms, such as hurricanes and winter storms, can have an immediate negative impact on the demand for the Company’s products. |

| ● | technological advances. Advances in automotive technology, such as electric vehicles, and parts design can result in cars needing maintenance less frequently and parts lasting longer. |

| ● | the number of miles vehicles are driven annually. Higher vehicle mileage increases the need for maintenance and repair. Mileage levels may be affected by gas prices, ride sharing, the COVID-19 pandemic and related restrictions to slow its spread and other factors. |

| ● | COVID-19 and the related increase in online shopping. Beginning in the second quarter of fiscal year 2020, the Company’s traffic and conversion rate increased substantially and its telephone calls to online traffic ratio decreased, each of which the Company’s management attributes to the COVID-19 pandemic and related restrictions to slow its spread. The Company’s financial projections assume its traffic and conversion rate will remain elevated going forward and its telephone calls to online traffic ratio will remain lower, so any reversal of these factors could cause the Company to fail to achieve its projections. |

| ● | the quality of the vehicles manufactured by original vehicle manufacturers and the length of the warranties or maintenance offered on new vehicles. |

| ● | restrictions on access to telematics and diagnostic tools and repair information imposed by the original vehicle manufacturers or by governmental regulation. These restrictions may cause vehicle owners to rely on dealers to perform maintenance and repairs. |

| ● | decreases in vehicle ownership due to wider adoption of on-demand transportation and ride sharing services. |

These factors could result in a decline in the demand for the Company’s products, which could adversely affect its business and overall financial condition.

The Company is dependent upon relationships with product vendors in Taiwan and China for the majority of its products.

The Company acquires a majority of its private label products, and its product vendors acquire a majority of their products, from manufacturers and distributors located in Taiwan and China. The Company does not have any long-term contracts or exclusive agreements with its foreign product vendors that would ensure its ability to acquire the types and quantities of products it desires at acceptable prices and in a timely manner or that would allow it to rely on customary indemnification protection with respect to any third-party claims similar to some of its U.S. product vendors.

In addition, because many of the Company’s direct and indirect product vendors are outside of the United States, additional factors could interrupt its relationships or affect the Company’s ability to acquire necessary products on acceptable terms, including:

| ● | political, social and economic instability and the risk of war or other international incidents in Asia or abroad; |

| ● | fluctuations in foreign currency exchange rates that may increase cost of products; |

11

| ● | imposition of duties, taxes, tariffs or other charges on imports; |

| ● | difficulties in complying with import and export laws, regulatory requirements and restrictions; |

| ● | natural disasters and public health emergencies, such as COVID-19; |

| ● | import shipping delays resulting from foreign or domestic labor shortages, slow-downs, or stoppages; |

| ● | the failure of local laws to provide a sufficient degree of protection against infringement of its intellectual property; |

| ● | imposition of new legislation relating to import quotas or other restrictions that may limit the quantity of its product that may be imported into the U.S. from countries or regions where it does business; |

| ● | financial or political instability in any of the countries in which its products are manufactured; |

| ● | potential recalls or cancellations of orders for any product that does not meet its quality standards; |

| ● | disruption of imports by labor disputes or strikes and local business practices; |

| ● | political or military conflict involving the United States or any country in which its product vendors are located, which could cause a delay in the transportation of its products, an increase in transportation costs and additional risk to product being damaged and delivered on time; |

| ● | heightened terrorism security concerns, which could subject imported goods to additional, more frequent or more thorough inspections, leading to delays in deliveries or impoundment of goods for extended periods; |

| ● | inability of its non-U.S. product vendors to obtain adequate credit or access liquidity to finance their operations; and |

| ● | its ability to enforce any agreements with its foreign product vendors. |

If the Company were unable to import products from China and Taiwan in a cost-effective manner or at all, it could suffer irreparable harm to its business and be required to significantly curtail its operations, file for bankruptcy or cease operations.

From time to time, the Company may also have to resort to administrative and court proceedings to enforce its legal rights with foreign product vendors. However, it may be more difficult to evaluate the level of legal protection the Company enjoys in Taiwan and China and the corresponding outcome of any administrative or court proceedings than in comparison to its product vendors in the United States.

The Company depends on third-party delivery services to deliver products to its customers on a timely and consistent basis, and any deterioration in its relationship with any one of these third parties or increases in the fees that they charge could harm its reputation and adversely affect its business and financial condition.

The Company relies on third parties for the shipment of products, including a single carrier for the majority of its shipping needs, and it cannot be sure that these relationships will continue on terms favorable to it, or at all. Shipping costs have increased from time to time, and may continue to increase, and the Company may not be able to pass these costs directly to its customers. Any increased shipping costs could harm the Company’s business, prospects, financial condition and results of operations by increasing its costs of doing business and reducing gross margins, which could negatively affect its operating results. In addition, the Company utilizes a variety of shipping methods for outbound logistics. For outbound logistics, the Company relies on “Less-than-Truckload,” or LTL, and parcel freight based upon the product and quantities being shipped and customer delivery requirements. These outbound freight costs have increased on a year-over-year basis and may continue to increase in the future. The Company also ships a number of oversized automotive parts and accessories, which may trigger additional shipping costs by third-party delivery services. Any increases in fees or any increased use of LTL would increase the Company’s shipping costs, which could negatively affect its operating results.

12

In addition, if the Company’s relationships with these third parties, especially the single carrier the Company relies upon for the majority of its shipping needs, are terminated or impaired, or if these third parties are unable to deliver products for the Company, whether due to a labor shortage, slow down or stoppage, deteriorating financial or business conditions, responses to the COVID-19 pandemic, terrorist attacks or for any other reason, the Company would be required to use alternative carriers for the shipment of products to its customers. Changing carriers could have a negative effect on the Company’s business and operating results due to reduced visibility of order status and package tracking and delays in order processing and product delivery, and it may be unable to engage alternative carriers on a timely basis, upon terms favorable to it, or at all.

The Company relies on bandwidth and data center providers and other third parties to provide products to its customers, and any failure or interruption in the services provided by these third parties could disrupt its business and cause it to lose customers.

The Company relies on third-party vendors, including data center and bandwidth providers. Any disruption in the network access or co-location services, which are the services that house and provide internet access to the Company’s servers, provided by these third-party providers or any failure of these third-party providers to handle current or higher volumes of use could significantly harm the Company’s business. Any financial or other difficulties the Company’s providers face may have negative effects on the Company’s business, the nature and extent of which cannot be predicted. The Company exercises little control over these third-party vendors, which increases its vulnerability to problems with the services they provide.

The Company also licenses technology from third parties, including software packages, ERP systems, system applications, hosting services, and related databases, to facilitate elements of its digital commerce platform, back-office support and accounting systems. The Company has experienced and expects to continue to experience interruptions and delays in service and availability for these elements. Any errors, failures, interruptions or delays experienced in connection with these third-party technologies could negatively impact the Company’s relationship with its customers and adversely affect its business. The Company’s systems also heavily depend on the availability of electricity, which also comes from third-party providers.. Information systems such as the Company’s may be disrupted by even brief power outages, or by the fluctuations in power. This could disrupt the Company’s business and cause it to lose customers.

The Company is highly dependent upon key product vendors.

The Company’s top ten product vendors represented approximately 33.4% of its total revenue during the fiscal year ended December 31, 2020. The Company’s ability to acquire products from its product vendors in amounts and on terms acceptable to it is dependent upon a number of factors that could affect its product vendors and which are beyond its control. For example, financial or operational difficulties that some of the Company’s product vendors may face could result in an increase in the cost of the products the Company purchases from them. If the Company does not maintain its relationships with its existing product vendors or develop relationships with new product vendors on acceptable commercial terms, it may not be able to continue to offer a broad selection of merchandise at competitive prices and, as a result, it could lose customers and its sales could decline.

The Company outsources the distribution and fulfillment operation for most of the products it sells and is dependent on drop-ship product vendors to manage inventory, process orders and distribute those products to its customers in a timely manner. For the fiscal year ended December 31, 2020, products shipped by drop-ship product vendors represented the vast majority of the Company’s total revenue. Because the Company outsources a number of traditional retail functions to product vendors, it has limited control over how and when orders are fulfilled. The Company also has limited control over the products that its product vendors purchase or keep in stock. The Company’s product vendors may not accurately forecast the products that will be in high demand or they may allocate popular products to other resellers, resulting in the unavailability of certain products for delivery to the Company’s customers. Any inability to offer a broad array of products at competitive prices and any failure to deliver those products to the Company’s customers in a timely and accurate manner may damage the Company’s reputation and brand and could cause it to lose customers and its sales to decline.

13

In addition, the increasing consolidation among automotive parts and accessories product vendors may disrupt or end the Company’s relationship with some product vendors, result in product shortages and/or lead to less competition and, consequently, higher prices. Furthermore, as part of its routine business, product vendors extend credit to the Company in connection with its purchase of their products. In the future, the Company’s product vendors may limit the amount of credit they are willing to extend to the Company in connection with its purchase of their products, including as a result of the Company’s public disclosure of its financial statements. If this were to occur, it could impair the Company’s ability to acquire the types and quantities of products that it desires from the applicable product vendors on acceptable terms, severely impact its liquidity and capital resources, limit its ability to operate its business and could have a material adverse effect on its financial condition and results of operations.

The Company is dependent on its product vendors to supply it with products that comply with safety and quality standards at competitive prices and to comply with the terms of their stated customer warranties.

The Company is dependent on its vendors continuing to supply quality products at favorable prices. If the Company’s merchandise offerings do not meet its customers’ expectations regarding safety and quality, it could experience lost sales, increased costs and exposure to legal and reputational risk. All of the Company’s product vendors must comply with applicable product safety laws, and the Company is dependent on them to ensure that the products its customers buy comply with all safety and quality standards. Events that give rise to actual, potential or perceived product safety concerns could expose the Company to government enforcement action and private litigation and result in costly product recalls and other liabilities. To the extent the Company’s product vendors are subject to additional governmental regulation of their product design and/or manufacturing processes, the cost of the merchandise it purchases may rise. In addition, negative customer perceptions regarding the safety or quality of the products the Company sells could cause its customers to seek alternative sources for their needs, resulting in lost sales. In those circumstances, it may be difficult and costly for the Company to regain the confidence of its customers.

The Company is also dependent on its product vendors to comply with the terms of their stated customer product warranties. To the extent that the Company’s product vendors fail to satisfy legitimate warranty claims asserted by the Company’s customers, the Company may be directly responsible for reimbursing such customers, which could have a material adverse effect on its financial condition and results of operations, particularly if one or more of the Company’s larger product vendors fails to honor its warranty obligations.

The Company is dependent on entities controlled by a lead contractor in Ukraine to recruit and manage its development team and back-office support, as well to provide a physical facility to its contractors.

Based on management’s knowledge, the Company’s lead contractor and his affiliate have sole authority to recruit and retain the Company’s information technology subcontractors, and own the physical facility in Ukraine at which such subcontractors report to work. Because substantially all of the Company’s information technology functions are performed in Ukraine, the Company is dependent on the lead contractor and his affiliate with respect to such functions. If these contractors or subcontractors fail to perform according to agreed-upon terms and timetables or terminate the arrangements under which they perform these functions, the Company may be unable to engage a substitute on commercially reasonable terms, or at all. This would likely result in temporary service disruptions and increased costs, which could have a material adverse effect on the Company’s business, results of operations and financial condition.

If the Company fails to offer a broad selection of products at competitive prices or fails to locate sufficient inventory to meet customer demands, its revenue could decline.

In order to expand its business, the Company must successfully offer, on a continuous basis, a broad selection of automotive parts and accessories that meet the needs of its customers. Products sold by the Company are used by consumers for a variety of purposes, including repair, performance, improved aesthetics and functionality. In addition, to be successful, the Company’s product offerings must be broad and deep in scope, competitively priced, well-made, innovative and attractive to a wide range of consumers. The Company cannot predict with certainty that it will be successful in offering products that meet all of these requirements. Moreover, even if the Company offers a broad selection of products at competitive prices, it must maintain access to sufficient inventory to meet consumer demand. If the Company’s product offerings fail to satisfy its customers’ requirements or respond to changes in customer preferences or if the Company otherwise fails to locate sufficient inventory to meet customer demands, its revenue could decline.

Shifting online consumer behavior regarding automotive parts and accessories could adversely impact the Company’s financial results and the growth of its business.

Shifting consumer behavior indicates that the Company’s customers are becoming more inclined to shop for automotive parts and accessories through their mobile devices. For the year ended December 31, 2020, approximately 49% of the Company’s revenue and 64% of its traffic was attributable to mobile customers. Mobile customers exhibit different behaviors than more traditional desktop-based e-commerce customers. User sophistication and technological advances have increased consumer expectations around the user experience on mobile devices, including speed of response, functionality, product availability, security, and ease of use. If the Company is unable to continue to adapt its mobile device shopping experience in ways that improve its customers’ mobile experience and increase the engagement of its mobile customers, the Company’s sales may decline and its business and financial results may suffer.

14

If commodity prices such as fuel, plastic and steel increase, the Company’s margins may be negatively impacted.

Increasing prices in the component materials for the parts the Company sells may impact the availability, the quality and the price of its products, as product vendors search for alternatives to existing materials and increase the prices they charge. The Company cannot ensure that it can recover all the increased costs through price increases, and its product vendors may not continue to provide a consistent quality of product as they may substitute lower cost materials to maintain pricing levels, all of which may have a negative impact on the Company’s business and results of operations.

The Company faces intense competition and operates in an industry with limited barriers to entry, and some of its competitors may have greater resources than it and may be better positioned to capitalize on the growing online automotive aftermarket parts and accessories market.

The parts and accessories industries in which the Company sells its products are competitive and fragmented, and products are distributed through multi-tiered and overlapping channels. The Company competes with both online and offline sellers that offer parts and accessories, repair parts and original equipment manufacturer parts to either the DIY or the DIFM consumer segments. Current or potential competitors include (i) online retailers, including both niche retailers of uncommon, highly specialized products and general retailers of a larger number of broadly available products; (ii) national parts retailers such as Advance Auto Parts, AutoZone, NAPA and O’Reilly Auto Parts; (iii) internet-based marketplaces such as Amazon.com and eBay.com; (iv) discount stores and mass merchandisers; (v) local independent retailers; (vi) wholesale parts distributors and (vii) manufacturers, product vendors and other distributors selling online directly to consumers.

Barriers to entry are low, and current and new competitors can launch websites at a relatively low cost. Many of the Company’s current and potential competitors have longer operating histories, larger customer bases, greater brand recognition and significantly greater financial, marketing, technical, management and other resources than it does. For example, in the event that online marketplace companies such as Amazon or eBay, who have larger customer bases, greater brand recognition and significantly greater resources than the Company does, focus more of their resources on competing in the automotive parts and accessories market, it could have a material adverse effect on the Company’s business and results of operations. In addition, some of the Company’s competitors have used and may continue to use aggressive pricing tactics and devote substantially more financial resources to website and system development than the Company does. The Company expects that competition will further intensify in the future as internet use and online commerce continue to grow worldwide. Increased competition may result in reduced sales, lower operating margins, reduced profitability, loss of market share and diminished brand recognition.