false2019FY000169402812/31P2YP3Y00016940282019-01-012019-12-31iso4217:USD00016940282019-06-28xbrli:shares0001694028us-gaap:CommonClassAMember2020-02-210001694028us-gaap:CommonClassBMember2020-02-210001694028us-gaap:CommonClassAMemberus-gaap:IPOMember2018-01-172018-01-170001694028us-gaap:CommonClassAMemberus-gaap:IPOMemberlbrt:LibertyInc.Member2018-01-172018-01-170001694028lbrt:IPOSharesFromExistingShareholdersMemberus-gaap:CommonClassAMember2018-01-172018-01-170001694028us-gaap:CommonClassAMember2018-01-172018-01-17iso4217:USDxbrli:shares0001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-01-012019-12-310001694028us-gaap:CommonClassAMember2019-01-220001694028us-gaap:MemberUnitsMembersrt:SubsidiariesMember2019-10-012019-12-310001694028lbrt:RiverstoneMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberus-gaap:CommonStockMember2019-10-012019-12-310001694028lbrt:RiverstoneMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberus-gaap:CommonStockMember2019-01-012019-01-310001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-12-3100016940282019-12-3100016940282018-12-310001694028us-gaap:CommonClassAMember2018-12-310001694028us-gaap:CommonClassAMember2019-12-310001694028us-gaap:CommonClassBMember2018-12-310001694028us-gaap:CommonClassBMember2019-12-3100016940282018-01-012018-12-3100016940282017-01-012017-12-310001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMember2018-12-310001694028us-gaap:AdditionalPaidInCapitalMember2018-12-310001694028us-gaap:RetainedEarningsMember2018-12-310001694028us-gaap:ParentMember2018-12-310001694028us-gaap:NoncontrollingInterestMember2018-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMember2019-01-012019-12-310001694028us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310001694028us-gaap:ParentMember2019-01-012019-12-310001694028us-gaap:NoncontrollingInterestMember2019-01-012019-12-310001694028us-gaap:RetainedEarningsMember2019-01-012019-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMember2019-12-310001694028us-gaap:AdditionalPaidInCapitalMember2019-12-310001694028us-gaap:RetainedEarningsMember2019-12-310001694028us-gaap:ParentMember2019-12-310001694028us-gaap:NoncontrollingInterestMember2019-12-310001694028us-gaap:MemberUnitsMember2017-12-310001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2017-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMember2017-12-310001694028us-gaap:AdditionalPaidInCapitalMember2017-12-310001694028us-gaap:RetainedEarningsMember2017-12-310001694028us-gaap:ParentMember2017-12-310001694028us-gaap:NoncontrollingInterestMember2017-12-3100016940282017-12-310001694028us-gaap:MemberUnitsMember2018-01-012018-01-1700016940282018-01-012018-01-170001694028us-gaap:MemberUnitsMember2018-01-170001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-01-170001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMember2018-01-170001694028us-gaap:AdditionalPaidInCapitalMember2018-01-170001694028us-gaap:RetainedEarningsMember2018-01-170001694028us-gaap:ParentMember2018-01-170001694028us-gaap:NoncontrollingInterestMember2018-01-1700016940282018-01-170001694028us-gaap:MemberUnitsMember2018-01-182018-12-310001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-01-182018-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMember2018-01-182018-12-310001694028us-gaap:AdditionalPaidInCapitalMember2018-01-182018-12-310001694028us-gaap:RetainedEarningsMember2018-01-182018-12-310001694028us-gaap:ParentMember2018-01-182018-12-310001694028us-gaap:NoncontrollingInterestMember2018-01-182018-12-3100016940282018-01-182018-12-310001694028us-gaap:MemberUnitsMember2018-12-3100016940282016-12-310001694028us-gaap:CommonClassAMember2018-01-170001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2018-01-172018-01-170001694028srt:SubsidiariesMember2018-01-172018-01-170001694028us-gaap:CommonClassBMember2018-01-172018-01-170001694028us-gaap:CommonClassBMember2018-01-170001694028us-gaap:CommonClassAMemberus-gaap:IPOMember2018-01-170001694028lbrt:ABLCreditFacilityMember2018-01-172018-01-17xbrli:pure0001694028lbrt:TermLoanFacilityMember2018-01-172018-01-170001694028lbrt:LibertyLLCMembersrt:SubsidiariesMember2019-12-310001694028lbrt:LibertyLLCMembersrt:SubsidiariesMember2018-12-310001694028lbrt:PropertyAndEquipmentMembersrt:MinimumMember2019-01-012019-12-310001694028lbrt:PropertyAndEquipmentMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:AccountingStandardsUpdate201602Member2019-01-010001694028us-gaap:PrepaidExpensesAndOtherCurrentAssetsMemberus-gaap:AccountingStandardsUpdate201602Memberlbrt:OperatingLeaseMember2019-01-010001694028us-gaap:AccountingStandardsUpdate201602Memberus-gaap:OtherAssetsMemberlbrt:OperatingLeaseMember2019-01-010001694028us-gaap:PrepaidExpensesAndOtherCurrentAssetsMemberus-gaap:AccountingStandardsUpdate201602Member2019-01-010001694028lbrt:AccruedInterestAndOtherLiabilitiesMemberus-gaap:AccountingStandardsUpdate201602Member2019-01-01lbrt:agreement00016940282018-01-172018-01-170001694028srt:MinimumMember2019-01-012019-12-310001694028srt:MaximumMember2019-01-012019-12-31lbrt:fleet0001694028lbrt:ProppantsMember2019-12-310001694028lbrt:ProppantsMember2018-12-310001694028lbrt:ChemicalsMember2019-12-310001694028lbrt:ChemicalsMember2018-12-310001694028lbrt:MaintenancepartsMember2019-12-310001694028lbrt:MaintenancepartsMember2018-12-310001694028us-gaap:LandMember2019-12-310001694028us-gaap:LandMember2018-12-310001694028us-gaap:EnergyEquipmentMembersrt:MinimumMember2019-01-012019-12-310001694028us-gaap:EnergyEquipmentMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:EnergyEquipmentMember2019-12-310001694028us-gaap:EnergyEquipmentMember2018-12-310001694028srt:MinimumMemberus-gaap:VehiclesMember2019-01-012019-12-310001694028us-gaap:VehiclesMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:VehiclesMember2019-12-310001694028us-gaap:VehiclesMember2018-12-310001694028us-gaap:BuildingMembersrt:MinimumMember2019-01-012019-12-310001694028us-gaap:BuildingMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:BuildingMember2019-12-310001694028us-gaap:BuildingMember2018-12-310001694028lbrt:OfficeEquipmentFurnitureAndSoftwareMembersrt:MinimumMember2019-01-012019-12-310001694028lbrt:OfficeEquipmentFurnitureAndSoftwareMembersrt:MaximumMember2019-01-012019-12-310001694028lbrt:OfficeEquipmentFurnitureAndSoftwareMember2019-12-310001694028lbrt:OfficeEquipmentFurnitureAndSoftwareMember2018-12-310001694028us-gaap:FireMemberus-gaap:EnergyEquipmentMember2018-12-310001694028us-gaap:FireMemberus-gaap:EnergyEquipmentMember2018-01-012018-12-310001694028lbrt:TermLoanFacilityMember2019-12-310001694028lbrt:TermLoanFacilityMember2018-12-310001694028us-gaap:LineOfCreditMember2019-12-310001694028us-gaap:LineOfCreditMember2018-12-310001694028us-gaap:RevolvingCreditFacilityMember2017-09-190001694028us-gaap:RevolvingCreditFacilityMemberlbrt:ABLCreditFacilityMember2017-09-190001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:TermLoanFacilityMember2017-09-190001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:ABLCreditFacilityMember2019-12-310001694028us-gaap:LetterOfCreditMemberlbrt:ABLCreditFacilityMember2019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LondonInterbankOfferedRateLIBORMembersrt:MinimumMemberlbrt:ABLCreditFacilityMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:LondonInterbankOfferedRateLIBORMemberlbrt:ABLCreditFacilityMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:BaseRateMembersrt:MinimumMemberlbrt:ABLCreditFacilityMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:BaseRateMemberlbrt:ABLCreditFacilityMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembersrt:MinimumMemberlbrt:ABLCreditFacilityMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:ABLCreditFacilityMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:ABLCreditFacilityMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:TermLoanFacilityMember2019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:TermLoanFacilityMemberus-gaap:LondonInterbankOfferedRateLIBORMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberus-gaap:BaseRateMemberlbrt:TermLoanFacilityMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:TermLoanFacilityMembersrt:MinimumMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:TermLoanFacilityMembersrt:MaximumMember2019-01-012019-12-310001694028us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMemberlbrt:TermLoanFacilityMember2019-01-012019-12-310001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2019-12-310001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2018-12-310001694028us-gaap:CustomerConcentrationRiskMemberlbrt:LargestCustomerMemberus-gaap:AccountsReceivableMember2019-01-012019-12-310001694028lbrt:LargestTwoCustomersMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:AccountsReceivableMember2018-01-012018-12-310001694028us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberlbrt:LargestCustomerMember2019-01-012019-12-310001694028us-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMemberlbrt:LargestCustomerMember2018-01-012018-12-310001694028lbrt:LargestTwoCustomersMemberus-gaap:SalesRevenueNetMemberus-gaap:CustomerConcentrationRiskMember2017-01-012017-12-310001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2019-12-310001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2018-12-3100016940282016-12-212017-12-310001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockMember2019-01-012019-12-310001694028us-gaap:CommonClassAMemberlbrt:LongTermIncentivePlanMember2018-01-110001694028us-gaap:RestrictedStockUnitsRSUMember2019-01-012019-12-310001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockUnitsRSUMember2018-12-310001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockUnitsRSUMember2019-01-012019-12-310001694028us-gaap:CommonClassAMemberus-gaap:RestrictedStockUnitsRSUMember2019-12-310001694028us-gaap:PerformanceSharesMember2019-01-012019-12-310001694028us-gaap:PerformanceSharesMember2018-12-310001694028us-gaap:PerformanceSharesMember2019-12-310001694028us-gaap:RestrictedStockUnitsRSUMember2018-01-012018-12-310001694028us-gaap:RestrictedStockUnitsRSUMember2019-12-310001694028us-gaap:MemberUnitsMembersrt:SubsidiariesMember2019-01-012019-12-310001694028us-gaap:MemberUnitsMembersrt:SubsidiariesMember2018-01-012018-12-310001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-01-012018-12-310001694028lbrt:RestrictedStockAndRestrictedStockUnitsRSUsMemberus-gaap:CommonClassAMember2019-01-012019-12-310001694028lbrt:RestrictedStockAndRestrictedStockUnitsRSUsMemberus-gaap:CommonClassAMember2018-01-012018-12-310001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2018-09-100001694028us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-10-012019-12-310001694028lbrt:RiverstoneMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberus-gaap:CommonStockMember2018-01-012018-12-3100016940282018-01-182019-12-310001694028us-gaap:DomesticCountryMember2019-12-310001694028us-gaap:NoncontrollingInterestMember2018-01-012018-12-310001694028lbrt:RCIVNonUSLOSCorpMemberus-gaap:DomesticCountryMember2019-12-310001694028us-gaap:StateAndLocalJurisdictionMemberlbrt:RCIVNonUSLOSCorpMember2019-12-310001694028lbrt:RCIVNonUSLOSCorpMemberlbrt:TaxReceivableAgreementMember2019-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMemberlbrt:TaxReceivableAgreementMember2018-12-310001694028lbrt:TaxReceivableAgreementMember2018-12-310001694028us-gaap:CommonStockMemberus-gaap:CommonClassBMemberlbrt:TaxReceivableAgreementMember2019-12-310001694028lbrt:TaxReceivableAgreementMember2019-12-310001694028us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2019-01-012019-12-310001694028us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2017-04-012017-09-300001694028us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2017-10-012019-12-310001694028us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2018-01-012018-12-310001694028us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2017-01-012017-12-310001694028lbrt:RCIVNonUSLOSCorpMembersrt:AffiliatedEntityMemberlbrt:TaxReceivableAgreementMember2018-01-110001694028lbrt:RCIVNonUSLOSCorpMembersrt:AffiliatedEntityMemberus-gaap:CommonClassBMemberlbrt:TaxReceivableAgreementMember2019-01-012019-12-310001694028lbrt:RCIVNonUSLOSCorpMembersrt:AffiliatedEntityMemberus-gaap:CommonClassBMemberlbrt:TaxReceivableAgreementMember2019-12-310001694028lbrt:RiverstoneMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberus-gaap:CommonStockMember2019-01-012019-12-310001694028lbrt:EquityTransactionMembersrt:AffiliatedEntityMember2018-01-170001694028lbrt:EquityTransactionMembersrt:AffiliatedEntityMember2018-01-172018-01-170001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2019-10-012019-12-310001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2018-01-012018-12-310001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2017-01-012017-12-310001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2019-06-240001694028lbrt:LibertyResourcesLLCMembersrt:AffiliatedEntityMemberlbrt:HydraulicFracturingServicesMember2019-01-012019-12-310001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMembersrt:AffiliatedEntityMember2019-10-012019-12-310001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMembersrt:AffiliatedEntityMember2018-01-012018-12-310001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMembersrt:AffiliatedEntityMember2017-01-012017-12-310001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMemberus-gaap:CommonClassAMembersrt:AffiliatedEntityMemberus-gaap:IPOMemberus-gaap:CommonStockMember2018-01-112018-01-110001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMembersrt:AffiliatedEntityMember2018-12-310001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMembersrt:AffiliatedEntityMember2019-01-012019-12-310001694028lbrt:ServiceFeesMemberlbrt:RiverstoneMembersrt:AffiliatedEntityMember2019-12-310001694028srt:AffiliatedEntityMemberlbrt:ProppantExpressInvestmentsLLCMemberlbrt:AdministrativeSupportAndPurchaseAndLeaseProppantLogisticsEquipmentMember2019-10-012019-12-310001694028srt:AffiliatedEntityMemberlbrt:ProppantExpressInvestmentsLLCMemberlbrt:AdministrativeSupportAndPurchaseAndLeaseProppantLogisticsEquipmentMember2018-01-012018-12-310001694028srt:AffiliatedEntityMemberlbrt:ProppantExpressInvestmentsLLCMemberlbrt:AdministrativeSupportAndPurchaseAndLeaseProppantLogisticsEquipmentMember2017-01-012017-12-310001694028srt:AffiliatedEntityMemberlbrt:ProppantExpressInvestmentsLLCMemberlbrt:AdministrativeSupportAndPurchaseAndLeaseProppantLogisticsEquipmentMember2019-12-310001694028srt:AffiliatedEntityMemberlbrt:ProppantExpressInvestmentsLLCMemberlbrt:AdministrativeSupportAndPurchaseAndLeaseProppantLogisticsEquipmentMember2018-12-31utr:T0001694028lbrt:ProppantsMember2019-01-012019-12-310001694028lbrt:ProppantsMember2018-01-012018-12-31utr:gal0001694028lbrt:ChemicalsMember2019-01-012019-12-310001694028lbrt:ChemicalsMember2018-01-012018-12-3100016940282019-01-012019-03-3100016940282019-04-012019-06-3000016940282019-07-012019-09-3000016940282019-10-012019-12-3100016940282018-01-012018-03-3100016940282018-04-012018-06-3000016940282018-07-012018-09-3000016940282018-10-012018-12-310001694028us-gaap:CommonClassAMemberus-gaap:SubsequentEventMemberus-gaap:CommonStockMember2020-01-222020-01-220001694028us-gaap:CommonClassAMemberus-gaap:SubsequentEventMemberus-gaap:MemberUnitsMember2020-01-222020-01-22

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File No. 001-38081

| | | | | | | | | | | | | | |

Liberty Oilfield Services Inc. | | | | |

| (Exact Name of Registrant as Specified in its Charter) | | | | |

Delaware | | | | 81-4891595 |

| (State or Other Jurisdiction of Incorporation or Organization) | | | | (I.R.S. Employer Identification No.) |

950 17th Street, Suite 2400 Denver, Colorado | | | | 80202 |

| (Address of Principal Executive Offices) | | | | (Zip Code) |

| | (303) 515-2800 | | |

| (Registrant’s Telephone Number, Including Area Code) | | | | |

| Securities registered pursuant to section 12(b) of the Act: | | | | |

| | | | |

| Title of each class | | Trading symbol(s) | | Name of each exchange on which registered |

| | | | |

| Class A Common Stock, par value $0.01 | | LBRT | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this Chapter) during the presiding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

Large accelerated Filer ☒ | Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller reporting company ☐ |

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act): ☐ Yes ☒ No

As of June 28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant was approximately $732.8 million, determined using the per share closing price on the New York Stock Exchange on that date of $16.18. Shares of common stock held by each director and executive officer (and their respective affiliates) and each person who owns 10 percent or more of the outstanding common stock or who is otherwise believed by the registrant to be in a control position have been excluded. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

At February 21, 2020, the Registrant had 81,920,347 shares of Class A Common Stock and 30,638,960 shares of Class B Common Stock outstanding.

Documents Incorporated by Reference: Part III of this Annual Report on Form 10-K incorporates certain information by reference from the registrant’s proxy statement for the 2020 annual meeting of stockholders to be filed no later than 120 days after the end of the registrant’s fiscal year.

TABLE OF CONTENTS

| | | | | | | | |

| | Page No. |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| Item 15. | | |

| Item 16. | | |

| | |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and certain other communications made by us contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange of 1934, as amended (the “Exchange Act”), including statements about our growth, future operating results, estimates, beliefs and expected performance. For this purpose, any statement that is not a statement of historical fact should be considered a forward-looking statement. We may use the words “believe,” “anticipate,” “plan,” “expect,” “intend,” “may,” “will,” “should” and similar expressions to help identify forward-looking statements. We cannot assure you that our assumptions and expectations will prove to be correct. Important factors could cause our actual results to differ materially from those indicated or implied by forward-looking statements. We undertake no intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise and readers should not rely on the forward-looking statements as representing the Company’s views as of any date subsequent to the date of the filing of this Annual Report on Form 10-K. These forward-looking statements are based on management’s current belief, based on currently available information, as to the outcome and timing of future events.

Forward-looking statements may include statements about:

•our business strategy;

•our operating cash flows, the availability of capital and our liquidity;

•our future revenue, income and operating performance;

•our ability to sustain and improve our utilization, revenue and margins;

•our ability to maintain acceptable pricing for our services;

•our future capital expenditures;

•our ability to finance equipment, working capital and capital expenditures;

•competition and government regulations;

•our ability to obtain permits and governmental approvals;

•pending legal or environmental matters;

•oil and natural gas prices;

•acquisitions;

•general economic conditions;

•credit markets;

•demand for services in our industry;

•our ability to successfully develop our research and technology capabilities and implement technological developments and enhancements;

•uncertainty regarding our future operating results;

•return of capital to shareholders; and

•plans, objectives, expectations and intentions contained in this Annual Report on Form 10-K that are not historical.

We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control. These risks include, but are not limited to, decline in demand for our services, the cyclical nature and volatility of the oil and natural gas industry, a decline in, or substantial volatility of, oil and natural gas commodity prices, environmental risks, regulatory changes, the inability to comply with the financial and other covenants and metrics in our Credit Facilities (as defined herein), cash flow and access to capital, the timing of development expenditures and the other risks described under “Risk Factors” in this Annual Report on Form 10-K.

All forward-looking statements, expressed or implied, included in this Annual Report on Form 10-K are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue.

This Annual Report on Form 10-K includes market and industry data and certain other statistical information based on third-party sources including independent industry publications, government publications and other publish independent

sources, such as content and estimates provided by Coras Research, LLC as of December 31, 2019. Coras Research, LLC is not a member of the Financial Industry Regulator Authority (FINRA) or the Securities Investor Protection Corporation (SIPC) and is not a registered broker dealer or investment advisor. Although we believe these third-party sources are reliable as of their respective dates, we have not independently verified the accuracy or completeness of this information. Some data is also based on our own good faith estimates, which are supported by our management's knowledge of and experience in the markets and business in which we operate.

PART I

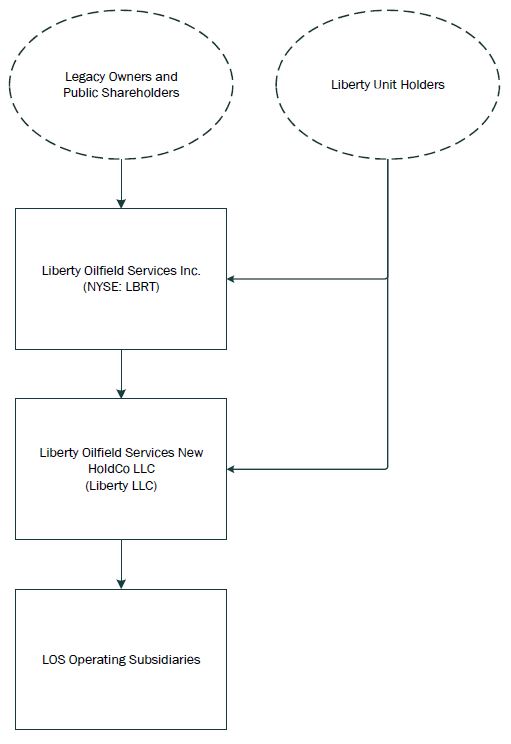

As used in this Annual Report on Form 10-K, unless the context otherwise requires, references to the term “Liberty Inc.” refers to Liberty Oilfield Services Inc. and references to the terms “Company,” “we,” “us” and “our” refer to, collectively, Liberty Oilfield Services LLC and LOS Acquisition Co I LLC and its subsidiaries (collectively, the “Predecessor”) for periods prior to the IPO (as defined herein), and, for periods as of and following the IPO, Liberty Inc. and its consolidated subsidiaries. References to “Liberty LLC” refer to Liberty Oilfield Services New HoldCo LLC. References to “Liberty Holdings” refer to Liberty Oilfield Services Holdings LLC.

Item 1. Business

Our Company

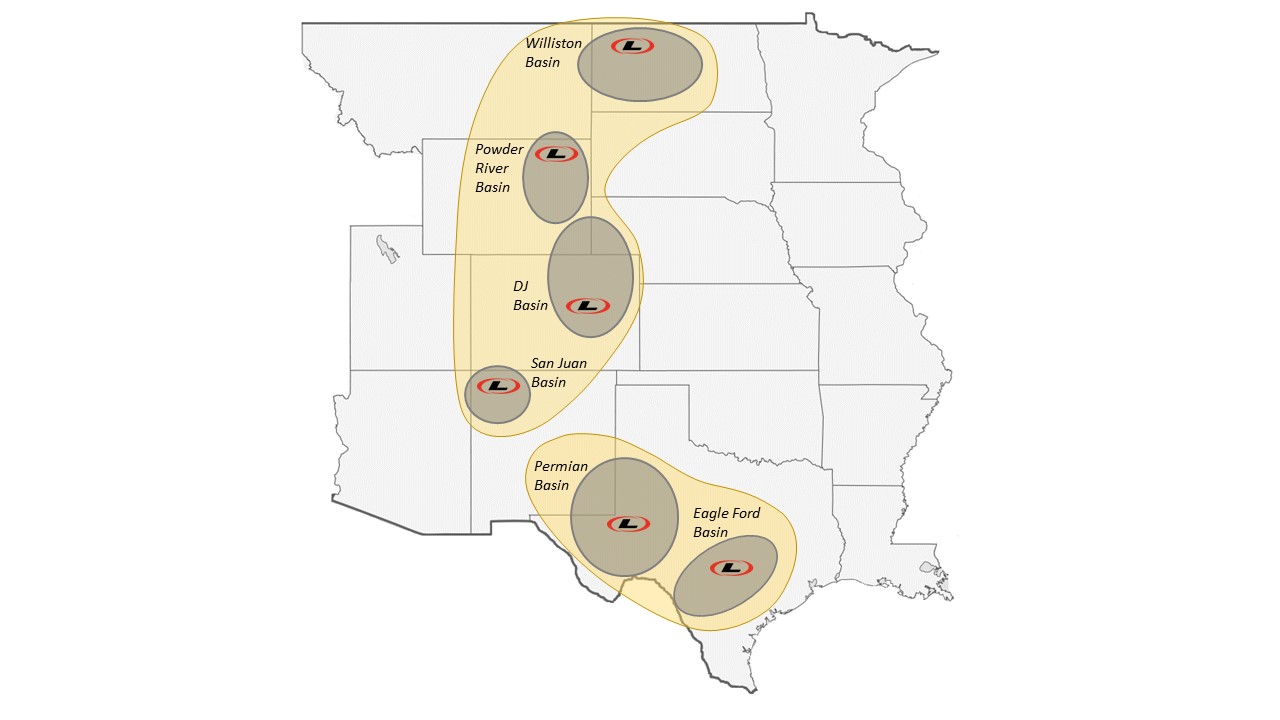

We are an independent provider of hydraulic fracturing services and goods to onshore oil and natural gas exploration and production (“E&P”) companies in North America. We provide our services primarily in the Permian Basin, the Eagle Ford Shale, the Denver-Julesburg Basin (the “DJ Basin”), the Williston Basin, the San Juan Basin and the Powder River Basin.

We have grown organically from one active hydraulic fracturing fleet in December 2011 to 24 active fleets in February 2020.

Our founders and existing management were pioneers in the development of data-driven hydraulic fracturing technologies for application in shale plays. Prior to founding Liberty Holdings, the majority of our management team founded and built Pinnacle Technologies, Inc. (“Pinnacle Technologies”) into a leading fracturing technology company. In 1992, Pinnacle Technologies developed the first commercial hydraulic fracture mapping technologies, analytical tools that played a major role in launching the shale revolution. Our extensive experience with fracture technologies and customized fracture design has enabled us to develop new technologies and processes that provide our customers with real time solutions that significantly enhance their completions. These technologies include hydraulic fracture propagation models, reservoir engineering tools, large, proprietary shale production databases and multi-variable statistical analysis techniques. Taken together, these technologies have enabled us to be a leader in hydraulic fracture design innovation and application.

We believe the following characteristics distinguish us from our competitors and are the foundations of our business: forming ongoing partnerships of trust and innovation with our customers; developing and utilizing technology to maximize well performance; and promoting a people-centered culture focused on our employees, customers and suppliers. We have developed strong relationships with our customers by investing significant time in fracture design collaboration, which substantially enhances their production economics. Our technological innovations have become even more critical as E&P companies have increased the completion complexity and fracture intensity of horizontal wells. We are proactive in developing innovative solutions to industry challenges, including developing: (i) our proprietary databases of U.S. unconventional wells to which we apply our proprietary multi-variable statistical analysis technologies to provide differential insight into fracture design optimization; (ii) our Liberty Quiet Fleet® design which significantly reduces noise levels compared to conventional hydraulic fracturing fleets; and (iii) hydraulic fracturing fluid systems tailored to the specific reservoir properties in the basins in which we operate. We foster a people-centered culture built around honoring our commitments to customers, partnering with our suppliers and hiring, training and retaining people that we believe to be the best talent in our field, enabling us to be one of the safest and most efficient hydraulic fracturing companies in the United States.

Recent Developments

In January 2020, we put our 24th fleet into production for a long-term existing customer. This fleet will utilize our Liberty Quiet Fleet® technology and have dual fuel capability. We expect our 25th fleet to be deployed later in 2020.

Initial Public Offering and Corporate Reorganization Transaction

Liberty Inc. was incorporated as a Delaware corporation on December 21, 2016, to become a holding corporation for Liberty LLC and its subsidiaries upon completion of a corporate reorganization (as detailed below, the “Corporate Reorganization”) and planned initial public offering of the Company (“IPO”). Liberty Inc. has no material assets other than its ownership in Liberty LLC.

On January 17, 2018, we completed our IPO of 14,640,755 shares of our Class A common stock, par value $0.01 per share (the “Class A Common Stock”) at a public offering price of $17.00 per share, of which 14,340,214 shares were offered by us and 300,541 shares were offered by the selling shareholder. We received approximately $220.0 million in net proceeds after deducting approximately $23.8 million of underwriting discounts and commissions and other offering costs. We did not receive any proceeds from the sale of the shares of Class A Common Stock by the selling shareholder.

We are a holding company with no direct operations. In connection with the IPO, we completed the Corporate Reorganization, including the following series of transactions:

•Liberty Holdings contributed all of its assets to Liberty LLC in exchange for units in Liberty LLC (the “Liberty LLC Units”);

•Liberty Holdings liquidated and distributed to its then-existing owners (the “Legacy Owners”) Liberty LLC Units pursuant to the terms of the limited liability company agreement of Liberty Holdings and the Master Reorganization Agreement dated as of January 11, 2018, by and among the Company, Liberty Holdings, Liberty LLC, and the other parties named therein (the “Master Reorganization Agreement”);

•certain of the Legacy Owners directly or indirectly contributed all or a portion of their Liberty LLC Units to Liberty Inc. in exchange for 55,685,027 shares of our Class A Common Stock, and 1,258,514 shares of restricted stock. Subsequent to the initial exchange, 1,609,122 shares of Class A Common Stock were redeemed for an aggregate purchase price of $25.9 million upon the exercise of the underwriters' overallotment option;

•Liberty Inc. issued the Legacy Owners that continued to own Liberty LLC Units (the “Liberty Unit Holders”) an aggregate amount of 48,207,372 shares of our Class B common stock, par value $0.01 per share (the “Class B Common Stock” and, together with the Class A Common Stock, the “Common Stock”); and

•Liberty Inc. contributed the net proceeds it received from the IPO to Liberty LLC in exchange for additional Liberty LLC Units such that Liberty Inc. held a total number of Liberty LLC Units equal to the number of shares of Class A Common Stock outstanding immediately following the IPO.

The below structure chart shows our organization upon the completion of our IPO. This chart is provided for illustrative purposes only and does not represent all legal entities affiliated with us.

Each share of Class B Common Stock has no economic rights but entitles its holder to one vote on all matters to be voted on by shareholders generally. Holders of Class A Common Stock and Class B Common Stock will vote together as a single

class on all matters presented to our shareholders for their vote or approval, except as otherwise required by applicable law or by our amended and restated certificate of incorporation. We do not intend to list our Class B Common Stock on any exchange.

Under the Second Amended and Restated Limited Liability Company Agreement of Liberty LLC (the “Liberty LLC Agreement”), each Liberty Unit Holder has, subject to certain limitations, the right (the “Redemption Right”) to cause Liberty LLC to acquire all or a portion of its Liberty LLC Units for, at Liberty LLC’s election, (i) shares of our Class A Common Stock at a redemption ratio of one share of Class A Common Stock for each Liberty LLC Unit redeemed, subject to conversion rate adjustments for stock splits, stock dividends and reclassification and other similar transactions or (ii) an equivalent amount of cash. Alternatively, upon the exercise of the Redemption Right, Liberty Inc. (instead of Liberty LLC) will have the right (the “Call Right”) to, for administrative convenience, acquire each tendered Liberty LLC Unit directly from the redeeming Liberty Unit Holder for, at its election, (i) one share of Class A Common Stock or (ii) an equivalent amount of cash. In addition, upon a change of control of Liberty Inc., Liberty Inc. has the right to require each holder of Liberty LLC Units (other than Liberty Inc.) to exercise its Redemption Right with respect to some or all of such unit holder’s Liberty LLC Units. In connection with any redemption of Liberty LLC Units pursuant to the Redemption Right or the Call Right, the corresponding number of shares of Class B Common Stock will be canceled.

In connection with the IPO, Liberty Inc. entered into two tax receivable agreements, (the “TRAs”) with the Liberty Unit Holders and the selling shareholder (each such person and any permitted transferee, a “TRA Holder” and together, the “TRA Holders”).

The first of the TRAs, which Liberty Inc. entered into with the Liberty Unit Holders, generally provides for the payment by Liberty Inc. to such TRA Holders of 85% of the net cash savings, if any, in U.S. federal, state and local income and franchise tax (computed using simplifying assumptions to address the impact of state and local taxes) that Liberty Inc. actually realizes (or is deemed to realize in certain circumstances) in periods after the IPO as a result of, as applicable to each such TRA Holder, (i) certain increases in tax basis that occur as a result of Liberty Inc.’s acquisition (or deemed acquisition for U.S. federal income tax purposes) of all or a portion of such TRA Holder’s Liberty LLC Units in connection with the IPO or pursuant to the exercise of the Redemption Right or Liberty Inc.’s Call Right and (ii) imputed interest deemed to be paid by Liberty Inc. as a result of, and additional tax basis arising from, any payments Liberty Inc. makes under such TRAs.

The second of the TRAs, which Liberty Inc. entered into with the selling shareholder, generally provides for the payment by Liberty Inc. to such TRA Holder of 85% of the net cash savings, if any, in U.S. federal, state and local income and franchise tax (computed using simplifying assumptions to address the impact of state and local taxes) that Liberty Inc. actually realizes (or is deemed to realize in certain circumstances) in periods after the IPO as a result of, as applicable to such TRA Holder, (i) any net operating losses available to Liberty Inc. as a result of the Corporate Reorganization and (ii) imputed interest deemed to be paid by Liberty Inc. as a result of any payments Liberty Inc. makes under such TRAs. For further discussion regarding the potential acceleration of payments under the TRAs and its potential impact, please read “Risk Factors—Risks Related to Our Class A Common Stock.”

Because Liberty Inc. is a holding company with no operations of its own, Liberty Inc.’s ability to make payments under the TRAs is dependent on the ability of Liberty LLC to make distributions to Liberty Inc. in an amount sufficient to cover its obligations under the TRAs. See “Risk Factors—Risks Related to Our Class A Common Stock—Liberty Inc. is a holding company. Liberty Inc.’s only material asset is its equity interest in Liberty LLC, and Liberty Inc. is accordingly dependent upon distributions from Liberty LLC to pay taxes, make payments under the TRAs and cover its corporate and other overhead expenses.” If Liberty Inc. experiences a change of control (as defined under the TRAs, which includes certain mergers, asset sales and other forms of business combinations) or the TRAs terminate early (at Liberty Inc.’s election or as a result of its breach), Liberty Inc. would be required to make a substantial, immediate lump-sum payment.

Cyclical Nature of Industry

We operate in a highly cyclical industry. The key factor driving demand for our services is the level of drilling activity by E&P companies, which in turn depends largely on the current and anticipated economics of new well completions. Global supply and demand for oil and the domestic supply and demand for natural gas are critical in assessing industry outlook. Demand for oil and natural gas is cyclical and subject to large, rapid fluctuations. E&P companies tend to increase capital expenditures in response to increases in oil and natural gas prices, which generally results in greater revenues and profits for oilfield service companies such as ours. Increased capital expenditures also ultimately lead to greater production, which historically has resulted in increased supplies and reduced prices which in turn tend to reduce demand for oilfield services. For these reasons, the results of our operations may fluctuate from quarter to quarter and from year to year, and these fluctuations may distort comparisons of results across periods.

Seasonality

Our results of operations have historically reflected seasonal tendencies relating to holiday seasons, inclement weather and the conclusion of our customers’ annual drilling and completion capital expenditure budgets. Our most notable declines typically occur in the fourth quarter of the year for the reasons described above. Additionally, some of the areas in which we have operations, including the DJ Basin, Powder River Basin and Williston Basin, are adversely affected by seasonal weather conditions, primarily in the winter and spring. During periods of heavy snow, ice or rain and frost law enforcement, we may be unable to move our equipment between locations, thereby reducing our ability to provide services and generate revenues. The exploration activities of our customers may also be affected during such periods of adverse weather conditions. Additionally, extended drought conditions in our operating regions could impact our ability or our customers’ ability to source sufficient water or increase the cost for such water.

Intellectual Property

Over the last several years we have significantly invested in our research and technology capabilities. Our efforts to date have been focused on developing innovative, fit-for-purpose solutions designed to enhance our core service offerings, increase completion efficiencies, provide cost savings to our operations and add value for our customers.

As a result of these efforts, we introduced several new products and progressed on differentiating technologies that we believe will provide a competitive advantage as our customers focus on extracting oil and natural gas in the most economical and efficient ways possible, including, for example, our Liberty Quiet Fleet®, which materially reduces noise levels compared to conventional fracturing fleets. These investments are delivering value added products and services that support our customers and create increasing demand for our services.

We seek patent and trademark protections for our technology when we deem it prudent, and we aggressively pursue protection of these rights when warranted. We believe our patents, trademarks, and other protections for our proprietary technologies are adequate for the conduct of our business and that no single patent or trademark is critical to our business. In addition, we rely, to a great extent, on the technical expertise and know-how of our personnel to maintain our competitive position, and we take commercially reasonable measures to protect trade secrets and other confidential and/or proprietary information relating to the technologies we develop.

Risk Management and Insurance

Our operations are subject to significant hazards often found in the oil and natural gas industry, such as, but not limited to, accidents, including accidents related to trucking operations provided in connection with our services, blowouts, explosions, craterings, fires, natural gas leaks, oil and produced water spills and releases of hydraulic fracturing fluids or other well fluids into the environment. These conditions can cause:

•disruption in operations;

•substantial repair or remediation costs;

•personal injury or loss of human life;

•significant damage to or destruction of property and equipment;

•environmental pollution, including groundwater contamination;

•unusual or unexpected geological formations or pressures and industrial accidents;

•impairment or suspension of operations; and

•substantial revenue loss.

In addition, our operations are subject to, and exposed to, employee/employer liabilities and risks such as wrongful termination, discrimination, labor organizing, retaliation claims and general human resource related matters.

Claims for loss of oil and natural gas production and damage to formations can occur in the well services industry. Litigation arising from a catastrophic occurrence at a location where our equipment and services are being used or trucking services provided in connection therewith may result in our being named as a defendant in lawsuits asserting large claims.

We do not have insurance against all foreseeable risks, either because insurance is not available or because of the high premium costs. The occurrence of an event not fully insured against or the failure of an insurer to meet its insurance obligations could result in substantial losses. In addition, we may not be able to maintain adequate insurance in the future at rates we consider reasonable. Insurance may not be available to cover any or all of the risks to which we are subject, or, even if

available, it may be inadequate, or insurance premiums or other costs could rise significantly in the future so as to make such insurance prohibitively expensive.

We enter into Master Service Agreements (“MSAs”) with substantially all of our customers for our hydraulic fracturing services. Such MSAs delineate our and our customer’s respective indemnification obligations with respect to the services we provide. Generally, under our MSAs relating to our hydraulic fracturing services, we assume responsibility for pollution or contamination originating above the surface from our equipment or handling. However, our customers assume responsibility for all other pollution or contamination that may occur during operations, including that which may result from seepage or any other uncontrolled flow of drilling and completion fluids. The assumed responsibilities include the control, removal and clean-up of any pollution or contamination. In such cases, we may be exposed to additional liability if we are grossly negligent or commit willful acts causing the pollution or contamination. Generally, our customers also agree to indemnify us against claims arising from their employees’ personal injury or death, in the case of our hydraulic fracturing operations, to the extent that their employees are injured by such operations, unless the loss is a result of our gross negligence or willful misconduct. Similarly, we generally agree to indemnify our customers for liabilities arising from personal injury to or death of any of our employees, unless resulting from the gross negligence or willful misconduct of our customer. The same principles apply to mutual indemnification for loss or destruction of property or equipment. Losses due to catastrophic events, such as blowouts, are generally the responsibility of the customer. However, despite this general allocation of risk, we may be unsuccessful in enforcing contractual terms, incur an unforeseen liability that is not addressed by the scope of the contractual provisions or be required to enter into an MSA with terms that vary from our standard allocations of risk, as described above. Consequently, we may incur substantial losses that could materially and adversely affect our financial condition and results of operations.

Employees

As of December 31, 2019, we had 2,571 employees and no unionized labor. We believe we have good relations with our employees.

Our Services

We primarily provide hydraulic fracturing services and goods to onshore oil and natural gas E&P companies operating in unconventional oil and natural gas reservoirs and requiring technically and operationally advanced services. Hydraulic fracturing services are performed to enhance production of oil and natural gas from formations with low permeability and restricted flow of hydrocarbons. Our customers benefit from our expertise in fracturing horizontal wells in shales and other unconventional geological formations.

The process of hydraulic fracturing involves pumping a pressurized stream of fracturing fluid—typically a mixture of water, chemicals and proppant—into a well casing or tubing in order to cause the underground formation to fracture or crack. These fractures release trapped hydrocarbon particles and provide a conductive channel for the oil or natural gas to flow freely to the wellbore for collection. The propping agent, or proppant,—typically sand—becomes lodged in the cracks created by the hydraulic fracturing process, “propping” them open to facilitate the flow of hydrocarbons from the reservoir to the well. The fracturing fluid is engineered to lose viscosity, or “break,” and is subsequently flowed back from the formation, leaving the proppant suspended in the mineral fractures. Once our customer has flushed the fracturing fluids from the well using a controlled flow-back process, the customer manages fluid and water recycling or disposal.

Our hydraulic fracturing fleets consist of mobile hydraulic fracturing units and other auxiliary heavy equipment to perform fracturing services. Our hydraulic fracturing units consist primarily of high-pressure hydraulic pumps, diesel engines, transmissions, radiators and other supporting equipment that are typically mounted on trailers. We refer to the group of units and other equipment, such as blenders, data vans, sand storage, tractors, manifolds and high pressure fracturing iron, which are necessary to perform a typical hydraulic fracturing job, as a “fleet,” and the personnel assigned to each fleet as a “crew.” As of February 2020, we had 24 active fleets.

An important element of our hydraulic fracturing services is our focus on providing custom-tailored completions solutions to our customers to maximize their well results. Our technologically innovative approach involves our review of a series of continually updated, proprietary databases of U.S. unconventional wells to which we apply our multi-variable data analysis, allowing us to gain differential insight into fracture design. The innovative completions solutions we provide to our customers help them complete more productive and cost efficient wells in shorter times with less environmental impact on their surroundings while increasing the useful lives of our equipment.

In addition to custom-tailored completions solutions, we also develop custom fluid systems, proppant logistics solutions, perforating strategies and pressure analysis techniques for our customers. An example of this is a hydraulic fracturing fluid that we developed for use in our DJ Basin operations called Liberty Spirit™, a specifically designed fracturing fluid system that enables material reductions in completion costs in the DJ Basin without compromising job execution or well results.

We provide our services in several of the most active basins in the United States, including the Permian Basin, the Eagle Ford Shale, the DJ Basin, the Williston Basin, the San Juan Basin and the Powder River Basin. The map below represents our current areas of operations:

Properties and Equipment

Properties

Our corporate headquarters are located at 950 17th Street, Suite 2400, Denver, Colorado 80202. We lease our general office space at our corporate headquarters. The lease expires in December 2024. We currently own or lease the following additional principal properties:

| | | | | | | | | | | | | | | | | | | | |

| District Facility Location | | Size | | Leased or Owned | | Expiration of Lease |

| Odessa, TX | | 77,500 sq. ft on 47 acres | | Owned | | N/A |

| Henderson, CO | | 50,000 sq. ft on 13 acres | | Leased | | December 31, 2034 |

| Williston, ND | | 30,000 sq. ft on 15 acres | | Owned | | N/A |

| Gillette, WY | | 32,757 sq. ft on 15 acres | | Leased | | December 31, 2034 |

| Cibolo, TX | | 90,000 sq. ft on 34 acres | | Owned | | N/A |

We also lease several smaller facilities, which leases generally have terms of one to three years. We believe that our existing facilities are adequate for our operations and their locations allow us to efficiently serve our customers. We do not believe that any single facility is material to our operations and, if necessary, we could readily obtain a replacement facility.

Equipment

As of February 2020, we have 24 hydraulic fracturing fleets. Eleven of our fleets currently utilize our Liberty Quiet Fleet® technology, approximately 28% of our capacity has dual fuel capability, and approximately 22% of our capacity utilizes the latest Tier 4 diesel engines.

Our hydraulic fracturing fleets are comprised of high-quality, heavy-duty equipment designed to reduce operational downtime and maintenance costs, while enhancing our ability to provide reliable, consistent service. Each hydraulic fracturing fleet includes the necessary blending units, manifolds, data vans and other ancillary equipment needed to provide a high level of service to our customers.

Our newbuild fleets are manufactured to a custom Liberty specification that identifies the input components, including such key parts as engines, transmissions and pumps and control systems. These components have been selected with our lowest total cost of ownership philosophy in mind. We have built a strong partnership with each of the key component suppliers that we believe will help ensure timely access to necessary components, early opportunities to adopt the latest technology, and high-level technical support. For example, our close partnership with Caterpillar Inc. enabled us to have ready access to their technical team as we worked through the development of the Liberty Quiet Fleet® technology and to be on the early test site for their new low-emission Tier 4 diesel and dynamic gas blending engines. This relationship ensured that the end product was delivered without compromise to engine performance, reliability or maintainability. We have also a built a strong relationship

with the assembler of the core equipment for our fracturing fleets. We believe the collaborative partnerships we have developed with our vendors should give us ready access to sufficient fabrication capacity for our growth.

Our Acquisitions

On February 22, 2017, we acquired all membership interests of Titan Frac Services LLC, a wholly owned subsidiary of TPIH Group Inc., for $65.0 million in cash.

Marketing and Customers

Our sales and marketing activities typically are performed through our local sales representatives in each geographic region, and are supported by our corporate headquarters. For the years ended December 31, 2019, 2018 and 2017, our top five customers collectively accounted for approximately 35%, 42% and 53% of our revenues, respectively. No customer accounted for more than 10% of our revenues for the year ended December 31, 2019. For the year ended December 31, 2018, Extraction Oil & Gas, Inc. accounted for more than 10% of our revenues. Extraction Oil & Gas, Inc. and SM Energy Company each accounted for more than 10% of our revenues for the year ended December 31, 2017.

Suppliers

We have a dedicated supply chain team that manages sourcing and logistics to ensure flexibility and continuity of supply in a cost effective manner across our areas of operation. We have built long-term relationships with multiple industry leading suppliers of proppant, chemicals and hydraulic fracturing equipment and have started to internally design and assemble key pump and maintenance parts. In addition, we have built a strong relationship with the assembler of our custom-designed hydraulic fracturing fleets and believe we will continue to have timely access to new, high capability fleets as we continue to grow.

We purchase a wide variety of raw materials, parts and components that are manufactured and supplied for our operations. We are not dependent on any single source of supply for those parts, supplies or materials. To date, we have generally been able to obtain the equipment, parts and supplies necessary to support our operations on a timely basis. While we believe that we will be able to make satisfactory alternative arrangements in the event of any interruption in the supply of these materials and/or products by one of our suppliers, we may not always be able to do so. In addition, certain materials for which we do not currently have long-term supply agreements could experience shortages and significant price increases in the future. As a result, we may be unable to mitigate any future supply shortages and our results of operations, prospects and financial condition could be adversely affected.

Competition

The markets in which we operate are highly competitive. We provide services in various geographic regions across the United States, and our competitors include many large and small oilfield service providers, including some of the largest integrated service companies. Our hydraulic fracturing services compete with large, integrated companies such as Halliburton Company and Schlumberger Limited as well as other companies including BJ Services Company, Calfrac Well Services Ltd., FTS International, Inc., NexTier Oilfield Solutions Inc., Patterson-UTI Energy, Inc., ProPetro Services, Inc., RPC, Inc. and U.S. Well Services, Inc. In addition, our industry is highly fragmented and we compete regionally with a significant number of smaller service providers.

We believe that the principal competitive factors in the markets we serve are technical expertise, equipment capacity, work force competency, efficiency, safety record, reputation, experience and price. Additionally, projects are often awarded on a bid basis, which tends to create a highly competitive environment. We seek to differentiate ourselves from our competitors by delivering the highest-quality services and equipment possible, coupled with superior execution and operating efficiency in a safe working environment.

Our operations are organized into a single business segment, which consists of hydraulic fracturing services and goods, and we have one reportable geographical business segment, the United States. Operating segments are defined under generally accepted accounting principles in the United States of America (“GAAP”) as components of an enterprise that engage in activities (i) from which it may earn revenues and incur expenses and (ii) for which separate operational financial information is available and is regularly evaluated by the chief operating decision maker for the purpose of allocating resources and assessing performance.

Environmental and Occupational Safety and Health Matters

Our operations in support of oil and natural gas exploration, development and production activities pursued by our customers are subject to stringent federal, tribal, regional, state and local laws and regulations governing occupational safety and health, the discharge of materials into the environment and environmental protection. Numerous governmental entities, including the U.S. Environmental Protection Agency (“EPA”), the U.S. Occupational Safety and Health Administration (“OSHA”), and analogous state agencies have the power to enforce compliance with these laws and regulations and the permits issued under them, often requiring difficult and costly actions, including the incurrence of potentially significant capital or operating expenditures to mitigate or prevent the releases of materials from our equipment, facilities or from customer locations where we provide our services. These laws and regulations may, among other things, (i) require the acquisition of permits or other authorizations for conducting regulated activities; (ii) limit or prohibit our operations on certain lands lying within wilderness, wetlands and other protected areas; (iii) require remedial measures to mitigate pollution from former and ongoing operations; (iv) impose restrictions on the types, quantities and concentrations of various substances that can be released into the environment or injected in formations in connection with oil and natural gas drilling and production activities; (v) impose specific safety and health criteria addressing worker protection; and (vi) impose substantial liabilities for pollution resulting from our operations. Any failure to comply with these laws and regulations may result in the assessment of sanctions, including administrative, civil and criminal penalties; the imposition of investigatory, remedial or corrective action obligations or the incurrence of capital expenditures; the occurrence of restrictions, delays or cancellations in the permitting, performance or development of projects or operations; and the issuance of orders enjoining performance of some or all of our operations in a particular area.

The trend in environmental regulation is to place more restrictions and limitations on activities that may adversely affect the environment, and thus any new laws and regulations, amendment of existing laws and regulations, reinterpretation of legal requirements or increased government enforcement with respect to environmental matters that result in more stringent and costly completion activities, pollution control equipment, waste handling, storage transport, disposal, or remediation requirements could have a material adverse effect on our financial position and results of operations. We may be unable to pass on such increased compliance costs to our customers. Moreover, accidental releases or spills may occur in the course of our operations, and we cannot assure you that we will not incur significant costs and liabilities as a result of such releases or spills, including any third-party claims for injuries to persons or damages to properties or natural resources. Our customers may also incur increased costs, or restrictions, delays or cancellations in permitting or operating activities as a result of more stringent environmental laws and regulations, which may result in a curtailment of exploration, development or production activities that would reduce the demand for our services. Historically, our worker health and safety as well as our environmental compliance costs have not had a material adverse effect on our results of operations; however, there can be no assurance that such costs will not be material in the future or that such future compliance will not have a material adverse effect on our business and operating results.

The following is a summary of the more significant existing environmental and occupational safety and health laws, as amended from time to time, to which our business is subject and for which compliance may have a material adverse impact on our capital expenditures, results of operations or financial position.

Worker Health and Safety

We are subject to the requirements of the federal Occupational Safety and Health Act, and comparable state statutes that regulate the protection of the health and safety of workers. In addition, the OSHA hazard communication standard, the EPA community right-to-know regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable state statutes require that information be maintained about hazardous materials used or produced in our operations and that this information be provided to employees, state and local government authorities and the public. These worker health and safety laws and regulations are subject to amendment including, for example, rulemaking adopted by OSHA in 2016 imposing more stringent permissible exposure limits for worker exposure to respirable crystalline silica, and any failure to comply with these laws could lead to the assertion of third-party claims against us, civil or criminal fines and changes in the way we operate our facilities, any of which could have an adverse effect on our financial position.

Motor Carrier Operations

In connection with the services we provide, we operate as a motor carrier and therefore are subject to regulation by the U.S. Department of Transportation (“DOT”) and analogous state agencies. These regulatory authorities exercise broad powers, governing activities such as the authorization to engage in motor carrier operations; regulatory safety; hazardous materials labeling, placarding and marking; financial reporting; and certain mergers, consolidations and acquisitions. There are additional regulations specifically relating to the trucking industry, including testing and specification of equipment and product handling requirements. The trucking industry is subject to possible regulatory and legislative changes that may increase our costs as well as affect the economics of the industry by requiring changes in operating practices or by changing the demand for common or contract carrier services or the cost of providing truckload services. Some of these possible changes include increasingly stringent environmental regulations, changes in the hours of service regulations that govern the amount of time a driver may drive in any specific period and requiring onboard electronic logging devices or limits on vehicle weight and size.

Interstate motor carrier operations are subject to safety requirements prescribed by DOT. Intrastate motor carrier operations are subject to state safety regulations that often mirror federal regulations but may be more stringent. Such matters as weight and dimension of motor carrier-related equipment are also subject to federal and state regulations. DOT regulations also mandate drug testing of drivers. From time to time, various legislative proposals are introduced, including proposals to increase federal, state or local taxes, such as, for example, taxes on motor fuels, which may increase our costs or adversely impact the recruitment of drivers. We cannot predict whether, or in what form, any increase in such taxes applicable to us would be enacted.

Radioactive Materials

Certain of our operations utilize equipment that contains sealed, low-grade radioactive sources. Our activities involving the use of radioactive materials are regulated by the U.S. Nuclear Regulatory Commission (“NRC”) and state regulatory agencies under agreement with the NRC. Standards implemented by these regulatory agencies require us to obtain licenses or other approvals for the use of such radioactive materials. Additionally, these regulatory agencies impose certain requirements concerning worker protection with respect to radioactive sources and may otherwise issue regulations regarding the handling and storage of this equipment that may result in increased costs. The violation of these laws and regulations may result in the denial or revocation of licenses or other approvals, issuance of corrective action orders, injunctions prohibiting some or all of our operations in a particular area, and assessment of sanctions, including administrative, civil and criminal penalties.

Hazardous Substances and Wastes and Naturally Occurring Radioactive Materials

The federal Resource Conservation and Recovery Act (“RCRA”), and comparable state statutes, regulate the generation, treatment, storage, transportation, disposal and clean-up of hazardous and non-hazardous wastes. Pursuant to rules issued by the EPA, individual states administer some or all of the provisions of RCRA, sometimes in conjunction with their own, more stringent requirements. Drilling fluids, produced waters, and most of the other wastes associated with the exploration, development, and production of oil or natural gas, if properly handled, are currently exempt from regulation as hazardous waste under RCRA and, instead, are regulated under RCRA’s less stringent non-hazardous waste provisions, state laws or other federal laws. However, it is possible that certain oil and gas drilling and production wastes now classified as non-hazardous could be classified as hazardous wastes in the future. For example, in response to a federal consent decree issued in 2016, the EPA was required during 2019 to determine whether certain Subtitle D criteria regulations required revision in a manner that could result in oil and natural gas wastes being regulated as RCRA hazardous wastes. In April 2019, the EPA made a determination that such revision of the regulations was unnecessary. A loss of the RCRA exclusion for drilling fluids, produced waters and related wastes could result in an increase in our and the oil and natural gas exploration and production industry’s costs to manage and dispose of generated hazardous wastes, which could have a material adverse effect on our results of operations and financial position. Additionally, other wastes handled at exploration and production sites or generated in the course of providing well services may not fall within this exclusion. In the course of our operations, we generate some amounts of ordinary industrial wastes that may be regulated as hazardous wastes.

Moreover, there have been public concerns expressed about naturally occurring radioactive materials (“NORM”) being detected in flow back water resulting from hydraulic fracturing that may contaminate extraction and processing equipment used in the oil and natural gas industry. NORM is subject primarily to individual state radiation control regulations while NORM handling and management activities are governed by regulations promulgated by OSHA. These state and federal regulations impose certain requirements concerning worker protection with respect to NORM as well as the treatment, storage, and disposal of NORM and NORM waste, management of NORM-contaminated waste piles, containers and tanks, and limitations on the relinquishment of NORM contaminated land for unrestricted use under RCRA and state laws. Concern over NORM in general, or NORM in groundwater in particular, could result in further regulation in the treatment, storage, handling and discharge of flow back water generated from oil and natural gas activities, including hydraulic fracturing, or handling of NORM-impacted

equipment that, if implemented, could increase our or our customers’ costs or liabilities associated with elevated levels of NORM as well as limit drilling by our customers, which developments may reduce demand for our services.

The federal Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”), also known as the “Superfund” law, and comparable state statutes impose liability, without regard to fault or legality of the original conduct, on classes of persons that are considered to have contributed to the release of a hazardous substance into the environment. Such classes of persons include the current and past owners or operators of sites where a hazardous substance was released, and anyone who disposed or arranged for the disposal of a hazardous substance released at the site. Under CERCLA, these persons may be subject to joint and several, strict liability for the costs of cleaning up the hazardous substances that have been released into the environment and for damages to natural resources even if the liability results from conduct that was lawful at the time it occurred or is due to the conduct, or conditions caused by, prior operators or third parties. In addition, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the hazardous substances released into the environment. We own, lease, or operate numerous properties and facilities that for many years have been used for industrial activities, including oil and natural gas-related operations. Hazardous substances, wastes, or hydrocarbons may have been released on or under the properties owned or leased by us, or on or under other locations where such substances have been taken for recycling or disposal. In addition, some of these properties have been operated by third parties or by previous owners whose treatment and disposal or release of hazardous substances, wastes, or hydrocarbons, was not under our control. These properties and the substances disposed or released on them may be subject to CERCLA, RCRA and analogous state laws. Under such laws, we could be required to remove previously disposed substances and wastes and remediate contaminated property (including groundwater contamination), including instances where the prior owner or operator caused the contamination, or perform remedial plugging of disposal wells or waste pit closure operations to prevent future contamination.

Water Discharges and Discharges into Belowground Formations

The Federal Water Pollution Control Act, also known as the Clean Water Act (“CWA”) and analogous state laws, impose restrictions and strict controls with respect to the discharge of pollutants, including spills and leaks of oil and hazardous substances, into state waters and waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA or an analogous state agency. Spill prevention, control and countermeasure plan requirements imposed under the CWA require appropriate containment berms and similar structures to help prevent the contamination of navigable waters in the event of a petroleum hydrocarbon tank spill, rupture or leak. In addition, the CWA and analogous state laws require individual permits or coverage under general permits for discharges of storm water runoff from certain types of facilities. The CWA also prohibits the discharge of dredge and fill material in regulated waters, including wetlands, unless authorized by a permit issued by the U.S. Army Corps of Engineers (“Corps”). The CWA and analogous state laws also may impose substantial civil and criminal penalties for non-compliance including spills and other non-authorized discharges.

In 2015, the EPA and the Corps under the Obama Administration published a final rule outlining their position on federal jurisdictional reach over waters of the United States, including wetlands. In 2017, the EPA and the Corps under the Trump Administration agreed to reconsider the 2015 rule and, thereafter, on October 22, 2019, the agencies published a final rule made effective on December 23, 2019, rescinding the 2015 rule. On January 23, 2020, the two agencies issued a final rule re-defining the CWA's jurisdiction over waters of the United States, which redefinition is narrower than found in the 2015 rule. Upon being published in the Federal Register and the passage of 60 days thereafter, the January 23, 2020 final rule will become effective, at which point the United States will be covered under a single regulatory scheme as it relates to federal jurisdictional reach over waters of the United States. However, there remains the expectation that the January 23, 2020 final rule also will be legally challenged in federal district court. To the extent that any challenge to the January 23, 2020 final rule is successful and the 2015 rule or a revised rule expands the scope of the CWA's jurisdiction in areas where we or our oil and natural gas exploration and production customers conduct operations, we or our customers could incur increased costs and our customers could incur delays or cancellations in permitting or projects, which could reduce demand for our products and services.

The Oil Pollution Act of 1990 (“OPA”) amends the CWA and sets minimum standards for prevention, containment and cleanup of oil spills. OPA applies to vessels, offshore facilities, and onshore facilities, including exploration and production facilities that may affect waters of the United States. Under OPA, responsible parties including owners and operators of onshore facilities may be held strictly liable for oil cleanup costs and natural resource damages as well as a variety of public and private damages that may result from oil spills. The OPA also requires owners or operators of certain onshore facilities to prepare facility response plans for responding to a worst-case discharge of oil into waters of the United States.

Our oil and natural gas producing customers dispose of flowback and produced water or certain other oilfield fluids gathered from oil and natural gas producing operations in accordance with permits issued by government authorities overseeing such disposal activities. While these permits are issued pursuant to existing laws and regulations, these legal requirements are

subject to change based on concerns of the public or governmental authorities regarding such disposal activities. One such concern relates to seismic events near underground disposal wells used for the disposal by injection of flowback and produced water or certain other oilfield fluids resulting from oil and natural gas activities. In 2016, the United States Geological Survey identified six states with more significant rates of induced seismicity that could be attributed to injection of oilfield fluids into underground disposal wells, including Oklahoma, Kansas, Texas, Colorado, New Mexico, and Arkansas. Since that time, the United States Geological Survey indicates that these rates have decreased in these states, although concern continues to exist over quakes arising from induced seismic activities. In response to concerns between use of underground disposal wells and the occurrence of seismic events, regulators in some states have imposed, or are considering imposing, additional requirements in the permitting of produced water disposal wells or otherwise to assess any relationship between seismicity and the use of such wells. For example, Texas and Oklahoma have issued rules for produced water disposal wells that impose certain permitting restrictions, operating restrictions and/or reporting requirements on disposal wells in proximity to faults. Additionally, from time to time, states may develop and implement plans directing certain wells where seismic incidents have occurred to restrict or suspend disposal well operations, as has occurred in Oklahoma. For example, in late 2016, the Oil and Gas Conservation Division of the Oklahoma Corporation Commission (“OCC”) and the Oklahoma Geological Survey released well completion seismicity guidance, which requires operators to take certain prescriptive actions, including an operator’s planned mitigation practices, following certain unusual seismic activity within 1.25 miles of hydraulic fracturing operations. In recent years the OCC’s Oil and Gas Conservation Division has issued orders limiting future increases in the volume of oil and natural gas produced water injected belowground into the Arbuckle formation in an effort to reduce the number of earthquakes in the state. Another consequence of seismic events may be lawsuits alleging that disposal well operations have caused damage to neighboring properties or otherwise violated state and federal rules regulating waste disposal. These developments could result in additional regulation and restrictions on the use of injection wells by our customers to dispose of flowback and produced water and certain other oilfield fluids. Increased regulation and attention given to seismicity events suspected of having been induced by injection of oilfield fluids into underground disposal wells also could lead to greater opposition to, and litigation concerning, oil and natural gas activities utilizing injection wells for waste disposal. Any of these developments may result in our customers having to limit disposal well volumes, disposal rates or locations, or require our customers or third party disposal well operators that are used to dispose of customer produced water to shut down disposal wells, which developments could adversely affect our customers’ business and result in a corresponding decrease in the need for our services, which would could have a material adverse effect on our business, financial condition, and results of operations.

Air Emissions