As filed with the Securities and Exchange Commission on

March 11, 2022.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

*

(Exact Name of Registrant as Specified in its Charter)

Delaware |

4924 |

47-1929160 | ||

(State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

700 Milam Street, Suite 1900

Houston, Texas 77002

(713)

375-5000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Zach Davis

President and Chief Financial Officer

700 Milam Street, Suite 1900

Houston, Texas 77002

(713)

375-5000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

George J. Vlahakos

Sidley Austin LLP

1000 Louisiana Street, Suite 5900

Houston, TX 77002

(713)

495-4522

Approximate date of commencement of proposed sale to the public

If the securities being registered on this Form are to be offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, as amended, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2

of the Exchange Act: | Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| ☒ | Smaller reporting company | |||||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule

13e-4(i)

(Cross-Border Issuer Tender Offer) ☐ Exchange Act Rule

14d-1(d)

(Cross-Border Third-Party Tender Offer) ☐ Each registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANT GUARANTORS

* |

The following are additional registrants that are guaranteeing the securities registered hereby: |

| Exact Name of Registrant Guarantor as Specified in its Charter(1) |

State or Other Jurisdiction of Incorporation or Organization |

I.R.S. Employer Identification Number | ||

| Corpus Christi Liquefaction, LLC |

Delaware |

35-2445602 | ||

| Cheniere Corpus Christi Pipeline, L.P. |

Delaware |

20-4711857 | ||

| Corpus Christi Pipeline GP, LLC |

Delaware |

47-1936771 |

(1) |

The address, including zip code, and telephone number, including area code, of each additional registrant guarantor’s executive offices is 700 Milam Street, Suite 1900, Houston, Texas 77002, (713) 375-5000. |

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED MARCH 11, 2022

PROSPECTUS

CHENIERE CORPUS CHRISTI HOLDINGS, LLC

Offer to exchange up to

$750,000,000 of 2.742% Senior Secured Notes due 2039

(CUSIP No. 16412X AL9)

that have been registered under the Securities Act of 1933

for

$750,000,000 of 2.742% Senior Secured Notes due 2039

(CUSIP NOS. 16412X AK1 AND U16327 AE5)

that have not been registered under the Securities Act of 1933

THE EXCHANGE OFFER EXPIRES AT 5:00 P.M., NEW YORK

CITY TIME, ON , 2022, UNLESS WE EXTEND IT

Terms of the Exchange Offer:

| • | We are offering to exchange up to $750,000,000 aggregate principal amount of registered 2.742% Senior Secured Notes due 2039 (CUSIP No. 16412X AL9) (the “New Notes”) for any and all of our $750,000,000 aggregate principal amount of unregistered 2.742% Senior Secured Notes due 2039 (CUSIP Nos. 16412X AK1 and U16327 AE5) (the “Old Notes” and together with the New Notes, the “notes”) that were issued on August 24, 2021. |

| • | We will exchange all outstanding Old Notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer for an equal principal amount of New Notes, as applicable. |

| • | The terms of the New Notes will be substantially identical to those of the outstanding Old Notes, except that the New Notes will be registered under the Securities Act of 1933, as amended (the “Securities Act”), and will not contain restrictions on transfer, registration rights or provisions for additional interest. |

| • | You may withdraw tenders of Old Notes at any time prior to the expiration of the exchange offer. |

| • | The exchange of Old Notes for New Notes will not be a taxable event for U.S. federal income tax purposes. |

| • | We will not receive any cash proceeds from the exchange offer. |

| • | The Old Notes are, and the New Notes will be, secured by first-priority liens on substantially all right, title and interest in or to substantially all of our assets and the assets of our current and any future guarantors along with certain other items listed under “Description of Senior Notes” (the “Collateral”). |

| • | The Old Notes are, and the New Notes will be, guaranteed on a senior basis by all of our existing subsidiaries and certain of our future domestic subsidiaries (as described herein). |

| • | There is no established trading market for the New Notes or the Old Notes. |

| • | We do not intend to apply for listing of the New Notes on any national securities exchange or for quotation through any quotation system. |

Please read “Risk Factors” beginning on page 16 for a discussion of certain risks that you should consider prior to tendering your outstanding Old Notes in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Each broker-dealer that receives New Notes for its own account pursuant to the exchange offer must acknowledge by way of letter of transmittal that it will deliver a prospectus in connection with any resale of such New Notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, such broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of New Notes received in exchange for Old Notes where such Old Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. Please read “Plan of Distribution.”

The date of this prospectus is , 2022.

TABLE OF CONTENTS

| ii | ||||

| ii | ||||

| ii | ||||

| iv | ||||

| 1 | ||||

| 16 | ||||

| 38 | ||||

| 39 | ||||

| 53 | ||||

| 62 | ||||

| 65 | ||||

| 66 | ||||

| 67 | ||||

| 86 | ||||

| 96 | ||||

| 146 | ||||

| 162 | ||||

| 207 | ||||

| 214 | ||||

| 216 | ||||

| 217 | ||||

| 218 | ||||

| 218 | ||||

| 219 | ||||

| 275 | ||||

F-1 |

This prospectus incorporates important business and financial information about us that is not included or delivered with this prospectus. We will provide this information to you at no charge upon written or oral request directed to Corporate Secretary, Cheniere Corpus Christi Holdings, LLC, 700 Milam Street, Suite 1900, Houston, Texas 77002 (telephone number (713)

375-5000).

In order to ensure timely delivery of this information, any request should be made by , 2022, five business days prior to the expiration date of the exchange offer.

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement we filed with the U.S. Securities and Exchange Commission, referred to in this prospectus as the SEC. No person has been authorized to give any information or any representation concerning us or the exchange offer (other than as contained in this prospectus or the related letter of transmittal) and we take no responsibility for, nor can we provide any assurance as to the reliability of, any other information that others may give you. We are not making an offer to sell these securities in any state or jurisdiction where the offer is not permitted. You should not assume that the information contained in or incorporated by reference into this prospectus is accurate as of any date other than the date on the front cover of this prospectus or the date of such incorporated documents, as the case may be.

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly, current and other reports with the SEC under the Securities and Exchange Act of 1934, as amended (the “Exchange Act”). Our SEC filings are available to the public over the Internet at the SEC’s website at . We will provide you upon request, without charge, a copy of the notes and the indenture governing the notes. You may request copies of these documents by contacting us at:

www.sec.gov

Cheniere Corpus Christi Holdings, LLC

Attention: Corporate Secretary

700 Milam Street, Suite 1900

Houston, Texas, 77002

(713)

375-5000

We also make all periodic and other information filed or furnished with the SEC available, free of charge, on our website at as soon as reasonably practicable after such information is electronically filed with or furnished to the SEC. Except as otherwise set forth herein, information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

www.cheniere.com

PRESENTATION OF INFORMATION

In this prospectus, we rely on and refer to information and statistics regarding our industry. We obtained this market data from independent industry publications or other publicly available information. Although we believe that these sources are reliable, we have not independently verified and do not guarantee the accuracy or completeness of this information.

In this prospectus, unless the context otherwise requires:

| • | Bcf |

| • | Bcf/d |

| • | Bcfe |

| • | Bcf/yr |

| • | DOE |

| • | Dth/d |

| • | EPC |

ii

| • | FERC |

| • | FOB |

| • | FTA |

| • | FTA countries |

| • | GAAP |

| • | Henry Hub |

| • | IPM Agreement |

| • | LIBOR |

| • | LNG |

| • | MMBtu |

| • | MMBtu/d |

| • | mtpa |

| • | non-FTA countries |

| • | SPA |

| • | SOFR |

| • | TBtu |

| • | Tcf |

| • | Train |

iii

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains certain statements that are, or may be deemed to be, “forward-looking statements.” All statements, other than statements of historical or present facts or conditions, included herein are “forward-looking statements.” Included among “forward-looking statements” are, among other things:

| • | statements that we expect to commence or complete construction of our proposed LNG terminal, liquefaction facility, pipeline facility or other projects, or any expansions or portions thereof, by certain dates, or at all; |

| • | statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of LNG imports into or exports from North America and other countries worldwide or purchases of natural gas, regardless of the source of such information, or the transportation or other infrastructure or demand for and prices related to natural gas, LNG or other hydrocarbon products; |

| • | statements regarding any financing transactions or arrangements, or our ability to enter into such transactions; |

| • | statements regarding our future sources of liquidity and cash requirements; |

| • | statements relating to the construction of our Trains and pipeline, including statements concerning the engagement of any EPC contractor or other contractor and the anticipated terms and provisions of any agreement with any EPC or other contractor, and anticipated costs related thereto; |

| • | statements regarding any SPA or other agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total natural gas liquefaction or storage capacities that are, or may become, subject to contracts; |

| • | statements regarding counterparties to our commercial contracts, construction contracts, and other contracts; |

| • | statements regarding our planned development and construction of additional Trains and pipelines, including the financing of such Trains and pipelines; |

| • | statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities; |

| • | statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections, or objectives, including anticipated revenues, capital expenditures, maintenance and operating costs and cash flows, any or all of which are subject to change; |

| • | statements regarding legislative, governmental, regulatory, administrative or other public body actions, approvals, requirements, permits, applications, filings, investigations, proceedings or decisions; |

| • | statements regarding the COVID-19 pandemic and its impact on our business and operating results, including any customers not taking delivery of LNG cargoes, the ongoing creditworthiness of our contractual counterparties, any disruptions in our operations or construction of our Trains and the health and safety of Cheniere’s employees, and on our customers, the global economy and the demand for LNG; and |

| • | any other statements that relate to non-historical or future information. |

All of these types of statements, other than statements of historical or present facts or conditions, are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as “may,” “will,” “could,” “should,” “achieve,” “anticipate,” “believe,” “contemplate,” “continue,” “estimate,” “expect,” “intend,” “plan,” “potential,” “predict,” “project,” “pursue,” “target,” the negative of such terms or

iv

other comparable terminology. The forward-looking statements contained in this prospectus are largely based on our expectations, which reflect estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe that such estimates are reasonable, they are inherently uncertain and involve a number of risks and uncertainties beyond our control. In addition, assumptions may prove to be inaccurate. We caution that the forward-looking statements contained in this prospectus are not guarantees of future performance and that such statements may not be realized or the forward-looking statements or events may not occur. Actual results may differ materially from those anticipated or implied in forward-looking statements as a result of a variety of factors described in this prospectus and in the reports and other information that we file with the SEC, including those discussed in “Risk Factors” and elsewhere in this prospectus. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these risk factors. These forward-looking statements speak only as of the date made, and other than as required by law, we undertake no obligation to update or revise any forward-looking statement or provide reasons why actual results may differ, whether as a result of new information, future events or otherwise.

v

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. It does not contain all of the information that you should consider before making an investment decision. You should carefully read this prospectus and should consider, among other things, the matters set forth under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto appearing elsewhere in this prospectus. Please read “Risk Factors” beginning on page 16 of this prospectus.

Throughout this prospectus, unless we indicate otherwise or the context otherwise requires, the term “CCH” refers to Cheniere Corpus Christi Holdings, LLC, and the terms “we,” “our,” “us” and similar terms refer to CCH and its subsidiaries. Certain terms used and not defined in this section shall have the meanings attributed to such terms in the “Glossary of Certain Finance Document Terms” or the “Glossary of Certain Defined Terms” below.

Overview of the Liquefaction Project

Overview

CCH is a Delaware limited liability company formed in September 2014 by Cheniere Energy, Inc. (“Cheniere”). We provide clean, secure and affordable LNG to integrated energy companies, utilities and energy trading companies around the world. We aspire to conduct our business in a safe and responsible manner, delivering a reliable, competitive and integrated source of LNG to our customers.

We operate a natural gas liquefaction and export facility (the “Liquefaction Facilities”) and operate a

21.5-mile

natural gas supply pipeline that interconnects the natural gas liquefaction and export facility at Corpus Christi (the “Corpus Christi LNG terminal”) with several interstate and intrastate natural gas pipelines (the “Corpus Christi Pipeline” and together with the Liquefaction Facilities, the “Liquefaction Project”) near Corpus Christi, Texas, through our subsidiaries Corpus Christi Liquefaction, LLC (“CCL”) and Cheniere Corpus Christi Pipeline, L.P. (“CCP”), respectively. We operate three Trains for a total production capacity of approximately 15 mtpa of LNG. The Liquefaction Project also includes three LNG storage tanks with aggregate capacity of approximately 10 Bcfe and two marine berths that can each accommodate vessels with nominal capacity of up to 266,000 cubic meters. Corpus Christi LNG Terminal

Liquefaction Facilities

We operate three Trains and two marine berths at the Liquefaction Project. We commenced commercial operating activities of Trains One, Two and Three of the Liquefaction Project in February 2019, August 2019 and March 2021, respectively.

The following summarizes the volumes of natural gas for which we have received approvals from FERC to site, construct and operate the Liquefaction Project and the orders we have received from the DOE authorizing the export of domestically produced LNG by vessel from the Liquefaction Project through December 31, 2050:

FERC Approved Volume |

DOE Approved Volume |

|||||||||||||||

(in Bcf/yr) |

(in mtpa) |

(in Bcf/yr) |

(in mtpa) |

|||||||||||||

| FTA countries |

875.16 | 17 | 875.16 | 17 | ||||||||||||

| Non-FTA countries |

875.16 | 17 | 767 | (1) | 15 | |||||||||||

| (1) | The authorization for an additional 108.16 Bcf/yr (approximately 2 mtpa) of natural gas is currently pending. |

1

Pipeline Facilities

In November 2019, the FERC authorized CCP to construct and operate the pipeline for the additional facilities for the liquefaction and export of domestically-produced natural gas (“Corpus Christi Stage 3”) at the existing Liquefaction Project and pipeline location, which is being developed by a wholly owned subsidiary of Cheniere that is not owned or controlled by us. The pipeline will be designed to transport 1.5 Bcf/d of natural gas feedstock required by Corpus Christi Stage 3 from the existing regional natural gas pipeline grid.

Natural Gas Supply, Transportation and Storage

CCL has secured natural gas feedstock for the Corpus Christi LNG terminal through traditional long-term natural gas supply and IPM agreements. Additionally, to ensure that CCL is able to transport and manage the natural gas feedstock to the Corpus Christi LNG terminal, it has entered into transportation precedent and other agreements to secure firm pipeline transportation and storage capacity from third-parties.

2

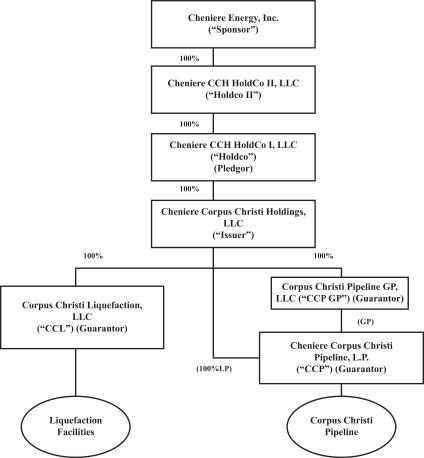

Organizational Structure

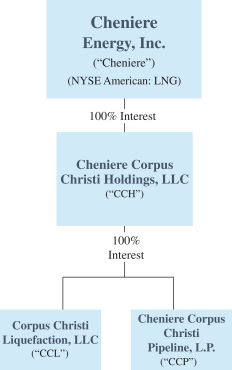

CCH owns 100% of the equity interests in (i) CCL, which owns the Liquefaction Facilities, (ii) CCP, which owns the Corpus Christi Pipeline, and (iii) Corpus Christi Pipeline GP, LLC (“CCP GP” and together with CCH, CCL and CCP collectively, the “Project Entities”), which holds all of the general partner interest in CCP. CCL, CCP and CCP GP constitute all of the current subsidiaries of CCH. CCH is an indirect wholly-owned subsidiary of Cheniere.

3

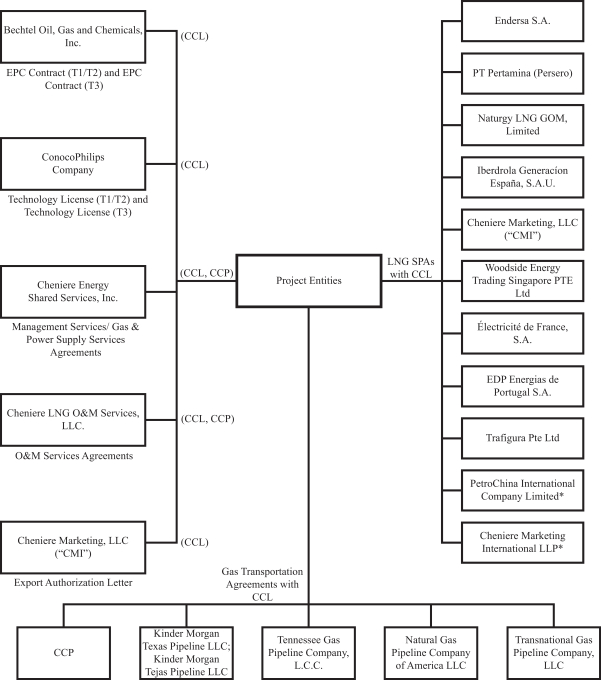

Certain Key Contractual Relationships

The following chart illustrates several of our current key contractual relationships for the Liquefaction Project. See “Description of Material Project Agreements” for additional information regarding certain of the agreements listed below.

4

| * | This SPA is structurally linked to the SPA between Cheniere Marketing International LLP and PetroChina International Company Limited. See “Description of Material Project Agreements—LNG Sale and Purchase Agreements—Stage 2—DES-Linked SPA.” |

LNG SPAs

We have contracted approximately 75% of the total production capacity from the Liquefaction Project through long-term SPAs, with approximately 18 years of weighted average remaining life as of December 31, 2021. The majority of the contracted capacity is comprised of fixed-price, long-term SPAs we have executed with third parties to sell LNG from Trains One through Three of the Liquefaction Project. Under the SPAs, the customers purchase LNG on a free on board (“FOB”) basis for a price consisting of a fixed fee per MMBtu of LNG (a portion of which is subject to annual adjustment for inflation) plus a variable fee per MMBtu of LNG generally equal to 115% of Henry Hub. Certain customers may elect to cancel or suspend deliveries of LNG cargoes, with advance notice as governed by each respective SPA, in which case the customers would still be required to pay the fixed fee with respect to the contracted volumes that are not delivered as a result of such cancellation or suspension. The variable fees under our SPAs were generally sized with the intention to cover the costs of gas purchases and variable transportation and liquefaction fuel to produce the LNG to be sold under each such SPA. In aggregate, the minimum annual fixed fee portion to be paid by the third-party SPA customers is approximately $1.8 billion for Trains One through Three of the Liquefaction Project. Our long-term SPA customers consist of creditworthy counterparties, with an average credit rating of BBB+, Baa1 and BBB+ by S&P Global Ratings, Moody’s Corporation and Fitch Ratings, respectively.

In addition to the third party SPAs discussed above, we have also executed SPAs with CMI UK to sell (1) approximately 15 TBtu per annum of LNG with a term through 2043, (2) any LNG produced by the Liquefaction Project in excess of that required for other customers at CMI UK’s option and (3) approximately 44 TBtu of LNG with a maximum term up to 2026 associated with our IPM agreement with EOG Resources, Inc. (“EOG”).

Natural Gas Supply, Transportation and Storage Service Agreements

We have secured natural gas feedstock for the Corpus Christi LNG terminal through long-term natural gas supply and IPM agreements. Under our IPM agreements, we pay for natural gas feedstock based on global gas market prices less fixed liquefaction fees and certain costs incurred by us. While IPM agreements are not revenue contracts for accounting purposes, the payment structure for the purchase of natural gas under the IPM agreements generates a style fixed liquefaction fee, assuming that LNG produced from the natural gas feedstock is subsequently sold at a price approximating the global LNG market price paid for the natural gas feedstock purchase.

take-or-pay

As of December 31, 2021, we have secured 87% of the natural gas supply required to support the total forecasted production capacity of the Liquefaction Project during 2022. Natural gas supply secured decreases as a percentage of forecasted production capacity beyond 2022. Natural gas supply is generally secured on an indexed pricing basis, with title transfer occurring upon receipt of the commodity. As further described in the section above, the pricing structure of our SPA arrangements with our customers incorporates a variable fee per MMBtu of LNG generally equal to 115% of Henry Hub, thus limiting our net exposure to future increases in natural gas prices. Inclusive of amounts under contracts with unsatisfied conditions precedent as of December 31, 2021, we have secured up to 2,642 TBtu of natural gas feedstock through agreements with remaining terms that range up to 10 years.

LNG SPAs

To ensure that we are able to transport natural gas feedstock to the Corpus Christi LNG terminal, we have entered into transportation precedent and other agreements to secure firm pipeline transportation capacity from third party pipeline companies. We have also entered into firm storage services agreements with third parties to assist in managing variability in natural gas needs for the Liquefaction Project.

5

Our Business Strategy

Our primary business strategy for the Liquefaction Project is to develop, construct and operate assets supported by long-term, fixed fee contracts. We plan to implement our strategy by:

| • | safely, efficiently and reliably operating and maintaining our assets; |

| • | procuring natural gas and pipeline transport capacity to our facility; |

| • | commencing commercial delivery for our long-term SPA customers, of which we have initiated for nine of ten third party long-term SPA customers as of December 31, 2021; |

| • | maximizing the production of LNG to serve our customers and generating steady and stable revenues and operating cash flows; |

| • | further expanding and/or optimizing the Liquefaction Project by leveraging existing infrastructure; |

| • | maintaining a prudent and cost-effective capital structure; and |

| • | strategically identifying actionable environmental solutions. |

Principal Executive Offices

Our principal executive office is located at 700 Milam Street, Suite 1900, Houston, Texas, 77002, and our telephone number is (713)

375-5000.

6

The Exchange Offer

On August 24, 2021, we completed a private offering of $750,000,000 aggregate principal amount of the Old Notes. As part of this private offering, we entered into a registration rights agreement with the initial purchasers of the Old Notes in which we agreed, among other things, to deliver this prospectus to you and to use our reasonable best efforts to consummate the exchange offer no later than 360 days after the August 24, 2021 private offering. The following is a summary of the exchange offer.

| Old Notes |

2.742% Senior Secured Notes due 2039, which were issued on August 24, 2021. |

| New Notes |

2.742% Senior Secured Notes due 2039. The terms of the New Notes are substantially identical to the terms of the outstanding Old Notes, except that the transfer restrictions, registration rights and provisions for additional interest relating to the Old Notes will not apply to the New Notes. |

| Exchange Offer |

We are offering to exchange up to $750 million aggregate principal amount of our New Notes that have been registered under the Securities Act for an equal amount of our outstanding Old Notes that have not been registered under the Securities Act to satisfy our obligations under the registration rights agreement. |

| The New Notes will evidence the same debt as the Old Notes for which they are being exchanged and will be issued under, and be entitled to the benefits of, the same indenture that governs the Old Notes. Holders of the Old Notes do not have any appraisal or dissenters’ rights in connection with the exchange offer. Because the New Notes will be registered, the New Notes will not be subject to transfer restrictions, and holders of Old Notes that have tendered and had their Old Notes accepted in the exchange offer will have no registration rights. The New Notes will have a CUSIP number different from that of any Old Notes that remain outstanding after the completion of the exchange offer. |

| Expiration Date |

The exchange offer will expire at 5:00 p.m., New York City time, on , 2022, unless we decide to extend the date. |

| Conditions to the Exchange Offer |

The exchange offer is subject to customary conditions, which we may waive. Please read “The Exchange Offer—Conditions to the Exchange Offer” for more information regarding the conditions to the exchange offer. |

| Procedures for Tendering Old Notes |

You must do one of the following on or prior to the expiration of the exchange offer to participate in the exchange offer: |

| • | tender your Old Notes by sending the certificates for your Old Notes, in proper form for transfer, a properly completed and duly executed letter of transmittal, with any required signature guarantees, and all other documents required by the letter of transmittal, to The Bank of New York Mellon, as registrar and |

7

| exchange agent, at the address listed under the caption “The Exchange Offer—Exchange Agent”; or |

| • | tender your Old Notes by using the book-entry transfer procedures described below and transmitting a properly completed and duly executed letter of transmittal, with any required signature guarantees, or an agent’s message instead of the letter of transmittal, to the exchange agent. In order for a book-entry transfer to constitute a valid tender of your Old Notes in the exchange offer, The Bank of New York Mellon, as registrar and exchange agent, must receive a confirmation of book-entry transfer of your Old Notes into the exchange agent’s account at The Depository Trust Company (“DTC”) prior to the expiration of the exchange offer. For more information regarding the use of book-entry transfer procedures, including a description of the required agent’s message, please read the discussion under the caption “The Exchange Offer—Procedures for Tendering—Book-entry Transfer.” |

| Withdrawal; Non-Acceptance |

You may withdraw any Old Notes tendered in the exchange offer at any time prior to 5:00 p.m., New York City time, on , 2022 by following the procedures described in this prospectus and the related letter of transmittal. If we decide for any reason not to accept any Old Notes tendered for exchange, the Old Notes will be returned to the registered holder at our expense promptly after the expiration or termination of the exchange offer. In the case of Old Notes tendered by book-entry transfer in to the exchange agent’s account at DTC, any withdrawn or unaccepted Old Notes will be credited to the tendering holder’s account at DTC. For further information regarding the withdrawal of tendered Old Notes, please read “The Exchange Offer—Withdrawal Rights.” |

| U.S. Federal Income Tax Consequences |

The exchange of New Notes for Old Notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes. Please read the discussion under the caption “Material United States Federal Income Tax Consequences” for more information regarding the tax consequences to you of the exchange offer. |

| Use of Proceeds |

The issuance of the New Notes will not provide us with any new proceeds. We are making this exchange offer solely to satisfy our obligations under the registration rights agreement. |

| Fees and Expenses |

We will pay all of our expenses incident to the exchange offer. |

| Exchange Agent |

We have appointed The Bank of New York Mellon as exchange agent for the exchange offer. For the address, telephone number and fax number of the exchange agent, please read “The Exchange Offer—Exchange Agent.” |

| Resales of New Notes |

Based on interpretations by the staff of the SEC, as set forth in no-action letters issued to third parties that are not related to us, we |

8

| believe that the New Notes you receive in the exchange offer may be offered for resale, resold or otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act so long as: |

| • | the New Notes are being acquired in the ordinary course of business; |

| • | you are not participating, do not intend to participate, and have no arrangement or understanding with any person to participate in the distribution of the New Notes issued to you in the exchange offer; |

| • | you are not our affiliate or an affiliate of any of our subsidiary guarantors; and |

| • | you are not a broker-dealer tendering Old Notes acquired directly from us for your account. |

| The SEC has not considered this exchange offer in the context of a no-action letter, and we cannot assure you that the SEC would make similar determinations with respect to this exchange offer. If any of these conditions are not satisfied, or if our belief is not accurate, and you transfer any New Notes issued to you in the exchange offer without delivering a resale prospectus meeting the requirements of the Securities Act or without an exemption from registration of your New Notes from those requirements, you may incur liability under the Securities Act. We will not assume, nor will we indemnify you against, any such liability. Each broker-dealer that receives New Notes for its own account in exchange for Old Notes, where the Old Notes were acquired by such broker-dealer as a result of market-making or other trading activities, must acknowledge that it will deliver a prospectus in connection with any resale of such New Notes. Please read “Plan of Distribution.” |

| Please read “The Exchange Offer—Resales of New Notes” for more information regarding resales of the New Notes. |

| Consequences of Not Exchanging Your Old Notes |

If you do not exchange your Old Notes in this exchange offer, you will no longer be able to require us to register your Old Notes under the Securities Act, except in the limited circumstances provided under the registration rights agreement. In addition, you will not be able to resell, offer to resell or otherwise transfer your Old Notes unless we have registered the Old Notes under the Securities Act, or unless you resell, offer to resell or otherwise transfer them under an exemption from the registration requirements of, or in a transaction not subject to, the Securities Act. |

| For information regarding the consequences of not tendering your Old Notes and our obligation to file a registration statement, please read “The Exchange Offer—Consequences of Failure to Exchange Old Notes” and “Description of Senior Notes.” |

9

Terms of the New Notes

The terms of the New Notes will be substantially identical to the terms of the Old Notes, except that the transfer restrictions, registration rights and provisions for additional interest relating to the Old Notes will not apply to the New Notes. As a result, the New Notes will not bear legends restricting their transfer and will not have the benefit of the registration rights and additional interest provisions contained in the Old Notes. The New Notes represent the same debt as the Old Notes for which they are being exchanged. The New Notes are governed by the same indenture as that which governs the Old Notes.

The following summary contains basic information about the New Notes and is not intended to be complete. For a more complete understanding of the New Notes, please refer to the section in this prospectus entitled “Description of Senior Notes.” When we use the term “notes” in this prospectus, unless the context requires otherwise, the term includes the Old Notes and the New Notes.

| Issuer |

Cheniere Corpus Christi Holdings, LLC. |

| Notes Offered |

$750,000,000 aggregate principal amount of 2.742% Senior Secured Notes due 2039. |

| Maturity Date |

The New Notes mature on December 31, 2039. |

| Interest |

Interest on the New Notes will accrue at a rate equal to 2.742% per annum, computed on the basis of a 360-day year comprising twelve 30-day months. |

| Interest Payment Dates |

We will pay interest on the New Notes semi-annually, in cash in arrears, on June 30 and December 31 of each year, commencing on June 30, 2022. |

| Guarantees |

The New Notes will be guaranteed by all of our existing Domestic Subsidiaries and certain of our future Domestic Subsidiaries. As of the date of this prospectus, the Guarantors consist of each of CCL, CCP and CCP GP. See “Description of Senior Notes—Guarantees of the Notes.” |

| Security and Collateral |

The New Notes will be secured by a first priority security interest in substantially all of our and the Guarantors’ assets. The Collateral securing the New Notes includes: |

| • | substantially all of our assets and the assets of our existing and any future Guarantors (including real and personal property whether owned or leased on the closing date of this exchange offer or thereafter acquired); |

| • | a pledge by Holdco of all ownership interests in CCH; |

| • | all contracts, agreements and documents, including the Material Project Agreements, hedging arrangements and insurance policies, and all of our rights thereunder; |

| • | certain Accounts; |

| • | cash flow and other revenues; and |

10

| • | other real and personal property which is subject, from time to time, to the Security Interests or liens granted by the Security Documents. |

| Ranking |

The New Notes will constitute direct and unconditional senior secured obligations, and will rank pari passu |

| The New Notes will be effectively senior to all of our future junior lien obligations and future unsecured senior indebtedness, to the extent of the value of the Collateral securing the notes. |

| The New Notes will be effectively junior to any of our or our Subsidiaries’ secured indebtedness that is secured by liens on assets other than the Collateral securing the notes, to the extent of the value of such assets. |

| The New Notes will be structurally subordinated to any future indebtedness of our non-Guarantor Subsidiaries. |

| As of December 31, 2021, we had $589 million of available commitments, $361 million aggregate amount of issued letters of credit and $250 million of loans outstanding under the $1.2 billion working capital facility (the “Working Capital Facility”). |

| As of December 31, 2021, we had approximately $10.4 billion of total debt outstanding (before unamortized discount and debt issuance costs). As of December 31, 2021, we had approximately $1.7 billion of outstanding borrowings under our Term Loan Facility, $1.25 billion of outstanding 7.000% Senior Secured Notes due 2024 (the “2024 Senior Notes”), $1.5 billion of outstanding 5.875% Senior Secured Notes due 2025 (the “2025 Senior Notes”), $1.5 billion of 5.125% Senior Secured Notes due 2027 (the “2027 Senior Notes”), $1.5 billion of outstanding 3.700% Senior Secured Notes due 2029 (the “2029 Senior Notes”), $750 million of outstanding Old Notes (the Old Notes, together with the 2024 Senior Notes, the 2025 Senior Notes, the 2027 Senior Notes and the 2029 Senior Notes, the “144A Senior Notes”), $727.0 million of outstanding 4.80% Senior Secured Notes due 2039 (the “4.80% Senior Notes”), $475.0 million of outstanding 3.925% Senior Secured Notes due 2039 (the “3.925% Senior Notes”) and $768.7 million of outstanding 3.52% Senior Secured Notes due 2039 (the “3.52% Senior Notes” and, together with the 144A Senior Notes, the 4.80% Senior Notes and the 3.925% Senior Notes, the “Outstanding Senior Notes”). |

| Optional Redemption |

At any time from time to time prior to July 4, 2039, we may redeem the New Notes, in whole or in part, at a redemption price equal to the Make-Whole Price as defined under the caption “Description of Senior Notes—Optional Redemption,” plus accrued and unpaid |

11

| interest to the redemption date. We also may, at any time on or after July 4, 2039, redeem the New Notes, in whole or in part, at a redemption price equal to 100% of the principal amount of the New Notes to be redeemed, plus accrued and unpaid interest on the New Notes redeemed to the redemption date. See “Description of Senior Notes—Optional Redemption.” |

| Change of Control |

Upon the occurrence of a Change of Control, we must commence, within 30 days, and subsequently consummate an offer to purchase all notes then outstanding at a purchase price in cash equal to 101% of their aggregate principal amount, plus accrued and unpaid interest on the notes repurchased to the date of repurchase. After the Project Completion Date, a Change of Control shall not be deemed to have occurred if we receive rating reaffirmations from two rating agencies (or one rating agency, if only one rating agency currently rates the New Notes) reaffirming the then-current rating of the New Notes as of the date of such change of control. We may not be able to repurchase notes upon a Change of Control in certain circumstances. See “Risk Factors —Risks Relating to the Exchange Offer and the New Notes—We may not be able to repurchase notes upon a Change of Control or upon the exercise of the holders’ options to require repurchase of notes if certain prepayment triggering events occur, and the occurrence of certain of these events and our repurchase of notes as a result thereof could result in an event of default under the indenture or other agreements governing our indebtedness.” |

| Additional Offers to Purchase |

If we sell assets under certain circumstances and do not use the proceeds for certain specified purposes, if we receive insurance proceeds following a Catastrophic Casualty Event and do not use the proceeds for certain specified purposes, if we receive Performance Liquidated Damages payments under certain circumstances and do not use the proceeds for certain specified purposes, if we fail to maintain our Qualifying LNG SPAs in accordance with the terms of the indenture, or if certain of our Required Export Authorizations are Impaired, we must offer to repurchase the New Notes and may be required to make a repayment of other Senior Debt in amounts specified in the indenture and in our agreements related to our other Senior Debt. In each case, under the indenture, the purchase price of the New Notes will be equal to 100% of the principal amount of the New Notes repurchased, plus accrued and unpaid interest on the New Notes to, but excluding, the applicable repurchase date. See “Description of Senior Notes—Repurchase at the Option of Noteholders—Asset Sales,” “—Events of Loss,” “—Performance Liquidated Damages,” and “—LNG SPA Mandatory Offer.” We may not be able to repurchase the New Notes upon an Asset Sale, Event of Loss, receipt of Performance Liquidated Damages or an Indenture LNG SPA Prepayment Event in certain circumstances. See “Risk Factors—Risks Relating to the Exchange Offer and the New Notes—We may not be able to repurchase notes upon a Change of Control or upon the exercise of the holders’ options to require repurchase of |

12

| notes if certain prepayment triggering events occur, and the occurrence of certain of these events and our repurchase of notes as a result thereof could result in an event of default under the indenture or other agreements governing our indebtedness.” |

| Pre-Completion Account Flows |

Disbursements of Loans will be deposited into the Construction Account subject to certain rules described in our CSAA (as defined herein). See “Description of Security Documents —Common Security and Account Agreement—Pre-Completion Cash Flows.” |

| Unless paid directly towards the purpose for which they are incurred, disbursements of Senior Debt in connection with an issuance of Senior Notes under any Indenture will be made into a Senior Note Disbursement Account(s), subject to certain rules described in our CSAA. See “Description of Security Documents—Common Security and Account Agreement—Pre-Completion Cash Flows.” |

| Prior to the Project Completion Date, the Construction Account will be funded with any funds withdrawn and transferred from the Equity Proceeds Account and proceeds from our Senior Debt, and may from time to time be funded with any Business Interruption Insurance Proceeds and Delay Liquidated Damages payments received by us. Amounts in the Construction Account will be used to pay Project Costs in accordance with the construction budget and schedule and any Operation and Maintenance Expenses. |

| Prior to the Project Completion Date, any revenues will be deposited into the Equity Proceeds Account and may be transferred to the Construction Account. |

| Prior to the Project Completion Date, we must fund the Operating Account from the Construction Account, and must use the Operating Account to pay Operation and Maintenance Expenses that are due in a manner consistent with our obligations under our Common Terms Agreement and our Finance Documents, then in effect. |

| Post-Completion Account Flows |

After the completion of Train One, Train Two and Train Three, revenues received by us will be applied in the following manner: |

| • | first |

| • | second |

| • | third pari passu |

13

| scheduled payments of hedge termination value and gas hedge termination value to be paid by us pursuant to Permitted Hedging Instruments secured on a pari passu |

| • | fourth |

| • | fifth |

| • | sixth |

| • | seventh |

| • | eighth |

| • | ninth |

| Covenants |

The indenture governing the New Notes will contain covenants that, among other things and subject to certain exceptions and/or conditions, limit our ability and the ability of our Restricted Subsidiaries to: |

| • | make Restricted Payments; |

| • | incur additional Indebtedness or issue preferred stock; |

| • | assume, incur, permit or suffer to exist any Lien on any asset of CCH or any Restricted Subsidiary; |

14

| • | create or permit to exist or become effective any consensual encumbrance or restriction on the ability of any Restricted Subsidiary to pay dividends, pay indebtedness owed to CCH or any of its Restricted Subsidiaries, make loans or advances to CCH or any of its Restricted Subsidiaries, or sell, lease or transfer any properties or assets to CCH or any of its Restricted Subsidiaries; |

| • | dissolve, liquidate, consolidate, merge, sell or lease all or substantially all of the assets or properties of CCH and its Restricted Subsidiaries taken as a whole in one or more related transactions or permit any Guarantor to dissolve, liquidate, consolidate, merge, sell or lease all or substantially all of its assets and properties; |

| • | enter into certain transactions or agreements with or for the benefit of any Affiliate of CCH or any of its Restricted Subsidiaries; |

| • | amend or modify Material Project Agreements; |

| • | enter into any lifting and balancing arrangement or Sharing Arrangement with an External Train Entity; and |

| • | amend or modify any Qualifying LNG SPA. |

| These covenants are subject to a number of important limitations and exceptions that are described in this prospectus under the caption “Description of Senior Notes—Covenants Applicable to the Notes.” |

| No Exchange Listing |

We do not intend to list the New Notes on any national securities exchange or to arrange for quotation on any automated dealer quotation systems. There can be no assurance that an active trading market will develop for the New Notes. If an active trading market does not develop, the market price and liquidity of the New Notes may be adversely affected. |

| Risk Factors |

You should refer to the section entitled “Risk Factors” beginning on page 16 of this prospectus for a discussion of factors you should carefully consider before deciding to participate in the exchange offer. |

15

RISK FACTORS

Before deciding to participate in the exchange offer, you should carefully consider the risks and uncertainties described below together with all other information contained in this prospectus. The following are some of the important factors that could affect our financial performance or could cause actual results to differ materially from estimates or expectations contained in our forward-looking statements. We may encounter risks in addition to those described below.

Certain terms used and not defined in this section shall have the meanings attributed to such terms in the Glossary of Certain Finance Document Terms or the Glossary of Certain Defined Terms.

Risk Factor Summary

Each of the risk factors outlined below are discussed more fully following this summary:

Risks Relating to Our Financial Matters

Our operating results, cash flows and/or liquidity could be adversely affected by the following factors:

| • | Our existing level of cash resources and significant debt |

| • | Our ability to generate cash |

| • | Our efforts to manage commodity and financial risks through derivative instruments |

Risks Relating to our Operations and Industry

The operations of our Liquefaction Project and the growth of our LNG business could be adversely affected by the following factors:

| • | Catastrophic weather events or other disasters |

| • | Disruptions to the third party supply of natural gas to our pipeline and facilities |

| • | Inability to purchase or receive physical delivery of sufficient natural gas to satisfy our delivery obligations under the SPAs |

| • | Significant construction and operating hazards and uninsured risks |

| • | Cyclical or other changes in the demand for and price of LNG and natural gas |

| • | Failure of exported LNG to be a competitive source of energy for international markets |

| • | Competition based upon the international market price for LNG |

| • | A cyber attack involving our business, operational control systems or related infrastructure, or that of third party pipelines which supply the Liquefaction Facilities |

| • | Outbreaks of infectious diseases, such as the outbreak of COVID-19, at our facilities |

| • | Our dependency on Cheniere, including employees of Cheniere and its subsidiaries, for key personnel, and the unavailability of skilled workers or our failure to attract and retain qualified personnel |

| • | Our contractual and commercial relationships, and conflicts of interest, with Cheniere and its affiliates, including CMI UK |

Risks Relating to Regulations

The following governmental regulations matters could adversely affect our business:

| • | Failure to obtain and maintain approvals and permits from governmental and regulatory agencies |

| • | Subjectivity to FERC regulation |

| • | Existing and future environmental and similar laws and governmental regulations |

| • | Pipeline safety and compliance programs and repairs |

16

Risks Relating to the Exchange Offer and the New Notes

The consummation of the Exchange Offer and the issuance of the New Notes could be adversely affected by the following factors:

| • | Failure to properly tender your Old Notes |

| • | Our ability to incur substantially more indebtedness in the future |

| • | Our substantial indebtedness |

| • | Requirement of significant amounts of cash to service our indebtedness |

| • | Additional financing required to finance the construction of any additional Trains |

| • | Restrictions in the indenture governing the New Notes |

| • | Our ability to repurchase notes upon a Change of Control or upon the exercise of the holders’ options to require repurchase of notes |

| • | Federal and state statutes could require note holders to return payments received from us |

| • | Your ability to resell the New Notes |

| • | Sufficient collateral to pay all or any amounts due on the New Notes |

| • | Potential liens on the real property comprising the Trains and the Corpus Christi Pipeline that are senior to the security interests securing the New Notes |

| • | Certain real property rights that will not be mortgage prior to the issuance of the New Notes |

| • | Title insurance policy that has only been obtained on the real property rights of the Liquefaction Facilities and not for the Corpus Christi Pipeline |

| • | surveys obtained in connection with the real property rights underlying the Liquefaction Facilities and the Corpus Christi Pipeline may be inaccurate or not comprehensive |

| • | Limitation of remedies available to the Security Trustee |

| • | Termination of certain real property rights held by us constituting collateral for the New Notes |

| • | CSAA provisions that may limit the remedies that could be exercised in respect of an event of default |

| • | Remedies available to the holders of the notes and the Security Trustee in bankruptcy may be limited |

| • | Failure to perfect security interest in your collateral and other issues generally associated with the realization of security interest in your collateral |

| • | Casualty risks of the collateral |

| • | Representations and warranties, covenants or events of default contained in the Common Terms Agreement that are not contained in the indenture governing the New Notes |

| • | Any future pledge of collateral might be avoidable in bankruptcy |

| • | An existing or future subsidiary’s guarantee of the New Notes may not be sufficient |

| • | The New Notes will be structurally subordinated in right of payment to the indebtedness and other liabilities of any subsidiaries that do not guarantee the New Notes |

| • | Your right to receive payments under the New Notes will be effectively subordinated |

| • | The ratings of the New Notes may be lowered or withdrawn |

| • | Changes in our credit rating |

Risks Relating to Our Financial Matters

Our existing level of cash resources and significant debt could cause us to have inadequate liquidity and could materially and adversely affect our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

As of December 31, 2021, we had no cash and cash equivalents, $44 million of restricted cash and cash equivalents, $589 million of available commitments under our CCH Working Capital Facility and $10.4 billion of total debt outstanding on a consolidated basis (before unamortized debt issuance costs). We incur, and will incur, significant interest expense relating to the assets at the Corpus Christi LNG terminal. Our ability to refinance our indebtedness will depend on our ability to access additional project financing as well as the debt and equity capital markets. A variety of factors beyond our control could impact the availability or cost of capital, including domestic or international economic conditions, increases in key benchmark interest rates and/or credit spreads, the adoption

17

of new or amended banking or capital market laws or regulations and the repricing of market risks and volatility in capital and financial markets. Our financing costs could increase or future borrowings or equity offerings may be unavailable to us or unsuccessful, which could cause us to be unable to pay or refinance our indebtedness or to fund our other liquidity needs. We also rely on borrowings under our CCH Working Capital Facility to fund our capital expenditures. If any of the lenders in the syndicates backing our CCH Working Capital Facility was unable to perform on its commitments, we may need to seek replacement financing, which may not be available as needed, or may be available in more limited amounts or on more expensive or otherwise unfavorable terms.

Our ability to generate cash is substantially dependent upon the performance by customers under long-term contracts that we have entered into, and we could be materially and adversely affected if any significant customer fails to perform its contractual obligations for any reason.

Our future results and liquidity are substantially dependent upon performance by our customers to make payments under long-term contracts. As of December 31, 2021, we had SPAs with a total of ten different third party customers. While substantially all of our long-term third party customer arrangements are executed with a creditworthy parent company or secured by a parent company guarantee or other form of collateral, we are nonetheless exposed to credit risk in the event of a customer default that requires us to seek recourse.

Additionally, our long-term SPAs entitle the customer to terminate their contractual obligations upon the occurrence of certain events which include, but are not limited to: (1) if we fail to make available specified scheduled cargo quantities; (2) delays in the commencement of commercial operations; and (3) under the majority of our SPAs upon the occurrence of certain events of force majeure.

Although we have not had a history of material customer default or termination events, the occurrence of such events are largely outside of our control and may expose us to unrecoverable losses. We may not be able to replace these customer arrangements on desirable terms, or at all, if they are terminated. As a result, our business, contracts, financial condition, operating results, cash flow, liquidity and prospects could be materially and adversely affected.

Our efforts to manage commodity and financial risks through derivative instruments, including our IPM agreements, could adversely affect our results of operations and financial condition.

We use derivative instruments to manage commodity, currency and financial market risks. The extent of our derivative position at any given time depends on our assessments of the markets for these commodities and related exposures. We currently account for all derivative sat fair value, with immediate recognition of changes in the fair value in earnings. As described in “Management’s Discussion and Analysis of Financial Condition, Results of Operations”, our net loss of $180 million for the year ended December 31, 2021 was primarily due to derivative losses, with substantially all of such losses relating to commodity derivative instruments indexed to international LNG prices, mainly our IPM agreements. These transactions and other derivative transactions have and may continue to result in substantial volatility in reported results of operations, particularly in periods of significant commodity, currency or financial market variability, or as a result of ineffectiveness of these contracts. For certain of these instruments, in the absence of actively quoted market prices and pricing information from external sources, the value of these financial instruments involves management’s judgment or use of estimates. Changes in the underlying assumptions or use of alternative valuation methods could affect the reported fair value of these contracts.

In addition, our liquidity may be adversely impacted by the cash margin requirements of the commodities exchanges or the failure of a counterparty to perform in accordance with a contract.

18

Risks Relating to Our Operations and Industry

Catastrophic weather events or other disasters could result in an interruption of our operations, a delay in the completion of our Liquefaction Project, damage to our Liquefaction Project and increased insurance costs, all of which could adversely affect us.

Hurricane Harvey in 2017 and Winter Storm Uri in 2021 caused interruptions or temporary suspension in construction or operations at our Liquefaction Project or caused minor damage to our Liquefaction Project. In August 2020, we entered into an arrangement with our affiliate to provide the ability, in limited circumstances, to potentially fulfill commitments to LNG buyers from the other facility in the event operational conditions impact operations at the Corpus Christi LNG terminal or at our affiliate’s terminal. During the years ended December 31, 2021 and 2020, four TBtu 17 and TBtu, respectively, were loaded at our facilities for our affiliate pursuant to this agreement. Future storms and related storm activity and collateral effects, or other disasters such as explosions, fires, floods or accidents, could result in damage to, or interruption of operations at, the Corpus Christi LNG terminal or related infrastructure, as well as delays or cost increases in the construction and the development of our other facilities and increase our insurance premiums. The U.S. Global Change Research Program has reported that the U.S.’s energy and transportation systems are expected to be increasingly disrupted by climate change and extreme weather events. An increase in frequency and severity of extreme weather events such as storms, floods, fires and rising sea levels could have an adverse effect on our operations.

Disruptions to the third party supply of natural gas to our pipeline and facilities could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

We depend upon third party pipelines and other facilities that provide gas delivery options to our Liquefaction Project. If the construction of new or modified pipeline connections is not completed on schedule or any pipeline connection were to become unavailable for current or future volumes of natural gas due to repairs, damage to the facility, lack of capacity, failure to replace contracted firm pipeline transportation capacity on economic terms, or any other reason, our ability to receive natural gas volumes to produce LNG or to continue shipping natural gas from producing regions or to end markets could be adversely impacted. Any significant disruption to our natural gas supply could result in a substantial reduction in our revenues under our long-term SPAs or other customer arrangements, which could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

We may not be able to purchase or receive physical delivery of sufficient natural gas to satisfy our delivery obligations under the SPAs, which could have a material adverse effect on us.

Under the SPAs with our customers, we are required to make available to them a specified amount of LNG at specified times. However, we may not be able to purchase or receive physical delivery of sufficient quantities of natural gas to satisfy those obligations, which may provide affected SPA customers with the right to terminate their SPAs. Our failure to purchase or receive physical delivery of sufficient quantities of natural gas could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

We are subject to significant construction and operating hazards and uninsured risks, one or more of which may create significant liabilities and losses for us.

The construction and operation of the Corpus Christi LNG terminal and the operation of the Corpus Christi Pipeline are, and will be, subject to the inherent risks associated with these types of operations, including explosions, breakdowns or failures of equipment, operational errors by vessel or tug operators, pollution, release of toxic substances, fires, hurricanes and adverse weather conditions and other hazards, each of which could result in significant delays in commencement or interruptions of operations and/or in damage to or destruction of our facilities or damage to persons and property. In addition, our operations and the facilities and vessels of third parties on which our operations are dependent face possible risks associated with acts of aggression or terrorism.

19

We do not, nor do we intend to, maintain insurance against all of these risks and losses. We may not be able to maintain desired or required insurance in the future at rates that we consider reasonable. The occurrence of a significant event not fully insured or indemnified against could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

Cyclical or other changes in the demand for and price of LNG and natural gas may adversely affect our LNG business and the performance of our customers and could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

Our LNG business and the development of domestic LNG facilities and projects generally is based on assumptions about the future availability and price of natural gas and LNG and the prospects for international natural gas and LNG markets. Natural gas and LNG prices have been, and are likely to continue to be, volatile and subject to wide fluctuations in response to one or more of the following factors:

| • | competitive liquefaction capacity in North America; |

| • | insufficient or oversupply of natural gas liquefaction or receiving capacity worldwide; |

| • | insufficient LNG tanker capacity; |

| • | weather conditions, including temperature volatility resulting from climate change, and extreme weather events may lead to unexpected distortion in the balance of international LNG supply and demand. For example, LNG procurement in Japan rose dramatically in 2011 and several years thereafter following a tsunami that caused extensive destruction to its nuclear power infrastructure; |

| • | reduced demand and lower prices for natural gas; |

| • | increased natural gas production deliverable by pipelines, which could suppress demand for LNG; |

| • | decreased oil and natural gas exploration activities which may decrease the production of natural gas, including as a result of any potential ban on production of natural gas through hydraulic fracturing; |

| • | cost improvements that allow competitors to offer LNG regasification services or provide natural gas liquefaction capabilities at reduced prices; |

| • | changes in supplies of, and prices for, alternative energy sources such as coal, oil, nuclear, hydroelectric, wind and solar energy, which may reduce the demand for natural gas; |

| • | changes in regulatory, tax or other governmental policies regarding imported or exported LNG, natural gas or alternative energy sources, which may reduce the demand for imported or exported LNG and/or natural gas; |

| • | political conditions in natural gas producing regions; |

| • | sudden decreases in demand for LNG as a result of natural disasters or public health crises, including the occurrence of a pandemic, and other catastrophic events; |

| • | adverse relative demand for LNG compared to other markets, which may decrease LNG imports into or exports from North America; and |

| • | cyclical trends in general business and economic conditions that cause changes in the demand for natural gas. |

Adverse trends or developments affecting any of these factors could result in decreases in the price of LNG and/or natural gas, which could materially and adversely affect the performance of our customers, and could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

20

Failure of exported LNG to be a competitive source of energy for international markets could adversely affect our customers and could materially and adversely affect our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

Operations of the Liquefaction Project are dependent upon the ability of our SPA customers to deliver LNG supplies from the United States, which is primarily dependent upon LNG being a competitive source of energy internationally. The success of our business plan is dependent, in part, on the extent to which LNG can, for significant periods and in significant volumes, be supplied from North America and delivered to international markets at a lower cost than the cost of alternative energy sources. Through the use of improved exploration technologies, additional sources of natural gas may be discovered outside the United States, which could increase the available supply of natural gas outside the United States and could result in natural gas in those markets being available at a lower cost than LNG exported to those markets.

Political instability in foreign countries that import or export natural gas, or strained relations between such countries and the United States, may also impede the willingness or ability of LNG purchasers or suppliers and merchants in such countries to import or export LNG from or to the United States. Furthermore, some foreign purchasers or suppliers of LNG may have economic or other reasons to obtain their LNG from, or direct their LNG to,

non-U.S.

markets or from or to our competitors’ liquefaction or regasification facilities in the United States. In addition to natural gas, LNG also competes with other sources of energy, including coal, oil, nuclear, hydroelectric, wind and solar energy. LNG from the Liquefaction Project also competes with other sources of LNG, including LNG that is priced to indices other than Henry Hub. Some of these sources of energy may be available at a lower cost than LNG from the Liquefaction Project in certain markets. The cost of LNG supplies from the United States, including the Liquefaction Project, may also be impacted by an increase in natural gas prices in the United States.

As a result of these and other factors, LNG may not be a competitive source of energy in the United States or internationally. The failure of LNG to be a competitive supply alternative to local natural gas, oil and other alternative energy sources in markets accessible to our customers could adversely affect the ability of our customers to deliver LNG from the United States or to the United States on a commercial basis. Any significant impediment to the ability to deliver LNG to or from the United States generally, or to the Corpus Christi LNG terminal or from the Liquefaction Project specifically, could have a material adverse effect on our customers and on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects.

We face competition based upon the international market price for LNG.

Our Liquefaction Project is subject to the risk of LNG price competition at times when we need to replace any existing SPA, whether due to natural expiration, default or otherwise, or enter into new SPAs. Factors relating to competition may prevent us from entering into a new or replacement SPA on economically comparable terms as existing SPAs, or at all. Such an event could have a material adverse effect on our business, contracts, financial condition, operating results, cash flow, liquidity and prospects. Factors which may negatively affect potential demand for LNG from our Liquefaction Project are diverse and include, among others:

| • | increases in worldwide LNG production capacity and availability of LNG for market supply; |

| • | increases in demand for LNG but at levels below those required to maintain current price equilibrium with respect to supply; |

| • | increases in the cost to supply natural gas feedstock to our Liquefaction Project; |

| • | decreases in the cost of competing sources of natural gas or alternate fuels such as coal, heavy fuel oil and diesel; |

| • | decreases in the price of non-U.S. LNG, including decreases in price as a result of contracts indexed to lower oil prices; |

21

| • | increases in capacity and utilization of nuclear power and related facilities; and |

| • | displacement of LNG by pipeline natural gas or alternate fuels in locations where access to these energy sources is not currently available. |

A cyber attack involving our business, operational control systems or related infrastructure, or that of third party pipelines which supply the Liquefaction Facilities, could negatively impact our operations, result in data security breaches, impede the processing of transactions or delay financial or compliance reporting. These impacts could materially and adversely affect our business, contracts financial condition, operating results, cash flow and liquidity.

The pipeline and LNG industries are increasingly dependent on business and operational control technologies to conduct daily operations. We rely on control systems, technologies and networks to run our business and to control and manage our pipeline, liquefaction and shipping operations. Cyber attacks on businesses have escalated in recent years, including as a result of geopolitical tensions, and use of the internet, cloud services, mobile communication systems and other public networks exposes our business and that of other third-parties with whom we do business to potential cyber attacks, including third party pipelines which supply natural gas to our Liquefaction Facilities. For example, in 2021 Colonial Pipeline suffered a ransomware attack that led to the complete shutdown of its pipeline system for six days. Should multiple of the third party pipelines which supply our Liquefaction Facilities suffer similar concurrent attacks, the Liquefaction Facilities may not be able to obtain sufficient natural gas to operate at full capacity, or at all. A cyber attack involving our business or operational control, systems or related infrastructure, or that of third party pipelines with which we do business, could negatively impact our operations, result in data security breaches, impede the processing of transactions or delay financial or compliance reporting. These impacts could materially and adversely affect our business, contracts, financial condition, operating results, cash flow and liquidity.

Outbreaks of infectious diseases, such as the outbreak of

COVID-19,

at our facilities could adversely affect our operations. Our facilities at the Corpus Christi LNG terminal are critical infrastructure and have continued to operate during the

COVID-19

pandemic through our implementation of workplace controls and pandemic risk reduction measures. While the COVID-19

pandemic, including the Delta and Omicron variants, has had no adverse impact on our on-going

operations during this time, the risk of future variants is unknown. While we believe we can continue to mitigate any significant adverse impact to our employees and operations at our critical facilities related to the virus in its current form, the outbreak of a more potent variant in the future at one or more of our facilities could adversely affect our operations. We are entirely dependent on Cheniere, including employees of Cheniere and its subsidiaries, for key personnel, and the unavailability of skilled workers or our failure to attract and retain qualified personnel could adversely affect us. In addition, changes in our senior management or other key personnel could affect our business results.