|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended |

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to |

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report |

Commission file number:

(Exact name of Registrant as specified in its charter)

Nu Holdings Ltd.

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

Grand Cayman,

+

(Address of principal executive offices)

Tel: +

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Copies to:

Manuel Garciadiaz | Byron B. Rooney

Davis Polk & Wardwell LLP

450 Lexington Avenue | New York, NY 10017

Phone: (212) 450-4000 Fax: (212) 701-5800

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

The number of outstanding shares as of December 31, 2021 was Class A ordinary shares (including Class A ordinary shares underlying the BDRs), and Class B ordinary shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ☐

Accelerated Filer ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this annual report:

U.S. GAAP ☐ International

Financial Reporting Standards as issued by Other ☐

☒

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

| ☐ | Item 18 ☐ |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

☐

Table of Contents

| |

Presentation of Financial and Other Information

All references to “U.S. dollars,” “dollars,” or “US$” are to the U.S. dollar. All references to “IFRS” are to International Financial Reporting Standards, as issued by the IASB.

Financial Statements

Nu Holdings Ltd., or “Nu,” was incorporated in the Cayman Islands on February 26, 2016 as an exempted company incorporated with limited liability.

We maintain our books and records in U.S. dollars, which is the presentation currency for our financial statements and also our functional currency. The functional currency of our Brazilian, Mexican and Colombian operating entities, respectively, is the Brazilian real, the Mexican peso and the Colombian peso. The financial statements of each of our subsidiaries are maintained using the relevant functional currency for such subsidiary, which we determine is the currency that best reflects the economic substance of the underlying events and circumstances relevant to that entity. See note 2.a to our audited consolidated financial statements, included elsewhere in this annual report, for more information about our and our subsidiaries’ functional currencies.

Form 20-F | 2021 | 1 |

| |

Our consolidated financial statements were prepared in accordance with IFRS. Unless otherwise noted, our consolidated statement of financial position data presented herein as of December 31, 2021, 2020 and 2019 and the consolidated statements of profit or loss for the years ended December 31, 2021, 2020, and 2019 is stated in U.S. dollars, our reporting currency. Our consolidated financial information contained in this annual report is derived from our audited consolidated financial statements as of December 31, 2021 and 2020 and for the years ended December 31, 2021, 2020 and 2019, together with the notes thereto. Any financial information contained in this annual report comparing growth in the year ended December 31, 2019 against the prior period has been prepared based on accounting records for the year ended December 31, 2018, which was prepared in accordance with IFRS.

This financial information should be read in conjunction with “Item 5—Operating and Financial Review and Prospects” and our consolidated financial statements, including the notes thereto, included elsewhere in this annual report.

Our fiscal year ends on December 31. References in this annual report to a fiscal year, such as “fiscal year 2021,” relate to our fiscal year ended on December 31 of that calendar year.

Special Note Regarding Non-IFRS Financial Measures

This annual report presents our Adjusted Net Income (Loss) and certain FX Neutral measures and their respective reconciliations for the convenience of investors, which are non-IFRS financial measures. A non-IFRS financial measure is generally defined as a numerical measure of historical or future financial performance, financial position, or cash flow that purports to measure financial performance but excludes or includes amounts that would not be so adjusted in the most comparable IFRS measure. Adjusted Net Income (Loss) and the FX Neutral measures, however, should be considered in addition to, and not as a substitute for or superior to, profit (loss), or other measures of the financial performance prepared in accordance with IFRS.

Adjusted Net Income (Loss)

Adjusted Net Income (Loss) is prepared and presented to eliminate the effect of items from profit (loss) attributable to shareholders of the parent company that we do not consider indicative of our core operating performance within the period presented. We define Adjusted Net Income (Loss) as profit (loss) attributable to shareholders of the parent company, adjusted for expenses related to share-based compensation, allocated tax effects on share-based compensation, finance costs related to results with convertible instruments, as well as expenses (revenue deduction) and allocated tax effects related to the Initial Public Offering (IPO)-related customer program (NuSócios).

Adjusted Net Income (Loss) is presented because our management believes that this non-IFRS financial measure can provide useful information to investors, securities analysts and the public in their review of our operating and financial performance, although it is not calculated in accordance with IFRS or any other generally accepted accounting principles and should not be considered as a measure of performance in isolation. We also use Adjusted Net Income (Loss) as a key profitability measure to assess the performance of our business. We believe that Adjusted Net Income (Loss) is useful to evaluate our operating and financial performance for the following reasons:

Form 20-F | 2021 | 2 |

| |

| · | Adjusted Net Income (Loss) is widely used by investors and securities analysts to measure a company’s operating performance without regard to items that can vary substantially from company to company and from period to period, depending on their accounting and tax methods, the book value and the market value of their assets and liabilities, and the method by which their assets were acquired; |

| · | Non-cash equity grants made to executives, employees or consultants at a certain price and point in time, and their income tax effects, do not necessarily reflect how our business is performing at any particular time and the related expenses are not key measures of our core operating performance; |

| · | Expenses related to the customer program (NuSócios), and their income tax effects, do not necessarily reflect how our business is performing at any particular time as they were related to a specific marketing effort event we carried out in connection with our IPO are not key measures of our core operating performance; and |

| · | Finance costs with convertible instruments include fair value adjustments relating to the embedded derivative conversion feature, which are based upon subjective assumptions and do not reflect the cash cost of our convertible debt, and do not directly reflect how our business is performing at any particular time. The related expense adjustment amounts are not key measures of our core operating performance. |

Adjusted Net Income (Loss) is not a substitute for profit (loss) attributable to shareholders of the parent company, which is the IFRS measure of earnings. Additionally, our calculation of Adjusted Net Income (Loss) may be different from the calculation used by other companies, including our competitors in the technology and financial services industries, because other companies may not calculate these measures in the same manner as we do, and therefore, our measure may not be comparable to those of other companies. A reconciliation of our Adjusted Net Income (Loss) to its most directly comparable measure of income (loss) can be found in “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Non-IFRS Financial Measures and Reconciliations.”

FX Neutral Measures

FX Neutral measures are prepared and presented to eliminate the effect of foreign exchange, or “FX,” volatility between the comparison periods, allowing management and investors to evaluate our financial performance despite variations in foreign currency exchange rates, which may not be indicative of our core operating results and business outlook.

FX Neutral measures are presented because our management believes that these non-IFRS financial measures can provide useful information to investors, securities analysts and the public in their review of our operating and financial performance, although they are not calculated in accordance with IFRS or any other generally accepted accounting principles and should not be considered as a measure of performance in isolation.

The FX Neutral measures included in this annual report were calculated to present what such measures in preceding years would have been had exchange rates remained stable from these preceding years until the date of our most recent financial information, as detailed below.

The FX Neutral measures for the years ended December 31, 2020, 2019 and 2018 were calculated by multiplying the as reported amounts of Adjusted Net Income (Loss) and the key business metrics for such years by the average Brazilian reais/U.S. dollars exchange rates for the years ended December 31, 2020, 2019 and 2018 (R$5.240, R$3.952 and R$3.681, to US$1.00, respectively), and using such results to re-translate the corresponding amounts back to U.S. dollars by dividing them by the average Brazilian reais/U.S. dollars exchange rate for the year ended December 31, 2021 (R$5.415 to US$1.00), so as to present what certain of our statement of profit and loss amounts and key business metrics would have been had exchange rates remained stable from these past periods/years until the year ended December 31, 2021.

Form 20-F | 2021 | 3 |

| |

The average Brazilian reais/U.S. dollars exchange rates were calculated as the average of the month-end rates for each month in the years 2021, 2020, 2019 and 2018, as reported by Bloomberg.

FX Neutral measures for deposits and interest-earning portfolio presented in this annual report were calculated by multiplying the as reported amounts as of December 31, 2020, 2019 and 2018 by the spot Brazilian reais/U.S. dollars exchange rates as of these dates (R$5.199, R$4.030 and R$3.875 to US$1.00, respectively), and using such results to re-translate the corresponding amounts back to U.S. dollars by dividing them by using the spot rate as of December 31, 2021 (R$5.576 to US$1.00) so as to present what these amounts would have been had exchange rates been the same as those on December 31, 2021. The Brazilian reais/U.S. dollars exchange rates were calculated using rates as of such dates as reported by Bloomberg.

FX Neutral measures do not include adjustments for any other macroeconomic effect, such as local currency inflation effects, or any price adjustment to compensate for local currency inflation or devaluation. A reconciliation of our FX Neutral measures to the most directly comparable financial measure calculated and presented in accordance with IFRS can be found in “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Non-IFRS Financial Measures and Reconciliations.”

Special Note Regarding Certain Operational Metrics

Customers and Active Customers

This annual report presents information regarding our number of customers and our number of monthly active customers.

Number of customers information is prepared and presented as an important indicator of the size and momentum of our business, particularly as we continue to operate at a high growth pace. We define customers for a given measurement period as the individuals or SMEs that have previously or within such measurement period opened an account with us and we exclude any such individuals or SMEs that have been charged-off or blocked or have voluntarily closed their account. Number of customers is presented because it allows us to track our capacity to attract and retain customers and can provide useful information to investors, securities analysts and the public in their review of our operating performance.

Monthly active customer information is prepared and presented as an important indicator of the size and momentum of our business based on the number of customers we consider to be active. We define monthly active customers as all customers that have generated revenue in the last 30 calendar days, for a given measurement period. Monthly active customers information is presented because it allows us to track our capacity to attract and retain active customers and can provide useful information to investors, securities analysts and the public in their review of our operating performance.

Moreover, we differentiate between total number of customers (which includes customers we consider to be non-active) and active customers, to enable our management to evaluate performance metrics exclusively on the customers that we define as active. Doing so allows us to track performance based on revenue (defined as Monthly ARPAC) and cost (defined as Monthly Average Cost to Serve). For an explanation of how we calculate Monthly ARPAC and Monthly Average Cost to Serve per Active Customer please see the “Glossary of Terms” and “Item 5. Operating and Financial Review and Prospects—A. Operating Results.”

Form 20-F | 2021 | 4 |

| |

Information regarding both total number of customers and monthly active customers should be analyzed in conjunction with other operating and financial metrics, and should not be considered as a measure of performance in isolation. Additionally, our calculation of these measures may be different from the calculation used by other companies, including our competitors in the technology and financial services industries, because other companies may not calculate these measures in the same manner as we do, and therefore, our measures may not be comparable to those of other companies.

Market Share and Other Information

This annual report contains data related to economic conditions in the markets in which we operate. The information contained in this annual report concerning economic conditions is based on publicly available information from third-party sources that we believe to be reasonable. Market data and certain industry forecast data used in this annual report were obtained from internal reports and studies, where appropriate, as well as estimates, market research, publicly available information (including information available from the U.S. Securities and Exchange Commission website) and industry publications. We obtained the information included in this annual report relating to the industry in which we operate, as well as the estimates concerning market shares, through internal research, a report dated October 28, 2021 by management consulting company Oliver Wyman Consultoria em Estratégia de Negócios Ltda. commissioned by us, public information and publications on the industry prepared by official public sources, such as the national association of financial and capital markets entities (Associação Brasileira das Entidades dos Mercados Financeiro e de Capitais, or “ANBIMA”); the World Bank; the International Monetary Fund, or the “IMF;” the Organization for Economic Co-operation and Development, or “OECD;” the Central Bank of Brazil; the Colombian Central Bank; the Central Bank of Mexico; the Inter-American Development Bank; the Brazilian social and economic development bank (Banco Nacional de Desenvolvimento Econômico e Social, or “BNDES”); the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística, or the “IBGE”); the Institute of Applied Economic Research (Instituto de Pesquisa Econômica Aplicada, or “IPEA”), the Superintendence of Private Insurance (Superintendência de Seguros Privados, or “SUSEP”), the CVM; the Colombian National Administrative Department of Statistics (DANE – Departamento Administrativo Nacional de Estadística); the Mexican National Institute of Statistics and Geography (INEGI – Instituto Nacional de Estadística, Geografía e Informática); the Brazilian Micro and Small Business Support Service (Serviço Brasileiro de Apoio às Micro e Pequenas Empresas) or “SEBRAE;” the GSMA; and the Brazilian Association of Credit Card and Services Companies (Associação Brasileira de Empresas de Cartões de Crédito e Serviços), or “ABECS;” as well as private sources, such as B3, Bloomberg and Forbes, consulting and research companies in the Brazilian financial services industry, and Fundação Getulio Vargas, or “FGV,” among others. We estimate that we are one of the largest digital banking platforms in the world by comparing what we believe to be the largest (by number of customers) digital banking platforms around the world (according to public statements made by these platforms and data from an independent research firm) to the number of customers on our platform.

Industry publications generally state that the information they include has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Although we have no reason to believe any of this information or these reports are inaccurate in any material respect and believe and act as if they are reliable, we have not independently verified it. Governmental publications and other market sources, including those referred to above, generally state that their information was obtained from recognized and reliable sources, but the accuracy and completeness of that information is not guaranteed. In addition, the data that we compile internally and our estimates have not been verified by an independent source. Except as disclosed in this annual report, none of the publications, reports or other published industry sources referred to in this annual report were commissioned by us or prepared at our request. Except as disclosed in this annual report, we have not sought or obtained the consent of any of these sources to include such market data in this annual report.

Form 20-F | 2021 | 5 |

| |

Calculation of Net Promoter Score

Net promoter score, or “NPS,” is a widely known survey methodology that measures the willingness of customers to recommend a company’s products and services. It is used to gauge customers’ overall satisfaction with a company’s products and services and their loyalty to the brand, and it is typically based on customer surveys. NPS measures satisfaction using a scale of zero to 10 based on a customer’s response to the following question: “How likely is it that you would recommend Nu to a friend or colleague?” Responses of nine or 10 are considered “promoters.” Responses of seven or eight are considered neutral. Responses of six or less are considered “detractors.” The NPS, a percentage expressed as a numerical value, is calculated by subtracting the percentage of respondents who are detractors from the percentage who are promoters.

Rounding

We have made rounding adjustments to some of the figures included in this annual report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

Form 20-F | 2021 | 6 |

| |

Cautionary Statement Regarding Forward-Looking Statements

This annual report contains forward-looking statements within the meaning of the federal securities laws, which statements involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential,” or “continue,” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans, or intentions. Forward-looking statements contained in this annual report include statements about:

| · | general economic, financial, political, demographic and business conditions in Brazil, Mexico and Colombia, as well as any other countries we may serve in the future and their impact on our business; |

| · | fluctuations in interest, inflation and exchange rates in Brazil, Mexico and Colombia and any other countries we may serve in the future; |

| · | our ability to timely and efficiently implement any measures that are necessary to combat or reduce the impacts of the COVID-19 pandemic on our business, results of operations, cash flow, prospects, liquidity and financial condition; |

| · | competition in the consumer technology and financial services industry; |

| · | our ability to implement our business strategy; |

| · | our ability to adapt to the rapid pace of technological changes in the sectors in which we operate; |

| · | the reliability, performance, functionality and quality of our products and services, reliability and performance of our suitability, risk management and business continuity policies and processes; |

| · | the availability of government authorizations on terms and conditions and within periods acceptable to us; |

| · | our ability to continue attracting and retaining new appropriately-skilled employees; |

| · | our capitalization and level of indebtedness; |

| · | the interests of our founding shareholder; |

| · | our ability to manage our growth effectively; |

| · | our ability to successfully expand in Latin America and other new markets; |

| · | changes in government regulations applicable to the financial services industry in Brazil, Mexico, Colombia and elsewhere; |

| · | our ability to compete and conduct our business in the future; |

| · | our ability to maintain, protect and enhance our brand and intellectual property; |

Form 20-F | 2021 | 7 |

| |

| · | the success of operating initiatives, including advertising and promotional efforts and new product, service and concept development by us and our competitors; |

| · | changes in consumer demands regarding the products and services we offer, and our ability to innovate to respond to such changes; |

| · | changes in labor, distribution and other operating costs; |

| · | our compliance with, and changes to, government laws, regulations and tax matters that currently apply to us; |

| · | the size of our addressable markets, market share and market trends; |

| · | other factors that may affect our financial condition, liquidity and results of operations; and |

| · | other risk factors discussed under “Item 3. Key Information—D. Risk Factors.” |

We caution you that the foregoing list may not contain all of the forward-looking statements made in this annual report. You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this annual report primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties, and other factors, including those described in “Item 3. Key Information—D. Risk Factors” and elsewhere in this annual report. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this annual report. We cannot guarantee that the results, events, and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events, or circumstances could differ materially from those described in the forward-looking statements.

Neither we nor any other person assumes responsibility for the accuracy and completeness of any of these forward- looking statements. Moreover, the forward-looking statements made in this annual report relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this annual report to reflect events or circumstances after the date of this annual report or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward- looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this annual report, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

Form 20-F | 2021 | 8 |

| |

PART I

Item 1. Identity of Directors, Senior Management and Advisors

| A. | Directors and Senior Management |

Not applicable.

| B. | Advisers |

Not applicable.

| C. | Auditors |

Not applicable.

Item 2. Offer Statistics and Expected Timetable

| A. | Offer Statistics |

Not applicable.

| B. | Method and Expected Timetable |

Not applicable.

Item 3. Key Information

| A. | [Reserved] |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Risk Factors Summary

Investing in our Class A ordinary shares, including in the form of BDRs, involves risks. You should carefully consider the risks described below before making a decision to invest in our Class A ordinary shares or BDRs. If any of these risks actually materialize, our business, financial condition or results of operations would likely be materially adversely affected. In such case, the trading price of our Class A ordinary shares and BDRs would likely decline, and you could lose all or part of your investment. The following is a summary of some of the principal risks we face:

Risks Relating to Our Business and Industry

| · | Our business depends on a well-regarded and widely known brand, and any failure to maintain, protect and enhance our brand and image, including through effective marketing strategies, would harm our business, financial condition and results of operations. |

| · | Failure to successfully implement and improve our risk management policies, procedures and methods, including our credit risk management system, would materially and adversely affect our business, results of operations and financial condition. |

Form 20-F | 2021 | 9 |

| |

| · | Our international expansion efforts may not be successful, or may subject our business to increased risks. |

| · | Our business is highly dependent on the proper functioning of information technology systems, particularly at scale. |

| · | Any failure of these systems would disrupt our business and impair our ability to provide our services and products effectively to our customers. |

| · | We depend on data centers operated by third parties and third-party Internet hosting providers and cloud computing platforms, and any disruption in the operation of these facilities or platforms or access to the Internet would adversely affect our business. |

| · | We have incurred losses since our inception, and we may not achieve profitability. |

Risks Relating to Intellectual Property, Privacy and Cybersecurity

| · | Unauthorized disclosure of sensitive or confidential customer information or our failure or the perception by our customers that we failed to comply with privacy laws or properly address privacy concerns could harm our business and standing with our customers. |

| · | Unauthorized disclosure of, improper access to, or destruction or modification of data through cybersecurity breaches, computer viruses or otherwise, or disruptions to our systems or services, could expose us to liability, protracted and costly litigation and damage our reputation. |

| · | Claims by others that we infringe their proprietary technology or other rights could have a material and adverse effect on our business, financial condition and results of operations. |

Risks Relating to Regulatory Matters and Litigation

| · | We are subject to extensive regulation and regulatory and governmental oversight as a digital banking platform and as a payment institution. Compliance with or violation of present or future regulations could be costly, expose us to substantial liability and force us to change our business practices, any of which could harm our business and results of operations. |

| · | Certain ongoing legislative and regulatory initiatives under discussion by the Brazilian Congress, the Central Bank of Brazil and the broader payments industry may result in changes to the regulatory framework of the Brazilian payments and financial industries and may have an adverse effect on us. |

| · | We are subject to costs and risks associated with enhanced or changing laws and regulations affecting our business, including those relating to data privacy, security and protection. Developments in laws and regulations could harm our business, financial condition or results of operations. |

Risks Relating to the Countries in Which We Operate

| · | Exchange rate and interest rate instability may have a material adverse effect on the economies of the countries in which we operate and the price of our Class A ordinary shares and BDRs. |

| · | Disruption or volatility in global financial and credit markets could adversely affect the financial and economic environment in the countries in which we operate, most notably Brazil, Colombia and Mexico, which could have a material adverse effect on us. |

Form 20-F | 2021 | 10 |

| |

| · | Governments have exercised, and continue to exercise, significant influence over the Brazilian economy and the other economies in which we operate. This influence, as well as political and economic conditions in Brazil and the other countries in which we operate, could harm us and the price of our Class A ordinary shares and BDRs. |

Risks Relating to Our Class A Ordinary Shares and Our BDRs

| · | An active trading market for our Class A ordinary shares may not be sustainable. If an active trading market is not maintained, you may not be able to resell your shares at or above the price paid and you could lose a significant part of your investment. |

| · | Our founding shareholder and CEO David Vélez Osorno owns 86.2% of our outstanding Class B ordinary shares, which represents 74.9% of the voting power of our issued share capital. This concentration of ownership and voting power may limit your ability to influence corporate matters. |

| · | We have granted the holders of our Class B ordinary shares preemptive rights to acquire shares that we may sell in the future, which may impair our ability to raise funds. |

Risks Relating to Our Business and Industry

Our business depends on a well-regarded and widely known brand, and any failure to maintain, protect and enhance our brand and image, including through effective marketing strategies, would harm our business, financial condition and results of operations.

We believe our brand has contributed significantly to the historical success of our business. Maintaining, protecting and enhancing our brand is critical to expanding our customer base, our loan portfolio and our third-party partnerships, as well as increasing engagement with our products and services. Our success in this regard will depend largely on our ability to remain – or, in markets into which we expand, become – widely known, gain and maintain our customers’ trust, be a technology leader and provide reliable, high-quality and secure products and services that continue to meet the needs of our customers at competitive prices, as well as the effectiveness of our marketing efforts and our ability to differentiate our services and platform capabilities from competitors’ products and services.

We believe that maintaining and promoting our brand in a cost-effective manner is critical to achieving widespread acceptance of our products and services and to expand our customer base. Maintaining and promoting our brand will depend largely on our ability to continue to provide useful, reliable and innovative products and services, which we may not do successfully. Our brand promotion activities may not generate customer awareness or increase revenue, and even if they do, any increase in revenue may not offset the expenses we incur in promoting our brand. If we fail to successfully promote and maintain our brand or if we incur excessive expenses in this effort, we would lose significant market share and our business would be materially and adversely affected. Further, our success in the introduction and promotion of new products and services, as well as the promotion of existing products and services, may be partly dependent on our visibility on third-party advertising platforms. Changes in the way these platforms operate or changes in their advertising prices or other terms could make the introduction and promotion of our products and services and our brand more expensive or more difficult. If we are unable to market and promote our brand on third-party platforms effectively, our ability to acquire new customers would be materially harmed, which would adversely affect our business, financial condition and results of operations.

Form 20-F | 2021 | 11 |

| |

Failure to successfully implement and improve our risk management policies, procedures and methods, including our credit risk management system, would materially and adversely affect our business, results of operations and financial condition.

The management of risk is an integral part of our activities. We seek to monitor and manage our risk exposure through a variety of separate but complementary financial, credit, market, operational, compliance and legal policies, procedures and reporting systems, among others. We employ a broad and diversified set of risk monitoring and risk mitigation techniques, which may not be fully effective in mitigating our risk exposure in all economic market environments or against all types of risk, including risks that we may fail to identify or anticipate.

We use certain tools and metrics for managing market risk, including statistical models, which are based upon our use of observed historical market behavior. We apply statistical and other tools to these observations to quantify our market risk. However, in part because these tools and metrics are based on historical market behavior, and in part because the models do not take all market risks into account, they may fail to predict future market risks, including those that arise from factors we did not anticipate or correctly evaluate in our statistical models. This would limit our ability to effectively manage our market risk, which could result in our losses being significantly greater than predicted.

Because certain of our operating subsidiaries are financial or payments institutions, our business is also subject to inherent credit risk. An important feature of our credit risk management system is an internal credit score system that assesses the particular risk profile of a customer. As this process involves detailed analysis of a customer that takes into account both quantitative and qualitative factors, it is subject to error, and our internal risk models may not always be able to accurately predict the future credit risk of our customers or assign an accurate credit score, which may result in our exposure to higher credit risks than indicated by our risk management system. We also rely on certain publicly available customer credit information, information relating to credit agreements and other public sources to assess a customer’s creditworthiness. Due to limitations in the availability of information and the underdeveloped information infrastructure in the markets in which we operate, our assessment of credit risk associated with a particular customer may not be based on complete, accurate or reliable information. In addition, we cannot ensure that our credit scoring systems collect complete or accurate information reflecting the actual behavior of customers or that their credit risk can be assessed correctly. Without complete, accurate and reliable information, we have to rely on other publicly available resources and our internal resources, which may not be effective. As a result, our ability to effectively manage our credit risk and subsequently determine our credit loss allowances may be materially adversely affected.

Relatedly, we are exposed to counterparty risk, which may arise from, for example, investing in securities of third parties, entering into derivative contracts under which counterparties have obligations to make payments to us or executing securities, futures or currency trades from proprietary trading activities that fail to settle at the required time due to non-delivery by the counterparty or systems failure by clearing agents, clearing houses or other financial intermediaries. Many of the routine transactions we enter into expose us to significant risk in the event of default by one of our significant counterparties, although we do not currently face specific counterparty risk from concentration within our loan portfolio. If these risks give rise to losses, this could materially and adversely affect us. Separately, because we routinely transact with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks and other institutional customers, defaults by, and even rumors or questions about the solvency of, certain financial institutions and the financial services industry could lead to market-wide liquidity problems that could lead to substantial losses for our business.

We also face operational and foreign exchange risk. Although we have adopted policies and procedures to identify, monitor and manage our operational risk, these policies and procedures may not be fully effective. For a discussion of the risks we face with respect to foreign exchange rates, see “—Risks Relating to the Countries in Which We Operate—Exchange rate and interest rate instability may have a material adverse effect on the economies of the countries in which we operate and the price of our Class A ordinary shares and BDRs.”

Form 20-F | 2021 | 12 |

| |

If our policies and procedures are not fully effective or we are not successful in capturing all risks to which we are or may be exposed, we may suffer harm to our reputation or be subject to litigation or regulatory actions that could have a material adverse effect on our business, results of operations or financial condition. Further, if management were to rely on risk models – whether with respect to market, credit or operational risks – that were flawed or poorly developed, implemented or used, or if management were to misunderstand or use such information for purposes for which it was not designed, we may fail to adequately manage our risk. In addition, if existing or potential customers or counterparties believe our risk management is inadequate, they could take their business elsewhere or seek to limit their transactions with us. Further, certain of the models and other analytical and judgment-based estimations we use in managing risk are subject to review by, and require the approval of, our regulators. If our models do not comply with their expectations, our regulators may require us to make changes to such models, may approve them with additional capital requirements or we may be precluded from using them, any of which could limit our ability to operate our businesses.

Failure to effectively implement, consistently monitor or continuously refine our risk management systems may result in a material adverse effect on our reputation, operating results and financial condition.

Our international expansion efforts may not be successful, or may subject our business to increased risks.

We currently operate in Brazil, Mexico and Colombia, and we have information technology and support operations in Argentina, Germany, the United States and Uruguay. As part of our growth strategy, we may expand our operations by offering our products and services in additional regions, as well as additional countries in Latin America, where we have little or no experience, and by expanding our business in the jurisdictions in which we currently operate. We may not be successful in expanding our operations into these or other markets in a cost-effective or timely manner, if at all, and our products and services may not experience the same market adoption in such international jurisdictions as we have enjoyed in Brazil. In particular, the expansion of our business into new geographies (or the further expansion in geographies in which we currently operate) may depend on the local regulatory environment or require a close commercial relationship with one or more local banks or other intermediaries, which could prevent, delay or limit the introductions of our products and services in such countries. Local regulatory environments may vary widely in terms of scope and sophistication.

Further, our international expansion efforts have and will continue to place a significant strain on our personnel (including management), technical, operational and financial resources, and our current resources may not be adequate to support our planned geographical expansion. We also may not be able to recoup our investments in new geographies in a timely manner, if at all. If our expansion efforts are unsuccessful, including because potential customers in a given jurisdiction fail to adopt our products and services, our reputation and brand may be harmed, and our ability to grow our business and revenue may be adversely affected.

Even if our international expansion efforts are successful, international operations will subject our business to increased risks, including:

| · | increased licensing and regulatory requirements; |

Form 20-F | 2021 | 13 |

| |

| · | competition from service providers or other entrenched market participants that have greater experience in the local markets than we do; |

| · | increased costs associated with and difficulty in obtaining, maintaining, processing, transmitting, storing, handling and protecting intellectual property, proprietary rights and sensitive data; |

| · | changes to the way we do business as compared with our current operations; |

| · | a lack of acceptance of our products and services; |

| · | the ability to support and integrate with local third-party service providers; |

| · | difficulties in staffing and managing foreign operations in an environment of diverse culture, language, laws and customs; |

| · | difficulties in recruiting and retaining qualified employees and maintaining our company culture; |

| · | increased travel, infrastructure and legal and compliance costs; |

| · | compliance obligations under multiple, potentially conflicting and changing, legal and regulatory regimes, including those governing financial institutions, payments, data privacy, data protection, information security, anti-corruption, anti-bribery and anti-money laundering; |

| · | compliance with complex and potentially conflicting and changing tax regimes; |

| · | potential tariffs, sanctions, fines or other trade restrictions; |

| · | exchange rate exposure; |

| · | increased exposure to public health issues such as the COVID-19 pandemic, and related industry and governmental actions to address these issues; and |

| · | regional economic and political instability. |

As a result of these risks, our international expansion efforts may not be successful or may be hampered, which would limit our ability to grow our business.

Our business is highly dependent on the proper functioning of information technology systems, particularly at scale. Any failure of these systems would disrupt our business and impair our ability to provide our services and products effectively to our customers.

Our continued growth depends in part on the ability of our existing and potential customers to access our products and platform capabilities at any time and within an acceptable amount of time. Continued access to our products and platform capabilities depends on the efficient and uninterrupted operation of numerous systems, including our computer systems, software, data centers and telecommunications networks, as well as the systems of third parties, such as credit and debit card transaction authorization providers, national financial system network infrastructure providers, back office and business process support, information technology production and support, Internet and telephone connections, network access, data center infrastructure services and cloud storage and computing. However, these systems and technologies are vulnerable to disruptions, failures or slowdowns. We have experienced, and may in the future experience, disruptions, outages and other performance problems due to a variety of factors, including infrastructure changes, introductions of new functionality, human or software errors, capacity constraints due to an overwhelming number of customers accessing our products and platform capabilities simultaneously, denial of service attacks or other security-related incidents, natural disasters, power outages, terrorist attacks, hostilities, and other events beyond our control.

Form 20-F | 2021 | 14 |

| |

As our business grows, it may become increasingly difficult to maintain and improve the performance of our information technology systems, especially during peak usage times and as our products and platform capabilities become more complex and our customer traffic increases. To the extent that we do not effectively address capacity constraints, upgrade our systems as needed and continually develop our technology and network architecture to accommodate actual and anticipated changes in technology, our business, financial condition and results of operations may be adversely affected. Specifically, if our products and platform capabilities are unavailable or if our customers are unable to access our products and platform capabilities within a reasonable amount of time, we may experience a loss of customers, lost or delayed market acceptance of our platform and products, delays in payment to us by customers, injury to our reputation and brand, the diversion of our resources, additional operating and development costs, loss of revenue, legal claims against us, the loss of licenses, loss of Central Bank of Brazil authorizations or fines or other penalties imposed by the Central Bank of Brazil (including intervention, temporary special management systems, the imposition of insolvency proceedings or the out-of-court liquidation of our operating subsidiaries), or by the Brazilian National Data Protection Authority (Autoridade Nacional de Proteção de Dados, or the “ANPD”). In addition, we do not maintain insurance policies specifically for property and business interruptions, meaning we would directly and without setoff incur any losses we suffer as a result of the aforementioned occurrences. For further information, see “—Our insurance policies may not be sufficient to cover all claims.”

Our business is highly dependent on the ability of our information technology systems to accurately process a large number of highly complex transactions across numerous and diverse markets and products in a timely manner and at high processing speeds, and on our ability to rely on our digital technologies, computer and email services, software and networks, as well as on the secure processing, storage and transmission of confidential data and other information on our computer systems and networks. Specifically, the proper functioning of our financial control, risk management, accounting, customer service and other data processing systems is critical to our business and our ability to compete effectively. Any failure to deliver an effective and secure service, or any performance issue that arises with a service, could result in significant processing or reporting errors or other losses. See “—We depend on data centers operated by third parties and third-party Internet hosting providers and cloud computing platforms, and any disruption in the operation of these facilities or platforms or access to the Internet would adversely affect our business.”

We do not operate all of our systems on a real-time basis and cannot assure that our business activities would not be materially disrupted if there were a partial or complete failure of any of these primary information technology systems or communication networks. In particular, because all customer transactions on the Nu Plataforma occur on our mobile application, any failure of our mobile application would cause our platform and services to be unavailable to our customers. Such failures could be caused by, among other things, major natural catastrophes, software bugs, computer virus attacks, conversion errors due to system upgrading, security breaches caused by unauthorized access to information or systems or malfunctions, loss or corruption of data, software, hardware or other computer equipment. Any such failures would disrupt our business and impair our ability to provide our services and products effectively to our customers, which could adversely affect our reputation as well as our business, results of operations and financial condition.

Our ability to remain competitive and achieve further growth will depend in part on our ability to upgrade our information technology systems and increase our capacity on a timely and cost-effective basis. We must continually make significant investments and improvements in our information technology infrastructure in order to remain competitive. We cannot guarantee that in the future we will be able to maintain the level of capital expenditures necessary to support the improvement or upgrading of our information technology systems. Any substantial failure to improve or upgrade our information technology systems effectively or on a timely basis would materially and adversely affect our business, financial condition or results of operations.

Form 20-F | 2021 | 15 |

| |

We depend on data centers operated by third parties and third-party internet-hosting providers and cloud computing platforms, and any disruption in the operation of these facilities or platforms or access to the Internet would adversely affect our business.

Our business requires the ongoing availability and uninterrupted operation of internal and external transaction processing systems and services. We primarily serve our customers from third-party data center hosting facilities provided by a third-party service provider, which we rely on to operate certain aspects of our products and services, and we depend on third-party Internet-hosting providers and third-party bandwidth providers for continuous and uninterrupted access to the Internet to operate our business. Any disruption of or interference with our use of such services would impair our ability to deliver our products and services to our customers, resulting in customer dissatisfaction, damage to our reputation, loss of customers and harm to our business. Further, we have designed our products and services and computer systems to use data processing, storage capabilities and other services provided by such third-party service providers. As such, we cannot easily switch our operations to another cloud provider, so any disruption of or interference with our use of such providers’ services would increase our operating costs and could materially and adversely affect our business, financial condition and results of operations, and we might not be able to secure service from an alternative provider on similar terms or at all.

While we maintain oversight of our third-party data center hosting facilities and Internet-hosting providers, such third parties are ultimately responsible for maintaining their own network security, disaster recovery and system management procedures, and such third-parties do not guarantee that our customers’ access to our solutions will be uninterrupted, error-free or secure. These third-party providers may experience website disruptions, outages and other performance problems, which may be caused by a variety of factors, including infrastructure changes, human or software errors, viruses, security attacks, fraud, spikes in customer usage and denial of service issues. In some instances, we may not be able to identify the cause or causes of these performance problems within an acceptable period of time. In particular, we do not control the operation of the third-party data center hosting facilities, and such facilities are vulnerable to damage or interruption from human error, intentional bad acts, power loss, hardware failures, telecommunications failures, improper operation, unauthorized entry, data loss, power loss, cyberattacks, fires, wars, terrorist attacks, floods, earthquakes, hurricanes, tornadoes, natural disasters or similar catastrophic events. They also could be subject to break-ins, computer viruses, sabotage, intentional acts of vandalism and other misconduct. The occurrence of a natural disaster or an act of terrorism, a decision to close the facilities without adequate notice or terminate our hosting arrangement or other unanticipated problems could result in lengthy interruptions in the delivery of our solutions, cause system interruptions, prevent our customers from accessing their accounts online, reputational harm and loss of critical data, prevent us from supporting our solutions or cause us to incur additional expense in arranging for new facilities and support.

If we lose the services of one or more of our Internet-hosting or bandwidth providers for any reason or if their services are disrupted, for example due to viruses or denial of service or other attacks on their systems, or due to human error, intentional bad acts, power loss, hardware failures, telecommunications failures, fires, wars, terrorist attacks, floods, earthquakes, hurricanes, tornadoes or similar catastrophic events, we could experience disruption in our ability to offer our solutions and adverse perception of our solutions’ reliability, or we could be required to retain the services of replacement providers, which could increase our operating costs and materially and adversely affect our business, financial condition and results of operations.

Form 20-F | 2021 | 16 |

| |

Furthermore, prolonged interruption in the availability, or reduction in the speed or other functionality, of our products or services could materially harm our reputation and business. Frequent or persistent interruptions in our products and services could cause customers to believe that our products and services are unreliable, leading them to switch to our competitors or to avoid our products and services, and would likely permanently harm our reputation and business.

Any of the foregoing, in addition to any of the factors described in “—We are dependent on third-party service providers in our operations, any failure of a third-party service provider could disrupt our operations,” could have a material adverse effect on our business, financial condition and results of operations.

Negative publicity about us (including our directors or employees) or our industry could adversely affect our business, financial condition, results of operations and future prospects.

Negative publicity about us (including our directors or employees) or our industry, including the transparency, fairness, customer experience, quality and reliability of our products or services, effectiveness of our risk model, our ability to effectively manage and resolve complaints, our privacy and security practices, our ESG and diversity and inclusion practices, litigation, regulatory activity, misconduct by or statements made by our directors or employees, funding sources, service providers or others in our industry, could adversely affect our reputation and the confidence in, and the use of, our products and services. For example, in late 2020, we issued a public apology and reaffirmed our commitment to diversity after comments made by one of our co-founders received significant negative publicity. This and any future negative publicity could harm our reputation and cause disruptions to business. Any such reputational harm could further affect the behavior of customers and, as a result, materially and adversely affect our business, results of operations, financial condition and future prospects.

The credit quality of our loan portfolio may deteriorate and our ECL allowance could be insufficient to cover our losses, which would have a material adverse effect on our business, financial condition and results of operations.

Risks arising from changes in credit quality and the recoverability of amounts due from counterparties are inherent in many aspects of our businesses, in particular our customer credit card and lending businesses. We expect the amount of reported non-performing loans to increase in the future on an absolute basis as a result of the expected growth in our total loan portfolio, the credit quality of which may turn out to be worse than anticipated. The amount of reported non-performing loans may also increase due to factors beyond our control, such as adverse changes in the credit quality of our borrowers and counterparties or a general deterioration in economic conditions in the markets in which we operate.

Our provisions for credit losses are based on our current assessments and expectations concerning various factors affecting the quality of our loan portfolio. These factors include, among other things, our borrowers’ financial condition, government macroeconomic policies, interest rates and the legal and regulatory environment. As many of these factors are beyond our control and there is no infallible method for predicting loan and credit losses, we cannot guarantee that our current or future reserves for credit losses will be sufficient to cover actual losses. If our assessment of and expectations concerning the above-mentioned factors differ from actual developments, if the quality of our total loan portfolio deteriorates, for any reason, or if the future actual losses exceed our estimates of expected losses, we may be required to increase our provisions for credit losses, which may adversely affect our financial condition. As such, any unexpected increase in the level of our non-performing loans could have a material adverse effect on our financial condition.

Form 20-F | 2021 | 17 |

| |

We depend on key management, as well as our experienced and capable employees, and any failure to attract, motivate and retain our employees would harm our ability to maintain and grow our business.

Our business functions at the intersection of rapidly changing technological, social, economic and regulatory developments that require a wide-ranging set of expertise and intellectual capital. Our future success is significantly dependent upon the continued service of our executives and other key employees, and in particular our founding shareholder and chief executive officer David Vélez Osorno. If we lose the services of any member of management or any key employee, we may not be able to locate a suitable or qualified replacement, and we may incur additional expenses to recruit and train a replacement, which would severely disrupt our business and growth.

To maintain and grow our business, we will need to identify, attract, hire, develop, motivate and retain highly skilled employees, which requires significant time, expense and effort. Competition for highly skilled personnel is intense, in our industry in particular. We may need to invest significant amounts of cash and equity to attract and retain new employees, and we may never realize returns on these investments. In addition, from time to time, there may be changes in our management team that may be disruptive to our business. If our management team, including any new hires that we make, fail to work together effectively and to execute our plans and strategies on a timely basis, our business would be harmed.

Furthermore, our international expansion and our business in general may be materially adversely affected if legislative or administrative changes to immigration or visa laws and regulations impair our hiring processes or projects involving personnel who are not citizens of the country where their work is to be performed. If we are not able to add and retain employees effectively, our ability to achieve our strategic objectives will be adversely affected, and our business and growth prospects will be harmed.

Increases in our remuneration expenses for our management that will be recognized in our future results will have an adverse effect on our accounting results

Our operations and strategies depend on the attraction and retention of qualified personnel with different levels of expertise, and as such, we offer competitive remuneration structures. As discussed in “Item 6. Directors, Senior Management and Employees—B. Compensation—Executive Compensation—Contingent Share Awards,” the cost of remuneration for our managers increased in the year ended 2021 compared to the year ended 2020 given the 2021 Contingent Share Awards and we expect that the cost of remuneration for our managers will continue to increase in the next few years. Total expenses for the 2021 Contingent Share Awards was determined to be US$422.6 million and the expenses will be recognized over a period of 7.5 years since its issuance. The recognition of these additional expenses as management remuneration will have an adverse effect on our results of operations.

If we fail to manage our growth effectively, our business would be harmed.

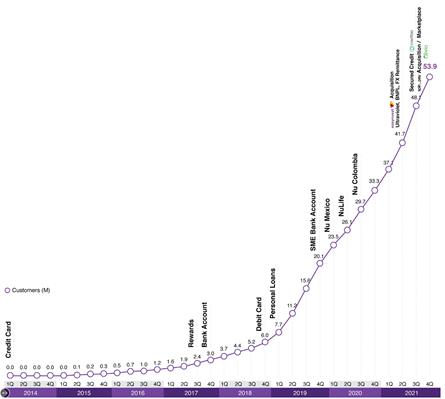

We have experienced and expect in the near term to continue to experience rapid growth. For instance, our total revenue increased by 130.4%, reaching US$1,698 million in 2021 from US$737.1 million in 2020. On a FX Neutral basis, our total revenue increased by 138.0%, reaching US$1,698 million in 2021 from US$713.3 million in 2020. See “Presentation of Financial and Other Information—Special Note Regarding Non-IFRS Financial Measures—FX Neutral Measures.” The number of our full-time employees increased by 107%, reaching 6,068 on December 31, 2021 compared to 2,929 as on December 31, 2020. Our growth has placed and will continue to place significant demands on our administrative, operational and financial resources. Our ability to effectively manage our growth will depend on a number of factors, including our ability to:

| · | expand our sales and marketing, technology, finance and administration teams; |

Form 20-F | 2021 | 18 |

| |

| · | grow our facilities and infrastructure; |

| · | adapt and scale our information technology systems; |

| · | refine our operational, financial and risk management controls and reporting systems and procedures; |

| · | recruit, integrate, train and retain a growing employee base and maintain our corporate culture; |

| · | maintain and grow our customer base and provide quality customer service; and |

| · | obtain, maintain, protect and develop our strategic assets, including our intellectual property and other proprietary rights. |

Executing on these factors will require significant capital expenditures and the allocation of valuable management and employee resources. We may be unable to effectively manage any future growth in an efficient, cost-effective or timely manner, or at all. Any failure to successfully implement systems enhancements and improvements will likely negatively impact our ability to manage our expected growth, ensure uninterrupted operation of key business systems and comply with the rules and regulations that are applicable to public reporting companies. Moreover, if we do not effectively manage the growth of our business and operations, the quality of our platform would suffer, which would negatively affect our reputation, results of operations and overall business. Furthermore, we encourage employees to quickly develop and launch new features for our products and services; as we grow, we may not be able to execute as quickly as smaller, more efficient organizations.

A decline in the use of credit or prepaid cards as a payment mechanism for consumers or adverse developments with respect to the payment processing industry in general would have a materially adverse effect on our business, financial condition and results of operations.

If consumers do not continue to use credit or prepaid cards as a payment mechanism for their transactions or if there is a change in the mix of payments between cash, credit, and prepaid cards and other means of payment, including real-time payments, that is adverse to us, it would have a material adverse effect on our business, financial condition and results of operations. We believe future growth in the use of credit, prepaid cards and other means of payment will be driven by the cost, ease-of-use and quality of services offered to consumers and businesses. In order to consistently increase and maintain our profitability, consumers and businesses must continue to use electronic payment methods including credit, debit and prepaid cards and real-time payment methods, such as PIX. Moreover, if there is an adverse development in the payments industry or Brazilian market in general, such as new legislation or regulation that makes it more difficult for our customers to do business or utilize such payment mechanisms, our business, financial condition and results of operations may be adversely affected.

We have historically derived a substantial portion of our revenue from our credit card business, and losses or a significant reduction in our credit card business, or our failure to successfully expand and diversify our revenue sources beyond our credit card business, would adversely affect our business, financial condition and results of operations.

The commercial success of our consumer technology platform has depended and may continue to depend in part on the success of our credit card business. We have historically derived a significant portion of our revenue from (i) the interchange fees we collect when a customer uses a Nu credit card to make a purchase and (ii) the interest rates we receive from the financing or revolving of Nu credit card balance by our customers. In the year ended December 31, 2021, interchange fees and interest related to credit cards accounted for 27.8% and 22.1% of our revenue, respectively (34.5% and 29.5% in the year ended December 31, 2020). While we expect our revenue concentration to decline in the future as we expand our suite of products and services, our efforts to diversify our revenue sources, such as new products and regional diversification, may not be successful and our reliance on credit card-related revenue may increase. Further, our revenue would be significantly harmed if we were to lose all or a substantial portion of our credit card business, whether due to loss of customers, regulatory or legislative developments or otherwise. In particular, our revenue would be harmed if the interchange fees that we collect or the interest rates that we charge become capped by regulators (or, in markets in which regulatory caps already exist, if such caps were reduced). Please see “—Risks Relating to Regulatory Matters and Litigation—Certain ongoing legislative and regulatory initiatives under discussion by the Brazilian Congress, the Central Bank of Brazil and the broader payments industry may result in changes to the regulatory framework of the Brazilian payments and financial industries, which may have an adverse effect on our business and cause us to incur increased compliance costs.”

Form 20-F | 2021 | 19 |

| |

Further, on July 2, 2021, Brazilian Law No. 14,181, or the “Super Indebtedness Law,” created a chapter in the Brazilian Consumer Protection Code dedicated to responsible credit and financial education, with new provisions that require specific information to be provided to the consumer when granting credit or in installment sales, such as the effective monthly interest rate, interest on arrears and late payment charges. This new set of rules may contribute to driving customers and potential customers away from our credit card product, which could adversely impact our business, financial condition and results of operations. For more information, see “—A decline in the use of credit or prepaid cards as a payment mechanism for consumers or adverse developments with respect to the payment processing industry in general would have a materially adverse effect on our business, financial condition and results of operations.”

If we are unable to attract new and retain existing customers, our business, financial condition and results of operations will be adversely affected.

We believe that our customer base is the cornerstone of our business. The growth of our business depends on existing customers expanding their use of our products and services and on our ability to attract new customers, including customers who may be reluctant to seek alternatives to incumbent financial institutions, by offering new products and services. If we are unable to attract new customers to our platform or encourage customers to broaden their use of our products and services, our growth may slow or stop, and our business may be materially and adversely affected.

Our ability to maintain and expand our customer base depends on a number of factors, including our ability to provide relevant and timely products and services to meet their changing needs at a reasonable cost. We have invested and will continue to invest in improving our platform and our suite of products and services. For example, we recently acquired NuInvest, our broker-dealer subsidiary, and have announced plans to expand our insurance broker activities. However, if new or improved features, products and services fail to meet shifting customer demands and fail to attract new customers or encourage existing customers to expand their engagement with our products and services, our growth may slow or decline. Further, these and other new products and services must achieve high levels of market acceptance before we are able to recoup our up-front investment costs, which may never occur if such products and services fail to attract new and retain existing customers.

Our existing and new products and services, including our payments, investments, insurance and credit solutions, could fail to attract new and retain existing customers for many reasons, including:

| · | we may fail to predict market demand accurately and provide products and services that meet this demand in a timely fashion; |

| · | customers may not like, find useful or agree with any changes we make to our products or services; |

Form 20-F | 2021 | 20 |

| |

| · | the reliability, performance or functionality of our products and services could be compromised or the quality of our products and services could decline; |

| · | we may fail to provide sufficient customer support; |

| · | customers may dislike our pricing, in particular in comparison to the pricing of competing products and services; |

| · | competing products and services may be introduced or anticipated to be introduced by our competitors; and |

| · | there may be negative publicity about our products and services or our platform’s performance or effectiveness, including negative publicity on social media platforms. |

Further, our customers have no obligation to continue to use our products and services, and we can make no assurances that our customers will continue to do so. We generally do not have long-term contracts with our customers; customer deposits and investments may be withdrawn without notice, and the consumer credit solutions we offer may be prepaid and canceled at any time. Further, recent changes in regulations have increasingly enabled customers to more easily switch to our competitors.

Any one or a combination of these factors could lead to customer attrition, and in particular at rates that are higher than we expect, which would adversely affect our business, financial condition and results of operations.

If we cannot keep pace with rapid technological developments to provide new and innovative products and services, the use of our products and services and, consequently, our revenue could decline or our revenue growth rate could slow.

Rapid, significant and disruptive technological changes have impacted or may in the future impact the industries in which we operate, including changes in:

| · | artificial intelligence and machine learning (e.g., in relation to fraud and risk assessment); |

| · | payment technologies (e.g., real-time payments, payment card tokenization, virtual and crypto currencies, including distributed ledger and blockchain technologies, and proximity payment technology, such as near-field communication and other contactless payments); |

| · | mobile and internet technologies (e.g., mobile phone app technology); |

| · | commerce technologies, including for use in-store, online and via mobile, virtual, augmented or social-media channels; and |

| · | digital banking features (e.g., balance and fraud monitoring and notifications). |