UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2022

OR

for the transition period from to

Commission file number: 001-39367

(Exact name of Registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

(Address of principal executive offices) (Zip Code)

(844 ) 733-8666

(Registrant’s telephone number including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☑ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☑ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☑ No

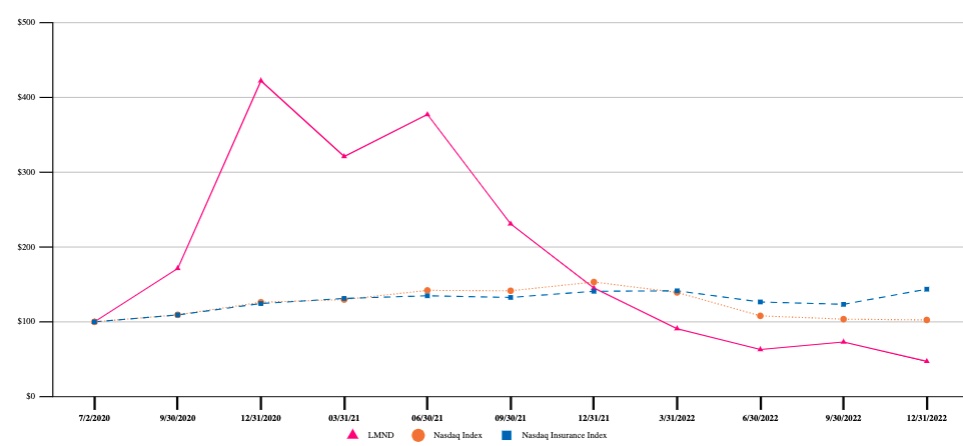

The aggregate market value of the common stock held by non-affiliates of the registrant, based on the closing sales price of $18.26 on June 30, 2022, was approximately $753,587,881 .

Registrant had 69,301,430 shares of common stock outstanding as of March 3, 2023.

DOCUMENTS INCORPORATED BY REFERENCE

| Page | ||||||||

| Part I | ||||||||

| Item 1 | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Part II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Part III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Part IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

1

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Annual Report”) contains forward-looking statements. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements other than statements of historical fact contained in this Annual Report are forward-looking statements, including without limitation, statements regarding our future results of operations and financial position, our ability to attract, retain and expand our customer base, our ability to operate under and maintain our business model, our ability to maintain and enhance our brand and reputation, our ability to effectively manage the growth of our business, the effects of seasonal trends on our results of operations, our ability to attain greater value from each customer, our ability to compete effectively in our industry, the future performance of the markets in which we operate, our ability to maintain reinsurance contracts, the anticipated benefits of the Metromile acquisition and the plans and objectives of management for future operations and capital expenditures. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential”, or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Annual Report are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of important factors that could cause actual results to differ materially from those in the forward-looking statements, including the factors described under the sections in this Annual Report titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

You should read this Annual Report and the documents that we reference in this Annual Report completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

In this Annual Report, unless we indicate otherwise or the context otherwise requires, "Lemonade," the “Company," "we," "our," "ours" and "us" refer to Lemonade, Inc. and its consolidated subsidiaries, including Lemonade Insurance Company, Lemonade Insurance Agency, LLC, and Metromile, Inc.

2

SUMMARY RISK FACTORS

Our business is subject to numerous risks and uncertainties, including those described in Part I Item 1A. “Risk Factors” in this Annual Report. You should carefully consider these risks and uncertainties, together with all of the other information contained in this Annual Report, when investing in our common stock. The principal risks and uncertainties affecting our business include the following:

•We have a history of losses and we may not achieve or maintain profitability in the future.

•Our success and ability to grow our business depend on retaining and expanding our customer base. If we fail to add new customers or retain current customers, our business, revenue, operating results and financial condition could be harmed.

•The "Lemonade" brand may not become as widely known as incumbents' brands or the brand may become tarnished.

•Denial of claims or our failure to accurately and timely pay claims could materially and adversely affect our business, financial condition, results of operations, and prospects.

•Our future revenue growth and prospects depend on attaining greater value from each user.

•The novelty of our business model makes its efficacy unpredictable and susceptible to unintended consequences.

•We could be forced to modify or eliminate our Giveback, which could undermine our business model and have a material adverse effect on our results of operations and financial condition.

•Our limited operating history makes it difficult to evaluate our current business performance, implementation of our business model, and our future prospects.

•We may not be able to manage our growth effectively.

•Intense competition in the segments of the insurance industry in which we operate could negatively affect our ability to attain or increase profitability.

•Reinsurance may be unavailable at current levels and prices, which may limit our ability to write new business. Furthermore, reinsurance subjects us to counterparty risk and may not be adequate to protect us against losses.

•Failure to maintain our risk-based capital at the required levels could adversely affect the ability of our insurance subsidiaries to maintain regulatory authority to conduct our business.

•If we are unable to expand our product offerings, our prospects for future growth may be adversely affected.

•Our proprietary artificial intelligence algorithms may not operate properly or as we expect them to, which could cause us to write policies we should not write, price those policies inappropriately or overpay claims that are made by our customers. Moreover, our proprietary artificial intelligence algorithms may lead to unintentional bias and discrimination.

•Regulators may limit our ability to develop or implement our proprietary artificial intelligence algorithms and/or may eliminate or restrict the confidentiality of our proprietary technology.

•New legislation or legal requirements may affect how we communicate with our customers, which could have a material adverse effect on our business model, financial condition, and results of operations.

•We rely on artificial intelligence and our digital platform to collect data points that we evaluate in pricing and underwriting our insurance policies, managing claims and customer support, and improving business processes, and any legal or regulatory requirements that restrict our ability to collect this data could thus materially and adversely affect our business, financial condition, results of operations and prospects.

•We may require additional capital to grow our business, which may not be available on terms acceptable to us or at all.

•Security incidents or real or perceived errors, failures or bugs in our systems, website or app could impair our operations, result in loss of personal customer information, damage our reputation and brand, and harm our business and operating results.

•We are periodically subject to examinations by our primary state insurance regulator, and insurance regulators of other states in which we are licensed to operate, which could result in adverse examination findings and necessitate remedial actions. We collect, process, store, share, disclose and use customer information and other data, and our actual or perceived failure to protect such information and data, respect customers' privacy or comply with data privacy and security laws and regulations could damage our reputation and brand and harm our business and operating results.

3

•If we are unable to underwrite risks accurately and charge competitive yet profitable rates to our customers, our business, results of operations and financial condition will be adversely affected.

•Our product development cycles are complex and subject to regulatory approval, and we may incur significant expenses before we generate revenues, if any, from new products.

•Our expansion within the United States and any future international expansion strategy will subject us to additional costs and risks and our plans may not be successful.

•The insurance business, including the market for renters and homeowners insurance, is historically cyclical in nature, and we may experience periods with excess underwriting capacity and unfavorable premium rates, which could adversely affect our business.

•We are subject to extensive insurance industry regulations.

•State insurance regulators impose additional reporting requirements regarding enterprise risk on insurance holding company systems, with which we must comply as an insurance holding company.

•Severe weather events and other catastrophes, including the effects of climate change and global pandemics, are inherently unpredictable and may have a material adverse effect on our financial results and financial condition.

•Climate risks, including risks associated with disruptions due to any transition to a low-carbon economy, could adversely affect our business, results of operations and financial condition.

•Increasing scrutiny, actions, and changing expectations from investors, customers, regulators and our employees with respect to environmental, social and governance (“ESG”) matters may impose additional costs on us, impact our access to capital, or expose us to new or additional risks.

•We expect our results of operations to fluctuate on a quarterly and annual basis. In addition, our operating results and operating metrics are subject to seasonality and volatility, which could result in fluctuations in our quarterly revenues and operating results or in perceptions of our business prospects.

•We rely on data from our customers and third parties for pricing and underwriting our insurance policies, handling claims and maximizing automation, the unavailability or inaccuracy of which could limit the functionality of our products and disrupt our business.

•Our results of operations and financial condition may be adversely affected due to limitations in the analytical models used to assess and predict our exposure to catastrophe losses.

•Our actual incurred losses may be greater than our loss and loss adjustment expense reserves, which could have a material adverse effect on our financial condition and results of operations.

•Our insurance subsidiaries are subject to minimum capital and surplus requirements, and our failure to meet these requirements could subject us to regulatory action.

•We are subject to assessments and other surcharges from state guaranty funds, and mandatory state insurance facilities, which may reduce our profitability.

•As a public benefit corporation, our focus on a specific public benefit purpose and producing a positive effect for society may negatively impact our financial performance.

•Our directors have a fiduciary duty to consider not only our stockholders' interests, but also our specific public benefit and the interests of other stakeholders affected by our actions. A joint investment committee consisting of our Co-Founders and an executive of SoftBank will have sole voting and dispositive control over the shares owned by the entities affiliated with SoftBank Group Corp. This joint investment committee further concentrates voting power with our Co-Founders, which could limit your ability to influence the outcome of important transactions, including a change in control.

•We conduct certain of our operations in Israel and therefore our results may be adversely affected by political, economic and military instability in Israel and the region.

4

PART I

Item 1. Business

Overview

Lemonade is rebuilding insurance from the ground up on a digital substrate and an innovative business model. By leveraging technology, data, artificial intelligence, contemporary design, and social impact, we believe we are making insurance more delightful, more affordable, and more precise. To that end, we have built a vertically-integrated company with wholly-owned insurance carriers in the United States and Europe, and the full technology stack to power them.

A brief chat with our bot, AI Maya, is all it takes to get covered with renters, homeowners, pet, car or life insurance, and we expect to offer a similar experience for other insurance products over time. Claims are filed by chatting with another bot, AI Jim, who pays claims in as little as three seconds. This breezy experience belies the extraordinary technology that enables it: a state-of-the-art platform that spans marketing to underwriting, customer care to claims processing, finance to regulation. Our architecture melds artificial intelligence with the human kind, and learns from the prodigious data it generates to become ever better at delighting customers and evaluating risk.

In addition to digitizing insurance end-to-end, we also reimagined the underlying business model to minimize volatility while maximizing trust and social impact. To lessen the volatility inherent in an industry directly impacted by the weather, we utilize several forms of reinsurance, with the goal of dampening the impact on our gross margin. The result is that excess claims are generally offloaded to reinsurers, while excess premiums can be donated to nonprofits selected by our customers as part of our annual "Giveback". These two ballasts, reinsurance and Giveback, reduce volatility, while creating an aligned, trustful, and values-rich relationship with our customers.

Our Business Model

At the foundation of our business model is a direct, digital, customer-centric experience that delivers rapid growth and strong retention. Our customer-centricity runs deep, and our underlying business model is designed to align interests between us and our customers. This technology-first customer acquisition and retention strategy, combined with our unconflicted business model, results in a highly attractive financial model.

We leverage technology in everything we do. More than 93% of homeowners insurance policies in the United States are sold via agents, making a platform that finds, onboards, and digitally serves consumers end-to-end very much an outlier. Our digital substrate enables us to integrate marketing and onboarding with underwriting and claims processing, collecting and deploying data throughout, to constantly drive efficient customer acquisition, enhance the experience, and mitigate risk. This approach results in significant, rapid scale coupled with high customer satisfaction.

To align our interests with those of our customers, encourage good behavior and build a long-term relationship based on mutual trust, we endeavor to decouple our financial incentives from variability in claims. Unlike many of our competitors, we work to minimize incentives to deny legitimate claims as we aim to give back, rather than pocket, leftover monies. Our reinsurance contracts serve to lessen volatility in our operating results, as a material portion of claims are borne by our reinsurance partners. See "Risk Factors — Risks Relating to Our Business”. Reinsurance may be unavailable at current levels and prices, which may limit our ability to write new business. Furthermore, reinsurance subjects us to counterparty risk and may not be adequate to protect us against losses, which could have a material effect on our results of operations and financial condition.

After our customers purchase a policy, we ask them to designate a charitable cause for us to support. As a result, we believe customers are less inclined to embellish claims as they could be hurting a nonprofit they care about, rather than an insurance company they do not.

Strong retention rates and a subscription-based model create highly-recurring and naturally-growing revenue streams, and provide visibility into our top-line results. Our reinsurance construct, in turn, mitigates the bottom-line volatility inherent in traditional insurance companies, where profits quite literally depend on the weather. With our reinsurance agreements offloading residual claims, and our Giveback policy offloading residual premiums, we have two powerful ballasts that reduce volatility, while creating an aligned, trustful, and values-rich relationship with our customers.

5

This combination of a customer-focused onboarding experience, a customer-aligned business model, and a revenue stream that grows along with our customers' insurance needs, has created a sustainable financial model that we are proud of. Over time, we believe our platform will continue to efficiently acquire new customers and give us the ability to service their growing needs at a lower cost, and with higher satisfaction levels, than the industry at large.

Our Technology

Data Advantage

Our proprietary and entirely integrated technology stack is a key enabler of our strategy and business model. Interactions with our customers across our platform generate a trove of data, which in turn improves interactions with our customers across our platform.

AI Maya

AI Maya, our playful onboarding and customer experience bot, uses natural language to guide customers through an easy and fun process of joining Lemonade. Maya handles everything from collecting information and personalizing coverage to creating quotes and facilitating payments securely. By asking customers a limited number of high-impact questions, and adapting based on their responses, AI Maya is able to dramatically reduce onboarding times while still collecting and utilizing the data that is central to our continuous improvement.

AI Jim

AI Jim is our claims bot, and, as of December 31, 2022, 98% of the time, it is AI Jim that will take the first notice of loss from a Lemonade customer making a claim, paying the claimant or declining the claim without human intervention (and with zero claims overhead, known as loss adjustment expense, or LAE). AI Jim triages and assigns claims he is not authorized to settle, or ones where he identifies concerns, to human claims experts, analyzing each expert's specialty, qualifications, workload, and schedule to determine to whom to assign the claim. Even where human escalation is needed, AI Jim will have done much of the heavy lifting so our team can settle claims and support customers in their hour of need as quickly and smoothly as possible.

The claims process represents the most acute pain point in the insurance experience, and it is where animosity toward the industry is most commonly cultivated. Re-imagining claims for the benefit of the customer, by aligning interests and incentives and by removing friction, hassle, cost, and delays, is therefore a key driver of our leadership in customer satisfaction.

CX.AI

CX.AI is our bot platform built to understand and instantly resolve customer requests without human intervention. About 27% of all Lemonade customer inquiries are currently handled this way. Customers often require assistance pre- or post-purchase, ranging from coverage questions to making changes to their policy, such as adding a spouse, updating coverage amounts, changing payment methods, or adding newly purchased items. CX.AI uses Natural Language Processing to analyze and understand customers' requests, helping them perform a growing set of tasks.

The efficiency boost CX.AI delivers is exemplified by its impact on 'moving' tickets. Until December 2018, a large number of support tickets handled by our human CX (Customer Experience) team were requests related to customers moving to new apartments or homes. CX.AI understands what customers are saying, asks for the information it needs, and takes it from there: canceling the existing policy when the time is right, evaluating the risk of the new address, transferring all customized coverages to the new policy, pricing it, processing the payment, and sending the new policy to the customer by email. The process takes a few seconds.

Our customer-facing technologies, AI Maya, AI Jim, and CX.AI deliver a superior experience at a fraction of the cost, all the while collecting and utilizing far more data than their human counterparts. A similar construct powers the rest of the Company.

Our 'behind the scenes technology' is structured within three proprietary applications: Forensic Graph, Blender, and Cooper.

6

Forensic Graph

Forensic Graph utilizes the combined power of behavioral economics, big data, and AI to predict, deter, detect, and block fraud throughout the customer engagement. The FBI estimates that insurance fraud in the United States (excluding health insurance fraud) costs more than $40 billion per year in increased premiums. It is a complicated problem to solve for traditional insurers, mostly due to data paucity. Forensic Graph tracks untold signals and analyzes relationships between things which may appear trivial or invisible to humans, but in which our machine learning uncovers complex multivariate links that have helped us avoid millions of dollars' worth of potential losses.

Blender

Blender is a robust insurance management platform that we built with customer centricity and exponential efficiency in mind. This is a built-from-scratch, cutting edge backend system, designed as a single, cohesive, and streamlined management tool for our customer experience, underwriting, claims, growth, marketing, finance, and risk teams. When a claims experience specialist logs in to Blender, for example, they instantly see all claims assigned to them by AI Jim. Blender then provides them with instructions for next steps, and when possible, includes coverage determinations, and alerts of suspicious activity. Critically, they will also see an extraordinary amount of information about the users' behavior patterns and their claim, background information, risk indicators, insurance history, and much more. If a vendor is needed, for example, to assess the damage, all appropriate suppliers will pop up in Blender, and can be dispatched to the field, and paid, at the push of a button. Blender brings similar integrated, customer-centric, and focused workflows to the other Lemonade teams as well.

Cooper

Cooper is our internal bot (we like to think of him as our own Jarvis) who runs important parts of our Company. Cooper handles complex as well as repetitive tasks, from helping our customer experience team handle lengthy, manual processes such as processing paper checks, to automatically running tens of thousands of tests on each release of our software. Cooper continuously analyzes spectrometry imaging beamed from NASA's satellites, identifying wildfires in real time and blocking ads and sales in the affected areas; Cooper collates and formats materials for our regulatory filings; and he even handles most of our engineering task allocation, code deployment, Q&A, and more. Cooper makes our team dramatically more efficient and keeps evolving and learning with time.

Forensic Graph, Blender, and Cooper, together with AI Maya, AI Jim, and CX.AI, run atop our Customer Cortex. The Customer Cortex, like a central nervous system, is the place where all data about our customers is transmitted, continuously analyzed, and then used by all six applications.

Growth Opportunities

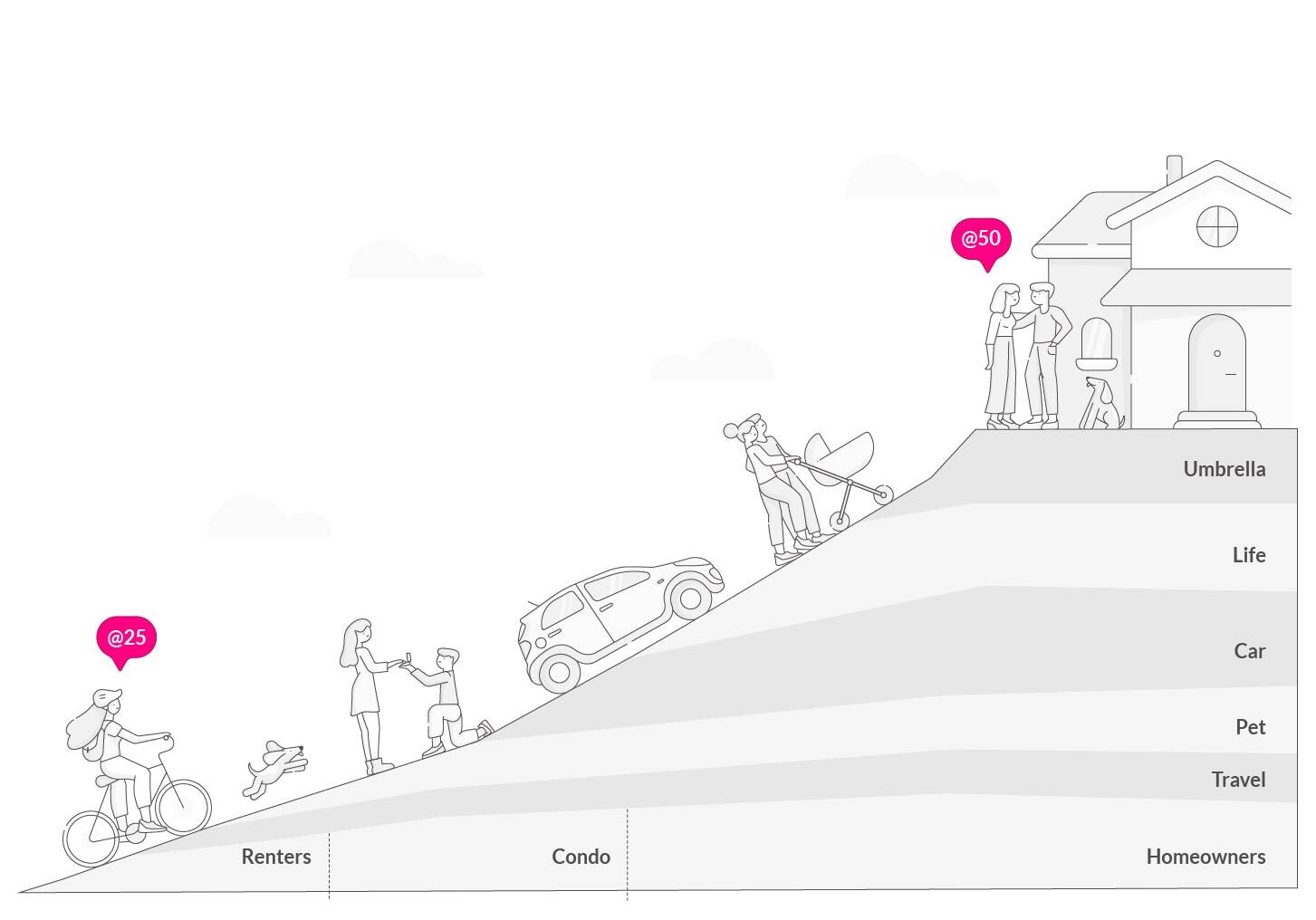

Acquire more customers

About 90% of our current home and renters customers said that they were not switching to Lemonade from another carrier. We are well positioned to grow our customer base by continuing to attract first time buyers, an underserved population replenishing every year.

Our delightful experience and competitive pricing also attract customers who switch from their existing carriers. Our bot automatically files the necessary paperwork to cancel a customer's old policy, removing what is typically a barrier to switching. As we continue to strengthen brand recognition and execute our marketing strategy, we will look to increase the number of customers migrating to the Lemonade platform.

7

Grow within our existing customer base

As our customers move up the economic ladder and through lifecycle events, their insurance needs evolve to higher value products: renters continuously acquire more property and frequently upgrade to successively larger homes. Growing households often need car, pet, and life insurance, and additional coverage. These progressions regularly trigger orders of magnitude jumps in insurance premiums, and within states that offer all of Lemonade’s “suite of products” - Renters, Home, Car, Pet, and Life - we are seeing more and more customers have multi Lemonade policies. For example in Illinois, the first state to have all of Lemonade’s suite of products for the 12-month period, the rate of “bundling”, that is, customers who went from a single-policy to a multi-policy, is growing quarter after quarter, increasing both premium and retention. We aim to provide an unmatched user experience in order to retain customers throughout their lifespan, expanding their lifetime value without incurring any incremental costs of acquisition.

Expand to new products

Our strategy of growing with our customers also lends itself to expanding into new lines of insurance, as lifecycle events trigger the need for additional insurance products.

Our regulatory framework, technology stack, and brand are all extensible to new lines of insurance, and we anticipate that these will contribute to our growth in the future. In just the last two years, we have added life, pet and car insurance to our growing portfolio of offerings, and expect to add additional coverage types over time.

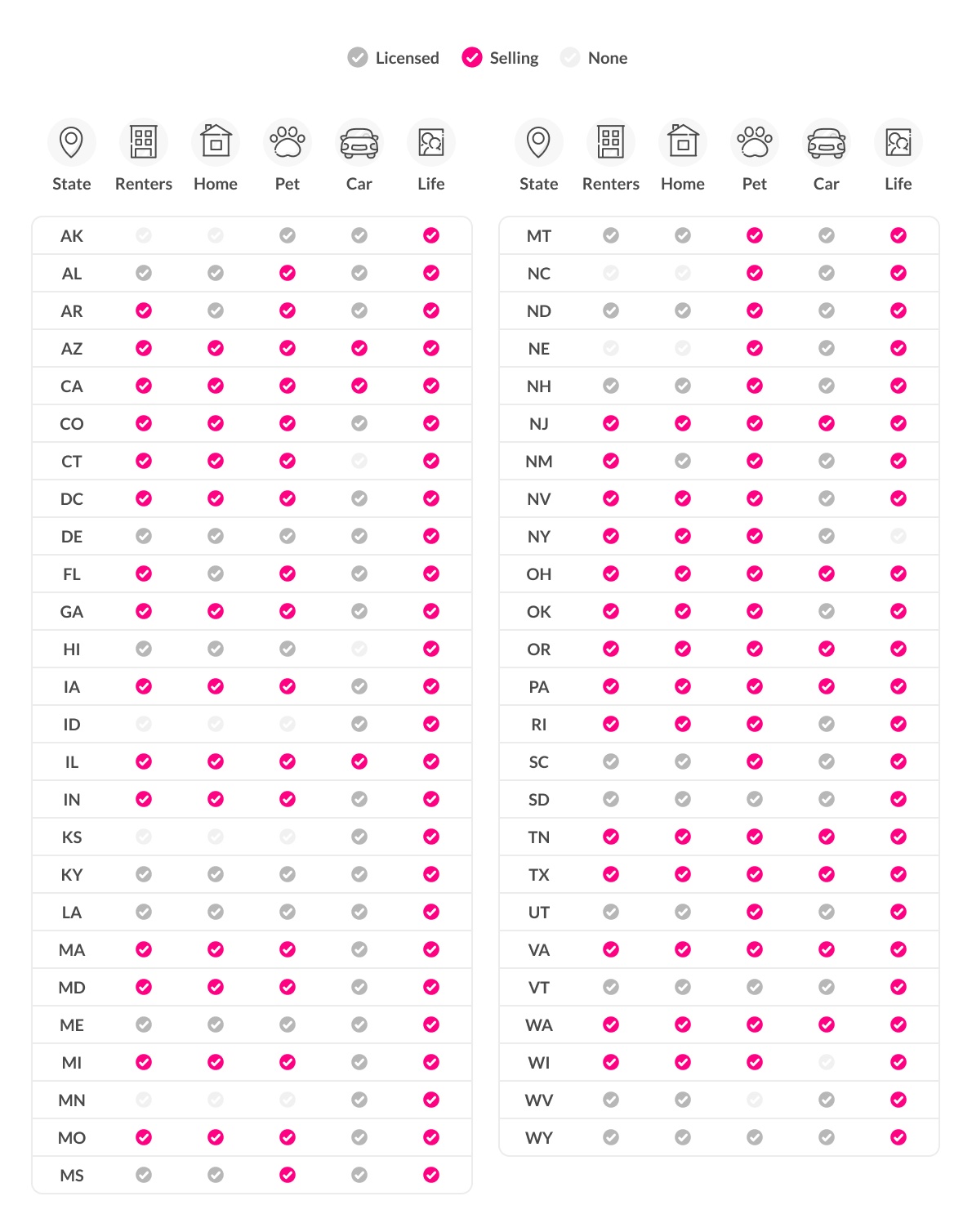

Expand to new geographies

As of December 31, 2022, we are licensed to sell renters, homeowners, pet and/or car insurance policies in 50 states of the United States and Washington, D.C. We operate in 38 of those states and Washington, D.C., which collectively represents approximately 92% of the U.S. population. Our strong brand and unique business model drive rapid growth and allow us to quickly gain share in new markets. We also hold a pan-European license, enabling us to passport into and sell in 30 countries across Europe, and subject to the temporary permissions regime in the U.K.,and commenced operations in Germany in 2019, and in the Netherlands and France in 2020. In October, 2022, we began selling contents insurance in the United Kingdom (“UK”) on a cross border basis under the UK’s Temporary Permission Regime. We also registered two UK branches: (i) Lemonade Insurance N.V., UK

8

Branch and its affiliate (ii) Lemonade Agency B.V., UK Branch as part of its process to become a fully licensed insurance branch in the UK.

The Lemonade platform is inherently multilingual and agile by design, so that we can efficiently expand into new markets and new products both within the United States and internationally.

Our Product Offerings

Renters and Homeowners Insurance

We currently offer our products to renters and homeowners in the United States, contents and liability insurance in Germany, the Netherlands, France, and the United Kingdom. The insurance we offer in the United States covers stolen or damaged property, and also covers personal liability, which protects our customers if they are responsible for an accident or damage to another person or their property. In a number of states, we also offer landlord insurance policies to condo and co-op owners who rent out their property less than five times a year.

The full Lemonade experience is available through our iOS and Android app, as well as through our website. Before a customer purchases one of our policies, we allow the customer to review a summary of their coverage and a sample policy. We also enable the customer to reconfigure their coverage and other policy settings, such as the deductible and start date. After payment via a credit or debit card, we instantly issue the customer their policy documents and send it to them via email. From start to finish, the entire process is completed digitally.

In the U.S., our products automatically cover all residents of a household who are related to the customer by marriage, blood, or adoption. In addition to the base coverage we offer for personal property, electronics, furniture, and clothing, our customers can purchase extra coverage to protect against accidental loss, damage, and theft, worldwide, of their jewelry, fine art, and other personal property.

Pet Insurance

We currently offer pet insurance that covers diagnostics, procedures, medication, accidents or illness. Even our basic pet insurance offering covers blood tests, urinalysis, X-rays, MRIs, lab work, and CT scans. We also offer two optional add-ons to the basic plan, a wellness package and an extended accident and illness package. These provide additional coverage for preventative care costs, including annual exams and vaccines, and recovery treatments, including physical therapy and hydrotherapy.

We believe our expansion into pet insurance will allow us to further achieve our long-term strategy of growing with our young customer base by offering new insurance experiences to customers as they progress in their lifecycles. As of December 31, 2022, about 72% of our pet insurance policies were sold to new customers, and about 5% of those have already added a renters or homeowners policy to their pet policy. Customers that bundle our insurance offerings typically save money. The remaining 28% or so of pet insurance policies were sold to existing customers, whose median premium per customer grew roughly 3.7x with little to no incremental customer acquisition costs.

Car

We launched car insurance in December 2021 in Illinois, and now offer it in a handful of states. Lemonade Car insurance covers car accidents, weather damage, theft and vandalism, damage from fire, trees, or animals, glass and windshield repair, liability for bodily injury and property damage, medical expenses, roadside assistance, and reimburses drivers for expenses relating to temporary transportation when a car is being repaired, subject to certain exceptions. For each added Lemonade Car customer, we plant trees based on drivers’ mileage to help offset carbon emissions, and our product was built for drivers with low mileage and environment-friendly cars.

In July 2022, we announced the completion of the acquisition of Metromile, a pay-per-mile car insurance provider. As part of the acquisition, we received a full-stack insurance entity with 49 state licenses plus the District of Columbia, and precision data from 500 million car trips.

9

Life

Lemonade also provides life insurance product through an arrangement with a third-party administrator (“TPA”) which operates as an insurance agent and TPA for a third-party life and health insurance company. With Lemonade’s term life insurance offering, individuals age 18 to 60 can apply online for up to $1.5 million in coverage, for terms of 10, 15, 20, 25, and 30 years, without a medical exam or a lab test. Applicants simply answer some basic questions about their health to apply for coverage. With term life offered by Lemonade, policyholders pay a fixed annual premium for the entire term of the policy.

Giveback Feature

Giveback is a distinctive feature, whereby each year we aim to donate leftover money to causes our customers care about. After our customers purchase a policy, we ask them to select, from a pre-vetted list, a charitable cause to support with the residual premiums from their policy. Behind the scenes, customers who select the same charitable cause are classified as members of the same "cohort." Once a year we look at the loss ratio of each cohort, and provided that we pass the financial ratio tests required by our regulators, we aim to donate the funds remaining, if any, to the charitable cause selected by that cohort. Cohorts with a loss ratio above 40% usually will not receive a Giveback.

The Giveback is paid only if payment is authorized by our board of directors in its sole discretion and consistent with its duty of care. See "Risk Factors — We could be forced to modify or eliminate our Giveback, which could undermine our business model and have a material adverse effect on our results of operations and financial condition." Our 2022 Giveback for the 12 month period ended June 30, 2022 amounted to approximately 1% of earned premiums. We calculate our annual Giveback on each anniversary of our primary reinsurance contract. The Giveback is not a contractual obligation to any customer or to any cause, and customers may not take a tax deduction related to the donations.

We have informed, and intend to continue to inform, our customers of the amount donated to their selected nonprofit during each Giveback on an annual basis, details of which follow:

| Giveback Year | Number of Nonprofit Organizations | Amount | ||||||

| 2022 | 59 | $ | 1,873,588 | |||||

| 2021 | 65 | $ | 2,303,381 | |||||

| 2020 | 34 | $ | 1,128,109 | |||||

| 2019 | 26 | $ | 631,540 | |||||

| 2018 | 15 | $ | 162,135 | |||||

Selected nonprofit organizations chosen by customers in 2022 included: Charity Water, Malala Fund, Habitat for Humanity, and many others. Although new and untested, we believe that donating a portion of the money left over after paying claims to nonprofits will discourage fraud and promote greater trust between us and our customers.

Our Vertically-Integrated Platform

Sales and Marketing

Our goal is to increase brand awareness and the number of customers migrating to our platform by utilizing a number of marketing channels to aid our direct-to-consumer sales model. Our primary channel of advertisement is the internet, where we promote our ads and services through various media and social media platforms, including Facebook and Instagram. We also use the data generated in customer support interactions to constantly refine and improve our marketing campaigns. We conduct drip campaigns via email to follow up with those who have inquired about us or started the on-boarding process. Additionally, we enter into agreements with parties who have access to potential customers, including insurance agencies, apartment building owners, and property management companies.

10

Underwriting

Our digital platform enables us to ask fewer questions of our customers but derive many times more data points from each customer interaction than our competitors. To date we have collected over 8.2 billion data entries, a trove that grows by the minute. Applying machine learning to these data allows us to identify predictive patterns, and these inform our underwriting. Our underwriting process involves collecting this information, classifying and evaluating each individual risk exposure, assessing the impact of the risk on our existing portfolio, and pricing the risk accordingly. When we launched, and had no data of our own, pricing and underwriting were done using easily obtainable industry information. Due to the limitations of these data, customers appeared relatively undifferentiated. As we collected more data, we found that groups our competitors viewed as monolithic were actually made up of predictable sub-groups with over 600% variation in their likelihood to file a claim.

Claims Process

Powered and driven by our technology, our claims process is conducted via our digital platform, which includes our iOS and Android mobile apps. Claims can be substantiated with receipts, notes of where and when the item was purchased, and in certain cases, police reports. We also ask the customer to record a video explaining their claim to enhance the claim review process. After the customer completes a claim report on our mobile app, the customer is asked to enter bank account information. If the claim is approved, a payment is issued and deposited directly into the customer's account. Claims are commonly paid or declined through our claims-bot, AI Jim, within seconds.

While a meaningful portion of simple theft claims are paid almost instantly, in many cases the incident is also reviewed by a human before the claim is approved, and certain property damage claims or liability claims may take longer to settle. In an event that requires immediate assistance or temporary housing as a result of fire, ongoing water damage, or any other structural damage that leaves the customer's home exposed, we contact the customer to assess the situation and provide emergency services, such as water or fire damage cleanup, temporary housing, or a designated specialist.

Reinsurance

Insurance often produces businesses with highly recurring revenue streams, and hence predictable top lines, but with significant bottom-line volatility, as profits can literally fluctuate with the weather. Earthquakes, hailstorms, wildfires and hurricanes strike with caprice, and can push an otherwise profitable business deep into the red with little or no warning.

The first-order consequence of this uncertainty is that insurers often see unwelcome swings in their results. The second-order consequence is that regulators require insurers to keep significant reserves to absorb these swings, making them capital intensive. In defiance of these industry norms, we set out to architect our business to be at once capital-light and possessed of predictable and growing gross margin. Through judicious use of "reinsurance," we believe we have largely achieved these goals.

Reinsurance is a financial instrument under which one insurer, the "reinsurer," agrees to cover a portion of the claims of another insurer, the "primary insurer," in return for a portion of their premiums. While this description characterizes all reinsurance, implementations come in different flavors, each with its own costs and benefits. We have entered into a range of reinsurance agreements, differing in both duration and terms, which combine, we believe, to deliver maximum capital efficiency, while optimizing our gross margin for both stability and size.

Proportional Reinsurance: Maximize Capital Efficiency

The low cost of capital for reinsurance companies creates an opportunity to share premiums and maintain our gross margin while dramatically reducing our capital requirements through a structure called "proportional reinsurance" (also known as "quota share reinsurance"). We currently have proportional reinsurance covering a significant proportion of our business (the "Proportional Reinsurance Contracts"). Under the Proportional Reinsurance Contracts, which span all of our products and geographies, we transfer, or "cede, a fixed share of our premiums to our reinsurers. In exchange, these reinsurers pay us a "ceding commission" of up to 25% for every dollar ceded, in addition to funding all of the corresponding claims. This arrangement mirrors our fixed fee, and hence shields our gross margin from the volatility of claims, while boosting our capital efficiency dramatically.

11

Under U.S. and E.U. regulatory laws, insurance companies are required to set aside "surplus capital" in accordance with various formulae. These requirements tend to be more onerous for younger companies experiencing rapid growth, such that without reinsurance we would need to reserve as much as 50 cents for every dollar of premiums sold. Our proportional reinsurance structure shifts most of that surplus capital requirement to the reinsurer, reducing these capital requirements significantly.

Non-Proportional Reinsurance: Optimize Gross Margin

As described above, our Proportional Reinsurance Contracts provide that we cede a significant portion of our premiums to our reinsurers, pushing our capital efficiency to near maximized levels. We have opted to manage the remaining portion of our business with alternative forms of reinsurance, with a view to maximizing profitability.

These two remaining goals live in tension with one another: leaving zero "wiggle room" around our fixed fee would guarantee its stability, but would preclude our benefiting from our improving loss ratio. Conversely, any room for improved profitability would also introduce additional volatility into our business.

To balance our desire for both growing and stable gross margin, we set out to structure our remaining reinsurance such that variability in our gross margin will be largely contained, though not eliminated entirely. We believe we have achieved this through a combination of reinsurance structures known as "per risk reinsurance" and "facultative reinsurance" (the "Non-Proportional Reinsurance Contracts"). Together, these contracts reduce the maximum amount we would need to pay for any one claim.

Our business is exposed to the risk of severe weather conditions and other catastrophes which are inherently unpredictable. To reduce this risk, we also purchase one year property catastrophe excess protection as well as reinsurance to protect us from the peril of earthquake.

We believe our reinsurance structure achieves important goals: making us capital-light, buffering our gross margin from the vicissitudes of claims, and leaving room for our gross margin to grow.

Duration

Our goal of maximizing predictability of our results, while growing gross margin over time, led us to vary not only the terms of our reinsurance agreements, but their term, too.

The Proportional Reinsurance Contracts are issued by a consortium of five reinsurers, including Hannover Ruck SE, Lloyd’s Underwriter Syndicate No. 1084 CSL, MAPFRE Re (Spain), and Swiss Re America (US), each holding an ‘A’ or better rating from A.M. Best, and each holding a share of the agreement’s commitments. Our Non-Proportional Reinsurance Contracts are issued by a collection of reinsurers, each holding an ‘A’ or better rating from A.M. Best, have a one-year term that expired on June 30, 2022.

All told, approximately half of our book is reinsured on a three-year term through June 30, 2023, with the remainder coming up for renewal and renegotiation on an annual basis. We believe that staggering the terms this way provides an appropriate balance between maximizing predictability, and enabling us to capture more margin over time.

Investments

Our portfolio of investable assets is primarily held in cash, money market funds, and fixed income securities which includes U.S. government and government agencies obligations, corporate debt securities and asset-backed securities with relatively short durations. We manage the portfolio in accordance with the investment policies and guidelines approved by the board of directors.

We have designed our investment policy and objectives to provide a balance between current yield, conservation of capital, and liquidity requirements of our operations setting guidelines that provide for a well-diversified investment portfolio that is compliant with insurance regulations applicable to the states in which we operate. Furthermore, our investment policy considers our focus on ESG and prohibits investments in areas such as oil and gas, coal, tobacco, controversial weapons, and non-compliance with the United Nations Global Compact. The policy, which may change from time to time, is approved by the board of directors and is reviewed on a regular basis in order to ensure that the policy evolves in response to changes in the financial markets. See "Note 4 —

12

Summary of Significant Accounting Policies" in the Notes to Consolidated Financial Statements included in this Annual Report.

Competition

The homeowners, pet, car and, to a lesser extent, the renters insurance industries in which we operate are highly competitive. While we believe we are well positioned to execute our business model and reinvent insurance, we face significant competition from traditional insurance companies such as Allstate, Farmers, Liberty Mutual, State Farm, GEICO, Progressive and Travelers. Although we are tapping into markets that our competitors have struggled to reach, the incumbent insurance companies are larger than us and have significant competitive advantages over us, including increased name recognition, higher financial ratings, greater resources, additional access to capital and more types of insurance coverage to offer, such as car, health and life insurance, than we currently do. In particular, unlike us, many of these competitors offer consumers the ability to purchase homeowners and multiple other types of insurance products and "bundle" them together, in certain circumstances, include an umbrella liability policy for additional coverage at competitive prices. Moreover, as we expand into new lines of business and offer additional products beyond renters and homeowners insurance, pet and car insurance, we face intense competition from traditional insurance companies that are already established in such markets. Competitors in the pet insurance space include companies such as Nationwide, Embrace, and Trupanion. Competitors in the car insurance space include companies such as Progressive, GEICO and Allstate.

We also compete with new market entrants. Competition is based on many factors, including the reputation and experience of the insurer, coverages offered, pricing and other terms and conditions, customer service, relationships with brokers and agents (including ease of doing business, service provided, and commission rates paid), size, and financial strength ratings, among other considerations. We believe we compete favorably across many of these factors, and have developed a digital platform and business model based on artificial intelligence and behavioral economics that we believe will be difficult for incumbent insurance providers to emulate.

Intellectual Property

The protection of our technology and intellectual property is an important aspect of our business. We intend to rely upon a combination of trademarks, trade secrets, copyrights, confidentiality procedures, contractual commitments, and other legal rights to establish and protect our intellectual property. We generally enter into confidentiality agreements and invention of work product assignment agreements with our employees and consultants to control access to, and clarify ownership of, our proprietary information.

As of December 31, 2022, we have 5 issued patents and 2 pending patent applications in the United States. The issued patents generally related to determining the route and parking location of a vehicle, recording trip data associated with a vehicle, and estimating the usage of a vehicle based on refueling events. The issued patents are expected to expire between September 1, 2035 and January 11, 2036. We do not own any foreign patents and do not have any foreign patent applications pending. As of December 31, 2022, we hold 120 foreign registered trademarks and 4 registered trademarks in the United States, including the Lemonade mark, have 16 foreign trademark applications pending and no U.S. trademark applications pending, and hold three copyrights in the United States, covering certain videos, texts, photographs, and artwork displayed on our mobile app and website. We continually review our development efforts to assess the existence and patentability of new intellectual property.

Intellectual property laws, procedures, and restrictions provide only limited protection and any of our intellectual property rights may be challenged, invalidated, circumvented, infringed, or misappropriated. Further, the laws of certain countries do not protect proprietary rights to the same extent as the laws of the United States, and, therefore, in certain jurisdictions, we may be unable to protect our proprietary technology.

Certified B Corp Status

While not required by Delaware law or the terms of our certificate of incorporation, we have been designated as a Certified B Corp. The term "Certified B Corp" does not refer to a particular form of legal entity, but instead refers to companies that are certified by B Lab, an independent nonprofit organization, as meeting rigorous standards of social and environmental performance, accountability, and transparency.

13

The first step in becoming a Certified B Corp is completing a comprehensive and objective assessment of a business's positive impact on society and the environment. The assessment varies depending on the company's size (number of employees), and sector. The standards in the assessment are created and revised by an independent governing body that determines eligibility to be a Certified B Corp.

By completing a set of over 200 questions that reflect impact indicators, best practices, and outcomes, a company receives a composite score on a 200-point scale representative of its overall impact on its employees, customers, communities, and the environment. Representative indicators in the assessment range from payment above a living wage, employee benefits, charitable giving/community service, and use of renewable energy.

Recognition as a Certified B Corp currently requires that a company achieve a reviewed assessment score of at least 80. The review process includes a phone review and a random selection of indicators for purposes of verifying documentation. The assessment also includes a corporate structure review and a disclosure questionnaire, including certain practices, fines, and sanctions related to the company or its partners.

Our certification also required us to adopt the public benefit corporation structure, a step we have already completed. Once certified, every Certified B Corp must make its assessment score transparent on the independent non-profit organization's website. Acceptance as a Certified B Corp and continued certification is at the sole discretion of the independent nonprofit organization.

Human Capital Resources

Employees

As of December 31, 2022, we had 1,367 employees, 951 of whom were based in the United States and the rest of whom were based outside of the United States, primarily in Israel and the Netherlands. In the Netherlands, certain employees are subject to a collective agreement between the Dutch Association of Insurers and various trade unions. The collective agreement covers wages and terms and conditions of employment. Participation in the collective agreement is mandatory for members of the Dutch Association of Insurers, a leading association of private insurance companies operating in the Netherlands. Beyond this, to our knowledge, none of our employees are represented by a labor union. We consider our relationships with our employees to be good and have not experienced any interruptions of operations due to labor disagreements.

As of December 31, 2022, and based on public information from five competing insurance companies in the United States, we estimate that the number of customers per employee for those companies ranges from approximately 150 to approximately 450 customers per employee. We base this estimate on publicly available information, which we have adjusted for comparability. The calculation of "employees" includes insurance agents and brokers because they are a significant cost component for other insurance companies. In comparison to these competitors, our number of customers per employee was approximately 1,300 as of December 31, 2022.

Culture and Values

Our status as a Certified B Corp and our commitment to charitable giving, in particular our Giveback program distinguishes us from our competitors, with the goal of building a trusting relationship between us, our employees, and our customers. We value the power of creativity and encourage and support the sharing of ideas to enhance our business model. Like the industry in which we operate, we understand the importance and value of a community pooling its resources together for the public good. We value inclusivity, respecting differences, and seamless teamwork in every facet of our business.

In 2020, we issued 500,000 shares of common stock as the initial endowment of the Lemonade Foundation, a 501(c)(4) social welfare organization established under Arizona law. By contributing approximately 1% of our common stock to the Lemonade Foundation, we hope to promote charitable giving and other community-centric activities with a nexus to our community.

In addition, the Foundation recently launched a first of its kind blockchain based insurance product for the world’s most vulnerable farmers. The product was built with a goal of protecting subsistence farmers against the effects of climate change. Thousands of families in Kenya have already been protected by this product, and the Foundation expects to continue scaling this product in the coming months. The product was launched as part of the Lemonade Foundation Crypto Climate Coalition - in cooperation with a number of strategic partners: Hannover Re, Pula, Chainlink, Avalanche, Etherisc and DAOstack.

14

Diversity

We understand that strength lies in the diversity of our employees and drives the innovation behind our product. We encourage employees to bring their lived experiences, and personal strengths, to develop new ideas, improve customer experience and shape our brand. We engage with employees for ideas of nonprofits to partner with, or resources to learn more about a social issue, and their candid (and anonymous, should they choose) feedback about our workplace culture and environment. In the wake of the social justice movements, our employees founded in 2020 an internal anti-racism education group, and continued to share resources, promote racial equity, and develop anti-bias training.

Health, Safety and Wellness

As a B Corp, it is part of our legal mission to advance the health, well-being and equity of employees. To that end, employees have access to health and wellness programs, and healthcare plans.

Geographic Scope of Business

In the United States, as of December 31, 2022, Lemonade Insurance Company (“LIC”) and Metromile Insurance Company (“MIC”) are licensed to sell our insurance products in the following states:

We also currently hold a pan-European license, which enables us to sell in 30 countries across Europe, and subject to the temporary permissions regime in the U.K. We commenced operating in Germany in 2019, in the Netherlands and France in 2020, and in the U.K. in 2022.

15

Seasonality

For information regarding the seasonality of our business, please refer to Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report.

Regulation of our Business

Insurance Regulation

Certain of our U.S. insurance subsidiaries are regulated by insurance regulatory authorities in the states in which we operate. State insurance laws and regulations generally are designed to protect the interests of customers, consumers, and claimants rather than stockholders or other investors. State regulation generally have broad administrative power with respect to all aspects of the insurance business. The regulatory requirements and restrictions include, among others, the following:

•approval of policy forms and premium rates;

•approval for intercompany service agreements;

•advertising, marketing, and trade practices; and

•restrictions on the ability of our regulated insurance subsidiaries to pay dividends to us or enter into certain related party transactions

Regulation of insurance companies constantly changes as governmental agencies and legislatures react to real or perceived issues. Recently, state insurance regulators have been scrutinizing the industry’s practices with respect to the collection and uses of consumer data.

Required Licensing

Our regulated U.S. insurance subsidiaries are domiciled and admitted in the states of New York and Delaware. Under a provision of the California Insurance Code, MIC is deemed “commercially domiciled” in California, meaning that the California Department of Insurance is entitled to regulate certain aspects of MIC’s business as if it were actually domiciled in California.

LIC, MIC, Lemonade Insurance Agency, LLC, Lemonade Life Insurance Agency, LLC, Lemonade E&S Insurance Agency, LLC and Metromile Insurance Services LLC must apply for and maintain licenses to provide and sell insurance in those jurisdictions in which they transact insurance businesses.

Our insurance company and insurance producer subsidiaries are required to adhere to myriad laws and regulatory requirements. The insurance regulators in the states in which our subsidiaries do the business of insurance are empowered to conduct on-site visits and examine the financial affairs and market conduct practices of those entities. Insurance regulators have broad administrative powers to impose monetary penalties and/or restrict or revoke licenses to transact business for violations of applicable laws and regulations.

Restrictions on Paying Dividends

We are a holding company that transacts a majority of our business through operating subsidiaries. Consequently, our ability to pay dividends to stockholders and meet our debt payment obligations is largely dependent on dividends and other distributions from our subsidiaries. Applicable insurance laws restrict the ability of our regulated insurance subsidiaries to declare stockholder dividends. Applicable insurance regulators require insurance companies to maintain specified levels of statutory capital and surplus.

Insurance regulators have broad powers to prevent reduction of statutory surplus to inadequate levels, and there is no assurance that dividends of the maximum amounts calculated under any applicable formula would be permitted to be made by our insurance subsidiaries. State insurance regulatory authorities that have jurisdiction over the payment of dividends by our regulated insurance subsidiaries may in the future adopt statutory provisions more restrictive than those currently in effect.

16

Investment Regulation

LIC is subject to New York’s insurance laws and MIC is subject to Delaware and California’s laws regarding the composition of their investments. Those laws generally require diversification of their investment portfolios and limits on the amount of their investments in certain categories. Failure to comply with these laws and regulations would cause non-conforming investments to be treated as non-admitted assets for purposes of measuring statutory surplus and, in some instances, would require those companies to sell those investments.

Licensing of Our Employees and Adjusters

In most states in which we operate, insurance claims adjusters are required to be licensed and some must fulfill annual continuing education requirements. In most instances, our employees who are negotiating coverage terms are underwriters and are not required to be licensed agents. As of December 31, 2022, 365 employees were required to maintain and did maintain requisite licenses for these activities in most states in which we operate.

Enterprise Risk, Cybersecurity, and Other Recent Developments

The National Association of Insurance Commissioners (“NAIC”) has engaged in a concerted effort to strengthen the ability of U.S. state insurance regulators to monitor U.S. insurance holding company groups. Among other things, the NAIC’s model, when adopted, requires the ultimate controlling person of an insurance company to submit an annual enterprise risk management report that describes the risk that an activity, circumstance, event, or series of events involving one or more affiliates of an insurer will, if not remedied promptly, be likely to have a material adverse effect upon the financial condition or liquidity of the insurer or its insurance holding company system as a whole. Recently, the NAIC has developed model laws requiring annual reports concerning the nature of corporate governance within an insurance holding company.

In 2012, the NAIC adopted the Risk Management and Own Risk and Solvency Assessment (“ORSA”) Model Act (the “ORSA Model Act”) to require domestic insurers to maintain a risk management framework and establishes a legal requirement for domestic insurers to conduct an ORSA in accordance with the NAIC’s ORSA Guidance Manual. The ORSA Model Act provides that domestic insurers, or their insurance group, must regularly conduct an ORSA consistent with a process comparable to the ORSA Guidance Manual process. The ORSA Model Act also provides that, no more than once a year, an insurer’s domiciliary regulator may request that an insurer submit an ORSA summary report, or any combination of reports that together contain the information described in the ORSA Guidance Manual, with respect to the insurer and the insurance group of which it is a member. When the ORSA Model Act is adopted by a particular state, it imposes more extensive filing requirements on parents and affiliates of domestic insurers. Delaware has adopted its version of the ORSA Model Act and New York has implemented portions of the ORSA Model Act.

In the course of our business, we collect and maintain confidential and personal information. As a result, we are subject to U.S. federal and state privacy and data security laws and regulations that, among other things, require that we institute and maintain certain policies and procedures to safeguard this information from improper use or disclosure. For example, in 2017, the NYDFS adopted a broad cybersecurity regulation that requires financial services institutions to, among other things, implement and maintain a cybersecurity program and a cybersecurity policy that will be monitored and tested periodically, develop controls and technology standards for data protection, meet minimum standards in response to any cybersecurity breach and annually certify their compliance with the regulation. Additionally, in 2017 the NAIC adopted the Insurance Data Security Model Law, which established standards for data security and for the investigation and notification of insurance commissioners of cybersecurity events involving unauthorized access to, or the misuse of, certain nonpublic information. A number of states have enacted the Insurance Data Security Model Law or similar laws, and we expect more states to follow.

California has enacted legislation restricting the use of automated systems to communicate with people online. California enacted a statute making it unlawful for any person to use a bot to communicate with another person in California online with the intent to mislead the other person about its artificial identity for the purpose of knowingly deceiving the person about the content of the communication in order to incentivize a purchase or sale of goods or services in a commercial transaction. The statute provides that a person using a bot will not be liable under the statute if the person discloses that it is a bot. See “Risk Factors — Risks Relating to Our Business — New legislation or legal requirements may affect how we communicate with our customers, which could have a material adverse effect on our business model, financial condition, and results of operations.”

17

GDPR

The General Data Protection Regulation (E.U.) 2016/679 (the “GDPR”) applies to our activities to the extent that those activities take place in the context of our establishments in the European Union and the United Kingdom General Data Protection Regulation and Data Protection Act 2018 (collectively, the “U.K. GDPR”) applies to our activities to the extent that those activities take place in the context of our establishments in the U.K.. In addition, the GDPR/U.K. GDPR may apply to our activities that involve the processing of personal data of individuals in the European Union or U.K. to whom we offer our products or services. The GDPR/U.K. GDPR could also apply to our business if we were to monitor the activities of individuals in the European Union or U.K.. As we expand into Europe or U.K., the compliance obligations under the GDPR/U.K. GDPR (as set out above) will become more significant. See “Risk Factors — Risks Relating to Our Business — We may face particular privacy, data security, and data protection risks as we continue to expand into Europe or U.K. in connection with the GDPR/U.K. GDPR and other data protection regulations.”

Federal and State Legislative and Regulatory Changes

A number of federal laws affect and apply to the insurance industry, including various privacy laws, the Fair Credit Reporting Act (“FCRA”), and the economic and trade sanctions implemented by the Office of Foreign Assets Control (“OFAC”) of the U.S. Department of the Treasury. OFAC maintains and enforces economic sanctions against certain foreign countries and groups and prohibits U.S. persons from engaging in certain transactions with certain persons or entities. OFAC has imposed civil penalties on persons, including insurance and reinsurance companies, arising from violations of its economic sanctions program.

Credit for Reinsurance

State insurance laws permit U.S. insurance companies, as ceding insurers, to take financial statement credit for reinsurance that is ceded, so long as the assuming reinsurer satisfies the state’s credit for reinsurance laws. There are several different ways in which the credit for reinsurance laws may be satisfied by an assuming reinsurer, including being licensed in the state, being accredited in the state, or maintaining certain types of qualifying collateral. We ensure that LIC and MIC are able to take full financial statement credit for their reinsurance.

Insolvency Funds and Associations, Mandatory Pools, and Insurance Facilities

Most states require admitted property and casualty insurance companies to become members of insolvency funds or associations which generally protect customers against the insolvency of the admitted insurance companies. Members of the fund or association must contribute to the payment of certain claims made against insolvent insurance companies through annual assessments. The annual assessments required in any one year will vary from state to state, and are subject to various maximum assessments per line of insurance.

Risk-Based Capital

Risk-based capital laws are designed to assess the minimum amount of capital that an insurance company needs to support its overall business operations and to ensure that it has an acceptably low expectation of becoming financially impaired. State insurance regulators use risk-based capital to set capital requirements, considering the size and degree of risk taken by the insurer and taking into account various risk factors including asset risk, credit risk, underwriting risk, and interest rate risk. As the ratio of an insurer’s total adjusted capital and surplus decreases relative to its risk-based capital, the risk-based capital laws provide for increasing levels of regulatory intervention culminating with mandatory control of the operations of the insurer by the domiciliary insurance department at the so-called mandatory control level. Our regulators in New York, Delaware and California require annual reporting to confirm that LIC and MIC hold in excess of the minimum amount of risk-based capital necessary for their operations. Insurers falling below a calculated threshold may be subject to varying degrees of regulatory action. Failure to maintain risk-based capital at the required levels could adversely affect the ability of LIC and MIC to maintain the regulatory approvals necessary to conduct their businesses. As of December 31, 2022, LIC maintained a risk-based capital level of 376% and MIC maintained a risk-based capital level of 440%.

18

IRIS Ratios

The NAIC Insurance Regulatory Information System (“IRIS”) is a collection of analytical tools designed to provide state insurance regulators with an integrated approach to screening and analyzing the financial condition of insurance companies operating in their respective states. IRIS consists of two phases: statistical and analytical. In the statistical phase, the NAIC database generates key financial ratio results based on financial information obtained from insurers’ annual statutory statements. The statistical phase highlights those insurers that merit the highest priority in the allocation of the state insurance regulators’ resources. The ratios are not, in themselves, indicative of adverse financial conditions. The analytical phase is a review of the annual statements, financial ratios, and other automated solvency tools. An insurance company may fall out of the usual range for one or more ratios for any number of reasons and a ratio falling outside the prescribed "usual range" is not considered a failing result. Rather, unusual values are viewed as part of the regulatory early monitoring system. The primary goal of the analytical phase is to identify companies that appear to require immediate regulatory attention.

Statutory Accounting Principles

Statutory accounting principles (“SAP”) is a basis of accounting developed by U.S. insurance regulators to monitor and regulate the solvency of insurance companies. In developing SAP, insurance regulators were primarily concerned with evaluating an insurer’s ability to pay all its current and future obligations to customers. As a result, statutory accounting focuses on conservatively valuing the assets and liabilities of insurers, generally in accordance with standards specified by the insurer’s domiciliary jurisdiction. Uniform statutory accounting practices are established by the NAIC and generally adopted by regulators in the various U.S. jurisdictions. These accounting principles and related regulations determine, among other things, the amounts our regulated insurance subsidiaries may pay to us as dividends and differ somewhat from U.S. Generally Accepted Accounting Principles (“GAAP”), which are designed to measure a business on a going-concern basis. GAAP gives consideration to matching of revenue and expenses and, as a result, certain expenses are capitalized when incurred and then amortized over the life of the associated policies. The valuation of assets and liabilities under GAAP is based in part on best estimate assumptions made by the insurer. Stockholders’ equity represents both amounts currently available and amounts expected to emerge over the life of the business. As a result, the values for assets, liabilities, and equity reflected in financial statements prepared in accordance with GAAP may be different from those reflected in financial statements prepared under SAP.

Rate Regulation

Nearly all states have insurance laws requiring personal property and casualty insurers to file rating plans, policy or coverage forms, and other information with the state’s regulatory authority. In many cases, such rating plans, policy forms, or both must be approved prior to use.

The speed with which an insurer can change rates in response to competition or increasing costs depends, in part, on whether the rating laws are (i) prior approval, (ii) file-and-use, or (iii) use-and-file laws. In states having prior approval laws, the regulator must approve a rate before the insurer may use it. In states having file-and-use laws, the insurer does not have to wait for the regulator’s approval to use a rate, but the rate must be filed with the regulatory authority prior to being used. A use-and-file law requires an insurer to file rates within a certain period of time after the insurer begins using them. Eighteen states, including California and New York, have prior approval laws. Under all three types of rating laws, the regulator has the authority to disapprove a rate filing.

An insurer’s ability to adjust its rates in response to competition or to changing costs is dependent on an insurer’s ability to demonstrate to the regulator that its rates or proposed rating plan meets the requirements of the rating laws. In those states that significantly restrict an insurer’s discretion in selecting the business that it wants to underwrite, an insurer can manage its risk of loss by charging a rate that reflects the cost and expense of providing the insurance. In those states that significantly restrict an insurer’s ability to charge a rate that reflects the cost and expense of providing the insurance, the insurer can manage its risk of loss by being more selective in the type of business it underwrites. When a state significantly restricts both underwriting and pricing, it becomes more difficult for an insurer to maintain its profitability.

19

From time to time, the personal lines insurance industry comes under pressure from state regulators, legislators, and special-interest groups to reduce, freeze, or set rates at levels that do not correspond with our analysis of underlying costs and expenses. We expect this kind of pressure to persist. State regulators may interpret existing law or rely on future legislation or regulations to impose new restrictions that adversely affect profitability or growth. We cannot predict the impact on our business of possible future legislative and regulatory measures regarding insurance rates.

European Regulation