UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported):

(Exact name of Registrant as specified in its charter)

|

| |||

(State or other jurisdiction of incorporation or organization) | (Commission file number) | (I.R.S. Employer Identification No.) | ||

(Address of principal executive offices) | (Zip Code) | |||

Registrant’s telephone number, including area code: (

Former name or former address, if changed since last report:

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instructions A.2.):

Securities registered pursuant to Section 12(b) of the Act:

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Item 2.02Results of Operations and Financial Condition

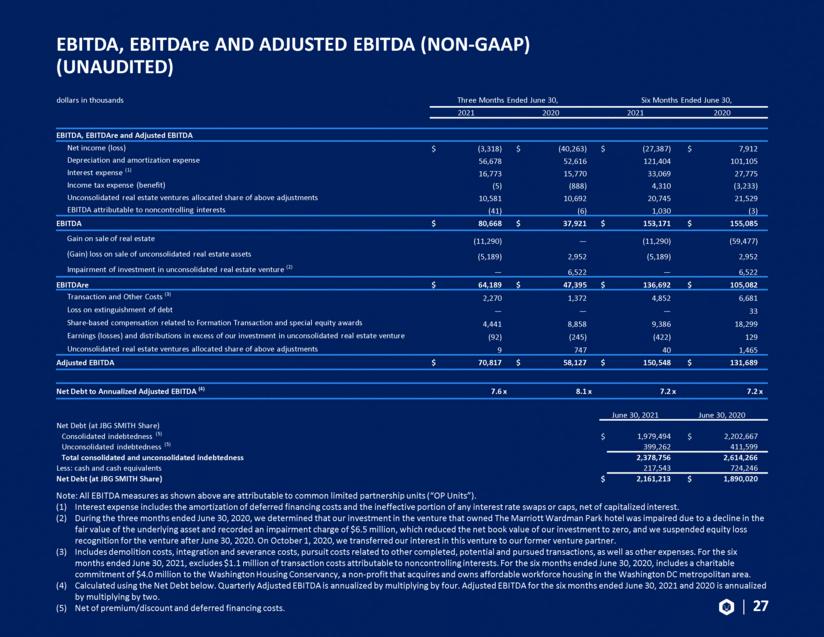

On August 3, 2021, JBG SMITH Properties (the “Company”) announced its financial results for the three and six months ended June 30, 2021. The Company also released a Quarterly Investor Package, which contains a letter to shareholders, the earnings press release and supplemental information. A copy of the Quarterly Investor Package is furnished as Exhibit 99.1 to this Current Report on Form 8-K.

Item 7.01Regulation FD Disclosure

On August 3, 2021, the Company posted an investor presentation to its website at www.jbgsmith.com on the “Investor Relations” page. A copy of the investor presentation is furnished as Exhibit 99.2 to this Current Report on Form 8-K and is incorporated herein solely for purposes of this Item 7.01 disclosure.

The information contained in this Current Report on Form 8-K, including Exhibit 99.1 and Exhibit 99.2, shall not be deemed “filed” with the Securities and Exchange Commission for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), or otherwise subject to liabilities of that section, nor incorporated by reference into any filing of the Company under the Securities Act of 1933, as amended, or the Exchange Act.

Item 9.01Financial Statements and Exhibits

(d) Exhibits

99.1 Quarterly Investor Package for the quarter ended June 30, 2021.

99.2JBG SMITH Properties Investor Presentation.

104 | Cover Page Interactive Data File (the cover page XBRL tags are embedded in the Inline XBRL document). |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

JBG SMITH PROPERTIES | ||||

August 3, 2021 | By: | /s/ M. Moina Banerjee | ||

M. Moina Banerjee | ||||

Chief Financial Officer | ||||

(Principal Financial Officer) | ||||