UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2018

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 333-217924

PHILLIPS EDISON GROCERY CENTER REIT III, INC.

(Exact Name of Registrant as Specified in Its Charter)

Maryland | 32-0499883 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

11501 Northlake Drive Cincinnati, Ohio | 45249 |

(Address of Principal Executive Offices) | (Zip Code) |

(513) 554-1110

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large Accelerated Filer | o | Accelerated Filer | o |

Non-Accelerated Filer | o (Do not check if a smaller reporting company) | Smaller reporting company | þ |

Emerging growth company | þ | ||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. þ

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

As of July 31, 2018, there were 6,371,403 outstanding shares of Class A common stock, 758 outstanding shares of Class I common stock, and no outstanding shares of Class T common stock of the Registrant.

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

-1

w PART I. FINANCIAL INFORMATION |

ITEM 1. FINANCIAL STATEMENTS

PHILLIPS EDISON GROCERY CENTER REIT III, INC.

CONSOLIDATED BALANCE SHEETS

AS OF JUNE 30, 2018 AND DECEMBER 31, 2017

(Unaudited)

(In thousands, except per share amounts)

June 30, 2018 | December 31, 2017 | ||||||

ASSETS | |||||||

Investment in real estate: | |||||||

Land and improvements | $ | 17,063 | $ | 12,122 | |||

Building and improvements | 32,307 | 25,439 | |||||

Acquired in-place lease assets | 6,319 | 4,686 | |||||

Acquired above-market lease assets | 1,860 | 1,779 | |||||

Total investment in real estate assets | 57,549 | 44,026 | |||||

Accumulated depreciation and amortization | (2,018 | ) | (684 | ) | |||

Total investment in real estate assets, net | 55,531 | 43,342 | |||||

Cash and cash equivalents | 479 | 2,659 | |||||

Deferred financing expense, net of accumulated amortization of $717 and $448, respectively | 1,433 | 1,702 | |||||

Other assets, net | 1,065 | 973 | |||||

Total assets | $ | 58,508 | $ | 48,676 | |||

LIABILITIES AND EQUITY | |||||||

Liabilities: | |||||||

Debt obligation | $ | 7,000 | $ | 9,000 | |||

Acquired below-market lease liabilities, net | 2,342 | 2,314 | |||||

Accounts payable – affiliates | 4,066 | 2,157 | |||||

Accounts payable and other liabilities | 2,201 | 2,157 | |||||

Total liabilities | 15,609 | 15,628 | |||||

Commitments and contingencies (Note 6) | — | — | |||||

Equity: | |||||||

Preferred stock, $0.01 par value per share, 10,000 shares authorized, and none | |||||||

issued and outstanding at June 30, 2018 and December 31, 2017 | — | — | |||||

Common stock - Class A, $0.01 par value per share, 75,000 and 1,000,000 shares authorized, 6,358 | |||||||

and 4,502 shares issued and outstanding, at June 30, 2018 and December 31, 2017, respectively | 64 | 45 | |||||

Common stock - Class T, $0.01 par value per share, 750,000 and zero shares authorized at | |||||||

June 30, 2018 and December 31, 2017, respectively, and none issued and outstanding | — | — | |||||

Common stock - Class I, $0.01 par value per share, 75,000 and zero shares authorized, 1 and zero | |||||||

shares issued and outstanding, at June 30, 2018 and December 31, 2017, respectively | — | — | |||||

Stock dividends to be distributed | — | 644 | |||||

Additional paid-in capital | 53,760 | 38,836 | |||||

Accumulated deficit | (10,925 | ) | (6,477 | ) | |||

Total equity | 42,899 | 33,048 | |||||

Total liabilities and equity | $ | 58,508 | $ | 48,676 | |||

See notes to consolidated financial statements.

-2

PHILLIPS EDISON GROCERY CENTER REIT III, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2018 AND 2017

(Unaudited)

(In thousands, except per share amounts)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | ||||||||||||

Revenues: | |||||||||||||||

Rental income | $ | 1,116 | $ | 269 | $ | 2,072 | $ | 540 | |||||||

Tenant recovery income | 510 | 79 | 920 | 171 | |||||||||||

Other property income | 7 | 1 | 14 | 3 | |||||||||||

Total revenues | 1,633 | 349 | 3,006 | 714 | |||||||||||

Expenses: | |||||||||||||||

Property operating | 243 | 42 | 471 | 104 | |||||||||||

Real estate taxes | 391 | 48 | 714 | 96 | |||||||||||

General and administrative | 624 | 220 | 947 | 441 | |||||||||||

Depreciation and amortization | 661 | 147 | 1,267 | 295 | |||||||||||

Total expenses | 1,919 | 457 | 3,399 | 936 | |||||||||||

Other: | |||||||||||||||

Interest expense | (351 | ) | (387 | ) | (695 | ) | (518 | ) | |||||||

Other expense, net | (82 | ) | — | (88 | ) | — | |||||||||

Net loss | $ | (719 | ) | $ | (495 | ) | $ | (1,176 | ) | $ | (740 | ) | |||

Earnings per common share: | |||||||||||||||

Loss per share - basic and diluted | $ | (0.11 | ) | $ | (0.45 | ) | $ | (0.20 | ) | $ | (0.90 | ) | |||

Weighted-average common shares outstanding: | |||||||||||||||

Basic and diluted | 6,344 | 1,102 | 5,951 | 825 | |||||||||||

See notes to consolidated financial statements.

-3

PHILLIPS EDISON GROCERY CENTER REIT III, INC.

CONSOLIDATED STATEMENTS OF EQUITY

FOR THE SIX MONTHS ENDED JUNE 30, 2018 and 2017

(Unaudited)

(In thousands, except per share amounts)

Common Stock Par Value | Additional Paid-in Capital | Stock Dividend to be Distributed | Accumulated Deficit | Total Equity | |||||||||||||||||||||||

Class A | Class T | Class I | |||||||||||||||||||||||||

Balance at January 1, 2017 | $ | 4 | $ | — | $ | — | $ | 3,911 | $ | 56 | $ | (226 | ) | $ | 3,745 | ||||||||||||

Issuance of common stock | 11 | — | — | 10,901 | (56 | ) | — | 10,856 | |||||||||||||||||||

Distribution Reinvestment Plan (“DRIP”) | — | — | — | 54 | — | — | 54 | ||||||||||||||||||||

Common distributions declared, $0.30 per share | — | — | — | — | — | (247 | ) | (247 | ) | ||||||||||||||||||

Stock dividends declared, 0.0887 shares per share | 1 | — | — | 517 | 207 | (725 | ) | — | |||||||||||||||||||

Offering costs | — | — | — | (2,863 | ) | — | — | (2,863 | ) | ||||||||||||||||||

Net loss | — | — | — | — | — | (740 | ) | (740 | ) | ||||||||||||||||||

Balance at June 30, 2017 | $ | 16 | $ | — | $ | — | $ | 12,520 | $ | 207 | $ | (1,938 | ) | $ | 10,805 | ||||||||||||

Balance at January 1, 2018 | $ | 45 | $ | — | $ | — | $ | 38,836 | $ | 644 | $ | (6,477 | ) | $ | 33,048 | ||||||||||||

Issuance of common stock | 16 | — | — | 16,206 | (644 | ) | — | 15,578 | |||||||||||||||||||

DRIP | 1 | — | — | 707 | — | — | 708 | ||||||||||||||||||||

Common distributions declared, $0.30 per share | — | — | — | — | — | (1,771 | ) | (1,771 | ) | ||||||||||||||||||

Stock dividends declared, 0.0289 shares per share | 2 | — | — | 1,499 | — | (1,501 | ) | — | |||||||||||||||||||

Offering costs | — | — | — | (3,488 | ) | — | — | (3,488 | ) | ||||||||||||||||||

Net loss | — | — | — | — | — | (1,176 | ) | (1,176 | ) | ||||||||||||||||||

Balance at June 30, 2018 | $ | 64 | $ | — | $ | — | $ | 53,760 | $ | — | $ | (10,925 | ) | $ | 42,899 | ||||||||||||

See notes to consolidated financial statements.

-4

PHILLIPS EDISON GROCERY CENTER REIT III, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE SIX MONTHS ENDED JUNE 30, 2018 AND 2017

(Unaudited)

(In thousands)

2018 | 2017 | ||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||

Net loss | $ | (1,176 | ) | $ | (740 | ) | |

Adjustments to reconcile net loss to net cash provided by operating activities: | |||||||

Depreciation and amortization | 1,269 | 295 | |||||

Net amortization of above- and below-market leases | 3 | (17 | ) | ||||

Amortization of deferred financing expense | 269 | 181 | |||||

Straight-line rental income | (92 | ) | (10 | ) | |||

Changes in operating assets and liabilities: | |||||||

Accounts receivable, net | 281 | (182 | ) | ||||

Other assets | (385 | ) | (28 | ) | |||

Accounts payable and other liabilities | 222 | 352 | |||||

Accounts payable - affiliates | 7 | 306 | |||||

Net cash provided by operating activities | 398 | 157 | |||||

CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||

Real estate acquisitions | (13,345 | ) | — | ||||

Capital expenditures | (260 | ) | — | ||||

Net cash used in investing activities | (13,605 | ) | — | ||||

CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||

Net change in credit facility borrowings | (2,000 | ) | — | ||||

Payments of deferred financing expenses | — | (2,173 | ) | ||||

Distributions paid, net of DRIP | (964 | ) | (144 | ) | |||

Payment of offering costs | (1,587 | ) | (926 | ) | |||

Proceeds from issuance of common stock | 15,578 | 10,856 | |||||

Net cash provided by financing activities | 11,027 | 7,613 | |||||

NET (DECREASE) INCREASE IN CASH, CASH EQUIVALENTS, AND RESTRICTED CASH | (2,180 | ) | 7,770 | ||||

CASH, CASH EQUIVALENTS, AND RESTRICTED CASH: | |||||||

Beginning of period | 2,659 | 790 | |||||

End of period | $ | 479 | $ | 8,560 | |||

SUPPLEMENTAL CASH FLOW DISCLOSURE, INCLUDING NON-CASH INVESTING AND FINANCING ACTIVITIES: | |||||||

Cash paid for interest | $ | 420 | $ | 7 | |||

Accrued capital expenditures and acquisition costs | 48 | 147 | |||||

Change in offering costs payable | 1,902 | 1,898 | |||||

Change in distributions payable | 99 | 49 | |||||

Stock dividends distributed | 1,501 | 725 | |||||

Distributions reinvested | 708 | 54 | |||||

See notes to consolidated financial statements.

-5

Phillips Edison Grocery Center REIT III, Inc.

Notes to Consolidated Financial Statements

(Dollars and shares in thousands)

1. ORGANIZATION |

Phillips Edison Grocery Center REIT III, Inc. (“we,” the “Company,” “our,” or “us”) was formed as a Maryland corporation on April 15, 2016. Substantially all of our business is conducted through Phillips Edison Grocery Center Operating Partnership III, L.P. (“Operating Partnership”), a Delaware limited partnership formed on July 29, 2016. We are a limited partner of the Operating Partnership, and our wholly owned subsidiary, Phillips Edison Grocery Center OP GP III LLC, is the sole general partner of the Operating Partnership.

We completed a private placement offering of shares of Class A common stock on a “reasonable best efforts” basis to accredited investors and ceased offering Class A shares in the private offering during the first quarter of 2018. During the private placement offering, we raised $57,683 in gross offering proceeds from the issuance of 5,859 Class A shares, inclusive of the DRIP.

Pursuant to our Registration Statement on Form S-11 (SEC Registration No. 333-217924), as amended (“Registration Statement”), declared effective on May 8, 2018, we are offering to the public (“Public Offering”) $1,500,000 in shares of common stock in the primary offering, consisting of two classes of shares: Class T and Class I, at purchase prices of $10.42 per share and $10.00 per share, respectively, with discounts available to some categories of investors with respect to Class T shares (“Primary Offering”). In addition, we are also offering $200,000 in Class A, Class T, and Class I shares of our common stock pursuant to the DRIP at a price of $9.80 per share. For more detail on the DRIP, see Note 7. We are offering any combination of Class T and Class I shares in the Primary Offering and any combination of Class A, Class T, and Class I shares through the DRIP. We reserve the right to reallocate shares between the Primary Offering and the DRIP. We have retained Griffin Capital Securities, LLC (“Dealer Manager”) to serve as the dealer manager of the Public Offering, which commenced May 8, 2018. The Dealer Manager is responsible for marketing our shares in the Public Offering. As of June 30, 2018, we had raised $8 in gross offering proceeds from the issuance of Class I shares, inclusive of the DRIP, as well as $136 in gross offering proceeds from the issuance of Class A shares pursuant to the DRIP. Through June 30, 2018, there have been no sales of Class T shares to report.

Our property managers are owned by Phillips Edison & Company, Inc. and its subsidiaries (“PECO” or “Manager”). Our advisor is PECO-Griffin REIT Advisor, LLC (“Advisor”), a limited liability company that was formed in the state of Delaware on May 23, 2016, and is jointly owned by PECO and Griffin Capital Corporation (“Griffin sponsor”). We have entered into an Amended and Restated Advisory Agreement (“Advisory Agreement”), which makes the Advisor ultimately responsible for the management of our day-to-day activities and the implementation of our investment strategy.

We intend to invest primarily in well-occupied, grocery-anchored neighborhood and community shopping centers leased to a mix of national and regional creditworthy retailers selling necessity-based goods and services in strong demographic markets throughout the United States. In addition, we may invest in other retail properties including power and lifestyle shopping centers, multi-tenant shopping centers, free-standing single-tenant retail properties, and other real estate and real estate-related loans and securities depending on real estate market conditions and investment opportunities that we determine are in the best interests of our stockholders.

As of June 30, 2018, we owned fee simple interests in four grocery-anchored shopping centers acquired from third parties unaffiliated with us or our Advisor.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

Basis of Presentation and Principles of Consolidation—The accompanying consolidated financial statements have been prepared pursuant to accounting principles generally accepted in the United States of America (“GAAP”). The consolidated financial statements include our accounts and the accounts of our consolidated subsidiaries (over which we exercise financial and operating control). All intercompany balances and transactions are eliminated upon consolidation.

Partially-Owned Entities—If we determine that we are an owner in a variable-interest entity (“VIE”), and we hold a controlling financial interest, then we will consolidate the entity as the primary beneficiary. For a partially-owned entity determined not to be a VIE, we analyze rights held by each partner to determine which would be the consolidating party. We will generally consolidate entities (in the absence of other factors when determining control) when we have over a 50% ownership interest in the entity. We will assess our interests in VIEs on an ongoing basis to determine whether or not we are the primary beneficiary. However, we will also evaluate who controls the entity even in circumstances in which we have greater than a 50% ownership interest. If we do not control the entity due to the lack of decision-making abilities, we will not consolidate the entity. We have determined that the Operating Partnership is considered a VIE. We are the primary beneficiary of the VIE, and our partnership interest is considered a majority voting interest. As such, we have consolidated the Operating Partnership and its subsidiaries.

Use of Estimates—The preparation of the consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the consolidated financial statements, and the reported amounts of revenues and expenses during the reporting periods. For example, significant estimates and assumptions have been made with respect to the useful lives of assets; recoverable amounts of receivables; initial valuations of tangible and intangible assets and liabilities and

-6

related amortization periods of deferred costs and intangibles, particularly with respect to property acquisitions; and other fair value measurement assessments required for the preparation of the consolidated financial statements. Actual results could differ from those estimates.

Cash and Cash Equivalents—We consider all highly liquid investments purchased with an original maturity of three months or less to be cash equivalents. Cash equivalents may include cash and short-term investments. Short-term investments are stated at cost, which approximates fair value and may consist of investments in money market accounts. The cash and cash equivalent balances at one or more of our financial institutions exceeds the Federal Depository Insurance Corporation insurance coverage.

Investment in Property and Lease Intangibles—Real estate assets are stated at cost less accumulated depreciation. Depreciation is computed using the straight-line method. The estimated useful lives for computing depreciation are generally not to exceed 5-7 years for furniture, fixtures and equipment, 15 years for land improvements, and 30 years for buildings and building improvements. Tenant improvements are amortized over the shorter of the respective lease term or the expected useful life of the asset. Major replacements that extend the useful lives of the assets are capitalized, and maintenance and repair costs are expensed as incurred.

Real estate assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of the individual property may not be recoverable. In such an event, a comparison will be made of the projected operating cash flows of each property on an undiscounted basis to the carrying amount of such property. If deemed unrecoverable on an undiscounted basis, such carrying amount would be adjusted, if necessary, to estimated fair values to reflect impairment in the value of the asset. We recorded no impairments as of June 30, 2018 and December 31, 2017.

The results of operations of acquired properties are included in our results of operations from their respective dates of acquisition. The acquisition-date fair values of all tangible assets, identifiable intangibles, and assumed liabilities are assessed using methods (e.g., discounted cash flow analysis and replacement cost) that utilize appropriate discount and/or capitalization rates and available market information. Estimates of future cash flows are based on a number of factors including historical operating results, known and anticipated trends, and market and economic conditions. The fair value of tangible assets of an acquired property considers the value of the property as if it were vacant. Most acquisition-related costs are capitalized and allocated to the tangible and identifiable intangible assets based on their respective acquisition-date fair values, and amortized over the same useful lives of the respective tangible and identifiable intangible assets.

The fair values of buildings and improvements are determined on an as-if-vacant basis. The estimated fair value of acquired in-place leases is the cost we would have incurred to lease the properties to the occupancy level of the properties at the date of acquisition. Such estimates include leasing commissions, legal costs, and other direct costs that would be incurred to lease the properties to such occupancy levels. Additionally, we evaluate the time period over which such occupancy levels would be achieved. Such evaluation includes an estimate of the net market-based rental revenues, net operating costs (primarily consisting of real estate taxes, insurance and utilities), and capital expenditures that would be incurred during the lease-up period. Acquired in-place leases as of the date of acquisition are amortized over the weighted-average remaining lease terms.

Acquired above- and below-market lease values are recorded based on the present value (using discount rates that reflect the risks associated with the leases acquired) of the difference between the contractual amounts to be paid pursuant to the in-place leases and management’s estimate of the market lease rates for the corresponding in-place leases. The capitalized above- and below-market lease values are amortized as adjustments to rental income over the remaining terms of the respective leases. We also consider fixed rate renewal options in our calculation of the fair value of below-market leases and the periods over which such leases are amortized. If a tenant has a unilateral option to renew a below-market lease and we determine that the tenant has a financial incentive to exercise such option, we include such an option in the calculation of the fair value of such lease and the period over which the lease is amortized.

We estimate the value of tenant origination and absorption costs by considering the estimated carrying costs during hypothetical expected lease-up periods, considering current market conditions. In estimating carrying costs, management includes real estate taxes, insurance and other operating expenses and estimates of lost rentals at market rates during the expected lease-up periods.

We estimate the fair value of assumed mortgage notes payable based upon indications of then-current market pricing for similar types of debt with similar maturities. Assumed mortgage notes payable are initially recorded at their estimated fair value as of the assumption date, and the difference between such estimated fair value and the note’s outstanding principal balance is amortized over the life of the mortgage note payable as an adjustment to interest expense.

Deferred Financing Expenses—Deferred financing expenses are capitalized and amortized on a straight-line basis over the term of the related financing arrangement, which approximates the effective interest method. Deferred financing costs related to term loan facilities and mortgages will be recorded in Debt Obligation, while deferred financing costs related to our revolving credit facility are recorded in Deferred Financing Expense, Net, on our consolidated balance sheets.

Other Assets, Net—Other Assets, Net on our consolidated balance sheets consists primarily of accounts receivable, prepaid expenses, and deferred rent receivable. Prepaid expenses and deferred rent receivable are amortized using the straight-line method over the terms of the respective agreements.

Fair Value Measurement—Accounting Standards Codification (“ASC”) 820, Fair Value Measurement (“ASC 820”) defines fair value, establishes a framework for measuring fair value in accordance with GAAP and expands disclosures about fair value measurements. ASC 820 emphasizes that fair value is intended to be a market-based measurement, as opposed to a transaction-specific measurement. Fair value is defined by ASC 820 as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Depending on the nature of the asset or liability, various techniques and assumptions can be used to estimate the fair value. Assets and liabilities are measured using inputs from three levels of the fair value hierarchy, as follows:

-7

Level 1—Inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that we have the ability to access at the measurement date. An active market is defined as a market in which transactions for the assets or liabilities occur with sufficient frequency and volume to provide pricing information on an ongoing basis.

Level 2—Inputs include quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active (markets with few transactions), inputs other than quoted prices that are observable for the asset or liability (i.e., interest rates, yield curves, etc.), and inputs that are derived principally from or corroborated by observable market data correlation or other means (market corroborated inputs).

Level 3—Unobservable inputs, only used to the extent that observable inputs are not available, reflect our assumptions about the pricing of an asset or liability.

Considerable judgment is necessary to develop estimated fair values of financial and non-financial assets and liabilities. Accordingly, the estimates presented herein are not necessarily indicative of the amounts we did or could actually realize upon disposition of the financial assets and liabilities previously sold or currently held.

The following describes the methods we use to estimate the fair value of our financial and non-financial assets and liabilities:

Cash and Cash Equivalents, Accounts Receivable, and Accounts Payable—We consider the carrying values of these financial instruments to approximate fair value because of the short period of time between origination of the instruments and their expected realization.

Real Estate Investments—The purchase prices of the investment properties, including related lease intangible assets and liabilities, were allocated at estimated fair value based on Level 3 inputs, such as discount rates, capitalization rates, comparable sales, replacement costs, income and expense growth rates, and current market rents and allowances as determined by management.

Debt Obligation—We estimate the fair value of our debt by discounting the future cash flows of each instrument at rates currently offered for similar debt instruments of comparable maturities by our lenders using Level 3 inputs. The discount rate used approximates current lending rates for loans or groups of loans with similar maturities and credit quality, assuming the debt is outstanding through maturity and considering the debt’s collateral (if applicable). We have utilized market information, as available, or present value techniques to estimate the amounts required to be disclosed.

Repurchases of Common Stock—We offer a share repurchase program (“SRP”) which may provide a limited opportunity for stockholders to have their shares repurchased subject to approval and certain limitations and restrictions (see Note 7). We account for approved requests to repurchase shares as liabilities to be reported at settlement value.

The maximum amount of common stock that we may redeem, at the stockholder’s election, during any calendar year is limited, among other things, to 5% of the weighted-average number of shares outstanding during the prior calendar year. The maximum amount is reduced each reporting period by the current year share redemptions to date. In addition, the cash available for repurchases on any particular date is generally limited to the proceeds from the DRIP during the preceding four fiscal quarters, less amounts already used for repurchases since the beginning of that period. The board of directors may, in its sole discretion, amend, suspend, or terminate the share repurchase program at any time upon 30 days’ written notice. In addition, the board of directors reserves the right, in its sole discretion, to reject any request for repurchase.

Revenue Recognition—The majority of our revenue is lease revenue from our wholly-owned properties, which is accounted for under ASC 840, Leases. We commence revenue recognition on our leases based on a number of factors. In most cases, revenue recognition under a lease begins when the lessee takes possession of or controls the physical use of the leased asset. The determination of who is the owner, for accounting purposes, of the tenant improvements determines the nature of the leased asset and when revenue recognition under a lease begins. If we are the owner, for accounting purposes, of the tenant improvements, then the leased asset is the finished space, and revenue recognition begins when the lessee takes possession of the finished space, typically when the improvements are substantially complete.

If we conclude that we are not the owner, for accounting purposes, of the tenant improvements (the lessee is the owner), then the leased asset is the unimproved space and any tenant allowances funded under the lease are treated as lease incentives, which reduce revenue recognized over the term of the lease. In these circumstances, we begin revenue recognition when the lessee takes possession of the unimproved space to construct their own improvements. We consider a number of different factors in evaluating whether we or the lessee is the owner of the tenant improvements for accounting purposes. These factors include:

• | whether the lease stipulates how and on what a tenant improvement allowance may be spent; |

• | whether the tenant or landlord retains legal title to the improvements; |

• | the uniqueness of the improvements; |

• | the expected economic life of the tenant improvements relative to the length of the lease; and |

• | who constructs or directs the construction of the improvements. |

We recognize rental income on a straight-line basis over the term of each lease that includes periodic and determinable adjustments to rent. The difference between rental income earned on a straight-line basis and the cash rent due under the provisions of the lease agreements is recorded as deferred rent receivable and is included as a component of other assets. Due to the impact of the straight-line adjustments, rental income generally will be greater than the cash collected in the early years and will be less than the cash collected in the later years of a lease. For percentage rental income, we defer recognition of contingent rental income until the specified target (i.e. breakpoint) that triggers the contingent rental income is achieved.

Reimbursements from tenants for recoverable real estate tax and operating expenses are accrued as revenue in the period in which the applicable expenses are incurred. We make certain assumptions and judgments in estimating the reimbursements

-8

at the end of each reporting period. We do not expect the actual results to materially differ from the estimated reimbursements.

We periodically review the collectability of outstanding receivables. Allowances will be taken for those balances that we deem to be uncollectible, including any amounts relating to straight-line rent receivables and/or receivables for recoverable expenses.

We record lease termination income if there is a signed termination agreement, all of the conditions of the agreement have been met, collectability is reasonably assured and the tenant is no longer occupying the property. Upon early lease termination, we provide for losses related to unrecovered tenant-specific intangibles and other assets.

Effective January 1, 2018, we adopted the guidance of ASC 610-20, Other Income - Gains and Losses from the Derecognition of Nonfinancial Assets (“ASC 610-20”), which applies to sales or transfers to non-customers of non-financial assets, or in substance, nonfinancial assets that do not meet the definition of a business. Generally, our sales of real estate would be considered a sale of a non-financial asset as defined by ASC 610-20.

ASC 610-20 refers to the revenue recognition principles under Accounting Standards Update (“ASU”) 2014-09, Revenue from Contracts with Customers (Topic 606) (“ASU 2014-09”). Under ASC 610-20, if we determine we do not have a controlling financial interest in the entity that holds the asset and the arrangement meets the criteria to be accounted for as a contract, we would de-recognize the asset and recognize a gain or loss on the sale of the real estate when control of the underlying asset transfers to the buyer.

Income Taxes—We intend to make an election to be taxed as a real estate investment trust (“REIT”) under the Internal Revenue Code of 1986, as amended (the “Code”), beginning with the taxable year ended December 31, 2017. Our qualification and taxation as a REIT depends on our ability, on a continuing basis, to meet certain organizational and operational qualification requirements imposed upon REITs by the Code. If we fail to qualify as a REIT for any reason in a taxable year, we will be subject to tax on our taxable income at regular corporate rates. We would not be able to deduct distributions paid to stockholders in any year in which we fail to qualify as a REIT. We will also be disqualified for the four taxable years following the year during which qualification was lost unless we are entitled to relief under specific statutory provisions. Additionally, GAAP prescribes a recognition threshold and measurement attribute for the financial statement recognition of a tax position taken, or expected to be taken, in a tax return. A tax position may only be recognized in the consolidated financial statements if it is more likely than not that the tax position will be sustained upon examination. We believe it is more likely than not that our tax positions will be sustained in any tax examinations.

Notwithstanding our qualification as a REIT, we may be subject to certain state and local taxes on our income or properties. In addition, our consolidated financial statements include the operations of one wholly owned subsidiary that has jointly elected to be treated as a Taxable REIT Subsidiary (“TRS”) and is subject to U.S. federal, state and local income taxes at regular corporate tax rates.

We are continuing to evaluate the impact of the 2017 Tax Cuts and Jobs Act on the organization as a whole. We do not expect the impact of the Act to have a material impact on the consolidated financial statements.

Organizational and Offering Costs—The Advisor has paid and will pay organizational and offering expenses on our behalf. Pursuant to the terms of our current advisory agreement with the Advisor, we will generally reimburse the Advisor for these costs and future offering costs it or any of its affiliates may incur on our behalf in connection with the private placement of our Class A shares and Public Offering of Class T and Class I shares. Organizational and offering expenses consist of all expenses (other than selling commissions and dealer manager fees) to be paid by us in connection with the offering, including our legal, accounting, printing, mailing, filing and registration fees, and other accountable offering expenses including (a) legal, tax, accounting and escrow fees, (b) expenses for printing, engraving, amending, supplementing and mailing, (c) distribution costs, (d) compensation to employees of the Advisor while engaged in registering, marketing and wholesaling our common stock or providing administrative services relating thereto, (e) telegraph and telephone costs, (f) all advertising and marketing expenses (including the costs related to investor and broker-dealer sales meetings), (g) charges of transfer agents, registrars, trustees, escrow holders, depositories, and experts, (h) fees, expenses and taxes related to the filing, registration and qualification of the sale of our common stock under federal and state laws, including accountants’ and attorneys’ fees and other accountable offering expenses, (i) amounts to reimburse the Advisor for all marketing related costs and expenses such as compensation to and direct expenses of the Advisor’s employees or employees of the Advisor’s affiliates in connection with registering and marketing our common stock, (j) travel and entertainment expenses related to the offering and marketing of our common stock, (k) facilities and technology costs and other costs and expenses associated with the offering and ownership of our common stock and to facilitate the marketing of our common stock, including web site design and management, (l) costs and expenses of conducting training and educational conferences and seminars, (m) costs and expenses of attending broker-dealer sponsored retail seminars or conferences, and (n) payment or reimbursement of bona fide due diligence expenses, including compensation to employees while engaged in the provision or support of bona fide due diligence services.

All organizational and offering costs incurred in connection with the private placement had been billed to us by the Advisor as of June 30, 2018 and December 31, 2017. In connection with the Public Offering, the Advisor will pay organizational and offering expenses up to 1% of gross offering proceeds from the Primary Offering, which the Advisor intends to recoup through the receipt of a contingent advisor payment (see Note 8). We will reimburse the Advisor for any amounts in excess of 1% up to a maximum of 3.5% of gross offering proceeds from the Primary Offering.

Organizational and offering costs that have been billed to us by the Advisor as of June 30, 2018 and December 31, 2017, are recorded in Accounts Payable - Affiliates on the consolidated balance sheets. Whether additional organizational and offering costs will be billed to us is at the discretion of the Advisor and will likely depend on the success of our Public Offering. We will evaluate organizational and offering costs incurred by the Advisor at the end of each period to determine if the amounts incurred represent a liability to us based on the applicable facts and circumstances.

-9

When recognized by us, organizational expenses will be expensed as incurred, and offering costs will be recorded as a reduction to stockholders’ equity as such amounts will be reimbursed to the Advisor or its affiliates from the gross proceeds of the Public Offering.

Earnings Per Share—Earnings per share is calculated based on the weighted-average number of common shares outstanding during each period. All classes of common stock are allocated net income (loss) at the same rate per share and receive the same distributions per share. Diluted earnings per share considers the effect of any potentially dilutive share equivalents, of which we had none for the three and six months ended June 30, 2018 and 2017.

Segment Reporting—We internally evaluate the operating performance of our portfolio of properties and currently do not differentiate properties by geography, size, or type. As operating performance is reviewed at a portfolio level rather than at a property level, our entire portfolio of properties is considered one operating segment. Accordingly, we did not report any other segment disclosures for the three and six months ended June 30, 2018.

Impact of Recently Issued Accounting Pronouncements—The following table provides a brief description of newly adopted accounting pronouncements and their effect on our consolidated financial statements:

Standard | Description | Date of Adoption | Effect on the Financial Statements or Other Significant Matters | |||

ASU 2017-05, Other Income - Gains and Losses from the Derecognition of Nonfinancial Assets (Sub-topic 610-20) | This update amends existing guidance in order to provide consistency in accounting for the derecognition of a business or non-profit activity. | January 1, 2018 | We did not record any cumulative adjustment in connection with the adoption of the new pronouncement as we determined that these changes did not have any impact on our consolidated financial statements. | |||

ASU 2016-15, Statement of Cash Flows (Topic 230); ASU 2016-18, Statement of Cash Flows (Topic 230) | These updates address the presentation of eight specific cash receipts and cash payments on the statement of cash flows as well as clarify the classification and presentation of restricted cash on the statement of cash flows. | January 1, 2018 | As we have no restricted cash, there was no impact on our consolidated statement of cash flows for all periods presented. | |||

ASU 2014-09, Revenue from Contracts with Customers (Topic 606) | This update outlines a comprehensive model for entities to use in accounting for revenue arising from contracts with customers. ASU 2014-09 states that “an entity recognizes revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.” While ASU 2014-09 specifically references contracts with customers, it also applies to certain other transactions such as the sale of real estate or equipment. Expanded quantitative and qualitative disclosures are also required for contracts subject to ASU 2014-09. | January 1, 2018 | The majority of our revenue is lease revenue from our wholly-owned properties. We record these amounts as Rental Income and Tenant Recovery Income on the consolidated statements of operations. These revenue amounts are excluded from the scope of ASU 2014-09. As a result, the adoption of ASU 2014-09 did not result in any adjusting entries to prior periods as our revenue recognition related to these revenues aligned with the updated guidance. | |||

-10

The following table provides a brief description of recent accounting pronouncements that could have a material effect on our consolidated financial statements:

Standard | Description | Date of Adoption | Effect on the Consolidated Financial Statements or Other Significant Matters | |||

ASU 2016-13, Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments | The amendments in this update replace the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. This update is effective for public entities in fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. Early adoption is permitted after December 15, 2018. | January 1, 2020 | We are currently evaluating the impact the adoption of this standard will have on our consolidated financial statements. | |||

ASU 2016-02, Leases (Topic 842); ASU 2018-01, Leases (Topic 842): Land Easement Practical Expedient for Transition to Topic 842; ASU 2018-10, Codification Improvements to Topic 842, Leases; and ASU 2018-11, Leases (Topic 842): Targeted Improvements | These updates amend existing guidance by recognizing lease assets and lease liabilities on the balance sheet and disclosing key information about leasing arrangements. Early adoption is permitted as of the original effective date. | January 1, 2019 | We are currently evaluating the impact the adoption of these standards will have on our consolidated financial statements. We have identified areas within our accounting policies we believe could be impacted by the new standard. This standard impacts the lessor’s ability to capitalize certain costs related to leasing, which will result in a reduction in the amount of execution costs currently being capitalized in connection with leasing activities and an increase to our Property Operating expenses. The standard will also require new disclosures within the accompanying notes to the consolidated financial statements. We expect to adopt the practical expedients available for implementation under the standard. By adopting these practical expedients, we will not be required to reassess (i) whether an expired or existing contract meets the definition of a lease; (ii) the lease classification at the adoption date for existing leases; and (iii) whether the costs previously capitalized as initial direct costs would continue to be amortized. This allows us to continue to account for our leases where we are the lessee as operating leases, however, any new or renewed leases may be classified as financing leases. We currently have an immaterial number of leases of this type. We also expect to recognize right of use assets and lease liability on our consolidated balance sheets related to certain leases where we are the lessee. In July 2018, the FASB issued an ASU related to ASC 842. The update allows lessors to use a practical expedient to account for non-lease components and related lease components as a single lease component instead of accounting for them separately, if certain conditions are met. We expect to utilize this practical expedient We will continue to evaluate the effect the adoption of these ASUs will have on our consolidated financial statements. However, we currently believe that the adoption will not have a material impact for operating leases where we are a lessor and will continue to record revenues from rental properties for our operating leases on a straight-line basis. We are still evaluating the impact for leases where we are the lessee. | |||

-11

3. REAL ESTATE AQUISITIONS |

During the six months ended June 30, 2018, we acquired one grocery-anchored shopping center. During the six months ended June 30, 2017, we did not acquire any properties. The acquisition was classified as an asset acquisition. As such, most acquisition-related costs were capitalized and are included in the total purchase price shown below. Our real estate asset acquired during the six months ended June 30, 2018, was as follows:

Property Name | Location | Anchor Tenant | Acquisition Date | Purchase Price | Square Footage | Leased % of Rentable Square Feet at Acquisition | |||||||||

Albertville Crossing | Albertville, MN | Coborn’s | 2/21/2018 | $ | 13,156 | 99,013 | 89.7% | ||||||||

The fair value and weighted-average useful lives for in-place, above-market, and below-market lease intangibles acquired during the six months ended June 30, 2018, are as follows (useful life in years):

2018 | ||||||

Fair Value | Weighted-Average Useful Life | |||||

Acquired in-place leases | $ | 1,633 | 9 | |||

Acquired above-market leases | 81 | 7 | ||||

Acquired below-market leases | (93 | ) | 8 | |||

4. ACQUIRED INTANGIBLE LEASES |

Acquired intangible lease assets and liabilities consisted of the following amounts as of June 30, 2018 and December 31, 2017:

June 30, 2018 | December 31, 2017 | ||||||

In-place leases | $ | 6,319 | $ | 4,686 | |||

Above-market leases | 1,860 | 1,779 | |||||

Total intangible lease assets | 8,179 | 6,465 | |||||

Accumulated amortization | (503 | ) | (124 | ) | |||

Net intangible lease assets | $ | 7,676 | $ | 6,341 | |||

Below-market liabilities | $ | 2,455 | $ | 2,362 | |||

Accumulated amortization | (113 | ) | (48 | ) | |||

Net below-market lease liabilities | $ | 2,342 | $ | 2,314 | |||

Summarized below is the amortization recorded on the intangible assets and liabilities for the periods ended June 30, 2018 and 2017:

June 30, 2018 | June 30, 2017 | ||||||

In-place leases | $ | 309 | $ | 48 | |||

Above-market leases | 70 | 3 | |||||

Below-market leases | (65 | ) | (20 | ) | |||

Estimated future amortization of the respective acquired intangible lease assets and liabilities as of June 30, 2018, for each of the next five years is as follows:

Year | In-Place Leases | Above-Market Leases | Below- Market Leases | ||||||||

Remaining 2018 | $ | 323 | $ | 71 | $ | (69 | ) | ||||

2019 | 662 | 143 | (136 | ) | |||||||

2020 | 662 | 143 | (136 | ) | |||||||

2021 | 662 | 143 | (136 | ) | |||||||

2022 | 662 | 143 | (136 | ) | |||||||

-12

5. DEBT OBLIGATION |

We have an unsecured $250 million revolving credit facility, with an interest rate spread over LIBOR based on our leverage ratio. The revolving credit facility requires interest-only payments until it matures in March 2021 and has two six-month extension options. Due to borrowing base restrictions included in the loan agreement, the borrowing capacity on the credit facility was $25.1 million and $24.0 million as of June 30, 2018 and December 31, 2017, respectively.

The interest rate on our debt approximated the market interest rate, and as such, the fair value and recorded value of our debt were both $7,000 on June 30, 2018, and $9,000 on December 31, 2017.

The following is a summary of the outstanding principal balance of our debt obligation and corresponding interest rate as of June 30, 2018 and December 31, 2017:

June 30, 2018 | December 31, 2017 | ||||||

Outstanding principal balance | $ | 7,000 | $ | 9,000 | |||

Interest rate | 4.2 | % | 3.6 | % | |||

Gross borrowings under our revolving credit facility were $26.0 million and gross payments on our revolving credit facility were $28.0 million during the six months ended June 30, 2018.

6. COMMITMENTS AND CONTINGENCIES |

Litigation—We may become involved in various claims and litigation matters arising in the ordinary course of business, some of which may involve claims for damages. Many of these matters are covered by insurance, although they may nevertheless be subject to deductibles or retentions. There are no material legal proceedings pending, or known to be contemplated, against us.

Environmental Matters—In connection with the ownership and operation of real estate, we may potentially be liable for costs and damages related to environmental matters. In addition, we may own or acquire certain properties that are subject to environmental remediation. Generally, the seller of the property, the tenant of the property, and/or another third party is responsible for environmental remediation costs related to a property. Additionally, in connection with the purchase of certain properties, the respective sellers and/or tenants may agree to indemnify us against future remediation costs. We also carry environmental liability insurance on our properties that provides limited coverage for any remediation liability and/or pollution liability for third-party bodily injury and/or property damage claims for which we may be liable. We are not aware of any environmental matters which we believe are reasonably likely to have a material effect on our consolidated financial statements.

7. EQUITY |

General—The holders of all classes of common stock are entitled to one vote per share on all matters voted on by stockholders, including election of the board of directors. Our charter does not provide for cumulative voting in the election of directors, but does permit our board of directors to create classes of common stock and to establish the rights of each class of common stock. The differences among the classes of common stock relate to upfront selling commissions, dealer manager fees, and ongoing stockholder servicing fees. See Note 8 for more detail.

Common Stock Activity—The following table summarizes our common stock outstanding as of June 30, 2018:

Common Stock | |||||||||||

Class A | Class T | Class I | Total | ||||||||

Balance at January 1, 2018 | 4,502 | — | — | 4,502 | |||||||

Common stock issued | 1,566 | — | 1 | 1,567 | |||||||

Cash distributions reinvested | 75 | — | — | 75 | |||||||

Stock dividends | 215 | — | — | 215 | |||||||

Balance at June 30, 2018 | 6,358 | — | 1 | 6,359 | |||||||

The following table summarizes our common stock outstanding as of June 30, 2017:

Common Stock | ||

Class A | ||

Balance at January 1, 2017 | 435 | |

Common stock issued | 1,099 | |

Cash distributions reinvested | 6 | |

Stock dividends | 53 | |

Balance at June 30, 2017 | 1,593 | |

-13

Distributions and Dividends—We have adopted a DRIP that allows stockholders to reinvest cash distributions in additional shares of our common stock at a price equal to $9.80 per share. Prior to the commencement of the Public Offering in May 2018, the dividend reinvestment plan price was $9.50 per share. During the private offering, our board of directors declared and issued stock dividends in the amount of 0.0004901961 shares per day per share to Class A stockholders of record during the period from December 1, 2016 through February 28, 2018. We are no longer issuing any such stock dividends to our Class A stockholders. Cash distributions are paid to stockholders of record based on the number of daily shares owned by each stockholder during the period covered by the declaration. Such distributions are issued on the first business day after the end of each month.

Share Repurchase Program—Our share repurchase program may provide a limited opportunity for stockholders to have shares of common stock repurchased, subject to certain restrictions and limitations, at a price equal to or at a discount from the purchase price paid for the shares being repurchased. The cash available for repurchases on any particular date will generally be limited to the proceeds from the DRIP during the preceding four fiscal quarters, less amounts already used for repurchases since the beginning of that period. The board of directors reserves the right, in its sole discretion, at any time and from time to time, to reject any request for repurchase or amend, suspend, or terminate the program.

8. RELATED PARTY TRANSACTIONS |

Economic Dependency—We are dependent on the Advisor, the Manager, and their respective affiliates for certain services that are essential to us, including asset acquisition and disposition decisions, asset management, operating and leasing of our properties, and other general and administrative responsibilities. PECO owns a partial interest in the Advisor and wholly owns our property managers. In the event that the Advisor, the Manager, and/or their respective affiliates are unable to provide such services, we would be required to find alternative service providers, which could result in higher costs and expenses.

Advisor—The Advisor is responsible for the management of our day-to-day activities and the implementation of our investment strategy.

Acquisition Fee—We pay the Advisor an acquisition fee related to services provided in connection with the selection and purchase or origination of real estate and real estate-related investments. The acquisition fee is equal to an amount up to 2% of the contract purchase price of each property we acquire or originate, including any debt attributable to such investments.

Contingent Advisor Payment—During the Public Offering, we will pay the Advisor an additional contingent advisor payment of 2.15% of the contract purchase price of each property or other real estate investments we acquire. The contingent advisor payment allows the Advisor to recoup the portion of the dealer manager fee and other organizational and offering expenses funded by the Advisor. Therefore, the amount of the contingent advisor payment paid upon the closing of an acquisition shall not exceed the then outstanding amounts paid by the Advisor for dealer manager fees and other organizational and offering expenses related to the Public Offering at the time of such closing. For these purposes, the amounts paid by the Advisor and considered as “outstanding” will be reduced by the amount of the contingent advisor payment previously paid.

Notwithstanding the foregoing, the contingent advisor payment holdback, which is the initial $4,500 of amounts to be paid by the Advisor to fund the dealer manager fee and other organizational and offering expenses related to the Public Offering, shall be retained by us until the termination of the Public Offering, at which time such amount shall be paid to the Advisor or its affiliates. As of June 30, 2018, the Advisor had not reached the initial $4,500 of organizational and offering expenses related to the Public Offering.

Asset Management Fee—We pay the Advisor a monthly asset management fee in connection with the ongoing management and monitoring of the performance of our investments. The asset management fee is paid monthly in an amount of one-twelfth of 1% of the cost of our assets, which is equal to the purchase price, acquisition expenses, capital expenditures, and other customarily capitalized costs, but excludes acquisition fees, as of the last day of the preceding monthly period. The Advisor may elect to receive the asset management fee in cash, units of the Operating Partnership (“OP units”), common stock, or any combination thereof. All asset management fees paid during the six months ended June 30, 2018 and 2017, were paid in cash.

Disposition Fee—We will pay the Advisor or its affiliates for substantial assistance in connection with the sale of properties or other investments a disposition fee in an amount equal to 2% of the contract sales price of each property or other investment sold. Whether the Advisor or its affiliates have provided substantial assistance to us in connection with the sale of an asset is determined by a majority vote of the board of directors, including a majority of independent directors. Substantial assistance in connection with the sale of a property includes the Advisor or its affiliates’ preparation of an investment package for the property (including a new investment analysis, rent rolls, tenant information regarding credit, a property title report, an environmental report, a list of prospective buyers, a structural report, and exhibits) or such other substantial services performed by the Advisor or its affiliates in connection with a sale. The disposition fee may be paid in addition to real estate commissions paid to non-affiliates, provided that the total disposition fee and real estate commission together do not exceed an amount equal to the lesser of (i) 6% of the contract sales price of each property sold or (ii) a competitive real estate commission rate. For the six months ended June 30, 2018 and 2017, we incurred no disposition fees as we did not sell any properties.

Acquisition Expenses—We reimburse the Advisor for direct expenses incurred, including certain personnel costs, related to sourcing, selecting, evaluating, and acquiring assets on our behalf.

Organization & Operating Costs—Under the terms of the advisory agreement, we are to reimburse the Advisor for cumulative organizational and offering costs and future organizational and offering costs they may incur on our behalf. Please refer to Note 2 for additional information on organizational and offering costs.

-14

General and Administrative Expenses—As of June 30, 2018 and December 31, 2017, we owed the Advisor $4 and $13, respectively, for general and administrative expenses paid on our behalf.

Summarized below are the fees earned by and the expenses reimbursable to the Advisor, except for unpaid general and administrative expenses, which we disclosed above, for the periods ended June 30, 2018 and 2017, and any related amounts unpaid as of June 30, 2018 and December 31, 2017:

Three Months Ended | Six Months Ended | Unpaid Amount as of | |||||||||||||||||||||

June 30, | June 30, | June 30, | December 31, | ||||||||||||||||||||

2018 | 2017 | 2018 | 2017 | 2018 | 2017 | ||||||||||||||||||

Acquisition fees(1) | $ | — | $ | — | $ | 256 | $ | — | $ | — | $ | — | |||||||||||

Acquisition expenses(1) | 45 | — | 72 | — | — | — | |||||||||||||||||

Asset management fees(2) | 135 | 36 | 257 | 73 | 45 | 72 | |||||||||||||||||

Organizational and offering costs | — | — | — | — | 3,902 | 2,000 | |||||||||||||||||

Total | $ | 180 | $ | 36 | $ | 585 | $ | 73 | $ | 3,947 | $ | 2,072 | |||||||||||

(1) | The majority of acquisition fees and expenses are capitalized and allocated to the related investment in real estate assets on the consolidated balance sheets based on the acquisition-date fair values of the respective assets and liabilities acquired. |

(2) | Asset management fees are presented as General and Administrative on the consolidated statements of operations. |

Manager—Our real property is managed and leased by the Manager. The Manager also manages real properties acquired by PECO affiliates and other third parties.

Property Management Fee—We pay to the Manager a monthly property management fee equal to 4% of the gross receipts of each property managed by the Manager.

Leasing Commissions—In addition to the property management fee, if the Manager provides leasing services with respect to a property, we will pay the Manager leasing fees in an amount equal to the leasing fees charged by unaffiliated persons rendering comparable services in the same geographic location of the applicable property.

Construction Management and Development Fees—If we engage the Manager to provide construction management or development services with respect to a particular property, we will pay a construction management fee or a development fee in an amount that is usual and customary for comparable services rendered to similar projects in the geographic market of the property.

Expenses and Reimbursements—The Manager hires, directs and establishes policies for employees who have direct responsibility for the operations of each real property it manages, which may include, but is not limited to, on-site managers and building and maintenance personnel. Certain employees of the Manager may be employed on a part-time basis and may also be employed by us or certain of our affiliates. The Manager also directs the purchase of equipment and supplies and will supervise all maintenance activity. We reimburse the costs and expenses incurred by the Manager on our behalf, including employee compensation, legal, travel and other out-of-pocket expenses that are directly related to the management of specific properties, as well as fees and expenses of third-party accountants.

Summarized below are the fees earned by and the expenses reimbursable to the Manager for the periods ended June 30, 2018 and 2017, and any related amounts unpaid as of June 30, 2018 and December 31, 2017:

Three Months Ended | Six Months Ended | Unpaid Amount as of | |||||||||||||||||||||

June 30, | June 30, | June 30, | December 31, | ||||||||||||||||||||

2018 | 2017 | 2018 | 2017 | 2018 | 2017 | ||||||||||||||||||

Property management fees(1) | $ | 70 | $ | 12 | $ | 116 | $ | 26 | $ | 17 | $ | — | |||||||||||

Leasing commissions(2) | 25 | — | 53 | 4 | 19 | — | |||||||||||||||||

Construction management fees(2) | 53 | — | 56 | — | 4 | 2 | |||||||||||||||||

Other fees and reimbursements(3) | 56 | 42 | 105 | 96 | 75 | 70 | |||||||||||||||||

Total | $ | 204 | $ | 54 | $ | 330 | $ | 126 | $ | 115 | $ | 72 | |||||||||||

(1) | The property management fees are included in Property Operating on the consolidated statements of operations. |

(2) | Leasing commissions paid for leases with terms less than one year are expensed and included in Depreciation and Amortization on the consolidated statements of operations. Leasing commissions paid for leases with terms greater than one year, and construction management fees, are capitalized and amortized over the life of the related leases or assets. |

(3) | Other fees and reimbursements are included in Property Operating and General and Administrative on the consolidated statements of operations based on the nature of the expense. |

Dealer Manager—The Dealer Manager is a Delaware limited liability company and has been a member firm of the Financial Industry Regulatory Authority, Inc. (“FINRA”) since 1995. The Dealer Manager is under common ownership with our Griffin sponsor and will provide certain sales, promotional, and marketing services in connection with the distribution of the shares of common stock offered under our offering. The following table summarizes the reimbursement rates of dealer manager fees, selling commissions, and stockholder servicing fees for Class T and Class I shares of common stock for the Primary Offering,

-15

as well as the Class A shares sold during the private offering:

T Shares | I Shares | A Shares | |||

Dealer manager fees | The fee will be up to 3% of gross offering proceeds from the Primary Offering, of which 1% of gross offering proceeds will be funded by us, with the remaining amounts funded by the Advisor. | The fee will be up to 1.5% of gross offering proceeds from the Primary Offering, all of which will be funded by the Advisor. | 3% of gross offering proceeds | ||

Selling commissions | Up to 3% of gross offering proceeds | N/A | 7% of gross offering proceeds | ||

Stockholder servicing fees | The fee will accrue daily at an annual rate of 1.0% of the most recent purchase price per share of Class T sold in the Primary Offering, up to a maximum of 4.0% in the aggregate. | N/A | N/A | ||

The following table summarizes the dealer manager fees and selling commissions for shares of common stock as of June 30, 2018 and 2017:

Three Months Ended | Six Months Ended | Unpaid Amount as of | |||||||||||||||

June 30, | June 30, | June 30, | December 31, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Dealer manager fees | — | 383 | 1,682 | 427 | — | — | |||||||||||

Selling commissions | — | 353 | (214 | ) | 588 | — | — | ||||||||||

Share Purchases by Advisor—Our Advisor has made an initial investment in us through the purchase of 22 shares of our Class A common stock. The Advisor may not sell any of these shares while serving as the Advisor. As of June 30, 2018, the Advisor owned 28 shares of our Class A common stock.

9. OPERATING LEASES |

The terms and expirations of our operating leases with our tenants vary. The lease agreements frequently contain options to extend the terms of leases and other terms and conditions as negotiated. We retain substantially all of the risks and benefits of ownership of the real estate assets leased to tenants.

Approximate future rentals to be received under non-cancelable operating leases in effect at June 30, 2018, assuming no new or renegotiated leases or option extensions on lease agreements, are as follows:

Year | Amount | ||

Remaining 2018 | $ | 2,156 | |

2019 | 4,065 | ||

2020 | 3,426 | ||

2021 | 2,568 | ||

2022 | 2,370 | ||

2023 and thereafter | 9,397 | ||

Total | $ | 23,982 | |

Our major tenants include Publix Super Markets, Coborn’s, and Albertsons Companies, which comprised 21.5%, 14.7%, and 14.2% respectively, of our aggregate annualized base rent (“ABR”) as of June 30, 2018. As a result, the tenant concentration of our portfolio makes it particularly susceptible to adverse economic developments for those tenants.

-16

10. SUBSEQUENT EVENTS |

Distributions—Cash distributions equal to a daily amount of $0.0016438356 per share of all classes of common stock outstanding were paid subsequent to June 30, 2018, to the stockholders of record from June 1, 2018 through July 31, 2018, as follows:

Distribution Period | Record Date | Date Distribution Paid | Gross Amount of Distribution Paid | Distribution Reinvested through the DRIP | Net Cash Distribution | |||||||||||

June 1, 2018 through June 30, 2018 | 6/29/2018 | 7/2/2018 | $ | 313 | $ | 132 | $ | 181 | ||||||||

July 1, 2018 through July 31, 2018 | 7/16/2018 | 8/1/2018 | 325 | 138 | 187 | |||||||||||

In August 2018, our board of directors authorized cash distributions to all classes of common stockholders of record from September 1, 2018 through November 30, 2018 in a daily amount of $0.0016438356 per share.

Acquisitions

Subsequent to June 30, 2018, we acquired the following property:

Property Name | Location | Anchor Tenant (1) | Acquisition Date | Contractual Purchase Price | Square Footage | Leased % of Rentable Square Feet at Acquisition | |||||||||

Sudbury Crossing | Sudbury, MA | TJ Maxx | 7/24/2018 | $ | 18,968 | 89,952 | 98 | % | |||||||

(1) We do not own the portion of the shopping center that contains the grocery anchor, which is Sudbury Farms (Roche Bros.).

-17

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Cautionary Note Regarding Forward-Looking Statements

Certain statements contained in this Quarterly Report on Form 10-Q of Phillips Edison Grocery Center REIT III, Inc. (“we,” the “Company,” “our,” or “us”) other than historical facts may be considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We intend for all such forward-looking statements to be covered by the applicable safe harbor provisions for forward-looking statements contained in those acts. Such statements include, in particular, statements about our plans, strategies, and prospects and are subject to certain risks and uncertainties, including known and unknown risks, which could cause actual results to differ materially from those projected or anticipated. Therefore, such statements are not intended to be a guarantee of our performance in future periods. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” or other similar words. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date this report is filed with the U.S. Securities and Exchange Commission (“SEC”). We make no representations or warranties (expressed or implied) about the accuracy of any such forward-looking statements contained in this Quarterly Report on Form 10-Q, and we do not intend to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

Any such forward-looking statements are subject to risks, uncertainties, and other factors and are based on a number of assumptions involving judgments with respect to, among other things, future economic, competitive, and market conditions, all of which are difficult or impossible to predict accurately. To the extent that our assumptions differ from actual conditions, our ability to accurately anticipate results expressed in such forward-looking statements, including our ability to generate positive cash flows from operations, make distributions to stockholders, and maintain the value of our real estate properties, may be significantly hindered. Except as required by law, we do not undertake any obligation to update or revise any forward-looking statements contained in this Form 10-Q. Important factors that could cause actual results to differ materially from the forward-looking statements are disclosed in Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

All references to “Notes” throughout the document refer to the footnotes to the consolidated financial statements in Part I, Item 1. Financial Statements.

Overview

Organization—We were formed as a Maryland corporation on April 15, 2016, and intend to elect to be taxed as a REIT for U.S. federal income tax purposes commencing with the taxable year ended December 31, 2017.

We completed a private placement offering of shares of Class A common stock on a “reasonable best efforts” basis to accredited investors. We ceased the private offering during the first quarter of 2018. Pursuant to our Registration Statement, declared effective on May 8, 2018, we are offering $1.5 million in shares of common stock in the Primary Offering, consisting of two classes of shares: Class T and Class I, at purchase prices of $10.42 per share and $10.00 per share, respectively, with discounts available to some categories of investors with respect to Class T shares. In addition, we are also offering $200 million in Class A, Class T, and Class I shares of our common stock pursuant to the DRIP at a price of $9.80 per share. The Dealer Manager is responsible for marketing our shares in the Public Offering.

We intend to invest primarily in well-occupied, grocery-anchored neighborhood and community shopping centers leased to a mix of national and regional creditworthy retailers selling necessity-based goods and services in strong demographic markets throughout the United States. In addition, we may invest in other retail properties including power and lifestyle shopping centers, multi-tenant shopping centers, free-standing single-tenant retail properties, and other real estate and real estate-related loans and securities depending on real estate market conditions and investment opportunities that we determine are in the best interests of our stockholders. As of June 30, 2018, we owned four real estate properties acquired from third parties unaffiliated with us or our Advisor.

Equity Raise Activity—As of June 30, 2018, we had issued 5.9 million shares of Class A common stock, including 0.1 million shares issued through the DRIP, generating gross cash proceeds of $57.7 million since our inception. As of June 30, 2018, we had raised approximately $8,000 in gross offering proceeds from the issuance of Class I shares, inclusive of the DRIP.

Portfolio—Below are statistical highlights of our portfolio:

Total Portfolio as of June 30, 2018 | Property Acquisitions During the Six Months Ended June 30, 2018 | ||||

Number of properties | 4 | 1 | |||

Number of states | 3 | 1 | |||

Total square feet (in thousands) | 381 | 99 | |||

Leased % of rentable square feet | 94.6 | % | 89.7 | % | |

Average remaining lease term (in years)(1) | 4.8 | 8.3 | |||

(1) | The average remaining lease term in years excludes future options to extend the term of the lease. |

-18

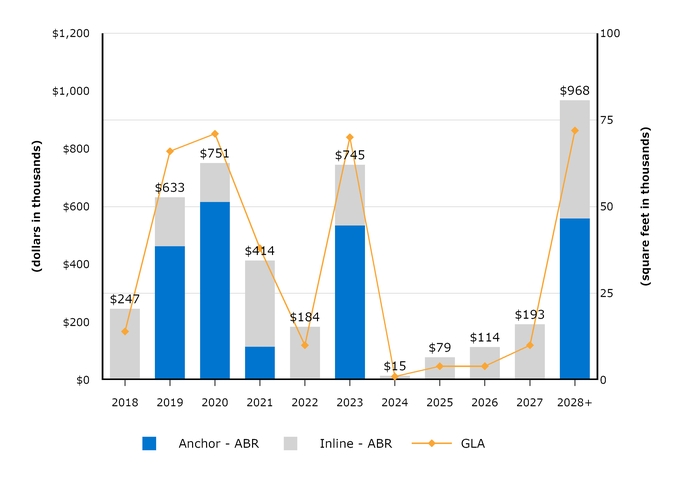

Lease Expirations—The following table lists, on an aggregate basis, all of the scheduled lease expirations after June 30, 2018, for each of the next ten years and thereafter for our four shopping centers, including month-to-month (“M2M”) leases. The chart shows the leased square feet and annual base rent (“ABR”) represented by the applicable lease expiration year (dollars and square feet are presented in thousands):

Subsequent to June 30, 2018, we renewed approximately 3,000 total square feet and $0.1 million of total ABR of the leases expiring.

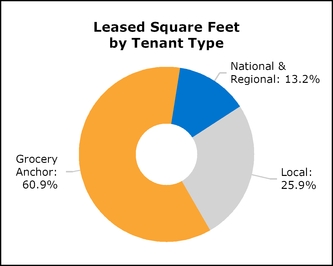

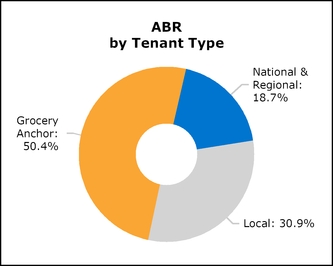

Portfolio Tenancy—Prior to the acquisition of each property, we assess the suitability of the grocery-anchor tenant and other tenants in light of our investment objectives, namely, preserving capital and providing stable cash flows for distributions. Generally, we assess the strength of the tenant by consideration of company factors, such as its financial strength and market share in the geographic area of the shopping center, as well as location-specific factors, such as the store’s sales, local competition, and demographics. When assessing the tenancy of the non-anchor space at the shopping center, we consider the tenant mix at each shopping center in light of our portfolio, the proportion of national and national franchise tenants, the creditworthiness of specific tenants, and the timing of lease expirations. When evaluating non-national tenancy, we attempt to obtain credit enhancements to leases, which typically come in the form of deposits and/or guarantees from one or more individuals.

-19

We define national tenants as those tenants that operate in at least three states. Regional tenants are defined as those

tenants that have at least three locations. The following charts present the composition of our portfolio by tenant type as of

June 30, 2018:

The following charts present the composition of our portfolio by tenant industry as of June 30, 2018:

The following table presents our grocery-anchor tenants, grouped according to parent company, by ABR as of June 30, 2018 (dollars and square feet are presented in thousands):

Tenant | ABR | % of ABR | Leased Square Feet | % of Leased Square Feet | Number of Locations(1) | ||||||||||

Publix Super Markets | $ | 932 | 21.5 | % | 99 | 27.4 | % | 2 | |||||||

Coborn's | 639 | 14.7 | % | 58 | 16.2 | % | 1 | ||||||||

Albertsons Companies | 617 | 14.2 | % | 62 | 17.3 | % | 1 | ||||||||

$ | 2,188 | 50.4 | % | 219 | 60.9 | % | 4 | ||||||||

(1) | Number of locations excludes auxiliary leases with grocery anchors such as fuel stations and liquor stores. |

Results of Operations

We owned four properties as of June 30, 2018, and one property as of June 30, 2017. Unless otherwise discussed below, year-over-year comparative differences for the three and six months ended June 30, 2018 and 2017, are almost entirely attributable to the number of properties owned and the length of ownership of these properties.

-20

Summary of Operating Activities for the Three Months Ended June 30, 2018 and 2017

Three Months Ended June 30, | Favorable (Unfavorable) Changes | ||||||||||

(dollars are presented in thousands, except per share amounts) | 2018 | 2017 | |||||||||

Total revenues | $ | 1,633 | $ | 349 | $ | 1,284 | |||||

Property operating expenses | (243 | ) | (42 | ) | (201 | ) | |||||

Real estate tax expenses | (391 | ) | (48 | ) | (343 | ) | |||||

General and administrative expenses | (624 | ) | (220 | ) | (404 | ) | |||||

Depreciation and amortization | (661 | ) | (147 | ) | (514 | ) | |||||