Exhibit 8.1

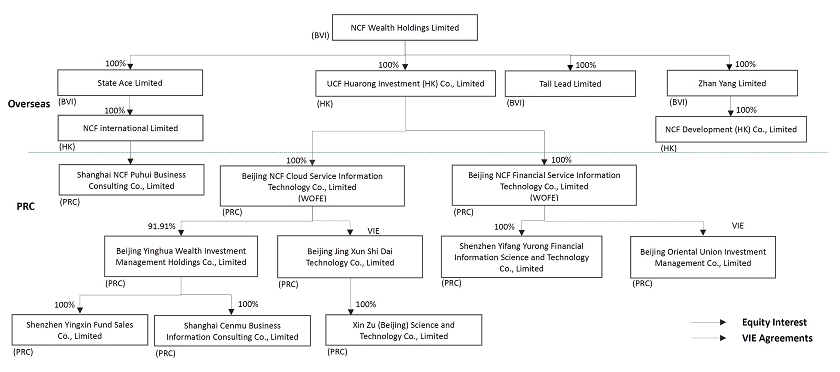

The following is a diagram of Hunter Maritime’s subsidiaries. NCF Wealth Holdings Limited is a wholly owned subsidiary of Hunter Maritime.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark one)

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended ________________. |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| for the transition period from __________ to ___________ |

OR

| x | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Date of event requiring this shell company report: March 21, 2019 |

Commission file number: 000-37947

Hunter Maritime Acquisition Corp.

________________________________

(Exact name of the Registrant as specified in its charter)

Republic of the Marshall Islands

_____________________________

(Jurisdiction of incorporation or organization)

Tower A, WangXin Building

28 Xiaoyun Rd

Chaoyang District, Beijing, 100027

___________________________

(Address of principal executive offices)

Jia Sheng

Chief Executive Officer

Tower A, WangXin Building

28 Xiaoyun Rd

Chaoyang District, Beijing, 100027

(646) 308-0546

___________________________

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of each exchange on which registered | |

| Class A Common Stock, par value $0.0001 per share | The Nasdaq Stock Market LLC | |

| Warrants to purchase one share of Class A Common Stock | The Nasdaq Stock Market LLC | |

| Units, each consisting of one share of Class A Common Stock and one half of one Warrant | The Nasdaq Stock Market LLC |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

On March 21, 2019, the registrant had 204,041,004 shares of Class A common stock outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| ¨ Yes | x No |

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

| ¨ Yes | ¨ No |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| xYes | ¨ No |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| xYes | ¨ No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer, "accelerated filer,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ¨ Large Accelerated filer | x Accelerated filer | ¨ Non-accelerated filer |

| x Emerging Growth Company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| x US GAAP | ¨ International Financial Reporting Standards as issued by the International Accounting Standards Board | ¨ Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

| ¨ Item 17 | ¨ Item 18 |

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| ¨ Yes | x No |

TABLE OF CONTENTS

| 3 |

| 4 |

CERTAIN INFORMATION

In this Shell Company Report on Form 20-F (the “Report”), unless otherwise indicated, “Hunter Maritime,” “we,” “us,” “our,” or “Company” refers to Hunter Maritime Acquisition Corp., a company incorporated under the laws of the Marshall Islands, and its subsidiaries subsequent to the Business Combination (as defined and described below). The “Business Combination” refers to the merger of Hunter Maritime (BVI) Limited, a British Virgin Islands company (“Merger Sub”) with and into NCF Wealth Holdings Limited (“NCF”) , a British Virgin Islands company, which was consummated on March 21, 2019, which resulted in NCF becoming a wholly owned subsidiary of Hunter Maritime.

References to the “PRC” refers to the People’s Republic of China. All references to “provincial-level regions” or “regions,” include provinces as well as autonomous regions and directly controlled municipalities in China, which have an administrative status equal to provinces, including Beijing.

All references to “Renminbi,” “RMB” or “yuan” are to the legal currency of the People’s Republic of the PRC and all references to “U.S. dollars,” “dollars,” “$” are to the legal currency of the United States. This Report contains translations of Renminbi amounts into U.S. dollars at specified rates solely for the convenience of the reader. We make no representation that the Renminbi or U.S. dollar amounts referred to in this Report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

| 5 |

FORWARD-LOOKING STATEMENTS

This Report contains ‘‘forward-looking statements’’ that represent our beliefs, projections and predictions about future events. All statements other than statements of historical fact are ‘‘forward-looking statements’’ including any projections of earnings, revenue or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new projects or other developments, any statements regarding future economic conditions or performance, any statements of management’s beliefs, goals, strategies, intentions and objectives, and any statements of assumptions underlying any of the foregoing. Words such as “may,” “‘will,” “‘should,” “could,” “would,” “predicts,” “potential,” “continue,” “expects,” “anticipates,” “future,” “intends,” “plans,” “believes,” “estimates” and similar expressions, as well as statements in the future tense, identify forward-looking statements.

These statements are necessarily subjective and involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements, or industry results, to differ materially from any future results, performance or achievements described in or implied by such statements. Actual results may differ materially from expected results described in our forward-looking statements, including with respect to correct measurement and identification of factors affecting our business or the extent of their likely impact, the accuracy and completeness of the publicly available information with respect to the factors upon which our business strategy is based or the success of our business.

Forward-looking statements should not be read as a guarantee of future performance or results, and will not necessarily be accurate indications of whether, or the times by which, our performance or results may be achieved. Forward-looking statements are based on information available at the time those statements are made and management’s belief as of that time with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to, those factors discussed under the headings “Risk Factors,” “Operating and Financial Review and Prospects,” “Information on our Company” and elsewhere in this Report.

| 6 |

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | Directors and Senior Management |

Our directors and executive officers are as follows, each of whom was appointed to such position in connection with the closing of the Business Combination on March 21, 2019:

| Name(1) | Age | Position in Hunter Maritime | ||

| Huanxiang Li | 47 | President and Director | ||

| Jia Sheng | 38 | Chief Executive Officer and Director | ||

| Li Wei | 38 | Chief Financial Officer | ||

| Xin Li | 34 | Chief Operating Officer | ||

| Ruoshi Zhang | 38 | Chief Technology Officer | ||

| Tao Yang | 45 | Independent Director | ||

| David X. Li | 55 | Independent Director | ||

| Kevin C. Wei | 51 | Independent Director |

(1) The business address of each such person is the address

of the Company, which is Tower A, WangXin Building

28 Xiaoyun Rd, Chaoyang District, Beijing, 100027.

Huanxiang Li (President)

Ms. Li has been the President and a director of NCF since 2014. Ms. Li has 15 years of experience in the financial industry. Prior to joining NCF, she was Vice-President of the United Venture Financial Guarantee Group from 2003 to 2013, President of Tianjin United Venture Capital Guarantee Co., Ltd. from 2013 to 2015, and President of Dongfang Credit Management Co., Ltd. from 2015 to 2017. Ms. Li holds an EMBA degree from the PBC School of Finance of Tsinghua University.

Jia Sheng (Chief Executive Officer)

Mr. Sheng has been the Chief Executive Officer and a director of NCF since June 2013. Mr. Sheng has 12 years of experience in the Internet and the financial industry. Prior to joining NCF Wealth Holdings, he was Product Manager in Google China and Mountain View from June 2007 to October 2010, and a Co-founder of Yunrang (Beijing) Information Technology Co. Ltd. From November 2010 to May 2013. Mr. Sheng holds an EMBA degree from the PBC School of Finance of Tsinghua University, a Master degree in Computer Science from the University of Toronto in Canada and a Bachelor degree in Computer Science and Technology from Tsinghua University.

Li Wei (Chief Financial Officer)

Ms. Wei joined the management team of NCF in October 2014. She has 12 years of experience in auditing & consulting services and more than 12 years of management experience. Prior to joining NCF, Ms. Wei worked at KPMG from August 2002 to April 2008 and PricewaterhouseCoopers from May 2008 to October 2014. Ms. Wei got her MBA from the School of Economics and Management of Tsinghua University. She obtained her bachelor's degree in Finance from Renmin University of China. Ms. Wei is a CICPA and an internationally registered internal auditor.

| 7 |

Xin Li (Chief Operating Officer)

Ms. Li joined the management team of NCF in February 2014. She worked at China Ping An Life Insurance Co., Ltd. from September 2007 to November 2010 and China International Futures Co., Ltd. from April 2012 to January 2014. Ms. Li has more than 10 years of experience in the finance industry and is an expert in operations management, marketing, and financial product design. She holds a bachelor's degree in finance from Heilongjiang University.

Ruoshi Zhang (Chief Technology Officer)

Mr. Zhang joined the management team of NCF in May 2014. He has more than 10 years of experience in R&D management and distributed system design and development. Mr. Zhang worked at Visual China Group from October 2005 to August 2011, IFeng.com from August 2011 to August 2012 and Credit Ease from January 2013 to April 2013. Mr. Zhang specializes in the development and design of distributed storage systems, social networking sites and financial trading systems. Mr. Zhang got his Bachelor from Information Engineering University.

Tao Yang (Independent Director)

Mr. Yang has been a researcher and an advisor to doctoral candidates of the Institute of Finance & Banking of the Chinese Academy of Social Sciences since August 2003. He has also been the Chief Economist of the China FinTech 50 Forum since April 2017. Mr. Yang’s main scope of research covers monetary and fiscal policies, financial markets, financial technology as well as payments and settlements. He received his PhD degree in Economics from Graduate School of Chinese Academy of Social Sciences, a master’s degree from Chinese Academy of Fiscal Sciences, and a bachelor’s degree from Nanjing University of Science and Technology.

David X. Li (Independent Director)

Mr. Li has been a professor of finance, and faculty co-director of Master of Finance (MF) program at Shanghai Advanced Institute of Finance (SAIF) since Jan 2018, and an associate director of Chinese Academy of Financial Research (CAFR) at Shanghai Jiaotong University since Jan 2018. Previously, he worked at leading financial institutions for more than two decades in the areas of new product development, risk management, asset/liability management and investment analytics. He was the chief-risk-officer for China International Capital Corporation (CICC) Ltd from May 2008 to Jan 2013, head of credit derivative research and analytics at Citigroup and Barclays Capital from Oct 2001 to April 2008, and head of modeling for AIG Investments from Jan 2012 to March 2016.

David has a PhD degree in statistics from the University of Waterloo, a Master’s degrees in economics, finance and actuarial science, and a bachelor’s degree in mathematics. Mr. Li is currently an associate editor for North American Actuarial Journal, an adjunct professor at the University of Waterloo. Mr. Li was one of the pioneers in credit derivatives. His seminal work of using copula functions for credit portfolio modeling has been widely cited by academic research, broadly used by practitioners for credit portfolio trading, risk management and rating, and well covered by media such as Wall Street Journal, Financial Times, Nikkei, CBC News.

Kevin C. Wei (Independent Director)

Mr. Wei has been a managing partner of Fontainburg Corporation Limited, a corporate finance advisory firm, since November 2013. Mr. Wei served as chief financial officer of IFM Investments Limited (stock code: CTC), a New York Stock Exchange listed company headquartered in Beijing, from December 2007 to September 2013, and served as its director from November 2008 until December 2014. From 2006 to 2007, Mr. Wei served as the chief financial officer of a Chinese solar company listed on Nasdaq. From 1999 to 2005, Mr. Wei worked in the internal audit and risk management functions for multinational companies including LG Philips Displays International Ltd. From 1991 to 1999, Mr. Wei worked with KPMG LLP and Deloitte Touche LLP in various audit and consulting roles in the United States of America and China. Mr. Wei graduated from Central Washington University in 1991, where he received his bachelor’s degree (cum laude) with a double major in accounting and business administration.

| 8 |

There are no family relationships between the officers or directors of the Company.

| B. | Advisers |

Not applicable.

| C. | Auditors |

UHY LLP, located at 1185 Avenue of the Americas, 38th Floor New York, NY 10036. UHY LLP has been our auditor since October 2018 and the auditor of NCF since 2018.

KPMG Bedrijfsrevisoren—Réviseurs d' Entreprises CVBA ("KPMG") was the Company’s auditor from the Company’s inception until October 2018. KPMG’s address is Business Park De Alverberg

Herkenrodesingel 6B bus 4.01, 3500 Hasselt, Belgium.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

| A. | Selected Financial Data |

The disclosure under the caption “Selected Historical Financial Information of NCF” beginning on page 43 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| B. | Capitalization and Indebtedness |

The following table shows the capitalization of NCF as of February 28, 2019

| Actual (unaudited) | ||||

| Current Assets | ||||

| Cash and cash equivalents | $ | 167,987,450 | ||

| Restricted Cash | 14,334,653 | |||

| Current Liabilities | ||||

| Total current liabilities | $ | 49,562,586 | ||

| Long term debt | 4,077,000 | |||

| Shareholders’ Equity | ||||

| Common Stock: | $ | 10,916 | ||

| Series B preferred shares | 294 | |||

| Series C-1 preferred shares | 247 | |||

| Shares in Employee Benefit Trust | -4,077,600 | |||

| Statutory reserve | 6,667,678 | |||

| Additional paid-in capital | 140,250,168 | |||

| Retained Earnings | 21,610,036 | |||

| Accumulated other comprehensive income | 5,735,128 | |||

| Non-controlling interest | -167,698 | |||

| Total shareholders’ equity | 170,029,169 | |||

| Total liabilities and shareholders’ equity | $ | 223,668,755 | ||

| 9 |

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

The disclosure under the caption “Risk Factors” beginning on page 12 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

ITEM 4. INFORMATION ON THE COMPANY

| A. | History and Development of the Company |

Our Corporate Structure

The disclosure under the caption “Information about the Companies” beginning on page 40 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

Capital Expenditures

We incurred capital expenditures of RMB67.2million (US$9.8 million), RMB37.1 million (US$5.5 million) and RMB11.9 million (US$1.8 million) in 2018, 2017 and 2016, respectively. In these periods, our capital expenditures were mainly used for purchases of equity shares, equipment and software. We will continue to incur capital expenditures in connection with the expected growth of our business. We incurred capital divestitures of RMB16.6 million (US$2.4 million), RMB0.0 million (US$0.0 million) and RMB0.0 million (US$0.0million) in 2018, 2017 and 2016, respectively.

We incurred capital expenditures of RMB0.9 million (US$0.1 million) and capital divestitures of RMB0.0 million (US$0.0 million) in two months as of February 28, 2019. The capital expenditures were mainly used for purchases of equipment and software.

The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC and state the address of that site (http://

www.sec.gov). We maintain a website at ir.ncfwx.com.

| B. | Business Overview |

The disclosure under the caption “Description of the Combined Company Following the Business Combination” beginning on page 66 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| C. | Organizational Structure |

The disclosure under the caption “Information about the Companies” beginning on page 40 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| 10 |

| D. | Property, Plant and Equipment |

The disclosure under the caption “Description of the Combined Company Following the Business Combination - Facilities” beginning on page 74 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

ITEM 4A. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS

The disclosure under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations of NCF Wealth Group” beginning on page 86 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF HUNTER MARITIME

The following discussion contains forward-looking statements that reflect Hunter Maritime’s future plans, estimates, beliefs and expected performance. The forward-looking statements are dependent upon events, risks and uncertainties that may be outside Hunter Maritime’s control. Hunter Maritime’s actual results could differ materially from those discussed in these forward-looking statements. Please read “Risk Factors” and “Forward-Looking Statements.” In light of these risks, uncertainties and assumptions, the forward-looking events discussed may not occur.

Overview

We are a blank check company formed on June 24, 2016 under the laws of the Republic of the Marshall Islands for the purpose of acquiring through a merger, capital stock exchange, asset acquisition, debt acquisition, stock purchase, reorganization or other similar business combination, vessels, vessel contracts (including for the purchase and charter-in by us of vessels) or one or more operating businesses or assets, intended to be in the international maritime shipping industry.

Description of Merger:

On October 5, 2018, Hunter Maritime and

Merger Sub entered into the Merger Agreement with NCF and Zhenxin Zhang, as representative of the NCF Stockholders, pursuant to

which NCF merged with and into Merger Sub, with NCF continuing as the surviving company and as a wholly-owned subsidiary of Hunter

Maritime.

NCF is a fintech company in China. Among other businesses, NCF operates an online consumer and business finance marketplace in China, focused on facilitating the origination of debt financing by directly connecting individual and commercial borrowers with lenders as an alternative to traditional lending sources. NCF generates revenues primarily from fees charged to borrowers for services in matching them with lenders through the facilities of its online platform. NCF’s platform does not pool funds from investors or grant loans to any customer or provide any credit services; that is, NCF does not itself finance the loans offered on its platform with its own funds.

On November 6, 2018, we completed the Extension Tender Offer, funded with the proceeds then held in the Trust Account, in connection with an amendment to our Amended and Restated Articles of Incorporation to extend the deadline by which a business combination must be consummated, by a period of five months, until April 23, 2019. Our shareholders approved the Extension Amendment at a special meeting of shareholders held on October 31, 2018. We purchased 12,999,350 Class A common shares at $10.125 per share, for an aggregate purchase price of approximately $131.6 million in the Extension Tender Offer.

| 11 |

On March 21, 2019, the Merger closed. The aggregate consideration provided by Hunter Maritime to the NCF Stockholders pursuant to the Merger Agreement consists of: (i) 200,000,000 Class A common shares (the “Closing Payment Shares”), of which 15,000,000 Class A common shares were deposited into escrow to secure certain indemnification obligations of NCF and the NCF Stockholders (the “Escrow Shares”), plus (ii) earnout payments consisting of up to an additional 50,000,000 Class A common shares if Hunter Maritime (and its subsidiaries on a consolidated basis) meets certain financial performance targets for the 2019 and 2020 fiscal years.

Accounting for the Acquisition

The merger will be accounted for, in accordance with GAAP, as a “reverse merger” and recapitalization at the date of the consummation of the transaction since the stockholders of NCF will own at least 50.1% of the outstanding common stock of Hunter Maritime immediately following the completion of the merger, NCF will have its current officers assuming all corporate and day-to-day management offices of Hunter Maritime, including chief executive officer and chief financial officer, and board members appointed by NCF will constitute a majority of the board of the Successor after the Business Combination. Accordingly, NCF will be deemed to be the accounting acquirer in the transaction and, consequently, the transaction is treated as a recapitalization of NCF. Accordingly, the assets and liabilities and the historical operations that will be reflected in the Hunter Maritime financial statements after consummation of the merger will be those of NCF and will be recorded at the historical cost basis of NCF. Hunter Maritime’s assets, liabilities and results of operations will be consolidated with the assets, liabilities and results of operations of NCF upon consummation of the merger.

Results of Operations

For the period from June 24, 2016 (inception) through December 31, 2018, our activities consisted of formation and preparation for the Public Offering and subsequent to the Public Offering, and efforts directed toward locating and completing a suitable business combination. Our operating costs for those periods include our search for a business combination and are largely associated with our governance and public reporting, and charges of $10,000 per month payable to an affiliate of our Sponsor for administrative services.

For the period from June 24, 2016 (inception) to December 31, 2016 (‘the period ended December 31, 2016’) and for the year ended December 31, 2017 we had a net loss of $398,874 and $382,605, respectively. The formation and operating costs for the year ended December 31 2017 was $1,324,088, an increase of $926,721, from $397,367 for the period ended December 31, 2016. The overall increase was mainly caused by increased expenses for Directors and Officers Liability Insurance, advisory and legal fees. The interest income from investments in our Trust Account for the year ended December 31, 2017 was $1,084,213, an increase of $1,052,405, from $31,808 for the period ended December 31, 2016. During the year ended December 31, 2017 we earned a full year of interest income from our investment whereas for the period ended December 31, 2016,we only earned investment income during one month.

For the years ended December 31, 2018 and 2017, we had a net loss of 1,550,352 and $382,605, respectively. The formation and operating costs for the year ended December 31 2018 was $949,114, a decrease of $374,974, from $1,324,088 for the year ended December 31, 2017. The decrease was mainly caused by a reduction in legal fees. The interest income from investments in our Trust Account for the year ended December 31, 2018 was $1,482,889, an increase of $398,676 as a result of an increase in US Treasury Bond rates, from $1,084,213 for the year ended December 31, 2017. During the years ended December 31, 2018 and December 31, 2017, we earned the full year of interest income from our investment.

| 12 |

Liquidity and Capital Resources

On July 11, 2016, Bocimar Hunter NV, the Company’s sponsor (the "Sponsor") purchased 4,312,500 Class B Common Shares of the Company (the "Founder Shares") for $25,000, or $0.006 per share.

On November 23, 2016, Hunter Maritime consummated its initial public offering of 15,000,000 Units. Each Unit (“Unit”) issued in the Initial Public Offering (‘IPO’) consists of one Class A common share and one-half of one Warrant (“Warrant”). Each whole Warrant entitles the holder to purchase one Class A common share at a price of $11.50. Simultaneously with the consummation of the IPO, Hunter Maritime completed a private placement of 3,333,333 Warrants (“private placement Warrants”) at a purchase price of $1.50 per Warrant to its Sponsor, generating gross proceeds of $5,000,000. On November 18, 2016, the Units commenced trading on the NASDAQ under the symbol “HUNTU.”

On December 16, 2016, the underwriters of the IPO exercised their overallotment option in part, for a total of an additional 173,100 Units. As a result of the partial exercise of the overallotment option, as of January 3, 2017, the Sponsor forfeited 519,225 Class B common shares in order to maintain its ownership, on an as-converted basis, at 20% of Hunter Maritime’s issued and outstanding common shares. In addition, Hunter Maritime completed the private sale of an additional 23,080 private placement Warrants to the Sponsor at a purchase price of $1.50 per Warrant, generating gross proceeds of $34,620, in accordance with the terms of the private placement agreement entered into concurrently with the IPO.

The 15,173,100 Units sold in the IPO, including the 173,100 Units sold pursuant to the overallotment option, were sold at an offering price of $10.00 per Unit, generating gross proceeds of $151,731,000, which been placed in the Trust Account pending Hunter Maritime’s completion of an initial business combination.

On January 9, 2017, the Class A common shares and Warrants underlying the Units sold in the IPO began to trade separately.

On September 27, 2018, pursuant to the terms of a Securities Purchase Agreement, Bocimar Hunter transferred ownership of its (i) 3,793,275 Class B common shares and (ii) 3,356,413 private placement Warrants of the Company to CMB NV (“CMB”) which we now consider the Sponsor. See also Note 9 Related Party Transactions.

On November 6, 2018, we completed a tender offer, funded with the proceeds then held in the Trust Account, in connection with an amendment to our Amended and Restated Articles of Incorporation to extend the deadline (the “Extension Amendment”) by which a business combination must be consummated to April 23, 2019 (the “Extended Date” or “Business Combination Deadline”), pursuant to which we purchased 12,999,350 Class A common shares at $10.125 per share, for an aggregate purchase price of approximately $131.6 million (the “Extension Tender Offer”). In connection with the Extension Tender Offer, we deposited into the Trust Account an additional $1,896,638 to make the total amount on deposit in the Trust Account equal to $10.125 per Class A common share (the “First Tender Contribution”). As a result, approximately $22.1 million remained in the Trust Account.

In connection with the Extension Amendment, the Sponsor, or persons on its behalf, has agreed to contribute to us $0.03 for each Public Share that was not purchased in the Extension Tender Offer for each calendar month commencing on November 23, 2018 (the day by which were initially required to complete our initial business combination) until April 23, 2019, or such earlier date that we complete our initial business combination (the “Monthly Extension Contribution”). The aggregate amount of the Monthly Extension Contribution will be repayable by us to the Sponsor if we complete an initial business combination. On each of December 27, 2018 and January 30, 2019, $65,213 was contributed to the Trust Account for the Monthly Extension Contribution. As a result, following the Extension Tender Offer, First Tender Contribution, and Monthly Extension Contributions, approximately $22.1 million remains in the Trust Account.

| 13 |

At November 6, 2018, the per public share redemption or conversion price increased to $10.125 per share as a result of the $1,896,638 deposit into the Trust Account relating to the other expenses to extend the time to complete the initial business combination. At November 23, 2018, the per public share redemption or conversion price increased to $10.155 per share as a result of the $65,213 deposit into the Trust Account relating to the other expenses to extend the time to complete the initial business combination.

On November 6, 2018, December 19, 2018 and January 30, 2019, Hunter Maritime has drawn an amount of $500,000, $300,000 and $200,000 respectively under a promissory note with its sponsor CMB. These loans are unsecured and bear interest at a rate per annum of LIBOR plus 0.60%.

On February 19, 2019 Hunter Maritime announced the commencement of a tender offer pursuant to the terms of the Merger Agreement by and among Hunter Maritime, and NCF Wealth Holdings Limited.

On February 22, 2019, Hunter Maritime has drawn an amount of $400,000, under a promissory note with its Sponsor. The loan is unsecured and bears interest at a rate per annum of LIBOR plus 0.60%.

On March 20, 2019, Hunter Maritime announced the final results of its previously announced tender offer. A total of 1,926,021 Class A common shares were validly tendered and accepted for purchase for a total cost of approximately $19.7 million, excluding fees and expenses related to the Tender Offer, which will be released from the Company’s trust account.

On March 21, 2019, Hunter Maritime closed the Merger.

Prior to the closing of the Merger Hunter Maritime has neither engaged in any operations nor generated significant revenue to date. Hunter Maritime’s only activities between inception and the closing of its Public Offering were organizational activities and those necessary to prepare for and close the Public Offering. Since the consummation of the Public Offering, Hunter Maritime’s activity has been limited to evaluating candidates for its initial business combination.

Critical Accounting Policies

Management’s discussion and analysis of our results of operations and liquidity and capital resources are based on our audited financial information. We describe our significant accounting policies in Note 2 - Significant Accounting Policies, of the Notes to Financial Statements included as Exhibit 99.1 to this Shell Company Report. Our audited financial statements have been prepared in accordance with U.S. GAAP. Certain of our accounting policies require that management apply significant judgments in defining the appropriate assumptions integral to financial estimates. On an ongoing basis, management reviews the accounting policies, assumptions, estimates and judgments to ensure that our financial statements are presented fairly and in accordance with U.S. GAAP. Judgments are based on historical experience, terms of existing contracts, industry trends and information available from outside sources, as appropriate. However, by their nature, judgments are subject to an inherent degree of uncertainty, and, therefore, actual results could differ from our estimates.

ITEM 6. DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES

| A. | Directors and Senior Management |

The information set forth in Item 1.A. of this Shell Company Report on Form 20-F is incorporated herein by reference.

| B. | Compensation |

Compensation of Directors and Executive officers of Hunter Maritime

Prior to the Business Combination, Hunter Maritime did not provide any compensation to its officers and directors.

| 14 |

For the fiscal year ended December 31, 2018, NCF paid an aggregate of approximately RMB3.1 million (US$0.45 million) in cash to our executive officers, and it did not pay any compensation to its non-executive directors.

We have not set aside or accrued any amount to provide pension, retirement or other similar benefits to our executive officers and directors. We also have not provided any profit sharing plan and stock options to our executive officers and directors. Our PRC subsidiaries and our variable interest entity are required by law to make contributions equal to certain percentages of each employee’s salary for his or her pension insurance, medical insurance, unemployment insurance, maternity insurance, on-the job injury insurance, and housing fund plans through a PRC government-mandated defined contribution plan.

| C. | Board Practices |

Term of Service

Our board of directors consists of five directors and is divided into three classes with only one class of directors being elected in each year and each class serving a three-year term.

The members of our board of directors are expected to play a key role in identifying and evaluating prospective acquisition candidates, selecting the target business, and structuring, negotiating and consummating its acquisition..

Our Audit Committee consists of Tao Yang, David X. Li and Kevin C. Wei. Kevin C. Wei serves as chairman and as the Audit Committee financial expert. The Audit Committee provides assistance to our board of directors in fulfilling their responsibilities to shareholders, and investment community relating to our corporate accounting, reporting practices, and the quality and integrity of our financial reports. The Audit Committee, among other duties, recommends the independent auditors to be selected to audit our consolidated financial statements, meets with our independent auditors and financial management to review the scope of the proposed audit for the current year and the audit procedures to be utilized, reviews with the independent auditors, and financial and accounting personnel, the adequacy and effectiveness of our accounting and financial controls, and reviews the consolidated financial statements contained in the annual report to shareholders with management and the independent auditors.

There are no contracts between us and any of our directors providing for benefits upon termination of their employment.

| D. | Employees |

The disclosure under the caption “Description of the Combined Company Following the Business Combination - Employees” beginning on page 74 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| E. | Share Ownership |

The disclosure set forth in Item 7A of this Shell Company Report on Form 20-F is incorporated herein by reference.

ITEM 7. MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS

| A. | Major Shareholders |

The following table sets forth information with respect to the beneficial ownership of Hunter Maritime’s common shares as of March 21, 2019:

| 15 |

| ¨ | each person known to us to own beneficially more than 5% of our common shares; |

| ¨ | each of our current executive officers and directors; and |

| ¨ | each of our directors and executive officers as a group. |

Beneficial ownership is determined in accordance with SEC rules and includes voting or investment power with respect to securities. Except as indicated by the footnotes below, Hunter Maritime believes that the persons and entities named in the table below have, as of March 21, 2019, sole voting and investment power with respect to all stock that they beneficially own, subject to applicable community property laws. All Hunter Maritime stock subject to options or warrants exercisable within 60 days of the consummation of the Business Combination are deemed to be outstanding and beneficially owned by the persons holding those options or warrants for the purpose of computing the number of shares beneficially owned and the percentage ownership of that person. They are not, however, deemed to be outstanding and beneficially owned for the purpose of computing the percentage ownership of any other person.

Subject to the paragraph above, percentage ownership of outstanding shares is based on 204,041,004 Class A common shares of Hunter Maritime to be outstanding upon consummation of the Business Combination. All of the below shareholders acquired their shares in the Business Combination. The shares owned by such persons do not have voting rights different from the shares owned by other holders.

| Name and Address (1) | Number of Shares Beneficially Owned | Percentage of Ownership | ||||||

| Zhenxin Zhang(2) | 122,815,857 | 60.2 | % | |||||

| Great Reap Ventures Limited (3) | 103,613,734 | 50.8 | % | |||||

| TMF (Cayman) Ltd.(4) | 19,202,123 | 9.4 | % | |||||

| Ever Step Holdings Limited(5) | 17,625,804 | 8.6 | % | |||||

| Highlight Limited(6) | 12,114,794 | 5.9 | % | |||||

| Huanxiang Li(7) | 349,129 | * | ||||||

| Jia Sheng(7) | 209,477 | * | ||||||

| Ruoshi Zhang(7) | 192,021 | * | ||||||

| Xin Li(7) | 122,195 | * | ||||||

| Li Wei(7) | 78,989 | * | ||||||

| Tao Yang | 0 | 0 | ||||||

| David X. Li | 0 | 0 | ||||||

| Kevin C. Wei | 0 | 0 | ||||||

| All directors and executive officers as a group (8 individuals) | 951,811 | * | ||||||

| * | Less than 1% |

| (1) | Unless otherwise indicated, the business address of each of the individuals is Tower A, WangXin Building, 28 Xiaoyun Rd, Chaoyang District, Beijing, 100027. |

| (2) | Consists of shares owned by Great Reap Ventures Limited and TMF (Cayman) Ltd. |

| (3) | Great Reap Ventures Limited is owned and controlled by Mr. Zhenxin Zhang. |

| (4) | TMF (Cayman) Ltd is owned by employees of NCF Wealth Holdings Limited and Mr. Zhenxin Zhang has voting power over the shares owned by TMF (Cayman) Ltd. |

| (5) | Ever Step Holdings Limited is owned and controlled by Chong Sing Holdings FinTech Group Limited, a company listed on the Hong Kong Stock Exchange with stock code 8207. |

| (6) | Highlight Limited is owned and controlled by Mr. Kecun Hu. |

| (7) | Consists of shares owned by TMF (Cayman) Ltd., which the beneficial owner can demand TMF (Cayman) Ltd. distribute to the beneficial owner at any time. |

Except as disclosed herein, we are not aware of any arrangement that may, at a subsequent date, result in a change of control of the combined company.

| 16 |

| B. | Related Party Transactions |

The disclosure under the caption “Certain Relationships and Related party Transactions” beginning on page 127 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| C. | Interests of Experts and Counsel |

Not Applicable.

| A. | Consolidated Statements and Other Financial Information. |

See Item 17.

| B. | Significant Changes |

None.

Not applicable.

ITEM 10. ADDITIONAL INFORMATION

| A. | Share Capital |

Status of Outstanding Ordinary Shares.

As of March 21, 2019, we had a total of 204,041,004 shares of Class A Common Stock issued and outstanding. No classes of stock are issued or outstanding.

The information contained in Item 10(B) of this Shell Company Report is incorporated by reference herein.

| B. | Memorandum and Articles of Association |

We are a corporation formed under the laws of the Republic of the Marshall Islands on June 24, 2016 and our affairs are governed by our amended and restated articles of incorporation, our amended and restated bylaws, which are filed as exhibit 1.1 and 1.2, respectively, to this annual report, and the laws of the Republic of the Marshall Islands.

Below is a summary of the description of our capital stock, including the rights, preferences and restrictions attaching to each class of stock. Because the following is a summary, it does not contain all information that you may find useful. For more complete information, you should read our amended and restated articles of incorporation and amended and restated bylaws, which are incorporated by reference herein.

Purpose

Our purpose, as stated in our amended and restated articles of incorporation, is to engage in any lawful act or activity for which corporations may be organized under the Marshall Islands Business Corporation Act (the “BCA”), and we may exercise all the powers and privileges that are necessary or convenient to the conduct, promotion or attainment of our business or purposes.

| 17 |

Authorized Capitalization

Pursuant to our amended and restated articles of incorporation, we are authorized to issue up to 400,000,000 Class A common shares, par value $0.0001 per share, 100,000,000 Class B common shares, par value $0.0001 per share, and 50,000,000 preferred shares, par value $0.0001 per share. As of the date of this annual report, we had 15,173,100 Class A common shares and 3,793,275 Class B common shares outstanding, and no preferred shares outstanding.

Units

Each unit consists of one Class A common share and one-half warrant. Holders have the option to continue to hold units or separate their units into the component securities. Holders must have their brokers contact our transfer agent in order to separate the units into Class A common shares and warrants. No fractional warrants will be issued upon separation of the units and only whole warrants will trade. Accordingly, unless you purchase at least two units, you will not be able to receive or trade warrants.

Common Shares

Our shareholders are entitled to one vote for each share held of record on all matters to be voted on by shareholders. Our Class A common shares have no conversion, preemptive, or other subscription rights and there are no sinking fund or redemption provisions applicable to the common shares.

Preferred Shares

Our amended and restated articles of incorporation authorize the issuance of up to 50,000,000 shares, par value $0.0001 per share, of blank check preferred stock with such designation, rights and preferences as may be determined from time to time by our board of directors. No shares of preferred stock have been or are being issued or registered in the IPO. Accordingly, our board of directors is empowered, without shareholder approval, to issue preferred stock with dividend, liquidation, conversion, voting, or other rights which could adversely affect the voting power or other rights of the holders of common shares. In addition, the preferred stock could be utilized as a method of discouraging, delaying or preventing a change in control of us. Although we do not currently intend to issue any shares of preferred stock, we cannot assure you that we will not do so in the future.

Warrants

Public Warrants

Each full warrant entitles the holder to purchase one Class A common share at a price of $11.50 per share, subject to adjustment as discussed below, at any time, unless the warrants have previously expired, commencing on the later of:

| · | 30 days after the consummation of the initial Business Combination; and |

| · | 12 months from the closing of the IPO; provided that, during the period in which the warrants are exercisable, a registration statement under the Securities Act covering the Class A common shares issuable upon exercise of the warrants is effective and a current prospectus relating to the Class A common shares issuable upon the exercise of the warrants is available. |

We have agreed to use our best efforts to have an effective registration statement covering our Class A common shares reserved for issuance upon exercise of the warrants from the date the warrants become exercisable and to maintain a current prospectus relating to those Class A common shares until the warrants expire or are redeemed by us.

The warrants will expire at 5:00 p.m., New York City time, March 21, 2024 or, if an effective registration statement covering the Class A common shares issuable upon exercise of the warrants is not then effective and a prospectus relating to such Class A common shares is not then available, upon such registration statement being effective and such prospectus being available for five consecutive business days, or in either case, earlier upon redemption or liquidation or, in either case, earlier upon redemption or liquidation by us. If we elect to redeem the warrants, we will have the option to require all holders who elect to exercise their warrants prior to redemption to do so on a cashless basis. We may redeem the warrants (except as described herein with respect to the private placement warrants) at any time after the warrants become exercisable:

| 18 |

| · | in whole and not in part; |

| · | at a price of $0.01 per warrant; |

| · | upon a minimum of 30 days' prior written notice of redemption to each warrant holder; and |

| · | only if (x) the closing price of our Class A common shares on NASDAQ, or any other national securities exchange on which our Class A common shares may be traded, equals or exceeds $18.00 per share for any 20 trading days within a 30 trading-day period ending three business days before we send the notice of redemption to warrant holders, (y) a registration statement under the Securities Act covering Class A common shares issuable upon exercise of the warrants is effective and remains effective from the date on which we send a redemption notice to and including the redemption date and (z) a current prospectus relating to the Class A common shares issuable upon exercise of the warrants is available from the date on which we send a redemption notice to and including the redemption date. |

We established this last criterion to provide warrant holders with the opportunity to realize a premium to the warrant exercise price prior to the redemption of their warrants, as well as to provide them with a degree of liquidity to cushion the market reaction, if any, to our election to redeem the warrants. If the foregoing conditions are satisfied and we call the warrants for redemption, each warrant holder will then be entitled to exercise his, her or its warrants prior to the scheduled redemption date. There can be no assurance that the price of our Class A common shares will not fall below the $18.00 per share trigger price or the $11.50 per share warrant exercise price after the redemption notice is delivered. We do not need the consent of the underwriters or our shareholders to redeem the outstanding warrants.

If we call the warrants for redemption, our management will have the option to require all holders that elect to exercise such warrants to do so on a "cashless basis," provided that such cashless exercise is permitted under the laws of our corporate jurisdiction. In such event, each holder would pay the exercise price by surrendering the warrants and would receive on exercise that number of Class A common shares equal to the quotient obtained by dividing (x) the product of the number of common shares underlying the warrants being surrendered, multiplied by the difference between the exercise price of the warrants and the "fair market value" by (y) the fair market value and then would receive Class A common shares underlying the non-surrendered warrants. The "fair market value" shall mean the average reported closing price of our Class A common shares for the 10 trading days ending on the third trading day prior to the date on which the notice of redemption is sent to the holders of warrants. Such warrants may not be settled on a cashless basis unless they have been called for redemption and we have required all such warrants to be settled on a cashless basis.

The right to exercise the warrants will be forfeited unless they are exercised before the redemption date specified in the notice of redemption. From and after the redemption date, the record holder of a warrant will have no further rights except to receive, upon surrender of the warrants, the redemption price.

The warrants are issued in registered form under a warrant agreement between Continental Stock Transfer & Trust Company, as warrant agent, and us, which is attached to this shell company report as Exhibit 4.2.

The exercise price and number of Class A common shares issuable on exercise of the warrants may be adjusted in certain circumstances, including in the event of a stock dividend or our recapitalization, reorganization, merger or consolidation.

| 19 |

If the number of outstanding Class A common shares is increased by a capitalization or share dividend payable in Class A common shares, or by a split-up of Class A common shares or other similar event, then, on the effective date of such share dividend, split-up or similar event, the number of Class A common shares issuable on exercise of each warrant will be increased in proportion to such increase in the outstanding Class A common shares. A rights offering to holders of Class A common shares entitling holders to purchase Class A common shares at a price less than the fair market value will be deemed a capitalization of a number of Class A common shares equal to the product of (i) the number of Class A common shares actually sold in such rights offering (or issuable under any other equity securities sold in such rights offering that are convertible into or exercisable for Class A common shares) multiplied by (ii) one (1) minus the quotient of (x) the price per Class A ordinary share paid in such rights offering divided by (y) the fair market value. For these purposes (i) if the rights offering is for securities convertible into or exercisable for Class A common shares, in determining the price payable for Class A common shares, there will be taken into account any consideration received for such rights, as well as any additional amount payable upon exercise or conversion and (ii) fair market value means the volume weighted average price of Class A common shares as reported during the ten (10) trading day period ending on the trading day prior to the first date on which the Class A common shares trade on the applicable exchange or in the applicable market, regular way, without the right to receive such rights.

If the number of outstanding Class A common shares is decreased by a consolidation, combination, reverse share split or redesignation of Class A common shares or other similar event, then, on the effective date of such consolidation, combination, reverse share split, redesignation or similar event, the number of Class A common shares issuable on exercise of each warrant will be decreased in proportion to such decrease in outstanding Class A common shares.

Whenever the number of Class A common shares purchasable upon the exercise of the warrants is adjusted, as described above, the warrant exercise price will be adjusted by multiplying the warrant exercise price immediately prior to such adjustment by a fraction (x) the numerator of which will be the number of Class A common shares purchasable upon the exercise of the warrants immediately prior to such adjustment, and (y) the denominator of which will be the number of Class A common shares so purchasable immediately thereafter.

In case of any redesignation or reorganization of the outstanding Class A common shares (other than those described above or that solely affects the par value of such Class A common shares), or in the case of any merger or consolidation of us with or into another corporation (other than a consolidation or merger in which we are the continuing corporation and that does not result in any redesignation or reorganization of our outstanding Class A common shares), or in the case of any sale or conveyance to another corporation or entity of the assets or other property of us as an entirety or substantially as an entirety in connection with which we are dissolved, the holders of the warrants will thereafter have the right to purchase and receive, upon the basis and upon the terms and conditions specified in the warrants and in lieu of our Class A common shares immediately theretofore purchasable and receivable upon the exercise of the rights represented thereby, the kind and amount of shares of stock or other securities or property (including cash) receivable upon such redesignation, reorganization, merger or consolidation, or upon a dissolution following any such sale or transfer, that the holder of the warrants would have received if such holder had exercised their warrants immediately prior to such event. However, if the holders of our Class A common shares were entitled to exercise a right of election as to the kind or amount of securities, cash or other assets receivable upon such consolidation or merger, then the kind and amount of securities, cash or other assets for which each warrant will become exercisable will be deemed to be the weighted average of the kind and amount received per share by the holders of Class A common shares in such consolidation or merger that affirmatively make such election, and if a tender, exchange or redemption offer has been made to and accepted by such shareholders under circumstances in which, upon completion of such tender or exchange offer, the maker thereof, together with members of any group (within the meaning of Rule 13d-5(b)(1) under the Exchange Act) of which such maker is a part, and together with any affiliate or associate of such maker (within the meaning of Rule 12b-2 under the Exchange Act) and any members of any such group of which any such affiliate or associate is a part, own beneficially (within the meaning of Rule 13d-3 under the Exchange Act) more than 50% of the outstanding Class A common shares, the holder of a warrant will be entitled to receive the highest amount of cash, securities or other property to which such holder would actually have been entitled as a shareholder if such warrant holder had exercised the warrant prior to the expiration of such tender or exchange offer, accepted such offer and all of the Class A common shares held by such holder had been purchased pursuant to such tender or exchange offer, subject to adjustment (from and after the consummation of such tender or exchange offer) as nearly equivalent as possible to the adjustments provided for in the warrant agreement. Additionally, if less than 70% of the consideration receivable by the holders of Class A common shares in such a transaction is payable in the form of capital stock or shares in the successor entity that is listed for trading on a national securities exchange or is quoted in an established over-the-counter market, or is to be so listed for trading or quoted immediately following such event, and if the registered holder of the warrant properly exercises the warrant within thirty days following the public disclosure of such transaction, the warrant exercise price will be reduced as specified in the warrant agreement based on the per share consideration minus Black-Scholes Warrant Value (as defined in the warrant agreement) of the warrant.

| 20 |

The warrants may be exercised upon surrender of the warrant certificate on or prior to the expiration date at the offices of the warrant agent, with the exercise form on the reverse side of the warrant certificate completed and executed as indicated, accompanied (except in the event we have required cashless exercise of the warrants in connection with a redemption) by full payment of the exercise price, by certified check payable to us, for the number of warrants being exercised. The warrant holders do not have the rights or privileges of holders of Class A common shares and any voting rights until they exercise their warrants and receive Class A common shares. After the issuance of Class A common shares upon exercise of the warrants, each holder will be entitled to one vote for each share held of record on all matters to be voted on by shareholders.

No warrants will be exercisable unless at the time of exercise a registration statement relating to Class A common shares issuable upon exercise of the warrants is effective and a prospectus relating to Class A common shares issuable upon exercise of the warrants is available and the Class A common shares have been registered or qualified or deemed to be exempt under the securities laws of the state of residence of the holder of the warrants. Holders of the warrants are not entitled to net cash settlement and the warrants may only be settled by delivery of shares of our Class A common shares and not cash. Under the terms of the warrant agreement, we have agreed to meet these conditions and use our commercially reasonable efforts to maintain an effective registration statement and to make available a current prospectus relating to Class A common shares issuable upon exercise of the warrants until the expiration or earlier redemption of the warrants. However, we cannot assure you that we will be able to do so. We have no obligation to settle the warrants or otherwise permit the warrants to be exercised in the absence of an effective registration statement or a currently available prospectus. The warrants may never become exercisable if we fail to comply with these registration requirements. The warrants may be deprived of any value and the market for the warrants may be limited if holders are prohibited from exercising warrants because an effective registration statement and the prospectus relating to the Class A common shares issuable upon the exercise of the warrants is not currently available or if the Class A common shares are not qualified or exempt from qualification in the jurisdictions in which the holders of the warrants reside and we will not be required to cash settle any such warrant exercise. Warrants included in the units sold in the IPO will not be exercisable at the option of the holder on a cashless basis, provided that in connection with a call for redemption of the warrants, we may require all holders who wish to exercise their warrants to do so on a cashless basis. The private placement warrants will not be exercisable at any time unless a registration statement is effective and a prospectus is available. We have not registered the Class A common shares issuable upon exercise of the warrants at this time. However, we have agreed that, as soon as practicable, but in no event later than 30 days after the closing of our initial Business Combination, we will use our best efforts to file with the SEC a registration statement covering the Class A common shares issuable upon exercise of the warrants. After the filing of such registration statement, we will use our best efforts to cause the effectiveness thereof as soon as reasonably practicable and to maintain a current prospectus relating to those Class A common shares until the warrants expire or are redeemed, as specified in the warrant agreement. See "Risk Factors—Risks Associated with the Company and the Offering—We have not registered the Class A common shares issuable upon exercise of the warrants under the Securities Act or any state securities laws at this time, and such registration may not be in place when an investor desires to exercise warrants, thus precluding such investor from being able to exercise its warrants and causing such warrants to expire worthless."

| 21 |

Private Placement Warrants

CMB NV, the sponsor in our initial public offering (the “sponsor”), purchased an aggregate of 3,333,333 private placement warrants at a price of $1.50 per warrant in private placement transactions that occurred in connection with our IPO. Pursuant to the underwriters' partial exercise of the overallotment option on December 16, 2016, we sold an additional 23,080 private placement warrants to the sponsor. Each private placement warrant entitles the holder to purchase one Class A common share at $11.50 per share.

The private placement warrants are identical to the warrants included in the units sold in the IPO, except that:

| · | the private placement warrants will be exercisable at the option of the holder on a cashless basis so long as they are held by the original purchaser or its permitted transferees and such cashless exercise is permitted under the laws of our corporate jurisdiction; |

| · | the private placement warrants will not be redeemable by us; and |

| · | the private placement warrants (including the Class A common shares issuable upon exercise of the private placement warrants) may not, subject to certain limited exceptions, be transferred, assigned or sold until 30 days after the completion of our initial Business Combination. |

If a holder of the private placement warrants elects to exercise them on a cashless basis, that holder would pay the exercise price by surrendering his, her or its warrants for that number of Class A common shares equal to the quotient obtained by dividing (x) the product of the number of Class A common shares underlying the warrants, multiplied by the difference between the exercise price of the warrants and the "fair market value" by (y) the fair market value. The "fair market value" shall mean the average reported closing price of the Class A common shares for the 10 trading days ending on the third trading day prior to the date on which the notice of redemption is sent to the holders of warrants.

On March 21, 2019, we issued an additional 933,333 private warrants to the sponsor in exchange for the cancellation of $1,400,000 of promissory notes which we made in the sponsor’s favor.

Directors

Our directors are elected by a plurality of the votes cast by shareholders entitled to vote. There is no provision for cumulative voting.

Our amended and restated articles of incorporation require our board of directors to consist of at least one member. Our board of directors currently consists of six members. Our amended and restated bylaws may be amended by the vote of a majority of our entire board of directors. Directors are elected annually on a staggered basis, with the term of office of one or another of the three classes expiring each year. Each director elected holds office for a three-year term or until his successor is duly elected and qualified, except in the event of his death, resignation, removal or the earlier termination of his term of office.

Shareholder meetings

Under our amended and restated bylaws, annual meetings of shareholders will be held at a time and place selected by our board of directors. The meetings may be held in or outside of the Marshall Islands. Special meetings may be called at any time by a majority of our board of directors or our Chief Executive Officer. Our board of directors may set a record date between 15 and 60 days before the date of any meeting to determine the shareholders that will be eligible to receive notice and vote at the meeting. One or more shareholders representing at least one-third of the total voting rights of our total issued and outstanding shares present in person or by proxy at a shareholder meeting shall constitute a quorum for the purposes of the meeting.

| 22 |

Dissenters' rights of appraisal and payment

Under the BCA, our shareholders have the right to dissent from various corporate actions, including any merger or consolidation and the sale of all or substantially all of our assets not made in the usual course of our business, and receive payment of the fair value of their shares. In the event of any further amendment of our amended and restated articles of incorporation, a shareholder also has the right to dissent and receive payment for his or her shares if the amendment alters certain rights in respect of those shares. The dissenting shareholder must follow the procedures set forth in the BCA to receive payment. In the event that we and any dissenting shareholder fail to agree on a price for the common shares, the BCA procedures involve, among other things, the institution of proceedings in the high court of the Republic of the Marshall Islands or in any appropriate court in any jurisdiction in which our shares are primarily traded on a local or national securities exchange.

Shareholders' derivative actions

The BCA authorizes corporations to limit or eliminate the personal liability of directors to corporations and their shareholders for monetary damages for certain breaches of directors' fiduciary duties. Our amended and restated articles of incorporation and amended and restated bylaws include a provision that eliminates the personal liability of directors for monetary damages for actions taken as a director to the fullest extent permitted by law. Our amended and restated articles of incorporation provide that we must indemnify our directors and officers to the fullest extent authorized by law, and further, that we may advance expenses incurred while defending a civil or criminal proceeding. The foregoing obligations could result in us incurring substantial expenditures to cover the cost of settlement or damage awards against our officers and directors, which we may be unable to recoup.

Our amended and restated bylaws further permit us to secure insurance on behalf of any officer, director or employee for any liability arising out of his or her actions, regardless of whether Marshall Islands law would permit indemnification. We have purchased a policy of directors' and officers' liability insurance that insures our directors and officers against the cost of defense, settlement or payment of a judgment in some circumstances and insures us against our obligations to indemnify the directors and officers.

These provisions and resultant costs may discourage us and our shareholders from bringing a lawsuit against our officers and directors for breaches of their fiduciary duties, and may similarly reduce the likelihood of derivative litigation by our shareholders against our officers and directors even though such actions, if successful, might otherwise benefit us and our shareholders. Furthermore, a shareholder's investment may be adversely affected to the extent we pay the costs of settlement and damage awards against directors and officers pursuant to these indemnification provisions. We believe that these provisions, the insurance and the indemnity agreements are necessary to attract and retain talented and experienced directors and officers.

Insofar as indemnification for liabilities arising under the Securities Act may be permitted to our directors, officers and controlling persons pursuant to the foregoing provisions, or otherwise, we have been advised that in the opinion of the SEC such indemnification is against public policy as expressed in the Securities Act and is, therefore, unenforceable.

There is currently no pending material litigation or proceeding involving any of our directors, officers or employees for which indemnification is sought.

Anti-takeover effect of certain provisions of our Amended and Restated Articles of Incorporation and Amended and Restated Bylaws

Several provisions of our amended and restated articles of incorporation and amended and restated bylaws, which are summarized below, may have anti-takeover effects. These provisions are intended to avoid costly takeover battles, lessen our vulnerability to a hostile change of control and enhance the ability of our board of directors to maximize shareholder value in connection with any unsolicited offer to acquire us. However, these anti-takeover provisions, which are summarized below, could also discourage, delay or prevent (1) the merger or acquisition of us by means of a tender offer, a proxy contest or otherwise that a shareholder may consider in its best interest and (2) the removal of incumbent officers and directors.

| 23 |

Blank check preferred stock

Under the terms of our amended and restated articles of incorporation, our board of directors has authority, without any further vote or action by our shareholders, to issue up to 50,000,000 shares of blank check preferred stock. Our board of directors may issue preferred shares on terms calculated to discourage, delay or prevent a change of control of us or the removal of our management and might harm the market price of our common shares. We have no current plans to issue any preferred shares.

Election and removal of directors

Our amended and restated articles of incorporation prohibit cumulative voting in the election of directors. Our amended and restated bylaws require parties other than the board of directors to give advance written notice of nominations for the election of directors. Our amended and restated articles of incorporation also provide that our directors may be removed for cause upon the affirmative vote of not less than 70% of the outstanding shares of our capital stock entitled to vote for those directors. These provisions may discourage, delay or prevent the removal of incumbent officers and directors.

Limited actions by shareholders

Our amended and restated articles of incorporation and our amended and restated bylaws provide that any action required or permitted to be taken by our shareholders must be effected at an annual or special meeting of shareholders or by the unanimous written consent of our shareholders. Our amended and restated articles of incorporation and our amended and restated bylaws provide that, unless otherwise prescribed by law, only a majority of our board of directors or the Chief Executive Officer may call special meetings of our shareholders and the business transacted at the special meeting is limited to the purposes stated in the notice. Accordingly, a shareholder will be prevented from calling a special meeting for shareholder consideration of a proposal unless scheduled by our board of directors and shareholder consideration of a proposal may be delayed until the next annual meeting.

Advance notice requirements for shareholder proposals and director nominations

Our amended and restated bylaws provide that shareholders seeking to nominate candidates for election as directors or to bring business before an annual meeting of shareholders must provide timely notice of their proposal in writing to the corporate secretary. Generally, to be timely, a shareholder's notice must be received at our principal executive offices not less than 150 days nor more than 180 days prior to the one year anniversary of the immediately preceding annual meeting of shareholders. Our amended and restated bylaws also specify requirements as to the form and content of a shareholder's notice. These provisions may impede shareholders' ability to bring matters before an annual meeting of shareholders or make nominations for directors at an annual meeting of shareholders.

Classified Board of Directors

As described above, our amended and restated articles of incorporation provide for the division of our board of directors into three classes of directors, with each class as nearly equal in number as possible, serving staggered three year terms beginning on the expiration of the initial term for each class. Accordingly, approximately one-third of our board of directors will be elected each year. This classified board provision could discourage a third party from making a tender offer for our shares or attempting to obtain control of us. It could also delay shareholders who do not agree with the policies of our board of directors from removing a majority of our board of directors for two years.

Listing

Our units, Class A common shares and warrants are listing for trading on NASDAQ under the symbols "HUNTU", "HUNT" and "HUNTW", respectively.

| 24 |

Transfer Agent

The registrar and transfer agent for securities and the warrant agent for our warrants is Continental Stock Transfer & Trust Company.

| C. | Material Contracts |

All material contracts entered into other than during the ordinary course of our business and for the two years preceding the date hereof are described elsewhere in this Shell Company Report on Form 20-F or in the information incorporated by reference herein.

| D. | Exchange Controls |

The disclosure under the caption “Description of the Combined Company Following the Business Combination – Regulations Relating to Foreign Exchange” beginning on page 82 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| E. | Taxation |

The disclosure under the caption “Material U.S. Federal Income Tax Consequences” beginning on page 129 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

| F. | Dividends and Paying Agents |

None.

| G. | Statement by Experts |

Not applicable.

| H. | Documents on Display |

Documents concerning us that are referred to in this document may be inspected at our principal executive offices at Tower A, WangXin Building, 28 Xiaoyun Rd, Chaoyang District, Beijing, 100027.

In addition, we will file annual reports and other information with the Securities and Exchange Commission. We will file annual reports on Form 20-F and submit other information under cover of Form 6-K. As a foreign private issuer, we are exempt from the proxy requirements of Section 14 of the Exchange Act and our officers, directors and principal shareholders will be exempt from the insider short-swing disclosure and profit recovery rules of Section 16 of the Exchange Act. The Commission maintains a web site that contains reports and other information regarding registrants (including us) that file electronically with the Commission which can be assessed at http://www.sec.gov.

| I. | Subsidiary Information |

Not required.

ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK

The disclosure under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations of NCF Wealth Group - Quantitative and Qualitative Disclosures about Market Risk” beginning on page 116 of the Company’s offer to purchase dated February 12, 2019 included as exhibit (a)(1)(A) to the Company’s Schedule TO dated February 12, 2019 is incorporated by reference herein.

ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES

Not applicable.

| 25 |

| ITEM 13. | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES. |

Not required.

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

Not required.

| ITEM 15. | CONTROLS AND PROCEDURES. |

Not required.

| ITEM 16. | [RESERVED] |