UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

_________________________________________________________________________________

OF THE SECURITIES EXCHANGE ACT OF 1934

| For the Fiscal Year Ended | Commission File Number | |||||||||||||

| State of Incorporation | I.R.S. Employer Identification No. | ||||

Principal Executive Offices

Telephone Number: (856 ) 342-4800

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. þ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. ☐ Yes þ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). þ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

☑ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes þ No

Based on the closing price on the New York Stock Exchange on January 28, 2022 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of capital stock held by non-affiliates of the registrant was approximately $8,597,234,004 . There were 299,364,411 shares of capital stock outstanding as of September 14, 2022.

Portions of the Registrant’s Proxy Statement for the 2022 Annual Meeting of Shareholders are incorporated by reference into Part III.

TABLE OF CONTENTS

Information about our Executive Officers | ||||||||

Item 6. Reserved | ||||||||

2

PART I

This Report contains "forward-looking" statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements reflect our current expectations regarding our future results of operations, economic performance, financial condition and achievements. These forward-looking statements can be identified by words such as "anticipate," "believe," "estimate," "expect," "intend," "plan," "pursue," "strategy," "target," "will" and similar expressions. One can also identify forward-looking statements by the fact that they do not relate strictly to historical or current facts, and may reflect anticipated cost savings or implementation of our strategic plan. These statements reflect our current plans and expectations and are based on information currently available to us. They rely on several assumptions regarding future events and estimates which could be inaccurate and which are inherently subject to risks and uncertainties. Risks and uncertainties include, but are not limited to, those discussed in "Risk Factors" and in the "Cautionary Factors That May Affect Future Results" in "Management’s Discussion and Analysis of Financial Condition and Results of Operations" in this Report. Our consolidated financial statements and the accompanying notes to the consolidated financial statements are presented in "Financial Statements and Supplementary Data."

Item 1. Business

The Company

Unless otherwise stated, the terms "we," "us," "our" and the "company" refer to Campbell Soup Company and its consolidated subsidiaries.

We are a manufacturer and marketer of high-quality, branded food and beverage products. We organized as a business corporation under the laws of New Jersey on November 23, 1922; however, through predecessor organizations, we trace our heritage in the food business back to 1869. Our principal executive offices are in Camden, New Jersey 08103-1799.

Business Divestitures

We completed the sale of our Kelsen business on September 23, 2019. On December 23, 2019, we completed the sale of our Arnott’s business and certain other international operations, including the simple meals and shelf-stable beverages businesses in Australia and Asia Pacific (the Arnott’s and other international operations). In addition, on October 11, 2019, we completed the sale of our European chips business.

We used the net proceeds from the sales to reduce debt as described below in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

Beginning in the fourth quarter of 2019, we have reflected the results of operations of our Kelsen business and the Arnott’s and other international operations (collectively referred to as Campbell International) as discontinued operations in the Consolidated Statements of Earnings for all periods presented. These businesses were historically included in the Snacks reportable segment. The results of the European chips business through the date of sale were reflected in continuing operations within the Snacks reportable segment.

In the fourth quarter of 2021, we completed the sale of our Plum baby food and snacks business. The results of the Plum baby food and snacks business through the date of sale were reflected in continuing operations within the Meals & Beverages reportable segment.

See Note 3 to the Consolidated Financial Statements for additional information on our divestitures.

Reportable Segments

Our reportable segments are:

•Meals & Beverages, which consists of our soup, simple meals and beverages products in retail and foodservice in the U.S. and Canada. The segment includes the following products: Campbell’s condensed and ready-to-serve soups; Swanson broth and stocks; Pacific Foods broth, soups and non-dairy beverages; Prego pasta sauces; Pace Mexican sauces; Campbell’s gravies, pasta, beans and dinner sauces; Swanson canned poultry; V8 juices and beverages; and Campbell’s tomato juice. The segment also includes snacking products in foodservice and Canada. The segment included the results of our Plum baby food and snacks business, which was sold on May 3, 2021; and

•Snacks, which consists of Pepperidge Farm cookies*, crackers, fresh bakery and frozen products, including Goldfish crackers*, Snyder’s of Hanover pretzels*, Lance sandwich crackers*, Cape Cod potato chips*, Kettle Brand potato chips*, Late July snacks*, Snack Factory pretzel crisps*, Pop Secret popcorn, Emerald nuts, and other snacking products in retail in the U.S. Beginning in 2022, we refer to the * brands as our "power brands." The segment includes the retail business in Latin America. The segment also included the results of our European chips business, which was sold on October 11, 2019.

Beginning in 2022, the foodservice and Canadian business formerly included in our Snacks segment is now managed as part of the Meals & Beverages segment. Segment results have been adjusted retrospectively to reflect this change. See Note 6 to

3

the Consolidated Financial Statements and "Management's Discussion and Analysis of Financial Condition and Results of Operations" for additional information regarding our reportable segments.

Ingredients and Packaging

The ingredients and packaging materials required for the manufacture of our food and beverage products are purchased from various suppliers, substantially all of which are located in North America. During 2022, we experienced significantly elevated commodity and supply chain costs including the costs of labor, raw materials, energy, fuel, packaging materials and other inputs necessary for the production and distribution of our products. In addition, many of these items are subject to price fluctuations from a number of factors, including but not limited to climate change, changes in crop size, cattle cycles, herd and flock disease, crop disease, crop pests, product scarcity, demand for raw materials, commodity market speculation, energy costs, currency fluctuations, supplier capacities, government-sponsored agricultural programs and other government policy, import and export requirements (including tariffs), drought and excessive rain, temperature extremes and other adverse weather events, water scarcity, scarcity of suitable agricultural land, scarcity of organic ingredients, pandemic illness (such as the COVID-19 pandemic), armed hostilities (including the ongoing conflict between Russia and Ukraine) and other factors that may be beyond our control. To help reduce some of this price volatility, we use a combination of purchase orders, short- and long-term contracts, inventory management practices and various commodity risk management tools for most of our ingredients and packaging. Ingredient inventories are generally at a peak during the late fall and decline during the winter and spring. Since many ingredients of suitable quality are available in sufficient quantities only during certain seasons, we make commitments for the purchase of such ingredients in their respective seasons. Although we are unable to predict the impact of our ability to source these ingredients and packaging materials in the future, we expect these supply pressures to continue throughout 2023. We also expect the pressures of input cost inflation to continue into 2023.

Customers

In most of our markets, sales and merchandising activities are conducted through our own sales force and/or third-party brokers and distribution partners. Our products are generally resold to consumers through retail food chains, mass discounters, mass merchandisers, club stores, convenience stores, drug stores, dollar stores, e-commerce and other retail, commercial and non-commercial establishments. Our Snacks segment has a direct-store-delivery distribution model that uses independent contractor distributors.

Our five largest customers accounted for approximately 47 % of our consolidated net sales from continuing operations in 2022, 46% in 2021 and 44% in 2020. Our largest customer, Wal-Mart Stores, Inc. and its affiliates, accounted for approximately 22 % of our consolidated net sales from continuing operations in 2022 and 21

Trademarks and Technology

As of September 14, 2022, we owned over 2,800 trademark registrations and applications in over 150 countries. We believe our trademarks are of material importance to our business. Although the laws vary by jurisdiction, trademarks generally are valid as long as they are in use and/or their registrations are properly maintained and have not been found to have become generic. Trademark registrations generally can be renewed indefinitely as long as the trademarks are in use. We believe that our principal brands, including Campbell's, Cape Cod, Chunky, Emerald, Goldfish, Kettle Brand, Lance, Late July, Milano, Pace, Pacific Foods, Pepperidge Farm, Pop Secret, Prego, Snack Factory, Snyder's of Hanover, Spaghettios, Swanson, and V8, are protected by trademark law in the major markets where they are used.

Although we own a number of valuable patents, we do not regard any segment of our business as being dependent upon any single patent or group of related patents. In addition, we own copyrights, both registered and unregistered, proprietary trade secrets, technology, know-how, processes and other intellectual property rights that are not registered.

Competition

We operate in a highly competitive industry and experience competition in all of our categories. This competition arises from numerous competitors of varying sizes across multiple food and beverage categories, and includes producers of private label products, as well as other branded food and beverage manufacturers. Private label products are generally sold at lower prices than branded products. Competitors market and sell their products through traditional retailers and e-commerce. All of these competitors vie for trade merchandising support and consumer dollars. The number of competitors cannot be reliably estimated. Our principal areas of competition are brand recognition, taste, nutritional value, price, promotion, innovation, shelf space and customer service.

Capital Expenditures

During 2022, our aggregate capital expenditures were $242 million. We expect to spend approximately $325 million for capital projects in 2023. Major capital projects based on planned spend in 2023 include a cracker capacity expansion for our Snacks business and a new manufacturing line for our Meals & Beverages business.

4

Government Regulation

The manufacture and sale of consumer food products is highly regulated. In the U.S., our activities are subject to regulation by various federal government agencies, including the Food and Drug Administration, the Department of Agriculture, the Federal Trade Commission, the Department of Labor, the Department of Commerce, the Occupational Safety and Health Administration and the Environmental Protection Agency, as well as various state and local agencies. Our business is also regulated by similar agencies outside of the U.S. Additionally, we are subject to data privacy and security regulations, tax and securities regulations, accounting and reporting standards, and other financial laws and regulations. We believe that we are in compliance with current laws and regulations in all material respects and do not expect that continued compliance with such laws and regulations will have a material effect on capital expenditures, earnings or our competitive position.

Environmental Matters

We have requirements for the operation and design of our facilities that meet or exceed applicable environmental rules and regulations. Of our $242 million in capital expenditures made during 2022, approximately $9 million were for compliance with environmental laws and regulations in the U.S. We further estimate that approximately $13 million of the capital expenditures anticipated during 2023 will be for compliance with U.S. environmental laws and regulations. We believe that the continued compliance with existing environmental laws and regulations (both within the U.S. and elsewhere) will not have a material effect on capital expenditures, earnings or our competitive position. In addition, we continue to monitor existing and pending environmental laws and regulations within the U.S. and elsewhere relating to climate change and greenhouse gas emissions. While the impact of these laws and regulations cannot be predicted with certainty, we do not believe that compliance with these laws and regulations will have a material effect on capital expenditures, earnings or our competitive position.

Seasonality

Demand for soup products is seasonal, with the fall and winter months usually accounting for the highest sales volume. Demand for our other products is generally evenly distributed throughout the year.

Human Capital Management

A core pillar of our strategic plan is to build a winning team and culture. To do this, we are committed to building a company where everyone can be real, and feel safe, valued and supported to do their best work. We believe that our employees are the driving force behind our success and prioritize attracting, developing and retaining diverse, world-class talent and creating an inclusive culture that embodies our purpose: Connecting people through food they love. On July 31, 2022, we had approximately 14,700 employees.

Training, Development and Engagement

We invest in our employees through training and development programs. We have partnered with leading online content experts and have recently increased internal learning development to expand our catalog of courses and support our culture of continuous learning. A suite of training and education programs are available to employees ranging from role-specific training to education on soft skills to assist them with enhancing their careers through continuous learning. Through objective-setting, individual development plans, learning opportunities, feedback and coaching, employees are encouraged to continue their professional growth. Our education programs allow employees to focus on timely and topical development areas including leadership, management excellence, functional capabilities and inclusion and diversity. We communicate frequently and transparently with our employees through regular company-wide and business unit check-ins, and we conduct employee engagement surveys that provide our employees with an opportunity to share anonymous feedback with management in a variety of areas including confidence in leadership, growth and career opportunities, available resources, compensation and overall engagement. These surveys allow our leaders to develop action plans for their business units as well as the broader organization.

Our Campbell Employee Experience Framework enhances the foundational moments that are key to an employee's career at our company - from the candidate experience and onboarding through career advancement - to help our employees thrive at work, with the goal of building an inclusive, engaging and high-performing culture.

Inclusion and Diversity

We believe that having an inclusive and diverse culture strengthens our ability to recruit and develop talent and allows all employees to thrive and succeed. Diversity of input and perspectives is an essential part of our strategic plan to build a winning team and culture, and we believe one key to success is attracting and retaining a diverse workforce that reflects our consumers of today and tomorrow. Our commitment to inclusion and diversity ("I&D") is based on three guiding pillars:

•Capabilities - providing resources and tools to employees to build capabilities to build a winning team and culture and to drive systemic change;

•Advocacy - strengthening ally networks by supporting our employees, our partners and the communities where we live and work; and

5

•Accountability - having individual, management and organizational accountability and transparency about our progress on building an inclusive culture.

We also continue to provide I&D learning experiences and foster employee resource groups to highlight issues that impact underrepresented communities. Throughout 2022 the board of directors (Board) received regular updates from management on our inclusion and diversity efforts.

Wellness and Safety

Our employees' health, safety and well-being are our top priorities. We have maintained an unwavering commitment to supporting the health and well-being of our employees during the COVID-19 pandemic and we implemented an enterprise-wise response to ensure safety. We have implemented safety and sanitation measures to help ensure employees' health and well-being, embraced remote work for those who were able, and introduced enhanced sanitation, mask use and other protective equipment protocols and social distancing measures for our front-line employees.

In addition, our Resources for Living program provides information, education tools and resources to help support our employees' physical, financial, social and emotional well-being. As part of this focus on well-being, we emphasize the need for our employees to embrace healthy lifestyles and we offer a variety of wellness education opportunities for our employees. We continue to modernize our workspaces and in 2022 announced a hybrid work policy to allow office-based employees to work remotely several days per week.

Total Rewards

We provide market-based competitive compensation through our salary, annual incentive and long-term incentive programs, and a robust benefits package that promotes the overall well-being of our employees. We provide a variety of resources and services to help our employees plan for retirement and provide a 401(k) plan with immediate vesting. We benchmark and establish compensation structures based on competitive market data. Individual pay is based on various factors such as an employee's role, experience, job location and contributions. Performance discussions for salaried employees are conducted throughout the year to assess contributions and inform individual development plans. We have enhanced our focus on the employee experience by highlighting key moments in the employment life-cycle and providing enhanced communications about our comprehensive offerings.

Websites

Our primary corporate website can be found at www.campbellsoupcompany.com. We make available free of charge at the Investor portion of this website (under the "About Us—Investors—Financials—SEC Filings" caption) all of our reports (including amendments) filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, including our annual reports on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K. These reports are made available on the website as soon as reasonably practicable after their filing with, or furnishing to, the Securities and Exchange Commission.

All websites appearing in this Annual Report on Form 10-K are inactive textual references only, and the information in, or accessible through, such websites is not incorporated into this Annual Report on Form 10-K, or into any of our other filings with the Securities and Exchange Commission.

Item 1A. Risk Factors

In addition to the factors discussed elsewhere in this Report, the following risks and uncertainties could materially adversely affect our business, financial condition and results of operations. Although the risks are organized and described separately, many of the risks are interrelated. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations and financial condition.

Business and Operational Risks

We may not be able to increase prices to fully offset inflationary pressures on costs, such as raw and packaging materials, labor and distribution costs

As a manufacturer of food and beverage products, we rely on plant labor, distribution resources and raw and packaging materials including tomato paste, grains, beef, poultry, dairy, vegetable oil, wheat, potatoes and other vegetables, steel, aluminum, glass, paper and resin. During 2022, we experienced significantly elevated commodity and supply chain costs including the costs of labor, raw materials, energy, fuel, packaging materials and other inputs necessary for the production and distribution of our products, and we expect elevated levels of inflation to continue in 2023. In addition, many of these materials are subject to price fluctuations from a number of factors, including but not limited to changes in crop size, cattle cycles, herd and flock disease, crop disease, crop pests, product scarcity, demand for raw materials, commodity market speculation, energy costs, currency fluctuations, supplier capacities, government-sponsored agricultural programs and other government policy, import and export requirements (including tariffs), drought and excessive rain, temperature extremes and other adverse weather events, water scarcity, scarcity of suitable agricultural land, scarcity of organic ingredients, pandemic illness (such as the

6

COVID-19 pandemic), armed hostilities (including the ongoing conflict between Russia and Ukraine) and other factors that may be beyond our control.

We try to mitigate some or all cost increases through increases in the selling prices of, or decreases in the packaging sizes of, some of our products. Higher product prices or smaller packaging sizes may result in reductions in sales volume. Consumers may be less willing to pay a price differential for our branded products and may increasingly purchase lower-priced offerings, or may forego some purchases altogether, during an economic downturn or times of increased inflationary pressure. To the extent that price increases or packaging size decreases are not sufficient to offset these increased costs adequately or in a timely manner, and/or if they result in significant decreases in sales volume, our business results and financial condition may be adversely affected. Furthermore, we may not be able to fully offset any cost increases through productivity initiatives or through our commodity hedging activity.

Disruption to our supply chain could adversely affect our business

Our ability to manufacture and/or sell our products may be impaired by damage or disruption to our manufacturing, warehousing or distribution capabilities, or to the capabilities of our suppliers, contract manufacturers, logistics service providers or independent distributors. This damage or disruption could result from execution issues, as well as factors that are hard to predict or beyond our control such as increased temperatures due to climate change, water stress, extreme weather events, natural disasters, product or raw material scarcity, fire, terrorism, pandemics (such as the COVID-19 pandemic), armed hostilities (including the ongoing conflict between Russia and Ukraine), strikes, labor shortages, cybersecurity breaches, government shutdowns, disruptions in logistics, supplier capacity constraints or other events. Commodity prices continue to be volatile and generally increased due to the COVID-19 pandemic, supply chain disruptions and labor and transportation shortages. Production of the agricultural commodities used in our business may also be adversely affected by drought and excessive rain, temperature extremes and other adverse weather events, water scarcity, scarcity of suitable agricultural land, scarcity of organic ingredients, crop size, cattle cycles, herd and flock disease, crop disease and crop pests. Failure to take adequate steps to mitigate the likelihood or potential impact of such events, or to effectively manage such events if they occur, may adversely affect our business or financial results, particularly in circumstances when a product is sourced from a single supplier or location. Disputes with significant suppliers, contract manufacturers, logistics service providers or independent distributors, including disputes regarding pricing or performance, may also adversely affect our ability to manufacture and/or sell our products, as well as our business or financial results.

We have experienced temporary workforce disruptions in our supply chain as a result of the COVID-19 pandemic. We have implemented employee safety measures, which exceed guidance from the Centers for Disease Control and Prevention and World Health Organization, across all our supply chain facilities. Even with these measures, and the availability of vaccines, given the emergence and spread of COVID-19 variants, there is continued risk that COVID-19 may spread through our workforce. Illness, labor shortages, absenteeism, or other workforce disruptions could negatively affect our supply chain, manufacturing, distribution, or other business processes. We may face additional production disruptions in the future, which may place constraints on our ability to produce products in a timely manner or may increase our costs.

Short-term or sustained increases in consumer demand at our retail customers may exceed our production capacity or otherwise strain our supply chain. Our failure to meet the demand for our products could adversely affect our business and results of operations.

The COVID-19 pandemic and related ongoing implications could adversely impact our business and results of operations

The COVID-19 pandemic has had, and could continue to have, a negative impact on financial markets, economic conditions, and portions of our industry as a result of changes in consumer behavior, retailer inventory levels, cost inflation, manufacturing and supply chain disruption, vaccination rates and effectiveness, and overall macroeconomic conditions. Although our business has benefited from increased at-home consumption due to COVID-19, our ability to sustain heightened sales is dependent on consumer purchasing behavior. The continued availability and effectiveness of vaccines may partially mitigate the risks around the continued spread of COVID-19, however, with the spread of the COVID-19 variants, the ongoing implications of the COVID-19 pandemic could adversely impact our business and results of operations in a number of ways, including but not limited to:

•a shutdown of one or more of our manufacturing, warehousing or distribution facilities, or disruption in our supply chain, including but not limited to, as a result of illness, labor shortages, government restrictions or other workforce disruptions;

•the failure of third parties on which we rely, including but not limited to, those that supply our packaging, ingredients, equipment and other necessary operating materials, co-manufacturers and independent contractors, to meet their obligations to us, or significant disruptions in their ability to do so;

7

•a strain on our supply chain, which could result from short-term or sustained changes and volatility in consumer purchasing and consumption patterns that increase demand at our retail customers and exceed our production capacity for our products;

•continued volatility in commodity and other input costs, which may not be sufficiently offset by our commodity hedging activities;

•a disruption to our distribution capabilities or to our distribution channels, including those of our suppliers, contract manufacturers, logistics service providers or independent distributors;

•new or escalated government or regulatory responses in markets where we manufacture, sell or distribute our products, or in the markets of third parties on which we rely, could prevent or disrupt our business operations;

•a significant portion of our workforce, including our management team, could become unable to work as a result of illness, or the attention of our management team could be diverted if key employees become ill and become unable to work;

•a change in demand for or availability of our products as a result of retailers, distributors, or carriers modifying their inventory, fulfillment or shipping practices;

•an inability to effectively modify our trade promotion and advertising activities to reflect changing consumer shopping habits due to, among other things, reduced in-store visits and travel restrictions;

•a shift in consumer spending during periods of economic uncertainty or inflation could result in consumers moving to private label or lower price products; and

•additional business disruptions and uncertainties related to the COVID-19 pandemic could result in additional delays or modifications to our strategic plans and other initiatives.

These and other impacts of the COVID-19 pandemic could also have the effect of heightening many of the other risk factors included in this Item 1A. The ultimate impact depends on the severity and duration of the COVID-19 pandemic, including the emergence and spread of COVID-19 variants, the continued availability and effectiveness of vaccines and actions taken by governmental authorities and other third parties in response to the pandemic, each of which is uncertain, rapidly changing and difficult to predict. Any of these disruptions could adversely impact our business and results of operations.

Our results of operations can be adversely affected by labor shortages, turnover and labor cost increases

Labor is a primary component of operating our business. A number of factors may adversely affect the labor force available to us or increase labor costs, including high employment levels, federal unemployment subsidies, and other government regulations. During 2022, we observed an overall tightening and increasingly competitive labor market. A sustained labor shortage or increased turnover rates within our employee base, caused by the continued spread of COVID-19 or as a result of general macroeconomic factors, could lead to increased costs, such as increased overtime to meet demand and increased wage rates to attract and retain employees, and could negatively affect our ability to efficiently operate our manufacturing and distribution facilities and overall business. If we are unable to hire and retain employees capable of performing at a high-level, or if mitigation measures we may take to respond to a decrease in labor availability, such as overtime and third-party outsourcing, have unintended negative effects, our business could be adversely affected. In addition, we distribute our products and receive raw materials primarily by truck. Reduced availability of trucking capacity due to shortages of drivers has caused an increase in the cost of transportation for us and our suppliers. An overall labor shortage, lack of skilled labor, increased turnover or labor inflation, caused by COVID-19 or as a result of general macroeconomic factors, could have a material adverse impact on the company’s operations, results of operations, liquidity or cash flows.

Our intellectual property rights are valuable, and any inability to protect them could reduce the value of our products and brands

We consider our intellectual property rights, particularly our trademarks, to be a significant and valuable aspect of our business. We protect our intellectual property rights through a combination of trademark, patent, copyright and trade secret protection, contractual agreements and policing of third-party misuses of our intellectual property. Our failure to obtain or adequately protect our intellectual property or any change in law that lessens or removes the current legal protections of our intellectual property may diminish our competitiveness and adversely affect our business and financial results.

Competing intellectual property claims that impact our brands or products may arise unexpectedly. Any litigation or disputes regarding intellectual property may be costly and time-consuming and may divert the attention of our management and key personnel from our business operations. We also may be subject to significant damages or injunctions against development, launch and sale of certain products. Any of these occurrences may harm our business and financial results.

8

Our results may be adversely impacted if consumers do not maintain their favorable perception of our brands

We have a number of iconic brands with significant value. Maintaining and continually enhancing the value of these brands is critical to the success of our business. Brand value is primarily based on consumer perceptions. Success in promoting and enhancing brand value depends in large part on our ability to provide high-quality products. Brand value could diminish significantly due to a number of factors, including consumer perception that we have acted in an irresponsible manner, adverse publicity about our products, packaging or ingredients (whether or not valid), our failure to maintain the quality of our products, the failure of our products to deliver consistently positive consumer experiences, or the products becoming unavailable to consumers. The growing use of social and digital media by consumers increases the speed and extent that information and opinions can be shared. Negative posts or comments about us, our brands, products or packaging on social or digital media could seriously damage our brands and reputation. If we do not maintain the favorable perception of our brands, our results could be adversely impacted.

We may be adversely impacted by a disruption, failure or security breach of our information technology systems

Our information technology systems are critically important to our operations. We rely on our information technology systems (some of which are outsourced to third parties) to manage our data, communications and business processes, including our marketing, sales, manufacturing, procurement, logistics, customer service, accounting and administrative functions and the importance of such networks and systems has increased due to an increase in our employees working remotely. If we do not obtain and effectively manage the resources and materials necessary to build, sustain and protect appropriate information technology systems, our business or financial results could be adversely impacted. Furthermore, our information technology systems are subject to attack or other security breaches (including the access to or acquisition of customer, consumer, employee or other confidential information), service disruptions or other system failures. If we are unable to prevent or adequately respond to and resolve these breaches, disruptions or failures, our operations may be impacted, and we may suffer other adverse consequences such as reputational damage, litigation, remediation costs, ransomware payments and/or penalties under various data protection laws and regulations.

To address the risks to our information technology systems and the associated costs, we maintain an information security program that includes updating technology and security policies, cyber insurance, employee awareness training, and monitoring and routine testing of our information technology systems. We believe that these preventative actions provide adequate measures of protection against security breaches and generally reduce our cybersecurity risks, however, cyber threats are constantly evolving, are becoming more frequent and more sophisticated and are being made by groups of individuals with a wide range of expertise and motives, which increases the difficulty of detecting and successfully defending against them. Additionally, continued geopolitical turmoil, including the ongoing conflict between Russia and Ukraine, has heightened the risk of cyberattacks. We have experienced threats to our data and systems and although we have not experienced a material incident to date, there can be no assurance that these measures will prevent or limit the impact of a future incident. We may incur significant costs in protecting against or remediating cyberattacks or other cyber incidents.

In addition, in the event our suppliers or customers experience a breach or system failure, their businesses could be disrupted or otherwise negatively affected, which may result in a disruption in our supply chain or reduced customer orders, which would adversely affect our business and financial results. We have also outsourced several information technology support services and administrative functions to third-party service providers, and may outsource other functions in the future to achieve cost savings and efficiencies. Our information security program includes capabilities designed to evaluate and mitigate cyber risks arising from third-party service providers. We believe that these capabilities provide insights and visibility to the security posture of our third-party service providers, however, cyber threats to those organizations are beyond our control. If these service providers do not perform effectively due to breach or system failure, we may not be able to achieve the expected benefits and our business may be disrupted.

We may not be able to attract and retain the highly skilled people we need to support our business

We depend on the skills and continued service of key personnel, including our experienced management team. In addition, our ability to achieve our strategic and operating goals depends on our ability to identify, hire, train and retain qualified individuals. We also compete with other companies both within and outside of our industry for talented personnel, and we may lose key personnel or fail to attract, train and retain other talented personnel. Any such loss or failure may adversely affect our business or financial results. In addition, activities related to identifying, recruiting, hiring and integrating qualified individuals may require significant time and expense. We may not be able to locate suitable replacements for any key employees who leave, or offer employment to potential replacements on reasonable terms, each of which may adversely affect our business and financial results.

If we do not fully realize the expected cost savings and/or operating efficiencies associated with our strategic initiatives, our profitability could suffer

Our future success and earnings growth depend in part on our ability to achieve the appropriate cost structure and operate efficiently in the highly competitive food industry, particularly in an environment of volatile cost inputs. We continuously

9

pursue initiatives to reduce costs and increase effectiveness. See "Management's Discussion and Analysis of Financial Condition and Results of Operations - Restructuring Charges and Cost Savings Initiatives" for additional information on these initiatives. We also regularly pursue cost productivity initiatives in procurement, manufacturing and logistics. Any failure or delay in implementing our initiatives in accordance with our plans could adversely affect our ability to meet our long-term growth and profitability expectations and could adversely affect our business. If we do not continue to effectively manage costs and achieve additional efficiencies, our competitiveness and our profitability could decrease.

Our results may be adversely affected by our inability to complete or realize the projected benefits of acquisitions, divestitures and other strategic transactions

We have historically made strategic acquisitions of brands and businesses and we may undertake additional acquisitions or other strategic transactions in the future. Our ability to meet our objectives with respect to acquisitions and other strategic transactions may depend in part on our ability to identify suitable counterparties, negotiate favorable financial and other contractual terms, obtain all necessary regulatory approvals on the terms expected and complete those transactions. Potential risks also include:

•the inability to integrate acquired businesses into our existing operations in a timely and cost-efficient manner, including implementation of enterprise-resource planning systems;

•diversion of management's attention from other business concerns;

•potential loss of key employees, suppliers and/or customers of acquired businesses;

•assumption of unknown risks and liabilities;

•the inability to achieve anticipated benefits, including revenues or other operating results;

•operating costs of acquired businesses may be greater than expected;

•the inability to promptly implement an effective control environment; and

•the risks inherent in entering markets or lines of business with which we have limited or no prior experience.

In addition, we have previously made strategic divestitures and may do so in the future. Any businesses we decide to divest in the future may depend in part on our ability to identify suitable buyers, negotiate favorable financial and other contractual terms and obtain all necessary regulatory approvals on the terms expected. Potential risks of divestitures may also include:

•diversion of management's attention from other business concerns;

•loss of key suppliers and/or customers of divested businesses;

•the inability to separate divested businesses or business units effectively and efficiently from our existing business operations; and

•the inability to reduce or eliminate associated overhead costs.

If we are unable to complete or realize the projected benefits of future acquisitions, divestitures or other strategic transactions, our business or financial results may be adversely impacted.

Competitive and Industry Risks

We face significant competition in all our product categories, which may result in lower sales and margins

We operate in the highly competitive food and beverage industry mainly in the North American market and experience competition in all of our categories. The principal areas of competition are brand recognition, taste, nutritional value, price, promotion, innovation, shelf space and customer service. A number of our primary competitors are larger than us and have substantial financial, marketing and other resources, and some of our competitors may spend more aggressively on advertising and promotional activities than we do. In addition, reduced barriers to entry and easier access to funding are creating new competition. A strong competitive response from one or more of these competitors to our marketplace efforts, or a continued shift towards private label offerings, particularly during periods of economic uncertainty or significant inflation, could result in us reducing prices, increasing marketing or other expenditures, and/or losing market share, each of which may result in lower sales and margins.

10

Our ability to compete also depends upon our ability to predict, identify, and interpret the tastes and dietary habits of consumers and to offer products that appeal to those preferences. There are inherent marketplace risks associated with new product or packaging introductions, including uncertainties about trade and consumer acceptance. If we do not succeed in offering products that consumers want to buy, our sales and market share will decrease, resulting in reduced profitability. If we are unable to accurately predict which shifts in consumer preferences will be long-lasting, or are unable to introduce new and improved products to satisfy those preferences, our sales will decline. Weak economic conditions, recessions, significant inflation and other factors, such as pandemics, could effect consumer preferences and demand. In addition, given the variety of backgrounds and identities of consumers in our consumer base, we must offer a sufficient array of products to satisfy the broad spectrum of consumer preferences. As such, we must be successful in developing innovative products across a multitude of product categories. In addition, the COVID-19 pandemic has altered, and in some cases, delayed product innovation efforts. Finally, if we fail to rapidly develop products in faster-growing and more profitable categories, we could experience reduced demand for our products, or fail to expand margins.

We may be adversely impacted by a changing customer landscape and the increased significance of some of our customers

Our businesses are largely concentrated in the traditional retail grocery trade, which has experienced slower growth than other retail channels, such as dollar stores, drug stores, club stores and e-commerce retailers. We expect this trend away from traditional retail grocery to alternate channels to continue in the future. These alternative retail channels may also create consumer price deflation, affecting our retail customer relationships and presenting additional challenges to increasing prices in response to commodity or other cost increases. In addition, retailers with increased buying power and negotiating strength are seeking more favorable terms, including increased promotional programs and customized products funded by their suppliers. These customers may also use more of their shelf space for their private label products, which are generally sold at lower prices than branded products. If we are unable to use our scale, marketing, product innovation and category leadership positions to respond to these customer dynamics, our business or financial results could be adversely impacted.

In 2022, our five largest customers accounted for approximately 47 % of our consolidated net sales from continuing operations, with the largest customer, Wal-Mart Stores, Inc. and its affiliates, accounting for approximately 22 % of our consolidated net sales from continuing operations. There can be no assurance that our largest customers will continue to purchase our products in the same mix or quantities, or on the same terms as in the past. Disruption of sales to any of these customers, or to any of our other large customers, for an extended period of time could adversely affect our business or financial results.

Financial and Economic Risks

An impairment of the carrying value of goodwill or other indefinite-lived intangible assets could adversely affect our financial results and net worth

As of July 31, 2022, we had goodwill of $3.979 billion and other indefinite-lived intangible assets of $2.549 billion. Goodwill and indefinite-lived intangible assets are initially recorded at fair value and not amortized, but are tested for impairment at least annually in the fourth quarter or more frequently if impairment indicators arise. We test goodwill at the reporting unit level by comparing the carrying value of the net assets of the reporting unit, including goodwill, to the unit's fair value. Similarly, we test indefinite-lived intangible assets by comparing the fair value of the assets to their carrying values. Fair value for both goodwill and other indefinite-lived intangible assets is determined based on a discounted cash flow analysis. If the carrying values of the reporting unit or indefinite-lived intangible assets exceed their fair value, the goodwill or indefinite-lived intangible assets are considered impaired. Factors that could result in an impairment include a change in revenue growth rates, operating margins, weighted average cost of capital, future economic and market conditions or assumed royalty rates. If current expectations for growth rates for sales and profits are not met, or other market factors and macroeconomic conditions that could be affected by the COVID-19 pandemic or otherwise were to change, we may be required in the future to record impairment of the carrying value of goodwill or other indefinite-lived intangible assets, which could adversely affect our financial results and net worth.

We may be adversely impacted by increased liabilities and costs related to our defined benefit pension plans

We sponsor a number of defined benefit pension plans for certain employees in the U.S. and certain non-U.S. locations. The major defined benefit pension plans are funded with trust assets invested in a globally diversified portfolio of securities and other investments. Changes in regulatory requirements or the market value of plan assets, investment returns, interest rates and mortality rates may affect the funded status of our defined benefit pension plans and cause volatility in the net periodic benefit cost, future funding requirements of the plans and the funded status as recorded on the balance sheet. A significant increase in our obligations, future funding requirements, or net periodic benefit costs could have a material adverse effect on our financial results.

11

We face risks related to heightened inflation, recession, financial and credit market disruptions and other economic conditions

Customer and consumer demand for our products may be impacted by weak economic conditions, recession, equity market volatility or other negative economic factors in the U.S. or other nations. For instance in 2022, the U.S. experienced significantly heightened inflationary pressures which we expect to continue into 2023. We may not be able to fully mitigate the impact of inflation through price increases, productivity initiatives and cost savings, which could have a material adverse effect on our financial results. In addition, if the U.S. economy enters a recession in 2023, we may experience sales declines and may have to decrease prices, all of which could have a material adverse impact on our financial results.

Similarly, disruptions in financial and/or credit markets may impact our ability to manage normal commercial relationships with our customers, suppliers and creditors and might cause us to not be able to continue to have access to preferred sources of liquidity when needed or on terms we find acceptable, and our borrowing costs could increase. An economic or credit crisis could occur and impair credit availability and our ability to raise capital when needed. A disruption in the financial markets may have a negative effect on our derivative counterparties and could impair our banking or other business partners, on whom we rely for access to capital and as counterparties to our derivative contracts. In addition, changes in tax or interest rates in the U.S. or other nations, whether due to recession, economic disruptions or other reasons, may adversely impact us.

Legal and Regulatory Risks

We may be adversely impacted by legal and regulatory proceedings or claims

We are a party to a variety of legal and regulatory proceedings and claims arising out of the normal course of business. See Note 18 to the Consolidated Financial Statements for information regarding reportable legal proceedings. Since these actions are inherently uncertain, there is no guarantee that we will be successful in defending ourselves against such proceedings or claims, or that our assessment of the materiality or immateriality of these matters, including any reserves taken in connection with such matters, will be consistent with the ultimate outcome of such proceedings or claims. In particular, the marketing of food products has come under increased scrutiny in recent years, and the food industry has been subject to an increasing number of proceedings and claims relating to alleged false or deceptive marketing under federal, state and foreign laws or regulations, including claims relating to the presence of heavy metals in food products. Additionally, the independent contractor distribution model, which is used in our Snacks segment, has also come under increased regulatory scrutiny. Our independent contractor distribution model has also been the subject of various class and individual lawsuits in recent years. In the event we are unable to successfully defend ourselves against these proceedings or claims, or if our assessment of the materiality of these proceedings or claims proves inaccurate, our business or financial results may be adversely affected. In addition, our reputation could be damaged by allegations made in proceedings or claims (even if untrue).

Increased regulation or changes in law could adversely affect our business or financial results

The manufacture and marketing of food products is extensively regulated. Various laws and regulations govern the processing, packaging, storage, distribution, marketing, advertising, labeling, quality and safety of our food products, as well as the health and safety of our employees and the protection of the environment. In the U.S., we are subject to regulation by various federal government agencies, including but not limited to the Food and Drug Administration, the Department of Agriculture, the Federal Trade Commission, the Department of Labor, the Department of Commerce, the Occupational Safety and Health Administration and the Environmental Protection Agency, as well as various state and local agencies. We are also regulated by similar agencies outside the U.S.

Governmental and administrative bodies within the U.S. are considering a variety of tax, trade and other regulatory reforms. Trade reforms include tariffs on certain materials used in the manufacture of our products and tariffs on certain finished products. We regularly move data across national and state borders to conduct our operations and, consequently, are subject to a variety of laws and regulations in the U.S. and other jurisdictions regarding privacy, data protection, and data security, including those related to the collection, storage, handling, use, disclosure, transfer, and security of personal data. There is significant uncertainty with respect to compliance with such privacy and data protection laws and regulations because they are continuously evolving and developing and may be interpreted and applied differently from country to country and state to state and may create inconsistent or conflicting requirements.

Changes in legal or regulatory requirements (such as new food safety requirements and revised regulatory requirements for the labeling of nutrition facts, serving sizes and genetically modified ingredients), or evolving interpretations of existing legal or regulatory requirements, may result in increased compliance cost, capital expenditures and other financial obligations that could adversely affect our business and financial results.

If our food products become adulterated or are mislabeled, we might need to recall those items, and we may experience product liability claims and damage to our reputation

We have in the past and we may, in the future, need to recall some of our products if they become adulterated or if they are mislabeled, and we may also be liable if the consumption of any of our products causes sickness or injury to consumers. A

12

widespread product recall could result in significant losses due to the costs of a recall, the destruction of product inventory, and lost sales due to the unavailability of product for a period of time. We could also suffer losses from a significant adverse product liability judgment. A significant product recall or product liability claim could also result in adverse publicity, damage to our reputation, and a loss of consumer confidence in the safety and/or quality of our products, ingredients or packaging. In addition, if another company recalls or experiences negative publicity related to a product in a category in which we compete, consumers might reduce their overall consumption of products in that category.

Climate change, or legal, regulatory or market measures to address climate change, may negatively affect our business and operations

There is growing concern that carbon dioxide and other greenhouse gases in the atmosphere may have an adverse impact on global temperatures, weather patterns, and the frequency and severity of extreme weather and natural disasters. In the event that such climate change has a negative effect on agricultural productivity, we may be subject to decreased availability or less favorable pricing for certain commodities that are necessary for our products, such as wheat, tomatoes, potatoes, cashews and almonds. Adverse weather conditions and natural disasters can reduce crop size and crop quality, which in turn could reduce our supplies of raw materials, lower recoveries of usable raw materials, increase the prices of our raw materials, increase our cost of storing and transporting our raw materials, or disrupt production schedules. We may also be subjected to decreased availability or less favorable pricing for water as a result of such change, which could impact our manufacturing and distribution operations. In addition, natural disasters and extreme weather conditions may disrupt the productivity of our facilities or the operation of our supply chain.

There is an increased focus by foreign, federal, state and local regulatory and legislative bodies regarding environmental policies relating to climate change, regulating greenhouse gas emissions, energy policies, and sustainability. Increased compliance costs and expenses due to the impacts of climate change and additional legal or regulatory requirements regarding climate change or designed to reduce or mitigate the effects of carbon dioxide and other greenhouse gas emissions on the environment may cause disruptions in, or an increase in the costs associated with, the running of our manufacturing facilities and our business, as well as increase distribution and supply chain costs. Moreover, compliance with any such legal or regulatory requirements may require us to make significant changes in our business operations and strategy, which will likely require us to devote substantial time and attention to these matters and cause us to incur additional costs. Even if we make changes to align ourselves with such legal or regulatory requirements, we may still be subject to significant penalties or potential litigation if such laws and regulations are interpreted and applied in a manner inconsistent with our practices. The effects of climate change and legal or regulatory initiatives to address climate change could have a long-term adverse impact on our business and results of operations.

Additionally, we might fail to effectively address increased attention from the media, stockholders, activists and other stakeholders on climate change and related environmental sustainability matters. Such failure, or the perception that we have failed to act responsibly regarding climate change, whether or not valid, could result in adverse publicity and negatively affect our business and reputation. Moreover, from time to time we establish and publicly announce goals and commitments, including to reduce our impact on the environment. For example, in 2022, we established science-based targets for Scope 1, 2 and 3 greenhouse gas emissions. Our ability to achieve any stated goal, target or objective is subject to numerous factors and conditions, many of which are outside of our control. Examples of such factors include evolving regulatory requirements affecting sustainability standards or disclosures or imposing different requirements, the pace of changes in technology, the availability of requisite financing and the availability of suppliers that can meet our sustainability and other standards. If we fail to achieve, or are perceived to have failed or been delayed in achieving, or improperly report our progress toward achieving these goals and commitments, it could negatively affect consumer preference for our products or investor confidence in our stock, as well as expose us to enforcement actions and litigation.

Actions of activist shareholders could cause us to incur substantial costs, divert management's attention and resources and have an adverse effect on our business

We were the target of activist shareholder activities in 2019. If a new activist investor purchased our stock, our business could be adversely affected because responding to proxy contests and reacting to other actions by activist shareholders can be costly and time consuming, disruptive to our operations and divert the attention of management and our employees. In addition, perceived uncertainties as to our future direction, strategy or leadership created as a consequence of activist shareholder initiatives may result in the loss of potential business opportunities, harm our ability to attract new investors, customers, employees, suppliers and strategic partners, and cause our share price to experience periods of volatility or stagnation.

Our business, financial condition and results of operations could be adversely affected by disruptions in the global economy caused by the ongoing conflict between Russia and Ukraine.

The global economy has been negatively impacted by the military conflict between Russia and Ukraine. Furthermore, governments in the U.S., United Kingdom, and European Union have each imposed export controls on certain products and financial and economic sanctions on certain industry sectors and parties in Russia. Although we have no operations in Russia or

13

Ukraine, we have experienced shortages in materials and increased costs for transportation, energy, and raw material due in part to the negative impact of the Russia-Ukraine military conflict on the global economy. The scope and duration of the military conflict in Ukraine is uncertain, rapidly changing and hard to predict. Further escalation of geopolitical tensions related to the military conflict, including increased trade barriers or restrictions on global trade, could result in, among other things, cyberattacks, supply disruptions, lower consumer demand, and changes to foreign exchange rates and financial markets, any of which may adversely affect our business and supply chain.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Our principal executive offices are company-owned and located in Camden, New Jersey. The following table sets forth our principal manufacturing facilities and the reportable segment that primarily uses each of the facilities:

Inside the U.S.

| Arizona | Massachusetts | Pennsylvania | ||||||||||||

| Goodyear (S) | Hyannis (S) | Denver (S) | ||||||||||||

| California | North Carolina | Downingtown (S) | ||||||||||||

| Dixon (MB) | Charlotte (S) | Hanover (S) | ||||||||||||

| Stockton (MB) | Maxton (MB) | Texas | ||||||||||||

| Connecticut | Ohio | Paris (MB) | ||||||||||||

| Bloomfield (S) | Ashland (S) | Utah | ||||||||||||

| Florida | Napoleon (MB) | Richmond (S) | ||||||||||||

| Lakeland (S) | Willard (S) | Wisconsin | ||||||||||||

| Illinois | Oregon | Beloit (S) | ||||||||||||

| Downers Grove (S) | Salem (S) | Franklin (S) | ||||||||||||

| Indiana | Tualatin (MB) | Milwaukee (MB) | ||||||||||||

| Jeffersonville (S) | ||||||||||||||

______________________________

MB - Meals & Beverages

S - Snacks

Each of the foregoing manufacturing facilities is company-owned, except the Tualatin, Oregon facility, which is leased. We also maintain principal business unit offices in Charlotte, North Carolina; Doral, Florida; Hanover, Pennsylvania; Norwalk, Connecticut; Tualatin, Oregon; and Mississauga, Canada.

We also own and lease distribution centers across the U.S. We believe that our manufacturing and processing plants and distribution centers are well maintained and, together with facilities operated by our contract manufacturers, are generally adequate to support the current operations of the businesses.

Item 3. Legal Proceedings

Information regarding reportable legal proceedings is contained in Note 18 to the Consolidated Financial Statements and incorporated herein by reference.

Item 4. Mine Safety Disclosures

Not applicable.

14

Information about our Executive Officers

The section below provides information regarding our executive officers as of September 14, 2022:

| Name, Present Title & Business Experience | Age | Year First Appointed Executive Officer | ||||||

| Mick J. Beekhuizen, Executive Vice President and Chief Financial Officer. Executive Vice President and Chief Financial Officer, Chobani LLC (2016-2019). Executive Vice President and Chief Financial Officer, Education Management Corporation (2013-2016). | 46 | 2020 | ||||||

Adam G. Ciongoli, Executive Vice President, General Counsel and Chief Sustainability, Corporate Responsibility and Governance Officer. Executive Vice President and General Counsel, Lincoln Financial Group (2012-2015). | 54 | 2015 | ||||||

Mark A. Clouse, President and Chief Executive Officer. Chief Executive Officer, Pinnacle Foods, Inc. (2016-2018). Chief Commercial Officer (2016) and Executive Vice President and Chief Growth Officer (2014-2016), Mondelez International, Inc. | 54 | 2019 | ||||||

| Christopher D. Foley, Executive Vice President and President, Meals & Beverages. We have employed Mr. Foley in an executive or managerial capacity for at least five years. | 50 | 2019 | ||||||

| Diane Johnson May, Executive Vice President and Chief Human Resources Officer. Senior Vice President, People and Culture, Manpower Group (2020-2021). Executive Vice President, Chief Human Resources Officer, Brookdale Senior Living (2019-2020). Managing Vice President, The Deli Source, Inc. (2017-2019). | 64 | 2022 | ||||||

Valerie J. Oswalt, Executive Vice President and President, Snacks. Chief Executive Officer, Century Snacks (2018-2020). President, Mondelez North America Confections (2017-2018). President, Mondelez North America Sales (2015-2017). | 49 | 2020 | ||||||

| Daniel L. Poland, Executive Vice President and Chief Supply Chain Officer. Chief Operating Officer, KIND Snacks (2019-2021). Executive Vice President and Chief Supply Chain Officer, Pinnacle Foods, Inc. (2018-2019). Chief Supply Chain Officer - North American Operations, Danone (2016-2017). | 59 | 2022 | ||||||

| Anthony J. Sanzio, Executive Vice President and Chief Communications Officer. We have employed Mr. Sanzio in an executive or managerial capacity for at least five years. | 55 | 2022 | ||||||

| Craig S. Slavtcheff, Executive Vice President, Chief R&D and Innovation Officer. We have employed Mr. Slavtcheff in an executive or managerial capacity for at least five years. | 55 | 2019 | ||||||

15

PART II

Item 5. Market for Registrant’s Capital Stock, Related Shareholder Matters and Issuer Purchases of Equity Securities

Market for Registrant’s Capital Stock

Our capital stock is traded on the New York Stock Exchange under the symbol "CPB." On September 14, 2022, there were 299,364,411 holders of record of our capital stock.

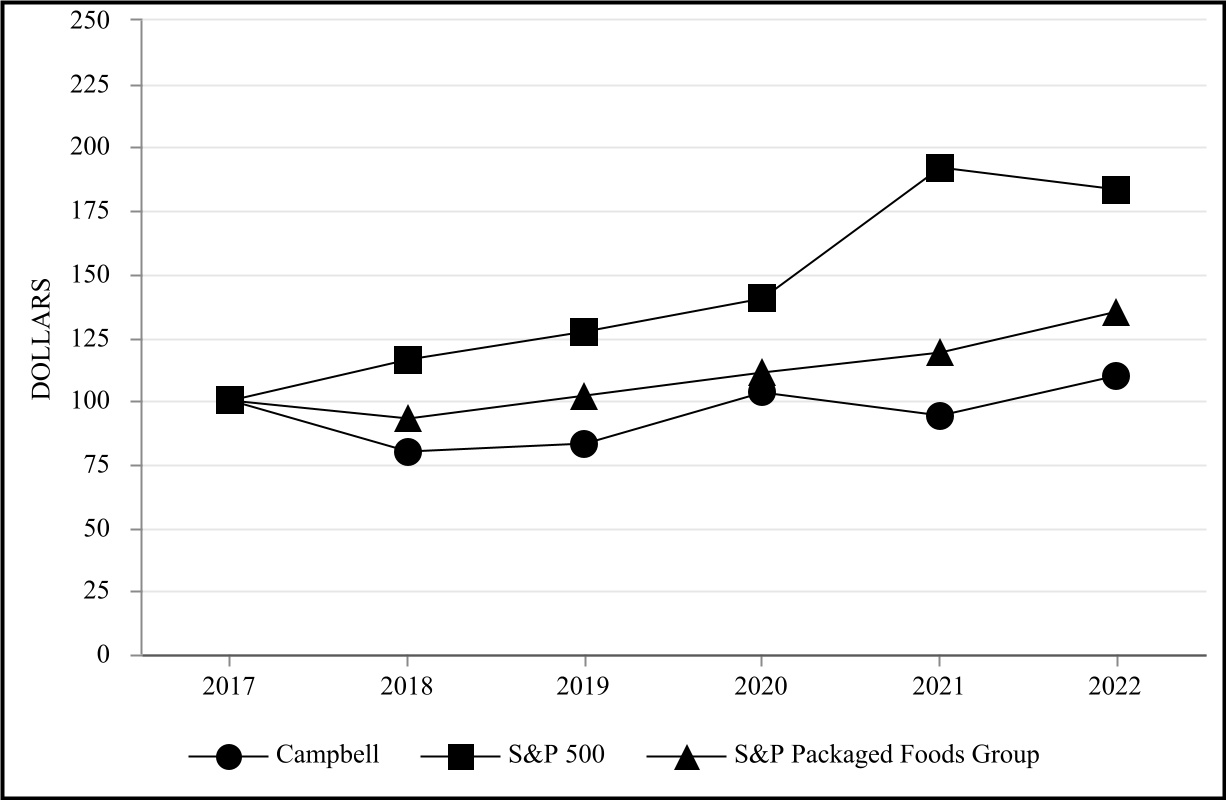

Return to Shareholders* Performance Graph

The information contained in this Return to Shareholders Performance Graph section shall not be deemed to be "soliciting material" or "filed" or incorporated by reference in future filings with the Securities and Exchange Commission, or subject to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended (the Exchange Act), except to the extent we specifically incorporate it by reference into a document filed under the Securities Exchange Act of 1933, as amended, or the Exchange Act.

The following graph compares the cumulative total shareholder return (TSR) on our stock with the cumulative total return of the Standard & Poor’s 500 Stock Index (the S&P 500) and the Standard & Poor’s Packaged Foods Index (the S&P Packaged Foods Group). The graph assumes that $100 was invested on July 28, 2017, in each of our stock, the S&P 500 and the S&P Packaged Foods Group, and that all dividends were reinvested. The total cumulative dollar returns shown on the graph represent the value that such investments would have had on July 31, 2022.

* Stock appreciation plus dividend reinvestment.

| 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |||||||||||||||||||||||||||||||||

| Campbell | 100 | 80 | 83 | 103 | 94 | 110 | ||||||||||||||||||||||||||||||||

| S&P 500 | 100 | 116 | 127 | 140 | 192 | 183 | ||||||||||||||||||||||||||||||||

| S&P Packaged Foods Group | 100 | 93 | 102 | 111 | 119 | 135 | ||||||||||||||||||||||||||||||||

16

Issuer Purchases of Equity Securities

| Period | Total Number of Shares Purchased (1) | Average Price Paid Per Share (2) | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (3) | Approximate Dollar Value of Shares that may yet be Purchased Under the Plans or Programs ($ in Millions) (3) | |||||||||||||||||||

| 5/2/22 - 5/31/22 | — | $ | — | — | $ | 598 | |||||||||||||||||

| 6/1/22 - 6/30/22 | 1,117,289 | $ | 46.05 | 1,117,289 | $ | 547 | |||||||||||||||||

| 7/1/22 - 7/29/22 | — | $ | — | — | $ | 547 | |||||||||||||||||

| Total | 1,117,289 | $46.05 | 1,117,289 | $ | 547 | ||||||||||||||||||

____________________________________

(1)Shares purchased are as of the trade date.

(2)Average price paid per share is calculated on a settlement basis and excludes commission.

(3)In June 2021, our Board of Directors authorized an anti-dilutive share repurchase program of up to $250 million (June 2021 program) to offset the impact of dilution from shares issued under our stock compensation programs. The June 2021 program has no expiration date, but it may be suspended or discontinued at any time. Repurchases under the June 2021 program may be made in open-market or privately negotiated transactions. In September 2021, the Board approved a strategic share repurchase program of up to $500 million (September 2021 program). The September 2021 program has no expiration date, but it may be suspended or discontinued at any time. Repurchases under the September 2021 program may be made in open-market or privately negotiated transactions.

Item 6. Reserved

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

This Management’s Discussion and Analysis of Financial Condition and Results of Operations is provided as a supplement to, and should be read in conjunction with, our consolidated financial statements and the accompanying notes to the consolidated financial statements presented in "Financial Statements and Supplementary Data," as well as the information contained in "Risk Factors."

Unless otherwise stated, the terms "we," "us," "our" and the "company" refer to Campbell Soup Company and its consolidated subsidiaries.

Executive Summary

We are a manufacturer and marketer of high-quality, branded food and beverage products. We operate in a highly competitive industry and experience competition in all of our categories.

In 2022, we delivered solid full-year results while advancing our strategic plan in a volatile macroeconomic environment. During 2022, we navigated through a challenging environment marked by supply chain pressures, particularly around labor and high inflation. We enhanced and accelerated our recruiting efforts and hiring and onboarding processes, which improved our ability to meet sustained consumer demand. Our improved supply chain execution combined with inflation-driven pricing, continued supply chain productivity improvements and cost savings initiatives partially mitigated ongoing inflationary pressures experienced in 2022. We expect that inflation will continue to be a headwind in 2023. In addition, we expect a pre-tax headwind of approximately $35 million in 2023 related to lower net periodic pension and postretirement benefit income.

Strategy

Our strategy is to unlock our full growth potential by focusing on our core brands in two divisions within North America while delivering on the promise of our purpose - Connecting people through food they love. Our strategic plan is based on four pillars: build a winning team and culture; accelerate profitable growth; fuel investments and margins with targeted cost savings; and deliver on the promise of our purpose all as further discussed below.

We plan to continue our focus on building a winning team and culture by investing in our employee experience and improving employee engagement, prioritizing our inclusion and diversity strategy and investing in strategic capabilities and digitization that support our core brands in North America. In addition, we plan to continue to deliver on the promise of our purpose with consumer transparency initiatives, progress on our sustainability goals and strengthening our connection to the communities in which we operate.

We believe that we can accelerate our profitable growth model by growing market share and driving integrated business planning programming throughout the company. We expect to grow market share through the development of more consumer-

17

oriented product quality, marketing and innovation plans and prioritizing growth channels and retailers within our defined portfolio roles. In addition, we expect to continue to focus on accelerating the growth of our Snacks brands while also sustaining the growth in U.S. soup and our other core brands. We expect that changes in consumer behavior driven by the COVID-19 pandemic will continue to support ongoing elevated consumer demand for food at home, relative to pre-pandemic levels. We plan to capitalize on this opportunity by addressing evolving consumer needs through our unique and differentiated portfolio.

We also expect to fuel investments and margins by continuing to focus on mitigating the effects of inflation. We implemented price increases beginning in 2022 and continue to pursue our multi-year cost savings initiatives with targeted annualized cost savings of $1 billion for continuing operations by the end of 2025, with $850 million in synergies and run-rate cost savings achieved through 2022. See "Restructuring Charges and Cost Savings Initiatives" for additional information on these initiatives.

Business Trends

Our businesses are being influenced by a variety of trends that we anticipate will continue in the future, including: cost inflation; changing consumer preferences; and a competitive and dynamic retail environment.

Our strategy is designed, in part, to capture growing consumer preferences for snacking and convenience. For example, we believe that consumers are changing their eating habits by increasing the type and frequency of snacks they consume and are continuing in-home eating behaviors that were driven by the COVID-19 pandemic.

Retailers continue to use their buying power and negotiating strength to seek increased promotional programs funded by their suppliers and more favorable terms, including customized products funded by their suppliers. Any consolidations among retailers would continue to create large and sophisticated customers that may further this trend. Retailers also continue to grow and promote store brands that compete with branded products, especially on price.

Throughout 2022 we experienced elevated demand for our retail products versus pre-pandemic levels, but volumes were lower than fiscal 2021. In the first half of the year we experienced lower net sales due primarily to supply constraints based on materials availability and in the second half of the year, although supply significantly improved volumes declined due to inflation-driven pricing actions. We anticipate that demand related to at-home food consumption will remain elevated through 2023.