|

As filed with the Securities and Exchange Commission on June 5, 2018 |

Registration No. 333-212479 |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 5 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VanEck SolidX Bitcoin Trust

(Exact name of Registrant as specified in its charter)

|

Delaware |

|

6221 |

|

35-7161067 |

|

(State or Other Jurisdiction of |

|

(Primary Standard Industrial |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

|

|

|

|

200 Park Avenue |

|

|

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Daniel H. Gallancy

Chief Executive Officer

SolidX Management LLC

200 Park Avenue

New York, New York 10166

(212) 273-9585

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to

Stuart M. Strauss, Esq.

Jeremy Senderowicz, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, New York 10036

Approximate date of commencement of proposed sale to the public: As soon as practicable after the registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [x]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer [ ] |

Accelerated filer [ ] |

Non-accelerated filer |

Smaller reporting |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company x

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. x

CALCULATION OF REGISTRATION FEE

|

|

|

|

|

|

|

Title of Each |

Amount to be |

Proposed |

Proposed |

Amount of |

|

|

|

|

|

|

|

VanEck SolidX Bitcoin Shares |

[ ] |

[ ] |

$1,000,000 |

$100.70 |

(1) Estimated solely for the purpose of determining the amount of the registration fee in accordance with Rule 457(d) under the Securities Act of 1933.

(2) $100.70 was previously paid in the initial filing of the registration statement on Form S-1, filed on July 12, 2016.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 5, 2018

[ ],000 VanEck SolidX Bitcoin Shares

VANECK SOLIDX BITCOIN TRUST

The VanEck SolidX Bitcoin Trust (“Trust”) will issue VanEck SolidX Bitcoin Shares (“Shares”), which represent units of fractional undivided beneficial interest in and ownership of the Trust. The investment objective of the Trust is for the Shares to reflect the performance of the price of bitcoin, less the expenses of the Trust’s operations. The Trust is not actively managed.

The Trust’s assets will consist of bitcoin, an asset that can be transferred among parties via the Internet, but without the use of a central administrator or clearing agency. The Trust will occasionally hold cash for short periods in connection with the purchase and sale of bitcoin, and to pay Trust expenses. The Trust will be responsible for custody of the Trust’s bitcoin.

SolidX Management LLC is the sponsor of the Trust (“Sponsor”). Delaware Trust Company is the trustee (“Trustee”). The Bank of New York Mellon is the administrator (“Administrator”), transfer agent (“Transfer Agent”) and the custodian, with respect to cash, (“Cash Custodian”) of the Trust. Foreside Fund Services, LLC is the order examiner (“Marketing Agent”) in connection with the creation and redemption of Baskets of Shares. Van Eck Securities Corporation (“VanEck”) provides assistance in the marketing of the Shares.

The Shares are issued by the Trust only in one or more blocks of 5 Shares, called a “Basket,” principally in exchange for cash. The Trust will issue and redeem Shares in Baskets to certain registered broker-dealers who have entered into a contract with the Sponsor and Transfer Agent (“Authorized Participants”) on an ongoing basis as described in “Creation and Redemption of Shares.” Baskets will be issued and redeemed on an ongoing basis at net asset value (“NAV”) on the day that an order to create a Basket is accepted by the Transfer Agent and approved by the Marketing Agent.

Prior to this offering, there has been no public market for the Shares. The Shares of the Trust are expected to be listed for trading, subject to notice of issuance, on the Cboe BZX Exchange, Inc. (“Cboe” or the “Exchange”), under the symbol “XBTC”. The market price of the Shares may be different from the NAV per Share for a number of reasons, including price volatility, trading volume, and closing of bitcoin trading platforms due to fraud, failure, security breaches or otherwise.

Except when aggregated in Baskets, Shares are not redeemable securities.

AN INVESTMENT IN THE TRUST MAY NOT BE SUITABLE FOR RETAIL INVESTORS. THE TRUST WILL HOLD BITCOIN AND THEREFORE MAY BE RISKIER THAN OTHER EXCHANGE TRADED PRODUCTS THAT DO NOT HOLD BITCOIN OR FINANCIAL INSTRUMENTS RELATED TO BITCOIN. THE SHARES ARE SPECULATIVE SECURITIES AND THEIR PURCHASE INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD CONSIDER ALL RISK FACTORS BEFORE INVESTING IN THE TRUST. PLEASE REFER TO “THE RISKS YOU FACE” BEGINNING ON PAGE 13.

|

· Bitcoin is a new technological innovation with a limited history. There is no assurance that usage of bitcoin will continue to grow. A contraction in use of bitcoin may result in increased volatility or a reduction in the price of bitcoin, which could adversely impact the value of the Shares. |

|

· Bitcoin trading prices are volatile and shareholders could lose all or substantially all of their investment in the Trust. |

|

|

|

|

|

· Loss of the Trust’s bitcoin may be irreversible and could result in the loss of all or substantially all of an investment in the Trust. |

|

· Regulation of bitcoin continues to evolve in both the U.S. and foreign jurisdictions, which may restrict the use of bitcoin or otherwise impact the demand for bitcoin. |

|

|

|

|

Neither the Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or disapproved of the securities offered in this prospectus (“Prospectus”), or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The Trust qualifies as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (“JOBS Act”). “Emerging growth company” does not mean the Trust is a “growth” type of investment vehicle or that it will utilize a “growth” investment strategy. However, the Trust will not take advantage of any exemptions or other relief provided to emerging growth companies under the JOBS Act. See “Emerging Growth Company Status.”

The Shares are neither interests in nor obligations of the Sponsor, the Trustee, the Administrator, the Transfer Agent, the Cash Custodian, the Marketing Agent, VanEck or any of their respective affiliates. The Shares are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency. The Trust is not an investment company registered under the Investment Company Act of 1940, as amended. The Trust is not a commodity pool for purposes of the Commodity Exchange Act of 1936, as amended, and the Sponsor is not subject to regulation by the Commodity Futures Trading Commission as a commodity pool operator or a commodity trading advisor.

On [·], 2018, an initial purchaser, subject to conditions, deposited cash for the purchase of [·] initial Basket[s] totaling [·] Shares. Delivery of the initial Baskets will be made on or about the date of this Prospectus, upon condition of effectiveness of the related registration statement. The Trust received all proceeds from the offering of the initial Basket[s] in cash in an amount equal to the full price for the initial Basket[s].

|

|

Per Share(1) |

Per Basket |

|

Public offering price for initial Baskets(2) |

$[·] |

$[·] |

(1) The initial Basket[s] [were/was] created at a per share price equal to the value of [25] bitcoin on [ ].

(2) The initial purchaser may receive commissions/fees from shareholders who purchase shares from the initial Basket[s] through their commission/fee-based brokerage accounts. The price per basket that will be paid in the future by the Authorized Participants may be different than the initial Basket price.

The date of this Prospectus is [ ], 2018.

|

|

i | |

|

|

1 | |

|

|

8 | |

|

|

12 | |

|

|

13 | |

|

|

32 | |

|

|

32 | |

|

|

46 | |

|

|

47 | |

|

|

51 | |

|

|

52 | |

|

|

53 | |

|

|

53 | |

|

|

57 | |

|

|

58 | |

|

|

64 | |

|

|

66 | |

|

|

69 | |

|

|

71 | |

|

|

73 | |

|

|

74 | |

|

|

76 | |

|

|

77 | |

|

|

78 | |

|

|

82 | |

|

|

83 | |

|

|

84 | |

|

|

84 | |

|

|

84 | |

|

|

84 | |

|

|

|

|

This Prospectus contains information you should consider when making an investment decision about the Shares. You may rely on the information contained in this Prospectus. The Trust and the Sponsor have not authorized any person to provide you with different information and, if anyone provides you with different or inconsistent information, you should not rely on it. This Prospectus is not an offer to sell the Shares in any jurisdiction where the offer or sale of the Shares is not permitted.

The Shares are not registered for public sale in any jurisdiction other than the United States.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus includes statements which relate to future events or future performance. In some cases, you can identify such forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or the negative of these terms or other comparable terminology. All statements (other than statements of historical fact) included in this Prospectus that address activities, events or developments that may occur in the future, including such matters as changes in asset prices and market conditions (for bitcoin and the Shares), the Trust’s operations, the Sponsor’s plans and references to the Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially. These statements are based upon certain assumptions and analyses made by the Sponsor on the basis of its perception of historical trends, current conditions and expected future developments, as well as other factors it believes are appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including the special considerations discussed in this Prospectus, general economic, market and business conditions, changes in laws or regulations, including those concerning taxes, made by governmental authorities or regulatory bodies, and other world economic and political developments. See “The Risks You Face.” Consequently, all the forward-looking statements made in this Prospectus are qualified by these cautionary statements, and there can be no assurance that the actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will result in the expected consequences to, or have the expected effects on, the Trust’s operations or the value of the Shares. Moreover, neither the Sponsor, nor any other person assumes responsibility for the accuracy or completeness of the forward-looking statements. Neither the Trust nor the Sponsor undertakes an obligation to publicly update or conform to actual results any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

The following is only a summary of this Prospectus and, while it contains material information about the Trust, it does not contain or summarize all of the information about the Trust and the Shares contained in this Prospectus that is material and that may be important to you. You should read this entire Prospectus, including “The Risks You Face” beginning on page 13, and the material incorporated by reference herein before making an investment decision about the Shares.

Bitcoin

A bitcoin is an asset that can be transferred among parties via the Internet, but without the use of a central administrator or clearing agency. Bitcoin with an upper case “B” describes the system as a whole (i.e., the network of computers running the software protocol underlying bitcoin involved in maintaining the database of bitcoin ownership and facilitating the transfer of bitcoin among parties). When written with a lower case “b”, the word bitcoin refers to the unit of account within the Bitcoin network. The Bitcoin network and the asset, bitcoin, are intrinsically linked and inseparable.

The Bitcoin network, which has existed since 2009, can be used both as a value transfer system (i.e. the transfer of bitcoin from one party to another) and for non-financial applications. Development of the Bitcoin network’s usage for non-financial applications has become increasingly prominent, including applications such as: asset title transfer, secure timestamping, counterfeit and fraud detection systems, secure document and contract signing, distributed cloud storage and identity management. As a mechanism purely for the transfer of value, the Bitcoin network has processed more than 280 million transactions since its inception. Hundreds of thousands of merchants worldwide accept bitcoin for goods and services. To date, venture capitalists have invested more than $1 billion in businesses related to Bitcoin and the blockchain, the technology underlying the Bitcoin network.

The Trust

VanEck SolidX Bitcoin Trust (the “Trust”) was formed as a Delaware statutory trust on September 15, 2016. The Trust is governed by the Amended and Restated Declaration of Trust and Trust Agreement (“Trust Agreement”) dated [ ] between SolidX Management LLC (the “Sponsor”) and Delaware Trust Company (the “Trustee”). The Trust will issue common units of beneficial interest, or “Shares,” which represent units of fractional undivided beneficial interest in the Trust’s net assets. The Trust’s assets will consist of bitcoin, the unit of account within the Bitcoin network as described in the preceding paragraphs. The Trust will occasionally hold cash for short periods in connection with the Basket creation and redemption process, and to pay the Sponsor’s Management Fee, the bitcoin Insurance Fee, bitcoin storage fees, salaries of Trust principals and employees and any other Trust expenses and liabilities not assumed by the Sponsor. The Trust will not hold any assets other than bitcoin or cash.

The Trust will buy and sell bitcoin with a view to causing the performance of the Trust to track the price of bitcoin, less the expenses of the Trust’s operations. The Trust will also be responsible for custody of the Trust’s bitcoin. The value of bitcoin will be reported on the Trust’s website daily as measured by the MVIS® Bitcoin OTC Index (“MVBTCO”).

Shares are issued by the Trust only in blocks of 5 Shares called “Baskets” principally in exchange for cash from certain registered broker-dealers (“Authorized Participants”). See “Creation and Redemption of Shares” for requirements to qualify as an Authorized Participant. Baskets will be redeemed by the Trust principally in exchange for the amount of cash corresponding to their redemption value. Baskets may also be created or redeemed partially or wholly in exchange for bitcoin at the discretion of the Sponsor if the Authorized Participant can convey bitcoin directly to the Trust. The Trust issues and redeems Baskets on an ongoing basis at net asset value (“NAV”) to Authorized Participants who have entered into a contract with the Sponsor and the Transfer Agent.

Individual Shares will not be redeemed by the Trust, but are expected to be listed for trading, subject to notice at issuance, on the Exchange under the symbol “XBTC.” The material terms of the Trust and the Shares are discussed in greater detail under the sections “Description of the Trust” and “Description of the Shares.” The Trust is not a registered investment company under the Investment Company Act of 1940, as amended (“1940 Act”), and is not required to register with the Securities and Exchange Commission thereunder. The Trust is not a commodity pool for purposes of the Commodity Exchange Act of 1936, as amended, and the Trust and the Sponsor are not subject to regulation by the Commodity Futures Trading Commission as a commodity pool operator or a commodity trading advisor.

An investment in the Trust may not be suitable for retail investors. Secondary market purchases and sales of Shares are subject to customary brokerage commissions and charges.

The market price of the Shares may not be identical to the NAV per Share. The intra-day indicative value per Share is based on the prior day’s final NAV per Share, adjusted every 15 seconds throughout the day to reflect the continuous price changes of the Trust’s bitcoin holdings, to provide a continuously updated indicative intra-day value per Share. The Trust is not involved in or responsible for the calculation or dissemination of the indicative intra-day value per Share and makes no warranty as to the accuracy of the indicative intra-day value per Share.

The Sponsor

The Sponsor is a Delaware limited liability company. The Shares are neither interests in nor obligations of, and are not guaranteed by, the Sponsor, its member(s), or any of its affiliates.

The Sponsor: (1) will select the Trustee, Administrator, Transfer Agent, Cash Custodian, Marketing Agent and any other Trust service providers; (2) will negotiate various agreements and fees for the Trust; (3) will develop a marketing plan for the Trust on an ongoing basis and prepare marketing materials regarding the Shares, and in this respect the Sponsor has engaged Van Eck Securities Corporation (“VanEck”) pursuant to a marketing agent agreement to provide assistance in the marketing of the Shares; (4) will maintain the Trust’s website; and (5) will perform such other services as the Sponsor believes that the Trust may require. The general role and responsibilities of the Sponsor are discussed in greater detail under the section “The Sponsor.”

The Sponsor arranged for the creation of the Trust, the registration of the Shares for their public offering in the United States and the listing of the Shares on the Exchange. The Sponsor generally oversees the performance of the Trust’s principal service providers, but does not exercise day-to-day oversight of the Trustee, Administrator, Transfer Agent, Cash Custodian, Marketing Agent, VanEck or other such service providers.

The Sponsor may compensate its affiliates for providing marketing and other services to the Trust without any additional cost to the Trust. The Sponsor maintains a public website on behalf of the Trust, containing information about the Trust and the Shares. The Internet address of the Trust’s website is [·]. This Internet address is only provided here as a convenience to you, and the information contained on or connected to the Trust’s website is not considered part of this Prospectus.

The Sponsor has agreed to assume the following administrative and marketing expenses incurred by the Trust: each of the Trustee’s, Administrator’s, Cash Custodian’s, Transfer Agent’s and Marketing Agent’s monthly fee and out-of-pocket expenses and expenses reimbursable in connection with such service provider’s respective agreement; the marketing support fees and expenses; exchange listing fees; SEC registration fees; index license fees; printing and mailing costs; maintenance expenses for the Trust’s website; audit fees and expenses; and up to $100,000 per annum in legal expenses. The Sponsor will not be responsible for paying the premiums associated with the bitcoin insurance that will be maintained by the Trust. The Sponsor also paid the costs of the Trust’s organization and the initial sale of the Shares. See “The Sponsor,” “The Trust’s bitcoin Security System” and “The Trust’s bitcoin Insurance.”

The Trustee

Delaware Trust Company, a Delaware trust company, acts as the trustee of the Trust for the purpose of creating a Delaware statutory trust in accordance with the Delaware Statutory Trust Act (“DSTA”). The Trustee is appointed to serve as the trustee of the Trust in the State of Delaware for the sole purpose of satisfying the requirement of Section 3807(a) of the DSTA that the Trust have at least one trustee with a principal place of business in the State of Delaware. The duties of the Trustee will be limited to (i) accepting legal process served on the Trust in the State of Delaware and (ii) the execution of any certificates required to be filed with the Delaware Secretary of State which the Trustee is required to execute under the DSTA. To the extent that, at law or in equity, the Trustee has duties (including fiduciary duties) and liabilities relating thereto to the Trust or the Trust’s shareholders, such duties and liabilities will be replaced by the duties and liabilities of the Trustee expressly set forth in the Trust Agreement. The Trustee will have no obligation to supervise, nor will it be liable for, the acts or omissions of the Sponsor, Trust principals and employees, Administrator, Transfer Agent, Cash Custodian, Marketing Agent, VanEck or any other person. See “The Trustee.”

The Administrator

The Administrator is The Bank of New York Mellon. The Administrator is generally responsible for the day-to-day administration and operation of the Trust, including: (1) valuing the Trust’s bitcoin and calculating the net asset value per share of the Trust and the net asset value of the Trust; (2) supplying pricing information to the Sponsor for the Trust’s website; and (3) receiving and reviewing reports on the custody of and transactions in cash and bitcoin from the Cash Custodian and the Trust, respectively, and taking such other actions in connection with the custody of cash as the Sponsor instructs. The general role and responsibilities of the Administrator are discussed in greater detail under the section “The Administrator.”

The Transfer Agent

The Transfer Agent is The Bank of New York Mellon. Pursuant to the Transfer Agency and Service Agreement between the Trust and the Transfer Agent, the Transfer Agent serves as the Trust’s transfer agent and agent in connection with certain other activities as provided under the Transfer Agency and Service Agreement. The Transfer Agent’s responsibilities include: (1) receiving and processing orders from Authorized Participants for the creation and redemption of Baskets; and (2) coordinating the processing of orders from Authorized Participants with the Marketing Agent, the Trust, the Cash Custodian and The Depository Trust Company (“DTC”). See “The Transfer Agent.”

The Marketing Agent

Foreside Fund Services, LLC is the Marketing Agent. The Marketing Agent’s responsibilities include: (1) working with the Transfer Agent to review and accept or reject orders placed by Authorized Participants with the Transfer Agent; (2) reviewing and approving all sales and marketing materials for compliance with applicable laws, and filing such materials with FINRA as required by the Securities Act of 1933, as amended (the “Securities Act”), and the rules promulgated thereunder, and (3) facilitating arrangements between the Sponsor, the Transfer Agent and broker-dealers for the purchase and redemption of Baskets. All such sales and marketing materials must be approved, in writing, by the Marketing Agent prior to use.

Custodial Arrangements

The Bank of New York Mellon is the custodian (the “Cash Custodian”) of the cash held by the Trust and has entered into the Cash Custody Agreement in connection therewith. The Trust will provide custody services relating to custody of the Trust’s bitcoin. See “The Cash Custodian” and “The Trust.”

Trust Objective

The investment objective of the Trust is for the Shares to reflect the performance of the price of bitcoin, less the expenses of the Trust’s operations. The Trust intends to achieve this objective by investing substantially all of its assets in bitcoin traded primarily in the over-the-counter (“OTC”) markets, though the Trust may also invest in bitcoin traded on domestic and international bitcoin exchanges, depending on liquidity and otherwise at the Trust’s discretion. The Trust will invest in bitcoin on a non-discretionary basis (i.e., without regard to whether the value of bitcoin is rising or falling over any particular period).

Bitcoin is an asset that is not issued by any government, bank or organization. A bitcoin is an asset that can be transferred among parties via the Internet, but without the use of a central administrator or clearing agency. The asset, bitcoin, is generally written with a lower case “b.” When written with an uppercase “B,” the word “Bitcoin” generally refers to the computers and software (or the protocol) involved in the transfer of bitcoin among users. The computers running Bitcoin software constitute the Bitcoin network. The asset, bitcoin, is the intrinsically linked unit of account that exists within the Bitcoin network.

The Bitcoin network records each bitcoin balance (i.e., the quantity of bitcoin) held by each user on a database referred to as the blockchain. Each transfer of bitcoin between users is known as a bitcoin transaction. Approximately every ten minutes, the Bitcoin network groups together new transactions into what are referred to as blocks. Transactions in each block refer to transactions in previous blocks, thereby growing the blockchain and enabling it to serve as a consistent database of all bitcoin transactions and balances. The blockchain’s record of transactions and balances provides a complete historical record of all activity within the Bitcoin network since Bitcoin’s inception in January 2009. Copies of the blockchain are stored on various computers participating in the Bitcoin network. The blockchain can be used for a variety of non-financial applications, but all uses involve the expenditure of some quantity of bitcoin. See “Bitcoin and the Bitcoin Industry.”

The Trust will be insured against loss or theft of bitcoin held by the Trust. The insurance will cover loss of bitcoin by, among other things, theft, destruction, bitcoin in transit, computer fraud (i.e., hacking attack), and other loss of numerical codes, known as “private keys,” which are necessary to access the bitcoin held by the Trust. The insurance will not cover certain losses including, but not limited to the following:

· Loss caused or contributed by theft or any other fraudulent, dishonest or criminal act committed by a partner, employee or director of the Sponsor or the Trust, controlling more than 25% of the issued share capital of the Sponsor or any of its subsidiaries.

· Loss caused by an employee if an elected or appointed official of the Trust or the Sponsor (not in collusion) knows of any act or acts of theft, fraud or dishonesty involving amounts in excess of $5,000 by such employee prior to the Trust’s or Sponsor’s discovery of a loss caused by such act or acts of the employee.

· Any and all losses caused by an employee who has access to the private key(s) associated with the Trust’s bitcoin if an elected or appointed official of the Trust or Sponsor becomes aware of any act or acts of theft, fraud or dishonesty by such employee prior to the Trust’s or Sponsor’s discovery of a loss caused by such act or acts.

· Loss of the private key(s) associated with the Trust’s bitcoin where such private key(s) is stored or being transmitted between computers or similar electronic devices that are connected to the Internet.

· Any and all loss resulting from the network failure of the Bitcoin protocol.

The insurance carries a $500,000 deductible; the Trust will be responsible for any losses up to that amount.

See “The Trust’s bitcoin Insurance.”

Advantages of investing in the Shares include:

· Ease and Flexibility of Investment. The Shares will trade on the Exchange and provide shareholders with indirect exposure to the price of bitcoin. The Shares may be bought and sold throughout the business day at real-time market prices on the Exchange like other exchange-listed securities.

· Insurance. As noted above, the bitcoin held by the Trust will be insured against loss or theft of bitcoin.

· Diversification. The correlation between bitcoin and global financial markets for equities, commodities and fixed income has, since bitcoin’s inception in 2009, generally been low, so the Shares may help to diversify an investment portfolio.

The Index

MV Index Solutions GmbH (“MVIS”) is the sponsor for the MVBTCO. MVIS, with the assistance of its affiliates, is also the calculation agent for the MVBTCO.

The MVBTCO is a real-time U.S. dollar-denominated composite reference rate for the price of bitcoin. The MVBTCO calculates the intra-day price of bitcoin every 15 seconds, including a ‘closing price’ as of 4:00 p.m. E.T. The intra-day price and closing price are based on a methodology that consists of collecting actual firm bid/ask spreads and calculating a mid price from several bitcoin OTC platforms, all of which are U.S.-based entities, included within the index. As of [ ], 2018, the bitcoin OTC platforms that have entered into an agreement with MVIS for inclusion in the MVBTCO are [ ]. The logic utilized for the derivation of the daily closing index level for the MVBTCO is intended to analyze actual firm bid/ask data, verify and refine the data set, and yield an objective, fair-market value of one bitcoin as of 4:00 p.m. E.T. each weekday, priced in U.S. dollars. As discussed herein, the MVBTCO intra-day price and the MVBTCO closing price are collectively referred to as the MVBTCO price, unless otherwise noted. MVIS’s MVBTCO index has been in operation since [ ]. In the event the MVBTCO is unavailable for use in calculating the intra-day and closing prices, the Sponsor will use the alternative pricing sources described under “DESCRIPTION OF THE TRUST – Pricing Sources.”

The key elements of the algorithm underlying the MVBTCO include:

· Equal weighting of OTC platforms. This mitigates the impact of spikes at single platforms.

· Using firm bid/ask spreads and the respective mid prices, which are consistently available.

Pricing Information Available on the Exchange and Other Sources

The following table lists the Exchange symbols and their descriptions with respect to the Shares and the MVBTCO:

Ticker Description

XBTC Market price per Share on the Exchange

[·] Indicative intra-day value per Share

[·] End of day NAV

[·] Number of outstanding Shares

The intra-day data in the above table is published once every 15 seconds throughout each trading day.

The current market price per Share (symbol: “XBTC”) will be published continuously as trades occur throughout each trading day on the consolidated tape by market data vendors.

The intra-day indicative value per Share (symbol: “[·]”) will be published by the Exchange once every 15 seconds throughout each trading day on the consolidated tape by market data vendors.

The most recent end-of-day NAV (symbol: “[·]”) will be published as of the close of business by market data vendors and available on the Sponsor’s website at [·], or any successor thereto, and will be published on the consolidated tape.

The number of outstanding Shares (symbol: “[·]”) will be published once every 15 seconds throughout the trading day and as of the close of business for the Exchange on the consolidated tape by market data vendors.

Any adjustments made to the MVBTCO will be published on the MVIS website at https://www.mvis-indices.com/ or any successor thereto.

The intra-day levels and closing levels of the MVBTCO are published by MVIS, and the closing NAV is published by the Administrator.

The Shares are not issued, sponsored, endorsed, sold or promoted by the Exchange, and the Exchange makes no representation regarding the advisability of investing in the Shares.

MVIS makes no warranty, express or implied, as to the results to be obtained by any person or entity from the use of the MVBTCO index for any purpose. Index information and any other data calculated and/or disseminated, in whole or part, by MVIS is for informational purposes only, not intended for trading purposes, and provided on an “as is” basis. MVIS does not warrant that the index information will be uninterrupted or error-free, or that defects will be corrected. MVIS also does not recommend or make any representation as to possible benefits from any securities or investments, or third-party products or services. Investors should undertake their own due diligence regarding securities and investment practices.

Summary Risk Factors

An investment in the Shares is speculative and involves a high degree of risk. There is no assurance the Trust will achieve its investment objective or avoid substantial losses. A potential shareholder should not invest in the Shares unless he or she can afford to lose the entire investment. Before investing in the Shares, a potential shareholder should be aware of the various risks of investing in the Trust, including those described below. Additional risks and uncertainties not presently known by the Trust or not presently deemed material by the Trust may also impair the Trust’s operations and performance. The summary risk factors set forth below are intended to highlight certain risks of investing in the Trust. A more extensive discussion of these risks appears beginning on page 13 in “The Risks You Face.”

· Bitcoin is a new technological innovation with a limited history. There is no assurance that usage of bitcoin and the blockchain will continue to grow. A contraction in use of bitcoin or the blockchain may result in increased volatility or a reduction in the price of bitcoin, which could adversely impact the value of the Shares.

· A decline in the adoption of bitcoin could negatively impact the performance of the Trust.

· The loss or destruction of certain “private keys” (numerical codes required by the Trust to access its bitcoin) could prevent the Trust from accessing its bitcoin. Loss of these private keys may be irreversible and could result in the loss of all or substantially all of an investment in the Trust.

· Bitcoin trading prices are volatile and shareholders could lose all or substantially all of their investment in the Trust.

· Regulation of bitcoin continues to evolve in both the U.S. and foreign jurisdictions, which may restrict the use of bitcoin or otherwise impact the demand for bitcoin.

· The Trust’s return may not match the performance of the price of bitcoin due to, among other factors, the Trust incurring operating expenses.

· Sales of newly mined bitcoin may cause the price of bitcoin to decline, which could negatively affect an investment in the Shares.

· The NAV of the Trust may not always correspond to the market price of the Shares for a number of reasons, including price volatility, trading volume, and closing of bitcoin trading platforms due to fraud, failure, security breaches or otherwise. As a result, Baskets may be created or redeemed at a value that differs from the market price of the Shares.

· Disruptions at bitcoin trading platforms (including in the OTC market and on exchanges) and potential consequences of a bitcoin exchange’s or OTC trading desk’s failure could adversely affect an investment in the Shares.

· The Trust’s bitcoin trading may subject the Trust to the risk of counterparty non-performance, potentially negatively impacting the market price of the Shares.

· The Trust’s bitcoin insurance may be unavailable and may not protect the Trust against all losses and liabilities.

· Shareholders of the Trust will be subject to taxation on their allocable share of the Trust’s taxable income, whether or not they receive cash distributions.

Principal Offices

The offices of the Trust and the Sponsor are located at 200 Park Avenue, New York, New York 10166 and the Trust’s telephone number is (212) 273-9585. The office of the Trustee is located at 2711 Centerville Road, Wilmington, Delaware 19808. The offices of the Administrator, Transfer Agent and Cash Custodian are located at 2 Hanson Place, Brooklyn, New York 11217. The offices of the Marketing Agent are located at Three Canal Plaza, Suite 100, Portland, Maine 04101.

Emerging Growth Company Status

The Trust is an “emerging growth company,” as defined in the JOBS Act, and is eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 and reduced disclosure obligations that are not otherwise applicable to the Trust. In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act, for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. However, the Trust is choosing to “opt out” of such extended transition period, and as a result, will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that the decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Offering The Shares represent units of fractional undivided beneficial interest in the net assets of the Trust.

Use of proceeds Proceeds received by the Trust from the issuance and sale of Baskets will consist of cash and, in some instances, may consist partially or wholly of bitcoin. Cash proceeds will be received by the Cash Custodian and transferred to the Trust to purchase bitcoin. The Trust will hold the bitcoin purchased and the bitcoin received by the Trust from the issuance and sale of Baskets, until (1) bitcoin is sold for cash, which is distributed to Authorized Participants in connection with redemptions of Baskets, (2) bitcoin is distributed to Authorized Participants in connection with redemptions of Baskets, (3) bitcoin is sold for cash or transferred to the Sponsor in kind to pay the Sponsor’s Management Fee and the insurance premium related to the insurance policies on the Trust’s bitcoin, or (4) bitcoin is sold for cash to pay Trust expenses and liabilities not assumed by the Sponsor. See “Description of the Trust—Trust Expenses.”

Cboe Symbol XBTC

CUSIP 83422Y101

Creation and Redemption

Authorized Participants The Trust receives cash deposited with the Cash Custodian only by Authorized Participants in exchange for the creation of “Baskets,” each equal to 5 Shares. Conversely, the Trust delivers cash in exchange for Baskets surrendered to it for redemption by Authorized Participants. The Trust issues and redeems Baskets on a continuous basis only to Authorized Participants. Baskets are only issued or redeemed in exchange for the amount of cash (and, potentially, in

-kind for bitcoin) determined by the Administrator on each day that the Exchange is open for regular trading based on the combined net asset value of the Shares included in the Baskets being created or redeemed. No Shares are issued unless the Cash Custodian and/or the Trust confirms that the Trust has been allocated the corresponding amount of cash and/or bitcoin.

The initial amount of cash required for deposit with the Trust to create Shares was [·] per Basket.

Fees are assessed in connection with the creation and redemption of Baskets by Authorized Participants. See “Creation and Redemption of Shares” for more details.

Net Asset Value Net asset value means the total assets of the Trust including, but not limited to, all bitcoin and cash less total liabilities of the Trust, each determined on the basis of generally accepted accounting principles.

The Administrator determines the net asset value of the Trust on each day that the Exchange is open for regular trading, as promptly as practical after 4:00 PM E.T. The net asset value of the Trust is the aggregate value of the Trust’s assets less its estimated accrued but unpaid liabilities (which include accrued expenses). In determining the Trust’s net asset value, the Administrator values the bitcoin held by the Trust based on the price set by the MVBTCO as of 4:00 p.m. E.T. (“MVBTCO Price”). The Administrator also determines the net asset value per share. If on a day when the Trust’s net asset value is being calculated the MVBTCO Price for that day is not available, the Administrator will value the bitcoin held by the Trust based on alternative means. See “Description of the Trust—Pricing Sources.”

Trust Fees and Expenses The Trust’s only ordinary recurring operating expenses are expected to be the Sponsor’s management fee of [·]% of the net asset value of the Trust (“Management Fee”), the insurance premium related to the insurance policies on the Trust’s bitcoin, which is expected to be approximately [·]% of the net asset value of the Trust (“bitcoin Insurance Fee”) and salaries paid to the Trust principals and employees and expenses related to custody of the Trust’s bitcoin, which together with the Trust principal and employee salaries is expected to be approximately $200,000 per annum. In exchange for the Management Fee, the Sponsor has agreed to assume the ordinary administrative and marketing expenses that the Trust is expected to incur.

The Sponsor’s Management Fee will accrue daily based on the prior business day’s net asset value and will be payable on a monthly basis in arrears. The Trust will sell bitcoin to raise cash to pay the Management Fee, the bitcoin Insurance Fee and other expenses not assumed by the Sponsor. At the Sponsor’s discretion, the Trust may pay the Sponsor’s Management Fee in bitcoin. See “Description of the Trust—Trust Expenses.”

Organization and Offering Expenses The Sponsor will be responsible for paying all of the expenses incurred in connection with organizing the Trust as well as the expenses incurred in connection with the offering of the Trust’s Shares.

Extraordinary Fees and Expenses The Trust will be responsible for paying, or for reimbursing the Sponsor or its affiliates for paying, all the extraordinary fees and expenses, if any, of the Trust. Extraordinary fees and expenses are fees and expenses which are non-recurring and unusual in nature, such as legal claims and liabilities, litigation costs or indemnification or other unanticipated expenses. Extraordinary fees and expenses also include material expenses which are not currently anticipated obligations of the Trust. Such extraordinary fees and expenses, by their nature, are unpredictable in terms of timing and amount.

Insurance The Trust will be responsible for paying the premiums associated with the insurance coverage for the bitcoin held by the Trust. The Trust will also be responsible for losses up to the insurance’s deductible of $500,000.

Tax Considerations A shareholder will be treated, for federal tax purposes, as if it directly owns a pro rata share of the Trust’s assets and directly receives that share of any Trust income and incurs that share of the Trust’s expenses. Shareholders of the Trust will be subject to taxation on their allocable share of the Trust’s taxable income, whether or not they receive cash distributions. Each delivery, transfer or sale of bitcoin by the Trust in connection with redemptions or to pay the Sponsor’s Management Fee, bitcoin Insurance Fee, Trust principal and employee salaries, bitcoin custody expenses or other expenses could be a taxable event to shareholders. See “Federal Income Tax Consequences—Taxation of U.S. Shareholders” and “Purchases by Employee Benefit Plans.”

Suspension of Issuance,

Transfers and Redemptions The Sponsor may suspend the delivery or registration of transfers of Shares, or may refuse a particular deposit or transfer at any time, if the Sponsor considers it advisable or necessary for any reason. Redemptions by Authorized Participants of Shares may and, on the direction of the Sponsor, shall, be generally suspended or particularly rejected by the Transfer Agent or Marketing Agent (1) during any period in which regular trading on the Exchange is suspended or restricted, or the Exchange is closed, (2) the order is not in proper form as determined by the Trust, Transfer Agent or Marketing Agent, (3) during an emergency as a result of which delivery, disposal or evaluation of bitcoin is not reasonably practicable, or (4) for such other period as the Sponsor determines to be necessary for the protection of shareholders. In addition, the Trust will reject a redemption order if the fulfillment of the order might be unlawful or if, as a result of the redemption, the number of remaining outstanding Shares would be reduced to fewer than the number of Shares in one Basket. See “Creation and Redemption of Shares—Rejection of purchase orders” and “Creation and Redemption of Shares—Suspension or rejection of redemption orders.”

Termination Events The Trust will terminate and liquidate if certain events occur. See “Description of the Trust—Termination of the Trust.”

Authorized Participants Authorized Participants may create and redeem Baskets.

Each Authorized Participant must: (1) be a registered broker-dealer and a member in good standing with the Financial Industry Regulatory Authority (“FINRA”); (2) be a participant in DTC; and (3) have entered into an agreement with the Sponsor and the Transfer Agent (the “Authorized Participant Agreement”). The Authorized Participant Agreement provides the procedures for the creation and redemption of Baskets. A list of the current Authorized Participants can be obtained from the Administrator or the Sponsor.

Clearance and Settlement The Shares will be evidenced by one or more global certificates that the Trust will issue to DTC. The Shares are issued only in book-entry form. Shareholders may hold their Shares through DTC, if they are participants in DTC, or indirectly through entities that are participants in DTC.

As of the close of business on [·], 2018, the net asset value of the Trust, which represents the value of the bitcoin and cash deposited into and held by the Trust, was $ [·] and the net asset value per Share was $ [·].

An investment in the Trust involves the risk of losing money. Consider the risks below as well as the rest of the information in this Prospectus before making an investment decision.

Risks Associated With Investing Directly or Indirectly in bitcoin

Bitcoin Has a Short History.

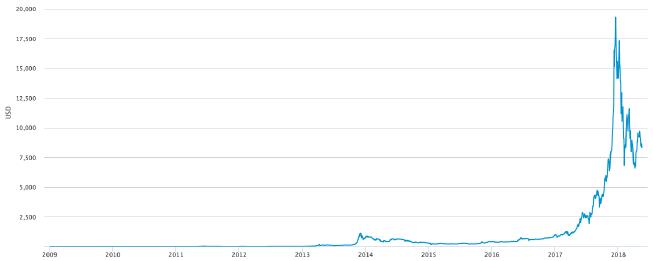

Bitcoin was invented in 2009: the asset, bitcoin, and its trading history thus have existed for a relatively short time, which limits a potential shareholder’s ability to evaluate an investment in the Trust.

The Volatility of the Price of bitcoin May Affect the Value of the Shares.

The Shares are designed to provide shareholders with exposure to the daily change in the U.S. dollar price of bitcoin, as measured by the MVBTCO, and the value of the Shares correlates directly to the value of the bitcoin held by the Trust, less the Trust’s fees and expenses. The price of bitcoin is volatile and may be influenced by, among other things, trading volume and closing of bitcoin trading platforms due to fraud, failure, security breaches or otherwise. Speculators and investors who seek to profit from trading and holding bitcoin generate a significant portion of bitcoin demand. The Sponsor believes that bitcoin speculation regarding future appreciation in the value of bitcoin may inflate and make more volatile the price of a bitcoin as measured by the MVBTCO. As a result, bitcoin may be more likely to fluctuate in value due to changing investor confidence in future appreciation in the price of bitcoin. In the event the price of bitcoin declines, the value of the Shares would decline proportionately. The price of the Shares may change quickly in response to changes in the price of bitcoin.

A Decline in the Adoption of Bitcoin Could Impact the Price of the Shares.

As a new asset and technological innovation, the Bitcoin industry is subject to a high degree of uncertainty. The adoption of bitcoin will require growth in its usage and in the blockchain, for various applications. Adoption of bitcoin will also require an accommodating regulatory environment. The Trust is not actively managed and will not have any strategy relating to the development of bitcoin and non-financial applications for the blockchain. A lack of expansion in usage of bitcoin and the blockchain could adversely affect an investment in the Shares.

In addition, there is no assurance that bitcoin will maintain its value over the long-term. The value of bitcoin is subject to risks related to its usage. Even if growth in bitcoin adoption occurs in the near or medium-term, there is no assurance that bitcoin usage will continue to grow over the long-term. A contraction in use of bitcoin may result in increased volatility or a reduction in the price of bitcoin, which would adversely impact the value of the Shares.

Sales of Newly Mined bitcoin May Cause the Price of bitcoin to Decline, Which Could Negatively Affect an Investment in the Shares.

Newly created bitcoin are generated through a process referred to as “mining,” and such bitcoin are referred to as “newly mined bitcoin” (see “Bitcoin and the Bitcoin Industry—bitcoin Mining and Transaction Fees”). If entities engaged in bitcoin mining choose not to hold the newly mined bitcoin, and, instead, make them available for sale, there can be downward pressure on the price of bitcoin. A bitcoin mining operation may be more likely to sell a higher percentage of its newly created bitcoin, and more rapidly so, if it is operating at a low profit margin, thus reducing the price of bitcoin. Lower bitcoin prices may result in further tightening of profit margins for miners and worsening profitability, thereby potentially causing even further selling pressure. Decreasing profit margins and increasing sales of newly mined bitcoin could result in a reduction in the price of bitcoin, which could adversely impact an investment in the Shares.

The Loss or Destruction of a Private Key Required to Access bitcoin may be Irreversible.

Transfers of bitcoin among users are accomplished via bitcoin transactions (i.e., sending bitcoin from one user to another). The creation of a bitcoin transaction requires the use of a unique numerical code known as a “private key.” In the absence of the correct private key corresponding to a holder’s particular bitcoin, the bitcoin is inaccessible for usage. The Trust safeguards and keeps private the private keys relating to the Trust’s bitcoin holdings. Although the Trust maintains insurance (see “The Risks You Face—Insurance Related Risks”), to the extent the Trust’s private key is lost, destroyed or otherwise compromised and no backup of the private key is accessible, the Trust will be unable to access its bitcoin. Any such loss could adversely affect an investment in the Shares.

A Failure to Properly Monitor and Upgrade the Bitcoin Protocol by the Contributors of the Protocol Could Adversely Affect the Bitcoin Industry.

As discussed more fully below in “Bitcoin and the Bitcoin Industry,” the Bitcoin protocol runs on open source software that can be altered. The Bitcoin protocol could contain unknown flaws, which, upon detection by a malicious actor, could be used to damage the Bitcoin network. To the extent that software developers involved in maintaining the bitcoin protocol are unable to address potential flaws in the Bitcoin protocol adequately and in a timely manner, the Bitcoin industry may be adversely affected and any such result could adversely affect an investment in the Shares.

A Temporary or Permanent Blockchain “Fork” Could Adversely Affect an Investment in the Shares.

The Bitcoin software and protocol are open source. Any user can download the software, modify it and then propose that Bitcoin users and miners adopt the modification. When a modification is introduced and a substantial majority of users and miners consent to the modification, the change is implemented and the Bitcoin network remains uninterrupted. However, if less than a substantial majority of users and miners consent to the proposed modification, and the modification is not compatible with the software prior to its modification, the consequence would be what is known as a “fork” (i.e., “split”) of the Bitcoin network (and the blockchain), with one prong running the pre-modified software and the other running the modified software. The effect of such a fork would be the existence of two (or more) versions of the Bitcoin network running in parallel, but with each version’s bitcoin (the asset) lacking interchangeability.

Additionally, a fork could be introduced by an unintentional, unanticipated software flaw in the multiple versions of otherwise compatible software users run. Although chain forks could be addressed by community-led efforts to merge the two chains (and in fact, prior historical forks have been so merged), there have also been other forks where a substantial number of Bitcoin users and miners adopted an incompatible version of Bitcoin while resisting community-led efforts to merge the two chains. This is referred to as a permanent fork. Permanent forks have occurred already (such as the fork in August 2017, which resulted in the creation of “bitcoin cash”). If another permanent fork occurs, then the Trust would hold equal amounts of both the original bitcoin and the alternative new bitcoin. As a result, the Trust would need to decide whether to continue to hold the original bitcoin, the alternative new bitcoin or both, and what action to take with respect to the unselected bitcoin, such as the possible sale of the unselected bitcoin. The Trust’s decision to continue to hold either the original, the alternative new bitcoin or both would be based on factors such as the market value and liquidity of the original bitcoin versus the alternative new bitcoin, the computer processing power devoted by miners to the original network versus the alternative new network, technical stability of the alternative new network and the establishment of a technical and commercial ecosystem for the alternative new network.

A Bitcoin fork could adversely affect an investment in the Shares or the ability of the Trust to operate.

A Disruption of the Internet May Affect Bitcoin Operations, Which May Adversely Affect the Bitcoin Industry and an Investment in the Shares.

The Bitcoin network’s functionality relies on the Internet. A significant disruption of Internet connectivity (i.e., affecting large numbers of users or geographic regions) could prevent the Bitcoin network’s functionality and operations until the Internet disruption is resolved. An Internet disruption could adversely affect an investment in the Shares or the ability of the Trust to operate.

An Actor Capable of Gaining Control In Excess of 50 Percent of the Transaction Confirmation Processing Power Could Manipulate the Blockchain and Adversely Affect the Bitcoin Industry.

The process of bitcoin mining adds new blocks to the blockchain. Blocks are sets of bitcoin transactions (i.e., records of transfers of bitcoin among users) and the blockchain is the database of all bitcoin transactions. The blockchain is stored and updated by computers participating in the Bitcoin network. Through the bitcoin mining process, unconfirmed bitcoin transactions are validated and grouped into a new block, which is then added to the blockchain (relatedly, bitcoin mining is the process by which new bitcoin are created). Bitcoin transactions can only be confirmed via the mining process, which makes mining a crucial component of the Bitcoin network.

The Bitcoin protocol is designed to work properly so long as no bitcoin miner has more than 50 percent of mining processing power in operation on the Bitcoin network. If a malicious actor obtains more than 50 percent of the processing power dedicated to mining, the malicious actor may be able to prevent transactions from being confirmed or change the date and time at which transactions are confirmed.

By possessing more than 50 percent of mining processing capacity, and thus having the majority of block creation power, a malicious actor might be able to create a fictional version of the blockchain database, in an attempt to modify the historical transaction record in the blockchain. By virtue of the fact that newer transactions in newer blocks in the blockchain refer to older transactions in prior blocks, the blockchain provides a historical record of all bitcoin transactions. A modification of the historical record could be used to trick Bitcoin users regarding the confirmation status of their transactions. A user may believe that he or she has already received a quantity of bitcoin in a confirmed transaction, but the malicious actor could, in essence, undo the transaction by changing the historical record. The victimized user(s) would later discover the bitcoin they thought to have received had, in fact, gone to another recipient. The perpetuation of changes to the historical transaction record would be detrimental to the Bitcoin network and adversely affect an investment in the Shares.

In addition, a reduction in the aggregate processing power expended by Bitcoin miners could increase the likelihood of a malicious actor obtaining control in excess of 50 percent of the mining processing power, potentially permitting such actor to manipulate the blockchain. To the extent such a malicious actor does not yield its majority control of the processing power or the Bitcoin community does not reject the blocks produced by the malicious actor, reversing any changes made to the blockchain may not be possible. Such changes could adversely affect an investment in the Shares or the ability of the Trust to operate.

Entities Engaged in the Mining Process Could be Coerced Into Acting in a Manner Detrimental to the Bitcoin Network.

If a nation state or other large and well-capitalized entity wanted to damage the Bitcoin network, an attack could be attempted on bitcoin miners. The attacking entity could attempt to coerce, by legal or illegal means, bitcoin miners who, in the aggregate, control more than 50 percent of the bitcoin mining capacity into manipulating the blockchain in a manner detrimental to the Bitcoin network. Such an attack could adversely affect an investment in the Shares or the ability of the Trust to operate.

A Well-Capitalized Entity Could Create Large Amounts of Mining Processing Power as a Means of Acting in a Manner Detrimental to the Bitcoin Network.

If a nation state or other large and well-capitalized entity wanted to damage the Bitcoin network, the entity could attempt to create, either from scratch or via large-scale purchases, a massive amount of mining processing power. If the entity were to create an amount of mining processing power in excess of 50 percent of the aggregate mining processing power, the entity could attempt to manipulate the blockchain in a manner detrimental to the Bitcoin network. Such an attack could adversely affect an investment in the Shares or the ability of the Trust to operate.

Miners May Cease Expanding Processing Power to Create Blocks and Verify Transactions if They Are Not Adequately Compensated, Which May Adversely Affect an Investment in the Shares or the Ability of the Trust to Operate.

Miners generate revenue from both newly created bitcoin (known as the “block reward”) and from fees taken upon verification of transactions. If the aggregate revenue from transaction fees and the block reward is below a miner’s cost, the miner may cease operations. Additionally, in the event of a fork of the Bitcoin network, some miners may choose to mine the alternative new bitcoin resulting from the fork, thus reducing processing power on the original bitcoin blockchain. An acute cessation of mining operations would reduce the collective processing power on the blockchain, which would adversely affect the transaction verification process by temporarily decreasing the speed at which blocks are added to the blockchain and make the blockchain more vulnerable to a malicious actor obtaining control in excess of 50 percent of the processing power on the blockchain. Reductions in processing power could result in material, though temporary, delays in transaction confirmation time. Any reduction in confidence in the transaction verification process or mining processing power may adversely impact an investment in the Shares or the ability of the Trust to operate.

Miners Could Act in Collusion to Raise Transaction Fees, Which May Adversely Affect the Usage of the Bitcoin Network.

Bitcoin miners, functioning in their transaction confirmation capacity, collect fees for each transaction they confirm. Miners validate unconfirmed transactions by adding the previously unconfirmed transactions to new blocks in the blockchain. Miners are not forced to confirm any specific transaction, but they are economically incentivized to confirm valid transactions as a means of collecting fees. Miners have historically accepted relatively low transaction confirmation fees, because miners have a very low marginal cost of validating unconfirmed transactions (see “Bitcoin and the Bitcoin Industry—bitcoin Mining and Transaction Fees”). If miners collude in an anticompetitive manner to reject low transaction fees, then Bitcoin users could be forced to pay higher fees, thus reducing the attractiveness of the Bitcoin network. Bitcoin mining occurs globally and it may be difficult for authorities to apply antitrust regulations across multiple jurisdictions. Any collusion among miners may adversely impact the attractiveness of the Bitcoin network and may adversely impact an investment in the Shares or the ability of the Trust to operate.

The Incentive for Miners to Continue to Contribute Processing Power to the Blockchain Will Transition to Transaction Verification Fees as Block Rewards Decrease. Higher Transaction Verification Fees May Negatively Impact Demand for bitcoin, Which May Adversely Affect the Price of bitcoin and an Investment in the Shares.

The block reward will decrease over time. In the summer of 2020, the block reward will reduce from 12.5 to 6.25 bitcoin, and to 3.125 bitcoin in 2024. As the block reward continues to decrease over time, the mining incentive structure will transition to a higher reliance on transaction verification fees in order to incentivize miners to continue to dedicate processing power to the blockchain. If transaction verification fees become too high, the marketplace may be reluctant to use bitcoin. Decreased demand for bitcoin may adversely affect its price, which may adversely affect an investment in the Shares.

Any Widespread Delays in Recording bitcoin Transactions Could Result in a Loss of Confidence in Bitcoin, Which Could Adversely Impact an Investment in the Shares.

To the extent that bitcoin miners cease to record transactions in newly created blocks, such transactions will not be recorded on the blockchain. In a newly formed block, miners can include as few as zero transactions (e.g., an “empty block”) or as many as several thousand transactions. Currently, there are no known incentives for miners to elect to exclude the recording of transactions in newly created blocks. However, to the extent that any such incentives arise, actions of miners creating a significant number of empty blocks could delay the recording and confirmation of transactions on the blockchain. Any systemic delays in the recording and confirmation of transactions on the blockchain could result in greater risk of fraudulent activity, and a loss of confidence in Bitcoin, which could adversely impact an investment in the Shares or the ability of the Trust to operate.

It is Possible that a Small Group of Early bitcoin Adopters Control Large Amounts of Existing bitcoin. To the Extent these Individuals Sell their bitcoin, the Price of bitcoin May Decline.

There is no registry showing which individuals or entities own bitcoin or the quantity of bitcoin owned by any particular person or entity. It is possibly, and in fact, reasonably likely, that a small group of early bitcoin adopters hold a significant proportion of the bitcoin that has thus far been created. There are no regulations in place that would prevent a large holder of bitcoin from selling their bitcoin. Such bitcoin sales may adversely affect the price of bitcoin and an investment in the Shares.

A Successful Competitor to Bitcoin May Negatively Impact the Price of bitcoin and Adversely Affect an Investment in the Shares.

Bitcoin currently enjoys a first-mover advantage, with the largest user base, technological adoption, infrastructure development and dedicated transaction confirmation power (i.e., computing power dedicated to bitcoin mining) among its competitors. Having a large amount of dedicated computing power for mining results in greater user confidence regarding the security and long-term stability of the Bitcoin network and the blockchain. As a result, the advantage of more users and miners makes Bitcoin increasingly secure, which makes it more attractive to new users and miners, resulting in a network effect that strengthens its first-to-market advantage. There are numerous Bitcoin competitors, however, referred to as “altcoins.” To the extent an altcoin gains in popularity and greater market share, the use and price of bitcoin could be negatively impacted, which may adversely affect an investment in the Shares. Similarly, bitcoin or the price of bitcoin could be negatively impacted by competition from incumbents in the credit card and payments industries, which may adversely affect an investment in the Shares.

An Investment in the Shares May Be Adversely Affected By Competition From Other Methods of Investing in bitcoin.

The Trust will compete with direct investments in bitcoin and other potential financial vehicles, including derivatives on bitcoin and/or potentially other securities backed by or linked to bitcoin and exchange traded products similar to the Shares. Market and financial conditions, and other conditions beyond the Sponsor’s control, may make it more attractive to invest in other financial instruments or to invest in bitcoin directly, which could limit the market for the Shares and reduce the liquidity of the Shares.

Large-Scale Sales of bitcoin, Including as a Result of Political or Economic Crisis, May Adversely Affect an Investment in the Shares.

Political or economic events, either domestically or in foreign jurisdictions, may motivate large-scale buys or sales of bitcoin. Large-scale bitcoin sales may result in a decline in the price of bitcoin, which may adversely affect an investment in the Shares.

Market Related Risks

The Trust is Subject to Market Risk.

Market risk refers to the risk that the market price of bitcoin held by the Trust will rise or fall, sometimes rapidly or unpredictably. An investment in the Trust’s Shares is subject to market risk, including the possible loss of the entire principal of the investment.

NAV May Not Always Correspond to the Market Price of bitcoin and, as a Result, Baskets May Be Created or Redeemed at a Value that Differs From the Market Price of the Shares.

The NAV of the Trust will change as fluctuations occur in the market price of the Trust’s bitcoin holdings. Shareholders should be aware that the public trading price of a Basket may be different from the NAV of a Basket (i.e., Shares may trade at a premium over, or a discount to, the NAV of a Basket) and similarly the public trading price per Share may be different from the NAV for a number of reasons, including price volatility, trading volume, and closing of bitcoin trading platforms due to fraud, failure, security breaches or otherwise. Consequently, an Authorized Participant may be able to create or redeem a Basket at a discount or a premium to the public trading price per Share. This price difference may be due, in large part, to the fact that supply and demand forces at work in the secondary trading market for Shares are related, but not identical, to the supply and demand forces influencing the market price of bitcoin, including as reflected on the MVBTCO. Shareholders also should note that the size of the Trust in terms of total bitcoin held may change substantially over time and as Baskets are created and redeemed.

Authorized Participants or their clients may have an opportunity to realize a riskless profit if they can purchase a Basket at a discount to the public trading price of the Shares or can redeem a Basket at a premium over the public trading price of the Shares. The Sponsor believes that the exploitation of such arbitrage opportunities by Authorized Participants and their clients and customers should cause the public trading price of the Shares to track NAV closely over time; however, there can be no assurance that this will be the case.

To the extent the Sponsor permits Authorized Participants to create and redeem Baskets in-kind, Authorized Participants may purchase bitcoin for Basket creation or sell bitcoin from Basket redemptions on public or private markets not included among the constituent bitcoin OTC platforms of the MVBTCO, and such transactions may take place at prices materially higher or lower than the MVBTCO spot price. Furthermore, while the MVBTCO provides a spot price based on the price of bitcoin on the MVBTCO’s constituent bitcoin OTC platforms at any given time, the prices on each such bitcoin OTC platform may not be equal to the value of a bitcoin as represented by the MVBTCO. It is possible that the price of bitcoin on the bitcoin OTC platform(s) or bitcoin exchange(s) used by an Authorized Participant could be materially higher or lower than the MVBTCO representation of the bitcoin price. Under either such circumstance, the arbitrage mechanism will function to link the price of the Shares to the prices at which Authorized Participants are able to purchase or sell large aggregations of bitcoin. To the extent such prices differ materially, the price of the Shares may no

longer track, whether temporarily or over time, the price of bitcoin, which could adversely impact an investment in the Trust by reducing shareholders’ confidence in the Shares’ ability to track the price of bitcoin. Furthermore, to the extent the market price of bitcoin is particularly volatile, Authorized Participants may not wish to create and redeem Baskets with the Trust at any given time.

Suspension or Disruptions of Market Trading May Adversely Affect the Value of Shares.

The Shares will be listed and traded on the Exchange. Trading in Shares may be halted due to market conditions, or in light of the Exchange rules and procedures, for reasons that, in view of the Exchange, make trading in Shares inadvisable. In addition, trading is subject to trading halts caused by extraordinary market volatility pursuant to “circuit breaker” rules that require trading to be halted for a specific period based on a specific market decline. There can be no assurance that the requirements necessary to maintain the listing of the Shares will continue to be met or will remain unchanged.

The Lack of Active Trading Markets For the Shares of the Trust May Result in Losses on an Investment in the Trust at the Time of Disposition of Shares.

Although the Shares will be listed and traded on the Exchange, there can be no guarantee that an active trading market for the Shares will develop or will be maintained. Even if an active trading market does develop, it may not provide significant liquidity, and the Shares may not trade at prices advantageous to shareholders. If a shareholder wishes to sell Shares at a time when no active market for such Shares exists, the price received for the Shares (assuming that the shareholder is able to sell them) likely will be lower than the price a shareholder would receive if an active market did exist and, accordingly, the shareholder may suffer significant losses.

Shareholders That Are Not Authorized Participants May Only Purchase or Sell Their Shares in Secondary Trading Markets, and the Conditions Associated With Trading in Secondary Markets May Adversely Affect Shareholders’ Investment in the Shares.

Only Authorized Participants may create or redeem Baskets at a price equal to the NAV of a Basket. In addition to creating or redeeming Baskets directly with the Trust, Authorized Participants may also buy or sell Shares through the secondary market at market prices. In contrast, ordinary shareholders who are not Authorized Participants are limited to secondary market transactions at market prices. Because ordinary shareholders who are not Authorized Participants may not create or redeem Baskets, these shareholders do not have identical arbitrage opportunities that are available to Authorized Participants, and therefore, ordinary shareholders who are not Authorized Participants are subject to the state of the secondary market at the time of a transaction. Ordinary shareholders who are not Authorized Participants may be required to conduct a transaction on the secondary market when conditions are adverse to a shareholder’s interests, such as when the market price for Shares is lower than the NAV per Share and the ordinary shareholder seeks to sell Shares.

The Trust’s Acquisition and Sale of bitcoin May Impact the Supply and Demand of bitcoin, Which May Have a Negative Impact on the Price of the Shares.

If the number of bitcoin acquired by the Trust is large enough relative to global bitcoin supply and demand, further creations and redemptions of Shares could have an impact on the supply of and demand for bitcoin in a manner unrelated to other factors affecting the global market for bitcoin. Such an impact could affect the MVBTCO, which would directly affect the price at which Shares are traded on the Exchange or the price of future Baskets created or redeemed by the Trust.

A Possible “Short Squeeze” Due to a Sudden Increase in Demand for the Shares that Largely Exceeds Supply May Lead to Price Volatility in the Shares.

Bitcoin price speculation may involve long and short exposures. To the extent that aggregate short exposure exceeds the number of Shares available for purchase (for example, in the event that large redemption requests by Authorized Participants dramatically affect Share liquidity), shareholders with short exposure may have to pay a premium to repurchase Shares for delivery to Share lenders. Those repurchases may, in turn, dramatically increase the price of the Shares until additional Shares are created through the creation process. This is often referred to as a “short squeeze.” A short squeeze could lead to volatile price movements in the Shares that are not directly correlated to the price of bitcoin.