UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

FOR THE QUARTERLY PERIOD ENDED

or

Commission File Number:

(Exact Name of Registrant as Specified in its Charter)

| (State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification Number) |

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Trading symbol: |

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past

90 days.

Indicate by check mark whether the registrant

has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and

posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☐ | (Do not check if a smaller reporting company) | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is

a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes ☐ No

As of December 12, 2022, the registrant had the following shares outstanding:

| Class A common stock, $.01 par value: | |

| Class B common stock, $.01 par value: |

ZEDGE, INC.

TABLE OF CONTENTS

i

PART I. FINANCIAL INFORMATION

Item 1. Condensed Consolidated Financial Statements

ZEDGE, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except par value data)

| October 31, | July 31, | |||||||

| 2022 | 2022 | |||||||

| (Unaudited) | ||||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Trade accounts receivable | ||||||||

| Prepaid expenses and other receivables | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Goodwill | ||||||||

| Deferred tax assets, net | ||||||||

| Other assets | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities and stockholders’ equity | ||||||||

| Current liabilities: | ||||||||

| Trade accounts payable | $ | $ | ||||||

| Deferred acquisition payment payable | - | |||||||

| Contingent consideration-current portion | ||||||||

| Accrued expenses and other current liabilities | ||||||||

| Deferred revenues | ||||||||

| Total current liabilities | ||||||||

| Term Loan, net of deferred financing costs | - | |||||||

| Contingent consideration-long term portion | ||||||||

| Other liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and contingencies (Note 10) | ||||||||

| Stockholders’ equity: | ||||||||

| Preferred stock, $ | ||||||||

| Class A common stock, $ | ||||||||

| Class B common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Retained earnings | ||||||||

| Treasury stock, | ( | ) | ( | ) | ||||

| Total stockholders’ equity | ||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||

See accompanying notes to unaudited condensed consolidated financial statements.

1

ZEDGE, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME

(in thousands, except for per share data)

(Unaudited)

| Three Months Ended | ||||||||

| October 31 | ||||||||

| 2022 | 2021 | |||||||

| Revenues, net | $ | $ | ||||||

| Costs and expenses: | ||||||||

| Direct cost of revenues (excluding amortization of capitalized software and technology development costs which is included below) | ||||||||

| Selling, general and administrative | ||||||||

| Depreciation and amortization | ||||||||

| Change in fair value of contingent consideration | ( | ) | ||||||

| (Loss) income from operations | ( | ) | ||||||

| Interest and other income, net | ||||||||

| Net loss resulting from foreign exchange transactions | ( | ) | ( | ) | ||||

| (Loss) income before income taxes | ( | ) | ||||||

| (Benefit from) provision for income taxes | ( | ) | ||||||

| Net (Loss) Income | $ | ( | ) | $ | ||||

| Other comprehensive (loss) income: | ||||||||

| Changes in foreign currency translation adjustment | ( | ) | ||||||

| Total other comprehensive (loss) income | ( | ) | ||||||

| Total comprehensive (loss) income | $ | ( | ) | $ | ||||

| (Loss) income per share attributable to Zedge, Inc. common stockholders: | ||||||||

| Basic | $ | ( | ) | $ | ||||

| Diluted | $ | ( | ) | $ | ||||

| Weighted-average number of shares used in calculation of (loss) income per share: | ||||||||

| Basic | ||||||||

| Diluted | ||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

2

ZEDGE, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(in thousands)

(Unaudited)

| Class A Common Stock | Class B Common Stock | Additional Paid-in | Accumulated Other Comprehensive | Retained | Treasury Stock | Total Stockholders’ | ||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Loss | Earnings | Shares | Amount | Equity | |||||||||||||||||||||||||||||||

| Balance – July 31, 2022 | $ | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | |||||||||||||||||||||||||||||

| Stock-based compensation | - | |||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||||

| Net loss | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||||

| Balance – October 31, 2022 | $ | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | |||||||||||||||||||||||||||||

| Class A Common Stock | Class B Common Stock | Additional Paid-in | Accumulated Other Comprehensive | Accumulated | Treasury Stock | Total Stockholders’ | ||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Loss | Deficit | Shares | Amount | Equity | |||||||||||||||||||||||||||||||

| Balance – July 31, 2021 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||||||

| Stock-based compensation | - | |||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | ||||||||||||||||||||||||||||||||||||||

| Net income | - | - | ||||||||||||||||||||||||||||||||||||||

| Balance -October 31, 2021 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

3

ZEDGE, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(Unaudited)

| Three months ended October, 31 | 2022 | 2021 | ||||||

| Operating activities | ||||||||

| Net (loss) income | $ | ( | ) | $ | ||||

| Adjustments to reconcile net (loss) income to net cash provided by operating activities: | ||||||||

| Depreciation | ||||||||

| Amortization of intangible assets | ||||||||

| Amortization of capitalized software and technology development costs | ||||||||

| Change in fair value of contingent consideration | ( | ) | - | |||||

| Stock-based compensation | ||||||||

| Change in assets and liabilities: | ||||||||

| Trade accounts receivable | ( | ) | ( | ) | ||||

| Prepaid expenses and other current assets | ( | ) | ( | ) | ||||

| Other assets | ( | ) | ||||||

| Trade accounts payable and accrued expenses | ||||||||

| Deferred revenue | ( | ) | ( | ) | ||||

| Net cash provided by operating activities | ||||||||

| Investing activities | ||||||||

| Final payments for asset acquisitions | ( | ) | - | |||||

| Capitalized software and technology development costs and purchase of equipment | ( | ) | ( | ) | ||||

| Net cash used in investing activities | ( | ) | ( | ) | ||||

| Financing activities | ||||||||

| Proceed from term loan payable | - | |||||||

| Payment of deferred financing costs | ( | ) | - | |||||

| Purchase of treasury stock in connection with share buyback program and restricted stock vesting | ( | ) | ( | ) | ||||

| Net cash provided by (used in) financing activities | ( | ) | ||||||

| Effect of exchange rate changes on cash and cash equivalents | ( | ) | ||||||

| Net increase in cash and cash equivalents | ||||||||

| Cash and cash equivalents at beginning of period | ||||||||

| Cash and cash equivalents at end of period | $ | $ | ||||||

| SUPPLEMENTAL SCHEDULE OF NON-CASH INVESTING AND FINANCING ACTIVITIES | ||||||||

| Acquisition of Emojipedia through release of escrow funds of $ | $ | $ | ||||||

| Accounts receivable from certain Emojipedia websites collected by Seller | $ | $ | ||||||

See accompanying notes to unaudited condensed consolidated financial statements.

4

ZEDGE, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

Note 1—Basis of Presentation and Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements of Zedge, Inc. and its subsidiaries, GuruShots Ltd. (“GuruShots”), Zedge Europe AS and Zedge Lithuania UAB (the “Company”), have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 8 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the three months ended October 31, 2022 are not necessarily indicative of the results that may be expected for the fiscal year ending July 31, 2023 or any other period. The balance sheet at July 31, 2022 has been derived from the Company’s audited financial statements at that date but does not include all of the information and footnotes required by U.S. GAAP for complete financial statements. For further information, please refer to the consolidated financial statements and footnotes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended July 31, 2022, as filed with the U.S. Securities and Exchange Commission (the “SEC”).

The Company’s fiscal year ends on July 31 of each calendar year. Each reference below to a fiscal year refers to the fiscal year ending in the calendar year indicated (e.g., fiscal 2022 refers to the fiscal year ending July 31, 2022).

Reportable Segments

Effective August 1, 2022, the Company revised the presentation of segment information to reflect the addition, following the acquisition of GuruShots, of the GuruShots App to the Company’s portfolio of mobile apps resulting from the GuruShots acquisition (see Note 5). As such, the Company now reports operating results through two reportable segments: Zedge App and GuruShots App, as further discussed in Note 12.

Use of Estimates

The preparation of the Company’s unaudited condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenue and expenses, as well as related disclosure of contingent assets and liabilities. Actual results could differ materially from the Company’s estimates due to risks and uncertainties, including uncertainty in the current economic environment due to various global events. To the extent that there are material differences between these estimates and actual results, the Company’s financial condition or operating results will be affected. The Company bases its estimates on past experience and other assumptions that the Company believes are reasonable under the circumstances, and the Company evaluates these estimates on an ongoing basis.

Recently Issued Accounting Pronouncements Not Yet Adopted

In June 2016, the FASB issued ASU 2016-13, Financial Instruments - Credit Losses (Topic 326), which requires the measurement and recognition of expected credit losses for financial assets held at amortized cost. ASU 2016-13 replaces the existing incurred loss impairment model with an expected loss model which requires consideration of forward-looking information to calculate credit loss estimates. These changes will result in an earlier recognition of credit losses. The Company’s financial assets held at amortized cost include accounts receivable. The amendments in ASU 2020-05 deferred the effective date for Topic 326 to fiscal years beginning after December 15, 2022. The Company will adopt the new standard effective August 1, 2023 and does not expect the adoption of this guidance to have a material impact on its consolidated financial statements.

In October 2021, the FASB issued ASU No. 2021-08, Accounting for Contract Assets and Contract Liabilities From Contracts With Customers. ASU 2021-08 requires an acquirer in a business combination to recognize and measure contract assets and contract liabilities from acquired contracts using the revenue recognition guidance in Accounting Standards Codification (“ASC”) Topic 606, Revenue from Contracts with Customers, rather than the prior requirement to record them at fair value. The guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2022. Early adoption is permitted. The Company will adopt the new standard effective August 1, 2023 and does not expect the adoption of this guidance to have a material impact on its consolidated financial statements.

5

With the exception of the standards discussed above, there have been no other recent accounting pronouncements or changes in accounting pronouncements during the three months ended October 31, 2022, as compared to the recent accounting pronouncements described in the Company’s Annual Report on Form 10-K for the fiscal year ended July 31, 2022, that are of significance or potential significance to the Company.

Significant Accounting Policies

Other than intangible assets described below, there have been no material changes to the Company’s significant accounting policies from its Annual Report on Form 10-K for the fiscal year ended July 31, 2022.

Related Party Transactions

The Company has no material related party transactions that have impacted the consolidated balance sheets for the years ended October 31, 2022 or July 31, 2022, or the consolidated statements of operations and comprehensive (loss) income for the three months ended October 31, 2022 or 2021.

Note 2—Revenue

Disaggregation of Revenue

The following table presents revenue disaggregated by segment and type (in thousands):

| Three Months Ended October 31, | ||||||||||||

| 2022 | 2021 | %Changes | ||||||||||

| Zedge App | ||||||||||||

| Advertising revenue | $ | $ | - | % | ||||||||

| Paid subscription revenue | - | % | ||||||||||

| Zedge Premium revenue | % | |||||||||||

| Emojipedia revenue | - | % | ||||||||||

| Applovin integration bonus | ||||||||||||

| Other revenues | % | |||||||||||

| Total Zedge App revenue | - | % | ||||||||||

| GuruShots App | ||||||||||||

| Virtual items used for online game | ||||||||||||

| Total revenue | $ | $ | % | |||||||||

nm-not meaningful

Contract Balances

The Company enters into contracts with its customers, which may give rise to contract liabilities (deferred revenue) and contract assets (unbilled revenue). The payment terms and conditions within the Company’s contracts vary by products or services purchased, the substantial all of which are due in less than one year. When the timing of revenue recognition differs from the timing of payments made by customers, the Company recognizes only deferred revenue (customer payment is received in advance of performance). The Company does not have unbilled revenue (its performance precedes the billing date).

Deferred revenues

On April 1, 2022, the Company received from AppLovin

Corporation a one-time integration bonus of $

6

The Company records deferred revenues related to the unsatisfied performance obligations with respect to subscription revenue. As of October 31, 2022, the Company’s deferred revenue balance related to paid subscriptions was approximately $1.4 million related to approximately 674,000 active subscribers. As of July 31, 2022, the Company’s deferred revenue balance related to paid subscribers was approximately $1.5 million, related to approximately 692,000 active subscribers. The amount of revenue related to subscribers recognized in the three months ended October 31, 2022 that was included in the deferred balance at July 31, 2022 was $0.7 million.

The Company also records deferred revenues when

users purchase or earn Zedge Credits. Unused Zedge Credits represent the value of the Company’s unsatisfied performance obligation

to its users. Revenue is recognized when Zedge App users use Zedge Credits to acquire Zedge Premium content or upon expiration of the

Zedge Credits upon 180 days of account inactivity. As of October 31, 2022, and July 31, 2022, the Company’s deferred revenue balance

related to Zedge Premium was approximately $

Total deferred revenues decreased by $

Significant Judgments

The advertising networks and advertising exchanges to which the Company sell its inventory track and report the impressions and installs to Zedge and Zedge recognizes revenues based on these reports. The networks and exchanges base their payments off of those reports and Zedge independently compares the data to each of the client sites to validate the imported data and identify any differences. The number of impressions and installs delivered by the advertising networks and advertising exchanges is determined at the end of each month, which resolves any uncertainty in the transaction price during the reporting period.

Practical Expedients

The Company expenses the fees retained by Google Play related to subscription revenue when incurred as marketing expense because the duration of the contracts for which the Company pays commissions are less than one year. These costs are included in the selling, general and administrative expenses of the condensed consolidated statements of operations and comprehensive (loss) income.

Note 3—Fair Value Measurements

The following tables present the balance of assets and liabilities measured at fair value on a recurring basis (in thousands):

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| October 31, 2022 | ||||||||||||||||

| Liabilities: | ||||||||||||||||

| Contingent consideration-short term | $ | $ | $ | $ | ||||||||||||

| Contingent consideration-long term | $ | $ | $ | $ | ||||||||||||

| Foreign exchange forward contracts | $ | $ | $ | $ | ||||||||||||

| July 31, 2022 | ||||||||||||||||

| Liabilities: | ||||||||||||||||

| Contingent consideration-short term | $ | $ | $ | $ | ||||||||||||

| Contingent consideration-long term | $ | $ | $ | $ | ||||||||||||

| Foreign exchange forward contracts | $ | $ | $ | $ | ||||||||||||

(1) – quoted prices in active markets for identical assets or liabilities

(2) – observable inputs other than quoted prices in active markets for identical assets and liabilities

(3) – no observable pricing inputs in the market

Contingent Consideration

Contingent consideration related to the business combinations discussed below in Note 5 are classified within Level 3 of the fair value hierarchy as the determination of fair value uses considerable judgement and represents the Company’s best estimate of an amount that could be realized in a market exchange for the asset or liability.

7

The following table provides a rollforward of the contingent consideration related to the GuruShots acquisition (in thousands):

| Balance at July 31, 2022 | $ | |||

| Change in fair value | ( | ) | ||

| Balance at October 31, 2022 | $ |

The overall fair value of the contingent consideration decreased by

$

Fair Value of Other Financial Instruments

Fair value of the outstanding foreign exchange forward contracts are marked to market price at the end of each measurement period.

The Company’s other financial instruments at October 31, 2022 and July 31, 2022 included trade accounts receivable and trade accounts payable. The carrying amounts of the trade accounts receivable and trade accounts payable approximated fair value due to their short-term nature.

Note 4—Derivative Instruments

The primary risk managed by the Company using derivative instruments is foreign exchange risk. Foreign exchange forward contracts are entered into as hedges against unfavorable fluctuations in the U.S. Dollar (USD) to Norwegian Kroner (NOK) and USD to Euro (EUR) exchange rates. The Company is party to a Foreign Exchange Agreement with Western Alliance Bank allowing the Company to enter into foreign exchange contracts under its revolving credit facility with the bank (see Note 11). The Company does not apply hedge accounting to these contracts, and therefore the changes in fair value are recorded in unaudited condensed consolidated statements of operations and comprehensive income. By using derivative instruments to mitigate exposures to changes in foreign exchange rates, the Company is exposed to credit risk from the failure of the counterparty to perform under the terms of the contract. The credit or repayment risk is minimized by entering into transactions with high-quality counterparties.

The outstanding contracts at October 31, 2022, were as follows:

| Settlement Date | U.S. Dollar Amount | NOK Amount | ||||||

| Nov-22 | ||||||||

| Dec-22 | ||||||||

| Jan-23 | ||||||||

| Feb-23 | ||||||||

| Mar-23 | ||||||||

| Apr-23 | ||||||||

| May-23 | ||||||||

| Total | $ | |||||||

| Settlement Date | U.S. Dollar Amount | EUR Amount | ||||||

| Nov-22 | ||||||||

| Dec-22 | ||||||||

| Jan-23 | ||||||||

| Feb-23 | ||||||||

| Mar-23 | ||||||||

| Apr-23 | ||||||||

| May-23 | ||||||||

| Total | $ | |||||||

8

The fair value of outstanding derivative instruments recorded in the accompanying unaudited condensed consolidated balance sheets were as follows:

| Assets and Liabilities Derivatives: | Balance Sheet Location | October 31, 2022 | July 31, 2022 | |||||||

| Derivatives not designated or not qualifying as hedging instruments | (in thousands) | |||||||||

| Foreign exchange forward contracts | $ | $ | ||||||||

The effects of derivative instruments on the condensed consolidated statements of operations and comprehensive (loss) income were as follows:

| Three Months Ended October 31, | ||||||||||

| Amount of (Loss) Gain Recognized on Derivatives | 2022 | 2021 | ||||||||

| Derivatives not designated or not qualifying as hedging instruments | Location of Loss Recognized on Derivatives | (in thousands) | ||||||||

| Foreign exchange forward contracts | $ | ( | ) | $ | ||||||

Note 5—Business Combination and Assets Acquisition

GuruShots Acquisition

On April 12, 2022, the Company consummated the

acquisition of

The purchase price for the equity securities of

GuruShots consists of approximately $

Under the SPA, the Company has agreed to make certain minimum investments in user acquisition for GuruShots in the period covered by the Earnout, subject to GuruShots maintaining agreed upon levels of Return On Ad Spend (“ROAS”).

In addition,

The parties to the SPA have made customary representations, warranties and covenants therein. The assertions embodied in those representations and warranties were made for purposes of the SPA and are subject to qualifications and limitations agreed by the respective parties in connection with negotiating the terms of the SPA.

The cash purchase price and the earnout have been allocated to GuruShots’ tangible assets, identifiable intangible assets, and assumed liabilities based on their estimated fair values. The preliminary fair value estimates of the net assets acquired are based upon preliminary calculations and valuations, and those estimates and assumptions are subject to change as the Company obtains additional information for those estimates during the measurement period (up to one year from the acquisition date). The excess of the total consideration over the tangible assets, identifiable intangible assets, and assumed liabilities was recorded as goodwill.

9

The Company will record measurement period adjustments based on its ongoing valuation and purchase price allocation procedures. The Company is still finalizing the valuation and purchase price allocation as it relates to the net working capital amount in the table below.

The allocation of the preliminary purchase price is as follows (in thousands):

| (Dollar Amounts in Thousands) | ||||

| Purchase price consideration: | ||||

| Cash consideration paid at close | $ | |||

| Cash contributed to escrow accounts at close | ||||

| Cash deducted from purchase price and contributed to GuruShots’ working capital | ||||

| Fair value of contingent consideration to be achieved at year 1 | ||||

| Fair value of contingent consideration to be achieved at year 2 | ||||

| Fair value of total consideration transferred | ||||

| Total purchase price, net of cash acquired | $ | |||

| Fair value allocation of purchase price: | ||||

| Cash and cash equivalents | $ | |||

| Trade accounts receivable | ||||

| Prepaid expenses | ||||

| Property and equipment, net | ||||

| Other assets (including ROU) | ||||

| Accounts payable and accrued expenses | ( | ) | ||

| Operating lease liabilities, current | ( | ) | ||

| Operating lease liabilities, noncurrent | ( | ) | ||

| Acquired intangible assets | ||||

| Goodwill | ||||

| Total purchase price | $ | |||

The cash consideration paid includes $

The earnout amount to be paid (up to the maximum

of $

The Company has issued 616,848 (net of forfeiture

of 9,394 shares) shares of the Company’s Class B common in respect of the retention pool to the GuruShots founders and employees,

which will be held by a trustee based in Israel. These shares will vest, in equal tranches, over three years assuming that the recipients

remain employed by the Company or a subsidiary through the vesting dates. The $4 million fair value of these unvested restricted stock

is not included as purchase consideration above, as it has a post-combination service requirement and will be accounted for separately

from the business combination as stock compensation expense. Additionally, the founders and employees are also entitled to receive an

aggregate of up to $4 million retention cash bonus over three years subject to the same continued service requirement, which was not included

in the purchase price above. As of October 31, 2022, the Company has accrued $

Identified intangible assets consist of trade names, technology and customer relationships. The fair value of intangible assets and the determination of their respective useful lives were made in accordance with ASC 805 and are outlined in the table below:

| (Dollar Amounts in Thousands) | Asset Value | Useful Life | ||||

| Identified intangible assets: | ||||||

| Trade names | $ | |||||

| Acquired developed technology | ||||||

| Customer relationships | ||||||

| Total identified intangible assets | $ | |||||

The Company’s initial fair value estimates related to the various identified intangible assets were determined under various valuation approaches including the Relief-from-Royalty Method and Multi-period excess earnings. These valuation methods require management to project revenues, operating expenses, working capital investment, capital spending and cash flows for GuruShots over a multiyear period, as well as determine the weighted average cost of capital to be used as a discount rate.

10

The Company amortizes its intangible assets assuming no residual value over periods in which the economic benefit of these assets is consumed.

The Company recorded the excess of the purchase

price over the identified tangible and intangible assets as goodwill. The Company believes that the investment value of the future enhancement

of the Company’s products and offerings created as a result of this acquisition has principally contributed to a purchase price

that resulted in the recognition of $

Acquisition-related transaction costs (e.g., legal,

due diligence, valuation, and other professional fees) are not included as a component of consideration transferred but are required to

be expensed as incurred. During fiscal 2022, we incurred $

Emojipedia Acquisition

The assets purchased include emojipeida.org, a

set of smaller websites, a bank of emoji related URLs related to the seller’s business, including World Emoji Day, the annual World

Emoji Awards, and Emojitracker. The asset purchase does not qualify as a business combination under FASB ASC 805, Business Combinations,

and has therefore been accounted for as an asset acquisition. The total purchase price for this acquisition was allocated to intangible

assets are amortized on a straight-line basis over their estimated useful lives of

Note 6—Intangible Assets and Goodwill

The following table presents the detail of intangible assets, net as of October 31, 2022 and July 31, 2022 (in thousands):

| October 31, 2022 | July 31, 2022 | |||||||||||||||||||||||

| Gross Carrying Value | Accumulated Amortization | Net Carrying Value | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||||||

| Emojipedia.org and other internet domains acquired | ||||||||||||||||||||||||

| Acquired developed technology | ||||||||||||||||||||||||

| Customer relationships | ||||||||||||||||||||||||

| Trade names | ||||||||||||||||||||||||

| Total intangible assets | $ | $ | $ | $ | $ | $ | ||||||||||||||||||

Estimated future amortization expense as of October 31, 2022 is as follows (in thousands):

| Fiscal 2023 | ||||

| Fiscal 2024 | ||||

| Fiscal 2025 | ||||

| Fiscal 2026 | ||||

| Fiscal 2027 | ||||

| Thereafter | ||||

| Total | $ |

The Company’s amortization expense for

intangible assets were $

11

Goodwill

Changes in the carrying amount of goodwill in the three months ended October 31, 2022 are as follows (in thousands):

| Carrying Amount | ||||

| Balance at July 31, 2022 | $ | |||

| Foreign currency translation adjustments | ( | ) | ||

| Balance at October 31, 2022 | $ | |||

Note 7—Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities consist of the following (in thousands):

| October 31, | July 31, | |||||||

| 2022 | 2022 | |||||||

| Accrued vacation | $ | $ | ||||||

| Accrued income taxes payable | ||||||||

| Accrued payroll taxes | ||||||||

| Accrued payroll and bonuses | ||||||||

| Accrued expenses | ||||||||

| Operating lease liability-current portion | ||||||||

| Derivative liability for foreign exchange contracts | ||||||||

| Due to artists | ||||||||

| Other | ||||||||

| Total accrued expenses and other current liabilities | $ | $ | ||||||

Note 8—Stock-Based Compensation

On November 10, 2021, the Company’s

Board of Directors amended the Company’s 2016 Stock Option and Incentive Plan (as amended to date, the “2016 Incentive Plan”)

to increase the number of shares of the Company’s Class B common stock available for the grant of awards thereunder by an additional

On March 23, 2022, the Company’s

Board of Directors amended the 2016 Incentive Plan to increase the number of shares of the Company’s Class B common stock available

for the grant of awards thereunder by an additional

At October 31, 2022, there were

In addition to stock options and restricted

stock awards, the Company occasionally issues DSU’s. On September 7, 2021, the Company granted a total of

30% of the DSU’s (or 87,396) have service vesting conditions only, with a vesting schedule of 25% on September 7, 2022, 33% on September 7, 2023, and as to all remaining DSUs on September 7, 2024. Vesting of the remaining 70% of the DSUs (or 203,924) is subject to continued service as well as a market condition. These DSUs will vest if the grantee remains in service to the Company and only if the aggregate market capitalization of the Company’s equity securities has reached or exceeded $451 million for five consecutive trading days between the grant date and the vest date. Subject to satisfaction of both of those conditions, these DSU’s with both service and market conditions have a vesting schedule of 25% September 7, 2022, up to 58% (the 25% eligible to vest in 2022 and an additional 33%) on September 7, 2023, and up to 100% on September 7, 2024. In the event the market capitalization condition has not been met prior to a vesting date, but is met by a subsequent vesting date, all DSUs with a market condition eligible for vesting prior to that date shall vest. In the event that the market capitalization condition has not been met by September 7, 2024, the DSUs with a market condition shall expire.

12

The Company recognizes stock-based compensation for stock-based awards, including stock options, restricted stock and DSUs based on the estimated fair value of the awards and recognized over the relevant service period. The Company estimates the fair value of stock options on the measurement date using the Black-Scholes option valuation model. The Company estimates the fair value of the restricted stock and DSU’s with service conditions only using the current market price of the stock. The Company estimates the fair value of the DSU’s with both service and market conditions using the Monte Carlo Simulation valuation model.

The Black-Scholes and Monte Carlo Simulation

valuation models incorporate assumptions as to stock price volatility, the expected life of options or awards, a risk-free interest rate

and dividend yield. We recognize stock-based compensation expense related to options and restricted stock units on a straight-line basis

over the service period of the award, which is generally

In our accompanying unaudited condensed consolidated statements of operations and comprehensive (loss) income, the Company recognized stock-based compensation for our employees and non-employees as follows:

| Three Months Ended | ||||||||||||

| October 31, | ||||||||||||

| 2022 | 2021 | % Change | ||||||||||

| (in thousands) | ||||||||||||

| Stock-based compensation expense | $ | $ | % | |||||||||

The DSUs with both service and market conditions

were valued using a Monte Carlo simulation model, with a valuation of $

As of October 31, 2022, the Company’s unrecognized

stock-based compensation expense was $

In the three months ended October 31, 2022 and

2021, the Company purchased

Note 9—Earnings Per Share

Basic earnings per share is computed by dividing net income attributable to all classes of common stockholders of the Company by the weighted average number of shares of all classes of common stock outstanding during the applicable period. Diluted earnings per share is computed in the same manner as basic earnings per share, except that the number of shares is increased to include restricted stock still subject to risk of forfeiture, issuances to be made on the vesting of unvested DSUs and the exercise of potentially dilutive stock options using the treasury stock method, unless the effect of such increase is anti-dilutive.

13

The rights of holders of Class A common stock and Class B common stock are identical except for certain voting and conversion rights and restrictions on transferability. As such, the Company is not required to break out EPS by class.

The weighted-average number of shares used in the calculation of basic and diluted earnings per share attributable to the Company’s common stockholders consists of the following (in thousands):

| Three Months Ended | ||||||||

| October 31, | ||||||||

| 2022 | 2021 | |||||||

| Basic weighted-average number of shares | ||||||||

| Effect of dilutive securities: | ||||||||

| Stock options | ||||||||

| Non-vested restricted Class B common stock | ||||||||

| Deferred stock units | ||||||||

| Diluted weighted-average number of shares | ||||||||

The following shares were excluded from the dilutive earnings per share computations because their inclusion would have been anti-dilutive (in thousands):

| Three Months Ended | ||||||||

| October 31, | ||||||||

| 2022 | 2021 | |||||||

| Stock options | ||||||||

| Non-vested restricted Class B common stock | ||||||||

| Deferred stock units | ||||||||

| Shares excluded from the calculation of diluted earnings per share | ||||||||

For the three months ended October 31, 2022, the diluted earnings per share equals basic earnings per share because the Company incurred a net loss during that period and the impact of the assumed exercise of stock options and vesting of restricted stock and DSUs would have been anti-dilutive.

Note 10—Commitments and Contingencies

Commitments

In connection with the acquisition

of GuruShots, the Company has (i) committed to a retention pool of $

Legal Proceedings

The Company may from time to time be subject to other legal proceedings that arise in the ordinary course of business. Although there can be no assurance in this regard, the Company does not expect any of those legal proceedings to have a material adverse effect on the Company’s results of operations, cash flows or financial condition.

Note 11—Term Loan and Revolving Credit Facilities

As of September 27, 2016, the Company entered into a loan and security

agreement with Western Alliance Bank for a revolving credit facility of up to $

14

Pursuant to the Amended Loan Agreement, the Company

discontinued the existing $

Pursuant to the Amended Loan Agreement, $

Interest accrued under the Amended Loan Agreement

is due monthly, and the Company shall make monthly interest-only payments related to the term loan through the eighteen (18) month anniversary

of the closing date. From the nineteen (19) month anniversary of the Closing Date through the maturity date, the Company shall repay each

outstanding term loan by paying the Applicable Term Advance Amortization Payment equal to 1/12th of

The Amended Loan Agreement may also require early repayments if certain conditions are met. The Amended Loan Agreement is secured by substantially all of the assets of the Company, its subsidiaries, and certain of its affiliates.

The Amended Loan Agreement includes the following financial covenants:

| a) | Debt Service Coverage Ratio.

Zedge shall maintain, at all times, a Debt Service Coverage Ratio of no less than |

| b) | Maximum Debt to EBITDA. Zedge shall maintain, at all times, a ratio of (a) indebtedness owed by Zedge to Western Alliance Bank, to (b) Zedge’s EBITDA for the trailing twelve (12) month period ended on such date of determination, shall not be greater than the amount set forth under the heading “Maximum Debt to EBITDA Ratio” as of, and for each of the dates appearing adjacent to such Maximum Debt to EBITDA Ratio”. |

| Maximum Debt to Quarter Ending | EBITDA Ratio | |

| October 31, 2022 | ||

| January 31, 2023 | ||

| April 30, 2023 | ||

| July 31, 2023 | ||

| October 31, 2023 | ||

| January 31, 2024 | ||

| April 30, 2024 | ||

| July 31, 2024 | ||

| Thereafter |

The Amended Loan Agreement also includes customary negative covenants, subject to exceptions, which limit transfers, capital expenditures, indebtedness, certain liens, investments, acquisitions, dispositions of assets, restricted payments and the business activities of the Company, as well as customary representations and warranties, affirmative covenants and events of default, including cross defaults and a change of control default.

15

Note 12—Segment and Geographic Information

Segment

Operating segments are components of an enterprise about which separate financial information is available that is evaluated regularly by the chief operating decision maker (“CODM”), or decision-making group, in deciding how to allocate resources and in assessing performance. The Company’s chief operating decision maker is its Chief Executive Officer as of October 31, 2022. Based on the criteria established by ASC 280, Segment Reporting, the Company had one operating and reportable segment as of July 31, 2022.

Beginning in the first quarter of fiscal 2023, the Company revised the presentation of segment information to align with changes to how the Company’s CODM manages the business, allocates resources and assesses operating performance reports operating results based on two reportable segments which are Zedge App and GuruShots App.

The CODM evaluates the performance of each operating segment using revenue and income (loss) from operations. The following table provides information about the Company’s two reportable segments:

| Three Months Ended | ||||||||||||||||

| October 31, | Change | |||||||||||||||

| 2022 | 2021 | $ | % | |||||||||||||

| Revenue: | ||||||||||||||||

| Zedge App | $ | $ | $ | ( | ) | - | % | |||||||||

| GuruShots App | nm | |||||||||||||||

| Total Revenue | $ | $ | % | |||||||||||||

| Segment income (loss) from operation | ||||||||||||||||

| Zedge App | $ | $ | $ | ( | ) | - | % | |||||||||

| GuruShots App | ( | ) | ( | ) | nm | |||||||||||

| Segment income (loss) from operation | $ | ( | ) | $ | ( | ) | - | % | ||||||||

Nm-not meaningful

The CODM does not evaluate operating segments using asset information and, accordingly, the Company does not report asset information by segment.

Geographic Information

Net long-lived assets and total assets held outside of the United States, which are located primarily in Israel and Norway, were as follows (in thousands):

| United States | Foreign | Total | ||||||||||

| Long-lived assets, net: | ||||||||||||

| October 31, 2022 | $ | $ | $ | |||||||||

| July 31, 2022 | $ | $ | $ | |||||||||

| Total assets: | ||||||||||||

| October 31, 2022 | $ | $ | $ | |||||||||

| July 31, 2022 | $ | $ | $ | |||||||||

Note 13— Operating Leases

The Company has operating

leases primarily for office space. Operating lease right-of-use assets recorded and included in other assets were $

16

Other than the above, there were no other material changes in the Company’s operating and finance leases in the three months ended October 31, 2022, as compared to the disclosure in the Company’s Annual Report on Form 10-K for the fiscal year ended July 31, 2022.

Note 14—Provision for Income Taxes

The Company’s tax provision or benefit from income taxes for interim periods has generally been determined using an estimate of its annual effective tax rate applied to year-to-date income and records the discrete tax items in the period to which they relate. In each quarter, the Company updates the estimated annual effective tax rate and makes a year-to-date adjustment to the tax provision as necessary.

The Company’s annual effective tax rate for the fiscal year ending July 31, 2023 differs from the United States federal statutory tax rate due to certain factors with temporary differences primarily related to equity compensation expenses.

As of October 31, 2022, the Company had $

The Company is subject to taxation in the United States and certain foreign jurisdictions. Earnings from non-U.S. activities are subject to local country income tax. The material jurisdictions where the Company is subject to potential examination by tax authorities include the United States, Norway, Lithuania and Israel.

Note 15—Subsequent Events

The Company performed a review for subsequent events through the date of these unaudited condensed consolidated financial statements and noted no material items for disclosure.

17

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following information should be read in conjunction with the accompanying unaudited condensed consolidated financial statements and the associated notes thereto of this Quarterly Report, and the audited consolidated financial statements and the notes thereto and our Management’s Discussion and Analysis of Financial Condition and Results of Operations contained in our Annual Report on Form 10-K for the fiscal year ended July 31, 2022 (the “Form 10-K”), as filed with the U.S. Securities and Exchange Commission (the “SEC”).

As used below, unless the context otherwise requires, the terms “the Company,” “Zedge,” “we,” “us,” and “our” refer to Zedge, Inc., a Delaware corporation and its subsidiary Zedge Europe AS, collectively.

Forward-Looking Statements

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including statements that contain the words “believes,” “anticipates,” “expects,” “plans,” “intends,” and similar words and phrases. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from future results. Factors that may cause such differences include, but are not limited to: (1) Economic, geopolitical and market conditions can adversely affect our business, results of operations and financial condition, including our revenue growth and profitability, which in turn could adversely affect our stock price; (2) Our ability to successfully make acquisitions and/or successfully integrate acquisitions that we have made into Zedge without incurring unanticipated costs or without being subject to other integration issues that may disrupt our existing operations; (3) Delay or failure to realize the expected synergies and benefits of the GuruShots acquisition; (4) The impact of the Covid-19 pandemic on our employees, customers, partners, and the global financial markets; and (5) Russia’s recent invasion of Ukraine, and the international community’s response. For further information regarding risks and uncertainties associated with our business, please refer to Item 1A to Part I “Risk Factors” in the Form 10-K. The forward-looking statements are made as of the date of this report and we assume no obligation to update the forward-looking statements, or to update the reasons why actual results could differ from those projected in the forward-looking statements. Investors should consult all of the information set forth in this report and the other information set forth from time to time in our reports filed with the SEC pursuant to the Securities Act of 1933 and the Securities Exchange Act of 1934, including the Form 10-K.

Current Economic Conditions and COVID-19

We are subject to risks and uncertainties caused by events with significant macroeconomic impacts, including but not limited to, the COVID-19 pandemic, the Russian invasion of Ukraine, and actions taken to counter inflation. Inflation, rising interest rates and reduced consumer confidence have caused and may continue to cause our clients to be cautious in their spending. The full impact of these macroeconomic events and the extent to which these macro factors may impact our business, financial condition, and results of operations in the future remains uncertain. The risks related to our business are further described in the section titled “Risk Factors” in Part II, Item 1A of this Quarterly Report on Form 10-Q and those discussed under Item 1A to Part I “Risk Factors” in the Form 10-K.

Impact of Russia’s recent invasion of Ukraine

We are closely monitoring the current and potential impact on our business, our people, and our clients as Russia’s war with Ukraine evolves. We have taken steps to comply with applicable domestic and international regulatory restrictions on international trade and financial transactions. In connection with our compliance efforts, we have identified active clients and vendors inside Russia and Belarus that are subject to evolving sanctions imposed by the United States and/or the European Union and have terminated or suspended our contracts with them. Revenues associated with clients and vendors in Russia and Belarus are not material to our consolidated financial results, and we anticipate that the termination of Russian and Belarus clients and vendors that are subject to duly authorized sanctions will not have a material impact on our business or other client relationships. Management and our Board of Directors are monitoring the regional and global ramifications of the continuing events.

Overview

Zedge, Inc. (“Zedge”) builds digital marketplaces and friendly competitive games around content that people use to express themselves. Our leading products include Zedge Ringtones and Wallpapers, a freemium digital content marketplace offering mobile phone wallpapers, video wallpapers, ringtones, and notification sounds which historically was branded as Zedge Premium, and GuruShots Ltd (“GuruShots”), a skill-based photo challenge game. Our vision is to connect creators who enjoy friendly competitions with a community of prospective consumers in order to drive commerce.

18

We are part of the ‘Creator Economy,’ where over 1 billion people create and share their content across social platforms, mobile, and video games, and content marketplaces. Within this group of individuals, over 200 million identify as creators, people who use their influence, skill, and creativity to amass an audience and monetize it. Furthermore, approximately 12% of full-time creators earn more than $50,000 per year, and 10% of influencers earn more than $100,000 per year. We view the Creator Economy as an untapped opportunity for Zedge to expand its business, especially as we execute by connecting our gamers with our marketplace.

The Zedge Ringtones and Wallpapers app (which is named “Zedge Wallpapers” in the App Store), which we refer to as our “Zedge App,” is a marketplace offering a wide array of mobile personalization content including wallpapers, video wallpapers, ringtones, and notification sounds, and is available both in Google Play and the App Store. As of October 31, 2022, our Zedge App has been installed nearly 583 million times since inception and, over the past two years, has had between 31.9 and 36.3 million monthly active users (“MAU”). MAU is a key performance indicator (“KPI”) that captures the number of unique users that used our Zedge App during the final 30 days of the relevant period. Our platform allows creators to upload content to our marketplace and avail it to our users either for free or for a price, via ‘Zedge Premium.’ In turn, our users utilize the content to personalize their phones and express their individuality.

In fiscal 2022 we introduced several new customer facing product features including ‘NFTs Made Easy’ and social and community features, all meant to improve customer engagement, MAU, and revenue growth over the long term. In addition, due to developments outside of our control, we migrated to a new ad mediation platform - Applovin MAX -, which monopolized internal resources and delayed the completion of other product initiatives we had planned for in fiscal 2022. Applovin paid us a one-time $2 million integration bonus and their performance has been on-par or better than our prior platform.

The Zedge App’s monetization stack consists of advertising revenue generated when users view advertisements when using the Zedge App or surfing our website, the in-app sale of Zedge Credits, our virtual currency, that is used to purchase Zedge Premium content, and a paid-subscription offering that provides an ad-free experience to users that purchase a monthly or annual subscription. As of October 31, 2022, we had approximately 674,000 active paying subscribers.

In late 2021, we introduced NFT functionality to a limited number of Zedge Premium creators via ‘NFTs Made Easy’. Over time we believe this product enhancement has the potential to drive significant artist growth and revenue production. ‘NFTs Made Easy’ is an eco-friendly platform that enables artists and consumers to sell and purchase NFTs within the Zedge App even though they may lack deep knowledge and proficiency in the crypto space. All transactions are made using Zedge Credits.

In April 2022, we acquired GuruShots a recognized category leader focused on gamifying the photography vertical. GuruShots offers a platform spanning iOS, Android, and the web that provides a fun, educational and structured way for amateur photographers to compete in a wide variety of contests showcasing their photos while gaining recognition with votes, badges, and awards. We estimate that the total addressable market of amateur photographers using their smartphones to take and publicly share artistic photos is 30-40 million people per month and that the market is still in its infancy. Every month, GuruShots stages more than 300 competitions that result in players uploading in excess of 1 million photographs and casting close to 4.5+ billion “perceived votes,” which are calculated by multiplying the number of votes that each player casts by a weighting factor based on various factors related to that user. To improve engagement, GuruShots has adopted a set of retention dynamics focused on individual, team and community dynamics that create a sense of belonging, inspiration, recognition, improvement, and competition.

Today, GuruShots utilizes a ‘Free-to-Play’ business model that leads to strong monetization with the purchase of resources that are used to give paying players an edge while still maintaining a fair and competitive experience for all participants. Over the past six years, the monthly average paying player spend has increased in excess of 14% annually to more than $55 per player.

As we look to the future, we are advancing several initiatives that we expect will drive user growth, increase engagement, drive in-app purchases, and advance our in-game economy. Some of these include:

| ● | On-Boarding. Revamping the customer onboarding experience in order to maximize first time purchasers by immediately drawing new players into simplified photo competitions that are limited to a small audience taking place in a short time duration. |

| ● | Subscriptions. Introducing value-adds that we can bundle into a subscription. For example, we started testing a feed of short and engaging instructional videos that offer players techniques for improving their photographs. If users engage with this content, we expect to bundle it into a paid subscription. |

19

| ● | Economy. Evolving the game economy by maturing the game’s progression mechanics and features, earn and spend dynamics, and introducing soft and premium currencies tied to resources and benefits. Furthermore, we hope to introduce an advertising layer in the monetization stack in the future. |

We market GuruShots to prospective players, primarily via paid user acquisition channels, and utilize a host of creative formats including static and video ads in order to promote the game. Our marketing team invests material resources in analyzing all attributes of a campaign ranging from the creative assets, offer acquisition channel, and platform (i.e., iOS, Android, and web), just to name a few, with the goal of determining whether a specific campaign is likely to yield a profitable customer. When we unearth a successful combination of these variables we scale up until we experience diminishing returns. Ultimately, we believe that the efforts we are making to advance the product coupled with the investment in user acquisition can significantly increase GuruShots’ player base.

Beyond our commitment to growing both the Zedge App and GuruShots on a standalone basis, we believe that there are many potential synergies that we can capitalize on that exist between the two businesses. Specifically, we plan to enable the ability for GuruShots players to become Zedge Premium artists and sell their photos to our audience of 30+ million MAU as standard digital images or NFTs. In addition, we look to benefit from the experience that the GuruShots team possesses and test gamifying the Zedge App. We believe that successful gamification can contribute to increasing engagement, retention, and lifetime value, all critical KPIs for our business. Longer term, we believe that there are complementary content verticals that lend themselves to gamification.

In August 2021, we acquired the assets of Emojipedia Pty Ltd (“Emojipedia”), including Emojipedia.org the world’s leading authority dedicated to providing up-to-date and well-researched emoji definitions, information, and news as well as World Emoji Day and the annual World Emoji Awards, and Emojitracker, which provides real time visualization of all emoji symbols used on Twitter. Emojipedia receives approximately 47 million monthly page views and has approximately 9.9 million monthly active users as of October 31, 2022 of which approximately 54% are located in well-developed markets. It is the top resource for all things emoji, offering insights into data and cultural trends. As a voting member of the Unicode Consortium, the standards body responsible for approving new emojis, Emojipedia works alongside major emoji creators including Apple, Google, Facebook, and Twitter.

We believe that Emojipedia provides growth potential to the Zedge App, and it was immediately accretive to earnings. In the past year, we have made many changes to Emojipedia including migrating to a new ad mediation platform, redesigning the Emojipedia website, and introducing localized versions of Emojipedia in Spanish, French, German, Italian, and Portuguese. We will continue to enhance this offering and are exploring new features including a native mobile offering as well as additional monetization opportunities.

Critical Accounting Policies

Our unaudited condensed consolidated financial statements and accompanying notes are prepared in accordance with accounting principles generally accepted in the United States of America, or U.S. GAAP. Our significant accounting policies are described in Note 1 to the consolidated financial statements included in the Form 10-K. The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses as well as the disclosure of contingent assets and liabilities. Critical accounting policies are those that require application of management’s most subjective or complex judgments, often as a result of matters that are inherently uncertain and may change in subsequent periods. Our critical accounting policies include those related to revenue recognition, business combination, intangible and goodwill, capitalized software and technology development costs and stock-based compensation. Management bases its estimates and judgments on historical experience and other factors that are believed to be reasonable under the circumstances. Actual results may differ from these estimates under different assumptions or conditions. For additional discussion of our critical accounting policies, see our Management’s Discussion and Analysis of Financial Condition and Results of Operations in the Form 10-K.

Recently Issued Accounting Standards Not Yet Adopted

Please refer to Note 1 to the unaudited condensed consolidated financial statements included in Item 1 to Part I of this Quarterly Report on Form 10-Q.

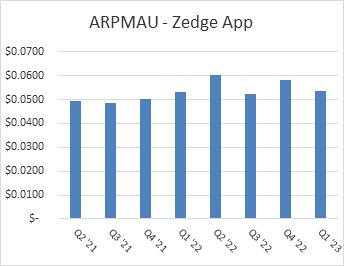

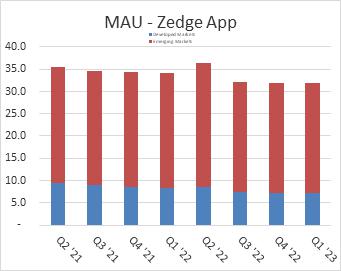

Key Performance Indicators (KPIs)

Zedge App-MAU and ARPMAU

The presentation of our results of operations includes disclosure of two key performance indicators - Monthly Active Users (MAU) and Average Revenue Per Monthly Active User (ARPMAU) from our Zedge App. MAU is a key performance indicator that we define as the number of unique users that used our Zedge App during the previous 30-day period, which is important to understanding the size of the user base for our Zedge App which is a main driver of our revenue. Changes and trends in MAU are useful for measuring the general health of our business, gauging both present and potential customers’ experience, assessing the efficacy of product improvements and marketing campaigns and overall user engagement.

20

ARPMAU is defined as (i) the total revenue derived from Zedge App in a monthly period, divided by (ii) MAU in that same period. ARPMAU for a particular time period longer than one month is the average ARPMAU for each month during that period. ARPMAU is valuable because it provides insight into how well we monetize our users and, changes and trends in ARPMAU are indications of how effective our monetization investments are.

MAU decreased 6.7% in Q1 of fiscal 2023 when compared to the same period a year ago and was flat on a sequential basis. Over the past several years, we have experienced a continuing shift in our regional customer make-up with MAU in emerging markets representing an increasing portion of our user base. As of October 31, 2022, users in emerging markets represented 78% of our MAU compared to 75% a year prior. This shift impacts our business because emerging markets do not monetize as well as well-developed markets due to lower effective cost per thousand ad impressions (“eCPM”) and lower monthly and annual subscription sales in these regions coupled with lower priced subscriptions SKUs. However, ARPMAU for the three months ended October 31, 2022 was up approximately 0.8% when compared to the same period a year ago, pointing to progress we have made in extracting more revenue from our users, particularly from paid subscriptions sales and improvement in ad optimization. ARPMAU declined 8.0% on a sequential basis due to seasonality.

The following tables present the MAU – Zedge App and ARPMAU – Zedge App for the three months ended October 31, 2022 as compared to the same period a year ago and the three months ended July 31, 2022:

YoY Comparison

| Three Months Ended October 31, | ||||||||||||

| (in millions, except ARPMAU - Zedge App) | 2022 | 2021 | % Change | |||||||||

| MAU- Zedge App | 31.9 | 34.2 | -6.7 | % | ||||||||

| Developed Markets MAU - Zedge App | 7.1 | 8.4 | -15.5 | % | ||||||||

| Emerging Markets MAU - Zedge App | 24.8 | 25.8 | -3.9 | % | ||||||||

| Emerging Markets MAU - Zedge App/Total MAU - Zedge App | 78 | % | 75 | % | 3.7 | % | ||||||

| ARPMAU - Zedge App | $ | 0.0537 | $ | 0.0533 | 0.8 | % | ||||||

QoQ Comparison

| Three Months Ended October 31, | Three Months Ended July 31, | |||||||||||

| (in millions, except ARPMAU) | 2022 | 2022 | % Change | |||||||||

| MAU- Zedge App | 31.9 | 32.0 | -0.3 | % | ||||||||

| Developed Markets MAU - Zedge App | 7.1 | 7.3 | -2.7 | % | ||||||||

| Emerging Markets MAU - Zedge App | 24.8 | 24.7 | 0.4 | % | ||||||||

| Emerging Markets MAU - Zedge App/Total MAU - Zedge App | 78 | % | 77 | % | 0.7 | % | ||||||

| ARPMAU - Zedge App | $ | 0.0537 | $ | 0.0584 | -8.0 | % | ||||||

The following charts present the MAU – Zedge App and ARPMAU – Zedge App for the consecutive eight quarters ended October 31, 2022:

|

|

|

| * | Please note the MAU-Zedge App graph above excludes MAU for both Emojipedia and GuruShots |

21

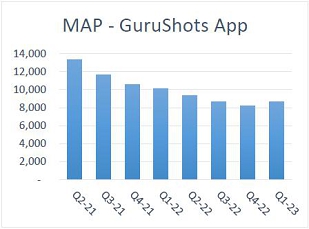

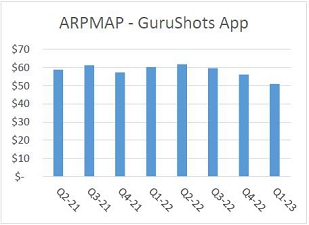

GuruShots App-MAPs and ARPMAP

Monthly Active Payers (“MAPs”). We define a MAP as a unique active user on the GuruShots App or GuruShots.com in a month that completed at least one in-app purchase (“IAP”) during that time period. MAPs for a time period longer than one month are the average MAPs for each month during that period. We estimate the number of MAPs by aggregating certain data from third-party attribution platforms.

Average Revenue Per Monthly Active Payer (“ARPMAP”). We define ARPMAP as (i) the total IAP derived from GuruShots App in a monthly period, divided by (ii) MAPs in that same period. ARPMAP for a particular time period longer than one month is the average ARPMAP for each month during that period. ARPMAP shows how efficiently we are monetizing each MAP.

The following table shows our Monthly Active Payers and Average Revenue Per Monthly Active Payer for the three months ended October 31, 2022 and 2021. Please note that we acquired GuruShots on April 12, 2022, as such, information for the three months ended October 31, 2021 is presented below as pro forma and is only used for comparative purpose.

| Three Months Ended October 31, | ||||||||||||

| (in thousands, except ARPMAP | 2022 | 2021 | % Change | |||||||||

| Monthly Active Payers | 8,690 | 10,112 | -14.1 | % | ||||||||

| Average Revenue per Monthly Active Payer | $ | 51 | $ | 60 | -15.0 | % | ||||||

The following charts present the MAP and ARPMAP – GuruShots App for the consecutive eight quarters ended October 31, 2022:

|

|

Our KPIs are not based on any standardized industry methodology and are not necessarily calculated in the same manner that other companies or third parties may use to calculate these or similarly titled measures. The numbers that we use to calculate MAP and ARPMAP are derived from data that we generate internally. While these numbers are based on what we believe to be reasonable judgments and estimates for the applicable period of measurement, there are inherent challenges in measuring usage and engagement. We regularly review and may adjust our processes for calculating our internal metrics to improve their accuracy.

22

Results of Operations

Three months ended October 31, 2022 Compared to Three months ended October 31, 2021

| Three Months Ended October 31, | Change | |||||||||||||||

| 2022 | 2021 | $ | % | |||||||||||||

| (in thousands) | ||||||||||||||||

| Revenues | $ | 6,900 | $ | 6,028 | $ | 872 | 14.5 | % | ||||||||

| Direct cost of revenues | 632 | 310 | 322 | 103.9 | % | |||||||||||

| Selling, general and administrative | 5,826 | 2,732 | 3,094 | 113.3 | % | |||||||||||

| Depreciation and amortization | 793 | 398 | 395 | 99.2 | % | |||||||||||

| Change in fair value of contingent consideration | (150 | ) | - | (150 | ) | nm | ||||||||||

| (Loss) income from operations | (201 | ) | 2,588 | (2,789 | ) | -107.8 | % | |||||||||

| Interest and other income, net | 35 | 13 | 22 | 169.2 | % | |||||||||||

| Net loss resulting from foreign exchange transactions | (76 | ) | (10 | ) | (66 | ) | 660.0 | % | ||||||||

| (Benefit from) provision for income taxes | (73 | ) | 536 | (609 | ) | nm | ||||||||||

| Net (loss) income | $ | (169 | ) | $ | 2,055 | $ | (2,224 | ) | -108.2 | % | ||||||

Revenues

The following table sets forth the composition of our revenues for the three months ended October 31, 2022 and 2021:

| Three Months Ended October 31, | ||||||||||||

| 2022 | 2021 | % Changes | ||||||||||

| Zedge App | ||||||||||||

| Advertising revenue | $ | 3,957 | $ | 4,569 | -13 | % | ||||||

| Paid subscription revenue | 891 | 960 | -7 | % | ||||||||

| Zedge Premium revenue | 187 | 186 | 1 | % | ||||||||

| Emojipedia revenue | 260 | 310 | -16 | % | ||||||||

| Applovin integration bonus | 250 | - | NM | |||||||||

| Other revenues | 26 | 3 | 767 | % | ||||||||

| Total Zedge App revenue | 5,571 | 6,028 | -8 | % | ||||||||

| GuiuShots App | ||||||||||||

| Virtual items used for online game | 1,329 | - | nm | |||||||||

| Total revenue | $ | 6,900 | $ | 6,028 | 14 | % | ||||||

nm-not meaningful

Advertising revenue. Advertising revenue decreased 13% in the three months ended October 31, 2022 compared to the three months ended October 31, 2021, primarily due to the decline in MAU in well-developed markets and lower effective advertising rates.

Paid subscription revenue. We offer users of our Zedge app a subscription option where they can pay a monthly or annual fee to remove unsolicited ads when using our Zedge app. We employ a regional pricing strategy in order to improve conversions. The U.S. constitutes our largest subscriber base and we generally charge $0.99 per month and $4.99 per year. Pricing in other markets is based on local conditions. We generated $829,000 in gross prepaid subscription in the three months ended October 31, 2022 compared to $920,000 in the three months ended October 31, 2021. The 10% decline in gross prepaid subscription sale for the three months ended October 31, 2022 when compared to the same period a year ago was primarily attributable to our decline in MAU. We expect that from time to time the prices of our subscription in each country/region may change and we may test other plan and price variations.

23

The following table summarizes subscription revenue for the three months ended October 31, 2022 and 2021:

| Three Months Ended | ||||||||||||

| 10/31/22 | 10/31/21 | % Change | ||||||||||

| (in thousands, except revenue per subscriber and percentages) | ||||||||||||

| Revenues | $ | 891 | $ | 960 | -7.2 | % | ||||||

| Active subscriptions net (decrease) increase | (18 | ) | 11 | nm | ||||||||

| Active subscriptions at end of period | 674 | 763 | -11.7 | % | ||||||||

| Average active subscriptions | 682 | 759 | -10.1 | % | ||||||||

| Average monthly revenue per active subscription | $ | 0.44 | $ | 0.42 | 4.8 | % | ||||||

Zedge Premium. Gross transaction value (the total sales volume transacting through the platform), or “GTV,” decreased 5% in the three months ended October 31, 2022 compared to the same period a year ago. Net revenue increased slightly in the three months ended October 31, 2022 compared to the same period a year ago.

The following table summarizes Zedge Premium gross and net revenue for the three months ended October 31, 2022 and 2021:

| Three Months Ended | ||||||||||||

| October 31, | ||||||||||||

| 2022 | 2021 | % Changes | ||||||||||

| (in thousands) | ||||||||||||

| Zedge Premium-gross revenue (“GTV”) | $ | 312 | $ | 329 | -5.2 | % | ||||||

| Zedge Premium-net revenue | $ | 187 | $ | 186 | 0.5 | % | ||||||

Virtual goods used for online game. GuruShots sells virtual game resources that provide game play benefits via in-app and online purchases. GuruShots recognizes revenue at the time of purchase because the overwhelming majority of users purchase game resources when they use them at a rate that exceeds the rate in which they earn them for free through participation. The $1.3 million revenue was earned in the three months ended October 31, 2022.

Direct cost of revenues. Direct cost of revenues consists primarily of content hosting and content delivery costs.

| Three Months Ended October 31, | ||||||||||||

| (in thousands) | 2022 | 2021 | % Change | |||||||||

| Direct cost of revenues | $ | 632 | $ | 310 | 103.9 | % | ||||||

| As a percentage of revenues | 9.2 | % | 5.1 | % | ||||||||

Direct cost of revenues increased by $322 thousand or 103.9% in the three months ended October 31, 2022 compared to three months ended October 31, 2021. The increase in the direct cost of revenues is a result of GuruShots’ infrastructure costs and the addition of analytical tools.

As a percentage of revenue, direct cost of revenues in three months ended April 30, 2022 was 9.2% compared to 5.1% in the prior year period. The higher percentage in the current period was primarily due to higher infrastructure costs related to the GuruShots App.

Selling, general and administrative expense. Selling, general and administrative expense (“SG&A”) consists mainly of payroll and benefits, paid user acquisition expenses, third-party payment processing fee relate to in-app purchases, recruiting fees, facilities, marketing, consulting, professional fees, software licensing (“SaaS”), and public company related expenses.

| Three Months Ended October 31, | ||||||||||||

| (in thousands) | 2022 | 2021 | % Change | |||||||||

| Selling, general and administrative | $ | 5,826 | $ | 2,732 | 113.3 | % | ||||||

| As a percentage of revenues | 84.4 | % | 45.3 | % | ||||||||

24

SG&A expense increased by $3.1 million or 113.3% in the three months ended October 31, 2022 compared to the prior year period. GuruShots accounted for $2.3 million of the increase. The remaining $0.8 million can be attributed to higher compensation costs resulting from additional headcount, higher stock-based compensation as discussed below, higher professional fees and offset by reductions in discretionary expenses.

As a percentage of revenue, SG&A expense in the three months ended October 31, 2022 were 84.4% compared to 45.3% in the prior year period, primarily due to the addition of GuruShots which has higher SG&A expenses relative to its revenue base.

Global headcount as of October 31, 2022 totaled 100 compared to 61 as of October 31, 2021 with the majority of our employees currently based in Lithuania and Israel.

SG&A expense also included stock-based compensation expense including equity grants to employees and consultants, as well as stock issuances to pay for board compensations and 401(k) matching contributions. Certain stock options, deferred stock unit and restricted stock grants are more fully described in Note 8 to the unaudited condensed consolidated financial statements included in Item 1 to Part I of this Quarterly Report on Form 10-Q.

Depreciation and amortization. Depreciation and amortization consist mainly of amortization of intangible assets and capitalized software and technology development costs of our internal developers on various projects that we invested in specific to the various platforms on which we operate our service.

| Three Months Ended October 31, | ||||||||||||

| (in thousands) | 2022 | 2021 | % Change | |||||||||

| Depreciation and amortization | $ | 793 | $ | 398 | 99.2 | % | ||||||

| As a percentage of revenues | 11.5 | % | 6.6 | % | ||||||||

Depreciation and amortization expenses increased $395 thousand or 99.2% in the three months ended October 31, 2022, compared to three months ended October 31, 2021. This increase was primarily attributable to the amortization of intangible assets related to the acquisition of GuruShots and Emojipedia which were $579 thousand and $115 thousand for the three months ended October 31, 2022 and 2021, respectively.

Interest and other income, net. Interest and other income, net in the three months ended October 31, 2022 increased $12,000 or 169.2% when compared to the prior periods due to higher interest rate earned from our cash balances.

| Three Months Ended October 31, | ||||||||||||

| (in thousands) | 2022 | 2021 | % Change | |||||||||

| Interest and other income, net | $ | 35 | $ | 13 | 169.2 | % | ||||||

| As a percentage of revenues | 0.5 | % | 0.2 | % | ||||||||

Net (loss) gain resulting from foreign exchange transactions. Net loss resulting from foreign exchange transactions is comprised of gains and losses generated from movements in NOK and EUR relative to the U.S. Dollar, including gains or losses from our hedging activities.

| Three Months Ended October 31, | ||||||||||||

| (in thousands) | 2022 | 2021 | % Change | |||||||||

| Net loss resulting from foreign exchange transactions | $ | (76 | ) | $ | (10 | ) | 660.0 | % | ||||

| As a percentage of revenues | -1.1 | % | -0.2 | % | ||||||||

In the three months ended October 31, 2022, we realized losses of $121,000 from NOK and EUR hedging activities, compared to gains of $10,000 in the three months ended October 31, 2021 due to the strengthening of the US dollar in current periods, as more fully described in Note 4 to the unaudited condensed consolidated financial statements included in Item 1 to Part I of this Quarterly Report on Form 10-Q.