As filed with the Securities and Exchange Commission on June 16, 2023

Registration No. 333-270755

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| Delaware | 7389 | 81-0971660 | ||

| (State or jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

251 N 1st Ave, Suite 200

Minneapolis, MN 5540

Telephone: (651) 504 5294

(Address, including Zip Code, and Telephone Number,

including Area Code, of Registrant’s Principal Executive Offices)

Copy to:

Jack Cohen, Esq. General Counsel Sezzle Inc. 251 N 1st Ave, Suite 200 Minneapolis, MN 55401 Telephone: (651) 504 5294 (Name, Address, Including

Zip Code, and |

Bradley Pederson, Esq. Maslon LLP 3300 Wells Fargo Center 90 South Seventh Street Minneapolis, Minnesota 55402 Telephone: (612) 672-8200 Fax: (612) 672-8341 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of the registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 7(a)(2)(B) of Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The Registered Stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is declared effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is prohibited.

SUBJECT TO COMPLETION DATED JUNE 16, 2023

PRELIMINARY PROSPECTUS

SEZZLE INC.

Common Stock

3,155,537 Shares

This prospectus relates to the proposed resale or other disposition from time to time of up to 3,155,537 shares of common stock, $0.00001 par value per share, of Sezzle Inc. (the “Company”), by the Registered Stockholders identified in this prospectus. We are not selling any shares of common stock under this prospectus and will not receive any proceeds from the sale or other disposition by the Registered Stockholders of common stock identified in this prospectus.

Unlike an initial public offering, the resale by the Registered Stockholders is not being underwritten by any investment bank. The Registered Stockholders may or may not elect to sell, in connection with a listing of our common stock on the Nasdaq Capital Market, or at any point thereafter, all or any portion their shares of common stock covered by this prospectus. The Registered Stockholders or their pledgees, assignees or successors-in-interest may offer and sell or otherwise dispose of the shares of common stock described in this prospectus from time to time through public or private transactions at prevailing market prices, at prices related to prevailing market prices or at privately negotiated prices. The Registered Stockholders will bear all commissions and discounts, if any, attributable to the sales of such shares. We will bear all other costs, expenses and fees in connection with the registration of the such shares. See “Plan of Distribution” beginning on page 107 for more information about how the Registered Stockholders may sell or dispose of its shares of common stock.

Our common stock is publicly traded on the Australian Securities Exchange, or the ASX, under the ticker “SZL” in the form of CHESS Depositary Interests, or CDIs. CDIs are units of beneficial ownership in shares of our common stock that are held in trust for CDI holders by CHESS Depositary Nominees Pty Limited, or CDN, a subsidiary of ASX Limited, the company that operates the ASX. The CDIs entitle holders to dividends, if any, and other rights economically equivalent to shares of our common stock on a 1-for-1 basis. CDN, as the stockholder of record, will vote the underlying shares in accordance with the directions of the CDI holders from time to time. In addition, holders of CDIs have the right to attend stockholders’ meetings. The CDIs are also convertible at the option of the holders into shares of our common stock on a 1-for-1 basis, such that for every CDI converted, a holder will receive one share of common stock. On June 15, 2023, the last reported per share price of our CDIs on the ASX was A$25.90 (US$17.79) per share.

In addition to the CDIs trading on the ASX, we have applied to list our common stock on the Nasdaq Capital Market under the symbol “SEZL.” We expect our common stock to begin trading within five business days of the date of this prospectus. The listing of our common stock on the Nasdaq Capital Market without underwriters is a novel method for commencing public trading in shares of our common stock outside of the ASX and, consequently, the trading volume and price of shares of our common stock may be more volatile than if shares of our common stock were initially listed in connection with an underwritten initial public offering on the Nasdaq Capital Market. There can be no guarantee that we will successfully list our common stock on the Nasdaq Capital Market. However, the registration of the Registered Stockholders’ resale of the Company’s common stock as described in this prospectus is not conditioned upon our successful listing on the Nasdaq Capital Market.

We are an “emerging growth company” as defined under the federal securities laws and have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings. See “Prospectus Summary — Implications of Being an Emerging Growth Company.”

Investing in our common stock involves a high degree of risk. Before making any investment in these securities, you should read and carefully consider the risks described in this prospectus under “Risk Factors” beginning on page 17 of this prospectus. We are a “smaller reporting company” under applicable law and are subject to reduced public company reporting requirements.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is June [__], 2023.

TABLE OF CONTENTS

i

ABOUT THIS PROSPECTUS

Unless otherwise stated or the context otherwise requires, the terms “we,” “us,” “our,” “SZL”, “SEZL” and the “Company” refer to Sezzle Inc. and its subsidiaries.

This prospectus is part of a registration statement that we have filed with the Securities and Exchange Commission (the “SEC”), pursuant to which the Registered Stockholders may, from time to time, offer and sell or otherwise dispose of the securities covered by this prospectus.

This prospectus is part of a registration statement on Form S-1 that we filed with the SEC using a “shelf” registration or continuous offering process. Under this process, the Registered Stockholders may, from time to time, sell the common stock covered by this prospectus in the manner described in the section titled “Plan of Distribution.” Additionally, we may provide a prospectus supplement to add information to, or update or change information contained in, this prospectus, including the section titled “Plan of Distribution.” You may obtain this information without charge by following the instructions under the section titled “Where You Can Find Additional Information” appearing elsewhere in this prospectus. You should read this prospectus and any prospectus supplement before deciding to invest in our common stock.

You should not assume that the information contained in this prospectus is accurate on any date subsequent to the date set forth on the front cover of this prospectus, even though this prospectus is delivered or securities are sold or otherwise disposed of on a later date. It is important for you to read and consider all information contained in this prospectus in making your investment decision. You should also read and consider the information in the documents to which we have referred you under the captions “Where You Can Find More Information” in this prospectus.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

Neither we nor the Registered Stockholders have authorized any dealer, salesman or other person to give any information or to make any representation other than those contained or incorporated by reference in this prospectus or contained in any free writing prospectus. You should not rely upon any information or representation not contained in this prospectus or contained in any free writing prospectus. This prospectus does not constitute an offer to sell or the solicitation of an offer to buy any of our securities other than the securities covered hereby, nor does this prospectus constitute an offer to sell or the solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction. For investors outside the United States: Neither we nor any of the Registered Stockholders have done anything that would permit the use or possession or distribution of this prospectus or any related free writing prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of our common stock by the Registered Stockholders and the distribution of this prospectus outside the United States.

We further note that the representations, warranties and covenants made in any agreement that is filed as an exhibit to the registration statement that includes this prospectus were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreements, and should not be deemed to be a representation, warranty or covenant to you. Moreover, such representations, warranties or covenants were accurate only as of the date when made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

Industry and Market Data

This prospectus includes estimates regarding market and industry data and forecasts, which are based on publicly available information, industry publications and surveys, reports from government agencies and our own estimates based on our management’s knowledge of, and experience in, the industry and markets in which we compete. In presenting this information, we have made certain assumptions that we believe to be reasonable based on such data and other similar sources, and on our knowledge of, and our experience to date in, the markets for our products. Market data is subject to change and may be limited by the availability of raw data, the voluntary nature of the data gathering process and other limitations inherent in any statistical survey of market data. This data involves a number of assumptions and limitations which are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause our future performance to differ materially from our assumptions and estimates. In addition, customer preferences are subject to change. Accordingly, you are cautioned not to place undue reliance on such market data. References herein to our being a leader in a market refer to our belief that we have a leading market share position in such specified market based on sales, unless the context otherwise requires.

Trademarks

This prospectus contains references to our trademarks and service marks and to those belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by any other companies.

ii

PROSPECTUS SUMMARY

This summary contains basic information about us and the offering contained elsewhere in this prospectus. Because it is a summary, it does not contain all the information that you should consider before investing in our common stock. You should read and carefully consider the entire prospectus before making an investment decision, especially the information presented under the headings “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our consolidated financial statements and the accompanying notes included elsewhere in this prospectus in its entirety before you decide whether to purchase any securities offered by this prospectus.

Company Overview

Our Company

We are a purpose-driven payments company that is on a mission to financially empower the next generation. Launched in 2017, we have built a digital payments platform that allows merchants to offer their consumers a flexible alternative to traditional credit. As of December 31, 2022, our platform supports the business growth of 42 thousand Active Merchants while serving approximately 2.9 million Active Consumers. Through our products, we aim to enable consumers to take control over their spending, be more responsible, and gain access to financial freedom. Our vision is to create a digital ecosystem benefiting all of our stakeholders— merchants, partners, consumers, employees, communities, and investors—while continuing to drive ethical growth.

We launched Sezzle amid a backdrop in which digitally-enabled shopping began to claim a larger share of the retail sector and younger generations (i.e., Gen Z and Millennials) started to demonstrate a need for credit. Gen Z and Millennial consumers, which we define as individuals currently between ages 18–26 and 27–45, respectively, use credit cards less frequently relative to other generations and, in many cases, lack access to traditional credit. These same consumers are tech-savvy, gravitating towards modern, streamlined commerce solutions whether online or in-person. We believe that our platform addresses the shortcomings in legacy payment offerings faced by consumers by providing a flexible, secure, omnichannel alternative, with the structural benefit of “creditizing” traditional debit products. The technology solutions we have designed specifically align with our ethos of helping the next generation pave their way forward financially.

We believe our multi-stakeholder approach gives us a competitive advantage and positions our company for success. Stakeholders want to be affiliated with a purpose-driven partner and, to that extent, we elected to become a Delaware public benefit corporation in June 2020. Public benefit corporations are for-profit corporations intended to produce a public benefit and operate in a responsible and sustainable manner. Under Delaware law, public benefit corporations must identify in their certificate of incorporation the public benefit or benefits they will promote, and their directors have a duty to manage the affairs of the corporation in a manner that balances the pecuniary interests of the stockholders, the best interests of those materially affected by the corporation’s conduct and the specific public benefit or public benefits identified in the public benefit corporation’s certificate of incorporation. Being a public benefit corporation offers advantages, including:

| ● | public benefit corporation status is a clear differentiator in an increasingly growing, and sometimes crowded, industry; |

| ● | we are more likely to become an employer of choice as the younger workforce increasingly seek employment from companies which align with their ethical values; |

| ● | further opportunities to conduct business with brands that also care about sustainability; |

| ● | the potential to expand our consumer base due to conscious consumers; |

| ● | added credibility to our mission statement and potential to grow capital through impact investing; and |

| ● | further opportunities for positive public relations and marketing. |

Additionally, on March 22, 2021, we became a certified B Corporation by B Lab, an independent non-profit organization, joining a movement of innovative, socially-conscious brands. In order to be designated as a Certified B Corporation, we were required to undertake a comprehensive and objective assessment of our environmental and social standards for transparency, accountability and commitment to improved performance. Our actions are part of a movement of innovative brands around the world intent on advancing environmental, social, and economic causes. To maintain our status as a certified B Corporation, we must satisfy re-certification requirements every three years. Our status as a B Corporation aligns with our mission to achieve growth, profitability, and returns for our investors while continuing to do right by our surrounding communities and our full set of stakeholders.

We primarily operate in the United States and Canada, and are currently winding down and exiting operations in India, Brazil, and certain countries in Europe.

1

Recent Developments

On May 11, 2023, the Company completed a reverse stock split of our issued and outstanding shares of common stock at a ratio of 1-for-38 shares, whereby every 38 shares of our issued and outstanding common stock were converted automatically into one issued and outstanding share of common stock without any change in the par value per share. All share and per share data in this registration statement reflects this reverse stock split.

Our Products

Sezzle Platform

At its core, the Sezzle Platform is a payments solution that instantly extends credit at point-of-sale, allowing consumers to purchase and receive the ordered merchandise at the time of sale and effectively split the payment for the purchase over four equal, interest-free payments over six weeks.

Our platform is integrated into merchants’ websites via our direct Application Programming Interface, and we provide technical support and onboarding services as part of the integration process. We are able to rapidly onboard merchants through an increasingly automated “merchant underwriting process”, and once integrated, merchants can immediately promote Sezzle to their shoppers on product and cart pages to start improving sales conversion. The Sezzle Platform is presented alongside other payment options on the merchant’s “Checkout” page. Consumers then select Sezzle as their payment option and create an account if they are a first-time user with Sezzle in a streamlined process that keeps consumers engaged throughout checkout.

The Sezzle Platform reviews the transaction and consumer profile in real-time and, if approved, quickly confirms the transaction for the merchant and consumer. Once approved, consumers are granted an initial spending limit. Further, our approval engine has a “counteroffer” function, which analyzes above-limit purchase attempts and provides alternative terms so that the consumer is not denied outright. Upon approval, the merchant ships the item(s) and receives payment, just as if the consumer had paid in cash or used a traditional credit or debit card, and the merchant pays us in the form of a merchant processing fee, which is subtracted from the sales price when we pay the merchant.

The Sezzle Platform is completely free to consumers who pay on time and use a bank account to make their installment payments, excluding their first payment. In order to complete their installment payments, consumers will receive a notification via email, SMS, or the Sezzle iOS or Android app two days prior to the date the installment payment is automatically debited by the Sezzle Platform. The consumer is also able to review and manage their Sezzle account via the Sezzle Platform’s online dashboard. From the dashboard, consumers are able to reschedule a payment without charge the first time, and can subsequently reschedule a payment up to two additional times for a small fee, subject to state jurisdiction. Consumers who fail to pay for their purchases on time may incur an account reactivation fee, which requires the settlement of an outstanding balance (including the reactivation fee) before they may use our platform again in the future. We typically do not report delinquent core Sezzle accounts to any credit bureaus or collection agencies, unless the consumer has elected to participate in Sezzle Up (as discussed below). As a result, consumer behavior on the core Sezzle Platform has no impact to a consumer’s credit score.

Consumers have the option to opt-in to our free Sezzle Rewards program, in which they earn reward points when making payments on their installments. These reward points can be used to redeem Sezzle Spend, which are credits issued to consumer accounts and can be applied to orders made on the Sezzle Platform.

Sezzle Up

We were an early, if not the first, mover among digital payments platforms that offer a credit-building solution to consumers. In partnership with TransUnion, we engineered Sezzle Up—an upgraded version of the core Sezzle experience that supports consumers in building their credit scores by permitting us to report their payment histories to credit bureaus. As these consumers pay on time, their credit scores and spending limits on the Sezzle Platform can increase. In order to qualify for Sezzle Up, existing Sezzle users who elect to participate must connect a bank account and pay off one order on time. As a condition to joining Sezzle Up, consumers commit to complete installment payments over the Automated Clearing House (“ACH”) network instead of over a card network. Consumers’ initial down payments are still completed over a card network. Using the ACH network benefits us by typically reducing processing fees and, in turn, lowering our transaction costs.

Sezzle Premium

In 2022, we launched the beta version of Sezzle Premium—a paid subscription service for our consumers to access large, non-integrated “premium merchants” for a monthly or annual fee. Besides being able to use Sezzle online or in-store at these premium merchants, consumers enrolled in Sezzle Premium also gain access to several other benefits, including one additional free reschedule per order and earning double the amount of rewards points on orders. Despite being in beta, Sezzle Premium has over 132,000 active subscribers as of February 22, 2023.

Sezzle Virtual Card

Other parts of our product suite and proprietary merchant interface are specifically designed to streamline the merchant experience. Our virtual card solution bolsters our omnichannel offering and provides a rapid-installation, point-of-sale option for brick-and-mortar retailers through its compatibility with Apple Pay and Google Pay. With our virtual card solution, consumers can enjoy in-store shopping with the convenience of immediately tapping into the Sezzle Platform with the “tap” of their virtual card at the point-of-sale.

2

Alternative Installment Options

With a select number of enterprise merchants, we offer customized installment terms that differ from our traditional four payment, six week terms. Examples of these alternative terms include a four payment, three month product and a six payment, five month product. We offer these special products to merchants at our discretion in situations where alternative terms would provide additional value to the consumer and merchant.

In addition, we began offering a “pay-in-full” option to consumers at certain merchants beginning in 2022. This option allows consumers to pay for the full value of their order up-front through the Sezzle Platform without the extension of credit. We believe this provides value for both new and existing consumers on the Sezzle Platform. For new consumers that apply for credit and may be denied, this allows them to complete their order through our platform without the need to re-enter any payment information. For existing consumers with payment information already saved, pay-in-full allows an express checkout option in instances where the consumer may not want to enter into a new installment plan.

We continue to evaluate additional alternative installments options that may provide additional value to consumers and merchants. Currently, we are developing and testing a shorter-term two payment, two week installment option to roll out at a future date.

Long-Term Lending

Through partnerships with third-party lenders, we offer our consumers at participating merchants access to interest-bearing monthly fixed-rate installment-loan products for larger-ticket items, which extend up to 60 months. We earn a fee from our lending partners for marketing and referring the potential consumers to them, and for processing applications and the use of our decision engine; however, we do not make final credit decisions or originate or hold the loans in our portfolio, which limits our capital needs and credit risk. We believe providing consumers access to long-term options has the potential to enhance our relationship with both merchants and consumers, while generating an attractive fee stream with no capital requirements or credit risk for us, and complementing our existing short-term, interest-free offering.

Product Innovation

Outside of our current suite of product offerings, we continuously strategize on new products that would complement our platform and current product offerings and add additional value for our stakeholders. As part of our next round of initiatives in product innovation, we are currently in the early stages of developing a “Sezzle Pay Anywhere Card” program.

Our Merchants

We offer a unique and user-friendly platform to our merchants. Our easy integration and seamless onboarding allows most merchants to go live on our platform within one day of activation to quickly realize the benefits of partnering with Sezzle. Our merchants benefit from our platform’s network effects through increased access to a deep and growing pool of consumers equipped with our flexible payment product, who would otherwise not be able to finance a transaction. Additionally, we believe that merchants benefit from associating with an innovative, B Corporation certified payments company which shares their consumers’ values across environmental, social, and economic causes. Our merchant segments are small-to-medium sized businesses (“SMBs”), mid-market merchants, and enterprise merchants, and span numerous categories with apparel and accessories; outdoors, sporting goods, and activities; and beauty and cosmetics representing the top three categories by UMS during 2022.

We also provide our merchants with a toolkit to grow their businesses, which we believe is unmatched among digital payments platforms. Our merchants gain access to our marketing efforts that begin with a launch campaign to introduce new brands to Sezzle consumers, and then follow with bi-weekly promotional support, quarterly “mega campaigns” that promote participating merchants with added incentives, and initiatives that enable consumers to “shop their values.” In addition, we provide select merchants with incentives to grow their sales and introduce Sezzle into new merchant categories through initiatives such as Sezzle Spend and co-branded marketing.

We offer a powerful value proposition to our merchant partners, evidenced by the fact that over 90% of our merchant additions are derived from inbound inquiries. The continued expansion of our platform should continue to enhance the benefits for our merchants. Our integration into scaled e-commerce platforms is expected to give more merchants the opportunity to seamlessly offer Sezzle as a payment option at checkout. Other products on the Sezzle Platform, such as long-term lending and alternative installment options, further adds to the value of our platform for merchants. This all occurs without any credit risk being transferred to the merchant.

SMBs

SMBs, which we define as merchants with UMS of less than $10 million per year, have historically comprised the largest segment of our merchant base. Our fast, easy application process makes onboarding simple, and our user-friendly merchant interface streamlines the integration process. Through Sezzle, these merchants are able to offer their consumers an optimized, effortless checkout process that enables them to complete sales.

Mid-Market Merchants

We are increasing our focus on mid-market merchants, which we define as merchants with UMS of between $10 million and $50 million per year. Mid-market merchants generally comprise a diverse array of growing “direct-to consumer” brands that are online-first and seek to connect with consumers without the use of secondary retailers, which naturally fits within our core offering. As we build out a larger consumer base, we believe we also enhance our value proposition to this segment by driving increased traffic toward brands that may not otherwise gain exposure through traditional retail channels by creating marketing campaigns designed to increase consumer exposure.

3

Enterprise Merchants

An ongoing major initiative is greater engagement with enterprise merchants, which we define as merchants with over $50 million in UMS per year. The core Sezzle product helps these merchants to facilitate a sale by providing access to credit for a consumer who has limited-to-no credit history. Without our payments platform, the consumer that lacks credit history may be rejected after applying for the store’s private label or co-brand credit card, which could tarnish the consumer’s view of that retailer’s brand. Importantly, we are not competing with a large retailer’s card offering. Instead, we work collaboratively with these retailers to drive sales, and over time, serve as a lead generator to consumers who are ready to graduate to the retailer’s card program. Our value proposition and engagement strategy have resonated with enterprise merchants.

Merchant Concentration

For the year ended December 31, 2022, approximately 14% of total income was driven by one merchant. For the year ended December 31, 2021, there were no merchants that exceeded 10% of total income. The concentration of a significant portion of our business and transaction volume with a limited number of scaled e-commerce platforms exposes us disproportionately to any of those partners choosing to no longer partner with us or choosing to partner with a competitor, and to any events, circumstances, or risks affecting such partners. In addition, a material modification in the financial operations of any significant scaled e-commerce partner could affect the results of our operations, financial condition, and future prospects.

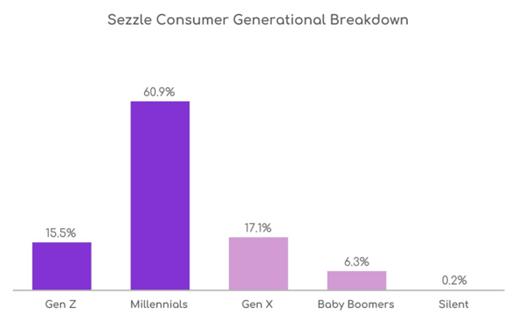

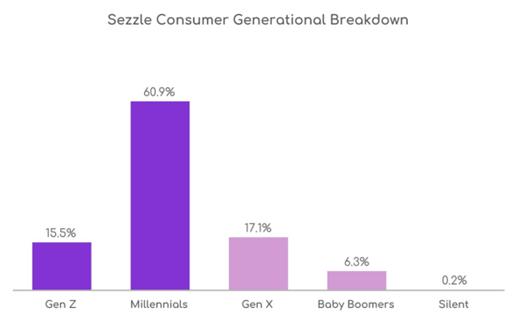

Our Consumers

Sezzle focuses on a young consumer base that is tech-savvy, socially-minded, and expects brands to possess ethical and social principles. As of December 31, 2022, 76.4% of our consumers are comprised of members of the Gen Z (18-26) and Millennial (27-45) generations which are generally early in their credit journey. For many of these consumers, we believe Sezzle has provided a way to improve financial responsibility—not only through enhanced budgeting and payments capabilities, but also through an opportunity to build credit history and develop a sense of financial empowerment with the Sezzle Up platform.

Source: Internal data based on orders placed during 2022 (Gen Z (18-26), Millennials (27-45), Gen X (46-57), Baby Boomers (58-76), and Silent (77 and greater)).

Gen Z and Millennial consumers use credit cards less frequently relative to other generations, and in many cases lack access to traditional credit. As a result, they tend to have fewer viable options for budgeting, achieving financial flexibility, and building credit history. Consumers in these generations also tend to transact frequently across e-commerce and brick-and-mortar retail, but spend less on average per transaction than older generations. In doing so, these consumers prefer to avoid loans that are not transparent or require payments that are not affordable. Sezzle’s core product provides these younger generations, who are newer to credit and are likely to move up the FICO score spectrum as they grow older and transact more often, with a unique solution to these payment challenges. In addition, consumers benefit from our platform’s network effects. As our platform grows and we establish more merchant partnerships, our consumers enjoy a wider variety of shopping options.

Our Employees

Our success to date would not be possible without our dedicated people, who we believe are our greatest asset. Bringing together a team of highly-skilled engineering, product, marketing and business development professionals is imperative to executing on our strategy. We do this by creating an inclusive, team-centric culture in which doing the right thing is celebrated. As of June 15, 2023, we had 279 employees (which includes approximately 246 full-time employees) working at Sezzle.

4

We are committed to fostering a diverse work environment of driven employees who believe in our mission. To this extent, our People Operations team works to create and execute sustainable hiring practices that span a diverse array of recruiting pipelines to find the best people for Sezzle. Additionally, our People Operations team continuously monitors and assesses key diversity, equity, and inclusion metrics to identify and refine processes.

For existing employees, or “Sezzlers”, we focus on developing an inclusive and fun culture with many opportunities for career and personal development to reward and retain our talented people. We have a diversity, equity, and inclusion group to ensure communication throughout the organization on issues impacting minorities, which also offers leadership opportunities to Sezzlers at any level of the organization. Despite all our Sezzlers having the option to work remotely, we also hold various company and community activities throughout the year to continue building a fun, team-centric culture.

Our Business Model

Revenue

We have built a sustainable, transparent business model in which our success is aligned with the financial success of our merchants and consumers. The Sezzle Platform is completely free to consumers who pay on time and use a bank account to make their installment payments, excluding their first payment. We make most of our revenue from merchant processing fees, which are based on a percentage of UMS plus a fixed fee per transaction. We pay our merchants for the transaction value upfront, net of the merchant fees owed to Sezzle, and assume all costs associated with consumer payments processing and credit risk. Merchant processing fees comprised 74% and 81% of our total revenues for the years ended December 31, 2022 and 2021, respectively, and 58% and 81% of our total revenues for the three-month periods ended March 31, 2023 and 2022. This decrease is primarily a result of the introduction of Sezzle Premium and other consumer related fees.

A smaller portion of our revenue is derived from our consumers. We do not charge our consumers any interest, finance charges, or initiation fees, and are not incentivized to profit from our consumers’ errors or financial adversity. Any consumer-based revenue that we earn is either from fees that we charge to reactivate an account following a failed payment and when consumers elect to reschedule a payment, or subscription revenue when consumers enroll in Sezzle Premium. Consumers who correct a failed payment within 48 hours after the failed payment have their account reactivation fees waived, and are not allowed to make any new purchases with us until any past-due principal and fees are paid. Additionally, consumers are able to reschedule a payment without charge the first time, and can subsequently reschedule a payment up to two additional times for a small fee, subject to state jurisdiction. We allow qualifying consumers to have fees waived under our hardship and fee forgiveness program.

Other sources of our revenue include partners and affiliates, including our long-term lending partners. For our long-term financing product where we take no balance sheet or credit risk, we charge a platform fee to our financial partners, which is a fixed percentage of UMS on a monthly basis. We also share a negotiated percentage of the merchant discount revenue with our financial partners. This amount may vary based on our partner and the volume of UMS. Our financial partners earns interest from consumers through this product, but we do not earn any interest or take any credit risk.

Credit Risk

A critical component of our business model is the ability to effectively manage the repayment risk inherent in allowing consumers to pay over time. To that end, a team of Sezzle engineers and risk specialists oversee our proprietary systems, identify transactions with elevated risk of fraud, assess the credit risk of the consumer and assign appropriate spending limits, and manage the ultimate receipt of funds. Further, we believe repayment risk is more limited relative to other traditional forms of unsecured consumer credit because consumers primarily settle 25% of the purchase value upfront. Additionally, ongoing user interactions allow us to continuously refine and enhance the effectiveness of these platform tools through machine learning.

Funding Our Operations

We have created an efficient funding strategy which has allowed us to scale our business and drive rapid growth. We have existing access to revolving credit facilities. Additionally, we pay merchants a fixed interest rate if they elect not to receive transaction proceeds upfront and instead leave their deposits in their merchant account.

Our products are entirely funded through our $100 million revolving credit facility and merchant account payables. The high-velocity with which we are able to recycle capital due to the short-term nature of our products has a multiplier effect on our committed capital. We do not currently require equity to directly fund product growth.

Our Competition

We operate in a highly competitive and dynamic industry. Our product offerings face competition from a variety of players, including those who enable transactions and commerce via digital payments. The point-of-sale financing market in which we operate includes several types of products. For example, consumers may make purchases with credit cards that have revolving balances and some of these products offer promotional terms, such as an introductory rate or deferred interest. In addition to traditional credit card products, some revolving balance products do not issue plastic credit cards to consumers (e.g., PayPal Credit). BNPL products, such as the Sezzle Platform, facilitate consumer purchases from retail merchants on installment plans. Credit card providers also offer products that allow consumers to pay for purchases made with their credit cards in installments rather than as a revolving balance (e.g., American Express and J.P. Morgan Chase). Visa and Mastercard, the major payments networks, have also introduced technology that facilitates this functionality.

5

We consider our main competitors to be other BNPL service providers. In the U.S. market, this includes Affirm, Afterpay (a subsidary of Block), Klarna, PayPal’s Pay in 4, and Zip (formerly QuadPay). In addition, PayBright by Affirm and Afterpay operate in the Canadian market. In July 2021, Apple announced its intention (as yet not launched to the general public) to provide a BNPL platform to its consumers called “Apple Pay Later.” We aim to differentiate our business to consumers by providing a product that is more simple, accessible, and consumer friendly than our competitors. This includes offering our product to consumers with little-to-no credit history, allowing consumers to shift their repayment schedule once per order for free, and waiving account reactivation fees when the consumer corrects a failed payment within 48 hours or qualifies for our hardship program. See “Risks Related to Our Industry - We operate in a highly competitive industry, and our inability to compete successfully would materially and adversely affect our business, results of operations, financial condition, and prospects” for further discussion about competition risks.

We face intense competitive pressure on the fees we charge our merchants, particularly our enterprise merchants. To stay competitive, we may need to adjust our pricing, offer incentives, enter new market segments, adapt to regulatory changes, or expand the use and functionality of our platform—all of which impact our growth and profitability. We have entered into merchant agreements that require us to make marketing, incentive or other payments to the merchant over the term of the agreement. If we are unable to fulfill our obligations under these merchant agreements, including any payments we have agreed to make with merchants, the merchant may terminate or not renew such agreement.

Our Intellectual Property

Our business depends on our ability to commercially exploit our technology and intellectual property rights, including our technological systems and data processing algorithms. We rely on laws in the United States, Canada and other countries relating to trade secrets, copyright, and trademarks to assist in protecting our proprietary rights. Our core intellectual property asset is the Sezzle Platform and the accumulation of transaction data, rules, and consumer insights generated from consumers using the Sezzle Platform, including the proprietary fraud and risk detection systems.

We developed our proprietary fraud and risk detection systems by creating valuable intellectual property that enables us to improve our products. The Sezzle Fraud Detection System was developed by our data sciences team, which utilizes numerous data points from a transaction to identify the likelihood of a fraudulent attempt. Consumer interactions with the Sezzle Platform are recorded and analyzed along with data points on the consumer and order itself. This data passes through the Sezzle Fraud Detection System, which scores the likelihood of the transaction being fraudulent. The Sezzle Underwriting Engine then assigns a score to each new consumer that passes through the Sezzle Fraud Detection System. Based on data obtained from traditional and non-traditional sources, along with the order data and retailer data, we assign varying initial spending limits for our shoppers. As consumers use the Sezzle Platform, our system learns from the behavior of the individual consumers and adapts the consumer’s limit to the appropriate level based on the consumer’s success level within the Sezzle Platform.

We do not currently have any issued patents, but continue to consider the most effective methods of protecting our intellectual property. We currently hold registered trademarks in the United States, the UK, the European Union, and India, and we have pending trademark applications in Canada and Brazil. However, continued operations within our existing markets and expansion into new markets risks conflicts with unrelated companies who may own registered trademarks for and/or otherwise use a similar name. See “Other Risks Related to Our Business – Our efforts to protect our intellectual property rights may not be sufficient.”

Our Regulatory Environment

Overview

Various aspects of our business and services are subject to U.S. federal, state, and local regulation, as well as regulation outside the United States including Canada. Certain of our services also are subject to rules promulgated by various card networks and other authorities, as more fully described below. These descriptions are not exhaustive, and these laws, regulations and rules frequently change and are increasing in number.

BNPL and Consumer Protection Regulation

The BNPL segment of the point-of-sale financing market in which we operate is a developing field. There has recently been an increased focus and scrutiny by regulators in various jurisdictions, including the United States and Canada, with respect to BNPL arrangements. We may become subject to additional legal or regulatory requirements if laws or regulations or the interpretation of such laws and regulations change in the future or industry standards for BNPL arrangements change in the future.

6

United States

In the United States, we are required to comply with the applicable provisions of the Truth-in-Lending Act and Regulation Z promulgated thereunder, which require certain disclosures to consumers regarding the terms and conditions of their loans and credit transactions and impose requirements on credit accessed through credit cards, Section 5 of the FTCA, which prohibits unfair and deceptive acts or practices (“UDAP”) in or affecting commerce, and analogous provisions in each state; the Consumer Financial Protections Act, which prohibits unfair, deceptive or abusive acts or practices (“UDAAP”) in connection with consumer financial products and services; the Equal Credit Opportunity Act and Regulation B promulgated thereunder, which prohibit creditors from discriminating against credit applicants on the basis of race, color, sex, age, religion, national origin, marital status, the fact that all or part of the applicant’s income derives from any public assistance program, or the fact that the applicant has in good faith exercised any right under the Federal Consumer Credit Protection Act or applicable state law; the Fair Credit Reporting Act (“FCRA”), which promotes the accuracy, fairness, and privacy of information in the files of consumer reporting agencies; the Fair Debt Collection Practices Act (the “FDCPA”), which provides guidelines and limitations concerning the conduct of third-party debt collectors in connection with the collection of consumer debts; and the and the Telephone Consumer Protection Act (the “TCPA”), which regulates the use of telephone and texting technology to contact customers.

We are also subject to the Holder in Due Course Rule of the Federal Trade Commission (“FTC”), and equivalent state laws, which requires any holder of a consumer credit contract to include a required notice and become subject to all claims and defenses that a borrower could assert against the seller of goods or services; the Electronic Fund Transfer Act, which provides disclosure requirements, guidelines, and restrictions on the electronic transfer of funds from consumers’ bank accounts; the Electronic Signatures in Global and National Commerce Act and similar state laws, which authorize the creation of legally binding and enforceable agreements utilizing electronic records and signatures; the Military Lending Act and similar state laws, which provide obligations and prohibitions relating to loans made to servicemembers and their dependents; and the Servicemembers Civil Relief Act, which allows active duty military members to suspend or postpone certain civil obligations.

We possess certain state lending licenses, and we continuously evaluate whether others are required, which subject us to supervisory oversight from these state license authorities and periodic examinations. The loans we may originate on our platform pursuant to these state licenses are subject to state licensing and interest rate fee restrictions, as well as numerous state requirements regarding consumer protection, interest rate, disclosure, prohibitions on certain activities, and loan term lengths. Our business may become subject to licensing requirements in states in which we currently do not hold licenses. For instance, in certain states we are currently not required to obtain a lending license because our extensions of credit in those states are structured as retail installment transactions. We continue to monitor state licensing regulations and how they may apply to our business, and may be required in the future to apply for additional state licenses, including states in which our loans are structured as retail installment transactions.

Canada

In Canada, we are required to comply with the Canada Anti-Spam Law, which regulates the transmittal of commercial email messages, the Canadian Personal Information Protection and Electronic Documents Act and equivalent provincial privacy laws in the provinces of Alberta, British Columbia and Quebec, each of which includes requirements surrounding the use, disclosure, and other processing of certain personal information about Canadian residents. In addition, we are required to comply with the Canadian federal and provincial human rights legislation which prohibits discriminatory practices to deny, deny access to, or to differentiate adversely in relation to any individual in respect of the provision of services customarily available to the general public on the basis of a certain prohibited grounds of discrimination. The Canadian provincial consumer protection and cost of credit disclosure laws prohibit late fees, impose limits on default charges, prohibit unfair practices, and include consumer contract disclosure and related process requirements, among other compliance requirements. We are also subject to Canadian provincial and territorial e-commerce laws.

We believe that we are appropriately licensed as a lender and/or have structured our business activities to avoid a licensing requirement in each of the Canadian provinces that require such licenses. In connection with our business activities, we are also generally subject to consumer protection legislation and other laws and, on that basis, our business is also generally subject to regulatory oversight and supervision from federal and/or provincial regulators in respect of those activities, regardless of whether we have a license. These regulators and enforcement agencies generally act on a complaints-basis and may receive consumer complaints about us. Investigations or enforcement actions may be costly and time consuming. Enforcement actions by such regulators and enforcement agencies could lead to fines, penalties, consumer restitution, the cessation of our business activities in whole or in part, or the assertion of private claims and lawsuits against us.

7

Payment Regulations

We are subject to the rules, codes of conduct and standards of Visa, Mastercard and other payment networks and their participants. In order to provide our payment processing services, we must be registered either indirectly or directly as service providers with the payment networks that we use. As such, we are subject to applicable card association and payment network rules, standards and regulations, which impose various requirements and could subject us to a variety of fines or penalties that may be levied by such associations or networks for certain acts or omissions. Card associations and payment networks and their member financial institutions regularly update and generally expand security expectations and requirements related to the security of consumer data and environments. Failure to comply with the networks’ requirements, or to pay the fees or fines they may impose, could result in the suspension or termination of our registration with the relevant payment networks and therefore require us to limit, suspend or cease providing the relevant payment processing services. We are also subject to the Payment Card Industry Data Security Standard (“PCI DSS”) with respect to the acceptance of payment cards, which provides for security standards relating to the processing of cardholder data and the systems that process such data. The failure of our products to comply with PCI DSS requirements may result in the loss of our status as a PCI DSS certified Service Provider and thereby impact our relationship with our merchant partners and their own ability to comply with PCI DSS.

In Canada, we are required to comply with the Payments Canada Rule H1- Pre-Authorized Debit Rules in respect of the acceptance of payments from Canadian bank accounts and the Quebec Charter of French Language laws which regulates the language of communication in commerce and business and applies to entities carrying on business in Quebec.

Data Privacy and Data Security Laws

We are subject to a number of laws, rules, directives, and regulations relating to the collection, use, retention, security, processing, and transfer of personally identifiable information about our customers, our merchants, and employees in the geographies where we operate. Our business relies on the processing of personal data in several jurisdictions and, in some cases, the movement of data across national borders. As a result, much of the personal data that we process, which may include certain financial information associated with individuals, is subject to one or more privacy and data protection laws in one or more jurisdictions. In many cases, these laws apply not only to third-party transactions, but also to transfers of information between or among us, our subsidiaries, and other parties with which we have commercial relationships.

Regulatory scrutiny of privacy, data protection, cybersecurity practices, and the processing of personal data is increasing around the world. Regulatory authorities are continuously considering numerous legislative and regulatory proposals and interpretive guidelines that may contain additional privacy and data protection obligations. Many jurisdictions in which we operate have adopted, or are in the process of adopting, or amending data privacy legislation or regulation aimed at creating and enhancing individual privacy rights. In addition, the interpretation and application of these privacy and data protection laws in the U.S., Europe, and elsewhere are subject to change and may subject us to increased regulatory scrutiny and business costs.

In the United States, we are subject to the Gramm-Leach-Bliley Act (the “GLBA”) and implementing regulations and guidance thereunder, in addition to applicable privacy and data protection laws in the other jurisdictions in which we carry on business activities or process personal information. Among other requirements, the GLBA imposes certain limitations on the ability to share consumers’ nonpublic personal information with nonaffiliated third parties and requires certain disclosures to consumers about information collection, sharing, and security practices and their right to “opt out” of the institution’s disclosure of their nonpublic personal information to nonaffiliated third parties. Privacy requirements, including notice and opt out requirements, under the GLBA and the FCRA are enforced by the FTC and by the Consumer Financial Protection Bureau (“CFPB”) through UDAAP claims, and are a standard component of CFPB examinations. State entities also may initiate actions for alleged violations of privacy or security compliance under state UDAAP claims, financial privacy, security and other laws.

Most states have in place data security laws requiring companies to maintain certain safeguards with respect to the processing of personal information, and all states require companies to notify individuals or government regulators in the event of a data breach impacting such information. In addition, most industrialized countries have or are in the process of adopting similar privacy or data security laws enforced through data protection authorities.

Other Applicable Regulations

We are subject to regulations relating to our corporate conduct and the conduct of our business, including securities laws, trade regulations and anti-money laundering (“AML”) laws and anti-corruption legislation. The United States and certain foreign jurisdictions have taken aggressive stances with respect to such matters and have implemented new initiatives and reforms.

8

We are required to comply with the U.S. Foreign Corrupt Practices Act, the Foreign Public Officials Act (Canada), and similar anti-bribery laws in other jurisdictions, which prohibit companies and their intermediaries from making improper payments for the purpose of obtaining or retaining business. Recent years have seen a substantial increase in anti-bribery law enforcement activity with more frequent and aggressive investigations and enforcement proceedings by both the Department of Justice and the SEC, increased enforcement activity by non-U.S. regulators and increases in criminal and civil proceedings brought against companies and individuals.

AML laws and related KYC requirements generally require certain companies to conduct necessary due diligence to prevent and protect against money laundering. AML enforcement activity could result in criminal and civil proceedings brought against companies and individuals, which could have a material adverse effect on our business. Regulators and enforcement agencies may receive consumer complaints about us. In the United States, these regulators and agencies include the Financial Crimes Enforcement Network (“FinCEN”), which could subject us to burdensome rules and regulations that could increase costs and use of our resources in order to satisfy our compliance obligations. We are also subject to certain economic and trade sanctions programs including Canadian sanctions laws and the sanctions programs administered by the U.S. Department of the Treasury’s Office of Foreign Assets Control (“OFAC”), which prohibit or restrict transactions or dealings with specified countries, individuals, and entities.

Our Sustainability

At our core, we are a stakeholder-centric company. Incorporated as a public benefit corporation (“PBC”) under Delaware law and certified as a B Corporation by B Lab, we pride ourself in our environmental, social, and governance (“ESG”) initiatives and are constantly striving to make an even greater impact across our stakeholder groups. To achieve a strong, transparent governance around ESG, we are in the process of incorporating material issues from a number of leading sustainability organizations into our own framework, including the IFRS’ Sustainability Accounting Standards Board (SASB) standards, the SEC’s Climate-Related Disclosures ruling, and B Lab’s Impact Assessment framework.

Our stakeholder approach looks at five distinct stakeholders: consumers, merchants, employees, communities, and investors. We integrate our stakeholder and their concerns into all decisions made across our business to enhance sustainability, promote equity, and support our communities.

Upon our initial B Corporation certification, we had a score of 80.7. We are currently evaluating initiatives to further improve our score and plan to implement them during 2023. Our B Corporation recertification will take place in 2024.

Consumers

We want to create an accessible, equitable, and sustainable product suite for consumers, many of which do not have access to traditional credit. Our management team and board of directors strongly believe that our commitment to providing alternative means for consumers to purchase items they need without incurring high-interest finance charges benefits our consumers. To create a sustainability product suite, we consider accessibility, data stewardship, responsible lending, and consumer feedback as critical areas of monitoring our product sustainability.

In 2020, we launched Sezzle Up, an upgraded version of the core Sezzle experience which provides a credit-building solution for new-to-credit consumers, helping consumers adopt credit responsibly and build their credit history.

Merchants

We strive to create sustainable partnerships with an ethical, sustainable, and diverse merchant base. To that extent, we are focusing on developing sustainable relationships with a diverse array of merchants and partners, prioritizing working with ethical and socially-good merchants, and creating trust with our merchants and partners through stewardship, transparency, and engagement.

Employees

Our goal for our employees is to create an equitable, inclusive work environment with a strong culture built around ethical values and good governance. Critical areas that we monitor for our employees’ happiness and wellness are diversity, hiring, financial security, and culture. Refer to the “Our Employees” section above for additional discussion.

Communities

Through environmental and social initiatives, we want to create net positive value for communities we serve. This includes engaging with our communities through volunteerism and local partnerships, reinvesting in the communities that helped us grow our business, and minimizing our corporate environmental impact and promoting environmental stewardship in other stakeholders.

9

We have collaborated with the University of Minnesota to provide full-ride scholarships to underrepresented students pursing degrees in technology. Additionally, we continue to identify and partner with nonprofits on initiatives that align with our company’s values and mission.

Investors

We want to create sustainable returns for our investors and have a strong, robust system of governance and controls. Management and the board of directors evaluate if we are meeting our overall mission, work towards fostering an ethical and transparent tone-at-the-top, and ensure that social responsibility remains a factor in our decision-making process. We maintain key performance indicators to measure and report to management and the board of directors on our sustainability efforts. These metrics are based on the frameworks noted above, but primarily relate to items reported in our B Lab Impact Assessment.

Certain Relationships and Related Party Transactions

Please see section “Certain Relationships and Related Party Transactions” in this prospectus for a summary of material agreements, other than material agreements entered into in the ordinary course of business, to which we are or have been a party.

Summary of Risk Factors

Our business is subject to a number of risks and uncertainties, as more fully described under “Risk Factors” in this prospectus. These risks could materially and adversely impact our business, financial condition, and results of operations, which could cause the trading price of our common stock to decline and could result in a loss of all or part of your investment. Additional risks, beyond those summarized below or discussed elsewhere in this prospectus, may apply to our business, activities, or operations as currently conducted or as we may conduct them in the future or in the markets in which we operate or may in the future operate. Some of these risks include:

Risks Related to Our Industry

| ● | The BNPL industry may become subject to increased regulatory scrutiny. |

| ● | We operate in a highly competitive industry. |

| ● | Our success is subject to macro-economic conditions that have an impact on consumer spending. |

| ● | Our industry may be subject to negative publicity. |

Risks Related to Our Strategy and Growth

| ● | We are an early-stage financial technology company with a limited operating history and a history of operating losses. |

| ● | Our failure to maintain our relationships with existing consumers and merchant partners, or to attract a diverse mix of merchant partners or new consumers to our platform. |

| ● | Our ability to effectively manage growth. | |

| ● | Our ability to maintain market share. | |

| ● | We may not be able to sustain our growth rate. | |

| ● | We may be unable to profitably manage our ongoing international operations. | |

| ● | We may require additional capital. |

10

Risks Related to Our Financing Program

| ● | Consumers may not treat their BNPL product loans with the same significance as other financial obligations. |

| ● | Merchants may fail to fulfill their obligations to consumers or comply with applicable law. |

| ● | Internet-based loan origination processes may give rise to greater risks than paper-based processes. |

| ● | Exposure to consumer bad debts and insolvency of merchants may adversely impact our financial success. |

| ● | Our ability to comply with the applicable requirements of payment processors. |

Risks Related to Our Technology and the Sezzle Platform

| ● | The integration, support and prominent presentation of our platform by our merchants. |

| ● | Unanticipated surges or increases in transaction volumes. |

| ● | The occurrence of data security breaches, cyberattacks, employee or other internal misconduct, malware, phishing or ransomware, physical security breaches, natural disasters, or similar disruptions. |

| ● | Real or perceived software failures or outages. |

| ● | Disruption in service on our platform that prevents us from processing transactions. |

| ● | Fraudulent activities occurring on our platform. |

Other Risks Related to Our Business

| ● | The failure of key vendors or merchants to comply with legal or regulatory requirements or to provide various services that are important to our operations. |

| ● | The loss of key partners and merchant relationships. |

| ● | Potential inaccuracies in third-party data we use. |

| ● | Changes in market interest rates. |

| ● | We maintain our cash at financial institutions, often in balances that exceed federally insured limits. |

| ● | Exchange rate fluctuations between the United States and Canada. |

| ● | Our ability to use net operating loss carryforwards and tax attributes. |

| ● | Our ability to protect our intellectual property rights. |

| ● | The loss of licenses or any quality issues with third-party technologies that support our business operations or are integrated with our products or services. |

| ● | Our inability to retain employees or recruit additional employees, and risks of employee misconduct. |

| ● | Potential inadequate insurance to cover losses and liabilities. |

Risks Related to Our Regulatory Environment

| ● | The costs of complying with various laws and regulations applicable to the BNPL industry in the United States and Canada. |

| ● | We are subject to various laws in the United States and Canada concerning lending programs, consumer finance and consumer protection. |

11

| ● | Failure to operate without obtaining necessary licenses. |

| ● | Violating applicable federal, state and/or local lending or other laws. |

| ● | Litigation, regulatory actions, and compliance issues could subject us to increased costs. |

| ● | Stringent and changing laws and regulations relating to privacy and data protection could result in claims, harm our results of operations, financial condition, and prospects, or otherwise harm our business. |

Risks Related to Our Corporate Structure

| ● | Our existing major stockholders own a large percentage of our stock and can exert significant influence over us. |

| ● | We are an “emerging growth company,” and the reduced U.S. public company reporting requirements applicable to emerging growth companies may make our shares of common stock less attractive to investors. |

| ● | We have and will continue to incur significant costs and are subject to additional regulations and requirements as a public company in both Australia and the United States. |

| ● | Failure to maintain effective internal control over financial reporting or disclosure controls may adversely affect our ability to report our financial results in a timely and accurate basis. |

| ● | Some provisions of our charter documents may have anti-takeover effects, and the exclusive forum designation may limit stockholders’ ability to obtain a favorable judicial forum for disputes with us. |

Risks Related to Shares of our Common Stock

| ● | Our existing major stockholders own a large percentage of our stock and can exert significant influence over us. |

| ● | We are an “emerging growth company,” and the reduced U.S. public company reporting requirements applicable to emerging growth companies may make our common stock less attractive to investors. |

| ● | We will incur significant costs and are subject to additional regulations and requirements as a public company in both Australia and the United States, including compliance with the reporting requirements of the Exchange Act, the requirements of the Sarbanes-Oxley Act and the listing standards of ASX and any U.S. securities exchange on which our shares may become listed for trading. In addition, key members of our management team have limited experience managing a public company |

| ● | If we discover a material weakness in our internal control over financial reporting that we are unable to remedy or otherwise fail to maintain effective internal control over financial reporting or disclosure controls and procedures, our ability to report our financial results on a timely and accurate basis may be adversely affected. |

| ● | The different characteristics of the capital markets in Australia and the United States may negatively affect the trading prices of our CDIs and common stock, and may limit our ability to take certain actions typically performed by a U.S. company. |

| ● | Our ability to list our common stock on the Nasdaq Capital Market is subject to us meeting applicable initial listing criteria. |

| ● | Our common stock may trade on more than one stock exchange and this may result in price variations between the markets and volatility in our stock price. |

| ● | If we are not able to maintain sufficient cash funds, we may cease trading on the ASX and the Nasdaq Capital Market. |

| ● | An active, liquid, and orderly market for our common stock may not develop or be sustained. You may be unable to sell your shares of common stock at or above the price at which you purchased them. |

| ● | None of our stockholders are party to any contractual lock-up agreement or other contractual restrictions on transfer. Following our listing, sales of substantial amounts of our common stock in the public markets, or the perception that sales might occur, could cause the trading price of our common stock to decline. |

| ● | Some provisions of our charter documents may have anti-takeover effects that could discourage an acquisition of us by others, even if an acquisition would be beneficial to our stockholders, and may prevent attempts by our stockholders to replace or remove our current management. |

| ● | Our charter designates the Court of Chancery of the State of Delaware as the exclusive forum for substantially all disputes between us and our stockholders and the federal district courts as the exclusive forum for Securities Act claims, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us. |

| ● | We do not currently expect to pay any cash dividends. |

12

Risks Related to Our Existence as a Public Benefit Corporation and a Certified B Corporation

| ● | As a public benefit corporation, we cannot provide any assurance that we will achieve our public benefit purpose. |

| ● | As a public benefit corporation, our focus on a public benefit purpose may negatively impact our financial condition. |

| ● | Our directors have a fiduciary duty to consider not only our stockholders’ interests, but also our specific public purpose and the interests of other stakeholders affected by our actions. |

| ● | Increased derivative litigation concerning our duty to balance stockholder and public benefit interest. |

| ● | If our ability to maintain our certification as a B Corporation or our publicly reported B Corporation score declines, our reputation could be harmed and our business could be adversely affected. |

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). For so long as we remain an emerging growth company, we are permitted and plan to rely on exemptions from certain disclosure requirements that are applicable to other public companies. These provisions include, but are not limited to:

| ● | being permitted to have only two years of audited financial statements and management’s discussion and analysis of financial condition and results of operations disclosure; |

| ● | being exempt from compliance with the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; |

| ● | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board (the “PCAOB”) regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; |

| ● | reduced disclosure obligations regarding executive compensation arrangements in our periodic reports, registration statements and proxy statements; and |

| ● | being exempt from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved by stockholders. |

We have elected to take advantage of certain reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in future filings. In addition, the JOBS Act permits us, as an emerging growth company, to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. As a result, the information that we provide to our stockholders may be different from what you might receive from other public reporting companies in which you hold equity interests.

We will remain an emerging growth company until the earliest of (i) the last day of our fiscal year following the fifth anniversary of the date of our first sale of our common stock pursuant to an effective registration statement under the Securities Act of 1933, as amended (the “Securities Act”), (ii) the first fiscal year after our annual gross revenues exceed $1.07 billion, (iii) the date on which we have, during the immediately preceding three-year period, issued more than $1.00 billion in non-convertible debt securities or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the SEC.

Additionally, we are a “smaller reporting company” as defined in Item 10(f)(1) of Regulation S-K. Smaller reporting companies may take advantage of certain reduced disclosure obligations, including, among other things, providing only two years of audited financial statements. We will remain a smaller reporting company until the last day of the fiscal year in which (i) the market value of our common stock held by non-affiliates exceeds $250 million as of the end of the second quarter of that fiscal year, or (ii) our annual revenues exceeded $100 million during such completed fiscal year and the market value of our common stock held by non-affiliates exceeds $700 million as of the end of the second quarter of that fiscal year. To the extent we take advantage of such reduced disclosure obligations, it may also make comparison of our financial statements and certain other disclosures with other public companies difficult or impossible.

Corporate Information